E-ASSESSMENT & ASSESSMENT PROCEDURES By Dr. CA Abhishek Murali M.Com, FCA, ACMA, CGMA, CIMA(Lon.), LLB, CISA(USA), DISA(ICAI), D.Litt, ADIT (UK)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

E-ASSESSMENT & ASSESSMENT PROCEDURESBy Dr. CA Abhishek Murali

M.Com, FCA, ACMA, CGMA, CIMA(Lon.), LLB, CISA(USA), DISA(ICAI), D.Litt, ADIT (UK)

• Hon’ble FM announced during Budget in July 2019

• Increase transparency and reduce undesirable practices

• Faceless assessment with no Human Interface

• Part of Digital India Drive of the Government

Background of E-Assessment

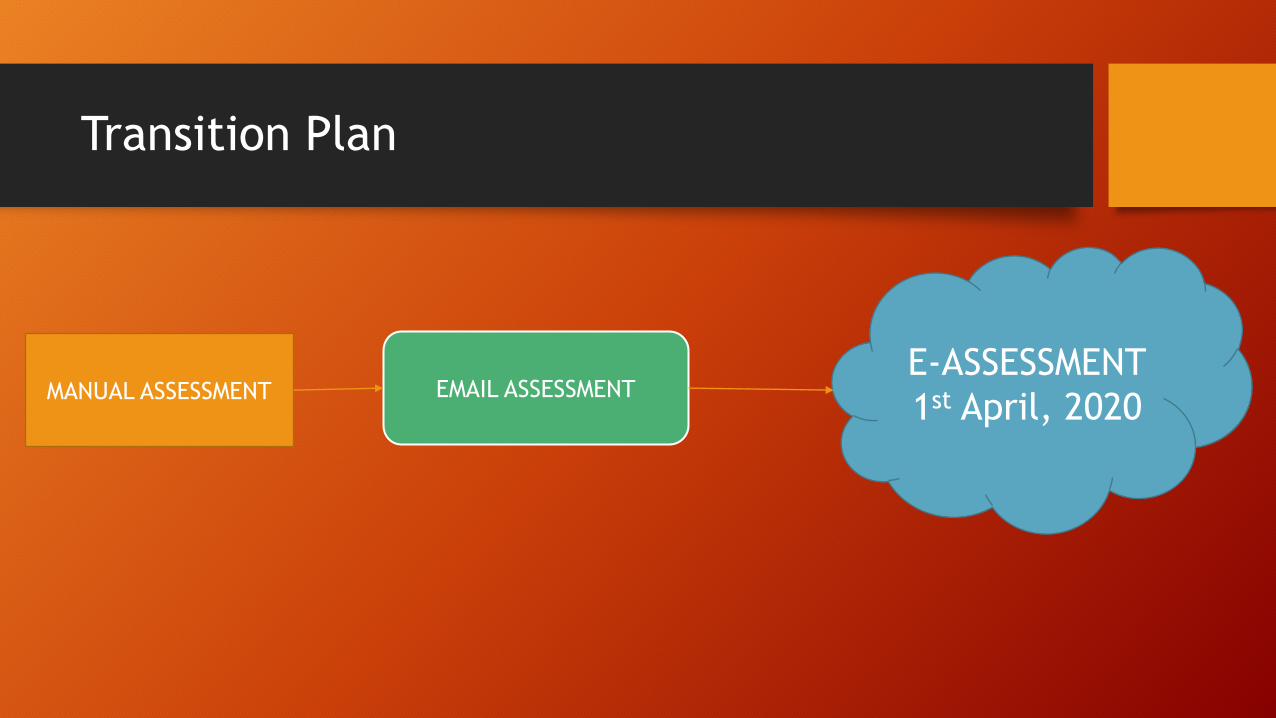

Transition Plan

MANUAL ASSESSMENT EMAIL ASSESSMENTE-ASSESSMENT

1st April, 2020

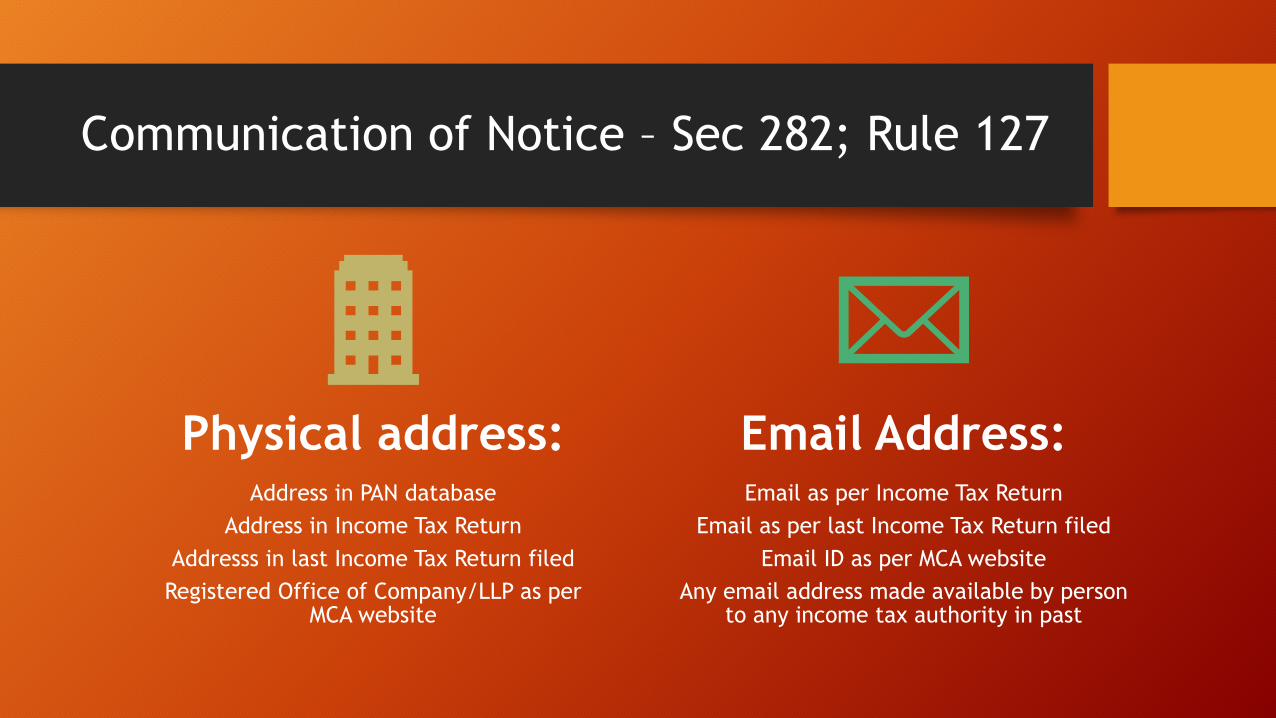

Communication of Notice

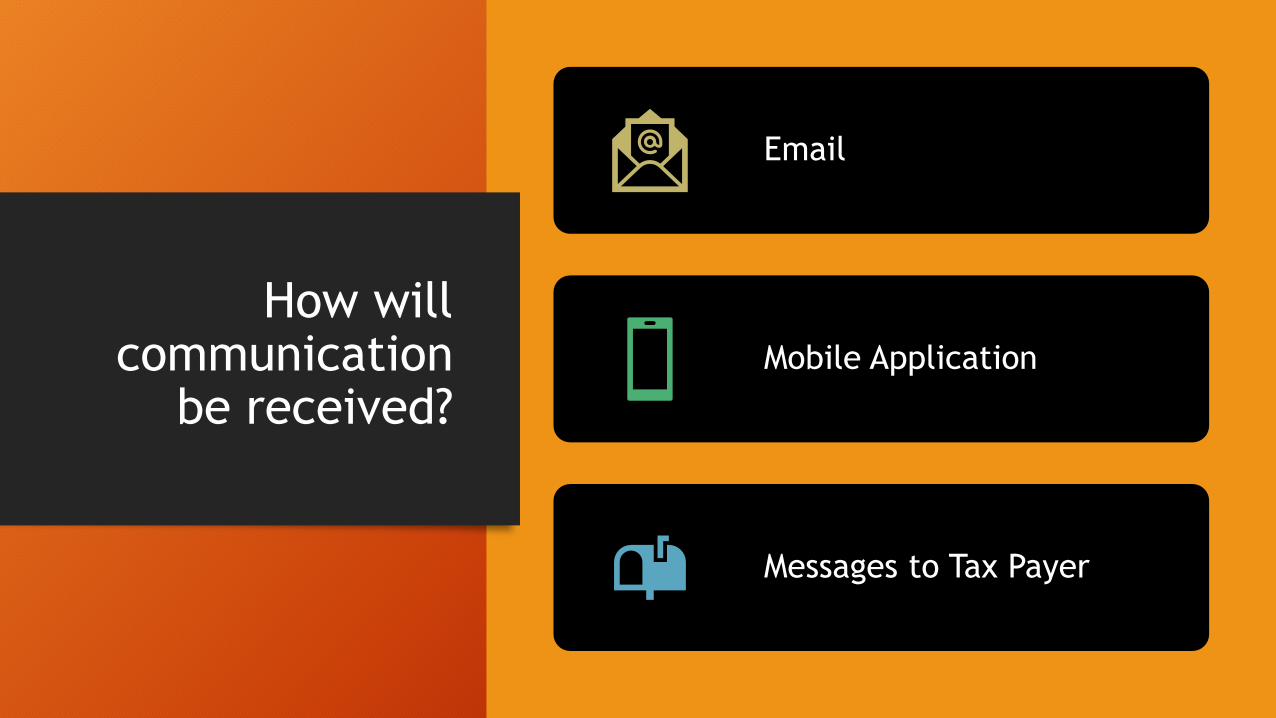

How will communication

be received?

