DOES A PORTFOLIO OF GROWTH STOCKS OUTPERFORM A PORTFOLIO OF VALUE STOCKS? Evidence from Sweden and Norway Lina Andersson, Daniella Holmgren Department of Business Administration Civilekonomprogrammet Degree Project, 30 Credits, Spring 2022 Supervisor: Siarhei Manzhynski

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DOES A PORTFOLIO OF

GROWTH STOCKS

OUTPERFORM A PORTFOLIO OF VALUE

STOCKS?

Evidence from Sweden and

Norway

Lina Andersson, Daniella Holmgren

Department of Business Administration

Civilekonomprogrammet

Degree Project, 30 Credits, Spring 2022

Supervisor: Siarhei Manzhynski

[This page was intentionally left blank]

Acknowledgement We would like to thank our supervisor Siarhei Manzhynski and all the participants at

the seminars for providing us with important feedback to improve our thesis. Also, we

would like to thank each other for the partnership and our different knowledge during

the work with the thesis, which made it possible to complete it.

Umeå, May 2022

Lina Andersson Daniella Holmgren

Abstract A high return is a driving factor for most investors. The ways to reach success are many

and different investment strategies on how to earn high returns have been discussed for

decades. Value stocks (low P/E ratios) and growth stocks (high P/E ratios) are two

strategies among the investment area with different and contrary results on which

strategy can give the highest possible return. However, studies of the P/E effect have

shown different results the last years compared to previous findings of a value premium

for low P/E stocks, with trends of a higher return for growth stocks compared to value

stocks. This led us to the research question “Does a portfolio of growth stocks present a

higher return than a portfolio with value stocks on the Swedish and Norwegian stock

markets?”.

The problem that the study aims to answer is therefore if a portfolio of growth stocks

provides a higher return than a portfolio of value stocks between the years 2001-2021.

The long timespan will give us the opportunity to evaluate the stock markets during

both booms and busts. Our study is made on historical data on the Swedish and the

Norwegian stock markets since we found a lack of previous research in these countries

within the research area. To fulfil the purpose of the study and to answer the research

question, a quantitative method is used with historical data provided from Eikon

(Thomson Reuters DataStream) where firms are sorted on the P/E ratios and after that

growth and value portfolios are created. We will present both the actual return as well

as a risk adjusted return for the stocks. The risk adjusted returns are conducted by using

the financial measurements Sharpe ratio and Jensen’s alpha.

The result of the study shows that on a 5 % significance level, growth stocks presented a

higher actual return than value stocks for both Sweden and Norway. The same evidence

was found for the returns for growth stocks compared to market index. Though, when

testing the risk adjusted returns, the null hypothesis could not be rejected, which implies

that a statistical difference between the portfolios could not be found.

Keywords: Growth stocks, value stocks, P/E ratio, Sharpe ratio, Jensen’s alpha,

behavioural finance, efficient market hypothesis, financial crises.

Table of Contents

1.Introduction .....................................................................................................................1

1.1 Problem background: .......................................................................................................... 1

1.2 Purpose: .............................................................................................................................. 3

1.3 Research gap and contribution ........................................................................................... 3

1.4 Delimitations ....................................................................................................................... 4

2. Theoretical method .........................................................................................................5

2.1 Research philosophies ......................................................................................................... 5

2.1.1 Epistemology ................................................................................................................ 6

2.1.2 Ontology ....................................................................................................................... 6

2.2 Research Approach ............................................................................................................. 7

2.3 Research Method ................................................................................................................ 7

2.4 Quality criteria ..................................................................................................................... 8

2.5 Time horizon ........................................................................................................................ 9

2.6 Social & Ethical Research .................................................................................................. 10

2.7 Literature and Data Sources .............................................................................................. 10

2.8 Source criticism ................................................................................................................. 11

2.9 Summary of the theoretical methodology ........................................................................ 12

3. Theoretical point of departure ....................................................................................... 13

3.1 Choice of topic ................................................................................................................... 13

3.2 Growth versus value stocks ............................................................................................... 13

3.3 Fama & French Factor Models .......................................................................................... 15

3.4 Efficient-market hypothesis .............................................................................................. 16

3.5 Random walk theory ......................................................................................................... 18

3.6 Behavioural finance ........................................................................................................... 19

3.7 Modern portfolio theory ................................................................................................... 20

3.8 Sharpe ratio ....................................................................................................................... 21

3.9 Jensen’s alpha ................................................................................................................... 21

3.10 The Magic Formula .......................................................................................................... 22

3.11 Additional research ......................................................................................................... 23

3.12 Summary of theoretical framework ................................................................................ 24

4. Practical method ............................................................................................................ 26

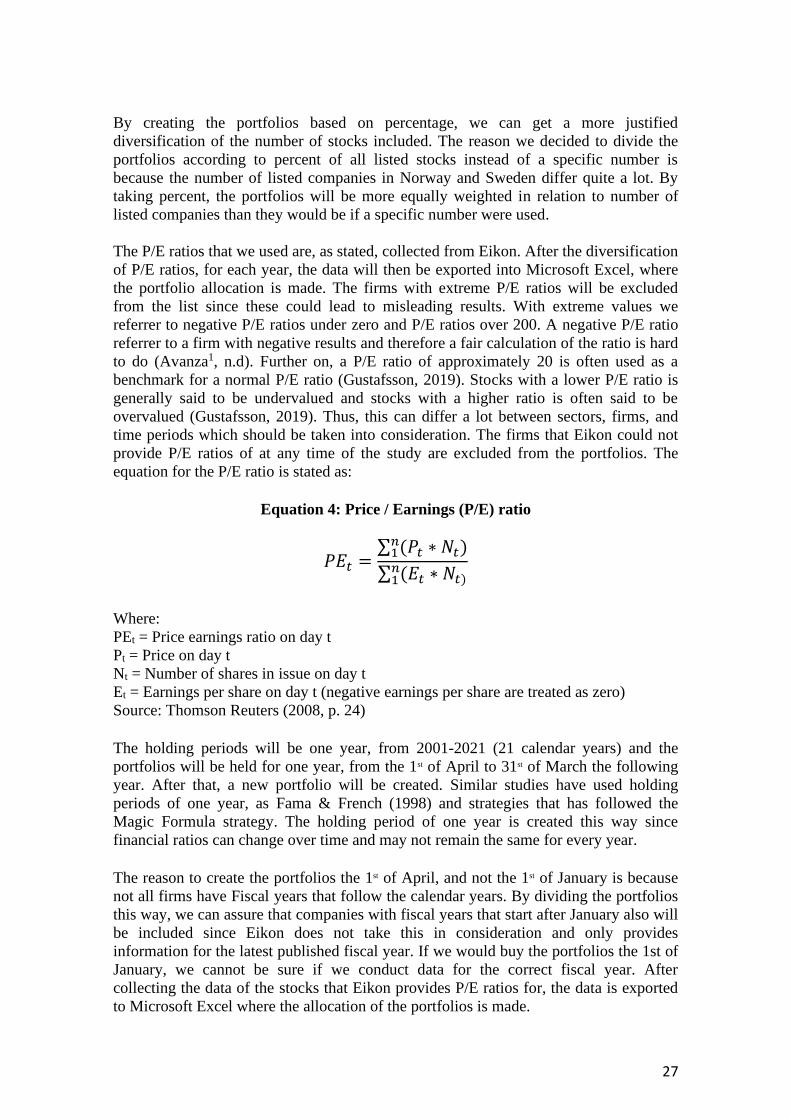

4.1 Data collection................................................................................................................... 26

4.1.1 Sample selection and Creation of portfolios .............................................................. 26

4.1.2 Sample size and the complete portfolios ................................................................... 28

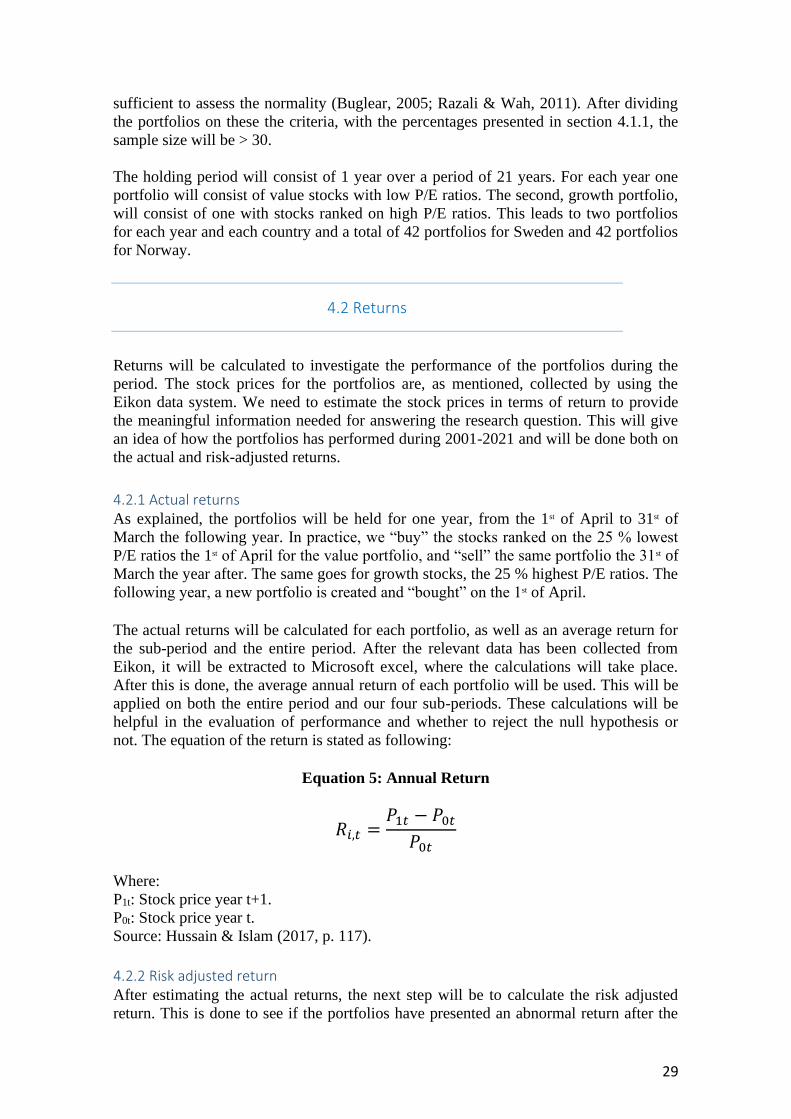

4.2 Returns .............................................................................................................................. 29

4.2.1 Actual returns ............................................................................................................. 29

4.2.2 Risk adjusted return ................................................................................................... 29

4.2.3 Risk-free rate .............................................................................................................. 30

4.2.4 Jensen’s alpha ............................................................................................................ 30

4.2.5 Market index returns ................................................................................................. 31

4.3 Hypothesis ......................................................................................................................... 31

4.4 Normality ........................................................................................................................... 33

4.5 Selection of significance test ............................................................................................. 33

4.5.1 Non-parametric tests ................................................................................................. 33

4.5.2 Parametric tests ......................................................................................................... 34

5. Empirical Findings .......................................................................................................... 35

