Divesting Power G. Federico 1 A. L. Lpez 2 October 2009 IEFE Seminar 1 Charles River Associates and IESE Business School (SP-SP). 2 IESE Business School (SP-SP). G. Federico, A. L. Lpez (October 2009) Divesting Power IEFE Seminar 1 / 30

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Divesting Power

G. Federico1 A. L. López2

October 2009

IEFE Seminar

1Charles River Associates and IESE Business School (SP-SP).2IESE Business School (SP-SP).

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 1 / 30

Motivation I: market power mitigation in electricity

Wholesale electricity markets prone to the exercise of market power

Low demand elasticityCost heterogeneity with capacity constraintsUniform pricingNational/local marketsStrong incumbency positions

Market power mitigation a key policy consideration

Ex-ante regulation (including merger control)Ex-post antitrust

Physical or virtual plant divestments are often the main market powermitigation measures available to competition authorities/regulators

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 2 / 30

Motivation II: examples of divestments/VPPs

Merger control

EDF/EnBW (VPP, 2000)Nuon/Reliant (VPP, 2003)EDP/GDP (VPP/lease, 2004)Gas Natural/Endesa (Divestment, 2005)EDF/British Energy (Divestment and VPP, 2008)Gas Natural/Union Fenosa (Divestment, 2009)

Ex-ante regulation

Great Britain: divestments used after liberalisation (mid-1990s)Italy: divestments used prior to liberalisation (late 1990s)Spain/Portugal: VPPs introduced to mitigate market power (2008onwards)

Remedy for abuse of dominance

Enel (VPP, 2006)RWE (VPP, 2008)E.On (divestment, 2008)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 3 / 30

Common intuitions - and outstanding questions

Distinction often made between ability and incentives assets

Ability assets have higher marginal cost: lower opportunity cost ofwithholdingIncentive assets have low marginal cost: provide incentives forwithholding ability assets

Divestments of ability assets can reduce scope for withholding - but:

Which ability assets should be divested?Does one need to also address incentives to withhold by divesting someincentive assets?Can virtual contracts replicate the optimal divestment of ability and/orincentives plants?

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 4 / 30

Related literature

Mostly focuses on the impact of �xed-price forward contracts(equivalent to baseload VPP)

Standard market-power mitigation (Allaz and Vila (1993); Newbery(1998))More recent papers highlight some potential de�ciencies of contracts inelectricity markets (Schultz (2007); Zhang and Zwart (2006); andFabra and de Frutos (2008))

No modelling of VPP vs divestments that we are aware of, or ofrelative e¤ectiveness of di¤erent types of divestments

Willems (2006) distinguishes between �nancial and physical VPPs butboth are contractsWolak and McRae (2009) discuss di¤erent types of divestments inqualitative terms, by reference to recent US merger (Exelon/PSEG)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 5 / 30

Aim of this paper

Investigate the market power mitigation policy that leads to thegreatest bene�t to consumers (for a given size of intervention)

Divestments vs VPPDi¤erent types of divestmentsDi¤erent types of VPPs

Model impact of (de)concentration of price-setting capacity

Allow for extensive cost asymmetries in generation portfolios (frombaseload to mid-merit and price-setting plants)

Simplify nature of market power to allow for rich set of divestmentoptions

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 6 / 30

Main results

A unique optimal divestment can be identi�ed in a model of adominant �rm with a competitive fringe

the divested capacity needs to include price-setting generation plants,which would otherwise be withheld by the dominant �rmfor divestments of intermediate size, the optimal divestment does notinclude the cheapest generation assets withheld by the dominant �rm,and the cost range of the divested capacity spans the post-divestmentpricethe optimal divestment is e¤ective because it makes the residualdemand faced by the dominant �rm more elastic, and can beseveral-fold more e¤ective than a baseload divestment

The e¤ectiveness of VPPs is maximised when all of the options whichare sold are exercised

in this case the VPP reduces prices as much as a divestment ofbaseload generation of the same sizethis implies that divestments are much more pro-competitive thanVPPs (in a one-shot setting)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 7 / 30

Model set-up

Standard model of dominant �rm with a competitive fringe

Increasing and linear marginal cost function (symmetric): ci = γqi fori = d , f

Demand is completely price-inelastic: qd + qf = µ

Fringe bids all of its output at cost: p = cf = γqf , whereqf = µ� qdImplies following pre-divestment equilibrium:

q�d =µ

3; and p� =

23

γµ

Prices are above the competitive level (p� > pc = 12γµ).

