Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

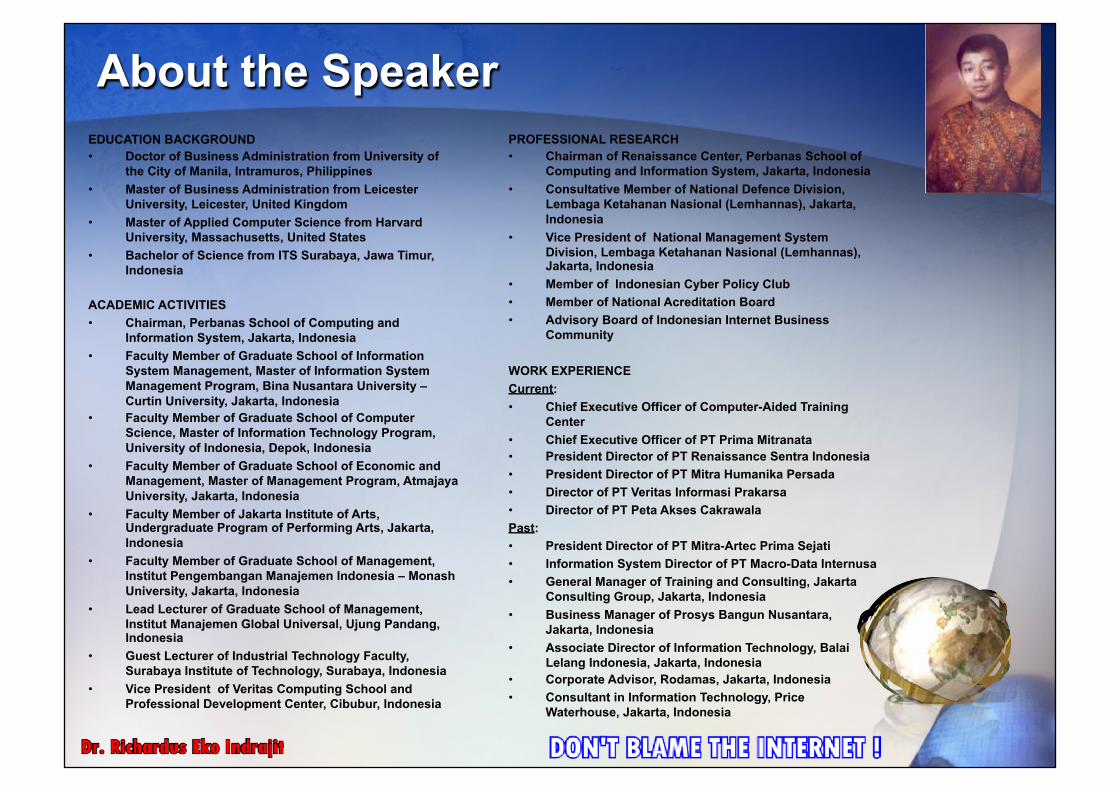

About the Speaker EDUCATION BACKGROUND Doctor of Business Administration from University of

the City of Manila, Intramuros, Philippines Master of Business Administration from Leicester

University, Leicester, United Kingdom Master of Applied Computer Science from Harvard

University, Massachusetts, United States Bachelor of Science from ITS Surabaya, Jawa Timur,

Indonesia ACADEMIC ACTIVITIES Chairman, Perbanas School of Computing and

Information System, Jakarta, Indonesia Faculty Member of Graduate School of Information

System Management, Master of Information System Management Program, Bina Nusantara University – Curtin University, Jakarta, Indonesia

Faculty Member of Graduate School of Computer Science, Master of Information Technology Program, University of Indonesia, Depok, Indonesia

Faculty Member of Graduate School of Economic and Management, Master of Management Program, Atmajaya University, Jakarta, Indonesia

Faculty Member of Jakarta Institute of Arts, Undergraduate Program of Performing Arts, Jakarta, Indonesia

Faculty Member of Graduate School of Management, Institut Pengembangan Manajemen Indonesia – Monash University, Jakarta, Indonesia

Lead Lecturer of Graduate School of Management, Institut Manajemen Global Universal, Ujung Pandang, Indonesia

Guest Lecturer of Industrial Technology Faculty, Surabaya Institute of Technology, Surabaya, Indonesia

Vice President of Veritas Computing School and Professional Development Center, Cibubur, Indonesia

PROFESSIONAL RESEARCH Chairman of Renaissance Center, Perbanas School of

Computing and Information System, Jakarta, Indonesia Consultative Member of National Defence Division,

Lembaga Ketahanan Nasional (Lemhannas), Jakarta, Indonesia

Vice President of National Management System Division, Lembaga Ketahanan Nasional (Lemhannas), Jakarta, Indonesia

Member of Indonesian Cyber Policy Club Member of National Acreditation Board Advisory Board of Indonesian Internet Business

Community

WORK EXPERIENCE Current: Chief Executive Officer of Computer-Aided Training

Center Chief Executive Officer of PT Prima Mitranata President Director of PT Renaissance Sentra Indonesia President Director of PT Mitra Humanika Persada Director of PT Veritas Informasi Prakarsa Director of PT Peta Akses Cakrawala

Past: President Director of PT Mitra-Artec Prima Sejati Information System Director of PT Macro-Data Internusa General Manager of Training and Consulting, Jakarta

Consulting Group, Jakarta, Indonesia Business Manager of Prosys Bangun Nusantara,

Jakarta, Indonesia Associate Director of Information Technology, Balai

Lelang Indonesia, Jakarta, Indonesia Corporate Advisor, Rodamas, Jakarta, Indonesia Consultant in Information Technology, Price

Waterhouse, Jakarta, Indonesia

Agenda for Today

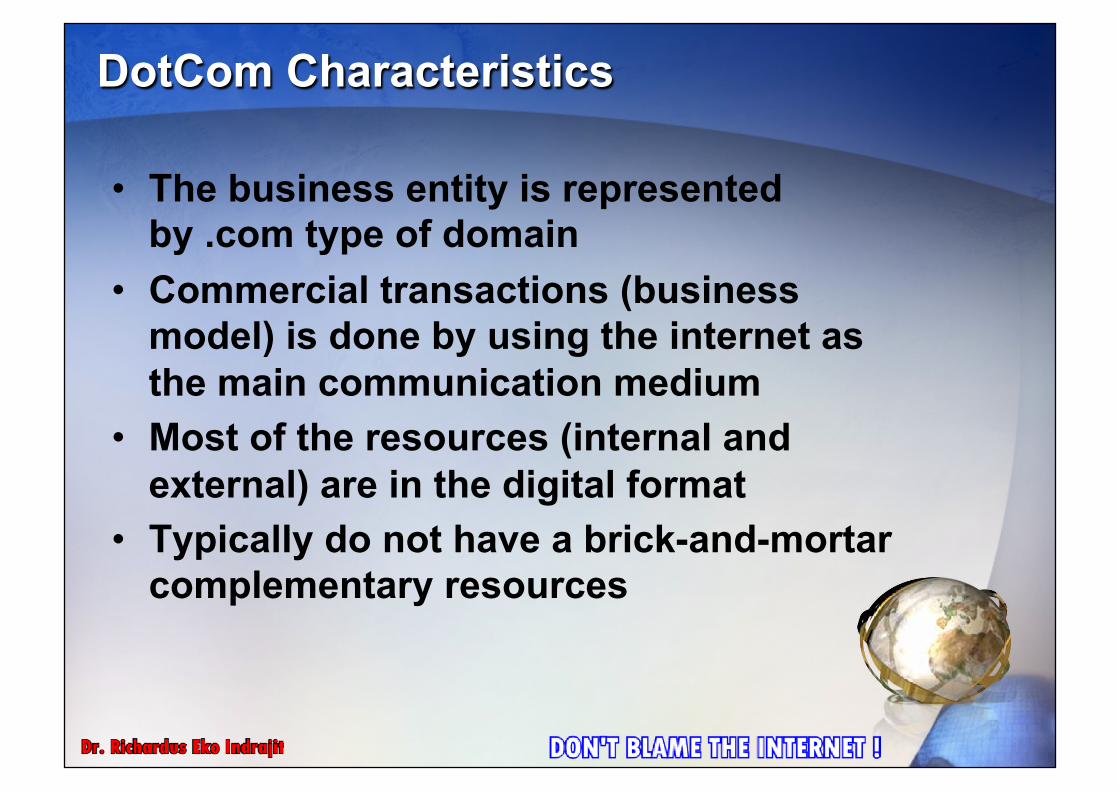

DotCom Characteristics

The business entity is represented by .com type of domain Commercial transactions (business

model) is done by using the internet as the main communication medium Most of the resources (internal and

external) are in the digital format Typically do not have a brick-and-mortar

complementary resources

2000 – The DotCom Bubble Bursts !

The Demise of Dot Com Retailers. Weak financials, intense competition, and investor flight will drive many of today's online retailers out of business in 2000. Those that survive must refocus funding on building hard assets to achieve scale, service, and speed.

Wall Street will run out of patience. Financial markets exasperated with non-existent online profits will turn a deaf ear to persistent "investment mode" rhetoric and soundly punish merchants who bleed red ink. Recent stock disasters like Value America and eToys -- whose market caps as of January 11, 2000, are down $3.1 billion and $7.7 billion respectively from 1999 highs -- serve as bad omens for online stores that lack a unique approach or technology.

The revenge of the brick-and-mortars will begin. The narrowing of the playing field in 2000 will rationalize but not resolve online retail competition. It will usher in a new era characterized by a few large players that exploit deep customer relationships and a presence across multiple channels to entrench themselves. To measure their success, these firms will ditch new economy platitudes in favor of unfashionable old metrics like margins, profits, and customer retention costs.

Forrester Research, 1999-2000

Four Models of Internet Usage

Corporate Enhancement Old Company plus Internet

DotCom

Start from Scratch in Internet Extended Supply Chain

Upstream Connection through Internet (Suppliers) Customer Relationship

Downstream Connection through Internet (Customers)

1

2

3

4

The Hype Cycle of Global eBusiness

IT in the Crossroads

Where are we ? – The end of the beginning – Technology more advanced than application – Transformative critical mass

Where are we going ? – A future with greater choice and higher expectations – A future increasingly interdependent – A future clouded in unpredictability

How do we get there ? – Best business practices – Leveraging resources – Delivering value to customers

Forecasting is a tricky business…

The Increasing Trend

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

198919901991199219931994199519961997199819992000200120022003200420052006

hosts mobiles?

