December, 2015 This document is only informative and should not be used to initiate or refrain from any actions. www.duijntax.com 1 of 16 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW [email protected] www.duijntax.com Dutch Tax / Bilateral Investment Treaty overview Q4, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

December, 2015This document is only informative and should not be used

to initiate or refrain from any actions. www.duijntax.com

1 of 16

Hendrik van DuijnDTS Duijn's Tax SolutionsZuidplein 36 (WTC Tower H)1077 XV Amsterdam The Netherlands

T +31 888 387 669T +31 888 DTS NOW

Dutch Tax / Bilateral Investment Treaty overview Q4, 2015

December, 2015 2 of 16

Dutch Tax / Bilateral Investment Treaty overview Q4, 2015

i. Which Dutch tax treaties have been concluded recently?

ii. Concluded tax treaty highlights

iii. Which Dutch tax treaties have been amended recently?

iv. Amended tax treaty highlights

v. Which tax treaties are being (re)negotiated?

vi. Recent Dutch treaty opportunities

vii. Dutch tax treaty and Dutch bilateral investment treaty list

viii. Dutch bilateral investment treaty only list

Contents

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

December, 2015 3 of 16

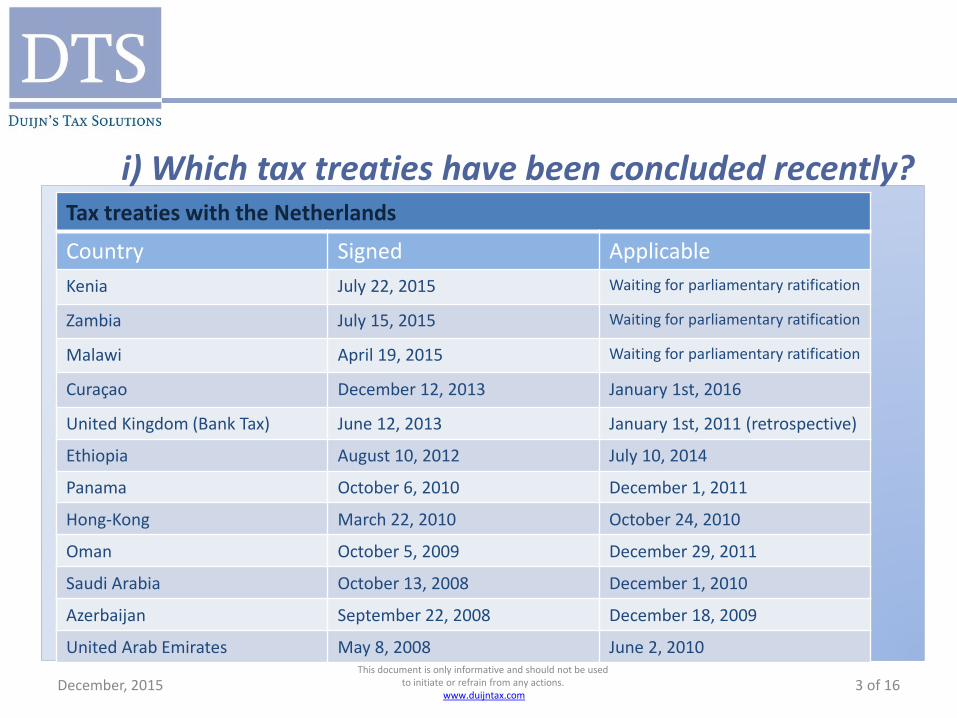

i) Which tax treaties have been concluded recently?

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

Tax treaties with the Netherlands

Country Signed Applicable

Kenia July 22, 2015 Waiting for parliamentary ratification

Zambia July 15, 2015 Waiting for parliamentary ratification

Malawi April 19, 2015 Waiting for parliamentary ratification

Curaçao December 12, 2013 January 1st, 2016

United Kingdom (Bank Tax) June 12, 2013 January 1st, 2011 (retrospective)

