Domestic Gas Scenario Processing, Distribution & Applications A K Deb Head Business Development &JV Group – ONGC Offshore India – Oil & Gas Summit Hyatt Regency, Mumbai September 22 nd , 2009 Petrofed Industry-Academia Wor kshop PLL LNG Terminal, Dahej October 19 , 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 1/48

Domestic Gas Scenario

Processing, Distribution&

Applications

A K Deb

Head Business Development &JV Group –

ONGC

Offshore India – Oil & Gas SummitHyatt Regency, MumbaiSeptember 22nd , 2009

Petrofed Industry-Academia WorkshopPLL LNG Terminal, Dahej

October 19 , 2011

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 2/48

Why Natural Gas ?

Lower GHG emissions

Reduced Environment Footprints

amongst energy sources

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 3/48

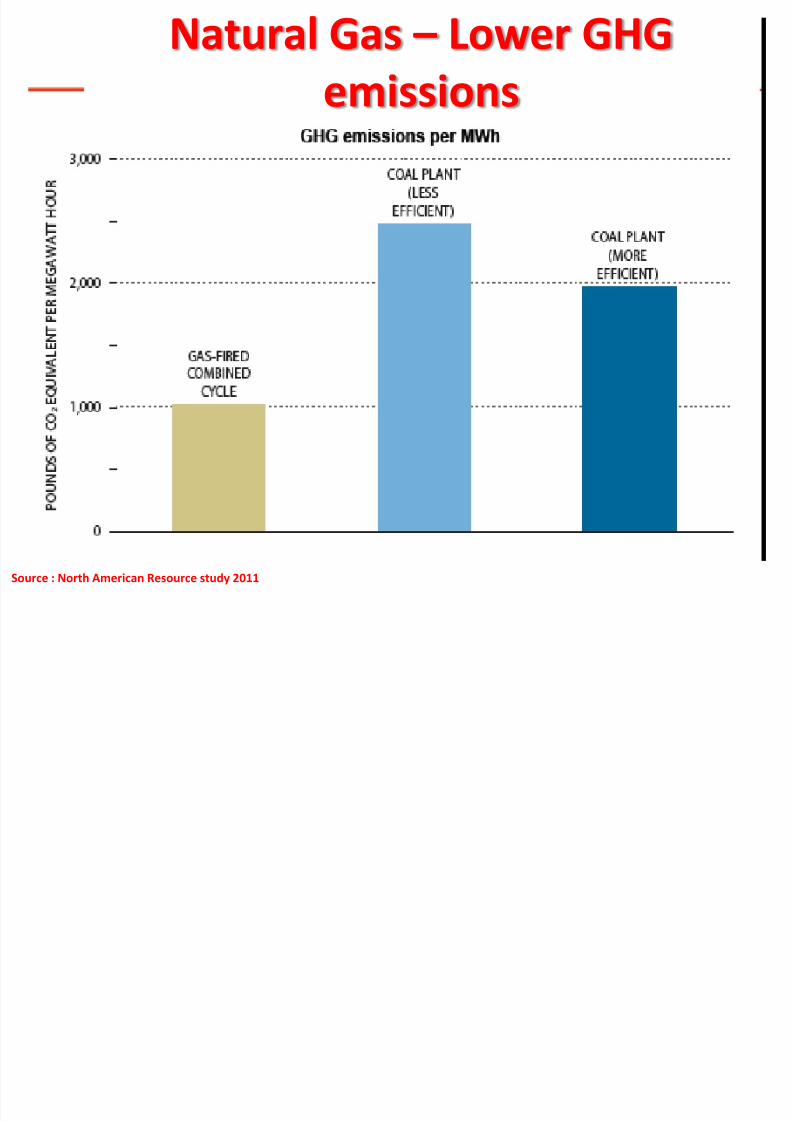

Natural Gas – Lower GHG

emissions

Source : North American Resource study 2011

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 4/48

Estimates of Environment Footprints of

Energy sources

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 5/48

Global Energy Scenario

The Canvass……

Natural Gas(NG) sources & ProcessingAssociated & Free NG / Rich or Lean Gas

Application and End Users

Characteristics of Indian NG market & Challenges

Coal Bed Methane gas

Shale Gas

Gas Resources/reserves & Supply scenario

Domestic Gas Scenario

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 6/48

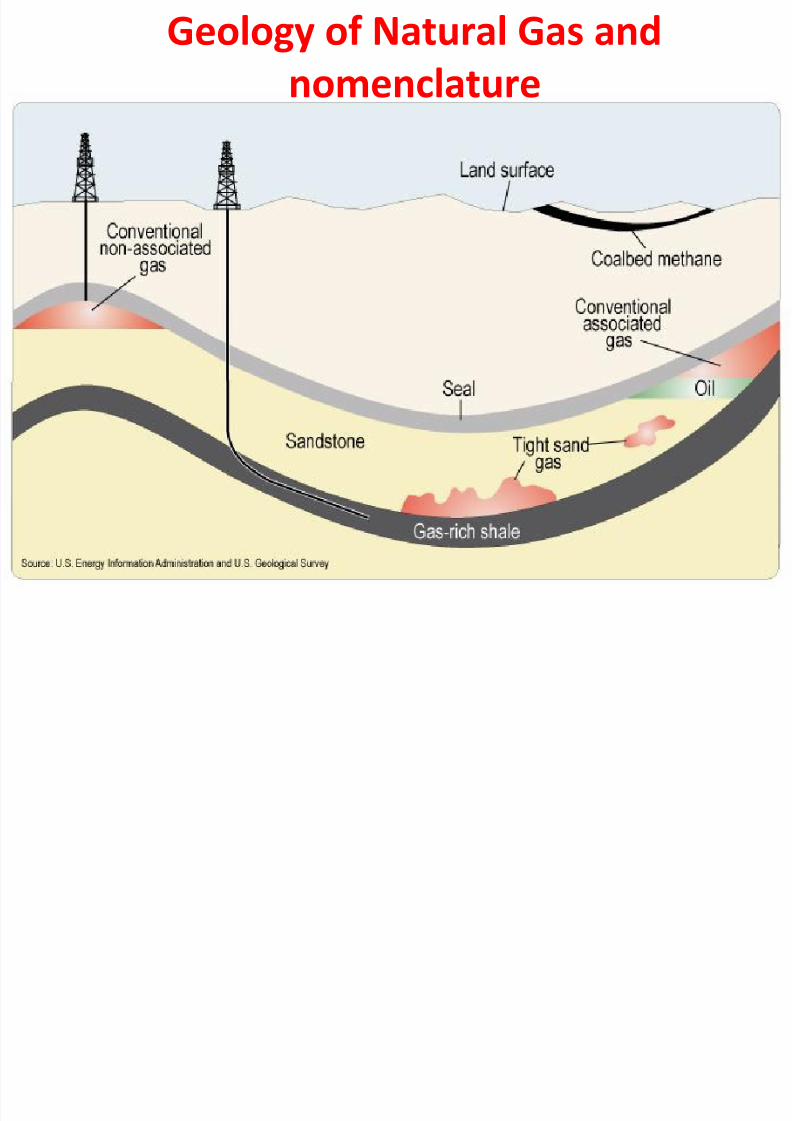

Geology of Natural Gas and

nomenclature

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 7/48

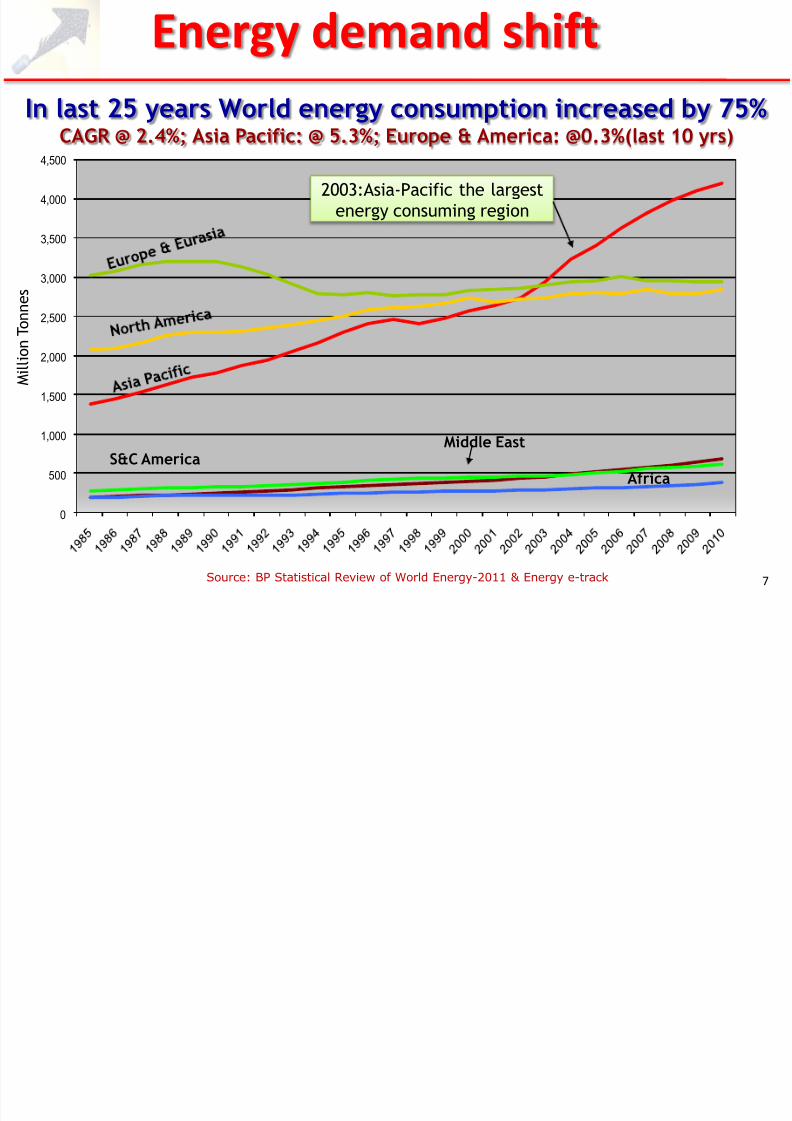

Energy demand shift

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Middle EastS&C America

Africa

In last 25 years World energy consumption increased by 75%

CAGR @ 2.4%; Asia Pacific: @ 5.3%; Europe & America: @0.3%(last 10 yrs)

