Internationalization of Chinese OEMs Understanding the dynamics of Chinese OEMs’ global strategic ambitions

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Internationalization of Chinese OEMs

Understanding the dynamics of Chinese OEMs’ global strategic ambitions

A. Summary 3

B. Snapshot Chinese Automotive Industry 4

C. International Footprint of Chinese OEMs 6

D. SWOT Analysis in Global Context 10

E. Case Study: Three OEMs – Three Strategies 11

F. Regional Case Study: Chinese OEMs in Brazil 14

G. Future Growth Targets and Trends 16

H. Outlook and Impact for International Automotive Supplier 19

Internationalization of Chinese OEMs

Understanding the dynamics of Chinese OEMs’ global strategic ambitions

Publication date: February 2013

A. Summary

The globalization of multinational companies (MNCs) in the automotiveindustry has historically been driven and dominated by players from leadingeconomies, such as the United States, Western Europe and Japan. Sales tothe Chinese high-volume growth market have become a key expansiondriver in their respective sales strategies. More recently, however, China’srole is transforming from host for foreign players to home base foraspiring Chinese headquartered car manufacturers aiming to ‘go global’ andchange the rules of the game in global automotive competition.

1. With 19.3 mio units produced in 2012 China has emerged as the world’s largest automotiveproduction market - accounting for a quarter of global vehicle production

2. Competition in the domestic market is rising - Chinese OEMs are losing market shares incomparison to international OEMs especially in the premium segment

3. Exports of Chinese OEMs have reached 850,000 units in 2011 with some exporters achievingannual growth rates of up to 50%. Focus regions are emerging markets in South America,Middle East and Russia

4. Ambitious growth targets in sales regions overseas are supported by a gradual build-up oflocal facilities in cooperation with local partners

5. Chinese strengths remain in cost advantages and beneficial domestic market dynamics,weaknesses include safety and quality features – future market demand in emerging marketsas opportunity

6. Internationalization strategies vary: from adapting own strengths in emerging markets,aggressive targeting of low-end Western customers to more long-term and incrementalglobal expansion strategies

7. Chinese OEMs push aggressively into emerging markets like Brazil with their competence toserve low-end consumers and ‘bottom of pyramid’ segments

8. The internationalization of Chinese OEMs is accelerated by ambitious growth targets of theChinese government: 13 mio units for export by 2015 and 10% global market share by 2020

9. Other internationalization push factors of include intensified domestic competition andupgrade of Chinese OEMs innovation ability

10. Internationalization efforts will provide mid- to long-term supply opportunities forinternational suppliers to Chinese OEMs abroad: “Local access, global supply”

In this compact study EAC has compiled some key characteristics of

the recent phenomenon of Chinese OEM internationalization:

3

A. Summary

B. Snapshot: The Chinese

Automotive Industry

1 With 19.3 million units produced in 2012 China has emerged as the world’s largest

automotive production market - accounting for a quarter of global vehicle production

In 2009 China’s automotive industry has surpassed the leading countries USA, Japan andGermany to become the world’s largest automotive market. With a total production of 19.3mio units in 2012, China now accounts for a quarter of total global vehicle production.Driven by continued strong economic growth and a comparatively low per capita vehicle density,China will most likely increase its global market share to over 35% within the next 5 years.

Vehicle market China 2009-2012

Source: CAAM 2012

However, growth from 2011 to 2012 has slowed recently in both passenger vehicle (7%) andcommercial vehicle segments (-6%). Besides an overall slowdown of Chinese economic growth,the expiration of major government subsidies for the purchase of new passenger vehicles at theend of 2010 and the implementation of registration limits for new passenger cars in major Chinesecities such as Beijing (240,000), Shanghai, Guangzhou or Guiyang in 2011 contributed to thedecline. The commercial vehicle market was hit by an overall downturn of the constructionindustry and the discontinuation of government-funded infrastructure projects. While thepassenger vehicle segment is expected to continue its growth path at a reduced speed, Chinesetruck manufacturers doubt a fast recovery of the commercial vehicle market.