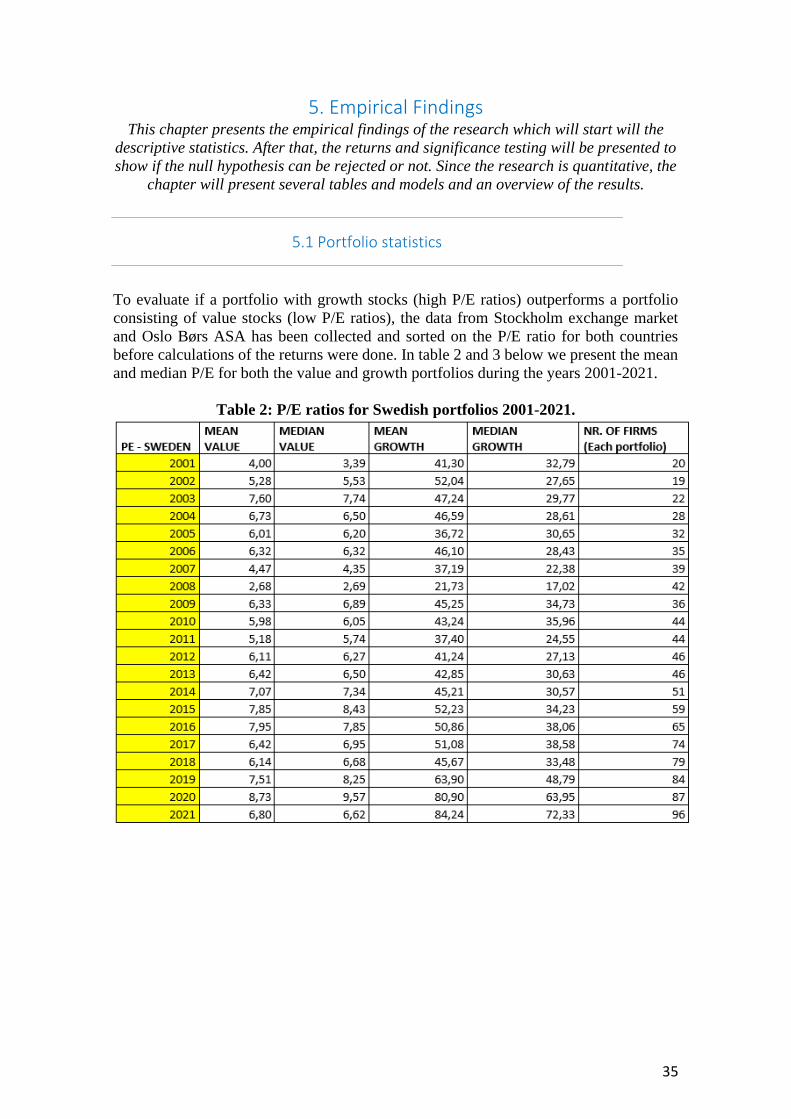

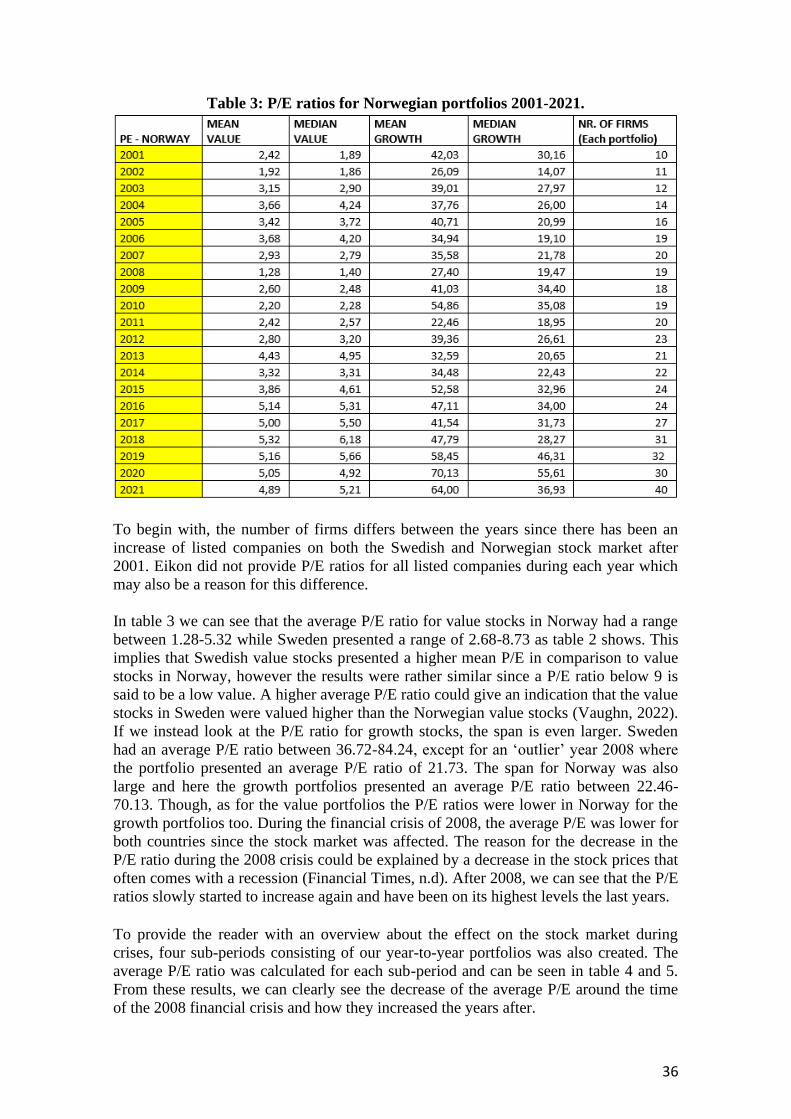

5.1 Portfolio statistics .............................................................................................................. 35

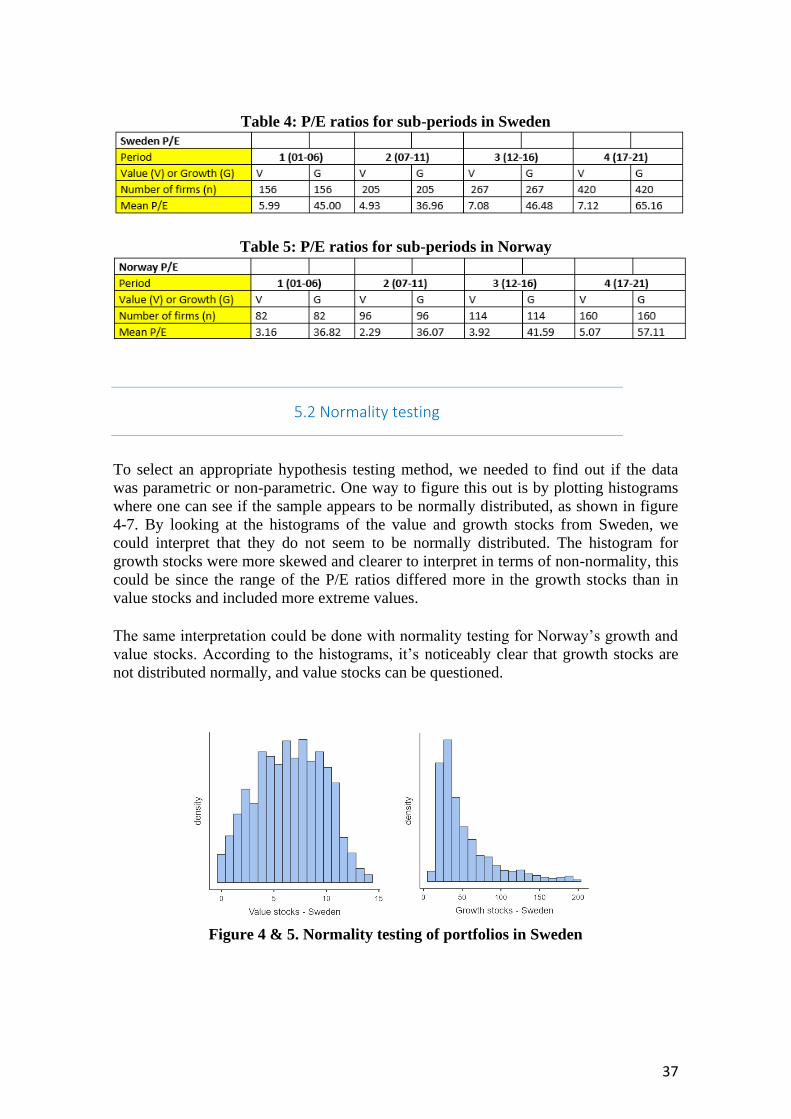

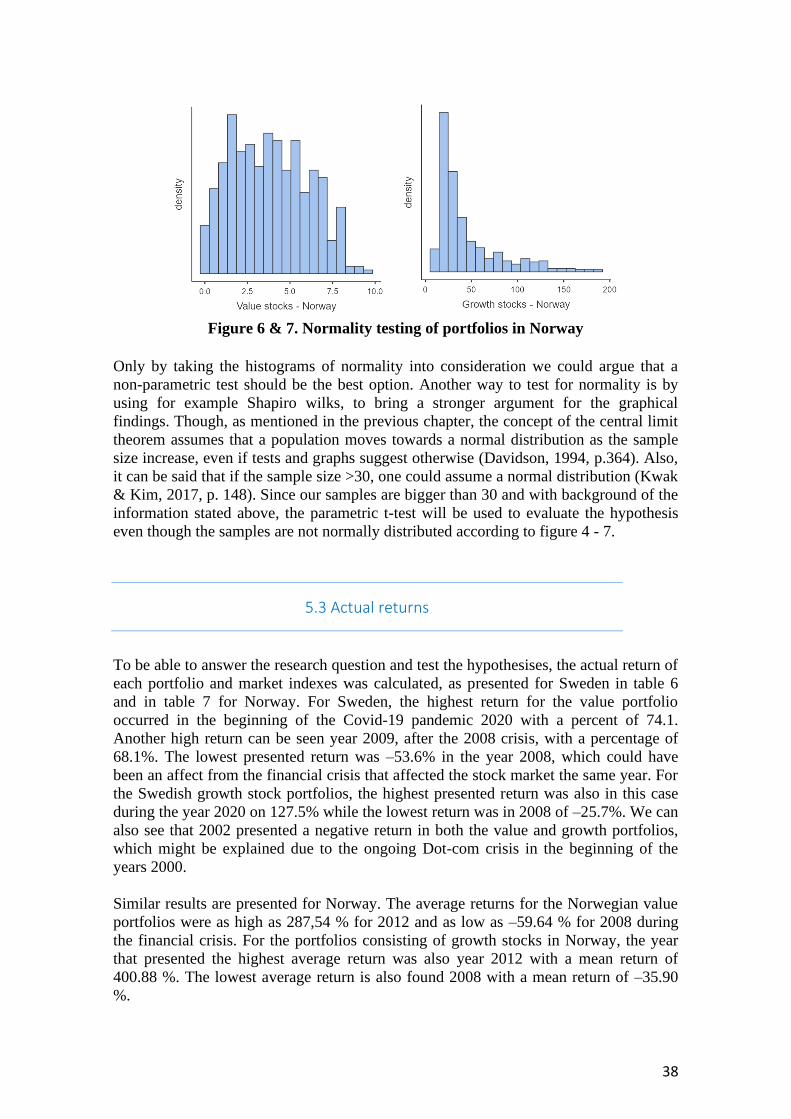

5.2 Normality testing ............................................................................................................... 37

