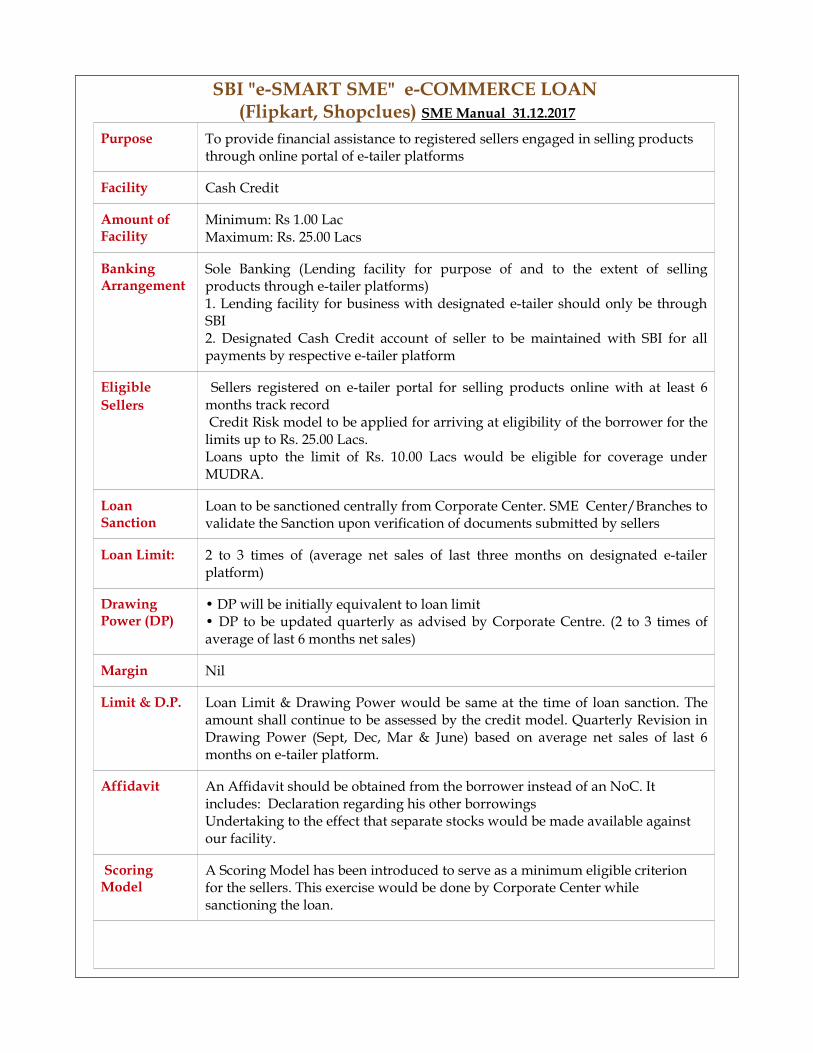

e-handout on SME ASSET PRODUCTS (updated as on 30.04.2019) Prepared by ANV Subbarao Chief Manager (Training) SBILD, Masulipatnam Please note that wherever circular reference no(s) are given in this e-handout, please click there (hyper-link) to get the circular soft copy for ready reference.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

e-handout onSME ASSET PRODUCTS

(updated as on 30.04.2019)

Prepared by ANV Subbarao

Chief Manager (Training)SBILD, Masulipatnam

Please note that wherever circular reference no(s) are given in this e-handout,please click there (hyper-link) to get the circular soft copy for ready reference.

INDEXSL.NO. NAME OF PRODUCT/SCHEME PAGE NO (S)

