THE STRATEGIES OF BRICS’ NATIONAL OIL COMPANIES FOR ENERGY SECURITY : JOINT VENTURES BARGAINING AND VERTICAL INTEGRATION Draga Claudia MARIN 31 st USAEE/IAEE North American Conference Sheraton Austin, Texas 4-7 November 2012

Draga Claudia MARIN

Jan 08, 2016

31 st USAEE/IAEE North American Conference Sheraton Austin, Texas 4-7 November 2012. THE STRATEGIES OF BRICS’ NATIONAL OIL COMPANIES FOR ENERGY SECURITY : JOINT VENTURES BARGAINING AND VERTICAL INTEGRATION. Draga Claudia MARIN. Agenda. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE STRATEGIES OF BRICS’ NATIONAL OIL COMPANIES FOR ENERGY SECURITY : JOINT VENTURES BARGAINING AND VERTICAL

INTEGRATION

Draga Claudia MARIN

31st USAEE/IAEE North American ConferenceSheraton Austin, Texas4-7 November 2012

Agenda

I. Introduction : BRICs and NOCs, how do they ensure their continuing growth on the energy market ?

II. Vertical integration for an enhanced oil supply security. China and India examples

III. The influence of vertical integration on oil supply security : construction of an econometrical model

Brazil : pre-salt reserves discovered in 2006 Russia : 2nd crude oil producer after Saudi Arabia

China : R/P ratio law (9.9) compared to the one of the world (54.2)

India : 4th most important consumer of oil in 2011

Population GDPGDP annual growth

Proved oilreserves

Crude production *

Oil consumption **

Crude exports

MillionBillion dollars

Annual %Thousand million barrels

Million barrels daily

Million barrels daily

Thousand barrels daily

Brazil 196,7 2 476,70 2,7% 15,05 2,19 2,65 556,61

Russia 141,9 1 857,79 4,3% 88,18 10,28 2,96 5 786,30

India 1 241,4 1 857,77 6,9% 5,70 0,86 3,47 1,47

China 1 344,1 7 298,10 9,1% 14,71 4,09 9,76 30,00

US 311,6 15 094,00 1,7% 30,87 7,84 18,84 21,00

Saudi Arabia 28,1 576,80 6,8% 265,40 11,16 2,86 7 281,30

Figure 1. Economic and energetic data for BRICs (2011)

* Includes crude oil, shale oil, oil sands and NGLs (the liquid content of natural gas where this is recovered separately). Excludes liquid fuels from other sources such as biomass and coal derivatives.

** Inland demand plus international aviation and marine bunkers and refinery fuel and loss. Consumption offuel ethanol and biodiesel is also included.

Source : World Bank ; BP Statistical Review of World Energy June 2012 ; OPEC Annual Statistical Bulletin 2012 ; CPDP (Comité Professionnel du Pétrole - Oil Professional Committee).

