Glanbia Market View European markets are set to open up this morning, buoyed by much better than expected Australian GDP growth in Q112, which came in at 1.3% versus 0.6% expected. This out performance was driven by a boom in mining investment and increased consumption. Yesterday’s G7 finance chiefs’ teleconference produced little of note, other than a call for Europe to act more aggressively to sort out its problems and the EU participants noting that they will respond to any issues speedily. Overnight, the Spanish budget minister was reported as saying that the Government will be looking for outside aid to address its banking crisis, in contrast to previous statements from the Prime Minister. That said, the main issue taxing the markets is how much will be needed (estimates are ranging from €40bn through €75bn to €350bn) and where it will be sourced (the temporary EFSF, the shortly to be implemented permanent ESM or a range of international sources). This morning, Moody downgraded seven German banks, including Commerzbank, and is still reviewing its Deutsche Bank rating. The main data release of note this morning is the ECB rate announcement at 12:45 and subsequent press conference at 13:30. The general expectation is that rates will be held at 1%, although the potential of a 25bps cut this month has been gaining some traction over the past few days. If rates remain on hold, the market focus will turn to Chairman Draghi’s comments at the press conference on future rate movements, potential to increase liquidity and/or relative role between the ECB and individual Governments in addressing the Eurozone debt crisis. www.dolmenstockbrokers.ie 6th JUNE 2012 Contents Market View: Australian growth proves tonic to European woes Vodafone: Looking to increase its presence in New Zealand Providence Resources: Barryroe technical update Company Note: Glanbia IRISH PAPERS TODAY Main banks may not hit business lending target (The Irish Times) Spain wants EU help for its banks (The Irish Independent) Domestic manufacturing activity up 1.2% (The Irish Times) INTERNATIONAL PAPERS TODAY Qantas slashes its profit forecast (Financial Times) Germany grapples with role in rescue (Wall Street Journal) Top Tory urges Greece to quit euro (Financial Times) Vodafone - Buy Previous Close 173p Target 195p Vodafone this morning confirmed that it is in talks with the Australian telecoms company Telstra over the potential acquisition of the latter’s New Zealand subsidiary, TelstraClear. The subsidiary is thought to be worth between $A300m and $A400m and could be bought from current cash resources (Vodafone has £8.5bn in cash on the balance sheet, although net debt stands at c.£26bn). Currently, the largest operator in New Zealand is Telecom NZ, followed by Vodafone. This acquisition, if successful, would see Vodafone become the largest operator. Currently, Vodafone’s New Zealand operations are relatively small and as such are not broken out in results, remaining part of “other”, which in total accounted for 7% of FY12 EBITDA. As such, this potential acquisition will have an incremental impact on the company but it does illustrate one of the company’ s strengths, its geographic diversity. That, coupled with a well covered, high yielding, dividend (note final went ex-div today) is why Vodafone remains one of our key portfolio stocks, which at only 10.3x FY13 earnings we would remain comfortable picking up at current levels. Providence Resources - Barryroe technical update Providence Resources has this morning provided a technical update on the Barryroe discovery which it is currently assessing and appraising post the reentry of the well last March. The latest process completed and announced today was an independent third crude assay which came in marginally better than expected. A sample of the crude from Barryroe verifies a light oil (API 43 degrees) and a wax content measured by weight of 17% which should prove moveable. The post drill studies are ongoing with core analysis expected to be completed in the next month and new independent in place volumetrics by the end of July. Last month, Providence announced that a horizontal well design/completion could support ~ 12,500 bopd & ~ 11MMSCFD. Providence Resources holds an 80% interest in Barryroe with Lansdowne Oil & Gas holding 20%.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Glanbia

Market View European markets are set to open up this morning, buoyed by much better than expected Australian GDP growth in

Q112, which came in at 1.3% versus 0.6% expected. This out performance was driven by a boom in mining

investment and increased consumption. Yesterday’s G7 finance chiefs’ teleconference produced little of note, other

than a call for Europe to act more aggressively to sort out its problems and the EU participants noting that they will

respond to any issues speedily. Overnight, the Spanish budget minister was reported as saying that the

Government will be looking for outside aid to address its banking crisis, in contrast to previous statements from the

Prime Minister. That said, the main issue taxing the markets is how much will be needed (estimates are ranging

from €40bn through €75bn to €350bn) and where it will be sourced (the temporary EFSF, the shortly to be

implemented permanent ESM or a range of international sources). This morning, Moody downgraded seven

German banks, including Commerzbank, and is still reviewing its Deutsche Bank rating. The main data release of

note this morning is the ECB rate announcement at 12:45 and subsequent press conference at 13:30. The general

expectation is that rates will be held at 1%, although the potential of a 25bps cut this month has been gaining some

traction over the past few days. If rates remain on hold, the market focus will turn to Chairman Draghi’s comments

at the press conference on future rate movements, potential to increase liquidity and/or relative role between the

ECB and individual Governments in addressing the Eurozone debt crisis.

www.dolmenstockbrokers.ie

6th JUNE 2012

Contents Market View: Australian growth proves tonic to European woes Vodafone: Looking to increase its presence in New Zealand Providence Resources: Barryroe technical update Company Note: Glanbia

IRISH PAPERS TODAY

Main banks may not hit business lending target (The Irish Times) Spain wants EU help for its banks (The Irish Independent) Domestic manufacturing activity up 1.2% (The Irish Times)

INTERNATIONAL

PAPERS TODAY

Qantas slashes its profit forecast (Financial Times) Germany grapples with role in rescue (Wall Street Journal) Top Tory urges Greece to quit euro (Financial Times)

Vodafone - Buy Previous Close 173p Target 195p

Vodafone this morning confirmed that it is in talks with the Australian telecoms

company Telstra over the potential acquisition of the latter’s New Zealand

subsidiary, TelstraClear. The subsidiary is thought to be worth between $A300m

and $A400m and could be bought from current cash resources (Vodafone has

£8.5bn in cash on the balance sheet, although net debt stands at c.£26bn).

Currently, the largest operator in New Zealand is Telecom NZ, followed by

Vodafone. This acquisition, if successful, would see Vodafone become the largest

operator. Currently, Vodafone’s New Zealand operations are relatively small and as

such are not broken out in results, remaining part of “other”, which in total

accounted for 7% of FY12 EBITDA. As such, this potential acquisition will have an

incremental impact on the company but it does illustrate one of the company’s

strengths, its geographic diversity. That, coupled with a well covered, high yielding,

dividend (note final went ex-div today) is why Vodafone remains one of our key

portfolio stocks, which at only 10.3x FY13 earnings we would remain comfortable

picking up at current levels.

Providence Resources - Barryroe technical update

Providence Resources has this morning provided a technical update on the

Barryroe discovery which it is currently assessing and appraising post the reentry of

the well last March. The latest process completed and announced today was an

independent third crude assay which came in marginally better than expected. A

sample of the crude from Barryroe verifies a light oil (API 43 degrees) and a wax

content measured by weight of 17% which should prove moveable. The post drill

studies are ongoing with core analysis expected to be completed in the next month

and new independent in place volumetrics by the end of July. Last month,

Providence announced that a horizontal well design/completion could support ~

12,500 bopd & ~ 11MMSCFD. Providence Resources holds an 80% interest in

Barryroe with Lansdowne Oil & Gas holding 20%.

Glanbia

Operation Transformation! Raising price target post solid Q1

Since initiating coverage on Glanbia on the 16th of February 2012 its share price has appreciated by 13%. Post the release of a reassuring interim management statement; we are upgrading our share price target from €5.75 to €6.70. The reiteration of its full year guidance of 5-7% adjusted EPS growth despite softer than expected global commodity markets and economic weakness only serves to highlight the benefits of its transformation into a leading player in the fast growing Global Nutritionals space, which is benefiting from a secular rise in demand. We believe market recognition of the transformation of the group into a leading player in the nutritionals space should lead to multiple expansion.