Ethiopia August 10, 2012 July 10, 2014

Panama October 6, 2010 December 1, 2011

Hong-Kong March 22, 2010 October 24, 2010

Oman October 5, 2009 December 29, 2011

Saudi Arabia October 13, 2008 December 1, 2010

Azerbaijan September 22, 2008 December 18, 2009

United Arab Emirates May 8, 2008 June 2, 2010

December, 2015 4 of 16

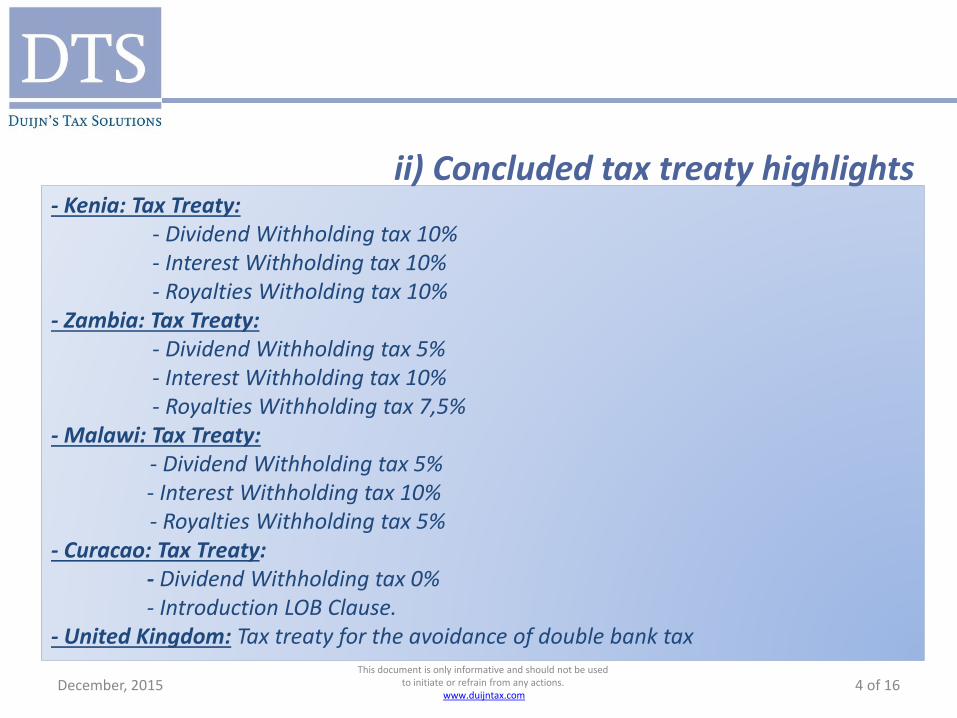

- Kenia: Tax Treaty:- Dividend Withholding tax 10%- Interest Withholding tax 10%- Royalties Witholding tax 10%

- Zambia: Tax Treaty:- Dividend Withholding tax 5%- Interest Withholding tax 10%- Royalties Withholding tax 7,5%

- Malawi: Tax Treaty: - Dividend Withholding tax 5%- Interest Withholding tax 10%- Royalties Withholding tax 5%

- Curacao: Tax Treaty:- Dividend Withholding tax 0%- Introduction LOB Clause.

- United Kingdom: Tax treaty for the avoidance of double bank tax

ii) Concluded tax treaty highlights

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

December, 2015 5 of 16This document is only informative and should not be used

to initiate or refrain from any actions. www.duijntax.com

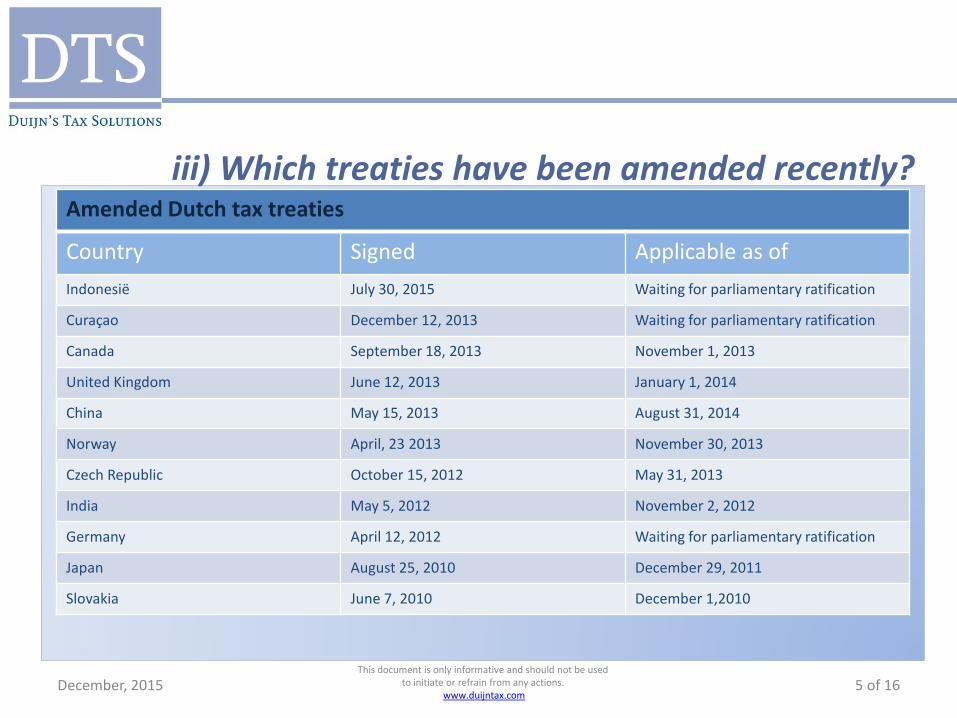

Amended Dutch tax treaties

Country Signed Applicable as of

Indonesië July 30, 2015 Waiting for parliamentary ratification

Curaçao December 12, 2013 Waiting for parliamentary ratification

Canada September 18, 2013 November 1, 2013

United Kingdom June 12, 2013 January 1, 2014

China May 15, 2013 August 31, 2014

Norway April, 23 2013 November 30, 2013

Czech Republic October 15, 2012 May 31, 2013

India May 5, 2012 November 2, 2012

Germany April 12, 2012 Waiting for parliamentary ratification

Japan August 25, 2010 December 29, 2011

Slovakia June 7, 2010 December 1,2010

iii) Which treaties have been amended recently?