1 SBI ASSET BACKED LOAN (ABL)7,8,92 SBI ASSET BACKED LOAN (CRE-CP)

3 SIMPLIFIED SMALL BUSINESS LOAN (SSBL) 10

4 SBI CORPORATE HOME LOAN 11

5 SME CREDIT CARD 12

6 SME SMART SCORE13, 147 SME CREDIT PLUS SCHEME

8 DAL MILL PLUS15, 169 COTTON GINNING PLUS

10 DOCTOR PLUS17, 1811 MEDICAL EQUIPMENT FINANCE SCHEME

12 LEASE RENTAL DISCOUNTING SCHEME 19, 20

13 SBI CONSTRUCTION EQUIPMENT LOAN21, 2214 SBI FLEET FINANCE SCHEME

15 ELECTRONIC DEALER FINANCE SCHEME (E-DFS) 23, 24, 25

16 MORTGAGE DEALER FINANCE SCHEME (M-DFS) 26, 27

17 DROP LINE OD FOR DEALERS UNDER E-DFS & M-DFS 28, 29

18 ELECTRONIC VENDOR FINANCING SCHEME (E-VFS) 30, 31, 32

19 E-SMART SME, E-COMMERCE LOANS (Flipkart, Shopclues) 33, 34

20 CORPORATE RETAIL TIE-UP for Financing Commercial Vehicle and Construction Equipment

35

21 TAXI AGGREGATOR SCHEME (OLA, UBER & ECORENTACAR) 36, 37

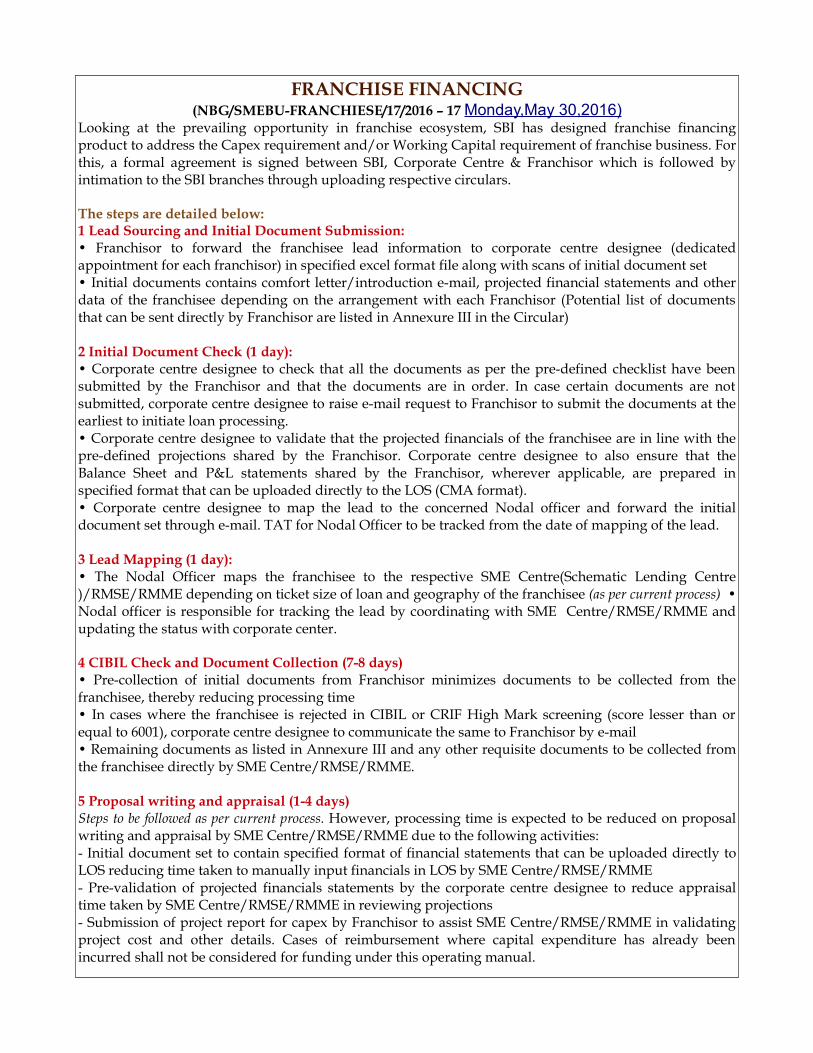

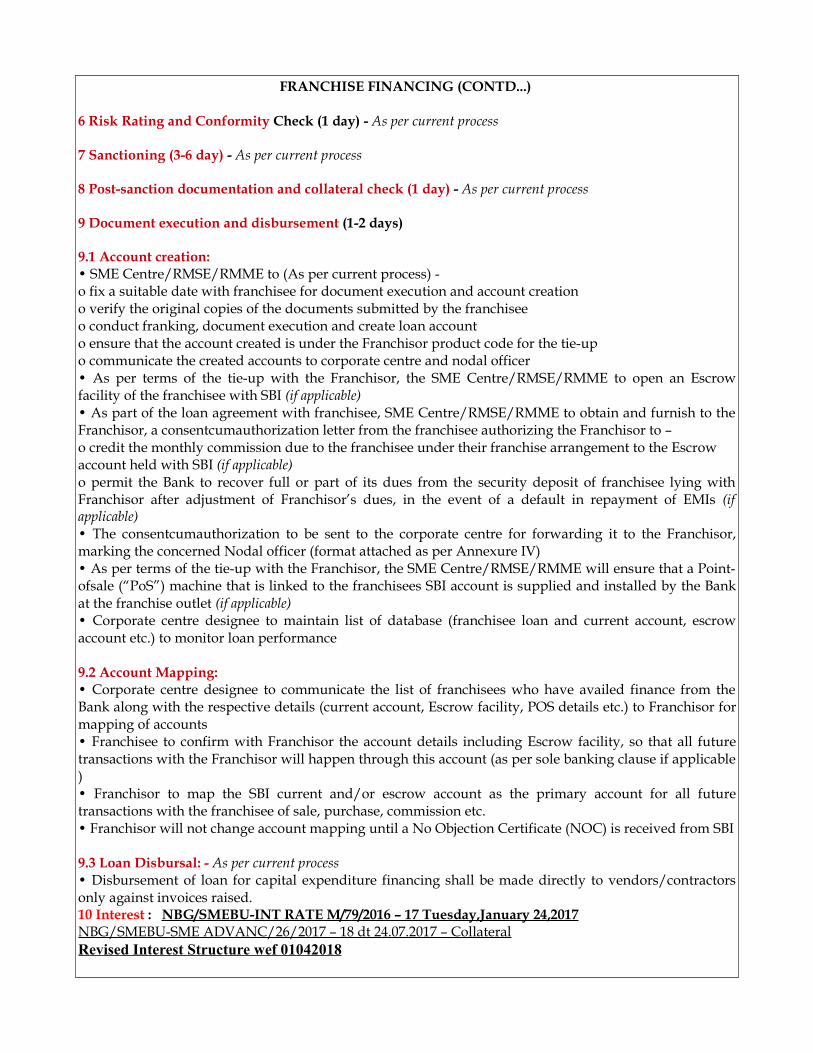

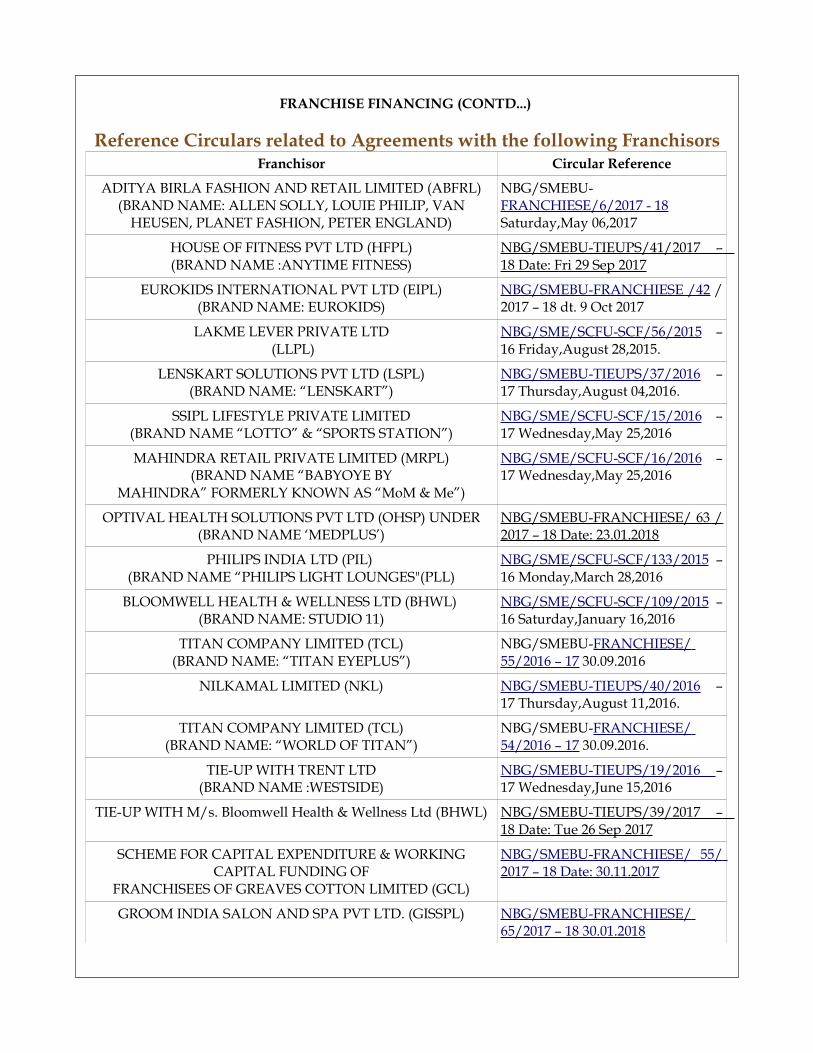

22 FRANCHISE FINANCING 38, 39, 40

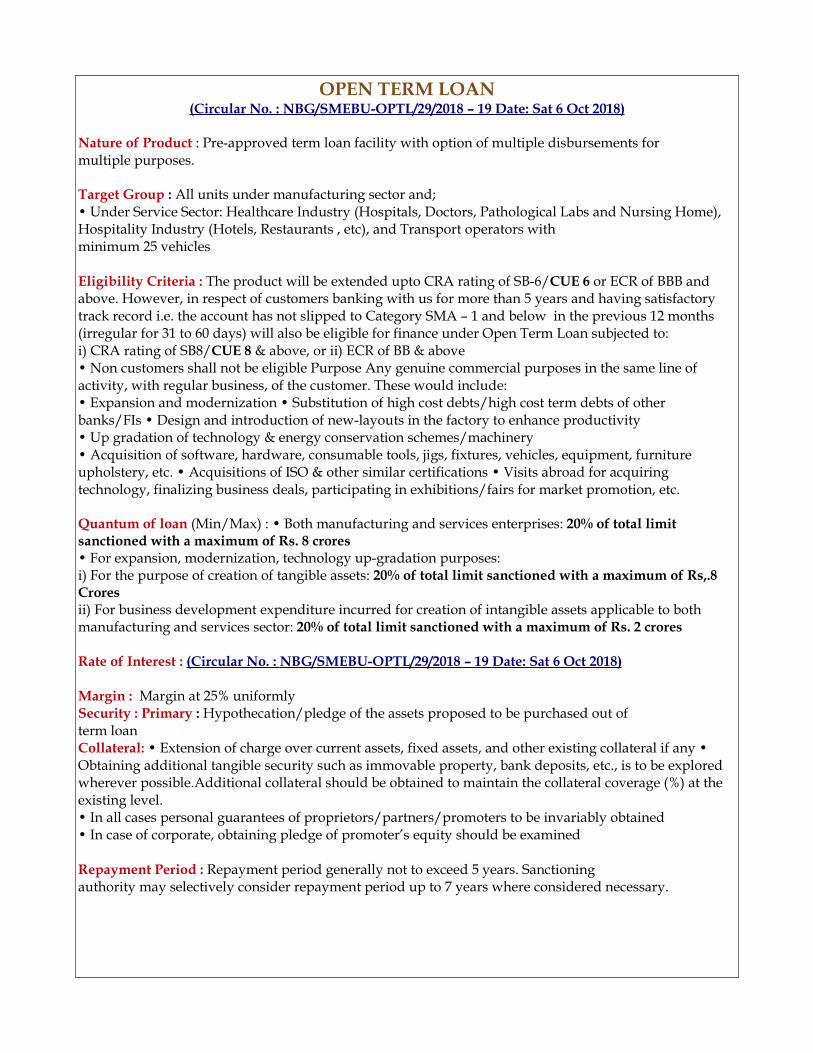

23 OPEN TERM LOAN 41

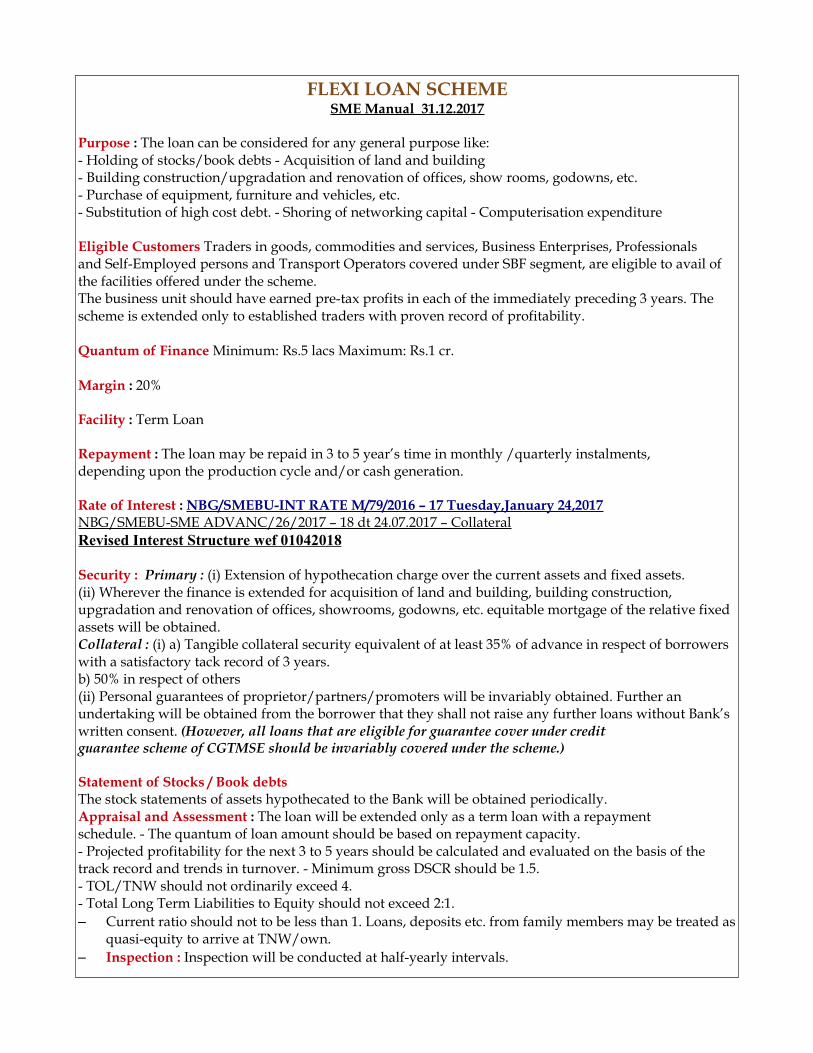

24 FLEXI LOAN 42

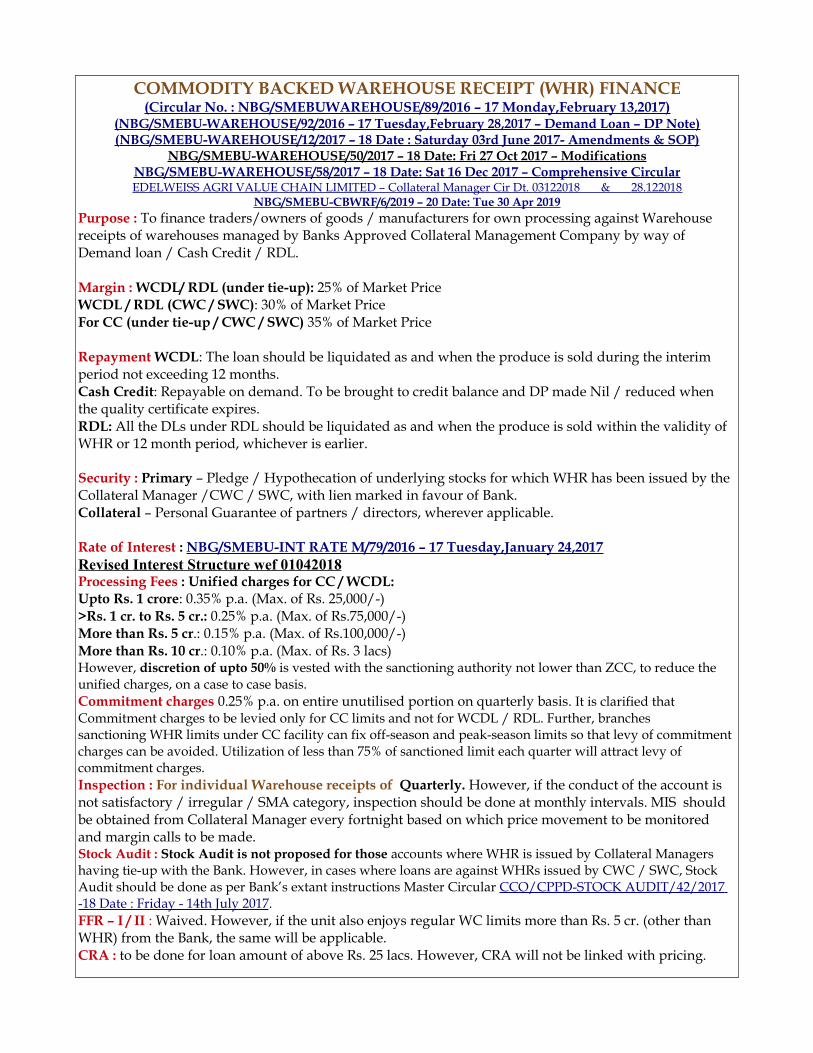

25 FINANCING AGAINST WAREHOUSE RECEIPTS 43

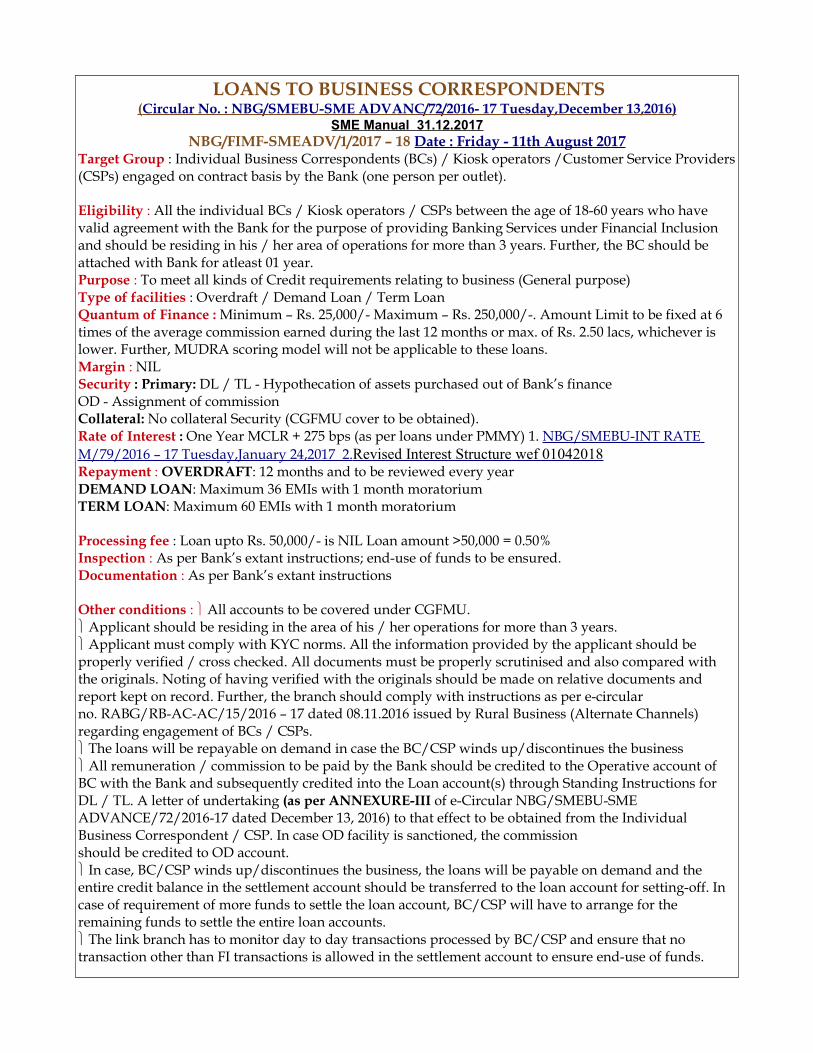

26 LOANS TO BUSINESS CORRESPONDENTS (BCs) 44

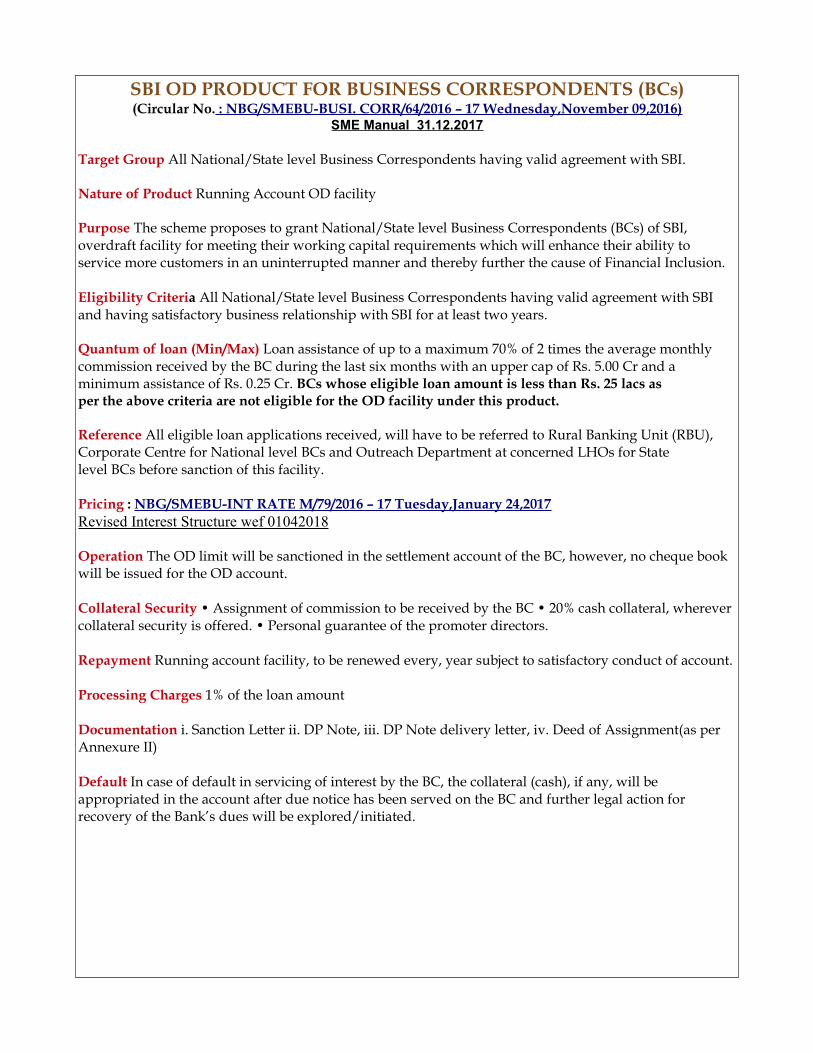

27 SBI OD FOR BUSINESS CORRESPONDENTS (BCs) 45

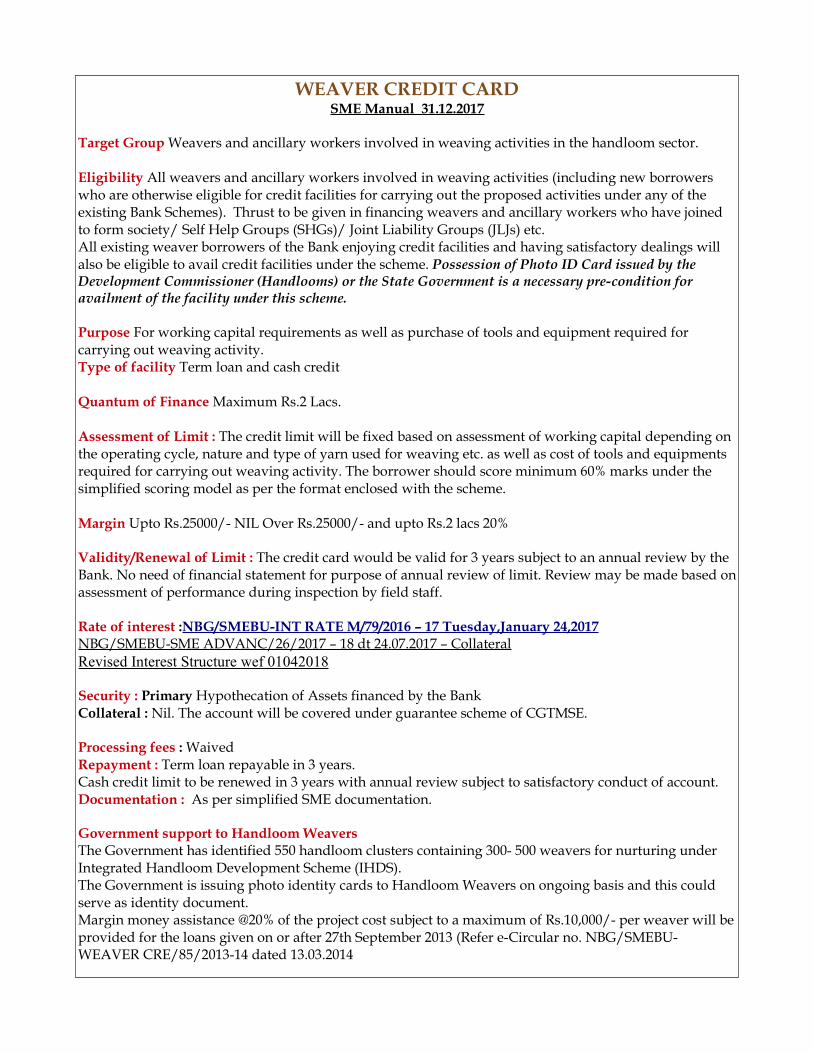

28 WEAVERS CREDIT CARD (PMMY) 46

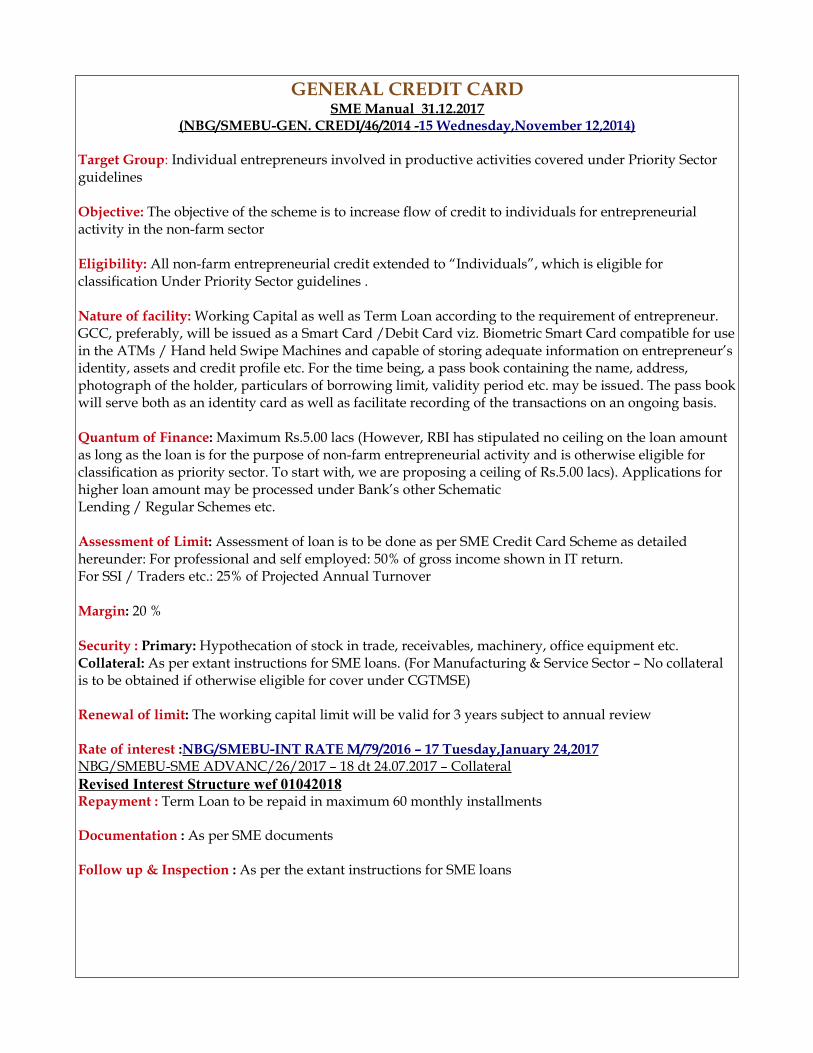

29 GENERAL CREDIT CARD 47

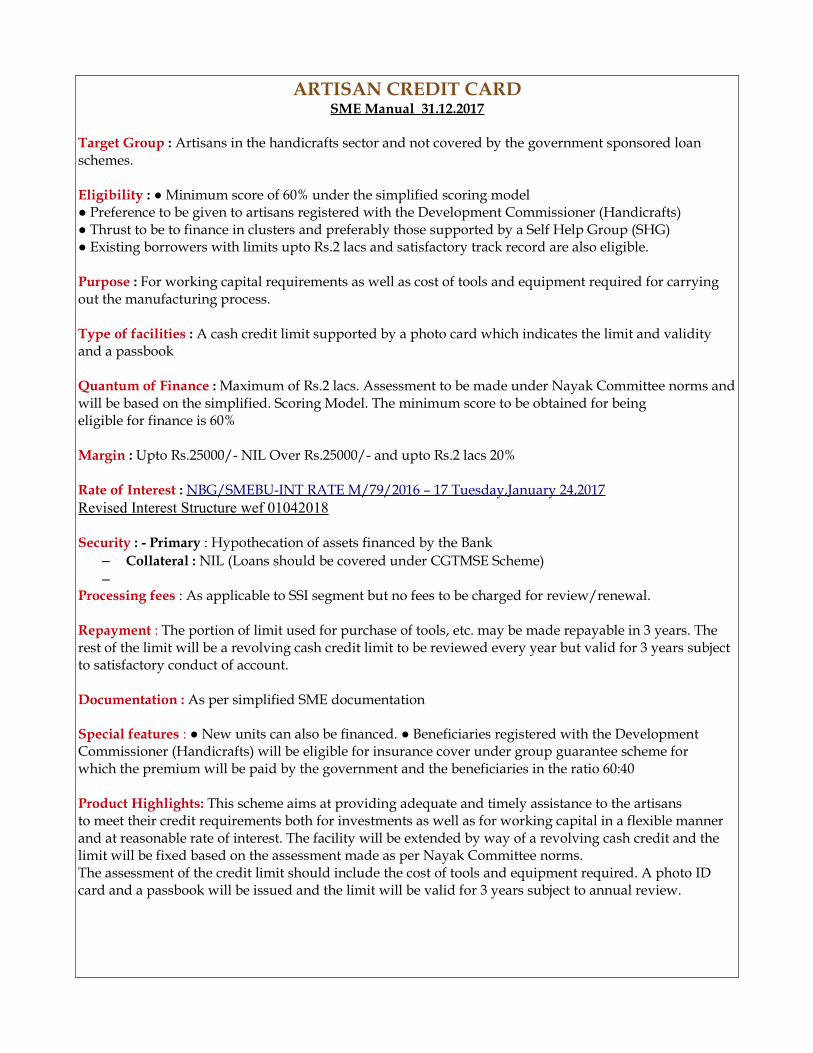

30 ARTISAN CREDIT CARD 48

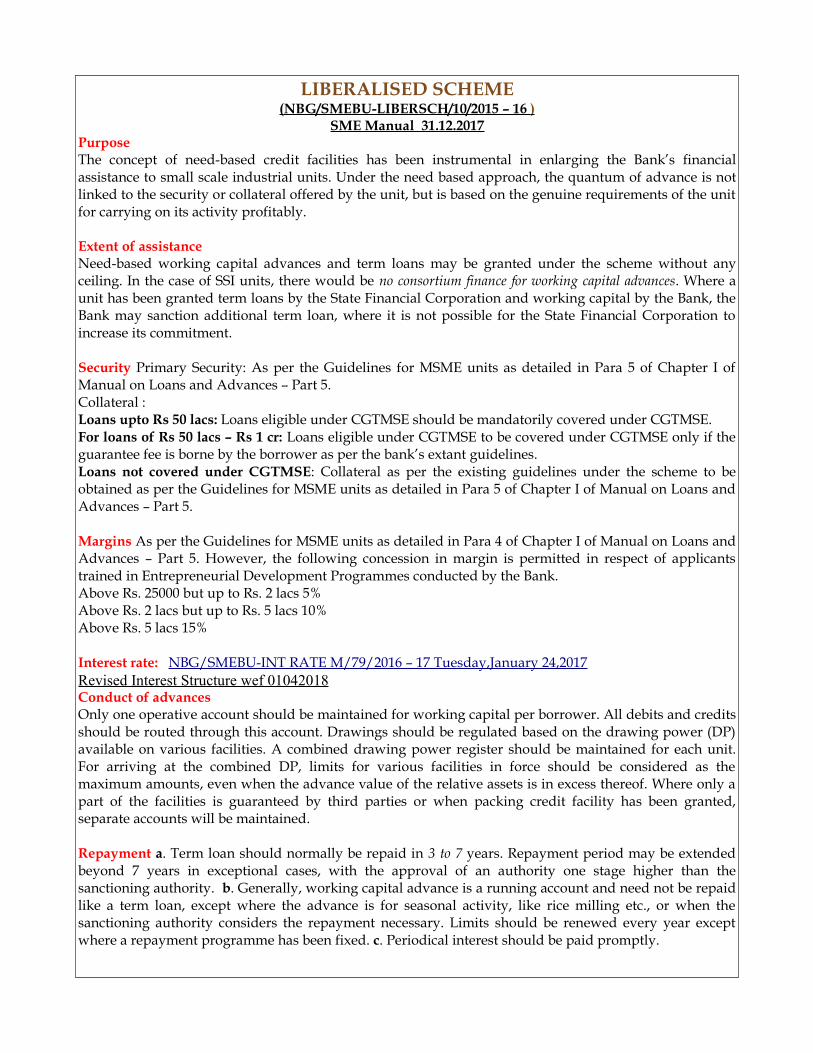

31 LIBERALISED SCHEME 49

32 STAND BY LINE OF CREDIT FOR W/C REQUIREMENT 50, 51

33 FLEXI LOAN FOR TRADE & SERVICES SECTOR 52, 53

34 CONSULTANCY SERVICES CELL & PROJECT UPTECH 54, 55

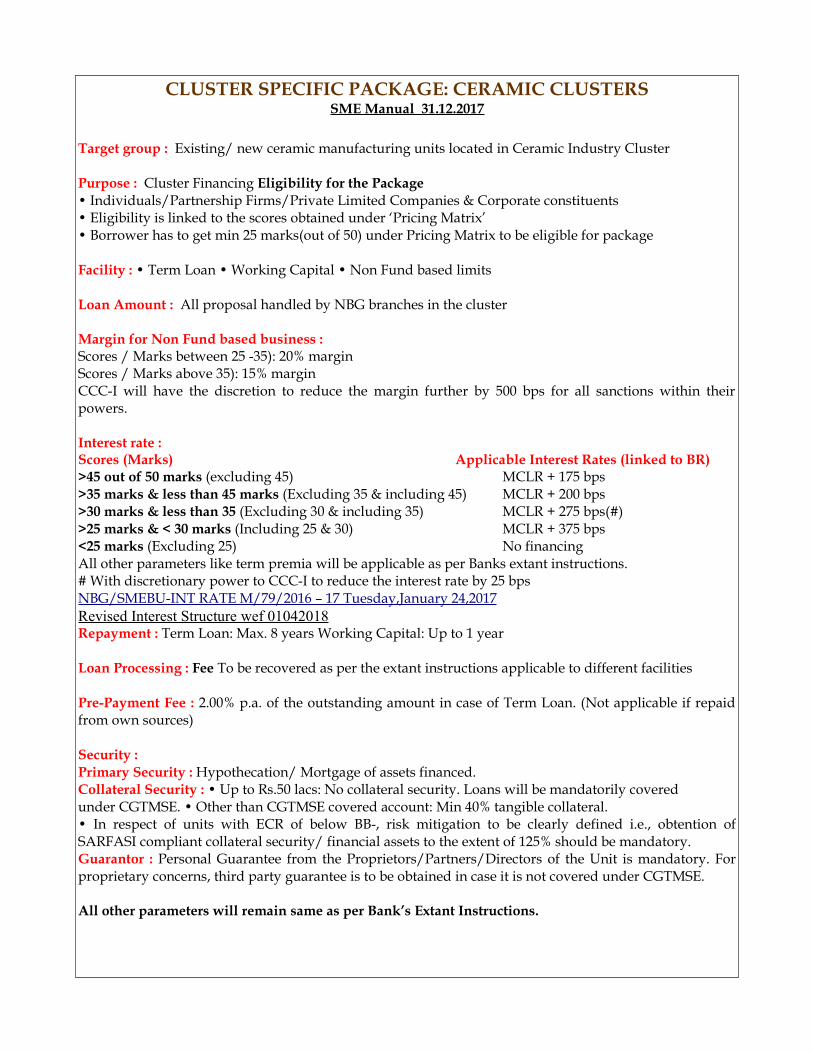

35 CLUSTER SPECIFIC PACKAGE: CERAMIC CLUSTERS 56

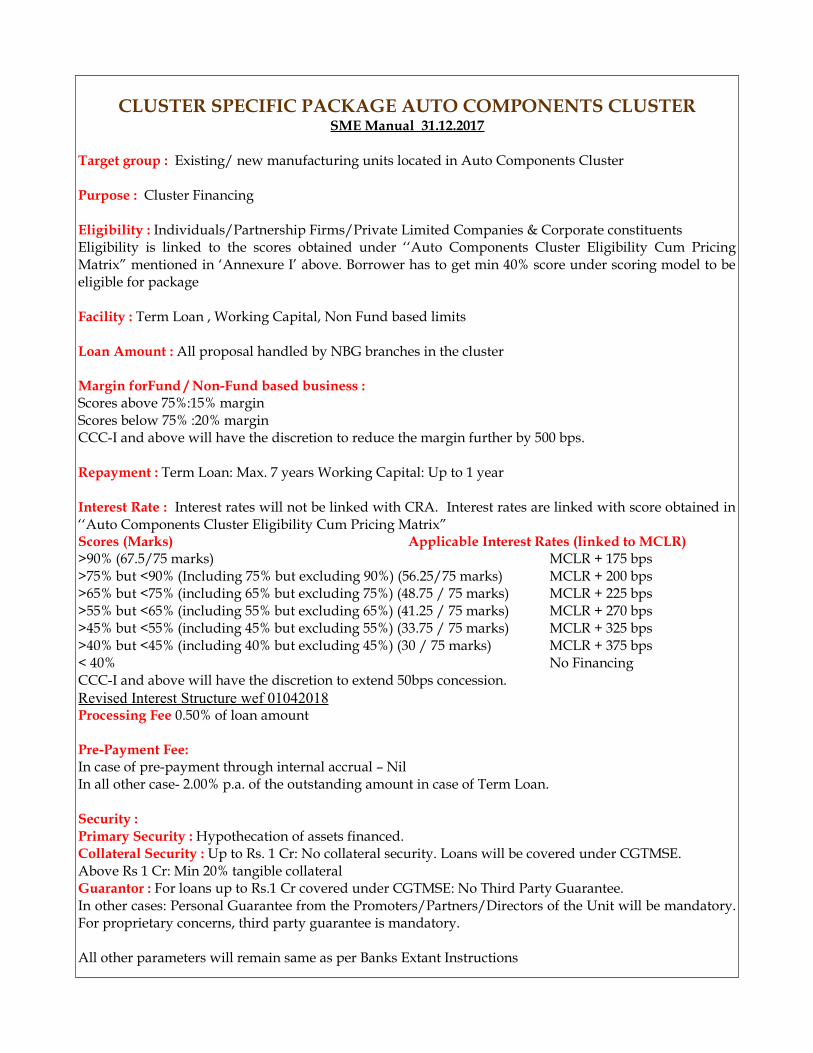

36 CLUSTER SPECIFIC PACKAGE AUTO COMPONENTS CLUSTER 57

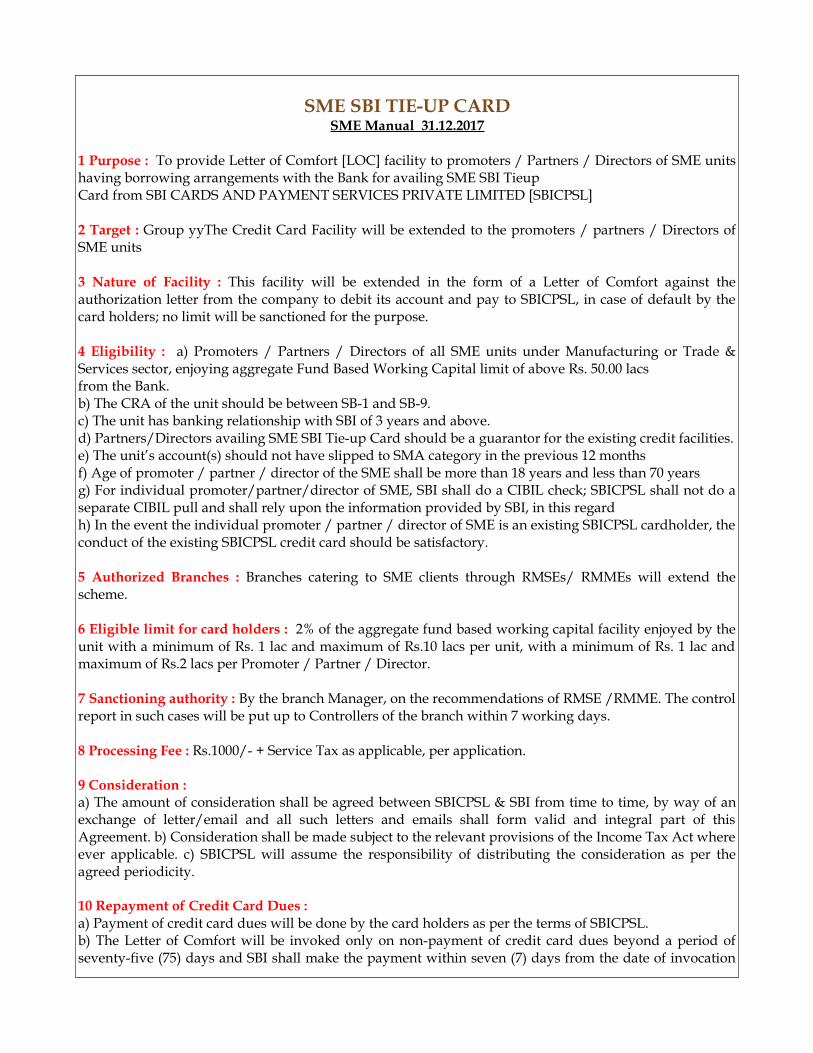

37 SME SBI TIE-UP CARD 58, 59

38 SBLC BACKED FINANCING FOR JAPANESE CORPORATES 60, 61

39 CAPEX FUNDING FOR DEALERS OF IOCL 62

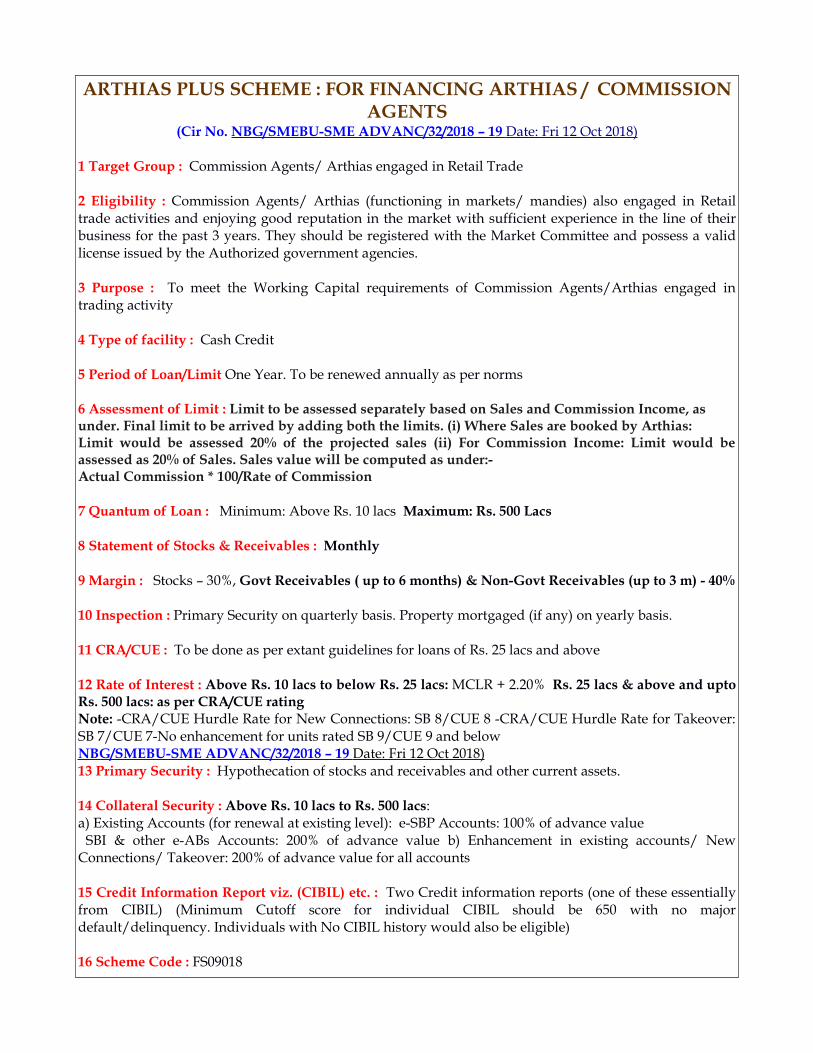

40 ARTHIAS PLUS SCHEME : FOR FINANCING ARTHIAS/ COMMISSION AGENTS (Revised wef 12102018)

63

INDEX SL.NO. NAME OF PRODUCT/SCHEME PAGE NO (S)

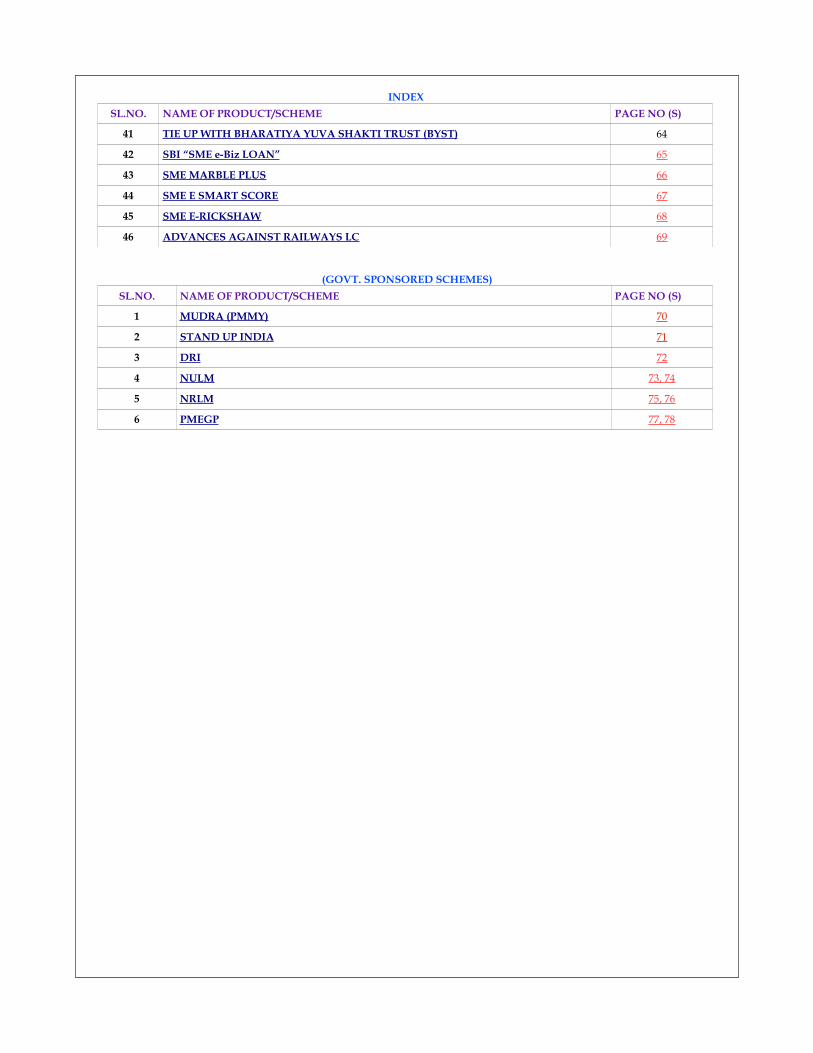

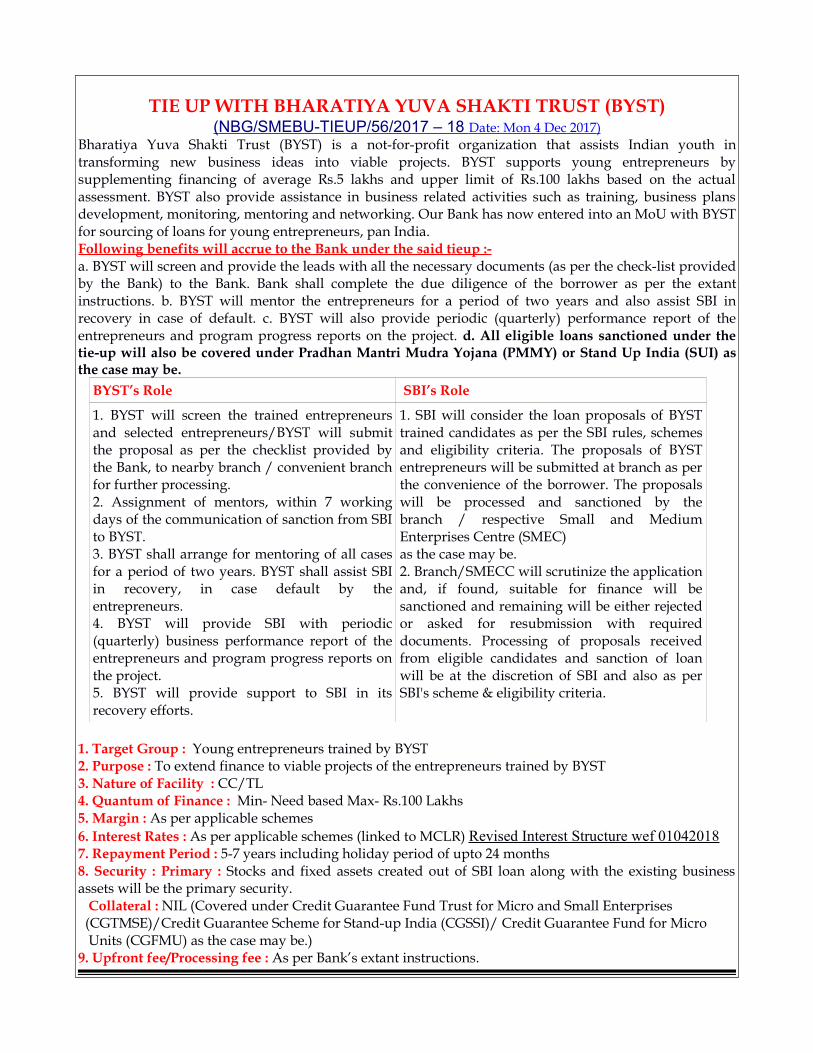

41 TIE UP WITH BHARATIYA YUVA SHAKTI TRUST (BYST) 64

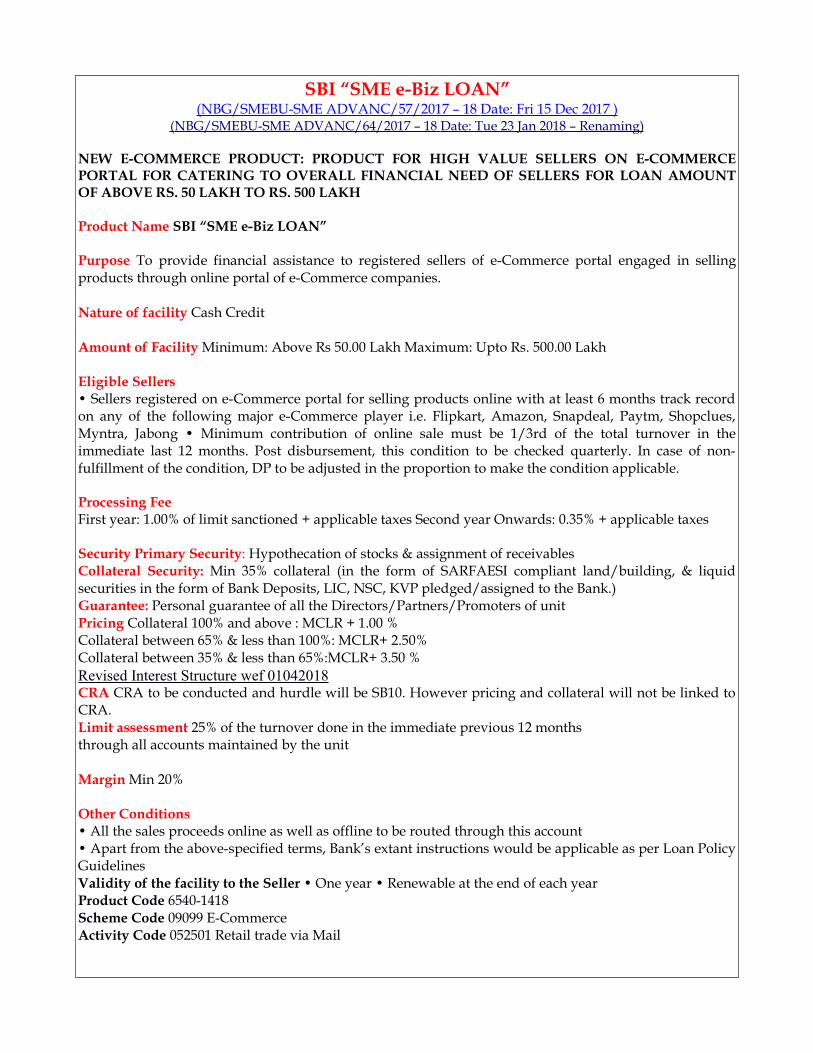

42 SBI “SME e-Biz LOAN” 65

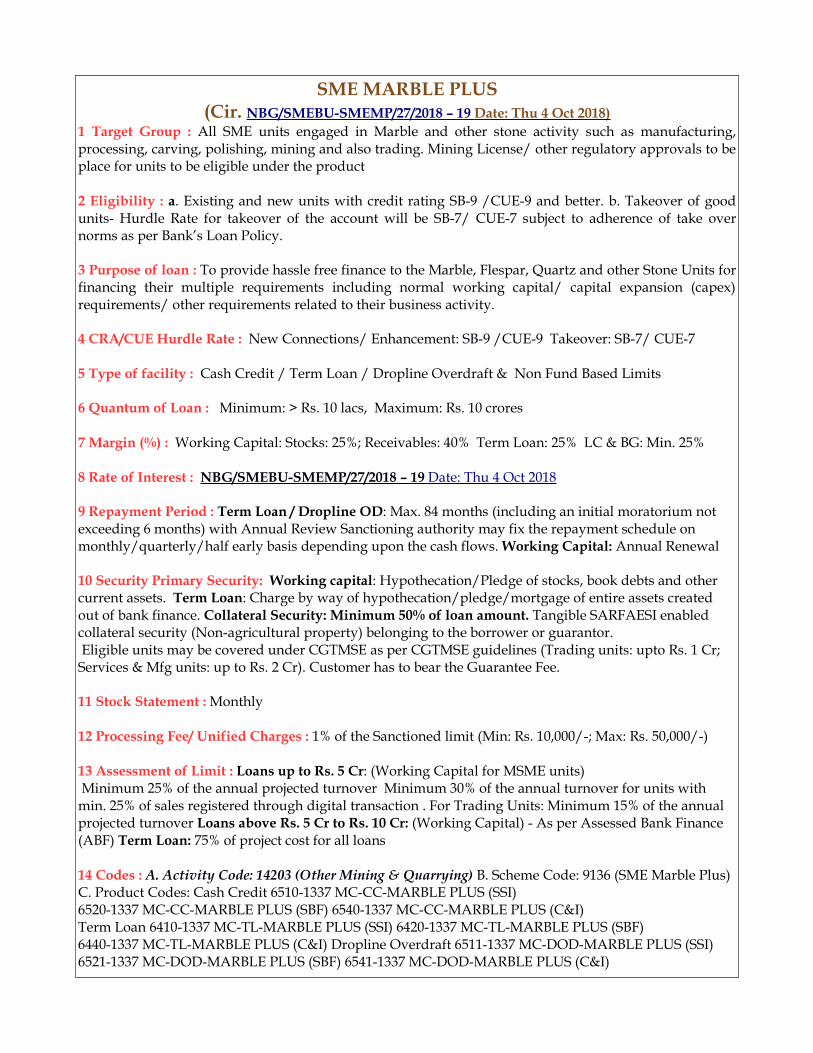

43 SME MARBLE PLUS 66

44 SME E SMART SCORE 67

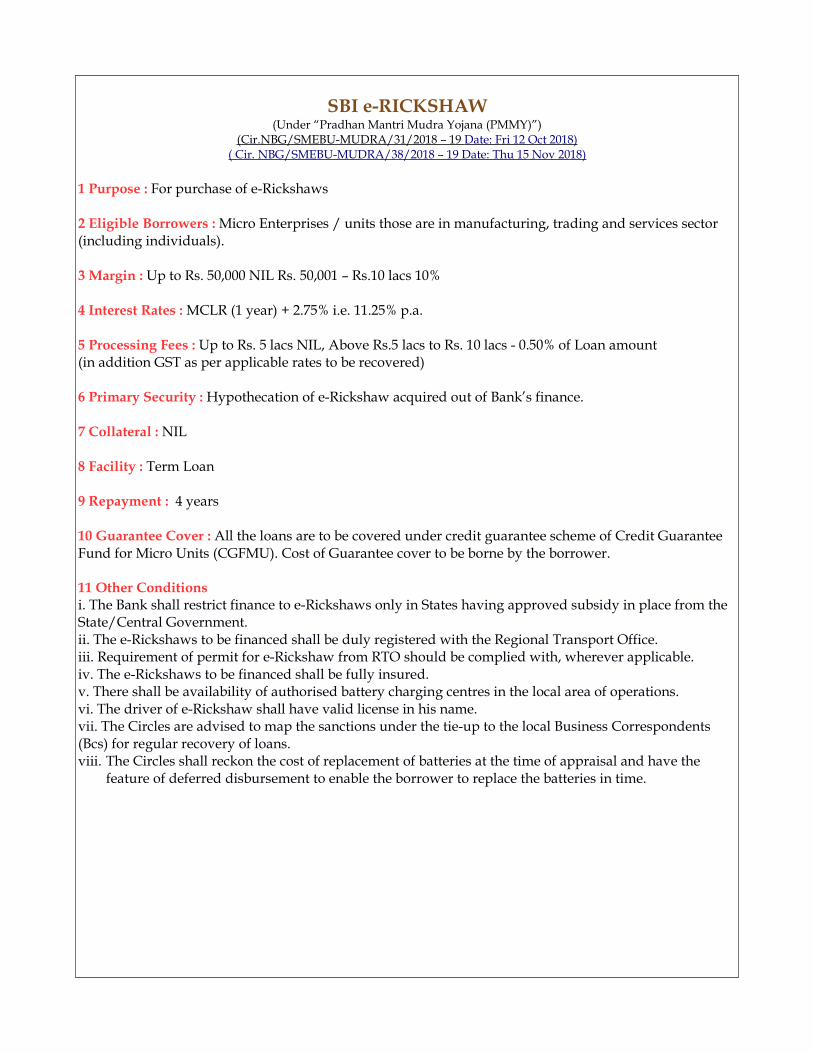

45 SME E-RICKSHAW 68

46 ADVANCES AGAINST RAILWAYS LC 69

(GOVT. SPONSORED SCHEMES)SL.NO. NAME OF PRODUCT/SCHEME PAGE NO (S)

