DRAFT — NOT FOR DISTRIBUTION VERSION 6 The Dynamics of Credit Expansion and Contraction Ben Honig and Michael Honig Electrical Engineering & Computer Science Department Northwestern University John Morgan Haas School of Business University of California at Berkeley Ken Steiglitz Computer Science Department Princeton University July 16, 2016 2016-07-16 03:52 Contents 1 Introduction 2 1.1 Brief, broad review: boom/bust cycles, monetary policy, RBC, NK, DSGE ...... 2 1.2 Summary of results ..................................... 2 1.3 Contributions of this paper, contrast with most previous work ............. 3 2 The baseline (no-CB) money-flow model 3 2.1 The four-sector model ................................... 3 2.2 Notation ........................................... 5 2.3 Loan term distribution ................................... 7 2.4 Measurements ........................................ 7 2.5 Financing capital: Calculations for escrow and balloon payments ........... 9 2.6 Modeling fractional-reserve banking ........................... 10 2.7 Dynamic equations for the mixed cash/credit baseline (no-CB) model ........ 10 3 The mixed cash/credit, no-CB equilibrium 13 3.1 Equilibrium calculation .................................. 13 3.2 Parameterizing the equilibrium manifold by r ...................... 15 3.3 Household debt ....................................... 16 3.4 The equilibrium manifold ................................. 18 4 Comparative statics 19 4.1 Equilibrium r vs. τ m , varying f and e .......................... 19 4.2 Loan rate and some other variables vs. fraction of transactions in cash ........ 21 4.3 Loan rate vs. fractional reserve rate ........................... 21 4.4 Various vs. fractional reserve rate ............................. 22 4.5 Various vs. Propensity-to-Save e ............................. 23 4.6 Calibration ......................................... 24 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DRAFT — NOT FOR DISTRIBUTION

VERSION 6

The Dynamics of Credit Expansion and Contraction

Ben Honig and Michael HonigElectrical Engineering & Computer Science Department

Northwestern University

John MorganHaas School of Business

University of California at Berkeley

Ken SteiglitzComputer Science Department

Princeton University

July 16, 20162016-07-16 03:52

Contents

1 Introduction 21.1 Brief, broad review: boom/bust cycles, monetary policy, RBC, NK, DSGE . . . . . . 21.2 Summary of results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.3 Contributions of this paper, contrast with most previous work . . . . . . . . . . . . . 3

2 The baseline (no-CB) money-flow model 32.1 The four-sector model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32.2 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52.3 Loan term distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72.4 Measurements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72.5 Financing capital: Calculations for escrow and balloon payments . . . . . . . . . . . 92.6 Modeling fractional-reserve banking . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.7 Dynamic equations for the mixed cash/credit baseline (no-CB) model . . . . . . . . 10

3 The mixed cash/credit, no-CB equilibrium 133.1 Equilibrium calculation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133.2 Parameterizing the equilibrium manifold by r . . . . . . . . . . . . . . . . . . . . . . 153.3 Household debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163.4 The equilibrium manifold . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

4 Comparative statics 194.1 Equilibrium r vs. τm, varying f and e . . . . . . . . . . . . . . . . . . . . . . . . . . 194.2 Loan rate and some other variables vs. fraction of transactions in cash . . . . . . . . 214.3 Loan rate vs. fractional reserve rate . . . . . . . . . . . . . . . . . . . . . . . . . . . 214.4 Various vs. fractional reserve rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 224.5 Various vs. Propensity-to-Save e . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 234.6 Calibration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

1

5 Baseline (no-CB) simulations 245.1 Sticky wages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245.2 A sample simulation of the baseline model (see Appendix) . . . . . . . . . . . . . . . 24

6 Modeling the Central Bank and defaults 246.1 Model with Central Bank . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 256.2 Illustrative Experiments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 326.3 Model Parameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 326.4 Transient and Steady-State Effects of Central Bank Injections . . . . . . . . . . . . . 336.5 Credit Expansion and Contraction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 366.6 Loan Defaults . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 386.7 Central Bank Injections Through the Bank versus Household Sectors . . . . . . . . . 42

7 Conclusions and future work 437.1 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 437.2 Future work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 437.3 To do . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

1 Introduction

1.1 Brief, broad review: boom/bust cycles, monetary policy, RBC, NK, DSGE

1.2 Summary of results

We now summarize our main results. These are properties of the model, which are illustrated inthe numerical examples shown in the sequence of figures in Sections 6.2.

CB injections have a real effect on interest rate and resource allocation This is true insteady-state with injections at a fixed rate taking into account inflation expectations. Specifically,the steady-state supply of loanable funds increases at the inflation (same as injection) rate, and thedemand for loans anticipates the nominal increase in expected capital expenditures due to inflation.Even so, injections cause the supply of loans normalized by the money supply to increase relativeto the normalized demand for loans, causing the real interest rate to fall in steady-state in order toclear the market. (The steady-state nominal interest rate increases, but by less than the inflationrate.)

The reason for this shift is due to the memory in the system introduced by the distributionover loan windows. The injections have the effect of discounting past loans issued by the Bank,thereby reducing Bank liabilities. Given a fixed reserve requirement, that leaves more room forthe Bank to expand credit (increase loans), causing an increase in the supply of loans and a dropin the real interest rate. That produces a shift in resource (labor) allocation from CG to thecapital sector. There is an associated increase in production (equivalently, consumption) due to thereduced friction for funding capital expenditures. That increase effectively represents the continualtransfer of future consumption to the present, corresponding to a decrease in time-value of money,as reflected by the drop in real interest rate. This is illustrated in Fig. 12.

The preceding scenario occurs when the CB injections are inflationary, meaning the flow of cashfrom the CB into the economy exceeds the flow of cash out of the economy (to the CB) from loanrepayments. CB injections with full repayment of loans, including principal and interest, results ina deflation. In that scenario, the real interest rate rises, there is a shift in resource allocation fromthe K to the CG sector, and production declines. Here the decline represents a continual defermentof consumption to the future, as reflected by the increase in time-value of money. This is illustratedin Fig. 13.

2

Credit contractions and downward wage-price friction cause unemployment across theentire economy A credit contraction in the model can be caused either by an increase in reservesheld by the Bank or a net decrease in the rate at which the CB injects cash. In either case thiscauses a decrease in the flow of money into the entire labor pool, including both the CG and Capitalsectors. This causes the wage-price (total wages divided by number of laborers) to decrease in bothsectors, and adding friction results in unemployment and a decrease in total productivity. Theseverity of the decrease increases with the relative size of the credit contraction. This is illustratedin Figs. 14 and 15. In contrast, unemployment does not generally occur in a credit expansionsince wages to both sectors increase. In general, additional numerical examples indicate that thetransient effects due to credit contractions are much more volatile than those associated with creditexpansions.

Widespread unemployment due to a credit contraction is different from sector-specific unem-ployment that may be caused by other types of shocks. For example, a sudden increase in returnon capital (output elasticity) causes an increase in K wages and a decrease in CG wages, so thatunemployment is confined to the CG sector. This is illustrated in Fig. 16.

Loan defaults cause a credit contraction only by triggering an increase in the Bankreserve ratio Loan defaults eliminate the corresponding Bank assets (and liabilities), whichreduces the return on savings to the Household sector. Although that shifts the equilibrium, itdoes not cause a credit contraction. In fact, to maintain the same reserve ratio, or equivalently,the amount of credit generated prior to the defaults, the Bank would need to increase loans toreplace those that default. A more likely scenario is that the Bank would react to the defaults byincreasing the reserve ratio causing a credit contraction. This is illustrated in Figs. 17 and 18.

CB injections through the Bank cause a larger increase in loans and capital expendi-tures than injections through the Household sector Injecting through the Household sectorrefers to the scenario in which the CB transfers cash directly to the Household sector, adding tonominal wealth, instead of by purchasing Bank loans. Both injection methods increase capitalexpenditures (when inflationary) in steady-state, although injections through the Bank cause agreater shift, which increases with the injection rate. This assumes that the monetization of CGdebt by the CB is not included in the CG revenue forecast. An increase in the injection rate throughthe Bank can then cause a drop in production due to over-allocation of capital. In contrast, House-hold injections cannot cause such an over-allocation in capital since the fraction of cash injections,which are consumed (as opposed to saved), contribute directly to CG revenue. That revenue isthen split between capital and labor to maximize production.

1.3 Contributions of this paper, contrast with most previous work

2 The baseline (no-CB) money-flow model

2.1 The four-sector model

Figure 1 shows the basic flow diagram of the monetary flow model proposed here, in which a CentralBank (CB) has not yet been introduced.

3

Figure 1: Money transfers in the baseline model.