2003:Asia-Pacific the largest

energy consuming region

M i l l i o n T o n n e s

Source: BP Statistical Review of World Energy-2011 & Energy e-track 7

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 8/48

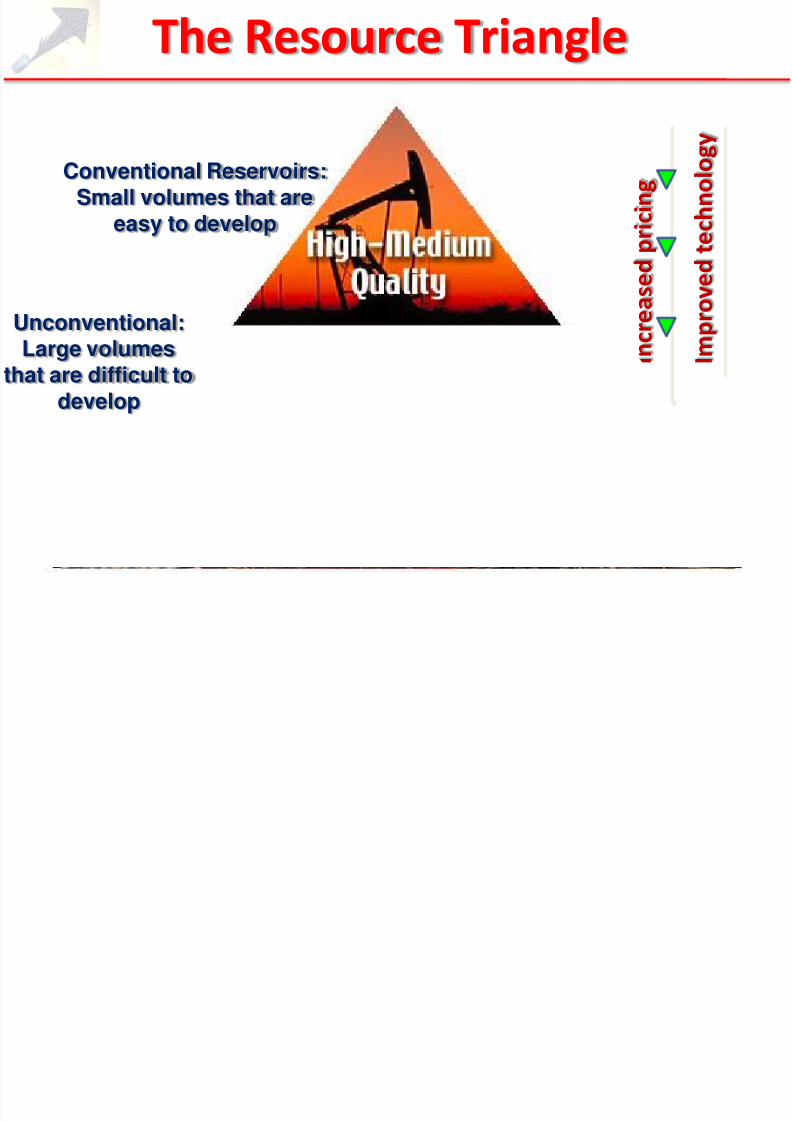

The Resource Triangle

Conventional Reservoirs:Small volumes that are

easy to develop

I m p r o v e d t e c h n o l o g y

I n c r e a s e d p r i c i n g

Unconventional:Large volumes

that are difficult todevelop

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 9/48

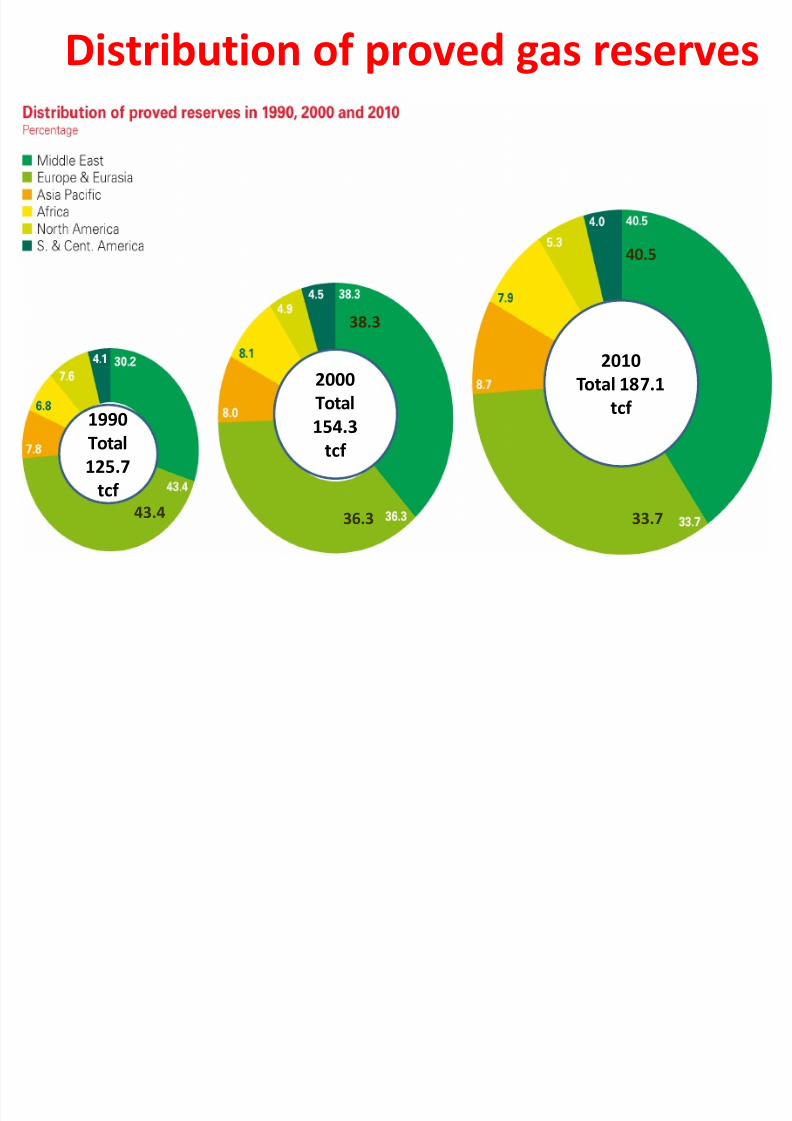

Distribution of proved gas reserves

2010

Total 187.1

tcf

2000

Total

154.3

tcf

1990Total

125.7

tcf

40.5

33.736.343.4

38.3

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 10/48

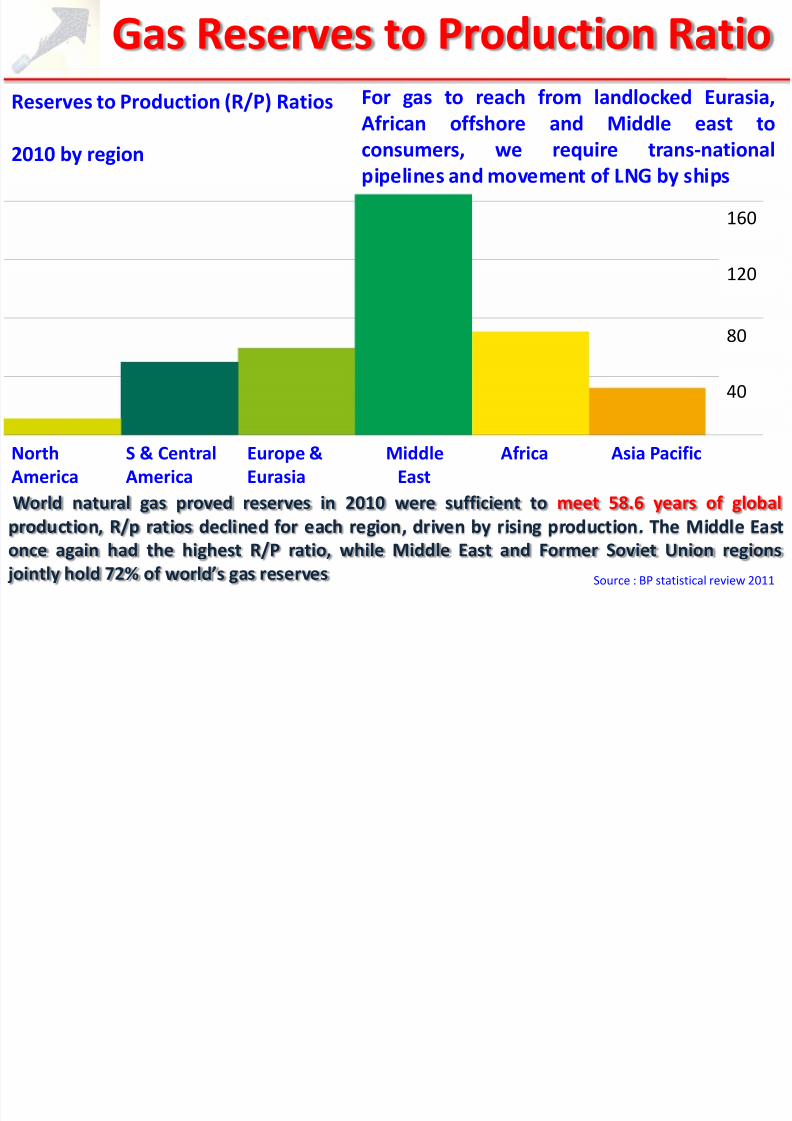

Gas Reserves to Production Ratio

World natural gas proved reserves in 2010 were sufficient to meet 58.6 years of global

production, R/p ratios declined for each region, driven by rising production. The Middle East

once again had the highest R/P ratio, while Middle East and Former Soviet Union regions jointly hold 72% of world’s gas reserves

North S & Central Europe & Middle Africa Asia Pacific

America America Eurasia East

Reserves to Production (R/P) Ratios

2010 by region

40

80

120

160

Source : BP statistical review 2011

For gas to reach from landlocked Eurasia,

African offshore and Middle east to

consumers, we require trans-national

pipelines and movement of LNG by ships

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 11/48

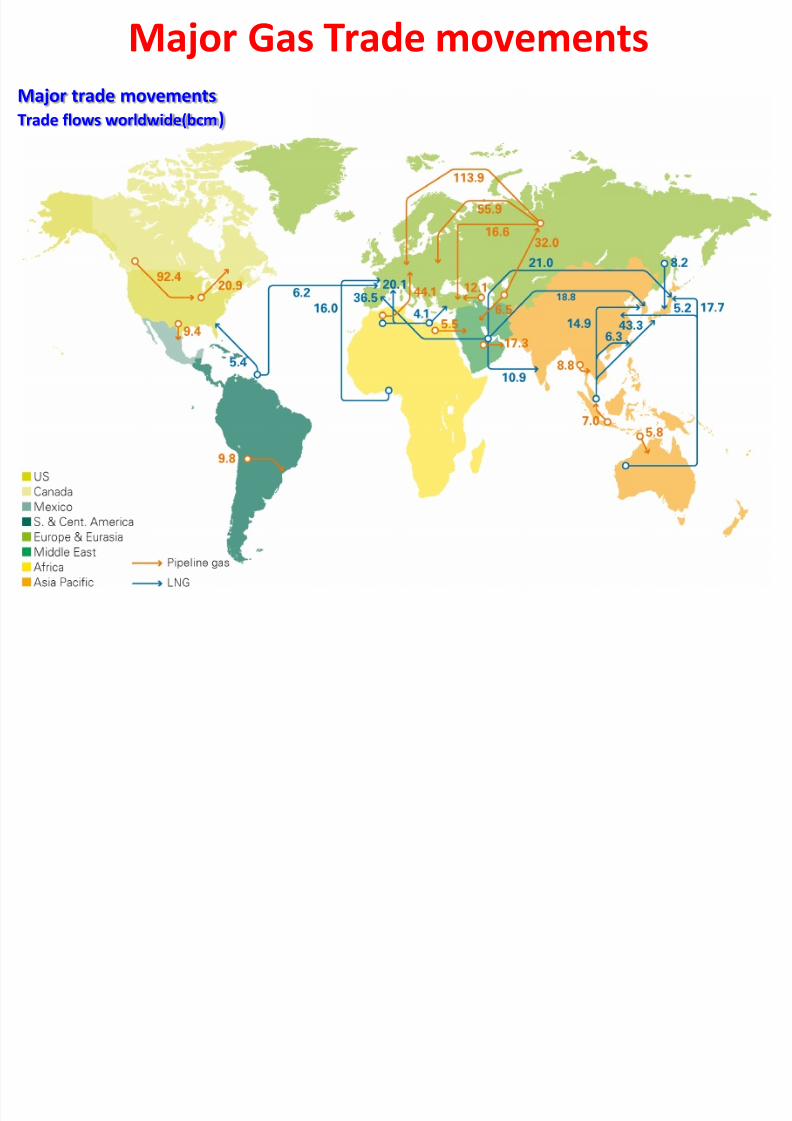

Major Gas Trade movements

Major trade movements

Trade flows worldwide(bcm)

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 12/48

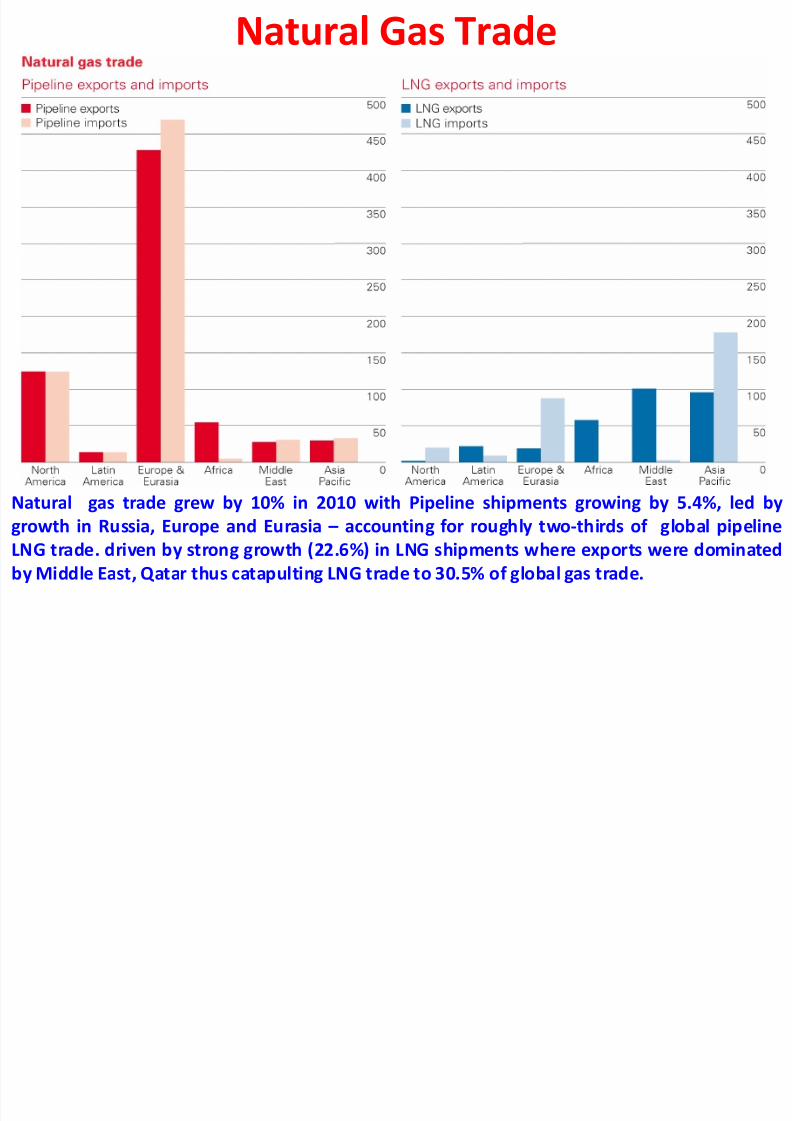

Natural Gas Trade

Natural gas trade grew by 10% in 2010 with Pipeline shipments growing by 5.4%, led by

growth in Russia, Europe and Eurasia – accounting for roughly two-thirds of global pipeline

LNG trade. driven by strong growth (22.6%) in LNG shipments where exports were dominatedby Middle East, Qatar thus catapulting LNG trade to 30.5% of global gas trade.