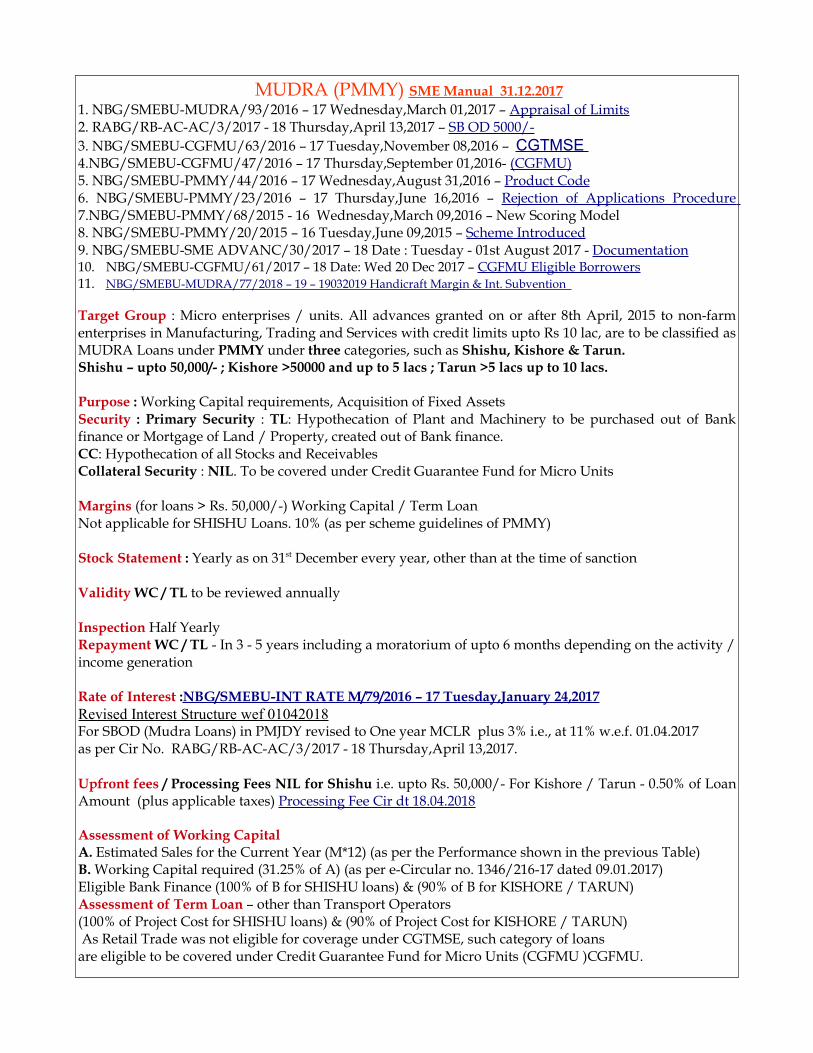

1 MUDRA (PMMY) 70

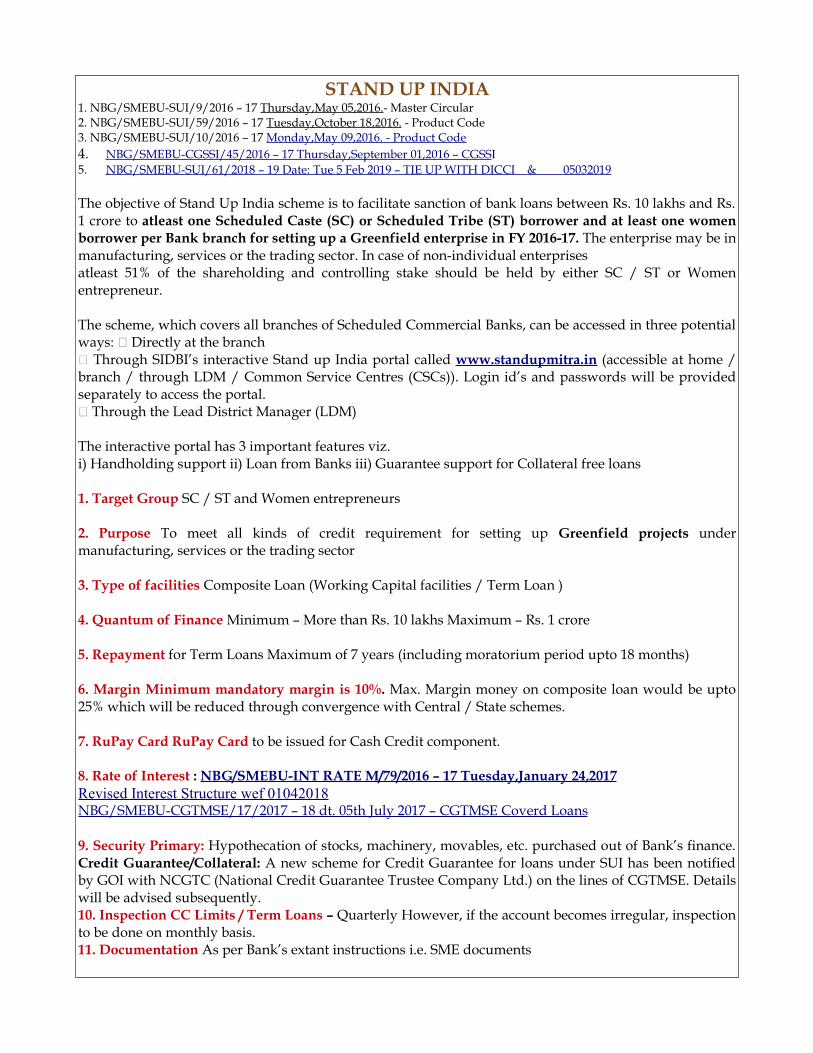

2 STAND UP INDIA 71

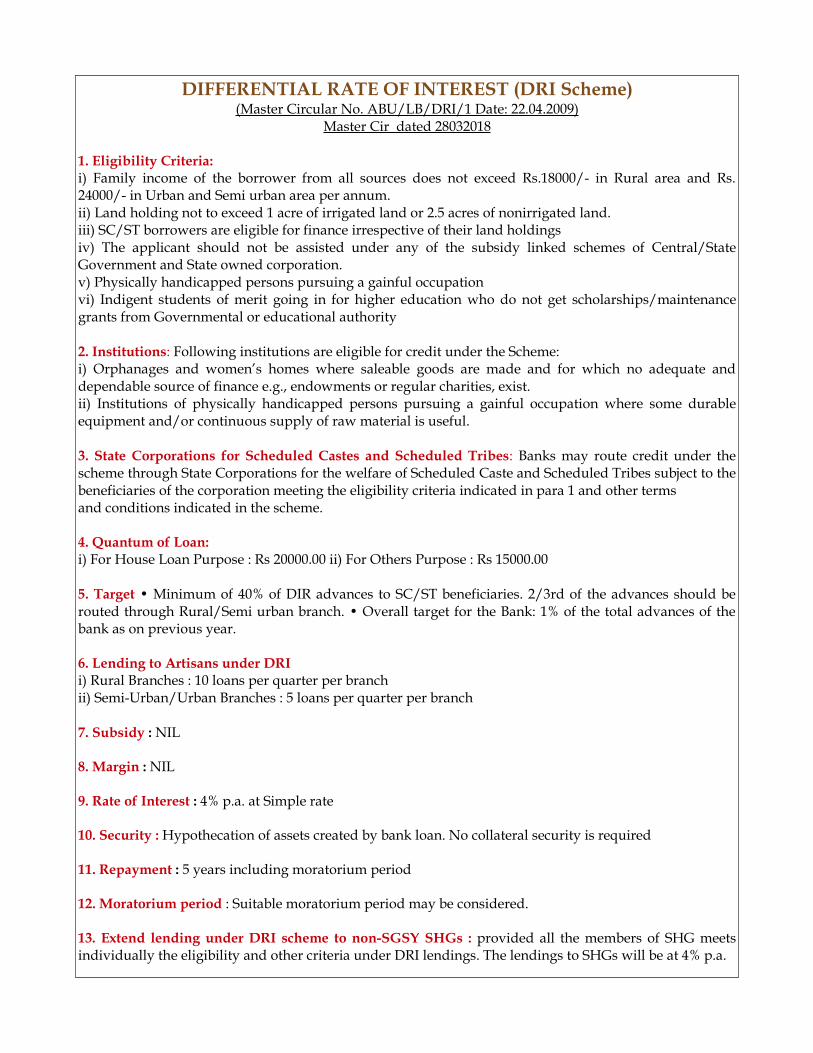

3 DRI 72

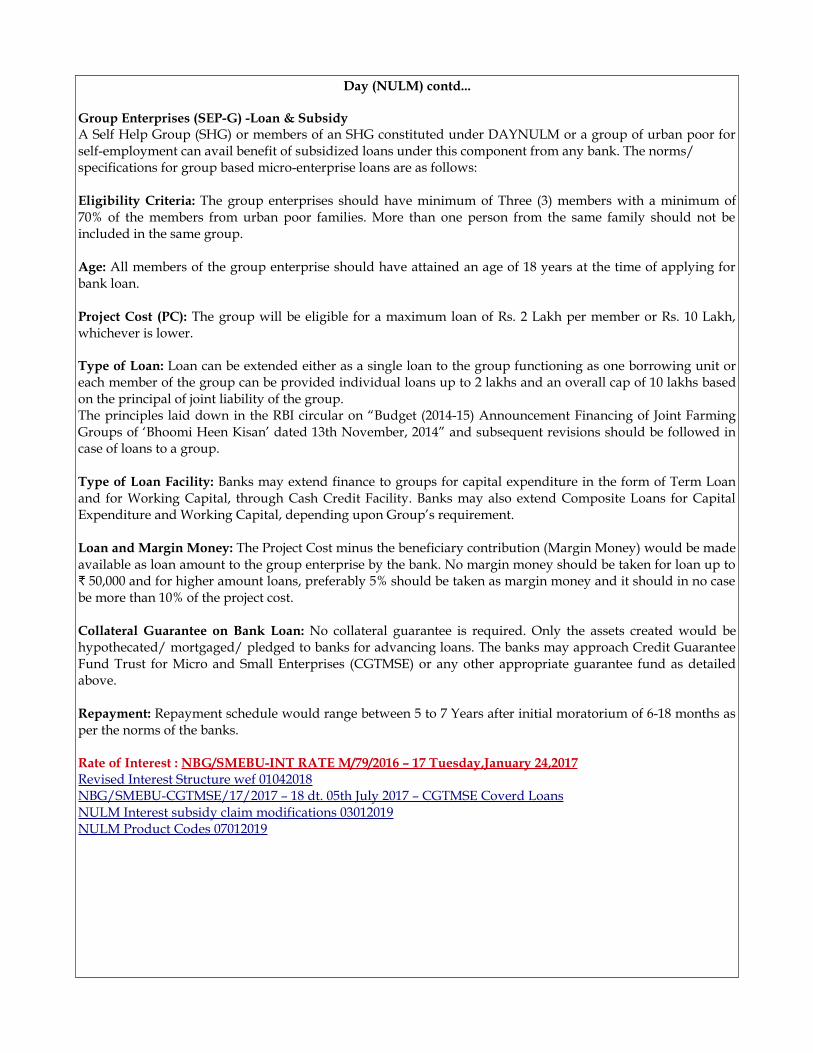

4 NULM 73, 74

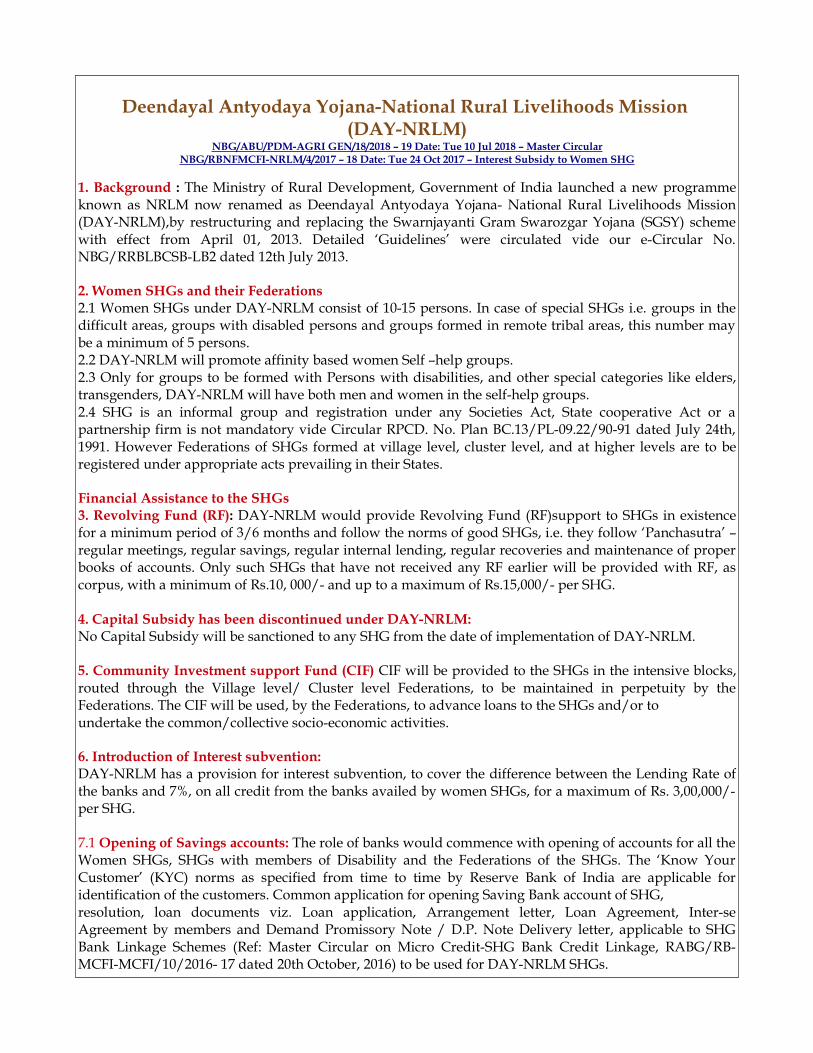

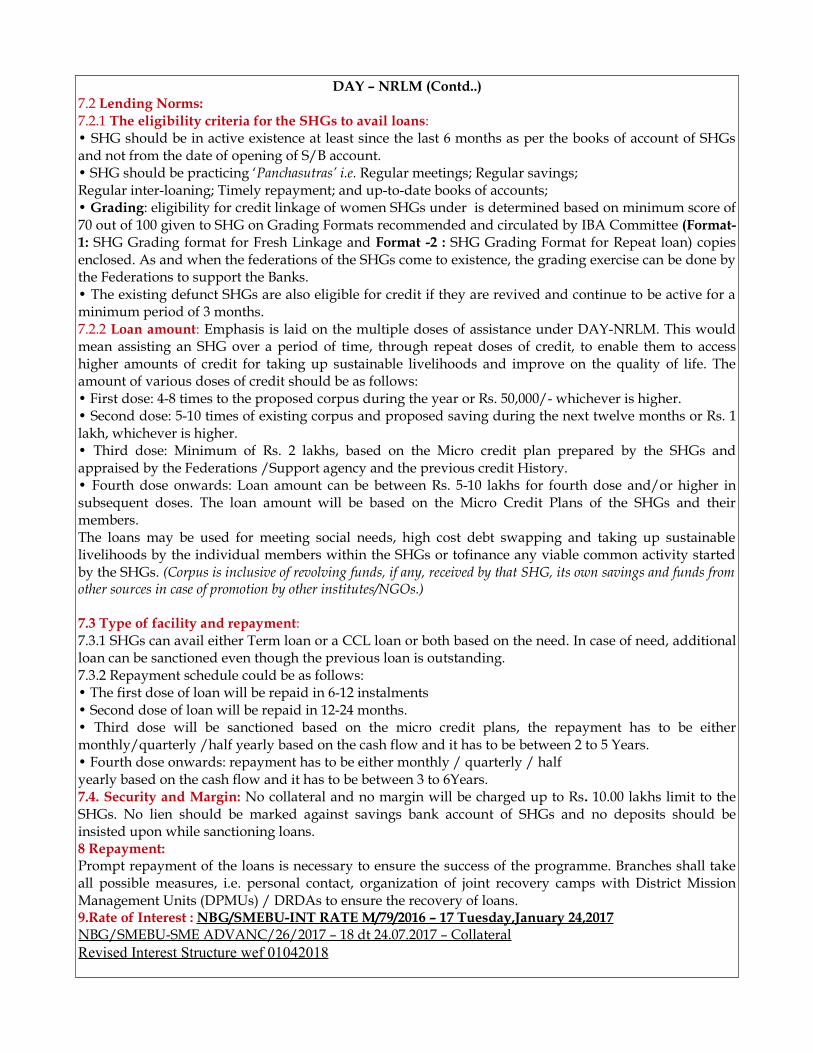

5 NRLM 75, 76

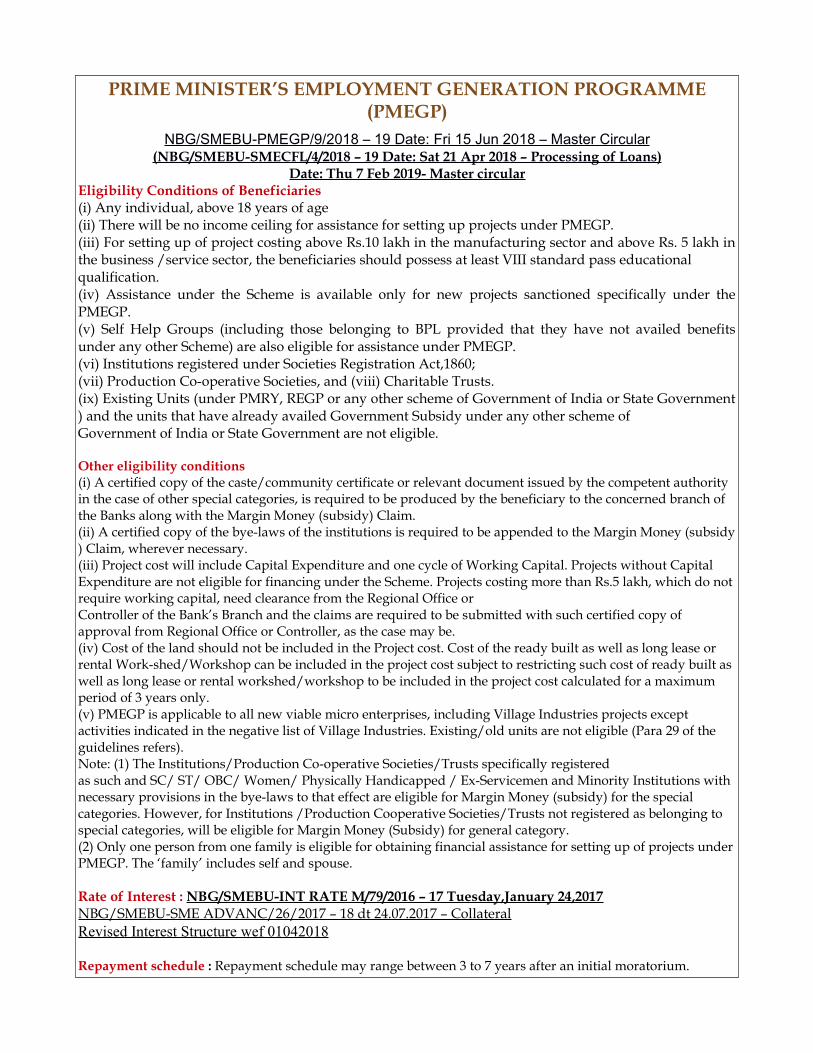

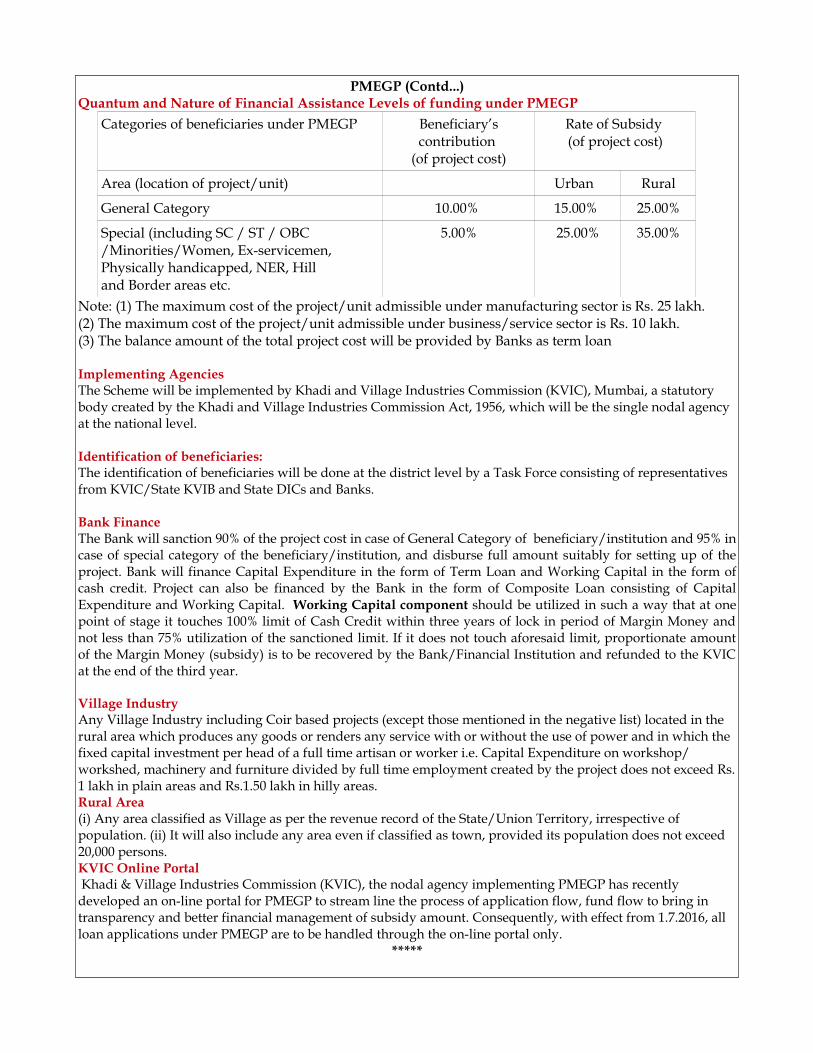

6 PMEGP 77, 78

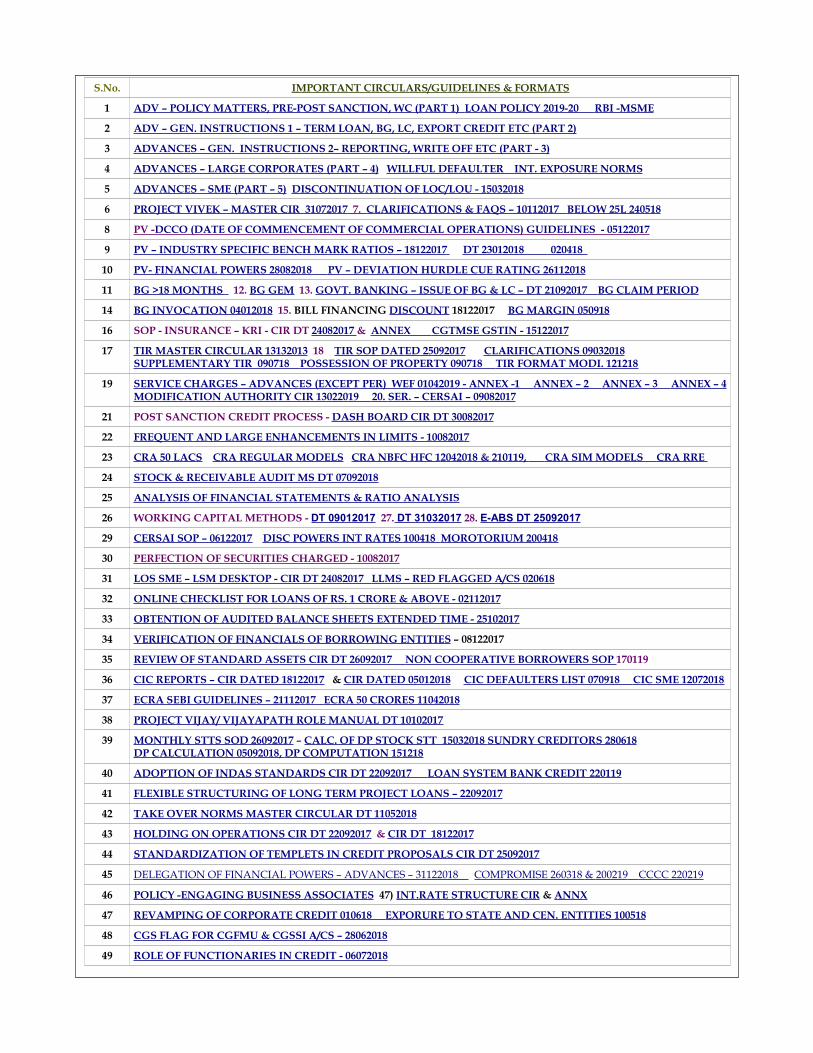

S.No. IMPORTANT CIRCULARS/GUIDELINES & FORMATS

1 ADV – POLICY MATTERS, PRE-POST SANCTION, WC (PART 1) LOAN POLICY 2019-20 RBI -MSME

2 ADV – GEN. INSTRUCTIONS 1 – TERM LOAN, BG, LC, EXPORT CREDIT ETC (PART 2)

3 ADVANCES – GEN. INSTRUCTIONS 2– REPORTING, WRITE OFF ETC (PART - 3)

4 ADVANCES – LARGE CORPORATES (PART – 4) WILLFUL DEFAULTER INT. EXPOSURE NORMS

5 ADVANCES – SME (PART – 5) DISCONTINUATION OF LOC/LOU - 15032018

6 PROJECT VIVEK – MASTER CIR 31072017 7. CLARIFICATIONS & FAQS – 10112017 BELOW 25L 240518

8 PV - DCCO (DATE OF COMMENCEMENT OF COMMERCIAL OPERATIONS) GUIDELINES - 05122017

9 PV – INDUSTRY SPECIFIC BENCH MARK RATIOS – 18122017 DT 23012018 020418

10 PV- FINANCIAL POWERS 28082018 PV – DEVIATION HURDLE CUE RATING 26112018

11 BG >18 MONTHS 12. BG GEM 13. GOVT. BANKING – ISSUE OF BG & LC – DT 21092017 BG CLAIM PERIOD

14 BG INVOCATION 04012018 15. BILL FINANCING DISCOUNT 18122017 BG MARGIN 050918

16 SOP - INSURANCE – KRI - CIR DT 24082017 & ANNEX CGTMSE GSTIN - 15122017

17 TIR MASTER CIRCULAR 13132013 18 TIR SOP DATED 25092017 CLARIFICATIONS 09032018SUPPLEMENTARY TIR 090718 POSSESSION OF PROPERTY 090718 TIR FORMAT MODI. 121218

19 SERVICE CHARGES – ADVANCES (EXCEPT PER) WEF 01042019 - ANNEX -1 ANNEX – 2 ANNEX – 3 ANNEX – 4 MODIFICATION AUTHORITY CIR 13022019 20. SER. – CERSAI – 09082017