The model has four types of agents associated with different, aggregated sectors of the economy:households (HH), consumer goods firms (CG), capital firms (K), and banks (B). We model thebank, as well as the firms, as zero-profit, so the flow of funds is balanced at each sector. The HHsector supplies the labor to the two kinds of firms. The CG Firms employ labor and capital toproduce their output, and we will model them in this paper, for concreteness, with the standardCobb-Douglas production function with constant returns to scale. Furthermore, as in the manyvariations of the New Keynesian Model where capital accumulation is modeled (for example, [1, 2,3, 4, 5, 6]) we assume that capital is financed, and the financing cost is accounted for in the costof capital.1 However, we also assume that the supply of money available for loans is determinedby savings accumulated by HH, and that the demand for loans is determined by the amount ofmoney the CG Firms wish to spend on capital. We clear the market for loanable funds by adaptivelyadjusting the loan interest rate across periods at the central bank—so the equilibrium is not reachedinstantaneously—thus modeling a tatonnement process.

At each period the HH laborers (working for either CG or K Firms) receive income consisting ofwages, and the HH receives interest on savings, which is added to its current total wealth. The HHsector then decides what fraction of its aggregate wealth to consume based on the current interestrate, saving the rest in the B sector. In principle, this decision can take any functional form, butwe assume that the fraction saved, the propensity-to-save, is a nondecreasing function of savingsinterest rate.

Similarly, firms in the aggregated CG sector receive revenue from the sale of the consumer goodsthey produce, and must decide how much to allocate across capital and labor. We assume that thisdecision maximizes production for a fixed budget. In the particular implementation described here,using the Cobb-Douglas production function with constant returns to scale, and the CG sectortherefore allocates a fixed fraction of its revenue to capital.

The critical behavioral decisions which form the microfoundation of the MFM are thus encap-sulated in two key functions: the HH sector’s savings/consumption split (determining the supplyof loanable funds), and the CG sector’s capital/labor split (determining the demand for loanablefunds). Clearing the resulting market for loans then determines the equilibrium (nominal) interestrate. The uniqueness of the equilibrium will be discussed in detail later; it will turn out that there

1Gali [7], p. 5, notes that, “Though endogenous capital accumulation, a key element of [Real Business Cycle]theory, is absent in the basic versions of the New Keynesian model, it is easy to incorporate and is a common featureof medium-scale versions.” At this point he cites Smets and R. Wouters [8, 9].

4

will be—perhaps surprisingly—a one-dimensional manifold of equilibria,A final key feature of the no-CB baseline model is the constant monetary base. We refer to this

high-powered money, in fixed supply, as cash, as distinguished from credit. The banking sector isassumed to be governed by a fractional reserve requirement, and hence can create credit up to thelimit imposed by this requirement.

2.2 Notation

In developing dynamic, period-to-period update equations for the model economy, we will payspecial attention to microfoundations and choice theory. This concern has been reflected in thedevelopment of macroeconomics for at least the last half-century. Snowdon et al. ([10], section3.5.2), for example, discuss the importance of the microfoundations of non-clearing markets, andcite numerous authors, going back at least to Phelps et al. in 1970 [11], who “...maintained that noself-respecting macroeconomic theory was complete without a thorough examination of its microe-conomic credentials.” Our goal, of course, is to simulate the natural trajectory of the system asan economy, rather than just solve static equations for an equilibrium. We therefore seek updateequations that move us from the state of the system at discrete time t to the state at time t + 1that are motivated by actions that would be taken by a representative agents.

We use the following notation for the main program state variables. When we indicate thedependence of period t explicitly, as in “r(t)”, we mean the dynamic variable. The plain symbol,as in “r”, will mean the equilibrium value.

r = loan interest rate (1)

s = deposit, or savings, interest rate

W = total household wealth

Dlf = demand for loanable funds

Slf = supply of loanable funds

G = total cash in the economy, usually fixed at G0

Wc = wages of labor in consumer goods sector

Wk = wages of labor in capital goods sector

S = household savings

B = demand-deposit Household account

Et = target demand-deposit Escrow account

E = demand-deposit Escrow account

C = household consumption

L = loans from Banking sector to finance capital

Ucg = unspent funds held by CG

R = bank cash reserves

I = interest earned by Household deposits

Ktar = target capital expenditures, per period

Kc = actual capital expenditures, per period

ξ = continuing debt, total outstanding loans

Bc = total current Bank cash .

5

We also need the following structural parameters:

f = fractional reserve requirement (2)

kr = adaptation coefficient for loan rate adjustment

e = propensity-to-save parameter

βK = output elasticity of capital

βL = output elasticity of labor .

From a formal point of view, if we represent these system variables at period t by the statevector ~x(t), we seek the state-transition rule

~x(t+ 1) = Φ(~x(t)) . (3)

We illustrate our style of describing the state-transition equations with three fundamental behav-ioral decisions: the loan rate update, the savings/consumption split, and the labor/capital split.

The loan rate r(t) is adjusted each period with the update

r(t) = r(t− 1) + kr · (Dlf (t− 1)− Slf (t− 1))/G0 . (4)

This is a simple tatonnement adjustment at the bank that moves the rate up when the demandfor loans exceeds supply, and vice versa.2 Notice that the step size is normalized by the (for nowfixed) size of the monetary base, G0, and is governed by a parameter kr. This step-size parameterkr reflects the speed with which the banking sector adjusts the loan rate. In general, when kris too large the economy as a whole becomes unstable, and when it is too small the convergenceto equilibrium is correspondingly sluggish. Ultimately, its determination is part of the calibrationprocess.

Another key dynamic equation is the one that determines the Household sector’s savings/consumptionsplit:

S(t) = g(s(t)) · W(t) (5)

C(t) = (1− g(s(t))) · W(t) , (6)

where g(·) is the propensity-to-save function, which is a function of the savings rate s(t) and isassumed nonnegative and nondecreasing. In the examples given later in this paper we will use thesimple form g(s) = es/(1 + es), which ensures g(s) ≤ 1, and g(s) ≈ es for small es.

The firms that produce consumer goods must decide on the split between expenditures forlabor and investment in capital. This depends on the production function P (L,K), where L is thequantity of labor and K is the quantity of capital. For now we will use the general form

Ktar(t) = h · C(t) , (7)

where Ktar(t) is the target capital expenditure, C(t) is the HH consumption, and, as mentionedabove, h is labor/capital split, which depends on the labor and capital elasticities, βL and βK , butwith constant returns to scale is a constant. In particular, we take h = βK/(βL + βK). This targetwill be measured in next-period dollars.

2In practical simulations we may use more strategic variations of this update rule, but all aim at equilibratingthe money market, and all lead to the same equilibria.

6

2.3 Loan term distribution

We assume that when per-period loans in the total amount L are taken, their amounts are dis-tributed as w(τ) for τ between 1 and τmax, where

∑τ w(τ) = 1 and w(τ) ≥ 0. That is, loans of

w(i)L are taken with terms i, i = 1, ..., τmax. We can think of this as the result of randomly selectedloan terms in the limit as the number of CG firms becomes large. Were all loans to have one-periodterms, the velocity of money would be infinite, all loans would be repaid without delay, and therewould be no continuing outstanding credit. This is clearly unrealistic, and is one important reasonfor introducing longer-term loans.

One further bit of notation: We will denote the loans of term τ at time t by Larray(τ, t),corresponding naturally to a corresponding array in code.

2.4 Measurements

Certain variables of interest in the present model of an economy can be considered measurements,in the sense that they relate directly to commonly used metrics, but don’t directly affect the pathof a flowgraph simulation, at least not as yet in the current development. The monetary base Gis, in this sense, one example. In this section we will describe the calculation of other importantmeasurements, including the GDP, labor apportionment, and prices.3

In the model developed to this point, the GDP is just the sum of the consumption of consumergoods and capital, C+KEc, since the economy is closed and there are no government expenditures.To find the CG price, we need the CG output. To this end, let the total number of laborers (fornow fixed and equal to the number of HHs) be denoted by N = Nc +Nk, with Nc and Nk laborersin the CG and K sectors, respectively. We assume a perfectly competitive labor market, whichimplies Wc/Nc = Wk/Nk, the per-period wages per worker in dollars.

To use the Cobbs-Douglas production function, we assume capital is measured in number ofmachines in service. To determine the amount of active capital in equilibrium, we need to takeinto account the fact that a machine with lifetime τ is going to provide service that increases withτ ; for simplicity we assume that a τ -machine provides τ times as much service as a 1-machine. Ina perfectly competitive market for capital, the price of machines needs to reflect this, or the moreeffective machines will drive the less effective ones out of the capital market. We model this byassuming that a τ -machine, being superior to a 1-machine for τ > 1, requires q(τ)T periods oflabor to produce, where q(τ) is nondecreasing in τ with q(1) = 1, and therefore costs q(τ)TWk/Nk

dollars per machine. For the remainder of this paper we make the simplifying assumption thatq(τ) = τ , which amounts to assuming that there are no economies of scale in the use of longer-lasting machines.

Next, we must think about what proportion of workers are engaged in producing machines withτ = 1, 2, ..., τmax. For now, assume that the distribution of workers over τ -machines is uniform—there is no reason to believe that short-term loans are used to produce short-life machines. Assumethen that the distribution of labor over machine terms is uniform, so a fraction 1/τmax of the workersare engaged in making τ -machines.4 There are then (1/τmax)Nk/(τT ) τ -machines produced eachperiod. But machines in general last more than one period, and for every τ -machine producedthere are at any given period τ such machines in service. The total number of machines in serviceat a given period is therefore, in equilibrium,

K =∑τ

1

τmax

Nk

τTτ =

Nk

T. (8)

3We continue with the convention that variables without superscripts or arguments are equilibrium values, asabove.