Nutritionals growth could drive ~22% margin expansion by 2016 We believe Glanbia EBITA margins could expand by 22% over the next five years. This would be facilitated by an increased contribution from the company’s rapidly growing and high margin Global Nutritionals division. Despite the division only being established ten years ago we expect it could make up 71% of the company’s earnings base by 2016. This will be driven in particular by growth in the performance nutrition market, which is expected to expand by 37% over the next five years. The Q1 updates of Glanbia and the US listed retailer GNC, (specialist in the sale of sports nutrition supplements) served to highlight that despite broader weakness in the global economy demand for nutritionals in particular sports nutrition remains strong.

Likely corporate restructuring should act as catalyst An imminent announcement on dairy processing expansion could result in an increase in the company’s free float and act as a share price catalyst. Glanbia Plc and its largest shareholder Glanbia Co-operative Society Limited are currently in discussions about a €150m+ expansion of processing facilities needed in advance of the abolition of milk quotas in 2015. There are a number of permutations with regard to the shape of a potential deal however we expect it could result in the Co-op crossing the Rubicon and bringing its stake in the company below the 50% threshold or entering into a Joint Venture arrangement with the Plc, which would allow the Plc to account for the low margin division below the operating profit line. Despite still being EPS dilutive, such a move could increase company EBITA margins by 120bps in 2012 and serve to accentuate the margins and growth rates being achieved in Global Nutritionals and make the company more attractive in the eyes of potential investors.

Catalyst

Dairy processing expansion announcement June 2012

Estimates (€m) 2011A 2012E 2013E 2014E

Revenue 2,671 2,771 2,929 3,133

EBITA 179 209 233 254

EBITA Margin 7% 8% 8% 8%

Adjusted EPS (cents) 46 50 53 59

Dividend Yield 1.5% 1.6% 1.8% 2.0%

Valuation P/E P/E+1 EV/EBITDA EV/EBITDA+1

Glanbia 11.1x 10.7x 8.9x 8.0x

Source: Company data, Dolmen estimates

www.dolmenstockbrokers.ie PAGE 1

Glanbia

Buy Previous Close: €5.60 Price Target: €6.70

www.dolmenstockbrokers.ie

6TH

JUNE 2012

Analyst: John Mullane

53%

13%

11%

6%

6%11%

Nutritionals CheeseDairy Ingredients Consumer ProductsAgribusiness JV & Associates

Global Nutritionals: The earnings driver

Source: Dolmen 2012 estimates

Company Description

Glanbia is a market leading international nutritional solutions and cheese group. It is organised into two divisions: Dairy Ireland and US Cheese & Global Nutritionals while it also owns stakes in three joint ventures, Southwest Cheese (US), Glanbia Cheese (UK) and Nutricima (Nigeria). The group is headquartered in Ireland however generates 42% of its revenue in the United States. Glanbia Co-op is the company’s largest shareholder with a 54.4% stake.

Investment Thesis

Glanbia should be a primary beneficiary from the growth in demand within the Global Nutritionals market. The sector is growing rapidly in particular the performance nutrition space where Glanbia is a market leader through brands such as Optimum Nutrition. Despite being established only ten years ago, Global Nutritionals should generate 53% of group earnings in 2012 and 71% by 2016. The growth of the division which has structurally higher margins than the remainder of the group, should result in gradual multiple expansion. The potential disposal or stake reduction in its lower margin Dairy Ireland business combined with the potential increase in its free float could act as a near term catalyst.

€2.00€2.50€3.00€3.50€4.00€4.50€5.00€5.50€6.00€6.50

ISEQ (RHS) Glanbia share price

Glanbia shares: Outpreforming the index

Source: Bloomberg

Glanbia

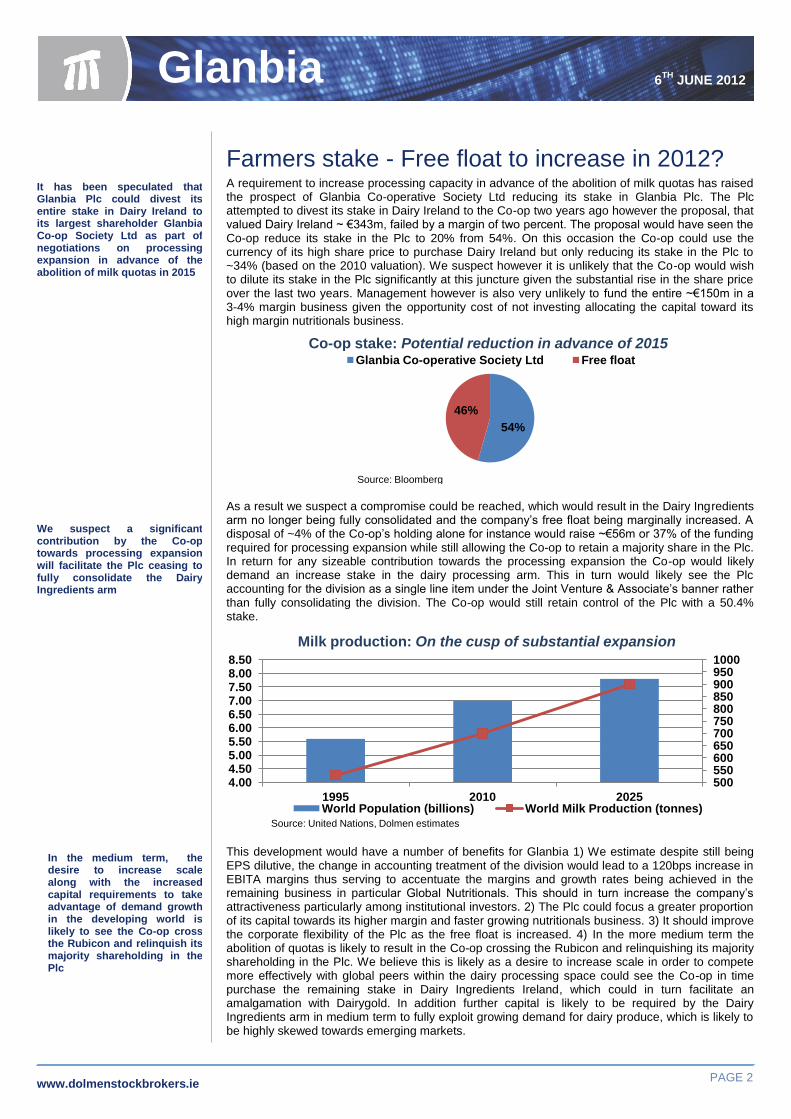

Farmers stake - Free float to increase in 2012? A requirement to increase processing capacity in advance of the abolition of milk quotas has raised the prospect of Glanbia Co-operative Society Ltd reducing its stake in Glanbia Plc. The Plc attempted to divest its stake in Dairy Ireland to the Co-op two years ago however the proposal, that valued Dairy Ireland ~ €343m, failed by a margin of two percent. The proposal would have seen the Co-op reduce its stake in the Plc to 20% from 54%. On this occasion the Co-op could use the currency of its high share price to purchase Dairy Ireland but only reducing its stake in the Plc to ~34% (based on the 2010 valuation). We suspect however it is unlikely that the Co-op would wish to dilute its stake in the Plc significantly at this juncture given the substantial rise in the share price over the last two years. Management however is also very unlikely to fund the entire ~€150m in a 3-4% margin business given the opportunity cost of not investing allocating the capital toward its high margin nutritionals business.

