International Journal of Industrial Organization 18 (2000) 773–792 www.elsevier.com / locate / econbase Distinction between intermediate and finished products in intra-firm trade a b, * ¨ Thomas Andersson , Torbjorn Fredriksson a ´ OECD/ DSTI, 2, rue Andre Pascal, 75775 Paris Cedex 16, France b Invest in Sweden Agency ( ISA), Box 90, 10121 Stockholm, Sweden Received 28 April 1994; accepted 31 August 1998 Abstract Although intra-firm trade has been viewed as associated with vertical integration, which exploits opportunities for exchange between inherently dissimilar economies, it is more common between developed countries where horizontal integration is expected to dominate. Using unique data from 1974 to 1990 on Swedish firms, application of a Tobit model explains variations in majority-owned manufacturing affiliates’ internal imports of inter- mediate and finished goods on the basis of firms’ international organization of production. Effects which are unobservable in aggregate figures show up only when finished and intermediate goods are separated. 2000 Elsevier Science B.V. All rights reserved. Keywords: Multinational firms; Intra-firm trade; Vertical and horizontal integration JEL classification: F23; L22; L23 1. Introduction The expansion of foreign production by multinational enterprises (MNEs) exerts a major impact on the direction, magnitude and composition of trade flows. One of the most conspicuous effects is the phenomenal increase in intra-firm transactions. UNCTAD (1996) estimates that one-third of all international trade occurs within * Corresponding author. Tel.: 146-8-4027815; fax: 146-8-4027878. 0167-7187 / 00 / $ – see front matter 2000 Elsevier Science B.V. All rights reserved. PII: S0167-7187(98)00041-1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Journal of Industrial Organization18 (2000) 773–792

www.elsevier.com/ locate /econbase

Distinction between intermediate and finished products inintra-firm trade

a b ,*¨Thomas Andersson , Torbjorn Fredrikssona ´OECD/DSTI, 2, rue Andre Pascal, 75775 Paris Cedex 16, FrancebInvest in Sweden Agency (ISA), Box 90, 10121 Stockholm, Sweden

Received 28 April 1994; accepted 31 August 1998

Abstract

Although intra-firm trade has been viewed as associated with vertical integration, whichexploits opportunities for exchange between inherently dissimilar economies, it is morecommon between developed countries where horizontal integration is expected to dominate.Using unique data from 1974 to 1990 on Swedish firms, application of a Tobit modelexplains variations in majority-owned manufacturing affiliates’ internal imports of inter-mediate and finished goods on the basis of firms’ international organization of production.Effects which are unobservable in aggregate figures show up only when finished andintermediate goods are separated. 2000 Elsevier Science B.V. All rights reserved.

Keywords: Multinational firms; Intra-firm trade; Vertical and horizontal integration

JEL classification: F23; L22; L23

1. Introduction

The expansion of foreign production by multinational enterprises (MNEs) exertsa major impact on the direction, magnitude and composition of trade flows. One ofthe most conspicuous effects is the phenomenal increase in intra-firm transactions.UNCTAD (1996) estimates that one-third of all international trade occurs within

*Corresponding author. Tel.: 146-8-4027815; fax: 146-8-4027878.

0167-7187/00/$ – see front matter 2000 Elsevier Science B.V. All rights reserved.PI I : S0167-7187( 98 )00041-1

774 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

MNEs, and even more in the case of individual countries. Nevertheless, there isstill scanty evidence on what determines the choice between trading at arm’slength and within organizations, and how internalization affects resource allocationand welfare.

Explanations of intra-firm trade are mostly related to theories of verticalintegration (cf. Williamson, 1971, 1979; Casson and Associates, 1986). Based onthe so-called Coase–Williamson paradigm, vertical integration has been inter-preted as the decision to organize exchange internally rather than externally. Thegrowth of intra-firm trade has consequently been viewed as an expansion ofvertically organized MNEs, which, on the basis of traditional factor-proportionmodels, are expected to exploit country-differences in, e.g. factor endowments andtechnology. By contrast, direct investment between similar countries has beenassociated with horizontal integration, i.e. the establishment of a similar productline in different locations, which would be based on trade in headquarters services

1but not in intermediate goods (Brainard, 1994; Markuson, 1994).Various observations speak against a clear-cut relationship between vertical

integration and intra-firm goods trade, however. Helleiner and Lavergne (1980)found more related-party trade in United States goods imports from the OECDthan from developing countries. Taking product differentiation and scaleeconomies into consideration, Helpman and Krugman (1985) suggested thatwidening factor cost differentials lead to more intra-firm trade in the form ofheadquarters services when there is horizontal integration. Intra-firm trade inintermediate products, on the other hand, would decline as factor cost differentialswiden, because divergence leads to a larger number of vertically integrated MNEsbut increases the self-sufficiency of affiliates. Meanwhile, Cho (1990) found nosignificant impact of vertical integration on the propensity of a product to be

2traded internally. It has further been observed that intra-firm goods trade ispositively influenced by the need for after-sales services (Lall, 1978; Zejan, 1989),which should be closely associated with horizontal rather than vertical integration.

The seemingly contrasting observations are likely to be partly attributed to the(sometimes implicit) assumption that intra-firm goods trade between affiliatedmanufacturing plants consists of intermediate products only (cf. Lall, 1978;Helleiner, 1979; Pearce, 1982; Zejan, 1989). In practice, however, goods trade

1 A third kind of organization is conglomerate expansion, which implies manufacturing of aninternationally diversified product range. The motive may be to spread business risks across multipleindustries (Caves, 1982). In the 1980s, this form became less important as sharpened requirements dueto technical progress and liberalization made firms increasingly focused on their core activities (e.g.Wernerfelt and Montgomery, 1988; Porter, 1991). As the implications for trade from conglomerateintegration are less clear, it is not explicitly dealt with in the study.

2 Cho’s measure of vertical integration is the ‘adjusted vertical integration index’ developed byTucker and Wilder (1977), i.e. the ratio of value added of a product to the same product’s total salesduring a certain year.

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 775

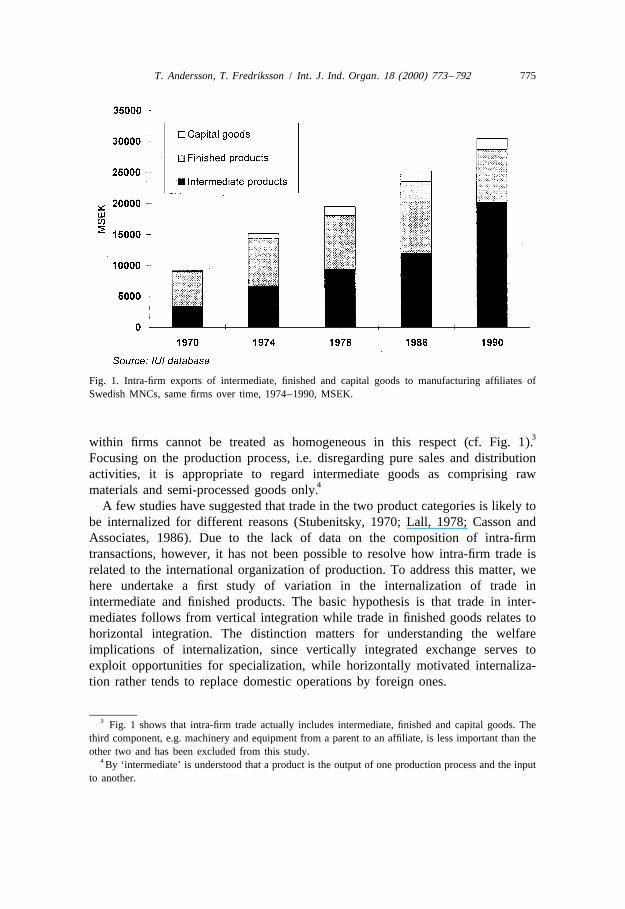

Fig. 1. Intra-firm exports of intermediate, finished and capital goods to manufacturing affiliates ofSwedish MNCs, same firms over time, 1974–1990, MSEK.