4Right now we assume that the ranges of machine lifetimes and loan terms are the same; perhaps we should usetwo separate ranges.

7

The production of CG is then

Yc = A

(Nk

T

)βKNβLc (9)

= AW βKk W βL

c

(Wc +Wk)βK+βL,

using Nc = NWc/(Wc +Wk) and Nk = NWk/(Wc +Wk).5 In the case of constant returns to scale,

βL + βK = 1 and

Yc = AW βKc W 1−βK

k

(Wc +Wk), (10)

where A = AT−βKN . Finally, the CG price per unit is Cc/Yc, the consumption divided by thenumber of units produced.

The same arguments go through to find the GDP and prices as functions of time. Considerthe numbers of laborers in the CG and K sectors, Nc(t) and Nk(t). To mimic the discussionabove of equilibrium values, we assume that the wage rate in the CG and K markets equilibrateinstantaneously6 each period, which enables us to write

Wc(t)/Nc(t) = Wk(t)/Nk(t) (11)

for every t, and not just in equilibrium. It then follows in the same way that

Nc(t) = NWc(t)/(Wc(t) +Wk(t)) and (12)

Nk(t) = NWk(t)/(Wc(t) +Wk(t)) (13)

for every t.However, the amount of active capital as a function of time cannot be written simply as Nk(t)/T ,

as in Eq. 8, because there is in general some time-varying distribution of machines with differentlifetimes; off equilibrium, history matters. To calculate the total active capital K(t) at period t,note first that the number of τ -machines manufactured at period t is

L(t)/τmaxτTWk(t)/Nk(t)

, (14)

since L(t)/τmax is spent for τ -machines and τTWk(t)/Nk(t) is the cost of a τ -machine. The totalnumber of τ -machines active at time t is therefore

1

τ

t−1∑j=t−τ

Nk(j)L(j)/τmaxTWk(j)

, (15)

and the total active capital is

K(t) =

τmax∑τ=1

1

τ

t−1∑j=t−τ

Nk(j)L(j)/τmaxTWk(j)

. (16)

We note that in equilibrium (see below), L = Wk, and Eq. 16 reduces to K = Nk/T , Eq. 8. Thedependence of active capital on history will be important for the dynamics; it means, for example,that the full effects of a sudden change in investment will be delayed by a time on the order of τmaxperiods.

The production of CG is then

Yc(t) = AK(t)βKNc(t)βL , (17)

and the price of CG per unit is simply C(t)/Yc(t).

5Notice that maximum production occurs when Nk = βkN and NL = βLN , assuming constant returns to scale,βK + βL = 1.

6Or at least in a time much less than a period. We should revisit this assumption.

8

2.5 Financing capital: Calculations for escrow and balloon payments

Suppose a unit loan for term τ at rate r is made at period 0, uniform payments of c per periodare made to an escrow account starting at period 1, and the escrow account earns at the rate s perperiod. We assume that when the loan is originated the rates r and s are contractually fixed at thethen-current values for the entire term of the loan. After i periods, the firm owes (1 + r)i to theBank, and has an accumulation of c

∑i−1j=0(1 + s)j = (c/s)[(1 + s)i− 1] in escrow. Thus, for the firm

to make the balloon payment of (1 + r)τ that is due at period τ , we require that the payments be

c =s(1 + r)τ

(1 + s)τ − 1, P (r, s, τ) , (18)

which is the generalization of the usual mortgage amortization formula to the case where there is aspread between the loan and savings rates. To check the end cases, when s = 0 this corresponds tosetting aside (1 + r)τ/τ per period with no reinvestment (the limit as s→ 0) for τ periods. Whens = r this corresponds to the usual mortgage formula, where the reinvestments earn at the Bank’slending rate. For reference the total accumulation in Escrow after i payments due to a unit loanwith term τ is

A(r, s, i, τ) = (1 + r)τ(1 + s)i − 1

(1 + s)τ − 1. (19)

The actual capital expenditures per period, which we call Kc(t), can now be written

Kc(t) =

τmax∑τ=1

τ∑i=1

P (r(t− i), s(t− i), τ)Larray(τ, t− i) . (20)

In equilibrium this yields the appropriate version of the functional Θ, the per-unit, per-period costof loans:

Kc = L

τmax∑τ=1

τw(τ)P (r, s, τ) , Θ(r, s)L . (21)

The balance in the Escrow account after t periods is

E(t) =

τmax∑τ=1

τ∑i=1

A(r(t− i), s(t− i), i, τ)Larray(τ, t− i) , (22)

using Eq. 19 for the accumulation in Escrow. This expression includes payments of interest on non-mature and maturing loans but does not include new loans. The maturing loans will drop off theend of the summation and comprise the balloon payments. It is the balance in the demand-depositaccount E(t), and is thus a liability of the Bank. The functional J for equilibrium Escrow is

E = L

τmax∑τ=1

w(τ)(1 + r)τ

(1 + s)τ − 1

τ∑i=1

[(1 + s)i − 1

](23)

= L

τmax∑τ=1

w(τ)(1 + r)τ

(1 + s)τ − 1

[(1 + s)τ+1 − 1

s− τ − 1

], J(r, s)L .

The balloon payments at time t are in total

LBP (t) =

τmax∑τ=1

A(r(t− τ), s(t− τ), τ, τ)Larray(τ, t− τ) (24)

=

τmax∑τ=1

(1 + r(t− τ))τLarray(τ, t− τ) ,

9

which is in equilibrium

LBP = L

τmax∑τ=1

w(τ)(1 + r)τ . (25)

The balloon payments can be broken down into principal and interest parts:

LBPP (t) =

τmax∑τ=1

Larray(τ, t− τ) (26)

LBPI(t) = LBP (t)− LBPP (t) , (27)

and in equilibrium

LBPP = L (28)

LBPI = LBP − L . (29)

We also introduce the functional X that gives us the equilibrium interest component of the balloonpayments:

LBPI = L

τmax∑τ=1

w(τ) [(1 + r)τ − 1] , X(r)L (30)

Thus, in equilibrium, the balloon payments are

LBP = LBPI + L = (X + 1)L . (31)

2.6 Modeling fractional-reserve banking

2.7 Dynamic equations for the mixed cash/credit baseline (no-CB) model

We now write the dynamic update equations for the basic no-CB model, but with the added featurethat money is in general a mixture of cash and credit. We will discuss the initialization later—it isin fact an interesting question exactly what initial values of the state variables across the economycorrespond to realistic and reachable states.

• Update loan rate rate:7

r(t) = r(t− 1) + krDlf (t− 1)− Slf (t− 1)

G0. (32)

• The savings rate is determined de facto, the fractional interest earned per period. Thisreflects the fact that the banking sector is zero-profit, and the households in effect receive thedistribution of income from financing operations as part of the savings rate:8

s(t) =LBPI(t− 1)

S(t− 1) + E(t− 1). (33)

• Savings and withdrawal from savings:

g(t) =e · s(t)

1 + e · s(t)(34)

∆S(t) = g(t) · W(t− 1)− S(t− 1) (35)

7As noted above, we may use more strategic variations of this update rule, but all will aim at the same equilibriumcondition, Dlf (t) = Slf (t).

8An adaptive version of this determination of s may be used in some implementations, but, as in the case of theloan rate, the equilibrium will be unaffected.

10

• Total Revenue (Consumption):

C(t) = [1− g(t)]W(t− 1) (36)

• Cash portion (assumed to be fraction c) of consumption and deposit by households:

Cc(t) = c · C(t) (37)

∆C(t) = Wcash(t− 1)− Cc(t) + c · Ucg(t− 1) (38)

• Target capital expenditures:9

Ktar(t) = h · [C(t) + Ucg(t− 1)] (39)

• The demand for loans is the target capital expenditures, but discounted by the per-unit,per-period cost of financing a loan, Θ(r, s) from Eq. 21:

Dlf (t) = Ktar(t)/Θ(r, s) . (40)

• Compute the escrow deposit (capital expenditures): First compute the expected (target)amount in escrow, and then the amount to deposit. The total accumulation in Escrow afteri payments due to a unit loan with term τ is, from Eq. 19,

A(r, s, i, τ) = (1 + r)τ(1 + s)i − 1

(1 + s)τ − 1, (41)

where r and s are evaluated at the time a loan is initiated, assuming contractual rates at thattime. The target escrow is therefore

Etar(t) =

τmax∑τ=1

τ∑i=1

A(r(t− i), s(t− i), i, τ)Larray(τ, t− i) , (42)

and the escrow deposit is∆E(t) = Etar(t)− E(t− 1) , (43)

and the cash portion of the escrow deposit is

∆Ec(t) = c ·∆E(t) . (44)

• The balloon payments on all CG loans can be computed from Larray(τ, t) using Eqs. 24, 26,and 27:

LBP (t) =

τmax∑τ=1

(1 + r(t− τ))τLarray(τ, t− τ) (45)

LBPP (t) =

τmax∑τ=1

Larray(τ, t− τ) (46)

LBPI(t) = LBP (t)− LBPP (t) . (47)

• Update bank cash and total assets:10

Bc(t) = Bc(t− 1)− ckL(t− 1) + ∆C(t) + ∆Ec(t) . (48)

9Revisit this, since firms could subtract interest from revenue, and split the remainder, which would maximizeproduction

10Can this go negative? If so, should we put back [...]+?