As a result we suspect a compromise could be reached, which would result in the Dairy Ingredients arm no longer being fully consolidated and the company’s free float being marginally increased. A disposal of ~4% of the Co-op’s holding alone for instance would raise ~€56m or 37% of the funding required for processing expansion while still allowing the Co-op to retain a majority share in the Plc. In return for any sizeable contribution towards the processing expansion the Co-op would likely demand an increase stake in the dairy processing arm. This in turn would likely see the Plc accounting for the division as a single line item under the Joint Venture & Associate’s banner rather than fully consolidating the division. The Co-op would still retain control of the Plc with a 50.4% stake.

This development would have a number of benefits for Glanbia 1) We estimate despite still being EPS dilutive, the change in accounting treatment of the division would lead to a 120bps increase in EBITA margins thus serving to accentuate the margins and growth rates being achieved in the remaining business in particular Global Nutritionals. This should in turn increase the company’s attractiveness particularly among institutional investors. 2) The Plc could focus a greater proportion of its capital towards its higher margin and faster growing nutritionals business. 3) It should improve the corporate flexibility of the Plc as the free float is increased. 4) In the more medium term the abolition of quotas is likely to result in the Co-op crossing the Rubicon and relinquishing its majority shareholding in the Plc. We believe this is likely as a desire to increase scale in order to compete more effectively with global peers within the dairy processing space could see the Co-op in time purchase the remaining stake in Dairy Ingredients Ireland, which could in turn facilitate an amalgamation with Dairygold. In addition further capital is likely to be required by the Dairy Ingredients arm in medium term to fully exploit growing demand for dairy produce, which is likely to be highly skewed towards emerging markets.

54%

46%

Glanbia Co-operative Society Ltd Free float

Co-op stake: Potential reduction in advance of 2015

Source: Bloomberg

500 550 600 650 700 750 800 850 900 950 1000

4.00 4.50 5.00 5.50 6.00 6.50 7.00 7.50 8.00 8.50

1995 2010 2025 World Population (billions) World Milk Production (tonnes)

Milk production: On the cusp of substantial expansion

Source: United Nations, Dolmen estimates

www.dolmenstockbrokers.ie PAGE 2

Glanbia 6TH

JUNE 2012

We suspect a significant contribution by the Co-op towards processing expansion will facilitate the Plc ceasing to fully consolidate the Dairy Ingredients arm

In the medium term, the desire to increase scale along with the increased capital requirements to take advantage of demand growth in the developing world is likely to see the Co-op cross the Rubicon and relinquish its majority shareholding in the Plc

It has been speculated that Glanbia Plc could divest its entire stake in Dairy Ireland to its largest shareholder Glanbia Co-op Society Ltd as part of negotiations on processing expansion in advance of the abolition of milk quotas in 2015

Glanbia

Global Nutritionals – Thinking outside the box Global Nutritionals is a complimentary business to US Cheese, utilising whey, a by-product of the cheese making process. The move into this sector serves to highlight the ingenuity of Glanbia’s management in turning what was traditionally treated as waste by cheese producers into value added concentrate. The commodity is used in all three of Glanbia’s nutritional businesses: Performance Nutrition, Ingredient Technologies and Customised Premix, which generate structurally higher margins than other business segments.

Global Nutritionals - Overview

1.) The Customised Premix Solutions business (~20% of divisional revenue) utilises the whey

pool produced by US Cheese to create specialist vitamins and minerals predominately for manufacturers in the food and nutritional space. The division has expanded primarily through acquisition since 2003 with the purchase of US based Seltzer (specialises in nutritional premixes along with the distribution of vitamins and minerals) and the German based Kortis (produces customised nutrient systems for the infant formula, clinical nutrition and dietics market). It also has a facility in Suzhou, China where it manufactures a range of vitamins, minerals, and nutraceuticals for infant formula and food and supplements customers. This leaves it well placed to capitalize on rapidly expanding emerging market growth.

2.) The Ingredients Technologies business (~20% of divisional revenue) processes whey into

ingredient inputs for third party manufacturers of nutritional products in a number of rapidly growing market segments. It provides stabilisation proteins systems for the Greek-Style Yoghurt, the market for which grew by 130% in North America alone in 2011. It also provides functional solutions for the protein bar market which grew at an estimated 15% in 2011.

3.) The Performance Nutrition business (~60% of divisional revenue), incorporates acquisitions:

Optimum Nutrition (market leader in protein powder market), Bio-Engineered Supplements and Nutrition (market leader in pre-mix work-out supplements) and American Body Building (experts in the production of high performance sports beverages).

0% 2% 4% 6% 8%

10% 12% 14%

16%

Dairy Ireland JV & Associates

US Cheese Global Nutritionals

2012 EBITA Margins

Global Nutritionals: Structurally higher margins

Source: Dolmen estimates

PAGE 3

Glanbia 6TH

JUNE 2012

Glanbia is a key supplier to manufacturers within the rapidly growing Greek- Style yoghurt and protein bar markets

Turning what was previously deemed waste into a value added concentrate serves to highlight the ingenuity of management

60% 20%

20%

Global Nutritionals: Performance dominates

Performance Nutrition Customised Premix Ingredient Technologies

Source: Dolmen estimates

www.dolmenstockbrokers.ie

Glanbia

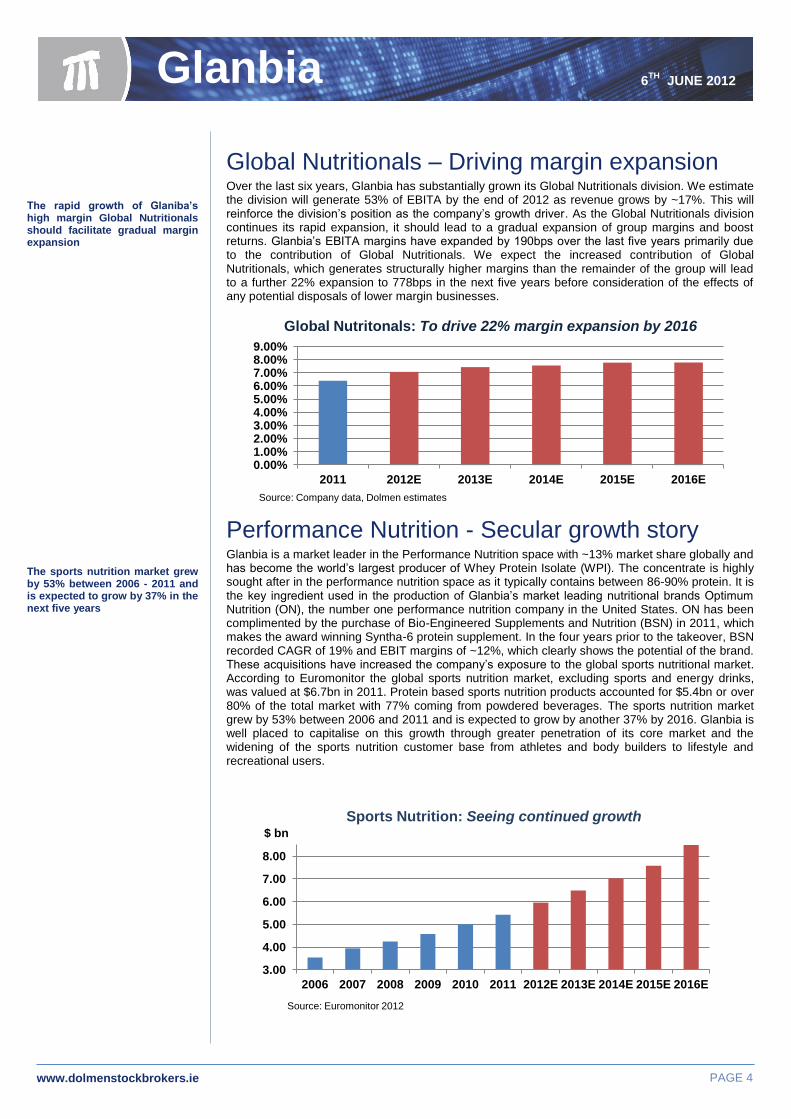

Global Nutritionals – Driving margin expansion Over the last six years, Glanbia has substantially grown its Global Nutritionals division. We estimate the division will generate 53% of EBITA by the end of 2012 as revenue grows by ~17%. This will reinforce the division’s position as the company’s growth driver. As the Global Nutritionals division continues its rapid expansion, it should lead to a gradual expansion of group margins and boost returns. Glanbia’s EBITA margins have expanded by 190bps over the last five years primarily due to the contribution of Global Nutritionals. We expect the increased contribution of Global Nutritionals, which generates structurally higher margins than the remainder of the group will lead to a further 22% expansion to 778bps in the next five years before consideration of the effects of any potential disposals of lower margin businesses.

