Doing Business in Doing Business in Europe Europe Legal rules, and Legal rules, and traps for the unwary traps for the unwary

Doing Business in Europe Legal rules, and traps for the unwary.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Doing Business in EuropeDoing Business in EuropeDoing Business in EuropeDoing Business in Europe

Legal rules, and traps for Legal rules, and traps for the unwarythe unwary

Legal rules, and traps for Legal rules, and traps for the unwarythe unwary

Osborne ClarkeOsborne ClarkeOsborne ClarkeOsborne Clarke

Pan European Law FirmPan European Law Firm

Providing a complete range of legal servicesProviding a complete range of legal services

Technology industry focusTechnology industry focus

Recognised as European Technology Law Recognised as European Technology Law Firm of the Year 2001 and 2002 by the Firm of the Year 2001 and 2002 by the European Technology ForumEuropean Technology Forum

Office in Palo Alto – European legal advice in Office in Palo Alto – European legal advice in Californian timeCalifornian time

European Law?European Law?European Law?European Law?

Not quiteNot quite

European Treaties, Regulations and European Treaties, Regulations and Directives are in place but….Directives are in place but….

Advice is still required on a country Advice is still required on a country by country basisby country basis

Do you need a presence in Do you need a presence in Europe?Europe?

Do you need a presence in Do you need a presence in Europe?Europe?

You could use existing channels – You could use existing channels – can be more can be more cost effective to employ an agent or distributor with cost effective to employ an agent or distributor with local knowledge local knowledge

Types of relationship which are dealt with very Types of relationship which are dealt with very differently from a legal perspective:differently from a legal perspective:

Agent - generates leads or enters into agreement with Agent - generates leads or enters into agreement with customer on behalf of the suppliercustomer on behalf of the supplier

Distributor – is an independent party which buys your Distributor – is an independent party which buys your product and sells them on its own accountproduct and sells them on its own account

Distributor is usually preferred choice as you can to Distributor is usually preferred choice as you can to a certain extent leave them to ita certain extent leave them to it

Why use an Agent?Why use an Agent?Why use an Agent?Why use an Agent?

Greater control over them. You also have Greater control over them. You also have more choice over who they sell to and more choice over who they sell to and prices they sell at (important in some prices they sell at (important in some industries e.g. fashion) – Unable to industries e.g. fashion) – Unable to impose such controls in distribution impose such controls in distribution agreements without falling foul of anti-agreements without falling foul of anti-trust lawtrust law

Agents are usually paid less commissionAgents are usually paid less commission

Agency AgreementsAgency AgreementsAgency AgreementsAgency Agreements

Key Aspects:Key Aspects:

ExclusivityExclusivity

TerritoryTerritory

TermTerm

Agent’s authority Agent’s authority

Commission/payment termsCommission/payment terms

Consequences of terminationConsequences of termination

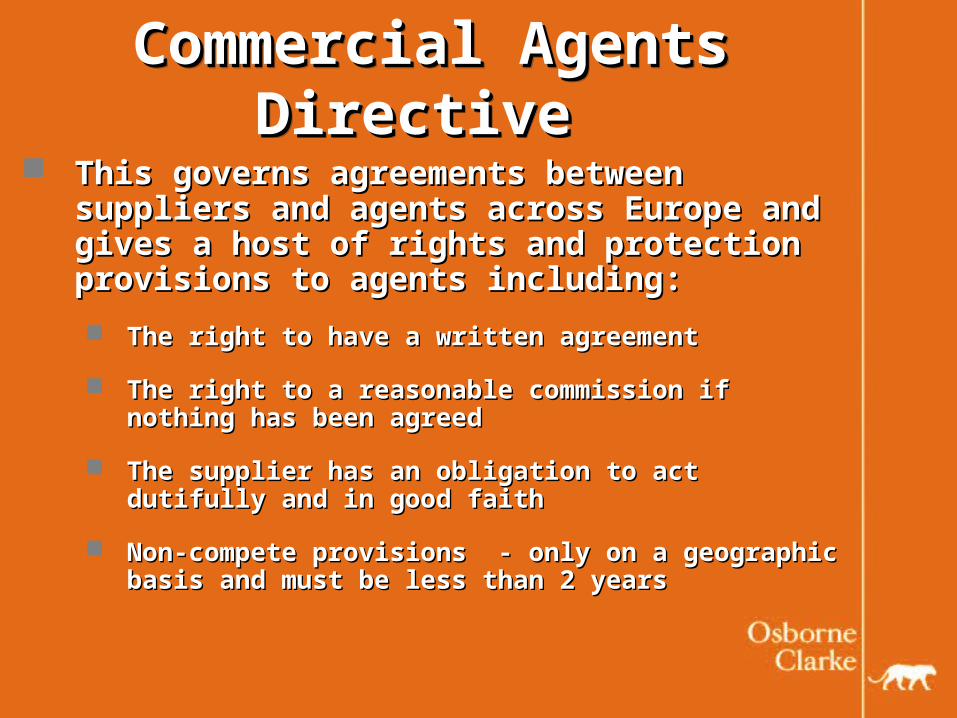

Commercial Agents Directive Commercial Agents Directive Commercial Agents Directive Commercial Agents Directive This governs agreements between suppliers This governs agreements between suppliers

and agents across Europe and gives a host of and agents across Europe and gives a host of rights and protection provisions to agents rights and protection provisions to agents including:including:

The right to have a written agreementThe right to have a written agreement

The right to a reasonable commission if nothing has The right to a reasonable commission if nothing has been agreedbeen agreed

The supplier has an obligation to act dutifully and in The supplier has an obligation to act dutifully and in good faith good faith

Non-compete provisions - only on a geographic basis Non-compete provisions - only on a geographic basis and must be less than 2 years and must be less than 2 years

Commercial Agents DirectiveCommercial Agents DirectiveCommercial Agents DirectiveCommercial Agents Directive