11

• Apportion total bank liabilities due to demand-deposit accounts (savings and escrow) amongthose accounts. The intermediate variables S′(t) and E′(t) are updated version of S(t) andE(t).

S′(t) = S(t− 1) + ∆S(t) (49)

E′(t) = E(t− 1) + ∆E(t)− LBP (t) (50)

B(t) = S′(t) + E′(t) (51)

A(t) = B(t) + LBPI(t) (52)

S(t) = L(t)S′(t)

B(t), E(t) = L(t)

E′(t)

B(t). (53)

• We now can determine the wages of the CG sector, and the supply of loans (cash at the bankand reserves). A fraction of loans ck is assumed to be cash:

Wc(t) = C(t)−∆E(t) (54)

Slf (t) =1

f + ck(1− f){Bc(t)− f · [S(t) + E(t) + (1− c)Wc(t)]} . (55)

• Loans this period:L(t) = min{Slf (t), Dlf (t)} . (56)

• Capital wages, equal to the loans per period by flow conservation:

Wk(t) = L(t) . (57)

• Cash portion of wages:Wcash(t) = ckWk(t) + cWc(t) . (58)

• Unspent funds held by CG:

Ucg(t) = C(t)−∆E(t)−Wc(t) . (59)

• Total household wealth:

W(t) = Wc(t) +Wk(t) + S(t) + Ucg(t) . (60)

The total cash at the end of each period is Bc(t) + cWc(t) + cUcg(t), which can be checked againstG0.

Remark 1 Notice that each state variable appears on the left-hand side of a dynamic equationin the (temporally ordered) loop exactly once, which means that a state variable x(t) is assignedits value exactly once. We define the state variable’s equilibrium value as x = limt→∞ x(t), if thatlimit exists.

12

3 The mixed cash/credit, no-CB equilibrium

3.1 Equilibrium calculation

In equilibrium11, the market for loanable funds equilibrates, so that we know that Dlf = Slf =L = Wk. Begin by collecting the dynamic equations in subsection 2.7 with equilibrium values forthe variables:

Dlf = Slf = L = Wk (61)

s = LBPI/(S + E) (62)

∆S = gW − S , g(s) a known function (63)

Rv = C = (1− g)W (64)

Cc = cC (65)

∆C = Wcash − Cc (66)

Ktar = hC (67)

Etar = known linear function of L (68)

∆E = Etar − E (69)

∆Ec = c∆E (70)

Dlf = Ktar/Θ(r, s) (71)

Wc = C −∆E (72)

LBP = known linear function of L (73)

LBPI = LBP − L (74)

B′c = Bc − ckL+ ∆C + ∆Ec (75)

S′ = S + ∆S (76)

E′ = Etar − LBP (77)

B = S′ + E′ (78)

L = B + LBPI (79)

S = LS′/B (80)

Bc = B′c (81)

E = LE′/B (82)

Slf = 1f+ck(1−f) · [Bc − f · (S + E + (1− c)Wc)] (83)

Wcash = ckWk + cWc (84)

W = Wc +Wk + S . (85)

We can now express all the state variables, except r and s, as functions proportional to L, andordered in such a way that they can be computed sequentially. As we will see below, the valueof L is determined by the monetary base, an arbitrary scale. First, though, it is easy enough toeliminate the variables Cc, ∆C, Wcash, ∆Ec, and B′c, by direct substitution:

Dlf = Slf = L = Wk (86)

s = LBPI/(S + E) (87)

∆S = gW − S (88)

Rv = C = (1− g)W (89)

Ktar = hC (90)

11We will make no distinction between an equilibrium and a fixed-point, and use the terms interchangeably.

13

Etar = known linear function of L (91)

∆E = Etar − E (92)

Dlf = Ktar/Θ(r, s) (93)

Wc = C −∆E (94)

LBP = known linear function of L (95)

LBPI = LBP − L (96)

S′ = S + ∆S (97)

E′ = Etar − LBP (98)

B = S′ + E′ (99)

L = B + LBPI (100)

S = LS′/B (101)

E = LE′/B (102)

Slf = 1f+ck(1−f) · [Bc − f · (S + E + (1− c)Wc)] (103)

W = Wc +Wk + S , (104)

Observe that the bookkeeping for the bank cash Bc, Eq. 75, yields the equilibrium cash-balancecondition

Bc = Bc − ckL+ ckWk + cWc − cC + c∆E , (105)

or

ck(L−Wk) = c(Wc − C + ∆E) = 0 , (106)

which tells us nothing new, except that the cash ratios 0 ≤ c, ck ≤ 1 can be chosen arbitrarily.We will use the following known functions of r, s:

LBP = L∑τmax

i=1 wi(1 + r)i , XL (107)

LBPI = (X − 1)L (108)

Etar = L∑τmax

τ=1 wτ∑τ

i=1 A(r, s, i, τ) , Y L (109)

Θ =∑τmax

τ=1 τwτP (r, s, τ) (110)

g = given function of s (111)

Q , Θ/(h(1− g)) (112)

Z , (Y − 1 + gQ)/(Y −X + gQ) . (113)

We can now write all the state variables (except the rates) explicitly as multiples of L, usingknown factors, the factors, however, depending on the rates.

Dlf = Slf = L = Wk (114)

Etar = Y L (115)

Ktar = ΘL (116)

LBP = XL (117)

LBPI = (X − 1)L (118)

C = (Θ/h)L (119)

W = QL (120)

E′ = (Y −X)L (121)

14

S′ = gQL (122)

B = (Y −X + gQ)L (123)

L = (Y − 1 + gQ)L (124)

S = gQZL (125)

E = (Y −X)ZL (126)

∆E = [1− gQ(1− Z)]L (127)

∆S = [gQ(1− Z)]L (128)

Wc = [Q(1− gZ)− 1]L (129)

s = (X − 1)/(Y − 1 + gQ) . (130)

We are thus left with the problem of calculating two unknowns: r and s. The explicit equationfor s, Eq. 130 immediately gives us one condition:

s =X − 1

Y − 1 + gQ...Condition 1 . (131)

Notice that this gives, implicitly, the relationship between equilibrium s vs. r, and that this rela-tionship does not depend on f , c, or ck. We are thus left with one unknown—but, without furtherassumptions, we have run out of conditions.

3.2 Parameterizing the equilibrium manifold by r

It is particularly easy to resolve the extra degree of freedom in our model by simply choosing r,although that choice is not forced. This enables us to find the corresponding fixed point by solving(using binary search, for example) the one-dimensional search problem Condition 1, Eq. 131. Oncethe pair (r, s) is determined, the remainder of the state variables can be found by direct evaluationof the equilibrium conditions, Eqs. 107-129.

We can solving Condition 1 numerically using binary search, writing Eq. 131 in the form “in-creasing function of s = left-hand side = g = right-hand side”:

g =1

1 + Θ/hX−1

s−Y+1

, (132)

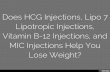

using Q = Θ/(h(1− g)). The binary search narrows the search down to a region where the right-hand side is decreasing, after which locating the crossing point is very easy. Figure 2 shows the(increasing) left- and right-hand sides of Eq. 132 for the case τmax = 60, r = 2%, c = ck = 0,and e = 500. There is a pole in right-hand side at about 4%, which makes it necessary to exercisecaution in the binary search. One way to make the search reasonably robust is to start with theright end of the initial search bracket very small, and expand it to the right (geometrically) untilthe value of the right-hand side is below that of the left-hand side, and then stop.

15

s, percent0 1 2 3 4 5 6

left-

and

rig

ht-h

and

side

s

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2Equil. Savings rate (%) vs. Loan rate (%)

e1= 500, tau

max= 60, f = 0.10, c=c

k= 0.00, at r= 2.00e-02, s (predicted)= 1.7013e-02...24-Dec-2015 16:27:46

Figure 2: An example showing the left- and right-hand sides of Condition 1. There is a pole in theright-hand side, which we need to exclude in the initial binary search bracket.

3.3 Household debt

Households are in debt to the bank a total Φ(t) (normalized value ϕ(t) , Φ(t)/G0). As describedbelow, we will choose the household debt exogenously (rather than the loan rate r) to render theequilibrium unique. We now calculate its value in terms of the other variables in the economy.

The total bank assets12 are

Bc(t)− ckL(t) + ξ(t) + Φ(t) , (133)

since Bc(t) − ckL(t) is the cash at the bank, and we define ξ(t) to be the total outstanding loansat the end of period t, (which thus includes the loans made in that period):

ξ(t) ,τmax∑τ=1

τ∑i=1

Larray(τ, t− i+ 1) . (134)

The equilibrium value of ξ(t), used below, is

ξ = L

τmax∑τ=1

τwτ , ΓL . (135)

We note that the cash at the bank can also be written13

Bc(t)− ckL(t) = f(S(t) + E(t) + (1− c)Wc(t) + (1− ck)Wk(t)) . (136)

12Explain.13Check numerically. Explain.