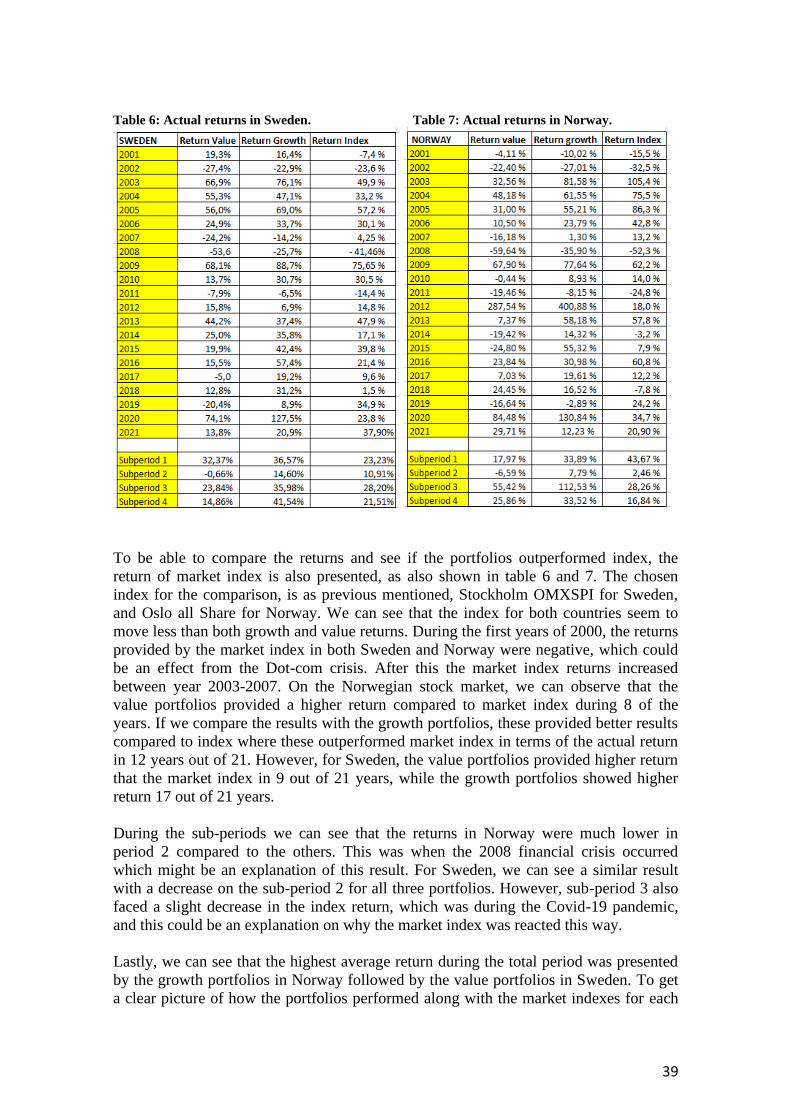

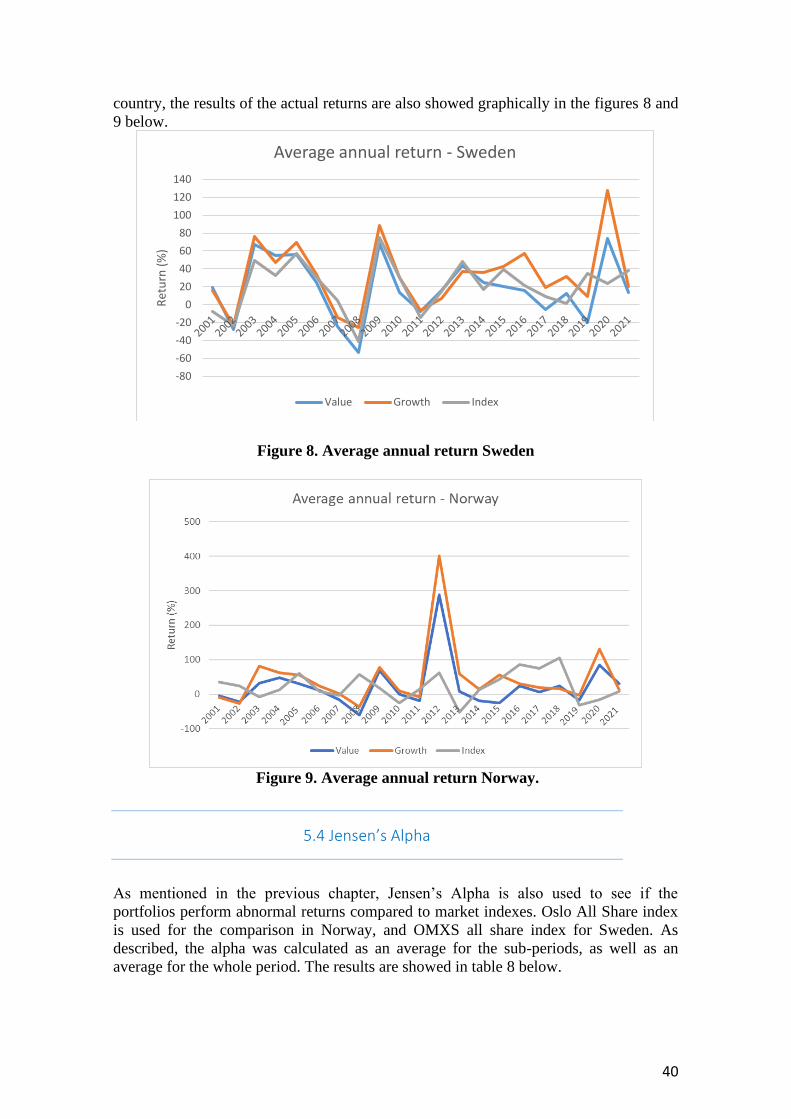

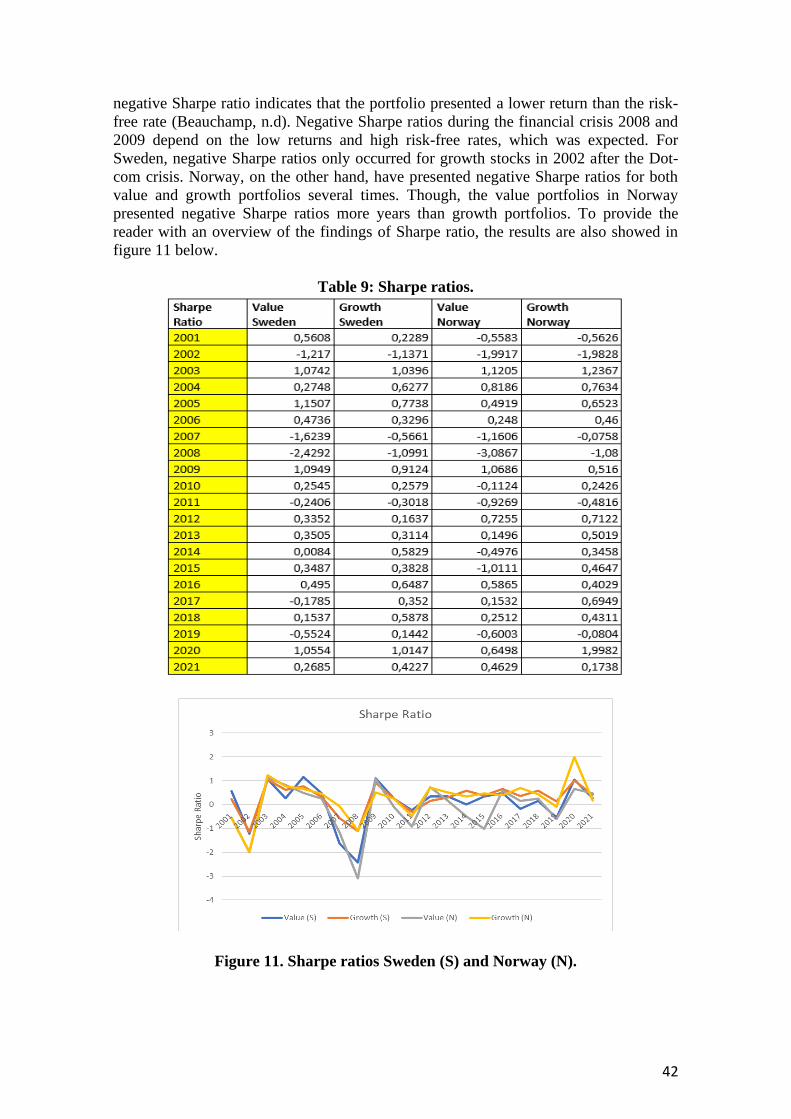

5.3 Actual returns .................................................................................................................... 38

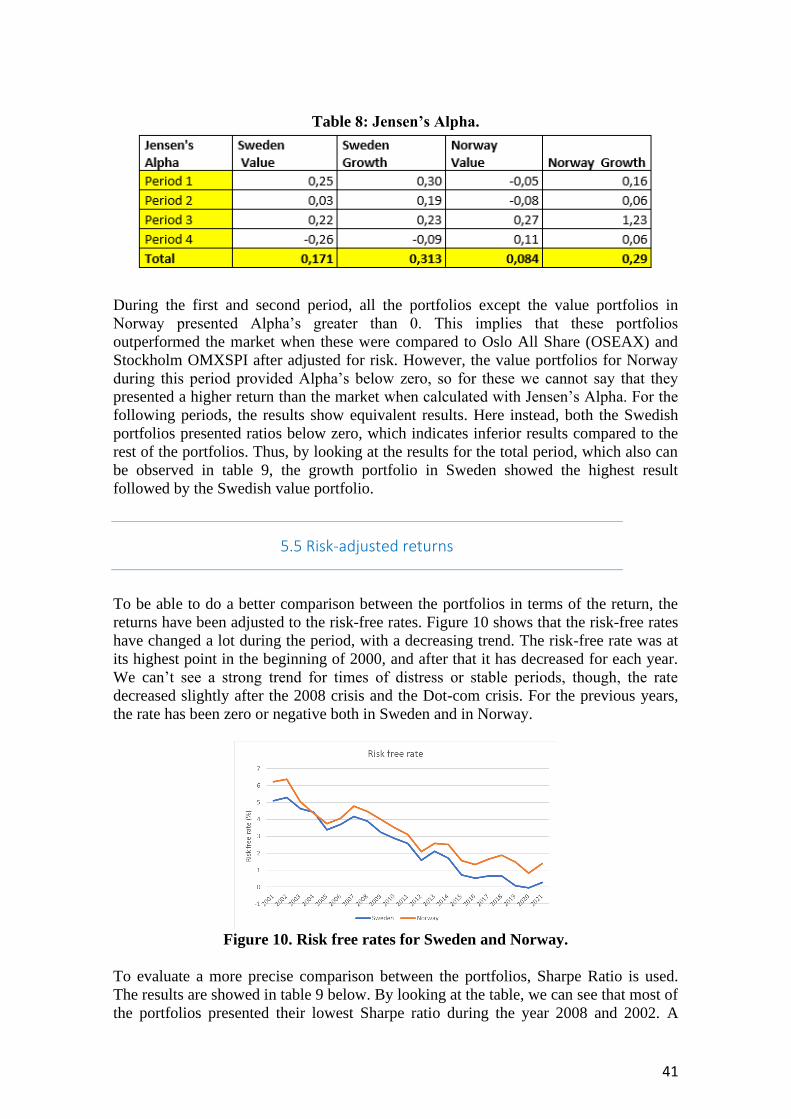

5.4 Jensen’s Alpha ................................................................................................................... 40

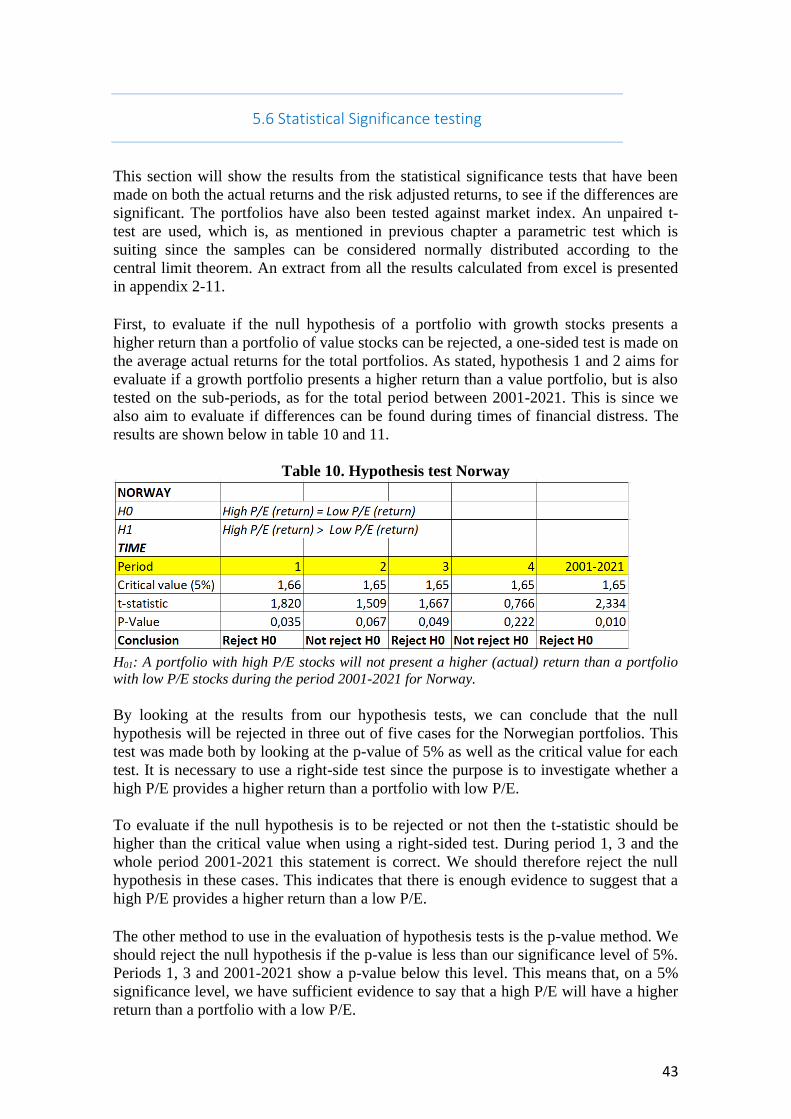

5.5 Risk-adjusted returns ........................................................................................................ 41

