ANALYSIS OF ANNUAL REPORT (2009-10) GROUP 3 ABHIJEET KUMAR 29 ADITYA KEDIA 51 AMIT KUMAR 79 ANUJ 76 HARMANJEET SINGH 77 MANISH NARULA 41 VINEET RANJAN 74

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 1/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 2/54

Real Estate Sector: An Overview

The real estate sector is of great importance in a

developing country like India.

An estimated shortage of 26.53 million houses

during the Eleventh Five Year Plan (2007-12)

provides a big investment opportunity.

India leads the pack of top real estate

investment markets in Asia for 2010, accordingto a study by PricewaterhouseCoopers (PwC)

and Urban Land Institute.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 3/54

DLF: An Overview

DLF- Delhi Land And Finance

India¶s biggest real estate developer

BUILDING INDIA- Mission and vision of company

Founded as Raisina Cold Storage and Ice Company

Current chairman- Mr. Kushal Pal Singh ± world¶s richestproperty developer- world¶s 98th richest man according toforbes

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 4/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 5/54

Major milestones

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 6/54

Balance Sheet

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 7/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 8/54

Cash Flow

2010 (Rs. Cr.) 2009 (Rs. Cr.)

Cash flow from Operating Activities (A) 39,524 1,36,586

Cash flow from Investing Activities (B) (2,41,999) (1,15,117)

Cash flow from Financing Activities (C) 1,43,494 (43,754)

Net increase/ decrease of cash and cash equivalents

(A+B+C)

(58,980) (22,284)

Cash and cash equivalents at the beginning 75,940 98,224

Cash and cash equivalents at the close 16,960 75,940

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 9/54

Implications

Cash flow from Operating Activities shows a decrease because

of a rise in debtors and decrease in overall current liabilities.

Cash flow from Investing Activities shows an outflow of cash

because the company sees a lot of scope to invest post

recession. It has started investing in its subsidiaries and has

several projects in hand.

Cash flow from Financing Activities shows and increase in cash

due to the company taking long term loans.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 10/54

Capital Structure

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 11/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 12/54

Economic Ratios

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 13/54

DEB T EQUITY RATIO

The company paid a debt of Rs. 5633 as

against a mandatory payment of Rs. 3549

The Average Cost of D

ebt stood at 10.5% ason 31st March 2010.

The Debt Equity Ratio lowered from o.78 in

2008-2009 to 0.53 in 2009-2010.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 14/54

The company has set a target for Rs. 250 bn

of core assets disinvestment for the next 6

quarters.

It has done Rs. 29 Bn in Q1FY11.

Key for the company to cut its debt burden.

DLF is also replacing short term loans with

long term loans which do not affect the debtand also have a lower interest rate.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 15/54