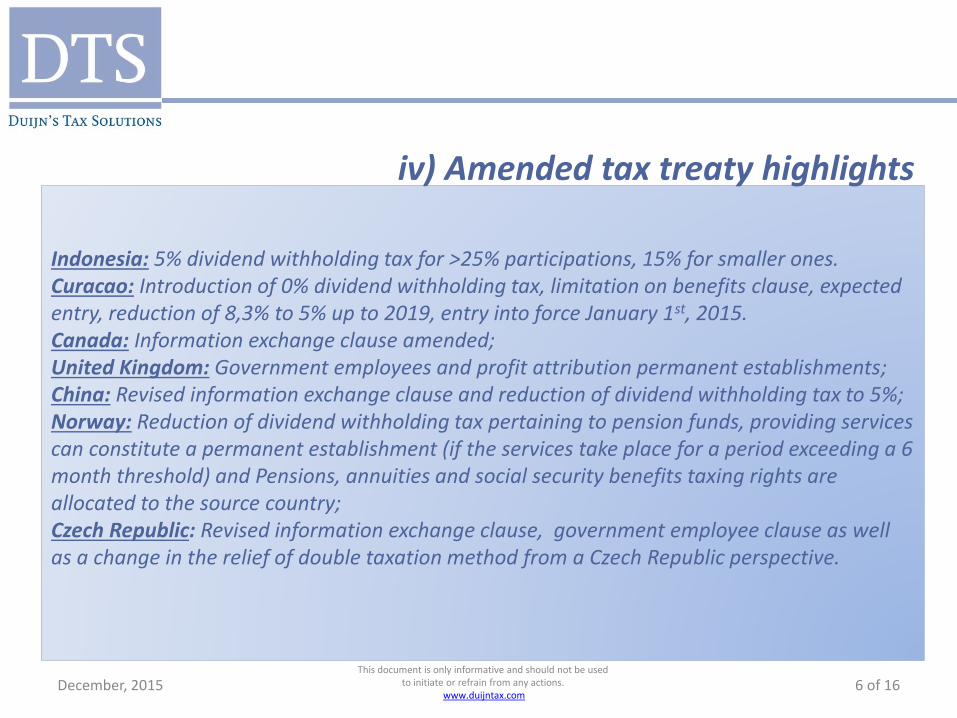

Indonesia: 5% dividend withholding tax for >25% participations, 15% for smaller ones.Curacao: Introduction of 0% dividend withholding tax, limitation on benefits clause, expected entry, reduction of 8,3% to 5% up to 2019, entry into force January 1st, 2015.Canada: Information exchange clause amended;United Kingdom: Government employees and profit attribution permanent establishments;China: Revised information exchange clause and reduction of dividend withholding tax to 5%;Norway: Reduction of dividend withholding tax pertaining to pension funds, providing services can constitute a permanent establishment (if the services take place for a period exceeding a 6 month threshold) and Pensions, annuities and social security benefits taxing rights are allocated to the source country; Czech Republic: Revised information exchange clause, government employee clause as well as a change in the relief of double taxation method from a Czech Republic perspective.

