/ ^ ^ District Attorney of the TWenty-Slxth Judicial District Parlshos of Bossier and Webster, Louisiana Financial Statements With Auditor's Report As of and for the Year Ended Decemt»er 31,2012 Under provisions of state law. tliis report is a public document. Acopy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the parish clerk of court. Release Date NOV 2 7 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

/ ^ ^

District Attorney of the TWenty-Slxth Judicial District Parlshos of Bossier and Webster, Louisiana

Financial Statements With Auditor's Report

As of and for the Year Ended Decemt»er 31,2012

Under provisions of state law. tliis report is a public document. Acopy of the report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the parish clerk of court.

Release Date NOV 2 7 2013

District Attorney of the Twenty-Sixth Judicial District Parishes of Bossier and Webster, Louisiana

Table of Contents

Page

Independent Auditors' Report

Required Supplementary Information

Management's Discussion and Analysis

Basic Financial Statements:

Government-wide Financial Statements

Statement of Net Position

Statement of Activities

Fund Financial Statements

Balance Sheet - Govemnriental Funds

Statement of Revenues, Expenditures, and Changes in Fund Balances - Governmental Funds

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities

Statement of Fiduciary Net Position

Notes to the Financial Statements

Required Supplementaiy Information

Budgetary Comparison Schedule - General Fund

Budgetary Comparison Schedule - Drug Court and Truancy Fund

Note to Required Supplementary Information

Schedule of Funding Progress for Retiree Health, Dental, and Ufe Plans Report on Internal Control over Financial Repoiting and on Compliance

and Other Matters Based on an Audit of Financial Statements Performed In Accordance With Government Auditing Standanis

Schedules For Louisiana Legislative Auditor

Summary Schedule of Prior Year Audit Findings

Current Year Audit Findings

1 -2

3 - 7

10

11

12

13

14-28

29

30

31

32

33-34

35

35

COOK & MOREHART

Cerdfkd PuhUc Aceountaaa

IlliC HAWN AVENUE " S H S E V e T O R T . LOUISIANA 71107 •> P.O. BOX ^ 2 4 0 • SHRCVEPOflT, LOUISIANA T | U 7 . « 2 4 0

TRAVISH MOREBART.CTA T E L E P H O N E (318) 212-5415 PAX P W M 2 - 5 4 4 I

A EDWASPfiALLCPA VICKIE D CASE. CrA

AMERICAN W n r t U T E STUAETL. REKW.CPA CERTIFIEDFUBUC ACCOUHTANTS

SOCIETY OP LOUISIANA CERTIFIED PUBUC ACOOUNTAJITS

Mepgndent Auditors'Report

District Attorney of the Twenty-Sixth Judicial District Parishes of Bossier and Wet>ster, Louisiana

Report on the Rnanclal Statements

We have audited the accompanying basic finandai statements of the governmental activities, each major fund, and the aggregate remaining fund infomiation of the District Attorney of the Twenty-Sixth Judicial District, a component unit of the Bossier Parish Police Jury, as of and for the year ended Decemt)er 3 1 . 2012. and the related notes to the financial statements, which collectively comprise the District Attorney of the Twenty-Sixth Judicial Districts basic finanaal statements as listed in the table of contents.

Management's Resp<m^baity for the Finandai Statements

IManagement is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of Internal control relevant to the preparatfon and fair presentation of financial statements that are free from notorial misstatement whether due to fraud or enor.

Auditors ' Responsibil ity

Our responsibility is to express opinions on these financial statements based on our audit We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are fi-ee from matertar misstatement

An audit involves perfomning procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's Judgment including the aS5essn>ent of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor conskiers internal control relevant to the entity's prsparatton and fair presentatk}n of the financial statements in order to design audit procedures that are appropriate in the circurmtances. but not tor the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opink>n. An audit also includes evaluating the approprateness of accounting policies used and the reasonableness of s ^ i f k ^ n t accounting estbnates made by nranagement as welt as evaluating the overall presentatton of 0ie financial statements.

We believe that the audit evkJence we have obtained is sufficient and approprfate to provkto a basis for our audit opinions.

opinions

In our opinion, the financial statements refen^d to above present fairty, In all material respects, the financial position of the governmental activities, each major fund, and the aggregate remaining fund infomiatton of the District Attorney of the T w e n t ^ i x t h Judicial District as of December 31 , 2012. and the respective changes in financial positton thereof for ttie year then ended in accordance with accounting principles generally accepted in ttie United States of America.

Other Matters

Required Supf^ementary Infdnnation

Accounting principles generally accepted in the United States of America require that the management's discussion and analysis, budgetary comparison intormatlon, and the schedule of funding progress for retiree health, dental, and life plans on pages 3 - 7, 29 - 31, and page 32 be presented to supplement the basic financial statements. Such infonnatton. although not a part of the basic financial staten:>ents, is required by the Governmental Accounting Standards Board, who conskters it to be an essential part of financial reporting tor placing the t^ask: financial statements in an appropriate operattonal, economk:. or historical context We have applied certain limited procedures to the required supplementary infbrmatbn in accordance with auditing standards generally accepted in the United States of America, which consisted of Inquires of ntanagentent about the methods of preparing the infbrmatton and comparing the infonnatton for consistency with management's responses to our inquires, the baste finandai statements, and other knowledge we obtained during our audit of the basto financial statements. We do not express an opinton or provMe any assurance on the infonnatton because the limited procedures do not provkle us with suffteient evkjence to express an opinton or provkie any assurance.

Other Reporting Required by Government Audit ing Standards

In accordance with Govsmmenf Auditing Standards, we have ateo issued a report dated July 12. 2013. on our consideration of the District Attorney of the Twenty-^xth Judteial District's internal control over financial reporting and our tests of its compliance with certain provisions of laws, regulattons. contracts and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of intemal control over finandai reporting and compliance and the results of that testing, and not to provkie an opinion on the intemal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the District Attorney of the TVventy-Sixth Judicial Districfs intemal control over financial reporting and compliance.

Cook & Vlorehart Certified Publte Accountants July 12.2013

MANAGEMENT'S DISCUSSION AND ANALYSIS

Our discussion and analysis of the District Attorney of the Twenty-Sixth Judicial District's financial performance provides an overview of the District Attorney's financial activities for the fiscal year ended December 31, 2012. Please read it in conjunction with the District Attorney's financial statements, which begin on page 8.

FINANCUL HIGHUGHTS

The Disti-ict Attorney's net position increased by $143,108.

The District Attorney's total general and program revenues were $3,140,964 in 2012 compared to $2,550,267 in2011.

During the year ended December 31, 2012, the District Attorney had total expenses, exchiding depreciation and net OPEB obligation of $2,764,498, compared to total expenses, excluding depreciation and net OPEB obligation of $2,865,743 fen- the year ended December 31,2011.

USING THIS ANNUAL REPORT

This annual report consists of a series of financial statements. The Statement of Net Position and the Statement of Activities (on pages 8 and 9) provide information about the activities of the District Attorney of the Twcn^Sixth Judicial District as a whole and present a ](mger-term view of the District Attorney's finances. Fund financial statements start on page 10. For governmental activities, these statements tell how these services were fmanced In the short term as well as what remains for future spending. Fund fmancial statements also report die District Attorney's operations in more detail than die govemment-^wide statements by providing information a(>out the District Attorney's most significant funds.

The District Attorney of the Twenty-Sixth Judicial District was determined to be a component unit of the Bossier Parish Police Jury. The District Attorney is fiscally dependent on the Police Jury for space and related costs. The accompanying financial statements present information only on the funds maintained by the District Attorney of the Twenty-Sixth Judicial District.

Reporting the District Attorney of the Twenty-Slxfli Judicial District as a Whole

Our analysis of the District Attorney of die Twenty-Sixth Judicial District as a whole begins on page 8. One of the most important questions asked about the District Attorney's finances is ''Is the District Attorney as a whole better off or worse off as a result of the year's activities?" The Statement of Net Position and the Statement of Activities report information about the funds maintained by the District Attorney of the Twenty-Sbcth Judicial District as a whole and about its activities in a way that helps answer this question. These statements include all assets and liabilities using the accrual basis of accounting, which is similar to the accounting used by most private^sector companies. Accrual of the current year's revenues and expenses are taken into account regardless of when cash is received or paid.

These two statements report the District Attorney's neS position and changes in it You can think of the District Attorney's net position - the difference between assets and liabilities - as one way to measure the District Attorney's financial health, or financial position. Over time, increases or decreases in the District Attorney's net position is one indicator of whether its financial healtit is improving or deteriorating. You will need to consider other non-financial factors, however, to assess the overall health of the District Attorney.

In the Statement of Net Position and the Statement of Activities, we record the funds maintained by the District Attorney as governmental activities.

Governmental activities - all of the expenses paid from the funds maintained by the District Attorney are reported here which consists primarily of personal services, materials and supplies, travel, repairs and maintenance and other program services. Fines and fees, state and federal grants and gaming tax revenue fmance most of these activities.

ReportiDg the District Attorney's Most Significant Funds

Our analysis of the major funds maintained by the District Attorney of tiie Twenty-Sixth Judicial District begins on page 10. The fund financial statements begin on page 10 and provide d ^ l e d information about the most significant funds maintained by the District Attorney - not the District Attorney as a whole. The District Attorney of the Twenty-Sbcth Judicial District's governmental fimds use tfte following accounting approaches:

Governmental fiinds - All of the District Attorney's basic services are reported in governmental funds, which focus on how money flows into and out of those funds and the balances left at year-end that are available for spending. These fimds are reported using an accounting method called modified accrual accounting, which measures cash and all other financial assets that can readily be converted to cash. The governmental fiind statements provide a detailed shorl-^rm view of the District Attorney's general government operations and the expenses paid from those fimds. Governmental fund information helps you detennine whether there are more or fewer financial resources that can be spent in the near future to finance certain District Attorney expenses. We describe the relationship (or differences) between governmental activities (reported in the Statement of Net Position and the Statement of Activities) and governmental fimds in a reconciliation at the bottom of the fund financial statements.

THE DISTRICT ATTORNEY OF THE TWENTY-SIXTH JUDICIAL DISTRICT AS A WHOLE

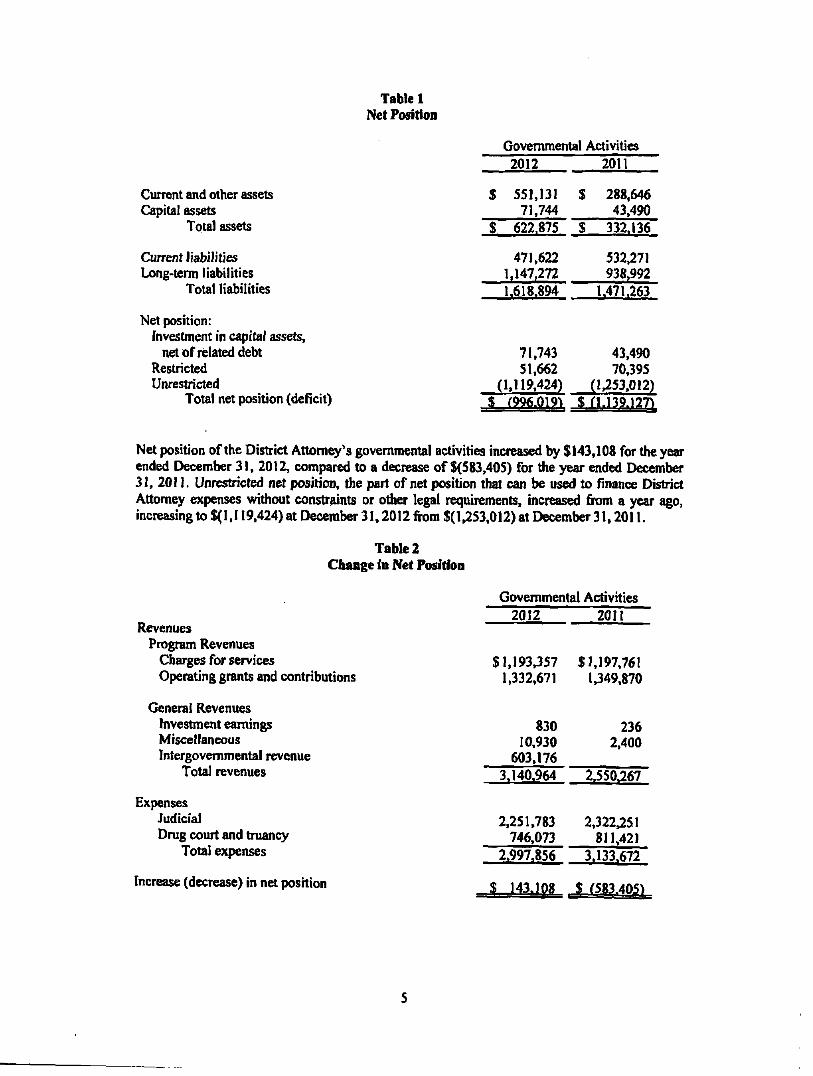

The District Attorney of the Twenty-Sixth Judicial District's total net position changed from a year ago, increasing from $(1,139,127) to (996,019).

Current and other assets Capital assets

Total assets

Current liabilities Long-term liabilities

Total liabilities

Net position: InvesUnent in capital assets,

net of related debt Restricted Unrestricted

Total net position (deficit)

Table 1 Net Position

Governmental Activities 2012

$ 551.131 71,744

$ 622,875

71.743 51,662

(1.119,424)

2011

$ 288,646 43.490

$ 332.136

532,271 938,992

1.471,263

43,490 70,395

(1,253.012)

Net position of the District Attom^'s governmental activities increased by $143,108 for the year ended December 31, 2012, compared to a decrease of $(583,405) for the year ended December 31, 20 n , Unrestricted net position, the part of net position that can be used to finance District Attorney expenses without constraints or otlier legal requirements, increased from a year ago, increasing to $(1.119,424) at December 31.2012 from $(1,253,012) at December 31,2011.