21 POST SANCTION CREDIT PROCESS - DASH BOARD CIR DT 30082017

22 FREQUENT AND LARGE ENHANCEMENTS IN LIMITS - 10082017

23 CRA 50 LACS CRA REGULAR MODELS CRA NBFC HFC 12042018 & 210119, CRA SIM MODELS CRA RRE

24 STOCK & RECEIVABLE AUDIT MS DT 07092018

25 ANALYSIS OF FINANCIAL STATEMENTS & RATIO ANALYSIS

26 WORKING CAPITAL METHODS - DT 09012017 27. DT 31032017 28. E-ABS DT 25092017

29 CERSAI SOP – 06122017 DISC POWERS INT RATES 100418 MOROTORIUM 200418

30 PERFECTION OF SECURITIES CHARGED - 10082017

31 LOS SME – LSM DESKTOP - CIR DT 24082017 LLMS – RED FLAGGED A/CS 020618

32 ONLINE CHECKLIST FOR LOANS OF RS. 1 CRORE & ABOVE - 02112017

33 OBTENTION OF AUDITED BALANCE SHEETS EXTENDED TIME - 25102017

34 VERIFICATION OF FINANCIALS OF BORROWING ENTITIES – 08122017

35 REVIEW OF STANDARD ASSETS CIR DT 26092017 NON COOPERATIVE BORROWERS SOP 170119

36 CIC REPORTS – CIR DATED 18122017 & CIR DATED 05012018 CIC DEFAULTERS LIST 070918 CIC SME 12072018

37 ECRA SEBI GUIDELINES – 21112017 ECRA 50 CRORES 11042018

38 PROJECT VIJAY/ VIJAYAPATH ROLE MANUAL DT 10102017

39 MONTHLY STTS SOD 26092017 – CALC. OF DP STOCK STT 15032018 SUNDRY CREDITORS 280618 DP CALCULATION 05092018, DP COMPUTATION 151218

40 ADOPTION OF INDAS STANDARDS CIR DT 22092017 LOAN SYSTEM BANK CREDIT 220119

41 FLEXIBLE STRUCTURING OF LONG TERM PROJECT LOANS – 22092017

42 TAKE OVER NORMS MASTER CIRCULAR DT 11052018

43 HOLDING ON OPERATIONS CIR DT 22092017 & CIR DT 18122017

44 STANDARDIZATION OF TEMPLETS IN CREDIT PROPOSALS CIR DT 25092017

45 DELEGATION OF FINANCIAL POWERS – ADVANCES – 31122018 COMPROMISE 260318 & 200219 CCCC 220219

46 POLICY -ENGAGING BUSINESS ASSOCIATES 47) INT.RATE STRUCTURE CIR & ANNX

47 REVAMPING OF CORPORATE CREDIT 010618 EXPORURE TO STATE AND CEN. ENTITIES 100518

48 CGS FLAG FOR CGFMU & CGSSI A/CS – 28062018

49 ROLE OF FUNCTIONARIES IN CREDIT - 06072018

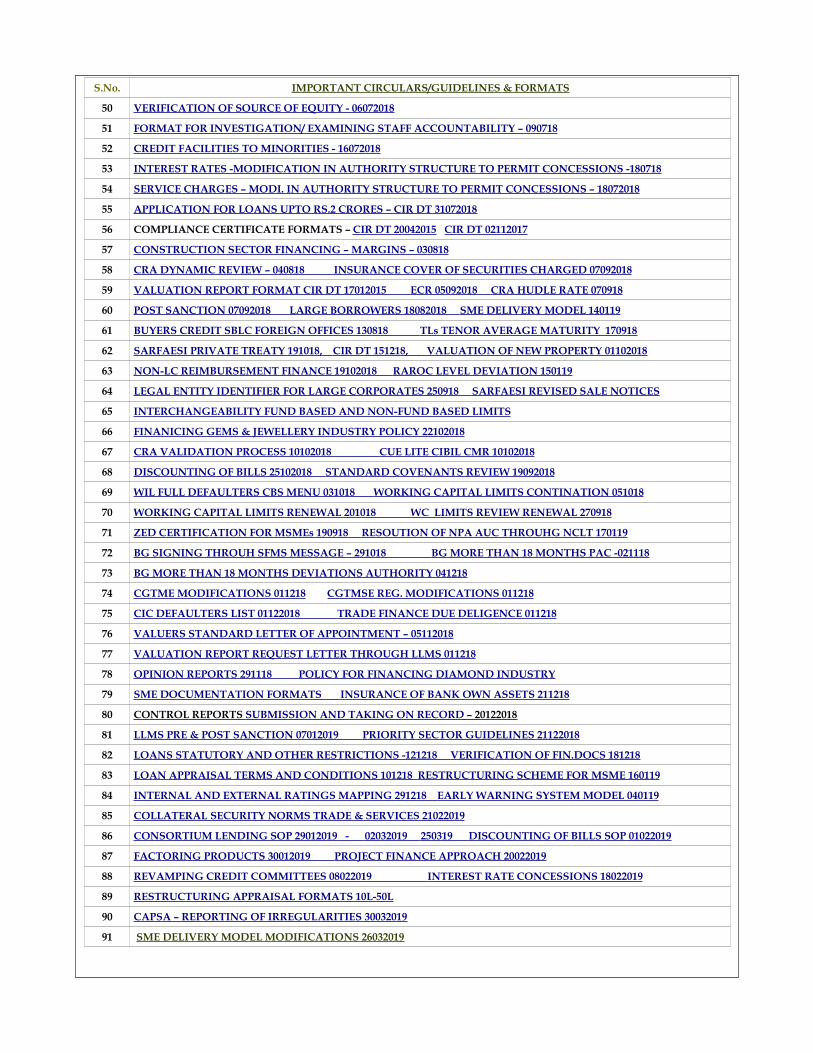

S.No. IMPORTANT CIRCULARS/GUIDELINES & FORMATS

50 VERIFICATION OF SOURCE OF EQUITY - 06072018

51 FORMAT FOR INVESTIGATION/ EXAMINING STAFF ACCOUNTABILITY – 090718

52 CREDIT FACILITIES TO MINORITIES - 16072018

53 INTEREST RATES -MODIFICATION IN AUTHORITY STRUCTURE TO PERMIT CONCESSIONS -180718

54 SERVICE CHARGES – MODI. IN AUTHORITY STRUCTURE TO PERMIT CONCESSIONS – 18072018

55 APPLICATION FOR LOANS UPTO RS.2 CRORES – CIR DT 31072018

56 COMPLIANCE CERTIFICATE FORMATS – CIR DT 20042015 CIR DT 02112017

57 CONSTRUCTION SECTOR FINANCING – MARGINS – 030818

58 CRA DYNAMIC REVIEW – 040818 INSURANCE COVER OF SECURITIES CHARGED 07092018

59 VALUATION REPORT FORMAT CIR DT 17012015 ECR 05092018 CRA HUDLE RATE 070918

60 POST SANCTION 07092018 LARGE BORROWERS 18082018 SME DELIVERY MODEL 140119

61 BUYERS CREDIT SBLC FOREIGN OFFICES 130818 TLs TENOR AVERAGE MATURITY 170918

62 SARFAESI PRIVATE TREATY 191018, CIR DT 151218, VALUATION OF NEW PROPERTY 01102018

63 NON-LC REIMBURSEMENT FINANCE 19102018 RAROC LEVEL DEVIATION 150119

64 LEGAL ENTITY IDENTIFIER FOR LARGE CORPORATES 250918 SARFAESI REVISED SALE NOTICES

65 INTERCHANGEABILITY FUND BASED AND NON-FUND BASED LIMITS

66 FINANICING GEMS & JEWELLERY INDUSTRY POLICY 22102018

67 CRA VALIDATION PROCESS 10102018 CUE LITE CIBIL CMR 10102018

68 DISCOUNTING OF BILLS 25102018 STANDARD COVENANTS REVIEW 19092018

69 WIL FULL DEFAULTERS CBS MENU 031018 WORKING CAPITAL LIMITS CONTINATION 051018

70 WORKING CAPITAL LIMITS RENEWAL 201018 WC LIMITS REVIEW RENEWAL 270918

71 ZED CERTIFICATION FOR MSMEs 190918 RESOUTION OF NPA AUC THROUHG NCLT 170119

72 BG SIGNING THROUH SFMS MESSAGE – 291018 BG MORE THAN 18 MONTHS PAC -021118

73 BG MORE THAN 18 MONTHS DEVIATIONS AUTHORITY 041218

74 CGTME MODIFICATIONS 011218 CGTMSE REG. MODIFICATIONS 011218

75 CIC DEFAULTERS LIST 01122018 TRADE FINANCE DUE DELIGENCE 011218

76 VALUERS STANDARD LETTER OF APPOINTMENT – 05112018

77 VALUATION REPORT REQUEST LETTER THROUGH LLMS 011218

78 OPINION REPORTS 291118 POLICY FOR FINANCING DIAMOND INDUSTRY

79 SME DOCUMENTATION FORMATS INSURANCE OF BANK OWN ASSETS 211218

80 CONTROL REPORTS SUBMISSION AND TAKING ON RECORD – 20122018

81 LLMS PRE & POST SANCTION 07012019 PRIORITY SECTOR GUIDELINES 21122018

82 LOANS STATUTORY AND OTHER RESTRICTIONS -121218 VERIFICATION OF FIN.DOCS 181218

83 LOAN APPRAISAL TERMS AND CONDITIONS 101218 RESTRUCTURING SCHEME FOR MSME 160119

84 INTERNAL AND EXTERNAL RATINGS MAPPING 291218 EARLY WARNING SYSTEM MODEL 040119

85 COLLATERAL SECURITY NORMS TRADE & SERVICES 21022019

86 CONSORTIUM LENDING SOP 29012019 - 02032019 250319 DISCOUNTING OF BILLS SOP 01022019

87 FACTORING PRODUCTS 30012019 PROJECT FINANCE APPROACH 20022019

88 REVAMPING CREDIT COMMITTEES 08022019 INTEREST RATE CONCESSIONS 18022019

89 RESTRUCTURING APPRAISAL FORMATS 10L-50L

90 CAPSA – REPORTING OF IRREGULARITIES 30032019

91 SME DELIVERY MODEL MODIFICATIONS 26032019

ftp://10.210.24.33/SME%20ASSET%20%20PRODUCTS/EARLY%20WARNING%20SYSTEM%20REVISED%20MODEL%20040119.pdf

ftp://10.210.24.33/SME%20ASSET%20%20PRODUCTS/ZED%20certification%20scheme%20for%20MSMEs%20190918.pdf

ftp://10.210.24.33/SME%20ASSET%20%20PRODUCTS/PURCHASE%20SALE%20OF%20PROPERTIES%20POLICY%20151218.pdf

ftp://10.210.24.33/SME%20ASSET%20%20PRODUCTS/BUYERS%20CREDIT%20SBLC%20FOREIGN%20OFFICES%20130818.pdf

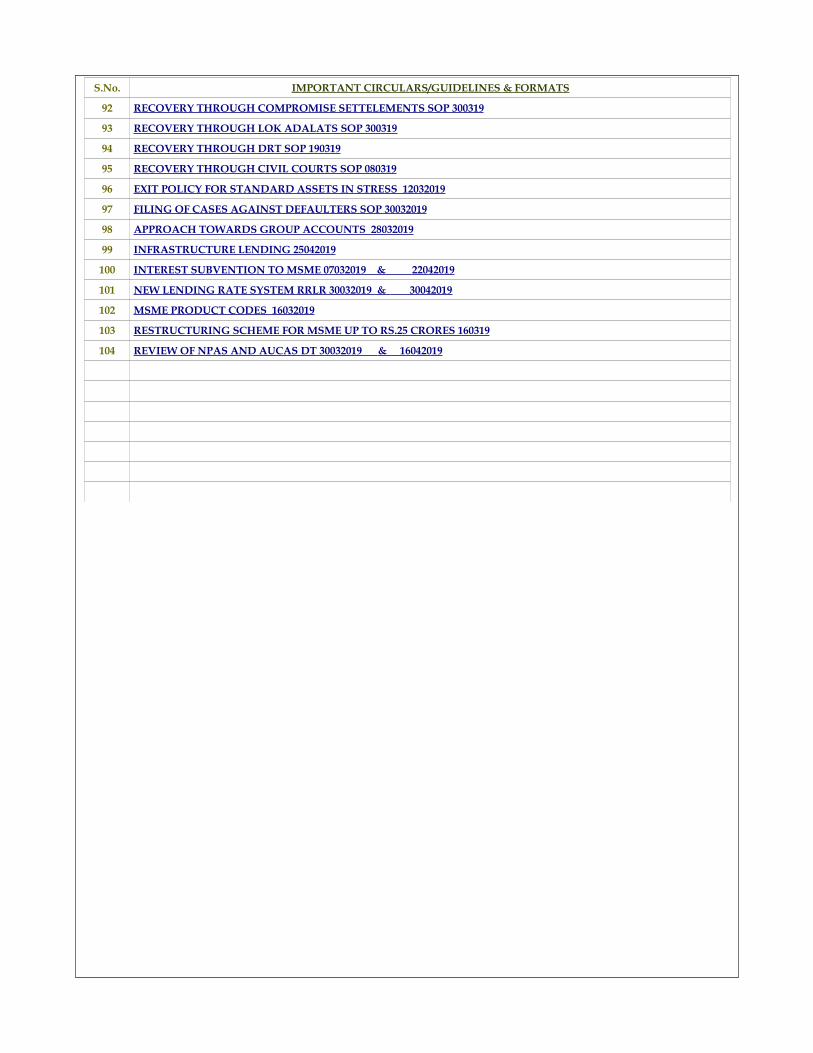

S.No. IMPORTANT CIRCULARS/GUIDELINES & FORMATS

92 RECOVERY THROUGH COMPROMISE SETTELEMENTS SOP 300319

93 RECOVERY THROUGH LOK ADALATS SOP 300319

94 RECOVERY THROUGH DRT SOP 190319

95 RECOVERY THROUGH CIVIL COURTS SOP 080319

96 EXIT POLICY FOR STANDARD ASSETS IN STRESS 12032019

97 FILING OF CASES AGAINST DEFAULTERS SOP 30032019

98 APPROACH TOWARDS GROUP ACCOUNTS 28032019

99 INFRASTRUCTURE LENDING 25042019

100 INTEREST SUBVENTION TO MSME 07032019 & 22042019

101 NEW LENDING RATE SYSTEM RRLR 30032019 & 30042019

102 MSME PRODUCT CODES 16032019

103 RESTRUCTURING SCHEME FOR MSME UP TO RS.25 CRORES 160319

104 REVIEW OF NPAS AND AUCAS DT 30032019 & 16042019

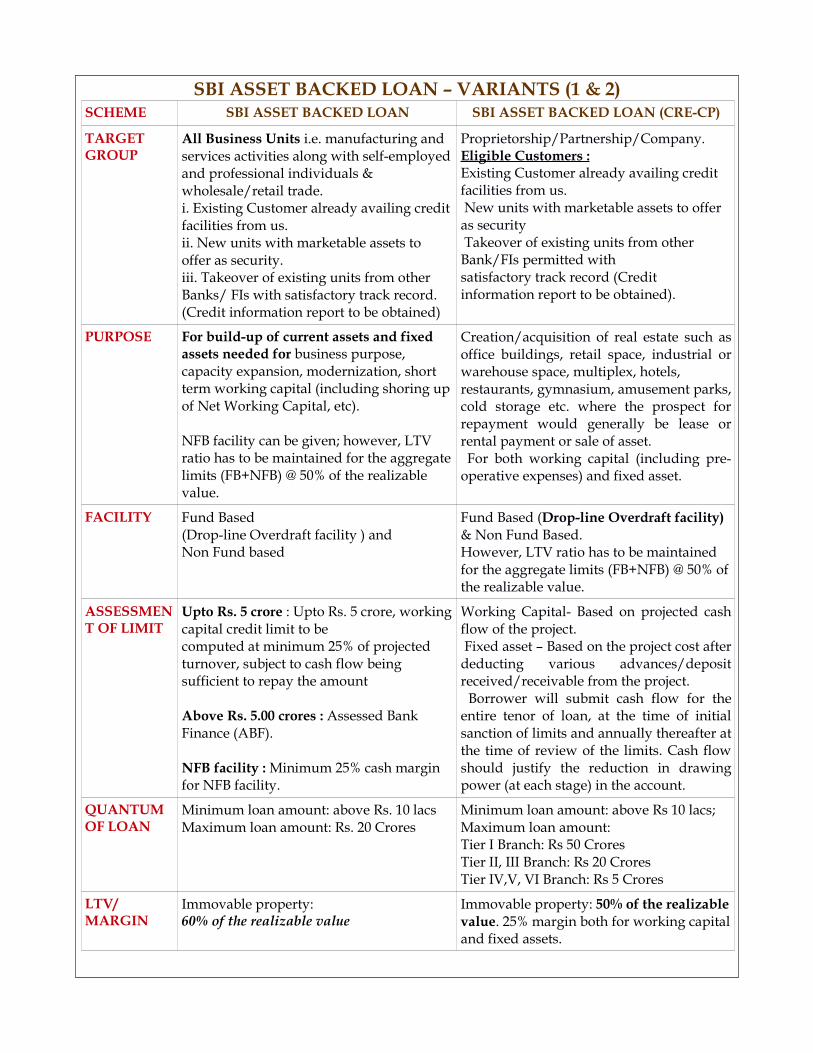

SBI ASSET BACKED LOAN – VARIANTS (1 & 2)SCHEME SBI ASSET BACKED LOAN SBI ASSET BACKED LOAN (CRE-CP)

TARGET GROUP

All Business Units i.e. manufacturing and services activities along with self-employed and professional individuals & wholesale/retail trade. i. Existing Customer already availing credit facilities from us.ii. New units with marketable assets to offer as security.iii. Takeover of existing units from other Banks/ FIs with satisfactory track record. (Credit information report to be obtained)

Proprietorship/Partnership/Company.Eligible Customers :Existing Customer already availing credit facilities from us. New units with marketable assets to offer as security Takeover of existing units from other Bank/FIs permitted withsatisfactory track record (Credit information report to be obtained).

PURPOSE For build-up of current assets and fixed assets needed for business purpose, capacity expansion, modernization, short term working capital (including shoring up of Net Working Capital, etc).

NFB facility can be given; however, LTV ratio has to be maintained for the aggregate limits (FB+NFB) @ 50% of the realizable value.

Creation/acquisition of real estate such as office buildings, retail space, industrial or warehouse space, multiplex, hotels,restaurants, gymnasium, amusement parks, cold storage etc. where the prospect for repayment would generally be lease or rental payment or sale of asset. For both working capital (including pre-operative expenses) and fixed asset.

FACILITY Fund Based (Drop-line Overdraft facility ) and Non Fund based

Fund Based (Drop-line Overdraft facility) & Non Fund Based.However, LTV ratio has to be maintainedfor the aggregate limits (FB+NFB) @ 50% of the realizable value.

ASSESSMENT OF LIMIT

Upto Rs. 5 crore : Upto Rs. 5 crore, working capital credit limit to becomputed at minimum 25% of projectedturnover, subject to cash flow being sufficient to repay the amount

Above Rs. 5.00 crores : Assessed Bank Finance (ABF).

NFB facility : Minimum 25% cash margin for NFB facility.

Working Capital- Based on projected cash flow of the project. Fixed asset – Based on the project cost after deducting various advances/deposit received/receivable from the project. Borrower will submit cash flow for the entire tenor of loan, at the time of initial sanction of limits and annually thereafter at the time of review of the limits. Cash flow should justify the reduction in drawing power (at each stage) in the account.

QUANTUM OF LOAN

Minimum loan amount: above Rs. 10 lacs Maximum loan amount: Rs. 20 Crores

Minimum loan amount: above Rs 10 lacs; Maximum loan amount:Tier I Branch: Rs 50 CroresTier II, III Branch: Rs 20 CroresTier IV,V, VI Branch: Rs 5 Crores

LTV/MARGIN

Immovable property: 60% of the realizable value

Immovable property: 50% of the realizable value. 25% margin both for working capital and fixed assets.

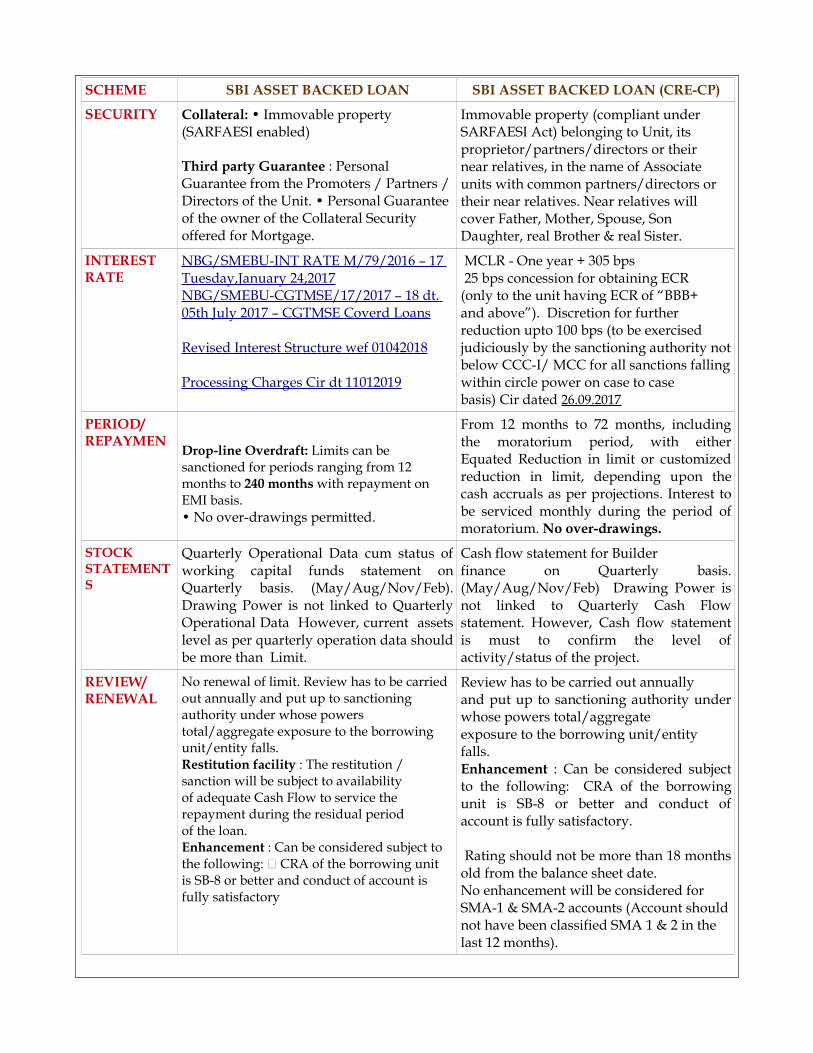

SCHEME SBI ASSET BACKED LOAN SBI ASSET BACKED LOAN (CRE-CP)

SECURITY Collateral: • Immovable property (SARFAESI enabled)

Third party Guarantee : Personal Guarantee from the Promoters / Partners / Directors of the Unit. • Personal Guarantee of the owner of the Collateral Security offered for Mortgage.

Immovable property (compliant underSARFAESI Act) belonging to Unit, itsproprietor/partners/directors or theirnear relatives, in the name of Associate units with common partners/directors or their near relatives. Near relatives will cover Father, Mother, Spouse, SonDaughter, real Brother & real Sister.

INTEREST RATE

NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017NBG/SMEBU-CGTMSE/17/2017 – 18 dt. 05th July 2017 – CGTMSE Coverd Loans

Revised Interest Structure wef 01042018

Processing Charges Cir dt 11012019

MCLR - One year + 305 bps 25 bps concession for obtaining ECR(only to the unit having ECR of “BBB+and above”). Discretion for further reduction upto 100 bps (to be exercised judiciously by the sanctioning authority not below CCC-I/ MCC for all sanctions falling within circle power on case to casebasis) Cir dated 26.09.2017

PERIOD/REPAYMEN

Drop-line Overdraft: Limits can be sanctioned for periods ranging from 12 months to 240 months with repayment on EMI basis. • No over-drawings permitted.

From 12 months to 72 months, including the moratorium period, with either Equated Reduction in limit or customized reduction in limit, depending upon the cash accruals as per projections. Interest to be serviced monthly during the period of moratorium. No over-drawings.

STOCK STATEMENTS

Quarterly Operational Data cum status of working capital funds statement on Quarterly basis. (May/Aug/Nov/Feb). Drawing Power is not linked to Quarterly Operational Data However, current assets level as per quarterly operation data should be more than Limit.

Cash flow statement for Builderfinance on Quarterly basis. (May/Aug/Nov/Feb) Drawing Power is not linked to Quarterly Cash Flow statement. However, Cash flow statement is must to confirm the level of activity/status of the project.

REVIEW/ RENEWAL

No renewal of limit. Review has to be carried out annually and put up to sanctioning authority under whose powers total/aggregate exposure to the borrowing unit/entity falls.Restitution facility : The restitution / sanction will be subject to availabilityof adequate Cash Flow to service the repayment during the residual periodof the loan.Enhancement : Can be considered subject tothe following: � CRA of the borrowing unitis SB-8 or better and conduct of account is fully satisfactory

Review has to be carried out annuallyand put up to sanctioning authority under whose powers total/aggregateexposure to the borrowing unit/entityfalls. Enhancement : Can be considered subject to the following: CRA of the borrowing unit is SB-8 or better and conduct of account is fully satisfactory.

Rating should not be more than 18 months old from the balance sheet date.No enhancement will be considered for SMA-1 & SMA-2 accounts (Account should not have been classified SMA 1 & 2 in the last 12 months).

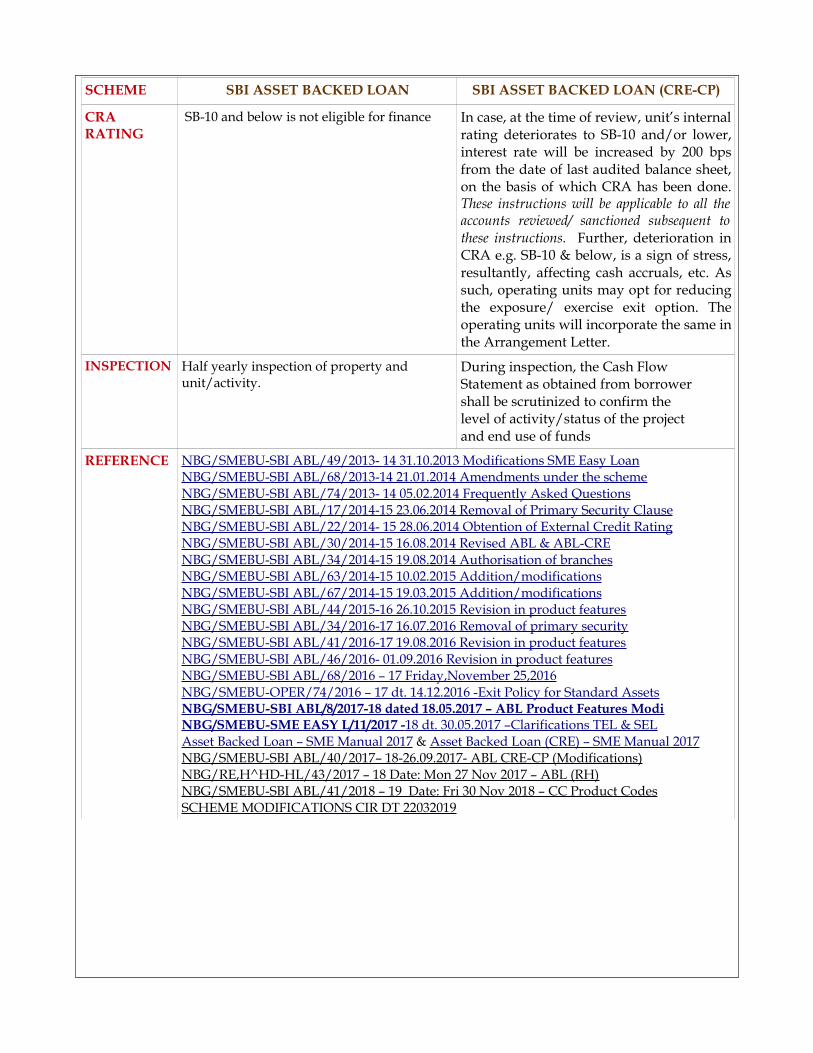

SCHEME SBI ASSET BACKED LOAN SBI ASSET BACKED LOAN (CRE-CP)

CRA RATING

SB-10 and below is not eligible for finance In case, at the time of review, unit’s internal rating deteriorates to SB-10 and/or lower, interest rate will be increased by 200 bps from the date of last audited balance sheet, on the basis of which CRA has been done. These instructions will be applicable to all the accounts reviewed/ sanctioned subsequent to these instructions. Further, deterioration in CRA e.g. SB-10 & below, is a sign of stress, resultantly, affecting cash accruals, etc. As such, operating units may opt for reducing the exposure/ exercise exit option. The operating units will incorporate the same in the Arrangement Letter.

INSPECTION Half yearly inspection of property and unit/activity.

