CHAPTER IV DISTRIBUTION CHANNELS OF LIFE INSURANCE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER IV

DISTRIBUTION CHANNELS

OF LIFE INSURANCE

Chapter 4

38

DISTRIBUTION CHANNELS OF LIFE INSURANCE

This chapter deals with the various aspects related to emergence of different

distribution channels after privatization of life insurance sector with a major focus on

the role of traditional distribution channels in insurance, emerging distribution channels

which are already in the adoption stream and ones to be adopted. Distribution channels

are the drivers which extends services to satisfy the demands of thousands of

customers. This chapter also looks at channel-wise performance of these in order to

create a platform of success for life insurance companies. When trying to achieve the

objective of this research, growth and financial analysis of distribution channels on life

insurance companies’ perspective was done and it was discovered that both public

sector insurer and private sector life insurance companies have adopted different

channels of distribution to deliver products and services to customers and it was

revealed that growth of channels is upwards which shows prospects of distribution

channels success in future.

4.1 Distribution Scenario in the Indian Market

In today’s Indian Insurance market, the challenge to insurers and intermediaries

is two-pronged:

Building faith about the company in the mind of the client

Intermediaries being able to build personal credibility with the clients

Prior to privatization, the only public sector insurer LIC was having the

monopoly in insurance sector.LIC was having its branches in almost all parts of the

country and it attracted people local people to become their agents..Traditionally, tied

agents had been the primary channel of insurance distribution in the Indian market. The

agents are from various segments in society and collectively cover the entire spectrum

of society. of course, the profile of the people who acted as agents, may not have been

sufficiently knowledgeable about the different products offered and may not have sold

the best possible product to the client. Nonetheless, the customer trusted the agent and

company. This arrangement worked adequately in the absence of competition.

Chapter 4

39

In today’s scenario, life insurance companies have adopted different channels

for distributing their products. A broad categorization of channels currently being used

in the distribution of life insurance products is presented in Figure 4.1

Figure 4.1

Distribution Channels of Life Insurance

Life Insurance companies have to provide servicing capabilities for the process

of sale, kind of products and demand of the customers as it differs significantly among

different distribution channels. This phenomena is explained in Figure 4.2. Which

shows that internet marketing does not involve direct interaction with the customer and

simple product will be suitable for the mass market segment. Figure 4.2 further

indicates that agency channel helps customers to plan their financial requirements by

personally interacting with them.

AGENCY

BANCASSURANCE

DIRECT

MARKETING

DISTRIBUTION

CHANNELS

BROKER

WORK SITE

MARKETING

INTERNET

MARKETING

CORPORATE

AGENCY

Chapter 4

40

Figure 4.2

Role of Distribution Channels in Purchase of Life Insurance Products

Individual

Advice

Customers

Mass

Market

Simple Products Complex

Source: www.shodhganga.inflibnet.ac.in

Bancassurance channel provides the same platform for banking and insurance

services. The customers are provided with well trained staff to access and plan their

financial security. It is further indicated that brokers play the role of one stop shop by

providing choice to the customers to make comparative analysis of insurance policies

of different life insurance companies and they provide the best suitable plan according

to the demand of the customer.

However, there is great excitement in the industry over the impending

regulations and companies are planning possible channels in their network to increase

volumes. The new companies have attempted appealing only to the middle, upper

middle and elite classes in the major cities. Contrasted with Life Insurance Corporation

of India and its offices across the country, the new companies have miles to go before

they reach anywhere. Both Life Insurance Corporation and private sector companies are

fighting their own battles from the perspective of customer perception management.

Internet

Marketing

Bancassurance

Agency

Broker

Chapter 4

41

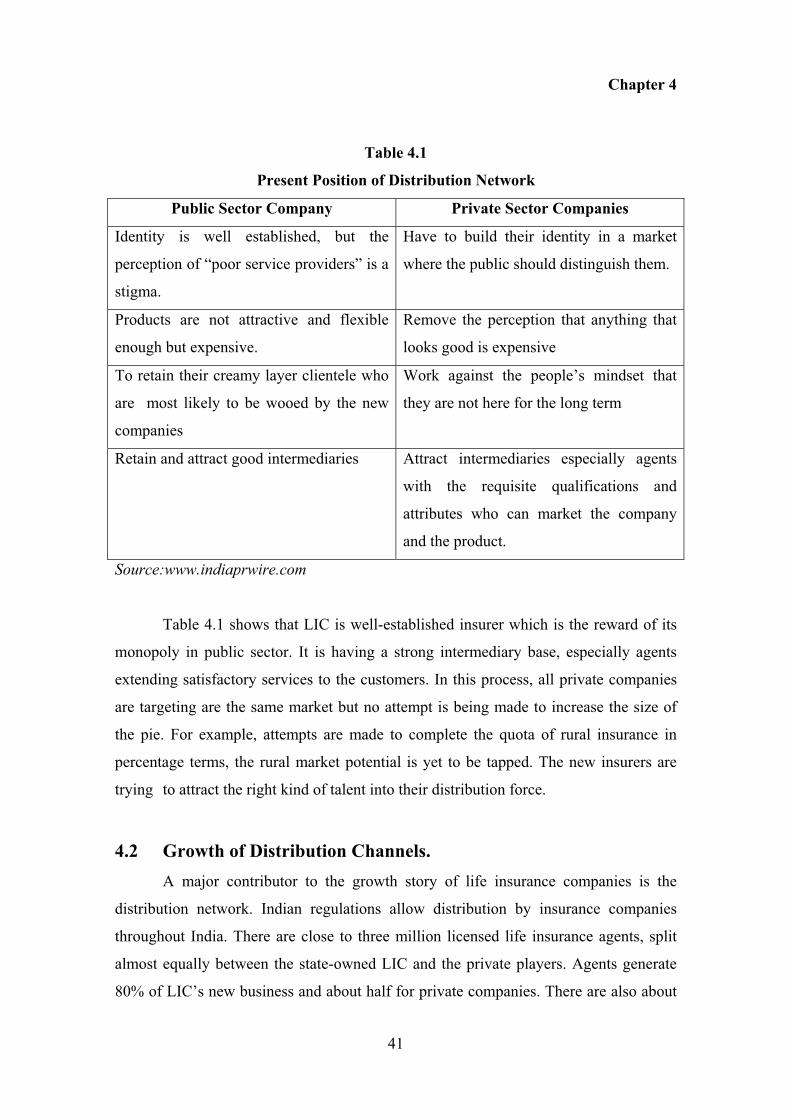

Table 4.1

Present Position of Distribution Network

Public Sector Company Private Sector Companies

Identity is well established, but the

perception of “poor service providers” is a

stigma.

Have to build their identity in a market

where the public should distinguish them.

Products are not attractive and flexible

enough but expensive.

