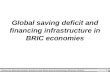

Looking Ahead 57 Source- Left Chart: “World Economic Outlook”, IMF, Apr. 2015 Source- Right Chart: Thomson Reuters DataStream Real GDP Growth (In % Y-o-Y Change, 2014 and 2015 ) Main Stock Market Indices In BRIC Countries over Time (In Index Jan. 2013=100, Jan. 2013-Jun. 2015) The BRIC economies are showing great heterogeneity. China and India are still growing (although China has slowed down), but Russia and Brazil are in recession, hurt by weak commodity and oil prices. (Brazil’s recession is expected to deepen in 2015.) Stock markets reflect the countries’ diverging fortunes, with Indian share prices gaining sharply. Meanwhile, China’s stock-market surge since 2014 has created concerns about a potential bubble BRIC ECONOMIES ARE DIVERGING, with India growing strongly, China slowing down, and Russia and Brazil struggling DIVERGING BRIC ECONOMIES 06 7.2 0.1 -3.8 -1.0 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 Russia 0.6 India 7.5 China 6.8 7.4 Brazil World (2015): 2.86 2015 2014 190 Jan-15 Jul-15 Jul-14 Jan-14 Jul-13 Jan-13 170 100 120 0 130 110 90 150 80 140 160 180 Russia (In MICEX Share Price Index) India (Bombay Stock Exchange National 100 Share Price Index) China (CSI 300 Index) Brazil (Bovespa Index)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

-

Looking Ahead 57

Source- Left Chart: “World Economic Outlook”, IMF, Apr. 2015Source- Right Chart: Thomson Reuters DataStream

Real GDP Growth (In % Y-o-Y Change, 2014 and 2015 )

Main Stock Market Indices In BRIC Countries over Time(In Index Jan. 2013=100, Jan. 2013-Jun. 2015)

The BRIC economies are showing great heterogeneity. China and India are still growing (although China has slowed down), but Russia and Brazil are in recession, hurt by weak commodity and oil prices. (Brazil’s recession is expected to deepen in 2015.) Stock markets reflect the countries’ diverging fortunes, with Indian share prices gaining sharply. Meanwhile, China’s stock-market surge since 2014 has created concerns about a potential bubble

BRIC ECONOMIES ARE DIVERGING, with India growing strongly, China slowing down, and Russia and Brazil struggling

DIVERGING BRIC ECONOMIES06

7.2

0.1

-3.8

-1.0

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

Russia

0.6

India

7.5

China

6.87.4

Brazil

World (2015): 2.86

20152014

190

Jan-15 Jul-15 Jul-14 Jan-14 Jul-13 Jan-13

170

100

120

0

130

110

90

150

80

140

160

180

Russia(In MICEX SharePrice Index)

India(Bombay StockExchange National100 Share PriceIndex)

China(CSI 300 Index)

Brazil(Bovespa Index)

LA_PublicVersion(Bleed3175)_ENG_V22.indd 57 10/28/15 1:26 PM

-

Looking Ahead 58

Source- Upper Chart: “World Economic Outlook”, IMF, Apr. 2015Source- Lower Chart: World Bank Development Indicators

Gross Fixed Capital Formation In Select Countries and Regions (In % Contribution to GDP, 1980-2013)

India’s GDP at PPP and Real GDP Growth over Time(In International $ Billion and In % Y-o-Y Growth, 1980-2020)

INDIA’S ECONOMY HAS MORE THAN DOUBLED SINCE 2005 IN TERMS OF PURCHASING POWER PARITY, though the growth has slowed in recent years

Effective policies to contain market volatility, ease inflation and improve business confidence have propelled India’s economy, boosting expected real GDP to International $8 Trillion in 2015 in PPP terms, and growth to 7.5%. Nonetheless, economic performance has come down from its peak in 2010, when growth exceeded 10%. Despite optimism in India’s financial markets, investment remains low, and significant structural reforms are still needed to improve the efficiency of local business and attract foreign resources

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0

2

4

6

8

10

12

+144%

202020182016201420122010200820062004200220001998199619941992199019881986198419821980