E l i d

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 13/48

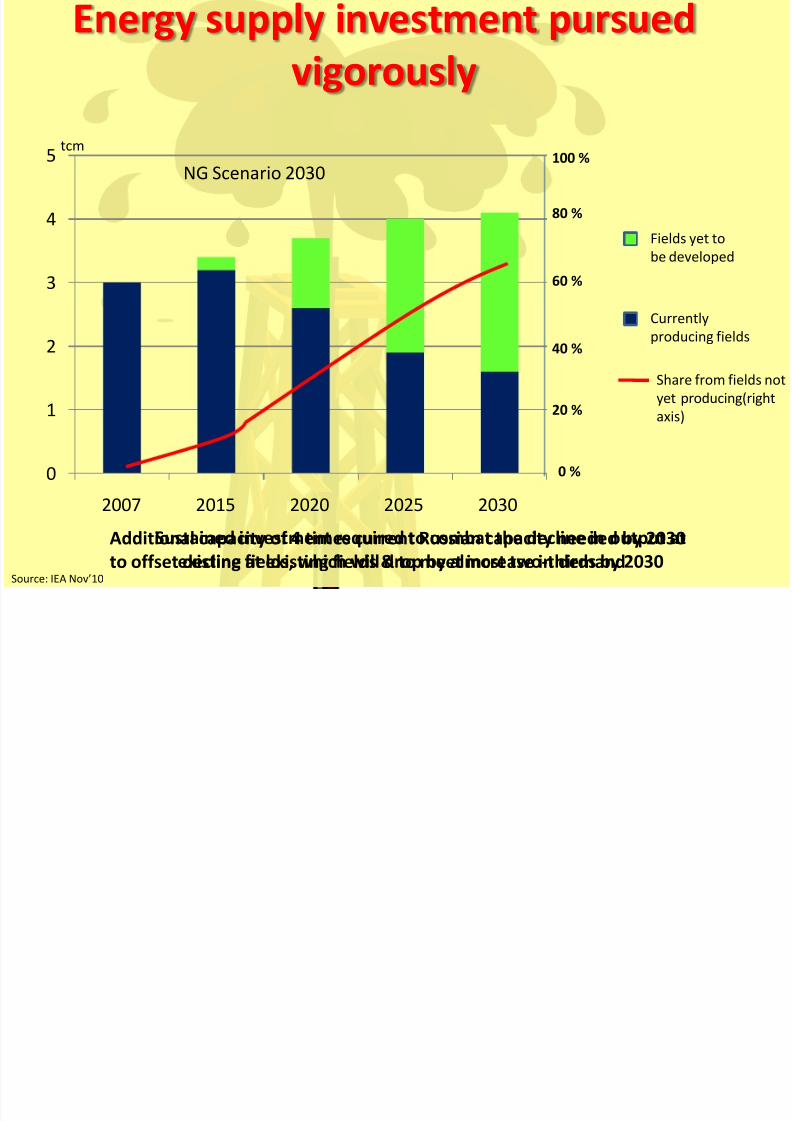

Energy supply investment pursued

vigorously

Sustained investment required to combat the decline in output at

existing fields, which will drop by almost two-thirds by 2030

Additional capacity of 4 times current Russian capacity needed by 2030

to offset decline at existing fields & to meet increase in demand

0

1

2

3

4

5

2007 2015 2020 2025 2030

0 %

20 %

40 %

60 %

80 %

100 %tcm

NG Scenario 2030

Fields yet to

be developed

Currently

producing fields

Share from fields not

yet producing(right

axis)

Source: IEA Nov’10

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 14/48

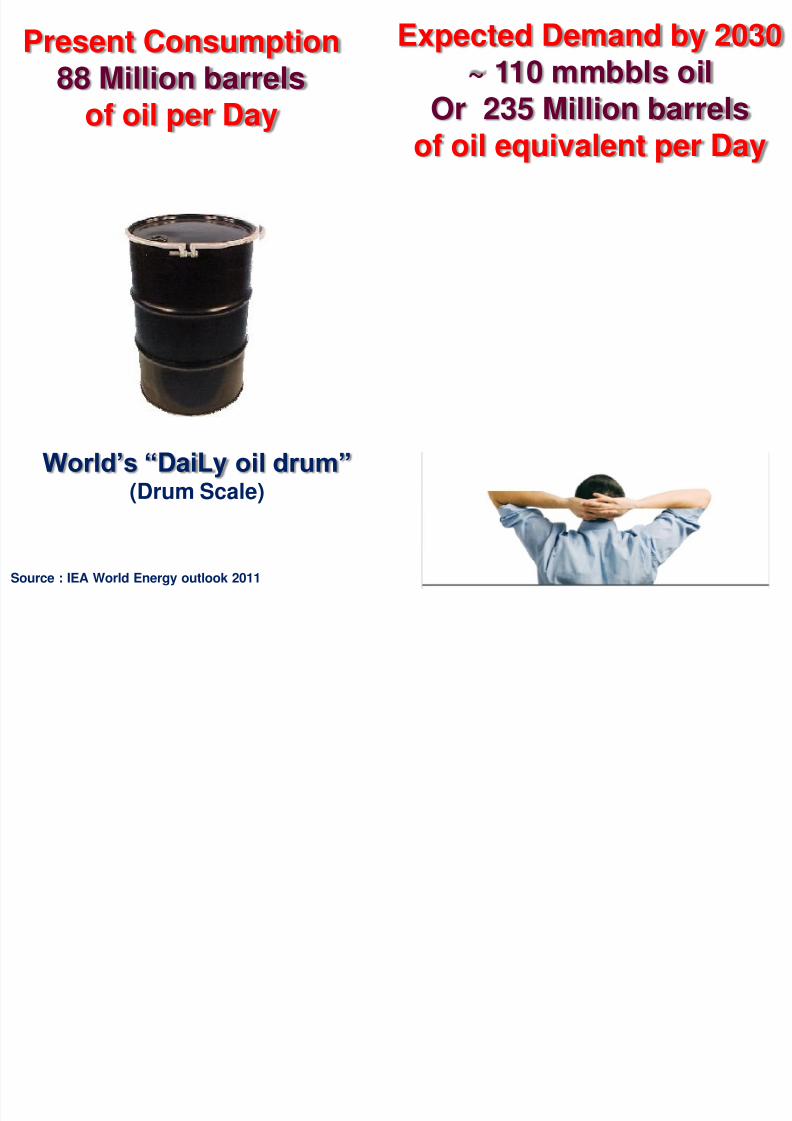

World’s “DaiLy oil drum”

(Drum Scale)

Source : IEA World Energy outlook 2011

Present Consumption88 Million barrels

of oil per Day

Expected Demand by 2030~ 110 mmbbls oil

Or 235 Million barrels

of oil equivalent per Day

f

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 15/48

Russia

Extra demand to be met from new

sources of Supply

West Africa

Nigeria

Angola

FSU countries – Kazakistan & Turkmenistan - gas

Oil Sands

Gulf of Mexico

Deepwater – New oil frontier

Brazil offshore

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 16/48

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 17/48

17

Oil

36%

Gas24%

Coal29%

Nuclear5%

Hydel6%

Source: BP Statistical Review 2008Gas consumption in India increased at a CAGR of >6% (Global:2.6%), next only to China in Asia Pacific(13%) in last ten years

Primary Energy Basket : India Vs Global

Oil32%

Gas10%

Coal51%

Nuclear1%

Hydel7% Oil

26%

Gas20%

Coal51%

Nuclear2%

Hydel2%

Source : BP statistical review 2011

Estimated Energy Basket 2025

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 18/4818

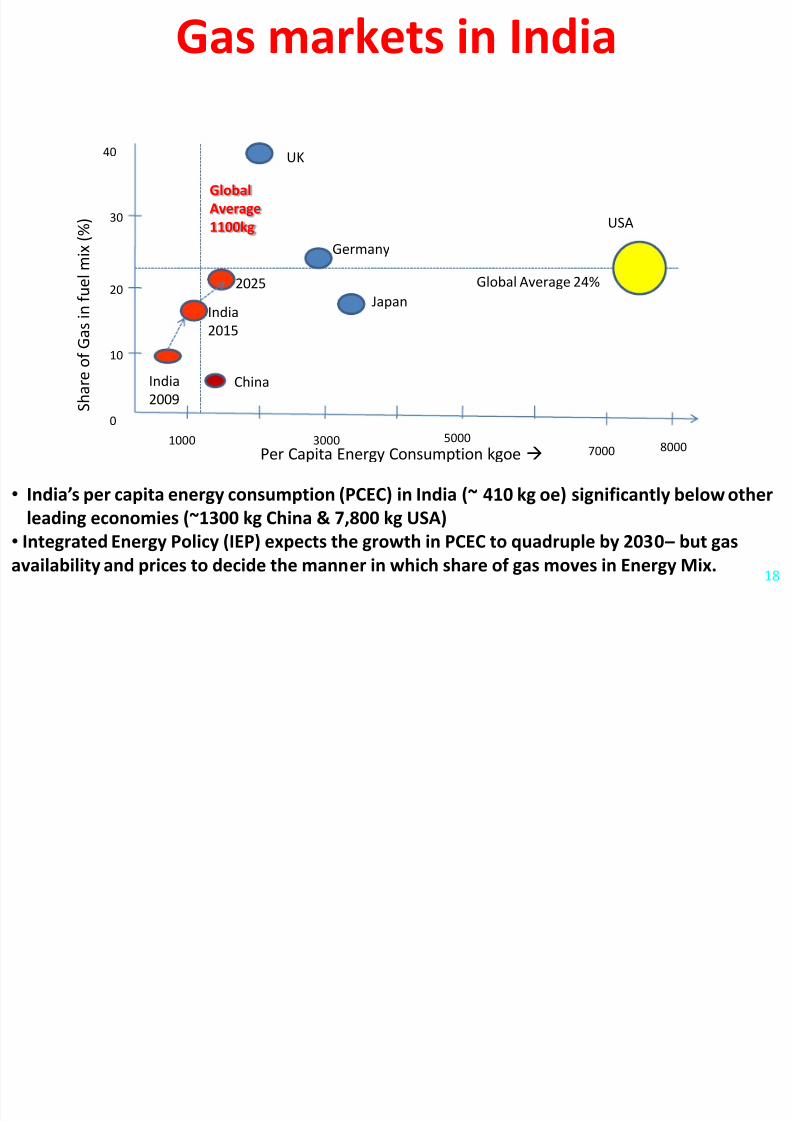

Gas markets in India

0

40

10

20

30

1000 3000 50007000 8000

UK

India

2009

China

India

2015

Japan

Germany

USA

Global Average 24%

Global

Average

1100kg

Per Capita Energy Consumption kgoe

S h a r e o f G a s i n f u e l m i x ( % )

• India’s per capita energy consumption (PCEC) in India (~ 410 kg oe) significantly below other

leading economies (~1300 kg China & 7,800 kg USA)

• Integrated Energy Policy (IEP) expects the growth in PCEC to quadruple by 2030 – but gas

availability and prices to decide the manner in which share of gas moves in Energy Mix.