Remove the perception that anything that

looks good is expensive

To retain their creamy layer clientele who

are most likely to be wooed by the new

companies

Work against the people’s mindset that

they are not here for the long term

Retain and attract good intermediaries Attract intermediaries especially agents

with the requisite qualifications and

attributes who can market the company

and the product.

Source:www.indiaprwire.com

Table 4.1 shows that LIC is well-established insurer which is the reward of its

monopoly in public sector. It is having a strong intermediary base, especially agents

extending satisfactory services to the customers. In this process, all private companies

are targeting are the same market but no attempt is being made to increase the size of

the pie. For example, attempts are made to complete the quota of rural insurance in

percentage terms, the rural market potential is yet to be tapped. The new insurers are

trying to attract the right kind of talent into their distribution force.

4.2 Growth of Distribution Channels.

A major contributor to the growth story of life insurance companies is the

distribution network. Indian regulations allow distribution by insurance companies

throughout India. There are close to three million licensed life insurance agents, split

almost equally between the state-owned LIC and the private players. Agents generate

80% of LIC’s new business and about half for private companies. There are also about

Chapter 4

42

3,000 corporate insurance agents, mostly banks, brokers and firms engaged in personal

loans. Bancassurance is now emerging as a key distribution channel through a network

of more than 70,000 branches of banks. Last year, banks generated about 20% of new

business for private life companies. Banks are the primary sales channel for a few

insurers such as HDFC Standard Life and SBI Life. They contribute about 40% of their

new business (Asia pacific insurance review, www.towerswatson.com).

The insurance market place is undergoing a transformation that may eventually

lead to significant changes in how consumers purchase insurance products. A variety of

distribution channels are currently used in this market place and some insurers utilize a

combination of distribution channels. These include the internet-led channels,

company-led channels, bank-led channels, and agent-led channels.

Although less frequently used, company-led distribution channels through

mediums such as direct mail or telephone call centers have seen increasing growth.

While an agent is still required in this setting, this person typically does not meet with

the insured. While it is true that insurance purchasers today have more options available

than they did five years ago, it is unclear if and when these channels will dominate

existing insurance distribution channels. Several obvious factors that impact on a

channel’s adoption are consumer attitudes and preferences (Trembly, 2001).

In India, the structure of economic development has undergone a considerable

change in the last decade with the service sector becoming a major part of the economy

contributing to more than 60% of real GDP in the last five years (RBI, 2010; IMF,

2010). Growth in the services sector has been substantive and has resulted in the

emergence of a new breed of larger more sophisticated service companies. Services

cover a wide gamut of activities like insurance, trading, banking & finance,

infotainment, real estate, transportation, security, management & technical consultancy

(Riddle, 1986).

Marketing of life insurance service is critical and complex for various obvious

reasons that include time span, periodicity and potentiality of claims and higher brand

switching costs affecting the buying behavior. In the present scenario, insurance

companies are facing problem of transiting from a perceived selling activity to a

structured strategic marketing activity. Insurance marketing is basically just the

marketing of life insurance products. Insurance marketing emphasizes the importance

Chapter 4

43

of the customer preferences and priorities. Major objectives of life insurance

distribution channels are to increase customer awareness, successful distribution of

insurance products, developing corporate image, improving customer service and

improving customer base. It is necessary to change the whole organizational

management structure of an insurance company, the channels of technologies of

communication with clients. Insurer has to analyze the nature of the customer’s needs

and plan their products and services in such a way that they can give satisfaction to the

customers and face the competitors. Planning needs analysis of the insurance market to

take a decision, prediction, and forecasting as to future needs of customers. All these

programs involve a number of functions (7Ps), which are to be planned carefully. The

combination of these functions is known as insurance service marketing mix

(Kotler,Bloom,1984).

Marketing mix is the planned package of elements, which will support the

organization in reaching its target markets and specific objectives. The marketing mix

has its origin in marketing of goods for consumer markets and consists of the well-

known 4Ps: Price, Promotion, Place and Product. Numerous modifications to the 4 Ps

have been proposed, the most concerted criticism came from the services marketing

area (Chakraborty, 2011).

4.3 Analysis of Distribution Channels

Distribution is a key determinant of success of all insurance companies. Section

4.3 states that in life insurance markets various insurance covers are provided either

directly or through various distribution channels individual agents, corporate agents

including bancassurance and brokers. These are generally called the traditional

channels. In today’s scenario agents continue as the prime channel for insurance

distribution in

India and almost all the players follow this model primarily. However, with new

developments in consumer behaviour, evaluation of technology and deregulation, new

distribution channels have been developed successfully and rapidly in recent years.

(Chakraborty, 2011).

To maximize reach in the market place, many insurers are aiming to derive

channel advantage because each channel has unique strengths. For example, a direct

Chapter 4

44

sales force is usually optimal for complex, high cost transactions where face-to-face

interaction is expected and required. Brokers and corporate agents can dramatically

expand market reach through local access and penetration. The internet can be used to

get the message out to untold millions, at an extremely low cost. The companies that

choose and cleverly integrate the right mix of channels can build go-to-market systems

that respond optimally to each of the requirements of the products and markets. They

can, for example, use expensive sales force representatives only to acquire and grow

the most important key accounts. They can then use brokers to reach dispersed groups

of smaller customers and to provide local sales support. They can use call centers to

close simple sales, generate sales leads for other channels and follow up on direct mail

campaigns. They can use the internet to reach customers who prefer to serve

themselves and want to save money. These efforts add up to a huge competitive

advantage in terms of revenue growth, market reach, customer loyalty and higher

productivity. (Rao, 2004).

4.3.1 Bancassurance

This section deals with analysis of bancassurance channel. Bancassurance in its

simplest form is the distribution of life insurance products through a bank’s distribution

channel. Insurance companies see bancassurance as a tool for increasing their market

penetration and premium turnover. It takes various forms in various countries

depending upon the demography, economic and legislative climate of that country. It

was introduced in India when insurance industry was opened up for private players. In

India, a bank can tie up with one general insurance and one life insurance Company as

mandated by IRDA bancassurance practice is yet to be much popular. (Singh, 2011).

The banking sector in India comprises of more than 67,000 branches and around 20

crore bank accounts.

Banks have expertise on the financial needs, saving patterns and life stages of

the customers they serve. A bank also has much lower distribution costs than insurance

companies and thus is the fastest emerging distribution channel. For insurers, tying up

with banks provides extensive geographical spread countrywide customer access; it is

the logical route for insurers to take.

Chapter 4

45

However, the evolution of bancassurance as a concept and its practical

implementation in various parts of the world, have thrown up a number of opportunities

and challenges. The motives behind bancassurance also vary. For banks, it is a means

of product diversification and a source of additional fee income. Insurance companies

see bancassurance as a tool for increasing their market penetration and premium

turnover. The customer sees bancassurance as a benefit in terms of reduced price, high

quality product and delivery at doorsteps.