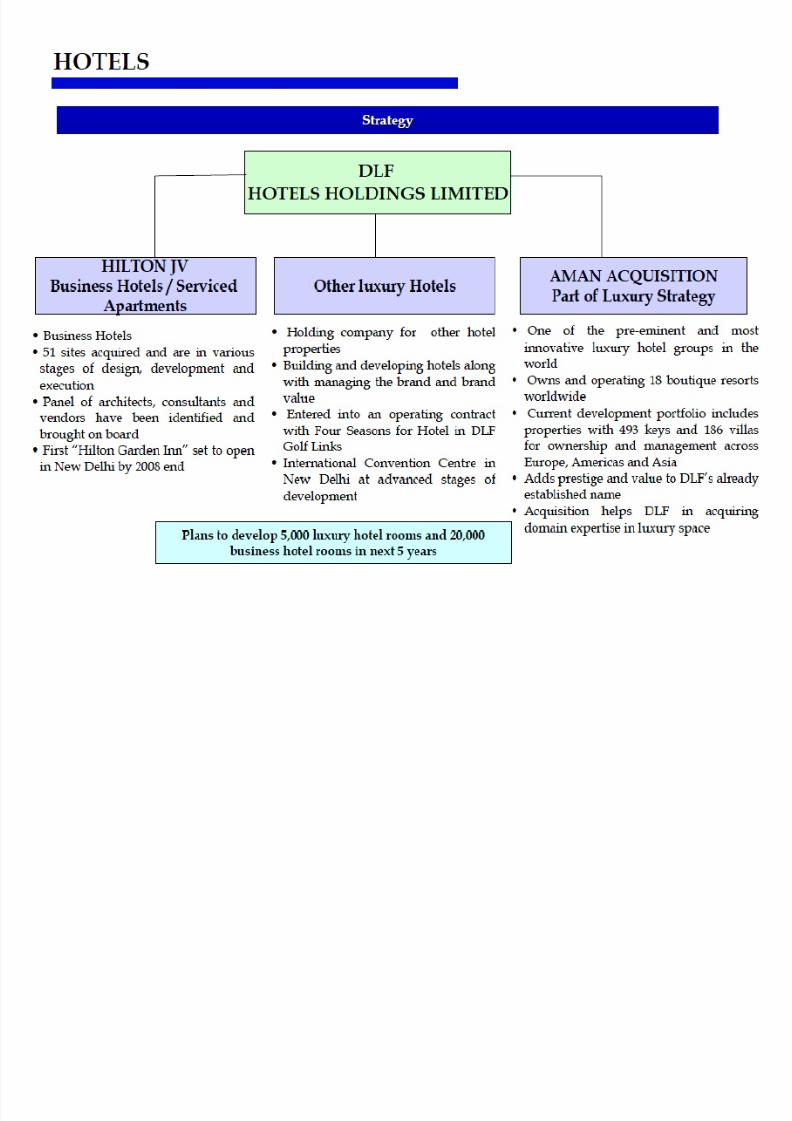

DLF, is making a quick exit from hospitality

sector by selling off its 97% stake from a

luxurious hotel group µAman Resorts¶.

Main motive of DLF is to become debt free

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 16/54

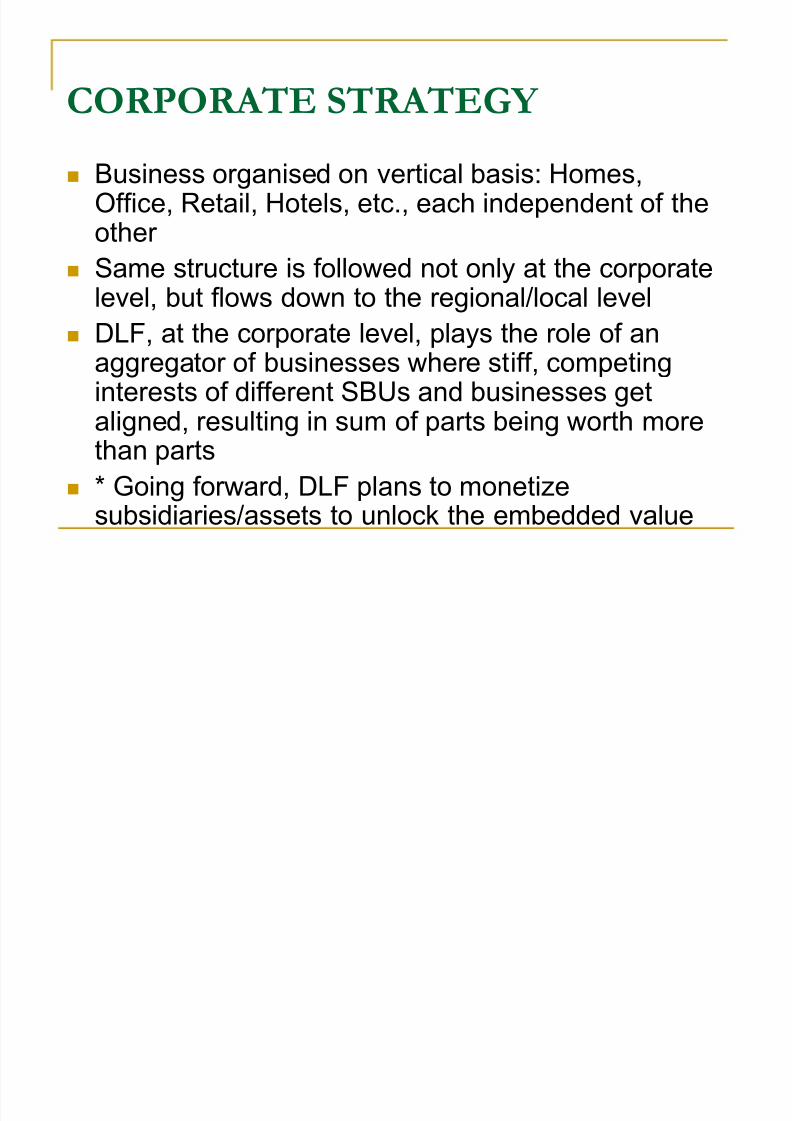

CORPORATE STRATEGY

Business organised on vertical basis: Homes,Office, Retail, Hotels, etc., each independent of theother

Same structure is followed not only at the corporatelevel, but flows down to the regional/local level

DLF, at the corporate level, plays the role of anaggregator of businesses where stiff, competinginterests of different SBUs and businesses get

aligned, resulting in sum of parts being worth morethan parts

* Going forward, DLF plans to monetizesubsidiaries/assets to unlock the embedded value

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 17/54

Corporate Strategy ( Continued)

* With core businesses reaching stable operating performance,focus is to aggressively ramp up new businesses like hotels,infrastructure, SEZs, etc.