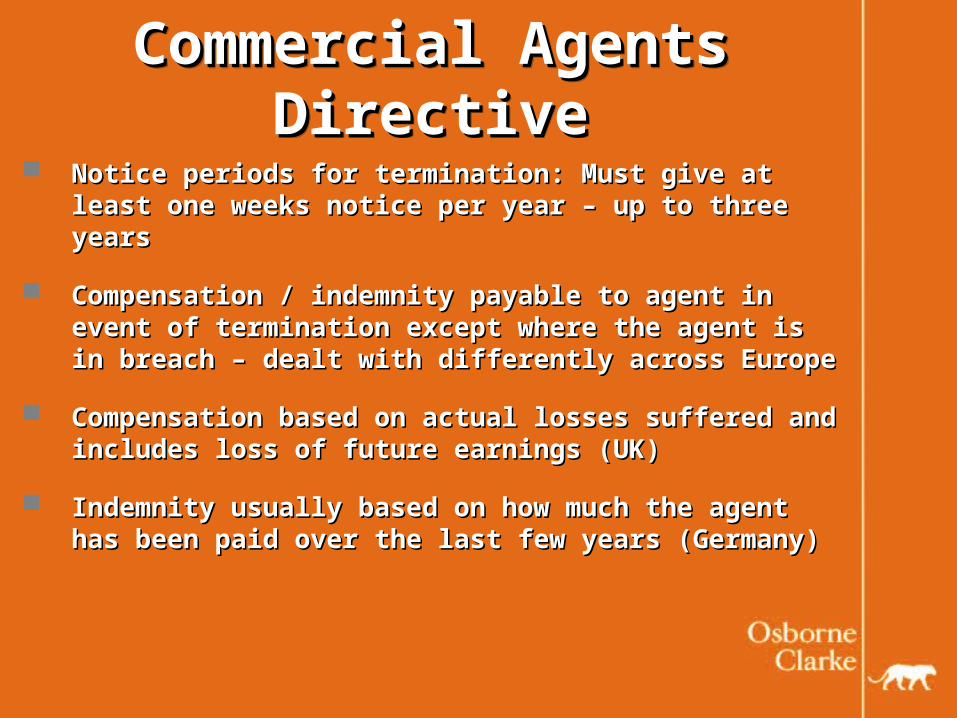

Notice periods for termination: Must give at least Notice periods for termination: Must give at least one weeks notice per year – up to three yearsone weeks notice per year – up to three years

Compensation / indemnity payable to agent in Compensation / indemnity payable to agent in event of termination except where the agent is in event of termination except where the agent is in breach – dealt with differently across Europebreach – dealt with differently across Europe

Compensation based on actual losses suffered Compensation based on actual losses suffered and includes loss of future earnings (UK)and includes loss of future earnings (UK)

Indemnity usually based on how much the agent Indemnity usually based on how much the agent has been paid over the last few years (Germany)has been paid over the last few years (Germany)

Commercial Agents DirectiveCommercial Agents DirectiveCommercial Agents DirectiveCommercial Agents Directive

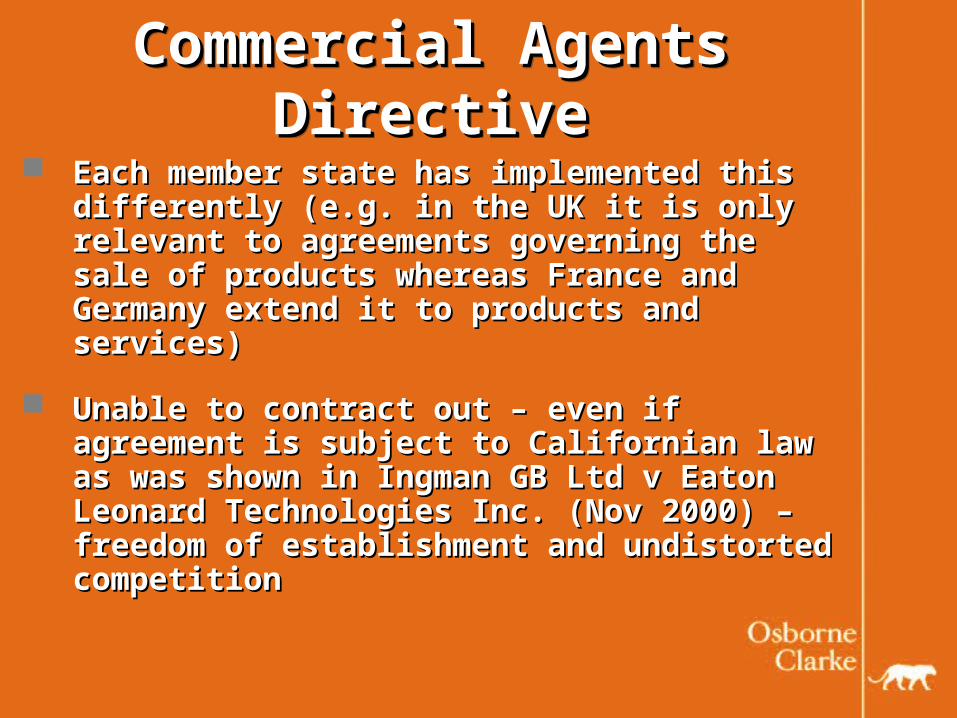

Each member state has implemented this Each member state has implemented this differently (e.g. in the UK it is only relevant differently (e.g. in the UK it is only relevant to agreements governing the sale of to agreements governing the sale of products whereas France and Germany products whereas France and Germany extend it to products and services)extend it to products and services)

Unable to contract out – even if agreement Unable to contract out – even if agreement is subject to Californian law as was shown is subject to Californian law as was shown in Ingman GB Ltd v Eaton Leonard in Ingman GB Ltd v Eaton Leonard Technologies Inc. (Nov 2000) – freedom of Technologies Inc. (Nov 2000) – freedom of establishment and undistorted competitionestablishment and undistorted competition

Distribution AgreementsDistribution AgreementsDistribution AgreementsDistribution Agreements

No EC Directive governing Distribution No EC Directive governing Distribution agreementsagreements

Many countries in continental Europe Many countries in continental Europe have similar provisions to those in the have similar provisions to those in the Commercial Agents DirectiveCommercial Agents Directive