Mobile Application

Messages to Tax Payer

Communication of Notice – Sec 282; Rule 127

Physical address:Address in PAN database

Address in Income Tax Return

Addresss in last Income Tax Return filed

Registered Office of Company/LLP as per MCA website

Email Address:Email as per Income Tax Return

Email as per last Income Tax Return filed

Email ID as per MCA website

Any email address made available by person to any income tax authority in past

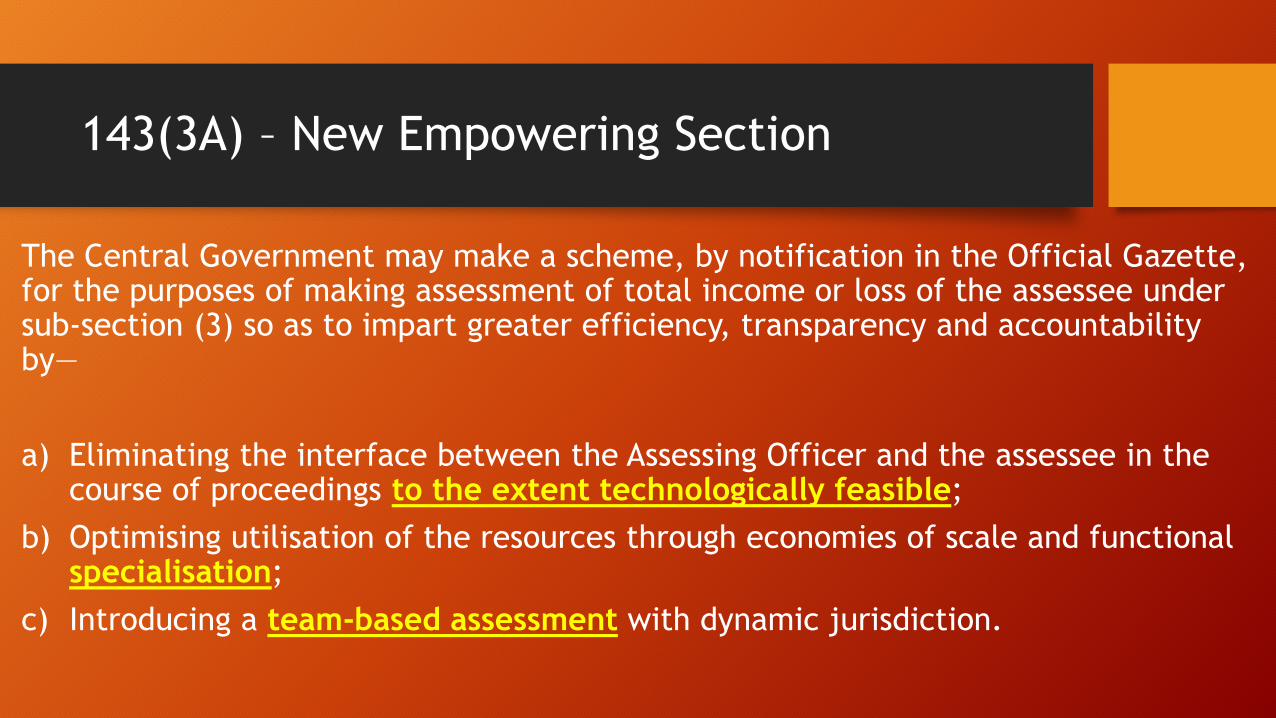

143(3A) – New Empowering Section

The Central Government may make a scheme, by notification in the Official Gazette, for the purposes of making assessment of total income or loss of the assessee under sub-section (3) so as to impart greater efficiency, transparency and accountability by—

a) Eliminating the interface between the Assessing Officer and the assessee in the course of proceedings to the extent technologically feasible;

b) Optimising utilisation of the resources through economies of scale and functional specialisation;

c) Introducing a team-based assessment with dynamic jurisdiction.

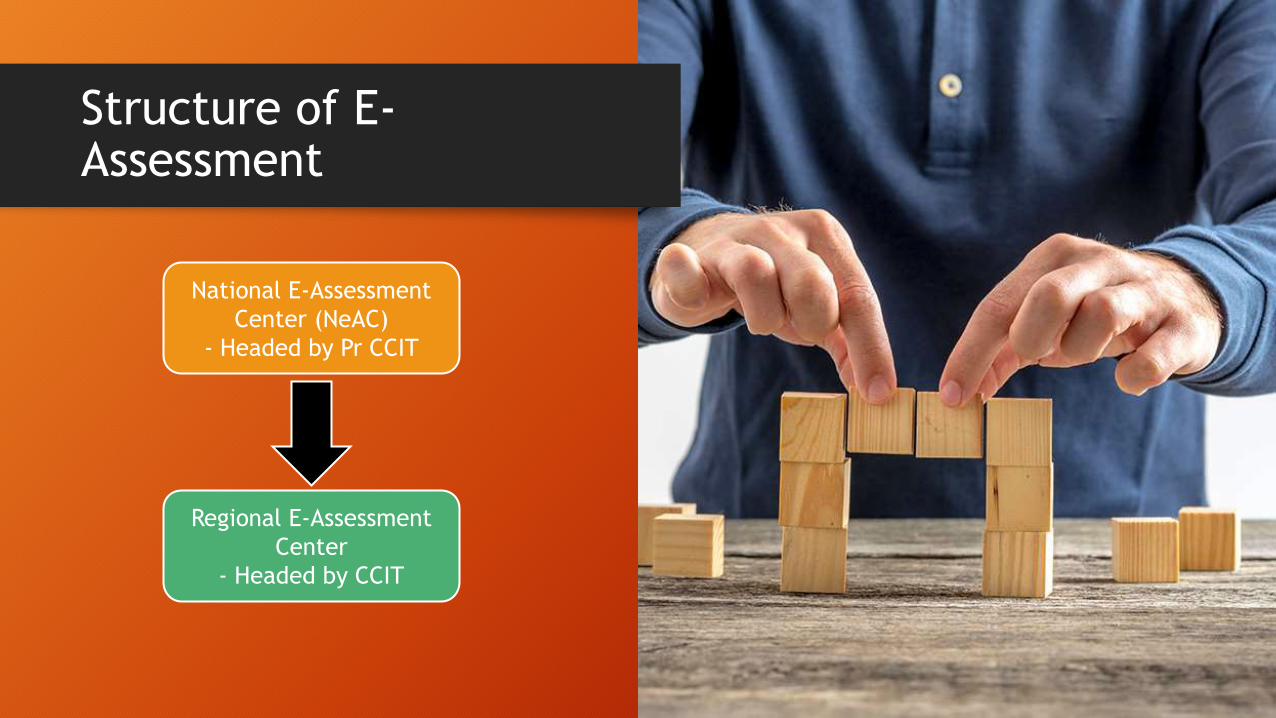

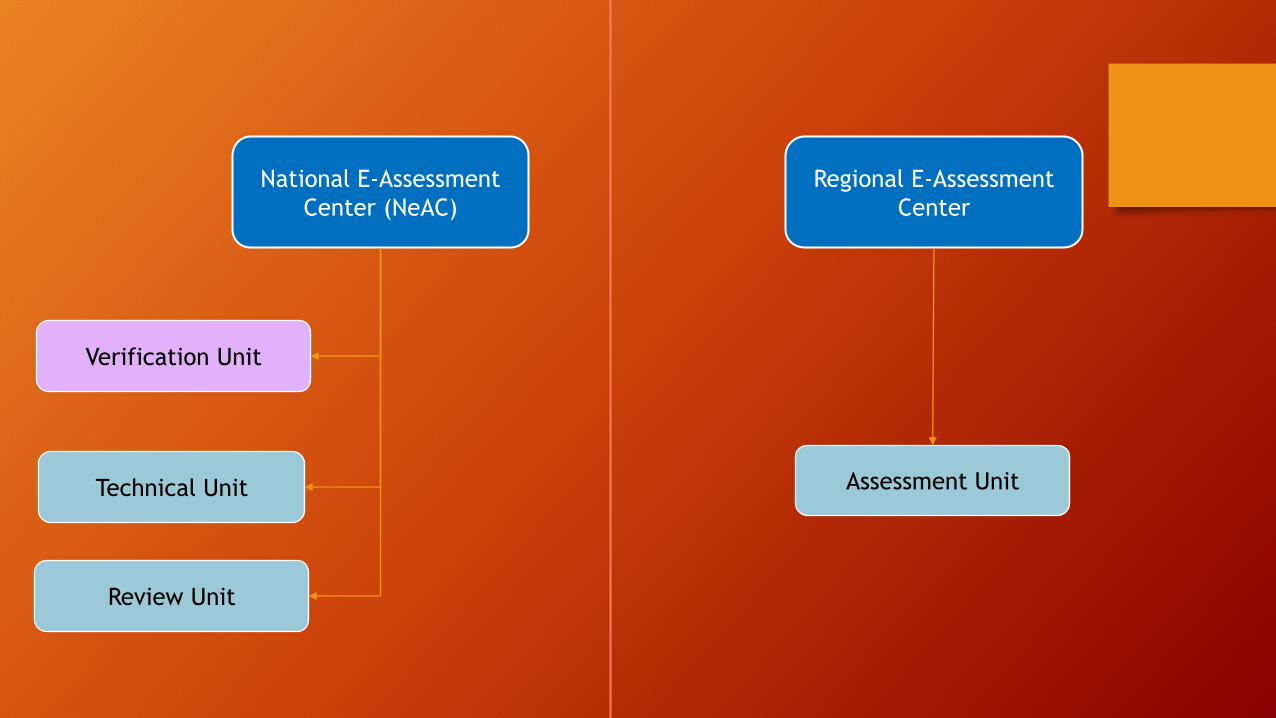

Structure of E-Assessment

National E-Assessment

Center (NeAC)

- Headed by Pr CCIT

Regional E-Assessment

Center

- Headed by CCIT

National E-Assessment

Center (NeAC)