December, 2015 6 of 16This document is only informative and should not be used

to initiate or refrain from any actions. www.duijntax.com

iv) Amended tax treaty highlights

December, 2015 7 of 16

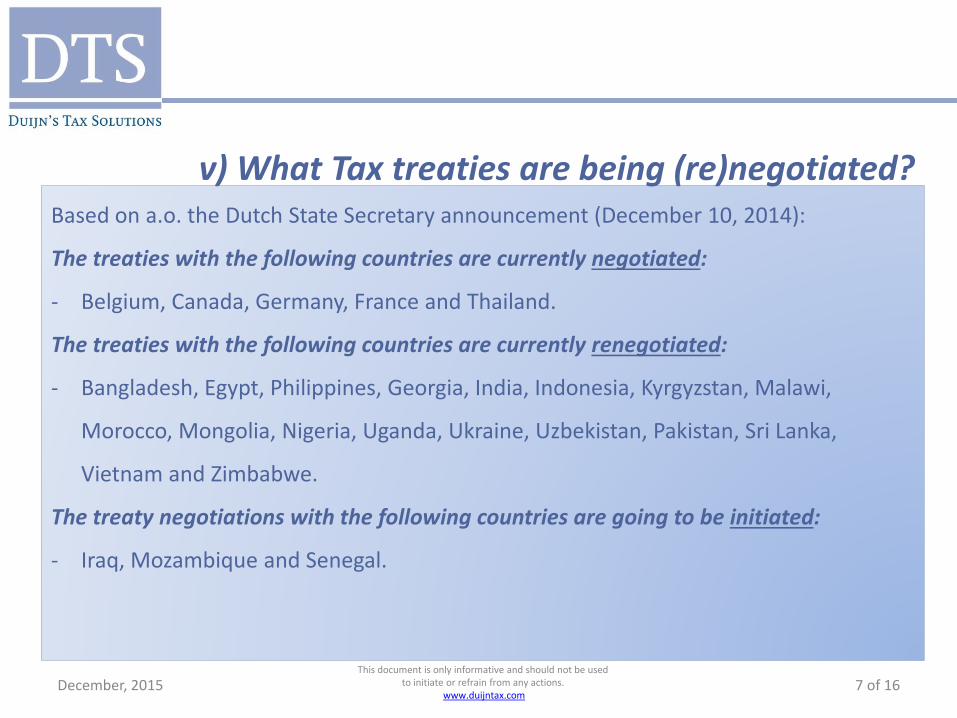

Based on a.o. the Dutch State Secretary announcement (December 10, 2014):

The treaties with the following countries are currently negotiated:

- Belgium, Canada, Germany, France and Thailand.

The treaties with the following countries are currently renegotiated:

- Bangladesh, Egypt, Philippines, Georgia, India, Indonesia, Kyrgyzstan, Malawi,

Morocco, Mongolia, Nigeria, Uganda, Ukraine, Uzbekistan, Pakistan, Sri Lanka,

Vietnam and Zimbabwe.

The treaty negotiations with the following countries are going to be initiated:

- Iraq, Mozambique and Senegal.

v) What Tax treaties are being (re)negotiated?

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

December, 2015 8 of 16

Germany, signed on 12 April, 2012, hopefully to apply as from January 1st, 2016,

comprehensive protocol;

Japan, amended as per August 25, 2010, applies as from December 29th, 2011, 0%

dividend withholding tax rate available, includes a limitation on benefits article;

Ethiopia, bilateral investment treaty in force, tax treaty in force as of July 10, 2014;

Argentina cancelled its tax treaty with several countries including Spain. Because the

Netherlands has a solid tax treaty as well as a Bilateral Investment Treaty, this is a

genuine treaty opportunity.

vi) Recent Dutch treaty opportunities?

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

December, 2015 9 of 16

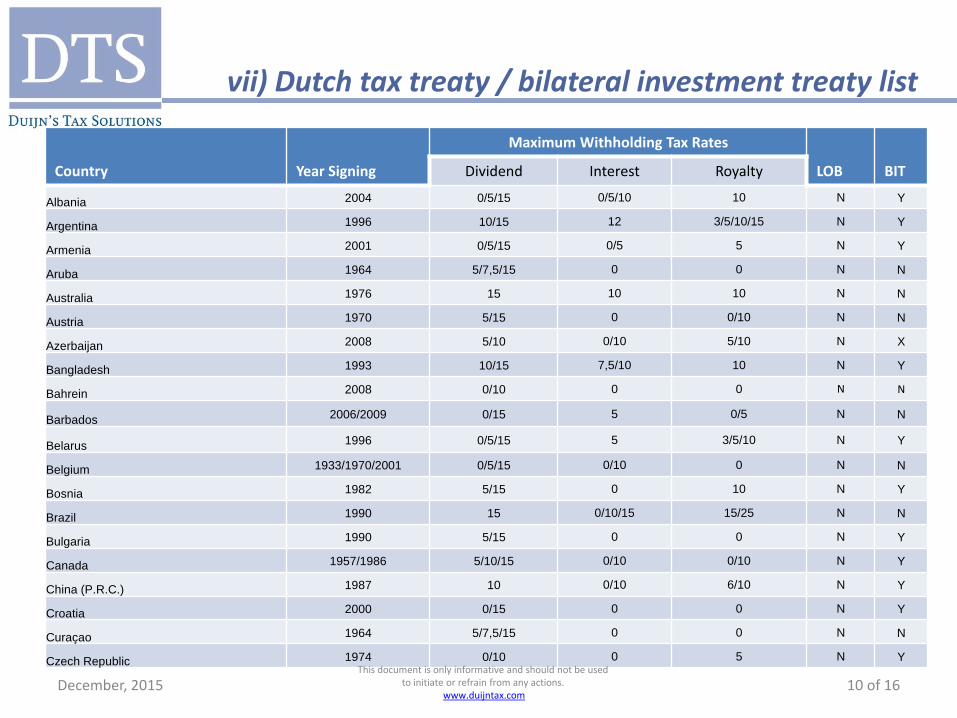

vii) Dutch tax treaty / bilateral investment treaty list

LEGENDA

Country

This is the country with wich the treaty had been signed, or its successor (for

instance former Sovjet Union states)