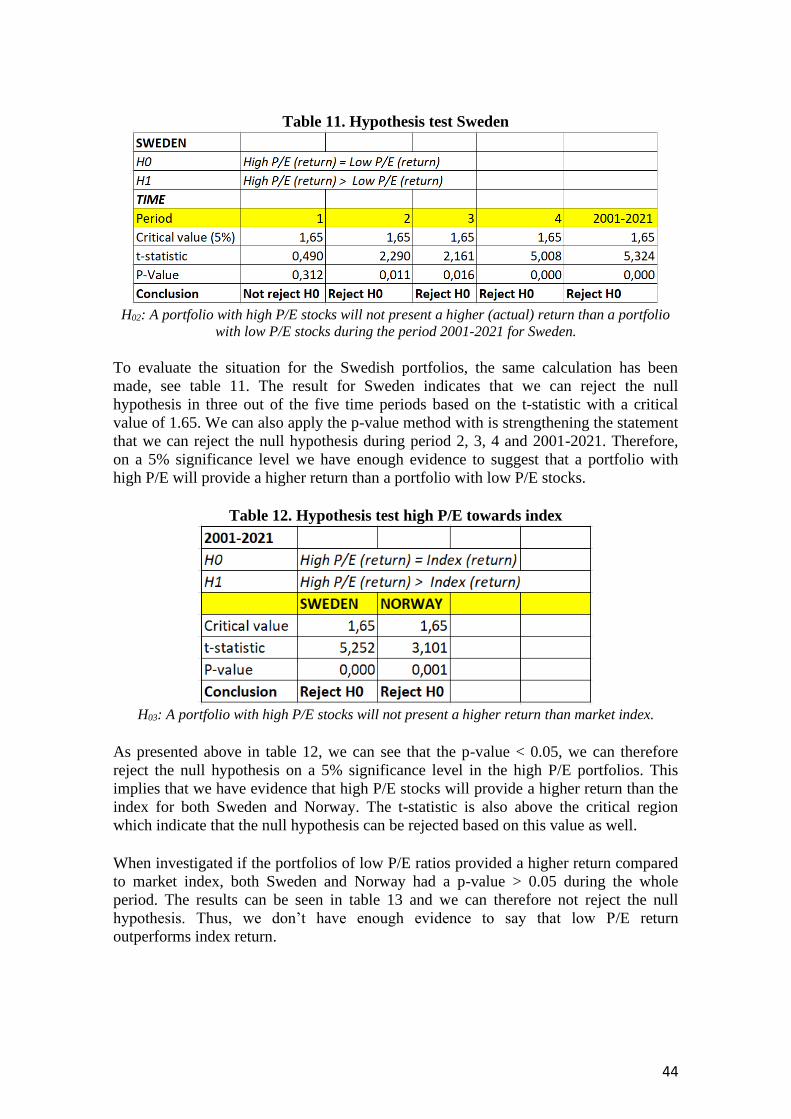

5.6 Statistical Significance testing ........................................................................................... 43

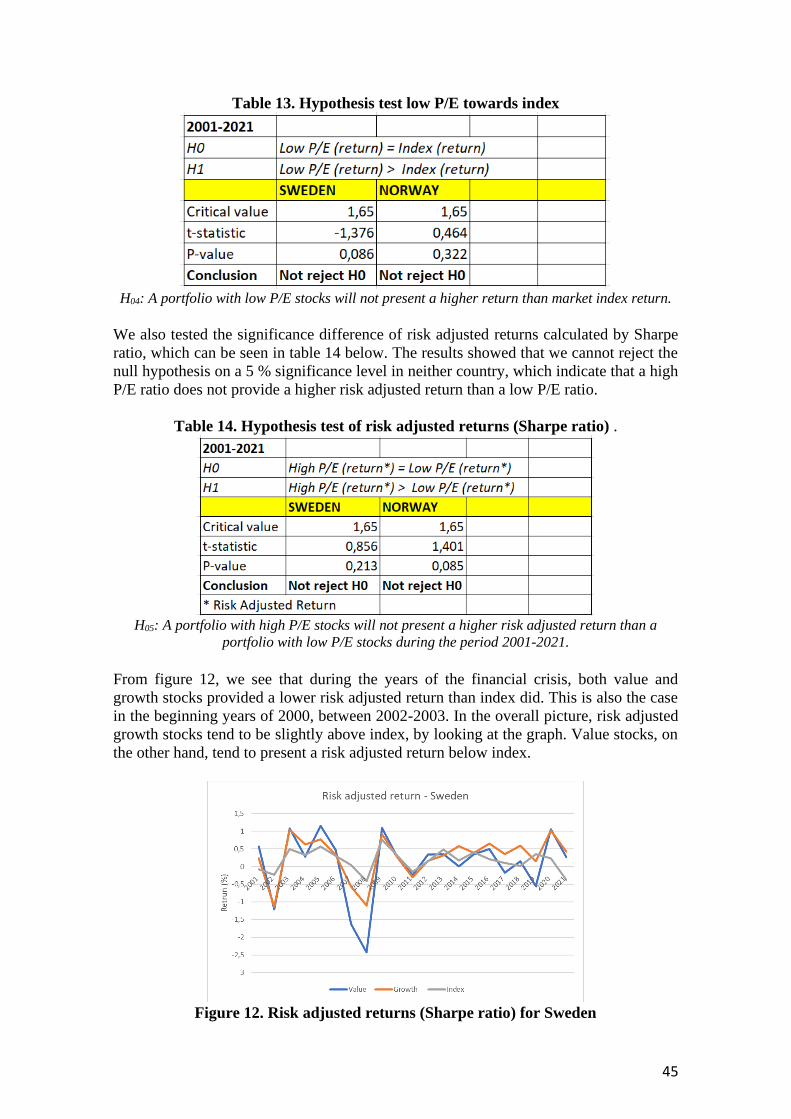

5.7 Summary of the hypothesis testing .................................................................................. 46

6. Analysis ......................................................................................................................... 47

6.1 Analysis of the results / hypothesis tests .......................................................................... 47

6.1.1 Hypothesis 1 ............................................................................................................... 47

6.1.2 Hypothesis 2 ............................................................................................................... 48

6.1.3 Hypothesis 3 ............................................................................................................... 49

6.1.4 Hypothesis 4 ............................................................................................................... 49

6.1.5 Hypothesis 5 ............................................................................................................... 50

6.2 The results compared to previous research ...................................................................... 50

6.3 The results compared to relevant theories ....................................................................... 51

7. Conclusion ..................................................................................................................... 53

7.1 General Conclusion ........................................................................................................... 53

7.2 Limitations ......................................................................................................................... 54

7.3 Contribution ...................................................................................................................... 54

7.3.1 Theoretical contribution ............................................................................................ 54

7.3.2 Practical contribution ................................................................................................. 55

7.4 Social and ethical aspects .................................................................................................. 55

7.5 Quality Criteria .................................................................................................................. 56

7.5.1 Reliability .................................................................................................................... 56

7.5.2 Validity ........................................................................................................................ 57

7.6 Suggestion for future research .......................................................................................... 58

Reference list .................................................................................................................... 60

Appendix 1: Risk free rate Sweden and Norway……………………………………………………………………66 Appendix 2: T-test Norway period 1………………………………………………………………….....................66 Appendix 3: T-test Norway period 2……………………………………………………………………………………. 67 Appendix 4: T-test Norway period 3…………………………………………………………………………………….67 Appendix 5: T-test Norway period 4…………………………………………………………………………………….67 Appendix 6: T-test Norway total period……………………………………………………………………………….68 Appendix 7: T-test Sweden period 1……………………………………………………………………………………68 Appendix 8: T-test Sweden period 2……………………………………………………………………………………68 Appendix 9: T-test Sweden period 3…………………………………………………………………………………….69 Appendix 10: T-test Sweden period 4…………………………………………………………………………………..69 Appendix 11: T-test Sweden total period………………………………………………………………………………69

List of figures Figure 1: The ‘research onion’……..……………………………………………………………...…………………….....5 Figure 2: The process of a deductive approach………………………………………..………………….……..…7 Figure 3: Diversification of portfolios based on P/E ratio……………………………………..…………….. 26 Figure 4: Normality testing of portfolios in Sweden…………………………………………….……………….37 Figure 5: Normality testing of portfolios in Sweden………………………………………..…….……………..37 Figure 6: Normality testing of portfolios in Norway…………………………………….…………..…………..38 Figure 7: Normality testing of portfolios in Norway……………………………………..……….……………..38 Figure 8: Average annual return Sweden………………………………………………………………..…………….40 Figure 9: Average annual return Norway……………………………………………………….……….…………….40 Figure 10: Risk free rates for Sweden and Norway……………………………………….……..……………….41 Figure 11: Sharpe ratios Sweden (S) and Norway (N)…………………………………………...………………42 Figure 12: Risk adjusted returns (Sharpe ratio) for Sweden………………………………….………………45 Figure 13: Risk adjusted returns (Sharpe ratio) for Norway…………………………………..……………..46

List of tables Table 1: Summary of the theoretical methodology…………………………………………….……………..…12 Table 2: P/E ratios for Swedish portfolios 2001-2021……………………………………………………………35 Table 3: P/E ratios for Norwegian portfolios 2001-2021…………………………….…………………………36 Table 4: P/E ratios for sub-periods in Sweden………………………………………………………………………37 Table 5: P/E ratios for sub-periods in Norway……………………………………………………………..……….37 Table 6: Actual returns in Sweden…………..................................................................................39 Table 7: Actual returns in Norway………………………………………………………………………………………..39 Table 8: Jensen’s Alpha………………………………………………………………………………………….……………..41 Table 9: Sharpe ratios……………………………………………………………………..…………………………………….42 Table 10: Hypothesis test Norway…………………………………………………………………….…………………..43 Table 11: Hypothesis test Sweden…………………………………………………………………..………………..….44 Table 12: Hypothesis test high P/E towards index……………………………………….……………………….44 Table 13: Hypothesis test low P/E towards index………………………………………..……………………….45 Table 14: Hypothesis test of risk adjusted returns (Sharpe ratio)……………..……………………..….45 Table 15: Summary of the hypotheses tests………………………………………………………………….…..…46

1

1.Introduction This chapter will contain a presentation of the research topic by introducing the

problem background and purpose in relation to the research question. At the end, the

research gap and delimitations for the thesis will be discussed to give the reader a

better overview of what to expect from the study.

1.1 Problem background:

Profit and the return on investment is a driving factor for the most investors who seek to

maximize these in their portfolios by the choice of investments they decide to include.

Though, the range of investors is huge; some do it in their spare time as a hobby while

others ‘put their whole life’ into the market. Even if all individuals have different

preferences when creating their portfolios, these preferences often include the amount

of risk an investor is willing to take and what kind of securities to invest in.

Value and growth stocks are one way to classify stocks and can be used to base the

investment strategies on. There are many ratios that are used for determining these

different stocks, but a common one is the P/E ratio and the P/E effect. In fact, the

discussion of the P/E effect is found as far back as from findings of Basu (1977) and has

after that been widely discussed. The P/E effect is connected to stocks with low P/E

ratios which are usually associated with value stocks. These stocks usually pay

dividends, are trading under their true value, and the return is expected to come when

the stock catches up to the fundamental value (Hayes, 2022). Contrary to value stocks,

there is growth stocks which can be described as stocks in a company that the market

expects to outperform the average growth for the market (Hayes, 2022). Further, growth

stocks are trading at high P/E ratios which often make them look expensive, but if the

expectations are correct, it will be followed by an increasing share price. On the other

hand, if the expected and the realized growth do not continue, the stock price can

instead decline and therefore growth stocks can be considered as a risky investment

(Hayes, 2022).

