“BAR STAR NOTES” TAXATION VER. 2010.06.12 copyrighted 2010 Prepared by Prof. Abelardo T. Domondon (AB (Econ), BSC (Acctg), LLB, MA (Econ), LLM, DCL (Cand.). Lawyer-CPA-Customs Broker, Management Consultant, Professor of Law and Pre-Bar Reviewer) How to use the “BAR STAR NOTES.” The “BAR STAR NOTES” in the form of questions and answers as well as textual discussion were specially prepared by Prof. Domondon for the exclusive use of Bar Reviewees who attended his 2010 Lectures on TAXATION held at the University of the Philippines. Included in the presentation are doctrines contained in Supreme Court decisions up to April 2010. The purpose of the ‘BAR STAR NOTES” is to provide the Bar Reviewee with a handy review material which serves as “memory-joggers” for the September 12, 2010 Bar Examinations in Taxation. The author tries to second guess what would be included in the Bar Exams using statistical analysis. The actual Bar questions may not be formulated in the same manner as the “BAR STAR NOTES”. However, the doctrines tested in the Bar would in all probability be included in these Notes. If pressed for time, the author suggests that the reader should focus his attention on the following: Nice to know Should know Must know and master It is further suggested that the reader should merely browse those without stars. WARNING: These materials are copyrighted and/or based on the writer’s books on Taxation and future revisions. It is prohibited to reproduce any part of these Notes in any form or any means, electronic or mechanical, including photocopying without the written permission of the author. Unauthorized users shall not be prosecuted but SHALL BE SUBJECT TO THE LAW OF KARMA SUCH THAT THEY WILL NEVER PASS THE BAR OR WOULD BE UNHAPPY IN LIFE for stealing the intellectual property of the author. THE BEST OF LUCK AND ADVANCE CONGRATULATIONS TAXATION GENERAL PRINCIPLES OF TAXATION TAXATION, IN GENERAL 1. State briefly and concisely the nature of taxation. Alternatively, define taxation.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

“BAR STAR NOTES”

TAXATIONVER. 2010.06.12copyrighted 2010

Prepared by Prof. Abelardo T. Domondon(AB (Econ), BSC (Acctg), LLB, MA (Econ), LLM,

DCL (Cand.). Lawyer-CPA-Customs Broker, ManagementConsultant, Professor of Law and Pre-Bar Reviewer)

How to use the “BAR STAR NOTES.” The “BARSTAR NOTES” in the form of questions and answers aswell as textual discussion were specially prepared byProf. Domondon for the exclusive use of Bar Revieweeswho attended his 2010 Lectures on TAXATION held at theUniversity of the Philippines. Included in thepresentation are doctrines contained in Supreme Courtdecisions up to April 2010.

The purpose of the ‘BAR STAR NOTES” is to providethe Bar Reviewee with a handy review material whichserves as “memory-joggers” for the September 12, 2010Bar Examinations in Taxation. The author tries tosecond guess what would be included in the Bar Examsusing statistical analysis. The actual Bar questionsmay not be formulated in the same manner as the “BARSTAR NOTES”. However, the doctrines tested in the Barwould in all probability be included in these Notes.

If pressed for time, the author suggests that thereader should focus his attention on the following:

Nice to know

Should know Must know and masterIt is further suggested that the reader should

merely browse those without stars.

WARNING:

These materials are copyrighted and/or based onthe writer’s books on Taxation and future revisions.It is prohibited to reproduce any part of these Notesin any form or any means, electronic or mechanical,including photocopying without the written permissionof the author. Unauthorized users shall not beprosecuted but SHALL BE SUBJECT TO THE LAW OF KARMASUCH THAT THEY WILL NEVER PASS THE BAR OR WOULD BEUNHAPPY IN LIFE for stealing the intellectualproperty of the author.

THE BEST OF LUCK ANDADVANCE CONGRATULATIONS

TAXATION

GENERAL PRINCIPLES OF TAXATION

TAXATION, IN GENERAL

1. State briefly and concisely the natureof taxation. Alternatively, define taxation.

SUGGESTED ANSWER: The inherent power of thesovereign exercised through the legislature to imposeburdens upon subjects and objects within itsjurisdiction for the purpose of raising revenues tocarry out the legitimate objects of government.

2. What is the nature of the State’s powerto tax ? Explain briefly.

SUGGESTED ANSWER: The nature of the state’s powerto tax is two-fold. It is both an inherent power and alegislative power. It is inherent in naturebeing an attribute of sovereignty. This is so,because without the taxes, the state’s existence wouldbe imperiled. There is thus, no need for aconstitutional grant for the state to exercise thispower.

It is a legislative power because it involves thepromulgation of rules. Taxation is a set of rules,how much is the tax to be paid, who pays the tax, towhom it should be paid, and when the tax should bepaid.

3. What is the underlying theory oftaxation ? Explain briefly.

SUGGESTED ANSWER: Taxes are the lifeblood of thenation. Without revenue raised from taxation,the government will not survive, resulting indetriment to society. Without taxes, the governmentwould be paralyzed for lack of motive power toactivate and operate it. (Commissioner of Internal Revenue v.Algue, Inc. et al., 158 SCRA 8, 16-17)

4. Marshall said that, “the power to taxinvolves the power to destroy.” On the otherhand, Holmes stated that “the power to tax isnot the power to destroy while the courtsits.” Reconcile

the statements. Inthe alternative, what are the implications thatflow from the above statements ?

SUGGESTED ANSWERS: Marshall’s view refers toa valid tax while the Holmes’ view refers to aninvalid tax. a. The impositionof a valid tax could not be judicially restrainedmerely because it would prejudice taxpayer’s property.

b. An illegal tax could bejudicially declared invalid and should not workto prejudice a taxpayer’s property.

5. Discuss briefly the basis/bases, orrationale of taxation.

SUGGESTED ANSWER: a. Reciprocalduties of protection and support between the stateand its citizens and residents. Also called“symbiotic relation” between the state and itscitizens.

b. Jurisdiction by the state overpersons and property within its territory.

6. Discuss briefly but comprehensively theobjectives or purposes of taxation.

SUGGESTED ANSWER: The purposes or objectives oftaxation are the following:

a. The primary purpose:1) Revenue purpose.

b. The secondary purposes1) Sumptuary or

regulatory purpose. 2)Compensatory purpose.3) To implement the power of eminent domain.

7. Distinguish a tax from a license fee. SUGGESTED ANSWER: The following are the

distinctions: a. Purpose: Tax imposed for

2

revenue while license fee for regulation. Tax forgeneral public purposes while license fee forregulatory purposes only.

b. Basis: Tax imposed under power oftaxation while license fee under police power.

c. Amount: Intaxation, no limit as to amount while license feelimited to cost of the license and the expenses ofpolice surveillance and regulation.

d. Time of payment:Taxes normally paid after commencement of businesswhile license fee before. e. Effectof payment: Failure to pay a tax does not make thebusiness illegal while failure to pay license feemakes business illegal. f. Surrender: Taxes,being the lifeblood of the state, cannot besurrendered except for lawful consideration while alicense fee may be surrendered with or withoutconsideration. (Cooley on Taxation, pp. 1137-1138; PacificCommercial Company v. Romualdez, et al., 49 Phil. 924)

8. How may the power to tax be utilized tocarry out the social justice program of ourgovernment ? SUGGESTED ANSWER: Thecompensatory purpose of taxation is to implement thesocial justice provisions of the constitution throughthe progressive system of taxation, which would resultto equal distribution of wealth, etc.

Progressive income taxes alleviate the marginbetween rich and poor. (Southern Cross Cement Corporation v.Cement Manufacturers Association of the Philippines, et al., G. R. No.158540, August 3, 2005)

In recent years, the increasing social challengesof the times expanded the scope of the state activity,and taxation has become a tool to realize socialjustice and the equitable distribution of wealth,economic progress and the protection of local

industries as well as public welfare and similarobjectives. (Batangas Power Corporation v. Batangas City, et al.,G. R. No. 152675, and companion case, April 28, 2004 citingNational Power Corporation v. City of Cabanatuan, G. R. No. 149110,April 9, 2003)

9. Explain the sumptuary purpose oftaxation.

SUGGESTED ANSWER: The sumptuary purpose oftaxation is to promote the general welfare and toprotect the health, safety or morals of theinhabitants. It is in the joint exercise of the powerof taxation and police power where regulatory taxes arecollected.

Taxation may be made the implement of the state’spolice power. The motivation behind many taxationmeasures is the implementation of police power goals.[Southern Cross Cement Corporation v. Cement Manufacturers Association of thePhilippines, et al., G. R. No. 158540, August 3, 2005) The readershould note that the August 3, 2005 Southern Cross case isthe decision on the motion for reconsideration of theJuly 8, 2004 Southern Cross decision.