4.3.1.1 Reasons behind Entry of Banks in Bancassurance Channel

By leveraging their strengths and finding ways to overcome their weaknesses,

banks could change the face of insurance distribution. Sale of personal line insurance

products through banks meets an important set of consumer needs. Most large retail

banks engender a great deal of trust in broad segments of consumers, which they can

leverage in selling them personal life insurance products. In addition, a bank’s branch

network allows face to face contact that is important in the sale of personal insurance.

Other bank strengths are their marketing and processing capabilities. Banks

have extensive experience in marketing to both existing customers (for retention and

cross selling) and non-customers (for acquisition and awareness). They also have

access to multiple communications channels, such as statement inserts, direct mail,

ATMs, telemarketing, etc. Banks’ proficiency in using technology has resulted in

improvements in transaction processing and customer service (Kumar, 2000)

Based on the above discussion, certain reasons for considering bancassurance

model can be explained as follows:

Life insurance premium represents 55% of the world insurance premium and as

the life insurance is basically a saving market. So, it is one of the methods to

increase deposits of banks.

Insurers operate through bancassurance, own and control relationships with

customers. Insurers found that direct relationships with customers gave them

greater control of their business at a lower cost. Insurers who operate through

the agency relationship are hardly having any control on their relationship with

their clients.

Chapter 4

46

The ratio of expenses to premium is an important efficiency factor. It is noticed

very well that expenses ratio in insurance activities through bancassurance is

extremely low. This is because the bank and the insurance company is

benefiting from the same distribution channels and people.

It is believed that the prospects for increased consolidation between banking

and insurance is more likely dominated and derived by the marketing

innovations that are likely to follow from financial service modernization. Such

innovations would include cross selling of insurance and increased use of

internet by consumers.

One of the most important reason of considering bancassurance by banks is

increased return on assets (ROA). One of the best ways to increase ROA,

assuming a constant asset base, is through fee income. Banks that build fee

income can cover more of their operating expenses, and one way to build fee

income is through the sale of insurance products. Banks those effectively cross-

sell financial products can leverage their distribution and processing capabilities

for profitable operating expense ratios.

Insurers have much to gain from marketing through banks as they have found it

difficult to grow using traditional agency systems because price competition has

driven down margins and increased the compensation demands of successful

agents. Over the last decade, life agents have sold fewer and larger policies to a

more upscale client base. Middle-income consumers, who comprise the bulk of

bank customers, get little attention from most life agents. By capitalizing on

bank relationships, insurers will recapture much of this underserved market.

Most insurers that have tried to penetrate middle-income markets through

alternative channels such as direct mail have not done well. Clearly, a change in

approach is necessary. As with any initiative, success requires a clear

understanding of what must be done, how it will be done and by whom. The

place to begin is to segment the strengths that the bank and insurer bring to the

business opportunity. (Karunagaran, 2006)

Chapter 4

47

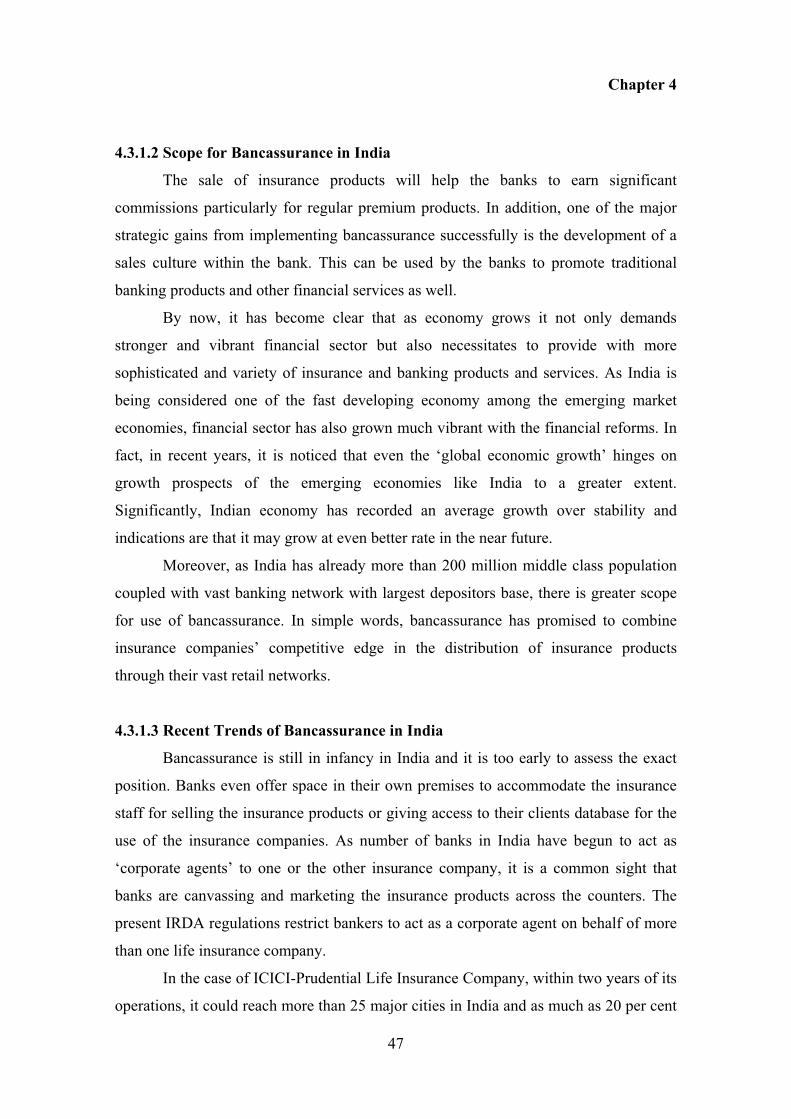

4.3.1.2 Scope for Bancassurance in India

The sale of insurance products will help the banks to earn significant

commissions particularly for regular premium products. In addition, one of the major

strategic gains from implementing bancassurance successfully is the development of a

sales culture within the bank. This can be used by the banks to promote traditional

banking products and other financial services as well.

By now, it has become clear that as economy grows it not only demands

stronger and vibrant financial sector but also necessitates to provide with more

sophisticated and variety of insurance and banking products and services. As India is

being considered one of the fast developing economy among the emerging market

economies, financial sector has also grown much vibrant with the financial reforms. In

fact, in recent years, it is noticed that even the ‘global economic growth’ hinges on

growth prospects of the emerging economies like India to a greater extent.

Significantly, Indian economy has recorded an average growth over stability and

indications are that it may grow at even better rate in the near future.