3within firms cannot be treated as homogeneous in this respect (cf. Fig. 1).Focusing on the production process, i.e. disregarding pure sales and distributionactivities, it is appropriate to regard intermediate goods as comprising raw

4materials and semi-processed goods only.A few studies have suggested that trade in the two product categories is likely to

be internalized for different reasons (Stubenitsky, 1970; Lall, 1978; Casson andAssociates, 1986). Due to the lack of data on the composition of intra-firmtransactions, however, it has not been possible to resolve how intra-firm trade isrelated to the international organization of production. To address this matter, wehere undertake a first study of variation in the internalization of trade inintermediate and finished products. The basic hypothesis is that trade in inter-mediates follows from vertical integration while trade in finished goods relates tohorizontal integration. The distinction matters for understanding the welfareimplications of internalization, since vertically integrated exchange serves toexploit opportunities for specialization, while horizontally motivated internaliza-tion rather tends to replace domestic operations by foreign ones.

3 Fig. 1 shows that intra-firm trade actually includes intermediate, finished and capital goods. Thethird component, e.g. machinery and equipment from a parent to an affiliate, is less important than theother two and has been excluded from this study.

4 By ‘intermediate’ is understood that a product is the output of one production process and the inputto another.

776 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

Focusing on manufacturing affiliates, the study uses a unique data base onintra-firm transactions which covers virtually all Swedish-owned multinationalfirms in manufacturing. With Sweden belonging to the category of small countrieswhich have become relatively more prominent sources of FDI since the early1980s, its population of MNEs represents an interesting case. Possible caveatsassociated with the delimitation of studying Swedish MNEs are discussed in thefinal section, which also offers some comments on the linkage between structuralchange and economic policy.

In Section 2, the database is introduced and some descriptive informationpresented. Section 3 reviews the connection between corporate organization andinternalization and presents our hypotheses. In Section 4, the Tobit model isintroduced and our variables are defined. Section 5 presents estimations andresults, and Section 6 concludes.

2. Description of the data

Detailed information on intra-firm trade is available at the Industrial Institute forEconomic and Social Research (IUI) for practically all Swedish multinationalfirms. The data base covers the consolidated operations of firms as well as eachmajority-owned manufacturing foreign affiliate for 1965, 1970, 1974, 1978, 1986and 1990. Information has been collected through questionnaires, and the responserate has exceeded 90% throughout. As some questions, which provide essentialinformation for this study, were not included before 1974, we here use only the

5last four surveys.Similar to developments in other countries, intra-firm transactions have gradual-

ly become more important for Swedish multinationals. The share of parent exportsgoing to foreign affiliates reached 50% in 1990 (Andersson et al., 1996). The bulkis channelled to sales affiliates, but manufacturing affiliates have been thedestination for a rising proportion, up from 13% of parent exports in 1970 to 20%in 1990. As the IUI database provides detailed information on manufacturingsubsidiaries only, the trade behavior of sales affiliates will not be further analyzedhere.

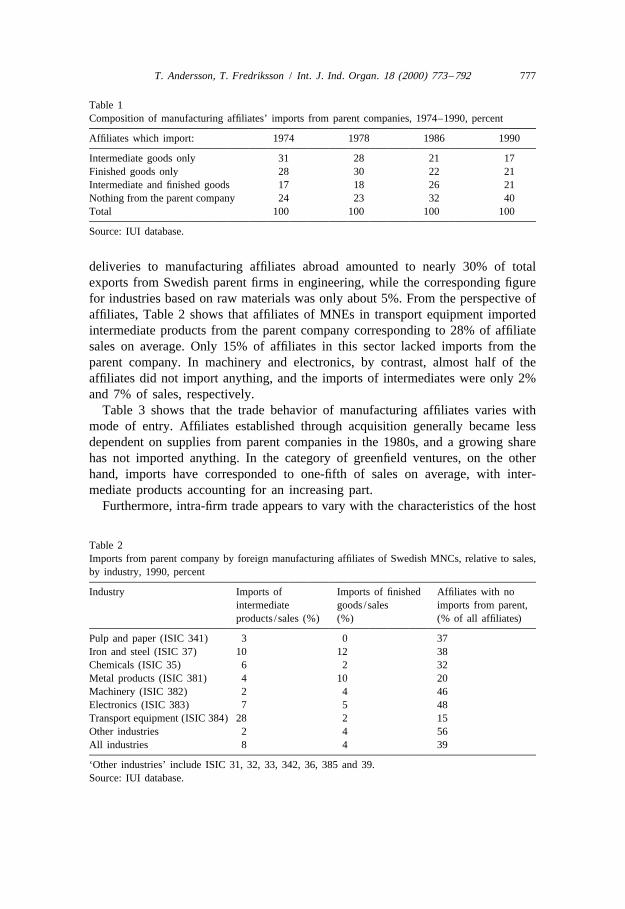

As can be seen from Table 1, the composition of intra-firm trade is far fromhomogeneous across affiliates. The share of affiliates which import both inter-mediate and finished products has declined over time. In 1990, 17% imported bothcategories, 21% imported only intermediate goods, and 21% purchased exclusivelyfinished products from the parent. Meanwhile, the proportion of affiliates with noimports from the parent increased from 23 to 40% between 1978 and 1990.

The trade pattern differs considerably between industries. For example, in 1990,

5 See Andersson et al. (1996) for a more detailed description of the IUI database.

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 777

Table 1Composition of manufacturing affiliates’ imports from parent companies, 1974–1990, percent

Affiliates which import: 1974 1978 1986 1990

Intermediate goods only 31 28 21 17Finished goods only 28 30 22 21Intermediate and finished goods 17 18 26 21Nothing from the parent company 24 23 32 40Total 100 100 100 100

Source: IUI database.

deliveries to manufacturing affiliates abroad amounted to nearly 30% of totalexports from Swedish parent firms in engineering, while the corresponding figurefor industries based on raw materials was only about 5%. From the perspective ofaffiliates, Table 2 shows that affiliates of MNEs in transport equipment importedintermediate products from the parent company corresponding to 28% of affiliatesales on average. Only 15% of affiliates in this sector lacked imports from theparent company. In machinery and electronics, by contrast, almost half of theaffiliates did not import anything, and the imports of intermediates were only 2%and 7% of sales, respectively.

Table 3 shows that the trade behavior of manufacturing affiliates varies withmode of entry. Affiliates established through acquisition generally became lessdependent on supplies from parent companies in the 1980s, and a growing sharehas not imported anything. In the category of greenfield ventures, on the otherhand, imports have corresponded to one-fifth of sales on average, with inter-mediate products accounting for an increasing part.

Furthermore, intra-firm trade appears to vary with the characteristics of the host

Table 2Imports from parent company by foreign manufacturing affiliates of Swedish MNCs, relative to sales,by industry, 1990, percent

Industry Imports of Imports of finished Affiliates with nointermediate goods /sales imports from parent,products / sales (%) (%) (% of all affiliates)

Pulp and paper (ISIC 341) 3 0 37Iron and steel (ISIC 37) 10 12 38Chemicals (ISIC 35) 6 2 32Metal products (ISIC 381) 4 10 20Machinery (ISIC 382) 2 4 46Electronics (ISIC 383) 7 5 48Transport equipment (ISIC 384) 28 2 15Other industries 2 4 56All industries 8 4 39

‘Other industries’ include ISIC 31, 32, 33, 342, 36, 385 and 39.Source: IUI database.