Mobile Solutions Spending by Government

0

500

1,000

1,500

2,000

2,500

2000 2001 2002 2003 2004 2005Year

($M

) GovernmentIndustry Average

Non-Stop Technology

The Challenge…

The Everywhere Use of the Technology

The Lifestyle

Ten Emerging Technology…

The Ongoing Research…

Very Long-Range Factors

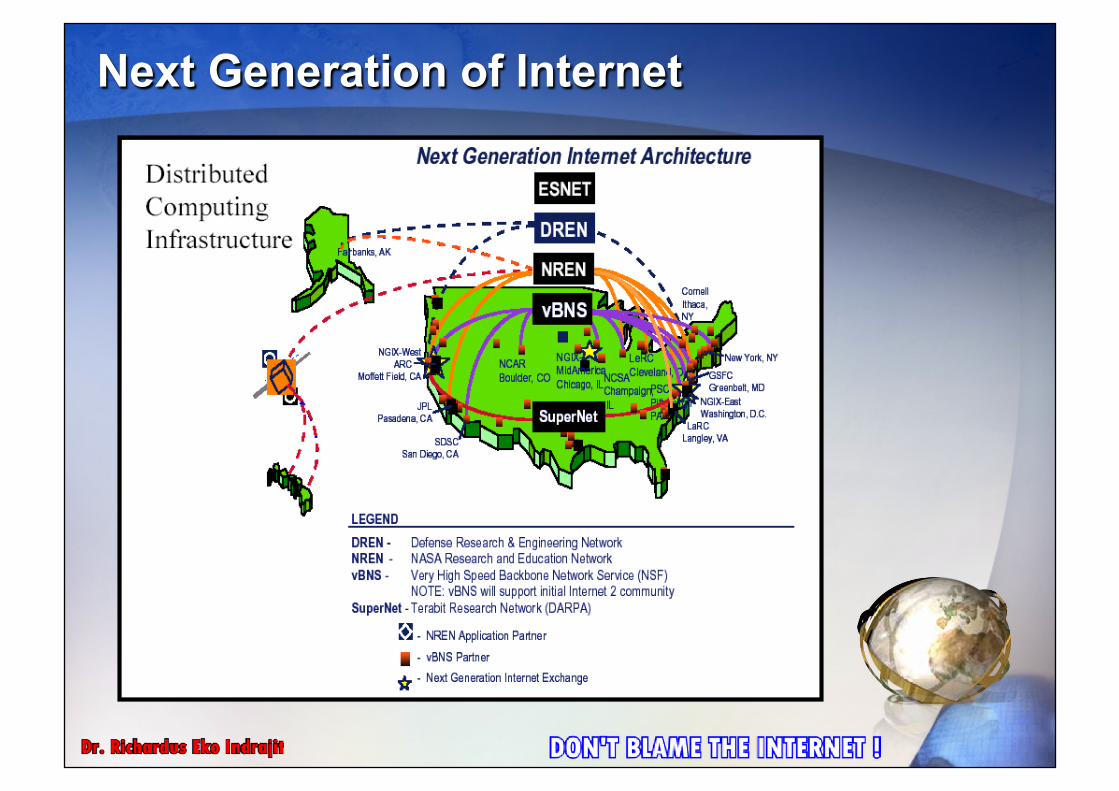

Next Generation of Internet

The Requirements…

Beyond the Earth…

+

+

+

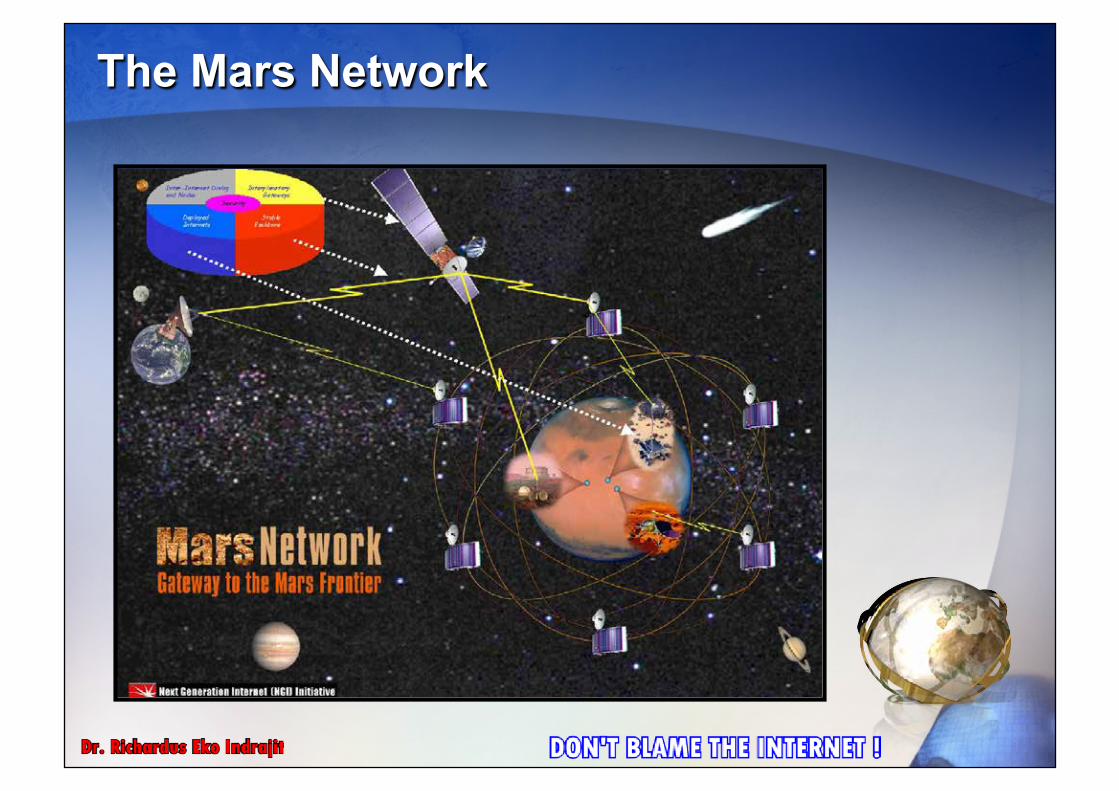

The Mars Network

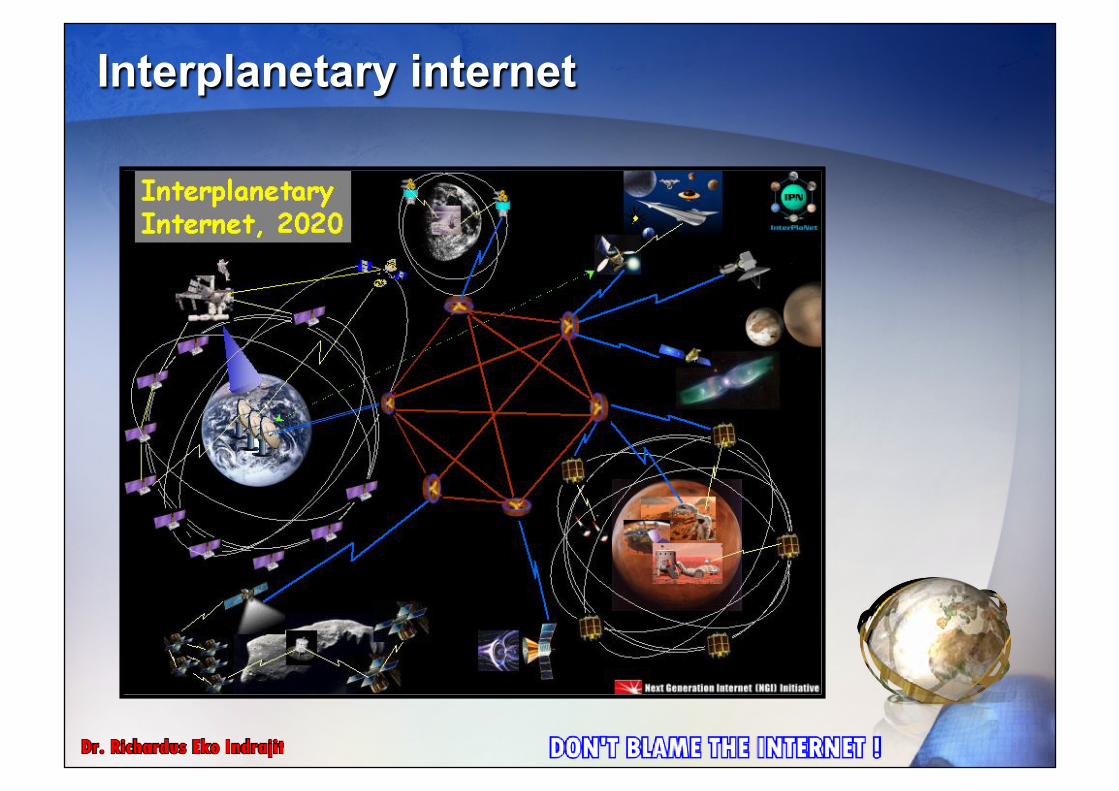

Interplanetary internet

Future Technology Enablers

DNA Computing

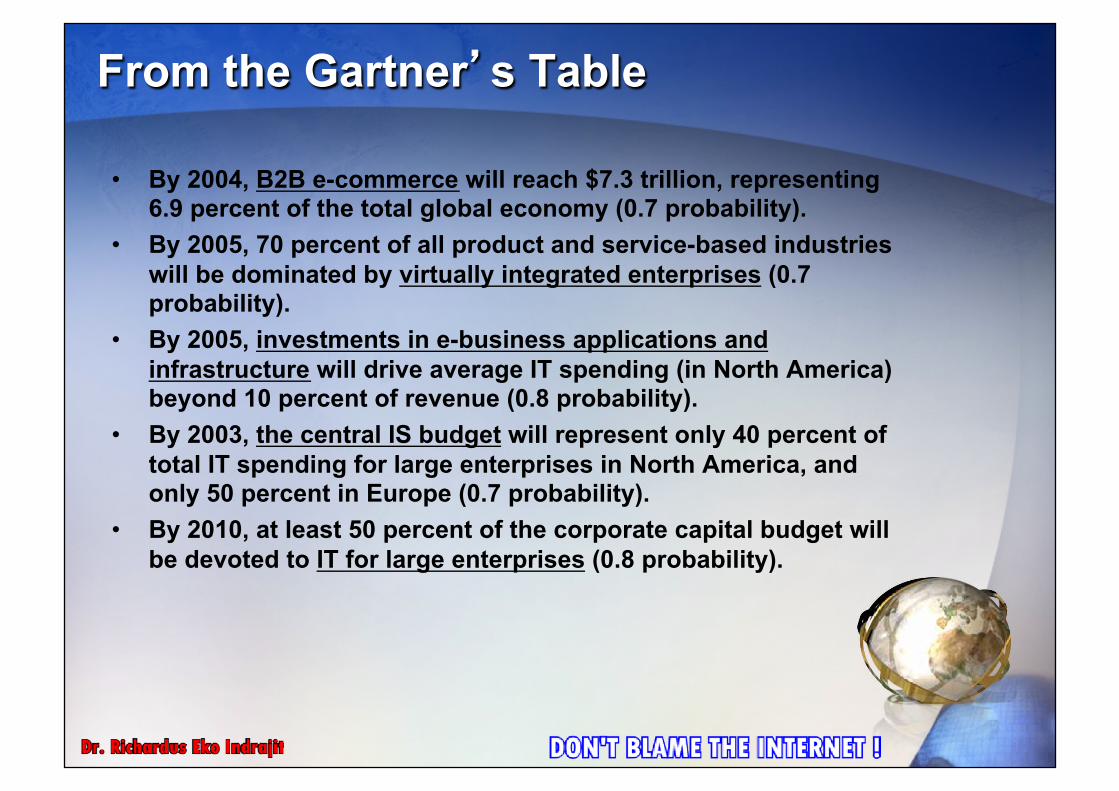

From the Gartner’’s Table

By 2004, B2B e-commerce will reach $7.3 trillion, representing 6.9 percent of the total global economy (0.7 probability).

By 2005, 70 percent of all product and service-based industries will be dominated by virtually integrated enterprises (0.7 probability).

By 2005, investments in e-business applications and infrastructure will drive average IT spending (in North America) beyond 10 percent of revenue (0.8 probability).

By 2003, the central IS budget will represent only 40 percent of total IT spending for large enterprises in North America, and only 50 percent in Europe (0.7 probability).

By 2010, at least 50 percent of the corporate capital budget will be devoted to IT for large enterprises (0.8 probability).