English law provides very little protection English law provides very little protection to distributors meaning it is possible to to distributors meaning it is possible to terminate on short notice with no terminate on short notice with no compensation payable compensation payable

Distribution AgreementsDistribution AgreementsDistribution AgreementsDistribution AgreementsKey aspects:Key aspects:

ExclusivityExclusivity

TerritoryTerritory

TermTerm

Conditions of supply/delivery Conditions of supply/delivery

Order terms and prices Order terms and prices

Local legal requirements Local legal requirements

Defective product liability/warranties Defective product liability/warranties

Confidentiality provisions Confidentiality provisions

Consequences of terminationConsequences of termination

Anti-trust LawAnti-trust LawAnti-trust LawAnti-trust Law Applicable to distribution agreements with an Applicable to distribution agreements with an

appreciable effect on trade – Look at market shareappreciable effect on trade – Look at market share

The Following are seen to be anti-competitive:The Following are seen to be anti-competitive:

Price fixingPrice fixing

Bid rigging – Agreeing tender prices with competitorsBid rigging – Agreeing tender prices with competitors

Obligations on the distributor not to purchase competing Obligations on the distributor not to purchase competing brandsbrands

Obligations on the distributor to only supply a particular Obligations on the distributor to only supply a particular buyerbuyer

ConsequencesConsequences

Other contractual mattersOther contractual mattersOther contractual mattersOther contractual matters

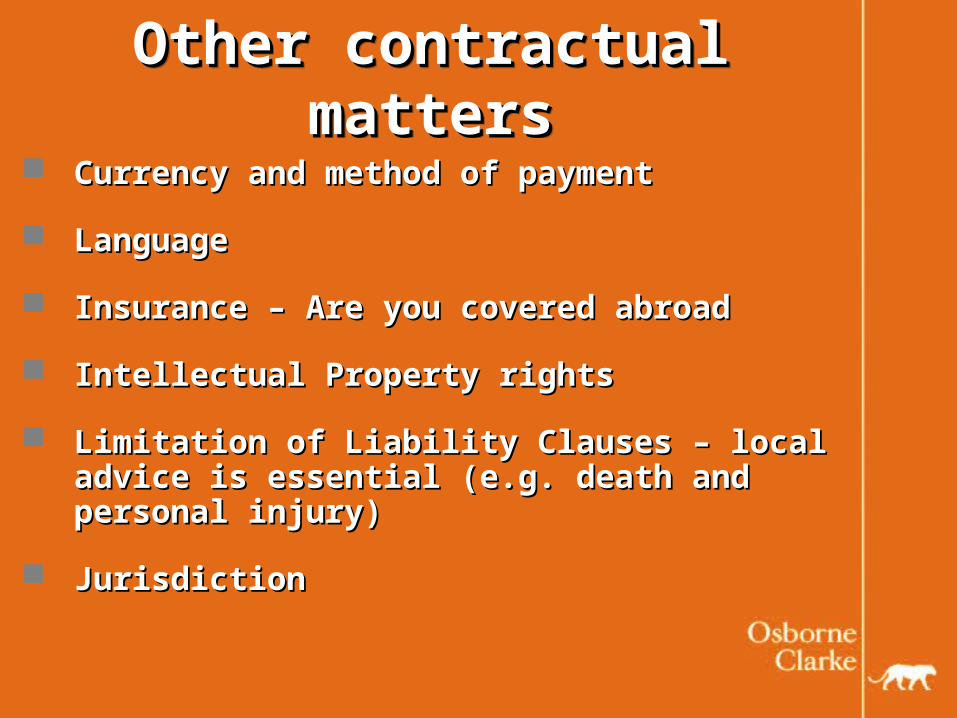

Currency and method of paymentCurrency and method of payment

LanguageLanguage

Insurance – Are you covered abroadInsurance – Are you covered abroad

Intellectual Property rightsIntellectual Property rights

Limitation of Liability Clauses – local advice Limitation of Liability Clauses – local advice is essential (e.g. death and personal injury)is essential (e.g. death and personal injury)

JurisdictionJurisdiction

European EstablishmentEuropean EstablishmentEuropean EstablishmentEuropean Establishment

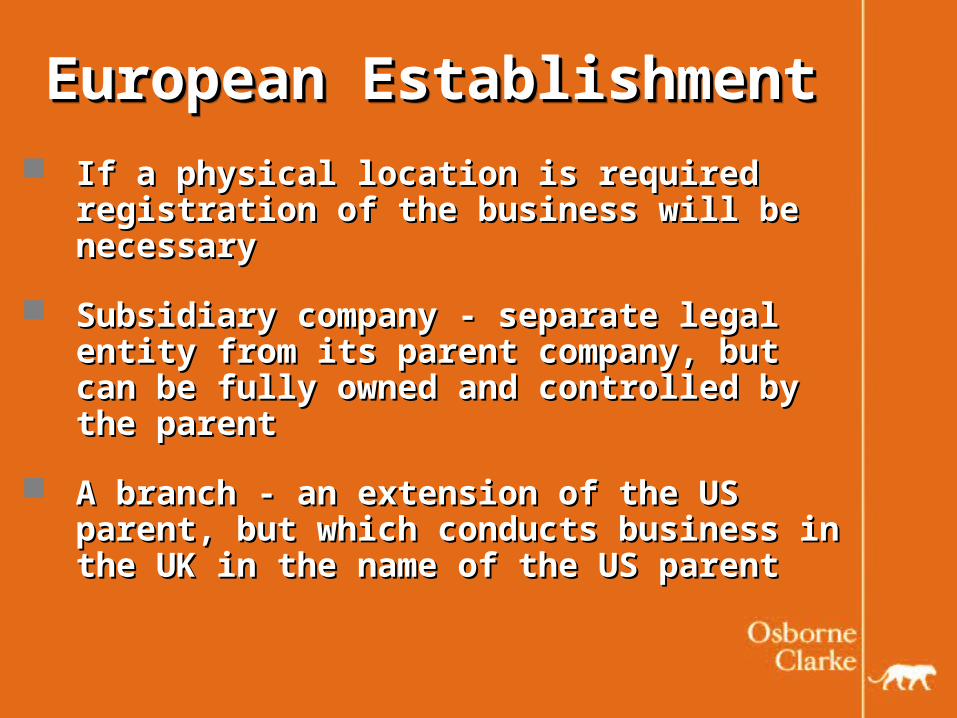

If a physical location is required If a physical location is required registration of the business will be registration of the business will be necessarynecessary