4

B. Snapshot: The Chinese

Automotive Industry

2 Competition in the domestic market is rising - Chinese OEMs are losing market shares in

comparison to international OEMs especially in the premium segment

Chinese OEMs are suffering most from the drop in domestic growth. Marketshare of Chinese brands decreased to 42% recently after a temporaryhigh of 44% in 2009. Daniel Berger, Partner of EAC in Shanghai explains:“To stay competitive in the domestic market, Chinese OEMs can no longerrely on cost leadership alone. Considerable investments in R&D will benecessary to build up an attractive automobile brand addressing the newChinese consumer.”

Foreign brands, especially in the premium segment, are highlypopular in the Chinese market and growing by 20 to 40%.German passenger vehicle production in China grew by 28% to 2.4 miounits in 2011. Similarly attractive are Japanese and American brands withgrowth rates of 28% and 25% respectively. Passenger vehicle importsincreased drastically at a rate of 59% to 1 mio imported vehicles in 2011and once again turned China into a net importer of cars.

Top 10 OEMs in China

Source: EAC Research

The commercial vehicle sector exhibits the opposite picture: International OEMs can barely gainfoothold in the Chinese market, 99% is still dominated by Chinese brands due to their focus onthe low-price segment. However, the need to comply with stricter emission standards set by thegovernment is fuelling partnering efforts with international technology leaders, exemplified byseveral recently signed JV agreements with both OEMs and TIER I suppliers.

5

3 Exports of Chinese OEMs have reached 850,000 units in 2011 with some exporters

achieving annual growth rates of up to 50%. Focus regions are emerging markets in

South America, Middle East and Russia

Leading Chinese automotive exporters, above all Chery, Great Wall, Changan and JAC Motors,currently demonstrate growth rates of up to 50% after a steep decline during the globalfinancial crisis. Chery is leading the statistics with annual production of 160,000 vehicles in 2011,for 2012 the company expects around 170,000 units.

Yet, not all of the important Chinese OEMs have significant exports – FAW as the thirdlargest car manufacturer in China does not occupy a leading role in exports.

Export dynamics of Chinese vehicle manufacturers 2007-2011

Source: CAAM 2012

6

Whereas foreign car manufacturers focus on China’s domestic market, Chinese manufacturerspromote focus increasingly on foreign markets. Hence exports of Chinese manufacturers roseon average 60% between 2009 and 2011 to a total of 850,000 vehicles (~4.6% ofproduction). The passenger vehicle sector amounted to 380,000 vehicles; 470,000 vehicles weresold in the commercial vehicle segment.