During inspection, the Cash FlowStatement as obtained from borrowershall be scrutinized to confirm thelevel of activity/status of the projectand end use of funds

REFERENCE NBG/SMEBU-SBI ABL/49/2013- 14 31.10.2013 Modifications SME Easy Loan NBG/SMEBU-SBI ABL/68/2013-14 21.01.2014 Amendments under the schemeNBG/SMEBU-SBI ABL/74/2013- 14 05.02.2014 Frequently Asked QuestionsNBG/SMEBU-SBI ABL/17/2014-15 23.06.2014 Removal of Primary Security Clause NBG/SMEBU-SBI ABL/22/2014- 15 28.06.2014 Obtention of External Credit Rating NBG/SMEBU-SBI ABL/30/2014-15 16.08.2014 Revised ABL & ABL-CRENBG/SMEBU-SBI ABL/34/2014-15 19.08.2014 Authorisation of branchesNBG/SMEBU-SBI ABL/63/2014-15 10.02.2015 Addition/modifications NBG/SMEBU-SBI ABL/67/2014-15 19.03.2015 Addition/modifications NBG/SMEBU-SBI ABL/44/2015-16 26.10.2015 Revision in product featuresNBG/SMEBU-SBI ABL/34/2016-17 16.07.2016 Removal of primary security NBG/SMEBU-SBI ABL/41/2016-17 19.08.2016 Revision in product featuresNBG/SMEBU-SBI ABL/46/2016- 01.09.2016 Revision in product featuresNBG/SMEBU-SBI ABL/68/2016 – 17 Friday,November 25,2016NBG/SMEBU-OPER/74/2016 – 17 dt. 14.12.2016 - Exit Policy for Standard Assets NBG/SMEBU-SBI ABL/8/2017-18 dated 18.05.2017 – ABL Product Features ModiNBG/SMEBU-SME EASY L/11/2017 - 18 dt. 30.05.2017 –Clarifications TEL & SEL Asset Backed Loan – SME Manual 2017 & Asset Backed Loan (CRE) – SME Manual 2017NBG/SMEBU-SBI ABL/40/2017– 18-26.09.2017- ABL CRE-CP (Modifications)NBG/RE,H^HD-HL/43/2017 – 18 Date: Mon 27 Nov 2017 – ABL (RH)NBG/SMEBU-SBI ABL/41/2018 – 19 Date: Fri 30 Nov 2018 – CC Product CodesSCHEME MODIFICATIONS CIR DT 22032019

ftp://10.210.24.33/SME%20ASSET%20%20PRODUCTS/ASSET%20BACKED%20LOAN%20EXTING%20TEL%20SEL%20300517.pdf

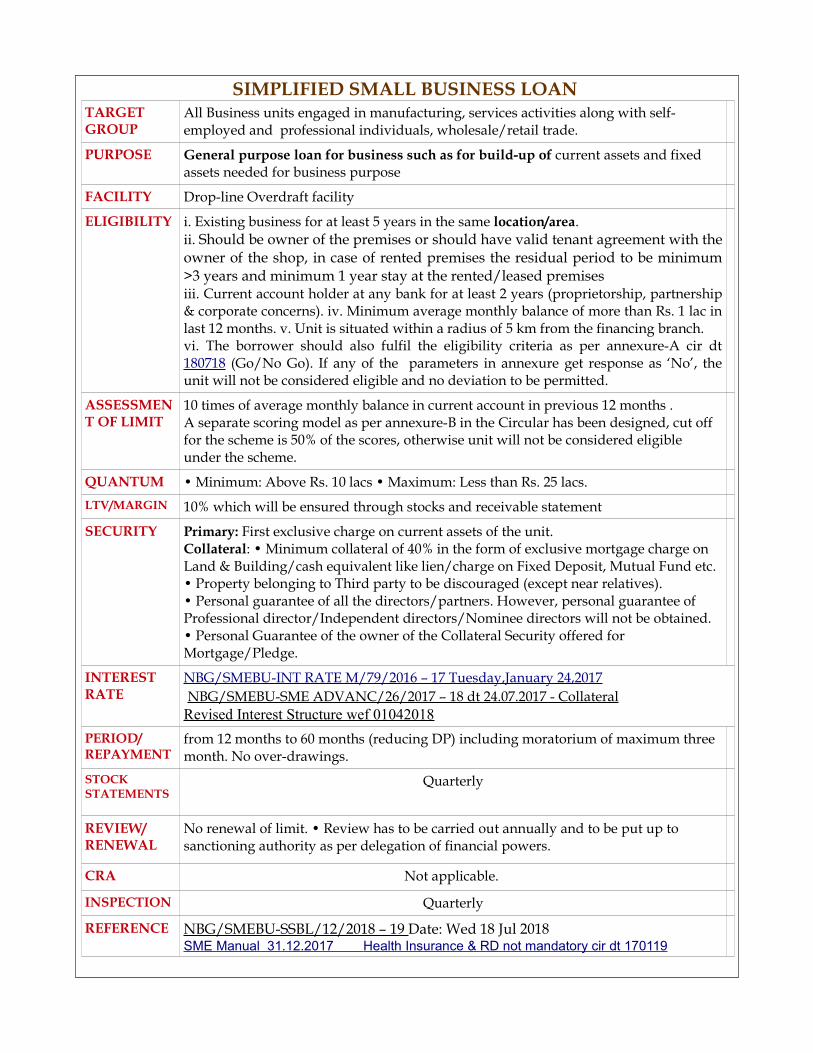

SIMPLIFIED SMALL BUSINESS LOAN TARGET GROUP

All Business units engaged in manufacturing, services activities along with self-employed and professional individuals, wholesale/retail trade.

PURPOSE General purpose loan for business such as for build-up of current assets and fixed assets needed for business purpose

FACILITY Drop-line Overdraft facility

ELIGIBILITY i. Existing business for at least 5 years in the same location/area.ii. Should be owner of the premises or should have valid tenant agreement with the owner of the shop, in case of rented premises the residual period to be minimum >3 years and minimum 1 year stay at the rented/leased premisesiii. Current account holder at any bank for at least 2 years (proprietorship, partnership & corporate concerns). iv. Minimum average monthly balance of more than Rs. 1 lac in last 12 months. v. Unit is situated within a radius of 5 km from the financing branch.vi. The borrower should also fulfil the eligibility criteria as per annexure-A cir dt 180718 (Go/No Go). If any of the parameters in annexure get response as ‘No’, the unit will not be considered eligible and no deviation to be permitted.

ASSESSMENT OF LIMIT

10 times of average monthly balance in current account in previous 12 months .A separate scoring model as per annexure-B in the Circular has been designed, cut off for the scheme is 50% of the scores, otherwise unit will not be considered eligible under the scheme.

QUANTUM • Minimum: Above Rs. 10 lacs • Maximum: Less than Rs. 25 lacs.LTV/MARGIN 10% which will be ensured through stocks and receivable statement

SECURITY Primary: First exclusive charge on current assets of the unit.Collateral: • Minimum collateral of 40% in the form of exclusive mortgage charge on Land & Building/cash equivalent like lien/charge on Fixed Deposit, Mutual Fund etc. • Property belonging to Third party to be discouraged (except near relatives).• Personal guarantee of all the directors/partners. However, personal guarantee of Professional director/Independent directors/Nominee directors will not be obtained.• Personal Guarantee of the owner of the Collateral Security offered for Mortgage/Pledge.

INTEREST RATE

NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017 NBG/SMEBU-SME ADVANC/26/2017 – 18 dt 24.07.2017 - Collateral Revised Interest Structure wef 01042018

PERIOD/REPAYMENT

from 12 months to 60 months (reducing DP) including moratorium of maximum three month. No over-drawings.

STOCK STATEMENTS

Quarterly

REVIEW/ RENEWAL

No renewal of limit. • Review has to be carried out annually and to be put up to sanctioning authority as per delegation of financial powers.

CRA Not applicable.

INSPECTION Quarterly

REFERENCE NBG/SMEBU-SSBL/12/2018 – 19 Date: Wed 18 Jul 2018 SME Manual 31.12.2017 Health Insurance & RD not mandatory cir dt 170119

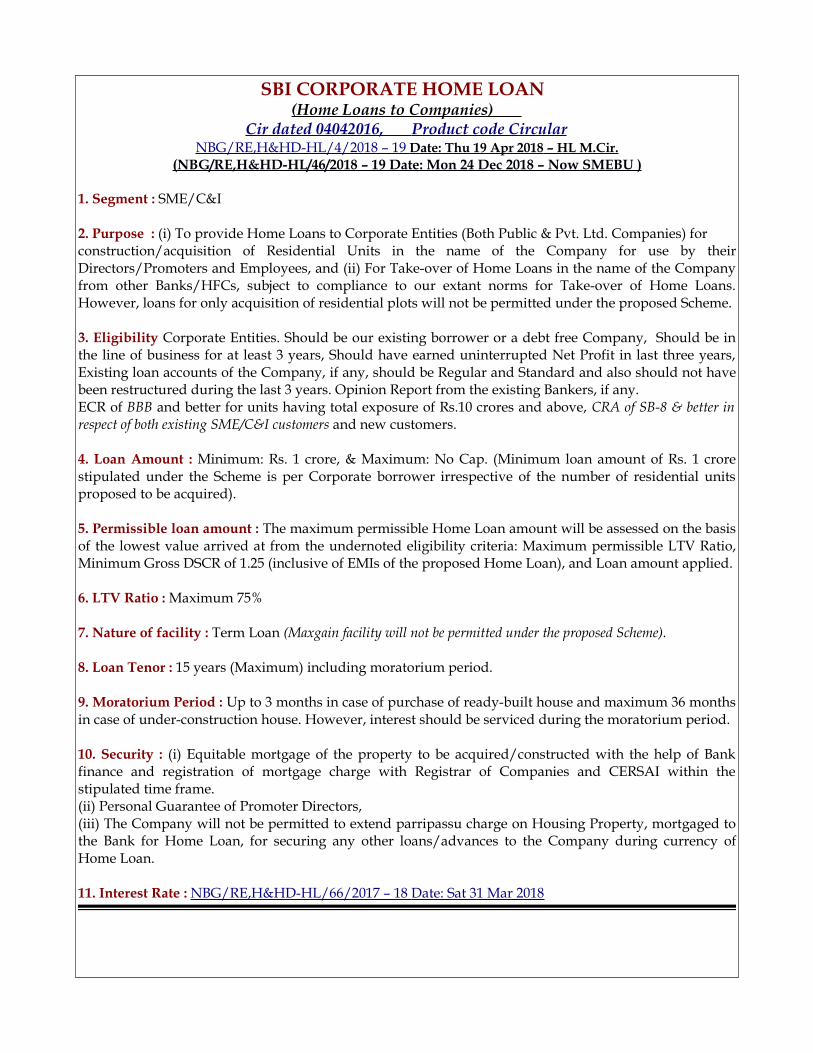

SBI CORPORATE HOME LOAN (Home Loans to Companies)

Cir dated 04042016, Product code Circular NBG/RE,H&HD-HL/4/2018 – 19 Date: Thu 19 Apr 2018 – HL M.Cir.

(NBG/RE,H&HD-HL/46/2018 – 19 Date: Mon 24 Dec 2018 – Now SMEBU )

1. Segment : SME/C&I

2. Purpose : (i) To provide Home Loans to Corporate Entities (Both Public & Pvt. Ltd. Companies) forconstruction/acquisition of Residential Units in the name of the Company for use by their Directors/Promoters and Employees, and (ii) For Take-over of Home Loans in the name of the Company from other Banks/HFCs, subject to compliance to our extant norms for Take-over of Home Loans. However, loans for only acquisition of residential plots will not be permitted under the proposed Scheme.

3. Eligibility Corporate Entities. Should be our existing borrower or a debt free Company, Should be in the line of business for at least 3 years, Should have earned uninterrupted Net Profit in last three years, Existing loan accounts of the Company, if any, should be Regular and Standard and also should not have been restructured during the last 3 years. Opinion Report from the existing Bankers, if any.ECR of BBB and better for units having total exposure of Rs.10 crores and above, CRA of SB-8 & better in respect of both existing SME/C&I customers and new customers.

4. Loan Amount : Minimum: Rs. 1 crore, & Maximum: No Cap. (Minimum loan amount of Rs. 1 crore stipulated under the Scheme is per Corporate borrower irrespective of the number of residential units proposed to be acquired). 5. Permissible loan amount : The maximum permissible Home Loan amount will be assessed on the basis of the lowest value arrived at from the undernoted eligibility criteria: Maximum permissible LTV Ratio, Minimum Gross DSCR of 1.25 (inclusive of EMIs of the proposed Home Loan), and Loan amount applied.

6. LTV Ratio : Maximum 75%

7. Nature of facility : Term Loan (Maxgain facility will not be permitted under the proposed Scheme).

8. Loan Tenor : 15 years (Maximum) including moratorium period.

9. Moratorium Period : Up to 3 months in case of purchase of ready-built house and maximum 36 months in case of under-construction house. However, interest should be serviced during the moratorium period.

10. Security : (i) Equitable mortgage of the property to be acquired/constructed with the help of Bank finance and registration of mortgage charge with Registrar of Companies and CERSAI within the stipulated time frame.(ii) Personal Guarantee of Promoter Directors,(iii) The Company will not be permitted to extend parripassu charge on Housing Property, mortgaged to the Bank for Home Loan, for securing any other loans/advances to the Company during currency of Home Loan.

11. Interest Rate : NBG/RE,H&HD-HL/66/2017 – 18 Date: Sat 31 Mar 2018

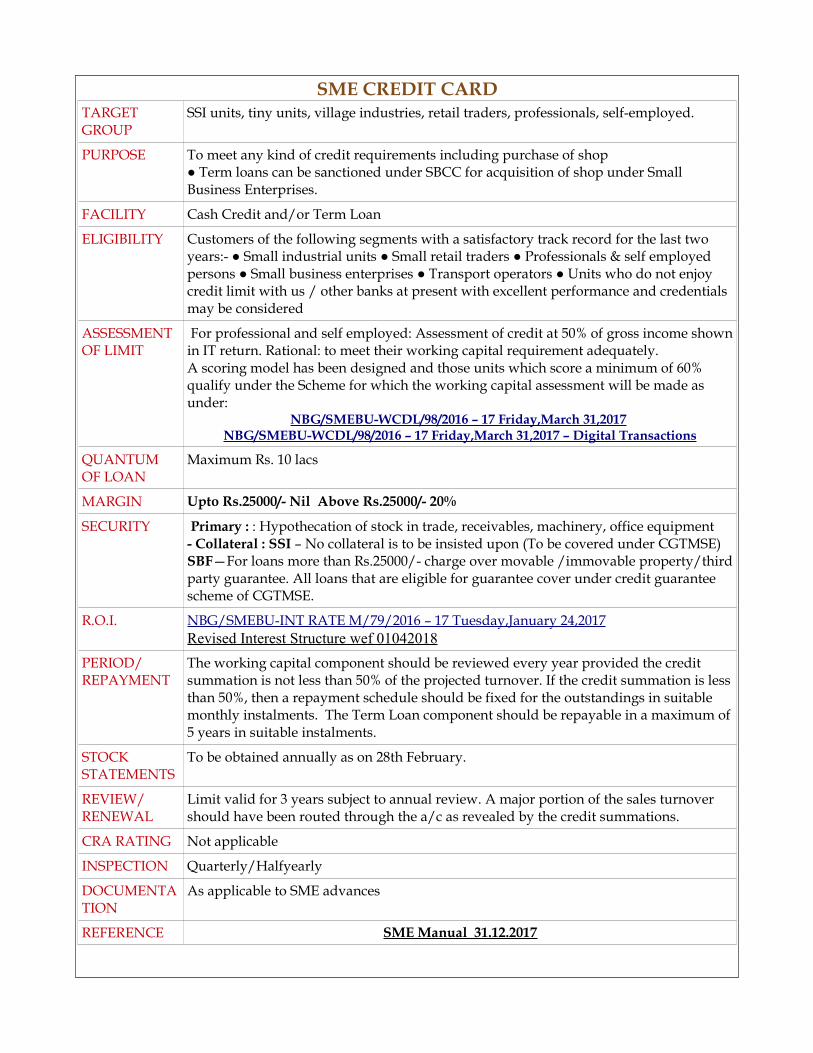

SME CREDIT CARDTARGET GROUP

SSI units, tiny units, village industries, retail traders, professionals, self-employed.

PURPOSE To meet any kind of credit requirements including purchase of shop● Term loans can be sanctioned under SBCC for acquisition of shop under Small Business Enterprises.

FACILITY Cash Credit and/or Term Loan

ELIGIBILITY Customers of the following segments with a satisfactory track record for the last two years:- ● Small industrial units ● Small retail traders ● Professionals & self employed persons ● Small business enterprises ● Transport operators ● Units who do not enjoy credit limit with us / other banks at present with excellent performance and credentials may be considered

ASSESSMENT OF LIMIT

For professional and self employed: Assessment of credit at 50% of gross income shown in IT return. Rational: to meet their working capital requirement adequately.A scoring model has been designed and those units which score a minimum of 60% qualify under the Scheme for which the working capital assessment will be made as under:

NBG/SMEBU-WCDL/98/2016 – 17 Friday,March 31,2017 NBG/SMEBU-WCDL/98/2016 – 17 Friday,March 31,2017 – Digital Transactions

QUANTUM OF LOAN

Maximum Rs. 10 lacs

MARGIN Upto Rs.25000/- Nil Above Rs.25000/- 20%

SECURITY Primary : : Hypothecation of stock in trade, receivables, machinery, office equipment- Collateral : SSI – No collateral is to be insisted upon (To be covered under CGTMSE) SBF—For loans more than Rs.25000/- charge over movable /immovable property/third party guarantee. All loans that are eligible for guarantee cover under credit guarantee scheme of CGTMSE.

R.O.I. NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017Revised Interest Structure wef 01042018

PERIOD/REPAYMENT

The working capital component should be reviewed every year provided the credit summation is not less than 50% of the projected turnover. If the credit summation is less than 50%, then a repayment schedule should be fixed for the outstandings in suitable monthly instalments. The Term Loan component should be repayable in a maximum of 5 years in suitable instalments.

STOCK STATEMENTS

To be obtained annually as on 28th February.

REVIEW/ RENEWAL

Limit valid for 3 years subject to annual review. A major portion of the sales turnover should have been routed through the a/c as revealed by the credit summations.

CRA RATING Not applicable

INSPECTION Quarterly/Halfyearly

DOCUMENTATION

As applicable to SME advances

REFERENCE SME Manual 31.12.2017

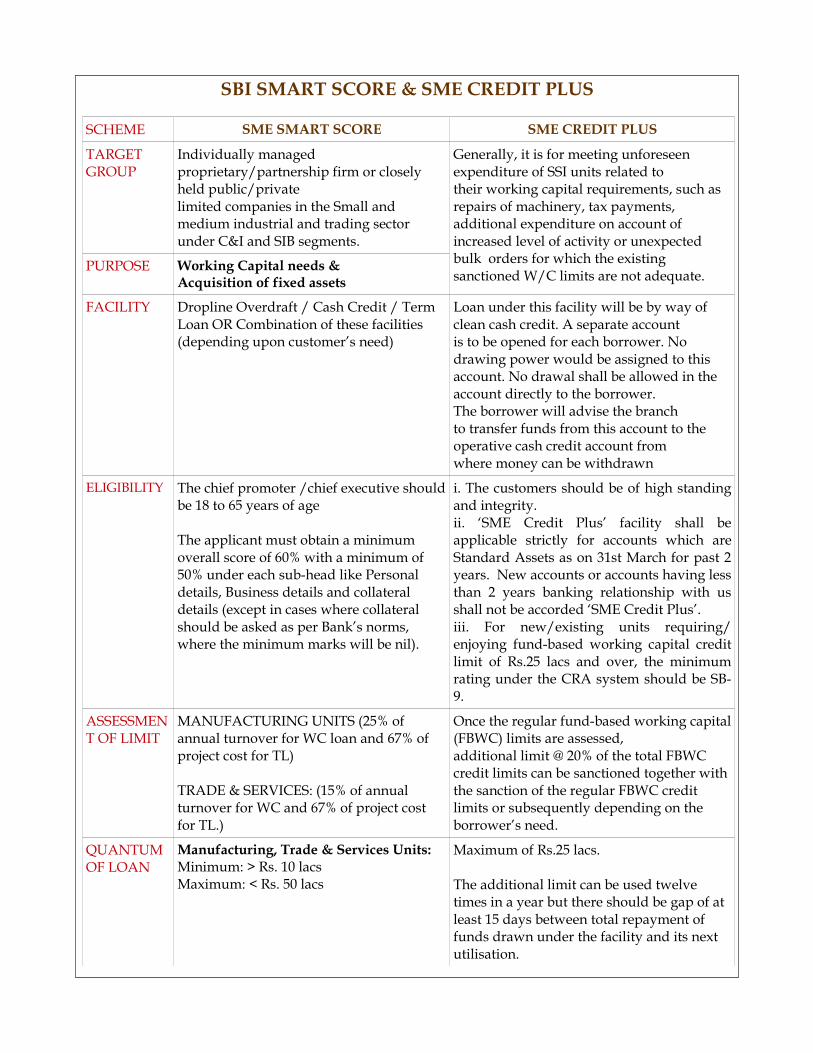

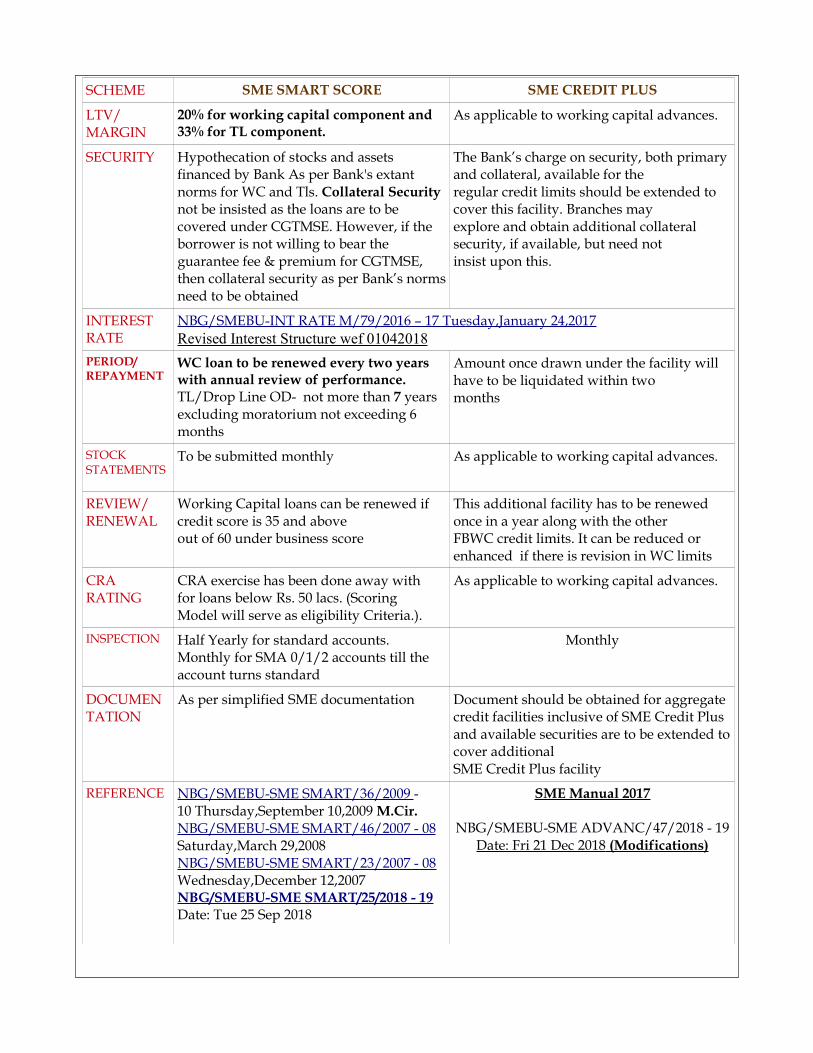

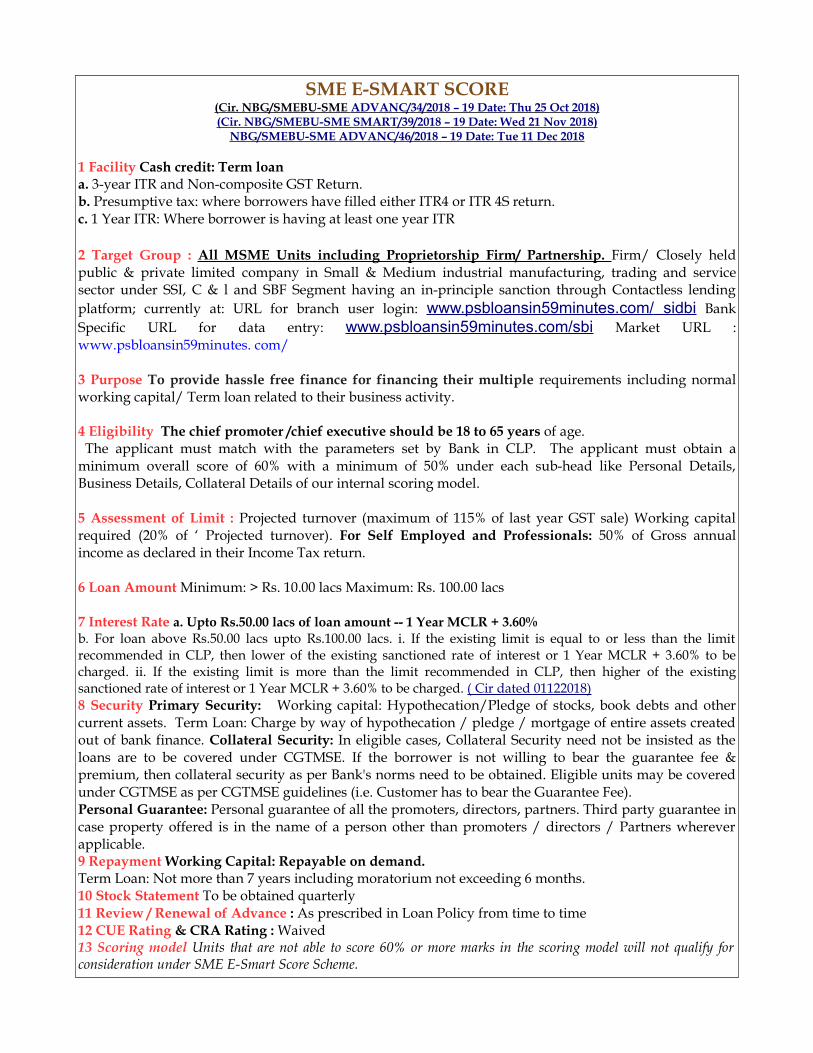

SBI SMART SCORE & SME CREDIT PLUS

SCHEME SME SMART SCORE SME CREDIT PLUS

TARGET GROUP

Individually managed proprietary/partnership firm or closely held public/privatelimited companies in the Small and medium industrial and trading sectorunder C&I and SIB segments.

Generally, it is for meeting unforeseen expenditure of SSI units related totheir working capital requirements, such as repairs of machinery, tax payments,additional expenditure on account of increased level of activity or unexpected bulk orders for which the existing sanctioned W/C limits are not adequate.

PURPOSE Working Capital needs & Acquisition of fixed assets

FACILITY Dropline Overdraft / Cash Credit / TermLoan OR Combination of these facilities (depending upon customer’s need)

Loan under this facility will be by way of clean cash credit. A separate accountis to be opened for each borrower. No drawing power would be assigned to thisaccount. No drawal shall be allowed in the account directly to the borrower.The borrower will advise the branchto transfer funds from this account to the operative cash credit account fromwhere money can be withdrawn

ELIGIBILITY The chief promoter /chief executive should be 18 to 65 years of age

The applicant must obtain a minimum overall score of 60% with a minimum of50% under each sub-head like Personal details, Business details and collateral details (except in cases where collateral should be asked as per Bank’s norms, where the minimum marks will be nil).

i. The customers should be of high standing and integrity. ii. ‘SME Credit Plus’ facility shall be applicable strictly for accounts which are Standard Assets as on 31st March for past 2 years. New accounts or accounts having less than 2 years banking relationship with us shall not be accorded ‘SME Credit Plus’.iii. For new/existing units requiring/ enjoying fund-based working capital credit limit of Rs.25 lacs and over, the minimum rating under the CRA system should be SB-9.

ASSESSMENT OF LIMIT

MANUFACTURING UNITS (25% of annual turnover for WC loan and 67% of project cost for TL)

TRADE & SERVICES: (15% of annual turnover for WC and 67% of project cost for TL.)

Once the regular fund-based working capital (FBWC) limits are assessed,additional limit @ 20% of the total FBWC credit limits can be sanctioned together with the sanction of the regular FBWC credit limits or subsequently depending on the borrower’s need.

QUANTUM OF LOAN

Manufacturing, Trade & Services Units:Minimum: > Rs. 10 lacsMaximum: < Rs. 50 lacs

Maximum of Rs.25 lacs.

The additional limit can be used twelve times in a year but there should be gap of at least 15 days between total repayment of funds drawn under the facility and its next utilisation.

SCHEME SME SMART SCORE SME CREDIT PLUS

LTV/MARGIN

20% for working capital component and 33% for TL component.

As applicable to working capital advances.

SECURITY Hypothecation of stocks and assets financed by Bank As per Bank's extant norms for WC and Tls. Collateral Security not be insisted as the loans are to be covered under CGTMSE. However, if the borrower is not willing to bear the guarantee fee & premium for CGTMSE, then collateral security as per Bank’s norms need to be obtained

The Bank’s charge on security, both primary and collateral, available for theregular credit limits should be extended to cover this facility. Branches mayexplore and obtain additional collateral security, if available, but need notinsist upon this.

INTEREST RATE

NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017Revised Interest Structure wef 01042018

PERIOD/REPAYMENT

WC loan to be renewed every two years with annual review of performance.TL/Drop Line OD- not more than 7 years excluding moratorium not exceeding 6 months

Amount once drawn under the facility will have to be liquidated within twomonths

STOCK STATEMENTS

To be submitted monthly As applicable to working capital advances.

REVIEW/ RENEWAL

Working Capital loans can be renewed if credit score is 35 and aboveout of 60 under business score

This additional facility has to be renewed once in a year along with the otherFBWC credit limits. It can be reduced or enhanced if there is revision in WC limits

CRA RATING

CRA exercise has been done away withfor loans below Rs. 50 lacs. (ScoringModel will serve as eligibility Criteria.).

As applicable to working capital advances.

INSPECTION Half Yearly for standard accounts.Monthly for SMA 0/1/2 accounts till theaccount turns standard

Monthly

DOCUMENTATION

As per simplified SME documentation Document should be obtained for aggregate credit facilities inclusive of SME Credit Plus and available securities are to be extended to cover additionalSME Credit Plus facility

REFERENCE NBG/SMEBU-SME SMART/36/2009 -10 Thursday,September 10,2009 M.Cir.NBG/SMEBU-SME SMART/46/2007 - 08 Saturday,March 29,2008NBG/SMEBU-SME SMART/23/2007 - 08Wednesday,December 12,2007NBG/SMEBU-SME SMART/25/2018 - 19Date: Tue 25 Sep 2018

SME Manual 2017

NBG/SMEBU-SME ADVANC/47/2018 - 19Date: Fri 21 Dec 2018 (Modifications)

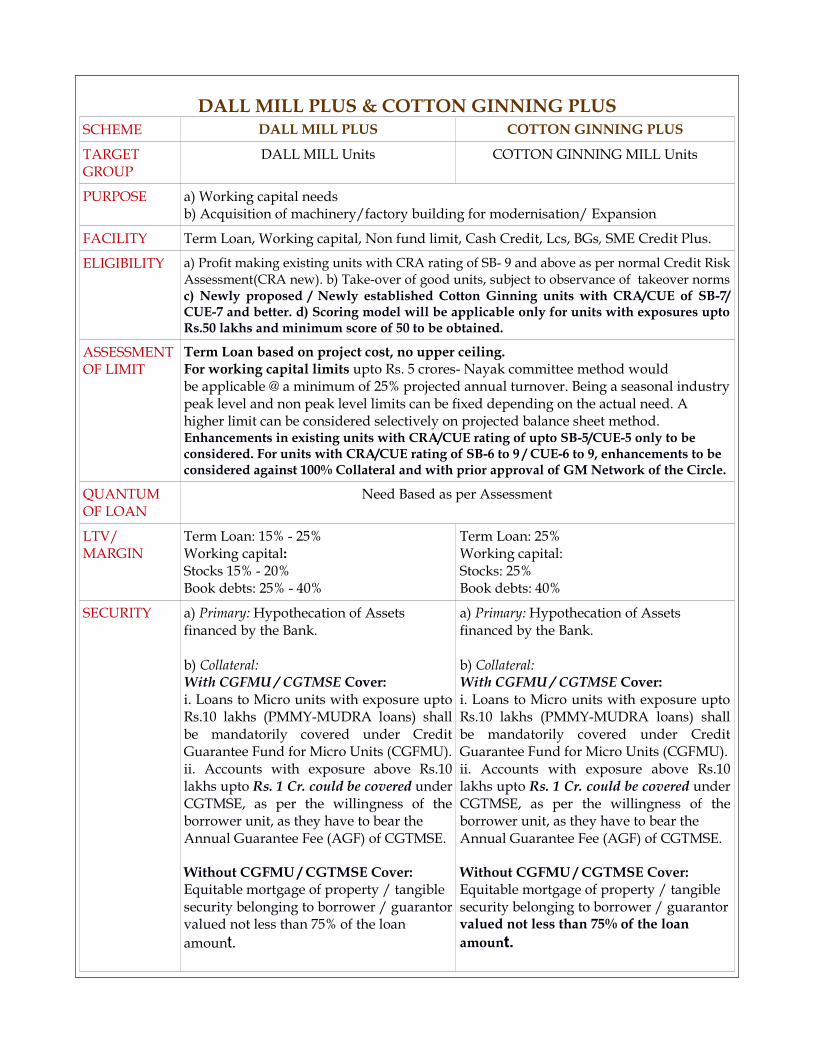

DALL MILL PLUS & COTTON GINNING PLUSSCHEME DALL MILL PLUS COTTON GINNING PLUS

TARGET GROUP

DALL MILL Units COTTON GINNING MILL Units

PURPOSE a) Working capital needsb) Acquisition of machinery/factory building for modernisation/ Expansion

FACILITY Term Loan, Working capital, Non fund limit, Cash Credit, Lcs, BGs, SME Credit Plus.