Year Signing

This is the year in which the treaty was signed. This typically does not

coincide with the year of enactment and/or the applicable year

Dividend

The dividend withholding tax rates are divided by a / to reflect the portfolio

investment rate on the one hand and the corporate participation rate (with a

certain percentage of vote and/or value threshold which needs to be met)

Interest

The interest withholding tax rates are divided by a / to reflect the different

applicable rates. The lower rate is typically the rate used by banks and

government owned businesses.

Royalty

The royalty withholding tax rates are divided by a / to reflect the different

applicable rates. The rates used differ by category of royalty income, such as

trademarks, patents or movie licenses.

LOB

Stands for Limitation On Benefits clause, which restricts the eligibility of the

treaty benefits to qualified persons under the treaty.

BIT

Bilateral Investment Treaty (the treaty with Venezuala has been cancelled,

therefore the X has been inserted. It still remains in force)

Dutch tax treaty DTT

Bilateral Investment Treaty BIT

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

December, 2015 10 of 16

Country Year Signing

Maximum Withholding Tax Rates

LOB BITDividend Interest Royalty

Albania 2004 0/5/15 0/5/10 10 N Y

Argentina 1996 10/15 12 3/5/10/15 N Y

Armenia 2001 0/5/15 0/5 5 N Y

Aruba 1964 5/7,5/15 0 0 N N

Australia 1976 15 10 10 N N

Austria 1970 5/15 0 0/10 N N

Azerbaijan 2008 5/10 0/10 5/10 N X

Bangladesh 1993 10/15 7,5/10 10 N Y

Bahrein 2008 0/10 0 0 N N

Barbados 2006/2009 0/15 5 0/5 N N

Belarus 1996 0/5/15 5 3/5/10 N Y

Belgium 1933/1970/2001 0/5/15 0/10 0 N N

Bosnia 1982 5/15 0 10 N Y

Brazil 1990 15 0/10/15 15/25 N N

Bulgaria 1990 5/15 0 0 N Y

Canada 1957/1986 5/10/15 0/10 0/10 N Y

China (P.R.C.) 1987 10 0/10 6/10 N Y

Croatia 2000 0/15 0 0 N Y

Curaçao 1964 5/7,5/15 0 0 N N

Czech Republic 1974 0/10 0 5 N YThis document is only informative and should not be used