C. International Footprint of

Chinese OEMs

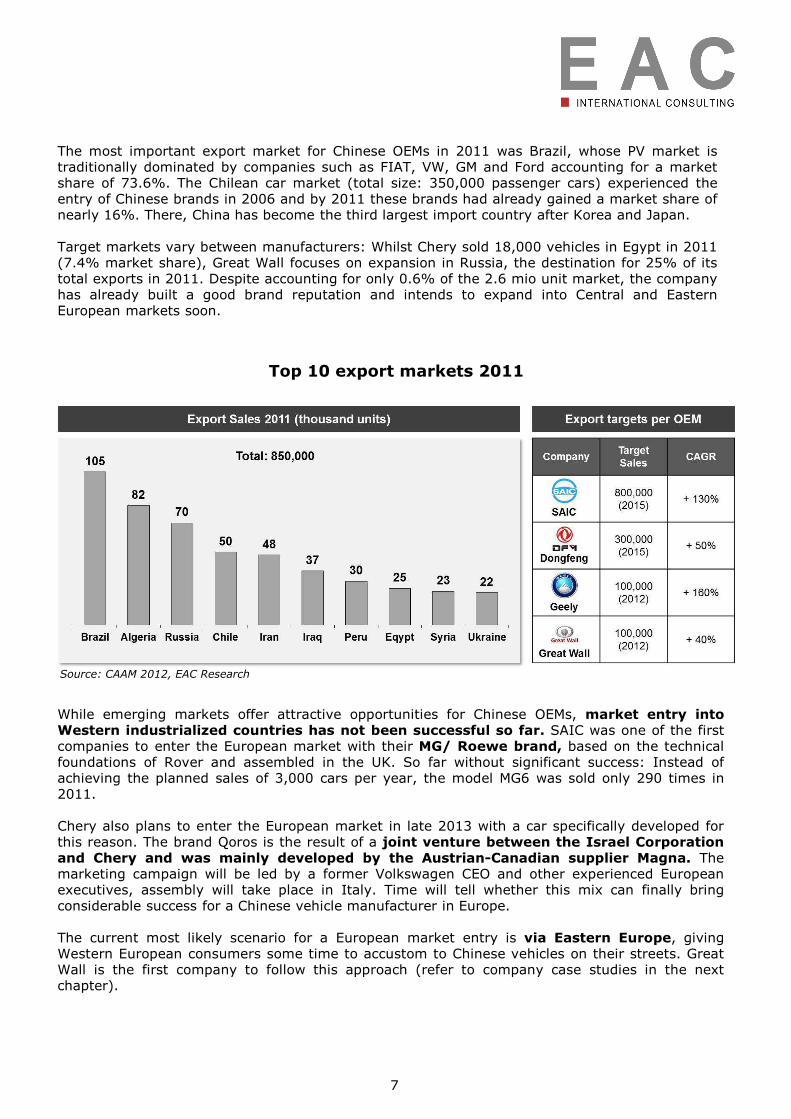

The most important export market for Chinese OEMs in 2011 was Brazil, whose PV market istraditionally dominated by companies such as FIAT, VW, GM and Ford accounting for a marketshare of 73.6%. The Chilean car market (total size: 350,000 passenger cars) experienced theentry of Chinese brands in 2006 and by 2011 these brands had already gained a market share ofnearly 16%. There, China has become the third largest import country after Korea and Japan.

Target markets vary between manufacturers: Whilst Chery sold 18,000 vehicles in Egypt in 2011(7.4% market share), Great Wall focuses on expansion in Russia, the destination for 25% of itstotal exports in 2011. Despite accounting for only 0.6% of the 2.6 mio unit market, the companyhas already built a good brand reputation and intends to expand into Central and EasternEuropean markets soon.

Top 10 export markets 2011

Source: CAAM 2012, EAC Research

While emerging markets offer attractive opportunities for Chinese OEMs, market entry intoWestern industrialized countries has not been successful so far. SAIC was one of the firstcompanies to enter the European market with their MG/ Roewe brand, based on the technicalfoundations of Rover and assembled in the UK. So far without significant success: Instead ofachieving the planned sales of 3,000 cars per year, the model MG6 was sold only 290 times in2011.

Chery also plans to enter the European market in late 2013 with a car specifically developed forthis reason. The brand Qoros is the result of a joint venture between the Israel Corporationand Chery and was mainly developed by the Austrian-Canadian supplier Magna. Themarketing campaign will be led by a former Volkswagen CEO and other experienced Europeanexecutives, assembly will take place in Italy. Time will tell whether this mix can finally bringconsiderable success for a Chinese vehicle manufacturer in Europe.

The current most likely scenario for a European market entry is via Eastern Europe, givingWestern European consumers some time to accustom to Chinese vehicles on their streets. GreatWall is the first company to follow this approach (refer to company case studies in the nextchapter).

7

4 Ambitious growth targets in the sales regions are supported by a gradual build-up of

local facilities in cooperation with local partners

In order to supply the target markets overseas, Chinese automotive manufacturers mostly exportsemi-knocked-down (SKD) or completely-knocked-down (CKD) kits, which are thenassembled with locally sourced parts in plants especially established for this purpose.

By exporting SKD and CKD units tariff advantages of up to 80% in comparison to completely-built-up-units (CBU) can be achieved. For example, in India, where import duties of 100% areapplied for fully assembled cars, knocked-down car parts can be imported for a tariff of only 10%.Similarly unattractive conditions for the import of complete cars exist in Egypt, Brazil or Russia.As a result, Chery and its Chinese competitors already assemble more than half of their exportedcars overseas.