Withheld output equals µ6

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 8 / 30

De�nition of (physical) divestment

Transfer of contiguous segment of the marginal cost function of thedominant �rm to the fringe (through a competitive auction)

Size of divestment de�ned as δ

Position of divestment identi�ed by highest (marginal) cost of thedivested units, de�ned as c (implies lowest cost of the divested unitsis c = c � γδ )

Divestment shifts both the marginal cost and residual demandschedules of the dominant �rm:

Cost-increasing e¤ectDemand-reducing e¤ect (coupled with a demand-slope e¤ect)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 9 / 30

Description of divestment

Slope =

Slope =

µ'q

γ

2γ

dqγ

γµ

( )δµγ −

c

γδ−c

δ−'q

Divested units

Quantity

Price, costs

( )δγ +dq

Predivestmentresidual demand

Predivestmentmarginal cost

Slope =

Slope =

µ'q

γ

2γ

dqγ

γµ

( )δµγ −

c

γδ−c

δ−'q

Divested units

Quantity

Price, costs

( )δγ +dq

Predivestmentresidual demand

Predivestmentmarginal cost

Figure:G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 10 / 30

Divestment size thresholds

Three cases can be identi�ed for the impact of a divestment onprices, depending on its size as a share of total demand ( δ

µ )

Small divestments: δµ < 1�

125p6� 0.02

Intermediate divestments: δµ 2

h1� 12

5p6, 1� 2p

6

iLarge divestments: δ

µ > 1�2p6� 0.18

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 11 / 30

Divestments of intermediate size

For intermediate divestments, the post-divestment price function isthe following (as a function of the position of the plant divestment):

Segment Price Range of c

I (baseload) p� � ∆p γδ � c < γ�

µ+δ3

�II γµ� c γ

�µ+δ3

�� c < γ

�µ+2δ3

�III p� � 2∆p γ

�µ+2δ3

�� c < γ

�2p63 � 1

�(µ� δ)

IV 38 (γ(µ� δ) + c) γ

�2p63 � 1

�(µ� δ) � c < γ( 35µ+ δ)

V c � γδ γ( 35µ+ δ) � c < p� + 3∆pVI p� c � p� + 3∆p

where ∆p � γδ3 .

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 12 / 30

Post-divestment price function (intermediate divestment)

*p

pp ∆−*

pp ∆− 2*

)(13

62 δµγ −

−

+ δµγ

53

pp ∆+ 3* c

p

I II III IV V VI

( )cp

pp

∆+2

*

pp

∆+ 22

*

*p

pp ∆−*

pp ∆− 2*

)(13

62 δµγ −

−

+ δµγ

53

pp ∆+ 3* c

p

I II III IV V VI

( )cp

pp

∆+2

*

pp

∆+ 22

*

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 13 / 30

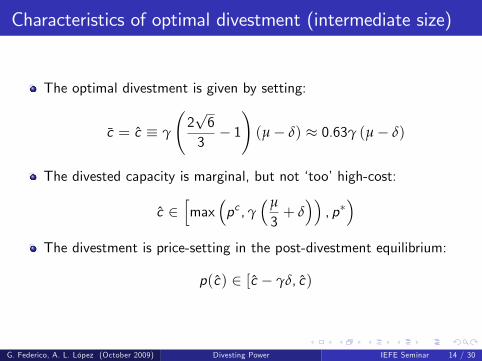

Characteristics of optimal divestment (intermediate size)

The optimal divestment is given by setting:

c = c � γ

2p63� 1!(µ� δ) � 0.63γ (µ� δ)

The divested capacity is marginal, but not �too�high-cost:

c 2hmax

�pc ,γ

�µ

3+ �, p��

The divestment is price-setting in the post-divestment equilibrium:

p(c) 2 [c � γδ, c)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 14 / 30

Position of the optimal divestment

For δµ =

120

µ

γµ

cγδ−c

Optimal divestmentof size

Quantity

Price, costsPredivestmentresidual demand

2µ

3µ

*p

cp

Predivestmentmarginal costs

δ

δ

µ

γµ

cγδ−c

Optimal divestmentof size

Quantity

Price, costsPredivestmentresidual demand

2µ

3µ

*p

cp

Predivestmentmarginal costs

δ

δ

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 15 / 30

E¤ectiveness of optimal divestment (intermediate size)

The optimal divestment is e¤ective because

it induces the �rm to price on the �atter segment of its residualdemand,it is not cost-increasing for the dominant �rm,it is su¢ ciently competitive to constrain the dominant �rm.