778 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

Table 3Propensity of Swedish-owned affiliates to import from parent, and the proportion of intermediates intheir overall imports, by entry mode, selected years, percent

Measure 1974 1978 1986 1990

Greenfield ventureTotal imports from parent / sales 21 21 20 20Share of intermediate products 44 46 53 78Proportion of affiliates with no 18 11 16 19imports from parent

TakeoverTotal imports from parent / sales 10 10 7 7Share of intermediate products 59 66 52 63Proportion of affiliates with no 28 30 38 47imports from parent

Source: IUI database.

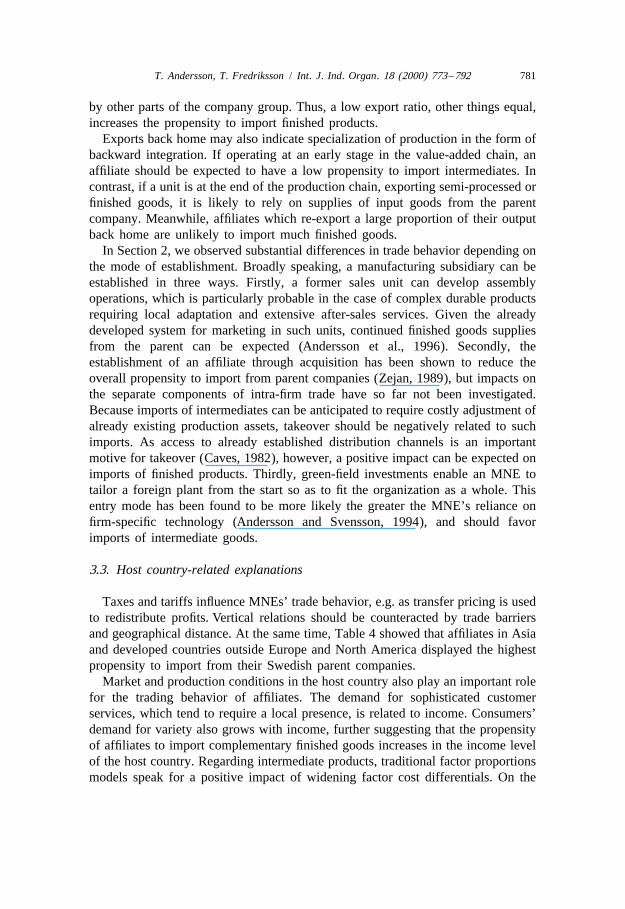

economy. The extent to which affiliates in different regions have received internalsupplies from the home country is reported in Table 4. There are no systematicdissimilarities between developed and developing countries, but a considerablevariation shows up within each group. In Europe, affiliates in the EC were moredependent on home country supplies than those in EFTA, particularly with regardto intermediates. In North America, parent deliveries of input goods correspondedto only 4% of affiliate sales. The geographical distance as well as the size of thehost market has favored local production rather than exports from Sweden(Andersson et al., 1996). Meanwhile, other developed countries report the highestimport ratios of both product categories. Regarding developing countries, high

Table 4Sales and imports from parents by foreign manufacturing affiliates of Swedish MNCs, by region, 1990,percent

Region Imports from Imports of Imports ofparent / sales intermediates / sales finished goods /sales

Developed countries 12 8 4EC-12 13 9 4EFTA 10 3 7North America 7 4 3Other 24 13 11

Developing countries 14 9 5Africa 1 0 1Asia 28 10 18Latin America 11 8 3

Total 12 7 5

Source: IUI database.

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 779

trade barriers have spurred tariff-jumping FDI and local manufacture in LatinAmerica, while relatively more openness to trade coupled with problems toacquire local firms have made the reverse apply in Asia.

Even within a given MNE, affiliates differ markedly in the degree to which theyrely on supplies from the parent company. Thus, there is a need of highlydisaggregated information in order to explain the links between foreign production

6and intra-firm trade. Finally, imports of finished and intermediate goods appear tobe determined differently. Understanding the connections between foreign pro-duction and intra-firm trade requires studying of structures within firms and anability to distinguish between finished and intermediate products.

3. Determinants of intra-firm trade

Trade is basically internalized as a means to reduce transaction costs inarm’s-length contracting, which may arise due to failures in commodity orinformation markets (Buckley and Casson, 1976; Casson, 1979). Partly dependingon the nature of transaction costs, however, international business activities can beorganized in different ways. In particular, vertical integration involves specializa-tion, as different units complement each other, and requires intra-firm trade inintermediate products. Hence, operations are concentrated in a relatively smallnumber of large plants which trade among each other. Trade liberalization,dissimilar technologies at different stages of production, variation in factor pricesand economies of scale at the plant level, favor this kind of organization. Incontrast, horizontal integration means that operations resemble those in the parentcompany. The rationale lies in potential gains from internalizing markets forproprietary assets such as, e.g. a patent or a trade mark, superior managementtechniques or greater access to financial resources. Foreign production is motivatedby the need for proximity to the local market, and less exports are expected. In thiscase, an affiliate’s sales compete with the parent’s arm’s-length exports, withoutany off-setting increase in parent exports of intermediate goods. However, if theaffiliate manufactures only a certain fraction of the firm’s full range of products,imports of complementary finished goods can benefit from economies of scope indistribution.

In the following, we analyze whether variations in the size and structure ofinternalized trade can be related to organizational mode. The propensity of foreignaffiliates’ to import, to import intermediate goods and to import finished goodsfrom the parent company are used as dependent variables in three separate

6 Most previous studies have been based on US data. The main sources of data on trade by USmultinationals are the three benchmark surveys from 1977, 1982 and 1987 (US Department ofCommerce, 1981, 1986, 1992), and the survey by the US Tariff Commission (1973).

780 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

regressions. The hypotheses regarding independent variables are based on linksbetween vertical and horizontal integration with intra-firm trade in intermediateproducts and complementary supplies of finished products, respectively. It shouldbe stressed, however, that the two modes of organization are neither mutuallyexclusive nor exhaustive. Both types can be present to varying degrees in MNEs,and individual companies or affiliates cannot easily be classified in accordancewith either type. Here we use proxy variables for either mode of organization, orvariables which are likely to influence the propensity to import given a certainform of organization. Based on previous theoretical and empirical findings, factorsinfluencing intra-firm trade are broken down into features relating to the firm, theaffiliate, and the host country.

3.1. Firm-related explanations

Investment in research and development (R&D) has been found to be positivelycorrelated with intra-firm trade (see Lall, 1978; Buckley and Pearce, 1979; Zejan,1989). Lall argued that internalization of trade is most probable when finished andintermediate goods are highly specific and embody proprietary information.Studying US firms, Sleuwaegen (1985) found R&D intensity, although high inboth cases, to be more strongly correlated with trade in intermediate products thanin finished goods. Nevertheless, the lack of well-functioning markets for intangibleassets should motivate internalization of both product types.

It has been suggested that increasing multinationality, measured as the share offoreign to total assets of a firm, should lower the dependence of affiliates on parentsupplies. Presuming that MNEs are vertically organized, Pearce (1982) and Zejan(1989) argued that trade is enhanced among foreign affiliates rather than with theparent. However, Andersson and Fredriksson (1996) found multinationality to benegatively related to the export intensity of affiliates, speaking for a connectionwith horizontal rather than vertical integration. Irrespective of organizationalmode, the relative weight of the parent should decline with multinationality,suggesting a smaller propensity of affiliates to import both kinds of products.

The presence of scale economies at the plant level favors vertical integrationand concentration of operations in a limited number of large units. The greater thenumber of production sites, and the smaller their size, by contrast, the more likelyis horizontal expansion.