Global presence of Chinese automotive OEMs

Source: EAC research

In addition, local capacities are continuously increasing: While current assembly plants rarelyexceed production capacities of 10,000 units, numerous new production facilities with annualcapacities of 40,000–50,000 units are under construction or in planning stage: Within thenext two years new factories by SAIC, FAW, Great Wall, Chery and JAC Motors are planned inThailand, Russia, Mexico, Argentina and Brazil.

8

To achieve better access to local markets and realize considerable cost advantages, mostcompanies to date focus on close cooperation with local partners to build up production,distribution and service networks.

Top 5 Chinese automotive exporters

Source: EAC research

Existing Western cooperation partners are the first choice for Chinese OEMs to open upinternational markets. Thus, SAIC considers using the global service network of Iveco,Dongfeng has signed a service agreement with Cummins for all globally marketed Dongfengvehicles equipped with Cummins engine and Brilliance plans to partner with BMW for distribution,sales and service in the Middle East. But also cooperation with local partners is intended: FAWuses the sales channels of the local distributor Salinas Group in Mexico, produces with the supplierBelayap in Ethiopia and distributes via car dealer Imperial in South Africa.

In the near future, a more independent FDI-driven approach to foreignmarkets is expected from Chinese OEMs. Chang’an Automobile Group plansto build up stand-alone subsidiaries in Russia and Brazil by 2012 and tocreate a network of 100 own 4S Service Centres worldwide. John Deng,Managing Consultant of EAC Shanghai explains: “By choosing a bottom-upstrategy in overseas markets and partnering with local experts, ChineseOEMs are able to achieve a high level of local adaption right from thebeginning. They are now using this first experience to transform theirmarket presence incrementally into an independent production and salesset-up via new investments, especially in other emerging markets.”

9

D. SWOT Analysis in

Global Context

5 The Chinese strengths remain in cost advantages and beneficial domestic market

dynamics, weaknesses include safety and quality features – future market demand in

emerging markets as opportunity

10

6 Chinese internationalization strategies vary: from replication of strengths in

emerging markets, aggressive targeting of low end Western customers to more

incremental, long term global expansion strategies.

Company case I: Chery’s bottom-up internationalization

Founded in 1997, Chery Automobile has quickly grown tobecome one of China’s biggest carmakers. The companycurrently builds about 15 models of passenger cars, minivansand commercial vehicles, including the QQ compact, the A5sedan and V5 crossover. Chery sells ~700,000 vehicles per yearand has a production capacity of 900,000 cars and 400,000 gearboxes per year. The company’s cars are sold under the brandsChery, Karry, Rely, and Riich. A fifth brand, Qoros, is set tolaunch in 2013.

Chery, based in East China’s Anhui province, has set an ambitious overseas sales target of170,000 units for 2012 - Chery exported a record 160,200 vehicles in 2011, maintaining its statusas a leading auto exporter in China.

Chery’s operations go beyond domestic sale and export.The company also produces in 16 locations overseas by usingfree capacities of local manufacturers and produces increasinglytailored vehicles for local customers. Its broad dealershipnetwork spans more than 1,150 dealers in over 80 countries

The company has an increasingly strong footprint inemerging markets. It opened a plant in Venezuela in August2011 and expects to start operations at a second plant currentlyunder construction in Brazil in September 2013. In addition,Chery has announced plans to build assembly plants in Myanmarand several African countries.

So far Chery has followed a bottom-up internationalization strategy with focus on emergingcountries in South America, Asia, Africa and the Middle East. For the planned market entry intoEurope in 2013 Chery has won over a chief designer of Mini as well as a VP of Volkswagen tofacilitate the market entry of the first Chinese five-star Euro NCAP car.