The ratio between the price reduction achieved by the optimaldivestment and of a baseload divestment can be expressed asR�

δµ

�= p��p(c )

∆p

at the lower bound of the relevant range of δµ , R

�δµ

�� 9.9,

at the upper bound of the range, R�

δµ

�� 2.7 (and also p(c) = pc )

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 16 / 30

De�nition of VPP

VPPs are call options that are imposed on the dominant producer fora certain fraction of its generation output

The options are sold through a one-o¤ VPP auction

The option holders obtain a right to acquire output from thedominant �rm at a strike (or exercise) price ps , and can re-sell thisoutput in the spot market to obtain the market price p

Each option is then exercised whenever p > ps

We assume that the VPP scheme entails the sale of a group ofin�nitesimally small call options each with a di¤erent strike price

The sum of the volumes associated with the aggregate set of optionsequals δThe strike prices associated with each option is de�ned by anincreasing and continuous linear function that has slope γ

The VPP therefore mimics a physical plant divestment of size δ, withcost slope γ

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 17 / 30

Pro�t functions with VPP

If the option is always exercised (i.e. pVPP (c) � c) then thedominant �rm maximises:

πd = pqd �γ

2(qd )

2 +Z q 0

q 0�δγxdx � pδ

If only part of the option is exercised (i.e. pVPP (c) < c ) then thedominant �rm maximises:

πd = pqd �γ

2(qd )

2 +Z µ�qd

q 0�δγxdx � p(µ� qd �

�q0 + δ

�)

which exploits the fact that p/γ = qf = µ� qd .

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 18 / 30

Impact of VPP

The post-VPP price function pVPP (c) has 3 distinct segments, forδ � µ

2 :

Segment Price Range of cIVPP p� � ∆p γδ � c < p� � ∆p

IIVPP 12

� c2 + γ

�µ� δ

2

��p� � ∆p � c < p� + 3∆p

IIIVPP p� c � p� + 3∆ppVPP (c) is weakly increasing in c .

The VPP which achieves the largest price reduction is achieved bysetting c < p� � ∆p (i.e. selecting a baseload VPP which is exercisedin its entirety)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 19 / 30

Impact of VPP

*p

pp ∆−*

c

p

( )cp

pp ∆+ 3*pp ∆−*

IIIVPPIIVPPIVPP

( )cpVPP

450

*p

pp ∆−*

c

p

( )cp

pp ∆+ 3*pp ∆−*

IIIVPPIIVPPIVPP

( )cpVPP

*p

pp ∆−*

c

p

( )cp

pp ∆+ 3*pp ∆−*

IIIVPPIIVPPIVPP

( )cpVPP

450

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 20 / 30

Impact of VPP

Segment I : a baseload VPP (i.e. the options are all exercised) yieldsthe same price reduction as a baseload divestment of the same size:

it removes an amount δ from the infra-marginal output of thedominant �rm, inducing it to price lowerequivalent to losing some infra-marginal (i.e. low-cost) output throughthe divestment of baseload capacity to a competitive fringe, and facinga reduction in residual demand of the same size

Segment II : the highest strike price rises above p� � ∆p , implyingthat it is not pro�table to exercise some of the call options:

a higher amount of output for the dominant bene�ts from spot prices,inducing it to set higher level spot pricesthe price in this segment increases with the level of the highest strikeprice of the VPP, until none of the options are exercised in equilibrium

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 21 / 30

Divestments vs VPP

VPPs are never more e¤ective than divestments of the samesize/position

The comparison between the optimal and baseload divestmentdescribes the relationship between the optimal divestment and theoptimal VPP as well

VPPs are less pro-competitive than divestments:they a¤ect the �nancial �ows obtained by the dominant �rm but notthe production capacity that is available to its competitorsdivestments can increase the output available to competitors withoutincreasing the cost of the dominant �rm (i.e. if withheld capacity isdivested)divestments can also induce the dominant �rm to price lower to �keepdivested units out of the market�(this incentive is absent with VPPs)

This comparison holds statically - it abstracts from the other possible(dis)advantages of VPPs

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 22 / 30

Welfare analysis (intermediate divestments)

A divestment changes total welfare through three e¤ects:

∆W (c) =

23 µZ

p(c )γ

γxdx

| {z }cost saving

competitive fringe

�

p(c )γZ

q�δ

γxdx

| {z }additional costdivested units

�

µ+q�δ4Z

µ3

γxdx

| {z }.

additional costdominant �rm

Welfare increases as long as the output of the dominant �rm (net ofthe divested output) does not decrease

This condition is satis�ed at the optimum divestmentIt is also satis�ed for other cost ranges, except for range III (in whichcase welfare can fall if the divestment is su¢ ciently small)

A baseload VPP is also welfare-increasing since it leads to a netoutput increase by the dominant �rm

However it increases welfare by less than the optimal divestment

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 23 / 30

Optimal small and large divestments

Small divestments ( δµ < 1�

125p6� 0.02)

it is optimal to divest plants which give incentives to the dominant �rmto set a price equal to the lowest cost of the divested capacity(corresponds to Segment V of the price function for intermediatedivestments)cost of divested plants is between the pre-divestment price and thecompetitive pricedivested plants do not produce in equilibrium