Regional E-Assessment

Center

Review Unit

Assessment Unit

Verification Unit

Technical Unit

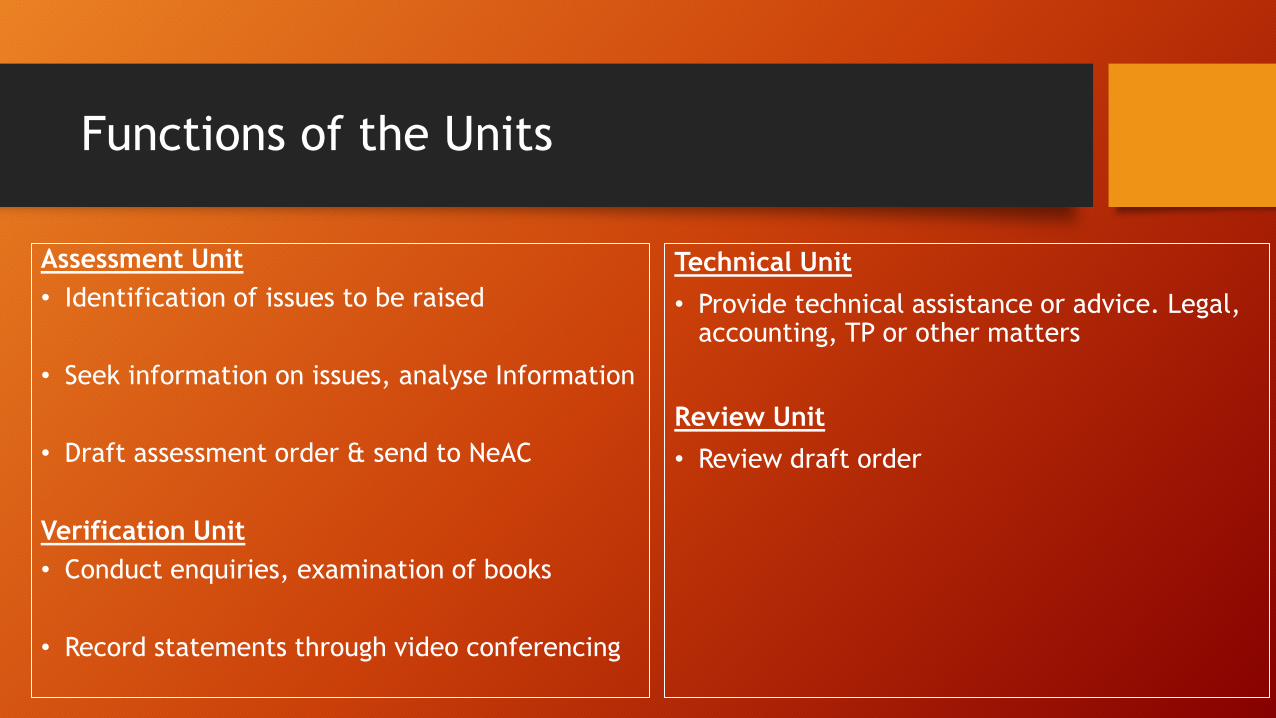

Assessment Unit

• Identification of issues to be raised

• Seek information on issues, analyse Information

• Draft assessment order & send to NeAC

Verification Unit

• Conduct enquiries, examination of books

• Record statements through video conferencing

Functions of the Units

Technical Unit

• Provide technical assistance or advice. Legal, accounting, TP or other matters

Review Unit

• Review draft order

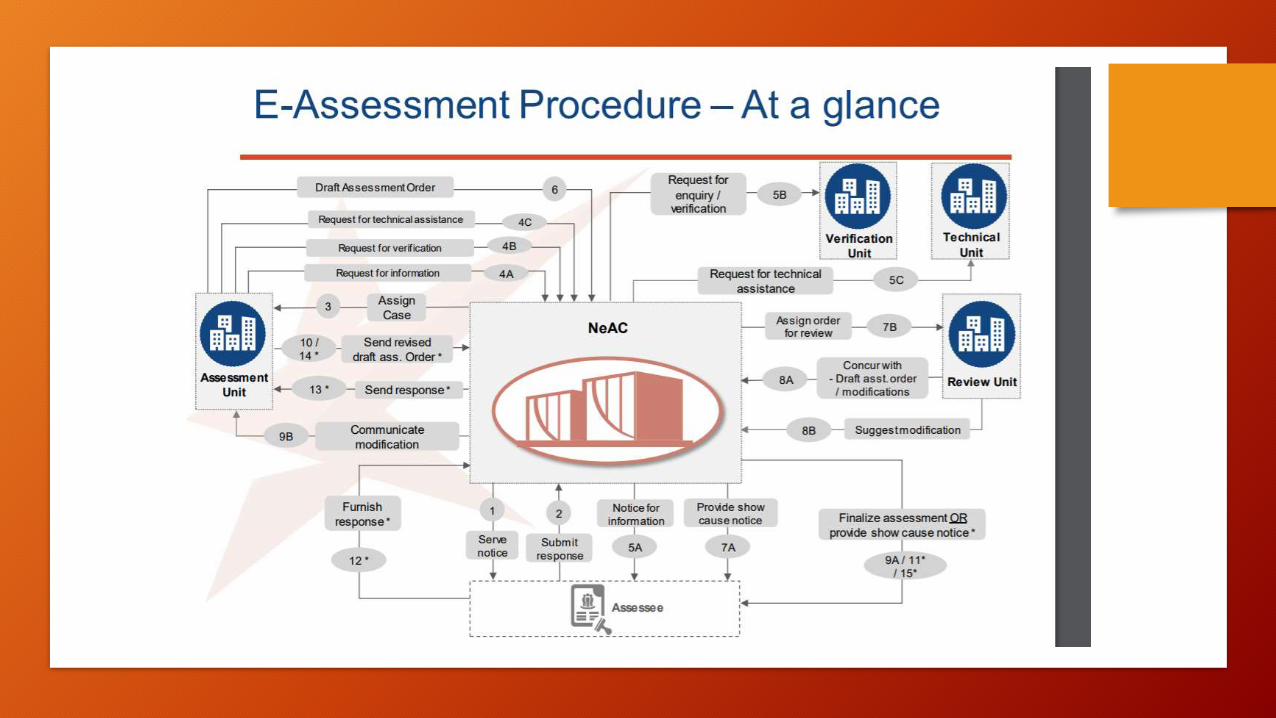

What’s the Procedure?

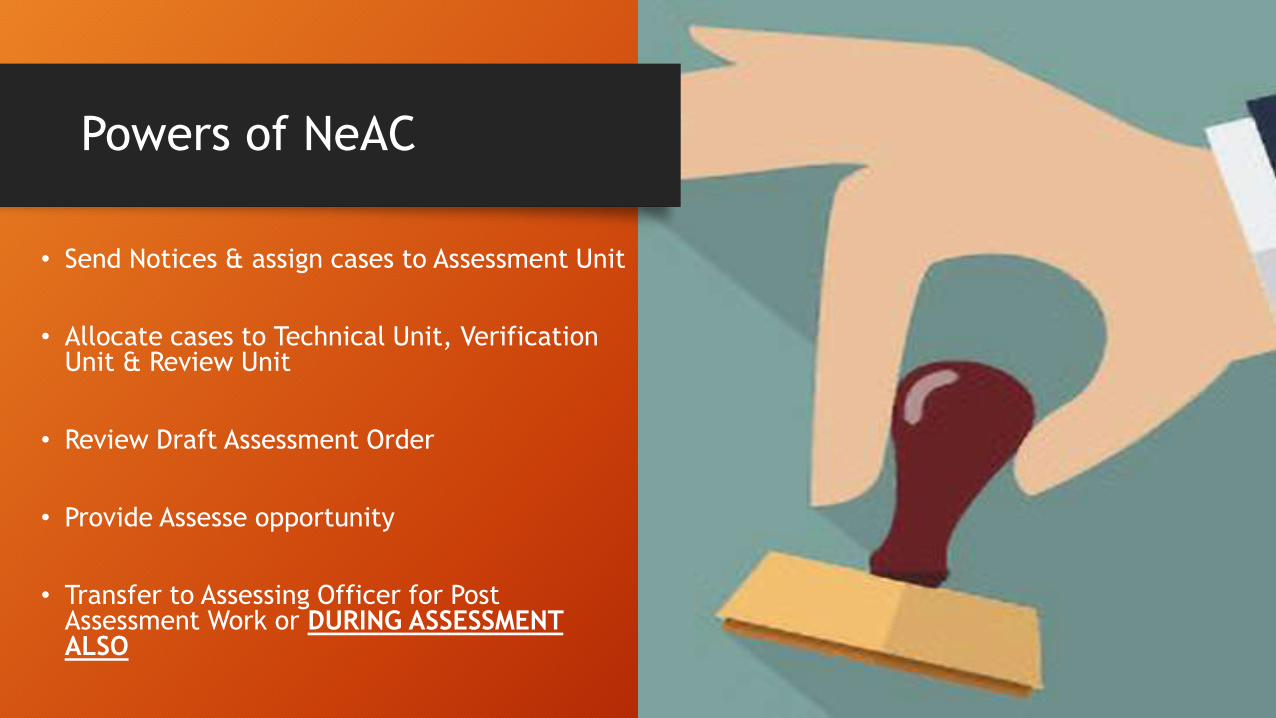

• Send Notices & assign cases to Assessment Unit

• Allocate cases to Technical Unit, Verification Unit & Review Unit

• Review Draft Assessment Order

• Provide Assesse opportunity

• Transfer to Assessing Officer for Post Assessment Work or DURING ASSESSMENT ALSO

Powers of NeAC

Personal Appearance Take Place in Following

• Where Books of Accounts has to be examined

• Where Sec 131 provisions are invoked (Summons)

• Examination/Cross-examination of witness is required

• Where Assessee requests specifically for Personal Hearing through online portal

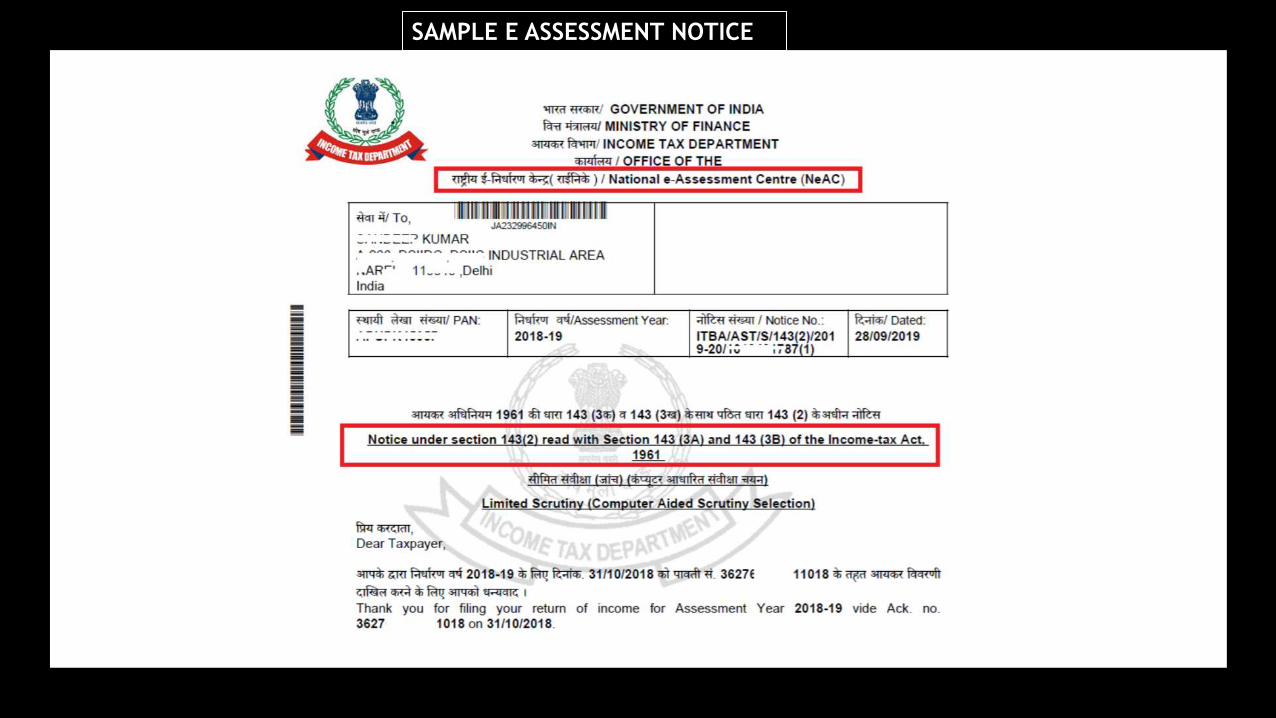

SAMPLE E ASSESSMENT NOTICE

• Collection, recovery of demand

• Rectification u/s 154

• Give effect to Appellate orders

• Proposal for launch of prosecution proceedings

What does Jurisdictional Officer now do?

Do I have Option to Opt out of Scheme?

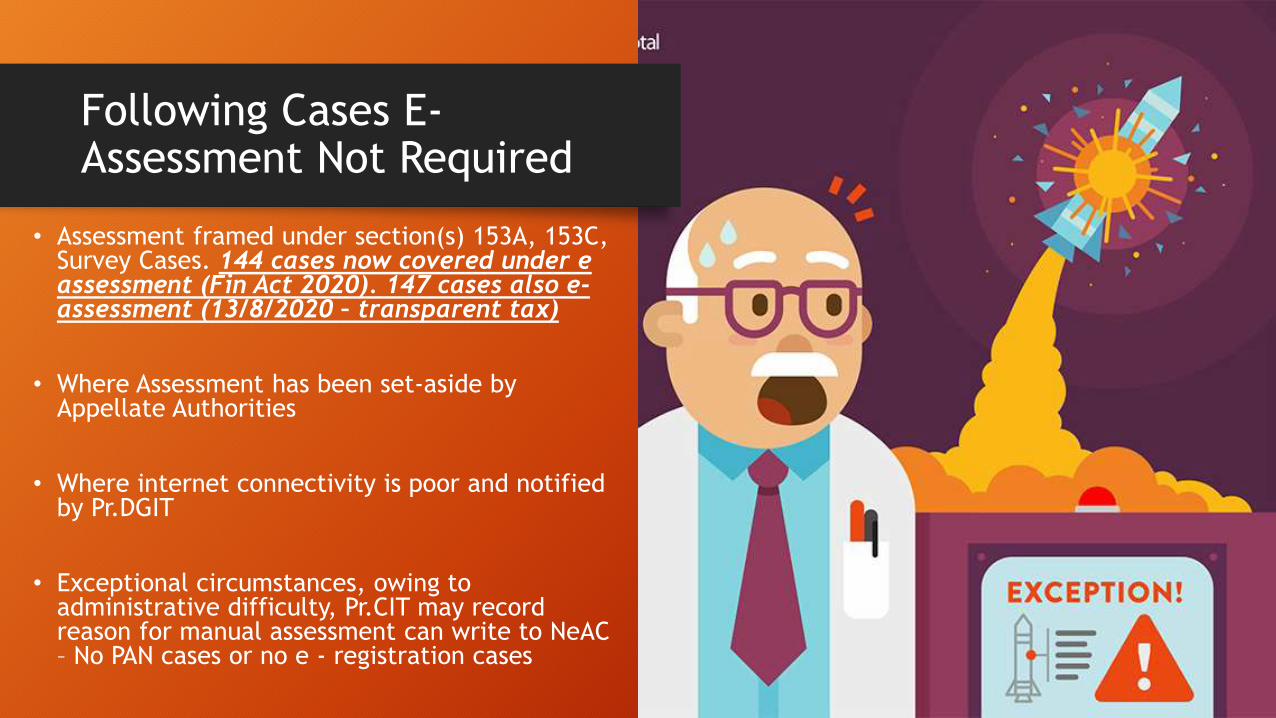

• Assessment framed under section(s) 153A, 153C, Survey Cases. 144 cases now covered under e assessment (Fin Act 2020). 147 cases also e-assessment (13/8/2020 – transparent tax)

• Where Assessment has been set-aside by Appellate Authorities

• Where internet connectivity is poor and notified by Pr.DGIT

• Exceptional circumstances, owing to administrative difficulty, Pr.CIT may record reason for manual assessment can write to NeAC– No PAN cases or no e - registration cases

Following Cases E-Assessment Not Required

What should we do?