3.2. Affiliate-related explanations

A high propensity to export to third countries implies international specializa-tion of production and, hence, should favor imports of intermediate products fromthe parent company. By contrast, emphasis on the host market suggests that theaffiliate’s distribution system can effectively be exploited also for goods produced

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 781

by other parts of the company group. Thus, a low export ratio, other things equal,increases the propensity to import finished products.

Exports back home may also indicate specialization of production in the form ofbackward integration. If operating at an early stage in the value-added chain, anaffiliate should be expected to have a low propensity to import intermediates. Incontrast, if a unit is at the end of the production chain, exporting semi-processed orfinished goods, it is likely to rely on supplies of input goods from the parentcompany. Meanwhile, affiliates which re-export a large proportion of their outputback home are unlikely to import much finished goods.

In Section 2, we observed substantial differences in trade behavior depending onthe mode of establishment. Broadly speaking, a manufacturing subsidiary can beestablished in three ways. Firstly, a former sales unit can develop assemblyoperations, which is particularly probable in the case of complex durable productsrequiring local adaptation and extensive after-sales services. Given the alreadydeveloped system for marketing in such units, continued finished goods suppliesfrom the parent can be expected (Andersson et al., 1996). Secondly, theestablishment of an affiliate through acquisition has been shown to reduce theoverall propensity to import from parent companies (Zejan, 1989), but impacts onthe separate components of intra-firm trade have so far not been investigated.Because imports of intermediates can be anticipated to require costly adjustment ofalready existing production assets, takeover should be negatively related to suchimports. As access to already established distribution channels is an importantmotive for takeover (Caves, 1982), however, a positive impact can be expected onimports of finished products. Thirdly, green-field investments enable an MNE totailor a foreign plant from the start so as to fit the organization as a whole. Thisentry mode has been found to be more likely the greater the MNE’s reliance onfirm-specific technology (Andersson and Svensson, 1994), and should favorimports of intermediate goods.

3.3. Host country-related explanations

Taxes and tariffs influence MNEs’ trade behavior, e.g. as transfer pricing is usedto redistribute profits. Vertical relations should be counteracted by trade barriersand geographical distance. At the same time, Table 4 showed that affiliates in Asiaand developed countries outside Europe and North America displayed the highestpropensity to import from their Swedish parent companies.

Market and production conditions in the host country also play an important rolefor the trading behavior of affiliates. The demand for sophisticated customerservices, which tend to require a local presence, is related to income. Consumers’demand for variety also grows with income, further suggesting that the propensityof affiliates to import complementary finished goods increases in the income levelof the host country. Regarding intermediate products, traditional factor proportionsmodels speak for a positive impact of widening factor cost differentials. On the

782 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

other hand, imperfect competition models have suggested that an increasingdiscrepancy in factor costs — conversely related to the income level of hostcountries — counteracts intermediate goods’ trade by vertically integrated MNEs(Helpman and Krugman, 1985). There are also arguments for vertical specializa-tion among high-income countries, particularly in knowledge-intensive productionwhose location may depend more on a free flow of trade, the quality ofinfrastructure, worker skills and the presence of qualified buyers and suppliers,than on factor cost differentials (c.f. Wheeler and Mody, 1992; Braunerhjelm andSvensson, 1994; Andersson and Fredriksson, 1996). However, the availability ofqualified local subcontractors should reduce the dependence on input goods from

7the home country. Thus, unless traditional factor models are valid, the relationshipbetween income level and affiliates’ propensity to import intermediates isambiguous a priori.

According to Kravis and Lipsey (1982), large host markets enable firms to meethigh entry costs and exploit economies of scale at the plant level, therebyattracting specialized and export-oriented activities. This suggests a positiverelationship between intra-firm imports of intermediates and market size. Otherempirical studies have shown that large markets are most likely to be served bylocal production (Swedenborg, 1979; Culem, 1988; Veugelers, 1991). Since a largemarket should facilitate a greater scale in production at the plant level, com-plementary imports of finished goods should decline with growing host marketsize.

4. The Tobit model and variable definitions

In the following, affiliates’ total imports, imports of intermediate products andimports of finished products from parent companies, measured as shares of netproduction and therefore interpreted as propensities, are chosen as dependent

8variables. As noted in Section 3, a large number of observations are zero with9those remaining being non-negative. Such a variable is left censored, and a Tobit

model is thus appropriate (Tobin, 1958). The model is defined as:

y 5 a 1 b9x 1 u if LHS . 0i i iH y 5 0 otherwisei

7 As has been shown by Swedenborg (1982), Swedish multinationals have located relatively littleproduction in low-income countries. The textiles and clothing industry is an exception, however.

8 Net production5total sales less imports from the parent company.9 Twenty-three percent of the observations are zero for the first, 47% for the second and 55% for the

third dependent variable.

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 783

where y is the propensity to import, x is a k31 vector of observations of thei i

independent variables, b is a k31 vector of parameters to be estimated, and u arei

the residuals assumed to be independent and normally distributed with zero mean10and a common variance.

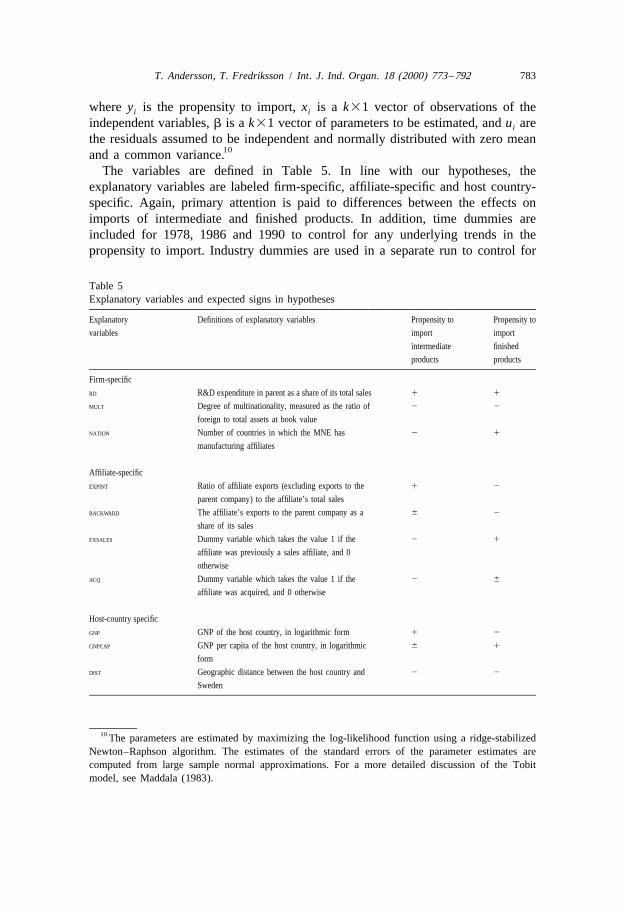

The variables are defined in Table 5. In line with our hypotheses, theexplanatory variables are labeled firm-specific, affiliate-specific and host country-specific. Again, primary attention is paid to differences between the effects onimports of intermediate and finished products. In addition, time dummies areincluded for 1978, 1986 and 1990 to control for any underlying trends in thepropensity to import. Industry dummies are used in a separate run to control for

Table 5Explanatory variables and expected signs in hypotheses

Explanatory Definitions of explanatory variables Propensity to Propensity to

variables import import

intermediate finished

products products

Firm-specific

RD R&D expenditure in parent as a share of its total sales 1 1

MULT Degree of multinationality, measured as the ratio of 2 2

foreign to total assets at book value

NATION Number of countries in which the MNE has 2 1

manufacturing affiliates

Affiliate-specific

EXPINT Ratio of affiliate exports (excluding exports to the 1 2

parent company) to the affiliate’s total sales

BACKWARD The affiliate’s exports to the parent company as a 6 2

share of its sales

EXSALES Dummy variable which takes the value 1 if the 2 1

affiliate was previously a sales affiliate, and 0

otherwise

ACQ Dummy variable which takes the value 1 if the 2 6

affiliate was acquired, and 0 otherwise

Host-country specific

GNP GNP of the host country, in logarithmic form 1 2

GNPCAP GNP per capita of the host country, in logarithmic 6 1

form

DIST Geographic distance between the host country and 2 2

Sweden

10 The parameters are estimated by maximizing the log-likelihood function using a ridge-stabilizedNewton–Raphson algorithm. The estimates of the standard errors of the parameter estimates arecomputed from large sample normal approximations. For a more detailed discussion of the Tobitmodel, see Maddala (1983).