Large divestments ( δµ > 1�

2p6� 0.18)

divesting the cheapest plants withheld by the dominant �rmpre-divestment (i.e. setting c = γ

� µ3 + δ

�) is optimal and achieves the

competitive priceoptimal divestment is not unique (cheaper plants can also achieve thecompetitive price)costs of divested capacity encompass post-divestment price (as inintermediate case)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 24 / 30

Relative e¤ectiveness of the optimal divestment

Intermediatedivestments

Largedivestments

Smalldivestments

µδR

µδ

µδR

( )γµ

cp at optimal divestment

( )γµ

cp

123456789

1011121314151617181920

0.025 0.050 0.075 0.100 0.125 0.150 0.175 0.200 0.225 0.250 0.275 0.300 0.325 0.350 0.375 0.400 0.425 0.450 0.475 0.5000.40

0.45

0.50

0.55

0.60

0.65

0.70

Intermediatedivestments

Largedivestments

Smalldivestments

µδR

µδ

µδR

( )γµ

cp at optimal divestment

( )γµ

cp

123456789

1011121314151617181920

0.025 0.050 0.075 0.100 0.125 0.150 0.175 0.200 0.225 0.250 0.275 0.300 0.325 0.350 0.375 0.400 0.425 0.450 0.475 0.5000.40

0.45

0.50

0.55

0.60

0.65

0.70

Figure:G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 25 / 30

Extension with variable demand

Consider a case where demand is variable and a single divestmentpackage needs to be selected

we constructed a numerical simulation based on demand and price datafrom the Italian spot market during 2007based on the minimum and maximum demand observed during theperiod, we selected divestment sizes consistent with the intermediatecasedi¤erent demand duration levels considered for the impact of thedivestment

Results of numerical illustration

For high demand variance (i.e. all demand levels considered), it isoptimal to select a divestment with a cost that is lower than that ofthe optimal divestment at average demand.For low demand variance (i.e. only highest demand levels considered),it is optimal to select a divestment with a cost that is higher than thatof the optimal divestment at average demand

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 26 / 30

Extension with variable demand

Price duration curves for λ = 100% and δ = 3GW

40

50

60

70

80

90

100

110

120

130

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%Duration

Pric

e (E

uro/

MW

h)

Predivestment pricePostdivestment price (optimal divestment)Postdivestment price (optimal divestment at average demand)Position of optimal divestment at average demandPosition of optimal divestment

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 27 / 30

Extension with variable demand

Table: Simulation results with variable demand (λ = 100%), Euro/MWh.

δ = 2GW δ = 3GW δ = 4GWc p(c) c p(c) c p(c)

Optimal 60.7 83.0 61.8 80.8 63.0 78.7Optimal avg. demand 75.9 83.6 73.8 81.4 71.6 79

Baseload 29.2 85.5 30.3 84.4 31.4 83.3

Table: Simulation results with variable demand (δ = 3GW ), Euro/MWh.

λ = 100% λ = 50% λ = 20%c p(c) c p(c) c p(c)

Optimal 61.8 80.8 88.3 89.5 100.9 95.1Optimal at avg. demand 73.8 81.4 87.0 89.6 94.9 97.4

Baseload 30.3 84.4 46.8 95.7 52.9 103.6

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 28 / 30

Conclusions

We have identi�ed the most e¤ective divestment in a model of adominant �rm with a competitive fringe

the divested capacity needs to include price-setting generation plants,which would otherwise be withheld by the dominant �rmthe optimal divestment is e¤ective because it makes the residualdemand faced by the dominant �rm more elastic, and can beseveral-fold more e¤ective than a baseload divestmentwith variable demand and high demand variance, optimal to divestcheaper capacity than the optimum at average demand (result reversedfor low demand variance)

The e¤ectiveness of VPPs is maximised when all of the options areexercised

in this case the VPP reduces prices as much as a divestment ofbaseload generation of the same sizethis implies that divestments are much more pro-competitive thanVPPs (in a one-shot setting)

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 29 / 30

Conclusions

Policy implications: remedies

the choice of divested plants makes a signi�cant di¤erence to theire¤ectiveness as a remedyif a VPP is chosen as a market-power mitigation measure, best to setlow strike prices rather than mimick the optimal divestment

Policy implications: merger control

acquisition of price-setting capacity by a �rm with market power can besigni�cantly more anti-competitive than baseload acquisition (i.e. itrelaxes a more signi�cant competitive constraint)on the other hand, a well-chosen marginal divestment can o¤set thee¤ects of a larger baseload acquisition

Results can be applied to antitrust cases in other industries withuniform pricing but increasing costs

G. Federico, A. L. López (October 2009) Divesting Power IEFE Seminar 30 / 30

Related Documents