Selecting between value and growth stocks is interesting, though hard, with the return as

the driving factor among investors, since previous research shows both contrary and

different results. Fama & French (1998) found that value stocks before 1998 performed

better with higher returns than growth stocks. An explanation to that were according to

the authors a correction after an undervaluation of the value stocks, while the growth

stocks were overvalued. Gregory et al. (2003) also found that value stocks outperformed

growth stocks, here on the US market during 1980 to 1998. The same results were

presented for the Australian market which showed that value stocks had a higher return

than growth stocks (Gharghoria et al., 2013).

Though, more recent studies have showed contrary results. Lev & Srivastava (2019)

found evidence that shows an outperformance of growth stocks compared to value

stocks on the US market. The authors even argue that value investing has not been as

successful as earlier among the 10-12 past years. Brindelid & Nilsson (2021) did similar

2

studies, but for the Nordic countries instead and found evidence for value investing

again. They tested The Magic formula, which is a strategy that aims for buying cheap

stocks in terms of a high earnings yield (equivalent to a low P/E-ratio) and a high ROC.

The study showed that portfolios that were created with the Magic Formula beat the

indexes in both Sweden and Norway during the time period 2012-2021, even if Norway

showed a greater return than the rest of the Nordic countries compared to index.

One cause of the more recent findings of lower success for value stocks could be a

result of the low rates the world has faced the last years. As Bratt (2021) explains it, the

expected future returns are higher when the rates are low since future cash flows are

predicted to be high. This can result in higher stock prices for growth stocks since these

often are highly valued with expectations of high future earnings and cash flows (Bratt,

2021). Contrary, when the rates are high, the expected returns and cash flows get lower

since a future discounted cash flow is not worth that much with high rates (Bratt, 2021),

which can result in lower stock prices for growth stocks.

Since the last years have been characterized by low and even negative rates and recent

studies have showed more favourable results for growth stocks, the angle of this thesis

will be to evaluate if growth stocks provide higher returns than value stocks. Research

among the P/E effect and growth versus value stocks have been implied on the US

market and over all on the European market. However, Oslo Børs ASA and Nasdaq

Stockholm have not been the focus in previous research, neither a comparison between

the countries has been found. The fact that previous studies show both contrary and

different results make further research interesting and shows the difficulty of predict the

return of portfolios consisting of growth and value stocks, based on the P/E ratio. Also,

as the countries are similar in size and are close geographically, but the economic and

the leading sectors of the stock markets in the countries differ from each other is an

interesting background for the comparison. Norway is one of the largest economies in

the world with a high export sector consisting of oil and gas, followed by the fishing-

sector (Globalis1, 2021). This of course affects the stock market and for example, the

Norwegian stock market is unique because of the index Oslobørs Seafood Index

(OBSFX) which is an index consisting of stocks of only seafood and particular salmon

(Henriksen, 2016). Sweden on the other hand is one of the most industrialised countries

in Scandinavia with engineering, mine and steel as the main sectors (Globalis2, 2021),

and the stock market of Sweden can also be said to be unique in terms of the high

numbers of small-cap lists and firms, especially growth and innovation firms

(Jinderman, n.d). According to Holliday (2018) is the ratio of market investors and

average interest in the stock market also higher in Sweden compared to Norway, which

can be explained by the larger proportion of microcap operations in Sweden versus

Norway. Also, the small size of various small-scale operations can make it difficult for

fund managers and investors to take significant positions.

Based on the background, the following research question is constructed:

“Does a portfolio of growth stocks present a higher return than a portfolio with value

stocks on the Swedish and Norwegian stock markets?”

3

1.2 Purpose:

The purpose of this study is to evaluate the investing strategies among value and growth

stocks. As stated, the study will examine if a portfolio of growth stocks (high P/E ratio)

produces a higher return than a portfolio of value stocks (low P/E ratios) which will be

done by using historical data from the Norwegian and Swedish stock exchange markets.

The portfolios will also be compared to market indexes to evaluate how these have

presented against index as well, to be able to compare the strategies to previous research

and theories.

The data for this study will be conducted from Oslo Børs ASA and Nasdaq Stockholm

during the period 2001-2021. Since this period both will cover both the Dot-com crisis,

financial crisis 2008-2009 and the Covid-19 pandemic one part of the purpose is also to

evaluate how growth and value portfolios perform during times of financial distress

which will be possible due to the long period of data. Thus, the financial crises will also

be compared to more stable financial periods to evaluate if differences among the

strategies can be found.

1.3 Research gap and contribution

As mentioned in the background, previous research has been conducted on this topic

and the performance of value and growth stocks are well discussed. Though, the results

from previous studies show different and contrary results, which is one argument for

further research among this area. Fama & French (1998); Gregory et al., (2003) among

others found that value stocks outperformed growth stocks in terms of return. Van Dinh

(2021) did not find the same results and stated that a higher return of value portfolios

could not be seen compared to portfolios of growth stocks. Previous research on the

Swedish and Norwegian stock markets among value and growth stocks exists but is not

as expanded as for the rest of the European countries and the US market, neither for our

chosen time period. This research gap became the first inspiration of investigating

Sweden and Norway, as well as the lack of comparisons between the two countries.

Concerning financial crises, which earlier only have been touched upon, will also be

contributively to investigate further. Both Sweden and Norway have their own currency

which is interesting to consider since they might not be as effected as, for example

Finland, when shifts or events happen that affect the euro. According to Holliday (2018)

both Norway and Sweden were able to avoid the worst Eurozone crisis of 2008, since

both countries have their own currency and low debt, compared to much of the Western

countries. Another similarity of the countries is the higher return compared to the

benchmark for real return. The European benchmark for real return, including the Credit

Suisse World index, were 5% between 1965-2015 but both Sweden and Norway were

ahead of this level on 8.7% and 6.3% respectively (Holliday, 2018). Because of this, we

felt it would be interesting to highlight the effect of value and growth stocks during this

period and investigate these countries. Also, by expanding the time span, both the Dot-

com crisis, 2008 financial crisis and the Covid-19 pandemic can be included, to see if

4

any differences can be determined and to develop the contribution about investing in

different economic times.

This study is primary aimed for investors in Sweden and Norway and can work as a

guideline for the choice between value and growth stocks when deciding an investment

strategy. The contribution will also hopefully be to evaluate if there is a difference

between investing in the different countries over various time periods, different

economic cycles and crises.

1.4 Delimitations

The study will be limited to stocks on the following exchange markets: NASDAQ

Stockholm and Oslo Børs ASA. Since the study will be conducted on the Swedish and

Norwegian stock exchange the result may therefore be irrelevant for other countries due

to business and investing differences. Only public listed companies are going to be

tested and private companies will therefore be excluded. Concerning the P/E ratios that

are used to allocate the portfolios, firms that do not have P/E ratios provided by Eikon

will be excluded in this research.

This study will also be conducted within the timeframe 2001-2021 which means that

data before and after this period will be excluded. Previous research shows that a too

long period of data can lead to that some effects might be ignored, therefore we will

also use the following sub-periods to increase the probability to be sure that we will find

and cover the effects of the different specific periods.

5

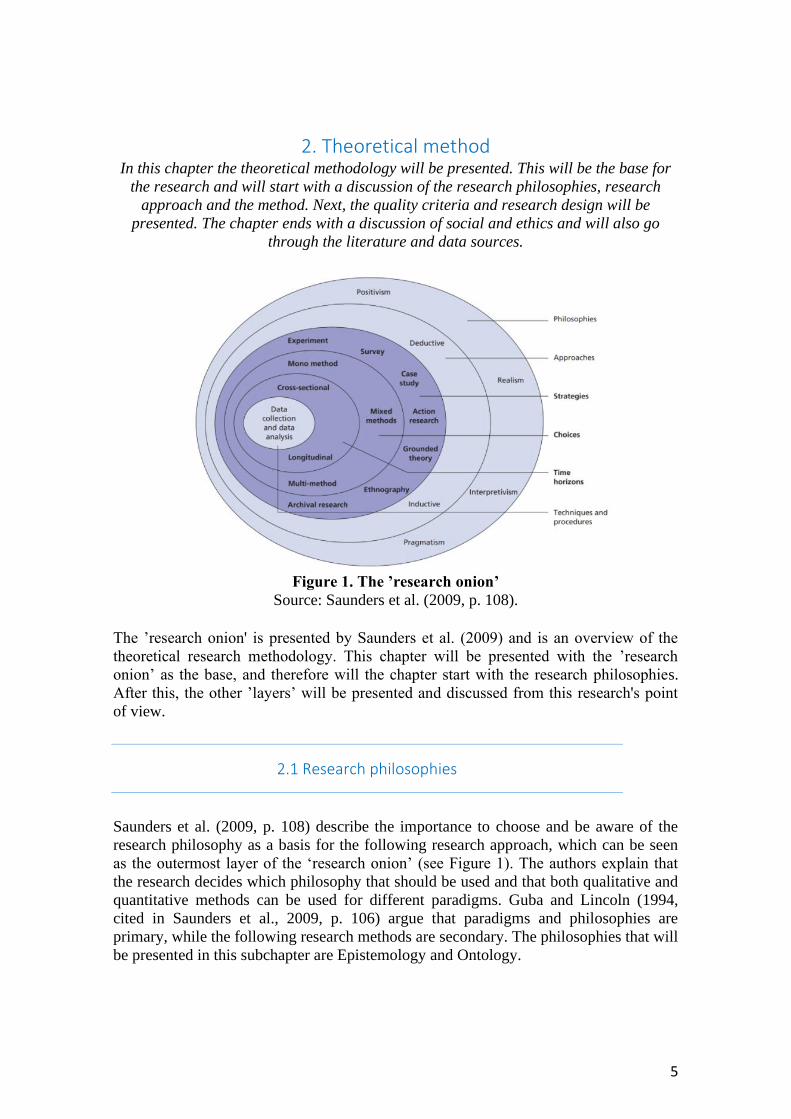

2. Theoretical method In this chapter the theoretical methodology will be presented. This will be the base for

the research and will start with a discussion of the research philosophies, research

approach and the method. Next, the quality criteria and research design will be

presented. The chapter ends with a discussion of social and ethics and will also go

through the literature and data sources.

Figure 1. The ’research onion’

Source: Saunders et al. (2009, p. 108).

The ’research onion' is presented by Saunders et al. (2009) and is an overview of the

theoretical research methodology. This chapter will be presented with the ’research

onion’ as the base, and therefore will the chapter start with the research philosophies.

After this, the other ’layers’ will be presented and discussed from this research's point

of view.

2.1 Research philosophies

Saunders et al. (2009, p. 108) describe the importance to choose and be aware of the

research philosophy as a basis for the following research approach, which can be seen

as the outermost layer of the ‘research onion’ (see Figure 1). The authors explain that

the research decides which philosophy that should be used and that both qualitative and

quantitative methods can be used for different paradigms. Guba and Lincoln (1994,

cited in Saunders et al., 2009, p. 106) argue that paradigms and philosophies are

primary, while the following research methods are secondary. The philosophies that will

be presented in this subchapter are Epistemology and Ontology.

6

2.1.1 Epistemology Epistemology is described as one way to think about the different research philosophies

with the issue of whether knowledge should be accepted or not, and if the social world

should be studied the same way as the natural sciences (Bryman & Bell, 2011, p. 15).

Further on, the authors explain that epistemology can be divided into positivism and

interpretivism. If you follow a positivistic philosophy you work like a natural scientist

and will not present data if it doesn’t come from phenomena's that has been observed

(Saunders et al., 2009, p. 113). Positivism is connected to a deductive research approach

through its state that theory is used to generate hypothesis to be answered (Bryman &

Bell, 2011, p. 15). Thus, for this study a positivism point of view will be the approach

among epistemologies. This is since secondary historical data will be used and will be

presented only if it has been observed. As the data is published we can state that it is

observed and according to positivism it implies that the data can be presented.

The other perspective of epistemology, interpretivism, has a believe that humans and

institutions are separated from natural sciences (Bryman & Bell, 2011, p. 16). This

philosophy believes that physical sciences are not enough to explain the social world of

business (Bryman & Bell, 2011, p. 16). With an interpretivist view, as Saunder et al.