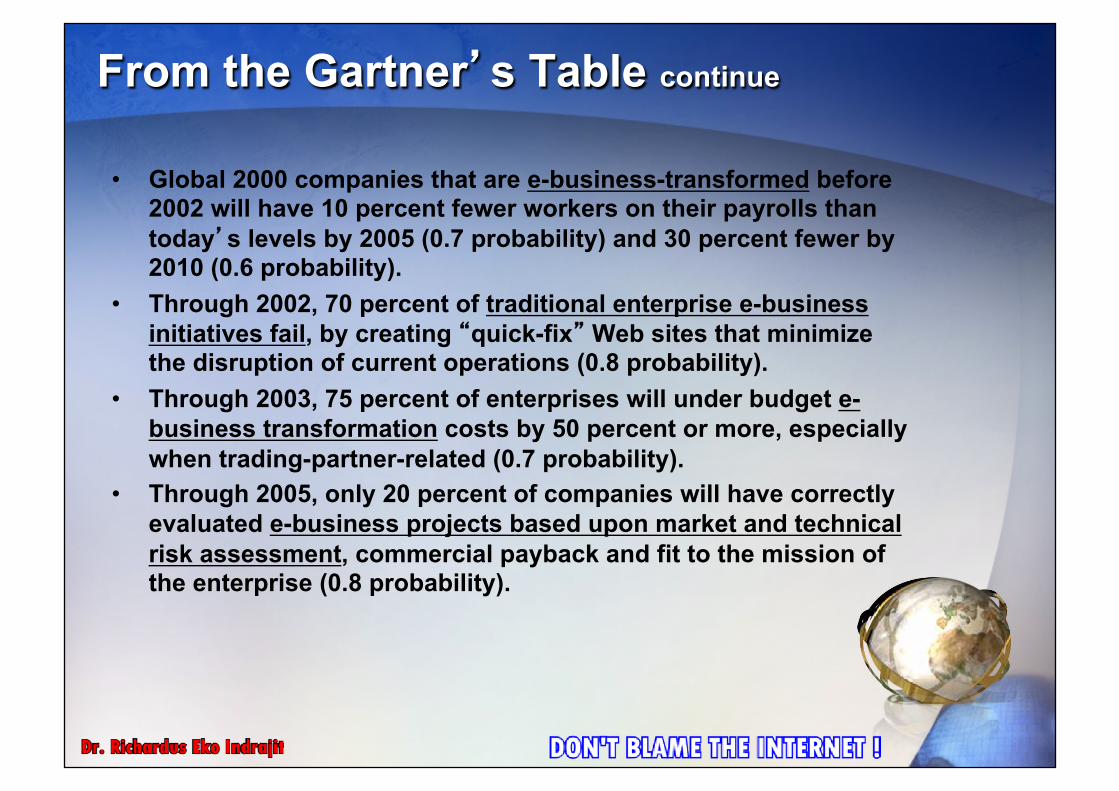

From the Gartner’’s Table continue

Global 2000 companies that are e-business-transformed before 2002 will have 10 percent fewer workers on their payrolls than today’’s levels by 2005 (0.7 probability) and 30 percent fewer by 2010 (0.6 probability).

Through 2002, 70 percent of traditional enterprise e-business initiatives fail, by creating ““quick-fix”” Web sites that minimize the disruption of current operations (0.8 probability).

Through 2003, 75 percent of enterprises will under budget e-business transformation costs by 50 percent or more, especially when trading-partner-related (0.7 probability).

Through 2005, only 20 percent of companies will have correctly evaluated e-business projects based upon market and technical risk assessment, commercial payback and fit to the mission of the enterprise (0.8 probability).

From the Gartner’’s Table continue

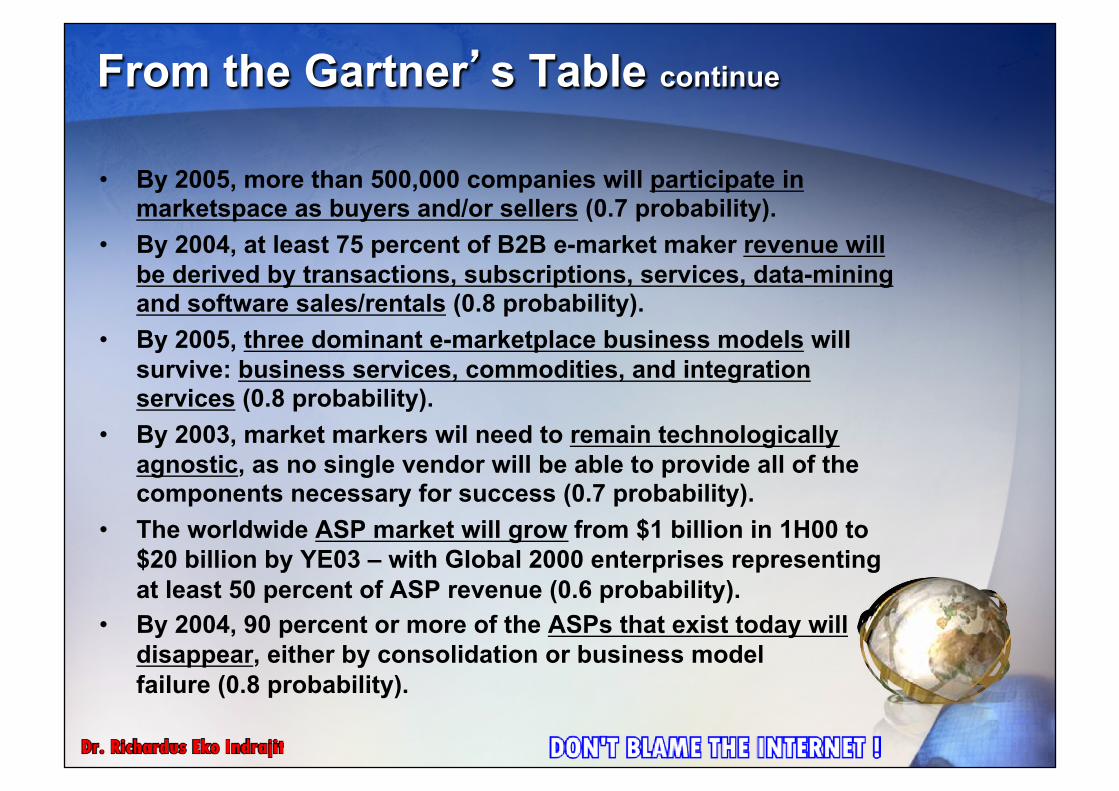

By 2005, more than 500,000 companies will participate in marketspace as buyers and/or sellers (0.7 probability).

By 2004, at least 75 percent of B2B e-market maker revenue will be derived by transactions, subscriptions, services, data-mining and software sales/rentals (0.8 probability).

By 2005, three dominant e-marketplace business models will survive: business services, commodities, and integration services (0.8 probability).

By 2003, market markers wil need to remain technologically agnostic, as no single vendor will be able to provide all of the components necessary for success (0.7 probability).

The worldwide ASP market will grow from $1 billion in 1H00 to $20 billion by YE03 – with Global 2000 enterprises representing at least 50 percent of ASP revenue (0.6 probability).

By 2004, 90 percent or more of the ASPs that exist today will disappear, either by consolidation or business model failure (0.8 probability).

From the Gartner’’s Table continue

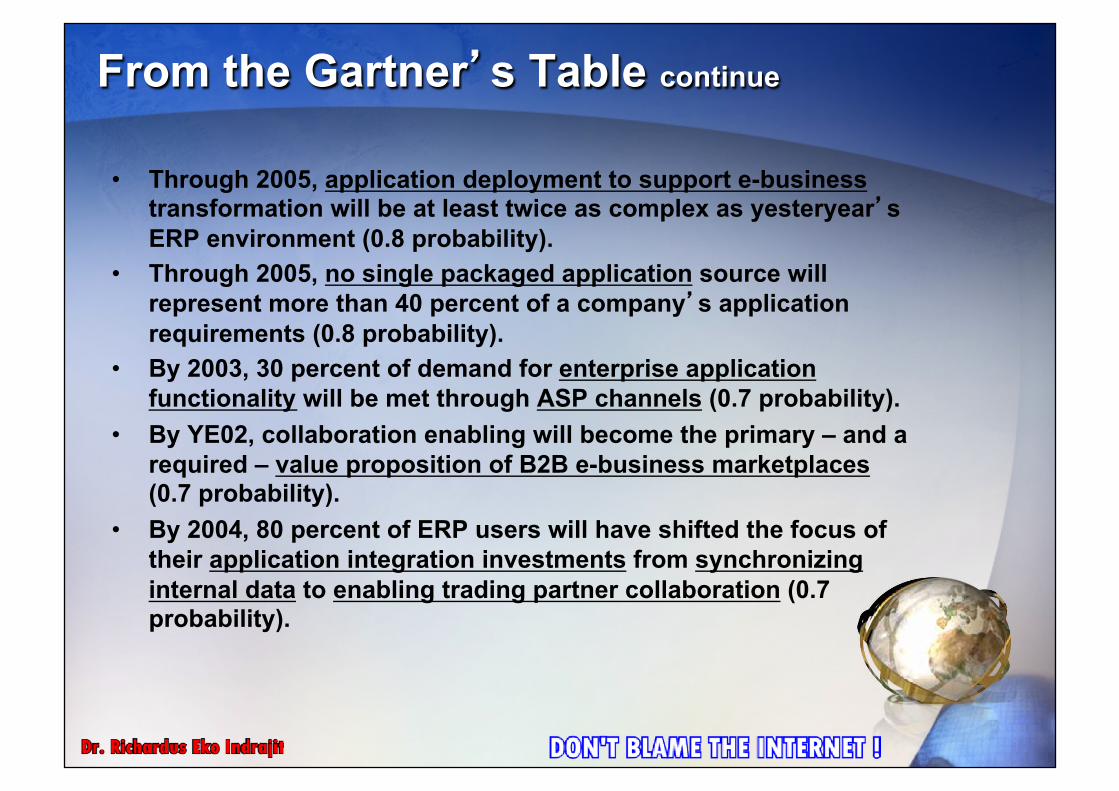

Through 2005, application deployment to support e-business transformation will be at least twice as complex as yesteryear’’s ERP environment (0.8 probability).

Through 2005, no single packaged application source will represent more than 40 percent of a company’’s application requirements (0.8 probability).

By 2003, 30 percent of demand for enterprise application functionality will be met through ASP channels (0.7 probability).

By YE02, collaboration enabling will become the primary – and a required – value proposition of B2B e-business marketplaces (0.7 probability).

By 2004, 80 percent of ERP users will have shifted the focus of their application integration investments from synchronizing internal data to enabling trading partner collaboration (0.7 probability).

From the Gartner’’s Table continue

By 2003, 50 percent of e-business project initiatives will be based upon consensus-seeking committees – minimizing their business impact and value (0.8 probability).

By 2002, the most successful e-business efforts will be czar-driven, but only when enterprise revenues are at severe risk and when the czar has unqualified, direct access to the CEO (0.7 probability).

By 2002, the primary focus of IT management shifts from operational efficiency and effectiveness to information exploitation and extraenterprise operability (0.7 probability).

By 2002, more than 60 percent of large enterprise CIOs are sourced from ““the business”” or ESPs, facilitating business/IT fusion and e-process innovation (0.7 probability).

By 2003, 75 percent of Type A and 40 percent of Type B enterprises will have integrated IT planning and governance as key elements of their mainstream management processes to implement strategic business goals (0.7 probability).