Agreement signing at Chery

production plant in Brazil

11

E. Case Study: Three OEMs –

Three Strategies

E. Case Study: Three OEMs –

Three Strategies

Company case II: Great Wall “going North” from CEE

Great Wall Motor (GWM), based in Chinas Hebei province, had setan overseas sales target of 100,000 units for 2012 implying anincrease of 40% from 2011. Great Wall has established 10 KDproduction bases and over 800 after sales service centres overseas.In 2011 GWM attended 36 auto shows to promote its brand globally.So far GWM sells the three product categories Haval SUV, Great WallPC and Wingle Pickup in 100 countries.

While until 2011 Great Wall used a pure export model, it is now contemplating localization intarget markets, taking Central and Eastern Europe (CEE) as a testing ground for futureexpansion. A major milestone has been achieved in February 2012 with a new CKD plant inLovech, Bulgaria (production capacity 50,000 units) – the first plant of a Chinese automotiveOEM in the European Union. The first locally produced model is the Voleex C10, a small-rangecar designed for the mass market. It is marketed aggressively in Bulgaria with very competitivepricing strategy.

Market offensive CEE: GWM “Made in Bulgaria”

Source: Litex Motors 2012

Great Wall’s strategy is to “go north”: the company has announced plans to sell its Voleex C10model not only in Bulgaria, but also in neighbouring countries Albania, Serbia, Macedonia,Romania, Turkey and other Balkan states. As the first independent auto brand in China its fourmain models passed EU Whole Vehicle Type Approval (WVTA) in 2009. By 2015, GWM plansexpansion into Sweden and Norway, most likely to target the British market and ultimately theGerman market – depending on the outcome of first market experiences.

Apart from its plans for Europe, Great Wall remains focused on sales in its primary market Russia.Here GWM sells 25% of its total export. In addition, GWM has a large logistics hub near Moscow.Other target regions are South America, the Middle East, Africa, Asia and Australia. Two plants arecurrently under construction in Russia and Brazil.

12

Company case III: SAIC’s incremental approach to high-end markets

Shanghai Automotive Industry Corp. is currently China’s largest vehicleproducer with an annual production capacity of 1.3 mio cars and nearly 1mio engines and other parts. In 2011, SAIC Motor sold over 4 mio vehicles,thus keeping its leadership on the domestic automotive market. SAIC islacking behind in foreign sales with only 61,000 exported vehicles linked toits strong domestic market position and little pressure to go abroad. Yet ithas set the ambitious target to sell 800,000 vehicles by 2015overseas alone.

SAIC currently has three overseas assembly plants in the UK, India and Egypt. One plant inthe US and one in Thailand are under construction. SAIC sells its cars under its own brands SAIC,Nanjing, MG, Roewe, SsangYong, Maxus, Yuejin as well as under JV brands Baojun, Buick,Chevrolet, Iveco, Skoda and VW, which are mostly local adaptations of the respective foreignmodel.

For the international market, MG/ Roewe is the only brand based on the originally MG Rovertechnology. In 2011 SAIC launched its European market entry with the model MG6 in theUK, however this has failed so far due to the lack of trust in Chinese-built cars. Hence only 290vehicles from the originally planned 3,000 had been sold in 2011.

The internationalization strategy of SAIC builds on joint ventures and local cooperation. In ChinaSAIC has JVs with VW and GM and will use these JVs as a basis for expansions in the future. SAICis determined to conquer developed markets reflected by its entry into the Australian marketin late 2012. John Deng explains: “SAIC’s technological advantage after the acquisition of Rovertechnology rights in 2005 and its stable domestic market position compensate pressures tointernationalize immediately. It allows for an incremental approach using FDI and local JVs forexpansion into the high-end car segment.”

13

F. Regional Case Study:

Chinese OEMs in Brazil

7 Chinese OEMs pushing aggressively into emerging markets like Brazil – both via

imports and local production, and capitalize on their competence for cars targeting

lower consumer segments

Chinese OEMs’ ambitions beyond the domestic market are mainly directed towards otheremerging markets such as Brazil, where they can benefit from their competitive costadvantage and experience with lower segment consumers. Chinese large-scale activities in theBrazilian market began as late as 2007, when Chery, Lifan and Geely began exports to Brazil asChinese pioneers. After a moderate start, sales kicked off in 2009 and reached a peak in 2011,when Brazil became China’s number one export destination.