2015

2005

GDP at PPP (In International $ Billion) Real GDP Growth (In %)

Real GDP GrowthGDP based on PPP

10

15

20

25

30

35

40

45

50

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

OECD members

Lower MiddleIncome

India

China

LA_PublicVersion(Bleed3175)_ENG_V22.indd 58 10/28/15 1:26 PM

-

Looking Ahead 59

INDIA’S FISCAL DEFICIT IS HIGH IN COMPARISON TO EMERGING MARKETS with expenditures increasingly stretched by oil, food and fertilizer subsidies

Latest data on fiscal indicators show the Indian economy on track towards stabilization in the short term. Large cuts in capital spending enabled a 0.4% reduction in the central government deficit in 2014. Nonetheless, significant policy overhaul, including tax and subsidy reform, is needed to meet mid- to long-term goals, including reducing the central government deficit to 3% of GDP in 2016

Central Government Gross Fiscal Deficit(In Trillion Rupees and In % of GDP, 2007-2020)

Breakdown of Government Spending by Type of Expenditure(In Ten Trillion Rupees, 2007/2008-2013/2014)

Source- Upper Chart: “World Economic Outlook”, IMF, Apr. 2015Source- Lower Chart: “Indian Public Finance Statistics 2013-2014”, Indian Ministry of Finance, 2015

-7.1-7.2-7.2-7.2-7.5-8.1-8.4

-9.8

-4.4

-6.4-6.5-6.7

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

00

-12

-16

-4

-20

-8

-11.4

-12.4-13.6

-14.9

2008

-7.2-6.5

20152009

-5.6

-10.0

2014

-2.2

-6.3

2007

-8.2-7.5

2010 20162011 2012 20182013

-9.0

-16.5

2017 2019 2020

-6.9

-10.1

Estimates

In Trillion Rupees In % of GDP

Gross Fiscal Deficit Share of GDP

2.0

1.5

1.0

0.5

0.0 5%6%

6%4%

45%

13%

21%

3%5%

1.0

0.8

2013/20142011/20122009/20102007/2008

1.21.3

1.9

1.4

4%

43%

13%

22%

0.7

3%4%

5%4%

54%

11%

20%

7%5%

6%5%

4%

50%

13%

20%1%6%6%4%

48%

14%

21%0%9%5%

49%

14%

23%0%5%5%

51%

14%

25%

Defence

Interest Petroleum SubsidyFood Subsidy

Fertilizer subsidyStatutory State Grants, Loans and Advances

Other Developmental & Non-Developmental

LA_PublicVersion(Bleed3175)_ENG_V22.indd 59 10/28/15 1:26 PM

-

Looking Ahead 60

Note: (1) Year represents India’s fiscal year (April 1 - March 31)Source- Upper Left Chart: IMF DatamapperSource- Upper Right Chart: Thompson Reuters DataStreamSources- Lower Chart: IMF Datamapper; “India: Country Report No. 15/61”, IMF, 2015

Current Account Deficit and Gold Imports over Time(1)(In % of GDP and In US$ Billion, 2004-2019)

India’s inflation rate dropped 4 percentage points to 6% in 2014, largely due to successful steps by the Reserve Bank of India to tighten monetary policy and falling energy prices. While policy changes have had a stabilizing effect on the economy and on exchange rates, forecasted inflation rates remain above the RBI’s inflation target for 2016. The exchange rate has stabilized since the Rupee’s depreciation in 2013. The current account deficit has narrowed dramatically as a result of the government’s successful efforts to curb gold imports

INFLATION RATES ARE AT THEIR LOWEST LEVELS SINCE 2007, THE RUPEE HAS STABILIZED AND EXTERNAL VULNERABILITIES HAVE DIMINISHED

Annual Inflation(In % Y-o-Y Change, 2005-2020)

US$ Value of 100 Indian Rupees over Time(In US$, Apr. 2005 - Apr. 2015)