Table 2 Change in Net Position

Governmental Activities

Revenues Program Revenues

Charges for services Operating grants and contributions

General Revenues Investment earnings Miscellaneous Intergovernmental revenue

Total revenues

Expenses Judicial Drug court and truancy

Total expenses

Increase (decrease) in net position

2012 2011

$1,193,357 $1,197,761 1,332,671 1,349,870

830 10,930

603,176 3,140,964

2,251,783 746,073

2,997,856

$ 143,108

236 2,400

2,550^67

2,322.251 811,421

3.133.672

$ (583.405^

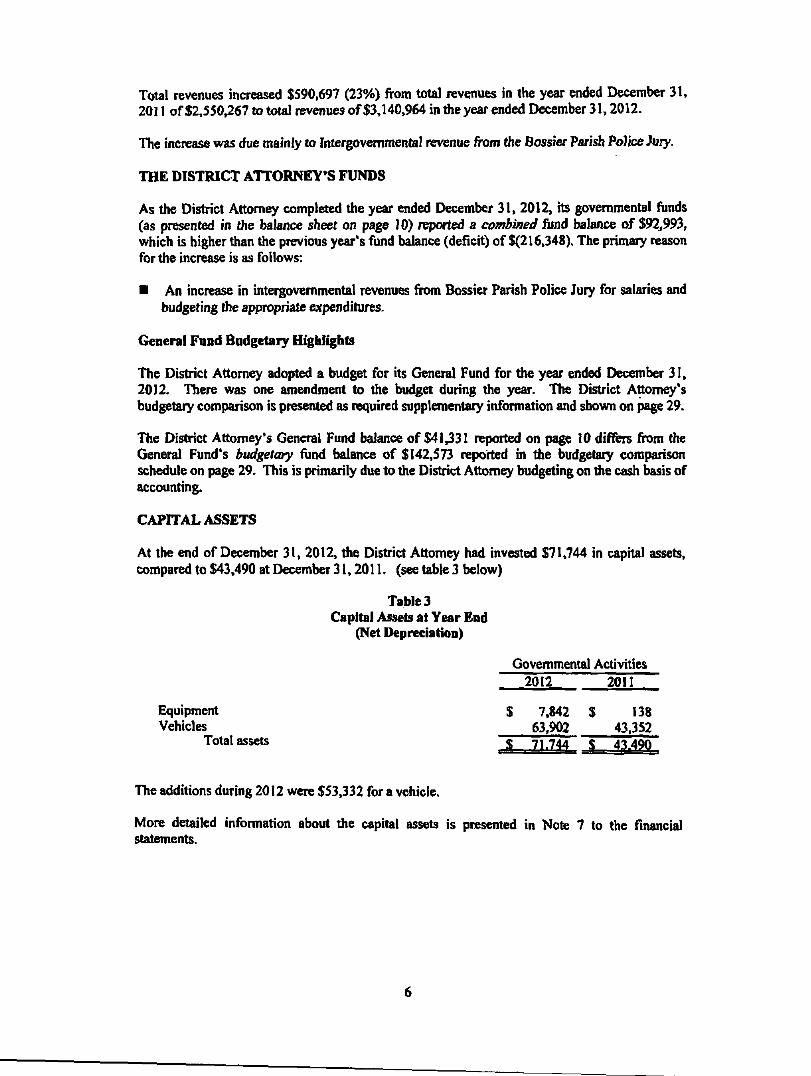

Total revenues increased $590,697 (23%) from total revenues in the year ended December 31, 2011 of $2,550,267 to total revenues of $3,140,964 in fte year ended December 31,2012.

The increase was due mainly to Intergovernmental revenue from the Bossier Parish Police Jury.

THE DISTRICT ATTORNEY'S FUNDS

As the District Attorney completed the year ended December 31, 2012. its governmental funds (as presented in the balance sheet on page 10) reported a combined fund balance of $92^993, which is higher than the previous year's fund balance (deficit) of $(216,348). The primaiy reason for the increase is as follows:

• An increase in intergovernmental revenues from Bossier Parish Police Jury for salaries and budgeting the appropriate expenditures.

General Fund Budgetary Highlights

The District Attorney adopted a budget for its General Fund for the year ended December 31, 2012. There was one amendment to the budget during the year. The District Attorney's budgetary comparison is presented as required supplementary information and shown on page 29.

The District Attorney's General Fund balance of $41331 reported on page 10 differs from the General Fund's budgetary fund ttalance of $142,573 reported in the budgetary comparison schedule on page 29. This is primarily due to the District Attorney budgeting on Ae cash basis of accounting.

CAPITAL ASSETS

At the end of December 31, 2012. the District Attorney had invested $71,744 in capital assets, compared to $43,490 at December 31,2011. (see table 3 below)

Equipment Vehicles

Total assets

The additions during 2012 were $53,332 for a vehicle.

Table 3 Capital Assets at Year End

(Net Depreciation)

Governmental Activities 2012 2011

$ 7,842 $ 138 63,902 43,352

$ 71,744 $ 43,49Q

More detailed information about the capital assets is presented in Note 7 to the financial statements.

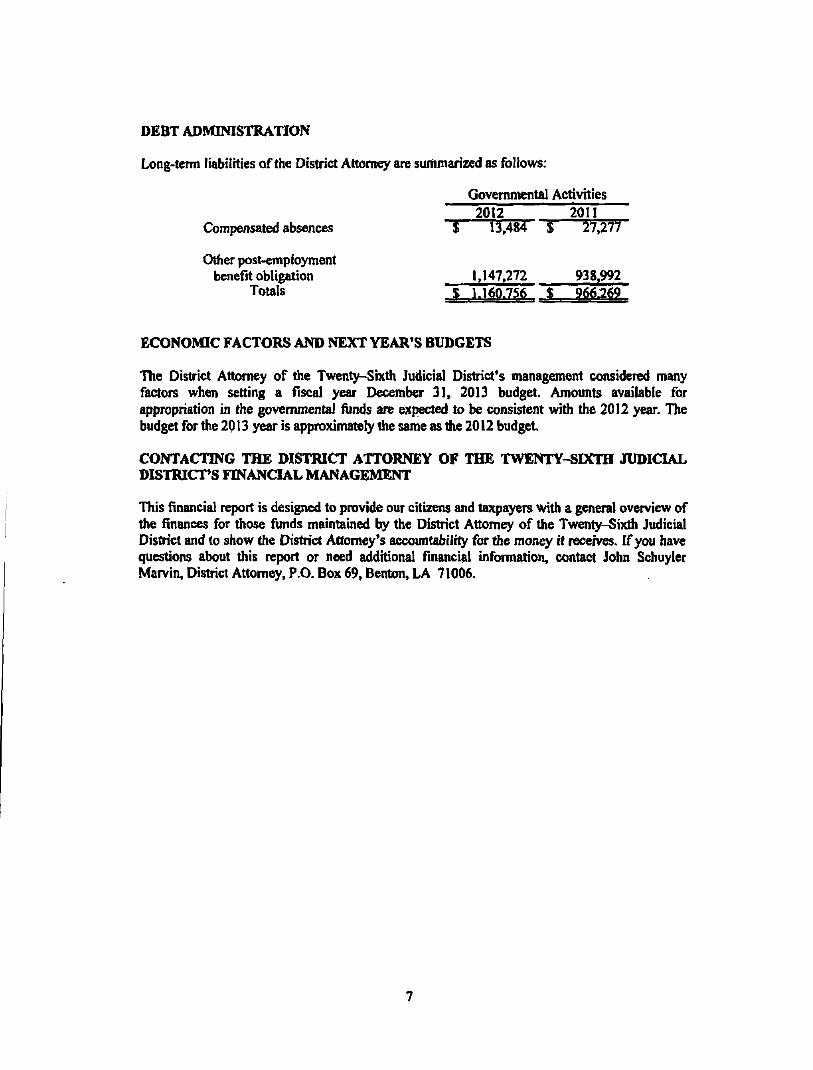

DEBT ADMINISTRATION

Long-term liabilities of the District Attorney are summarized as follows:

Governmental Activities

Compensated absences

Other post-employment benefit obligation

Totals

2012 2011 * 13,484 i l i a i l

1,147,272 938,992

ECONOMIC FACTORS AND NEXT YEAR'S BUDGETS

The District Attorney of the Twenty-Sixth Judicial District's management considered many factors when setting a fiscal year December 31, 2013 budget. Amounts available for appropriation in the governmental fiinds are expected to be consistent with the 2012 year. The budget for the 2013 year is approximately the same as the 2012 budget

CONTACTING THE DISTRICT ATTORNEY OF THE TWENTY-^SDC^I JUDICIAL DISTRICT'S FINANCUL MANAGEMENT

This financial report is designed to provide our citizens and taxps^ers with a general overview of the finances for those funds maintained by the District Attorney of the Twenty-Sixdt Judicial District and to show the District Attorney's accountability for the money it receives. If you have questions about this report or need additional financial infomuition, contact John Schuyler Marvin, District Attorney, P.O. Box 69, Benton, LA 71006.

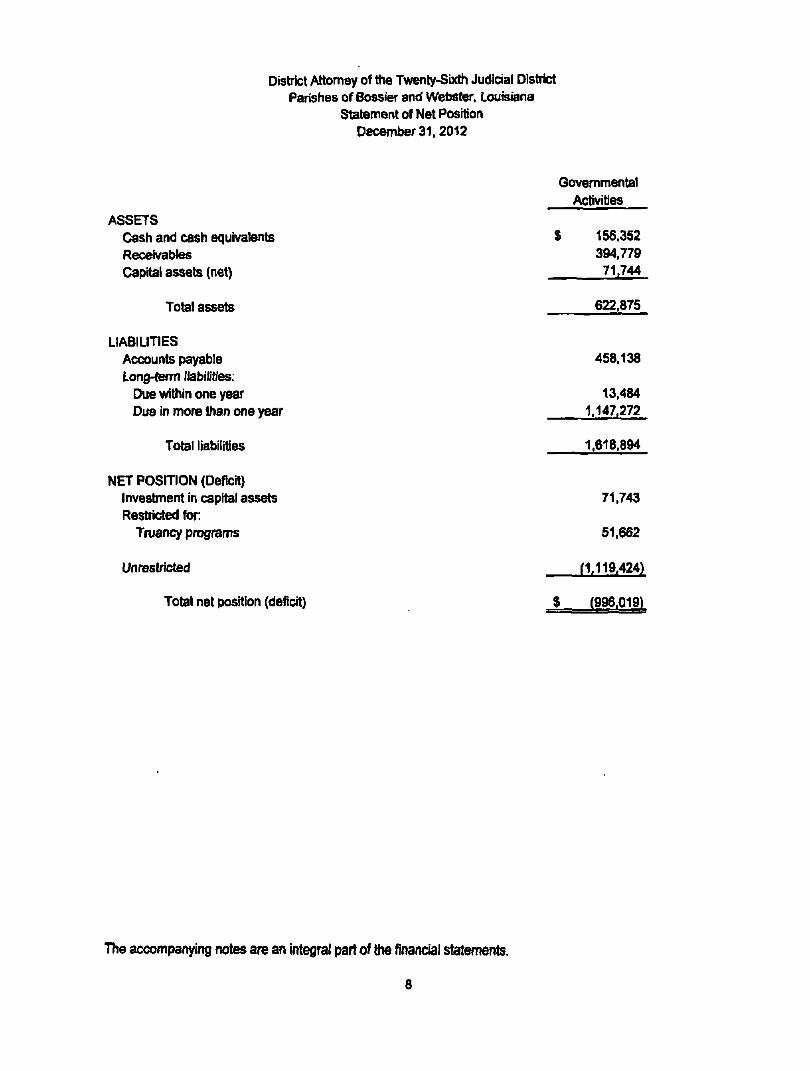

District Attorney of the Twenty-Sixth Judicial Dishlct Parishes of Bossier and Webster, Louisiana

Statement of Net Position December 31,2012

ASSETS Cash and cash equivalents Receivables Capital assets (net)

Total

LIABILITIES Accounts payable Long-term liabilities:

Due within one year Due in more than one year

Total liabilities

NET POSITION (Deficit) Investment In capital assets Restricted for

Truancy programs

UnresirictBd

Total net position (deficit)

Governmental Activities

% 156,352 394,779 71J44

622.875

458,138

13.484 1.147,272

1,618.894

71.743

51,662

n.iiM24)

(996.019)

The accompanying notes are an integral part of the finandai statements.

8

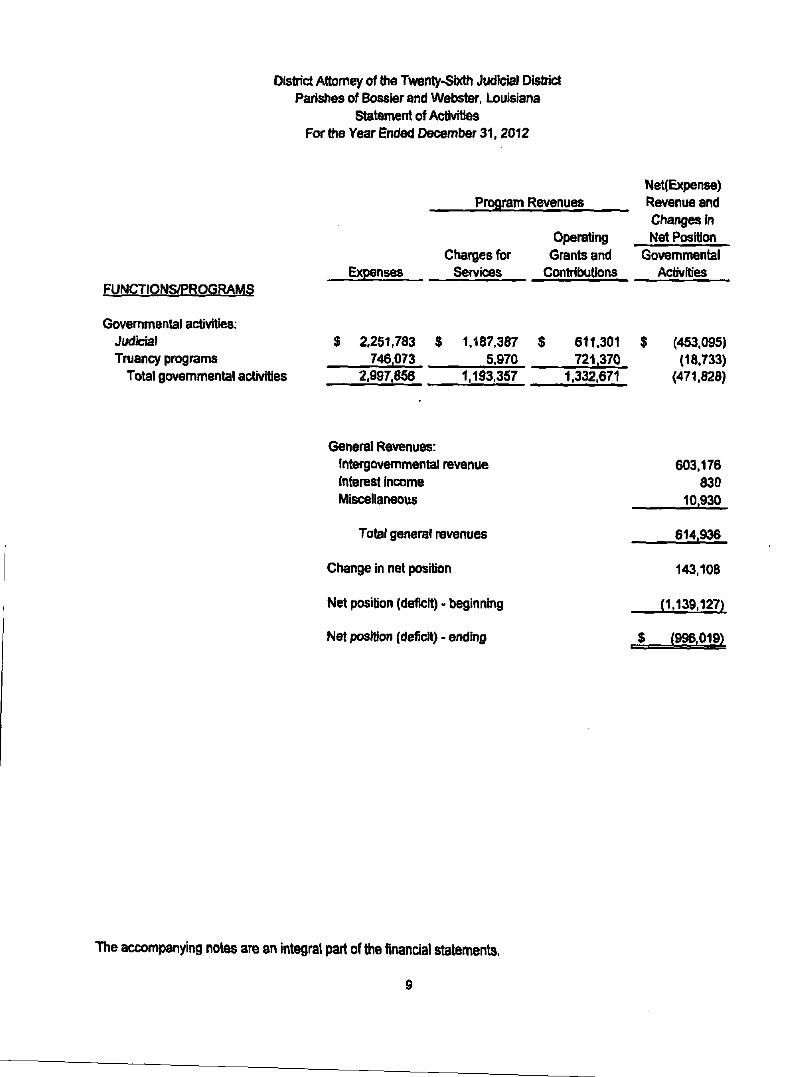

District Attorney of the Twenty-Sixth Judicial District Parishes of Bossier and Webster, Louisiana

Statement of Activities For the Year Ended December 31.2012

FUNPTlONS/PPOeRAM?