784 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

possible fixed effects. There are hypothesized differences regarding intermediateand finished products in each category of explanatory variables, and the expectedsigns are summarized in the table.

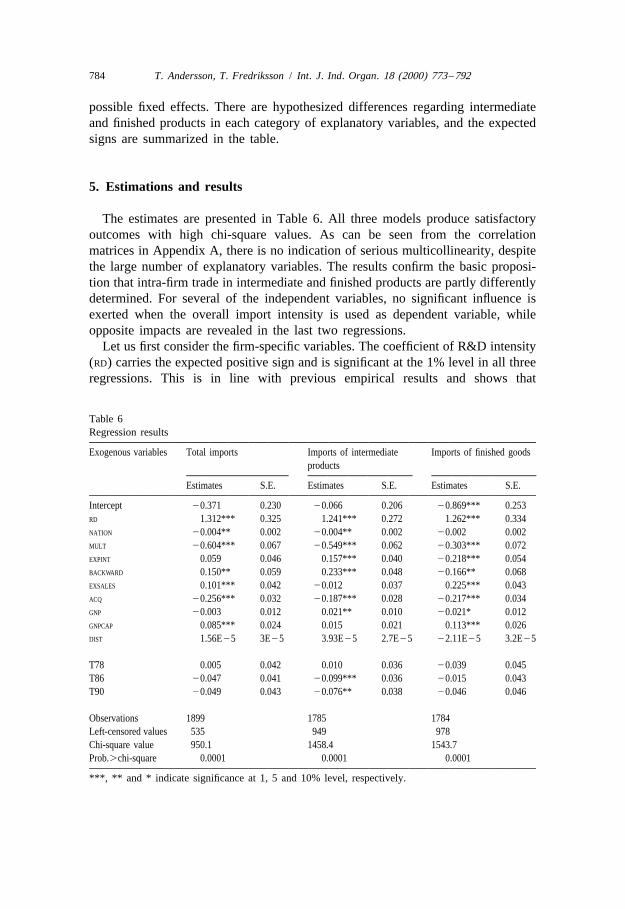

5. Estimations and results

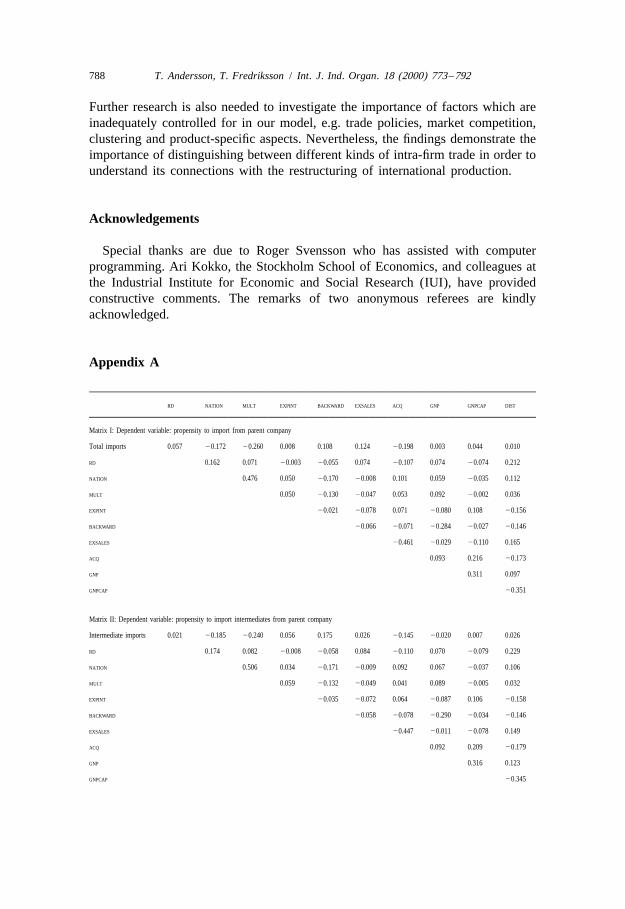

The estimates are presented in Table 6. All three models produce satisfactoryoutcomes with high chi-square values. As can be seen from the correlationmatrices in Appendix A, there is no indication of serious multicollinearity, despitethe large number of explanatory variables. The results confirm the basic proposi-tion that intra-firm trade in intermediate and finished products are partly differentlydetermined. For several of the independent variables, no significant influence isexerted when the overall import intensity is used as dependent variable, whileopposite impacts are revealed in the last two regressions.

Let us first consider the firm-specific variables. The coefficient of R&D intensity(RD) carries the expected positive sign and is significant at the 1% level in all threeregressions. This is in line with previous empirical results and shows that

Table 6Regression results

Exogenous variables Total imports Imports of intermediate Imports of finished goodsproducts

Estimates S.E. Estimates S.E. Estimates S.E.

Intercept 20.371 0.230 20.066 0.206 20.869*** 0.253RD 1.312*** 0.325 1.241*** 0.272 1.262*** 0.334NATION 20.004** 0.002 20.004** 0.002 20.002 0.002MULT 20.604*** 0.067 20.549*** 0.062 20.303*** 0.072EXPINT 0.059 0.046 0.157*** 0.040 20.218*** 0.054BACKWARD 0.150** 0.059 0.233*** 0.048 20.166** 0.068EXSALES 0.101*** 0.042 20.012 0.037 0.225*** 0.043ACQ 20.256*** 0.032 20.187*** 0.028 20.217*** 0.034GNP 20.003 0.012 0.021** 0.010 20.021* 0.012GNPCAP 0.085*** 0.024 0.015 0.021 0.113*** 0.026DIST 1.56E25 3E25 3.93E25 2.7E25 22.11E25 3.2E25

T78 0.005 0.042 0.010 0.036 20.039 0.045T86 20.047 0.041 20.099*** 0.036 20.015 0.043T90 20.049 0.043 20.076** 0.038 20.046 0.046

Observations 1899 1785 1784Left-censored values 535 949 978Chi-square value 950.1 1458.4 1543.7Prob..chi-square 0.0001 0.0001 0.0001

***, ** and * indicate significance at 1, 5 and 10% level, respectively.

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 785

possession of intangible assets is an important determinant of intra-firm trade inintermediate as well as finished goods. In terms of elasticities (for Y.0), whichare presented in Appendix B, this is one of the variables recording the strongestimpacts, as a 1% increase in the R&D intensity on average increases the affiliate’simport propensity of intermediate and finished products by 0.17 and 0.15%,respectively. The degree of multinationality (MULT) exerts a negative effect in allmodels while, in line with the hypotheses, NATION exerts a significant negativeimpact only on the propensity to import intermediates. As shown in Appendix A,there is a certain positive correlation, about 0.5, between NATION and MULT, whichindicates that horizontal integration dominates in highly internationalized firmsleading to less complementarity between affiliates and the parent and less trade on

11the whole. This is supported by the relatively high negative elasticity in the caseof MULT with regard to imports of intermediates.