Performance Nutrition - Secular growth story Glanbia is a market leader in the Performance Nutrition space with ~13% market share globally and has become the world’s largest producer of Whey Protein Isolate (WPI). The concentrate is highly sought after in the performance nutrition space as it typically contains between 86-90% protein. It is the key ingredient used in the production of Glanbia’s market leading nutritional brands Optimum Nutrition (ON), the number one performance nutrition company in the United States. ON has been complimented by the purchase of Bio-Engineered Supplements and Nutrition (BSN) in 2011, which makes the award winning Syntha-6 protein supplement. In the four years prior to the takeover, BSN recorded CAGR of 19% and EBIT margins of ~12%, which clearly shows the potential of the brand. These acquisitions have increased the company’s exposure to the global sports nutritional market. According to Euromonitor the global sports nutrition market, excluding sports and energy drinks, was valued at $6.7bn in 2011. Protein based sports nutrition products accounted for $5.4bn or over 80% of the total market with 77% coming from powdered beverages. The sports nutrition market grew by 53% between 2006 and 2011 and is expected to grow by another 37% by 2016. Glanbia is well placed to capitalise on this growth through greater penetration of its core market and the widening of the sports nutrition customer base from athletes and body builders to lifestyle and recreational users.

0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00% 9.00%

2011 2012E 2013E 2014E 2015E 2016E

Source: Company data, Dolmen estimates

Global Nutritonals: To drive 22% margin expansion by 2016

3.00

4.00

5.00

6.00

7.00

8.00

2006 2007 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E

Sports Nutrition: Seeing continued growth

Source: Euromonitor 2012

$ bn

The sports nutrition market grew by 53% between 2006 - 2011 and is expected to grow by 37% in the next five years

.

1ST

JUNE 2012

PAGE 4

Glanbia 6TH

JUNE 2012

The rapid growth of Glaniba’s high margin Global Nutritionals should facilitate gradual margin expansion

.

www.dolmenstockbrokers.ie

Glanbia

Developed player - Underdeveloped market Glanbia is well placed to be one of the primary beneficiaries from industry growth due to its status as a highly developed player in an underdeveloped market. The performance nutrition market while rapidly growing is still in its infancy with a proliferation of small and underdeveloped business with Muscletech and Cytosport being among the largest players of scale are both privately owned. As a result Glanbia has been able to grow at twice the market rate. The company should be able to use both its scale and market leading position to further consolidate its industry leading position through organic growth of its core brands such as Optimum Nutrition and BSN, which it is also likely to be complimented by further earnings accretive acquisitions in the performance nutrition space.

Cheese - World leading barrel cheese maker The US Cheese business has been a star performer in Glanbia’s stable. The business has grown rapidly and Glanbia now ranks as the number one cheese producer in the US and which generates 13% of group EBITA. The company also operates two Joint Ventures (JV’s) in the cheese segment. Through its 50/50 JV Greater South West Agency, it produces American style cheese and whey protein for sale in the US and on the global nutritional market. The Glanbia Cheese business, its 51% JV with Leprino Foods, is Europe’s largest supplier of mozzarella cheese to the food services and retail pizza sector. We expect the division should experience continued growth in the medium term driven by emerging market demand.

Consumer Foods - Well positioned for the turn The Consumer Foods division (~10% group revenue) uses ~17% of milk processed by Glanbia on an annual basis to create many leading Dairy brands such as Avonmore Milk and Kilmeaden cheese, while also operating the Yoplait franchise in Ireland. Last month’s announcement that Glanbia had sold its Irish Yoplait franchise back to Yoplait for €18m is a positive development. The move is unlikely to have a material impact on earnings however it will decrease Glanbia’s net debt levels by 3.7%. Currently, the operating environment remains challenging due to a combination of significant competition and substantial austerity measures facing the consumer. In the longer term however the fact the company has ~ 60% share of the branded milk products market in Ireland and a 15%-20% market share of the private label liquid milk market leaves it well positioned to take advantage of growth once near term economic headwinds abate.

PAGE 5

Glanbia 6TH

JUNE 2012

61%

39%

Global Nutritionals US Cheese

Revenue Split: US Cheese & Global Nutritionals

Source: Dolmen estimates

50%

24%

26%

Dairy Ingredients Agribusiness Consumer Products

Source: Company reports, Dolmen revenue estimates

Dairy Ireland: Ingredients division the dominant force

The US Cheese business has been one of the star performers in the Glanbia stable and is now the number one cheese producer in the US

Glanbia should be able to use its scale, expertise and resources to further consolidate its industry leading position in a market which is still in its infancy

Glanbia makes many of Irelands leading dairy brands such as Avonmore and Kilmeaden however the operating environment for the division remains challenging

www.dolmenstockbrokers.ie

Glanbia

Dairy Ingredients – Towards 2015 The Dairy Ingredients division (~ 20% of group revenue), which processes ~83% of Glanbia’s milk pool into whey, casesin and butter primarily for export. The division is the obvious beneficiary from the 50% forecasted increase in Irish milk production that will follow the abolition of the Common Agricultural Policy (CAP) quota system in 2015. The United Nations projects that the world population could grow to 7.8bn by 2025. This could see a requirement for an additional 200m tonnes of milk to meet the needs of a growing population. The majority of the demand increase will come from emerging markets whose inhabitants wish to mirror the consumption habits of their western peers. The Dairy Ingredients division is well positioned to exploit growth opportunities in the Middle East and Africa where the company has a strong foothold. Its position as one of the top three producers of Lactose worldwide should ensure it benefits from the growth in the infant formula market which is expanding at 15% a year, driven primarily by demand from Asia Pacific.

PAGE 6

Glanbia

Agribusiness - Driven by sector buoyancy This division (~9% group revenue) is engaged primarily in feed milling and the marketing of a range of farm inputs such as feed and grain to over 5,000 farm suppliers. These items aid farmers in the production of milk which is used by the company's Dairy Ingredients and Consumer Foods divisions. The division performance is highly correlated to that of the Irish dairy sector and as a result it should benefit from the forecasted ~50% increase in Irish milk output.