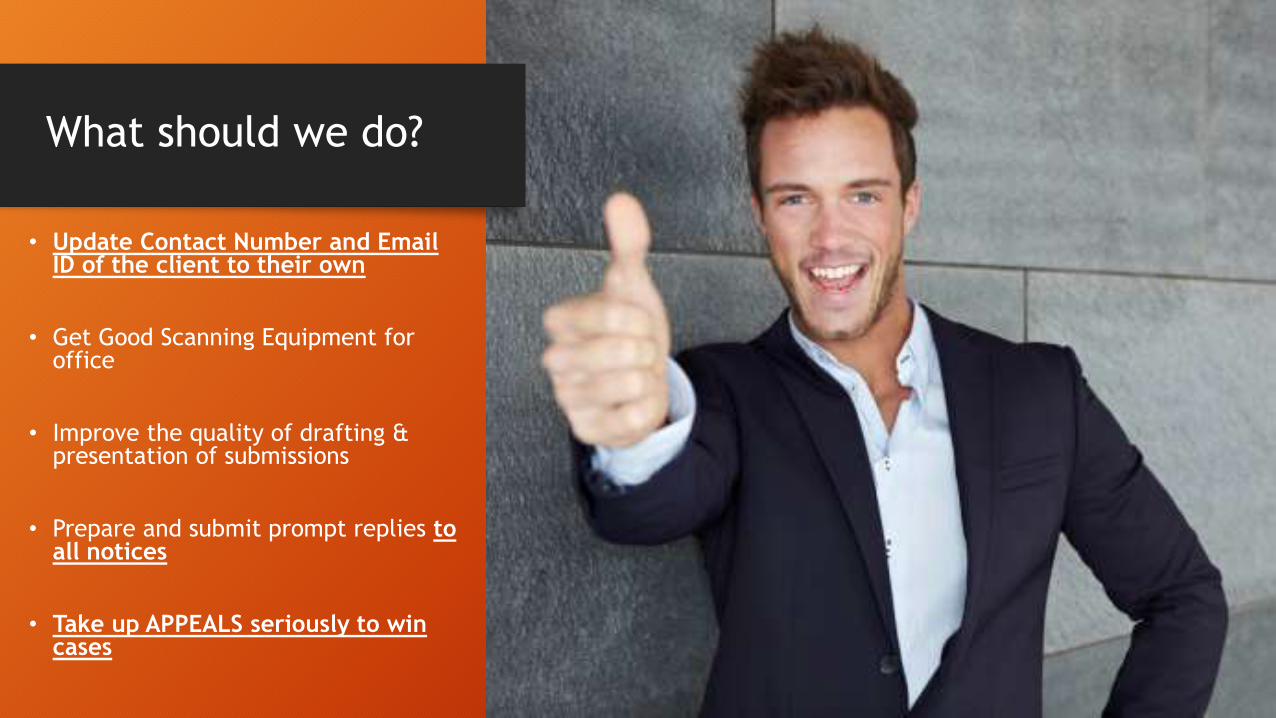

• Update Contact Number and Email ID of the client to their own

• Get Good Scanning Equipment for office

• Improve the quality of drafting & presentation of submissions

• Prepare and submit prompt replies to all notices

• Take up APPEALS seriously to win cases

Assessment Procedures

Intimation u/s 143(1)

Case Example – How should you proceed?

• Order u/s 143(1) passed disallowing bad debts claimed by the Assessee

• How should the Assessee proceed? Is this right or wrong?

• Bajaj Auto Finance vs CIT (Bombay High Court) – Disallowance cannot be made by intimation under section 143(1)(a) of the Act, as it requires that a party be given an opportunity to establish its claim before disallowing it

Intimation u/s 143(1)

• Intimation to make adjustments for arithmetical error/claim & prima-facie adjustments

• No intimation can be sent after the expiry of one year from the end of the FY in which return is made

• Intimation is not an Assessment Order

Regular/ Scrutiny

Assessment

Basic Conditions

• AO based on return is of the view to ensure Assessee has not • Understated Income

• Computed Excessive Loss

• Has not under-paid tax

• Service of notice u/s 143(2) is compulsory

• Notice must be served on Assessee before 6 months from end of FY in which return is filed. Eg: If return filed on 10/07/2016. Service of notice cannot be beyond 30/09/2017.

• Can 143(2) be issued when return has not been filed u/s 139. However, for 142(1), no return filing required.

• Where notice was served on the assesseeon 1st October, when notice issued on 30th

September. Held not served in time – CIT v Inderpal Malhotra (2008) 171 Taxman 359

• Compliance with time mandatory not merely procedural – CIT vs GitsonsEngineering 370 ITR 87 (Mad)

Key Points

Limited Scrutiny and Full Scrutiny

Inquiry before

Assessment u/s 142(1)

Inquiry before Assessment – Sec 142 (1)

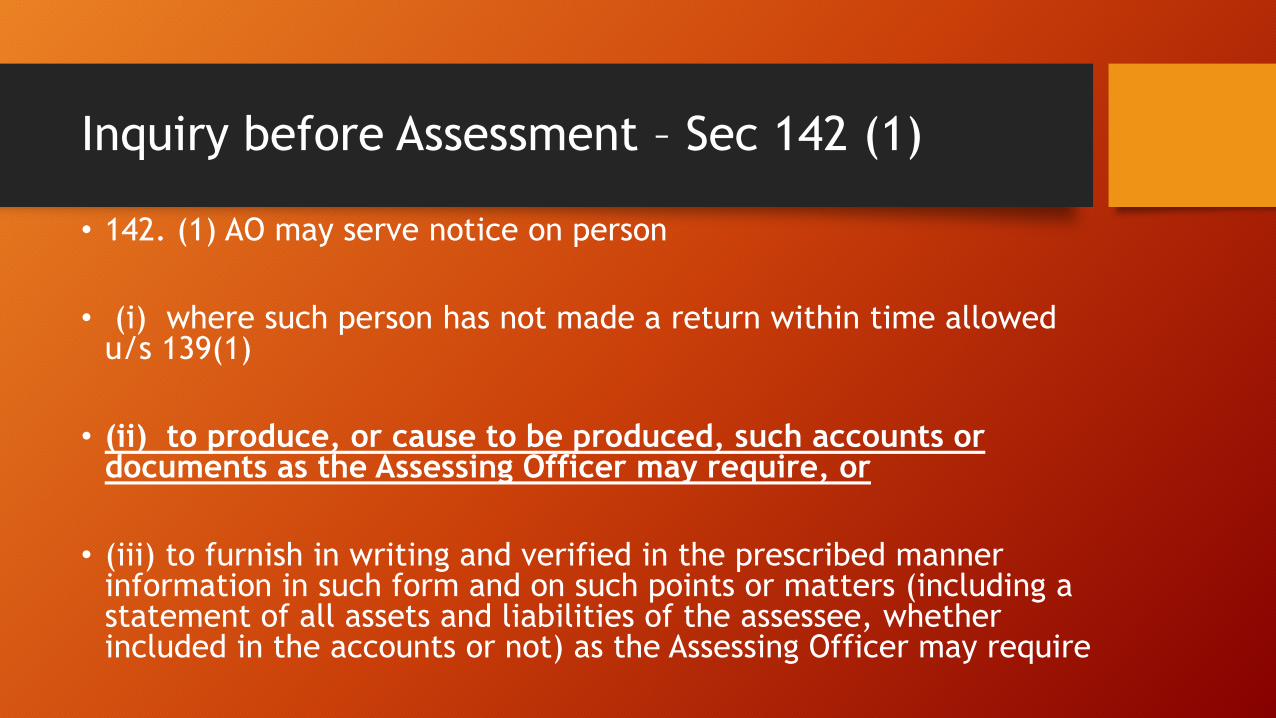

• 142. (1) AO may serve notice on person

• (i) where such person has not made a return within time allowed u/s 139(1)

• (ii) to produce, or cause to be produced, such accounts or documents as the Assessing Officer may require, or

• (iii) to furnish in writing and verified in the prescribed manner information in such form and on such points or matters (including a statement of all assets and liabilities of the assessee, whether included in the accounts or not) as the Assessing Officer may require

Inquiry before Assessment – Sec 142 (1)

• If AO asks for books of accounts for last 6 years. Does Assessee have to give it? – Calcutta Chromotype vs ITO (95 ITR 595) held that AO cannot summon books of account beyond 3 prior years

• It is not mandatory to serve 142(1) on Assessee before Sec. 144 assessment, when Assesse has not filed return of income before assessment

• U/s 142(2), AO is empowered to collect information from sources other than the Assessee