to initiate or refrain from any actions. www.duijntax.com

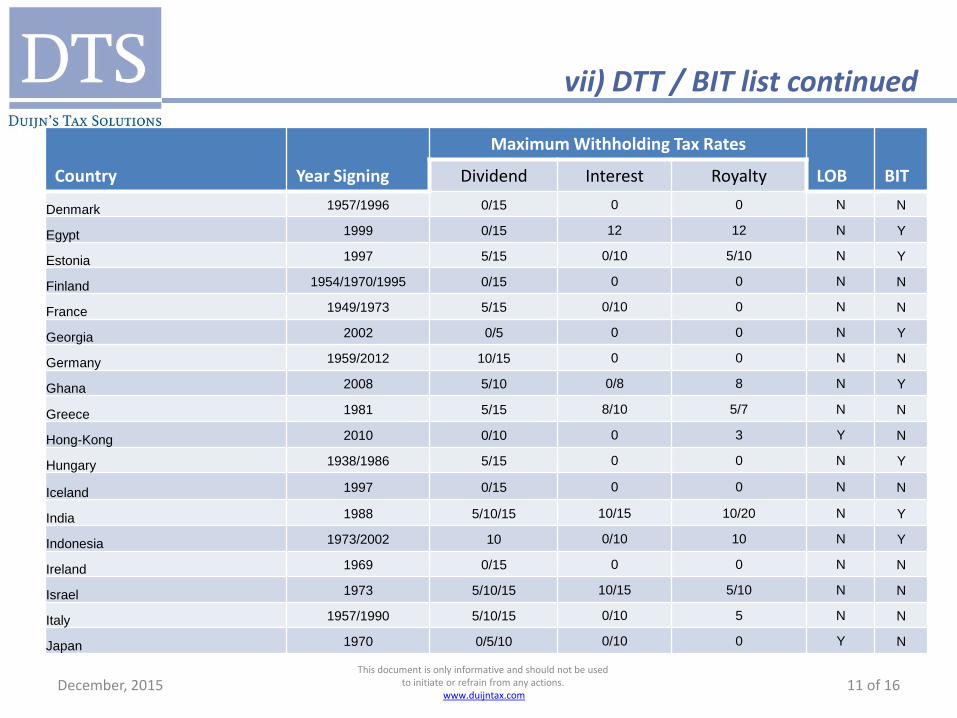

vii) Dutch tax treaty / bilateral investment treaty list

December, 2015 11 of 16

Country Year Signing

Maximum Withholding Tax Rates

LOB BITDividend Interest Royalty

Denmark 1957/1996 0/15 0 0 N N

Egypt 1999 0/15 12 12 N Y

Estonia 1997 5/15 0/10 5/10 N Y

Finland 1954/1970/1995 0/15 0 0 N N

France 1949/1973 5/15 0/10 0 N N

Georgia 2002 0/5 0 0 N Y

Germany 1959/2012 10/15 0 0 N N

Ghana 2008 5/10 0/8 8 N Y

Greece 1981 5/15 8/10 5/7 N N

Hong-Kong 2010 0/10 0 3 Y N

Hungary 1938/1986 5/15 0 0 N Y

Iceland 1997 0/15 0 0 N N

India 1988 5/10/15 10/15 10/20 N Y

Indonesia 1973/2002 10 0/10 10 N Y

Ireland 1969 0/15 0 0 N N

Israel 1973 5/10/15 10/15 5/10 N N

Italy 1957/1990 5/10/15 0/10 5 N N

Japan 1970 0/5/10 0/10 0 Y N

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

vii) DTT / BIT list continued

December, 2015 12 of 16

Country Year Signing

Maximum Withholding Tax Rates

LOB BITDividend Interest Royalty

Jordan 2006 0/5/15 5 10 N Y

Kazakhstan 1996 0/5/15 0/10 10 N Y

Kenya 2015 10/15 10 10 N Y

Korea – South 1978 10/15 10/15 10/15 N Y

Kosovo 1982 5/15 0 10 N N

Kuwait 2001 15 0 0 N Y

Kyrgyzstan 1982 15 0 0 N Y

Latvia 1994 5/15 0/10 5/10 N Y

Lithuania 1999 5/15 10 5/10 N Y