2025

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 19/48

19

For India, with ~16% of global population,

with~ 0.5% of world’s known Hydrocarbon reserves

&

~7 % of Coal reserve,

and 5.82% CAGR (last 10 years) in energy demand

the situation is pretty Challengingfor a

GDP Growth target of 7-9%…

India: Energy ScenarioMeeting Energy Demand

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 20/48

FY 09

32.84 bcm

Domestic gas Production

FY 11

52.22 bcm

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 21/48

21

Domestic Gas Production and Sectoral Supply

NOC’s production

57.3 mmscmd

LNG (Firm)

~ 47 mmscmd.

PMT & JV

15.26 mmscmd

KG – D640.0 mmscmd

New Discoveries

& Transnational P/L

Total Gas Supply

159.6 mmscmd

End-UserRequirement

166.17*

mmscmd

Power

66.4 mmscmd

Ferilizers

37.74 mmscmd

CGD + CNG

13.97 mmscmd

Petrochemicals

5.67 mmscmd

Refineries

19.77 mmscmd

Sponge iron

7.01 mmscmd

Others

20.59 mmscmd

Source: Global Gas Outlook Aug 2011

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 22/48

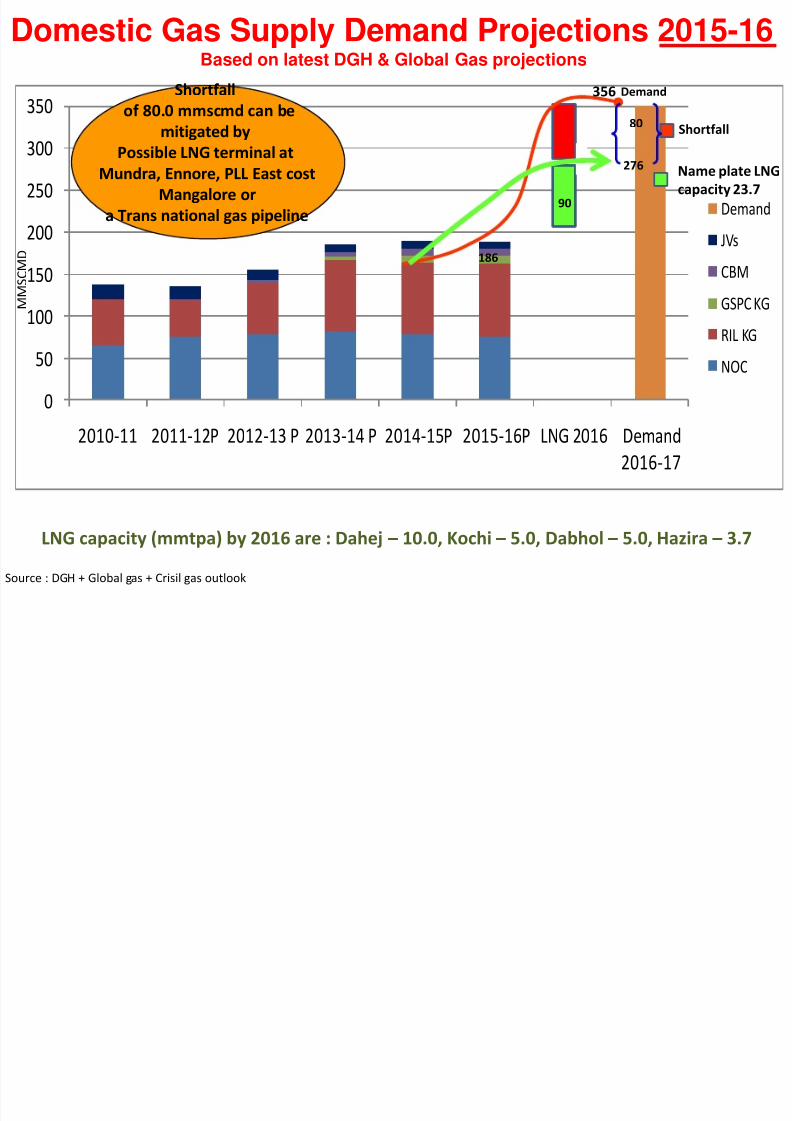

0

50

100

150

200

250

300

350

2010-11 2011-12P 2012-13 P 2013-14 P 2014-15P 2015-16P LNG 2016 Demand

2016-17

Demand

JVs

CBM

GSPC KG

RIL KG

NOC

Domestic Gas Supply Demand Projections 2015-16Based on latest DGH & Global Gas projections

LNG capacity (mmtpa) by 2016 are : Dahej – 10.0, Kochi – 5.0, Dabhol – 5.0, Hazira – 3.7