ELIGIBILITY a) Profit making existing units with CRA rating of SB- 9 and above as per normal Credit Risk Assessment(CRA new). b) Take-over of good units, subject to observance of takeover norms c) Newly proposed / Newly established Cotton Ginning units with CRA/CUE of SB-7/ CUE-7 and better. d) Scoring model will be applicable only for units with exposures upto Rs.50 lakhs and minimum score of 50 to be obtained.

ASSESSMENT OF LIMIT

Term Loan based on project cost, no upper ceiling. For working capital limits upto Rs. 5 crores- Nayak committee method wouldbe applicable @ a minimum of 25% projected annual turnover. Being a seasonal industry peak level and non peak level limits can be fixed depending on the actual need. A higher limit can be considered selectively on projected balance sheet method.Enhancements in existing units with CRA/CUE rating of upto SB-5/CUE-5 only to be considered. For units with CRA/CUE rating of SB-6 to 9 / CUE-6 to 9, enhancements to be considered against 100% Collateral and with prior approval of GM Network of the Circle.

QUANTUM OF LOAN

Need Based as per Assessment

LTV/MARGIN

Term Loan: 15% - 25%Working capital:Stocks 15% - 20%Book debts: 25% - 40%

Term Loan: 25%Working capital:Stocks: 25%Book debts: 40%

SECURITY a) Primary: Hypothecation of Assets financed by the Bank.

b) Collateral: With CGFMU / CGTMSE Cover: i. Loans to Micro units with exposure upto Rs.10 lakhs (PMMY-MUDRA loans) shall be mandatorily covered under Credit Guarantee Fund for Micro Units (CGFMU).ii. Accounts with exposure above Rs.10 lakhs upto Rs. 1 Cr. could be covered under CGTMSE, as per the willingness of the borrower unit, as they have to bear theAnnual Guarantee Fee (AGF) of CGTMSE.

Without CGFMU / CGTMSE Cover:Equitable mortgage of property / tangiblesecurity belonging to borrower / guarantorvalued not less than 75% of the loan amount.

a) Primary: Hypothecation of Assets financed by the Bank.

b) Collateral: With CGFMU / CGTMSE Cover: i. Loans to Micro units with exposure upto Rs.10 lakhs (PMMY-MUDRA loans) shall be mandatorily covered under Credit Guarantee Fund for Micro Units (CGFMU).ii. Accounts with exposure above Rs.10 lakhs upto Rs. 1 Cr. could be covered under CGTMSE, as per the willingness of the borrower unit, as they have to bear theAnnual Guarantee Fee (AGF) of CGTMSE.

Without CGFMU / CGTMSE Cover:Equitable mortgage of property / tangiblesecurity belonging to borrower / guarantorvalued not less than 75% of the loan amount.

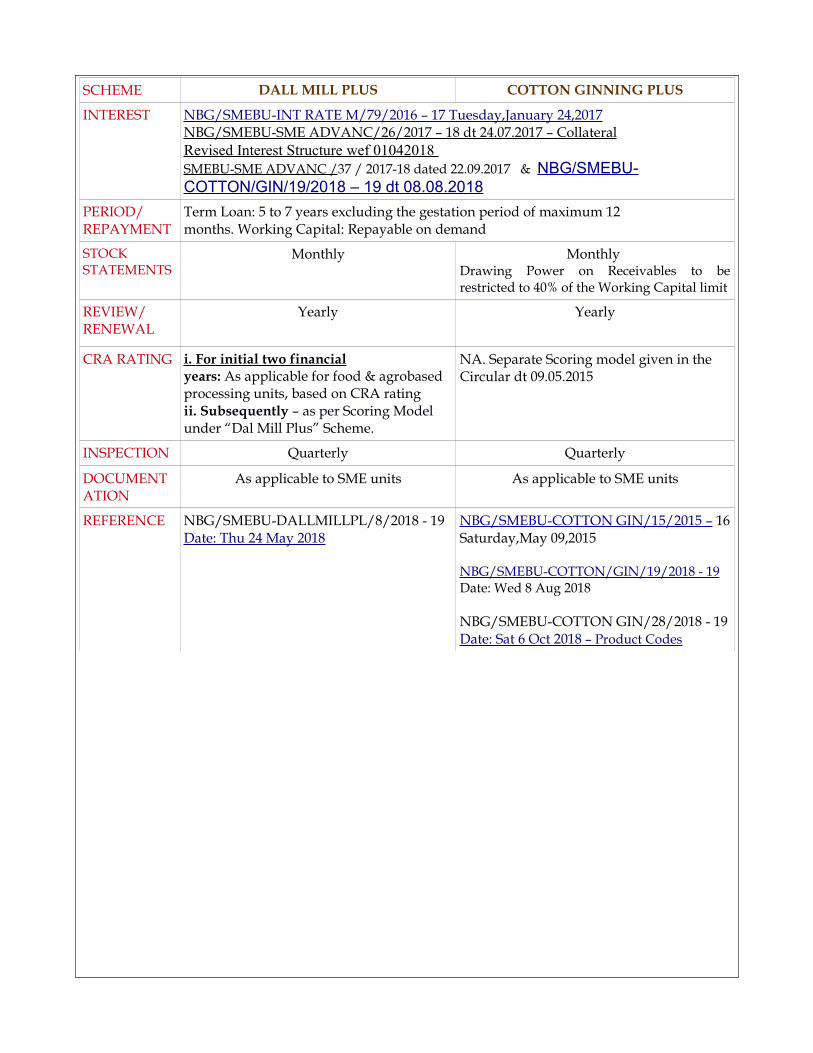

SCHEME DALL MILL PLUS COTTON GINNING PLUS

INTEREST NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017NBG/SMEBU-SME ADVANC/26/2017 – 18 dt 24.07.2017 – CollateralRevised Interest Structure wef 01042018 SMEBU-SME ADVANC /37 / 2017-18 dated 22.09.2017 & NBG/SMEBU-COTTON/GIN/19/2018 – 19 dt 08.08.2018

PERIOD/REPAYMENT

Term Loan: 5 to 7 years excluding the gestation period of maximum 12months. Working Capital: Repayable on demand

STOCK STATEMENTS

Monthly Monthly Drawing Power on Receivables to be restricted to 40% of the Working Capital limit

REVIEW/ RENEWAL

Yearly Yearly

CRA RATING i. For initial two financial years: As applicable for food & agrobasedprocessing units, based on CRA ratingii. Subsequently – as per Scoring Model under “Dal Mill Plus” Scheme.

NA. Separate Scoring model given in the Circular dt 09.05.2015

INSPECTION Quarterly Quarterly

DOCUMENTATION

As applicable to SME units As applicable to SME units

REFERENCE NBG/SMEBU-DALLMILLPL/8/2018 - 19Date: Thu 24 May 2018

NBG/SMEBU-COTTON GIN/15/2015 – 16 Saturday,May 09,2015

NBG/SMEBU-COTTON/GIN/19/2018 - 19Date: Wed 8 Aug 2018

NBG/SMEBU-COTTON GIN/28/2018 - 19Date: Sat 6 Oct 2018 – Product Codes

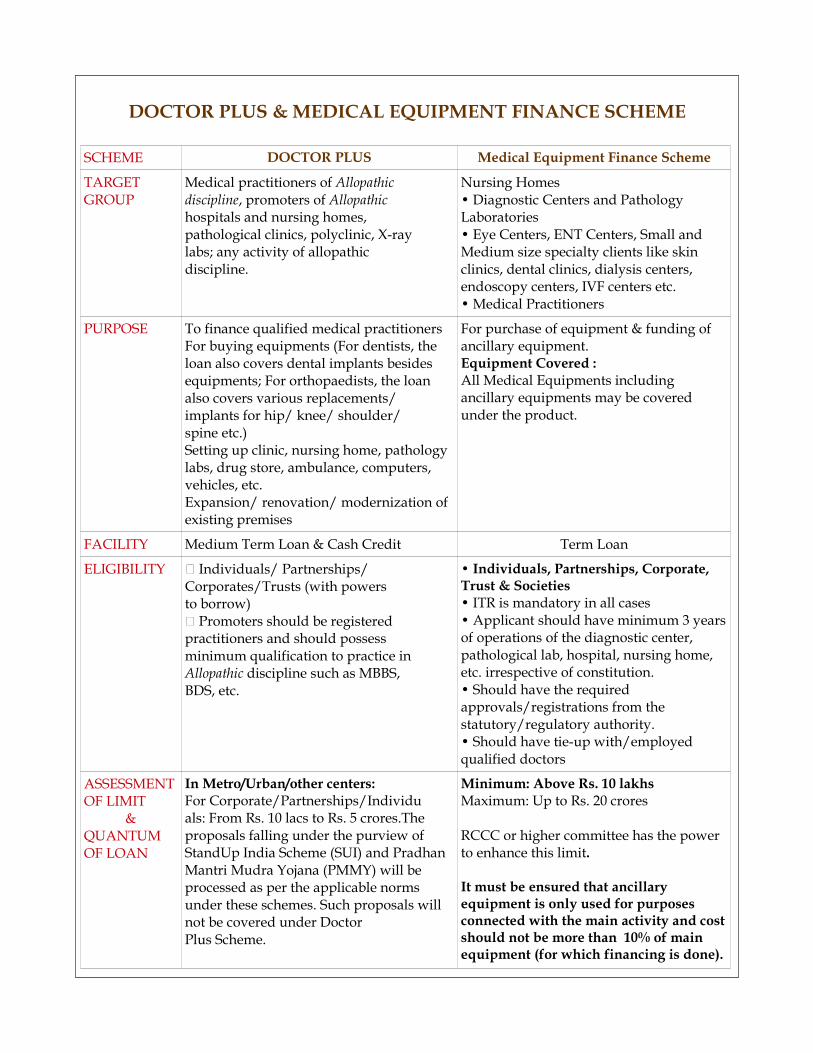

DOCTOR PLUS & MEDICAL EQUIPMENT FINANCE SCHEME

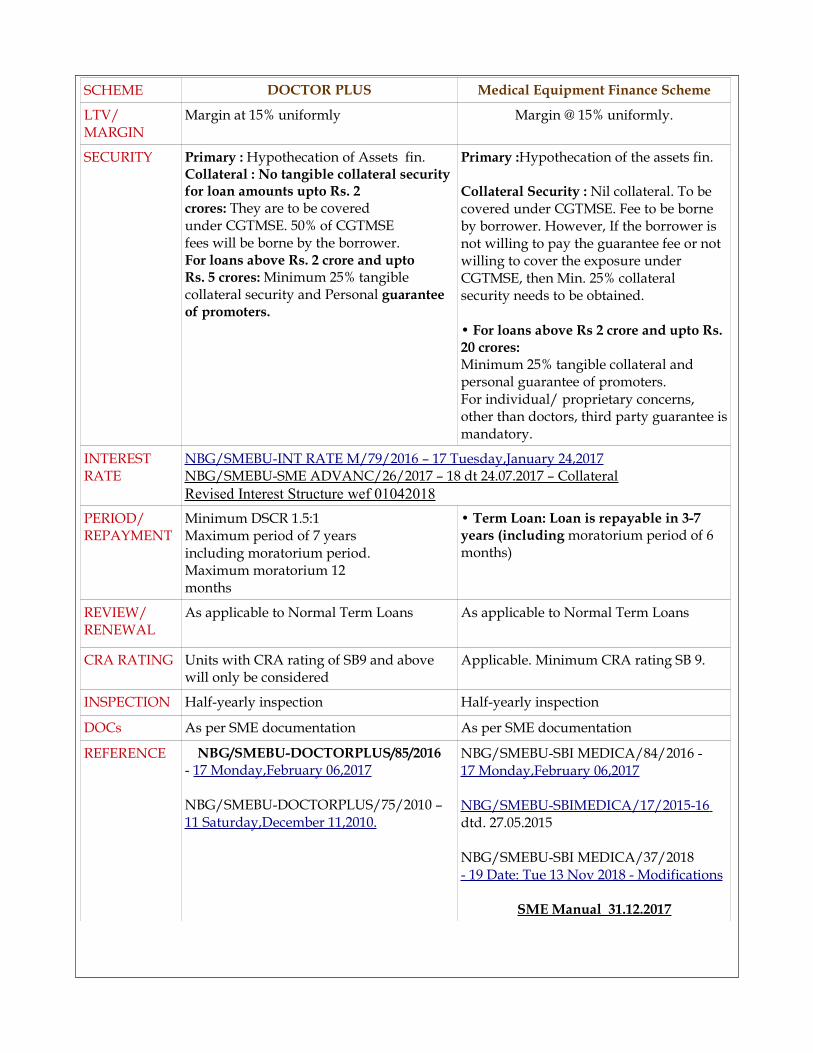

SCHEME DOCTOR PLUS Medical Equipment Finance Scheme

TARGET GROUP

Medical practitioners of Allopathicdiscipline, promoters of Allopathichospitals and nursing homes,pathological clinics, polyclinic, X-raylabs; any activity of allopathicdiscipline.

Nursing Homes• Diagnostic Centers and Pathology Laboratories• Eye Centers, ENT Centers, Small and Medium size specialty clients like skin clinics, dental clinics, dialysis centers,endoscopy centers, IVF centers etc.• Medical Practitioners

PURPOSE To finance qualified medical practitionersFor buying equipments (For dentists, the loan also covers dental implants besides equipments; For orthopaedists, the loan also covers various replacements/ implants for hip/ knee/ shoulder/spine etc.)Setting up clinic, nursing home, pathology labs, drug store, ambulance, computers, vehicles, etc.Expansion/ renovation/ modernization of existing premises

For purchase of equipment & funding of ancillary equipment.Equipment Covered :All Medical Equipments includingancillary equipments may be coveredunder the product.

FACILITY Medium Term Loan & Cash Credit Term Loan

ELIGIBILITY � Individuals/ Partnerships/ Corporates/Trusts (with powersto borrow)� Promoters should be registeredpractitioners and should possessminimum qualification to practice inAllopathic discipline such as MBBS,BDS, etc.

• Individuals, Partnerships, Corporate, Trust & Societies• ITR is mandatory in all cases• Applicant should have minimum 3 years of operations of the diagnostic center, pathological lab, hospital, nursing home, etc. irrespective of constitution.• Should have the required approvals/registrations from thestatutory/regulatory authority.• Should have tie-up with/employed qualified doctors

ASSESSMENT OF LIMIT

&QUANTUM OF LOAN

In Metro/Urban/other centers:For Corporate/Partnerships/Individuals: From Rs. 10 lacs to Rs. 5 crores.The proposals falling under the purview of StandUp India Scheme (SUI) and PradhanMantri Mudra Yojana (PMMY) will be processed as per the applicable norms under these schemes. Such proposals willnot be covered under DoctorPlus Scheme.

Minimum: Above Rs. 10 lakhsMaximum: Up to Rs. 20 crores

RCCC or higher committee has the power to enhance this limit.

It must be ensured that ancillary equipment is only used for purposesconnected with the main activity and cost should not be more than 10% of main equipment (for which financing is done).

SCHEME DOCTOR PLUS Medical Equipment Finance Scheme

LTV/MARGIN

Margin at 15% uniformly Margin @ 15% uniformly.

SECURITY Primary : Hypothecation of Assets fin.Collateral : No tangible collateral securityfor loan amounts upto Rs. 2crores: They are to be coveredunder CGTMSE. 50% of CGTMSEfees will be borne by the borrower.For loans above Rs. 2 crore and uptoRs. 5 crores: Minimum 25% tangiblecollateral security and Personal guarantee of promoters.

Primary :Hypothecation of the assets fin.

Collateral Security : Nil collateral. To be covered under CGTMSE. Fee to be borne by borrower. However, If the borrower is not willing to pay the guarantee fee or not willing to cover the exposure under CGTMSE, then Min. 25% collateral security needs to be obtained.

• For loans above Rs 2 crore and upto Rs. 20 crores:Minimum 25% tangible collateral and personal guarantee of promoters.For individual/ proprietary concerns, other than doctors, third party guarantee is mandatory.

INTEREST RATE

NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017NBG/SMEBU-SME ADVANC/26/2017 – 18 dt 24.07.2017 – CollateralRevised Interest Structure wef 01042018

PERIOD/REPAYMENT

Minimum DSCR 1.5:1Maximum period of 7 yearsincluding moratorium period.Maximum moratorium 12months

• Term Loan: Loan is repayable in 3-7 years (including moratorium period of 6 months)

REVIEW/ RENEWAL

As applicable to Normal Term Loans As applicable to Normal Term Loans

CRA RATING Units with CRA rating of SB9 and abovewill only be considered

Applicable. Minimum CRA rating SB 9.

INSPECTION Half-yearly inspection Half-yearly inspection

DOCs As per SME documentation As per SME documentation

REFERENCE NBG/SMEBU-DOCTORPLUS/85/2016- 17 Monday,February 06,2017

NBG/SMEBU-DOCTORPLUS/75/2010 – 11 Saturday,December 11,2010.

NBG/SMEBU-SBI MEDICA/84/2016 -17 Monday,February 06,2017

NBG/SMEBU-SBIMEDICA/17/2015-16 dtd. 27.05.2015

NBG/SMEBU-SBI MEDICA/37/2018- 19 Date: Tue 13 Nov 2018 - Modifications

SME Manual 31.12.2017

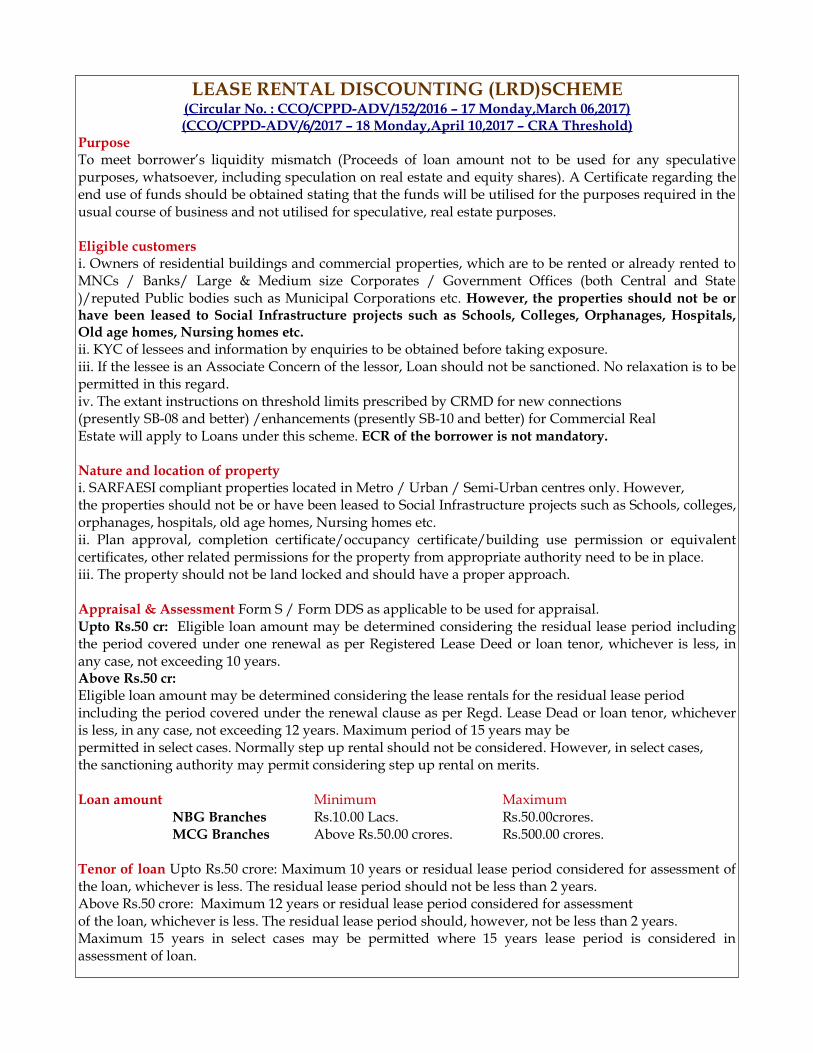

LEASE RENTAL DISCOUNTING (LRD)SCHEME(Circular No. : CCO/CPPD-ADV/152/2016 – 17 Monday,March 06,2017)(CCO/CPPD-ADV/6/2017 – 18 Monday,April 10,2017 – CRA Threshold)

PurposeTo meet borrower’s liquidity mismatch (Proceeds of loan amount not to be used for any speculative purposes, whatsoever, including speculation on real estate and equity shares). A Certificate regarding the end use of funds should be obtained stating that the funds will be utilised for the purposes required in the usual course of business and not utilised for speculative, real estate purposes.

Eligible customersi. Owners of residential buildings and commercial properties, which are to be rented or already rented to MNCs / Banks/ Large & Medium size Corporates / Government Offices (both Central and State)/reputed Public bodies such as Municipal Corporations etc. However, the properties should not be or have been leased to Social Infrastructure projects such as Schools, Colleges, Orphanages, Hospitals, Old age homes, Nursing homes etc.ii. KYC of lessees and information by enquiries to be obtained before taking exposure.iii. If the lessee is an Associate Concern of the lessor, Loan should not be sanctioned. No relaxation is to be permitted in this regard.iv. The extant instructions on threshold limits prescribed by CRMD for new connections(presently SB-08 and better) /enhancements (presently SB-10 and better) for Commercial RealEstate will apply to Loans under this scheme. ECR of the borrower is not mandatory.

Nature and location of propertyi. SARFAESI compliant properties located in Metro / Urban / Semi-Urban centres only. However,the properties should not be or have been leased to Social Infrastructure projects such as Schools, colleges, orphanages, hospitals, old age homes, Nursing homes etc.ii. Plan approval, completion certificate/occupancy certificate/building use permission or equivalent certificates, other related permissions for the property from appropriate authority need to be in place.iii. The property should not be land locked and should have a proper approach.

Appraisal & Assessment Form S / Form DDS as applicable to be used for appraisal.Upto Rs.50 cr: Eligible loan amount may be determined considering the residual lease period including the period covered under one renewal as per Registered Lease Deed or loan tenor, whichever is less, in any case, not exceeding 10 years. Above Rs.50 cr:Eligible loan amount may be determined considering the lease rentals for the residual lease periodincluding the period covered under the renewal clause as per Regd. Lease Dead or loan tenor, whichever is less, in any case, not exceeding 12 years. Maximum period of 15 years may bepermitted in select cases. Normally step up rental should not be considered. However, in select cases,the sanctioning authority may permit considering step up rental on merits.

Loan amount Minimum MaximumNBG Branches Rs.10.00 Lacs. Rs.50.00crores.MCG Branches Above Rs.50.00 crores. Rs.500.00 crores.

Tenor of loan Upto Rs.50 crore: Maximum 10 years or residual lease period considered for assessment of the loan, whichever is less. The residual lease period should not be less than 2 years.Above Rs.50 crore: Maximum 12 years or residual lease period considered for assessmentof the loan, whichever is less. The residual lease period should, however, not be less than 2 years.Maximum 15 years in select cases may be permitted where 15 years lease period is considered in assessment of loan.

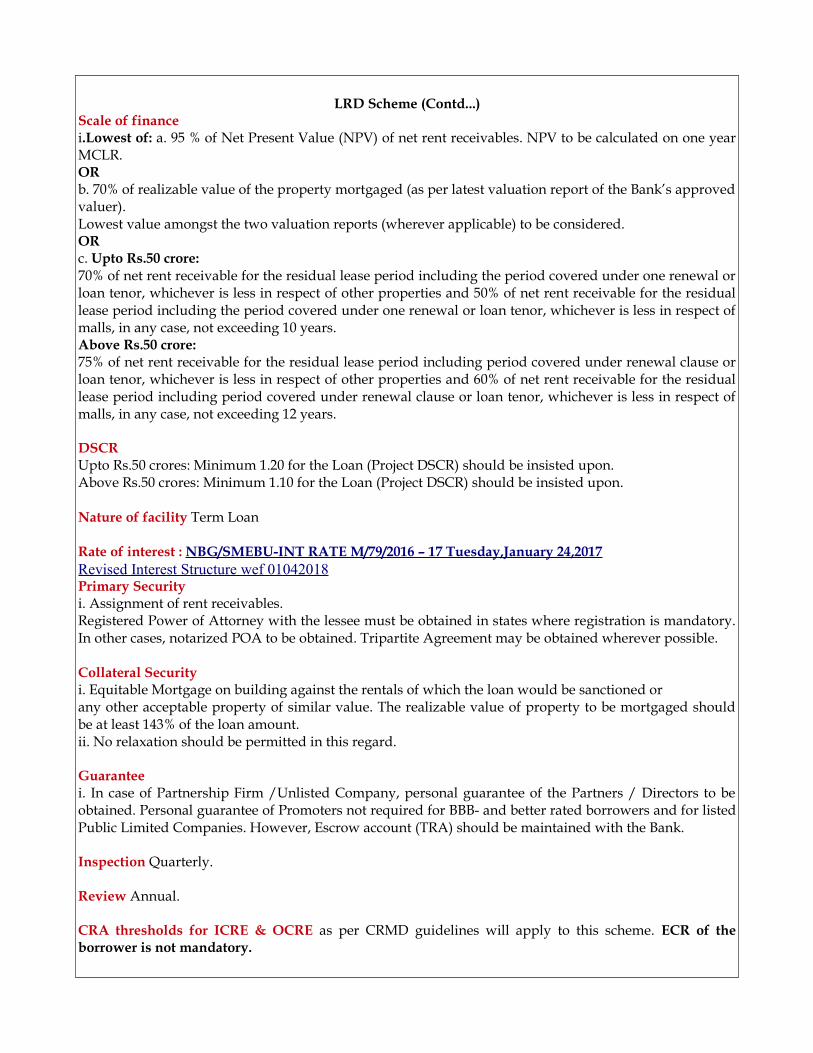

LRD Scheme (Contd...)Scale of financei.Lowest of: a. 95 % of Net Present Value (NPV) of net rent receivables. NPV to be calculated on one year MCLR.ORb. 70% of realizable value of the property mortgaged (as per latest valuation report of the Bank’s approved valuer).Lowest value amongst the two valuation reports (wherever applicable) to be considered.ORc. Upto Rs.50 crore:70% of net rent receivable for the residual lease period including the period covered under one renewal or loan tenor, whichever is less in respect of other properties and 50% of net rent receivable for the residual lease period including the period covered under one renewal or loan tenor, whichever is less in respect of malls, in any case, not exceeding 10 years. Above Rs.50 crore:75% of net rent receivable for the residual lease period including period covered under renewal clause or loan tenor, whichever is less in respect of other properties and 60% of net rent receivable for the residual lease period including period covered under renewal clause or loan tenor, whichever is less in respect of malls, in any case, not exceeding 12 years.

DSCRUpto Rs.50 crores: Minimum 1.20 for the Loan (Project DSCR) should be insisted upon.Above Rs.50 crores: Minimum 1.10 for the Loan (Project DSCR) should be insisted upon.

Nature of facility Term Loan

Rate of interest : NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017Revised Interest Structure wef 01042018Primary Securityi. Assignment of rent receivables. Registered Power of Attorney with the lessee must be obtained in states where registration is mandatory. In other cases, notarized POA to be obtained. Tripartite Agreement may be obtained wherever possible.

Collateral Securityi. Equitable Mortgage on building against the rentals of which the loan would be sanctioned orany other acceptable property of similar value. The realizable value of property to be mortgaged should be at least 143% of the loan amount.ii. No relaxation should be permitted in this regard.

Guaranteei. In case of Partnership Firm /Unlisted Company, personal guarantee of the Partners / Directors to be obtained. Personal guarantee of Promoters not required for BBB- and better rated borrowers and for listed Public Limited Companies. However, Escrow account (TRA) should be maintained with the Bank.

Inspection Quarterly.

Review Annual.

CRA thresholds for ICRE & OCRE as per CRMD guidelines will apply to this scheme. ECR of the borrower is not mandatory.