Best Judgement Assessment

u/s 144

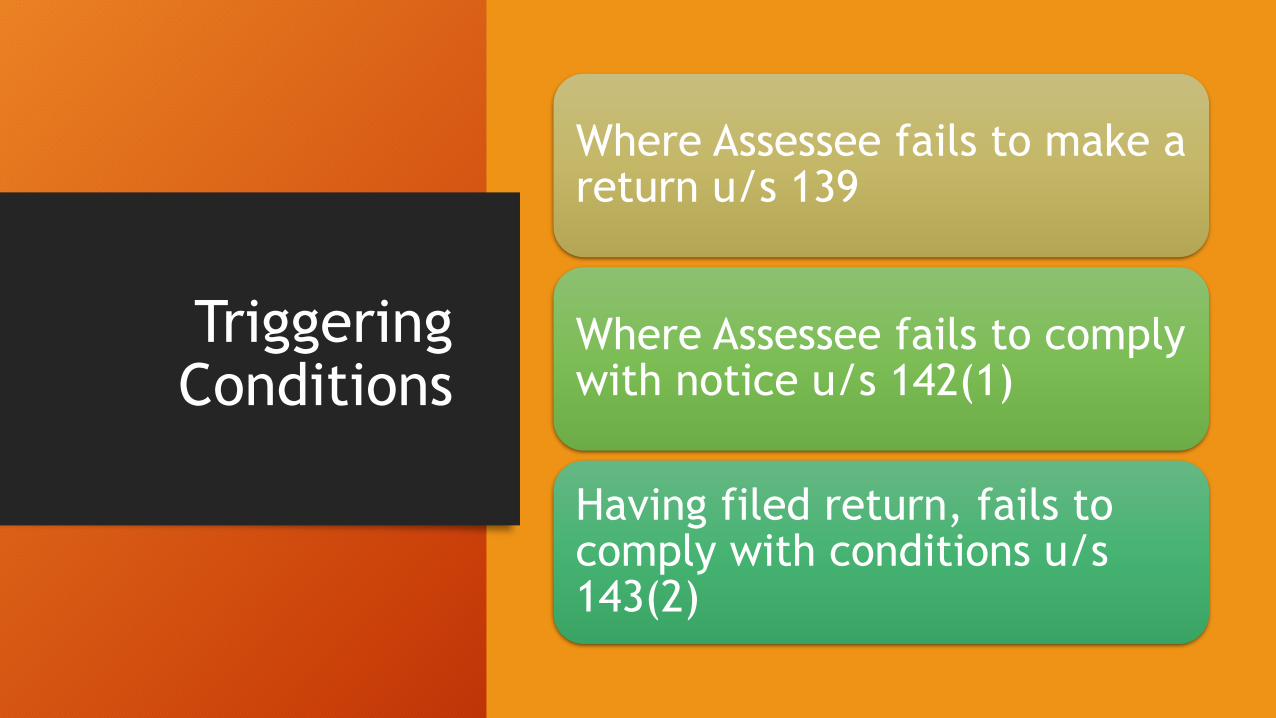

Triggering Conditions

Where Assessee fails to make a return u/s 139

Where Assessee fails to comply with notice u/s 142(1)

Having filed return, fails to comply with conditions u/s 143(2)

Key Points

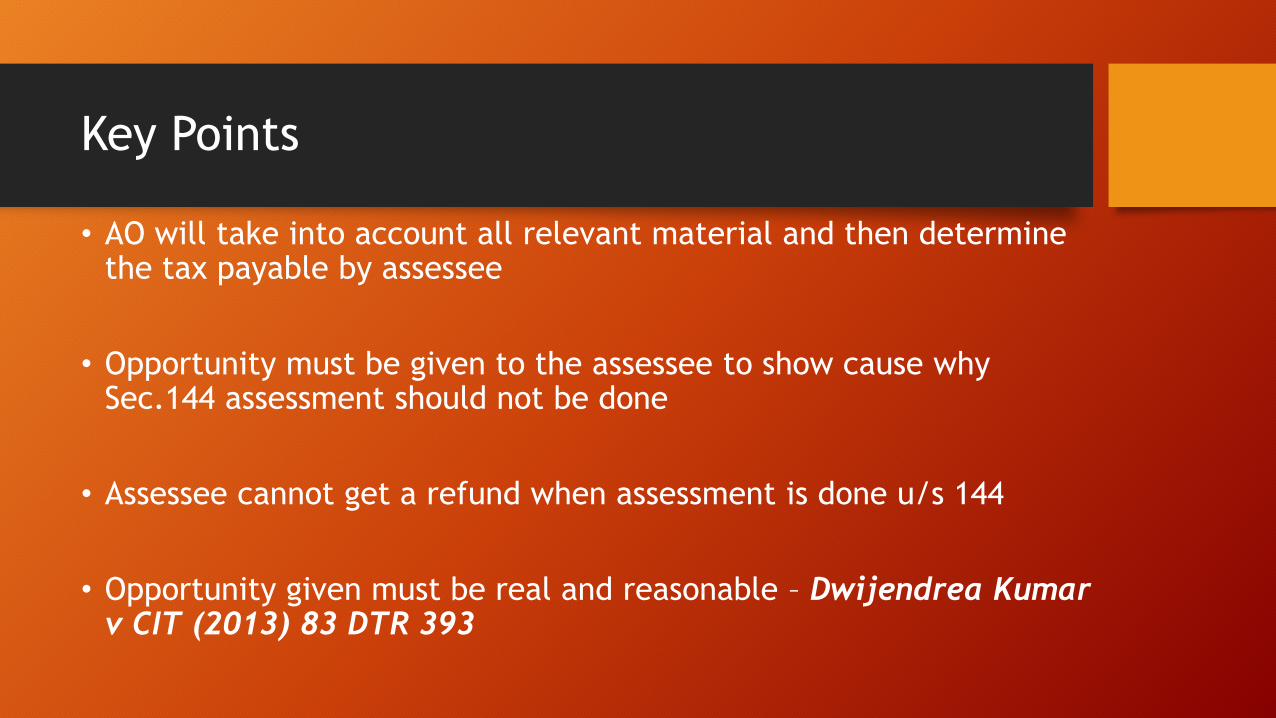

• AO will take into account all relevant material and then determine the tax payable by assessee

• Opportunity must be given to the assessee to show cause why Sec.144 assessment should not be done

• Assessee cannot get a refund when assessment is done u/s 144

• Opportunity given must be real and reasonable – Dwijendrea Kumar v CIT (2013) 83 DTR 393

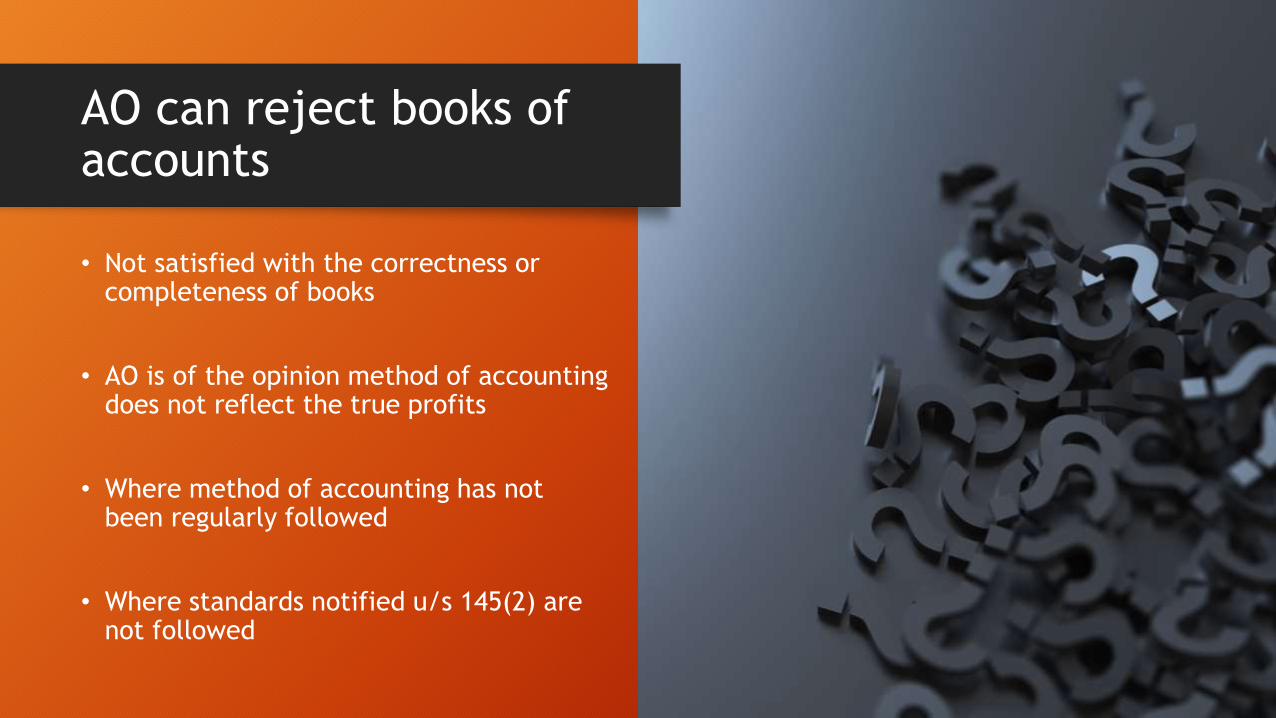

• Not satisfied with the correctness or completeness of books

• AO is of the opinion method of accounting does not reflect the true profits

• Where method of accounting has not been regularly followed

• Where standards notified u/s 145(2) are not followed

AO can reject books of accounts

Income Escaping Assessment u/s 147

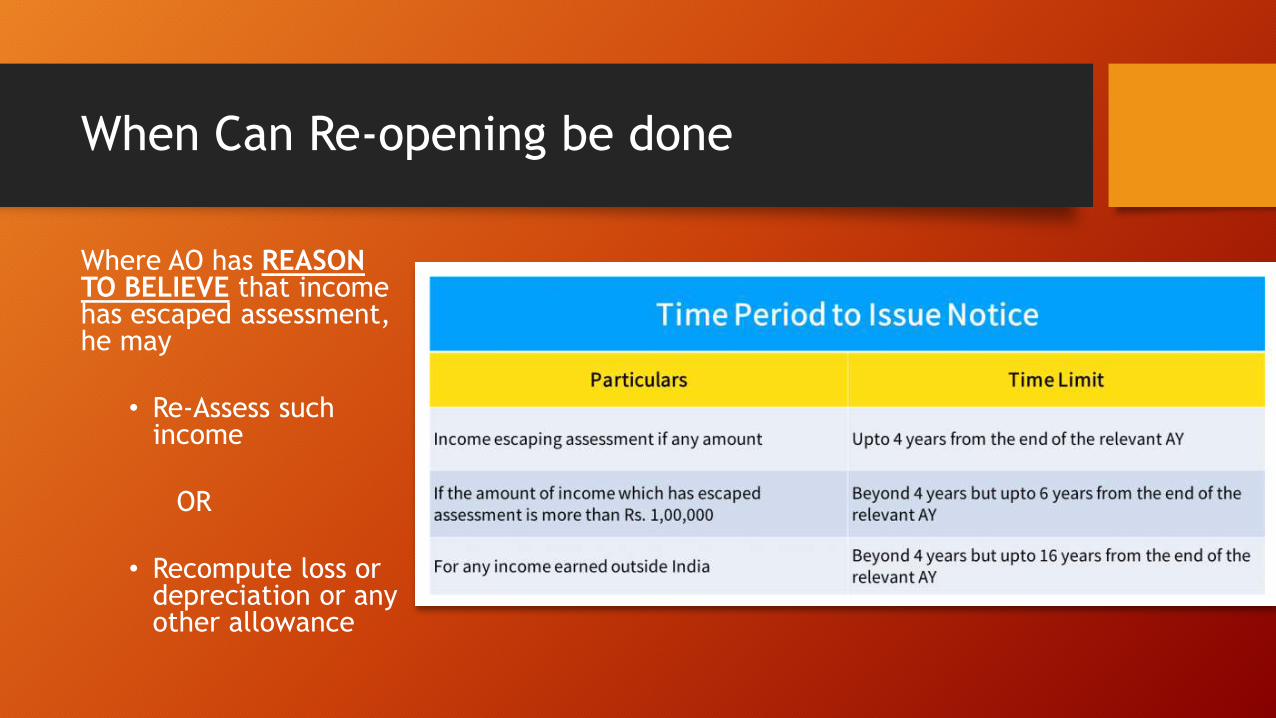

When Can Re-opening be done

Where AO has REASON TO BELIEVE that income has escaped assessment, he may

• Re-Assess such income

OR

• Recompute loss or depreciation or any other allowance

Question

• AO Hears a Rumour that Assessee has lot of income from property sales that he has not disclosed. Can he re-open assessment based on the same? – Jayesh Govindbhai vs ITO (71 tmn 221)

• Belief must be that what an honest and reasonable person would believe

• Supreme Court has held that action must be based on circumstantial or direct evidence. It cannot be on mere suspicion or rumour

Key Points - 1

• Can AO cover other points which have escaped assessment, even though re-opening is for some other purpose? - Yes

• Where reason to believe has not sustained, then other items which were not part of reasons cannot be added, even if it has escaped tax – Ganga Saran & Sons vs ITO (130 ITR 1)(SC)

• Time limit is for issue of notice and not for service. Postman told to deliver at one address, watchman asks postman to deliver at a different address, it is presumed to be a valid service – Mayawati vs CIT (2014) 363 ITR 349

Key Points - 2

• Can same AY be re-opened multiple times? – Kakkar Glass & Crockery House vs CIT (2002) 254 ITR 273 (P&H) said yes.