4

5

6

7

8

9

10

11

2004 2006 2008 2010 2012 2014 2016 2018 20201.4

1.6

1.8

2.0

2.2

2.4

2.6

Apr-07

Apr-14

Apr-12

Apr-05

Apr-10

Forecast

0

1

2

3

4

5

6

201620092006 2018201520102007 2013 20192008 2011 20142004 201720122005

Government of India imposes restrictionon gold imports

Government of India easesrestriction on gold imports

Gold Imports projected toremain below 2013 peak rates

Current Account Deficit(In % of GDP)

Gold Imports(In US$ Billion)

0

1

2

3

4

5

6

Gold Imports Current Account Deficit

LA_PublicVersion(Bleed3175)_ENG_V22.indd 60 10/28/15 1:26 PM

-

Looking Ahead 61

India’s Corporate Sector Financing Sources(In % of GDP, Four Quarter Moving Average, Q1 2007 - Q3 2014)

Note: (1) 2014 data for South Africa through Q2 onlySource- Upper Chart: “India Article IV Consultation Staff Report”, IMF, Mar. 2015Sources- Lower Left Chart: IMF Financial Soundness Indicators; “China Bank Bad-Load Ratio Jumps Most in At Least a Decade”, Bloomberg, 2015Source- Lower Right Chart: “India Article IV Consultation Staff Report”, IMF, Mar. 2015

Public banks still provide the largest share of credit to the market (private banks have about a quarter of banking assets). However, public banks are also highly exposed to the weakened corporate sector, which has caused their asset quality to deteriorate. This exposure remains a key vulnerability for public sector banks, and the percentage of non-performing loans is up 8% since 2013 and 63% since 2011. Going forward, capital markets could potentially meet more of the country’s financing needs

CREDIT GROWTH HAS BEEN ANEMIC IN INDIA, with public banks having a high incidence of non-performing loans, which has weakened their balance sheets and restricted their ability to extend credit

Gross Non-Performing Loans (NPLs)(In % of Outstanding Loans, 2011-2014)

Comparison of Non-Performing Loan Rates Across Key Emerging Markets(In % of Total Loans, 2011, 2012, 2013 and 2014(1))

0

2

4

6

8

10

12

14

16

18

20

22

20142013201220112010200920082007

Capital Markets Listed Equity Domestic Bank CreditExternal Commercial Borrowing Capital Markets Borrowing

4.68

3.47

2.14

0.96

4.04

3.45

1.77

4.03

3.50

2.85

2.07

1.64

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

-25%+63%

-18%

-3%

South Africa

3.64

India

4.35

3.37

2.67

Brazil

1.69

+71%

Indonesia

1.00

2.86

0.95

China

5

4

3

2

222

2

22

3

4

3

33

2013/142012/132011/122010/11

Foreign Banks

New Private Sector Banks

Old Private Sector Banks

Public Sector Banks 2014201320122011

LA_PublicVersion(Bleed3175)_ENG_V22.indd 61 10/28/15 1:26 PM

-

Looking Ahead 62

India Reaches Current Chinese LevelsIndia - Current Levels (2015 or Most Recent)China - Current Levels (2015 or Most Recent)

45

44

16.2

23

66

75

825

3.3

36

49.5

12.7

6.2

19

11.9

207

1.7Fertility Rates(Number of Births per Woman, 2012)

Tertiary Education (In % Enrollment, 2012)

Passenger Cars(In Number Cars per 1,000 people, 2010)

GDP per Capita (In Thousands,International $ at 2011 Prices, 2013)

GDP (In International $ Trillion at 2011Prices, 2013)

Population in Cities over 1 Million (In % of Total Population, 2013)

Middle Income Population(In % of People on $2-4/day, 2010)

Life Expectancy(In Average age of Mortality, 2012)

Patent Applications(In Number of Applications per Year, 2013)

Electrical Power per Capita(In kWh per Capita, 2011)

Median Age(In Year, 2015)

Urbanization (In % Population livingin Urban Areas, 2015)

Mortality Under 5 Years(In Number of Deaths per 1,000 Births, 2013)

Patents Granted(In Number of Patents, 2013)