(2009, p. 116) explain, it is important to see people as different when conducting

information of human behaviour. As stated, our study will collect data from NASDAQ

Stockholm and Oslo Børs ASA the study will not adopt an interpretivist view, so the

epistemological point of view must be positivism since it states that only phenomena's

that has been observed can provide trustworthy data (Saunders et al., 2009, p. 119). For

a positivistic point of view, a quantitative data collection with big samples of data often

is used, with an independent approach from the researcher, which goes in line with the

purpose of this research.

2.1.2 Ontology Ontology seeks for explaining the social entities and the nature of reality (Saunders et

al., 2009, p. 110) and is another way to see the different philosophies. The main

question within ontology is if social units should be described as an objective

phenomenon to the actors in it or if the entities are a result of actions of the humans in it

(Bryman & Bell, 2011, p. 20). Objectivism and constructionism are two different

contrary approaches within the ontology consideration (Bryman & Bell, 2011, p. 20).

Objectivism states that social entities and phenomena are independent of social actors in

the social world (Bryman & Bell, 2011, p. 21), which implies that the social

phenomena’s people use every day, are separated from actors. Constructionism, or

subjectivism, on the other hand, has the opposite view of the social reality according to

the authors. With a constructionism view, the perceptions and actions of social actors

are the background to the social phenomena’s (Saunders et al., 2009, p. 111). It can

therefore be said that it’s the social actors in a social entity that shape it, not the

opposite, and the organisation is a product of social actors. Among ontology, this study

will therefore have an objectivistic point of view since the data that will be collected

from a stock exchange site where the data are not affected by the social actors.

Therefore, the data is separated and not subjective since the data should appear whether

there were social actors behind it or not.

7

2.2 Research Approach

The aim of this research is to evaluate if growth stocks outperform value stocks in the

Nordic countries by creating hypotheses and test them, which will be done by testing

theories on the markets of each countries. Therefore, our purpose is not to create new

theories, rather testing existing ones, which is best described by a deductive approach.

According to Bryman & Bell (2011, p. 27) the deductive approach can be connected to

a quantitative study which will be the case for our thesis, which strengthen the choice of

this approach. The deductive approach is presented in figure 2 below, with the steps that

this study will follow. Inductive on the other hand is stated as the relation between

theory and research but the emphasis is on the generation of theories (Bryman & Bell,

2011, p. 27). Therefore, using an inductive approach, you will start with the collection

of data and develop the theoretical point of view after the data collection (Saunders et

al., 2009, p. 124). As Bryman & Bell (2011, p. 27) describe it, an inductive approach

also fits more well with a qualitative study, which is another argument that it is

irrelevant for this study.

Figure 2. The process of a deductive approach

Source: Bryman & Bell, 2011 p. 11.

2.3 Research Method

As Bryman & Bell (2011, p. 26) explain it, there are two different research methods

when conducting a research, quantitative and qualitative method. A quantitative

approach can often be seen as more objective since the researchers distant themselves

from the subject or participants that are being studied (Bryman & Bell, 2011, p. 410).

As this study will be conducted through numerical data from an already existing source

8

the statement of a quantitative method will hold, and the objectivity will not be

compromised. Another argument for this type of study would be that it aims to test

theories in order to evaluate whether to reject or not reject a null hypothesis. The

qualitative approach focuses the data collection on words and the researcher tend to

seek involvement with the participants for a higher understanding (Bryman & Bell,

2011, p. 410). With all this information in mind we can reinforce our choice to conduct

a quantitative study over a qualitative, since the data collection will not have a focus of

subjective interpretations, nor that the study will have participants that improve the

understanding.

Even if there are many differences, we should also present some of the similarities

between the methods since these are also worth to bear in mind. One similarity is that

both methods are concerned with reduction of data, which is done for the purpose to

make sense of the data and be able to draw conclusions (Bryman & Bell, 2011, p. 412).

Further on, the authors explain that quantitative methods often use a statistical analysis

for this while qualitative develop concepts out of their data. Answering research

questions is another similarity, even if the method to do this is different; they both are

fundamentally concerned with answering questions regarding the nature of social reality

(Bryman & Bell, 2011, p. 412). However, it is the quantitative approach that this study

will follow.

2.4 Quality criteria

To determine and to evaluate research there are according to Bryman & Bell (2011, p.

41) three criteria: reliability, validity and replication. The criteria reliability shows

whether the result of a research is possible to repeat (Bryman & Bell, 2011, p. 41). If

that is the case, a variety of studies should present the same results. Further on, there are

three questions that can be used to measure the reliability “Will the measures yield the

same results on other occasions?”, “Will similar observations be reached by other

observers?” and “Is there transparency in how sense was made from the raw data?”

(Easterby-Smith et al. 2008:109, referred in Saunders et al., 2009, p. 156). Beyond these

questions, Bryman & Bell (2011, p. 157-158) highlight three criteria to evaluate if a

measure is reliable: stability, inter-observer consistency and internal reliability. Stability

shows if the measure is stable enough, or not stable, to promise that a result will be

stable over time. Inter-observer consistency concerns the possibility that the research

has subject impact of the study which can affect the choices. Internal reliability

measures if the factors that affects the indexes or scales of the research is consistent and

if the answers have coherence to give an overall score. These criterions among

reliability are important to consider for us in this thesis and will further be discussed in

the conclusions. Since using secondary data from Eikon, it is important for us during the

study to be transparent about how the data are collected and to be consistent about the

returns, indexes and ratios to be able to make the study reliable, and repeatable.

Validity can be described as a criterion that measures the relevance of the results of the

study, “whether the findings are really about what they appear to be about” (Saunders et

al., 2009, p. 157). One thing often referred to external validity is generalizability which

implies that the study needs to be able to be applied to other studies or for example

9

other organisations, even if it is different from the organisation in the chosen study

(Saunders et al., 2009, p. 158). As for reliability, validity will also be considered in this

study. When drawing conclusions and analysing the results, we will have in mind to

make sure that the results measure exactly what they should measure to assure that the

study is valid. As Bryman & Bell (2011, p. 159) states, there are several different ways

to measure validity and that there are different types of validity. Measurement validity

is most common for quantitative studies and measure in general if the measure of the

study or concept measure exactly what is supposed to measure (Bryman & Bell, 2011,

p. 42), which is very appropriate for this quantitative study and as stated above

especially important to have in mind. To reach this, we will maintain a critical point of

view to reduce the risk of drawing wrong conclusions when later analysing the results.

Further on there is internal validity which measure the causality of the measurements

(Bryman & Bell, 2011, p. 42). The authors explain the problem of causality as if there

are other thing that causes the relationship between, for example the parameters, X and

Y, and if we can be sure that the chosen variable is the only thing that affects the

relationship. External validity is also related to the issue of whether the conclusions of

the study can be applied to other studies (Bryman & Bell, 2011. p. 43), which is similar

to the problems that have been discussed above.

Since reliability and replication almost describe the same thing (Bryman & Bell, 2011,

p. 41), we will consider reliability and validity in this thesis, as reliability is even more

common than replication.

2.5 Time horizon

There are different research designs to consider when conducting research. Bryman &

Bell (2011, p. 45) uses five different types when they discuss these which include

experimental design, cross-sectional design, longitudinal design, the case study design

and the comparative design. Among the research designs there are also, according to

Saunders et al. (2009, p. 155), time horizons to consider when conducting a study. From

the five different designs mentioned above, the study should apply either a cross-

sectional or a longitudinal time horizon. The main difference between these is the length

of the time horizon: a cross-sectional is often used for qualitative studies when

conducting information over a short period of time while longitudinal studies is used

when you want to study change of a period (Saunders et al., 2009, p. 155). Further on,

the authors describe the main question of a longitudinal design as “Has there been any

change over a period of time?”. Since this study will compare different stocks over

different periods of times, the longitudinal design is applied to be able to answer the

research question. As stated, a cross-sectional is more often used in qualitative studies

and as this study aims to evaluate the historical data during 2021-2021 this time horizon

would not be possible to conduct.

10

2.6 Social & Ethical Research

Saunders et al. (2009, p.183-184) refers to ethic, in a research context, as how to behave

in an appropriate way in relation to the rights of the participants that will become a

subject of your work. This is related to how we clarify and formulate the research

design, topic, data collection and analysis of data and should therefore be both morally

and methodologically defensible (Saunders et al., 2009, p.183-184). To give some

examples of what can be included in research ethics, the importance of privacy and

consent of participants as well as anonymity can be highlighted, as well the data

collected which should maintain confidential. The researchers should also act

objectively and with a good behaviour (Saunders et al., 2009, p.185-186). Since our

data will be collected by using secondary data and not involve people, these problems

should not be a big issue for this study, thus it is important to have knowledge about

them. Though, it is important since it is, except for anonymity and confidentiality, about

how the data collection and analysis of the data is done. Even if we will not face a big

problem in terms of anonymity, as we might if a qualitative method would been used, it

is important that these steps are done with good morals and that we act objective during

the conduction of the study.

Bradford & Cullen (2011) present in their book that even if many ethics considerations

are connected to research involving human participants, there are those that needs to be

taken into consideration with secondary data as well. Secondary data includes

information collected by someone else and it is therefore important that the information

gathered there was collected ethically (Bradford & Cullen, 2011, p. 156-157). Another

thing to keep in mind when using secondary data is to clarify the purpose of the

information collected, due to the importance of using the data for the research purpose

and not mislead it from the original reason (Bryman & Bell, 2011, p. 139). By taking

this into consideration, we tend to provide the readers with a clear and visible data

collection method to do the research as ethically as possible.

2.7 Literature and Data Sources

According to Saunders et al. (2009, p. 69) the literature sources can be divided into

three categories which include primary, secondary and tertiary sources. The authors

mention that sources frequently intersect with one another and exemplify the fact that

books can contain indexes to primary literature. Primary literature can be referred to as

“grey literature” since it can be more difficult to trace because they are sources of the

first occurrence of a work (Saunders et al., 2009, p. 69). Some examples of primary

sources can include reports, government publications, letters etc. Secondary literature,

on the other hand, is the later publication of primary sources, for example reports and

books (Saunders et al., 2009, p. 69) Compared to primary literature, secondary is easier

to trace, and the publications target a broader audience. Lastly, the authors describe

tertiary literature as the source developed to help in the location of primary and

secondary sources, often referred to as “search tools”. Abstracts and dictionaries are

some examples of tertiary literature (Saunders et al., 2009, p. 69).

11

Secondary literature sources such as academic journals, books, and data from databases

are used in this thesis. The main parts of the sources used, are collected from Google

Scholar and Umeå University Library. We will also use the database Eikon, provided by

the University, to gather the necessary numerical data, and Microsoft Excel to analyse

it. Since secondary literature will cover the main part of the data collection in this study, it

is important to highlight and evaluate the pros and cons of this type of source. Bryman

& Bell (2011) present some of the advantages and limitation for this method. First, it is

cost effective and time saving to use due to the easy access to good-quality data

(Bryman & Bell, 2011, p. 313). Although, by using already existing data, these can be

more complex to understand since the researcher lack familiarity with the structure and

contour of the data. Thus, since it is time saving, this provides the researcher with more

time to analyse and understand the data (Bryman & Bell, 2011, p. 320). Another

limitation worth mentioning is the difficulty to control the quality of the data collected.

However, by using peer-viewed sources, which can be considered as reliable, this

disadvantage could be minimized to avoid biases or mistakes (Bryman and Bell, 2011,

p. 321).

2.8 Source criticism

According to Bertilsson (2021, p. 2) it is of great importance to be critical towards the

gathering of information from different sources and data to avoid spreading wrongful

information. Bertilsson (2021, p. 2) explains that there are four main criteria of source

criticism: authenticity, time, dependency and tendency. By evaluating these criteria, we

can determine the trustworthy and credibility of the information. Further on, the author

refers authenticity to the importance of validating who the authors of the information

might be or where the original source comes from. To fulfil this criterion it is important,

during the work with this research, to locate the primary sources. If that’s not possible at

some time, it is then important to refer to the original source and validate the second

source. This goes hand in hand with dependency, which describes the connection

between different sources and whether one source relies on or repeats another source

(Bertilsson, 2021, p. 2). If there might be potential bias from the author’s side, this is

the criteria of tendency. This includes that the authors need to inspect the information

before including the data, to see if there could be personal, political or economic biases

from the source, which also is of great importance to consider along the work with this

research to fulfil that the sources remain objective. The last criteria to consider is time,

information or sources that are closer in time are often, but not necessary, more

trustworthy (Bertilsson, 2021, p.2).