The so-called “sin taxes” on alcohol and tobaccomanufacturers help dissuade the consumers fromexcessive intake of these potentially harmful products.(Southern Cross Cement Corporation v. Cement Manufacturers Association of thePhilippines, et al., G. R. No. 158540, August 3, 2005)

10. Taxation distinguished from policepower. Taxation is distinguishable from police poweras to the means employed to implement these publicgoals. Those doctrines that are unique to taxationarose from peculiar considerations such as thoseespecially punitive effects (Southern Cross CementCorporation v. Cement Manufacturers Association of the Philippines, et al.,G. R. No. 158540, August 3, 2005) as the power to taxinvolves the power to destroy and the belief that taxes

3

are lifeblood of the state. (Ibid.) taxes being thelifeblood of the government, their prompt and certainavailability is of the essence.”

These considerations necessitated the evolution oftaxation as a distinct legal concept from police power.(Ibid.)

11. How the power of taxation may be used toimplement power of eminent domain. Tax measuresare but ”enforced contributions exacted on pain ofpenal sanctions” and “clearly imposed for publicpurpose.” In most recent years, the power to tax hasindeed become a most effective tool to realize socialjustice, public welfare, and the equitable distributionof wealth. (Commissioner of Internal Revenue v. Central Luzon DrugCorporation, G.R. No. 159647, April 16, 2005)

Establishments granting the 20% senior citizensdiscount may claim the discounts granted to seniorcitizens as tax deduction based on the net cost of thegoods sold or services rendered: Provided, That the costof the discount shall be allowed as deduction fromgross income for the same taxable year that thediscount is granted. Provided, further, That the totalamount of the claimed tax deduction net of value addedtax if applicable, shall be included in their grosssales receipts for tax purposes and shall be subjectto proper documentation and to the provisions of theNational Internal Revenue Code, as amended. [M.E. HoldingCorporation v. Court of Appeals, et al., G.R. No. 160193, March 3, 2008citing Expanded Senior Citizens Act of 2003, Sec. 4 (a)]

12. What are the three basic principlesof a sound tax system? Explain each briefly.

SUGGESTED ANSWER: The canonsof a sound tax system, also known as thecharacteristics or, principles of a sound tax system,are used as a criteria in order to determine whether a

tax system is able to meet the purposes or objectivesof taxation. They are: a. Fiscal adequacy. b. Administrative feasibility. c. Theoretical justice.

13. What are the elements or characteristicsof a tax ? SUGGESTED ANSWER:

a. Enforced contribution.b. Generally payable in money.c. Proportionate in character.d. Levied on persons, property or exercise of a

right or privilege.e. Levied by the state having jurisdiction.f. Levied by the legislature.g. Levied for a public purpose.h. Paid at regular periods or intervals.

14. State the requisites of a valid tax. SUGGESTED ANSWER:

a. A valid tax should be within the jurisdictionof the taxing authority. b. That the assessment and collectionof certain kinds (The same as the inherent limitationsof the power of taxation) should be for a publicpurpose. c. The rule of taxation should beuniform. d. That either the person orproperty of taxes guarantees against injustice toindividuals, especially by way or notice andopportunity for hearing be provided.

e. The tax must not impinge on the inherentand Constitutional limitations on the power oftaxation.

4

15. What arethe classes or kinds of taxes according to thesubject matter or object ?

SUGGESTED ANSWER: a. Personal, poll or capitalization – imposed on

all residents, whether citizen or not. Example –Community Tax.

b. Property - Imposed on property. Example– Real property tax.

c. Excise – imposed upon theperformance of an act, the enjoyment of aprivilege or the engaging in an occupation. Example –income tax, estate tax.

16. What are the kinds of taxes classifiedas to who bears the burden ? Explain eachbriefly. SUGGESTED ANSWER: Based onthe possibility of shifting the incidence of taxation,or as to who shall bear the burden of taxation, taxesmay be classified into:

a. Direct taxes. Those that are extracted fromthe very person who, it is intended or desired, shouldpay them (Commissioner of Internal Revenue v. Philippine Long DistanceTelephone Company, G. R. No. 140230, December 15, 2005); theyare impositions for which a taxpayer is directlyliable on the transaction or business he is engagedin, (Commissioner of Internal Revenue v. Philippine Long Distance TelephoneCompany, supra) which liability cannot be shifted ortransferred to another. Example – income tax, estatetax, donor’s tax, etc. b. Indirect taxes are those that are demanded inthe first instance, from, or are paid by, one personin the expectation and intention that he can shift theburden to (Commissioner of Internal Revenue v. Philippine Long DistanceTelephone Company, supra) to someone else not as a tax butas part of the purchase price. (Commissioner, of Internal

Revenue v. American Express International, Inc. (Philippine Branch), G.R. No. 152609, June 29, 2005 citing various cases andauthorities) Example – value added tax (VAT),documentary stamp tax, excise tax, percentage tax,etc.

17.Silkair (Singapore) PTE, Ltd., aninternational carrier, purchased aviation gasfrom Petron Corporation, which it uses for itsoperations. It now claims for refund or taxcredit for the excise taxes it paid claiming thatit is exempt from the payment of excise taxesunder the provisions of Sec. 135 of the NIRC of1997 which provides that petroleum products areexempt from excise taxes when sold to “Exemptentities or agencies covered by tax treaties, conventions,and other international agreements for their use andconsumption: Provided, however, That the country of saidforeign international carrier or exempt entities oragencies exempts from similar taxes petroleum products soldto Philippine carriers, entities or agencies”

Silkair further anchors its claim on Article4(2) of the Air Transport Agreement between theGovernment of the Republic of the Philippines andthe Government of the Republic of Singapore (AirTransport Agreement between RP and Singapore)which reads: “Fuel, lubricants, spare parts, regularequipment and aircraft stores introduced into, or taken onboard aircraft in the territory of one Contracting party by,or on behalf of, a designated airline of the otherContracting Party and intended solely for use in theoperation of the agreed services shall, with the exceptionof charges corresponding to the service performed, be exemptfrom the same customs duties, inspection fees and otherduties or taxes imposed in the territories of the firstContracting Party , even when these supplies are to be usedon the parts of the journey performed over the territory of

5

the Contracting Party in which they are introduced into ortaken on board. The materials referred to above may berequired to be kept under customs supervision and control.”

Silkair likewise argues that it is exemptfrom indirect taxes because the Air TransportAgreement between RP and Singapore grantsexemption “from the same customs duties,inspection fees and other duties or taxes imposedin the territory of the first Contracting Party.It invokes Maceda v. Macaraig, Jr., G.R. No.88291, May 31, 1991, 197 SCRA 771.which upheldthe claim for tax credit or refund by theNational Power Corporation (NPC) on the groundthat the NPC is exempt even from the payment ofindirect taxes.

Is Silkair entitled to the tax refund orcredit it seeks ? Reason out your answer.

SUGGESTED ANSWER: Silkair is not entitled to taxrefund or credit for the following reasons:

a. The excise tax on aviation fuel is anindirect tax. The proper party to question, or seek arefund of, an indirect tax is the statutory taxpayer,the person on whom the tax is imposed by law and whopaid the same even if he shifts the burden thereof toanother. (Philippine Geothermal, Inc. v. Commissioner of Internal Revenue,G.R. No. 154028, July 29, 2005, 465 SCRA 308, 317-318)The NIRC provides that the excise tax should be paid bythe manufacturer or producer before removal of domesticproducts from place of production. Thus, PetronCorporation, not Silkair, is the statutory taxpayerwhich is entitled to claim a refund based on Section135 of the NIRC of 1997 and Article 4(2) of the AirTransport Agreement between RP and Singapore.

Even if Petron Corporation passed on to Silkairthe burden of the tax, the additional amount billed toSilkair for jet fuel is not a tax but part of the price

which Silkair had to pay as a purchaser. [PhilippineAcetylene Co., Inc. v. Commissioner of Internal Revenue, 127 Phil. 461, 470(1967)]

b. Silkair could not seek refuge under Maceda v.Macaraig, Jr., G.R. No. 88291, May 31, 1991, 197 SCRA771.which upheld the claim for tax credit or refund bythe National Power Corporation (NPC) on the ground thatthe NPC is exempt even from the payment of indirecttaxes.

In Commissioner of Internal Revenue v. Philippine Long DistanceTelephone Company, G.R. No. 140230, December 15, 2005,478 SCRA 61 the Supreme Court clarified the ruling inMaceda v. Macaraig, Jr., viz: It may be so that in Maceda vs.Macaraig, Jr., the Court held that an exemption from “alltaxes” granted to the National Power Corporation (NPC)under its charter includes both direct and indirecttaxes.

An exemption from “all taxes” excludes indirecttaxes, unless the exempting statute, like NPC’scharter, is so couched as to include indirect tax fromthe exemption. The amendment under Republic Act No.6395 enumerated the details covered by NPC’s exemption.Subsequently, P.D. 380, made even more specific thedetails of the exemption of NPC to cover, among others,both direct and indirect taxes on all petroleumproducts used in its operation. Presidential DecreeNo. 938 [NPC’s amended charter] amended the taxexemption by simplifying the same law in general terms.It succinctly exempts NPC from “all forms of taxes,duties, fees…” The use of the phrase “all forms” oftaxes demonstrates the intention of the law to give NPCall the tax exemptions it has been enjoying before.