16

The corresponding total bank liabilities are14

L(t) + (1− ck)Wk(t) + (1− c)Wc(t) . (137)

We model the bank as a zero-profit sector, so its total assets and liabilities are equal at the end ofevery period. Therefore,

Φ(t) = L(t) + L(t) + (1− c)Wc(t)−Bc(t)− ξ(t) , (138)

using Wk(t) = L(t). Now use Bc from Eq. 103:

Slf =1

f + ck(1− f)[Bc − f(S + E + (1− c)Wc)] , (139)

or

Bc = [f + ck(1− f)]L+ f(S + E + (1− c)Wc) , (140)

to write Φ as

Φ = L − ξ − [f + ck(1− f)]L− f(S + E + (1− c)Wc) + L+ (1− c)Wc (141)

= L − ξ − [f + ck(1− f)]L+ (1− f)(1− c)Wc − f(S + E) + L .

Using the equilibrium conditions Eqs. 107-129, this can be written, as usual, as a multiple of L,yielding

Φ/L = (1− f)(1− c) [Q(1− gZ)− 1] + (Y − 1 + gQ) (142)

−Γ + 1− [f + ck(1− f)]− f [(Y −X) + gQ]Z

= (1− f)(1− c) [Q(1− gZ)− 1] + (1− f)(Y − 1 + gQ)

−Γ + 1− [f + ck(1− f)] ,

simplifying using [(Y −X) + gQ]Z = Y − 1 + gQ, which follows from the definition of Z. To check:Notice that when f = 1, the case when total reserve is required, Φ = −ΓL = −ξ, which is correct;household debt is the negative of bank assets, which are in this case just outstanding loans ξ. Whenc = ck = 1, the all-cash case, Φ = (1− f) [Y − 1 + gQ]L− ΓL = (1− f)L − ξ.15

We may want to normalize Φ by G0, not L, so we write G0 in terms of L by combining the factthat G0 = Bc + cWc and Eq. 140. The result is

G0/L = (1− f)ck + f [Y + gQ+ (1− c)(Q− 1− gQZ)] + c [Q(1− gZ)− 1] (143)

, V , (144)

which, like X, Y , and Z, is a well defined function of r and s. We thus have ϕV = (Φ/G0)(G0/L) =Φ/L, and we have ϕ in terms of known functions of r and s:

ϕ =(1− f) [Y − 1 + gQ] + (1− f)(1− c) [Q(1− gZ)− 1]− Γ + 1− [f + ck(1− f)]

V.(145)

14Explain.15Is this right?

17

3.4 The equilibrium manifold

So far, we have left one extra degree of freedom in our model, and this means there is a curve, aone-dimensional manifold, in the state space, along which all possible equilibria are constrained tolie.16.

As we shall see later, if the loan rate is shocked, the model economy is knocked off the equilibriummanifold. When the shock is removed, it returns to exactly the same point on the equilibriummanifold. Why? The answer can be found in the fact that net bank assets ϕ(t), and hence thehousehold debt, is a conserved quantity, and fixing ϕ pins down the equilibrium to a unique point.

Remark 2 Household debt ϕ(t) is constant for every t, so long as there is no exogenous injectionor extraction of money. This follows from the fact that the bank sector balances accounts preciselyat the end of every period. The economy will therefore return to the same point on the equilib-rium manifold after state variables or parameters are perturbed, provided, of course, that systemparameters are restored to their original values after the shock.

Figure 3: Illustrating the fact that the system will return to the same equilibrium after statevariables or parameters are perturbed, provided that the parameters are returned to their originalvalues. This is true regardless of how the equilibrium manifold is parameterized, and follows fromthe fact that, with no exogenous injections or extractions of money, household debt is invariant.

This is illustrated diagrammatically in Fig. 3.Household debt will not play an important role in the policy experiments in this paper, and for

simplicity we now stipulate that it is zero, thereby making the equilibrium unique. We then havetwo equilibrium conditions for the two unknowns r and s, the first from Eq. 131, and the secondfrom the assumption that Φ = 0. We collect them here:

s =X − 1

Y − 1 + gQ...Condition 1 , (146)

Φ/L = 0 from Eq. 142 ...Condition 2 . (147)

To calculate equilibria numerically we now need to solve two equations in two unknowns, atwo-dimensional search problem instead of the one-dimensional problem if we choose r. This isa consequence of our choosing Φ instead of r to disambiguate the equilibrium. We found theNelder-Mead search algorithm [13] to be quite effective in this application.

16How is this related, if it is related at all, to the “equilibrium manifold” in [12]?

18

4 Comparative statics

There are several reasons for studying the comparative statics of the Monetary Flow Model proposedhere.

1. They can confirm our intuitive expectations of how equilibrium state variables depend onparameters, thus lending some confidence in the model’s economic realism.

2. They check that the simulations and the equilibrium analysis refer to the same system ofdynamic equations, an aid to debugging.

3. They can provide starting points for simulations, thus saving the time and possible difficultyof arriving at an equilibrium from a cold start.

4. They facilitate calibration.

4.1 Equilibrium r vs. τm, varying f and e

20 40 60 80 100 120 140 160

Loan Window =m

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

Loan

Rat

e r

(%)

f = 0.05f = 0.1f = 0.2

Equil. Loan Rate r vs. Loan Window =m

, for various fEquil. Loan Rate r vs. Loan Window =m

, for various f

Model parameters: e= 500,c=ck= 0.1, -K=-L= 0.5Model parameters: e= 500,c=ck= 0.1, -K=-L= 0.5

Figure 4: Equilibrium r vs. τm for various values of fractional reserve rate f .

19

Loan Window =m

20 40 60 80 100 120 140 160

Nor

mal

ized

Esc

row

, E/G

0

0

2

4

6

8

10

12

14

16

f = 0.05f = 0.1f = 0.2

Equil. Escrow r vs. Loan Window =m

, for various fEquil. Escrow r vs. Loan Window =m

, for various f

Model parameters: e= 500,c=c

k= 0.1, -

K=-

L= 0.5

Model parameters: e= 500,c=c

k= 0.1, -

K=-

L= 0.5

Figure 5: Equilibrium r vs. τm for various values of fractional reserve rate f .

20 40 60 80 100 120 140 160

Loan Window =m

0.2

0.4

0.6

0.8

1

1.2

1.4

Loan

Rat

e r

(%)

e = 250e = 500e = 1000

Equil. Loan Rate r vs. Loan Window =m

, for various e

Model parameters: f = 0.1,c=ck= 0.1, -K=-L= 0.5

Figure 6: Equilibrium r vs. τm for various values of propensity-to-save e.

20

4.2 Loan rate and some other variables vs. fraction of transactions in cash

Fraction of Transactions in Cash0 0.2 0.4 0.6 0.8 1

Per

cent

of M

oney

Sup

ply

250

300

350

400

450Household Wealth, Loans

6.4

6.6

6.8

7

7.2

Per

cent

of W

ealth

Fraction of Transactions in Cash0 0.2 0.4 0.6 0.8 1

Per

cent

0.85

0.9

0.95

1

1.05

1.1

1.15Loan Rate, Savings Rate (--)

Equilibrium Values vs Fraction of Transactions in Cash

Model parameters: f=0.1 e=500 =max

=60 -K

=-L=0.5

Figure 7: Experiment 2 1.

4.3 Loan rate vs. fractional reserve rate

Reserve Rate f0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Loan

Rat

e r

(%)

0

1

2

3

4

5

6

Equil. Loan Rate r vs. reserve rate f

Model parameters: e= 500,c=c

k= 0.1, =

m = 60, -

K=-

L= 0.5

Figure 8: Equilibrium loan rate r vs. fractional reserve rate f for various values of loan window τm.

21

4.4 Various vs. fractional reserve rate

f0 0.5 1

0

2

4

6r,s (%)

f0 0.5 1

0

2

4

6S,C (--)

f0 0.5 1

0

5

10

15E

f0 0.5 1

0

0.2

0.4

0.6L

f0 0.5 1

0

50

100Nc,Nk (--)

f0 0.5 1

0.35

0.4

0.45

0.5Production

r vs. f: c=ck=0.1

Figure 9: Various variables vs. fractional reserve rate f .

22

4.5 Various vs. Propensity-to-Save e

e0 500

0

2

4

6r,s(--) (%)

e0 500

0

2

4S,C(--)

e0 500

4

6

8

10E

e0 500

0.2951

0.2951

0.2951

0.2951L

e0 500

45

50

55Nc,Nk(--)

e0 500

0.498

0.4985

0.499

0.4995Production

Equil. vs. e: c=ck=0

Figure 10: Various variables vs. Propensity-to-Save e, for the case c = ck = 0 (all-credit).