Among the affiliate-specific factors, EXPINT and BACKWARD both exert theexpected opposite effects in the last two models. While the coefficients aresignificant at the 1% level in the second and third regressions, no effect appears onthe overall propensity to import. Backward vertical links with the parent companyreduce an affiliate’s imports of finished goods, but increase intermediate imports.This is again a variable displaying notable impacts as measured by elasticities. Thecorresponding elasticities are estimated to 0.10% and 20.13%, respectively.

The trade behavior of affiliates is further affected by the mode of entry, asspecified in the hypotheses. EXSALES exerts a strong positive impact on thepropensity to import finished products, but does not significantly affect inter-mediates. With respect to acquired affiliates (ACQ), a negative impact is noted in allthree regressions. Thus, compared with green-field ventures, previous sales unitshave a high propensity to import finished products, while acquired subsidiariesdisplay a generally lower dependence on parent supplies of both categories ofgoods.

Concerning host country factors, the propensity to import intermediates isincreasing in the size of the host country (GNP), suggesting that specializedoperations and vertical linkages are more pronounced the larger the host country.Meanwhile, there is a negative impact on imports of finished products, possiblyreflecting that market size supports economies of scale, thereby reducing the needfor complementary deliveries of goods for resale. Regressing the variable on theoverall propensity to import, no significant result is obtained. The income level(GNPCAP) exerts a significant positive effect on the overall propensity to importwhich, as noted, appears to contradict the notion that FDI among the developedeconomies mainly represent horizontal expansion. As hypothesized, however, theeffect mainly emanates from higher income levels generating larger imports of

11 The correlation is not sufficiently strong to create problems of multicollinearity, however. This hasbeen confirmed in separate runs with either of the variables removed.

786 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

goods for resale. The variable exerts the strongest effect on the propensity toimport finished products from the parent, with an elasticity of about 3.5. Theinsignificant coefficient in the second model speaks against any straight-forwardpositive relationship between widening factor-cost differentials and intra-firm tradein intermediates, as suggested by traditional factor-proportion models. Similarly,there is no support for the hypothesis of a negative relationship between thegeographical distance to the host market and intra-firm trade.

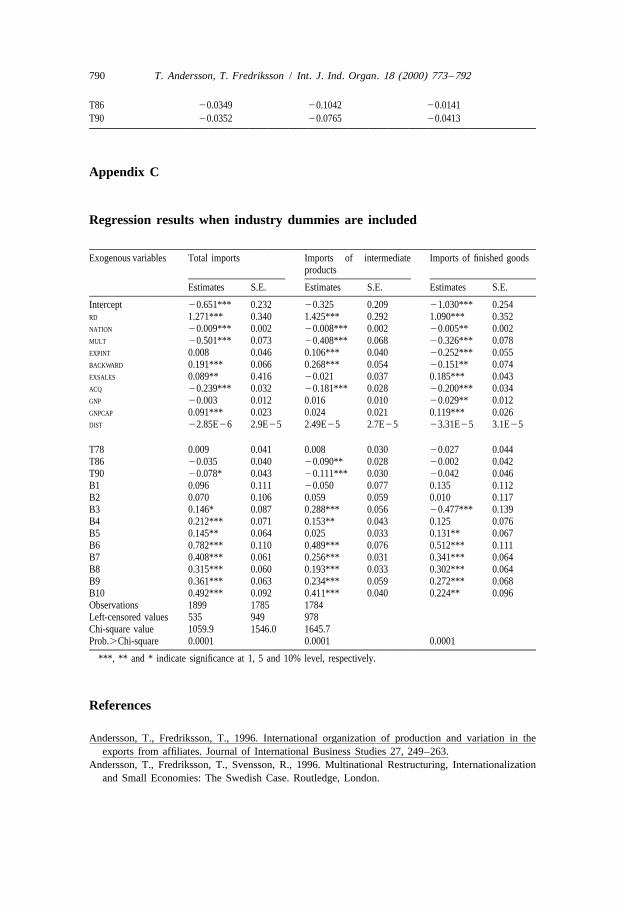

Appendix C shows the results when industry dummies are included. Theinclusion of industry dummies shows that there are some industry-specificdifferences. Nevertheless, the results for the other exogenous variables are mostlyunaffected, suggesting a high robustness of the parameter estimates. However,market size (GNP) no longer exerts a significant impact on the propensity to importintermediates when industry dummies are included. The fact that most of thedummies have a similar impact on imports of both intermediate and finished goodsfurther underlines that the linkages between intra-firm trade and the internationalorganization of MNEs cannot be understood by simply analyzing industry-leveldata. The only dummy that exerts a significant opposite effect in the last tworegressions is that for the raw-material-intensive pulp and paper industry (B3).Given Sweden’s natural endowments of forests, it seems that the rationale forforeign investment in this case is to integrate forward, with a relatively highdependence in the foreign manufacturing affiliates on intermediate inputs from theparent company. As Swedish exports of pulp and paper products are mainly sent toother European markets, the reason for setting up local manufacturing is likely tobe the need to adapt the products to local conditions, thus reducing the dependenceon finished products from the home country.

Finally, the time dummies are mostly insignificant. Given the increase ofintermediate goods exports from Swedish MNEs in the late 1980s shown in Fig. 1,it is worth noting that T86 and T90 are both negatively related to the propensity ofaffiliates to import inputs from the parent company compared to 1974.

6. Concluding remarks

Although intra-firm trade has been viewed as associated with vertical integra-tion, which exploits opportunities for exchange between inherently dissimilareconomies, it is more common between developed countries where horizontalintegration is expected to prevail. Using data on Swedish manufacturing firmsfrom 1974 to 1990, this paper has presented a first empirical analysis dis-tinguishing between intermediate and finished products in intra-firm trade. Since alarge part of total exports from parents to manufacturing affiliates consists offinished goods for resale, it is inaccurate to view all intra-firm trade as provisionsof intermediate goods in a strict sense.

Our results show that several characteristics of firms, affiliates and host

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 787

countries exert varying impacts on the exchange of the two product types.Affiliates’ propensity to import both product categories is increasing in theresearch intensity of the parent, and decreasing in the degree of multinationality aswell as by takeover as entry mode. Concentration of production to a small numberof countries favors internal supplies of intermediate goods but exerts no significanteffect on the propensity to import finished goods. High export ratios in affiliatesstimulate imports of intermediates, but diminish the propensity to import finishedgoods. Finally, a higher income level in the host country spurs greater intra-firmimports of finished goods, which is in line with an emphasis on market-seeking,horizontal investment in high-income countries. The absence of a negativerelationship between the income level of the host country and the propensity toimport intermediates leaves no support for traditional factor proportions models,however.

It may be asked to what extent the findings are home-country specific. MNEsbased in countries with larger home markets or industrial structures which differfrom that of Sweden may display another behavior. For example, a larger homemarket reduces the need for firms to internationalize operations in order to achieveeconomies of scale. The level of multinationality may consequently be lower, withimplications for trade behavior.