The exemption granted under Section 135 (b) ofthe NIRC of 1997 and Article 4(2) of the Air TransportAgreement between RP and Singapore cannot, without aclear showing of legislative intent, be construed asincluding indirect taxes. Statutes granting tax

6

exemptions must be construed in strictissimi jurisagainst the taxpayer and liberally in favor of thetaxing authority, and if an exemption is found toexist, it must not be enlarged by construction. (Silkair(Singapore) PTE, Ltd., v. Commissioner of Internal Revenue, G.R. No. 173594,February 6, 2008)

18. What are the different kinds oftaxes classified as to purpose ?

SUGGESTED ANSWER: a. General, fiscal or revenue – imposed

for the purpose of raising public funds for theservice of the government. b. Specialor regulatory – imposed primarily for the regulation ofuseful or non-useful occupation or enterprises andsecondarily only for the raising of public funds.

LIMITATIONS OR RESTRICTIONS ON THE POWER

1. Purpose for the limitations on the powerof taxation.The inherent and constitutional limitations to thepower of taxation are safeguards which would preventabuse in the exercise of this otherwise unlimited andplenary power.

The limitations also serve as a standard tomeasure the validity of a tax law or the act of ataxing authority. A violation of the limitationsserves to invalidate a tax law or act in the exerciseof the power to tax.

INHERENT LIMITATIONS

1. What are the inherent limitations onthe power of taxation ?

SUGGESTED ANSWERS:

a. Public purpose. The revenues collected fromtaxation should be devoted to a public purpose.

b. No improper delegation of legislativeauthority to tax. Only the legislature can exercisethe power of taxes unless the same is delegated to someother governmental body by the constitution or througha law which does not violate any provision of theconstitution.

c. Territoriality. The taxing power should beexercised only within territorial boundaries of thetaxing authority.

d. Recognition of government exemptions; and e. Observance of the principle of comity.

Comity is the respect accorded by nations to each otherbecause they are equals. On the other hand taxation isan act of sovereign. Thus, the power should be imposedupon equals out of respect.

Some authorities include no double taxation.

2. What are the principles to considerin the determination of whether tax revenues aredevoted for a public purpose ?

SUGGESTED ANSWER:a. The tax revenues are for a public purpose if

utilized for the benefit of the community in general.An alternative meaning is that tax proceeds should beutilized only to attain the objectives of government.

b. Inequalities resulting from the singling outof one particular class for taxation or exemptioninfringe no constitutional limitation. REASON: It is inherent in the power to taxthat the legislature is free to select the subjects oftaxation. BASIS: The lifeblood theory. c. An individual taxpayer need notderive direct benefits from the tax.

7

REASON: The paramount consideration is thewelfare of the greater portion of the population. d. A tax may be imposed, not so muchfor revenue purposes, but under police power for thegeneral welfare of the community. This would still befor a public purpose. e. Public purpose continuallyexpanding. Areas formerly left to private initiativenow lose their boundaries and may be undertaken by thegovernment if it is to meet the increasing socialchallenges of the times. f. Tax revenue must not be used forpurely private purposes or for the exclusive benefitof private persons. g. Private persons may be benefited butsuch benefit should be merely incidental as its mainobject is the benefit of the community in general. h. Determined at the time of enactmentof tax law and not at the time of implementation. i. There is a presumption of publicpurpose even if the tax law does not specificallyprovide for its purpose. (Santos & Co., v. Municipality ofMeycauayan, et al., 94 Phil. 1047)

j. Public use is no longer confined to thetraditional notion of use by the public but heldsynonymous with public interest, public benefit,public welfare, and public convenience. (Commissioner ofInternal Revenue v. Central Luzon Drug Corporation, G.R. No. 159647,April 16, 2005)

3. A law was enacted imposing a tax onmanufacturers of coconut oil, the proceeds ofwhich are to be used exclusively for theprotection and promotion of the coconutindustry, namely, to improve the workingconditions in coconut mills and to conductresearch on the use of coconut oil for motor

fuel. Some of the manufacturers of coconut oilchallenge the validity of the law, contendingthat the tax is to be used for a privatepurpose, and therefore, the law violates therule that public revenues shall not beappropriated for anything but a public purpose.Decide with reason.

SUGGESTED ANSWER: The levy is for a publicpurpose. It cannot be denied that the coconutindustry is one of the major industries supporting thenational economy. It is, therefore, the state’sconcern to make it a strong and secure source not onlyof the livelihood of the significant segment of thepopulation, but also of export earnings, thesustained growth of which is one of the imperatives ofeconomic growth. (Philippine Coconut Producers Federation, Inc.(Cocofed v. Presidential Commission on Good Government, 178 SCRA 236,252)

4.Requisites for taxpayers, concernedcitizens, voters or legislators to have locusstandi to sue. a. In general, the case should involveconstitutional issues. (David, et al., v. President GloriaMacapagal-Arroyo, etc., et al., G. R. No. 171396, May 3, 2006)

b. For taxpayers, there must be a showing: 1) That tax money is “being extracted and

spent in violation of specific constitutionalprotections against abuses of legislative power.”(Flast v. Cohen, 392 U.S. 83) 2) That public money is beingdeflected to any improper purpose (Pascual v. Secretary ofPublic Works, 110 Phil. 33) or a claim of illegaldisbursement of public funds or that the tax

measure is unconstitutional. (David, supra)

8

3) A taxpayer is allowed to sue where thereis a claim that public funds are illegallydisbursed, or that public money is being

deflected to any improper purpose, or that thereis a wastage of public funds through theenforcement of an invalid or unconstitutional law.(Abaya v. Ebdane, G. R. No. 167919, February 14,2007; Garcia v. Enriquez, Jr. G.R. No. 112655 December 9,

1993, Minute Resolution) A taxpayer’s suit is properly broughtonly when there is an exercise of the spending ortaxing power of Congress. (Automotive Industry WorkersAlliance (AIWA),etc., et al., v. Romulo, etc. ,et al., G. R. No. 157509,

January 18, 2005 citing Gonzales v. Narvasa, G. R. No. 140835, August 14, 2000, 337 SCRA 733, 741)c. For voters, there must be a showing of

obvious interest in the validity of the election lawin question.

d. For concerned citizens, there must be ashowing that the issues raised are of transcendentalimportance which must be settled early.

e. For legislators, there must be a claim thatthe official action complained of infringes upon theirprerogatives as legislators. (David, et al., v. President GloriaMacapagal-Arroyo, etc., et al., G. R. No. 171396, May 3, 2006)

5. Only those directly affected have locusstandi to impugn the alleged encroachment by theexecutive department into the legislative domainof Congress.

a. Only those who shall be directly affected bysuch executive encroachment, such as for exampleemployees who would find themselves subject todisciplinary powers that may be imposed under thequestioned Executive Order as they have a direct andspecific interest in raising the substantive issuetherein (Automotive Industry Workers Alliance (AIWA),etc., et al., v.

Romulo, etc. ,et al., G. R. No. 157509, January 18, 2005) oremployees who are going to be demoted, transferred orotherwise affected by any personnel action subject othe rule on exhaustion of administrative remedies.

b. Moreover, and if at all, only Congress, canclaim any injury from the alleged executiveencroachment of the legislative function to amend,modify and/or repeal laws. (Automotive Industry WorkersAlliance (AIWA),etc., et al., supra, citing Gonzales v. Narvasa, G. R.No. 140835, August 14,2000, 337 SCRA 733, 741)

6. Locus standi being merely a matter ofprocedure, have been waived in certain instanceswhere a party who is not personally injured maybe allowed to bring suit. The following areexamples of instances where suits have been brought byparties who have not have been personally injured bythe operation of a law or any other government act butby concerned citizens, taxpayers or voters who actuallysue in the public interest:

a. Taxpayer’s suits to question contractsentered into by the national government or government-owned or controlled corporations allegedly incontravention of the law.

b. A taxpayer is allowed to sue where there is aclaim that public funds are illegally disbursed, orthat public money is being deflected to any improperpurpose, or that there is a wastage of public fundsthrough the enforcement of an invalid orunconstitutional law. (Abaya v. Ebdane, G. R. No. 167919,February 14, 2007)

7. The VAT law provides that, thePresident, upon the recommendation of theSecretary of Finance, shall, effective January 1,2006, raise the rate of value-added tax to twelve

9

percent (12%) after any of the followingconditions have been satisfied. “(i) value-addedtax collection as a percentage of Gross DomesticProduct (GDP) of the previous year exceeds twoand four-fifth percent (2 4/5%) or (ii) nationalgovernment deficit as a percentage of GDP of theprevious year exceeds one and one-half percent (1½%).”

Was there an invalid delegation oflegislative power ?

SUGGESTED ANSWER: No. There is no unduedelegation of legislative power but only of thediscretion as to the execution of the law. This isconstitutionally permissible.