CO2 Emissions per Capita(In Metric Tons per Capita, 2010)

Internet Penetration (In % Population, 2013)

30 25 20 15 10 5 0 +5 +10 +15 +20 +25 +30

27

Years Since China was at Indian Levels Additional Years Required for India to Reach CurrentChinese Levels

25

15

12

14

11.9

5.4

31

66

43

0.7

27

32.3

52.7

3

2.5

1.6

Poverty (In % of People Living onless than $2/day, 2012)

59

Sources: “World Economic Outlook”, IMF, Apr. 2015; World Bank Development Indicators; UN Data; World Population Prospects 2012 Revision; World Bank PovCal; WIPO Statistics Database; “The World in 2050”, PWC, 2015

Socioeconomic Development Metrics: China vs. India on Various Indicators

India remains years, and in some cases decades, behind China in terms of key social and economic development indicators. Analysis of past and projected future growth rates suggests that India will take longer than China did to reach China’s state of development in many of these areas. In the case of GDP per capita, poverty rates and passenger car penetration, India is likely to advance at less than half China’s pace

DESPITE TREMENDOUS SOCIOECONOMIC GAINS, INDIA REMAINS FAR BEHIND CHINA ON MANY METRICS, and is unlikely to catch up any time soon

LA_PublicVersion(Bleed3175)_ENG_V22.indd 62 10/28/15 1:26 PM

-

Looking Ahead 63

India AheadPrior to 1980

X China’s value in 2030 (according to indicatormetric); Remains ahead of India post-2030 India value in 1980 (according to indicator metric);Ahead of China prior to 1980 and remains ahead

China AheadPost-2030

25

24

16

39

35

X India value at time of surpassing China(according to indicator metric)

2020 1990 1980 2030

68

1.5

48

GDP per Capita(In 2014 International $

Thousand)

Elderly Dependency Ratio(In % Ratio of Total

Population over 65 Years to Working Age Population)

Elderly Population(In % of Total

Population over 65 Years)

Working Age Population(In % of Total Population

15-64 Years)

Total Population(In Billions of People)

Gender Gap(In % Females out of

Total Population)

Youth Dependency Ratio(In % Ratio of Total

Population over 65 Years to Working Age Population)

Youth Population(In % of Total Population

0-14 Years)

Sources: “The World in 2050”, PWC, 2015; World Bank Development Indicators; UN Data; “Society at a Glace: Asia/Pacific 2014”, OECD, 2014

India Surpasses China on Various Indicators - Past and Projected

In the coming decades, India is expected to have a bigger total population than China and a bigger working age population, less gender imbalance and a lower old age dependency ratio. All of these things could become sources of competitive advantage for India. However, China will continue to be the top performer in terms of gross economic output for the foreseeable future, with a GDP nearly 50% higher than India’s in 2030

HOWEVER, INDIA HAS OVERTAKEN AND WILL OVERTAKE CHINA ON KEY DEMOGRAPHIC INDICATORS, giving it some economic advantages

LA_PublicVersion(Bleed3175)_ENG_V22.indd 63 10/28/15 1:26 PM

-

Looking Ahead 64

2

4

6

8

10

12

14

16

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

India

China

Indian growth surpassesChinese growth

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

75

70

65

60

0

India

China

9,826

17,180

XX GDP per Capita at Peak of Ratio of Working Age Population to Total Population(In Constant 2014 International $)

Note: (1) The turning point refers to the time when the working age population starts decreasingSource- Upper Chart: “World Economic Outlook”, IMF, Apr. 2015Sources- Lower Chart: UN Data; World Bank Development Indicators; “The World in 2050”, PWC, 2015

Working Age Population as a Share of Total Population(In % of People Aged 15-64 out of Total Population, 1950-2100)

Indian and Chinese Growth in Real GDP(In % Y-o-Y Growth of Real GDP, 2005-2020)