Shortfall

Name plate LNG

capacity 23.7

M M S C M D

276

80

356Shortfall

of 80.0 mmscmd can be

mitigated by

Possible LNG terminal at

Mundra, Ennore, PLL East cost

Mangalore or

a Trans national gas pipeline

Demand

Source : DGH + Global gas + Crisil gas outlook

90

186

i ifi h i ili

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 23/48

Power Fertilizers

Current

Installed capacity

2025

150 GW

366 GW

Current

Installed capacity

2025

12

20Nitrogeneous Fertilizer capacity

mtpa of N equivalent

• Hi capacity add’n

• Thrust by GoI to

set up clean fuelPower plants

• Gas preferred

feedstock

• GoI directive to

convert to gas –

subsidy savings

Industrial – fuel & feedstock

CurrentInstalled capacity

2025

41 mtoe

113 mtoe

• Conversion from liquid

fuels

• Industrial growth to fuel

demand

• Gas share to increase

City Gas – PNG & CNG

2025

• Environmental regulations

to drive growth

• GoI encouraging expansion

Significant growth in Power, Fertilizers,

Industrial fuel, CGD, CNG in next 15 years

Close Window Uses of crude oil

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 24/48

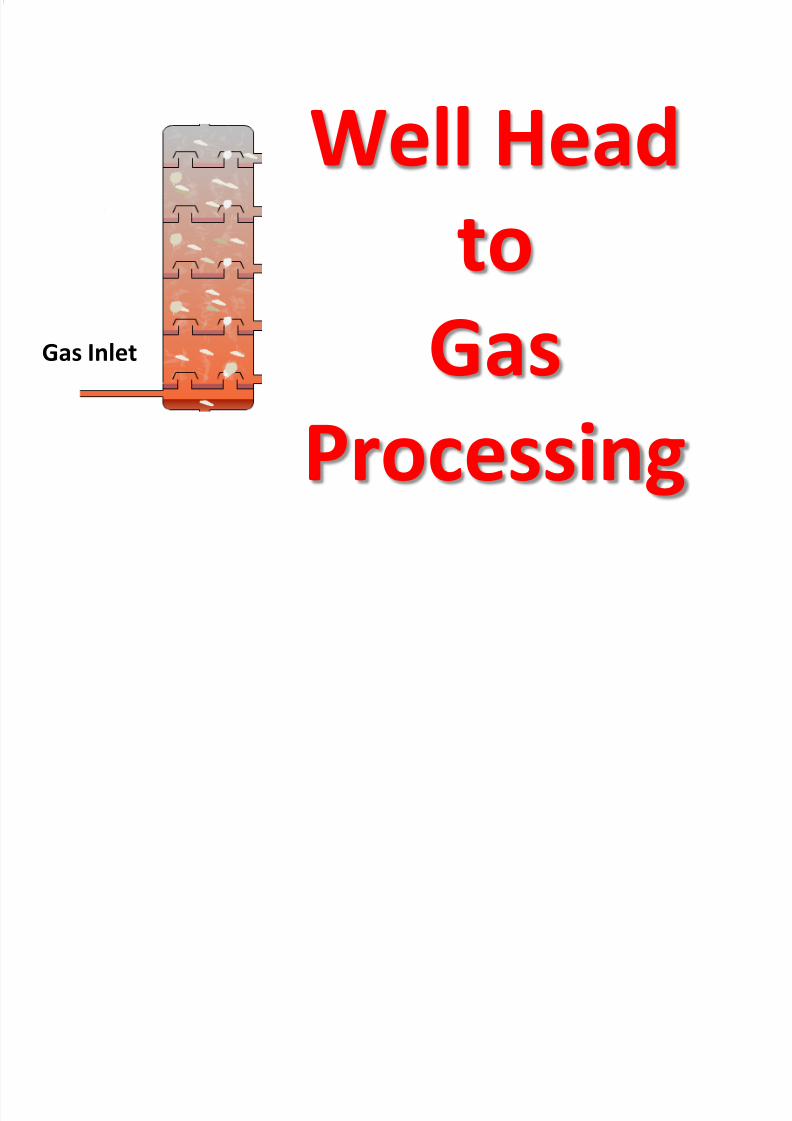

Residue

Gas Inlet

GlycolInletWell Head

toGas

Processing

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 25/48

Produced from Rajasthan block, this crude

is a medium API, highly viscous having

abnormally high Pour Point (only 2 crudes

have more pour point) AND

with a very high residue

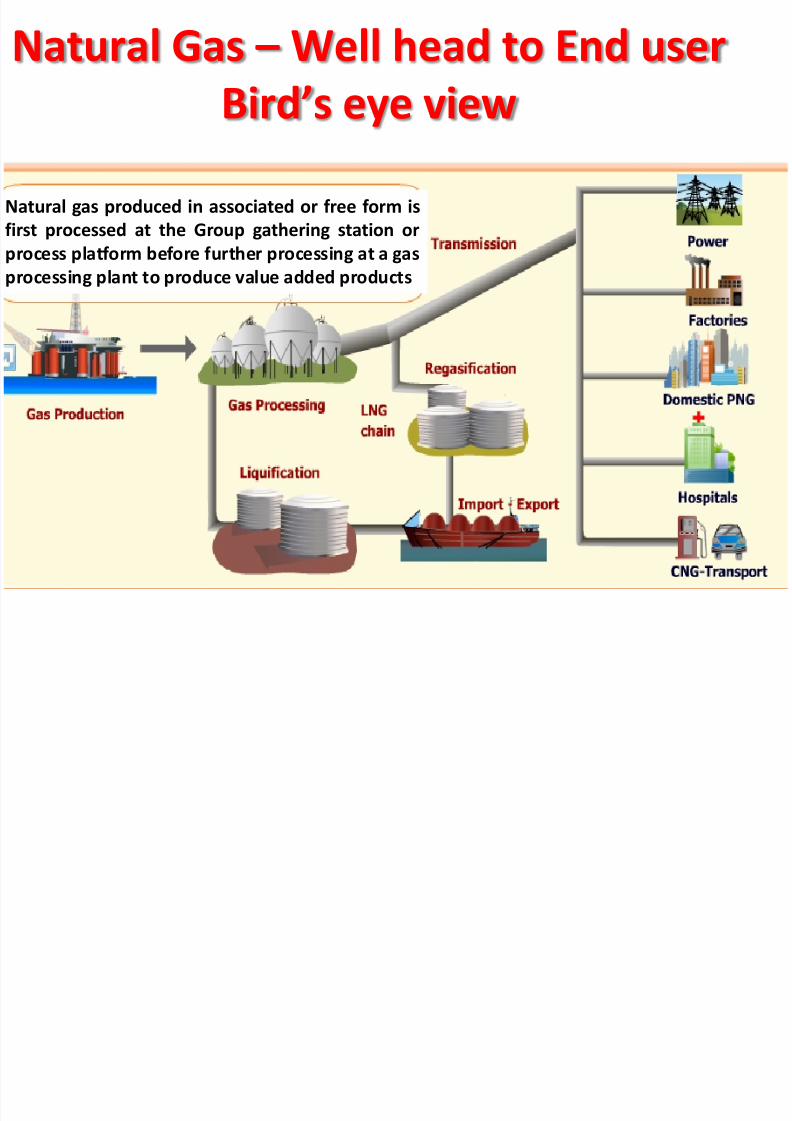

Natural Gas – Well head to End user

Bird’s eye view

Natural gas produced in associated or free form is

first processed at the Group gathering station or

process platform before further processing at a gas

processing plant to produce value added products

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 26/48

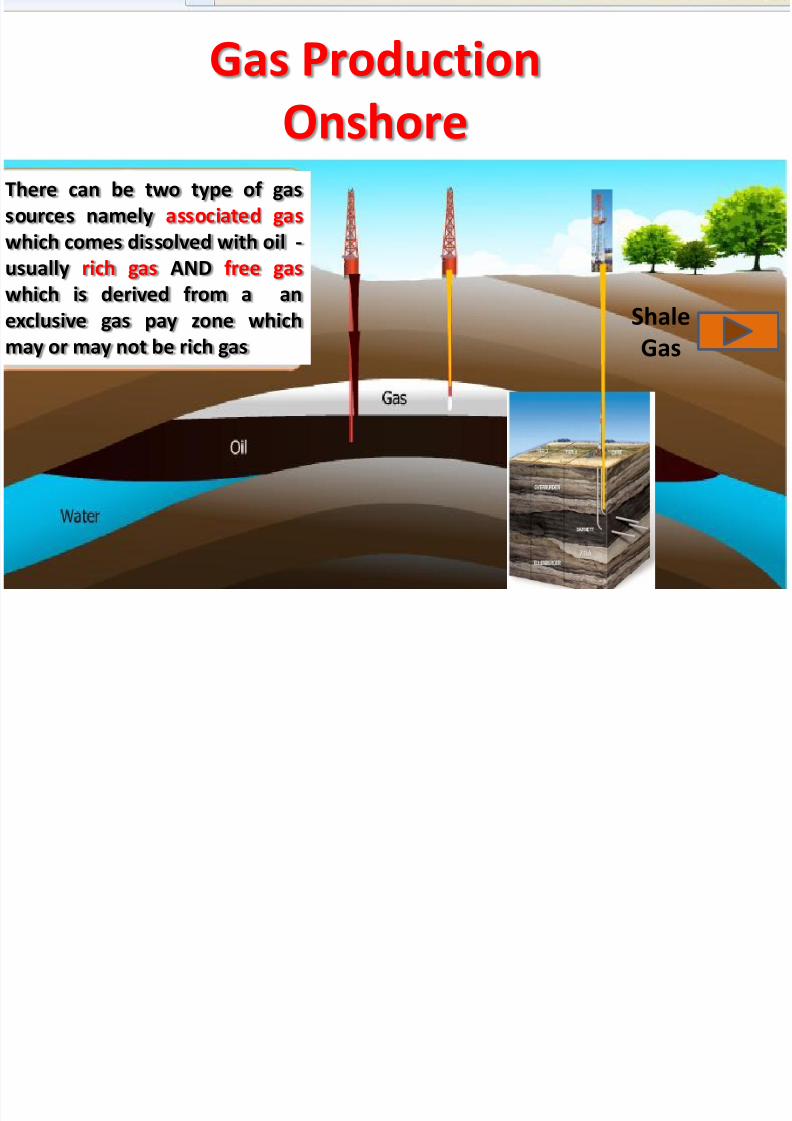

Gas Production

OnshoreThere can be two type of gas

sources namely associated gas

which comes dissolved with oil -

usually rich gas AND free gas

which is derived from a an

exclusive gas pay zone which

may or may not be rich gas

Shale

Gas

Gas Production

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 27/48

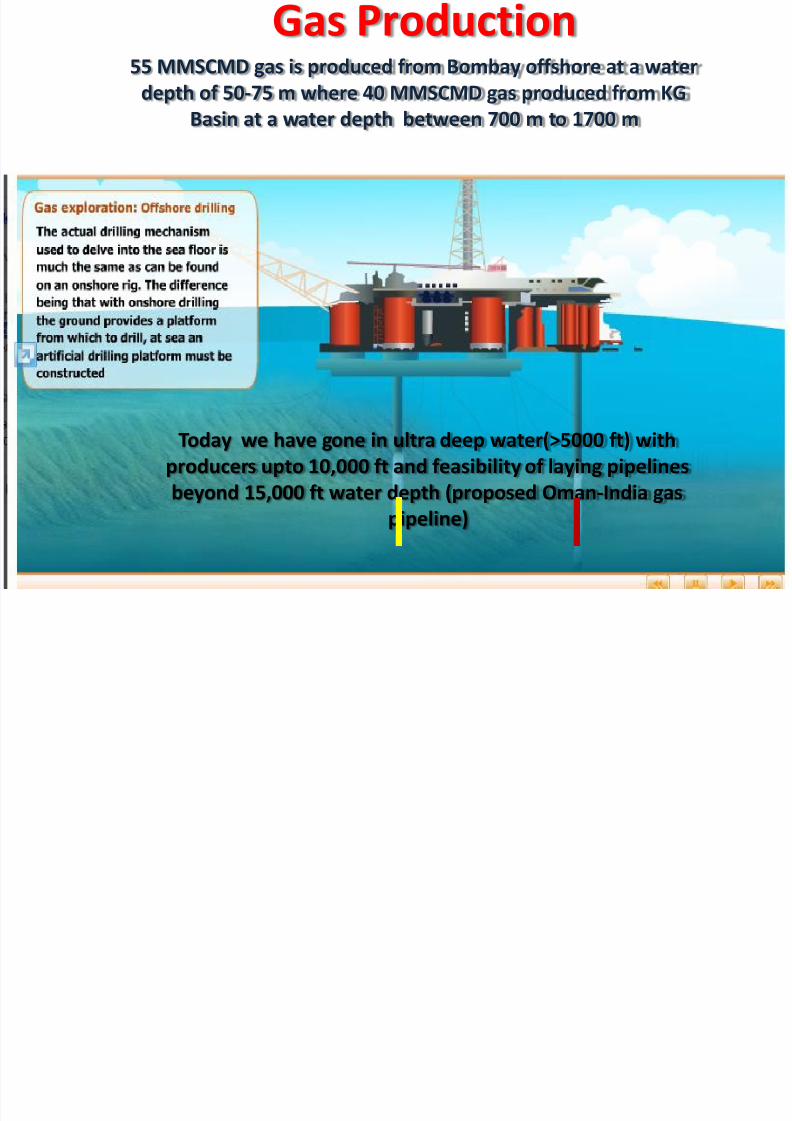

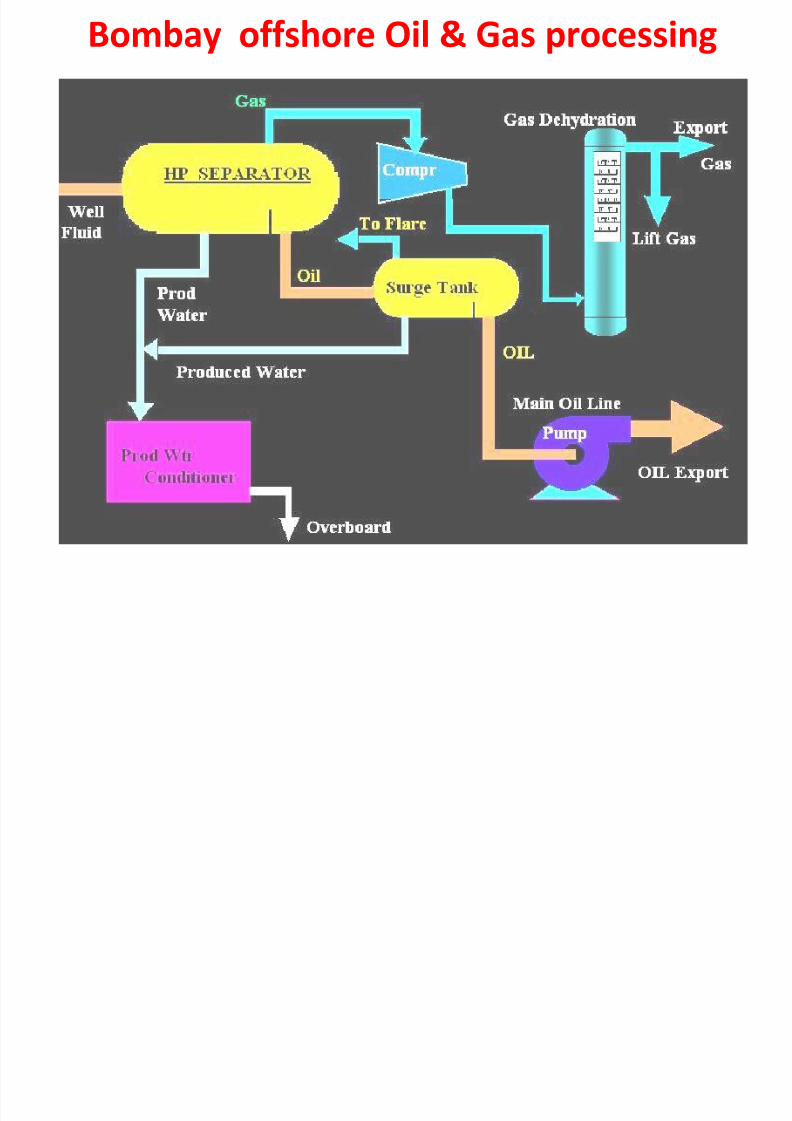

Gas Production55 MMSCMD gas is produced from Bombay offshore at a water

depth of 50-75 m where 40 MMSCMD gas produced from KG

Basin at a water depth between 700 m to 1700 m

Today we have gone in ultra deep water(>5000 ft) with

producers upto 10,000 ft and feasibility of laying pipelines

beyond 15,000 ft water depth (proposed Oman-India gas

pipeline)

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 28/48

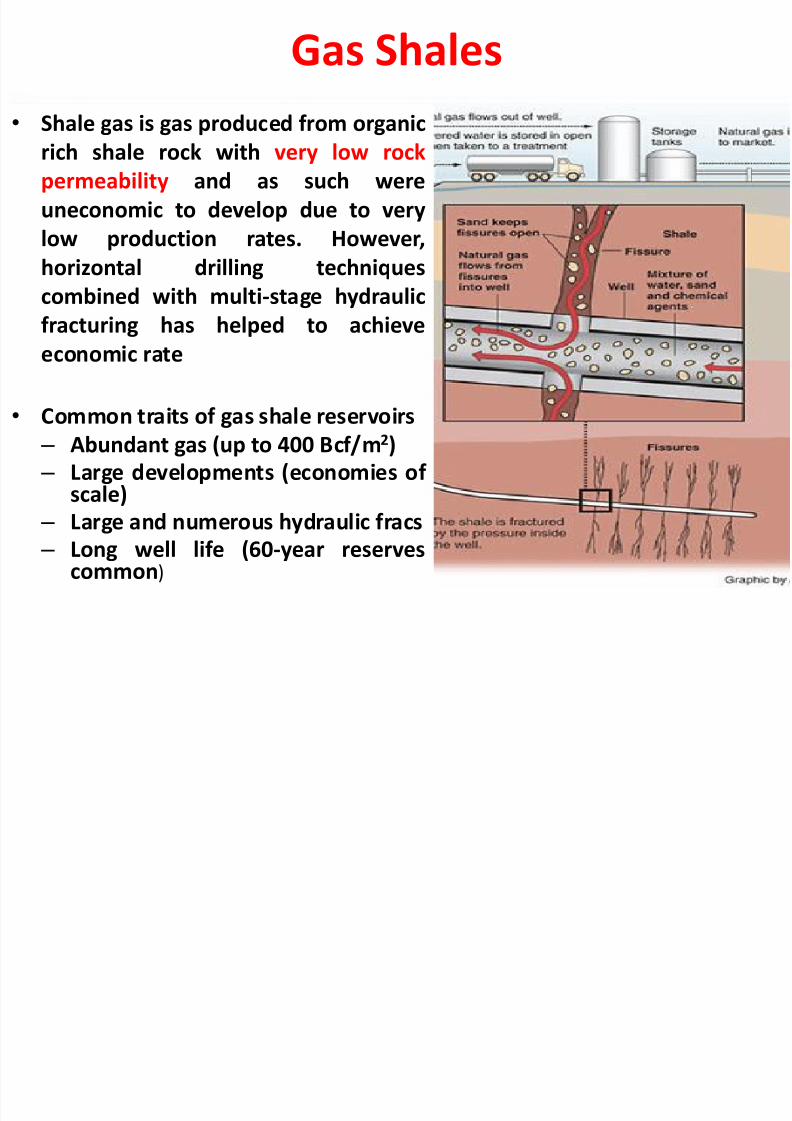

Gas Shales

• Shale gas is gas produced from organic

rich shale rock with very low rock

permeability and as such were

uneconomic to develop due to very

low production rates. However,

horizontal drilling techniques

combined with multi-stage hydraulic

fracturing has helped to achieve

economic rate

•Common traits of gas shale reservoirs – Abundant gas (up to 400 Bcf/m2)