Nutricma - Capitalising on rising dairy demand

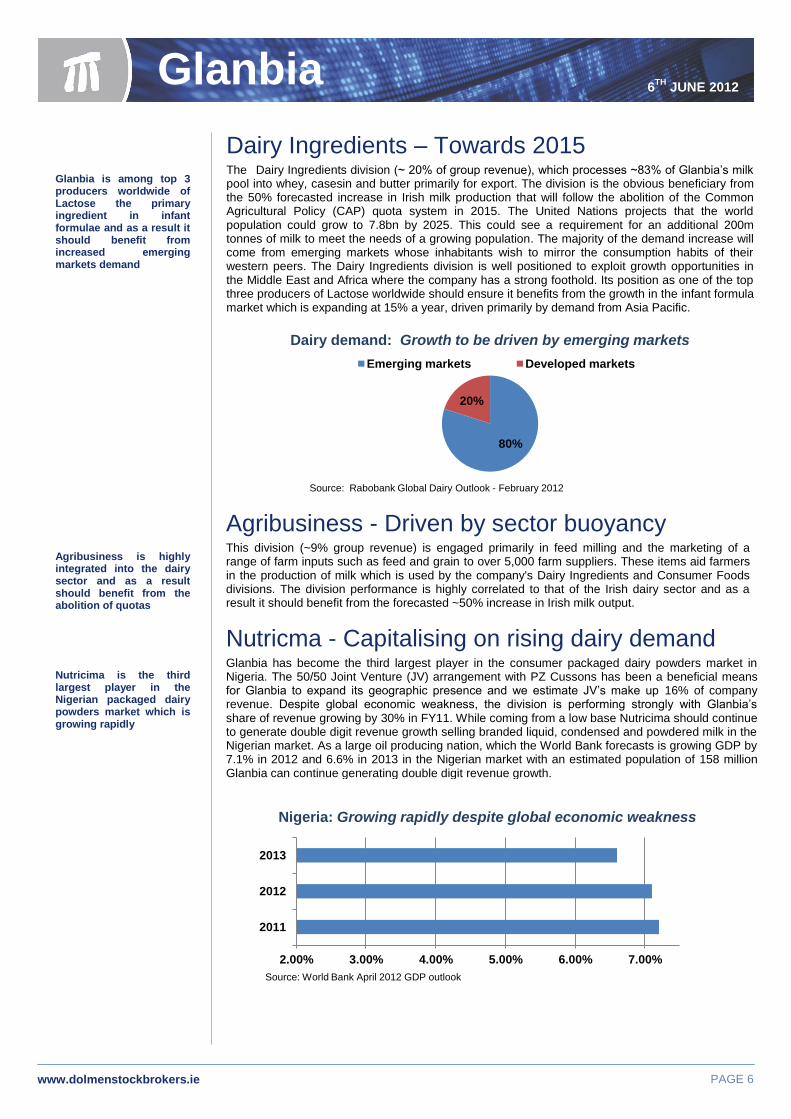

Glanbia has become the third largest player in the consumer packaged dairy powders market in Nigeria. The 50/50 Joint Venture (JV) arrangement with PZ Cussons has been a beneficial means for Glanbia to expand its geographic presence and we estimate JV’s make up 16% of company revenue. Despite global economic weakness, the division is performing strongly with Glanbia’s share of revenue growing by 30% in FY11. While coming from a low base Nutricima should continue to generate double digit revenue growth selling branded liquid, condensed and powdered milk in the Nigerian market. As a large oil producing nation, which the World Bank forecasts is growing GDP by 7.1% in 2012 and 6.6% in 2013 in the Nigerian market with an estimated population of 158 million Glanbia can continue generating double digit revenue growth.

2.00% 3.00% 4.00% 5.00% 6.00% 7.00%

2011

2012

2013

Nigeria: Growing rapidly despite global economic weakness

Source: World Bank April 2012 GDP outlook

Nutricima is the third largest player in the Nigerian packaged dairy powders market which is growing rapidly

Agribusiness is highly integrated into the dairy sector and as a result should benefit from the abolition of quotas

80%

20%

Emerging markets Developed markets

Dairy demand: Growth to be driven by emerging markets

Source: Rabobank Global Dairy Outlook - February 2012

6TH

JUNE 2012

Glanbia is among top 3 producers worldwide of Lactose the primary ingredient in infant formulae and as a result it should benefit from increased emerging markets demand

www.dolmenstockbrokers.ie

Glanbia

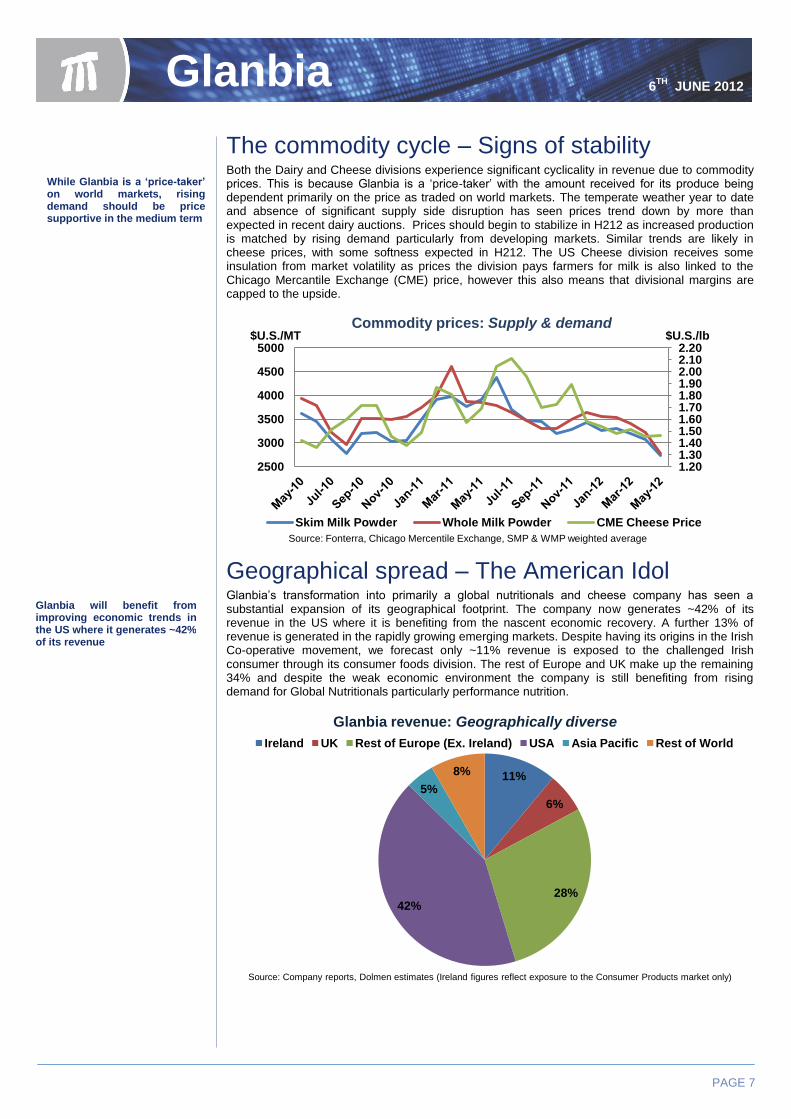

The commodity cycle – Signs of stability Both the Dairy and Cheese divisions experience significant cyclicality in revenue due to commodity prices. This is because Glanbia is a ‘price-taker’ with the amount received for its produce being dependent primarily on the price as traded on world markets. The temperate weather year to date and absence of significant supply side disruption has seen prices trend down by more than expected in recent dairy auctions. Prices should begin to stabilize in H212 as increased production is matched by rising demand particularly from developing markets. Similar trends are likely in cheese prices, with some softness expected in H212. The US Cheese division receives some insulation from market volatility as prices the division pays farmers for milk is also linked to the Chicago Mercantile Exchange (CME) price, however this also means that divisional margins are capped to the upside.

Geographical spread – The American Idol Glanbia’s transformation into primarily a global nutritionals and cheese company has seen a substantial expansion of its geographical footprint. The company now generates ~42% of its revenue in the US where it is benefiting from the nascent economic recovery. A further 13% of revenue is generated in the rapidly growing emerging markets. Despite having its origins in the Irish Co-operative movement, we forecast only ~11% revenue is exposed to the challenged Irish consumer through its consumer foods division. The rest of Europe and UK make up the remaining 34% and despite the weak economic environment the company is still benefiting from rising demand for Global Nutritionals particularly performance nutrition.