Congress does not abdicate its functions or undulydelegate power when it describes what job must be done,who must do it, and what is the scope of his authority.In the above case the Secretary of Finance becomesmerely the agent of the legislative department, todetermine and declare the even upon which its expressedwill takes place. The President cannot set aside thefindings of the Secretary of Finance, who is not underthe conditions acting as the execute alter ego orsubordinate. . [Abakada Guro Party List (etc.) v. Ermita, etc., et al.,G. R. No. 168056, September 1, 2005 and companion casesciting various cases]]

8. Instances of proper delegation: Whentaxing power could be delegated: Exceptions tothe rule on non-delegation:

a. Delegation of tariff powers by Congress tothe President under the flexible tariff clause,Section 28 (2), Article VI of the Constitution.

b. Delegation of emergency powers to thePresident under Section 23 (2) of Article VI of theConstitution.

c. The delegation to the President of thePhilippines to enter into executive agreements, and toratify treaties which may contain tax exemptionprovisions subject to the concurrence by the Senate inthe ratification made by the President.

d. Delegation to the people at large.e. Delegation to administrative bodies [Abakada

Guro Party List (Formerly AASJS), etc., v, Ermita, et al., G. R.No.168056, September 1, 2005], which is referred to assubordinate legislation. In this instance, there is a requirementthat the law is complete in all aspects so what isdelegated is merely the implementation of the law orthere exists sufficiently determinate standards toguide the delegate and prevent a total transference ofthe taxing power.

9. “Paradigm shift” from exclusiveCongressional power to direct grant of taxingpower to local legislative bodies. The power totax is no longer vested exclusively on Congress; locallegislative bodies are now given direct authority tolevy taxes, fees and other charges pursuant to ArticleX, section 5 of the 1987 Constitution. (Batangas PowerCorporation v. Batangas City, et al. G. R. No. 152675, and companioncase, April 28, 2004 citing National Power Corporation v. City ofCabanatuan, G. R. No. 149110, April 9, 2003)

Local government legislation, “is not regarded asa transfer of general legislative power, but rather asthe grant of authority to prescribe local regulations,according to immemorial practice, subject, of course,to the interposition of the superior in cases ofnecessity.” (People v. Vera, 65 Phil. 56)

10. Taxing power of the local government islimited. The taxing power of local governments is

10

limited in the sense that Congress can enactlegislation granting tax exemptions.

While the system of local government taxation haschanged with the onset of the 1987 Constitution, thepower of local government units to tax is stilllimited.

While the power to tax by local governments maybe exercised by local legislative bodies, no longermerely by virtue of a valid delegation as before, butpursuant to direct authority conferred by Section 5,Article X of the Constitution, the basic doctrine onlocal taxation remains essentially the same, “the powerto tax is [still] primarily vested in the Congress.” (Quezon City, et al., v.ABS-CBN Broadcasting Corporation, G. R. No. 166408, October 6,2008 citing City Government of Quezon City, et al. v. BayanTelecommunications, Inc., G.R. No. 162015, March 6, 2006, 484SCRA 169 in turn referring to Mactan Cebu International AirportAuthority, v. Marcos, G.R. No. 120082, September 11, 1996, 261SCRA 667, 680)

11. Further amplification by Bernas of thelocal government’s power to tax. “What is theeffect of Section 5 on the fiscal position ofmunicipal corporations? Section 5 does not change thedoctrine that municipal corporations do not possessinherent powers of taxation. What it does is toconfer municipal corporations a general power to levytaxes and otherwise create sources of revenue. Theyno longer have to wait for a statutory grant of thesepowers. The power of the legislative authorityrelative to the fiscal powers of local governments hasbeen reduced to the authority to impose limitations onmunicipal powers. Moreover, these limitations must be“consistent with the basic policy of local autonomy.”The important legal effect of Section 5 is thus toreverse the principle that doubts are resolved againstmunicipal corporations. Henceforth, in interpreting

statutory provisions on municipal fiscal powers,doubts will be resolved in favor of municipalcorporations. It is understood, however, that taxesimposed by local government must be for a publicpurpose, uniform within a locality, must not beconfiscatory, and must be within the jurisdiction ofthe local unit to pass.” (Quezon City, et al., v. ABS-CBNBroadcasting Corporation, G. R. No. 166408, October 6, 2008citing City Government of Quezon City, et al. v. Bayan Telecommunications,Inc., G.R. No. 162015, March 6, 2006, 484 SCRA 169)

12. Reconciliation of the local government’sauthority to tax and the Congressional generaltaxing power. Congress has the inherent power totax, which includes the power to grant tax exemptions.On the other hand, the power of local governments,such as provinces and cities for example Quezon City,to tax is prescribed by Section 151 in relation toSection 137 of the LGC which expressly provides thatnotwithstanding any exemption granted by any law orother special law, the City or a province may impose afranchise tax. It must be noted that Section 137 ofthe LGC does not prohibit grant of future exemptions.

The Supreme Court in a series of cases hassustained the power of Congress to grant taxexemptions over and above the power of the localgovernment’s delegated power to tax. (Quezon City, et al., v.ABS-CBN Broadcasting Corporation, G. R. No. 166408, October 6,2008 citing City Government of Quezon City, et al. v. BayanTelecommunications, Inc., G.R. No. 162015, March 6, 2006, 484SCRA 16)

“Indeed, the grant of taxing powers to localgovernment units under the Constitution and the LGCdoes not affect the power of Congress to grantexemptions to certain persons, pursuant to a declarednational policy. The legal effect of theconstitutional grant to local governments simply means

11

that in interpreting statutory provisions on municipaltaxing powers, doubts must be resolved in favor ofmunicipal corporations.” [Ibid., referring to Philippine LongDistance Telephone Company, Inc. (PLDT) vs. City of Davao]

13. General principles of incometaxation in the Philippines or the source ruleof income taxation as provided in the NIRC of1997.

a. A citizen of the Philippines residing thereinis taxable on all income derived from sources withinand without the Philippines;

b. A nonresident citizen is taxable only onincome derived from sources within the Philippines; c. An individual citizen of the Philippineswho is working and deriving income abroad as anoverseas contract worker is taxable only on incomefrom sources within the Philippines: Provided, That aseaman who is a citizen of the Philippines and whoreceives compensation for services rendered abroad asa member of the complement of a vessel engagedexclusively in international trade shall be treated asan overseas contract worker; d. An alien individual, whether a resident ornot of the Philippines, is taxable only on incomederived from sources within the Philippines; e. A domestic corporation is taxable on allincome derived from sources within and without thePhilippines; and f. A foreign corporation, whether engaged ornot in trade or business in the Philippines, istaxable only on income derived from sources within thePhilippines. (Sec. 23, NIRC of 1997, emphasis supplied)

14.Juliane a non-resident alien appointedas a commission agent by a domestic corporation

with a sales commission of 10% all sales actuallyconcluded and collected through her efforts. Thelocal company withheld the amount of P107,000from her sales commission and remitted the sameto the BIR.

She filed a claim for refund alleging thather sales commission is not taxable because thesame was a compensation for her services renderedin Germany and therefore considered as incomefrom sources outside the Philippines.

Is her contention correct ?SUGGESTED ANSWER: Yes. The important factor

which determines the source of income of personalservices is not the residence of the payor, or theplace where the contract for service is entered into,or the place of payment, but the place where theservices were actually performed.

Since the activity of securing the sales were inGermany, then the income did not originate from sourcesfrom within the Philippines. (Commissioner of Internal Revenue v.Baier-Nickel, G. R. No. 153793, August 29, 2006)

15. Ensite, Ltd.. is a Canadiancorporation not doing business in thePhilippines. It holds 40% of the shares ofPhilippine Stamping Plant, Inc.,., a Philippinecompany while the 60% is owned by FredCorporation, a Filipino-owned Philippinecorporation. Ensite Co. also owns 100% of theshares of Susanto Co., an Indonesian companywhich has a duly licensed Philippine branch. Dueto worldwide restructuring of the Ensite Ltd.,.group, Ensite Ltd.,. decided to sell all itsshares in Philippine Stamping Plant, Inc. andSusanto Co. The negotiations for the buy-out

12

and the signing of the Agreement of Sale wereall done in the Philippines. The Agreementprovides that the purchase price will be paid toEnsite Ltd’s bank account in the U.S. and thattitle to the Philippine Stamping Plant, Inc.and Susanto Co. shall be transferred to GeneralCo., in Toronto Canada where stock certificateswill be delivered. General Co. seeks youradvice as to whether or not it will subject thepayments of the purchase price to withholdingtax. Explain your advice. SUGGESTEDANSWER: The payments of the purchase price will besubject to withholding tax. Considering that all theactivities (sales) occurred within the Philippines,the income is considered as income from within,subject to Philippine income taxation. Ensite, Ltd.being a foreign corporation is to be taxed on itsincome derived from sources within the Philippines.