Key focus on execution of projects ±with current levels reaching

a run rate of 62 msf across businesses (excluding Hotels) * DLF will look into making small µpure¶investments in non-real

estate businesses, with target ROI of more than 20%

The compensation structure within the mid / senior levelempolyees allows for participation in the success of variousprojects/businesses

Base salary ±30% with a 70% variable component linked to theKPAs, overall through stock options.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 18/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 19/54

Land Resource as on 31-March-2008 (Mn SqFt)

Segment Total Super

metros

Metro

s

Tier I Tier II

Office 164 64 70 26 5

Retail 92 33 36 14 9

Super Luxury 4 4 0 0 0

Luxury 41 33 6 1 0

Mid income/Plots/Villas 432 113 231 73 16

Hotel/Convention centres 18 4 2 10 2

Grand Total 751 251 345 123 32

% 33% 46% 16% 4%

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 20/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 21/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 22/54

L ARGE INTEGRATED TOWNSHIPS

DLF pioneered development of large integratedtownships decades ago with the development of the3,000 acre DLF City, Gurgaon.

Townships include residential, commercial and retailproperties in a modern city infrastructure, completewith schools, hospitals, hotels, shopping malls andrecreational hubs

DLF has inked JV with Nakheel LLC of the UAE,

who have to their credit the development of ThePalms and Al Burj, among other outstandingarchitectural projects

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 23/54

L ARGE INTEGRATED TOWNSHIPS

BidadiTownship: An integrated township spread over 9,168 acres onthe outskirts of Bangalore with potential value creation of approx. Rs50,000 crore (approx USD 12.5 billion).Work to start by mid 2008.

ShivajiMarg: Acquisition of SwatantraBharatMill, along with pre-ownedlands, will have a development potential of approx. 10 msf with potentialvalue creation in excess of Rs 12,000 crore (approx USD 3 billion)

New Gurgaon: A 4,000 acres township falling in the new masterplanfor Gurgaon, with all segments of residential, commercial and retail

Dankuni, Kolkata: 5,000 acres of township on the western outskirts of Kolkata

South Maharshtra: Acquisition of land started for building a high-endresort city for holiday and luxurious lifestyle

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 24/54

OFFICE

India forms an important part of growth strategy for every major multinational worldwide

Entry of multinationals has grown by over 300% inlast two years alone leading to huge demand for

office space Demand for IT/ITES services (expected to grow at

15-20% CAGR over FY2010-16)

Indian corporatesgetting increasingly dynamiccreating huge demand for quality office space

Total commercial real estate demand likely to be ~450-530 msf by FY 2011.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 25/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 26/54