Governmental activities: Judicial Truancy programs

Total governmental activities

Program

Charges for Expenses Services

$ 2.251J83 $ 1,187,387 746.073 5.970

2.997.856 1.193.357

General Revenues: Intergovernmental revenue Interest income Miscellaneous

Total general revenues

Change in net position

Net position (deficit) - beginning

Net position (deficit) - ending

Revenues

Operating Grants and

Contributions

$ 611,301 721,370

1.332.671

Net(Expense) Revenue and Changes In Net Position

Governmental Activities

$ (453,095) (18J33)

(471.828)

603.176 830

10.930

614,936

143.108

(1.139.127)

$ (998,019)

The accompanying notes are an integral part of the financial statements.

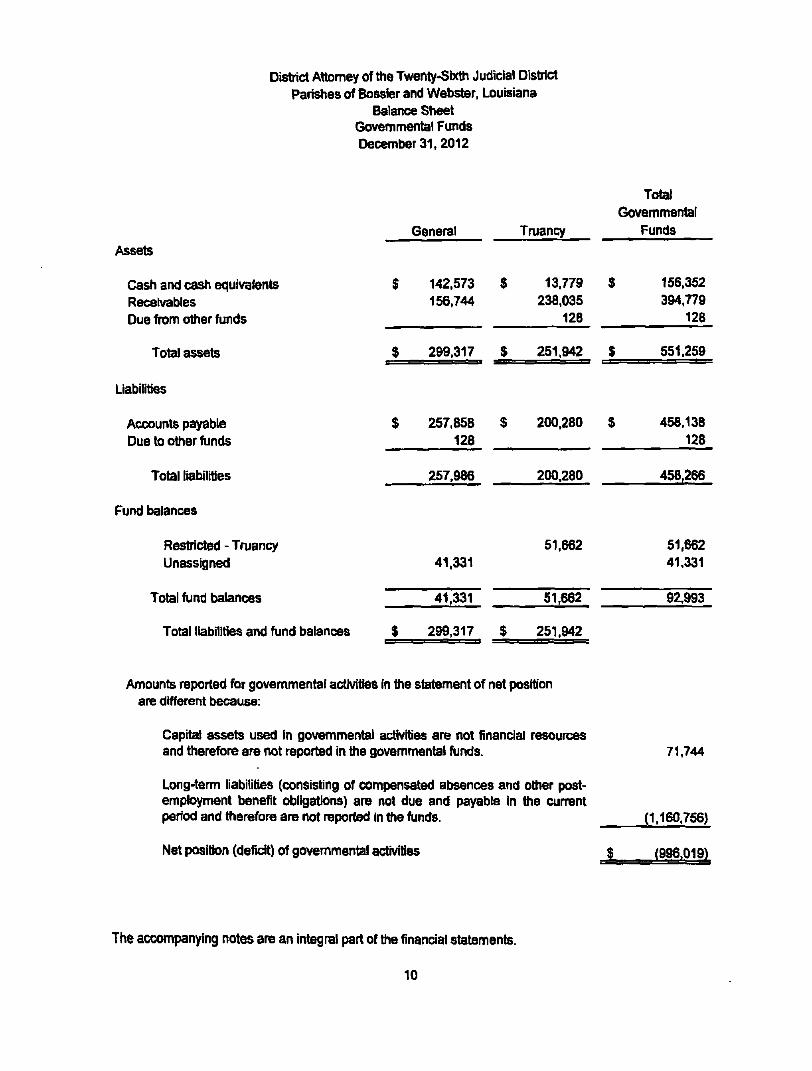

District Attorney of the Twenty^Sfocth Judicial District Parishes of Bossier and Webster, Louisiana

Balance Sheet Governmental Funds December 31.2012

ssets

Cash and cash equivalents Recetvabies Due from other funds

Total assets

$

$

General

142,573 156,744

299.317

$

$

Truancy

13.779 238.035

126

251.942

I

$

$

Total Governmental

Funds

156.352 394,779

128

551.259

Liabilities

Accounts payable Due to other funds

Total liabilities •

Fund balances

Restricted - Truancy Unassigned

Total fund balances

Total liabilities and fund balances

$ 257.858 $ 128

257,986

41,331

41.331

$ 299.317 $

i 200.280 $

200,280

51.662

51.662

251,942

458,138 128

458,266

51.662 41.331

92.993

Amounts reported for governmental activities In the statement of net position are different because:

Capital assets used In governmental activities are not financial resources and therefore are not reported in the governmental funds.

Long-temi liabilities (consisting of compensated absences and other post-employment benefit obligations) are not due and payable in the current period and therefore are not reported In the funds.

Net position (deficit) of governmental activities

71.744

(1.160.756)

(996.019)

The accompanying notes are an integral part of the financial statements.

10

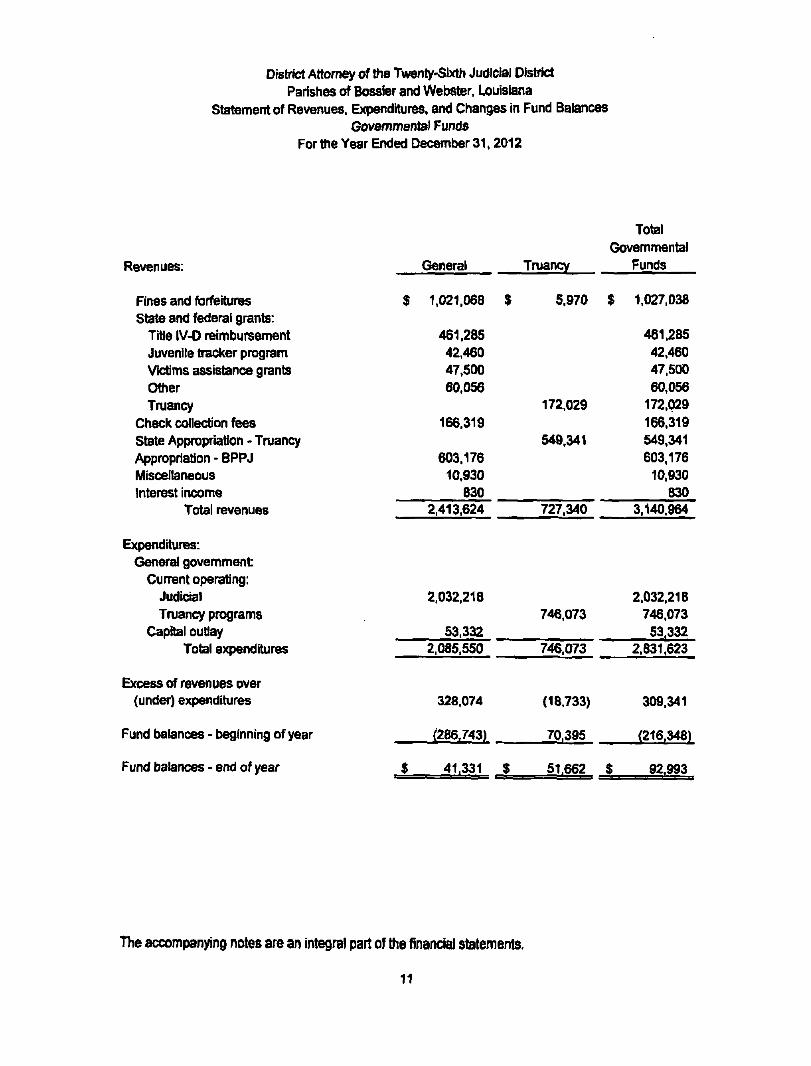

District Attorney of the Twenty-Sbcth Judicial District Parishes of Bossier and Webster, Louisiana

Statement of Revenues. Expenditures, and Changes In Fund Balances Governmental Funds

For the Year Ended December 31.2012

Revenues:

Fines and forfeitures State and federal grants:

Title IV-D reimbursen>ent Juvenile tracker program Victims assistance grants Other Truancy

Check collection fees State Appropiiation - Truancy Appropriation - BPPJ Miscellaneous Interest income

Total revenues

Expenditures: General government

Cunent operating: Judicial Truancy programs

Capital outlay Total expenditures

General

$ 1.021,068

461,285 42,460 47.500 60.056

166.319

603,176 10.930

830 2,413,624

2,032,218

53,332 2.085.550

Truancy

$ 5,970

172,029

549,341

727,340

746,073

746,073

Total Governmental

Funds

$ 1,027,038

461.285 42.460 47.500 60.056

172,029 166,319 549.341 603.176

10.030 830

3.140.964

2,032,218 746.073 53,332

2.831.623

Excess of revenues over (under) expendihires

Fund balances - t)egfnnlng of year

Fund balances - end of year

328,074

(286,743)

(18733)

70,395

41.331 51.662 $

309.341

(216.348)

92,993

The accompanying notes are an integral part of the financial statements.

11

District Attorney of the Twenty-Sbcth Judk:ial District Parishes of Bossier and Webster. Louisiana

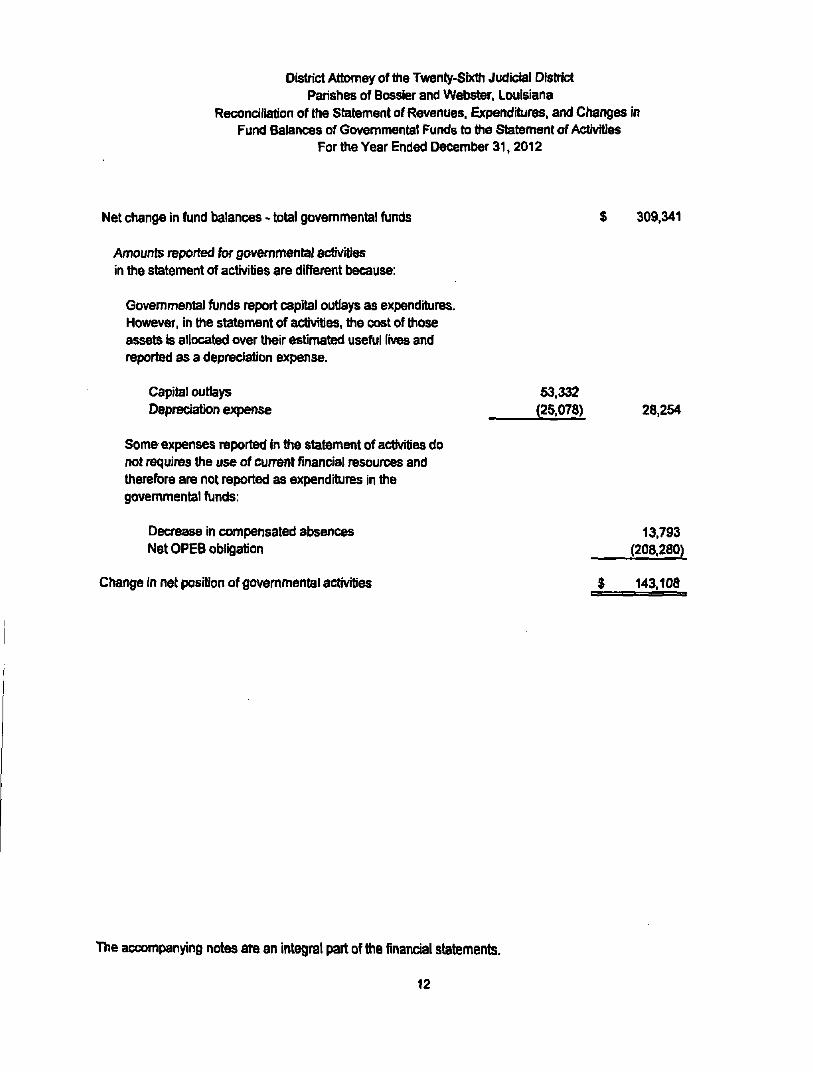

Reconciliation of the Statement of Revenues. Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities

For the Year Ended December 31.2012

Net change in fund balances - total governmental funds $ 309.341

Amounts reported for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of acthrities, the cost of those assets is allocated over their estimated useful lives and reported as a depreciation expense.

Capital outlays 53.332 Depreciation expense (25,078) 28,254

Some expenses reported In the statement of activities do not requires the use of current financial resources and therefore are not reported as expenditures in the governmental funds:

Decrease in compensated absences 13.793 Net OPEB obligation (208.280)

Change in net position of governmental activities $ 143.108

The accompanying notes are an integral part of the financial statements.