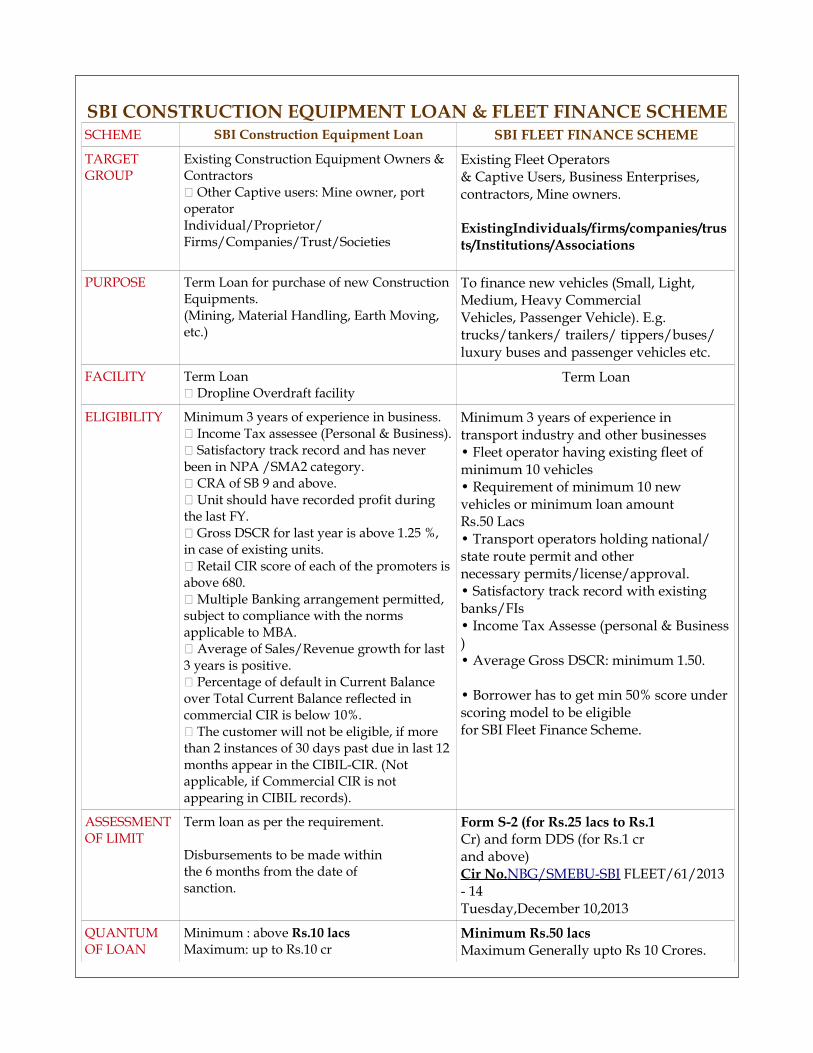

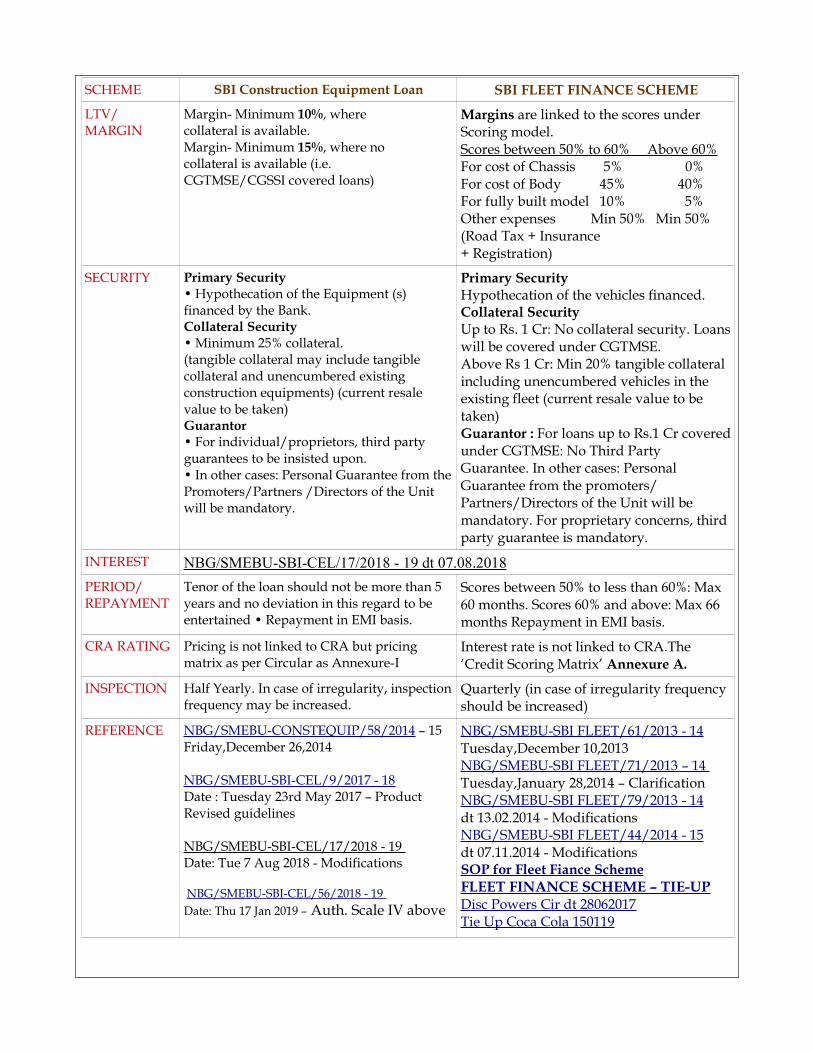

SBI CONSTRUCTION EQUIPMENT LOAN & FLEET FINANCE SCHEMESCHEME SBI Construction Equipment Loan SBI FLEET FINANCE SCHEME

TARGET GROUP

Existing Construction Equipment Owners & Contractors� Other Captive users: Mine owner, port operatorIndividual/Proprietor/ Firms/Companies/Trust/Societies

Existing Fleet Operators& Captive Users, Business Enterprises,contractors, Mine owners.

ExistingIndividuals/firms/companies/trusts/Institutions/Associations

PURPOSE Term Loan for purchase of new Construction Equipments.(Mining, Material Handling, Earth Moving, etc.)

To finance new vehicles (Small, Light, Medium, Heavy CommercialVehicles, Passenger Vehicle). E.g. trucks/tankers/ trailers/ tippers/buses/luxury buses and passenger vehicles etc.

FACILITY Term Loan� Dropline Overdraft facility

Term Loan

ELIGIBILITY Minimum 3 years of experience in business.� Income Tax assessee (Personal & Business).� Satisfactory track record and has never been in NPA /SMA2 category.� CRA of SB 9 and above.� Unit should have recorded profit during the last FY.� Gross DSCR for last year is above 1.25 %, in case of existing units.� Retail CIR score of each of the promoters is above 680.� Multiple Banking arrangement permitted, subject to compliance with the norms applicable to MBA.� Average of Sales/Revenue growth for last 3 years is positive.� Percentage of default in Current Balance over Total Current Balance reflected in commercial CIR is below 10%.� The customer will not be eligible, if more than 2 instances of 30 days past due in last 12 months appear in the CIBIL-CIR. (Not applicable, if Commercial CIR is not appearing in CIBIL records).

Minimum 3 years of experience intransport industry and other businesses• Fleet operator having existing fleet of minimum 10 vehicles• Requirement of minimum 10 new vehicles or minimum loan amountRs.50 Lacs• Transport operators holding national/ state route permit and othernecessary permits/license/approval.• Satisfactory track record with existing banks/FIs• Income Tax Assesse (personal & Business)• Average Gross DSCR: minimum 1.50.

• Borrower has to get min 50% score under scoring model to be eligiblefor SBI Fleet Finance Scheme.

ASSESSMENT OF LIMIT

Term loan as per the requirement.

Disbursements to be made withinthe 6 months from the date ofsanction.

Form S-2 (for Rs.25 lacs to Rs.1Cr) and form DDS (for Rs.1 crand above) Cir No. NBG/SMEBU-SBI FLEET/61/2013 - 14Tuesday,December 10,2013

QUANTUM OF LOAN

Minimum : above Rs.10 lacsMaximum: up to Rs.10 cr

Minimum Rs.50 lacsMaximum Generally upto Rs 10 Crores.

SCHEME SBI Construction Equipment Loan SBI FLEET FINANCE SCHEME

LTV/MARGIN

Margin- Minimum 10%, wherecollateral is available.Margin- Minimum 15%, where nocollateral is available (i.e.CGTMSE/CGSSI covered loans)

Margins are linked to the scores under Scoring model.Scores between 50% to 60% Above 60%For cost of Chassis 5% 0%For cost of Body 45% 40%For fully built model 10% 5%Other expenses Min 50% Min 50%(Road Tax + Insurance + Registration)

SECURITY Primary Security• Hypothecation of the Equipment (s) financed by the Bank. Collateral Security• Minimum 25% collateral.(tangible collateral may include tangible collateral and unencumbered existing construction equipments) (current resale value to be taken)Guarantor• For individual/proprietors, third party guarantees to be insisted upon.• In other cases: Personal Guarantee from the Promoters/Partners /Directors of the Unit will be mandatory.

Primary SecurityHypothecation of the vehicles financed.Collateral SecurityUp to Rs. 1 Cr: No collateral security. Loans will be covered under CGTMSE.Above Rs 1 Cr: Min 20% tangible collateral including unencumbered vehicles in the existing fleet (current resale value to be taken)Guarantor : For loans up to Rs.1 Cr covered under CGTMSE: No Third Party Guarantee. In other cases: Personal Guarantee from the promoters/ Partners/Directors of the Unit will be mandatory. For proprietary concerns, third party guarantee is mandatory.

INTEREST NBG/SMEBU-SBI-CEL/17/2018 - 19 dt 07.08.2018PERIOD/REPAYMENT

Tenor of the loan should not be more than 5 years and no deviation in this regard to beentertained • Repayment in EMI basis.

Scores between 50% to less than 60%: Max 60 months. Scores 60% and above: Max 66 months Repayment in EMI basis.

CRA RATING Pricing is not linked to CRA but pricing matrix as per Circular as Annexure-I

Interest rate is not linked to CRA.The ‘Credit Scoring Matrix’ Annexure A.

INSPECTION Half Yearly. In case of irregularity, inspection frequency may be increased.

Quarterly (in case of irregularity frequency should be increased)

REFERENCE NBG/SMEBU-CONSTEQUIP/58/2014 – 15 Friday,December 26,2014

NBG/SMEBU-SBI-CEL/9/2017 - 18Date : Tuesday 23rd May 2017 – Product Revised guidelines

NBG/SMEBU-SBI-CEL/17/2018 - 19 Date: Tue 7 Aug 2018 - Modifications

NBG/SMEBU-SBI-CEL/56/2018 - 19 Date: Thu 17 Jan 2019 – Auth. Scale IV above

NBG/SMEBU-SBI FLEET/61/2013 - 14Tuesday,December 10,2013NBG/SMEBU-SBI FLEET/71/2013 – 14 Tuesday,January 28,2014 – ClarificationNBG/SMEBU-SBI FLEET/79/2013 - 14dt 13.02.2014 - ModificationsNBG/SMEBU-SBI FLEET/44/2014 - 15dt 07.11.2014 - ModificationsSOP for Fleet Fiance SchemeFLEET FINANCE SCHEME – TIE-UPDisc Powers Cir dt 28062017Tie Up Coca Cola 150119

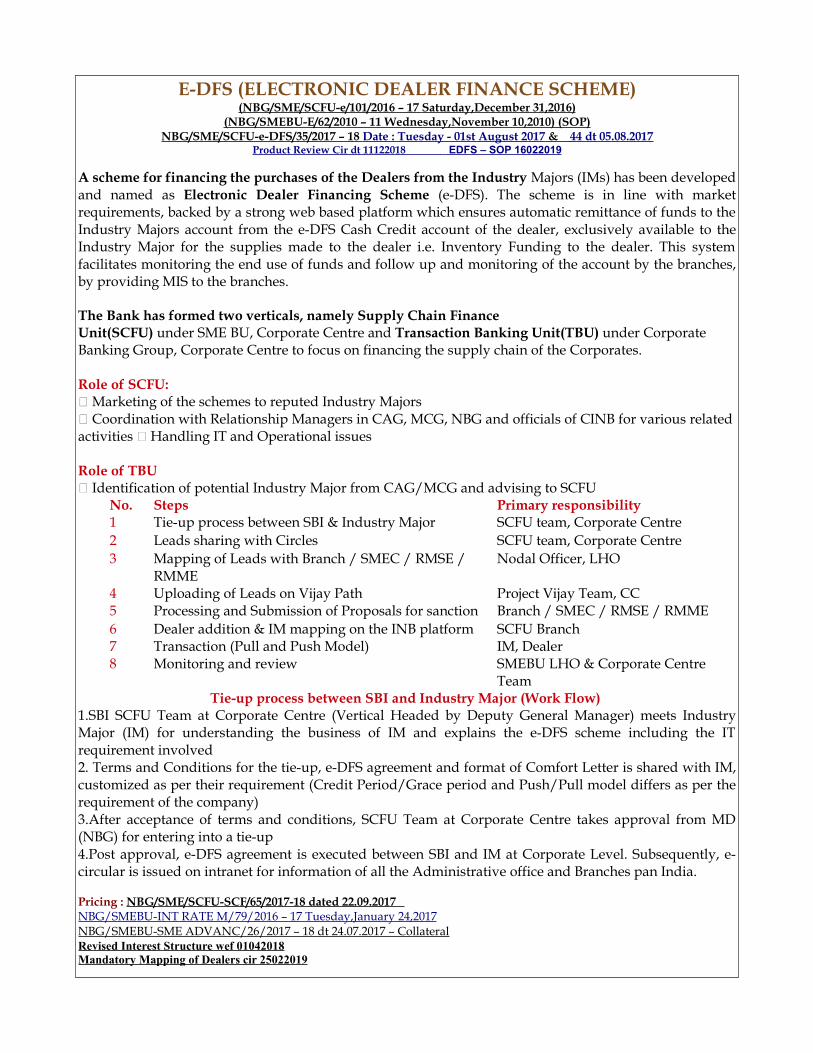

E-DFS (ELECTRONIC DEALER FINANCE SCHEME)(NBG/SME/SCFU-e/101/2016 – 17 Saturday,December 31,2016)

(NBG/SMEBU-E/62/2010 – 11 Wednesday,November 10,2010) (SOP)NBG/SME/SCFU-e-DFS/35/2017 – 18 Date : Tuesday - 01st August 2017 & 44 dt 05.08.2017

Product Review Cir dt 11122018 EDFS – SOP 16022019

A scheme for financing the purchases of the Dealers from the Industry Majors (IMs) has been developed and named as Electronic Dealer Financing Scheme (e-DFS). The scheme is in line with market requirements, backed by a strong web based platform which ensures automatic remittance of funds to the Industry Majors account from the e-DFS Cash Credit account of the dealer, exclusively available to the Industry Major for the supplies made to the dealer i.e. Inventory Funding to the dealer. This system facilitates monitoring the end use of funds and follow up and monitoring of the account by the branches, by providing MIS to the branches.

The Bank has formed two verticals, namely Supply Chain FinanceUnit(SCFU) under SME BU, Corporate Centre and Transaction Banking Unit(TBU) under Corporate Banking Group, Corporate Centre to focus on financing the supply chain of the Corporates.

Role of SCFU:� Marketing of the schemes to reputed Industry Majors� Coordination with Relationship Managers in CAG, MCG, NBG and officials of CINB for various related activities � Handling IT and Operational issues

Role of TBU� Identification of potential Industry Major from CAG/MCG and advising to SCFU

No. Steps Primary responsibility 1 Tie-up process between SBI & Industry Major SCFU team, Corporate Centre 2 Leads sharing with Circles SCFU team, Corporate Centre 3 Mapping of Leads with Branch / SMEC / RMSE /

RMME Nodal Officer, LHO

4 Uploading of Leads on Vijay Path Project Vijay Team, CC 5 Processing and Submission of Proposals for sanction Branch / SMEC / RMSE / RMME 6 Dealer addition & IM mapping on the INB platform SCFU Branch 7 Transaction (Pull and Push Model) IM, Dealer 8 Monitoring and review SMEBU LHO & Corporate Centre

Team Tie-up process between SBI and Industry Major (Work Flow)

1.SBI SCFU Team at Corporate Centre (Vertical Headed by Deputy General Manager) meets Industry Major (IM) for understanding the business of IM and explains the e-DFS scheme including the IT requirement involved 2. Terms and Conditions for the tie-up, e-DFS agreement and format of Comfort Letter is shared with IM, customized as per their requirement (Credit Period/Grace period and Push/Pull model differs as per the requirement of the company) 3.After acceptance of terms and conditions, SCFU Team at Corporate Centre takes approval from MD (NBG) for entering into a tie-up 4.Post approval, e-DFS agreement is executed between SBI and IM at Corporate Level. Subsequently, e- circular is issued on intranet for information of all the Administrative office and Branches pan India.

Pricing : NBG/SME/SCFU-SCF/65/2017-18 dated 22.09.2017 NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017NBG/SMEBU-SME ADVANC/26/2017 – 18 dt 24.07.2017 – CollateralRevised Interest Structure wef 01042018Mandatory Mapping of Dealers cir 25022019

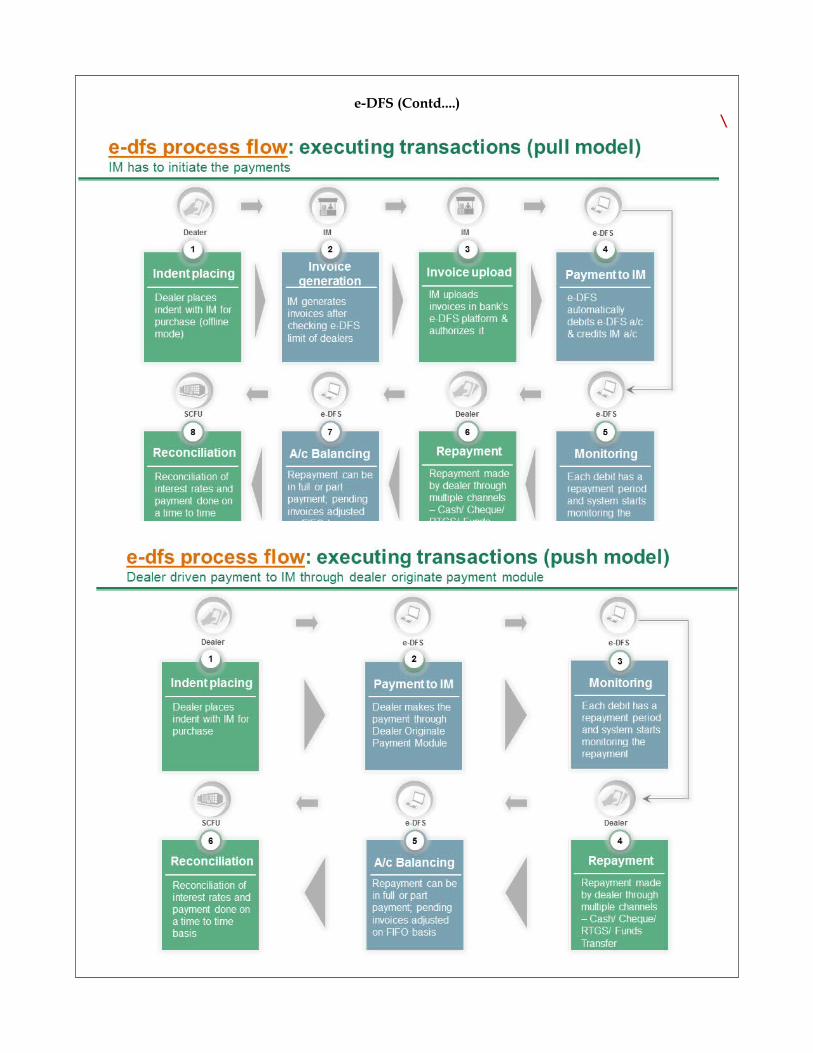

e-DFS (Contd....)\

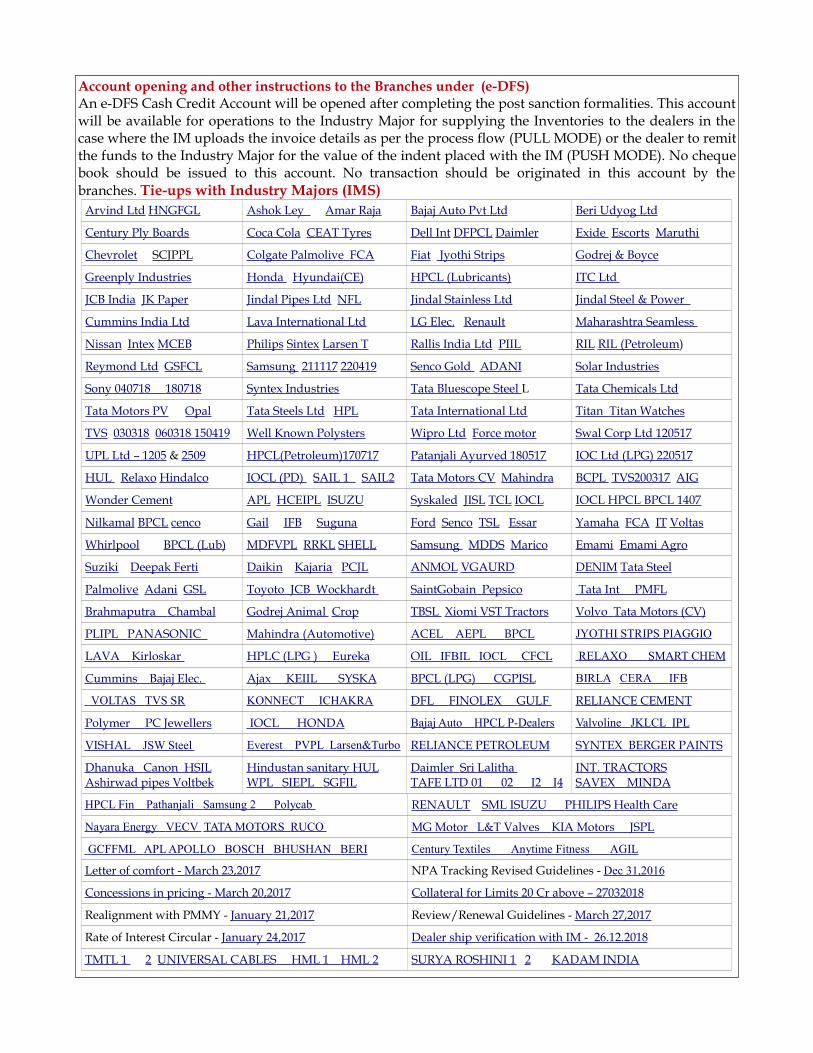

Account opening and other instructions to the Branches under (e-DFS)An e-DFS Cash Credit Account will be opened after completing the post sanction formalities. This account will be available for operations to the Industry Major for supplying the Inventories to the dealers in the case where the IM uploads the invoice details as per the process flow (PULL MODE) or the dealer to remit the funds to the Industry Major for the value of the indent placed with the IM (PUSH MODE). No cheque book should be issued to this account. No transaction should be originated in this account by the branches. Tie-ups with Industry Majors (IMS)

Arvind Ltd HNGFGL Ashok Ley Amar Raja Bajaj Auto Pvt Ltd Beri Udyog Ltd

Century Ply Boards Coca Cola CEAT Tyres Dell Int DFPCL Daimler Exide Escorts Maruthi

Chevrolet SCJPPL Colgate Palmolive FCA Fiat Jyothi Strips Godrej & Boyce

Greenply Industries Honda Hyundai(CE) HPCL (Lubricants) ITC Ltd

JCB India JK Paper Jindal Pipes Ltd NFL Jindal Stainless Ltd Jindal Steel & Power

Cummins India Ltd Lava International Ltd LG Elec. Renault Maharashtra Seamless

Nissan Intex MCEB Philips Sintex Larsen T Rallis India Ltd PIIL RIL RIL (Petroleum)

Reymond Ltd GSFCL Samsung 211117 220419 Senco Gold ADANI Solar Industries

Sony 040718 180718 Syntex Industries Tata Bluescope Steel L Tata Chemicals Ltd

Tata Motors PV Opal Tata Steels Ltd HPL Tata International Ltd Titan Titan Watches

TVS 030318 060318 150419 Well Known Polysters Wipro Ltd Force motor Swal Corp Ltd 120517

UPL Ltd – 1205 & 2509 HPCL(Petroleum)170717 Patanjali Ayurved 180517 IOC Ltd (LPG) 220517

HUL Relaxo Hindalco IOCL (PD) SAIL 1 SAIL2 Tata Motors CV Mahindra BCPL TVS200317 AIG

Wonder Cement APL HCEIPL ISUZU Syskaled JISL TCL IOCL IOCL HPCL BPCL 1407

Nilkamal BPCL cenco Gail IFB Suguna Ford Senco TSL Essar Yamaha FCA IT Voltas

Whirlpool BPCL (Lub) MDFVPL RRKL SHELL Samsung MDDS Marico Emami Emami Agro

Suziki Deepak Ferti Daikin Kajaria PCJL ANMOL VGAURD DENIM Tata Steel

Palmolive Adani GSL Toyoto JCB Wockhardt SaintGobain Pepsico Tata Int PMFL

Brahmaputra Chambal Godrej Animal Crop TBSL Xiomi VST Tractors Volvo Tata Motors (CV)

PLIPL PANASONIC Mahindra (Automotive) ACEL AEPL BPCL JYOTHI STRIPS PIAGGIO

LAVA Kirloskar HPLC (LPG ) Eureka OIL IFBIL IOCL CFCL RELAXO SMART CHEM

Cummins Bajaj Elec. Ajax KEIIL SYSKA BPCL (LPG) CGPISL BIRLA CERA IFB

VOLTAS TVS SR KONNECT ICHAKRA DFL FINOLEX GULF RELIANCE CEMENT

Polymer PC Jewellers IOCL HONDA Bajaj Auto HPCL P-Dealers Valvoline JKLCL IPL

VISHAL JSW Steel Everest PVPL Larsen&Turbo RELIANCE PETROLEUM SYNTEX BERGER PAINTS

Dhanuka Canon HSIL Ashirwad p ipes Voltbek

Hindustan sanitary HUL WPL SIEPL SGFIL

Daimler Sri Lalitha TAFE LTD 01 0 2 I 2 I 4

INT. TRACTORSSAVEX MINDA

HPCL Fin Pathanjali Samsung 2 Polycab RENAULT SML ISUZU PHILIPS Health Care

Nayara Energy VECV TATA MOTORS RUCO MG Motor L&T Valves KIA Motors JSPL

GCFFML APL APOLLO BOSCH BHUSHAN BERI Century Textiles Anytime Fitness AGIL

Letter of comfort - March 23,2017 NPA Tracking Revised Guidelines - Dec 31,2016

Concessions in pricing - March 20,2017 Collateral for Limits 20 Cr above – 27032018

Realignment with PMMY - January 21,2017 Review/Renewal Guidelines - March 27,2017

Rate of Interest Circular - January 24,2017 Dealer ship verification with IM - 26.12.2018

TMTL 1 2 UNIVERSAL CABLES HML 1 HML 2 SURYA ROSHINI 1 2 KADAM INDIA

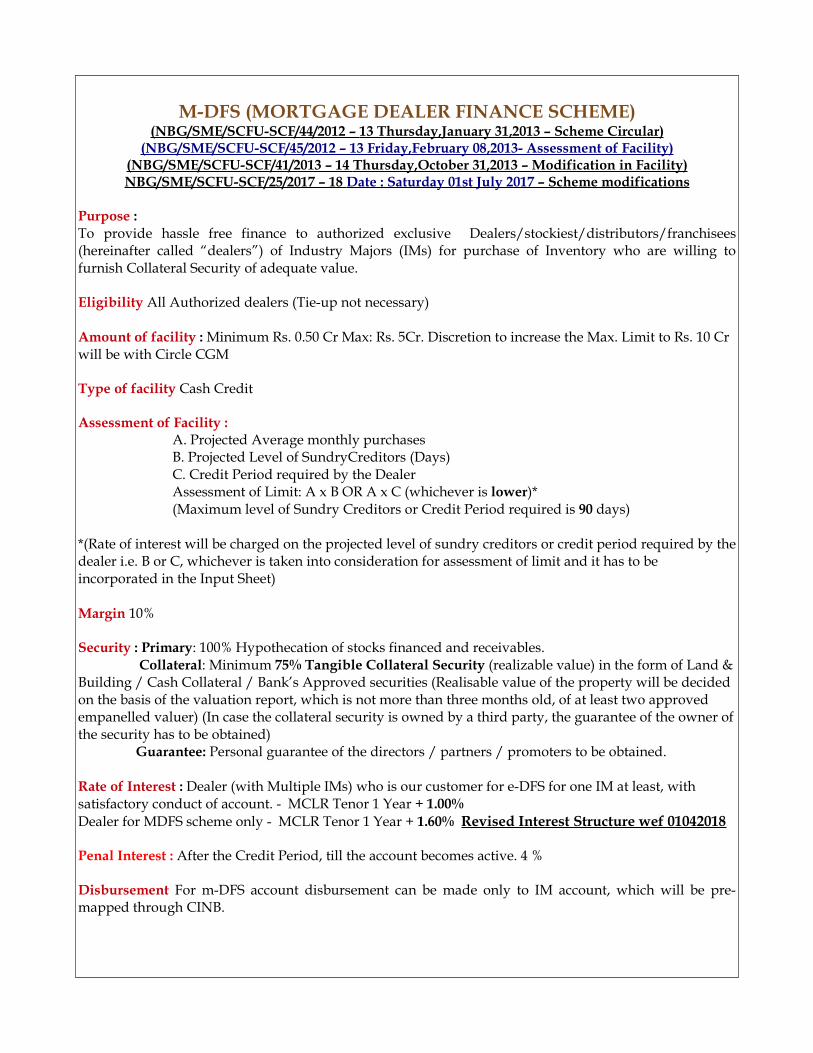

M-DFS (MORTGAGE DEALER FINANCE SCHEME)(NBG/SME/SCFU-SCF/44/2012 – 13 Thursday,January 31,2013 – Scheme Circular)

(NBG/SME/SCFU-SCF/45/2012 – 13 Friday,February 08,2013- Assessment of Facility)(NBG/SME/SCFU-SCF/41/2013 – 14 Thursday,October 31,2013 – Modification in Facility) NBG/SME/SCFU-SCF/25/2017 – 18 Date : Saturday 01st July 2017 – Scheme modifications

Purpose : To provide hassle free finance to authorized exclusive Dealers/stockiest/distributors/franchisees (hereinafter called “dealers”) of Industry Majors (IMs) for purchase of Inventory who are willing to furnish Collateral Security of adequate value.

Eligibility All Authorized dealers (Tie-up not necessary)

Amount of facility : Minimum Rs. 0.50 Cr Max: Rs. 5Cr. Discretion to increase the Max. Limit to Rs. 10 Cr will be with Circle CGM

Type of facility Cash Credit

Assessment of Facility : A. Projected Average monthly purchasesB. Projected Level of SundryCreditors (Days)C. Credit Period required by the DealerAssessment of Limit: A x B OR A x C (whichever is lower)*(Maximum level of Sundry Creditors or Credit Period required is 90 days)

*(Rate of interest will be charged on the projected level of sundry creditors or credit period required by the dealer i.e. B or C, whichever is taken into consideration for assessment of limit and it has to beincorporated in the Input Sheet)

Margin 10%

Security : Primary: 100% Hypothecation of stocks financed and receivables. Collateral: Minimum 75% Tangible Collateral Security (realizable value) in the form of Land &

Building / Cash Collateral / Bank’s Approved securities (Realisable value of the property will be decided on the basis of the valuation report, which is not more than three months old, of at least two approved empanelled valuer) (In case the collateral security is owned by a third party, the guarantee of the owner of the security has to be obtained)

Guarantee: Personal guarantee of the directors / partners / promoters to be obtained.

Rate of Interest : Dealer (with Multiple IMs) who is our customer for e-DFS for one IM at least, withsatisfactory conduct of account. - MCLR Tenor 1 Year + 1.00%Dealer for MDFS scheme only - MCLR Tenor 1 Year + 1.60% Revised Interest Structure wef 01042018

Penal Interest : After the Credit Period, till the account becomes active. 4 %

Disbursement For m-DFS account disbursement can be made only to IM account, which will be pre-mapped through CINB.