Luxembourg 1968 2,5/15 0 0 N N

Macedonia 1998 0/15 0 0 N Y

Malawi 2015 5/10/15 10 5 N Y

Malaysia 1988/1996/2009 0/15 10 8 N Y

Malta 1977 5/15 10 0/10 N Y

Mexico 1993/2008 0/5/15 0/5/10/15 10 N Y

Moldova2000 0/5/15 0/5 0 N Y

Morocco 1977 10/25 10/25 10 N Y

Netherlands Antilles 1964/1985/1996/2005 8,3/15 0 0 N N

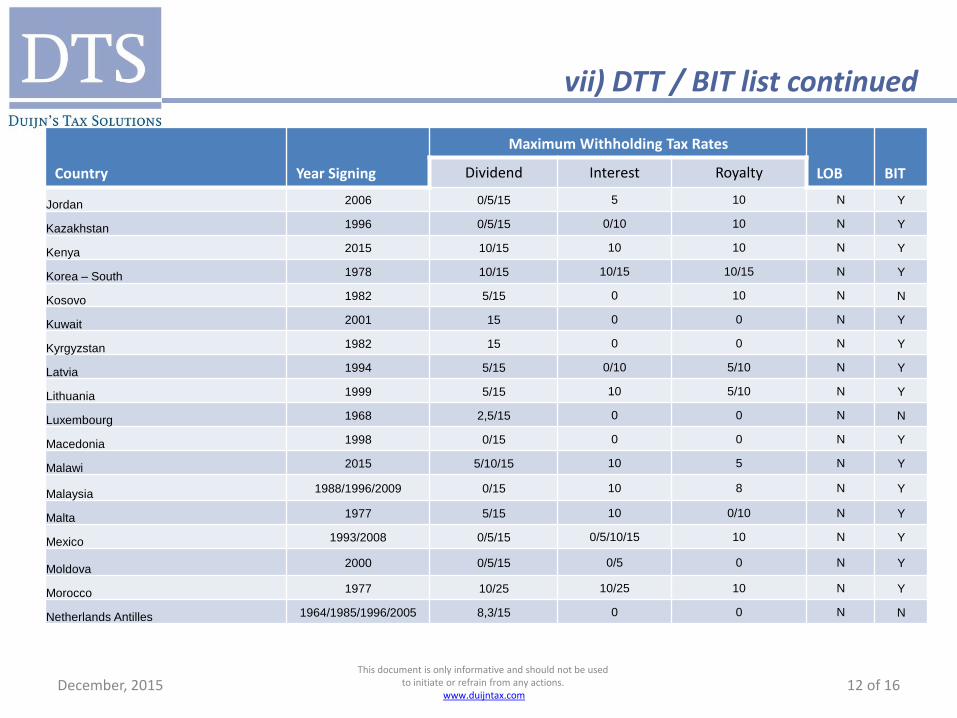

vii) DTT / BIT list continued

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

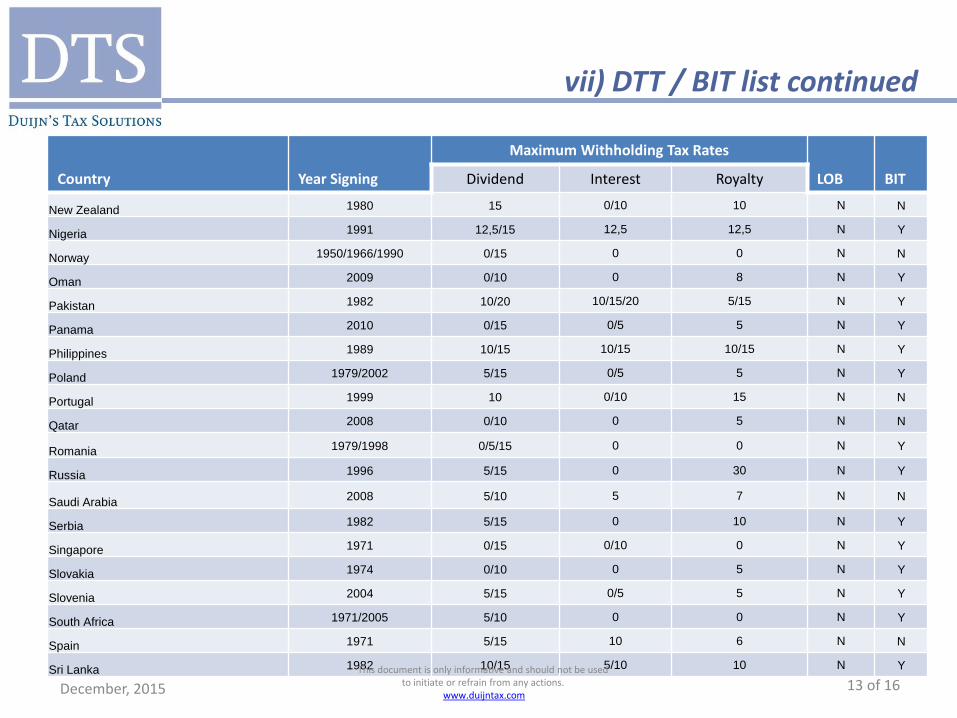

December, 2015 13 of 16

Country Year Signing

Maximum Withholding Tax Rates

LOB BITDividend Interest Royalty

New Zealand 1980 15 0/10 10 N N

Nigeria 1991 12,5/15 12,5 12,5 N Y

Norway 1950/1966/1990 0/15 0 0 N N

Oman 2009 0/10 0 8 N Y

Pakistan 1982 10/20 10/15/20 5/15 N Y

Panama 2010 0/15 0/5 5 N Y

Philippines 1989 10/15 10/15 10/15 N Y

Poland 1979/2002 5/15 0/5 5 N Y

Portugal 1999 10 0/10 15 N N

Qatar 2008 0/10 0 5 N N

Romania 1979/1998 0/5/15 0 0 N Y

Russia 1996 5/15 0 30 N Y

Saudi Arabia2008 5/10 5 7 N N

Serbia 1982 5/15 0 10 N Y

Singapore 1971 0/15 0/10 0 N Y

Slovakia 1974 0/10 0 5 N Y

Slovenia 2004 5/15 0/5 5 N Y

South Africa 1971/2005 5/10 0 0 N Y

Spain 1971 5/15 10 6 N N

Sri Lanka 1982 10/15 5/10 10 N YThis document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