For the late 1980s, Fig. 1 shows a shift in the composition of intra-firm exportsfrom Swedish parents in favor of intermediate products. The fact that the timedummy for 1990 was significantly negative speaks against any structural shift inthe determinants of the propensity to import from parent companies explaining thisdevelopment. The reasons are rather to be found in other structural changes,reflecting basic opportunities for trade, macro-economic conditions and economicperformance. With Sweden located outside the integrating European Community inthe late 1980s, an overwhelming majority of new subsidiaries of Swedish MNEswere established through takeover to secure rapid access to the new opportunitiesarising there. Meanwhile, conditions for manufacturing operations deteriorated inSweden (Lindbeck et al., 1993). Given wage increases surpassing productivitygrowth in a fixed exchange rate regime and high marginal tax rates in the homemarket, the increase of intermediate exports appears to be explained by firmsrelocating high value added, research-intensive and export-oriented productionfrom Sweden to the EC, with a shift of exports from home to exports from foreignaffiliates (Andersson et al., 1996; Svensson, 1996). In our model, this is capturedby the strong positive impacts of R&D intensity in parent companies and ofexports from affiliates on the propensity of affiliates to import intermediateproducts. The negative sign of the time dummy may also be explained by the highproportion of acquired affiliates with no imports from the parent in 1990.

Such observations for the late 1980s indicate an increased responsiveness tohome-country specific conditions, which may be particularly pronounced for firmsoriginating in small economies. Studies of firms based in other countries areclearly warranted to test the generality of the results presented in this study.

788 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

Further research is also needed to investigate the importance of factors which areinadequately controlled for in our model, e.g. trade policies, market competition,clustering and product-specific aspects. Nevertheless, the findings demonstrate theimportance of distinguishing between different kinds of intra-firm trade in order tounderstand its connections with the restructuring of international production.

Acknowledgements

Special thanks are due to Roger Svensson who has assisted with computerprogramming. Ari Kokko, the Stockholm School of Economics, and colleagues atthe Industrial Institute for Economic and Social Research (IUI), have providedconstructive comments. The remarks of two anonymous referees are kindlyacknowledged.

Appendix A

RD NATION MULT EXPINT BACKWARD EXSALES ACQ GNP GNPCAP DIST

Matrix I: Dependent variable: propensity to import from parent company

Total imports 0.057 20.172 20.260 0.008 0.108 0.124 20.198 0.003 0.044 0.010

RD 0.162 0.071 20.003 20.055 0.074 20.107 0.074 20.074 0.212

NATION 0.476 0.050 20.170 20.008 0.101 0.059 20.035 0.112

MULT 0.050 20.130 20.047 0.053 0.092 20.002 0.036

EXPINT 20.021 20.078 0.071 20.080 0.108 20.156

BACKWARD 20.066 20.071 20.284 20.027 20.146

EXSALES 20.461 20.029 20.110 0.165

ACQ 0.093 0.216 20.173

GNP 0.311 0.097

GNPCAP 20.351

Matrix II: Dependent variable: propensity to import intermediates from parent company

Intermediate imports 0.021 20.185 20.240 0.056 0.175 0.026 20.145 20.020 0.007 0.026

RD 0.174 0.082 20.008 20.058 0.084 20.110 0.070 20.079 0.229

NATION 0.506 0.034 20.171 20.009 0.092 0.067 20.037 0.106

MULT 0.059 20.132 20.049 0.041 0.089 20.005 0.032

EXPINT 20.035 20.072 0.064 20.087 0.106 20.158

BACKWARD 20.058 20.078 20.290 20.034 20.146

EXSALES 20.447 20.011 20.078 0.149

ACQ 0.092 0.209 20.179

GNP 0.316 0.123

GNPCAP 20.345

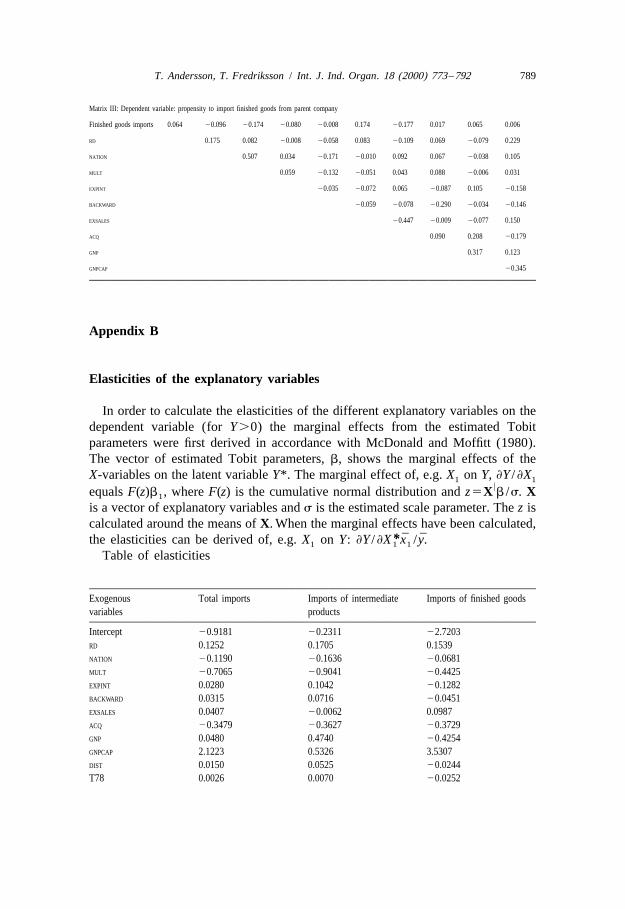

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 789

Matrix III: Dependent variable: propensity to import finished goods from parent company

Finished goods imports 0.064 20.096 20.174 20.080 20.008 0.174 20.177 0.017 0.065 0.006

RD 0.175 0.082 20.008 20.058 0.083 20.109 0.069 20.079 0.229

NATION 0.507 0.034 20.171 20.010 0.092 0.067 20.038 0.105

MULT 0.059 20.132 20.051 0.043 0.088 20.006 0.031

EXPINT 20.035 20.072 0.065 20.087 0.105 20.158

BACKWARD 20.059 20.078 20.290 20.034 20.146

EXSALES 20.447 20.009 20.077 0.150

ACQ 0.090 0.208 20.179

GNP 0.317 0.123

GNPCAP 20.345

Appendix B

Elasticities of the explanatory variables

In order to calculate the elasticities of the different explanatory variables on thedependent variable (for Y.0) the marginal effects from the estimated Tobitparameters were first derived in accordance with McDonald and Moffitt (1980).The vector of estimated Tobit parameters, b, shows the marginal effects of theX-variables on the latent variable Y*. The marginal effect of, e.g. X on Y, ≠Y /≠X1 1

uequals F(z)b , where F(z) is the cumulative normal distribution and z5X b /s. X1

is a vector of explanatory variables and s is the estimated scale parameter. The z iscalculated around the means of X. When the marginal effects have been calculated,

¯ ¯*the elasticities can be derived of, e.g. X on Y: ≠Y /≠X x /y.1 1 1

Table of elasticities

Exogenous Total imports Imports of intermediate Imports of finished goodsvariables products

Intercept 20.9181 20.2311 22.7203RD 0.1252 0.1705 0.1539NATION 20.1190 20.1636 20.0681MULT 20.7065 20.9041 20.4425EXPINT 0.0280 0.1042 20.1282BACKWARD 0.0315 0.0716 20.0451EXSALES 0.0407 20.0062 0.0987ACQ 20.3479 20.3627 20.3729GNP 0.0480 0.4740 20.4254GNPCAP 2.1223 0.5326 3.5307DIST 0.0150 0.0525 20.0244T78 0.0026 0.0070 20.0252

790 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

T86 20.0349 20.1042 20.0141T90 20.0352 20.0765 20.0413

Appendix C

Regression results when industry dummies are included

Exogenous variables Total imports Imports of intermediate Imports of finished goodsproducts

Estimates S.E. Estimates S.E. Estimates S.E.