Subsidiary company - separate legal entity Subsidiary company - separate legal entity from its parent company, but can be fully from its parent company, but can be fully owned and controlled by the parentowned and controlled by the parent

A branch - an extension of the US parent, A branch - an extension of the US parent, but which conducts business in the UK in but which conducts business in the UK in the name of the US parent the name of the US parent

Factors to consider Factors to consider Subsidiary vs. BranchSubsidiary vs. Branch

Factors to consider Factors to consider Subsidiary vs. BranchSubsidiary vs. Branch

ControlControl

LiabilityLiability issues issues

Practicalities Practicalities

Privacy law issuesPrivacy law issues

TaxTax

Formalities of EstablishmentFormalities of Establishment

Start-up Costs and SpeedStart-up Costs and Speed

On-going On-going obligations obligations

Labor LawLabor Law

ControlControlControlControl

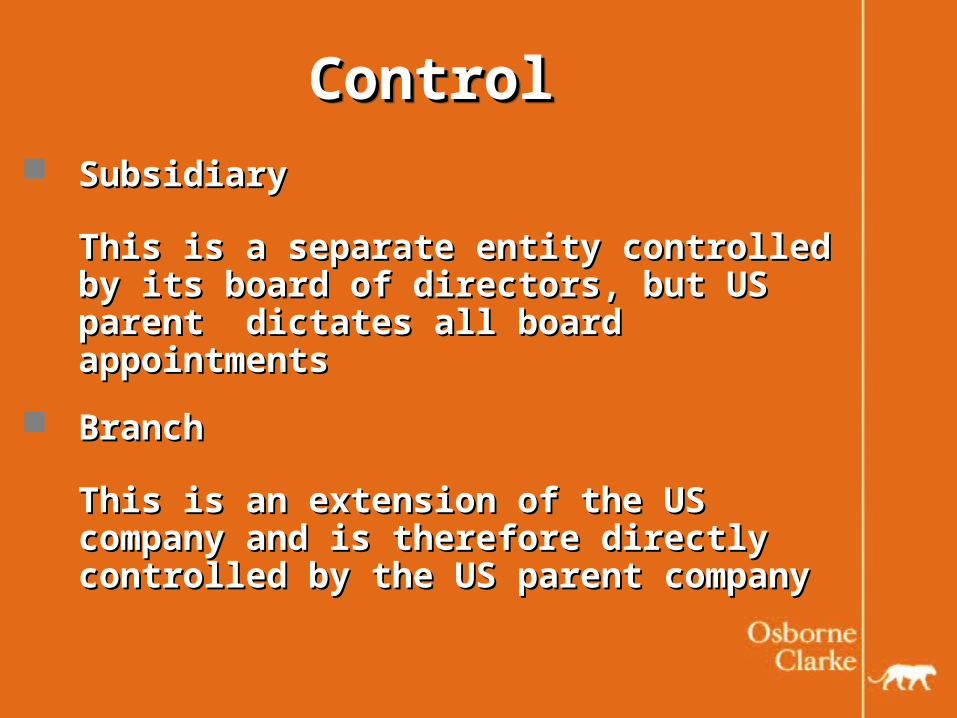

SubsidiarySubsidiary

This is a separate entity controlled by its This is a separate entity controlled by its board of directors, but US parent dictates board of directors, but US parent dictates all board appointments all board appointments

BranchBranch

This is an extension of the US company This is an extension of the US company and is therefore directly controlled by the and is therefore directly controlled by the US parent companyUS parent company

Liability IssuesLiability IssuesLiability IssuesLiability Issues SubsidiarySubsidiary

Shareholders (i.e US Parent) not generally liable for Shareholders (i.e US Parent) not generally liable for acts of the subsidiary company acts of the subsidiary company

Liability is limited to the share capital of the subsidiaryLiability is limited to the share capital of the subsidiary Product liability is a different regime Product liability is a different regime

Directors or other company officers may be personally Directors or other company officers may be personally liable in certain circumstances (e.g. fraudulent or liable in certain circumstances (e.g. fraudulent or wrongful trading)wrongful trading)

BranchBranch

The directors of the US parent are responsible for The directors of the US parent are responsible for ensuring local law compliance ensuring local law compliance

PracticalitiesPracticalitiesPracticalitiesPracticalities

A subsidiary is regarded as A subsidiary is regarded as indicative of a more substantial indicative of a more substantial presence and this will assist with:presence and this will assist with:

Getting a bank accountGetting a bank account

Obtaining a leaseObtaining a lease

Entering into commercial agreementsEntering into commercial agreements

PrivacyPrivacy Issues 1 Issues 1PrivacyPrivacy Issues 1 Issues 1

Data Protection Directive has been implemented Data Protection Directive has been implemented by all EU member statesby all EU member states

It introduced 8 fundamental principles dealing It introduced 8 fundamental principles dealing with how personal data is collected processed with how personal data is collected processed and transferred from one party to another and transferred from one party to another

It provides the individuals concerned certain It provides the individuals concerned certain rightsrights

Privacy Issues 2Privacy Issues 2Privacy Issues 2Privacy Issues 2 Restrictions on transfer of personal data outside the EEARestrictions on transfer of personal data outside the EEA

To comply with European legislation, if a US company To comply with European legislation, if a US company wishes to transfer personal data to the US from Europe it wishes to transfer personal data to the US from Europe it may only do so: may only do so:

If the data subjects have consented; orIf the data subjects have consented; or

If the company receiving the personal data is Safe If the company receiving the personal data is Safe Harbour Certified (approx 550 US companies are Harbour Certified (approx 550 US companies are certified); orcertified); or

If there is a contract in place that ensure that the If there is a contract in place that ensure that the company receiving the personal data has adequate company receiving the personal data has adequate protection in place. protection in place.