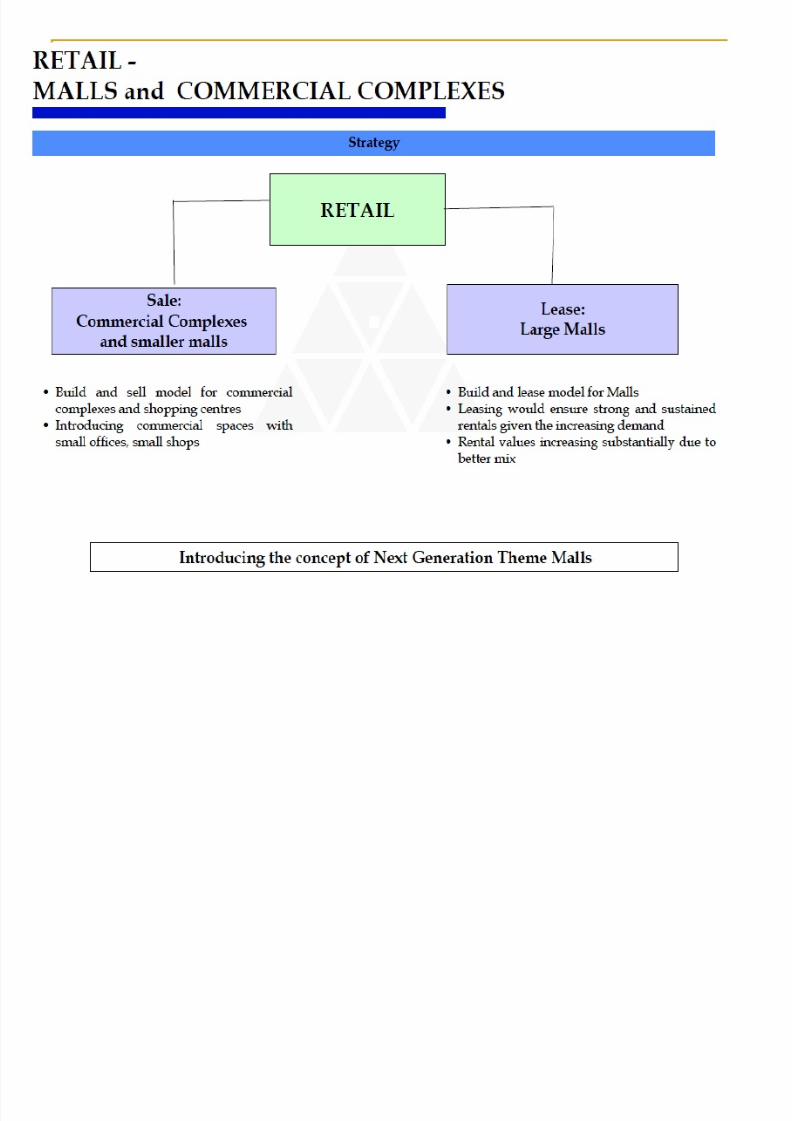

DLF and RETAIL

10-year annual target delivery of 8 mnsq ft every year.

Given the scarcity of quality organized retail, DLF enjoys thebenefits of a portfolio of premium locations across the countryand rush by large retailers

DLF envisages to introduce a new retail infrastructure to cater tothe need for shopping malls and commercial centresacross alsegments and all places in India

DLF has plans for delivering 1 msf of luxury malls, 4 msf of shopping malls and 3 msf of neighborhood malls annually

Current developable land resource earmarked for retail standsat92 msf

All major retail players, including new entrants pitch aggressivelyfor space in DLF Malls

11msf under construction

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 27/54

RETAIL MA LLS & COMMERCIA L COMPLEXES

Modern retail formats in India command just 3% of

total retail market, much lower than developed

markets (US ±85% share) and even Asian countries(Malaysia ±55%, Thailand ±40%, China 20%)

Organized retail segment in India is expected to

grow at a rate of 25% to 30% over the next 5 years.

Organized retailing would require around 350-400msf of retail real estate in India by FY 2016.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 28/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 29/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 30/54