vii) DTT / BIT list continued

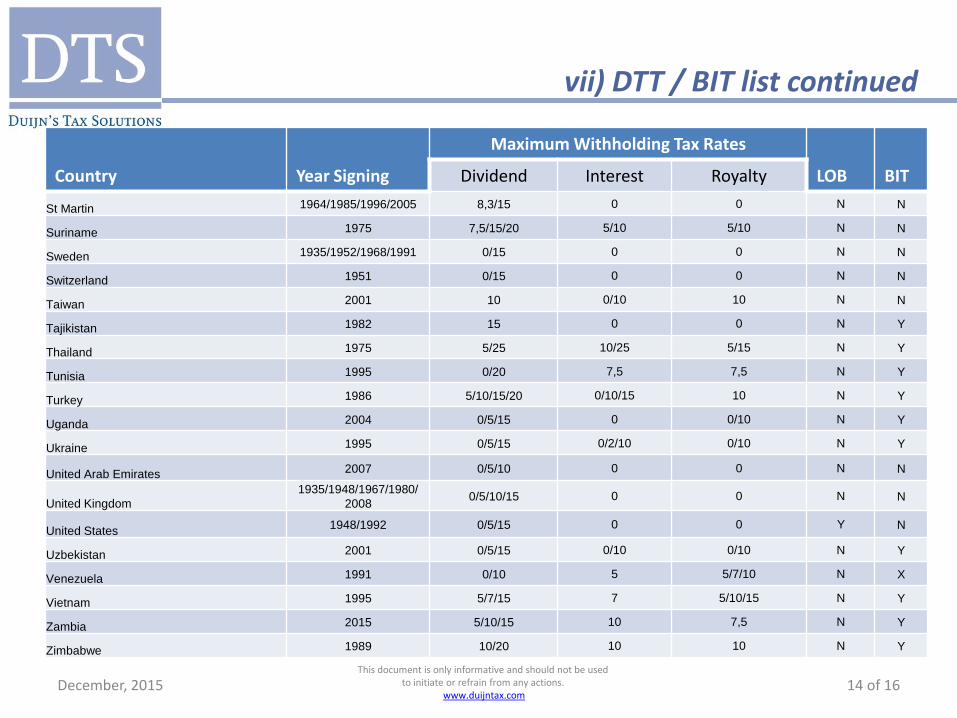

December, 2015 14 of 16

Country Year Signing

Maximum Withholding Tax Rates

LOB BITDividend Interest Royalty

St Martin 1964/1985/1996/2005 8,3/15 0 0 N N

Suriname 1975 7,5/15/20 5/10 5/10 N N

Sweden 1935/1952/1968/1991 0/15 0 0 N N

Switzerland 1951 0/15 0 0 N N

Taiwan 2001 10 0/10 10 N N

Tajikistan 1982 15 0 0 N Y

Thailand 1975 5/25 10/25 5/15 N Y

Tunisia 1995 0/20 7,5 7,5 N Y

Turkey 1986 5/10/15/20 0/10/15 10 N Y

Uganda 2004 0/5/15 0 0/10 N Y

Ukraine 1995 0/5/15 0/2/10 0/10 N Y

United Arab Emirates 2007 0/5/10 0 0 N N

United Kingdom

1935/1948/1967/1980/

20080/5/10/15 0 0 N N

United States1948/1992 0/5/15 0 0 Y N

Uzbekistan 2001 0/5/15 0/10 0/10 N Y

Venezuela 1991 0/10 5 5/7/10 N X

Vietnam 1995 5/7/15 7 5/10/15 N Y

Zambia 2015 5/10/15 10 7,5 N Y

Zimbabwe 1989 10/20 10 10 N Y

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

vii) DTT / BIT list continued

December, 2015 15 of 16

viii) Bilateral investment treaty only list

Country Country Country Country

Belize Cuba Jamaica Peru

Benin Ecuador Kenya Senegal

Bolivia El Salvador Laos Sudan

Burkina Faso Eritrea* Lebanon Tajikistan

Cambodia Ethiopia Mali Tanzania

Cameroon Gambia Mozambique Uruguay

Cape Verde Guatemala Namibia Yemen

Chile Honduras Nicaragua

Costa Rica Ivory Coast Paraguay

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

December, 2015 16 of 16

SCOPE LIMITATION

This presentation does not represent an opinion of DTS and should not be relied upon as such. The presentation has not been

prepared with the level of due diligence and analysis that would be needed to initiate or refrain from any actions. Further

research and analysis is required prior to initiate or refrain from any actions. This presentation has not been reconciled with

the Dutch tax authorities.

The information in this presentation is based on general information and cannot be used to base tax or business decisions on.

This presentation is intended to provide preliminary guidance in anticipation of further examination, discussions and analysis

of issues to be identified.

This document was not intended or written to be used, and it cannot be used, for the purpose of avoiding U.S. federal, state or local tax penalties. This includes penalties that may apply if the transaction that is the subject of this document is found to lack economic substance or fails to satisfy any other similar rule of law.

Pursuant to an engagement between DTS and Client, General Terms & Conditions of DTS are applicable to the work performed in the execution of the engagement by DTS. The liability with respect to the envisaged engagement is limited in accordance with the provisions laid down in the General Terms & Conditions .Please note that DTS is not liable in any event for lost profits or any consequential, indirect, punitive, exemplary or special damages.

Hendrik van DuijnDTS Duijn's Tax SolutionsZuidplein 36 (WTC Tower H)1077 XV Amsterdam The Netherlands

T +31 888 387 669T +31 888 DTS NOWF +31 88 8 387 601

This document is only informative and should not be usedto initiate or refrain from any actions.

www.duijntax.com

Related Documents

![Research on Develop Value Added Tax of Mongolia [Recovered]](https://static.cupdf.com/doc/110x72/577cdb6e1a28ab9e78a829cb/research-on-develop-value-added-tax-of-mongolia-recovered.jpg)