The coming decades will see increasing economic competition between India and China as China’s maturing economy continues to slow relative to growth rates witnessed in the 1990s and in the first decade of the 21st century. Driven by a youthful population and an emerging educated middle class, India is expected to exceed Chinese growth starting in 2015, although the difference in the two countries’ growth rates will remain within 1.5 percentage points through the end of the decade. India’s working age population as a share of the total is projected to peak at nearly double the GDP per capita witnessed in China, potentially boosting the country into a higher income class over the long term

INDIA IS FORECAST TO GROW FASTER THAN CHINA STARTING IN 2015 and is likely to reach its labor market turning point(1) at a much higher GDP per capita than China

LA_PublicVersion(Bleed3175)_ENG_V22.indd 64 10/28/15 1:26 PM

-

Looking Ahead 65

2,030

2,3532,3912,412

2,613

1,396

559560

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

-2

-1

0

1

2

3

4

5

6

7

8

20112010

2,209

2009

1,667

200820072006 20142005

892

200420032002

511

20012000

657

2016

1,928

2015

1,904

20132012

1,108

20202019

2,241

20182017

Forecast

Real GDP Growth Nominal GDP

670

1,695

2,132

2,354

Nominal GDP Real GDP Growth

Forecast

0.00

0.28

0.30

0.32

0.34

0.26

0.38

0.40

Ratio of Brazil to US GDP per CapitaBrazil's GDP per Capita at PPP

0.36

1980 1985 1990 1995 2000 2005 2010 2015 2020

0

5,000

10,000

15,000

20,000

Brazil's GDP per Capita at PPP Gap with US GDP per Capita

Source- Upper and Lower Charts: “World Economic Outlook”, IMF, Apr. 2015

Total Nominal GDP and Real GDP Growth over Time(In Current US$ Billion and In % Y-o-Y Growth, 2000-2020)

Brazil’s GDP per capita at PPP and Standards of Living Relative to the US over Time(In International $ and In Ratio of Brazilian GDP per capita to US GDP per capita, 1980-2020)

Brazil’s GDP grew by more than 9% a year from 2000 to 2014, earning Brazil a place among the world’s largest economies. However, in recent years this growth has slowed down because of supply constraints, lack of productivity growth, corruption scandals and low investment. Moreover, the drop in commodity prices has negatively affected Brazil’s growth prospects. While Brazil’s GDP per capita measured in international dollars has risen, the gap with US GDP per capita has widened, indicating a drop in relative standards of living (especially when compared to 1980)

BRAZIL’S PACE OF ECONOMIC GROWTH HAS SLOWED IN RECENT YEARS although it is expected to pick up slightly by 2020. Meanwhile, the discrepancy with US income standards is likely to expand

LA_PublicVersion(Bleed3175)_ENG_V22.indd 65 10/28/15 1:26 PM

-

Looking Ahead 66

2014

132.2

9%

2013

114.3

2012

96.08%

2011

82.8

12%

2014

298.7

2013

321.4

2012

331.6

2011

319.9

4%7%

21%

3% 5%

Other

International

US$ 2.1Billion

Non - Current DebtCurrent Debt

91%

88%92%

93%

7%

3%

Gas and Power

Refining, Transportationand Marketing

Exploration and Production

-7%

-23%

48.1

37.0

65%

30%

2013 2014

6%

US$ 17Billion

57%

Source- Upper Left Chart: “World Economic Outlook”, IMF, Apr. 2015Source- Upper Right Chart: “Brazil Article IV Consultation Staff Report”, IMF, 2013Sources- Lower Chart: “Doing Business”, World Bank, 2015; “Global Competitiveness Report”, WEF, 2014

Rankings in Business Friendliness and Infrastructure Quality(In Rank, 2015, and 2014-2015)

Brazil’s fiscal balances have been suffering from a high deficit, but fiscal consolidation is forecasted in the coming years. However, with most expenditures being directed to social benefits, the level of capital investment will still fall short of what’s needed. This will perpetuate the problem of low infrastructure quality in Brazil. Brazil’s lack of competitiveness also stems from its bureaucracy, red tape, and unfriendly business environment as measured by the World Bank’s Doing Business index