After Crossing the Bridge…

OLD ECONOMY

DIGITAL ECONOMY

New Phonemena

The Nature of Business

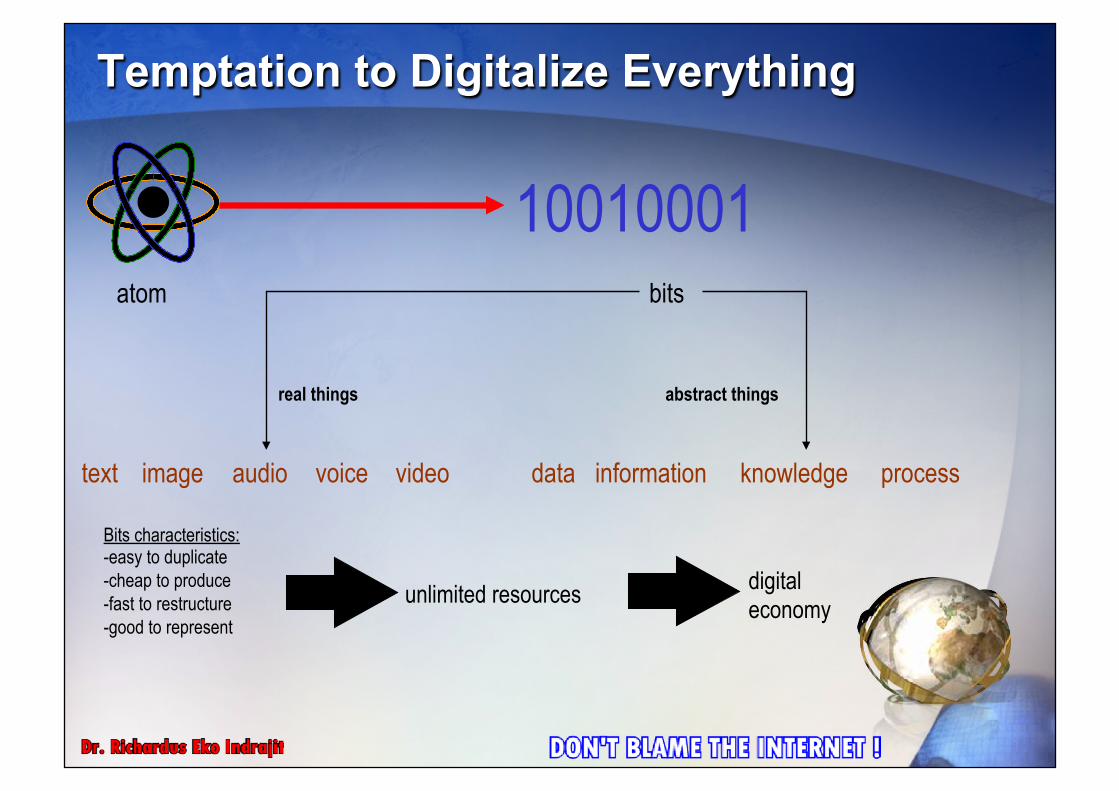

Temptation to Digitalize Everything

10010001 atom bits

text audio video image voice data knowledge information process

real things abstract things

Bits characteristics: - easy to duplicate - cheap to produce - fast to restructure - good to represent

unlimited resources digital economy

The Early Warning

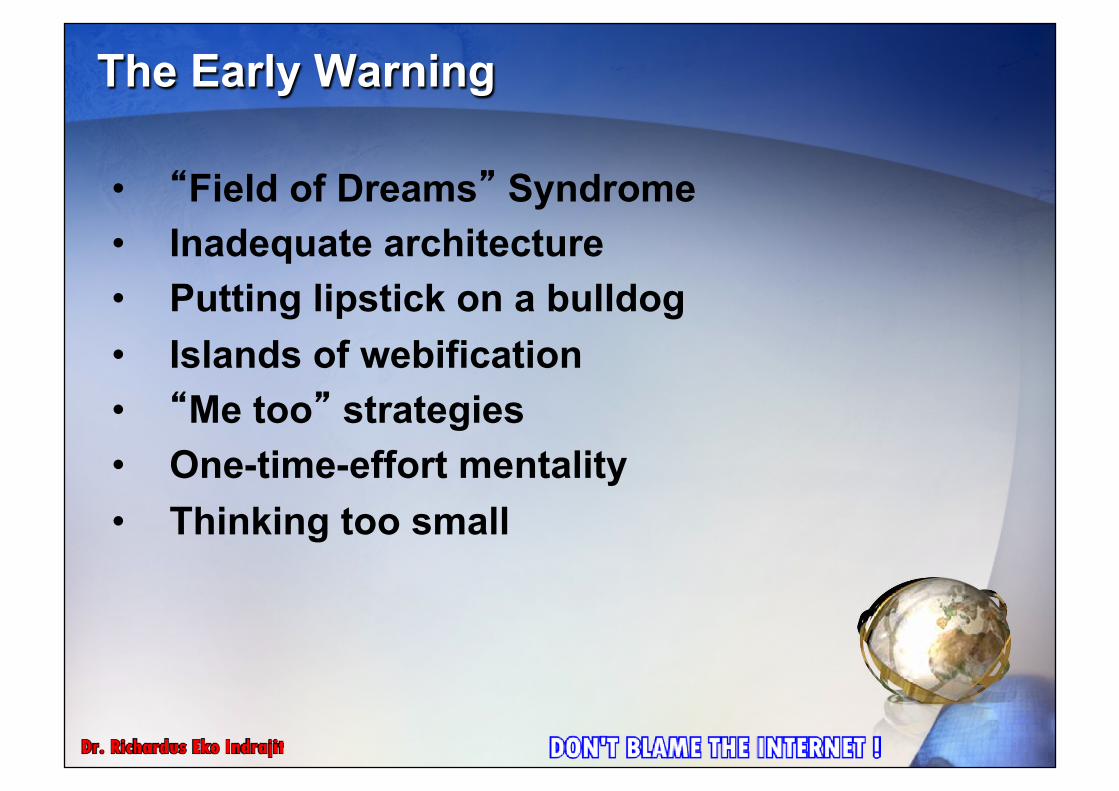

““Field of Dreams”” Syndrome Inadequate architecture Putting lipstick on a bulldog Islands of webification ““Me too”” strategies One-time-effort mentality Thinking too small

About the Cost Transparency

Avoid from having a high profit margin Change the product into commodity Weaken customer loyalty to brand Decrease company reputation due to

unfair pricing

Minimum Requirements

Understand the principles of new economy

Have a good vision Excellence in working stamina Able to cope with change Can manage people Collaborate to compete Combine professional with entrepreneur

Lack of Sustainable Business Model

Difficult to maintain competitive advantage

Compete with a great number of players Operate within a free market

environment Work with other business partners Require good competencies and skills

Opportunities = Threats

1. Power Shift to Customer 2. Global Sales Channel 3. Reduced Costs of Buying

and Selling 4. Converging Touch Points 5. Always Open for

Business 6. Reduced Time-to-Market 7. Enriched Buying

Experience 8. Customization 9. Self-Service 10. Reduced Barriers of

Market Entry 11. Demographics of the

Internet User

12. Power Shift to Communities-of-Interest

13. Cybermediation 14. Logistics and Physical

Distribution 15. Branding: Loyalty and

Acceptance Still Have to be Earned

16. When Most Markets Behave Like the Stock Market

17. Auctions Everywhere 18. Hyper-Efficiency

Why Fail? (Deloitte and Touche)

1. People 2. Product 3. Technology 4. Alliances 5. Market 6. Customer 7. Financing 8. Competition 9. Structure 10. Time

1. People

Visionaries who can’’t stop – After launch date – Constant focus on new market opportunities

There’’s no substitute for management depth and experience

The COO must manage Structured minds hate chaotic environments Lack of focus can blur the landscape No sense of urgency… but everything’’s at webspeed Human resource issues are not the last problem to

resolve

2. Product

Marketing myopia Intuition should support the research, not replace it Getting them used to a rhythmic release strategy Launch date is not the finish line Release strategies are made to be adhered to Narrow, non-competitive vs. bundled, diverse offerings Lack of understanding or experience in the marketplace

– B2B players don’’t understand how industrial buying really works

3. Technology

Architectural flaws are fatal in high availability businesses

Poor project management & QA – a recipe for failure Bifocal technology strategies – short term growth / long

term flexibility Ready, fire, aim Speed & specificity vs. generality Volume / load testing Demonstrate your security Lack of scalability Redundancy means more than backups Not everyone uses IE5.0 Bad software development practices breed contempt Document everything

4. Alliances

Building the imputed stock value through credibility? Long term alliances must bring value:

– Intellectual Property – Capital – Skills – Credibility – Customers

Poor partners made in haste – Quality and value – Integrity of character

Managing Expectations No risk & profit sharing model

5. Market

Where’’s the market research? Value Proposition – elevator pitches are about the

customer Understanding the difference between:

– Sales Force Strategy – Branding & Awareness Strategy – Marketing Strategy

No hybrid (traditional/cyber) approach Inexperienced help doesn’’t help at all Strong reliance on few channels Inability to migrate up the market The VP of Marketing doesn’’t work for the CFO

6. Customer

Customer experience management Reacting to feedback – more than having a ‘‘thick skin’’ Losing control of the customer contact points ‘‘24x7’’ means human availability Limited knowledge of the customer The investor is not a customer Advertising dollars buy awareness but certainly not

loyalty

7. Financing

A formal business plan is a living document Detailed financial projections Sensitivity analysis Poor positioning Shopping the idea Ongoing financial monitoring seems to be a rare event The best stock option models may not be the most

practical Investors like new ideas, not old ones re-packaged If it doesn’’t make cents… it doesn’’t make sense

8. Competition

We’’re the only one doing this Differentiation analysis Understand the substitutes as well as the competitors Build the IP fast Understand the barriers to entry Incumbents see the Internet as an enabler not a threat

9. Structure

No structure is not the same as a flat corporate structure No bricks… no clicks Adopting the Fortune 500 structure Communicate, collaborate and eliminate the silos A common vision does not equal common goals Manual processes are ‘‘bottlenecks’’ A complete website is not a back office Recognize an e-Business is ‘‘inside out’’

10. Time

Internet time waits for everyone Re-writing history takes time and patience Time to market is no excuse for poor business discipline First mover advantage is meaningless unless you’’re

ready Learning e-Business is easier than learning Business Incumbents get to mess it up many times, start-ups only

once

News from Information Week

Where Do You Wanna Go ?

AA: Traditional ““invest for future”” going- concern success

AB: Dark Model Profitless growth, war of corporate attrition

AC: Black Hole Massive company generates negative

cash flow, never recovers

Break Even

Top 10 eBusiness Success Imperatives

#1: Never Plan More than 24 Months Ahead #2: Do Not Develop an E-Business Strategy Independent of the Full Business Strategy #3: Use Separate Strategies According to Industry, Geography and Culture #4: During Analysis, Give Equal Weight to the Internal and External Processes #5: Obtain Total Buy-In From the Board #6: Deliberately Execute Alternatives to Buy, Spin Off or Transform the Business Model #7: Play By the ““New”” Rules #8: Enhance or Eliminate Distribution Channels Based on Their Power and Value #9: Establish a Metrics Program That Measures the True Effectiveness of the E-Business Initiative #10: Speed and Ruthless Execution Are Everything

Test the Initiatives

Form the

Idea

Determine Business Objective

Develop Business

Model

Resource Gathering

Setting the

Stage

Start the

Business

1 2 3 4 5 6

The Success

New Business (products/services) New Market (customers) New Revenue (business model) New Company (business transformation) New Image (business community) New Wealth (paradigm shift)

Etc.