TAXTAXTAXTAX

No one tax law relevant across EuropeNo one tax law relevant across Europe

Relevant to both branches and subsidiaries. Relevant to both branches and subsidiaries. A business is subject to tax if it has a A business is subject to tax if it has a permanent establishment in that country permanent establishment in that country

The US and EU member states have entered The US and EU member states have entered into double taxation treaties to ensure that into double taxation treaties to ensure that companies are not taxed in full both in the companies are not taxed in full both in the US and the European countries in which US and the European countries in which they trade. they trade.

Corporation Tax IssuesCorporation Tax IssuesCorporation Tax IssuesCorporation Tax Issues

Branch Vs SubsidiaryBranch Vs Subsidiary

A subsidiary is charged on the world-wide profit of the A subsidiary is charged on the world-wide profit of the subsidiary companysubsidiary company

A branch is taxed only on those profits which arise in A branch is taxed only on those profits which arise in that country that country

Start up costs usually can be carried forward and set-Start up costs usually can be carried forward and set-off against future profits both with a branch and a off against future profits both with a branch and a subsidiary. Branches can benefit from double tax subsidiary. Branches can benefit from double tax relief by setting its loses against worldwide profits of relief by setting its loses against worldwide profits of the parentthe parent

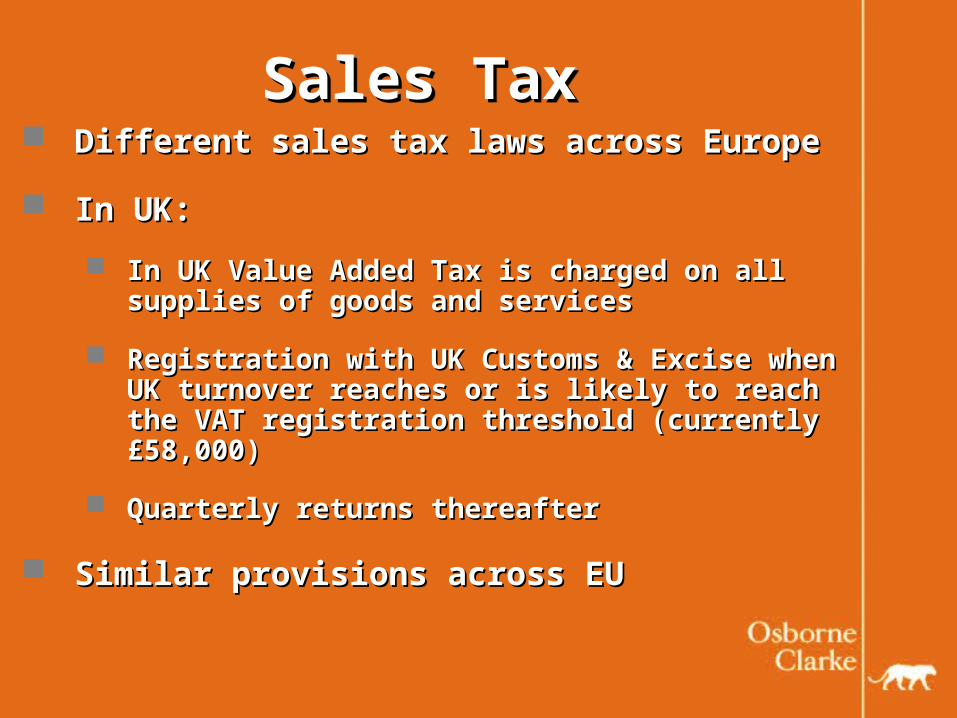

Sales TaxSales TaxSales TaxSales Tax Different sales tax laws across EuropeDifferent sales tax laws across Europe

In UK:In UK:

In UK Value Added Tax is charged on all In UK Value Added Tax is charged on all supplies of goods and servicessupplies of goods and services

Registration with UK Customs & Excise when Registration with UK Customs & Excise when UK turnover reaches or is likely to reach the UK turnover reaches or is likely to reach the VAT registration threshold (currently £58,000)VAT registration threshold (currently £58,000)

Quarterly returns thereafterQuarterly returns thereafter

Similar provisions across EUSimilar provisions across EU

Formalities: SubsidiaryFormalities: SubsidiaryFormalities: SubsidiaryFormalities: Subsidiary"Off the shelf" or form your own"Off the shelf" or form your own

Corporate name registrationCorporate name registration

Registered addressRegistered address

Share Capital requirements: In Denmark - Share Capital requirements: In Denmark - 125,000DKK, In France - €0 - €37,000 depending on 125,000DKK, In France - €0 - €37,000 depending on the type of company you incorporate, In UK - £1the type of company you incorporate, In UK - £1

How you do business and shareholders rights (UK How you do business and shareholders rights (UK - Memorandum and Articles of Association)- Memorandum and Articles of Association)

Appointment of directors and secretary Appointment of directors and secretary

Formalities: Branch Formalities: Branch Formalities: Branch Formalities: Branch

Statutory registration formsStatutory registration forms

Copy of parent company constitutional Copy of parent company constitutional documents, latest set of audited accountdocuments, latest set of audited accountss, , and other domestic filings, and other domestic filings, registration feeregistration fee

A separate branch registration is required A separate branch registration is required for each and every branch within a for each and every branch within a country that has a separate management country that has a separate management structure and separate reporting lines structure and separate reporting lines back to the US.back to the US.