While in 2009 Brazil was not represented among the Top 10 Chinese car export markets(below 3% of total Chinese automotive exports), it grew to become No.1 in 2011 (104,000 unitssold, 12.3 % of total Chinese automotive exports). As 2011 was a record year for Chineseautomotive exports overall (850,000 units sold) this fourfold increase in one year becomeseven more meaningful. Additionally, China became the No.1 importer of cars in Brazil,leaving the USA and Japan behind.

Measures

Targets

� Average 35 % tariffs for all imported cars� 65 % local value add required for tariff exemption

� Enforce increased local value add by Western OEMs

� Ease of ‚dumping price‘ pressure by China imports

� Strengthen local OEMs, TIER I and II operations

Recent Brazilian automotive policy changes

Source: EAC Research

14

F. Regional Case Study:

Chinese OEMs in Brazil

However, exports to Brazil are facing increasing restrictions after the Brazilian governmentannounced a raise of import tariffs for all cars to 35 %. Although this is currently on hold furthermeasures in this direction are expected. Import tariffs raise the relative attractiveness oflocal production, which companies like Fiat, Volkswagen and GM have been practicing for a longtime.

As such, Chinese imports will first and foremost be affected by the new policies.European manufacturers like BMW already reacted with increased localization plans –Chinese OEMs are bound to follow.

Chinese OEMs such as JAC Motors and Chery are responding quickly by announcing plans forlocal production in Brazil. Nevertheless, local production alone will not be sufficient in the mid-term – Brazil additionally demands minimum local value add of 65 % to avoid these tariffswhen producing locally.

Chinese OEMs are challenged and will have to develop local TIER I and TIER II supplierstrategies to succeed in Brazil. Chinese JAC Motors for example halted construction of its plantuntil reaching a deal with Brazilian government.

Lars Balzer, EAC Country Expert for Brazil sees strong potential forChinese OEMs in Brazil: “The bold Chinese investment plans for localmanufacturing plants go beyond an impulsive reaction to policy: theyare part of an expansion strategy in the lower-end segment. Bygenerating momentum towards the mid-segment they have the long-term potential to significantly challenge the market position ofWestern and Japanese OEMs.”

The Chinese government supports the OEM’s investment plans inBrazil and recently stated in a press release: „The sale of cars inforeign markets is sometimes connected with a lot of problems.These include transportation costs, import customs and competitionwith the local automotive industry. With production and developmentabroad these problems can be solved. At the same time we areproviding new workplaces, tax money and we bring new technologieswith us. This is the reason why we receive support, for examplefor the construction of new manufacturing facilities in Brazil. “