I. Introduction : BRICs and NOCs, how do they ensure their continuing growth on the energy market ?

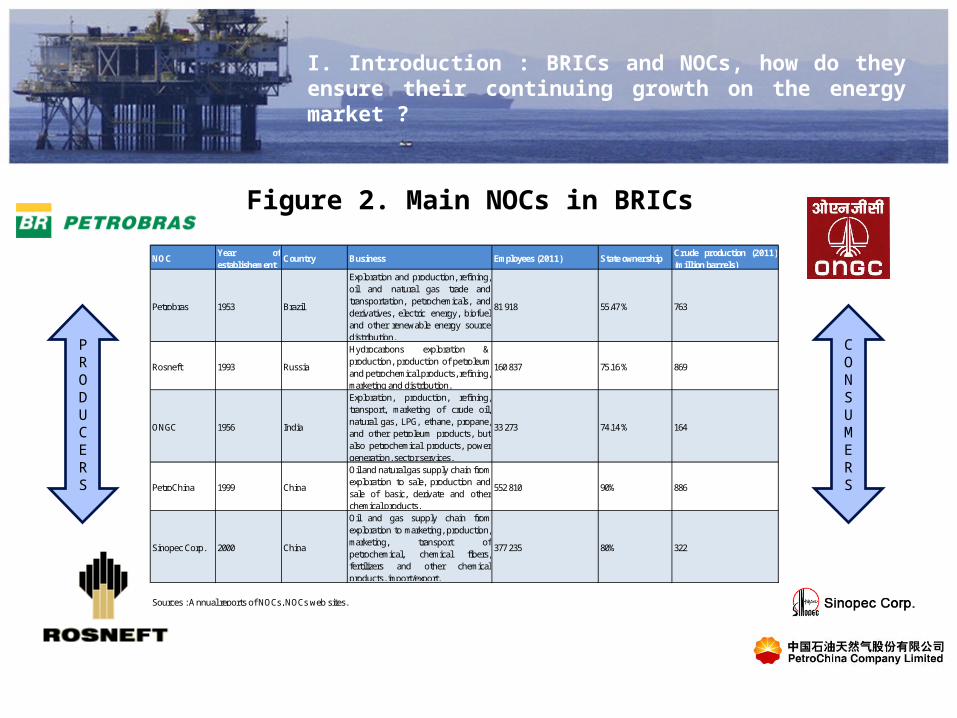

Figure 2. Main NOCs in BRICs

NOCYear ofestablishement

Country Business Employees (2011) State ownershipCrude production (2011)(million barrels)

Petrobras 1953 Brazil

Exploration and production, refining,oil and natural gas trade andtransportation, petrochemicals, andderivatives, electric energy, biofueland other renewable energy sourcedistribution.

81 918 55.47 % 763

Rosneft 1993 Russia

Hydrocarbons exploration &production, production of petroleumand petrochemical products, refining,marketing and distribution.

160 837 75.16 % 869

ONGC 1956 India

Exploration, production, refining,transport, marketing of crude oil,natural gas, LPG, ethane, propane,and other petroleum products, butalso petrochemical products, powergeneration, sector services.

33 273 74.14 % 164

PetroChina 1999 China

Oil and natural gas supply chain from exploration to sale, production andsale of basic, derivate and otherchemical products.

552 810 90% 886

Sinopec Corp. 2000 China

Oil and gas supply chain fromexploration to marketing, production,marketing, transport ofpetrochemical, chemical fibers,fertilizers and other chemicalproducts, import/export.

377 235 80% 322

Sources : Annual reports of NOCs, NOCs web sites.

PRODUCERS

CONSUMERS

I. Introduction : BRICs and NOCs, how do they ensure their continuing growth on the energy market ?

We analyze the strategy of NOCs from BRICs to enhance oil supply security in their countries

Econometrical model showing the influence of vertical integration on oil supply security

Vertical integration

Joint ventures bargaining

Oil supply securityChina and India- NOCs started activities in the upstream-Integration in downstream to ensure access to oil products and more efficiency

Brazil and Russia- NOCs don’t have the needed technology for upstream- Government and IOCs have different objectives, sometimes conflicting

I. Introduction : BRICs and NOCs, how do they ensure their continuing growth on the energy market ?

Advantages Disadvantages

Company level Company level- risky : function of technologies, it can increasecosts ;- flexibility loss ;- loss of competitivity ;

- economies of scale ; - possible capacity surplus.- reduction of opportunistic behavior ;

-price control by the government orregulation can be avoided ;-monopoly profits increase.

Market level Market level- increase of the market power ;- improve market strategy ;

- better control the environment ;- risk that company process and technologiesbecome obsolete ;

- product differenciation ; - possible antitrust problems ;

- vertical integration between downstreamand upstream companies permits to avoidtaxes or price control ;

-costs reduction : economies in terms ofcommunication, improvement of activitycoordination, elimination of certainproduction dictribution levels ;

- improve anticipation of demand and pricechanges.

- possible difficult access to supplier andconsumers, so loss of information ;

- synergies after vertical integration can besurevaluated.