23

e0 500

0

2

4

6r,s(--) (%)

e0 500

0

1

2

3S,C(--)

e0 500

2

4

6

8E

e0 500

0.178

0.179

0.18

0.181L

e0 500

45

50

55Nc,Nk(--)

e0 500

0.4975

0.498

0.4985

0.499Production

Equil. vs. e: c=ck=1

Figure 11: Various variables vs. Propensity-to-Save e, for the case c = ck = 1 (all-cash).

4.6 Calibration

Does this discussion go here?

5 Baseline (no-CB) simulations

5.1 Sticky wages

From now on the results of simulations may include the effects of sticky wages. By this we meanthat both the consumer good and the capital wages are not allowed to drop by more than a givenpercentage in one period, typically 0.1%. When this limit is encountered, the wages are set to theresulting bottom limit. This causes unemployment, plotted along with the numbers of workers, Nc

and Nk, as the variable U .

5.2 A sample simulation of the baseline model (see Appendix)

A baseline simulation showing many variables will be provided by Ben that is consistent with theother simulation plots.

6 Modeling the Central Bank and defaults

Version 07/09/16Mike has the lock to this section and the next (“Policy Experiments”).This needs to be checked against the baseline model and edited to eliminate repetitions.

24

6.1 Model with Central Bank

We now expand on the previous model by introducing injections of new money into the economyby a Central Bank (CB), as well as extractions of cash out of the economy. We also introduce loandefaults and Household loans. The following recursions assume that the CB expands the moneysupply at a fixed rate by injecting an amount of cash equal to a fixed fraction κ of the money supplyeach period through purchases of CG debt. Also, there is a constant default rate δ, which appliesuniformly to all loans. Policy experiments can then be simulated by changing these parameterseither across runs, to examine steady-state behavior17 or within a simulation to study dynamicbehavior.

The model is specified by the following set of recursions. Modifications to the Baseline set ofrecursions, i.e., for estimating the return on savings, and supply and demand for loans are includedthat use additional side information (the loan array) to provide a more accurate prediction of thosevariables in steady-state. In general, these modifications serve to reduce volatility and enhancestability.

Initialization As in the Baseline model, there is an initial distribution of cash among sectors:

Bc(0) = B0, Wcash(0) = W0, G(0) = B0 +Wcash(0) (148)

where Bc(0) is the initial cash, which the Bank keeps as reserves, Wcash(0) is the additional amountof cash in the economy flowing between sectors (or held in the CG sector), and G(0) is the initial(cash) money supply. Savings, Escrow, and total Wealth are initialized as:

S(0) = S0, E(0) = 0, W(0) = S0 +W0, (149)

where W(0) is the total initial wealth consisting of initial savings plus wages. We will assume thatall other variables are initialized at zero unless stated otherwise.

The following iterations for the model state variables are then computed for t = 1, 2, · · · .

Interest rate The update for loan interest rate is

r(t) = max

{0, r(t− 1) + kr

[Dlf (t− 1)− Slf (t− 1)]

G(t− 1)

}(150)

where G(t) is the total cash in the economy (bank cash plus cash flowing among and held byother sectors), which now varies with period t. This is effectively a gradient update for r(t), whichattempts to balance the supply and demand for loanable funds. Other methods for updating r(t)could be used. For example, it is possible to adjust r(t) myopically to balance Slf and Dlf at eachiteration. That, however, can lead to instability unless it is combined with (or replaced by) moresophisticated algorithms for forecasting state variables. While adding such features will certainlyaffect dynamics, they will not change the main results we present here.

Return on Investment It will be convenient to rewrite the expression for measured s(t) in theBaseline model as

s(t) = [L(t− 1)− B(t− 1)]/L(t− 1) (151)

17With CB injections we refer to “steady-state”, as opposed to “equilibrium”, to emphasize that if the systemdoes reach a steady-state, then all state variables representing money flows increase at the injection rate, as opposedto remaining constant. As we later emphasize, the corresponding normalized state variables, relative to the moneysupply, converge to constants in steady-state. Also, as in the Baseline model, we do not include Household debt, sothat a unique steady-state is always observed.

25

where

L(t) = S(t) + E(t) (152)

B(t) = S′(t) + E′(t) (153)

and S′ and E′ are intermediate updates after withdrawals and deposits (see (184)-(185)). Thevariable L(t) represents total liabilities (equivalently assets) owned by the Bank at the end ofthe period, whereas B(t) represents total liabilities (or assets) before interest payments are made.Hence the numerator L(t−1)−B(t−1) is the total return on outstanding loans from the precedingperiod. (The total return is updated in subsection (m), and includes assets left over from defaults,interest on Household debt, and premiums on loans purchased by the Fed.)

Because (151) is a myopic estimate, short-term fluctuations can lead to instability, especiallywhen the denominator is small. Instead we use the following adaptive estimate, which uses infor-mation about the current state, assumed to be known by the Bank:

s(t) = s(t− 1) + ks [RBPI(t− 1)− s(t− 1) · L(t− 1)] /G(t− 1) (154)

where ks is the step-size, RBPI is an expectation of total returns to the bank in steady-state giventhe state variables at time t, including interest on loans from balloon payments and household debt,plus reclaimed credit from defaults. In steady-state s(t) remains constant hence the second termon the right converges to zero. The total return to the bank is then given by

RBPI(t) =LBPI(t− 1)

LBPI(t− 1) + LCBI(t− 1)L(t− 1)

τm∑i=1

wiΠ(t− 1)−i+1(1− δ)i{[1 + r(t)]i − 1}

+ δ · E(t− 1) + pCB(t− 1) (155)

where L(t) is total outstanding loans (owned by both the Bank and the CB), and Π(t) is the“inflation multiplier” (1 + inflation rate in loans), which represents the rate at which loans increasein steady state. The last two terms on the right in (155) are then reclaimed credit from defaultsand pCB, which denotes the total premium on loans, which the CB purchases. (See the discussionin subsection (o).) The remaining (first) term is then the expected return on all outstanding loansto be repaid to the bank. The terms inside the sum include discounts due to defaults and inflation.The fraction preceding L is the fraction of interest repaid to the Bank, relative to the total repaidto the Bank and the CB. In steady state, L(t) = Slf (t), the supply of loanable funds, which equalsDlf (t), the demand for loanable funds. However, in a transient this is no longer true, so that forpurposes of estimating RBPI(t), we take L(t) = [Slf (t) +Dlf (t)]/2.

Household Savings, Consumption As before, Household savings is given by S(t) = g(t)·W(t),where W(t) is total wealth, to be defined (see (202)), and

g(t) =e · s(t)

1 + e · s(t)(156)

where s(t) is the real return on investment, which satisifes 1 + s(t) = [1 + s(t)]/Π(t). The savingsdeposit is then

∆S(t) = g(t) · W(t− 1)− S(t− 1). (157)

Note that ∆S(t) < 0 signifies a withdrawal of savings for consumption.

26

Total Revenue (Consumption) Total revenue received by the CG sector is given by

Rv(t) = C(t) = [1− g(t)] · W(t− 1) + Lh(t), (158)

where C(t) is total Household consumption and Lh(t) is loans to the Household sector. (In steady-state, Lh(t) = 0 and the Household credit revolves.) All Household loans are assumed to be spenton consumption.

The cash portions of the total amounts spent on consumption and deposited by Households aregiven by

Cc(t) = c · C(t) (159)

C(t) = Wcash(t− 1) + ck · Lh(t− 1)− Cc(t) (160)

where c and ck are constants (system parameters). That is, the fraction of cash spent on consump-tion can be different from the fraction of cash making up loans, although the numerical examples,to be presented, will assume c = ck.

Inflation The update (155) depends on Π(t), which is the rate of increase of loans. Similarly, theupdate for Dlf (t) will depend on the rate at which CG revenue increases. In steady state, the rateof increase for loans and revenue will be the same, which will be the same as the rate of increasein the price of CG goods (total revenue divided by quantity purchased) and wages (total amountspent on Labor divided by the number of Households). Although these inflation rates will generallybe different outside of steady state, for simplicity we will estimate a single “inflation rate” as therate at which revenue (consumption) increases. This is due to the central role this variable plays inestimating Dlf (t), and the observation that the inflation rate for loans tends to track the inflationrate for revenue. We also note that wage and price inflation is a direct consequence of the inflationin total wages and revenue, and in that sense plays a secondary role in understanding the modelbehavior. (This is ultimately because Dlf is a fixed fraction of total revenue.)

The inflation rate can be estimated by smoothing the log-revenue:

Rv(t) = logRv(t) (161)

∆R(t) = Rv(t)− Rv(t− 1) (162)

∆rev(t) = (1− krev)∆rev(t− 1) + krev∆R(t) (163)

Rv(t) = (1− krev)[Rv(t− 1) + ∆rev(t)] + krevRv(t) (164)

Π(t) = exp{∆rev(t)} (165)

An initial positive estimate of the revenue is needed to start the recursions. We remark that insome scenarios shocks combined with this inflation estimator can lead to short-term instability. Al-ternatively, the estimate can be determined from the actual rate of cash injections by the CB. Thatassumes households and CG have access to this information and forecast the effects by applying asmoothing filter.