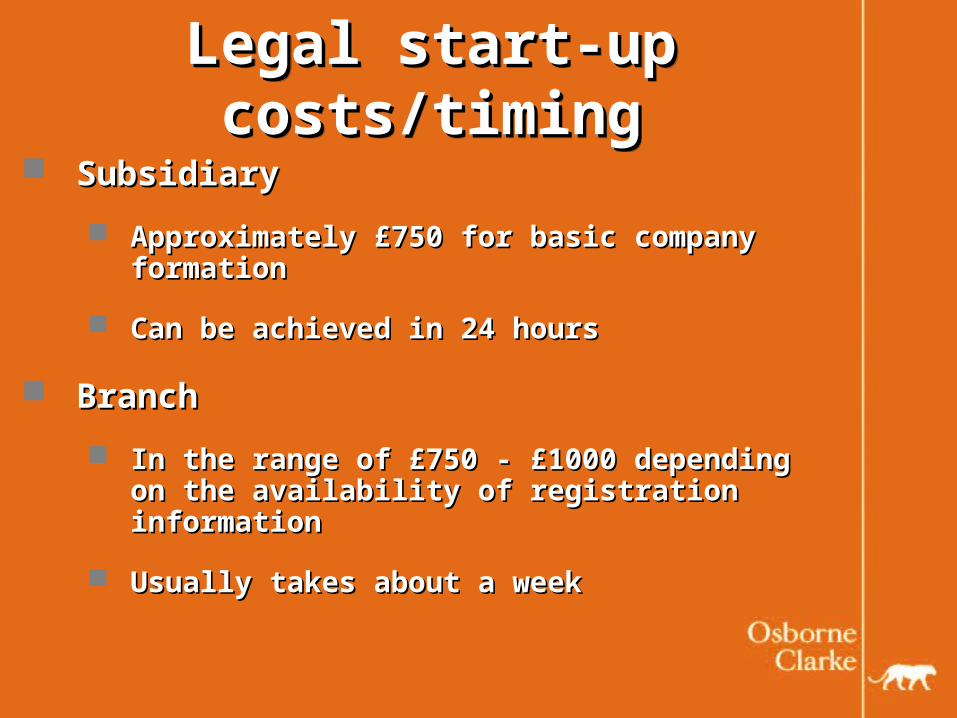

Legal start-up costs/timingLegal start-up costs/timingLegal start-up costs/timingLegal start-up costs/timing

SubsidiarySubsidiary

Approximately £750 for basic company Approximately £750 for basic company formationformation

Can be achieved in 24 hoursCan be achieved in 24 hours

BranchBranch

In the range of £750 - £1000 depending on the In the range of £750 - £1000 depending on the availability of registration informationavailability of registration information

Usually takes about a weekUsually takes about a week

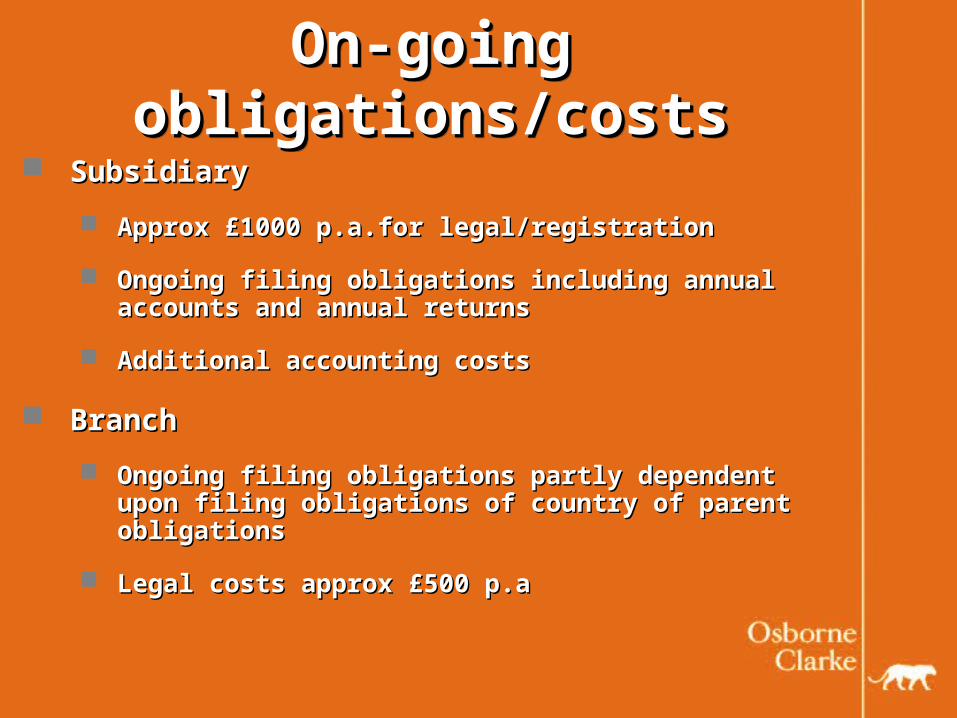

On-going obligations/costsOn-going obligations/costsOn-going obligations/costsOn-going obligations/costs SubsidiarySubsidiary

Approx £1000 p.a.for legal/registration Approx £1000 p.a.for legal/registration

Ongoing filing obligations including annual accounts Ongoing filing obligations including annual accounts and annual returnsand annual returns

Additional accounting costsAdditional accounting costs

BranchBranch

Ongoing filing obligations partly dependent upon Ongoing filing obligations partly dependent upon filing obligations of country of parent obligationsfiling obligations of country of parent obligations