Intercept 20.651*** 0.232 20.325 0.209 21.030*** 0.254RD 1.271*** 0.340 1.425*** 0.292 1.090*** 0.352NATION 20.009*** 0.002 20.008*** 0.002 20.005** 0.002MULT 20.501*** 0.073 20.408*** 0.068 20.326*** 0.078EXPINT 0.008 0.046 0.106*** 0.040 20.252*** 0.055BACKWARD 0.191*** 0.066 0.268*** 0.054 20.151** 0.074EXSALES 0.089** 0.416 20.021 0.037 0.185*** 0.043ACQ 20.239*** 0.032 20.181*** 0.028 20.200*** 0.034GNP 20.003 0.012 0.016 0.010 20.029** 0.012GNPCAP 0.091*** 0.023 0.024 0.021 0.119*** 0.026DIST 22.85E26 2.9E25 2.49E25 2.7E25 23.31E25 3.1E25

T78 0.009 0.041 0.008 0.030 20.027 0.044T86 20.035 0.040 20.090** 0.028 20.002 0.042T90 20.078* 0.043 20.111*** 0.030 20.042 0.046B1 0.096 0.111 20.050 0.077 0.135 0.112B2 0.070 0.106 0.059 0.059 0.010 0.117B3 0.146* 0.087 0.288*** 0.056 20.477*** 0.139B4 0.212*** 0.071 0.153** 0.043 0.125 0.076B5 0.145** 0.064 0.025 0.033 0.131** 0.067B6 0.782*** 0.110 0.489*** 0.076 0.512*** 0.111B7 0.408*** 0.061 0.256*** 0.031 0.341*** 0.064B8 0.315*** 0.060 0.193*** 0.033 0.302*** 0.064B9 0.361*** 0.063 0.234*** 0.059 0.272*** 0.068B10 0.492*** 0.092 0.411*** 0.040 0.224** 0.096Observations 1899 1785 1784Left-censored values 535 949 978Chi-square value 1059.9 1546.0 1645.7Prob..Chi-square 0.0001 0.0001 0.0001

***, ** and * indicate significance at 1, 5 and 10% level, respectively.

References

Andersson, T., Fredriksson, T., 1996. International organization of production and variation in theexports from affiliates. Journal of International Business Studies 27, 249–263.

Andersson, T., Fredriksson, T., Svensson, R., 1996. Multinational Restructuring, Internationalizationand Small Economies: The Swedish Case. Routledge, London.

T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792 791

Andersson, T., Svensson, R., 1994. Entry modes for direct investment determined by the compositionof firm-specific skills. Scandinavian Journal of Economics 4, 551–560.

Brainard, S.L., 1994. An empirical assessment of the proximity–concentration tradeoff betweenmultinational sales and trade. NBER Working Paper 4580.

Braunerhjelm, P., Svensson, R., 1994. Multinational firms, country characteristics and the pattern offoreign direct investment. Industrial Institute for Economic and Social Research (IUI), Stockholm,mimeo.

Buckley, P.J., Casson, M., 1976. The Future of the Multinational Enterprise. Macmillan, London.Buckley, P.J., Pearce, R.D., 1979. Overseas production and exporting by the world’s largest enterprises:

a study in sourcing policy. Journal of International Business Studies 10, 9–20.Casson, M.C., 1979. Alternatives to the Multinational Enterprise. Macmillan, London.Casson, M.C. and Associates, 1986. Multinationals and World Trade: Vertical Integration and the

Division of Labor in World Industries. Allen and Unwin, London.Caves, R.E., 1982. Multinational Enterprise and Economic Analysis. Cambridge University Press,

Cambridge.Cho, K.R., 1990. The role of product-specific factors in intra-firm trade of US manufacturing

multinational corporations. Journal of International Business Studies 21, 319–330.Culem, C., 1988. The locational determinants of direct investments among industrialized countries.

European Economic Review 32, 885–904.Helleiner, G.K., 1979. Transnational corporations and trade structure: the role of intra-firm trade. In:

Giersch, H. (Ed.), On the Economics of Intra-industry Trade: Symposium 1978. J.C.B. Mohr,¨Tubingen, pp. 159–181.

Helleiner and Lavergne, 1980. Author please supply.Helpman, E., Krugman, P., 1985. Market Structure and Foreign Trade: Increasing Returns, Imperfect

Competition, and the International Economy. MIT Press, Cambridge.Kravis, I.B., Lipsey, R.E., 1982. The location of overseas production and production for export by US

multinational firms . Journal of International Economics 12, 201–223.Lall, S., 1978. The pattern of intra-firm exports by US multinationals. Oxford Bulletin of Economics

and Statistics 40, 209–222.¨ ¨Lindbeck, A., et al., 1993. Nya villkor for ekonomi och politik — Ekonomikommissionens forslag.

¨ ¨Allmanna Forlaget, Stockholm.Maddala, G.S., 1983. Limited-dependent and qualitative variables in economics. Cambridge University

Press, New York.Markuson, J.R., 1994. Incorporating the multinational enterprise into the theory of international trade.

University of Colorado, Boulder, mimeo.McDonald, J.F., Moffitt, R.A., 1980. The uses of Tobit analysis. Review of Economics and Statistics

62, 318–321.Pearce, R.D., 1982. Overseas production and exporting performance: an empirical note. University of

Reading, Discussion Papers in International Investment and Business Studies, 64.Porter, M.E., 1991. M.E. Porter on Competition and Strategy. Harvard Business Review Paperback,

90079.Sleuwaegen, L., 1985. Monopolistic advantages and the international operations of firms: disaggregated

evidence from US-based multinationals. Journal of International Business Studies 16, 125–133.Stubenitsky, R., 1970. American Direct Investment in the Netherlands Industry. Rotterdam University

Press, Rotterdam.Svensson, R., 1996. Effects of overseas production on home country exports: evidence based on

Swedish multinationals. Weltwirtschaftliches Archiv 132, 304–329.Swedenborg, B., 1979. The Multinational Operations of Swedish Firms. The Industrial Institute for

Economic and Social Research (IUI), Stockholm.Swedenborg, B., 1982. Svensk industri i utlandet. En analys av drivkrafter och effekter. The Industrial

Institute for Economic and Social Research (IUI), Stockholm.

792 T. Andersson, T. Fredriksson / Int. J. Ind. Organ. 18 (2000) 773 –792

Tobin, J., 1958. Estimations of relationships for limited dependent variables. Econometrica 26, 24–36.Tucker, I., Wilder, R., 1977. Trends in vertical integration in the US manufacturing sector. Journal of

Industrial Economics, September, pp. 81–94.UNCTAD, 1996. World investment report: Investment, Trade and International Policy Arrangements.

United Nations, New York.US Department of Commerce, 1981. US direct investment abroad: 1977. Bureau of Economic

Analysis.US Department of Commerce, 1986. US direct investment abroad: 1982. Benchmark survey data.

Bureau of Economic Analysis.US Department of Commerce, 1992. US direct investment abroad: 1987. Benchmark survey data.

Bureau of Economic Analysis.US Tariff Commission, 1973. Implications of multinational firms for world trade and investment and

for US trade and labor. US Tariff Commission, Washington DC.Veugelers, R., 1991. Locational determinants and ranking of host countries: an empirical assessment.

Kyklos 44, 363–382.Wernerfelt, B., Montgomery, C.A., 1988. Tobin’s q and the importance of focus in firm performance.

American Economic Review 78, 246–250.Wheeler, D., Mody, A., 1992. International investment location decisions: the case of US firms. Journal

of International Economics 33, 57–76.Williamson, O.E., 1971. The vertical integration of production: market failure considerations. American

Economic Review 61, 112–123.Williamson, O.E., 1979. Transaction cost economics: the governance of contractual relations. Journal

of Law and Economics 22, 233–261.Zejan, M.C., 1989. Intra-firm trade and Swedish multinationals. Weltwirtschaftliches Archiv 125,

814–833.

Related Documents