Key Points: From ““nothing”” to ““existing”” From ““existing”” to ““creating”” From ““creating”” to ““improving”” From ““improving”” to ““growing”” From ““growing”” to ““performing””

The Failures

Loss market share (products and services) Loss revenue (customers) Loss competitive advantage (business model) Loss trust (business community) Loss resources (competition) Loss opportunity (cost)

Etc.

Key Points: From ““performing”” to ““stopping”” From ““stopping”” to ““decreasing”” From ““decreasing”” to ““surviving”” From ““surviving”” to ““eliminating””

Shifting to the Net Phase II

CHARACTERISTICS NET-PHASE 1 NET-PHASE 2

Ideal company Thin float IPO, all-new online standalone start up

Second generation bricks ‘‘n clicks hybrid with compelling market proposition

Foundation investor/shareholders

Individual online investor, buying anything in current Cant Miss sector on dips

Institution, adapting value investment principles to volatile internet

Key player Startup originators, early stage angles, VC, top IPO investment bankers

Killer model developers, secondary (mainstream) financiers

Primary management focus

Positioning: Being in the right sector

Viable business plan that ensures survival today, segment leadership tomorrow

Presence Participation Domination (40/40)

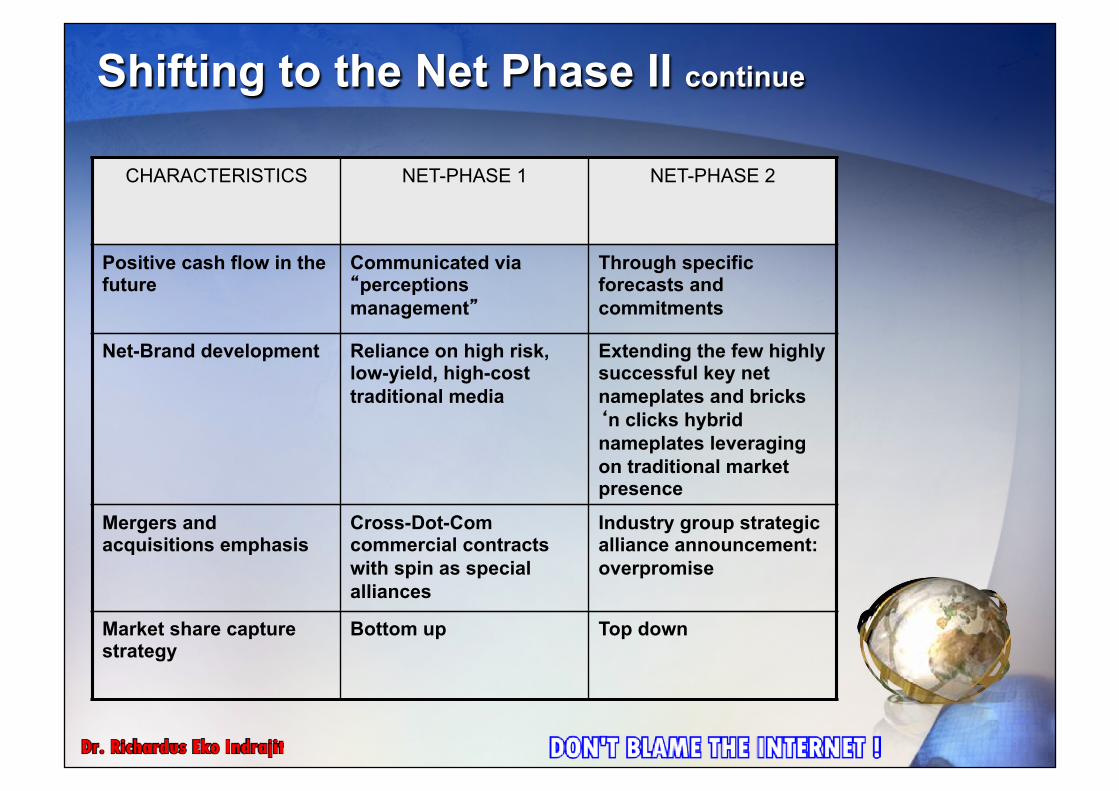

Shifting to the Net Phase II continue

CHARACTERISTICS NET-PHASE 1 NET-PHASE 2

Positive cash flow in the future

Communicated via ““perceptions management””

Through specific forecasts and commitments

Net-Brand development Reliance on high risk, low-yield, high-cost traditional media

Extending the few highly successful key net nameplates and bricks ‘‘n clicks hybrid nameplates leveraging on traditional market presence

Mergers and acquisitions emphasis

Cross-Dot-Com commercial contracts with spin as special alliances

Industry group strategic alliance announcement: overpromise

Market share capture strategy

Bottom up Top down

From Place to Space Business Models

1. Direct to Customer 2. Full-Service Provider 3. Whole of Enterprise 4. Portals, Agents, Auctions,

Aggregators, and Other Intermediaries

5. Shared Infrastructure 6. Virtual Community 7. Value Net Integrator 8. Content Provider

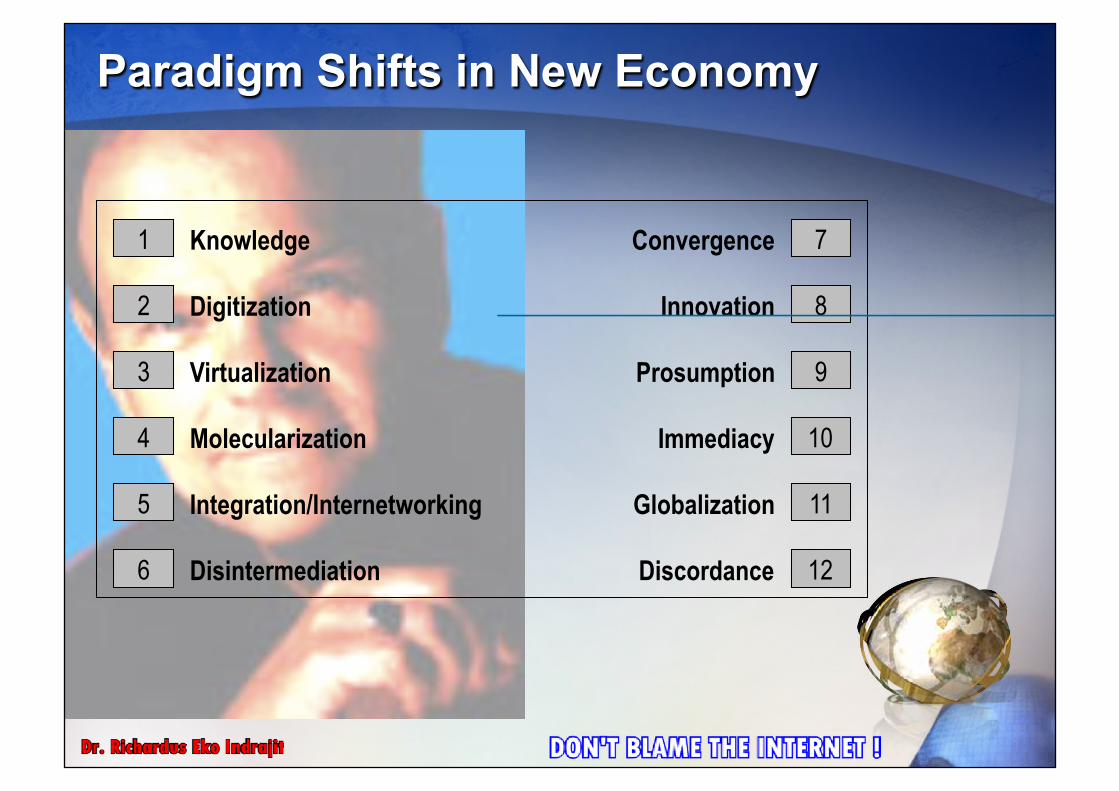

Knowledge

Digitization

Virtualization

Molecularization

Integration/Internetworking

Disintermediation

1

2

3

4

5

6

Convergence

Innovation

Prosumption

Immediacy

Globalization

Discordance

7

8

9

10

11

12

Paradigm Shifts in New Economy

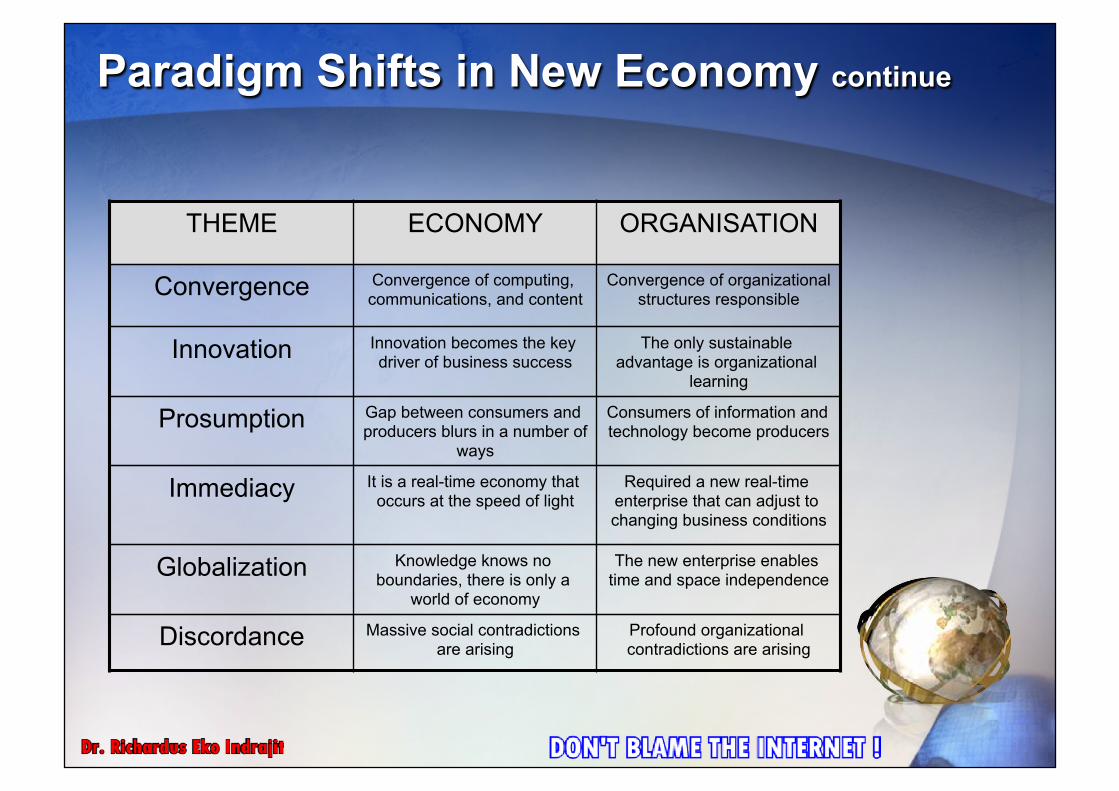

THEME ECONOMY ORGANISATION

Knowledge Knowledge becomes an important element of products

Knowledge work becomes the basis of value, revenue, and

profit

Digitization Products and services’ forms are transformed into ones and

zeros format

Internal communication shifts from analog to digital

Virtualization Physical things (institution and relationship) can become

virtual

The business transformation into virtual corporations type

company

Molecularization Replacement of the mass media into molecular media

End of command-and-control hierarchy, shifting to team-

based, molecular structures

Internetworking Networked economy with deep and reach interconnections of

economic entities

Integration of modular, independent, organizational components for network of

services

Disintermediation Elimination of intermediaries and any stand between

producers and consumers

Elimination of middle managers, internal agents, etc. who boost the communication

signals

Paradigm Shifts in New Economy continue

THEME ECONOMY ORGANISATION

Convergence Convergence of computing, communications, and content

Convergence of organizational structures responsible

Innovation Innovation becomes the key driver of business success

The only sustainable advantage is organizational

learning

Prosumption Gap between consumers and producers blurs in a number of

ways

Consumers of information and technology become producers

Immediacy It is a real-time economy that occurs at the speed of light

Required a new real-time enterprise that can adjust to changing business conditions