12

2.9 Summary of the theoretical methodology

Table 1: Summary of the theoretical methodology Epistemological position Positivism

Ontological position Objectivism

Research approach Deductive

Research method Quantitative

Research design Longitudinal design

To give an overview of the theoretical methodology used in this study, this chapter will

end with a summary, table 1. Concerning the research philosophies, a positivistic point

of view will present the epistemological position since only empirical results will be

accepted. An objectivistic position for the ontological position equals the fact that

human factors will not impact the results since it will have a view of reality which is

external from the human factors within it. Further on, a deductive approach will be used

since hypothesis will be designed from previous theories, and not the contrary. The

research method is quantitative as the empirical that will be used is secondary data.

Lastly, a longitudinal design is used for the time horizon.

13

3. Theoretical point of departure This chapter will discuss and explain the different theories that are connected to the

research question. It starts with a presentation of the choice of topic, then previous

research that is relevant for growth and value stocks are presented. Further on,

different financial models and theories will be presented.

3.1 Choice of topic

Both authors of this thesis are finishing their last semester of Master of Science in

Business and Economics. The choice of finance, and more exactly investments as the

main subject for the thesis came both from out personal interests in investing in the

stock market and because of the academic background of studies in business and

finance. At first, our thought was to conduct the research on the Swedish stock market,

since the Swedish stock market felt extra interesting as we both have invested in

different types of securities, stocks and funds on the Swedish stock market. However,

the more we read about the subject, we found already relevant research on the stock

market in Sweden, even if it was not as extensive as for the rest of Europe and US. We

then found that there was a research gap among the other Nordic countries and that

developed the idea to do a comparison between Sweden and Norway among value and

growth stocks. The fact that periods of financial distress only have been touched upon,

led us to the focus of financial crisis and to develop that area among value and growth

stocks. Lastly, to bring a wider knowledge about investment strategies in times of

financial distress.

The academic background within business, economics and master courses in finance

gave us a background and knowledge we needed to write this thesis since we are

already familiar with some of the theoretical parts, models and ratios. We are though

aware that the pre-knowledge can have an impact on the work, which we will take into

consideration and have in mind through the thesis to remain objective.

3.2 Growth versus value stocks

Since the study aims to investigate if a portfolio of growth stocks provides a higher

return than value stocks, the theoretical framework will start with an introduction of

growth and value stocks and how to distinguish these. Discussing differences between

value and growth stocks are important to provide the reader with basic knowledge

before several models and previous research among the topic will be presented.

As already stated, the price-to-earnings (P/E) ratio will be used to determine whether a

stock is defined as a value or a growth stock. As the name of the ratio implies, it is a

multiple that compares the share price with the earnings. More exactly, it equals the

price of the share divided by the earnings per share and tells us how much an investor of

the stock needs to pay for the earnings the company generates. It is also generally said

14

that the P/E ratio shows the markets expectations of future earnings. A high (low) P/E

ratio is because of that a sign that the market predicts that the earnings will be higher

(lower) in the future (Penman, 2010, p 49). Though, according to previous studies it can

be difficult to use ratios to categorize a stock into growth or value stocks. Schiessl

(2014) is one of the researchers who exemplify the difficulty of classification. The fact

that the ratios can change over time is one example given (Schiessl, 2014, p. 6). Another

difficulty is that both growth and value managers sometimes invest in the same

company (I.e., with the same ratio) even if they have different perceptions about it.

However, the P/E ratio will still be the categorization tool that will be used to

distinguish between value and growth stocks since it is one of the most common due to

previous studies (Basu, 1977; Schiessl, 2014).

Schiessl (2014, p. 4) described growth stocks as stocks that has an expectation of

making high earnings in the future with a growth rate higher than the average market,

which is synonymous with the explanation of a high P/E ratio. It can be explained that

the investors who invests in growth stocks has a belief that the company will

outperform the market both in the future and in the long run (Schiessl, 2014, p. 4-5).

Investors are therefore willing to pay more for a growth stock compared to value stocks.

The expectations about future earnings and growth are then high which indicate that if

these are correct, investing in a growth stock will be a good choice with increasing

stock prices as a result. Opposite, there is a risk in investing in growth stocks with a

declining stock price if the expectations are not fulfilled (Schiessl, 2014, p 5). Value

stocks, on the other hand, are often described as a firm with a past performance of not

providing as good results as growth stocks. Value stocks are often predicted to perform

below average (Schiessl, 2014). These, in contrast to growth stocks, often provide low

ratios such as P/E and high dividend yields (Schiessl, 2014, p. 1).

Chan & Chen (1991, cited in Jensen et al., 1997) stated that value stocks also can be

risky in terms of small firms and low ratios since there is a possibility that the firm

would not survive in periods of decline compared to bigger firms with high ratios. This

can have impacts on how the stocks perform during a financial crisis. Also, as Schiessl

(2014, p. 5) states, there is a risk that value stocks are traded under its true value

because of poor management. However, as mentioned in the first chapter, the

performance of value and growth stocks can among other things, depend on how high

the repo rate is. With a rising repo rate, the value stocks often present a higher return

since the performance of growth stocks are dependent of predicted future cash flows

and expected returns (Bratt, 2021). Further on, Bratt (2021) explains the expected cash

flows and returns are harder to predict when the rate is higher and this can be a cause of

low returns for growth stocks during times with high rates, since the growth stocks are

depending on future expected returns and cash flows. Thus, value stocks often present a

higher return during times of low rates. The Swedish Central Bank has provided

negative repo rates for most of the years the last decade, and 1.5 % at most (Sveriges

Riksbank, n.d.). Thus, the last decade has consisted of historical low rates, compared to

the 2000’s. In the previous decade (2000-2010) the rate was between 0.25 % and 4.5 %

on a quarterly basis (Sverige Riksbank, 2022). The same pattern is shown for the rate in

Norway, even if it has not been negative. During 2000-2010 the Norwegian policy rate

were between 1.25 and 7.00 % (Norges bank, n.d.) and after 2010 between 0.00 % and

2.5 %.

15

Besides the discussion of P/E ratio above, there is a concept that one can connect to this

measurement which is called P/E effect. We want to mention this since it is a concept

within finance that can provide an idea on how the P/E ratio can be used and the

outcome from its result. The P/E effect has been investigated in several studies. Basu

(1977) is one of the first findings of the research among the P/E ratio and he wanted to

investigate if there was empirical evidence that stocks are related to the P/E ratios. He

found, after dividing portfolios into percentiles based on the P/E ratios, that low P/E

ratios presented a higher return than these with high P/E ratios. These results go against

the Efficient market hypothesis and a semi strong form of market efficiency. However,

after Basu (1977) conducted his study there have been many researchers investigating

value and growth stocks and the P/E ratio with contrary results, which will be further

discussed in coming sub-chapters.

3.3 Fama & French Factor Models

To explain the fact that distressed (value) firms historically outperformed overvalued

(growth) firms, even if the growth firms have higher earnings, Fama & French (1993)

developed a three-factor model. Even though this model does not take the P/E ratio in

consideration, it is interesting to bring up since it gives a background for the discussion

of value and growth stocks. It also gives a background for the previous success for

value stocks and the P/E effect since more recent studies has showed contrary results.

Another reason of the relevance for Fama & French in connection to our study is since

it is a contrary model to what we are trying to investigate. Fama & French is based on

the statement that value tends to outperform growth companies and it will be interesting

to test if our result will go against this or not. By that we mean if growth stocks can

outperform value stocks. However, our intention will not be to investigate how our

result will present in comparison to the Fama & French model, rather provide an

alternative insight beyond the methods and financial measurement this study will focus

on.

The factors in the Fama & French model are size, excess return on the market and

value, which is specified as book-to-market values. According to Fama & French (1998,

p 1975) a capital asset pricing model were not enough to explain the value premium for

value stocks, and therefore they added size and value to their model. Fama & French

(1998, p. 1975) explains that value stocks outperformed growth stocks with an average

of 7.68 percent a year, in terms of firms with low versus high price to book ratios over

the years 1975-1995, and therefore they added size and value to their model.

Over the years it has been a discussion about whether this model is explained by market

efficiency or market inefficiency (Hayes, 2021). If the factor-model is explained by

market efficiency the higher return of the value stocks depends on the higher risk that

value stocks bring due to their bigger business risk and the higher cost of capital. The

supporters of market inefficiency instead hold on to the fact that the higher return is a

result of incorrectly pricing the value companies, which in turn leads to a greater return

among the way that the value adjusts (Hayes, 2021).

16

Equation 1: Fama & French 3-factor model

Rit – Rft = αit + β1(Rmt – Rft) + β2SMBt + β3HMLt + εit

Where:

Rit = Total return of a stock or portfolio i at time t

Rft = Risk-free rate of return at time t

Rmt = Total market portfolio return

Rit – Rft = Expected excess return

Rmt – Rft = Excess return on the market portfolio (Index)

SMBt = Size premium (small minus big)

HMLt = Value premium (high minus low)

Β1,2,3 = Factor coefficients

Source: Schiessl (2014, p. 18).

3.4 Efficient-market hypothesis

Whether the Fama & French findings of a higher return of a value firms can be

explained by market efficiency or market inefficiency, the Efficient Market Hypothesis

is one of the most well-studied financial theories and will therefore be discussed in this

paragraph. Bodie et al. (2014, p. 351) defines the concept of efficient market hypothesis (EMH) by

the belief that stocks reflect all information available. For example, the authors explain

that the announcement of a takeover would cause the stock prices to jump as soon as the

information becomes public. Thus, after the announcement date, there would be no

further flow in the prices, which means that prices reflect new information together with

the likely significance of the takeover premium by the end of the trading day (Bodie et

al. 2014, p. 351). According to Fama (1970, p. 415) the implication of the efficient

market hypothesis does not make sense to only look at historical data, neither does it

make sense to evaluate reports or get hold of information from companies that only

some within the company possesses, if there is information then it is reflected in the

stock prices (Fama, 1970, p. 415).

GCI investors (n.d) write about the assumption that an efficient market relies on

rationality among investors and that they act according in a logical manner towards

information and news. Criticism against the EMH includes the argument that humans

are not rational or efficient since we act irrational, emotional and likes to follow the

group behaviour. The authors provide an example of this that can be seen in the

beginning of Dot-com in the end of 1990s, where companies generated huge profits

only by putting Dot com after the company’s name and people went crazy to buy it,

which can’t be described as a rational behaviour (GCI investors, n.d). These

assumptions can thus be connected to theories of behavioural finance, which will be

discussed in a paragraph below. Bodie et al. (2014, p. 353-354) also present that the

17

implications are described more detailed in the three forms of market efficiency that

Fama created: weak, semi-strong and strong form.

3.4.1 Weak form According to Bodie et al. (2014, p 353) a weak form indicates that stock prices already

reflect the past information available that can be gathered by evaluating the history of

previous stock prices, short interest or volume. Past stock price data is freely available

and can be obtained at a small fee. The authors point out that the weak-form hypothesis,

if such data ever provided trustworthy signals about future performance, all investors

would have figured out how to profit from them by now. The prices of stocks would

instantly increase as the signals became more officially known, thus, a buy signal

should reduce the value. Therefore, according to this version of the theory, trend

analysis is useless (Bodie et al., 2014, p. 353).

3.4.2 Semi-strong form In a book written by Szylar (2013, p. 32) the semi-strong form means that publicly

available information concerning a company is already reflected in the stock prices. The

semi-strong form may appeal to our common sense the most and is therefore closer to

reality. It states that when significant new information is published, the market will

quickly absorb it by adjusting the price to a new equilibrium level that represents the

shift in supply and demand produced by the information's appearance. Szylar (2013, p.

32) states the semi-strong EMH makes up for its lack of intellectual rigor with empirical

strength, as it is easier to test than the strong EMH. One issue with the semi-strong

EMH is determining what constitutes "relevant publicly available information." As

appealing as the statement may appear, the reality is less so, because information does

not come with a handy label indicating which shares it affects and which it does not

(Szylar, 2013, p. 32).