11%

6%

28% 42%

5%

8%

Ireland UK Rest of Europe (Ex. Ireland) USA Asia Pacific Rest of World

Source: Company reports, Dolmen estimates (Ireland figures reflect exposure to the Consumer Products market only)

Glanbia revenue: Geographically diverse

Glanbia will benefit from improving economic trends in the US where it generates ~42% of its revenue

1ST

JU1STNE 2012

While Glanbia is a ‘price-taker’ on world markets, rising demand should be price supportive in the medium term

1.20 1.30 1.40 1.50 1.60 1.70 1.80 1.90 2.00 2.10 2.20

2500

3000

3500

4000

4500

5000

Commodity prices: Supply & demand

Skim Milk Powder Whole Milk Powder CME Cheese Price

$U.S./MT $U.S./lb

Source: Fonterra, Chicago Mercentile Exchange, SMP & WMP weighted average

Glanbia 6TH

JUNE 2012

PAGE 7

Glanbia

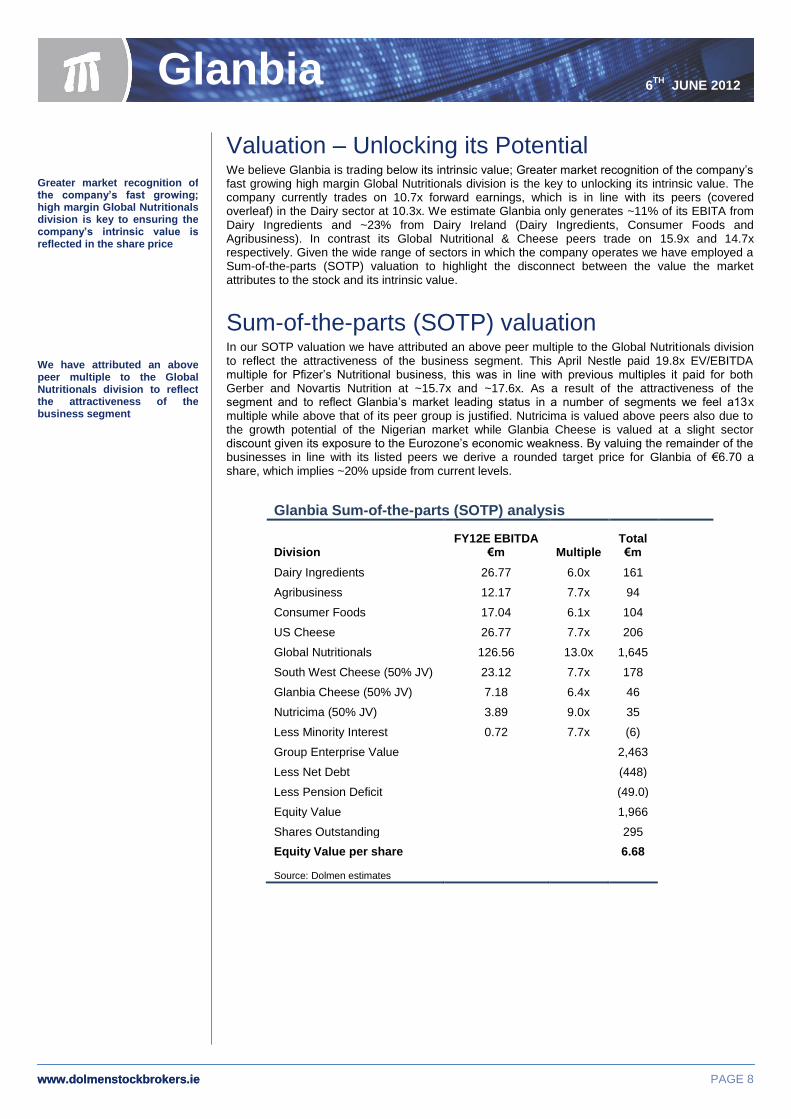

Valuation – Unlocking its Potential We believe Glanbia is trading below its intrinsic value; Greater market recognition of the company’s fast growing high margin Global Nutritionals division is the key to unlocking its intrinsic value. The company currently trades on 10.7x forward earnings, which is in line with its peers (covered overleaf) in the Dairy sector at 10.3x. We estimate Glanbia only generates ~11% of its EBITA from Dairy Ingredients and ~23% from Dairy Ireland (Dairy Ingredients, Consumer Foods and Agribusiness). In contrast its Global Nutritional & Cheese peers trade on 15.9x and 14.7x respectively. Given the wide range of sectors in which the company operates we have employed a Sum-of-the-parts (SOTP) valuation to highlight the disconnect between the value the market attributes to the stock and its intrinsic value.

Sum-of-the-parts (SOTP) valuation In our SOTP valuation we have attributed an above peer multiple to the Global Nutritionals division to reflect the attractiveness of the business segment. This April Nestle paid 19.8x EV/EBITDA multiple for Pfizer’s Nutritional business, this was in line with previous multiples it paid for both Gerber and Novartis Nutrition at ~15.7x and ~17.6x. As a result of the attractiveness of the segment and to reflect Glanbia’s market leading status in a number of segments we feel a13x multiple while above that of its peer group is justified. Nutricima is valued above peers also due to the growth potential of the Nigerian market while Glanbia Cheese is valued at a slight sector discount given its exposure to the Eurozone’s economic weakness. By valuing the remainder of the businesses in line with its listed peers we derive a rounded target price for Glanbia of €6.70 a share, which implies ~20% upside from current levels.

Glanbia Sum-of-the-parts (SOTP) analysis

Division FY12E EBITDA

€m Multiple Total €m

Dairy Ingredients 26.77 6.0x 161

Agribusiness 12.17 7.7x 94

Consumer Foods 17.04 6.1x 104

US Cheese 26.77 7.7x 206

Global Nutritionals 126.56 13.0x 1,645

South West Cheese (50% JV) 23.12 7.7x 178

Glanbia Cheese (50% JV) 7.18 6.4x 46

Nutricima (50% JV) 3.89 9.0x 35

Less Minority Interest 0.72 7.7x (6)

Group Enterprise Value

2,463

Less Net Debt

(448)

Less Pension Deficit

(49.0)

Equity Value

1,966

Shares Outstanding

295 Equity Value per share

6.68

Source: Dolmen estimates

www.dolmenstockbrokers.ie PAGE 8

Glanbia

www.dolmenstockbrokers.ie

Glanbia 6TH

JUNE 2012

Greater market recognition of the company’s fast growing; high margin Global Nutritionals division is key to ensuring the company’s intrinsic value is reflected in the share price

We have attributed an above peer multiple to the Global Nutritionals division to reflect the attractiveness of the business segment