12

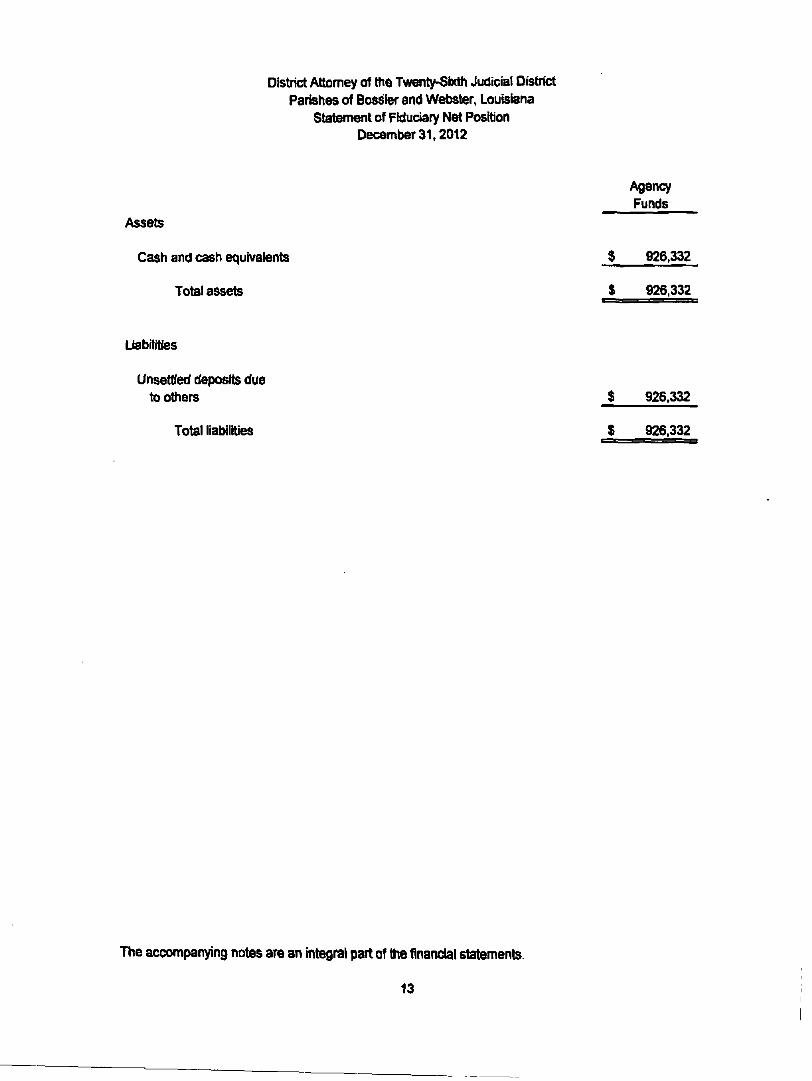

District Attorney of the Twenty-Sbctii Judicial District Parishes of Bossier and Webster. Louisiana

Statement of Fiduciary Net Position December 31.2012

Assets

Cash and cash equivalents

Total assets

Agency Funds

926,332

926.332

Liabilities

Unsettled deposits due toothers

Total liabilities

926.332

926.332

The accompanying notes are an integral part of the financial statements.

13

District Attorney of the Twenty-Sixth Judtoial District Parishes of Bossier and Webster, Louisiana

Notes to the Financial Statements December 31,2012

Introduction

As provkjed in ttie laws of the State of Louisiana, tiie Distiict Attorney has charge of e v ^ criminal prosecution by the state in his distiict. is the representative of the state before the grand jury in his dlstlct. and is the legal advisor to the grand jury. The District Attorney also performs other duties as provkfed by law. The District Attorney is elected by the qualified electors of the judicial district for a tarn of 6 years. The Twenty-Sixth Judicial District encompasses the parishes of Bossier and Webster. Louisiana.

(1) Summary of Significant Accounting Policies

The District Attorney of the Twenty-Sixth Judk:iaf District's financial statements are prepared in conformity witti generally accepted accounting prindples (GAAP). The Governmental Accounting Standards Board (GASB) Is responsible for establishing GAAP for state and k>cal governments through its pronouncements (Statements and Interpretations). The accompanying basto financial statements have been prepared in conformity with GASB Statement 34. Bash Financiai Statements -and Management's Discussion and Anatysis-fdr State and Local Governments, issued In June, 1999. The more significant accounting polk ies established in GAAP and used by the District Attorney of the Twenty-Sixtti Judicial District (Distiict Attorney) are discussed below.

A Reporting Entity

The Distiict Attorney is an independent elected official; however, tiie District Attorney Is fiscally dependent on the Bossier Parish Police Jury. The police jury maintains and operates the parish courthouse in which the Distiict Attorney's office is k)cated and provides funds for equipment and furniture of the District Attome/s office. In addition, the police jury's general purpose finandai statements would be incomplete or misleading wittiout inclusion of the District Attorney. For these reasons, the District Attorney was determined to be a component unit of the Bossier Parish Police Jury, the financial reporting entity.

The accompanying financial statements present infonnation only on the funds maintained by the District Attorney and do not present infonnation on the police jury, the general government services provided by that governmental unit or the otiter governmental units that comprise the financial reporting entity.

B. Bask: Financial Statements - Government-Wtde Statements

The District Attomey's bask: financial statements include both government-wide (reporting the funds maintained by the Distiict Attorney as a whole) and fiind finandai statements (reporting ttie District Attorney's major funds). Both the government-wide and fund financial statements categorize primary activities as ettiter governmental or business type. The District Attorney's General Fund and Truancy Fund are classified as governmental activities. The District Attorney does not have any business-type activities.

In the govemment-wKle Statement of Net Position, ttie governmental activities column is presented on a consolidated basis and is reported on a fiill accrual, economk: resource basis, which recognizes all long-term assets and receivables. The District Attorney's net position Is reported in three parts -Invested in capital assets (net of related debt), restricted n ^ position, and unrestricted net position.

(Continued) 14

District Attorney o f«» Twenty-Sbctii Judkaal Distiict Parishes of Bossier and Webster, Louisiana

Notes to the Financial Statements December 31.2012

(Continued)

The govemment-wkte Statement of Activities reports both tiie gross and net cost of each of the District Attome/s functions. The functions are supported by program revenues and general government revenues. The Statement of Activities reduces gross expenses (including depreciation) by any related pn3gram revenues, which must be directly assoc^ted with tiie function. Program revenues of the District Attorney consist of fines and forteitures, state and federal grants, check collection tees, and state appropriation revenues. The net costs (by fijnction) are normally covered by general revenues.

This govemment-wkle focus is more on the sustainabiTity of the District Attorney as an entity and the change in tiie District Attorney's net position resulting from the current year's activities.

C. Basic Financial Statements * Fund Financial Statenrtents

The financial transactions of the District Attorney are recorded in Individual funds in the fund financial statements. Each fund Is accounted for by prOTkiing a separate set of self-balancing accounts tiut comprises its assets, liabilities, resewes, fund equity, revenues and expenditures. The various funds are reported by generic classification wimin tiie financial statements.

The fbflowing fund types are used by ti^e District Attorney:

Governmental Funds - the focus of the governments funds' measurennent (in the fund statements) is upon detemiination of financial position and changes In financial position (sources, uses, and balances of financial resources) rather ttian upon net income. The foRowing is a description of tiie governmental funds of the District Attorney:

General Fund - tt>e general fund accounts for tiie operations of tiie District Attorney's office. Included in the general fund, to offset or defray tiie necessary expenditures of the District Attorney, are fines collected and bonds forfeited in compliance witii Louisiana Revised Statute (R.S.) 15:571.11; certain percentage of asset forfeiture revenue in regards to die Special Asset Forfeiture Trust Fund established kyy Louisiana Revised Statute 40:2616; reimbursements received from the Louisiana Department of Social Services for operation of the family and chBd support programs (Titie IV-D Reimbursement); worthless check collection fees collected in accordance witti Louisiana Revised StahJte 16:15; and all otiier financial resources not accounted for and reported in another fund.

Special Revenue Fund - the special revenue fund te used to account for the proceeds of specific revenue sources that are restricted or committed to expenditures fbr specified purposes ott er than debt sen/k» and capital projects. The special revenue fund of the District Attorney consists of the Tmancy Program operations.

Fiduciary Fund - the fidudary fund is used to report assets hekl in a tmst or agency capacity tor ottiere and tiierefore are not available to support District Attorney programs. Included in tills fund type is the Asset Foriielture Trust Fund estabfished by Louisiana Revised Statute 40:2616.

The emphasis in fund financial statements is on tiie major funds In the governmental category. Non-major funds by cat^ory are summarized into a single cokjmn. GASB Statements No. 34 sets forth minimum criteria (percentage of the assets, liabilities, revenues, or expencfitures/expenses of fiind category) for the detemiination of major funds. Botti governmental funds of ttie Distiict Attorney were determined to be major funds.

(Continued)

15

District Attorney of the Twenty-Sbdh Judicial Distiict Parishes of Bossier and Webster, Louisiana

Notes to the Financial Statements December 31.2012

(Continued)

The following major funds are presented in tiie fund finaricial statements:

General Fund - accounts for all financial resources except those required to be accounted fbr in anotiier fund.

Taiancy Program Fund - accounts for tiie operation of certain truancy programs.

D. Basis of Accounting

Basis of accounting refers to the point at which revenues or expenditajres are recognized in the accounts and reported In the financial statements. It relates to fi)e timing of the measurements made regardless of the measurement focus applied.

1. Accrual:

The governmental funds in tiie government-wide financial statements are presented on the accrual basis of accounting. Revenues are recognized when earned and expenses are recognized when incurred.

2. ft^odified Accrual

The governmental funds financial statements are presented on the modified accrual b a ^ of accounting. Under modified accrual basis of accounting, revenues are recorded when susceptible to accrual: i.e., botti measurabte and available. "AvaHabie" means collectibie wittiln me current period or wittiln 60 days after year end. Expenditures are generally recognized under the modified accrual basis of accounting when tiie related Hatrility is incuned. The exception to tills rule is that principal and interest on general obl^ation k>ng-term debt, if any. is recognized when due. Depreciation Is not recognized in tiie governmental fund financial statements.

E. Budgets

The Distiict Attorney uses the following budget practices:

1. The Distrfot Attorney prepares an operating budget for the general and special teverwie funds.

2. The budget is made available for public inspectk>n prior to the publk: hearing held to obtain taxpayer comment

3. The budget Is adopted at the publk: hearing.

4. The budget is adopted on a cash basis.

5. The budget may be revised during tiie year.

6. Appropriations lapse at ttie end of each fiscal year.

(Continued)

16

District Attorney of the Twenty-Sixth Judicial District Parishes of Bossier and Webster, Louisiana

Notes to the Finandai Statements December 31,2012

(Continued)

F. Cash, Cash Equivalents, and Investments

Cash includes amounts In demand d^x>slt$. interest-bearing demand deposits, and time deposits. Cash equivalents include amounts In time deposits and those investments wtth original maturities of 90 days or less. Under state law. ttie District Attorney may deposit funds in demand deposits. interest-bearing demand deposits, or time deposits witti state banks organized under Lou^lana law. or any ottier state of the United States, or under tiie laws of the United States.

Investments are limited by Louisiana Revised Statue (R.S.) 33:2955. These are classified as Investments if tiieir ongimeU maturities exceed 90 days; however, if ttie original mahirities are 90 days or less, tiiey are classified as cash equivalents.

G. Capital Assets

Capital assets purchased or acquired with an original cost of $2,500 or more are reported at historical cost or estimated historical cost Conttibuted assets are reported at f^ir market value as of tiie date received. Additions, improvements, and ottier capital outiays ttiat stgnificantiy extend ttie useful life of an asset are capttalirod. Other costs incurred for repa^ and maintenance are expensed as incurred.

Depreciation on all assets Is provkled on ttie sti lght-4ine basis over ttie following estimated useful lives:

Vehtoles 5 years Equipment 5 - 7 years

H. Compensated Absences

The Distiict Attorney has an informal poik^ fbr vacatfon and sick leave. Emptoyees of ttie District Attorney earn from 5 to 15 days of vacation leave each year, depending on their tengttis of service. Emptoyees may carry no more ttian one-haff of ttteir normal yearty benefit fonvard to ttte next benefit year. Upon termination of emptoyment. emptoyees will be paid for unused vacation time that ttiey are eltgible fbr according to the Distiict Attorney's polk:y.

Employees of ttie Distiict Attorney will accrue sick leave benefits which are calculated on ttie basis of a "benefit year" at tiie rate of 6 days per year. Unused sick leave will be altowed to accumulate without limit Unused sick leave btenefits will not be paki to employed while ttiey are emptoyed or upon termination of employment

The cunient portion of compensated absences payable (the amount estimated to be used during the period of availability) Is recorded as a liability In ttie fund financial stetements. The entire balance of compensated absences payable Is recognized as a liability in the govemment-wkJe financial stetements. The non-current portion represents a reconciling item between the fund and govemment-wkle statemente.

I. Use of Estimates

Management uses estimates and assumpttons in preparing financial statements. Those estimates and assumptions affect the reported amounts of assete and liabilities, the disclosure of contingent assets and liabilities, and reported revenues and expenses. Actual results couM differ from those estimates.

(Continued) 17

District Attorney of ttie Twenty^bctti Judicial District Parishes of Bossier and Webster, Louisiana

Notes to ttie Financial Statements December 31,2012

(Continued)

J. Net Position

Net position represents tiie difference between assete and liabilities. Net position Invested In capltel assete, net of related debt consist of capltel assete, net of accumulated depredation, reduced by the outstending balances of any borrowing used for ttie acquisition, construction, or improvement of Uiose assete. Net ponton is reported as restricted when ttiere are limitetions imposed on ttielr use either ttireugh constitotional provisions or enabling legislation adopted by ttie Distiict Attorney or ttirough external restrictions imposed by creditors, grantors, or laws or regulations of other govemmente. The Distttot Attomey*s policy is to first apply restricted resources when an expense is incuned for purposes for whk:h both restricted and unresticted net position is available.

K. Interfund Activity

Interfund activity is reported as either loans, relmbursemente, or transfers. Loans are reported as Interfund receivables and payables as appropriate and are subject to elimination upon consolkiation. Reimbursements are when one fund incurs a cost, charges the appropriate benefiting fund and reduces ite relate cost as a reimbursement Transfers between govemmentel funds are netted as part of ttie reconciliation to ttie government-wide financial stetemente.

L. Long-Temi Obligations

In ttie government-wide financial stetemente.. long-term obligations are reported as liabilities in the applicable governmental activities in ttie stetement of net assete.