Moreover, as India has already more than 200 million middle class population

coupled with vast banking network with largest depositors base, there is greater scope

for use of bancassurance. In simple words, bancassurance has promised to combine

insurance companies’ competitive edge in the distribution of insurance products

through their vast retail networks.

4.3.1.3 Recent Trends of Bancassurance in India

Bancassurance is still in infancy in India and it is too early to assess the exact

position. Banks even offer space in their own premises to accommodate the insurance

staff for selling the insurance products or giving access to their clients database for the

use of the insurance companies. As number of banks in India have begun to act as

‘corporate agents’ to one or the other insurance company, it is a common sight that

banks are canvassing and marketing the insurance products across the counters. The

present IRDA regulations restrict bankers to act as a corporate agent on behalf of more

than one life insurance company.

In the case of ICICI-Prudential Life Insurance Company, within two years of its

operations, it could reach more than 25 major cities in India and as much as 20 per cent

Chapter 4

48

of the life insurance sales are through the bancassurance channel (Malpani 2004). In the

case of ICICI bank, SBI and HDFC Bank insurance companies are subscribers of their

respective holding companies. ICICI bank sells its insurance products practically at all

its major branches, besides it has bancassurance partnership arrangements with 19 other

banks as also as many as 200 corporate tie-up arrangements. Thus, among the private

insurance companies, ICICI Prudential seems to exploit the bancassurance potential to

the maximum. ICICI stated that Bank of India has steadily grown the life insurance

segment of its business since its inception. ICICI Prudential had also reported to have

entered into similar tie-ups with a number of RRBS, to reap the potential of rural and

semi-urban Aviva Life Insurance had reported that it has tie-ups with as many as 22

banking companies, which includes private, public sector and foreign banks to market

its products. Similarly, Birla Sun Life insurer reported to have tie-up arrangements with

10 leading banks in the country. A distinct feature of the recent trend in tie-up

arrangements was that a number of cooperative banks have entered into bancassurance

arrangement. This has added advantage for insurer as well as the cooperative banks,

such as the banks can increase the non-fund based income without the risk participation

and for the insurers the vast rural and semi-urban market could be tapped without its

own presence. Bancassurance alone has contributed richly to as much as 45 per cent of

the premium income in individual life segment of Birla Sun Life Insurer (Javeri, 2006).

Incidentally, even the only public sector player LIC reported to have tie-up with 34

banks in the country, it is likely that this could be the largest number of banks selling

single insurance company’s products. Ironically, LIC also has the distinction of being

the oldest and the largest presence of its own in the country. SBI Life Insurance for

instance, is uniquely placed as a pioneer to usher bancassurance into India. The

company has been extensively utilizing the SBI Group as a platform for cross-selling

insurance products along with its numerous banking product packages such as housing

loans, personal loans and credit cards.

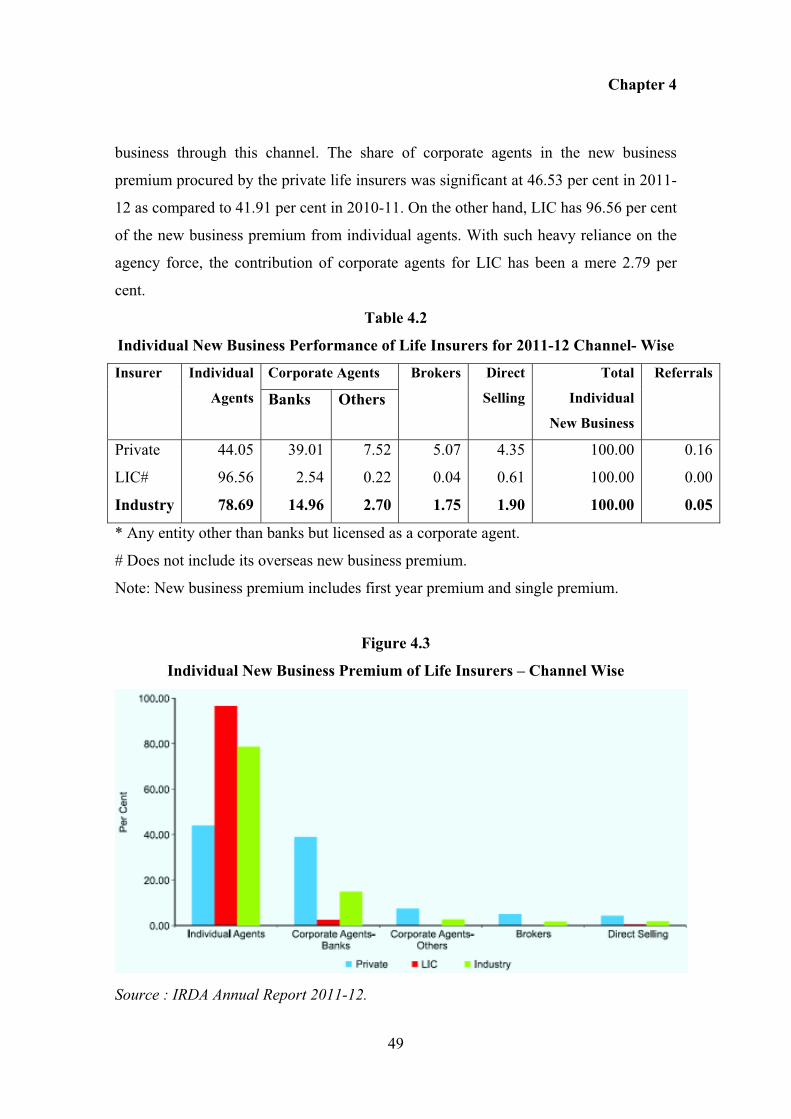

There has also been a decrease in the share of direct selling in the total

individual new business. Its share has gone down from 2.42 per cent in 2010-11 to 1.90

per cent in 2011-12. While private insurers have procured 4.35 per cent of their new

business through direct selling. LIC has procured only 0.61 per cent of their new

Chapter 4

49

business through this channel. The share of corporate agents in the new business

premium procured by the private life insurers was significant at 46.53 per cent in 2011-

12 as compared to 41.91 per cent in 2010-11. On the other hand, LIC has 96.56 per cent

of the new business premium from individual agents. With such heavy reliance on the

agency force, the contribution of corporate agents for LIC has been a mere 2.79 per

cent.

Table 4.2

Individual New Business Performance of Life Insurers for 2011-12 Channel- Wise

Corporate Agents Insurer Individual

Agents Banks Others

Brokers Direct

Selling

Total

Individual

New Business

Referrals

Private

LIC#

Industry

44.05

96.56

78.69

39.01

2.54

14.96

7.52

0.22

2.70

5.07

0.04

1.75

4.35

0.61

1.90

100.00

100.00

100.00

0.16

0.00

0.05

* Any entity other than banks but licensed as a corporate agent.