Globalization Knowledge knows no boundaries, there is only a

world of economy

The new enterprise enables time and space independence

Discordance Massive social contradictions are arising

Profound organizational contradictions are arising

Paradigm Shifts in New Economy continue

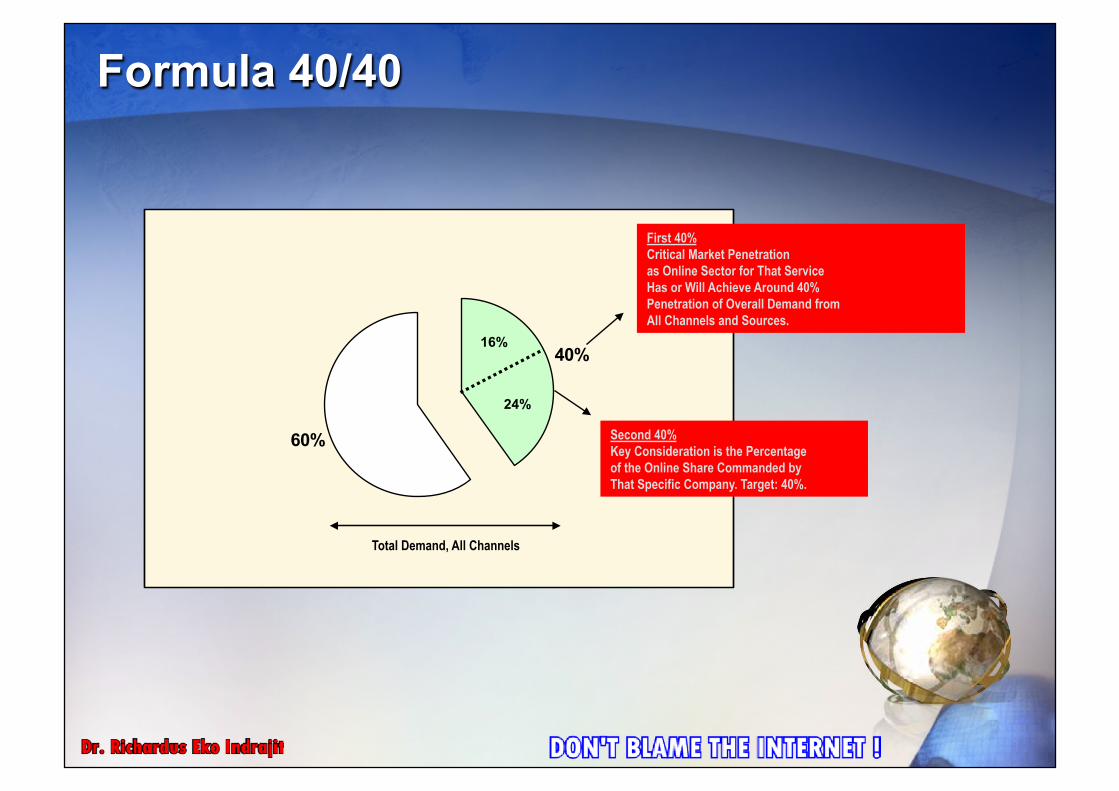

Formula 40/40

40%

60%

16%

24%

Total Demand, All Channels

First 40% Critical Market Penetration as Online Sector for That Service Has or Will Achieve Around 40% Penetration of Overall Demand from All Channels and Sources.

Second 40% Key Consideration is the Percentage of the Online Share Commanded by That Specific Company. Target: 40%.

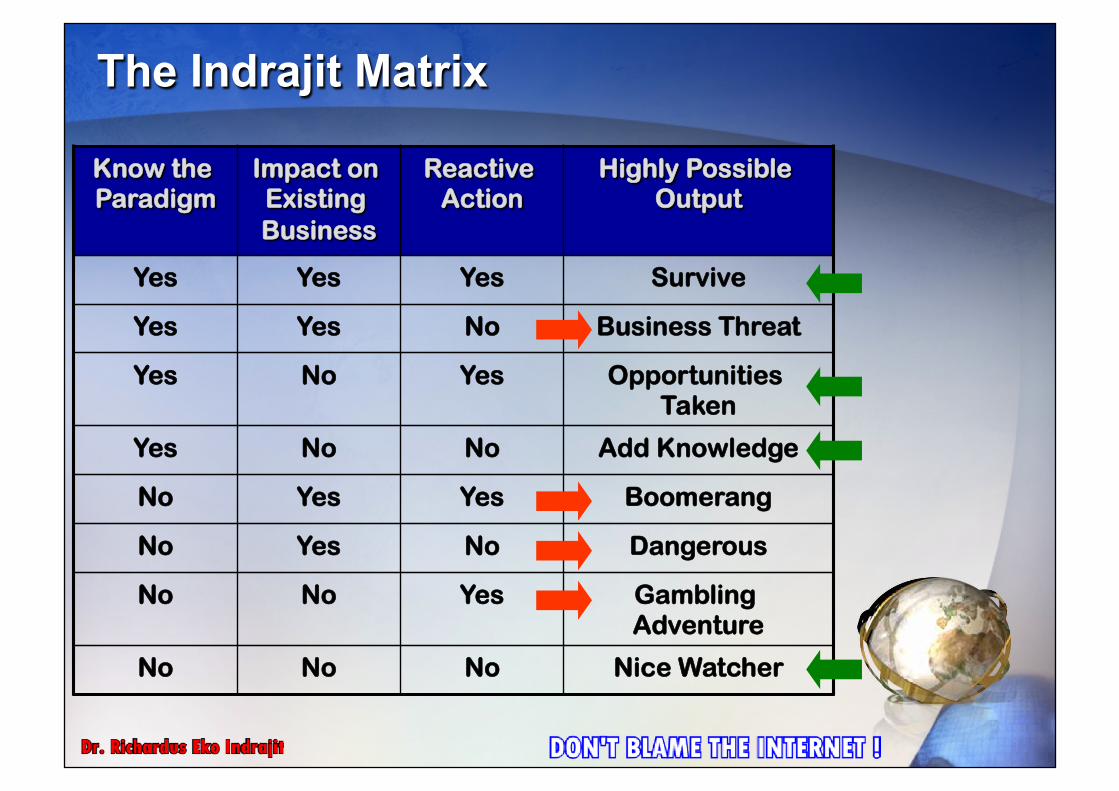

KKnnooww tthhee PPaarraaddiiggmm

IImmppaacctt oonn EExxiissttiinngg BBuussiinneessss

RReeaaccttiivvee AAccttiioonn

HHiigghhllyy PPoossssiibbllee OOuuttppuutt

YYeess YYeess YYeess SSuurrvviivvee

YYeess YYeess NNoo BBuussiinneessss TThhrreeaatt

YYeess NNoo YYeess OOppppoorrttuunniittiieess TTaakkeenn

YYeess NNoo NNoo AAdddd KKnnoowwlleeddggee

NNoo YYeess YYeess BBoooommeerraanngg

NNoo YYeess NNoo DDaannggeerroouuss

NNoo NNoo YYeess GGaammbblliinngg AAddvveennttuurree

NNoo NNoo NNoo NNiiccee WWaattcchheerr

The Indrajit Matrix

The Market Potential

Population

Internet Users

Internet Business

B2B

B2C

C2C

1

2 3

PHYSICAL WORLD of value chain

Business on the 80s-90s

Business after the year of 2000

VIRTUAL WORLD of value chain

+

Clicks ‘‘n Bricks

1. Flow of Physical/Digital Products 2. Flow of Money/Financial Data 3. Flow of Documents/Information 4. Flow of Services and Other Resources

Key Success Factors

FIRM INFRASTRUCTURE

HUMAN RESOURCE MANAGEMENT

TECHNOLOGY DEVELOPMENT

PROCUREMENT

INBOUND LOGISTICS OPERATIONS OUTBOUND

LOGISTICS MARKETING AND SALES SERVICE

FIRM INFRASTRUCTURE

HUMAN RESOURCE MANAGEMENT

TECHNOLOGY DEVELOPMENT

PROCUREMENT

INBOUND LOGISTICS OPERATIONS OUTBOUND

LOGISTICS MARKETING AND SALES SERVICE

FIRM INFRASTRUCTURE

HUMAN RESOURCE MANAGEMENT

TECHNOLOGY DEVELOPMENT

PROCUREMENT

INBOUND LOGISTICS OPERATIONS OUTBOUND

LOGISTICS MARKETING AND SALES SERVICE

FIRM INFRASTRUCTURE

HUMAN RESOURCE MANAGEMENT

TECHNOLOGY DEVELOPMENT

PROCUREMENT

INBOUND LOGISTICS OPERATIONS OUTBOUND

LOGISTICS MARKETING AND SALES SERVICE Industry Based Value Chain

Best Practice Oriented Software/Application Minded Physical Flow of Goods

The Physical Value Chain

Gather

Organize

Select

Synthesize

Distribute

Operation Mechanism: Info Based Process Flow of Bits Bit Restructuring Digital Asset