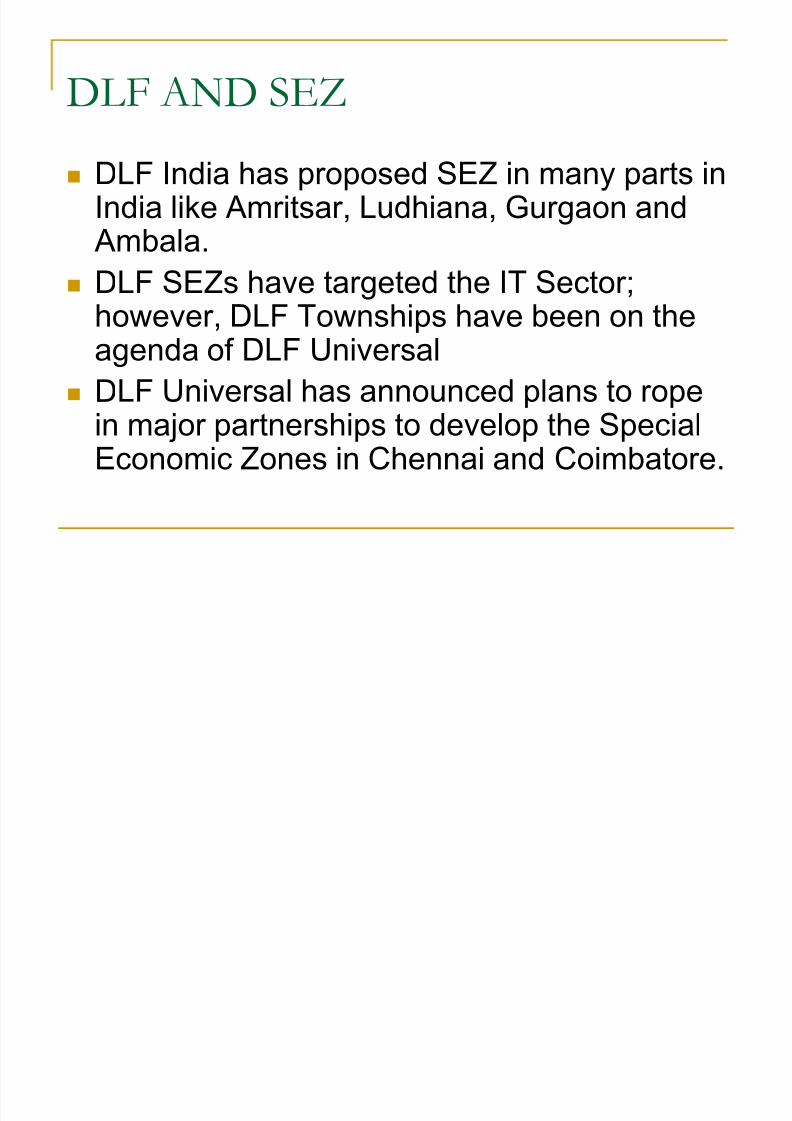

DLF AND SEZ

DLF India has proposed SEZ in many parts inIndia like Amritsar, Ludhiana, Gurgaon and Ambala.

DLF SEZs have targeted the IT Sector;however, DLF Townships have been on theagenda of DLF Universal

DLF Universal has announced plans to rope

in major partnerships to develop the SpecialEconomic Zones in Chennai and Coimbatore.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 31/54

Wind Power Projects by DLF

DLF group is the largest owner of wind power plants inIndia with an installed capacity of 228.7 MW.

DLF has initiated its wind power portfolio in March2008. Currently the group owns wind farms in the

states of Gujarat (150 MW), Rajasthan (34.5 MW),Tamil nadu (33MW), and Karnataka (11.2 MW).

These projects reduce about 4.7 tonne of CO2emissions on annual basis.

The wind power projects in the states of Gujarat and

Karnataka are already registered for carbon credits atUNFCCC and generating over 3 Lakh CERs (CertifiedEmission Reductions) annually.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 32/54