16.Ensite, Ltd. is a Canadian corporation,

which has a duly licensed Philippine branchengage in trading activities in the Philippines.Ensite, Ltd.. also invested directly in 40% ofthe shares of stock of Philippine StampingPlant, Inc.., a Philippine corporation. Theseshares are booked in the Head Office of Ensite,Ltd.. and are not reflected as assets of thePhilippine branch. In 2009, Philippine StampingPlant, Inc.. declared dividends to itsstockholders. Before remitting the dividends toEnsite Ltd.,., Philippine Stamping Plant, Inc.Co. seeks your advice as to whether it willsubject the remittance to withholding tax.There is no need to discuss WT rates, if

applicable. Focus your discussion on what isthe issue. SUGGESTEDANSWER: Philippine Stamping Plant, Inc.. shouldsubject the remittance to withholding tax.. SincePhilippine Stamping Plant. is a Philippinecorporation, its shares of stock have obtained abusiness situs in the Philippines, hence the dividendsare considered as income from within. Ensite. Ltd.,being a foreign corporation, should be subject to taxon its income from within.

17. Philippine Stamping Plant, Inc., aPhilippine corporation, has an executive Larrywho is a Filipino citizen. Philippine StampingPlant, Inc,. has a subsidiary in Malaysia (KualaLumpur Manufacturing, Inc.) and will assignLarry for an indefinite period to work full timefor Kuala Lumpur Manufacturing, Inc.. Larrywill bring his family to reside in Malaysia andwill lease out his residence in the Philippines.The salary of Larry will be shouldered 50% byPhilippine Stamping Plant, Inc.. while the other50% plus housing, cost of living and educationalallowances of Larry’s dependents will beshouldered by Kuala Lumpur Manufacturing, Inc..Philippine Stamping Plant, Inc.. will credit the50% of Larry’s salary to his Philippine bankaccount. Larry will sign the contract ofemployment in the Philippines. He will also bereceiving rental income for the lease of hisPhilippine residence.

Are these salaries, allowances andrentals subject to Philippine income tax?Explain briefly. SUGGESTEDANSWER: The salaries and allowances of Larry, being

13

derived from labor or personal services renderedoutside of the Philippines is considered as incomefrom without. Since Larry is an OCW, then he is to betaxed only on his income derived from within thePhilippines such as the rentals on his Philippineresidence, and not on his income from without.

18.Obama Airlines, Inc., a foreign airlinecompany which does not maintain any flight to andfrom the Philippines sold air tickets in thePhilippines, through a general sales agent,relating to the carriage of passengers and cargobetween two points, both outside the Philippines.

a. Is Obama, Inc., subject to income taxeson the sale of the tickets ?

SUGGESTED ANSWER: Yes. The source of incomewhich is taxable is that “activity” which produced theincome. The ”sale of tickets” in the Philippines isthe activity that determines whether such income istaxable in the Philippines.

The tickets exchanged hands here and payments forfares were also made here in Philippine currency. Thesitus of the source of payments is the Philippines.the flow of wealth proceeded from and occurred, withinthe Philippine territory, enjoying the protectionaccorded by the Philippine Government. In considerationof such protection, the flow of wealth should share theburden of supporting the government. [Commissioner ofInternal Revenue v. British Overseas Airways Corporation (BOAC), 149SCRA 395]

Off-line air carriers having general sales agentsin the Philippines are engaged in or doing business inthe Philippines and their income from sales ofpassage documents here is income from within thePhilippines. Thus, the off-line air carrier liable forthe 32% (now 30%) tax on its taxable income. [SouthAfrican Airways v. Commissioner of Internal Revenue, G.R. No. 180356,

February 16, 2010 citing Commissioner of Internal Revenue v. BritishOverseas Airways Corporation (British Overseas Airways), No. L-65773-74,April 30, 1987, 149 SCRA 395]

b. Supposing that Obama, Inc., sellstickets outside of the Philippines for passengersit carry from Gold City, South Africa to thePhilippines but returns to South Africa withoutany cargo or passengers. Would it then besubject to any Philippine tax on such sales ?

SUGGESTED ANSWER: It would not be subject to anytax. It is not subject to any income tax because theactivity which generated the income (the sale of thetickets) was performed outside of the Philippines.

It is not subject to the carrier’s tax based ongross Philippine billings because there were no liftsthat originated from the Philippines. “GrossPhilippine Billings” refers to the amount of grossrevenue derived from carriage of persons, excessbaggage, cargo and mail originating from thePhilippines in a continuous and uninterrupted flight,irrespective of the place of sale or issue and theplace of payment of the ticket or passage document.”[NIRC of 1997, Sec. 28(A)(3)(a)]

c. Would your answer be the same if Obama,Inc. sold tickets outside of the Philippines fortravelers who are going to picked up by Obama,Inc., planes from the Diosdado Macapagal Intl.Airport at Clark, Angeles, Pampanga, bound forNairobi, Kenya ? Reason out your answer.

SUGGESTED ANSWER: No more. This time Obama,Inc., would be subject to the carrier’s tax based onGross Philippine Billings. (GPB).

“Gross Philippine Billings” refers to the amountof gross revenue derived from carriage of persons,excess baggage, cargo and mail originating from thePhilippines in a continuous and uninterrupted flight,

14

irrespective of the place of sale or issue and theplace of payment of the ticket or passage document.”[NIRC of 1997, Sec. 28(A)(3)(a)]

The place of sale is irrelevant; as long as theuplifts of passengers and cargo occur from thePhilippines, income is included in GPB. (South AfricanAirways v. Commissioner of Internal Revenue, G.R. No. 180356, February16, 2010)

19. No improper delegation of legislativeauthority to tax. The power to tax is inherent inthe State, such power being inherently legislative,based on the principle that taxes are a grant of thepeople who are taxed, and the grant must be made bythe immediate representatives of the people; and wherethe people have laid the power, there it must remainand be exercised. (Commissioner of Internal Revenue v. FortuneTobacco Corporation, G. R. Nos. 167274-75, July 21, 2008)

CONSTITUTIONAL LIMITATIONS

1. Constitutional limitations on thepower of taxation . The general or indirectconstitutional limitations as well as the specific ordirect constitutional limitations.

2. The general or indirectconstitutional limitations on the power oftaxation are:

a. Due process clause;b. Equal protection clause;c. Freedom of the press;d. Religious freedom;e. No taking of private property without just

compensation;f. Non-impairment clause;

g. Law-making process:1) Bill should embrace only one subject

expressed in the title thereof;2) Three (3) readings on three separate

days;3) Printed copies in final form distributed

three (3) days before passage.h. Presidential power to grant reprieves,

commutations and pardons and remittal of fines andforfeiture after conviction by final judgment.

3. The specific or direct constitutionallimitation.

a. No imprisonment for non-payment of a poll tax;

b. Taxation shall be uniform and equitable;c. Congress shall evolve a progressive system of

taxation;d. All appropriation, revenue or tariff bills

shall originate exclusively in the House of Representatives, but the Senate may propose and concur with amendments;

e. The President shall have the power to veto anyparticular item or items in an appropriation, revenue,or tariff bill, but the veto shall not affect the itemor items to which he does not object;

f. Delegated power of the President to imposetariff rates, import and export quotas, tonnage andwharfage dues:

1) Delegation by Congress2) through a law3) subject to Congressional limits and

restrictions4) within the framework of national

development program.g. Tax exemption of charitable institutions,

churches, parsonages and convents appurtenant thereto,

15

mosques, and all lands, buildings and improvements ofall kinds actually, directly and exclusively used forreligious, charitable or educational purposes;

h. No tax exemption without the concurrence ofmajority vote of all members of Congress;

i. No use of public money or property forreligious purposes except if priest is assigned to thearmed forces, penal institutions, government orphanageor leprosarium;

j. Money collected on tax levied for a specialpurpose to be used only for such purpose, balance ifany, to general funds;

k. The Supreme Court's power to review judgmentsor orders of lower courts in all cases involving thelegality of any tax, impose, assessment or toll or thelegality of any penalty imposed in relation to theabove;

l. Authority of local government units to createtheir own sources of revenue, to levy taxes, fees andother charges subject to guidelines and limitationsimposed by Congress consistent with the basic policy oflocal autonomy;

m. Automatic release of local government's justshare in national taxes;

n. Tax exemption of all revenues and assets ofnon-stock, non-profit educational institutions usedactually, directly and exclusively for educationalpurposes;

o. Tax exemption of all revenues and assets ofproprietary or cooperative educational institutionssubject to limitations provided by law includingrestrictions on dividends and provisions forreinvestment of profits;

p. Tax exemption of grants, endowments,donations or contributions used actually, directly andexclusively for educational purposes subject toconditions prescribed by law.

5. Equal protection of the law clause issubject to reasonable classification. If thegroupings are characterized by substantial distinctionsthat make real differences, one class may be treatedand regulated differently from another. Theclassification must also be germane to the purpose ofthe law and must apply to all those belonging to thesame class. (Tiu, et al., v. Court of Appeals, et al., G.R. No. 127410,January 20, 1999)

6. Requisites for validclassification. All that is required of a validclassification is that it be reasonable, which meansthat a. the classification should be based onsubstantial distinctions which make for realdifferences,

b. that it must be germane to the purpose of thelaw;

c. that it must not be limited to existingconditions only; and

d. that it must apply equally to each member ofthe class.