Loan defaults If a loan defaults, then that loan is deducted from the corresponding value of theloan array L(τ, t− i; t), where τ is the loan term, and t− i is the time at which the loan was made.We have added dependence on t, since with defaults existing elements of the loan array can changeover time. Here we also have a loan array for loans owned by the CB, LCB(τ, t− i; t). In aggregatewe will assume that a fraction δ of all loans default so that

L′(τ, t− i; t) = (1− δ)L(τ, t− i; t− 1) (166)

L′CB(τ, t− i; t) = (1− δ)LCB(τ, t− i; t− 1) (167)

27

for each i = 1, 2, · · · , τ and τ = 1, · · · , τm. We define the intermediate variables L′ and L′CBsince the loan arrays will be subsequently modified due to the purchase of loans by the CB. (Seesubsection (o).) In general, δ could depend on i and τ ; however, for simplicity, we will assumethat defaults occur uniformly over all elements of the loan array. Since a loan can default at anarbitrary time within the duration of the loan, it is assumed that the CG sector makes escrowpayments up until the time of default. The bank then seizes the escrow account and returns whathas accumulated in that account to the Households and back to Escrow.

Here we assume that loans default at a constant rate δ. That is, at each iteration a fraction δ ofall loans default. With this assumption the aggregate amount left in escrow from loans that defaulteach iteration is δ · E(t). The return on Household savings then includes the balloon repaymentsfor all non-defaulting loans plus δ · E(t), as shown in (151).

Escrow deposit (capital expenditures) This is computed as before. Namely, the targetamount in escrow, and the escrow deposit are, respectively,

Etar(t) =

τm∑τ=1

τ∑i=1

wτL(τ, t− i; t) · [1 + s(t− i)]i − 1

[1 + s(t− i)]τ − 1[1 + r(t− i)]τ (168)

∆E(t) = Etar(t)− E(t− 1) (169)

and the cash portion of the escrow deposit is

∆Ec(t) = c ·∆E(t) (170)

Loan (balloon) repayments With CB injections loans are split between the two loan arraysL(τ, t− i; t) and LCB(τ, t− i; t). Loan repayments to the Bank are the same as before,

LBP (t) =

τm∑τ=1

[1 + r(t− τ)]τ · L′(τ, t− τ ; t) (171)

LBPI(t) =

τm∑τ=1

{[1 + r(t− τ)]τ − 1} · L′(τ, t− τ ; t) (172)

where LBP (t) is the total amount of loan repayments, and LBPI(t) is the corresponding interest.Similarly, loan (balloon) repayments for CB-owned loans are given by

LCBP (t) =

τm∑τ=1

[1 + r(t− τ)]τ · L′CB(τ, t− τ ; t) (173)

LCBI(t) =

τm∑τ=1

{[1 + r(t− τ)]τ − 1} · L′CB(τ, t− τ ; t) (174)

where LCBP (t) is the total repayment and LCBI(t) is the corresponding interest. The loans arepaid back to the CB in cash, reflecting the fact that the CB may attempt to control the amount ofcash reserves in the economy. Also, we assume that CG pays the CB out of current revenues, sodoes not keep an escrow account for loan repayments to the CB. This corresponds to the scenariowhere the CB buys government debt (here included in total CG debt), and loan repayments comefrom current tax revenues. Since the revenue contains a mix of cash and credit (according to theparameters), the CB cashes in the credit part, which is removed from Bank reserves. The fractionsof the principal and interest to be paid back to the CB are, respectively, ζP and ζI so that the cashflow to the CB is given by

Bout(t) = ζP · LCBP (t) + ζI · LCBI(t). (175)

28

Target capital expenditures, demand for loans As before, target capital expenditures aredetermined by minimizing the combined labor plus capital cost to produce a given output. For theCobb-Douglas production function this gives

Ktar(t) = h ·Rv(t) (176)

where h = βk/(βk + βl). The demand for loans Dlf (t) is then set so that the expected capitalexpenditures per iteration (escrow deposits plus repayments to the CB) in steady state is Ktar(t),assuming that Dlf (t) is in fact the amount of loans made in steady state.

In contrast to the scenario without a CB, here we have to distinguish three types of loans: (1)CG loans with escrow accounts (as before), (2) loans owned by the CB, which are paid back outof current revenues, and (3) loans owned by the CB, which are not paid back. Letting Λ(t) =LBP (t) + LCBP (t) + LCBI(t) be the total amount of loan repayments to both the bank and theCB, the fractions of loans in each of these categories, are, respectively,

a1 =LBP (t)

Λ(t)a2 =

Bout(t)

Λ(t)a3 =

LCBP (t) + LCBI(t)−Bout(t)Λ(t)

(177)

For category (1), a unit loan taken out each iteration in steady state results in an escrow depositgiven by

du,1(t) =

τm∑τ=τmin

τ∑i=1

wτP (r, s, τ)Π−i(t− 1) (178)

where wτ is the fraction of loans with duration τ , and P (r, s, τ) is the escrow payment for a unitloan of duration τ made at interest rate r and return on investment s, as derived in Section ??.For category (2), a unit loan taken out each iteration in steady state results in loan repayments tothe CB given by

du,2(t) =

τm∑τ=1

wτ [1 + r(t− τ)]τ . (179)

Loans in category (3) are not included in the computation of Dlf (t).The demand for loans is then

Dlf (t) = Ktar(t)/[a1 · du,1(t) + a2 · du,2(t)] (180)

Strictly speaking, this should apply only in steady state; however, we will assume that the CGsector always has access to the corresponding amounts of loan repayments, and computes Dlf inthe same way even outside of steady state.18

Comment: point out earlier that firms could subtract interest from revenue, and split theremainder, which would maximize production. That would increase production, but severs theconnection between time preference, deferred consumption, and investment. Hence the increasedproduction should not be sustainable in steady-state causing additional defaults.

CG wages, unspent capital budget These remain the same as before, namely

Wc(t) = min{[βl/(βc + βl)] ·Rv(t), Rv(t)−∆E(t)−Bout(t)}. (181)

The first term is the target wages, which is paid unless the capital expenditures ∆E(t) + Bout(t)exceed its corresponding target βc/(βc +βl) ·Rv(t). In the latter case, wages are what remain afterthe CG sector makes its loan payments. If the second term is larger than the first, meaning capital

18In practice, the loan amounts in (177) would likely be smoothed and forecasted.

29

expenditures are below the corresponding target, then CG retains an additional (unspent) amountfor capital:

Ucg(t) = Rv(t)−∆E(t)−Wc(t)−Bout(t). (182)

We assume that the CG sector uses this to purchase additional capital directly, so that this amountis added to capital wages (see (200)). Of course, in steady state Ucg(t) = 0.19

Bank cash The updated bank cash accounts for loans made at the preceding iteration, savingswithdrawals, and escrow deposits,

B′c(t) = [Bc(t− 1)− ckL(t− 1) + ∆C(t) + ∆Ec(t)]+ . (183)

This assumes that none of the cash reserves are needed to repay CB-owned loans. That is, there isenough revenue to cover those repayments, or if not, then the CB allows those loans to default.

Bank assets, updated Savings, Escrow The total bank assets after loan repayments areallocated to Savings and Escrow. This is done in proportion to the size of the Savings and Escrowaccounts, since it can be viewed as a return on investment. The following intermediate variablesare introduced, which are updated Savings and Escrow:

S′(t) = S(t− 1) + ∆S(t) (184)

E′(t) = (1− δ) · E(t− 1) + ∆E(t)− LBP (t). (185)

Total Bank liabilities are then given by (153). This is the same as the Baseline model, but nowdefaults are subtracted from Escrow, which is a reduction of bank liabilities. The banks seize whatit is in those defaulted accounts, and add those to Bank assets, which are distributed proportionallyacross the updated Savings and Escrow accounts.

Since all repayments to the CB are taken from the current revenue stream, the loan repaymentsfrom Escrow, LBP , do not include loans owned by the CB. Note that in practice the bank willown additional government bonds for which no escrow is kept. That is, here we are assuming thatescrow is kept only for bank-owned loans, and ignore the fact that there are many loans to thecombined CG-government sector for which no escrow accounts would be held.

Defaults on the bank assets side are subtracted from the total amount of loans owned by theBank at time t, Ltot(t) (see (199)), and affect both Savings and Escrow. Note that this does notchange the bank balance (assets less liabilities) since total assets are distributed across Savings andEscrow accounts as liabilities. In what follows, L(t) = S(t) +E(t) denotes total bank liabilities forSavings and Escrow only, and does not include liabilities for the credit part of wages. Collectingthose liabilities and allocating proportionally across Savings and Escrow gives

L(t) = B(t) + LBPI(t)− δ · Ltot(t− 1) + δ · E(t− 1) + pCB(t− 1) (186)

S(t) = L(t)S′(t)

B(t), E(t) = L(t)

E′(t)

B(t)(187)

Note that these updates do not include loans owned by the CB. Any CB-owned loans thatdefault are simply not repaid, i.e., reduce the value of Bout in (175), resulting in an effective gift tothe CG sector. The defaults are therefore combined with government bonds, which are not repaidfrom revenue streams; rather the treasury prints the money and transfers it directly to the CB.