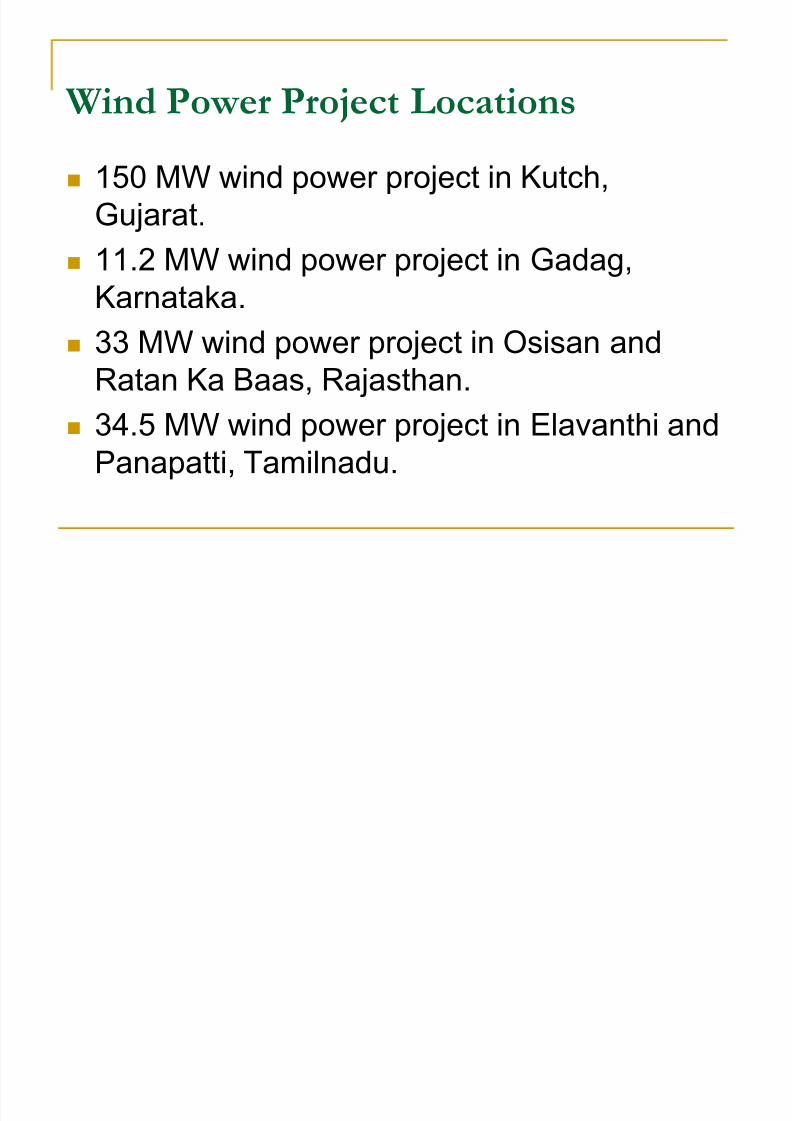

Wind Power Project Locations

150 MW wind power project in Kutch,

Gujarat.

11.2 MW wind power project in Gadag,

Karnataka.

33 MW wind power project in Osisan and

Ratan Ka Baas, Rajasthan.

34.5 MW wind power project in Elavanthi andPanapatti, Tamilnadu.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 33/54

DLF AND ITSSUBSID AIRES

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 34/54

Reasons why companies may have

subsidaires?

Risk

Acquisition Regulation

Territoriality

Taxation

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 35/54

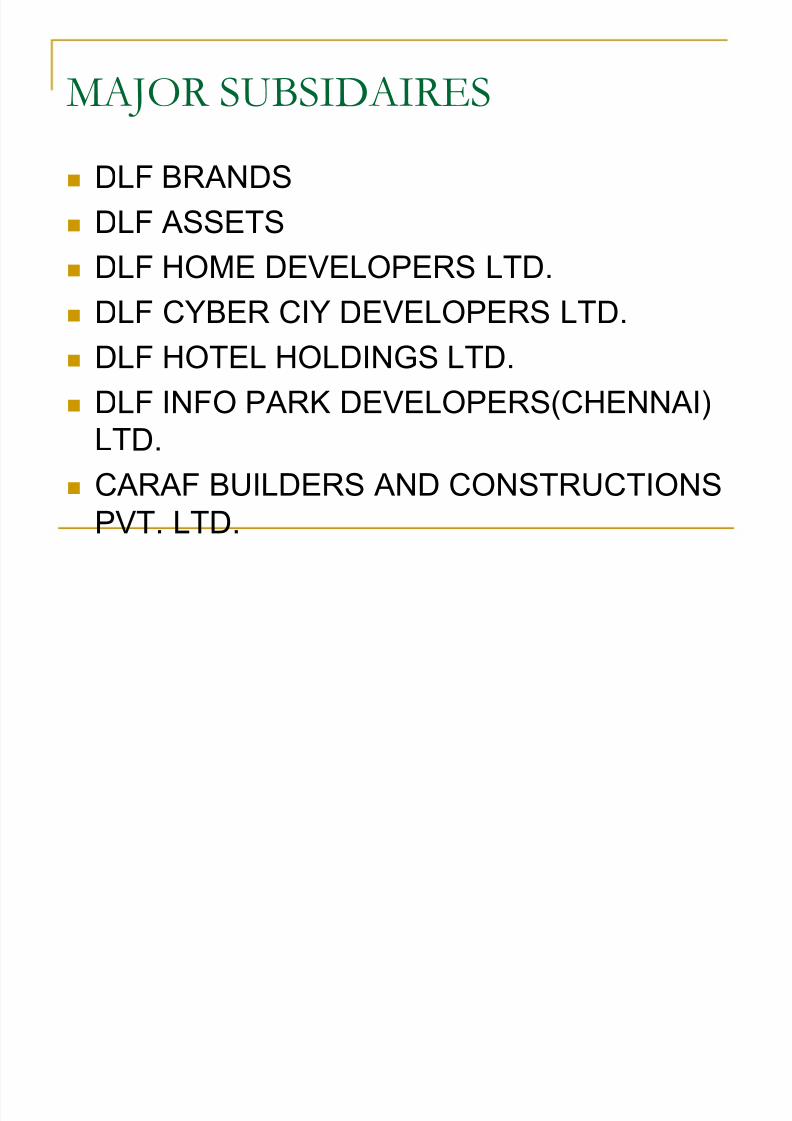

M AJOR SUBSID AIRES

DLF BRANDS

DLF ASSETS

DLF HOME

DEVELOPERS LT

D.