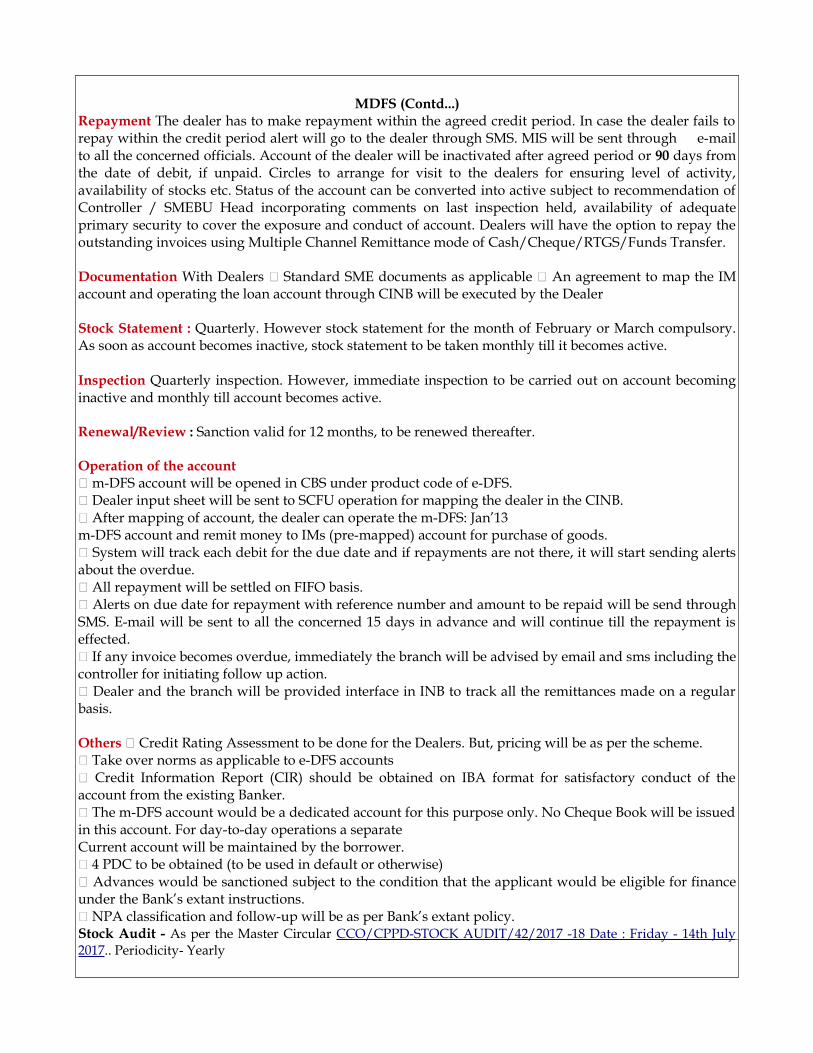

MDFS (Contd...)Repayment The dealer has to make repayment within the agreed credit period. In case the dealer fails to repay within the credit period alert will go to the dealer through SMS. MIS will be sent through e-mail to all the concerned officials. Account of the dealer will be inactivated after agreed period or 90 days from the date of debit, if unpaid. Circles to arrange for visit to the dealers for ensuring level of activity, availability of stocks etc. Status of the account can be converted into active subject to recommendation of Controller / SMEBU Head incorporating comments on last inspection held, availability of adequate primary security to cover the exposure and conduct of account. Dealers will have the option to repay the outstanding invoices using Multiple Channel Remittance mode of Cash/Cheque/RTGS/Funds Transfer.

Documentation With Dealers � Standard SME documents as applicable � An agreement to map the IM account and operating the loan account through CINB will be executed by the Dealer

Stock Statement : Quarterly. However stock statement for the month of February or March compulsory. As soon as account becomes inactive, stock statement to be taken monthly till it becomes active.

Inspection Quarterly inspection. However, immediate inspection to be carried out on account becoming inactive and monthly till account becomes active.

Renewal/Review : Sanction valid for 12 months, to be renewed thereafter.

Operation of the account� m-DFS account will be opened in CBS under product code of e-DFS.� Dealer input sheet will be sent to SCFU operation for mapping the dealer in the CINB.� After mapping of account, the dealer can operate the m-DFS: Jan’13m-DFS account and remit money to IMs (pre-mapped) account for purchase of goods.� System will track each debit for the due date and if repayments are not there, it will start sending alerts about the overdue.� All repayment will be settled on FIFO basis.� Alerts on due date for repayment with reference number and amount to be repaid will be send through SMS. E-mail will be sent to all the concerned 15 days in advance and will continue till the repayment is effected.� If any invoice becomes overdue, immediately the branch will be advised by email and sms including the controller for initiating follow up action.� Dealer and the branch will be provided interface in INB to track all the remittances made on a regular basis.

Others � Credit Rating Assessment to be done for the Dealers. But, pricing will be as per the scheme.� Take over norms as applicable to e-DFS accounts� Credit Information Report (CIR) should be obtained on IBA format for satisfactory conduct of the account from the existing Banker.� The m-DFS account would be a dedicated account for this purpose only. No Cheque Book will be issued in this account. For day-to-day operations a separateCurrent account will be maintained by the borrower.� 4 PDC to be obtained (to be used in default or otherwise)� Advances would be sanctioned subject to the condition that the applicant would be eligible for finance under the Bank’s extant instructions.� NPA classification and follow-up will be as per Bank’s extant policy.Stock Audit - As per the Master Circular CCO/CPPD-STOCK AUDIT/42/2017 -18 Date : Friday - 14th July 2017.. Periodicity- Yearly

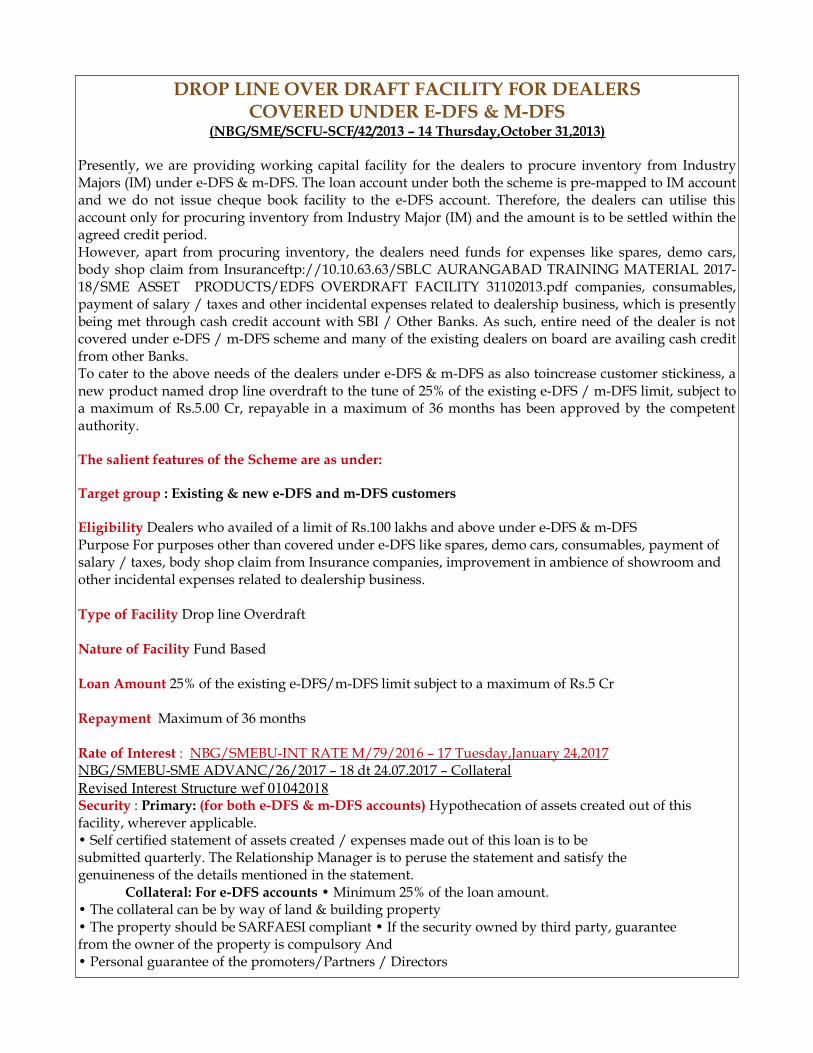

DROP LINE OVER DRAFT FACILITY FOR DEALERSCOVERED UNDER E-DFS & M-DFS

(NBG/SME/SCFU-SCF/42/2013 – 14 Thursday,October 31,2013)

Presently, we are providing working capital facility for the dealers to procure inventory from Industry Majors (IM) under e-DFS & m-DFS. The loan account under both the scheme is pre-mapped to IM account and we do not issue cheque book facility to the e-DFS account. Therefore, the dealers can utilise this account only for procuring inventory from Industry Major (IM) and the amount is to be settled within the agreed credit period.However, apart from procuring inventory, the dealers need funds for expenses like spares, demo cars, body shop claim from Insuranceftp://10.10.63.63/SBLC AURANGABAD TRAINING MATERIAL 2017-18/SME ASSET PRODUCTS/EDFS OVERDRAFT FACILITY 31102013.pdf companies, consumables, payment of salary / taxes and other incidental expenses related to dealership business, which is presently being met through cash credit account with SBI / Other Banks. As such, entire need of the dealer is not covered under e-DFS / m-DFS scheme and many of the existing dealers on board are availing cash credit from other Banks.To cater to the above needs of the dealers under e-DFS & m-DFS as also toincrease customer stickiness, a new product named drop line overdraft to the tune of 25% of the existing e-DFS / m-DFS limit, subject to a maximum of Rs.5.00 Cr, repayable in a maximum of 36 months has been approved by the competent authority.

The salient features of the Scheme are as under:

Target group : Existing & new e-DFS and m-DFS customers

Eligibility Dealers who availed of a limit of Rs.100 lakhs and above under e-DFS & m-DFSPurpose For purposes other than covered under e-DFS like spares, demo cars, consumables, payment of salary / taxes, body shop claim from Insurance companies, improvement in ambience of showroom and other incidental expenses related to dealership business.

Type of Facility Drop line Overdraft

Nature of Facility Fund Based

Loan Amount 25% of the existing e-DFS/m-DFS limit subject to a maximum of Rs.5 Cr

Repayment Maximum of 36 months

Rate of Interest : NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017NBG/SMEBU-SME ADVANC/26/2017 – 18 dt 24.07.2017 – CollateralRevised Interest Structure wef 01042018Security : Primary: (for both e-DFS & m-DFS accounts) Hypothecation of assets created out of this facility, wherever applicable.• Self certified statement of assets created / expenses made out of this loan is to besubmitted quarterly. The Relationship Manager is to peruse the statement and satisfy thegenuineness of the details mentioned in the statement.

Collateral: For e-DFS accounts • Minimum 25% of the loan amount.• The collateral can be by way of land & building property• The property should be SARFAESI compliant • If the security owned by third party, guaranteefrom the owner of the property is compulsory And• Personal guarantee of the promoters/Partners / Directors

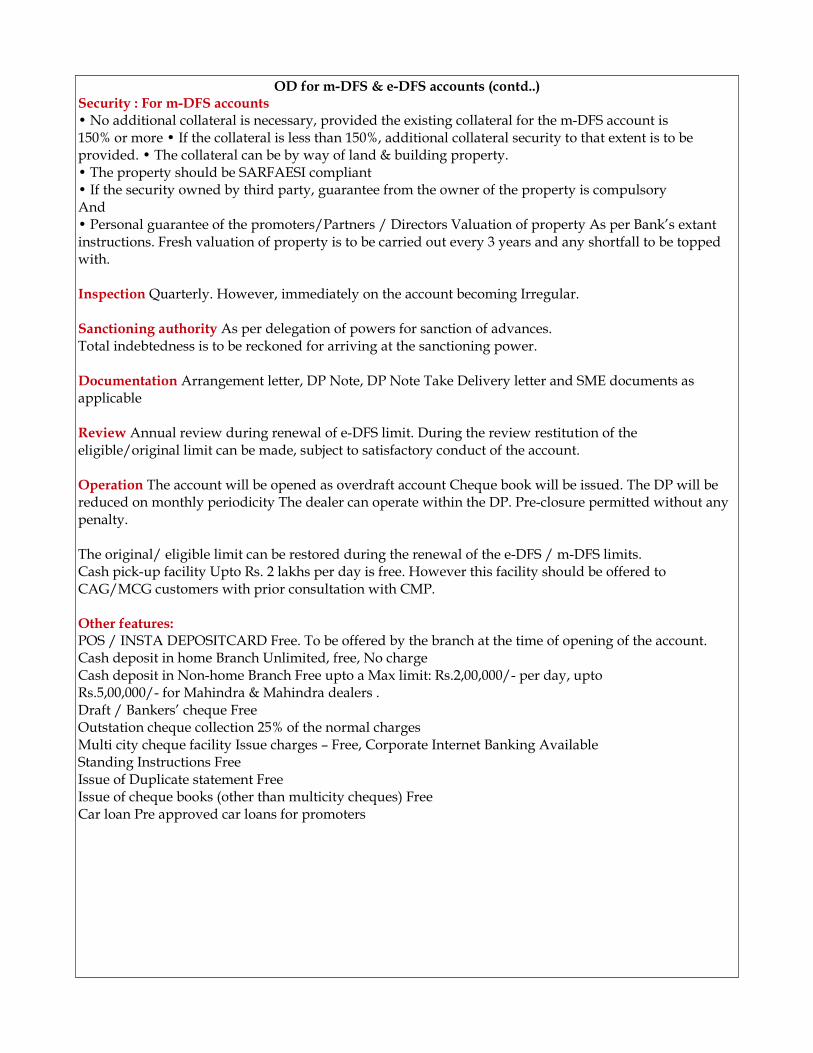

OD for m-DFS & e-DFS accounts (contd..)Security : For m-DFS accounts• No additional collateral is necessary, provided the existing collateral for the m-DFS account is150% or more • If the collateral is less than 150%, additional collateral security to that extent is to be provided. • The collateral can be by way of land & building property.• The property should be SARFAESI compliant• If the security owned by third party, guarantee from the owner of the property is compulsoryAnd • Personal guarantee of the promoters/Partners / Directors Valuation of property As per Bank’s extant instructions. Fresh valuation of property is to be carried out every 3 years and any shortfall to be topped with.

Inspection Quarterly. However, immediately on the account becoming Irregular.

Sanctioning authority As per delegation of powers for sanction of advances.Total indebtedness is to be reckoned for arriving at the sanctioning power.

Documentation Arrangement letter, DP Note, DP Note Take Delivery letter and SME documents as applicable

Review Annual review during renewal of e-DFS limit. During the review restitution of the eligible/original limit can be made, subject to satisfactory conduct of the account.

Operation The account will be opened as overdraft account Cheque book will be issued. The DP will be reduced on monthly periodicity The dealer can operate within the DP. Pre-closure permitted without any penalty.

The original/ eligible limit can be restored during the renewal of the e-DFS / m-DFS limits.Cash pick-up facility Upto Rs. 2 lakhs per day is free. However this facility should be offered to CAG/MCG customers with prior consultation with CMP.

Other features:POS / INSTA DEPOSITCARD Free. To be offered by the branch at the time of opening of the account. Cash deposit in home Branch Unlimited, free, No chargeCash deposit in Non-home Branch Free upto a Max limit: Rs.2,00,000/- per day, uptoRs.5,00,000/- for Mahindra & Mahindra dealers .Draft / Bankers’ cheque Free Outstation cheque collection 25% of the normal chargesMulti city cheque facility Issue charges – Free, Corporate Internet Banking AvailableStanding Instructions Free Issue of Duplicate statement FreeIssue of cheque books (other than multicity cheques) FreeCar loan Pre approved car loans for promoters

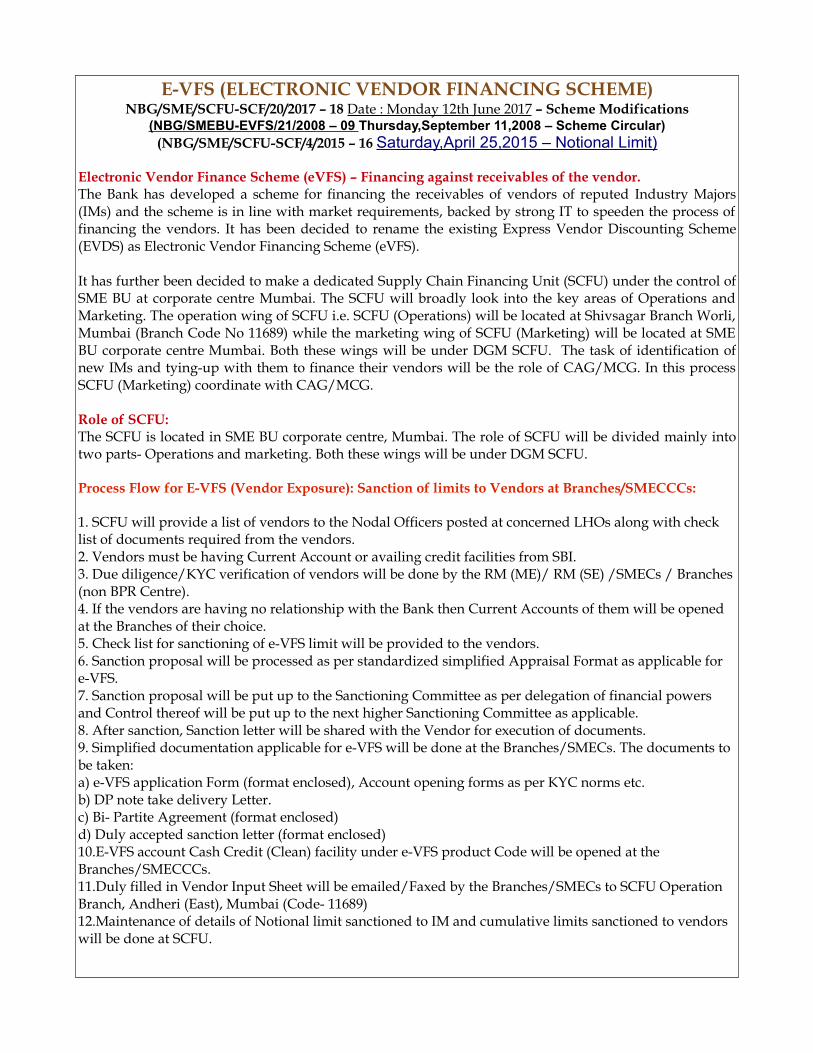

E-VFS (ELECTRONIC VENDOR FINANCING SCHEME)NBG/SME/SCFU-SCF/20/2017 – 18 Date : Monday 12th June 2017 – Scheme Modifications

(NBG/SMEBU-EVFS/21/2008 – 09 Thursday,September 11,2008 – Scheme Circular)(NBG/SME/SCFU-SCF/4/2015 – 16 Saturday,April 25,2015 – Notional Limit)

Electronic Vendor Finance Scheme (eVFS) – Financing against receivables of the vendor.The Bank has developed a scheme for financing the receivables of vendors of reputed Industry Majors (IMs) and the scheme is in line with market requirements, backed by strong IT to speeden the process of financing the vendors. It has been decided to rename the existing Express Vendor Discounting Scheme (EVDS) as Electronic Vendor Financing Scheme (eVFS).

It has further been decided to make a dedicated Supply Chain Financing Unit (SCFU) under the control of SME BU at corporate centre Mumbai. The SCFU will broadly look into the key areas of Operations and Marketing. The operation wing of SCFU i.e. SCFU (Operations) will be located at Shivsagar Branch Worli, Mumbai (Branch Code No 11689) while the marketing wing of SCFU (Marketing) will be located at SME BU corporate centre Mumbai. Both these wings will be under DGM SCFU. The task of identification of new IMs and tying-up with them to finance their vendors will be the role of CAG/MCG. In this process SCFU (Marketing) coordinate with CAG/MCG.

Role of SCFU:The SCFU is located in SME BU corporate centre, Mumbai. The role of SCFU will be divided mainly into two parts- Operations and marketing. Both these wings will be under DGM SCFU.

Process Flow for E-VFS (Vendor Exposure): Sanction of limits to Vendors at Branches/SMECCCs:

1. SCFU will provide a list of vendors to the Nodal Officers posted at concerned LHOs along with check list of documents required from the vendors.2. Vendors must be having Current Account or availing credit facilities from SBI.3. Due diligence/KYC verification of vendors will be done by the RM (ME)/ RM (SE) /SMECs / Branches (non BPR Centre).4. If the vendors are having no relationship with the Bank then Current Accounts of them will be opened at the Branches of their choice.5. Check list for sanctioning of e-VFS limit will be provided to the vendors.6. Sanction proposal will be processed as per standardized simplified Appraisal Format as applicable for e-VFS.7. Sanction proposal will be put up to the Sanctioning Committee as per delegation of financial powers and Control thereof will be put up to the next higher Sanctioning Committee as applicable.8. After sanction, Sanction letter will be shared with the Vendor for execution of documents.9. Simplified documentation applicable for e-VFS will be done at the Branches/SMECs. The documents to be taken:a) e-VFS application Form (format enclosed), Account opening forms as per KYC norms etc.b) DP note take delivery Letter.c) Bi- Partite Agreement (format enclosed)d) Duly accepted sanction letter (format enclosed)10.E-VFS account Cash Credit (Clean) facility under e-VFS product Code will be opened at the Branches/SMECCCs.11.Duly filled in Vendor Input Sheet will be emailed/Faxed by the Branches/SMECs to SCFU Operation Branch, Andheri (East), Mumbai (Code- 11689)12.Maintenance of details of Notional limit sanctioned to IM and cumulative limits sanctioned to vendors will be done at SCFU.

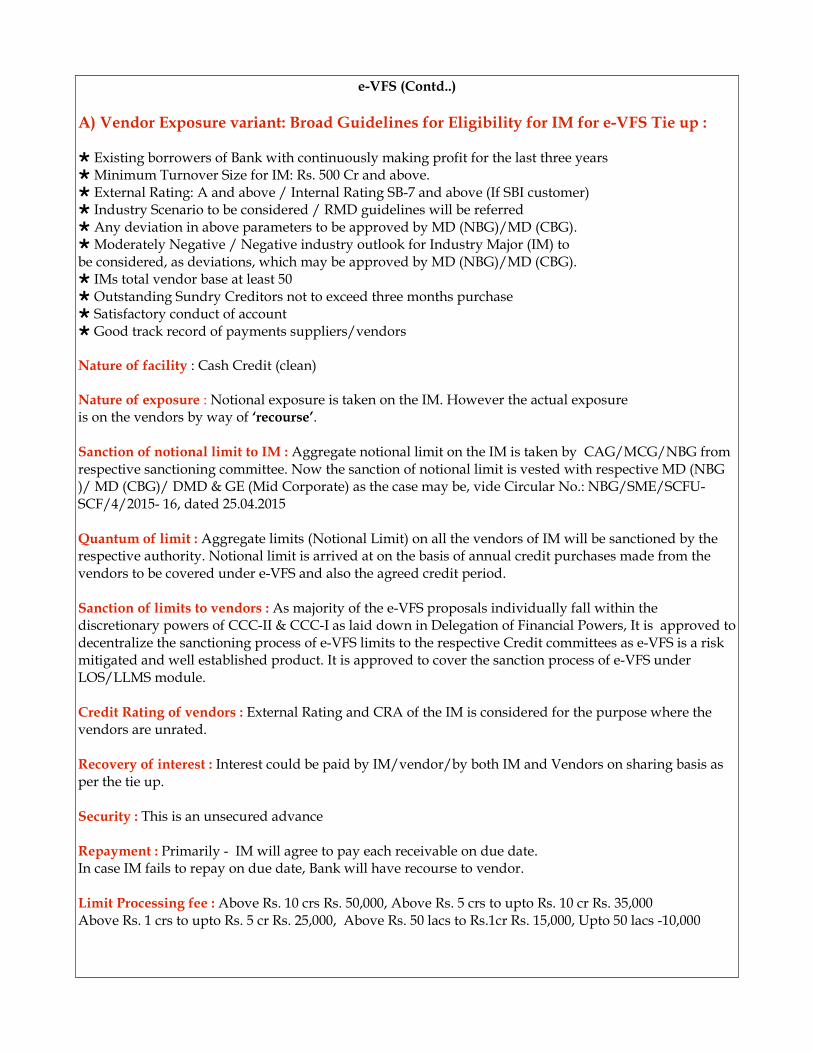

e-VFS (Contd..)

A) Vendor Exposure variant: Broad Guidelines for Eligibility for IM for e-VFS Tie up :

Existing borrowers of Bank with continuously making profit for the last three years Minimum Turnover Size for IM: Rs. 500 Cr and above. External Rating: A and above / Internal Rating SB-7 and above (If SBI customer) Industry Scenario to be considered / RMD guidelines will be referred Any deviation in above parameters to be approved by MD (NBG)/MD (CBG). Moderately Negative / Negative industry outlook for Industry Major (IM) to

be considered, as deviations, which may be approved by MD (NBG)/MD (CBG). IMs total vendor base at least 50 Outstanding Sundry Creditors not to exceed three months purchase Satisfactory conduct of account Good track record of payments suppliers/vendors

Nature of facility : Cash Credit (clean)

Nature of exposure : Notional exposure is taken on the IM. However the actual exposureis on the vendors by way of ‘recourse’.

Sanction of notional limit to IM : Aggregate notional limit on the IM is taken by CAG/MCG/NBG from respective sanctioning committee. Now the sanction of notional limit is vested with respective MD (NBG)/ MD (CBG)/ DMD & GE (Mid Corporate) as the case may be, vide Circular No.: NBG/SME/SCFU-SCF/4/2015- 16, dated 25.04.2015

Quantum of limit : Aggregate limits (Notional Limit) on all the vendors of IM will be sanctioned by the respective authority. Notional limit is arrived at on the basis of annual credit purchases made from the vendors to be covered under e-VFS and also the agreed credit period.

Sanction of limits to vendors : As majority of the e-VFS proposals individually fall within the discretionary powers of CCC-II & CCC-I as laid down in Delegation of Financial Powers, It is approved to decentralize the sanctioning process of e-VFS limits to the respective Credit committees as e-VFS is a risk mitigated and well established product. It is approved to cover the sanction process of e-VFS under LOS/LLMS module.

Credit Rating of vendors : External Rating and CRA of the IM is considered for the purpose where the vendors are unrated.

Recovery of interest : Interest could be paid by IM/vendor/by both IM and Vendors on sharing basis as per the tie up.

Security : This is an unsecured advance

Repayment : Primarily - IM will agree to pay each receivable on due date.In case IM fails to repay on due date, Bank will have recourse to vendor.

Limit Processing fee : Above Rs. 10 crs Rs. 50,000, Above Rs. 5 crs to upto Rs. 10 cr Rs. 35,000Above Rs. 1 crs to upto Rs. 5 cr Rs. 25,000, Above Rs. 50 lacs to Rs.1cr Rs. 15,000, Upto 50 lacs -10,000

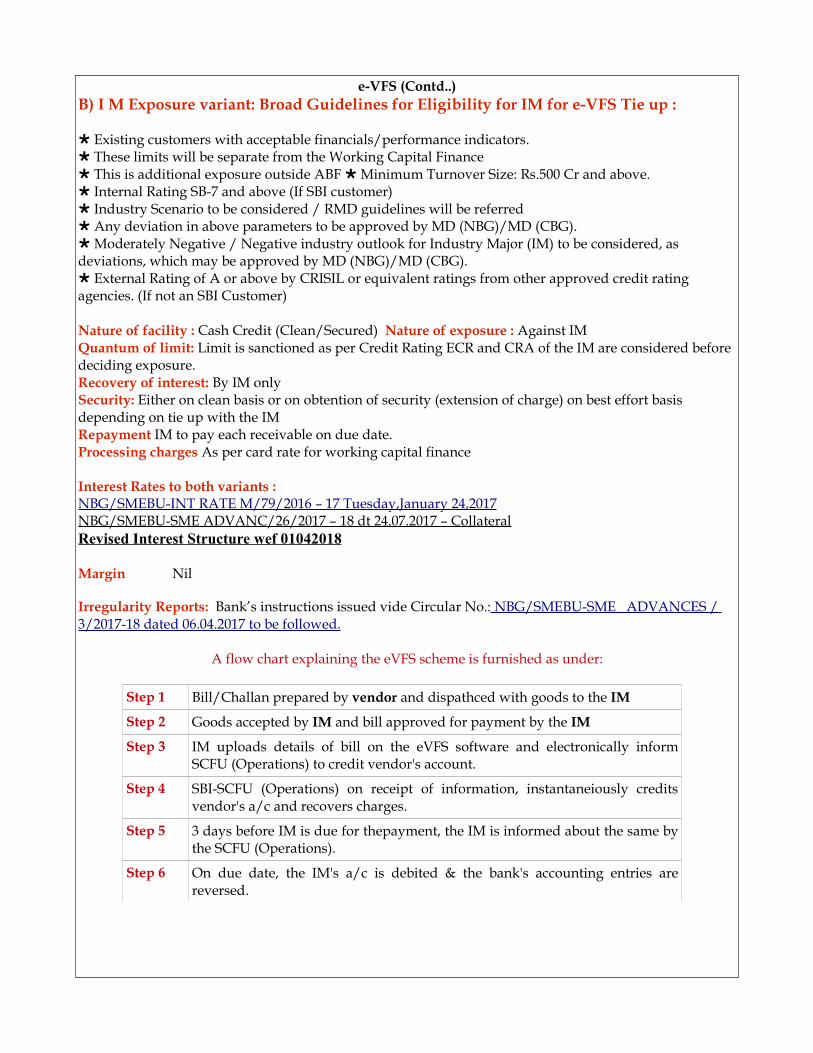

e-VFS (Contd..)B) I M Exposure variant: Broad Guidelines for Eligibility for IM for e-VFS Tie up :

Existing customers with acceptable financials/performance indicators. These limits will be separate from the Working Capital Finance This is additional exposure outside ABF Minimum Turnover Size: Rs.500 Cr and above. Internal Rating SB-7 and above (If SBI customer) Industry Scenario to be considered / RMD guidelines will be referred Any deviation in above parameters to be approved by MD (NBG)/MD (CBG). Moderately Negative / Negative industry outlook for Industry Major (IM) to be considered, as

deviations, which may be approved by MD (NBG)/MD (CBG). External Rating of A or above by CRISIL or equivalent ratings from other approved credit rating

agencies. (If not an SBI Customer)

Nature of facility : Cash Credit (Clean/Secured) Nature of exposure : Against IM Quantum of limit: Limit is sanctioned as per Credit Rating ECR and CRA of the IM are considered before deciding exposure.Recovery of interest: By IM only Security: Either on clean basis or on obtention of security (extension of charge) on best effort basis depending on tie up with the IMRepayment IM to pay each receivable on due date.Processing charges As per card rate for working capital finance

Interest Rates to both variants :NBG/SMEBU-INT RATE M/79/2016 – 17 Tuesday,January 24,2017NBG/SMEBU-SME ADVANC/26/2017 – 18 dt 24.07.2017 – CollateralRevised Interest Structure wef 01042018

Margin Nil

Irregularity Reports: Bank’s instructions issued vide Circular No.: NBG/SMEBU-SME ADVANCES / 3/2017-18 dated 06.04.2017 to be followed.

A flow chart explaining the eVFS scheme is furnished as under:

Step 1 Bill/Challan prepared by vendor and dispathced with goods to the IM

Step 2 Goods accepted by IM and bill approved for payment by the IM

Step 3 IM uploads details of bill on the eVFS software and electronically inform SCFU (Operations) to credit vendor's account.

Step 4 SBI-SCFU (Operations) on receipt of information, instantaneiously credits vendor's a/c and recovers charges.