# Does not include its overseas new business premium.

Note: New business premium includes first year premium and single premium.

Figure 4.3

Individual New Business Premium of Life Insurers – Channel Wise

Source : IRDA Annual Report 2011-12.

Chapter 4

50

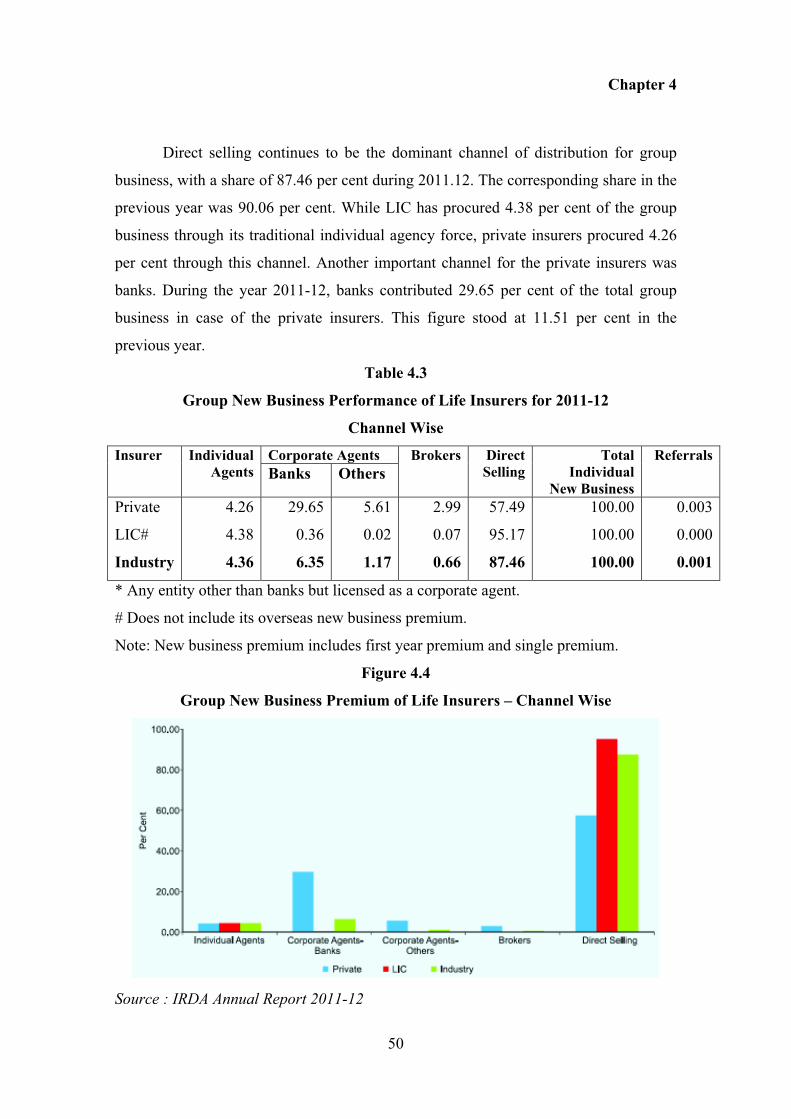

Direct selling continues to be the dominant channel of distribution for group

business, with a share of 87.46 per cent during 2011.12. The corresponding share in the

previous year was 90.06 per cent. While LIC has procured 4.38 per cent of the group

business through its traditional individual agency force, private insurers procured 4.26

per cent through this channel. Another important channel for the private insurers was

banks. During the year 2011-12, banks contributed 29.65 per cent of the total group

business in case of the private insurers. This figure stood at 11.51 per cent in the

previous year.

Table 4.3

Group New Business Performance of Life Insurers for 2011-12

Channel Wise

Corporate Agents Insurer Individual

Agents Banks Others

Brokers Direct

Selling

Total

Individual

New Business

Referrals

Private

LIC#

Industry

4.26

4.38

4.36

29.65

0.36

6.35

5.61

0.02

1.17

2.99

0.07

0.66

57.49

95.17

87.46

100.00

100.00

100.00

0.003

0.000

0.001

* Any entity other than banks but licensed as a corporate agent.

# Does not include its overseas new business premium.

Note: New business premium includes first year premium and single premium.

Figure 4.4

Group New Business Premium of Life Insurers – Channel Wise

Source : IRDA Annual Report 2011-12

Chapter 4

51

4.3.2 Brokers

Section 4.3.2 deals with broker regulations to be issued by IRDA and the

various aspects relating to working of the channel. The image that ‘broker’ carried in

the mind of the customer is not very favorable. Thus, the new breed of insurance

brokers faces the challenge of establishing credibility. The positives are that brokers in

the urban arena can attract the elite and the upper middle class customer. Brokers

represent the customer and will sell the products of more than one company. They seek

to determine the best fit for the client and can effectively address the mind block faced

by the public about the various companies. This is applicable in the case of life

insurance for the high-end and corporate group segment. However, the challenge lies in

establishing regulations that protect the customer and attract the right players into the

brokerage market rather than creating another middlemen segment eroding the

premium.

Insurance brokers are professionals who assess risk on behalf of a client, advice

on mitigation of that risk, identify the optional insurance policy structure, bring

together the insured and insurers. Brokers by definition are not tied to any one insurer

and have a chance to present as many options as possible to clients. Also, brokers have

a unique advantage as they can combine the life, non-life and health insurance

requirements of a client. This allows brokers to work with relatively smaller companies

in a profitable manner. Individual insurers and agents would not have the same

economies of scale in serving small clients. Brokers are constantly exposed to people

and product offerings of different companies. Brokers participate in training

programmes conducted by different companies. A few brokers are part of international

broking networks. This puts brokers in a unique position to understand market trends

and developments. A good broker will harness this information to create deep market

expertise. Such expertise has three main benefits. First, brokers educate clients about

product options and then push insurers hard to develop the appropriate products. The

result is a steady improvement in product quality. Second, brokers can express a

client’s case in language that insurers understand. Brokers bridge this gap. Thirdly,

brokers bridge the gap between insurer and insured (Chakraborty, 2011).

Chapter 4

52

People who have spent years in the industry take up the broking profession because it

provides the highest level of customer service and satisfaction. Entrepreneurs find that

the broking route provides them with excellent opportunities to serve customers in an

unbiased manner. The broker has to build customer servicing capability. In fact, the

ability of a broker to retain a client, quite often depends upon its servicing strengths.

When an insurance claim is made, it is the broker who is always the customer’s

champion and pushes the insurer towards timely and appropriate claim payment. No

insurer or agent can play this role adequately because of the inherent conflict of interest

between the claimant and the insurance company.

IRDA has significant role to play in strengthening the broker’s role in industry.