• Notice issued after death of Assessee & sent to legal heir after period of limitation was held not to be valid – Vipin Walia vs ITO 382 ITR 19 (2016)

• During regular assessment AO sought for complete details of shareholders, PAN no., confirmation letters which was given. Subsequently AY re-opened doubting credit worthiness of Investors. Is it valid? – Allied Strips vs ACIT (2016)(69 taxman 444) said No. This would be mere change of opinion

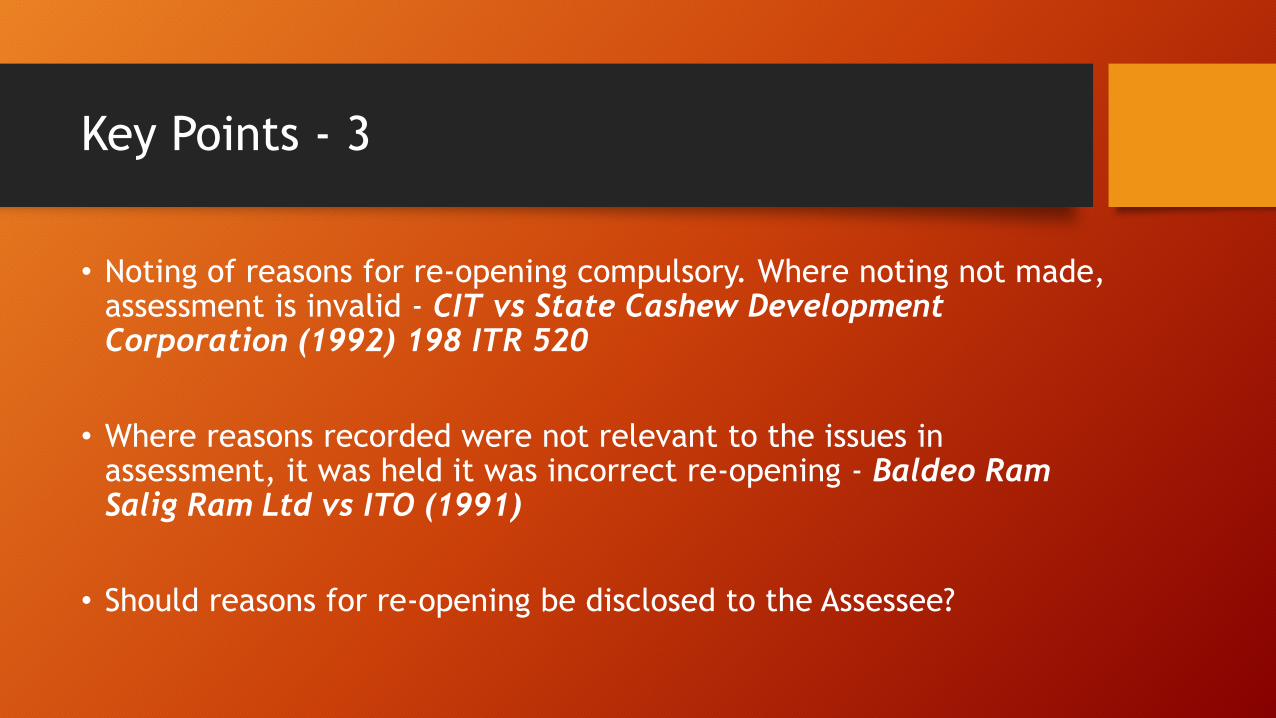

Key Points - 3

• Noting of reasons for re-opening compulsory. Where noting not made, assessment is invalid - CIT vs State Cashew Development Corporation (1992) 198 ITR 520

• Where reasons recorded were not relevant to the issues in assessment, it was held it was incorrect re-opening - Baldeo Ram Salig Ram Ltd vs ITO (1991)

• Should reasons for re-opening be disclosed to the Assessee?

Procedure to Handle Re-

Opening

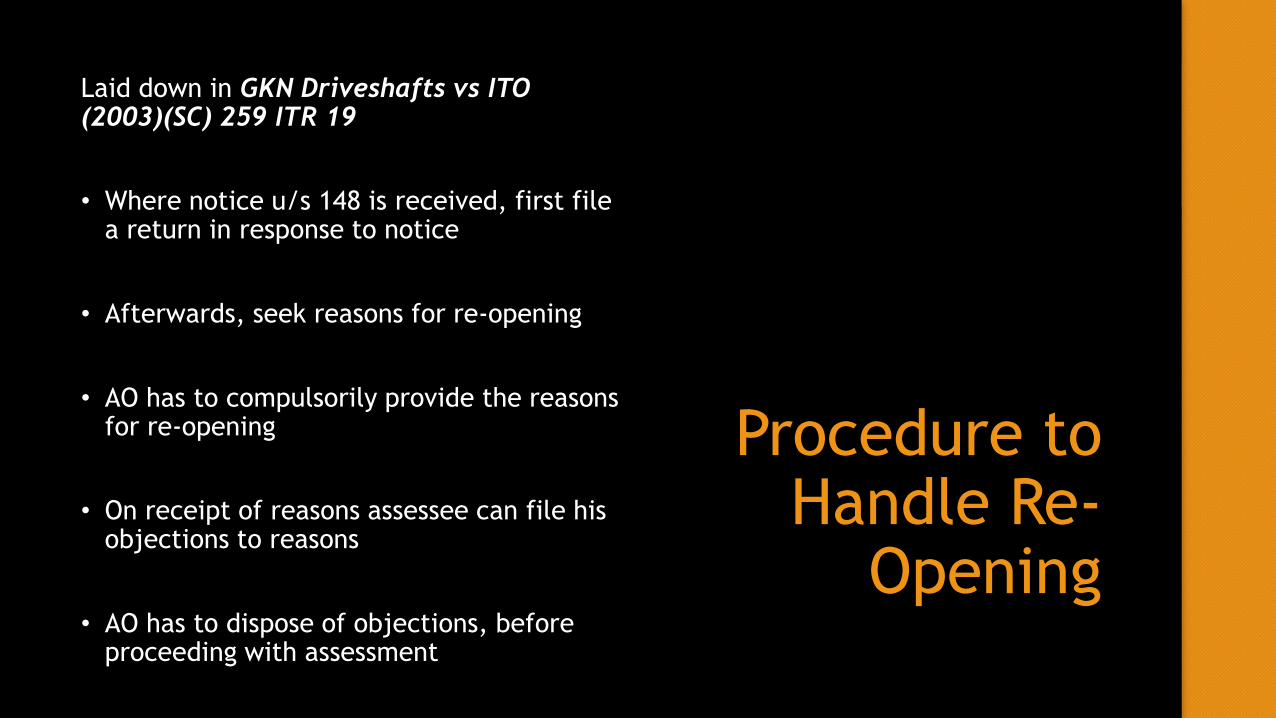

Laid down in GKN Driveshafts vs ITO (2003)(SC) 259 ITR 19

• Where notice u/s 148 is received, first file a return in response to notice

• Afterwards, seek reasons for re-opening

• AO has to compulsorily provide the reasons for re-opening

• On receipt of reasons assessee can file his objections to reasons

• AO has to dispose of objections, before proceeding with assessment

Key Points - 4

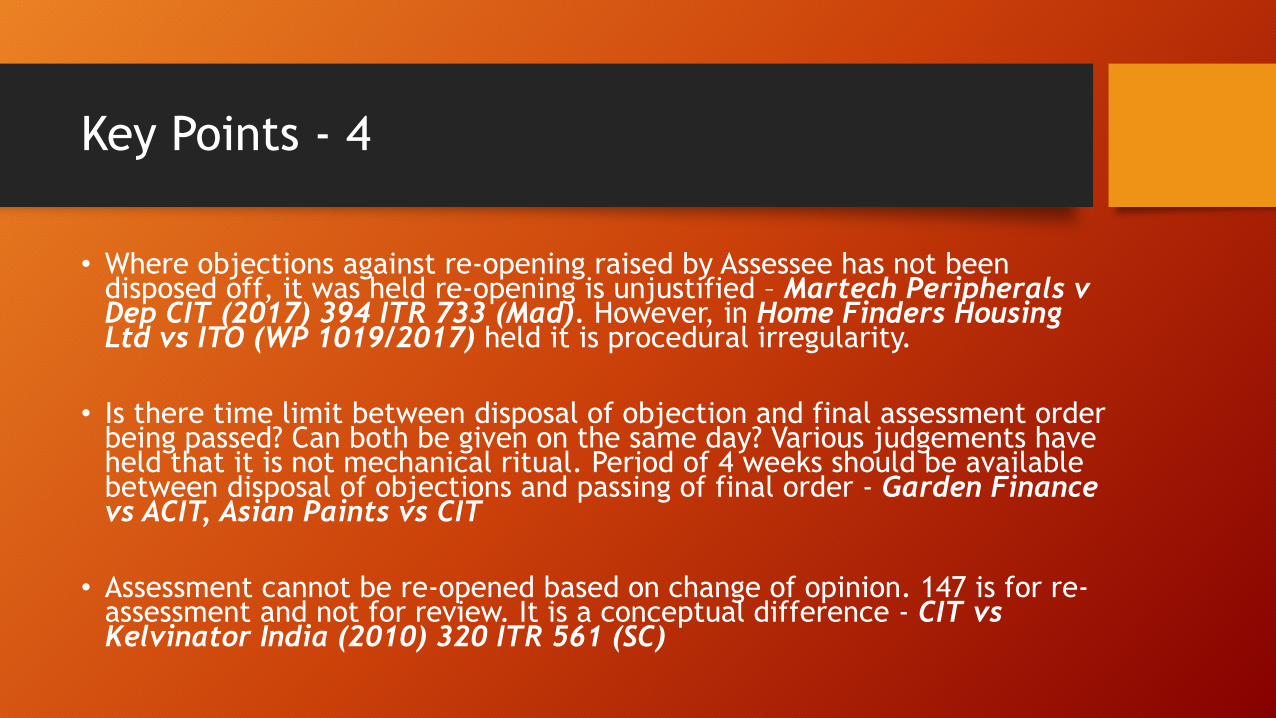

• Where objections against re-opening raised by Assessee has not been disposed off, it was held re-opening is unjustified – Martech Peripherals v Dep CIT (2017) 394 ITR 733 (Mad). However, in Home Finders Housing Ltd vs ITO (WP 1019/2017) held it is procedural irregularity.