Glanbia

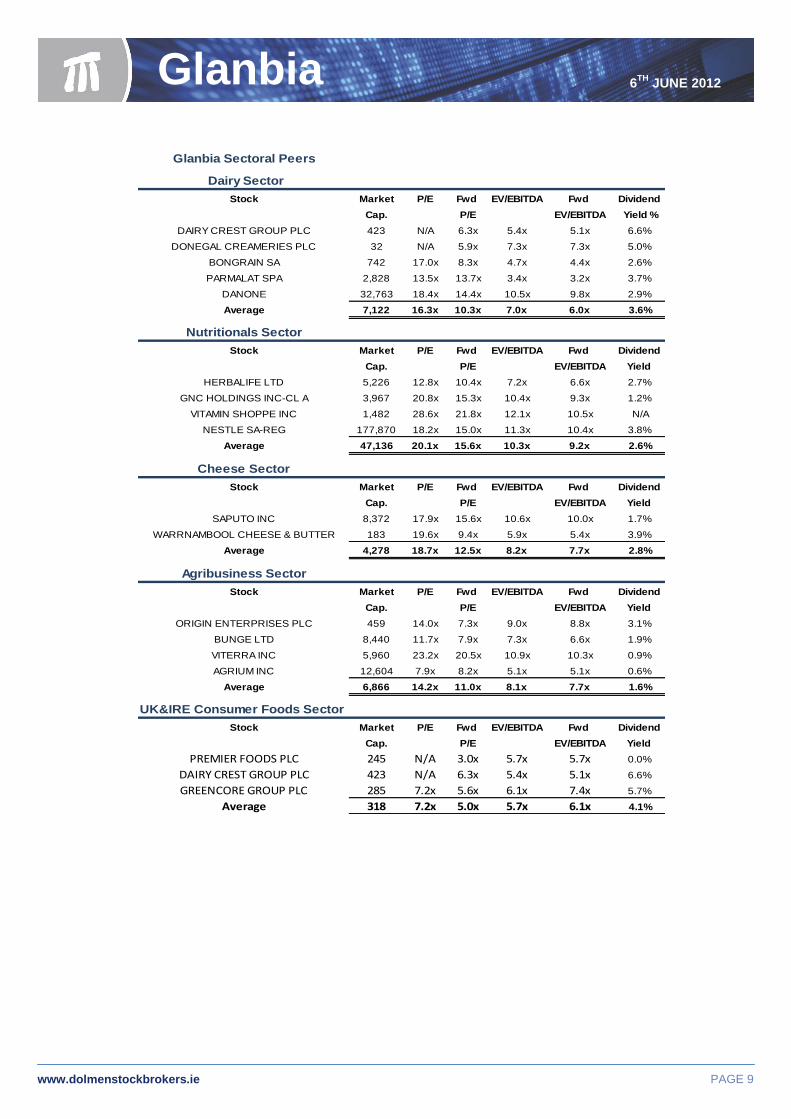

Glanbia Sectoral Peers

Dairy Sector

Stock Market P/E Fwd EV/EBITDA Fwd Dividend

Cap. P/E EV/EBITDA Yield %

DAIRY CREST GROUP PLC 423 N/A 6.3x 5.4x 5.1x 6.6%

DONEGAL CREAMERIES PLC 32 N/A 5.9x 7.3x 7.3x 5.0%

BONGRAIN SA 742 17.0x 8.3x 4.7x 4.4x 2.6%

PARMALAT SPA 2,828 13.5x 13.7x 3.4x 3.2x 3.7%

DANONE 32,763 18.4x 14.4x 10.5x 9.8x 2.9%

Average 7,122 16.3x 10.3x 7.0x 6.0x 3.6%

Nutritionals Sector

Stock Market P/E Fwd EV/EBITDA Fwd Dividend

Cap. P/E EV/EBITDA Yield

HERBALIFE LTD 5,226 12.8x 10.4x 7.2x 6.6x 2.7%

GNC HOLDINGS INC-CL A 3,967 20.8x 15.3x 10.4x 9.3x 1.2%

VITAMIN SHOPPE INC 1,482 28.6x 21.8x 12.1x 10.5x N/A

NESTLE SA-REG 177,870 18.2x 15.0x 11.3x 10.4x 3.8%

Average 47,136 20.1x 15.6x 10.3x 9.2x 2.6%

Cheese Sector

Stock Market P/E Fwd EV/EBITDA Fwd Dividend

Cap. P/E EV/EBITDA Yield

SAPUTO INC 8,372 17.9x 15.6x 10.6x 10.0x 1.7%

WARRNAMBOOL CHEESE & BUTTER 183 19.6x 9.4x 5.9x 5.4x 3.9%

Average 4,278 18.7x 12.5x 8.2x 7.7x 2.8%

Agribusiness Sector

Stock Market P/E Fwd EV/EBITDA Fwd Dividend

Cap. P/E EV/EBITDA Yield

ORIGIN ENTERPRISES PLC 459 14.0x 7.3x 9.0x 8.8x 3.1%

BUNGE LTD 8,440 11.7x 7.9x 7.3x 6.6x 1.9%

VITERRA INC 5,960 23.2x 20.5x 10.9x 10.3x 0.9%

AGRIUM INC 12,604 7.9x 8.2x 5.1x 5.1x 0.6%

Average 6,866 14.2x 11.0x 8.1x 7.7x 1.6%

UK&IRE Consumer Foods Sector

Stock Market P/E Fwd EV/EBITDA Fwd Dividend

Cap. P/E EV/EBITDA Yield

PREMIER FOODS PLC 245 N/A 3.0x 5.7x 5.7x 0.0%

DAIRY CREST GROUP PLC 423 N/A 6.3x 5.4x 5.1x 6.6%

GREENCORE GROUP PLC 285 7.2x 5.6x 6.1x 7.4x 5.7%

Average 318 7.2x 5.0x 5.7x 6.1x 4.1%

www.dolmenstockbrokers.ie PAGE 9

Glanbia 6TH

JUNE 2012

Glanbia

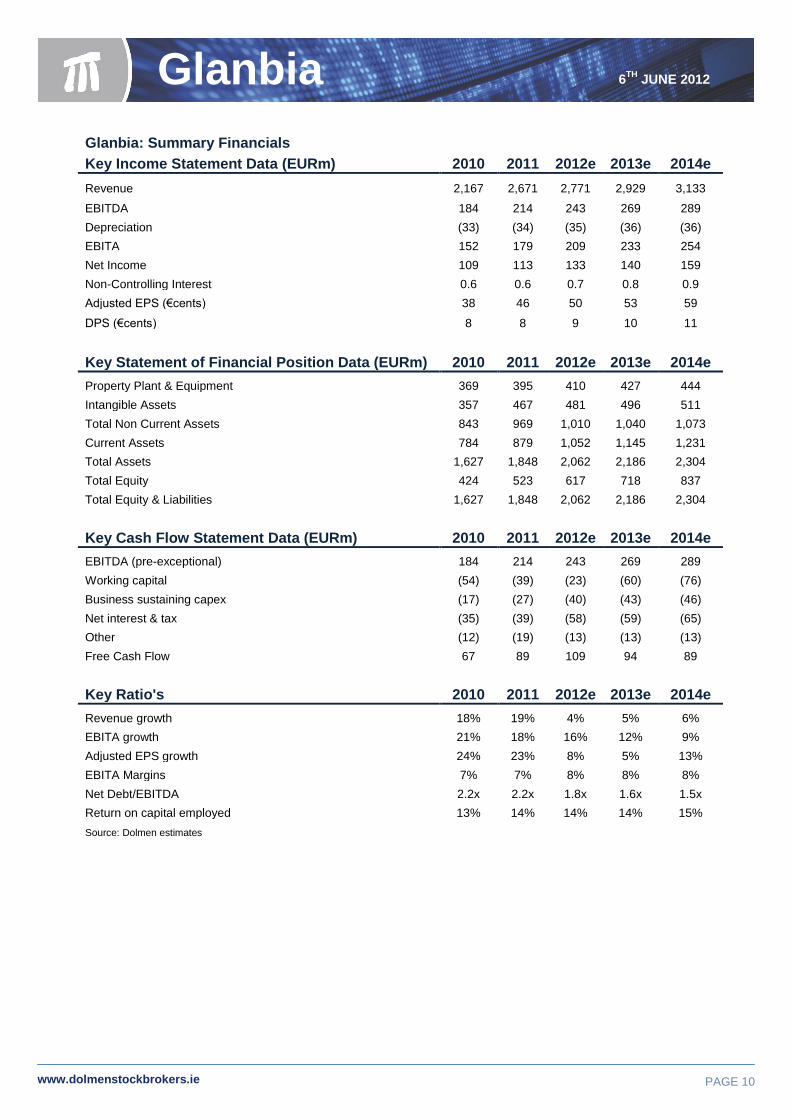

Glanbia: Summary Financials Key Income Statement Data (EURm) 2010 2011 2012e 2013e 2014e