First, it should attract high quality talent and capital in the channel. The quality of the

players will be the foremost determinant of the development of the channel. Second,

IRDA should incentivize focus of pure protection solutions. The low ticket size of pure

protection plans and the current commission structure results in small absolute earnings

for the channel. In the backdrop of low consumer awareness, the cost of acquiring a

customer is high, hence the current compensation does not provide an economic

rationale of intermediaries to focus on such pure risk products, (IRDA Journal, Nov

2012).

4.3.3 Agency Channel

Agency is the largest distribution channel of almost all life insurance

companies, comprising a large advisor force that targets various customer segments.

The strength of agency channels lies in an aggressive strategy of expanding and

procuring quality business. With focus on sales & people development, tied agency has

emerged as a robust, predictable and sustainable business model.

All life insurance companies have an agency-building distribution strategy

under which they recruit, train, finance, and supervise their agent/advisers. For decades,

agency was the only distribution channel for life insurance in India. Even today more

than 70% of business is carried through insurance agents. Through agency channel,

personal contact and relationship can be established with the customer. The system of

agents is a major source of both presales and post sales services to customers, since it

has the direct relationship with customers. Due to personal contact, it can provide

Chapter 4

53

valuable feedback about the need and expectation of consumers. However, it is

nowadays considered as an old fashioned channel and not fully updated with latest

technologies. (Chakraborty, 2011).

Table 4.4

Details of Individual Agents of Life Insurers

Insurer As on 1st

April, 2011

Additions

during 2011-12

Deletions during

2011-12

As on 31st

March, 2012

AEGON RELIGARE 10861 5107 8655 7313

AVIVA 23219 8625 12718 19126

BAJAJ ALLIANZ 189667 70796 87317 173146

BHARTI AXA 15210 6754 7122 14842

BIRLA SUNLIFE 144573 32165 45441 131297

CANARA HSBC 0 0 0 0

DLF PRAMERICA 5199 2149 226 7122

EDELWEISS TOKIO 0 828 3 825

FUTURE GENERALI 52666 12402 23787 41281

HDFC STANDARD 136009 16259 46024 106244

ICICI PRUDENTIAL 190407 26747 78271 138883

IDBI FEDERAL 7882 2252 2734 7400

INDIAFIRST 296 1364 2 1658

ING VYSYA 34957 20301 25862 29396

KOTAK MAHINDRA 38269 12263 19235 31297

MAX LIFE 43542 18443 26617 35368

METLIFE 28840 9894 9316 29418

RELIANCE 189433 45999 84842 150590

SAHARA 14180 415 17 14578

SBI LIFE 79628 49609 42248 86989

SHRIRAM LIFE 10139 202 3961 6380

STAR UNION DAI-ICHI 128 422 0 550

TATA AIA 87223 25215 65490 46948

PRIVATE TOTAL 1302328 368211 589888 1080651

LIC 1337064 345917 404747 1278234

INDUSTRY TOTAL 2639392 714128 994635 2358885

Source : IRDA Annual Report, 2011-12

Chapter 4

54

Today’s insurance agents has to know which product will appeal to the customer, and

also know his competitor’s products in the same space to be an effective salesman who

can sell his company, the product and himself to the customer. To the average

customer, every new company is the same.

Figure 4.5

Factors Affecting Performance of Agents

Source: www.shodhganga.inflibnet.ac.in

Agent

Recruitment

Agent

business

startup

plan

Agent

meeting the

customer

Agent

assisting the

customer

Follow up

and service

calls

Taking

reference

from

customer

Performance

of an Agent

Chapter 4

55

The new companies are looking for educated, aware individuals with marketing

flair, an elite group who can be attracted only with high remuneration, all of which may

not be possible in this business with its price pressures and the complexity of selling

insurance. Unable to attract this segment, they have started easing recruitment

conditions as against the stringent norms they had earlier, thereby diluting the process.

While the public sector insurer LIC is able to attract agents, it continues to suffer from

high attrition rates due to indiscriminate agent appointment. The challenge here is the

lack of knowledge of the competitive market and the inability to do intelligent

comparisons with the competitor’s products. Education and training of these agents is a

serious challenge for the insurance company.

Another social feature in the market is the considerable respect for age in Indian

society and a belief that an older person knows better. A very young up- market agent

who is typical salesman may not appeal to a large segment of the middle class, which is

looking for a solid trustworthy person from whom they can buy insurance.

Gender of agents is another relevant feature in the rural context that makes a

difference, especially for the female population. Women to whom the customers can

relate e.g. nurses, gram sevikas can target the female segment of the population more

effectively. What is applicable for the rural women and children health programs and

population control programs is equally applicable for insurance selling also. Max Life

has adopted a version of this strategy by appointing gram sahayaks to sell and service

the rural customers. With this kind of segmentation of intermediaries the challenge for

the insurance company lies in training and education these people to become effective

sales persons (Lakhsmikutty and Baskar, 2007).

4.3.4 Internet Marketing

The growth of the Internet has led to a great deal of speculation and discussion

regarding its potential impact on traditional distribution channels. Though India is

joining the fast growing breed of net users, using net for transactions has not yet caught

up. Though few companies provide online insurance service, the usage is still a small

fragment. The insecurity associated with transactions over the net is still an inhibiting

Chapter 4

56

factor. At present, most of the insurance companies have product information and

illustrative tools available on the web. But web is not seen evolving into a means for

direct selling of insurance in the current scenario. In the Indian market, where insurance

is sold after considerable persuasion and face to face selling, selling over the net which

must be initiated by the client, would take some more time (Gilbert and Bachedler,

2000).

While the adoption rate of the Internet as a distribution channel has been low,

companies have seen widespread adoption of the Internet as a support channel. Insurers

are using the Internet to provide general information of financial services products

(e.g., insurance, investments) and planning involving the use of these products, to

provide specific information of the company and its product lines, to provide

administrative support to its policyholders and to serve as a prospecting and

communication tool for its agent-led channel (Dumm,Hoyt 2002).

Rogers (1995) suggested that widespread diffusion of an innovation will lead to

significant changes in the market channels themselves. As noted above, we have seen

widespread diffusion of the usage of the internet in insurance industry. However, the

adoption patterns have been quite different in different companies. Internet helps to

collect information for consumers. It is a two-stage process. The consumers first use the

Internet to collect information on products or services. They, then return to the agent to

complete the purchase. This behavior highlights the current role that the Internet plays

in providing support to the agent-led channel (Dumm, Hoyt 2002).

Initially, insurance was seen as a complex product and buyers preferred face-to-

face interactions with intermediaries. Now a days, the advantage of technology allows

insurers to increase their reach into the market. All insurers have websites through

which they provide information about products and services. In India, internet

penetration is still low legality of agreements is posing a difficult problem. The

insecurity associated with transactions over the net is still an inhibiting factor. Internet

has not been evolved into a means for direct selling of insurance in the current scenario.