15

G. Future Growth

Targets and Trends

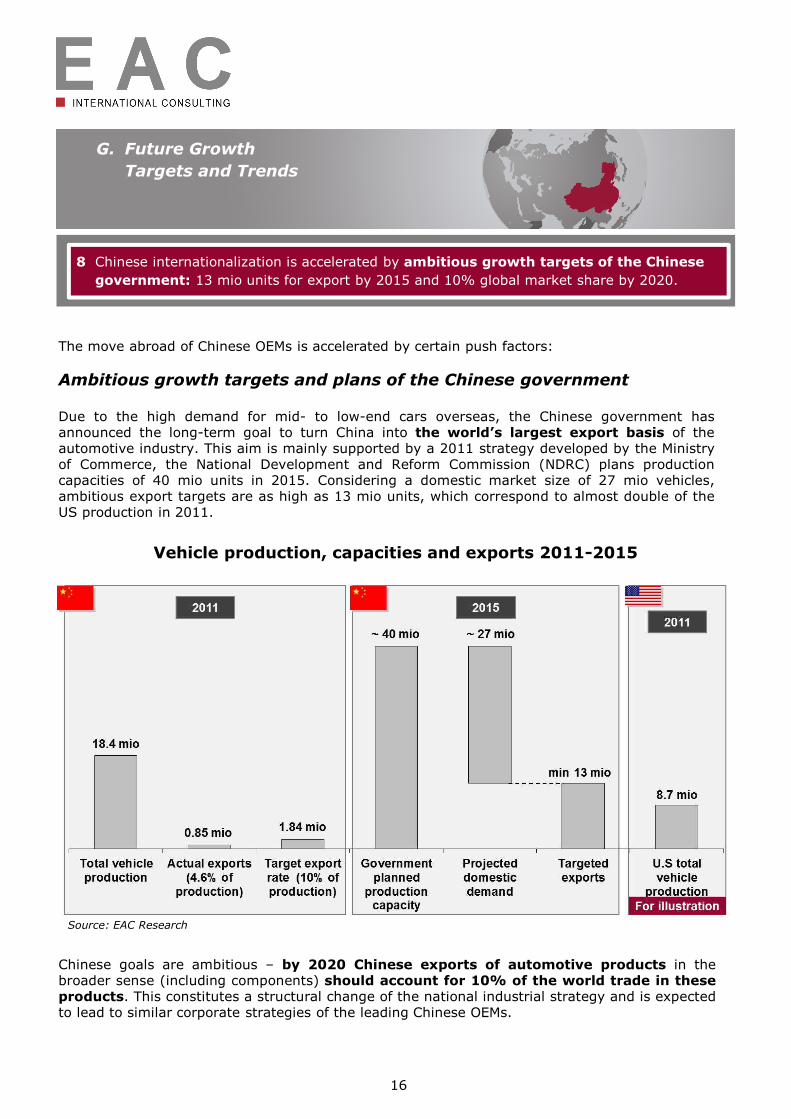

8 Chinese internationalization is accelerated by ambitious growth targets of the Chinese

government: 13 mio units for export by 2015 and 10% global market share by 2020.

The move abroad of Chinese OEMs is accelerated by certain push factors:

Ambitious growth targets and plans of the Chinese government

Due to the high demand for mid- to low-end cars overseas, the Chinese government hasannounced the long-term goal to turn China into the world’s largest export basis of theautomotive industry. This aim is mainly supported by a 2011 strategy developed by the Ministryof Commerce, the National Development and Reform Commission (NDRC) plans productioncapacities of 40 mio units in 2015. Considering a domestic market size of 27 mio vehicles,ambitious export targets are as high as 13 mio units, which correspond to almost double of theUS production in 2011.

Vehicle production, capacities and exports 2011-2015

Source: EAC Research

Chinese goals are ambitious – by 2020 Chinese exports of automotive products in thebroader sense (including components) should account for 10% of the world trade in theseproducts. This constitutes a structural change of the national industrial strategy and is expectedto lead to similar corporate strategies of the leading Chinese OEMs.

16

G. Future Growth

Targets and Trends

9 Other internationalization push factors of include intensified domestic competition

and upgrade of Chinese OEMs innovation ability

Increase in domestic competition

The high competition of international OEMs in the domestic markets is a factor that drivesChinese manufactures overseas. According to an international TIER I supplier in China „a largenumber of Chinese OEMs are currently not even competitive enough in their domestic market.Only their comparatively low pricing keeps market shares up; in the fields of technology,innovation and product quality they are lagging behind considerably.”

Chinese consumers are becoming increasingly interested in mid-ranged cars with a serious brandimage, a field in which Chinese OEMs cannot compete with international players: „Only first timecar buyers purchase Chinese vehicles - as soon as income levels increase consumers switch tointernational brands.”

Upgrade of Chinese OEMs innovation ability

Chinese car manufacturers go to great lengths to place international investments to furtherdevelop their design, research and development competencies. In the long run they not only aimat exporting Chinese models but also to localize their cars. The build-up of R&D facilities aroundthe world mainly focuses on industrialized countries: Chang’an, SAIC, BAIC and JAC Motors haveestablished R&D facilities in Europe, the USA and Japan to improve their product qualities. Lifanis the only company that established a Joint-Venture in the Brazilian market (70 mio USDinvestment) for the development of compact cars.