19It is possible that in a transient scenario, ∆E(t) + Bout(t) > Rv(t) in which case the CG sector goes bankruptand the program stops. The economy can subsequently be restarted by defaulting on loans or by having the CBinject cash.

30

CB injections, Supply of loans The CB is assumed to inject cash into the economy at a fixedrate by purchasing a constant fraction of CG debt each iteration. The amount injected, moneysupply, and bank cash are given by

F (t) = κ ·G(t− 1), G(t) = G(t− 1) + F (t) (188)

Bc(t) = B′c(t) + F (t) (189)

As before (without CB injections), the supply of loans is then given by

Slf (t) =1

f + ck(1− f){Bc(t)− f · [L(t) + (1− c)Wc(t)]}. (190)

This is a myopic estimate, which does not take into account side information the Bank may have.We can include information about the existing loan array to obtain an alternative estimate of Slfthat is expected in steady-state, given current state variables, and hence more forward-looking.Specifically, we note that L(t) + (1− c)Wc(t), which appears in (190), is total bank liabilities, andcan be replaced by total bank assets given by Bc(t) plus total outstanding loans. The latter is thesum of all loans in the CG loan array (excluding CB-owned loans), which in steady-state at time tis the total amount of loans made at time t times the multiplier

Γ(t) =

τm∑τ=1

τ−1∑i=1

wi[1− δ(t)]iΠ−i(t)[1− η(t)]i (191)

where η(t) is the fraction of loans bought by the CB (see (194)). That is, total loans are reducedby the default rate across the loan array, the inflation rate, and the fraction of loans transferred tothe CB. Also, we exclude loans that are paid back during the current period. Finally, in steady-state loans per period at time t are given by Slf (t). Including Γ(t) · Slf (t) in total Bank assets,substituting in (190) and solving for Slf (t) gives

Slf (t) =(1− f) ·Bc(t)

f + ck(1− f) + f · Γ(t). (192)

This is equivalent to (190) in steady-state, but is less volatile during transients.

Fraction of loans bought by CB For simplicity we assume that the CB purchases a fixedfraction of all CG loans. Let π(τ, t − i; t) denote the amount paid for loans L(τ, t − i; t). Wedetermine π(τ, t − i; t) by setting the amount accumulated for the remainder of the loan durationτ − i at interest r(t) equal to the balloon payment of the original loan:

[1 + r(t)]τ−iπ(τ, t− i; t) = [1 + r(t− i)]τL(τ, t− i; t) (193)

for i < τ . (We assume that the CB only purchases loans that expire after time t.) Given that theCB wishes to spend a total of F (t), the fraction of loans it buys is then

η(t) = F (t)/

[τm∑τ=1

τ−1∑i=1

π(τ, t− i− 1; t)

](194)

where π(τ, t− i; t) is given by (193). The new loans purchased by the CB are then transferred fromthe CG loan array to the CB loan array:

L(τ, t− i; t) = [1− η(t)]L′(τ, t− i; t) (195)

LCB(τ, t− i; t) = L′CB(τ, t− i; t) + η(t) · L′(τ, t− i; t) (196)

31

for τ = 1, · · · , τm and i = 1, · · · , τ − 1.The difference π(τ, t− i; t)− L(τ, t− i; t) is the premium the CB pays for purchasing the loans

corresponding to L(τ, t− i; t). Hence the total premium amount the CB pays at iteration t is

pCB(t) =

τm∑τ=1

τ−1∑i=1

η(t)[π(τ, t− i; t)− L′(τ, t− i; t)]. (197)

This is included as part of the return on investment in (155).20

CG Loans The amount of loans at period t is

L(t) = min{Slf (t), Dlf (t)}. (198)

The total amount of outstanding loans, excluding those owned by the CB, is

Ltot(t) =

τm∑τ=1

τ∑i=1

L(τ, t− i; t). (199)

This is needed to compute the total amount of defaults at the next iteration. (See (186).)

Wages and total Wealth As before, loans are passed through the Capital sector as wages, sothat total capital wages are

Wk(t) = L(t) + Ucg(t). (200)

The cash portion of wages is

Wcash(t) = ckWk(t) + c ·Wc(t) + c · Ucg(t) (201)

since ck determines the cash portion of loans. Total wealth is then given by

W(t) = Wc(t) +Wk(t) + S(t). (202)

Unemployment Unemployment again arises from the downward friction in wage-prices. **fillin details**

The labor-capital split and GDP are computed as before...

6.2 Illustrative Experiments

We now show a series of plots that illustrate some basic features of credit expansion and contractionassociated with the model. We begin by discussing the choice of system parameters used to generatethe plots, and subsequently show four sets of plots that are organized according to the main resultsdiscussed in Section 1.2.

6.3 Model Parameters

Our intent in this section is to show a representative set of experiments that illustrate some basicproperties exhibited by the model. While there is a range of parameters that could be selected, wehave chosen parameters that may correspond to a “reasonable” set of state variables (e.g., a loaninterest rate in the range of 0.5 to 1% per period). Unless specified otherwise, the plots assume theparameters shown in Table 1. The parameters above the double line are sufficient to determine theequilibrium and steady-state values, whereas the parameters below the double line affect dynamics

20We assume that F (t) never exceeds the entire amount of CG loans.

32

f = 10% fractional reserve requiremente = 500 propensity to saveτm = 60 maximum loan durationw(τ) = 1/τm, τ = 1, · · · , τm loan window distributionc = ck = 0 cash fraction of loans, consumption (all-credit model)βK = 0.5, βL = 0.5 return on capital, return on laborκ = 0.005 CB injection rate (fraction of money supply) (189)

kr = ... step-size for loan rateks = ... step-size for return on investmentki = ... step-size for inflation estimate

Table 1: Default parameters used to generate the results in Section 6.2.

(transients). Changing the latter set of parameters can speed up or slow down transients, and muteor enhance transient swings in state variables due to shocks. As previously discussed, selection ofthose parameters has a critical effect on the duration of transients and stability. However, inpractice the dominant influence on transient dynamics would likely be driven by traders in thefinancial sector, not modeled here. As for the baseline model, the duration of a single time periodis linked to the interpretation of loan durations. If we assume a maximum loan duration of fiveyears (after which the loans are possibly rolled over, or traded?**) then taking τm = 60 means thatthe each period represents approximately one month.

6.4 Transient and Steady-State Effects of Central Bank Injections

Figure 12 shows the effects of injections by the CB. The CB injects money by buying outstandingCG sector debt from the Bank sector at at period 400 after the system reaches an initial equilibrium.Thereafter, each period the amount of loans purchased by the CB is equal to 0.5% of the currentmoney supply. In this set of plots, the CB does not require repayments from the CG sector on theloans it purchases so that the cash it injects adds to the existing money supply and never leavesthe economy. (The next figure illustrates what happens when the loans are paid back to the CB.)As a consequence, as shown in the first (upper left) plot, both the amount of cash injected perperiod (amount shown on the left) and the money supply (amount shown on the right) increaseexponentially.

The top right plot shows both nominal and real loan interest rates. The real interest rate is thenominal rate minus the estimated inflation rate.21 The CB injections create a transient in whichthe nominal rate increases and the real interest rate decreases relative to the initial equilibriumrate. The system reaches a steady-state in which the nominal and real interest rates each convergeto their final values, different from the preceding equilibrium value. Hence this figure indicates thatthe CB injections have a real effect on the economy even in steady-state. This is further illustratedin the lower left plot, which shows the allocation of total labor capacity to the K and CG sectors.The decrease in the real interest rate makes capital less expensive, so the CG demand for capitalincreases. That increases the flow of total wages into the K sector relative to the flow of wagesgoing to the CG sector, which causes laborers to shift from the CG sector to the K sector. Thisshift in turn causes a slight increase in production, as shown in the lower right plot. The increasein K production also shown in the figure is more pronounced than that for CG, since it is moredirectly influenced by the labor shift. The relative insensitivity of CG production shown in thisexample (and the other examples in this section) is partially due to the choice of parameters22, and

21In all plots with CB injections the inflation estimate Π(t) is taken to be a smoothed version of the actual rateof CB injections. In steady-state the estimated inflation rate converges to the actual injection rate.

22Decreasing the propensity to save e would accentuate the shift in labor-capital split, but would also significantly

33

also due to the restrictive nature of the assumed Cobb-Douglas production function with constantreturns to scale.

The rise in nominal rate shown in the top right plot is due to inflation expectations. Thatis, demand for loanable funds Dlf (t) accounts for the anticipated rise in revenues due to theCB injections. (Recall that Dlf (t) is determined by the CG sector so that capital expendituresper iteration (escrow deposits) are a constant pre-determined fraction of revenue.) However, theincrease in nominal rate from the preceding equilibrium value is less than the inflation rate, causinga drop in the real interest rate. In other words, if the real interest rate were held constant, thenwhen injections commence, the supply of loanable funds Slf (t) would exceed Dlf (t). The reasonfor this is that the CB injections effectively discount the loan obligations held as liabilities by theBank, providing more room for the Bank to expand credit.