The standard is satisfied if the classificationor distinction is based on a reasonable foundation orrational basis and is not palpably arbitrary. [ABAKADAGuro Party List, etc., v. Purisima, etc., et al., G. R. No. 166715, August14, 2008]

7. Equal protection does not demandabsolute equality. It merely requires that allpersons shall be treated alike, under likecircumstances and conditions, both as to theprivileges conferred and liabilities enforced. (Santos v.People, et al, G. R. No. 173176, August 26, 2008)

It is imperative to duly establish that the oneinvoking equal protection and the person to which she

16

is being compared were indeed similarly situated, i.e.,that they committed identical acts for which they werecharged with the violation of the same provisions ofthe NIRC; and that they presented similar argumentsand evidence in their defense - yet, they were treateddifferently. (Santos, supra)

8. Tests to determine validity ofclassification. The United States Supreme Courthas established different tests to determine thevalidity of a classification and compliance with theequal protection clause. The recognized tests are: a. The traditional (or rational basis)test. b. The strict scrutiny (or compellinginterest) test. c. The intermediate level of scrutiny (orquasi-suspect class) test.

9. The traditional (or rational basis) testused in order to determine the validity ofclassification. The classification is valid if itis rationally related to a constitutionallypermissible state interest.

The complainant must prove that theclassification is “invidous,” “wholly arbitrary,” or”capricious,” otherwise the classification is presumedto be valid. (Lindsley v. Natural Carboinic Gas Co., 220 U.S. 61;McGowan v. Maryland, 366 U.S. 420; United States Railroad RetirementBoard v. Fritz, 449 U.S. 166)

10. The strict scrutiny (or compellinginterest) test used in order to determine thevalidity of the classification. Governmentregulation that intentionally discriminates against a“suspect class” such as racial or ethnic minorities,is subject to strict scrutiny and considered to

violate the equal protection clause unless foundnecessary to promote a compelling state interest.

A classification is necessary when it is narrowlydrawn so that no alternative, less burdensome means isavailable to accomplish the state interest.

Thus, it was held that denial of free publiceducation to the children of illegal aliens imposes anenormous and lasting burden based on a status overwhich the children have no control is violative ofequal protection because there is no showing that suchdenial furthers a “substantial” state goal. (Plyler v.Doe, 457 U.S. 202)

11. The intermediate level of scrutiny (orquasi-suspect class) test used in order todetermine the validity of he classification.Classification based on gender or legitimacy are not“suspect,” but neither are they judged by thetraditional or rational basis test.

Intentional discriminations against members of aquasi-suspect class violate equal protection unlessthey are substantially related to important governmentobjectives. (Craig v. Boren, 429 U.S. 190)

Thus, a state law granting a property taxexemption to widows, but not widowers, has been heldvalid for it furthers the state policy of cushioningthe financial impact of spousal loss upon the sex forwhom that loss usually imposes a heavier burden. (Kahnv. Shevin, 416 U.S. 351)

12. Equality and uniformity of taxationmay mean the same as equal protection. In such acase, the terms would mean that all subjects andobjects of taxation which are similarly situated shallbe subject to the same burdens and granted the sameprivileges without any discrimination whatsoever.

17

13. It is inherent in the power to taxthat the State be free to select the subjects oftaxation, and it has been repeatedly held that,"inequalities which result from a singling out of oneparticular class of taxation, or exemption, infringe noconstitutional limitation." (Commissioner of Internal Revenue,et al., v. Santos, et al., 277 SCRA 617)

9. Benjie is a law-abiding citizen whopays his real estate taxes promptly. Due to aseries of typhoons and adverse economicconditions, an ordinance is passed by SolimanCity granting a 50% discount for payment ofunpaid real estate taxes for the preceding yearand the condonation of all penalties on finesresulting from the late payment.

Arguing that the ordinance rewardsdelinquent tax payers and discriminates againstprompt ones, Benjie demands that he be refundedan amount equivalent to one-half of the realproperty taxes he paid. The municipal attorneyrendered an opinion that Benjie cannot bereimbursed because the ordinance did not providefor such reimbursement. Benjie files suit todeclare the ordinance void on the ground that itis a class legislation. Will his suit prosper ?Explain your answer briefly.

SUGGESTED ANSWER: No. There is no classlegislation because there is no violation of the equalprotection suit. There is a valid classificationbetween those who already paid their taxes and thosewho have not. Furthermore, the taxing authority hasthe prerogative to select the subjects and objects oftaxation, including granting a 50% discount in thepayment of unpaid real estate taxes, and the

condonation of all penalties on fines resulting fromlate payment.

10. The rewards law to tax collectors doesnot violate equal protection. The equalprotection clause recognizes a valid classification,that is, a classification that has a reasonablefoundation or rational basis and not arbitrary. Withrespect to RA 9335, it’s expressed public policy isthe optimization of the revenue-generation capabilityand collection of the BIR and the BOC. Since thesubject of the law is the revenue- generationcapability and collection of the BIR and the BOC, theincentives and/or sanctions provided in the law shouldlogically pertain to the said agencies. Moreover, thelaw concerns only the BIR and the BOC because theyhave the common distinct primary function ofgenerating revenues for the national governmentthrough the collection of taxes, customs duties, feesand charges.

Indubitably, such substantial distinction isgermane and intimately related to the purpose of thelaw. Hence, the classification and treatment accordedto the BIR and the BOC under RA 9335 fully satisfy thedemands of equal protection. (ABAKADA Guro Party List, etc., v.Purisima, etc., et al., G. R. No. 166715, August 14, 2008)

11. The prosecution of one guilty personwhile others equally guilty are not prosecuted,however, is not, by itself, a denial of theequal protection of the laws. Where the officialaction purports to be in conformity to the statutoryclassification, an erroneous or mistaken performanceof the statutory duty, although a violation of thestatute, is not without more a denial of the equalprotection of the laws.

18

The unlawful administration by officers of astatute fair on its face, resulting in its unequalapplication to those who are entitled to be treatedalike, is not a denial of equal protection unlessthere is shown to be present in it an element ofintentional or purposeful discrimination. This mayappear on the face of the action taken with respect toa particular class or person, or it may only be shownby extrinsic evidence showing a discriminatory designover another not to be inferred from the actionitself. (Santos v. People, et al, G. R. No. 173176, August 26, 2008)

12. Equal protection should not be used toprotect commission of crime. While all personsaccused of crime are to be treated on a basis ofequality before the law, it does not follow that theyare to be protected in the commission of crime. Itwould be unconscionable, for instance, to excuse adefendant guilty of murder because others havemurdered with impunity.

Likewise, if the failure of prosecutors toenforce the criminal laws as to some persons should beconverted into a defense for others charged withcrime, the result would be that the trial of thedistrict attorney for nonfeasance would become anissue in the trial of many persons charged withheinous crimes and the enforcement of law would suffera complete breakdown. (Santos v. People, et al, G. R. No. 173176,August 26, 2008)

13. Illustration of double taxation inlocal taxation. there is indeed double taxation ifCoca-Cola is subjected to the taxes under bothSections 14 and 21 of Tax Ordinance No. 7794, sincethese are being imposed: (1) on the same subjectmatter – the privilege of doing business in the City

of Manila; (2) for the same purpose – to make personsconducting business within the City of Manilacontribute to city revenues; (3) by the same taxingauthority – City of Manila; (4) within the sametaxing jurisdiction – within the territorialjurisdiction of the City of Manila; (5) for the sametaxing periods – per calendar year; and (6) of thesame kind or character – a local business tax imposedon gross sales or receipts of the business. (The City ofManila, et al., v. Coca-Cola Bottlers Philippines, Inc., G. R. No. 181845,August 4, 2009)

14. A lawful tax on a new subject, or anincreased tax on an old one, does not interferewith a contract or impairs its obligation, withinthe meaning of the constitution. (Tolentino v. Secretary ofFinance, et al., and companion cases, 235 SCRA 630) 15. The withdrawal of a taxexemption should not be construed as prohibitingfuture grants of exemption from all taxes.(Philippine Long Distance Telephone Company, Inc., v. City of Davao, et al., etc., G.R. No. 143867, August 22, 2001)

16. Tax exemptions in franchises are alwayssubject to withdrawal. A legislative franchise isgranted with the express condition that it is subjectto amendment, alteration, or repeal. (1987 Constitution,Art. XII, Sec. 11)

It is enough to say that the parties to acontract cannot, through the exercise of propheticdiscernment, fetter the exercise of the taxing powerof the State. For not only are existing laws read intocontracts in order to fix obligations as betweenparties, but the reservation of essential attributesof sovereign power is also read into contracts as abasic postulate of the legal order. The policy of

19

protecting contracts against impairment presupposesthe maintenance of a government which retains adequateauthority to secure the peace and good order ofsociety. (Smart Communications, Inc. v. The City of Davao, etc., et al., G.R. No. 155491, September 16, 2008)

NOTES AND COMMENTS: Philippine Long Distance TelephoneCompany, Inc., v. City of Davao, et al., etc., G. R. No. 143867, August 22,2001 made the observation that since Smart’s franchise wasgranted after the effectivity of the Local Government Codethat its tax exemption privilege was reinstated. However,Smart Communications, Inc. v. The City of Davao, etc., et al., G. R. No.155491, September 16, 2008 is explicit in its holding thatSmart is not entitled to a tax exemption.