HIGH DEFICIT, UNDERINVESTMENT AND SUPPLY CONSTRAINTS HAVE CONTRIBUTED TO SLOW GROWTH, as have low levels of competitiveness

Government Budget Balance over Time(In % of GDP, 2006-2020)

Government Expenditure Breakdown by Type(In Brazilian Real Billion, 2009-2018)

Forecast Forecast

3

5

55 6 5 5 5 5 5 5

7

77

7 7 77 7 7 7

4

44

4 4 44 4 4 4

5

44

4 4 44 4 4 4

1111111

2018

21

2017

21

2016

21

1

2015

21

1

2009

21

2014

22

2013

22

2012

23

2011

22

2010

23

3.03.5

4.2

5.3

6.2

3.1

2.5

3.22.7

3.6

2020

2.6

20182016

4.7

2014

2.7

2008

1.5

2012

2.6

2010

Other

Personnel

Transfers

Pension Benefits

Capital Expenditures

0

-1

-2

-3

-4

-5

-6

-7

2006

Switzerland Hong Kong

Singapore Singapore

US UAE

Russia Cyprus Brazil

China

South Africa

Brazil Sri Lanka

Brazil

Brazil Hungary

Vietnam

India

Morocco India

WEFCompetitiveness

InfrastructureQuality

WEF Competitiveness

BusinessConfidence

WEFCompetitiveness

World Bank’sDoing Business

Singapore

New Zealand

Hong Kong

China

Egypt

Nicaragua

Pakistan

Iran

1

2

3

90

112

119

120

72

71

60

128

130

57

1

2

3

56

54

87

81

76

47

75

1

2

3

45

46

92

91

63

51

50

3

2

1

Turkey

Portugal

Poland

Kazakhstan

Hungary

Germany

Switzerland

Japan

LA_PublicVersion(Bleed3175)_ENG_V22.indd 66 10/28/15 1:26 PM

-

2014

132.2

9%

2013

114.3

2012

96.08%

2011

82.8

12%

2014

298.7

2013

321.4

2012

331.6

2011

319.9

4%7%

21%

3% 5%

Other

International

US$ 2.1Billion

Non - Current DebtCurrent Debt

91%

88%92%

93%

7%

3%

Gas and Power

Refining, Transportationand Marketing

Exploration and Production

-7%

-23%

48.1

37.0

65%

30%

2013 2014

6%

US$ 17Billion

57%

Source- Upper Chart: Transparency InternationalSources- Lower Charts: Petrobras Financial Statements; “Corruption Scandal Will Cost Petrobras at Least US$ 2.1 Billion”, Nasdaq, Apr. 2015; “Petrobras Write-down May

Give New Ammunition to Class-Action Suit”, Reuters, Apr. 2015

Corruption in Brazil and Comparative Countries(In Corruption Perception Index Rank, 2014)

In 2015, it was revealed that Brazil, which already ranks low on the corruption index, had suffered a corruption scandal costing the government 5.7 Billion Real over the last 10 years. The Petrobras scandal has had major implications on the company’s operations forcing major asset writedowns and a decrease in its investments. The scandal also had implications on other sectors that are highly tied to it costing the Brazilian economy an estimated US$ 27.1 Billion. Even before the drop in oil prices and the revelation of extensive graft, Petrobras was the world’s most indebted oil company

CORRUPTION HAS DETRACTED FROM GROWTH, with the Petrobras scandal, the biggest in Brazil’s history, costing the country an estimated 1% of GDP

7170696866

4443

321

GreeceBulgariaBrazilSouth AfricaTurkeyLatviaSouth KoreaFinlandNew ZealandDenmark

PETROBRAS AFFECTED METRICS: High Debt, Write-down of Assets, and Drop in Investment

Petrobras Consolidated Debt(In US$ Billion, 2011-2014)

Petrobras Total Assets(In US$ Billion, 2011-2014)

Petrobras Total CAPEX and Investments(In US$ Billion, 2013 and 2014)