Revenue 2,167 2,671 2,771 2,929 3,133

EBITDA 184 214 243 269 289

Depreciation (33) (34) (35) (36) (36)

EBITA 152 179 209 233 254

Net Income 109 113 133 140 159

Non-Controlling Interest 0.6 0.6 0.7 0.8 0.9

Adjusted EPS (€cents) 38 46 50 53 59

DPS (€cents) 8 8 9 10 11

Key Statement of Financial Position Data (EURm) 2010 2011 2012e 2013e 2014e

Property Plant & Equipment 369 395 410 427 444

Intangible Assets 357 467 481 496 511

Total Non Current Assets 843 969 1,010 1,040 1,073

Current Assets 784 879 1,052 1,145 1,231

Total Assets 1,627 1,848 2,062 2,186 2,304

Total Equity 424 523 617 718 837

Total Equity & Liabilities 1,627 1,848 2,062 2,186 2,304

Key Cash Flow Statement Data (EURm) 2010 2011 2012e 2013e 2014e

EBITDA (pre-exceptional) 184 214 243 269 289

Working capital (54) (39) (23) (60) (76)

Business sustaining capex (17) (27) (40) (43) (46)

Net interest & tax (35) (39) (58) (59) (65)

Other (12) (19) (13) (13) (13)

Free Cash Flow 67 89 109 94 89

Key Ratio's 2010 2011 2012e 2013e 2014e

Revenue growth 18% 19% 4% 5% 6%

EBITA growth 21% 18% 16% 12% 9%

Adjusted EPS growth 24% 23% 8% 5% 13%

EBITA Margins 7% 7% 8% 8% 8%

Net Debt/EBITDA 2.2x 2.2x 1.8x 1.6x 1.5x

Return on capital employed 13% 14% 14% 14% 15%

Source: Dolmen estimates

1ST

JUNE 2012

www.dolmenstockbrokers.ie

Glanbia

6TH

JUNE 2012

PAGE 10

Glanbia

Dublin: 75 St. Stephen’s Green, Dublin 2, Ireland. Tel : +353 1 633 3800. Fax : +353 1 633 3856/+353 1 633 3857

CORK: Dolmen House, 45 South Mall, Cork. Tel: +353 21 422 2122.

LIMERICK: Theatre Court, Lower Mallow Street, Limerick. Tel: +353 61 436500.

Email : [email protected] web : www.dolmenstockbrokers.ie

www.dolmenstockbrokers.ie

Regulatory Information

Dolmen Securities Limited is regulated by the Central Bank of Ireland. Dolmen Securities Limited is a member firm of the London Stock Exchange. Dolmen Stockbrokers is regulated by the Central Bank of Ireland. Dolmen Stockbrokers is a member firm of the Irish Stock Exchange and the London Stock Exchange.

This report has been prepared by Dolmen Stockbrokers (‘Dolmen’) for information purposes in order to assist investors to make their own investment decisions and is not intended to and does not constitute personal recommendations nor provide the sole basis for any evaluation of the securities discussed. Specifically the information contained in this report should not be taken as an offer or solicitation of investment advice or, encourage the purchase or sale of any particular security, option, future or other derivative investment. Not all recommendations are necessarily suitable for all investors and Dolmen recommend that specific advice should always be sought prior to investment, based on the particular circumstances of the investor.

The purpose of the note is to provide clients with an update on relevant equity market developments. Stocks mentioned may not be formally covered by our research team and the attached commentary is by way of market update only. If a stock has neither a recommendation nor a target price then it is definitively not a stock formally covered by DSL and it is not feasible nor does DSL have any obligation to keep clients updated on developments in respect of such stocks.

If a piece of research is to be included in the daily research and no target price for the stock is included it is not intended to provide formal coverage of this stock. It arises as a result of Broker or Client request and there is no certainty that we will, nor any ensuing obligation to, provide follow up coverage to this note or formally cover this stock. Our buy/sell/hold recommendation is based on a desktop review of market consensus.

Although the information in this report has been obtained from sources, which Dolmen believes to be reliable and all reasonable efforts are made to present accurate information Dolmen give no warranty or guarantee as to, and do not accept responsibility for, the correctness, completeness, timeliness or accuracy of the information provided or its transmission. Nor shall Dolmen, or any of its employees, directors or agents, be liable to for any losses, damages, costs, claims, demands or expenses of any kind whatsoever, whether direct or indirect, suffered or incurred in consequence of any use of, or reliance upon, the information. Any person acting on the information contained in this report does so entirely at his or her own risk.

All estimates, views and opinions included in this report constitute Dolmen’s judgment as of the date of the report but may be subject to change without notice. Changes to assumptions may have a material impact on any recommendations made herein.

Unless specifically indicated to the contrary this report has not been disclosed to the covered issuer(s) in advance of publication.

Past performance is not a reliable guide to future performance. The value of your investment may go down as well as up. Investments denominated in foreign currencies are subject to fluctuations in exchange rates, which may have an adverse affect on the value of the investments, sale proceeds, and on dividend or interest income. The income you get from your investment may go down as well as up. Figures quoted are estimates only; they are not a reliable guide to the future performance of this investment. Investors should be aware that forwarding looking statements and forecasts may not be realised.

This report is the property of Dolmen and may not be reproduced (in whole or in part) altered, transmitted or made available to any other person without the prior written permission of Dolmen.

Conflicts of Interest & Share Ownership Policy

It is noted that research analysts' compensation is impacted upon by overall firm profitability and accordingly may be affected to some extent by revenues arising other Dolmen business units including Fund Management and Stockbroking. Revenues in these business units may derive in part from the recommendations or views in this report. Notwithstanding, Dolmen is satisfied that the objectivity of views and recommendations contained in this report has not been compromised.

Dolmen permits research analysts to own shares and/ or derivative positions in the companies they publish research, views and recommendations on. Accordingly analysts involved in the production of this report may have positions in any securities herein. Dolmen ensures that all staff dealing is undertaken in strict compliance with Dolmen’s internal staff dealing procedures. Therefore Dolmen is satisfied that the impartiality of research, views and recommendations remains assured.

Our conflicts of interest management policy is available at the following link;

http://www.dolmenstockbrokers.ie/regulation_mifld.shtml

Analyst Certification

Each research analyst responsible for the content of this report, in whole or in part, certifies that: (1) all of the views expressed accurately reflect his or her personal views about those securities or issuers; and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in the research report. Ian Hunter, Brian Gallagher and John Mullane are responsible for the production of this report. Ian Hunter, Brian Gallagher and John Mullane are equity analysts.

For US Persons Only

This report is only provided in the US to major institutional investors as defined by s.15 a-6 of the Securities Exchange Act, 1934 as amended. A US recipient of this report shall not distribute or provide this report or any part thereof to any other person.

Other important disclosures

A description of Dolmen’s basis of valuation or any other methodology used to evaluate a financial instrument or issuer or to set a price target and the meaning of any recommendation made such as buy, sell or hold is set out at: http://www.dolmenstockbrokers.ie/disclosures.shtml

Prices quoted in this report, unless otherwise indicated, are as of close on the previous trading day.

A summary of existing and prior price targets for each company under coverage is available at http://www.dolmenstockbrokers.ie/disclosures.shtml

Dolmen Stockbrokers, 75 St. Stephen’s Green, Dublin 2, Ireland.

Related Documents