– Large developments (economies of scale)

– Large and numerous hydraulic fracs

–

Long well life (60-year reservescommon)

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 29/48

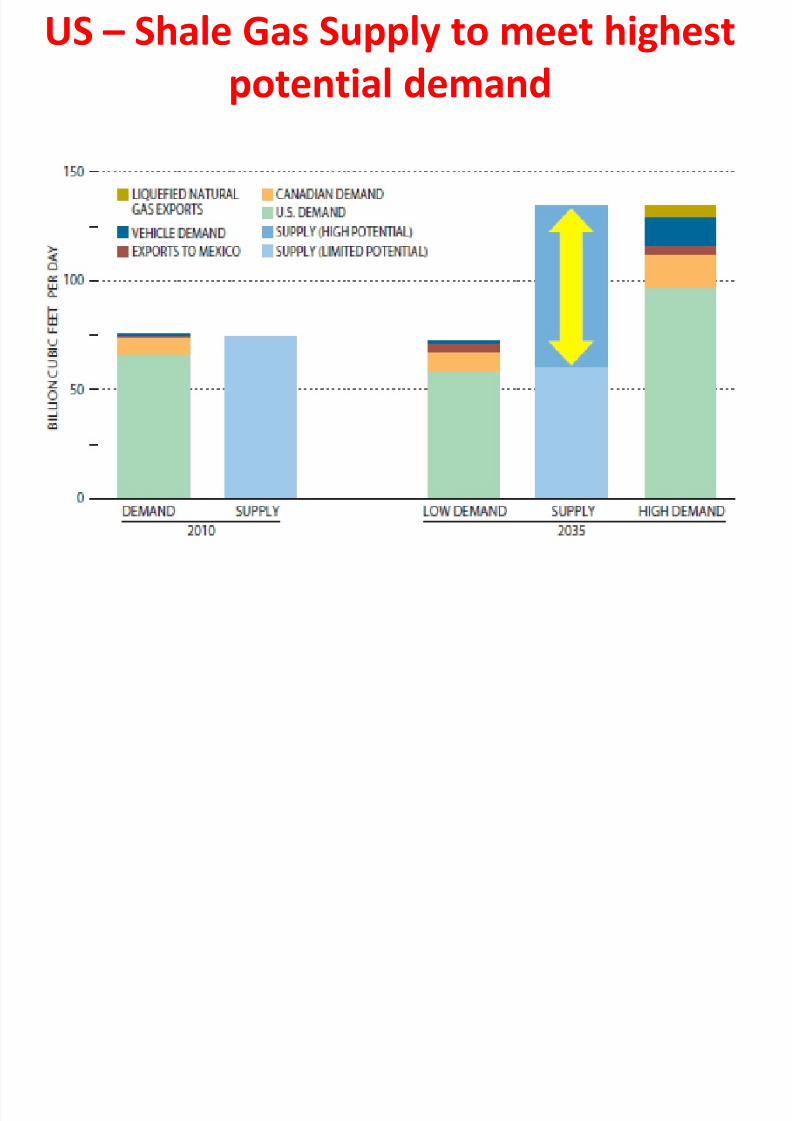

US – Gas supply augmented by Shale Gas

1990-2035

US Sh l G S l t t hi h t

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 30/48

US – Shale Gas Supply to meet highest

potential demand

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 31/48

Natural Gas Prices

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 32/48

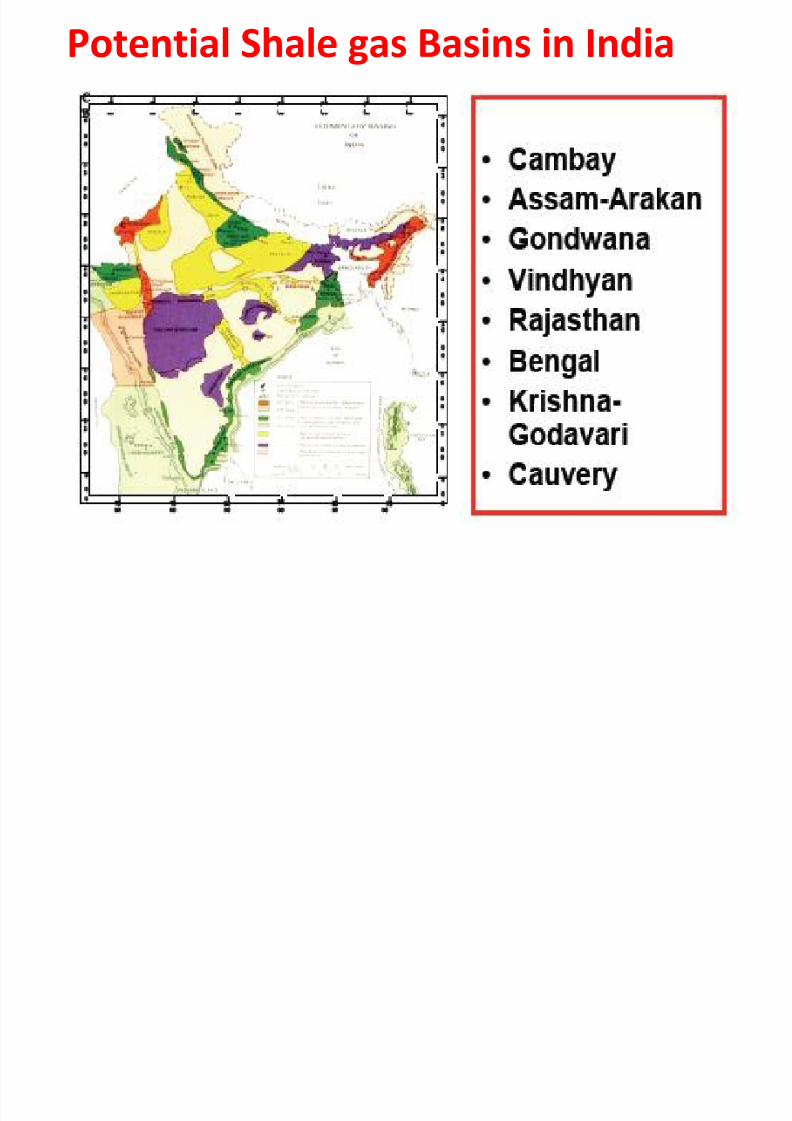

Potential Shale gas Basins in India

Sh l

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 33/48

Shale gas – efforts in India

ONGC in collaboration with Schlumberger has undertaken

an integrated pilot project to drill 4 wells, 2 in Raniganj,West Bengal and 2 wells in North Karanpura-Jharkahand to

find potential of Shale gas in Indian basins

First well proved presence of

Shale gas on 25th January 2011

R&D efforts continuing

h l

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 34/48

Shale Gas resource Estimations

in India

Oil & Gas Processing

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 35/48

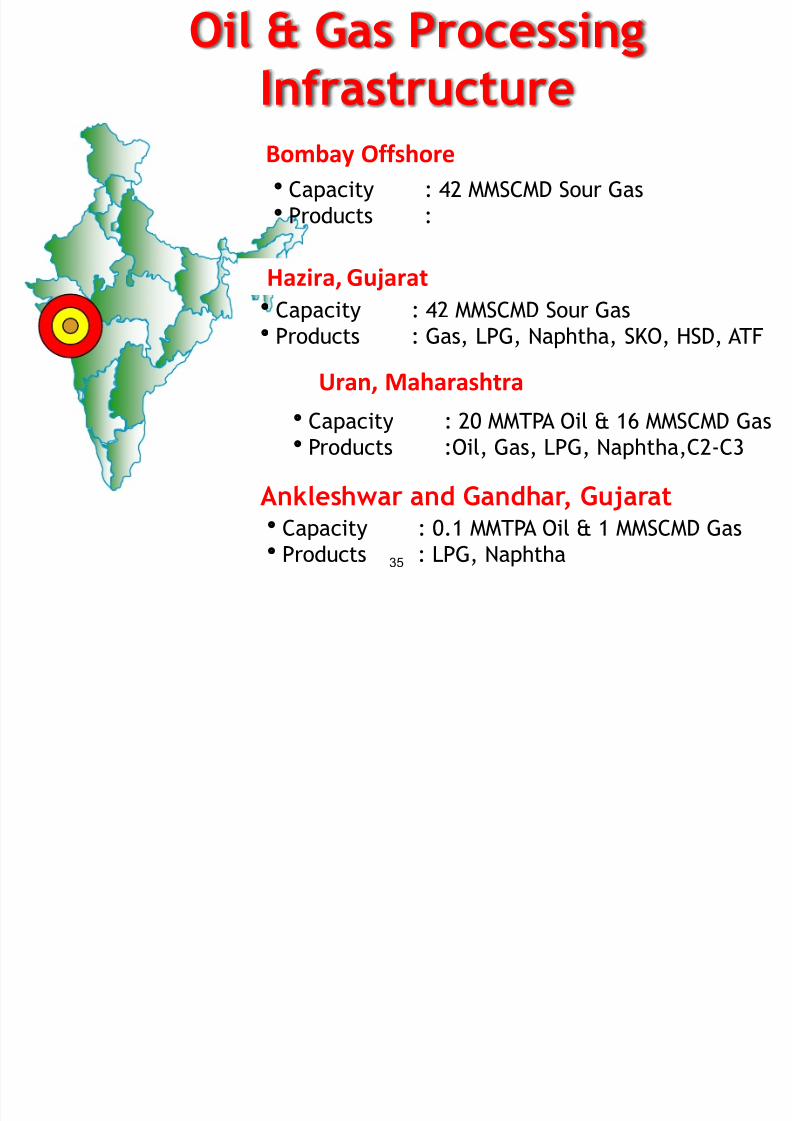

35

Oil & Gas ProcessingInfrastructure

Capacity : 42 MMSCMD Sour Gas

Products : Gas, LPG, Naphtha, SKO, HSD, ATF

Capacity : 20 MMTPA Oil & 16 MMSCMD GasProducts :Oil, Gas, LPG, Naphtha,C2-C3

Ankleshwar and Gandhar, GujaratCapacity : 0.1 MMTPA Oil & 1 MMSCMD Gas

Products : LPG, Naphtha

Hazira, Gujarat

Uran, Maharashtra

Bombay Offshore

Capacity : 42 MMSCMD Sour Gas

Products :

B b ff h Oil & G i

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 36/48

Bombay offshore Oil & Gas processing

NHazira Gas processing plant

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 37/48

Umbhrat

Daman

Mumbai

Vasai

Hazira

Vadodara

N

Arabian

Sea

PannaMukta

Tapti

36”

42”

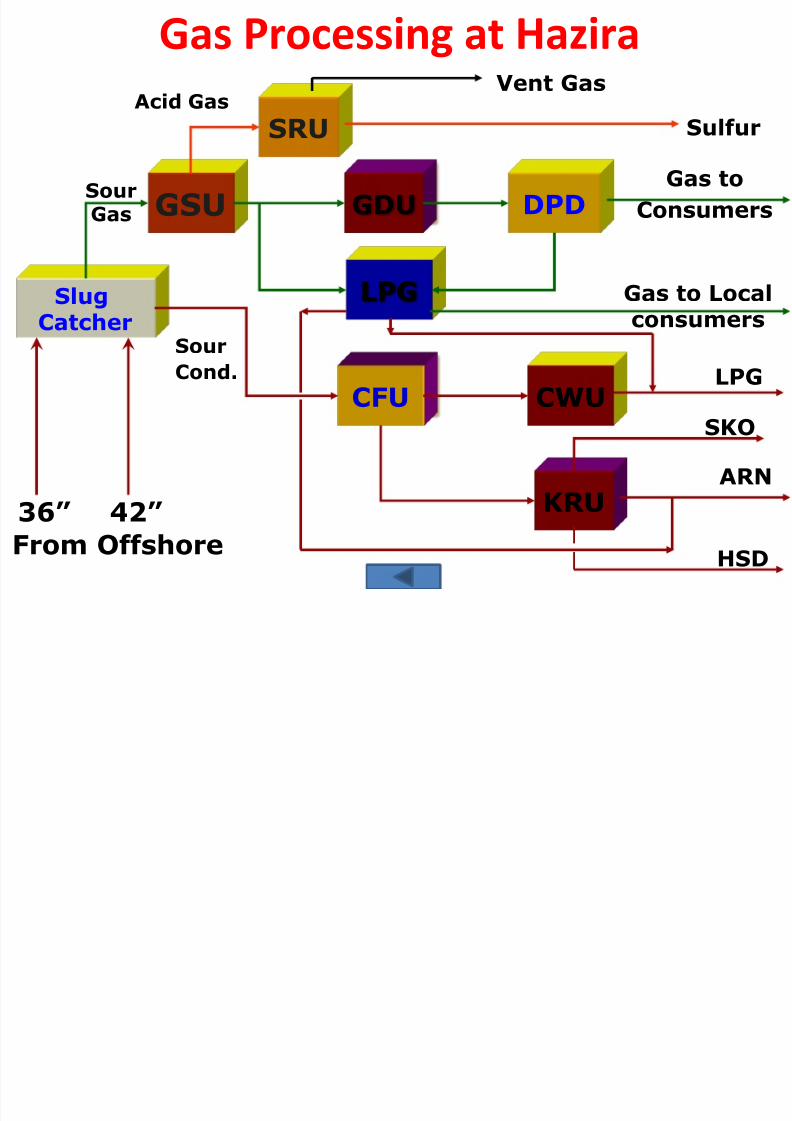

Hazira Gas processing plant

Gas Processing at Ha ira

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 38/48

SlugCatcher

GSU DPD

CFU

GDU

LPG

KRU

CWU

SRU

36” 42”

Sulfur

Gas to

Consumers

Gas to Localconsumers

LPG

ARN

SKO

Acid Gas

SourGas

Sour

Cond.