Figure 3. Advantages and disadvantages of vertical integration

II. Vertical integration for an enhanced oil supply security. China and India

examples

Sources : Deschamps and Méritet (2000), Godard and Lipczynski (2005), Harrigan (1984), Mitchell (1976)

II. Vertical integration for an enhanced oil supply security. China and India

examples

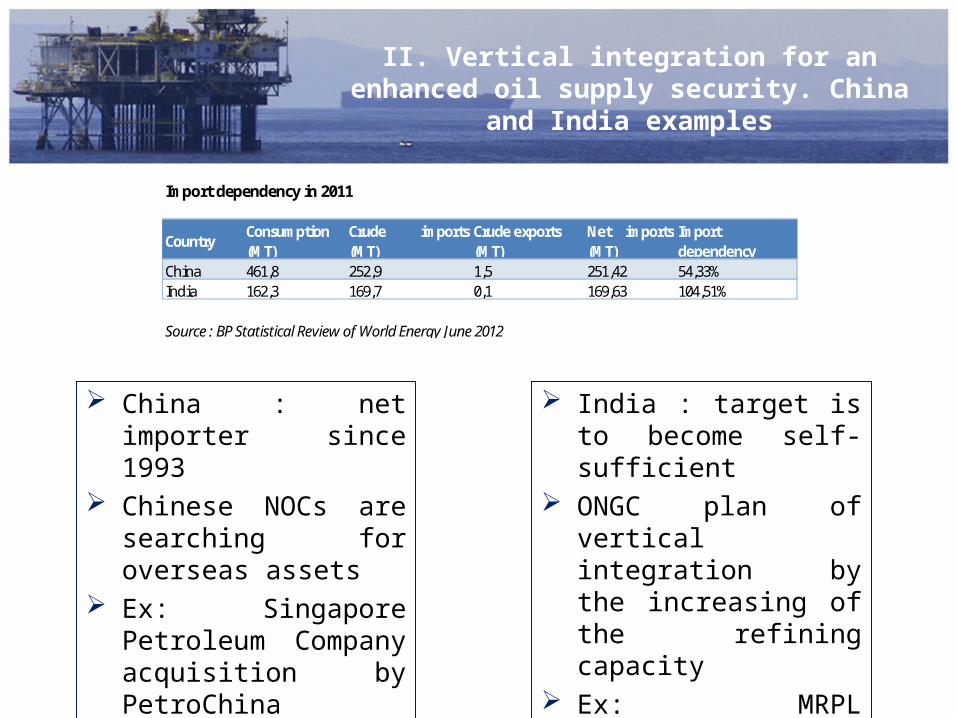

China : net importer since 1993

Chinese NOCs are searching for overseas assets

Ex: Singapore Petroleum Company acquisition by PetroChina

India : target is to become self-sufficient

ONGC plan of vertical integration by the increasing of the refining capacity

Ex: MRPL acquisition by ONGC

Import dependency in 2011

CountryConsumption (MT)

Crude imports(MT)

Crude exports (MT)

Net imports(MT)

Import dependency

China 461,8 252,9 1,5 251,42 54,33%India 162,3 169,7 0,1 169,63 104,51%

Source : BP Statistical Review of World Energy June 2012

Construction of oil supply indicators

Based on Arkel, Boots and Jansen’s (2004) report

4 indicators :• The diversity index • Diversity of supply regions • Diversity of supply regions and socio-politic stability• Resources depletion

Oil supply security index

III. The influence of vertical integration on oil supply security : construction of an econometrical model

Vertical integration measurement

Based on Harrigan (1986) work

4 dimensions : • Degree : measured at BU level, represents the % of a certain

semi-finished product transferred to downstream BU (or the % of needs of a certain product bought to upstream units).

• Number of stages of processing : index constructed as the sum of the number of steps multiplied by the value added for each step. We’ll compare NOCs with other private oil companies

• Breath of activities : number of activities in which the firm has engaged in (at a stage of production)/number of activities in which it was possible to engage in

• The form of ownership : % of participation in each strategic BU.

III. The influence of vertical integration on oil supply security : construction of an econometrical model

Regression model

• = indicator of oil supply security = average • i=2000…2011• =unknown parameters• indicator of degree of vertical integration = average (degree of

upstream integration; degree of downstream integration)• indicator of number of stages of processing• indicator of breadth of activities• indicator of ownership form• error term

III. The influence of vertical integration on oil supply security : construction of an econometrical model

The model is in a conceptual shape Data missing : For China and India (for the period 2000-2011) :Crude oil production abroad in each countryCrude oil imports from each sourceCrude oil production in some provinces of China For ONGC (for the period 2000-2011) : self-supply from

E&P

III. The influence of vertical integration on oil supply security : construction of an econometrical model

Concluding thoughts

Related Documents