In the Indian market, where insurance is sold after considerable persuasion even after

face-to-face selling, the selling over the net, which must be initiated by the client,

would take some more time (Chakraborty, 2011).

Chapter 4

57

4.3.5 Worksite Marketing

Worksite marketing is the distribution method providing voluntary insuance

products to employees at their work place with the sponsorship of their employer,

which is done on a deduction from their payroll. The contract for insurance is directly

made with the employee rather than the employer.

Benefits to the Insurer:

o Captive customer base

o Potential to sell individual insurance and group insurance

o High trust factor

o High hit ratio for the intermediaries

The challenges would be the cost effectiveness, product customization and

efficient post sales servicing, which would determine continued business. Technology

has a key role to play in worksite marketing to ensure cost benefits. Banks and financial

institutions have been successfully marketing credit cards and other financial products

using this channel (Laksmikutty and Baskar, 2006).

In this channel, life insurers send team to a target group and explain the

products either individual or group products suitable to them. The target group may be

employees of a particular company or an educational institute. Insurance companies

will be able to sell insurance products particularly, pension and health plans through

this channel. One possible reason for insufficient development of this channel in India

is that employers generally expect some kind of incentive to provide the facilities to the

life insurers for making presentations and making arrangements for deduction of

premium from salaries. With changes in human resources management polices and

compensation packages, group products or work site products do have a definite market

that cannot be ignored (Chakraborty, 2011).

Insurance companies have provided coverage with mix of group and individual

products. These include traditional group insurance products that have become

“voluntary” because the employee is now required to pay either some or all of the

premium, portable group insurance products that employees can take with them when

they change jobs and individual products of many kinds, including life insurance, long

Chapter 4

58

term care, disability, auto, home owners, critical illness, and annuities. Till date, many

insurance companies have been disappointed by low penetration for worksite marketed

products. The transition from defined benefit to defined contribution pension plans are

used to provide perspective on possible changes in life and health insurance products

sold in a worksite setting.

Numerous factors are important for these sales – innovative product design,

competitive pricing, superior marketing material. However, the most important

expertise is enrollment – actually signing up employees for the insurance coverage. In

today’s worksite business model, the insurers who open new employer account are

primarily responsible for enrolling employees, either by doing it themselves or

outsourcing the task .This enrollment procedures often do an inadequate job of

educating and counselling employees about their benefit choices and often do not

support the application process well, e.g. leaving employees to fill out their own forms.

The result is that employee enrollment often falls below target goals, raising unit costs

and threatening the insurer’s profitability. There are always more new customer

opportunities, which offer higher premium potential and consequently higher

commissions.

The emergence of worksite marketing from a small niche of the insurance

market to a major distribution channel depends on the integration of new technologies

with traditional distribution methods. This new marketing and sales platform will

generate substantially higher sales and customer satisfaction at reduced costs. The

future prospect for the worksite channel is extremely promising. But competing in the

worksite arena today requires the ability to do worksite marketing. Commitment and

focus are needed, but are not enough to guarantee success (News Direct Newsletter,

Fall 2000).

4.3.6 Corporate Agency Channel

The corporate agency channel is a key one for life insurance companies and it is

facing stringent licensing guidelines. Since April 2012, the life insurance industry has

lost nearly a third of its corporate agents, while for most of the bigger private life

insurers, the number has shrunk by more than 50 per cent. For instance, HDFC Life

now has only 10 corporate agents, compared with 374 in April 2010. Bajaj Allianz Life

Chapter 4

59

evidenced decline of 66 per cent. Life Insurance Corporation (LIC) of India has

reduced the number of corporate agency tie-ups by 42 per cent during the period

(Bhattacharya, 2012).

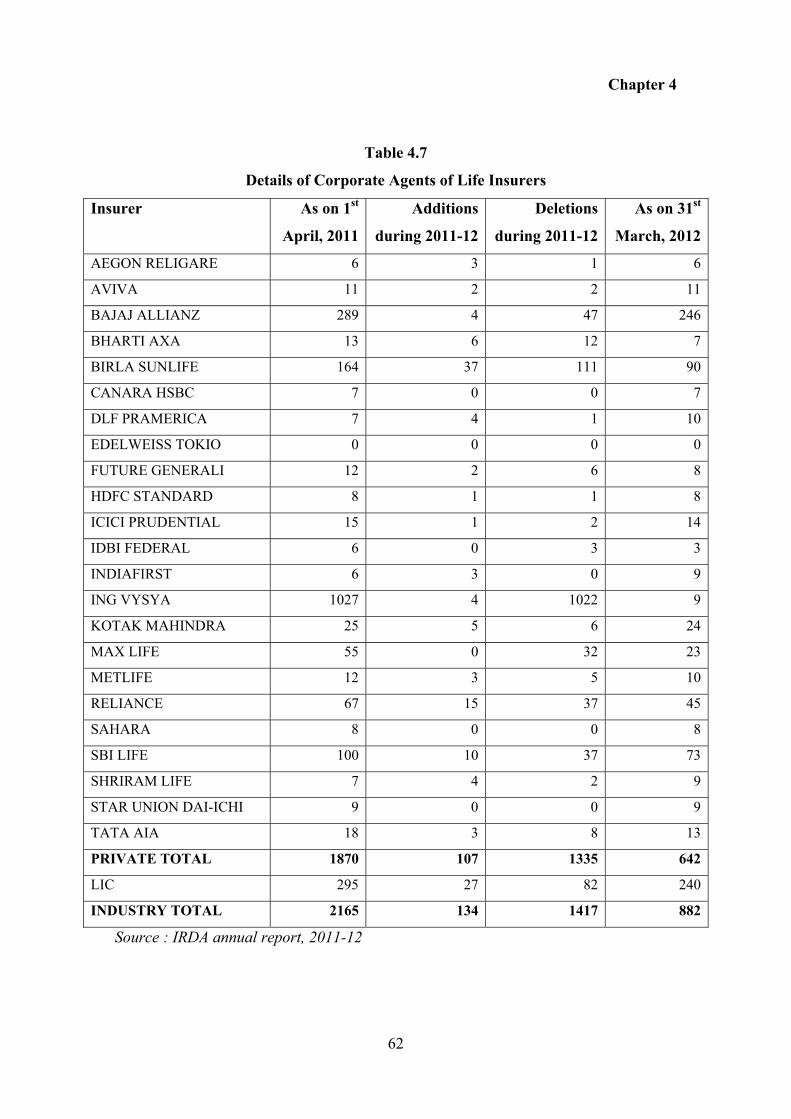

4.3.6.1 Details of Corporate Agents of Life Insurers and Number of Policies Sold

Table 4.5 shows that there was a noticeable change in the number of corporate

agents in year 2011-12 in comparison to 2010-11 due to strict IRDA regulations. At

present, in private sector life insurance companies 642 corporate agents are working

and incase of LIC there are 240 corporate agents.