DLF CYBER CIY DEVELOPERS LTD.

DLF HOTEL HOLDINGS LTD.

DLF INFO PARK DEVELOPERS(CHENNAI)

LTD.

CARAF BUILDERS AND CONSTRUCTIONS

PVT. LTD.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 36/54

COMPETITION

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 37/54

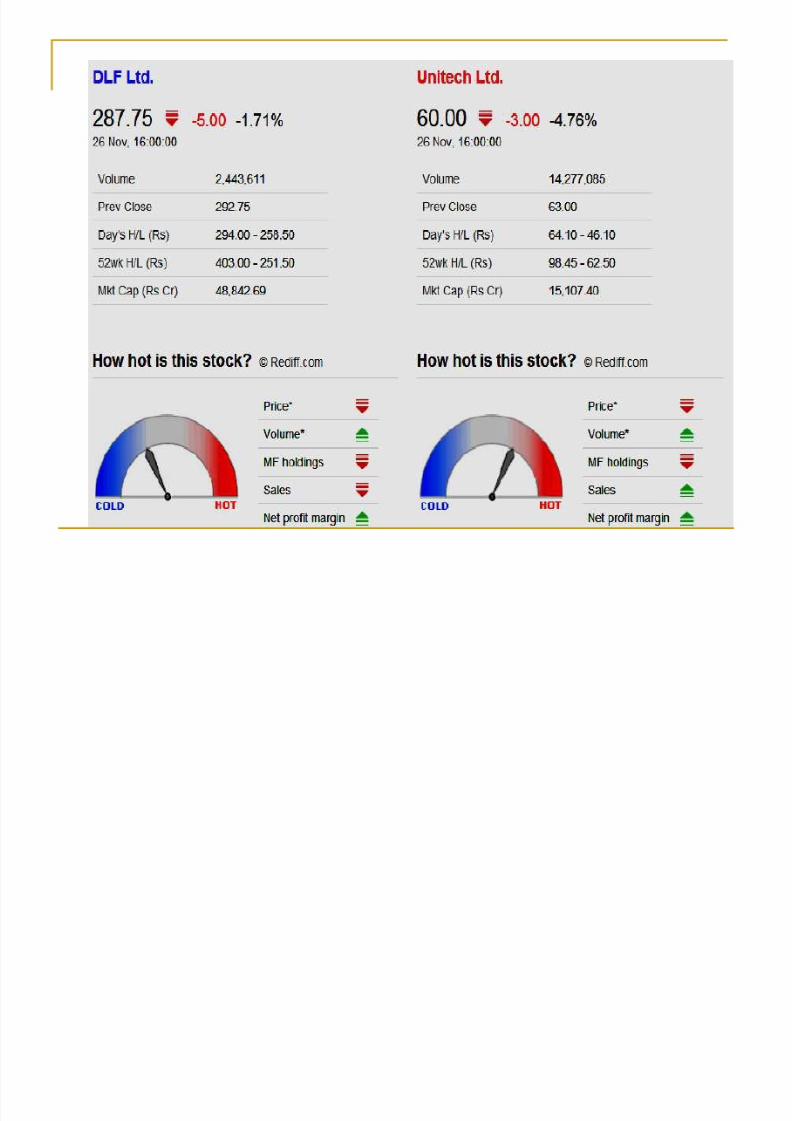

DLF VS. UNITECH

UNITECH CLAIMS TO BE INDIA¶S SECOND

LARGEST REAL-ESTATE INVESMENT

COMPANY - 10,538 CRORE RUPEES

TOTAL ASSETS (MARCH 2010)

DIVERSIFYING INTO TELECOMS IN

COOPERATION WITH NORWAY¶S

TELENOR GROUP ENVISION FOR 50% GROWTH PER YEAR

SINCE 2008

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 38/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 39/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 40/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 41/54

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 42/54

DLF SH ARE PRICE

The stock has underperformed in comparison

with the broader indices and is expected to

improve.

We believe that the current bullish

consolidation could lead to a potential upside

up to the levels of Rs 430 and above.

As the market stabilizes there are chances of growth.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 43/54

Recession and its Impact

Credit freeze stemming from the collapse of Lehman Brothers prompted investors andspeculators to withdraw investments from this

sector Property developers, who raised funds

through external sources, were left strandedwith minimal cash flows and huge debt

obligations surfacing in the near term.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 44/54

Recession and its Impact

The company¶s net profit for 2008-09 dipped over 41percent to Rs.4,629 crore from Rs.6,176 crore earnedthe previous year.