• Is there time limit between disposal of objection and final assessment order being passed? Can both be given on the same day? Various judgements have held that it is not mechanical ritual. Period of 4 weeks should be available between disposal of objections and passing of final order - Garden Finance vs ACIT, Asian Paints vs CIT

• Assessment cannot be re-opened based on change of opinion. 147 is for re-assessment and not for review. It is a conceptual difference - CIT vs Kelvinator India (2010) 320 ITR 561 (SC)

Key Points - 5

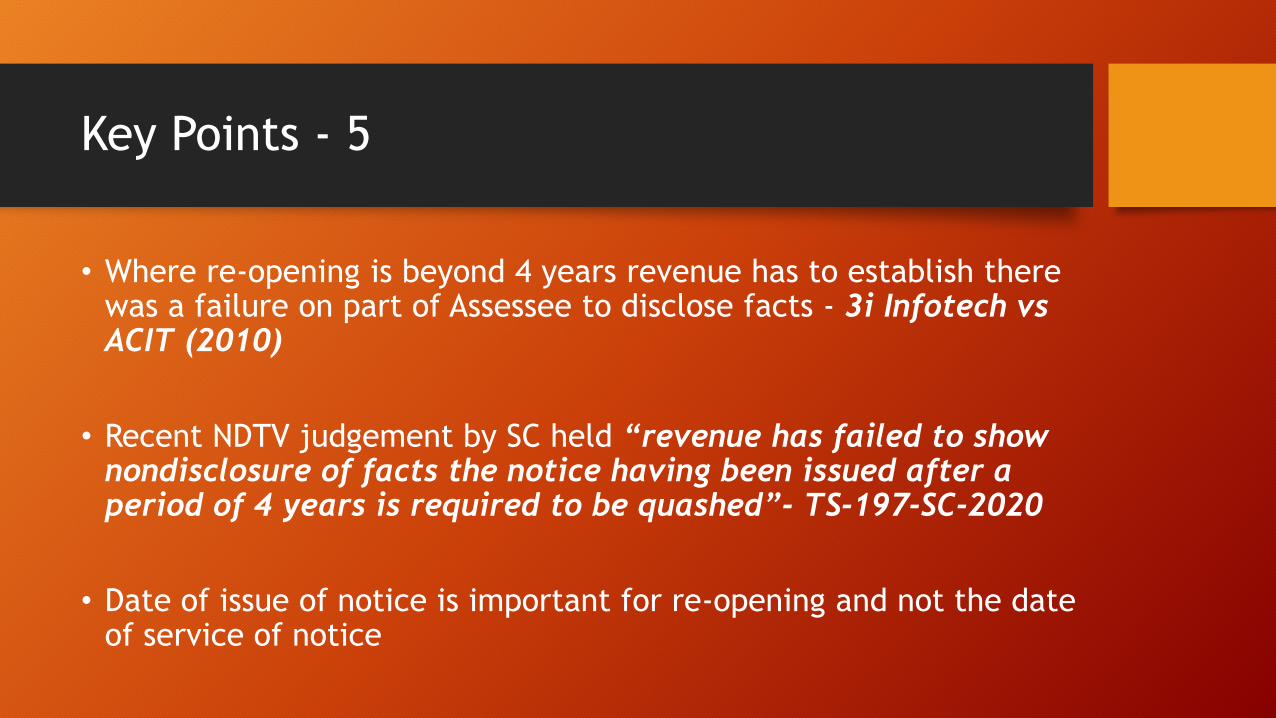

• Where re-opening is beyond 4 years revenue has to establish there was a failure on part of Assessee to disclose facts - 3i Infotech vs ACIT (2010)

• Recent NDTV judgement by SC held “revenue has failed to show nondisclosure of facts the notice having been issued after a period of 4 years is required to be quashed”- TS-197-SC-2020

• Date of issue of notice is important for re-opening and not the date of service of notice

Key Points - 6

• Calcutta Discount Co. Ltd vs ITO (1961)41 ITR 1961 (SC), the Apex Court held that twin conditions for re-opening is essential – i) income escaping assessment AND ii) omission or failure on the part of the assessee to disclose truly and fully all material facts.

Rectification u/s 154

Overview of Section 154

• To rectify an error that is committed by AO

• Application can be made by both AO or Assessee

• Mistake must be apparent on record

• Must be done 4 years from end of FY in which Assessment Order is passed

Key Points - 1

• Mistake must be patent and apparent on record – ITO vs Volkart Bros (1971) 82 ITR 40

• If the error goes to the root of the ground and entire order falls flat, it should still be allowed if apparent - Blue Star Engineering vs CIT 1969 73 ITR 283

• Assessment order passed without considering jurisdictional HC order. Is this error apparent on record – CIT vs Subodhchandra (2004) 138 Taxman 185 (Guj)

Revision of Income Tax Return

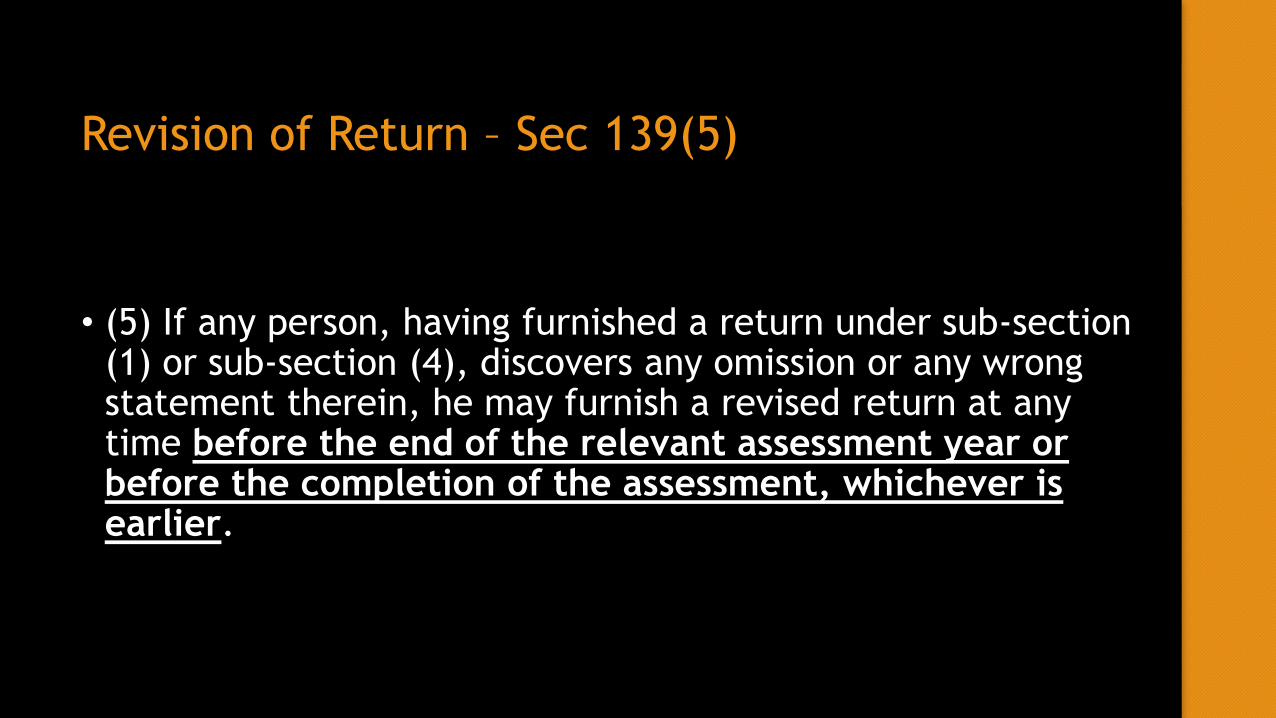

Revision of Return – Sec 139(5)

• (5) If any person, having furnished a return under sub-section (1) or sub-section (4), discovers any omission or any wrong statement therein, he may furnish a revised return at any time before the end of the relevant assessment year or before the completion of the assessment, whichever is earlier.

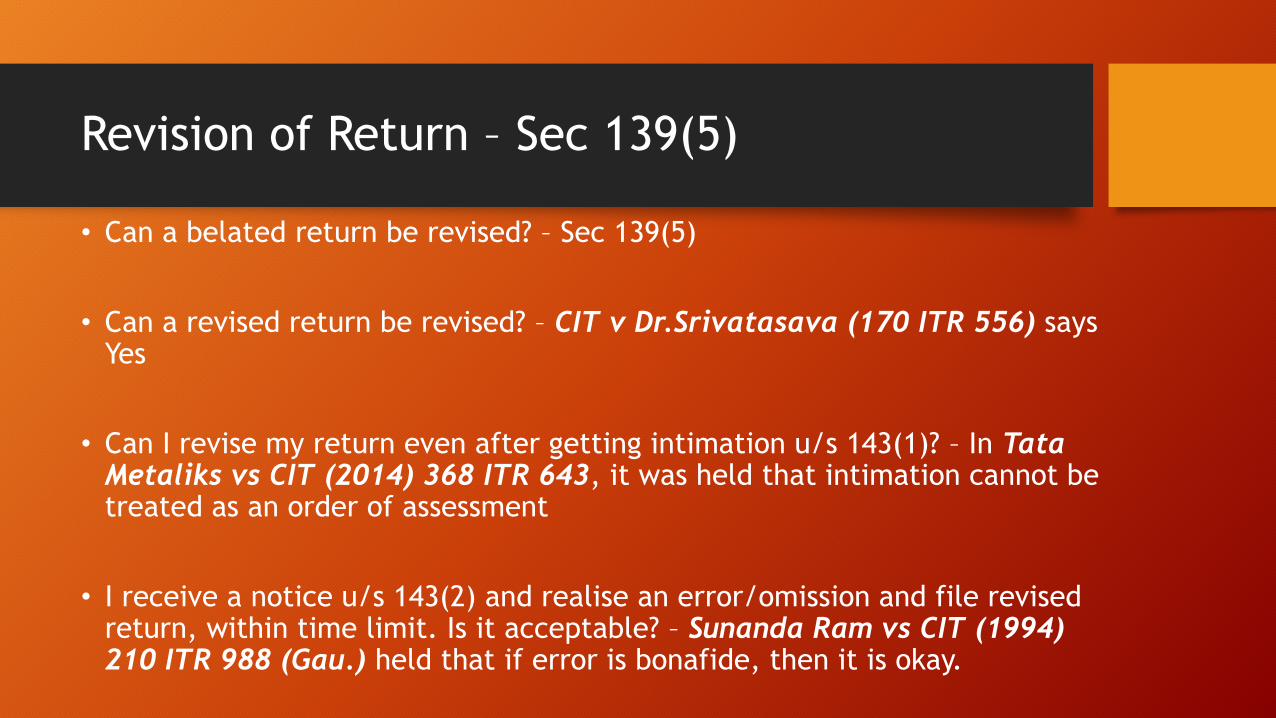

Revision of Return – Sec 139(5)

• Can a belated return be revised? – Sec 139(5)

• Can a revised return be revised? – CIT v Dr.Srivatasava (170 ITR 556) says Yes

• Can I revise my return even after getting intimation u/s 143(1)? – In Tata Metaliks vs CIT (2014) 368 ITR 643, it was held that intimation cannot be treated as an order of assessment

• I receive a notice u/s 143(2) and realise an error/omission and file revised return, within time limit. Is it acceptable? – Sunanda Ram vs CIT (1994) 210 ITR 988 (Gau.) held that if error is bonafide, then it is okay.