Legal costs approx £500 p.aLegal costs approx £500 p.a

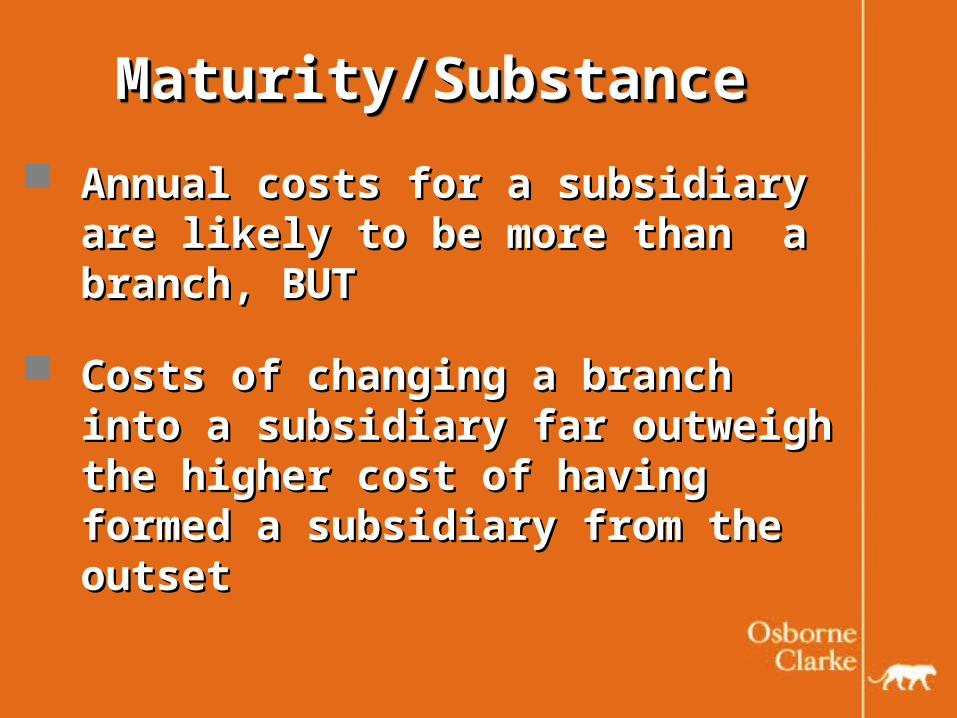

Maturity/SubstanceMaturity/SubstanceMaturity/SubstanceMaturity/Substance

Annual costs for a subsidiary are Annual costs for a subsidiary are likely to be more than a branch, BUTlikely to be more than a branch, BUT

Costs of changing a branch into a Costs of changing a branch into a subsidiary far outweigh the higher subsidiary far outweigh the higher cost of having formed a subsidiary cost of having formed a subsidiary from the outsetfrom the outset

Labor law issues 1Labor law issues 1Labor law issues 1Labor law issues 1

Work permits for non-European nationalsWork permits for non-European nationals

European labor laws are applicable to European labor laws are applicable to employees residing and working in the a employees residing and working in the a member state regardless of whether (1) member state regardless of whether (1) they are employees of a European they are employees of a European subsidiary or a branch of a US parent; or subsidiary or a branch of a US parent; or (2) (2) tthey are European nationals or non-hey are European nationals or non-European nationalsEuropean nationals

Beware: There are a host of consequencesBeware: There are a host of consequences

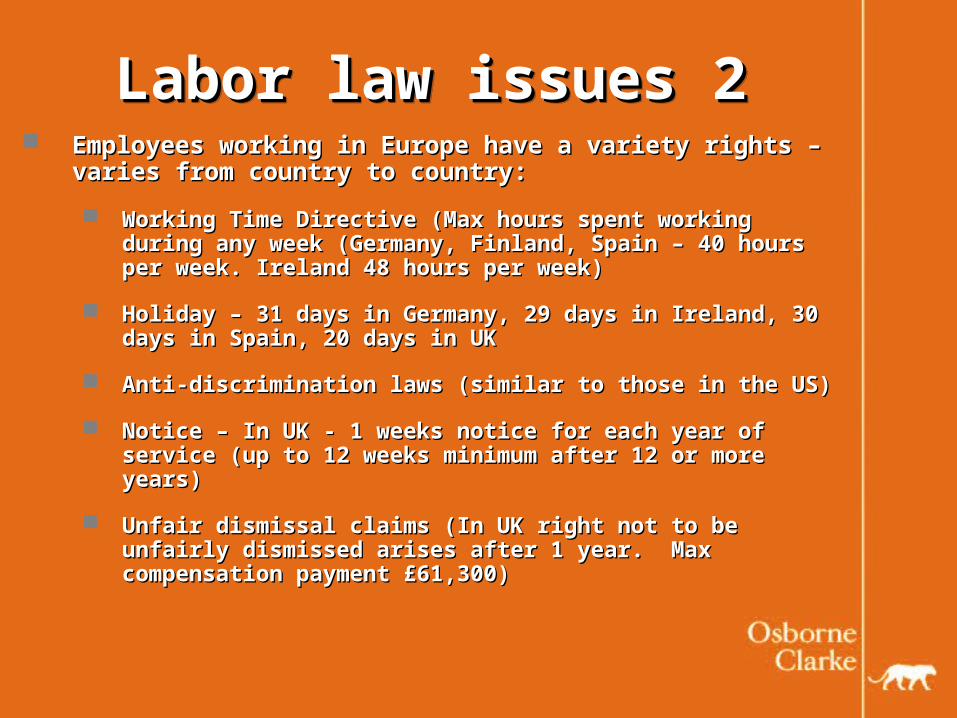

Labor law issues 2Labor law issues 2Labor law issues 2Labor law issues 2 Employees working in Europe have a variety rights – Employees working in Europe have a variety rights –

varies from country to country:varies from country to country:

Working Time Directive (Max hours spent working during Working Time Directive (Max hours spent working during any week (Germany, Finland, Spain – 40 hours per week. any week (Germany, Finland, Spain – 40 hours per week. Ireland 48 hours per week) Ireland 48 hours per week)

Holiday – 31 days in Germany, 29 days in Ireland, 30 days Holiday – 31 days in Germany, 29 days in Ireland, 30 days in Spain, 20 days in UKin Spain, 20 days in UK

Anti-discrimination laws (similar to those in the US)Anti-discrimination laws (similar to those in the US)

Notice – In UK - 1 weeks notice for each year of service (up Notice – In UK - 1 weeks notice for each year of service (up to 12 weeks minimum after 12 or more years)to 12 weeks minimum after 12 or more years)

Unfair dismissal claims (In UK right not to be unfairly Unfair dismissal claims (In UK right not to be unfairly dismissed arises after 1 year. Max compensation payment dismissed arises after 1 year. Max compensation payment £61,300)£61,300)