DLF is the market leader in this sector with net profit of 1547 cr.

It was way lower than its last year profit by more than1000 cr.

It also delayed a buyback of INR 1,100 crore as a resultof liquidity crunch.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 45/54

Recession and its Impact

It was well supported by the timely launch of IPL.

The share of this co. touched the all time highof 1727 in feb. 2008. but in the year 2008-09it was high at 446.90 and low at 124.15.

Its present market capital is Rs 74,704.46crore.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 46/54

SWOT Analysis

Strength Weakness

Opportunities Threats

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 47/54

Strengths Brand name and reputation: DLF retains internationally and nationally

renowned architectural, construction and consulting firms for its projects.

Extensive land reserves: The Company recognizes that extensive land

reserves are the most important resource for a real estate developer.

Scale of Operations: The Company¶s size allows it to benefit from

economies of scale. DLF is able to purchase large plots of land from

multiple sellers, thus enabling it to aggregate land at lower prices.

A tradition of innovation: DLF has a tradition of innovation in the Indian

real estate market. It is one of the first developers to anticipate the need

for townships on the outskirts of fast growing cities and is generallycredited with the growth of Gurgaon.

Experienced and dedicated management: The Company has an

experienced, highly qualified and dedicated management team.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 48/54

Weakness

No parallel products to support during times of bad economy

Macroeconomic risks:

Any weaker-than-expected GDP growth for the domestic economy

could negatively affect sentiment of buyers, leading to elusive demand,which could render sales and earnings estimates for DLF unrealizable

Real risk of decline in property prices, and concentration in

Gurgaon

NCR region still accounts for 42% of the development area for thecompany, thus exposing it to significant price movements in the regions

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 49/54

Opportunities

Expansion of business in other parts of India

It can invest more in Power generation projectslike Hydroelectric or Wind power

Investment in raw material ± Backward Vertical

Integration

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 50/54

Threats

Competitors may try to get more market share through improved

techniques

New rivals Bombay Dyeing, Golden Tobacco and Century Textiles. There has

been a precedent with groups like Tata, Mahindra and Godrej having turned

developers. The Tata group has Tata Housing and Tata Realty while

Mahindras venture is called Mahindra Lifespace Developers. Godrejs venturegoes by the name of Godrej Properties.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 51/54

FUTURE PROJEC TS

1. India's largest Exhibition and Convention Centre to be built by DLF in Sector

24, DWARKA, NEW DELHI by 2010.

2. Mall of India is an under-construction shopping mall in Gurgoan, India- area

of 4,500,000-square-foot (418,100 m2)- the largest mall ever built in India-

one of the largest in the world- estimated cost $ 298 million( 1500 crore

INR).

3. DLF Corporate Greens -located next to NH 8, in the upcoming Sector 74A,

Gurgaon -Spread over sprawling 25 acres-the project is to be developed on

the lines of district centre comprising premium Commercial , Retail and IT

spaces.

4. DLF Plaza Lucknow - catering to office, retail, leisure, entertainment

requirements- also internationally acclaimed Hilton Garden Inn hotel- area

of 69677 sq mts (approx)- will have 2 levels of basement parking to

accommodate approx 800 cars-24 hour security surveillance- equipped

with modern fire fighting systems.

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 52/54

CONCLUSION

India¶s largest real estate company in terms of revenues,earnings, market capitalisation and developable area with a 62-year track record of sustained growth, customer satisfaction andinnovation

Low risk due to multiple businesses and segments withinbusinesses, across geographies

All earnings enablers in place ±high quality / high value ³zoned´land resource in super metros & metros and motivated teams atlocal level to execute projects

CRISIL upgraded the rating from µA+ with a negative outlook¶ toµA+ with a stable outlook¶

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 53/54

Businesses (Commercial, retail & luxury homes) which contribute

more than 80% of long term value are at stable operating

platform Stupendous response to the launch of µmid-income homes¶±

strong validation of strategy

Set to change the hospitality landscape in India-

On way to set up 20,000 business hotel rooms in the next 5

years in partnership with Hilton

Acquisition of domain expertise & assets with buy-out of

Aman Resorts business

Only developer with the experience of setting up of large

townships

8/8/2019 DLF_2009-10 Annual Report

http://slidepdf.com/reader/full/dlf2009-10-annual-report 54/54

THANK YOU

Related Documents