SOME INTERESTING DECISIONS

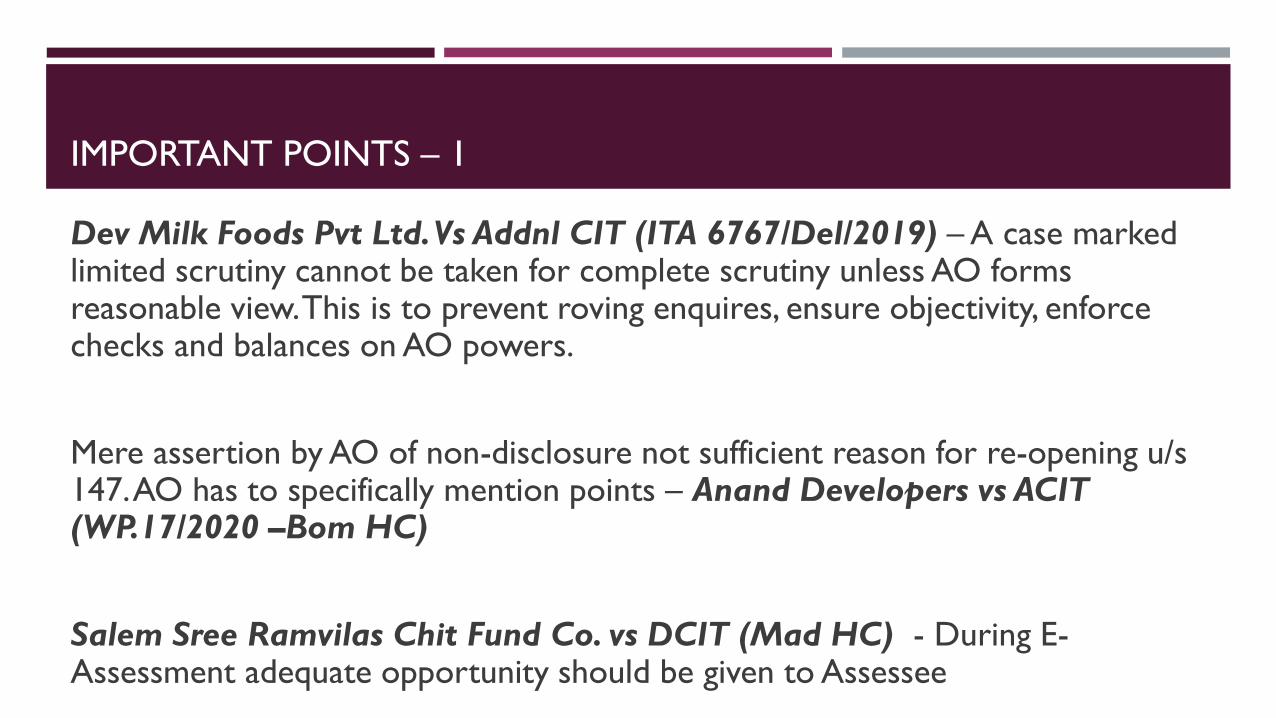

IMPORTANT POINTS – 1

Dev Milk Foods Pvt Ltd. Vs Addnl CIT (ITA 6767/Del/2019) – A case marked limited scrutiny cannot be taken for complete scrutiny unless AO forms reasonable view. This is to prevent roving enquires, ensure objectivity, enforce checks and balances on AO powers.

Mere assertion by AO of non-disclosure not sufficient reason for re-opening u/s 147. AO has to specifically mention points – Anand Developers vs ACIT (WP.17/2020 –Bom HC)

Salem Sree Ramvilas Chit Fund Co. vs DCIT (Mad HC) - During E-Assessment adequate opportunity should be given to Assessee

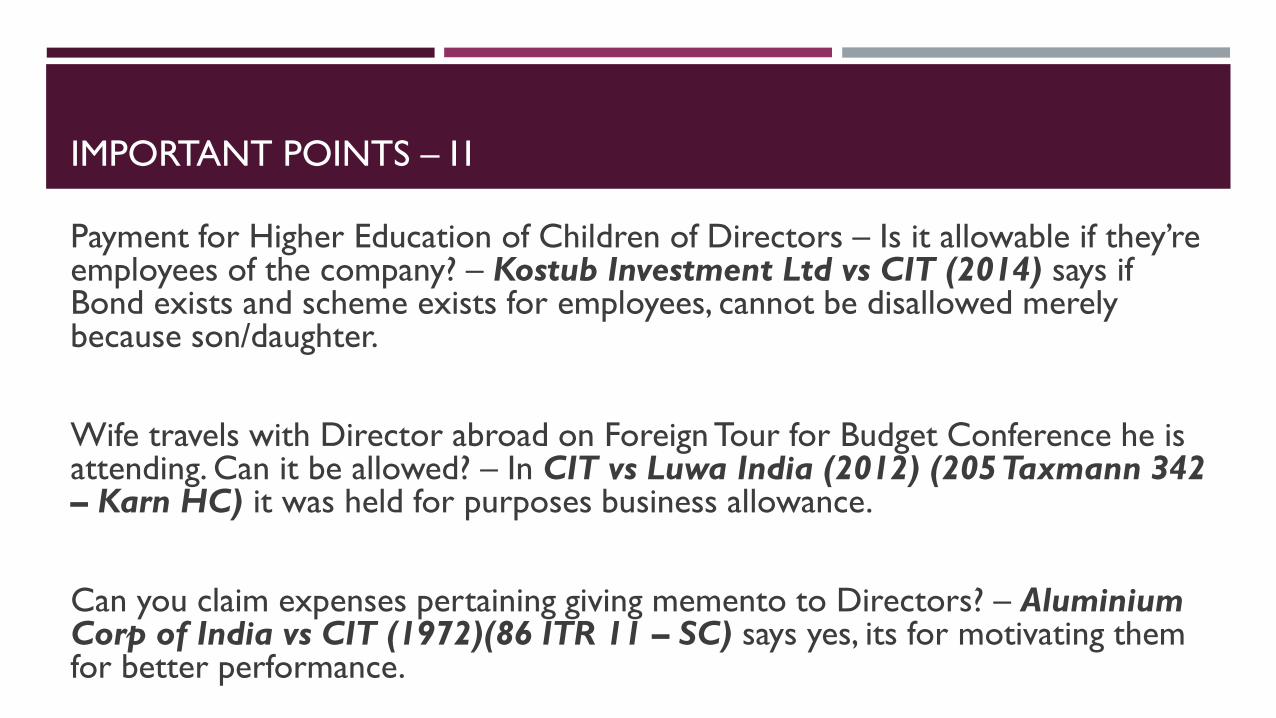

IMPORTANT POINTS – I1

Payment for Higher Education of Children of Directors – Is it allowable if they’re employees of the company? – Kostub Investment Ltd vs CIT (2014) says if Bond exists and scheme exists for employees, cannot be disallowed merely because son/daughter.

Wife travels with Director abroad on Foreign Tour for Budget Conference he is attending. Can it be allowed? – In CIT vs Luwa India (2012) (205 Taxmann 342 – Karn HC) it was held for purposes business allowance.

Can you claim expenses pertaining giving memento to Directors? – Aluminium Corp of India vs CIT (1972)(86 ITR 11 – SC) says yes, its for motivating them for better performance.

IMPORTANT QUESTION

Assessee is dead. Noticed served to legal heir after the expiration of time-barring date. Is it valid service of notice? – Sumit Balakrishna Gupta vs ACIT –2019 2 TMI 1209, Chandreshbhai Jayantibhai Patel vs ITO (Guj HC)

“The Hon’ble High Court has held that the issuance of a notice under Section 148 of the Act is the foundation for reopening of an assessment. Consequently, the sine qua non for acquiring jurisdiction to reopen an assessment is that such notice should be issued in the name of the correct person.

This requirement of issuing notice to a correct person and not to a dead person is not merely a procedural requirement but is a condition precedent to the impugned notice being valid in law”

IMPORTANT POINTS – 1II

What is Sale Consideration is lesser than 50C value? How much can I reinvest? – GouliMahadevappa vs ITO – 256 ITR 90 says 50C value

Can you borrow and invest or should it be same money received as consideration? –ITO vs KC Gopalan – 107 TM 591 (Kerala) says you can borrow – As does CIT vs Vasudevan Chetiar 234 ITR 705 (Mad), CIT vs R Srinivasan 45 DTR 208 (Mad)

Cost of plot also to be included for reinvestment u/s 54/54F – Aryama Sundaram (Mad HC)

Can Assessee invest in the name of Spouse? – CIT v Natarajan (Mad HC) says YES (also Kamal Wahal case (Delhi) says same )

IMPORTANT POINTS –I V

Is reinvestment date considered to be as per 139(1) or 139(4)? –Saraswathy vs ITO, Alagappan Natarajan vs ITO, ITO vs KS Narasimhhan

Is 2 apartments together 1 house or 2 houses? – CIT vs Gita Duggal says 1. Act says 1 house not 1 unit

Co-ownership will be a separate property – MJ Siwani vs CIT (SC) says if you have 50% ownership of 2 houses, it will be 2 houses not 1 house (i.e. 50% + 50%)

IMPORTANT POINTS –V

Sale Agreement – 13/08/2010.

Possession handing over – 15/10/2011. Sale Deed – 03/07/2012.

Reinvestment u/s 54F on 22/04/2010 – Is this allowable u/s 54 or 54F?

Kishorbhai Patel v ITO (Guj HC) says YES. Extinguishment of rights happens on 13/08/2010

For 54/54F – Can construction start prior to transfer of Capital Asset. Can

Exemption be claimed? – CIT vs JR Subramanya Bhat says yes

Money spent towards renovation and remodelling flat – Can it be claimed u/s

54F? – Nayana Kirit Parikh vs ACIT (Mumbai ITAT) says Yes

IMPORTANT POINTS –VI

Due to litigation consideration placed in escrow account. After litigation finished, in year of receipt, reinvested in 54EC bonds. Can still claim 54EC deduction – PrCIT vs Mahipinder Singh Sandhu – 416 ITR 175 P&H

Payment for release of share in house property from a co-owner. Will be it be acquisition of House Property – CIT v TN Aravinda Reddy (SC) 120 ITR 46 (1979) - says yes

54F says Residential House – Do they mean USE or do they mean NATURE of the Asset? – Hyd ITAT (N Revati vs ITO) vs Delhi ITAT (Sanjeev Puri vs DCIT), recently Navin Jolly vs ITO (Karn HC)(ITA No.320 of 2011)

IMPORTANT POINTS –VII

Delay by builder, beyond 3 years, in completing the construction of property. Still eligibilefor 54 or 54F? – CIT vs Girish Ragha 69 TM 95

Taxation of Sale of Life Interest – Taxable in both life-tenant and person who inherits it after – K Ramachandra Chettiar (Madras)(1983)

Capital gains arises in the hands of Owner, not GPA holder – Veerannagiri Gopal Reddy vs ITO (2019 – HydTribunal). Facts – Original owners entered into GPA in 2007. GPA mentions no consideration but original owners admit sale consideration of 8.4 lacs in 2007 return.

In 2014, GPA holder registers property in name of his daughter. Dept wants to Tax him for Capital Gains. He takes stand that his daughter only compensated original owners in 2007.

“

”

Thank You!

Dr. CA ABHISHEK MURALIM.Com, FCA, ACMA, CGMA, CIMA(Lon.), LLB, CISA(USA), DISA(ICAI), D.Litt, ADIT (UK)

Further doubts? Let’s discuss!

[email protected] ; [email protected]

Mobile: +91 99625 21966

Related Documents