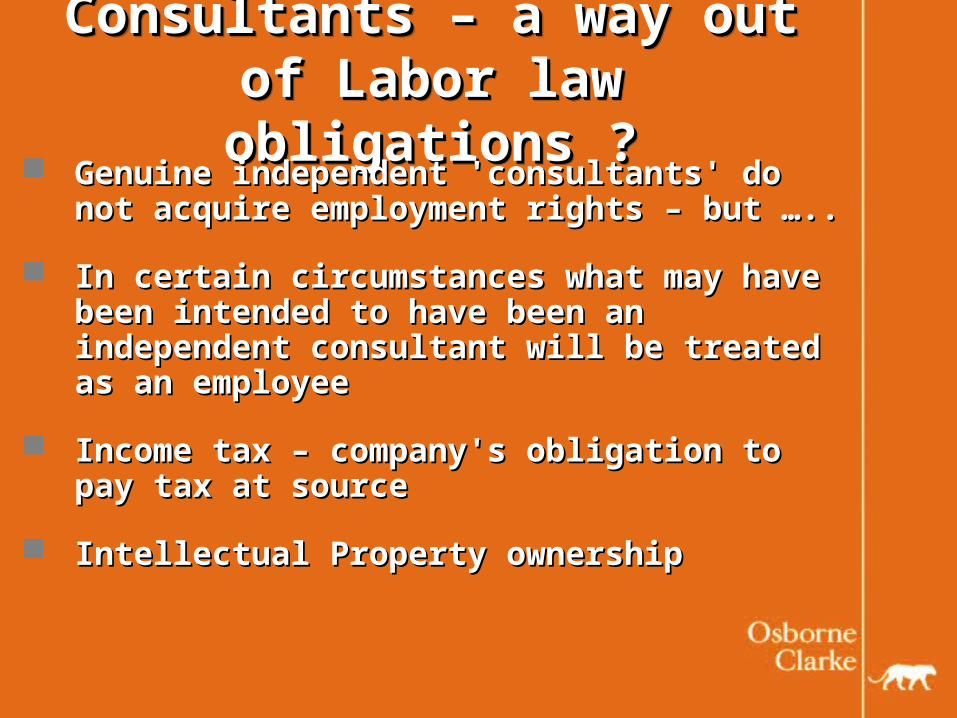

Consultants – a way out of Consultants – a way out of Labor law obligations ?Labor law obligations ?

Consultants – a way out of Consultants – a way out of Labor law obligations ?Labor law obligations ?

Genuine independent 'consultants' do not Genuine independent 'consultants' do not acquire employment rights – but …..acquire employment rights – but …..

In certain circumstances what may have In certain circumstances what may have been intended to have been an independent been intended to have been an independent consultant consultant will be treated as an employee will be treated as an employee

Income tax Income tax – company's obligation to pay – company's obligation to pay tax at sourcetax at source

Intellectual Property ownershipIntellectual Property ownership

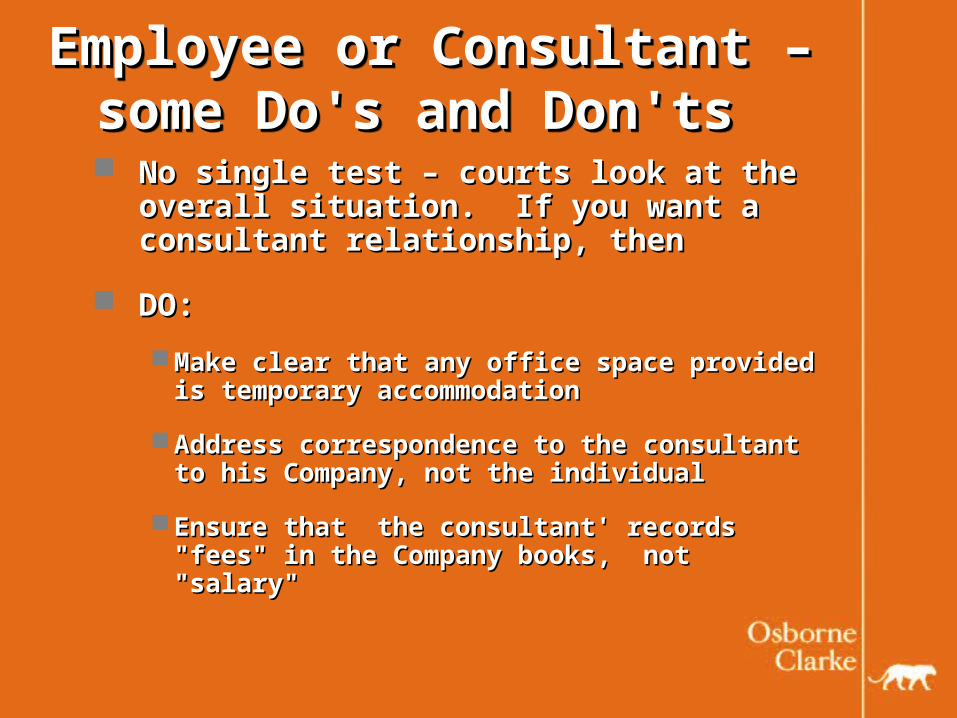

Employee or Employee or Consultant – some Consultant – some Do's and Don'ts Do's and Don'ts

Employee or Employee or Consultant – some Consultant – some Do's and Don'ts Do's and Don'ts

No single test – courts look at the overall No single test – courts look at the overall situation. If you want a consultant situation. If you want a consultant relationship, thenrelationship, then

DO:DO:

Make clear that Make clear that any office space provided any office space provided is is temporary accommodation temporary accommodation

Address Address correspondence to the correspondence to the consultantconsultant to his to his CompanyCompany, not the individual, not the individual

Ensure that the consultant' records "fees"Ensure that the consultant' records "fees" in the in the Company booksCompany books,, not not ""salarysalary""

Employee or Employee or Consultant – some Consultant – some Do's and Don'ts Do's and Don'ts

Employee or Employee or Consultant – some Consultant – some Do's and Don'ts Do's and Don'ts

DON'T:DON'T:

Allow paid holiday or paid Allow paid holiday or paid medical absencemedical absence

Include the consultant Include the consultant in any internal in any internal documentation such as a telephone listdocumentation such as a telephone lists s etcetc

Issue instructions regarding the work Issue instructions regarding the work undertaken by the Consultantundertaken by the Consultant

Prevent the Consultant from Prevent the Consultant from accepting accepting work from other sourceswork from other sources

More Questions ?More Questions ?More Questions ?More Questions ?

Andrew GowansAndrew [email protected]@osborneclarke.com(650) 462 4020(650) 462 4020

Rupert VernallsRupert [email protected]@osborneclarke.com(650) 462 4022(650) 462 4022

Related Documents