The expansion policy includes the gradual acquisition of Western companies. The goal of theacquisition of Volvo by Geely is to build up their brand as a leading Chinese manufacturer for thepremium segment and to gain Western technology.

A strategic target is to establish one Chinese automotive manufacturer in the world’s Top 10by 2016. Hence, several governmental departments declared Chinese car manufacturers Chery,Geely, FAW and Yutong – to called pilot projects which are entitled to governmental subsidies todevelop their brand and product portfolios.

17

H. Outlook and Impact

on International

Automotive Suppliers

10 Internationalization will provide mid- to long-term supply opportunities for

international suppliers to Chinese OEMs abroad: “access locally, supply globally”

In China’s domestic market, local car manufacturers currently show deficits in competing withglobal car manufacturers in multiple market segments. The situation in South America and Russiashows that Chinese providers were able to take away market shares from establishedOEMs, based on a rise in exports and local production. The new competition will put furtherpressure on the margins within the lower price segments.

Key questions remain: to what extent can this business model become profitable and whenwill the actual “break even” of investments be reached for Chinese players? The Chinesegovernment already declared its concern that an intense competition amongst Chinesemanufacturers already significantly reduced the margins within the export business. Accordingto Chinese customs the average price of Chinese mid-range cars was reduced by 1.5% in 2011,Minibuses by 0.8%.

In the long run the success of internationalization efforts of Chinese OEMs will depend on theability to enhance their technical and technological skill set. Thus Geely, BYD and others haveso far not been able to penetrate Western European and North American markets despite theirambitious plans. The advancement in these regions will significantly be influenced by theacquisition of Western know-how via strategic alliances or M&A. The most prominent caseto date has been Geely’s acquisition of car manufacturer Volvo. Volvo competitor Saab has alsotemporarily been a potential target for Chinese manufacturers.

An imminent advancement of Chinese manufacturers into the world’s automotive top league isunlikely, especially due to the lack of trust among potential customers - Chinese OEMs lackbrand image and references to gain market shares outside of the low budget price segment. Thegradual expansion of Chinese OEMs in the international sphere nonetheless implies an emergingopenness towards international automotive suppliers to enhance vehicle quality and brandimage, but also to fulfil localization requirements, reduce delivery times and costs.

Therefore, a focused build-up of a Chinese customer structure in China is an interestingoption for international automotive suppliers to consider. Once Chinese companies start fulllocalisation abroad and considerably increase production volume, international suppliers canleverage their Chinese customer relations to supply Chinese OEMs abroad as well: “Localaccess, global supply”.

19

H. Outlook and Impact

on International

Automotive Suppliers

Partners &

Principals

Headquarter (Munich):

China:

India: Russia: Brasil:

20

Partners &

Principals

EAC- Euro Asia Consulting PartGHeimeranstrasse 3780339 Munich / GermanyP: +49-89-922993-0 / F: +49-89-922993-33E-mail: [email protected]

EAC- Euro Asia Consulting

Sunyoung Centre, Rm. 1702

398 Jiangsu Road

200050 Shanghai / China

P: +86-21-6350 8150 / F: +86-21-3250 5960

E-mail: [email protected]

www.eac-consulting.cn

EAC- Euro Asia Consulting Pvt. Ltd.

306-310, Peninsula Plaza, A/ 16,

Veera Industrial Estate

Off New Link Road, Andheri (West)

400 053 Mumbai / India

P: +91-22-2674 2491 / F: +91-22-2674 2481

E-mail: [email protected]

www.eac-consulting.in

Changzhou Euro Asia Consulting

Building No.2, Tenglong Road

Wujin Economic Development Zone

Changzhou / Jiangsu Province / China

P: +86-21-6350 8150 / F: +86-21-3250 5960

E-mail: [email protected]

www.eac-consulting.cn

Related Documents