From Offshore

Gas Processing at Hazira

HSD

Vent Gas

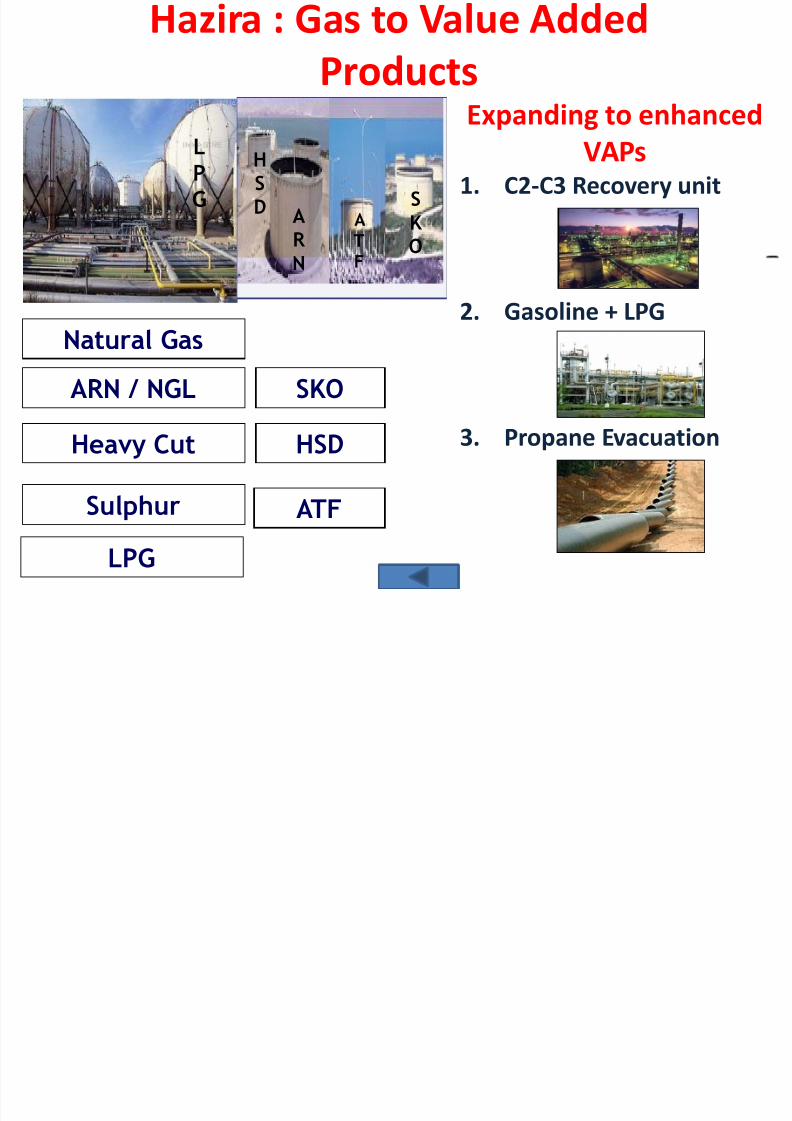

Hazira : Gas to Value Added

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 39/48

Natural Gas

LPG

ARN / NGL SKO

Heavy Cut HSD

Sulphur

Hazira : Gas to Value AddedProducts

LPG

AR N

SK O

HSD

ATF

ATF

Expanding to enhanced

VAPs1. C2-C3 Recovery unit

2. Gasoline + LPG

3. Propane Evacuation

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 40/48

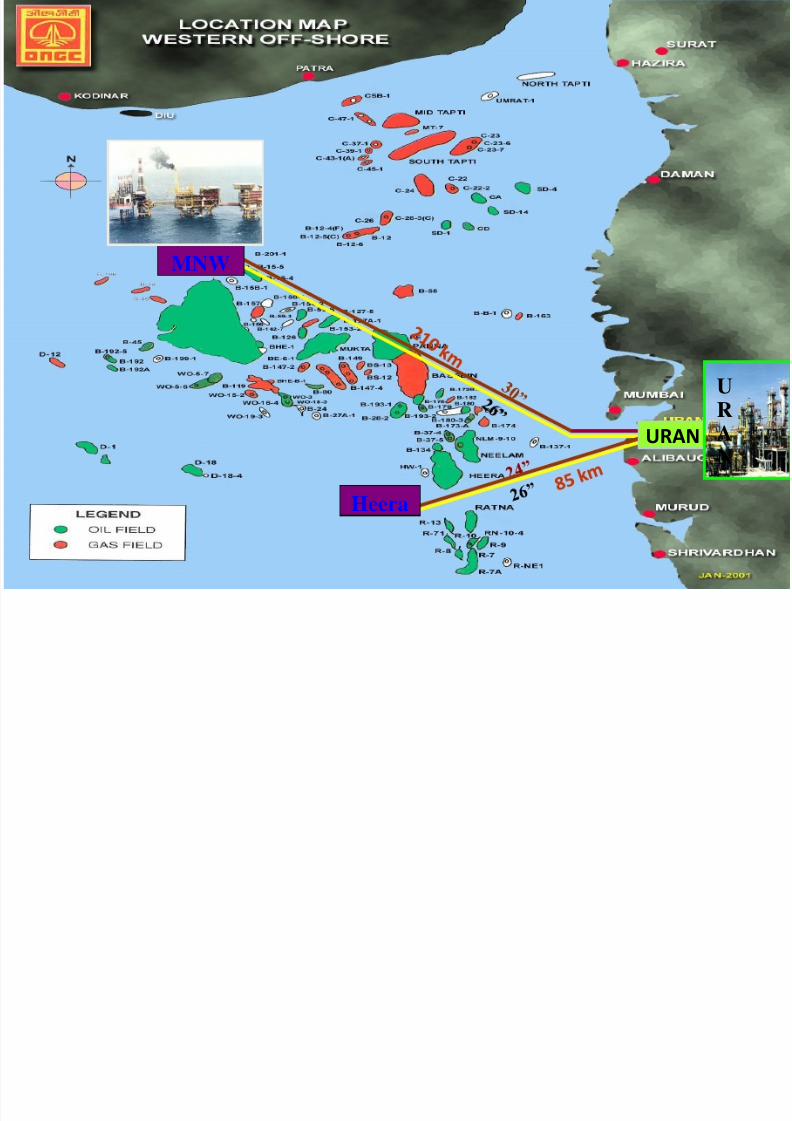

URAN

MNW

Heera

U

R

A

N

Uran PROCESS

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 41/48

GAS

SWEETENINGUNIT

SLUGCATCHER

LPGPLANT

C2C3

PLANT

CONDENSATEFRACTIONATING

UNIT

CSU OFFGASCOMPRESSOR

PRODUCED WATER TOETP - MINAS

CRUDE OIL TO STORAGE

NAPHTHA TO STORAGE

LPG TO STORAGE

SSV

LEF

ACID GAS

GAS TO CONSUMERS

GAS

CRUDE

STABILISATIONUNIT

C2C3 TO

STORAGE

Crude Oil

GAS

Uran PROCESS

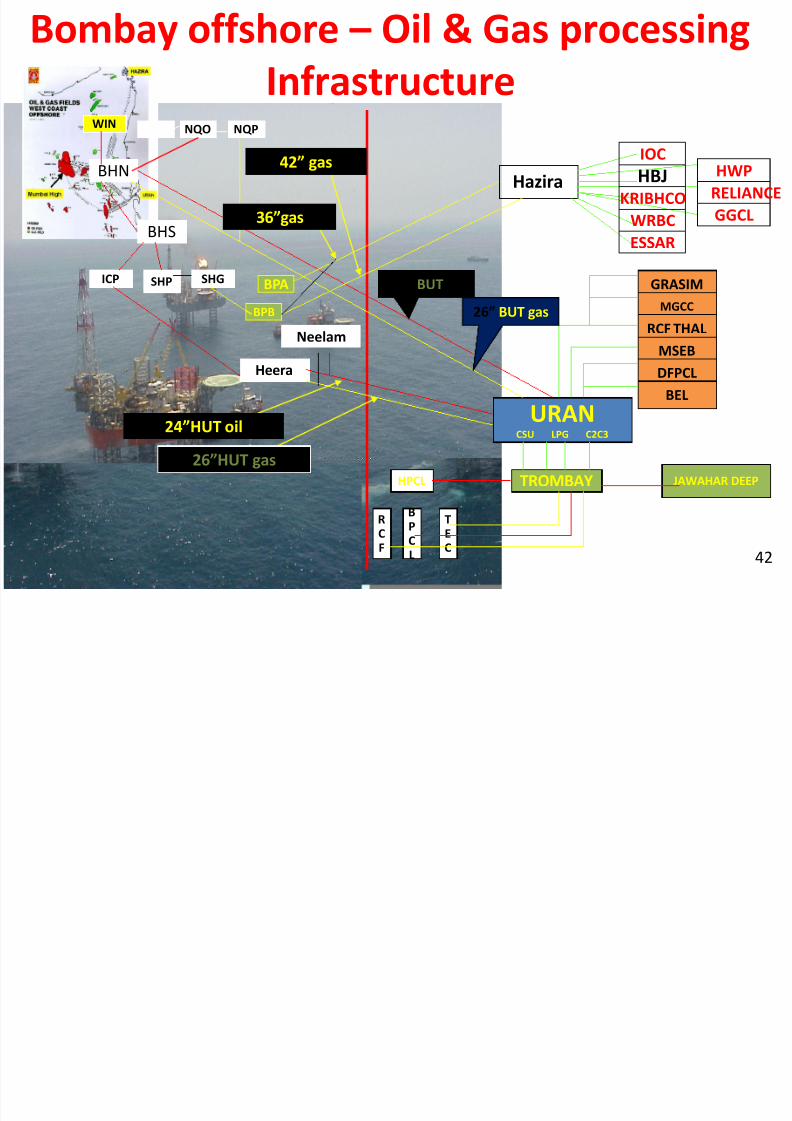

Bombay offshore – Oil & Gas processing

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 42/48

42

Bombay offshore – Oil & Gas processing

Infrastructure

GRASIMMGCC

RCF THAL

MSEB

DFPCL

BEL

JAWAHAR DEEP

Hazira

URANCSU LPG C2C3

TROMBAYHPCL

RCF

TEC

BPC

L

BHN

BHS

WIN NQO NQP

ICP SHP SHG

Heera

BPB

BPA

Neelam

30” BUT oil

26” BUT gas

IOC

HBJKRIBHCO

WRBC

ESSAR

HWP

RELIANCE

GGCL

26”HUT gas

24”HUT oil

36”gas

42” gas

G

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 43/48

Gas

Transmission

&

End Uses

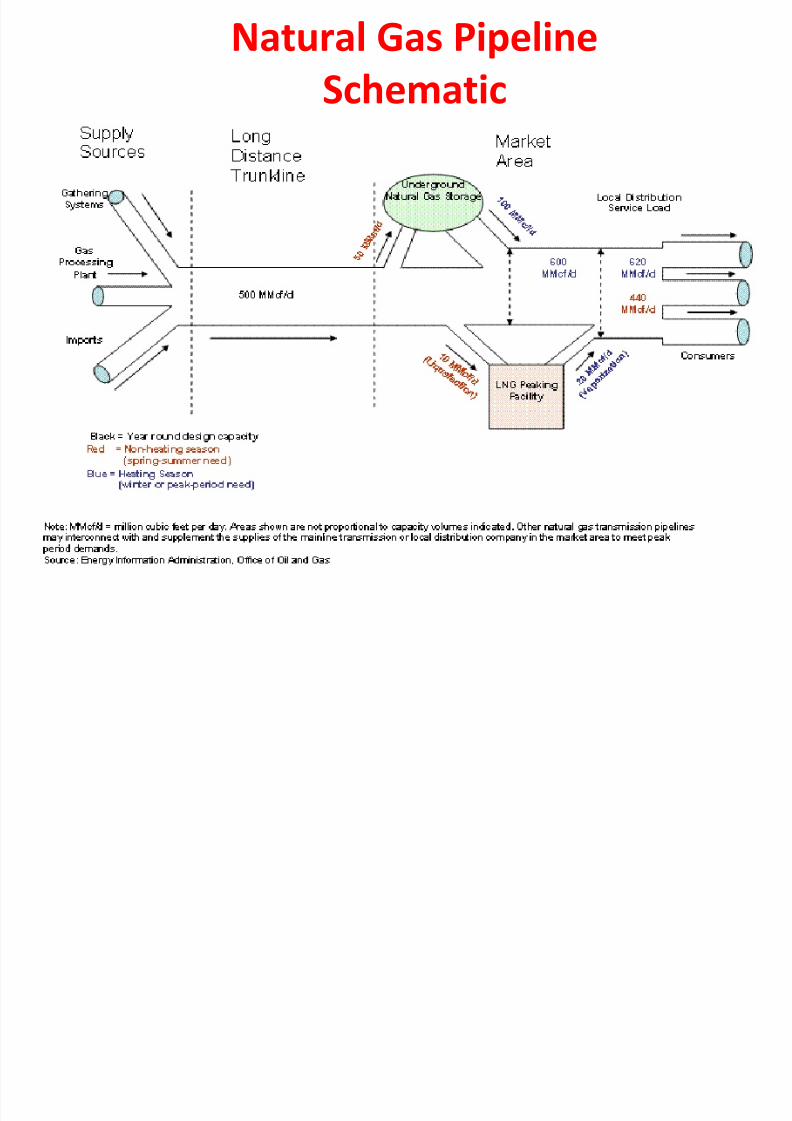

Natural Gas Pipeline

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 44/48