17. When withdrawal of a tax exemptionimpairs the obligation of contracts. The ContractClause has never been thought as a limitation on theexercise of the State’s power of taxation save onlywhere a tax exemption has been granted for a validconsideration. (Smart Communications, Inc. v. The City of Davao, etc., etal., G. R. No. 155491, September 16, 2008) citing Tolentino v.Secretary of Finance, G. R. No. 115455, August 25, 1994, 235 SCRA630, 685) The author opines that since practically allfranchises granted to telecommunications companies aresimilarly worded that the above doctrine findsapplication to the others)

18. The primary reason for the withdrawalof tax exemption privileges granted to governmentowned and controlled corporations and all otherunits of government was that such privilege resulted toserious tax base erosion and distortions in the taxtreatment of similarly situated enterprises, henceresulting in the need for these entities to share inthe requirements of development, fiscal or otherwise,by paying the taxes and other charges due them.(Philippine Ports Authority v. City of Iloilo, G. R. No. 109791, July 14,2003)

19. National Power Corporation (NPC) is ofthe insistence that it is not subject to thepayment of franchises taxes imposed by theProvince of Isabela because all of its shares areowned by the Republic of the Philippines. It isthus, an instrumentality of the NationalGovernment which is exempt from local taxation.As such it is not a private corporation engagedin “business enjoying franchise”

Is such contention meritorious ?SUGGESTED ANSWER: No. Philippine Long Distance

Telephone Company, Inc., v. City of Davao, et al., etc., G. R. No.143867, August 22, 2001, upheld the authority of theCity of Davao, a local government unit, to impose andcollect a local franchise tax because the LocalGovernment Code has withdrawn all tax exemptionspreviously enjoyed by all persons and authorized localgovernment units to impose a tax on business enjoying afranchise tax notwithstanding the grant of taxexemption to them.

20. “In lieu of all taxes” in the franchiseof ABS-CBN does not exempt it from localfranchise taxes. It does not expressly provide whatkind of taxes ABS-CBN is exempted from. It is notclear whether the exemption would include both local,whether municipal, city or provincial, and nationaltax. Whether the “in lieu of all taxes provision”would include exemption from local tax is notunequivocal.

The right to exemption from local franchise taxmust be clearly established and cannot be made out ofinference or implications but must be laid beyondreasonable doubt. Verily, the uncertainty in the “inlieu of all taxes” provision should be construed

20

against ABS-CBN. ABS-CBN has the burden to prove thatit is in fact covered by the exemption so claimed buthas failed to do so. (Quezon City, et al., v. ABS-CBN BroadcastingCorporation, G. R. No. 166408, October 6, 2008)

NOTES AND COMMENTS: This is practically the sameholding in an earlier case involving anothertelecommunications company Smart Communications, Inc. v. The City ofDavao, etc., et al., G. R. No. 155491, September 16, 2008. Theauthor opines that since practically all franchises grantedto telecommunications companies are similarly worded thatthe above doctrine finds application to the others.)

21. “In lieu of all taxes” refers tonational internal revenue taxes and not to localtaxes. The “in lieu of all taxes” clause appliesonly to national internal revenue taxes and not tolocal taxes. As appropriately pointed out in theseparate opinion of Justice Antonio T. Carpio in asimilar case involving a demand for exemption fromlocal franchise taxes:

[T]he "in lieu of all taxes" clause in Smart'sfranchise refers only to taxes, other than income tax,imposed under the National Internal Revenue Code. The"in lieu of all taxes" clause does not apply to localtaxes. The proviso in the first paragraph of Section 9of Smart's franchise states that the grantee shall"continue to be liable for income taxes payable underTitle II of the National Internal Revenue Code." Also,the second paragraph of Section 9 speaks of taxreturns filed and taxes paid to the "Commissioner ofInternal Revenue or his duly authorized representativein accordance with the National Internal RevenueCode." Moreover, the same paragraph declares that thetax returns "shall be subject to audit by the Bureauof Internal Revenue." Nothing is mentioned in Section9 about local taxes. The clear intent is for the "inlieu of all taxes" clause to apply only to taxes under

the National Internal Revenue Code and not to localtaxes. Even with respect to national internal revenuetaxes, the "in lieu of all taxes" clause does notapply to income tax.

If Congress intended the "in lieu of all taxes"clause in Smart's franchise to also apply to localtaxes, Congress would have expressly mentioned theexemption from municipal and provincial taxes.Congress could have used the language in Section 9(b)of Clavecilla's old franchise, as follows:

x x x in lieu of any and all taxes of any kind,nature or description levied, established or collectedby any authority whatsoever, municipal, provincial ornational, from which the grantee is hereby expresslyexempted, x x x. (Emphasis supplied).

However, Congress did not expressly exempt Smartfrom local taxes. Congress used the "in lieu of alltaxes" clause only in reference to national internalrevenue taxes. The only interpretation, under the ruleon strict construction of tax exemptions, is that the"in lieu of all taxes" clause in Smart's franchiserefers only to national and not to local taxes.[Smart Communications, Inc. v. The City of Davao, etc., et al., G. R. No.155491, September 16, 2008 citing Philippine Long DistanceTelephone Company, Inc. v. City of Davao, 447 Phil. 571, 594 (2003)]

NOTES AND COMMENTS: The author opines that theabove finds application to all telecommunicationscompanies.

22. The “in lieu of all taxes” clause in thefranchise of ABS-CBN has become functus officiowith the abolition of the franchise tax onbroadcasting companies with yearly grossreceipts exceeding Ten Million Pesos. The clause“in lieu of all taxes” does not pertain to VAT or anyother tax. It cannot apply when what is paid is a taxother than a franchise tax. Since the franchise tax

21

on the broadcasting companies with yearly grossreceipts exceeding ten million pesos has beenabolished, the “in lieu of all taxes” clause has nowbecome functus officio, rendered inoperative. (Quezon City, etal., v. ABS-CBN Broadcasting Corporation, G. R. No. 166408, October6, 2008)

NOTES AND COMMENTS: This is practically the sameholding in an earlier case involving anothertelecommunications company. Smart Communications, Inc. v.The City of Davao, etc., et al., G. R. No. 155491,September 16, 2008. The author opines that sincepractically all franchises granted to telecommunicationscompanies are similarly worded that the above doctrinefinds application to the others.)

23. Double taxation in its genericsense, this means taxing the same subject orobject twice during the same taxable period. Inits particular sense, it may mean direct duplicatetaxation, which is prohibited under the constitutionbecause it violates the concept of equal protection,uniformity and equitableness of taxation. Indirectduplicate taxation is not anathematized by the aboveconstitutional limitations.

24. Elements of direct duplicatetaxation:

a. Same1) Subject or object is taxed twice 2) by the same taxing authority3) for the same taxing purpose4) during the same taxable period

b. Taxing all of the subjects or objectsfor the first time without taxing all of them for thesecond time.

If any of the elements are absent then there isindirect duplicate taxation which is not prohibited bythe constitution.

NOTES AND COMMENTS: a. Presence of the 2 nd element violates the equal

protection clause. If only the 1st element is present,taxing the same subject or object twice, by the same taxingauthority, etc., there is no violation of the equalprotection clause because all subjects and objects that aresimilarly situated are subject to the same burdens andgranted the same privileges without any discriminationwhatsoever,

The presence of the 2nd element, taxing all of thesubjects and objects for the first time, without taxing allfor the second time, results to discrimination amongsubjects and objects that are similarly situated, henceviolative of the equal protection clause.

25. Double taxation a valid defense againstthe legality of a tax measure if the doubletaxation is direct duplicate taxation, because itwould violate the equal protection clause of theconstitution.

26. When an item of income is taxed inthe Philippines and the same income is taxed inanother country, this would be known asinternational juridical double taxation which isthe imposition of comparable taxes in two or morestates on the same taxpayer in respect of the samesubject matter and for identical grounds. (Commissioner ofInternal Revenue v. S.C. Johnson and Son, Inc., et al., G.R. No. 127105,June 25, 1999)

27. Methods for avoiding double taxation(indirect duplicate taxation).

a. Tax treaties which exempts foreign nationalsfrom local taxation and local nationals from foreigntaxation under the principle of reciprocity.

22

b. Tax credits where foreign taxes are allowedas deductions from local taxes that are due to be paid.

c. Allowing foreign taxes as a deduction fromgross income.

28. Tax credit generally refers to an amountthat is subtracted directly from one’s total taxliability, an allowance against the tax itself, or adeduction from what is owned.