3.4.3 Strong form Lastly, the strong hypothesis states that private information available within a company

as well as all relevant information connected to the firm is already reflected in the stock

prices (Bodie et al. 2014, p.354). An example of the strong form of market efficiency is

presented by Szylar (2013, p. 31). His example states that if one person possesses

confidential information and believe that the current market price is not justified to the

real value, the holders of that information will acquire the shares to take advantage of

the pricing anomaly. The holders of the classified information will keep acquire shares

until the oversupply of shares has pushed the price up to the level supported by their

classified information. They will have little motivation to keep buying at this point, so

they will exit the market, and the price will settle at this new equilibrium level (Szylar,

2013, p. 31).

EMH is a relevant theoretical framework to mention in this thesis since it would imply

that none of the stock portfolios should generate any major profits, if the EMH is to be

true. This is because the future gains from these stocks should be factored into the stock

prices. In other words, there should be no meaningful risk-adjusted returns. Thus, by

including this concept in the study we let the reader gain understanding of the theories

that propose a value premium cannot exist and why it cannot exist.

18

3.5 Random walk theory

The Efficient market hypothesis is evolved from previous theories and the random walk

theory is one of them (Kendall, 1953, p.13), which make this theory an important

background to understand the other theories that are presented. According to Mishkin

(2010) the random walk theory is an investment concept which assumes that the market

prices move up and down without following a certain pattern, with no power from

previous price fluctuations. With background of this, it is then impossible to predict

which way the market will go regardless of time. Keane (1983, cited in Chitenderu et

al., 2014, p. 1243) explains that the random walk theory argues that the direction a stock

price takes are random and can therefore not be forecasted based on previous price data.

According to the investors who agree with the RWT, they cannot outperform the market

without taking on greater risk. As a result, attempting to apply the theories will be a

waste of effort with no further benefits (Keane, 1983, cited in Chitenderu et al., 2014, p.

1243). Further on, Eugene F. Fama is one of the most influential researchers within the

area of random walk theory and has tested the theory a various amount of time. It could

be determined that there is no dependence in stock price series that can be considered as

important for investment purpose, which means that history can’t be used to increase

the investors expected profit (Fama, 1965, p. 87).

However, there are studies that talks both for and against the RWT. Van Horne &

Parker (1967) did a study consisting of industrial stock on the New York stock

exchange and wanted to test empirically the RWT in relation to past stock price

movements. They concluded that their study did support the random walk theory and

that trades who relied on past stock prices did not gain greater profits than buy-and-hold

investors (Van Horne & Parker, 1967). A study made by Hang & Grochevaia (2015)

tested to see if the Shanghai and Shenzhen markets, which are the most influential stock

markets in China, followed a random walk from 1992-2015. The overall result of this

thesis was that the return contradicted the random walk theory and that a pattern based

on the whole time period could be seen. Though, they also performed test on sub-

periods within the two markets which provided some inconsistency against the

statement to reject the null hypothesis of a random walk (Hang & Grochevaia, 2015, p.

29).

Worthington & Higgs (2004) performed a study which was made by looking at 20

markets in Europe. Their result provided evidence that most of the countries did not

meet the criteria for the random walk and its behaviour. Along with this study, more

research on the same theory is made which also proved to be against the random walk,

this result in difficulties to draw any conclusions about the RWT since the studies used

the same methods yet showed different results. Though, the authors explain that this of

course can depend on other factors, such as the economic situation during the tested

time-period, efficiency of the market or level of development in the researched country

but this is a subject for a future thesis (Worthington & Higgs, 2004). The random walk

theory is a core concept within the subject of finance that we have decided to conduct

this research on. Even if this theory wouldn’t be the main focus for us to test, it is

relevant to present since it is well connected to the efficient market hypothesis, which is

a theory that we will discuss later in the thesis. Both of these theories main statement is

19

that it is impossible to outperform and predict the market which is important to know in

order to gain a better understanding of the patterns of in the stock market.

3.6 Behavioural finance

According to several economists there are doubts on the precision of the Efficient

Market Hypothesis and the Random walk theories. Instead, they put their focus on the

concept of behavioural finance. Some of the arguments on this are that humans are not

logical in nature, and this is ignored in the Efficient Market Hypothesis (Bodie et al,

2014, p. 389). Therefore, theories of behavioural finance add further knowledge and

criticism against the previous theories brought up in this chapter.

Behavioural finance is a quite new concept within finance and has its roots from

behavioural economics, conventional finance and psychology. Discover biases, defects

and irrationalities in human decision-making can be said to be the main goal when it

comes to financial issues (Brealey et al., 2017, p. 340). Therefore, it is important to

recommend solutions and address them so that better decisions can be made. The

authors also describe that biases in behavioural finance may be due to individuals'

attitudes towards their own investing strategies. Conservatism is one of them, which

indicate that investors take too much time in the adjustment of their portfolios and

investment strategies when they are faced with new information (Brealey et al., 2017, p.

340). They tend to react in a correct way, though, to a less extent than would be

required (Brealey et al., 2017, p. 340). The other bias worth mentioning in terms of

behavioural finance is that some investors tend to be too overconfident in their

investment strategies which may attribute consequences to external causes or simply

bad luck (Brealey et al., 2017, p. 341).

Behavioural finance enables investors to gain a deeper understanding to the drivers of

their own, and their clients’ decision and apply this knowledge in their professional

practice to make better and more rational decisions (Valsova, 2016). In an article

written by Olsen (2008, p. 3) he states that people tend to connect larger groups with

comfort, which is also seen in finance. This can be referred to as herd instinct, and to

apply this into investment decisions we could say that a larger group can indicate a

lower risk. A positive affect from being associated as a member of a group also tend to

make us look past our own feelings and instead go with the group. Investors that follow

this behaviour can ignore their own forecasts and investment decisions in order to

follow the “reference group,” which may include other market participants, friends or

colleagues (Olsen, 2008, p. 3).

According to Ritter (2003, p.429) behavioural finance is founded on psychology, which

claims that human decision-making is prone to a variety of cognitive illusions. The

illusions can be divided into two categories. The first category, heuristic, can be defined

as “the rules of thumb.” This simplifies the decision-making, particularly in complicated

and uncertain situations (Ritter, 2003, p.431). This is done by reducing the complexity

of evaluating probability and forecasts to easier judgments (Kahneman & Tversky,

1974, p.1124). The heuristic concept is often useful, especially when time is short,

although they can lead to biases (Kahneman & Tversky, 1974, p.1124-1131). The

second category, prospect theory, can be defined as the concept where gains and losses

20

are valued differently. This will result in making decisions based on supposed rewards

rather than losses (Kahneman & Tversky, 1979, p.263). There is also evidence showing

that behavioural finance affects the price-volatility of securities. Olsen (1998) stated

that higher behavioural effects, intuitive decision procedures and stress, will result in

higher volatility. Further on, higher volatility can be a factor of poorly structured

decisions since the outcome can have higher unpredictability of decisions, bigger

differences of prices and a difficulty to measure returns. One reason of why we have

decided to present the behavioural finance theory is because it can be useful to have in

mind when discussing our results. The stock market is built on investors with different

behaviours and it will be interesting to evaluate if any pattern can be seen in terms of

behaviour, group pressure and irrationality.

3.7 Modern portfolio theory

Modern portfolio theory hold the same assumptions as the Efficient market hypothesis

and describes the fact that an investor can’t beat the market on a risk adjusted basis by

evaluating past prices. This theory can also be described as a theory that goes against

Behavioural finance, as it assume rational and risk adverse investors with no abnormal

risk adjusted returns. How to maximize the return for a given level of risk or decrease

risk for a given level of return can be described by the modern portfolio theory

(Markowitz, 1952). The theory states that the adaption of risk and return is done by

diversification, with intention to reduce unsystematic risk that investors may face when

owning one or few highly correlated stocks (Markowitz 1952, p.89).

To produce the best set of portfolios in theory, Markowitz (1959) created a

mathematical procedure for this. Investors could develop a table based on portfolios

with the same level of risk, where the risks are the same, but the returns differ, which

would indicate that the portfolio with the highest return is simply the best due to the

same risk level (Markowitz, 1959). The key to a reduction in risk is the correlation

between the stocks. This means that if a sector or a firm receives negative news, the

price of the stock in the portfolio will decrease. It would then lead to a fall in the stock

price of another highly related stock in the portfolio.

A study by Kierkegaard et al. (2006) investigated if investors can apply the MPT to

achieve a higher return than investing in an index. They concluded that the optimal

risky portfolio did provide a higher return than a passive index, during the five years the

study covered. The authors, on the other hand, are hesitant to conclude that investing

according to MPT, based solely on historical data and would be a preferable option to

an index portfolio (Kierkegaard et al., 2006, p. 35). In the context of this thesis, the idea

of distinguishing stocks that earn an abnormal risk adjusted return goes against MPT's

ideas. One reason why we decided to include the MPT in our thesis is because one of

the disadvantages of this theory is that it assumes that investors are rational and aim to

increase the return while reducing risk. However, as described in 3.6, investors tend to

act irrational and often end up following the groups behaviour which will be a limitation

for this theory. It will be interesting to see if we can draw any conclusions of

irrationality among investors based on our result.

21

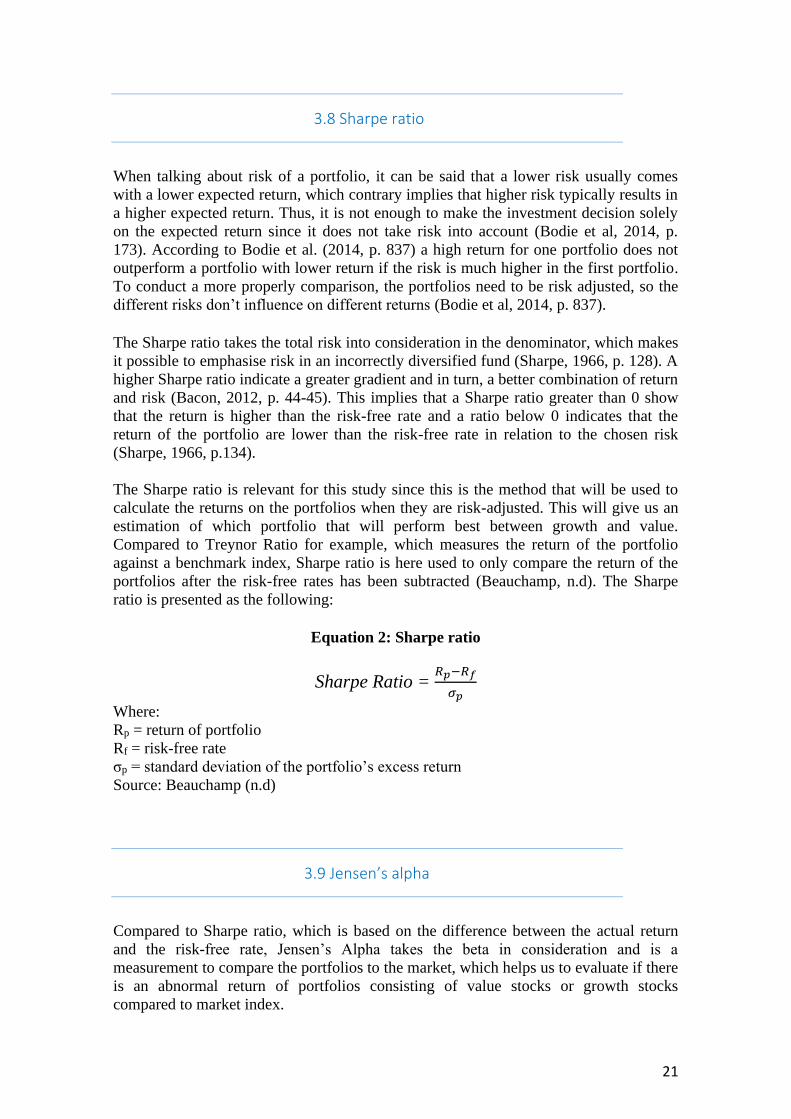

3.8 Sharpe ratio

When talking about risk of a portfolio, it can be said that a lower risk usually comes

with a lower expected return, which contrary implies that higher risk typically results in