M. Fund Balance

In ttie govemmentel fund finandai stetemente. fund batenoes are classified as foitows:

1. Nonspendable - amounte ttiat cannot be spent either because ttiey are not in spendable fomrt or because they are legally or contrectually required to be mainteined intact

2. Restricted - amounte ttiat can be spent only for specific purposes due to constrainte placed on the use of resources that are eittfer (a) externally imposed 1^ creditors, grentors. contiibutons. or laws or regulations of ottier govemmente, or (b) imposed by law through constitutional provisions or enabling legislation.

3. Committed - amounte that can be used only for the spedfic purposes as a result of constinlnte imposed by the District Attorney (ttie Dlsbk:t Attome/s highest level of decision making auttiority). Committed amounte cannot be used for any other purpose unless ttie Distiict Attorney removes those constrainte by teking the same type of action (I.e. legislation, resolution, ordinance).

4. Assigned - amounte ttiat are constrained by ttie District Attorney's intent to be used for specific purposes, but are neittier restricted nor commttted.

5. Unassigned - all amounte not induded In ottier spendable classifications

(Continued)

18

Distiict Attorney of ttie Twenty-Sixtti Judk:ial Distiict Parishes of Bossier and Webster, Louisiana

Notes to ttie Finandai Stetemente December 31,2012

(Continued)

The Disttk:! Attome/s policy is to apply expenditures against restiicted fund balance and tiien to ottier, less-resttictive classifications - committed and ttien assigned fund balances before using unassigned fund balances.

The cakujiation of fiind balance amounte begins with the determination of nonspendable fiind balances. Then restiicted fond balances for specific purposes are determined (not Induding non-spendable amounte). Then any remaining fund batence amounte for the non-general funds are dassified as restricted fund batence. It is possible for ttie non-general funds to have negative unassigned fond balance when non-spendable amounte plus the restricted fond balances fbr specific purpose amounte exceeds the positive fond balance for the non-general fond.

(2) New Accounting Stendards

Effective January 1,2012, ttie Distiid Attorney implemented ttie foltowing GASB stetement GASB Statement No. 63, 'Finance Reporting of Deferred Outtfows of Resources, Deferred /nftMvs of Resources, and Net f^xsition' This Statement establishes stendards fbr reporting deferred outftows of resources and defended inflows of resources, and net position.

(3) Cash and Cash Equivalente

At December 31, 2012, ttie District Attorney had cash and cash equivalents (book batences) toteling $1,082,684 as follows:

Demand depostte $ 36,554 Timedeposlte 10,454 Interest-bearing demand deposite 1.035.676

Total S 1.08^,684

Recondliation to government-wide Stetement of Net Assete:

Cash and cash equh^lents $ 156.352 Agency fonds (not on govemment-^vkle

stetemente) 926.332 S 1.08^684

Custodial Credit Risk

Custodial credit risk is ttie risk that in ttie event of a bank foilure. ttie government's deposite may not be returned to it As of December 31. 2012. $793,397 of ttie Disttk t Attome/s bank balance of $1.155.519 was exposed to custodial credit risk as follows:

Uninsured and collateral heto by the pledging bank's trust department not in the Town*s name:

Cash and cash equivalente $ 793.397

Even ttiough ttie pledged securities are con^dered uncollateralized (Category 3) under ttie provistons of GASB Stetement 3. R.S. 39:1229 imposes a stetijtory requirement on ttie custodial bank to advertise and sell ttie pledged securities wittiin 10 days of being notified tiiat ttie fiscal agent has foiled to pay deposited fonds upon demand.

(Continued)

19

District Attorney of ttie Twenty-Sbtth Judicial Distiict Parishes of Bossier and Webster, Louisiana

Notes to ttie Finandai Stetemente December 31,2012

(Continued)

(4) Pension Plan - District Attorney and Assistant [Str ict Attorneys

Plan Description. The distttot attorney and assistant district attorneys are members of the Louisiana Distiict Attorneys Retirement System (System), a cost-sharing, multiple-omptoyer defined benefit pensfon ptan administered by a separate board of tiojstees.

Assistant district attorneys who earn, as a minimum, ttie amount paid by the state for assistant distttot attorneys and are under ttie age of 60 at ttie time of original emptoyment and all distiict attorneys are required to partidpate In the System. For members who joined ttie System before July 1.1990. and who elected not to be covered by ttie new provistons. ttie following applies: Any member witti 23 or more years of creditable service regardless of age may retire with a 3 percent benefit reduction for each year betow age 55. provkled that no reduction is applied if ttie member has 30 or more years of service. Any member witti at least 18 years of service may retire at age 55 witti a 3 percent benefit reduction for each year betow age 60. In addition, any member witti at least 10 years of service may retire at age 60 with a 3 percent benefit reduction for each year retiring betow the age of 62. The retirement benefit is equal to 3 percent of the member's average final compensation multiplied by ttie number of years of his membership sen/ice, not to exceed 100% of his average final compensation.

For members who joined the System after July 1. 1990, or who elected to be covered by ttie new provistons ttie following applies: Members are etiglbte to receive nomnal retirement benefite if ttiey are age 60 and have 10 yeare of service credit are age 55 and have 24 years of servtoe credit, or have 30 years of servtoe credit regardless of age. The nomnal retirement benefit is equal to 3.5 percent of the member's final-average compensation multiplied by years of membership service. A member Is eliglbte for eariy retirement if he is age 55 and has 18 years of service credit The eariy retirement benefit is equal to the nomnal retirement benefit reduced 3 percent for each year the member retires in advance of normal retirement age. Benefite may not exceed 100 percent of average final compensatton. The System also provides death and disability benefite. Benefite are established or amended by state stafote.

The System issues an annual publtoly available financial report that includes finandai stetemente and required supplementery information fbr the System. That report may be obtelned by writing to ttie Louisiana Distiict Attorneys Retirement System. 2109 Decatur Street, New Orteans, Louisiana 70116^2091, or by calling (504) 947-5551.

Funding Policy. Plan members are required by state statute to contribute 7.0 percent of their annual covered salary and ttie district attorney is required to contribute at an actuarially determined rate. The current rate effective July 1.2011 ttirough June 30, 2012 Is 9.75% of annual covered payroll, and 10.25% effective July 1. 2012. Conttibutions to ttie System also indude .2 percent of ttie ad valorem taxes collected throughout the state and revenue sharing fonds as appropriated by ttie legistature. The contribution requiremente of plan members and ttie distiict attorney are established and may be amended by state statute. As provkled by Louisiana Revised Stafote 11:103. the emptoyer contributions are determined by actuarial valuation and are subject to change each year based on the resutte of the valuation for ttie prior fiscal year. The district attorney's contributions to ttie System for ttie years ended December 31 . 2012. 2011. and 2010 were $60,886, $41,677, and $31,484. respectively.

(Continued)

20

Distiict Attorney of ttie Twenty-Sbctti Judtoial Distiict Parishes of Bossier and Webster, Louisiana

Notes to ttie Finandai Statemente December 31,2012

(Continued)

(5) Pension Plan - Other Emptoyees

Ptan Description:

Substantially all emptoyees of the Distiict Attorney, except for ttie distiict attorney and his assistante. are members of ttie Parochial Employees Retirement System of Louisiana (System), a cost-faring, multiple-emptoyer defined benefit penston ptan administered by a separate board of trustees. The System is composed of two distinct plans. Plan A and Plan B. witti separate assete and benefit provistons. All emptoyees of the Distiict Attorney are memb^s of Plan A.

All pennanent emptoyees wwking at least 28 hours per week who are pakJ wholly or in part from parish fonds and alt elected parish offictais are eliglbte to partk:ipate in the S ^ m . Under Ptan A, employees who retire at or after age 65 witti at least 7 years of creditable service, at or after age 60 witti at least 10 years of creditable service, or after age 55 witti at least 25 years of creditabte servtoe, or at any age witti at toast 30 years of creditable service are entitied to a retirement benefit, payable monttily for life, equal to 3 percent of their finaV-average salary for each year of creditable servtoe. Final-average salary is the emptoyee's average salary over ttie 36 consecutive or joined monttis ttiat produce ttie highest average. The System also provides death and disability benefite. Benefite are esteblished or amended by state stafote.

The System issues an annual publidy available finandai report ttiat includes finandai stetemente and required supplementary information for ttie System. That report may be obtained by writing to tiie Parochial Employees* Retirement System. Post Office Box 14619. Baton Rouge. Loulstana 70898-4619. or by calling (504) 928-1361.

Funding Poltoy:

State stafote requires covered emptoyees to contiibute a percentage of their salaries to ttie plan. As provtoed by R.S. 11:103. the emptoyer conttibutions are detemnined by an acfoarial valuation and are subject to change each year based on ttie resuHs of ttie valuation for the pnor fiscal year.

Under Ptan A. members are required by state statijte to contribute 9.5 percent of ttieir annual covered salary and ttie Distiict Attorney of ttie Twenty-Sbctti Judicial District is required to contribute at an acfoariatly detennined rate. Contribution rates were 15.75%, 15.75% and 12.75% of annual covered payroll for 2012. 2011 and 2010. respectively. Contributions to ttie System include one-fourtti of one percent (except Orieans and East Baton Rouge Parishes) of ttie taxes shown to be collectible by the tax rolls of each parish. These tax dollars are dMded behween Plan A and Ptan B based proportionately on the sataries of the active members of each plan. The contiibution requiremente of plan members and ttie District Attorney are esteblished and may be amended by stete statute. The District Attorneys conttibutions to ttie System under Plan A for ttie yeare ended December 31, 2012, 2011 and 2010 were $170,413, $193,422, and $202,503. respectively, equal to ttie required conttibutions for the year.

(Continued)

21

Distttot Attorney of ttie Twenty^ixtti Judtotal District Parishes of Bossier and Webster. Loulstana

Notes to ttie Finandai Stetemente December 31.2012

(Continued)

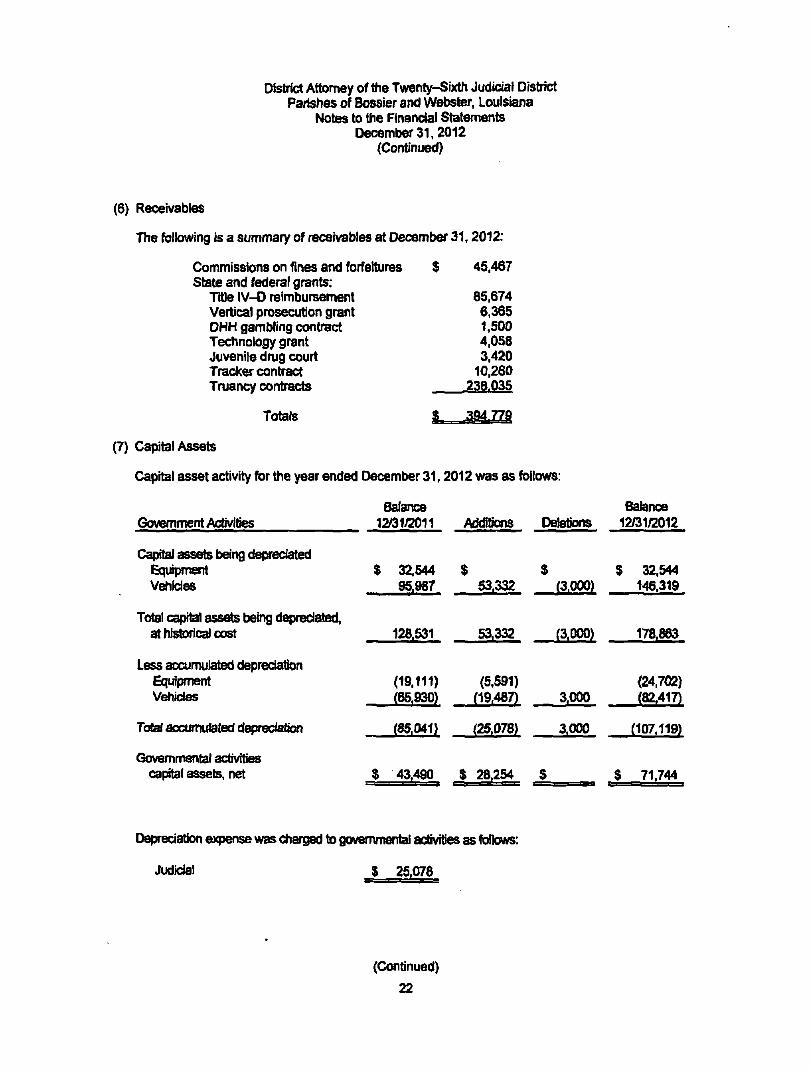

(6) Receivables

The foltowing Is a summary of receivables at December 31.2012:

Commisstons on fines and forfettures Stete and federal grante:

TiOe IV-D reimbursement Vertical prosecution grant DHH gambling conttact Technotogy grant Juvenite drug court Tracker contract Truancy contracte

Totals

$ 45.467

85,674 6,365 1.500 4,058 3,420

10,280 239.P35

$ 394.779

(7) Capital Assete

Capital asset activity for the year ended December 31,2012 was as follows:

Government Activities

Capital assete being deprectatei Equipment Vehkdes

Total capital assete being depredated, at historical cost

Less accumulated depreciation Equipment Vehides

T c ^ accumulated depredatton

Governmental activities capital assets, net

Balance 12/31>2011

$ 32.544 95,987

128,531

(19.111) (65.930)

(85.041)

% 43.490

Additions

$ 53.332

53,332

(5.591) (19.487)

(25.078)

$ 28,254

Deletions

$ (3,000)

(3,000)

3.000

3.000

$

Balance 12/31^2012

$ 32.544 146.319

178.883

(24.702) (82.417)

(107.119)

$ 71.744

Depredation expense was charged to governmental activities as follows:

Judk:tal $ 25.078

(Continued)

22

Distiict Attorney of the Twenty-Slxtti Judctal District Parishes of Bos^er and Webster. Louisiana

Notes to ttte Financial Statemente December 31,2012

(Continued)