The Virtual Value Chain

Opportunity in the eBusiness

The Value Matrix

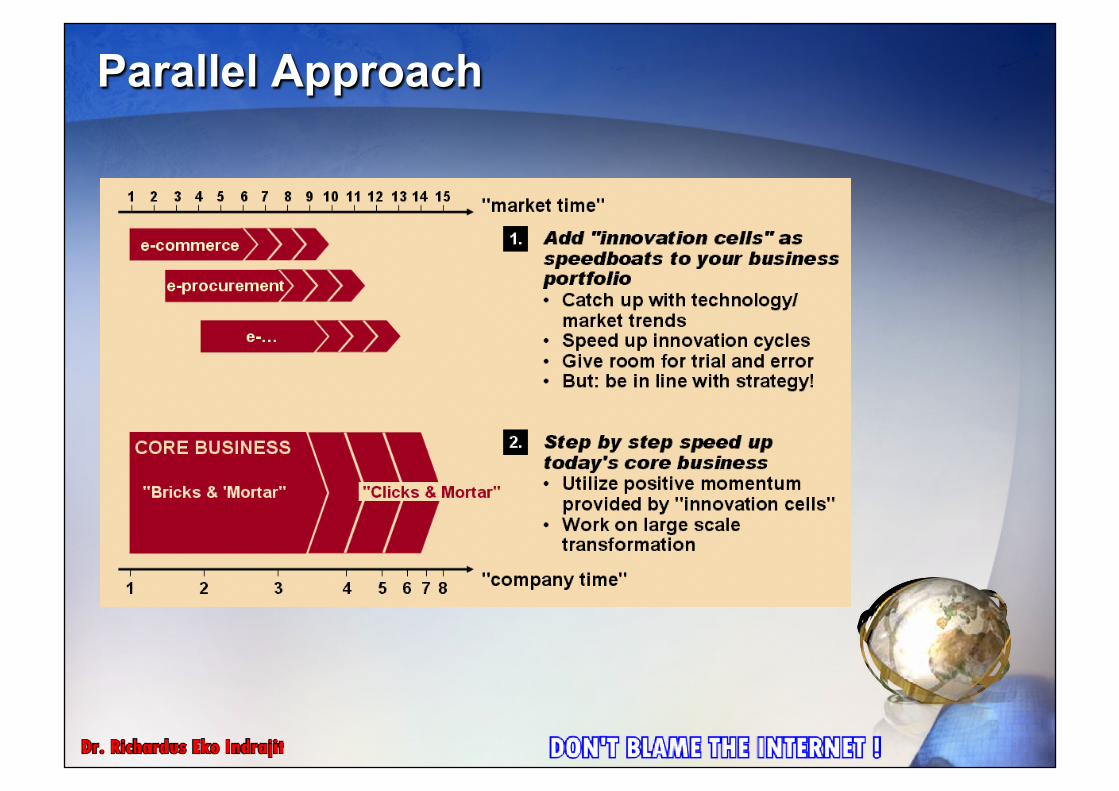

Parallel Approach

P1 Purchasing

and Inbound Logistic

P2 Production

and Operation

P3 Outbound

Logistic and Distribution

P4 Sales and

Marketing

P5 Customer

Supports and Services

P1 V1 Gather

P1 V2 Organize

P1 V3 Select

P1 V4 Synthesize

P1 V5 Distribute

P2 V1 Gather

P2 V2 Organize

P2 V3 Select

P2 V4 Synthesize

P2 V5 Distribute

P3 V1 Gather

P3 V2 Organize

P3 V3 Select

P3 V4 Synthesize

P3 V5 Distribute

P4 V1 Gather

P4 V2 Organize

P4 V3 Select

P4 V4 Synthesize

P4 V4 Distribute

P5 V1 Gather

P5 V2 Organize

P5 V3 Select

P5 V4 Synthesize

P5 V5 Distribute

P1OB P2OR P3OB P4OB P5OB

P1OC P2OC P3OC P4OC

Po5C

PiV1OB

PiV2OB

PiV3OB

PiV4OB

PiV5OB

PiV1OC

PiV2OC

PiV3OC

PiV4OC

PiV5OC

P1IB P2IB P3IB P4IB P5IB

P1IC P2IC P3IC P4IC P4IC

Business

Consumers

The Indrajit Model

Customers

Customers

Enterprise A

Enterprise B

Enterprise C

Enterprise D

The Internetworking

P1 Books

Publisher

P2 Inventory

P3 Distribution

P4 Physical

Bookstore

P5 Courier Services

P1 V1 Gather

P1 V2 Organize

P1 V3 Select

P1 V4 Synthesize

P1 V5 Distribute

P2 V1 Gather

P2 V2 Organize

P2 V3 Select

P2 V4 Synthesize

P2 V5 Distribute

P3 V1 Gather

P3 V2 Organize

P3 V3 Select

P3 V4 Synthesize

P3 V5 Distribute

P4 V1 Gather

P4 V2 Organize

P4 V3 Select

P4 V4 Synthesize

P4 V4 Distribute

P5 V1 Gather

P5 V2 Organize

P5 V3 Select

P5 V4 Synthesize

P5 V5 Distribute

C U S T O M E R S

C U

S T O M

E R S P

A R

T N

E R

S

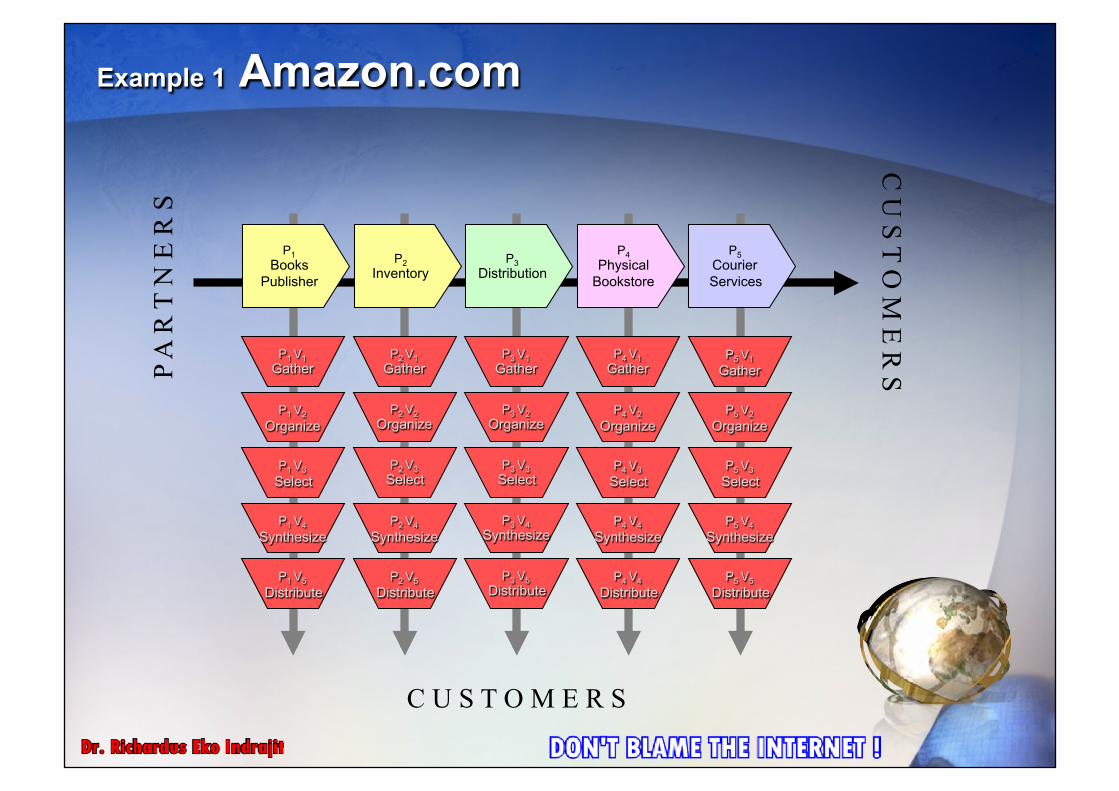

Example 1 Amazon.com

P1 Subjects & Contents

P2 Online

Training

P3 Formal Exam

P4 Retake Exam

P5 Certificate Deliverable

P1 V1 Gather

P1 V2 Organize

P1 V3 Select

P1 V4 Synthesize

P1 V5 Distribute

P2 V1 Gather

P2 V2 Organize

P2 V3 Select

P2 V4 Synthesize

P2 V5 Distribute

P3 V1 Gather

P3 V2 Organize

P3 V3 Select

P3 V4 Synthesize

P3 V5 Distribute

P4 V1 Gather

P4 V2 Organize

P4 V3 Select

P4 V4 Synthesize

P4 V4 Distribute

P5 V1 Gather

P5 V2 Organize

P5 V3 Select

P5 V4 Synthesize

P5 V5 Distribute

C U S T O M E R S

C U

S T O M

E R S

P A

R T

N E

R S

C

U S

T O

M E

R S

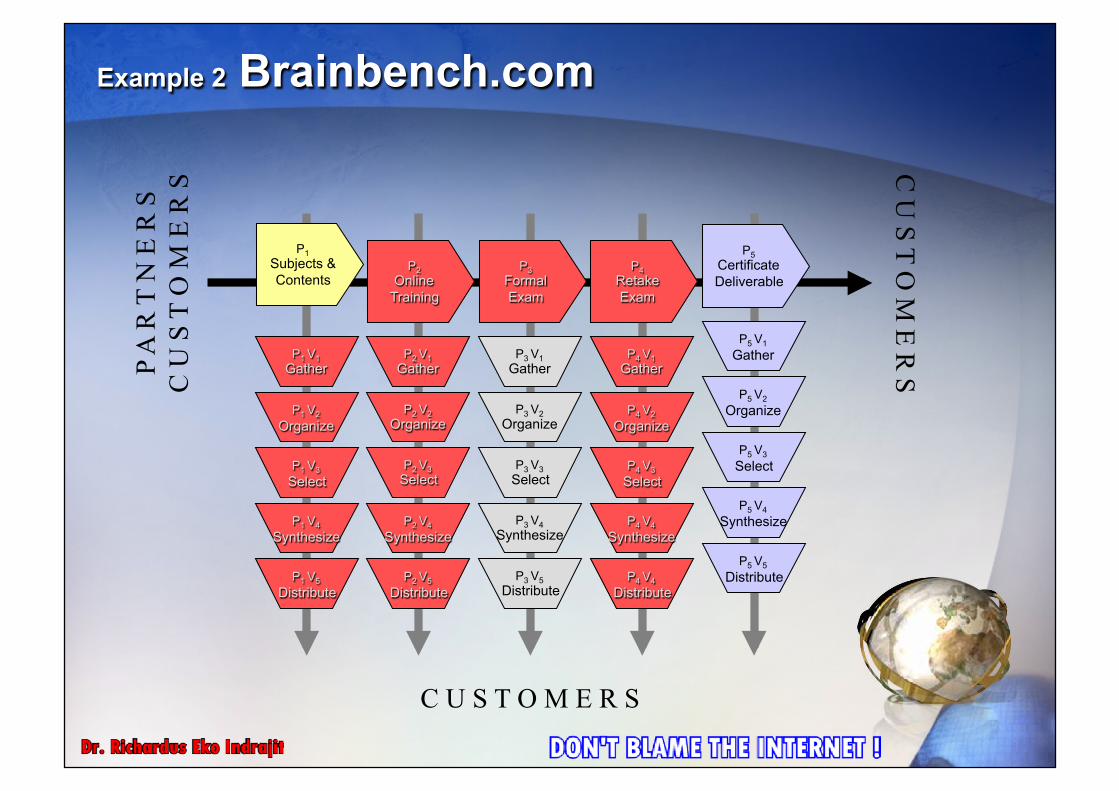

Example 2 Brainbench.com

P1 Freeware & Shareware Warehouse

P2 Components

Download

P3 Software

Demo

P4 Purchasing

P5 Full

Download

P1 V1 Gather

P1 V2 Organize

P1 V3 Select

P1 V4 Synthesize

P1 V5 Distribute

P2 V1 Gather

P2 V2 Organize

P2 V3 Select

P2 V4 Synthesize

P2 V5 Distribute

P3 V1 Gather

P3 V2 Organize

P3 V3 Select

P3 V4 Synthesize

P3 V5 Distribute

P4 V1 Gather

P4 V2 Organize

P4 V3 Select

P4 V4 Synthesize

P4 V4 Distribute

P5 V1 Gather

P5 V2 Organize

P5 V3 Select

P5 V4 Synthesize

P5 V5 Distribute

C U S T O M E R S

C U

S T O M

E R S

P A

R T

N E

R S

Example 3 Download.com

P1 List of Used

Goods

P2 Auction

Registration

P3 Auction Session

& Winner

P4 Payment

& Settlement

P5 Goods

Deliverable

P1 V1 Gather

P1 V2 Organize

P1 V3 Select

P1 V4 Synthesize

P1 V5 Distribute

P2 V1 Gather

P2 V2 Organize

P2 V3 Select

P2 V4 Synthesize

P2 V5 Distribute

P3 V1 Gather

P3 V2 Organize

P3 V3 Select

P3 V4 Synthesize

P3 V5 Distribute

P4 V1 Gather

P4 V2 Organize

P4 V3 Select

P4 V4 Synthesize

P4 V4 Distribute

P5 V1 Gather

P5 V2 Organize

P5 V3 Select