A tax credit reduces the tax due, including –whenever applicable – the income tax that is determinedafter applying the corresponding tax rates to taxableincome. (Commissioner of Internal Revenue v. Central Luzon DrugCorporation, G. R. No. 159647, April 15, 2005)

29. A tax deduction is defined as a subtractionfro income for tax purposes, or an amount that isallowed by law to reduce income prior to theapplication of the tax rate to compute the amount oftax which is due.

A tax deduction reduces the income that is subjectto tax in order to arrive at taxable income. (Commissionerof Internal Revenue v. Central Luzon Drug Corporation, G. R. No. 159647,April 15, 2005)

30. The petitioners allege that the R-VAT law is constitutional because the BicameralConference Committed has exceeded its authorityin including provisions which were never includedin the versions of both the House and Senate suchas inserting the stand-by authority to thePresident to increase the VAT from 10% to 12%;deleting entirely the no pass-on provisions foundin both the House and Senate Bills; inserting theprovision imposing a 70% limit on the amount ofinput tax to be credited against the output tax;

and including the amendments introduced only bySenate Bill No. 1950 regarding other kinds oftaxes in addition to the value-added tax. Thus,there was a violation of the constitutionalmandate that revenue bills shall originateexclusively from the House of Representatives.

Are the contentions of such weight as toconstitute grave abuse of discretion which mayinvalidate the law ? Explain briefly.

SUGGESTED ANSWER: No. There was no grave abuseof discretion because all the changes andmodifications made by the Bicameral ConferenceCommittee were germane to subjects of the provisionsreferred to it for reconciliation.

The Bicameral Conference Committee merelyexercised the judicially recognized long-standinglegislative practice of giving said conferencecommittee ample latitude for compromising differencesbetween the Senate and the House. [Abakada Guro Party List(etc.) v. Ermita, etc., et al., G. R. No. 168056, September 1, 2005 andcompanion cases]

31. The VAT while regressive is NOTviolative of the mandate to evolve a progressivesystem of taxation. Do you agree ? The mandateto Congress is not to prescribe but to evolve aprogressive system of taxation. Otherwise, sales taxeswhich perhaps are the oldest form of indirect taxes,would have been prohibited with the proclamation of theconstitutional provision. Sales taxes are alsoregressive. . [Abakada Guro Party List (etc.) v. Ermita, etc., et al., G. R.No. 168056, September 1, 2005 and companion cases citingTolentino v. Secretary of Finance, et al., G. R. No. 115455, August 25,1994, 235 SCRA 630]

23

32. All revenues and assets of non-stock, non-profit educational institutions thatare actually, directly and exclusively used foreducational purposes shall be exempt fromtaxation.

33. Revenues and assets of proprietaryeducational institutions, including those whichare cooperatively owned, may be entitled toexemptions subject to limitations provided by lawincluding restrictions on dividends andprovisions for reinvestments. There is no law atthe present which grants exemptions, other theexemptions granted to cooperatives.

OTHER CONCEPTS

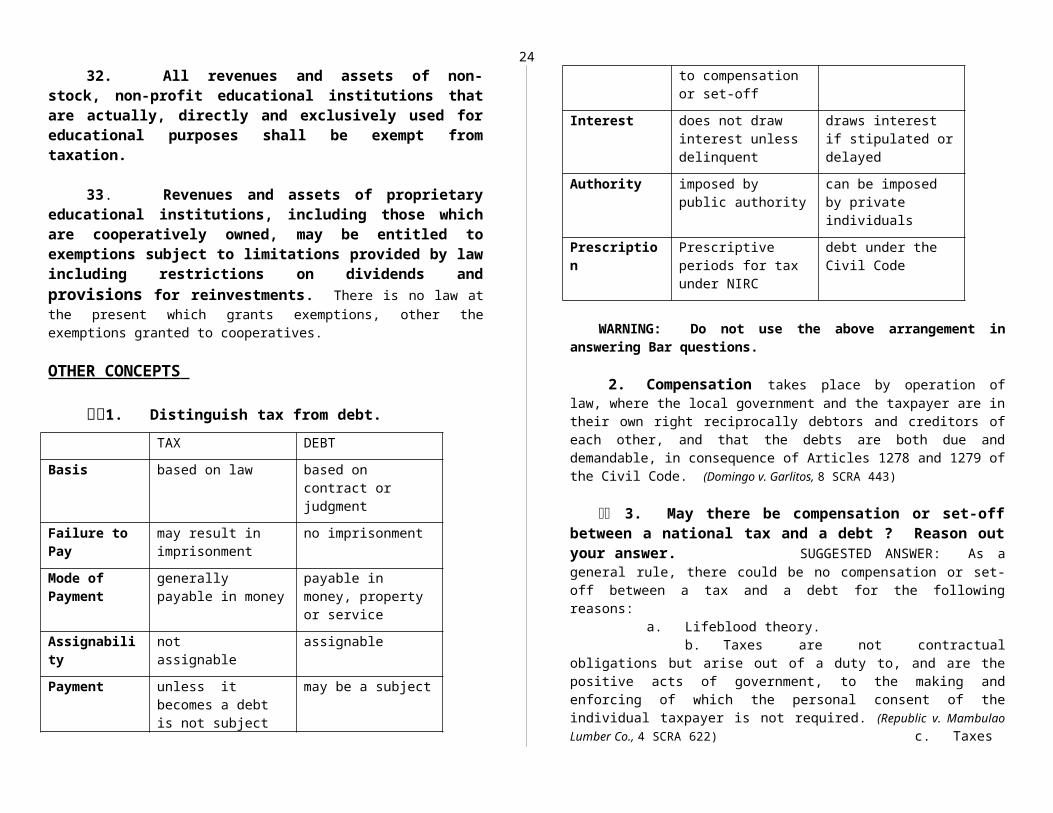

1. Distinguish tax from debt. TAX DEBT

Basis based on law based on contract or judgment

Failure to Pay

may result in imprisonment

no imprisonment

Mode of Payment

generally payable in money

payable in money, property or service

Assignability

not assignable

assignable

Payment unless it becomes a debt is not subject

may be a subject

to compensation or set-off

Interest does not draw interest unless delinquent

draws interest if stipulated ordelayed

Authority imposed by public authority

can be imposed by private individuals

Prescription

Prescriptive periods for tax under NIRC

debt under the Civil Code

WARNING: Do not use the above arrangement inanswering Bar questions.

2. Compensation takes place by operation oflaw, where the local government and the taxpayer are intheir own right reciprocally debtors and creditors ofeach other, and that the debts are both due anddemandable, in consequence of Articles 1278 and 1279 ofthe Civil Code. (Domingo v. Garlitos, 8 SCRA 443)

3. May there be compensation or set-offbetween a national tax and a debt ? Reason outyour answer. SUGGESTED ANSWER: As ageneral rule, there could be no compensation or set-off between a tax and a debt for the followingreasons:

a. Lifeblood theory. b. Taxes are not contractual

obligations but arise out of a duty to, and are thepositive acts of government, to the making andenforcing of which the personal consent of theindividual taxpayer is not required. (Republic v. MambulaoLumber Co., 4 SCRA 622) c. Taxes

24

cannot be the subject of compensation because thegovernment and taxpayer are not mutually creditors anddebtors of each other and a claim for taxes is notsuch a debt, demand, contract or judgment as isallowed to be set-off.

Thus, it is correct to say that the offsettingof a taxpayer’s tax refund with its alleged taxdeficiency is unavailing under Art. 1279 of the CivilCode. (South African Airways v. Commissioner of Internal Revenue, G.R.No. 180356, February 16, 2010 reiterating Caltex Philippines,Inc. v. Commission on Audit, which applied Francia v. IntermediateAppellate Court)

4. Exceptions: When set-off or compensationallowed for local taxes.

a. Where both claims already become overdueand demandable as well as fully liquidated.Compensation takes place by operation of law underArt. 1200 in relation to Arts. 1279 and 1290 all ofthe Civil Code. (Domingo v. Garlitos, 8 SCRA 443)

b. Compensation takes place byoperation of law, where the government and thetaxpayer are in their own right reciprocally debtorsand creditors of each other, and that the debts areboth due and demandable. This is in consequence ofArticle 1278 and 1279 of the Civil Code. (Domingo v.Garlitos, 8 SCRA 443) c.

,The Supreme Court upheld the validity of a set-off between the taxpayer and the government. In bothcases, the claims of the taxpayers therein werecertain and liquidated. The claims were certain sincethere were no doubts or disputes as to theirrefundability. In fact, the government admitted thefact of over-payment. (Commissioner of Internal Revenuev. Esso Standard Eastern, Inc., 172 SCRA 364) d. Incase of a tax overpayment, the BIR’s obligation to

refund or off-set arises from the moment the tax waspaid. REASON: Solutio indebeti. (Commissioner of Internal Revenue v.Esso Standard Eastern, Inc 172 SCRA 364)

e. While judgmentshould be rendered in favor of Republic for unpaidtaxes, judgment ought at the same time to issue forSampaguita Pictures commanding payment to the latterby the Republic of the value of the backpaycertificates which the Republic received. (Republic v.Ericta, 172 SCRA 623)