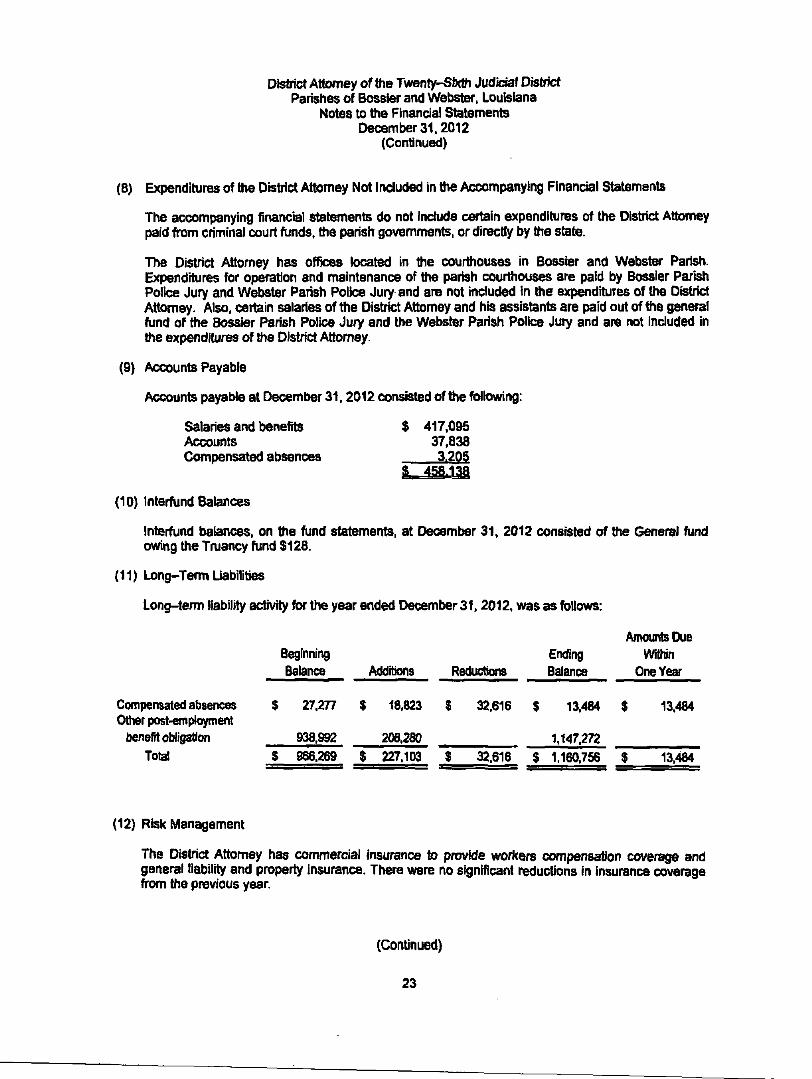

(8) Expendifores of ttie Distiict Attorney Not Included in ttie Accompanying Finandai Statemente

The accompanying financial stetemente do not Include certain expendifores of ttie District Attorney paid from criminal court fonds. ttie parish govemmente, or directty by ttie state.

The Distiict Attorney has offtoes tocated in ttie courthouses in Bosster and Webster Parish. Expendifores for operation and maintenance of tiie parish courthouses are paid by Bossier Parish Police Jury and Webster Parish Police Jury and are not included in ttie expendifores of ttie Distiict Attorney. Also, certain salaries of the District Attorney and his assistente are paid out of ttie general fond of ttie Bossier Parish Polu^e Jury and the Webster Parish Poltoe Jury and are not included in ttie expendifores of ttie Distiict Attorney.

(9) Accounte Payable

Accounte payabta at December 31,2012 consisted of the fbltowing:

Salaries and benefite Accounts Compensated absences

$ 417.095 37.838 3.20S

$ 458.138

(10) Interfond Balances

Interfond batances, on the fond statemente, at December 31. 2012 consisted of ttie General fund owing ttie Truancy fond $128.

(11) Long-Tenm Uabilities

Long-term liability activity fbr ttie year ended December 31.2012. was as follows:

Compensated absences Ottier post-employment

benefit obligation

Total

Beginning

Balance

$ 27.277

938.992

$ 966.269

Additions

$ 18.823

208.260

$ 227.103

Reductions

1 32,616

$ 32.616

Ending Balance

$ 13.484

1.147.272

$ 1,160.756

Amounts Due

vmn One Year

$ 13.484

$ 13.484

(12) Risk Management

The District Attorney has commercial insurance to provkife workers compensation coverage and general liability and property insurance. There were no significant reductions in insurance coverege from the previous year.

(Continued)

23

Distiict Attorney of tt>e Twenty-Sixtti Judtoial District Parishes of Bossier and Webster. Louisiana

Notes to ttie Financial Statemente December 31.2012

(Continued)

(13) Leases

The Distiict Attorney leases certain offtee space under operating leases. Rentel coste for ttie year ended December 31.2012 was $5,550. There are no commitinente under lease agreemente having terms in excess of one year.

(14) Ottier Post-Employment Benefite

Plan Description. The Distiict Attorney administers a single-emptoyer defined benefit Ottier Post Employment Benefit plan (OPEB). The Distttot Attorney's medtoal benefite are provtoed ttirough a comprehensive medical plan and are made available to emptoyees upon actual retirement

Most employees are covered by the Parochial Emptoyees' Retirement System of Louisiana, whose retirement eligibility (D.R.O.P. entry) provistons are as foitows: 30 years of servtoe at any age; age 55 and 25 years of senrice; age 60 and 10 years of servtoe; or. age 65 and 7 years of service. For employees hired on and after January 1. 2007. retirement etiglbilrty (D.R.O.P. entry) provistons are as follows: age 55 and 30 years of service; age 62 and 10 years of service; or. age 67 and 7 years of service. For the few employees not covered by that system, ttie same retirement eligibility has been assumed. Complete pten provisions are Included in the official plan documente.

Dentel Insurance coverage is provided to retirees. The employer pays 80% of the cost of the dentel Insurance for the retiree dependente. We have used the unbtended rates provided. Alt of ttie assumptions used fbr ttie valuatton of ttie medtoal benefite have been used for dentel insurance except for ttte trend assumption; zero Uend was used for dentel insurance. The dentel acfoarial coste and liabilities are induded In ttie medical resulte.

Life insurance coverage is avaitabte to retirees and ttie blended rate (active and retired) is approximately $0.24 per $1,000 of Insurance. The emptoyee pays 20% of ttie "cost" of ttie retiree life insurance, but it is based on ttie blended rate. Since GASB 45 requires ttie use of "unbtended" rates, we have used the 94GAR mortelity teble described above to "unblend" ttie rates so as to reproduce the composite btended rate overall as ttie rate strucfore to calculate ttie acfoarial valuatton resulte fbr life insurance. All of the assumptions used for the valuation of tine medtoal benefite have been used except for ttie hand assumption; zero ttend was used for life insurance. Retiree insurance coverage amounte are reduced to a flat $9,000. atthough certain current retirees have different amounte from prior schedules.

Contribution Rates. Employees do not contribute to their post emptoyment benefite coste until they t}ecome retirees and begin receiving those benefite. The plan provistons and contribution rates are conteined in the official pten documente.

Fund Policy. Until 2008, the Distiict Attorney recognized the cost of providing post-emptoyment medical and life insurance benefite (the District Attorney's portion of the retiree medtoal and life benefit premiums) as an expense when the benefit premiums were due and thus financed the cost of ttie post-employment benefite on a pay-as-you-go basis. In 2012 and 2011. ttie Distiict Attorney's portion of health care and life insurance fonding cost for retired emptoyees toteied $13,315 and $5,804. respectively.

Effective January 1, 2008, ttie Distiict Attorney implemented Government Accounting Stendards Board Stetement Number 45. Accounting and Financial Reporting by Employers for Post employment Benents Other than Pensions (GASB 45). This amount was applied tt)ward ttie New OPEB Benefit Obtigatton as shown in ttie following tabte.

(Continued) 24

Distttot Attomey of tiie Twenty-Sixtti Judicial Distiict Parishes of Bossier and Webster. Louisiana

Notes to the financial Statemente December 31.2012

(Continued)

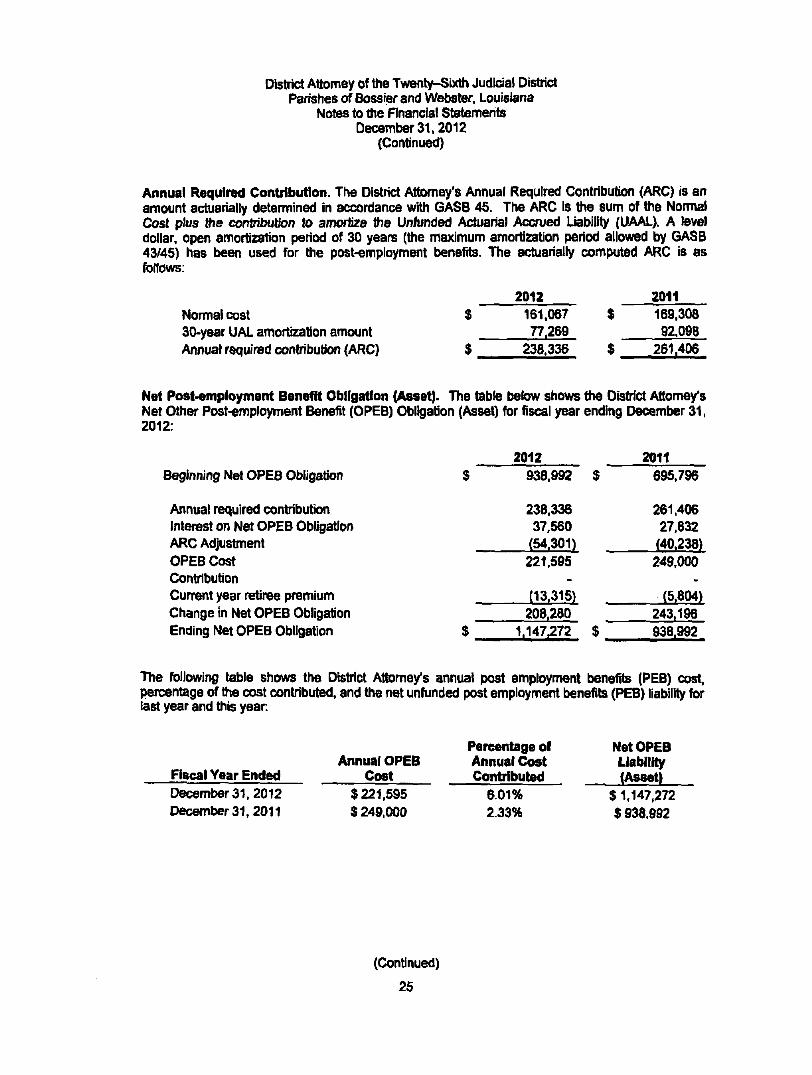

Annual Required Contribution. The District Attome/s Annual Required Contiibution (ARC) is an amount acfoarially detennined in accordance witti GASB 45. The ARC is the sum of the Nonmat Cost plus ttie contiibution to amortize ttie Unfonded Actuarial Accrued Uablllty (UAAL). A tevel dollar, open amortization period of 30 years (ttie maximum amortization period allowed by GASB 43/45) has been used for ttie post-employment benefite. The acfoarially computed ARC is as follows:

Nomial cost 30-year UAL amortization amount Annual required contribution (ARC)

2012 161.067 77.269

238.336

2011

169.308 92.098

$ 261.406

Net Post-employment Benefit Obligation (Asset). The teble betow shows the Distiict Attome/s Net Ottier Post-employment Benefit (OPEB) Obligation (Asset) for fiscal year ending December 31, 2012:

2012 2011 Beginning Net OPEB Obligation

Annual required contribution Interest on Net OPEB Obligation ARC Adjustment OPEB Cost Contiibution Current year retiree premium Change in Net OPEB Obligation Ending Net OPEB Obligation

938.992 $

238.336 37.560 (54.301)

221.595

(13,315)

208,280

1.147.272 $

695.796

261.406 27.832 (40.238)

249.000

(5.804)

243.196

938.992

The following table shows the Distiict Attome/s annual post employment benefite (PEB) cost, percentege of tiie cost conttibuted. and ttie net unfonded post employment benefite (PEB) liability for last year and this year.