P5 V4 Synthesize

P5 V5 Distribute

C U S T O M E R S

C U

S T O M

E R S C

U S

T O

M E

R S

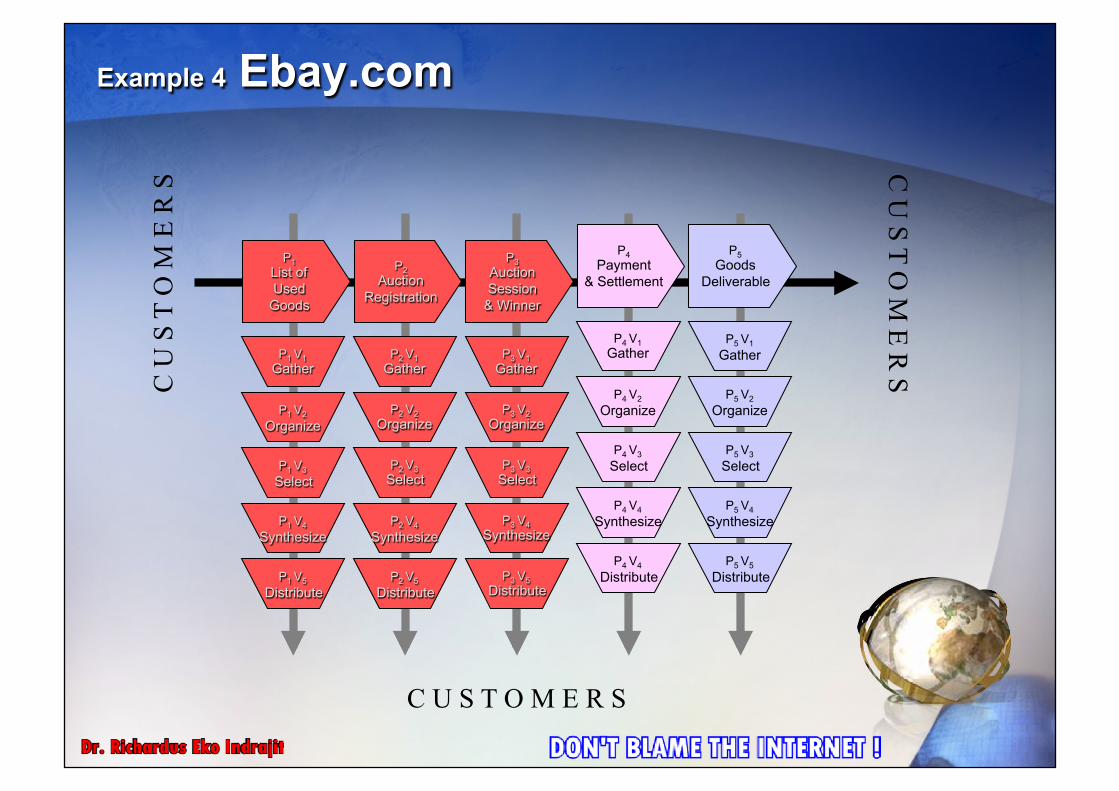

Example 4 Ebay.com

The Business Model: Who Wins ?

10 Driving Principles

1. Matter 2. Space 3. Time 4. People 5. Growth

6. Value 7. Efficiency 8. Markets 9. Transactions 10. Impulse

Recipes from eEntrepreneurs

How to transform traditional media players into "clicks & mortar" companies

Strategies for and management of transformation

How to integrate traditional and new business models

Development of new substantial business

How to re-build the organization to ensure sustainable advantages – real time adaption

Solid implementation of business innovation

How to utilize and and motivate human resources to transform the organization

HRM, leadership and corporate culture: success factors in the transformation process

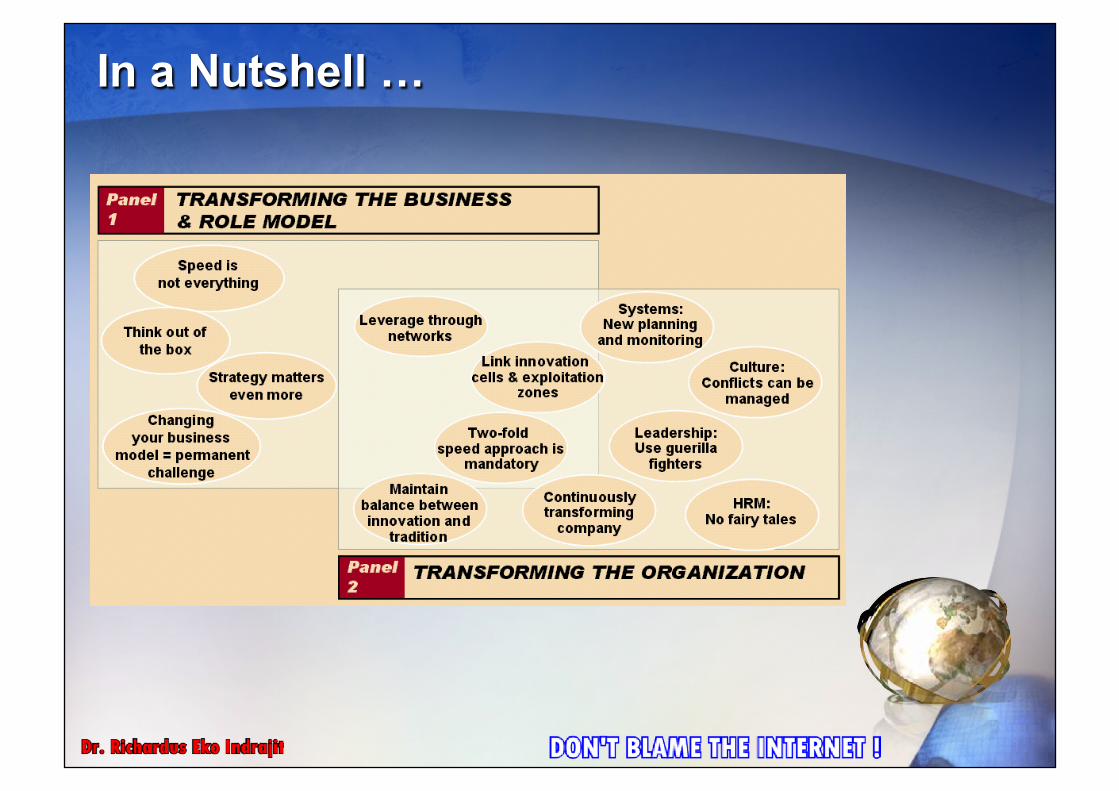

In a Nutshell …

In Five Years …

Ed Barton, ““Futurist””, stated at the NOAA Constituent Workshop that -

““To stay current with technology, industry must re-invent 20% of their business every year. This means that in 5 years, successful companies have totally changed the way they do business.””

About the Economic Revolution

“There is one economy, all of it being transformed by information technology. What is happening is no dot.com fad that will come and go – it is a profound economic revolution.

Tony Blair

11 September 2000

Some Final Thoughts

The dot.com era is over… the Internet era has only just started The real Internet companies have not yet arrived Disintermediation is not a threat when the customer becomes king Software companies and consultancies got it… both ways Pure-plays are becoming very ‘‘physical’’ The network effect only works in true Internet businesses Its almost nearly impossible to institutionalize entrepreneurship Decide whether you are in it for the company or the cash Dot.coms will change their spots… to become invisible Everyone will become an internal e-Business consultant The ““e”” will soon be gone

““There won’’t be any Internet companies. All companies will be Internet

companies, or they’’ll be dead”” Andy Grove - CEO, Intel Corporation

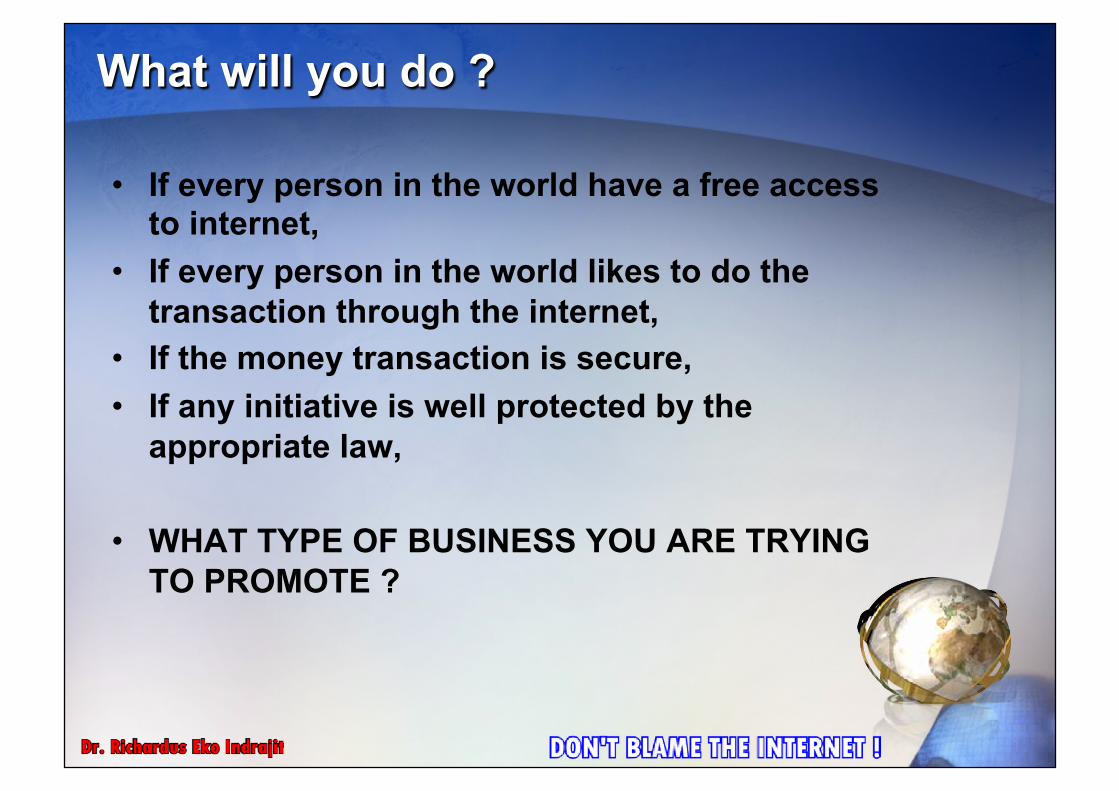

What will you do ?

If every person in the world have a free access to internet,

If every person in the world likes to do the transaction through the internet,

If the money transaction is secure, If any initiative is well protected by the

appropriate law,

WHAT TYPE OF BUSINESS YOU ARE TRYING TO PROMOTE ?

Summary: Let’’s Get Started !

1. Even after the start-up-mania is over, net economy offers tremendous opportunities especially for established players

2. The levers for successful transformation seem all too clear –

new instruments need to be utilized

Innovation cells to be implemented as – speed boats to quickly adapt your business with innovative ideas/

models – pacemaker for full scale e-transformation!

In parallel, (e-)transformation of the whole corporation must be supported by the "classical" transformation levers (but with "new" contents/tools)

3. After all: There are no conceptual, but mindset and implementation deficits to overcome – so let's get started!

Who will ruin the world…

The New Economy and the Old Economy Go Climbing …

Once upon a time,

Thank You

References

Related Documents