Table 4.5

Details of Corporate Agents of Life Insurers

Insurer As on 1st

April, 2011

Additions during

2011-12

Deletions during

2011-12

As on 31st

March, 2012

Private

LIC

Industry

1870

295

2165

107

27

134

1335

82

1417

642

240

882

Source : Indian Insurance Statistics 2011-12

Figure 4.6

Details of Number of Corporate Agents

Source : Indian Insurance Statistics 2011-12

Chapter 4

60

Over the years, there has been a perceptible shift away from the individual agency

channel. The contribution to the new business premium procured through individual

agents has slightly decreased to 78.69 per cent during 2011-12 from 78.95 per cent

reported during the previous year. The share of corporate agents, which was 16.86 per

cent during 2010-11, has increased to 17.67 per cent in the year 2011-12.

Since the new guidelines on the corporate agency channel were introduced,

many small corporate agents have made a quit. Hence, the numbers have come down.

The main focus remains the traditional agency channel, which accounts for nearly 65

per cent of total new business.. After introducing stringent guidelines on licensing of

corporate agents in June 2012, which tightened the licence renewal process, IRDA also

recommended regular on-site inspection of corporate agents to curb various

malpractices that had crept into the system. There have been many instances in which

the same set of individuals have floated different corporate agencies and employed

people without valid licences for selling products. With IRDA’s regular

recommendations regarding on-site inspection of corporate agents, these companies are

getting out of the system (Bhattacharya, 2012). The movement of the number of

corporate agents.

Table 4.6

Analysis of Average Number of Policies Sold

AVERAGE NUMBER OF INDIVIDUAL POLICIES SOLD BY

CORPORATE AGENTS

2007-08 2008-09 2009-10 2010-11 2011-12

Private

LIC

Industry

1798

1905

1815

1857

2190

1908

2289

1606

2172

1976

1708

1933

2533

2194

2474

Source: IRDA annual report, 2011-12

Chapter 4

61

Figure 4.7

Average Number of Policies Sold

Source: IRDA annual report, 2011-12

From the Table 4.6, it is observed that the average number of individual policies

sold by the corporate agents of LIC has shown significant increase during the last two

years. The share of business in number of individual policies of private insurers and

LIC is exhibited in Table 4.6. It is interesting to see that the share of individual policies

sold through corporate agents of the private insurers is increasing over the years.

4.3.6.2 Details of Corporate Agents of Life Insurers

This section deals with detailed number of corporate agents of life insurance

companies presently operating in India along with additions and deletions.

Chapter 4

62

Table 4.7

Details of Corporate Agents of Life Insurers

Insurer As on 1st

April, 2011

Additions

during 2011-12

Deletions

during 2011-12

As on 31st

March, 2012

AEGON RELIGARE 6 3 1 6

AVIVA 11 2 2 11

BAJAJ ALLIANZ 289 4 47 246

BHARTI AXA 13 6 12 7

BIRLA SUNLIFE 164 37 111 90

CANARA HSBC 7 0 0 7

DLF PRAMERICA 7 4 1 10

EDELWEISS TOKIO 0 0 0 0

FUTURE GENERALI 12 2 6 8

HDFC STANDARD 8 1 1 8

ICICI PRUDENTIAL 15 1 2 14

IDBI FEDERAL 6 0 3 3

INDIAFIRST 6 3 0 9

ING VYSYA 1027 4 1022 9

KOTAK MAHINDRA 25 5 6 24

MAX LIFE 55 0 32 23

METLIFE 12 3 5 10

RELIANCE 67 15 37 45

SAHARA 8 0 0 8

SBI LIFE 100 10 37 73

SHRIRAM LIFE 7 4 2 9

STAR UNION DAI-ICHI 9 0 0 9

TATA AIA 18 3 8 13

PRIVATE TOTAL 1870 107 1335 642

LIC 295 27 82 240

INDUSTRY TOTAL 2165 134 1417 882

Source : IRDA annual report, 2011-12

Chapter 4

63

In an overall sense, the new guidelines bring some discipline into the system.

The insurers will incur additional expenditure if it has to monitor the compliance of its

corporate agents. The decision has to permit only insurance qualified persons to man

the corporate agency, the Met Life has start up with capital of Rs. 15 Lakh, appeared

high and would restrict the small professional players from entering the business. The

old regulations permit partnership firms and sole proprietorships to act as corporate

agents.. IRDA restricting multiple corporate agencies with different insurers and

prohibition of sub-agencies and other intermediaries under the corporate agents will

prove to be a positive step (www.indiaprwire.com).

4.3.7 Direct Marketing Channel

Section 4.3.7 deals with the details about another key distribution channel that is

direct marketing. Direct marketing means selling products by dealing directly with

consumers rather than through intermediaries. More recently telemarketing, direct radio

selling, magazine and T.V advertising, and on-line computer shopping have been

developed.

4.3.7.1 Benefits of Direct Marketing

There is no need to share profit margins and the insurer has complete control

over the sales process.

There may also be specific market factors that encourage direct selling.

There may be a need for an expert sales force, to demonstrate products, provide

detailed presale information and after-sales service.

Retailers, distributors, dealers and other intermediaries may be unwilling to sell

the product.

Existing distribution channels making it hard to obtain clientele like direct

marketing channel.

Insurers have resorted to direct marketing wherein insurance companies get in

touch with the customers without the aid of an intermediary. A separate department

has been set up and officers were deputed to solicit and administer insurance

Chapter 4

64

business. The advantage of this system is the reduction of cost incurred by the

agency system. Company owned sales team concept is now employed by a majority

of new players and has proved more effectiveness in customer creation and

retention. However, as compared to the system of agents, contribution of direct

marketing is considerably low. It was reported that contribution of direct marketing

channel in case of public sector insurer is 26.86% and private sector life insurance

companies is reported as 23.63%) in the year 2010-11 (Chakraborty, 2011).

This chapter highlights different distribution channels of life insurance

companies available for conducting insurance business. Intelligent segmentation of

these channels to match the market segmentation is something indispensible that

will help the companies to move towards the appropriate direction. The choice of

right channel lies on the hands of insurance companies, to make sure that they have

fulfilled the demands of their customers. These channels are identified as the prime

driver for growth of any organization. Distribution channels are the enabling

mechanism through which organizations ensure that their products and services

reach the market and it also decides the growth graph of companies. The identified

challenges are impacting and hindering the fast developing distribution scenario in

the insurance industry. Social, legal, corporate and many other factors were

identified to have slowed down the fast pace of distribution network.

Related Documents