Fiscal Year Ended December 31, 2012 December 31.2011

Annual OPEB Cost

$221,595 $ 249,000

Percentage off Annual Cost Contributed

6.01% 2.33%

Net OPEB Ltebllity (Asset)

$ 1.147,272 $ 938.992

(Continued)

25

District Attomey of ttie Twenty-Sixtti Judtoial Distiict Parishes of Bossier and Webster. Louisiana

Notes to ttie Rnanciat Stetemente December 31.2012

(Continued)

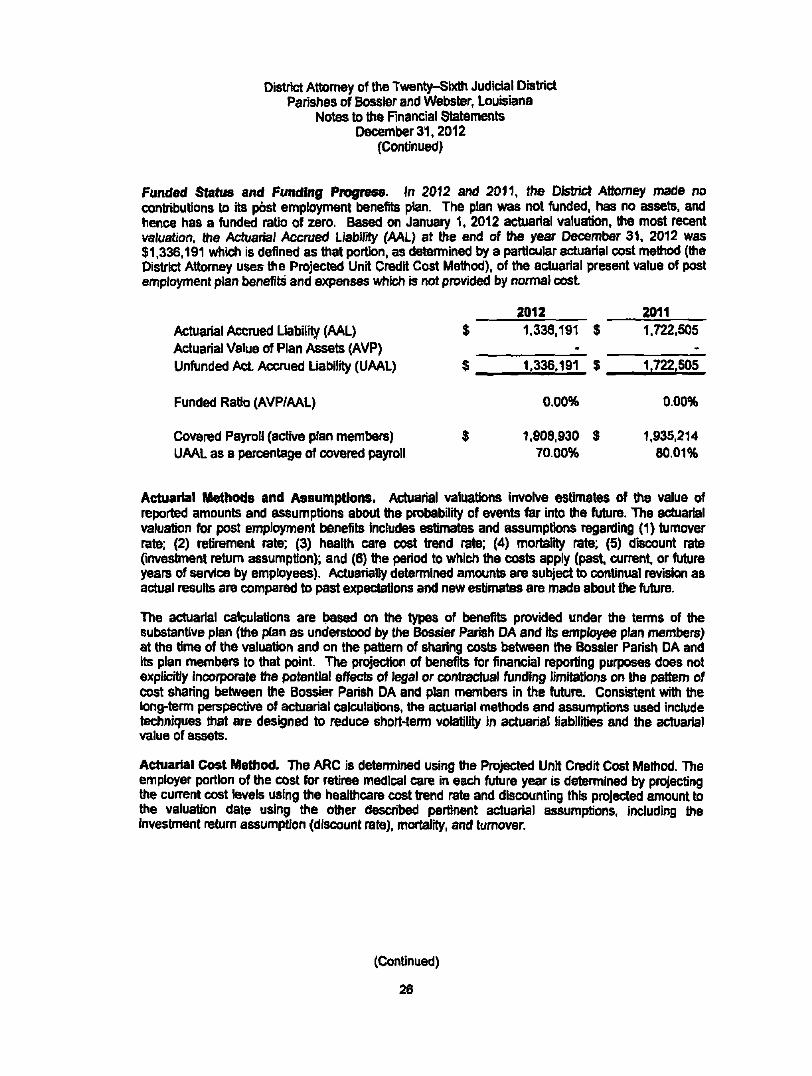

Funded Stetus and Funding Progress. In 2012 and 2011. ttie Disttict Attomey made no conttibutions to ite post emptoyment benefite plan. The plan was not fonded, has no assete. and hence has a fonded ratio of zero. Based on January 1. 2012 actuarial valuation, ttie most recent valuation, ttie Acfoarial Accrued Liat lJty (AAL) at ttie end of ttie year December 31. 2012 was $1,336,191 which is defined as ttiat portion, as determined by a particular acfoarial cost mettiod (ttie Disttict Attomey uses ttie Projected Unit Credit Cost Mettiod), of ttie actuarial present value of post employment plan benefite and expenses which is not provided by normal cost

2012 2011 Acfoarial Accrued Liability (AAL) Actuarial Value of Plan Assete (AVP) Unfonded Act Accrued Liability (UAAL)

Funded Ratio (AVP/AAL)

Covered Payroll (active plan members) UAAL as a percentege of covered payroll

Actuarial Mettiods and Assumptions. Acfoarial valuations i^vo^e estimates of ttie value of reported amounte and assumptions about ttie probability of evente far into ttie fufore. TYie actuarial valuation for post employment t^nefite Includes estimates and assumptions reganjlng (1) fomover rate; (2) retirement rate; (3i) health care cost ti^nd rate; (4) mortelity rate: (5) discount rate (invesbnent refom assumption); and (6) the period to which ttie coste apply (past, current or fufore years of service by employees). Acfoarially determined amounte are subject to continual reviston as acfoal resutts are compared to past expectations and new estimates are made about the fufore.

The acfoarial cak:ulations are based on ttie types of benefite provtoed under ttie terms of ttie substentive plan (the pten as understood by ttie Bossier Parish DA and ite emptoyee plan members) at the time of the valuation and on the pattern of sharing coste between ttie Bossier Parish DA and ite plan members to that point. The projection of benefite for financial repoiting purposes does not expltoitiy incorporete ttie potential effects of legal or contt3cfoal fonding limitetions on the pattern of cost sharing between ttie Bossier Parish DA and pten members in tiie fofore. Consistent with ttie tong-term perspective of acfoarial catoulations, the actuarial methods and assumptions used include techniques ttiat are designed to reduce short-term volatility In actuarial liabilities and the acfoarial value of assete.

Actuartel Cost Method. The ARC is determined using ttie Projected Unit Credit Cost Mettiod. The emptoyer portton of tiie cost for retiree medical care In each fufore year is determined by protecting ttie current cost levels using the healthcare cost trend rate and discounting this projected amount to ttie valuation date using the ottier described pertinent acfoarial assumptions, including ttie investtnent return assumption (discount rate), mortality, and turnover.

$

$

$

1,336,191 •

1.336.191

0.00%

1.908,930 70.00%

$

$ _

$

1,722.505

1.722.505

0.00%

1,935,214 80.01%

(Continued)

26

Distiict Attomey of ttie Twenty-Sbctti Judicial Disttict Parishes of Bossier and Webster, Louisiana

Notes to ttie Finandai Stetemente December 31.2012

(Continued)

Actuarial Value of Plan Assete. There are not any plan assete. It is anticipated ttiat in ttie fofore valuations, should fonding teke place, a smoottied maricet value consistent wiUi Acfoarial Standards Board Acfoarial Stendards of Practice Number 6 (ASOP 6). as pnsvided in paragraph number 125 of GASB Stetement 45.

Turnover Rate - An age-related fomover scale based on acfoal experience has been used. The retes, when applied to ttie ac^e employee census, produce a composite average annual fomover of approximately 5%.

Post employment Benefit Plan Eligibility Requirements. It Is assumed ttiat entitlement to benefite will commence three years after satisfaction of the minimum retirement/D.R.O.P. entry eligibility requiremente. Medical benefite are provided to employees upon acfoal retirement Most employees are covered by the Parochial Employees' Retirement System of Louisiana, whose retirement eligibility (D.R.O.P. entry) provistons are as follows: 30 years of service at any age; age 55 and 25 years of service; age 60 and 10 years of service; or, age 65 and 7 years of service. For employees hired on and after January 1. 2007, retirement eligibility (D.R.O.P. entty) provisions are as follows: age 55 and 30 years of service; age 62 and 10 years of sen/ice; or, age 67 and 7 years of service. For the few emptoyees not covened by that system, ttie same retirement el'^lbility has been assumed. Entitiement to benefite continue through Medicare to deatti.

Investment Return Assumption (Discount Ftate). GASB Stetement 45 states tiiat ttie investtnent refom assumption should be the estimated long-temi invesbnent yield on ttie investmente ttiat are expected to be used to finance ttie payment of benefite (ttiat is, for a plan which is fonded). Based on the assumption ttiat the ARC will not be fonded. a 4% annual investtnent refom has been used in ttils valuatton.

Health Care Cost Trend Rate. The expected rate of increase to medical cost is based on projections performed by ttie Office of ttie Acfoary at the Centere for Medicare & Medicaid Services as published in National Mealtti Care Expenditures Prpiections: 2003 to 2013. Tabte 3: National Healtti Expendifores. Aggregate and per Capita Amounte. Percent DIsttlbutton and Average Annual Percent Change by Source of Funds: Selected Calendar Years 1990-2013. released in January. 2004 by the Healtti Care Financing Administration (www.cms.hhs.gov). "State and Locaf rates for 2008 ttirough 2013 from ttite report were used, witti rates beyond 2013 graduated down to an ultimate annual rate of 5.0% for 2016 and later.

Mortality Rate. The 1994 Group Annuity Reserving (94GAR) tabte. projected to 2002. based on a fixed blend of 50% of ttie unloaded mate mortelity rate and 50% of tiie unloaded female mortality rates, was used. This is a published mortelity table which was designed to be used in determining ttie value of accrued benefite in defined benefit pension plans.

Method of Determining Value of Benefits. The "value of benefite" has been assumed to be ttie portion of ttie premium after retirement date expected to be paid by ttie employer for each retiree and has been used as the basis for calculating ttie acfoarial present value of OPEB benefite to be paid. The emptoyer pays 80% of ttte cost of ttie medical insurance for ttie retirees and dependente. The rates provided applicable before age 65 are "blended" rates. Since GASB 45 mandates ttiat "^unblended" rates be used, we have estimated ttie "unblended** rates for two broad groups: active and retired before Medicare eligibility. It has been assumed ttiat ttie retiree rate before Medicare eligibility is 130% of the blended rate.

(Continued)

27

Disttict Attomey of ttie Twenty-Sbctti Judtotel Disttict Parishes of Bossier and Webster. Louisiana

Notes to the Financial Statemente December 31,2012

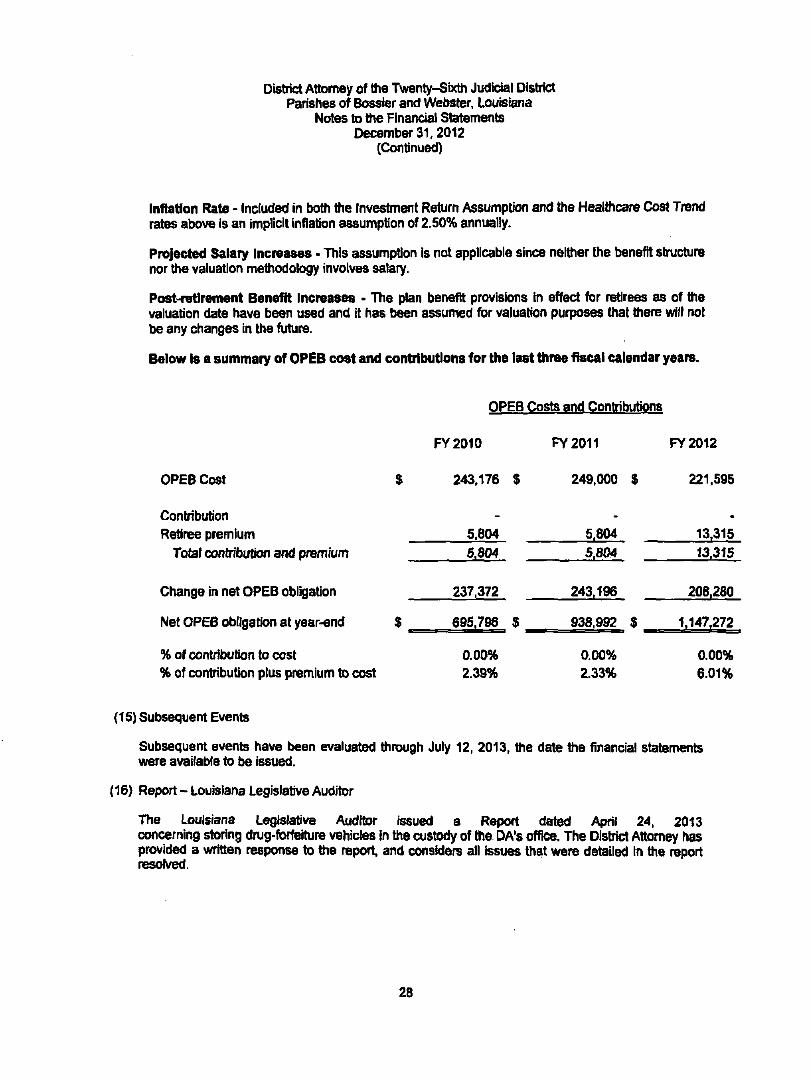

(Continued)

Inflation Ftate - Induded in botti ttie Investtnent Reforn Assumption and ttte Healtticare Cost Trend rates above Is an implicit inflation assumption of 2.50% annually.

Projected Salary Increases • This assumption Is not applicable since neither ttie benefit sbrucfore nor ttie valuation mettiodology involves salary.

Post-retirement Benefit Increases - The pten benefit provistons in effect for retirees as of ttie valuation date have been used and it has been assumed for valuatton purposes ttiat ttiere will not be any changes in the fufore.

Below to a summary of OPEB cost and contributions for the last three fiscal calendar years.

OPEB Coste and Conttibutions

FY 2010 FY 2011 FY 2012

OPEB Cost

Contiibution Retiree premium

Total contiibution and premium

Change in net OPEB obligation

Net OPEB obligation at year-end

% of contribution to cost % of contribution plus premium to cost

(IS) Subsequent Evente

Subsequent evente have been evaluated through July 12, 2013, ttie date the financial statemente were available to be issued.

(16) Report - Louisiana Legislative Auditor

The Louisiana Legislative Audttor issued a Report dated April 24, 2013 concerning storing drog-forfeifore vehictes in ttie custody of ttie DA's office. The Disttict Attomey has provided a written response to ttie report, and considers all issues tiiat were detailed in ttie report resolved.

$

$

243.176

5.804 5.804

237,372

695,796

0.00% 2.39%

$

$

249.000

5.804 5.804

243.196

938,992

0.00% 2.33%

$

—

_

$

221,595

• 13.315 13.315

206,280

1.147.272

0.00% 6.01%

28

Distiict Attomey of ttie Twenty-Sbctti Judicial Distiict Parishes of Bossier and Webster, Louisiana

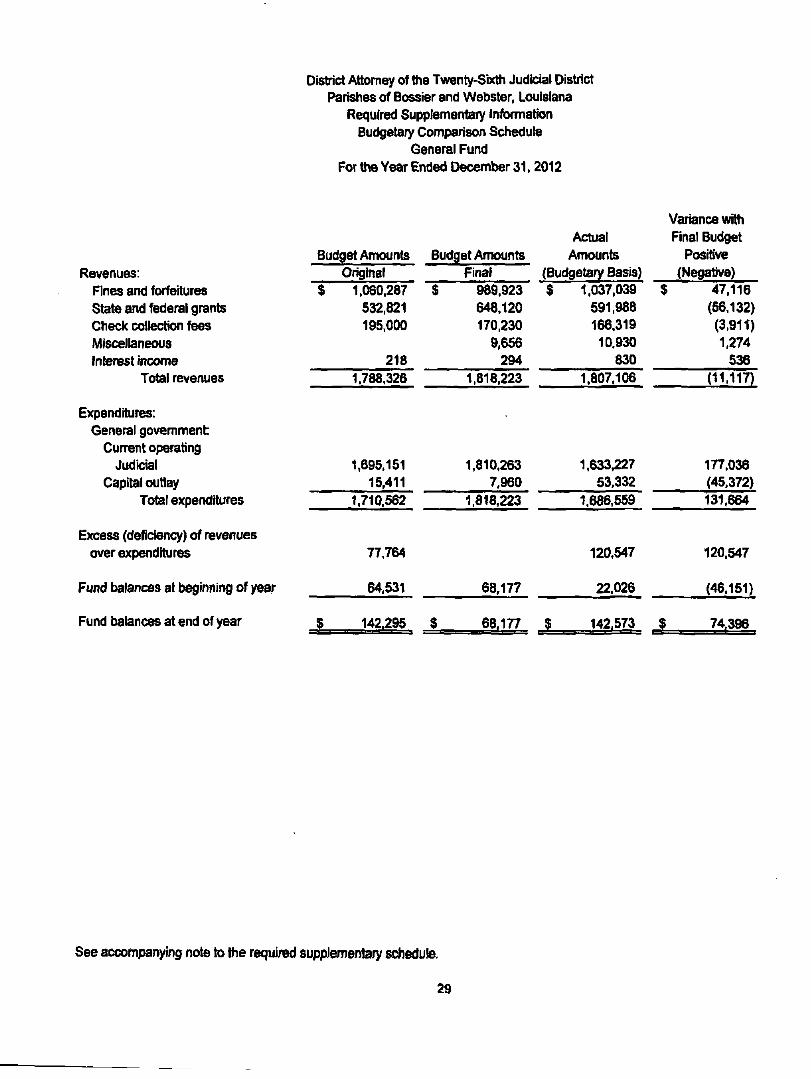

Required Supplementary Informatton Budgeted Comparison Schedule

General Fund For ttie Year Ended December 31.2012

Excess (deficiency) of revenues over expendifores

Fund balances at beginning of year

Fund balances at end of year

Revenues: Fines and forfeifores State and federal grante Check collection fees MIscelteneous Interest income

Total revenues

Expendifores: General govemment

Current operating Judicial

Capital outtay Total expenditures

Budget Amounte Original

$ 1.060,287 532,821 195.000

218 1,788.326

1.695.151 15.411

1.710.562

Budget Amounte Final

$ 989.923 648.120 170,230

9,656 294

1,818,223

1,810.263 7.960

1,818.223

Actual Amounte

(Budgetary Basis) $ 1,037,039

591,988 166.319 10.930

830 1,807.106

1.633.227 53,332

1,686.559

Variance Witti Final Budget

Positive (Negative)

$ 47.116 (56,132) (3.91t) 1,274

536 (11.117)

177.036 (45.372) 131.664

77,764

64,531

142_.295

68,177

120.547

22,026

68.177 $ 142.573 J ^

120.547

(46.151)

74.396

See accompanying note to ttie required supplementary schedute.