Natural Gas Pipeline

Schematic

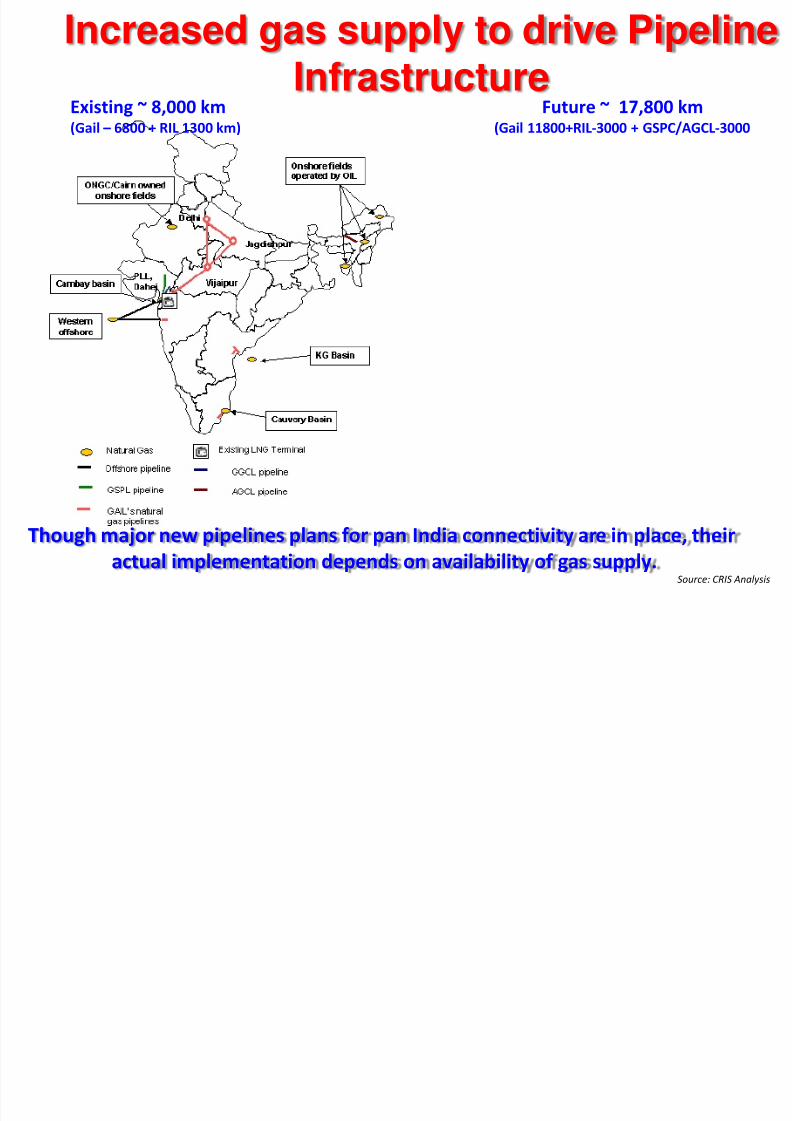

Increased gas supply to drive Pipeline

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 45/48

Though major new pipelines plans for pan India connectivity are in place, their

actual implementation depends on availability of gas supply.Source: CRIS Analysis

Increased gas supply to drive PipelineInfrastructure

Existing ~ 8,000 km(Gail – 6800 + RIL 1300 km)

Future ~ 17,800 km(Gail 11800+RIL-3000 + GSPC/AGCL-3000

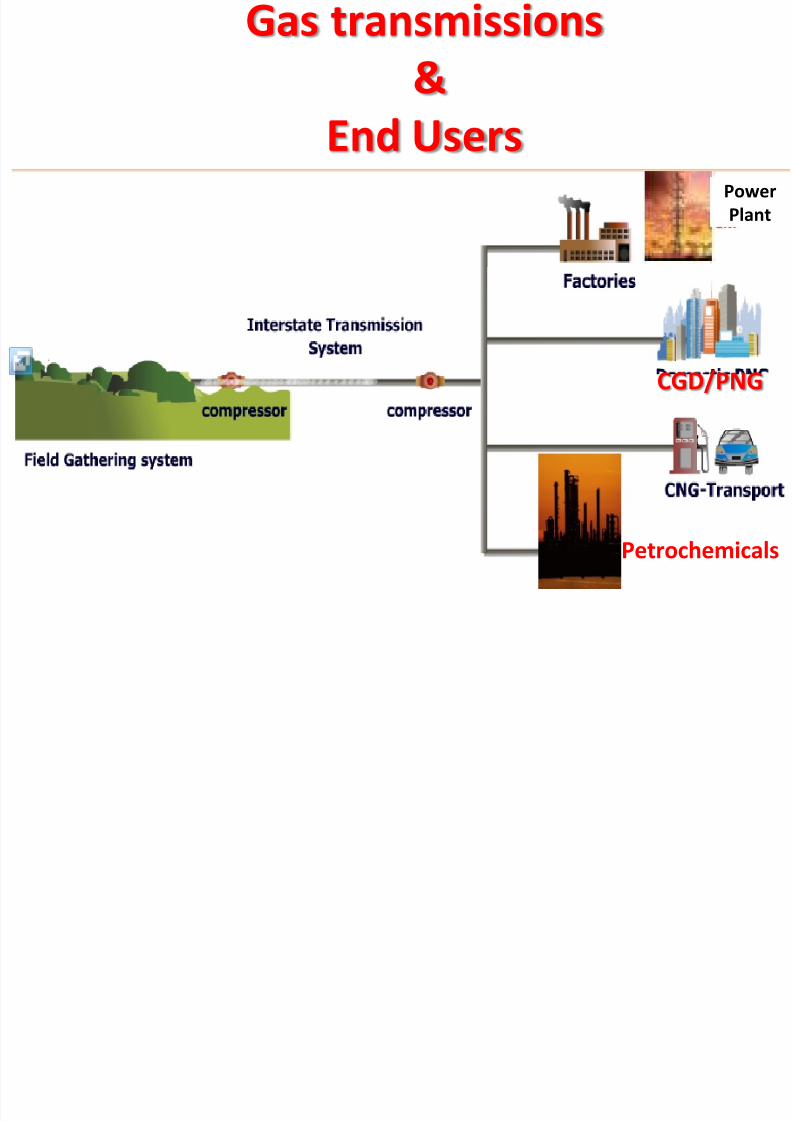

Gas transmissions

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 46/48

Gas transmissions&

End UsersPower

Plant

CGD/PNG

Petrochemicals

To Conclude

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 47/48

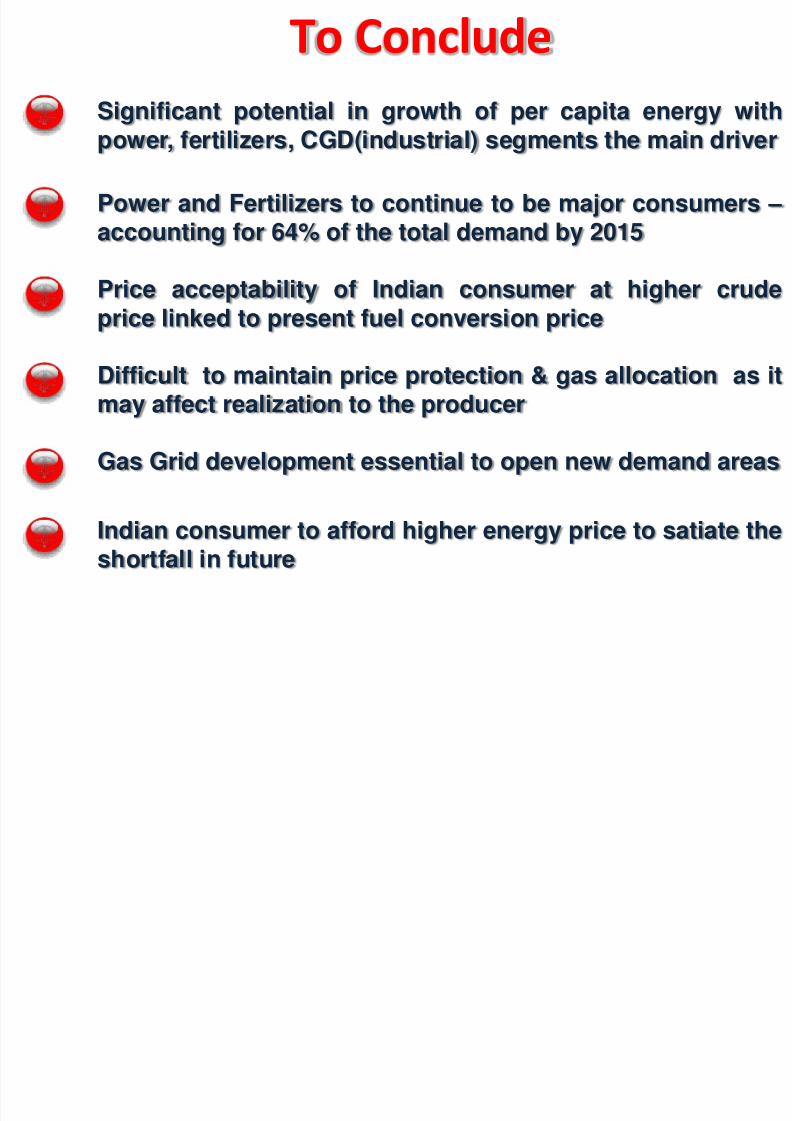

To Conclude

Price acceptability of Indian consumer at higher crudeprice linked to present fuel conversion price

Significant potential in growth of per capita energy with

power, fertilizers, CGD(industrial) segments the main driver

Difficult to maintain price protection & gas allocation as itmay affect realization to the producer

Power and Fertilizers to continue to be major consumers –

accounting for 64% of the total demand by 2015

Gas Grid development essential to open new demand areas

Indian consumer to afford higher energy price to satiate the

shortfall in future

7/29/2019 Domestic Gas Scenario Processing, Distribution & Applications

http://slidepdf.com/reader/full/domestic-gas-scenario-processing-distribution-applications 48/48

Questions, Thoughts?

Related Documents