Petrobras Loss Due to Corruption

Assets Write-Downs

Looking Ahead 67

LA_PublicVersion(Bleed3175)_ENG_V22.indd 67 10/28/15 1:26 PM

-

Looking Ahead 68

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20150.0

8.5

8.0

7.5

7.0

6.5

6.0

5.5

5.0

4.5

4.0

3.5

13.0

12.5

12.0

11.5

11.0

10.5

10.0

9.5

9.0

8.5

8.0

7.5

0.0

Jan 15Jan 14Jan 13Jan 12

2.8

3.0

3.2

2.2

0.0

2.4

1.8

2.6

2.0

Jul 14 Jan 15

3.13

Jul12 Jan 13 Jul 13 Jan 14Jan 12

Source- Upper Chart: “World Economic Outlook”, IMF, Apr. 2015Sources- Lower Charts: Thompson Reuters DataStream; “International Financial Statistics Yearbook”, IMF, 2014

Inflation Rate(In %, 2005-2015)

Inflation in Brazil rose to 7.7% recently--the highest level in a decade. In response—and to cool the economy--policymakers raised the interest rate to 12.75%. However, the tight monetary policy dampens growth and runs the risk of pushing Brazil deeper into stagflation. Meantime, US monetary policy and potential rising rates have led to major capital outflows and to a depreciation of the Brazilian real. While depreciation should boost Brazil’s exports and thus its competitiveness in the long term, the speed of recent currency declines could also have negative effects

BRAZIL’S ECONOMY IS GOING INTO “STAGFLATION” WITH HIGH INFLATION COINCIDING WITH LOW GROWTH and capital outflows and depreciating currency adding to the economic woes

Exchange Rate Against US Dollar(In BRL/US$, Jan. 2012 - Jan. 2015)

Interest Rates(In %, Jan. 2012 - Jan. 2015)

LA_PublicVersion(Bleed3175)_ENG_V22.indd 68 10/28/15 1:26 PM

-

Looking Ahead 69

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20150.0

8.5

8.0

7.5

7.0

6.5

6.0

5.5

5.0

4.5

4.0

3.5

4

6

8

10

-8

-6

-4

-2

0

2

100

110

90

80

70

60

50

40

30

0

10

20

20202010200920082007 20152014201320122011 2017 2018 20192016

Nominal GDP

Nominal GDP (In Ruble Trillion)

Real GDP Growth Rate

(In % Y-o-Y Change)

Real GDP Growth Rate

Estimates

105

100

95

85

80

75

90

60

110

115

May05

May06

May07

May08

May09

May10

May11

May12

May13

May14

Feb15

-140

-120

-100

-80

-60

-40

-20

0

20

40

Q1 Q1 Q1 Q1 Q1 Q1 Q1 Q1

2008 2009 2010 2011 2012 2013 2014 2015

Source- Upper Chart: “World Economic Outlook”, IMF, Apr. 2015Source- Lower Left Chart: Central Bank of RussiaSources- Lower Right Chart: Thomson Reuters Datastream; Business Insider

Russian Nominal GDP and GDP Growth over Time(In Ruble Trillion and In Y-o-Y % Change, 2007-2020)

Falling oil prices and the crisis in Ukraine have had a damaging effect on Russia’s economy, lowering growth rates that had already been slowing since peaking at 10% in 2000. Real GDP growth is estimated to dip as low as ~3.8% in 2015 before returning to positive territory in 2017. Capital flight more than doubled in 2014 to US$ 151.5 Billion, with more than US$ 79 Billion lost in the fourth quarter alone, more than quadruple the value lost during the same quarter in 2013. Although the Russian ruble showed some signs of rebounding in early 2015, the ruble’s real effective exchange rate was at only 70% of its average rate in 2014

RUSSIA’S ECONOMY IS PROJECTED TO CONTINUE TO CONTRACT, being highly affected by outflow of capital and a depreciating currency

Capital Outflows(In US$ Billion, Q1 2008 - Q2 2015)

Real Effective Exchange Rate of Russian Ruble over Time(In REER Index 2010=100, May. 2005 - Feb. 2015)