29

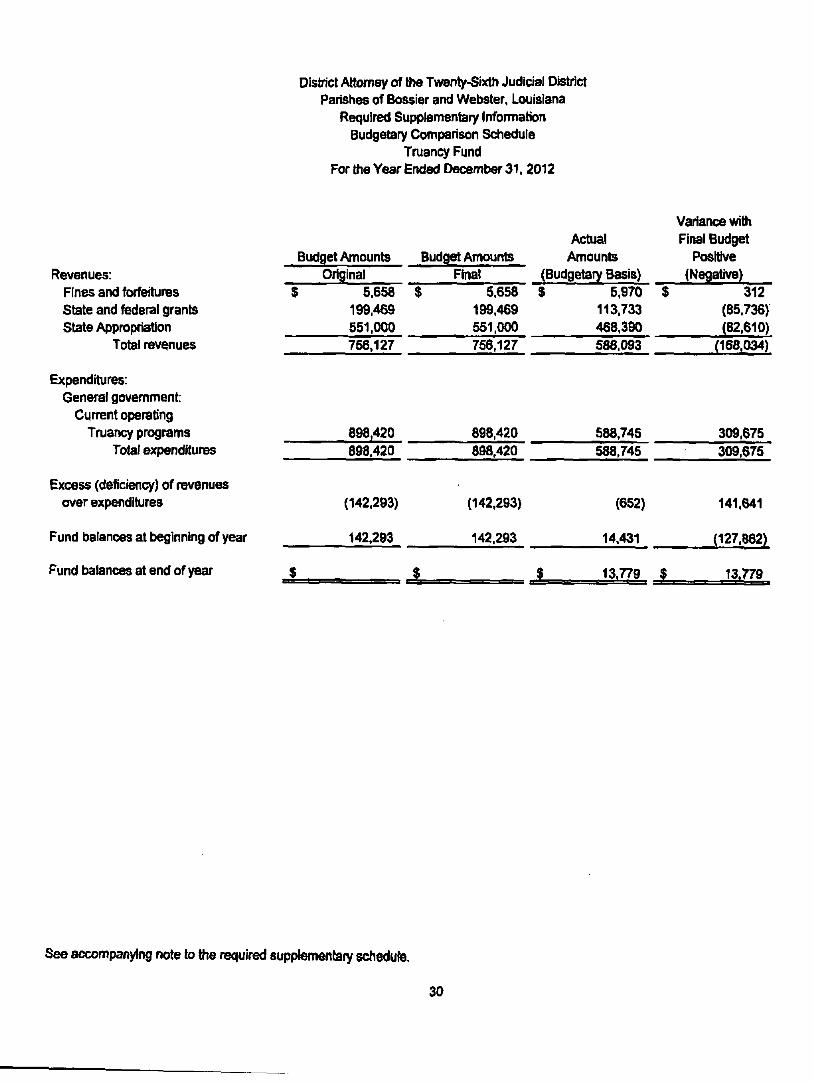

District Attomey of ttie Twenty-Sixtti Judicial Disttict Parishes of Bossier and Webster, Louisiana

Required Supplementary Infonmatton Budgetary Comparison Schedule

Truancy Fund For ttie Year Ended December 31, 2012

Revenues: Fines and forfeifores State and federal grante State Appropriation

Total revenues

Expendifores: General govemment:

Current operating Truancy programs

Total expenditures

Excess (deficiency) of revenues over expendifores

Fund balances at beginning of year

Fund batences at end of year

Budget Amounte Original

$ 5.658 199,469 551.000 756.127

898,420 898,420

(142.293)

142.293

$

Budget Amounte Final

$ 5.658 199.469 551,000 756.127

898,420 898.420

(142.293)

142,293

J

Acttjal Amounte

(Budgeta7 Basis) $ 5.970

113.733 468.390 588,093

J=

588.745 588,745

(652)

14.431

13.779

Variance witti Final Budget

Positive (Negative)

$ 312 (85.736) (82.610)

(168.034)

309,675 309,675

141.641

(127.862)

$ 13.779

See accompanying note to ttie required supplementary schedute.

30

District Attomey of ttie Twenty^bctti Judicial Disttict Parishes of Bossier and Webster, Loulstana Note to Required Supplementary Information

December 31,2012

Budget comparison schedute inducted in ttie accompanying financial statemente include the original adopted budgete and all subsequent amendmente. There was one budget amendment during 2012. The foilawing schedule reconciles excess (deficiency) of revenues and other sources over expendifores and other uses on ttie statement of revenues, expendifores and changes in fond batence (budget basis) witti amounte shown on ttie stetement of revenues, expendifores and changes in fond balances (GAAP basis):

General Fund

Excess (deficiency) of revenues over expendifores (budget basis)

Adjusttnente: Revenue accruals - net Expendifore accruals - net

Excess (deficiency) of revenues over expendifores (GAAP basis)

3.343 204.184

Truancy Fund

120.547 $ ( 652)

S 328074

139.247 i 157.328)

31

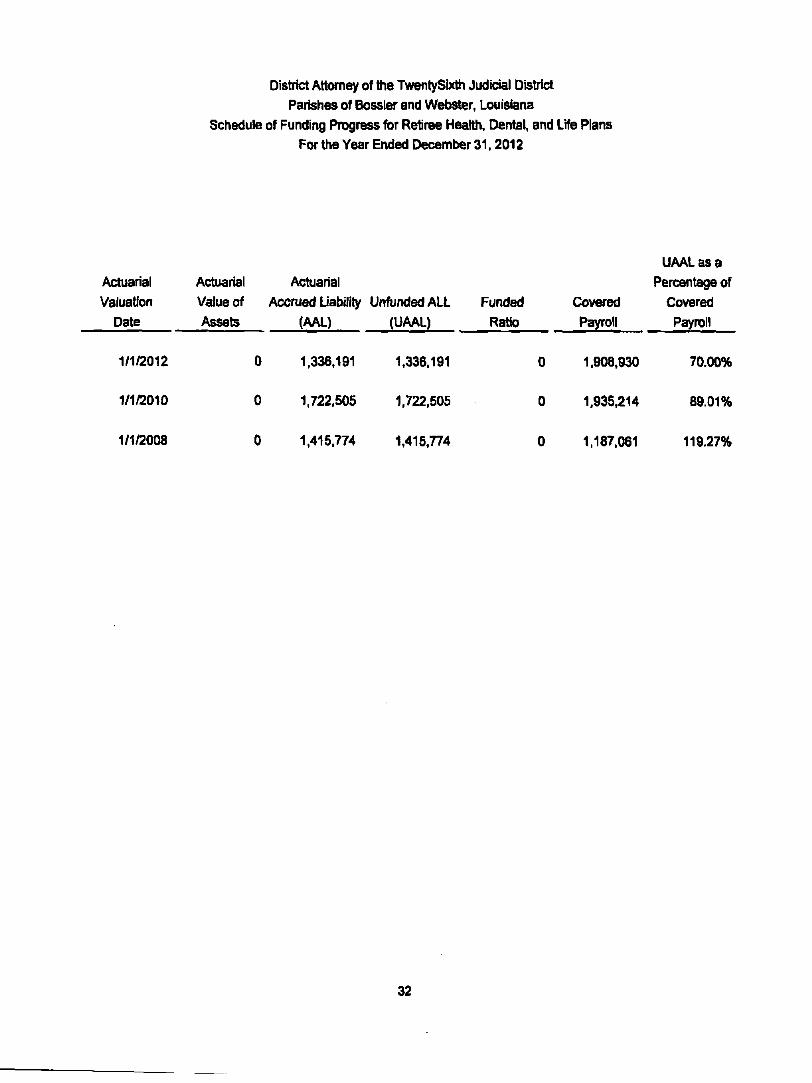

Disttict Attomey of ttie TwentySbctti Judicial Disttict

Parishes of Bossier and Webster, Louisiana

Schedute of Funding Progress for Retiree Meattti. Dental, and Lite Plans

For ttie Year Ended December 31,2012

Actuarial

Valuation

Date

Actuarial

Value of

Assete

Acfoarial

Accrued Uability Unfonded ALL

(AAL) (UAAL)

Funded

Ratto

Covered

Payroll

UAAL as a

Percentage of

Covered

Payroll

1/1/2012 1.336.191 1.336.191 1.908.930 70.00%

1/1/2010 0 1,722,505 1,722.505 1.935.214 89.01%

1/1/2008 1,415.774 1.415.774 0 1,187.061 119.27%

32

COOK & MOREHART

Certified PublieAccouHUmta

t i n HAWN AVB^aJE • S H R E V E P O R T . L O U I S I A N A T I 107• P ^ . B O X TOMO • S H R E V C P O R T , L O U I S I A N A 7 I U 7 - 8 2 < O

TTIAVIS H MOREHART. CPA TELEPHONE p l S ) tt^54^S FAX (JlSl 122-5441 A. EDWARD BALI, CP A VlOUfi D. CASE, CPA

MEtAER AMERICAN CNSTnUTE

STUART L REEKS, CPA CERTIFIED PUBUC ACCOUNT ANTS

SOCIETY OP LOUIStANA CERTtneD PUBliC ACCOUNTANTS

Report on Intemal Control Over FinarKiai Reoortinq and on Compliance And Other Matters Based on an Audit of Financial Statements

Peffbmoed In Accordance With Govemment AuditinQ Standards

Independent Auditor's Report

District Attomey of the Twenty-Sfxth Judicial District Parishes of Bossier and Wet>ster. Louisiana

We have audited, in accordance with auditing standards generally accepted in the United States of America and the standards applicable to the financial audits contained in Govemment Aud^ng Standards issued by the Comptroller General of the United States, the financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of the District Attomey of the Twenty-Sixth Judicial District as of and for the year ended Decemt)er 31, 2012. and the related notes to the ^ancia l statements, which collectively comprise the District Attomey of the Twenty-Sixth Judicial Districfs basic finandai statements, and have issued our report thereon dated July 12,2013.

Intemal Control Over Firianclal Reporting

In planning and performing our audit of the financial statements, we considered the District Attomey of the Twenty-Sixth Judicial District's intemal control over financial reporting (intemal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an o|»nion on the effectiveness of the District Attomey of the Twenty-Sixth Judicial District's internal control. Accordingly, we do not express an opinion on the effectiveness of the District Attomey of the Twenty-^ixtt) Judicial Disbicts intemal coritrol.

A deficiency in intemal control exists when the design or operation of a control does not allow management or employees, in the nomnal course of performing their assigned functions, to prevent, or detect and connect misstatements on a timely basis. A material weal<ness is a deficiency, or combination of deficiencies, in intemal control, such that there is a reasonable possibility that a material misstatement of the ent i t /s finandai statements win not be prevented, or detected and conBCted on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in intemal control that is less severe than a material wealcness, yet important enough to n^erit attention by those charged with governance.

Our consideration of intemal control over financial reporting was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in Intemal control that might be material weal(nes5es or significant defidencies. Given these limitations, during our audit we did not identify any deficiencies in intemal control that we consider to be material wealcnesses. However, material weaknesses may exist that have not been identified.

33

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the District Attomey of the Twenty-Sixth Judicial District's financial statements are f r i^ from material misstatanrtent, we perfomied tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effiect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an ot^ective of our audit and accordingly, we do not express such an opinion. The results of our tests disclosed an instance of noncompliance or other matters that is required to be reported under Govemment Auditing Standards and which is described in the accompanying Schedule of Audit Findings fbr Louisiana Legislative Auditor as item 2012-1.

District Attomey of the Twonty-Sbrth Judicial District's Response to Finding

The District Attomey of the Twenty-Sixth Judicial Districfs response to the finding identified in our audit is described in the accompanying Schedule of Audit Findings for the Louisiana Legislative Auditor The District Attomey of the Twenty-Sixth Judicial District's response was not subjected to the auditing procedures applied in the audit of the financial statements and. accordingly, we express no opinion on it

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of intemal control and complianoe and the results of that testing, and not to provide an opinion on the effectiveness of the entity's intemal control or on compliance. This report Is an integral part of an audit performed in accordance with Govemment Auditing Standards in considering the entity's internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Cooic & Morehart Certified Public Accountants July 12,2013

34