LA_PublicVersion(Bleed3175)_ENG_V22.indd 69 10/28/15 1:26 PM

-

Looking Ahead 70

26242220181614121086420

12

56

54

52

50

48

46

44

14

10

8

6

4

2

07674727034323028

Latvia

Spain

Czech Republic

Kazakhstan

Ukraine

US

Japan

Turkey

Italy

Belarus

Poland

South Korea

Netherlands

Germany

China

UK

Finland

France

Belgium

Switzerland

Latvia

Imports From Russia

Sanctions

No Sanctions

No Sanctions - Negative Growth

Size Represents Real GDP Growth(In % Change Y-o-Y, 2015)

World3.5%

Exp

orts

to R

ussi

a

Sources: UNCTAD; IMF Datamapper

Top Russian Trading Partners(In US$ Billion of Aggregate Absolute Values of Imports and Exports, 2014)

Russia is burdened by sanctions and slow growth in top export markets, contributing further to the negative outlook for the country’s economy. Of the country’s top 15 trade partners, only China will see growth above the projected 2015 global average of 3.5%. Ten of these trading partners have imposed sanctions, cutting off important import and export markets for Russia. Sanctions are estimated to have cost Russia US$ 26.7 Billion in 2014 and the impact in 2015 may be two or three times that amount, according to economists’ forecasts

RUSSIA’S ECONOMIC DOWNTURN HAS BEEN DEEPENED BY SANCTIONS AND BY A SLOWDOWN IN THE GROWTH OF ITS MAJOR TRADE PARTNERS

LA_PublicVersion(Bleed3175)_ENG_V22.indd 70 10/28/15 1:26 PM

-

Looking Ahead 71

17%

Germany

18%

82%

ChinaBelarus

92%

Italy

26%

74%

Netherlands

29%

71%

Russia

Other

Latvia

28%

72%

99%

1%

Finland

68%

32%

UK

8%

92%

South Korea

8% 4%

96%

Japan

7%

93%

Poland

83%

Origin ofCountryPetroleumand NaturalGas Imports

RussianDependency

ImporterDependency

Top Destinations = 66% of Russian Petroleum and Natural Gas Exports

Note: (1) Values represent aggregate of five UNCTAD product groups: 333, 334, 335, 343 and 344 Source- Upper Chart: UNCTADSources- Lower Left Chart: Wall Street Journal; “Russia’s Restrictions on Imports”, FAO, 2014Source- Lower Right Chart: Federal State Statistics Service, Russia

To date, sanctions have stopped short of bans on natural gas and petroleum exports. With nearly one-third of EU oil and gas imports coming from Russia, any steps to significantly cut trade flows would hurt economies on both sides. Russia has made efforts to leverage economic influence by imposing retaliatory sanctions on agricultural imports. While these sanctions have caused some strain in European and American markets, they have also hurt Russia’s domestic economy, contributing to food price increases of 15% in 2014 and more in 2015

RETALIATORY RUSSIAN SANCTIONS ARE HAVING AN IMPACT ON SOME EUROPEAN ECONOMIES, but are also causing domestic inflation

Dependency of Top Export Destinations for Russian Petroleum and Natural Gas Exports(1)(Width=In % of Russian Petroleum Exports, 2013 and Height=In % of Russian Imports as a Share of Total Country Imports, 2013)

Exporting Countries Affected by Russian Agricultural Sanctions over US$ 100 Million(In US$ Million, 2013)

Russia’s Food Inflation(In % Y-o-Y, May 2014 - Apr. 2015)

0 200 400 600 800 1,000 1,200

France

Lithuania

Denmark

US

Spain

Finland

Canada

Germany

Netherlands

Poland

Norway

Poultry

Vegetables

Fruits

Milk and Milk Products

Pork

Fish and Seafood

0

5

10

15

20

25

30

Apr-15

Mar-15

Feb-15

Jan-15

Dec-14

Nov-14

Oct-14

Sep-14

Aug-14

Jul-14

May14

Jun-14

LA_PublicVersion(Bleed3175)_ENG_V22.indd 71 10/28/15 1:26 PM

Related Documents