1 School of Business and Management, Queen Mary, University of London Author: Leila Hsieh Course Title: MSc International Management with Finance Subject Code: BUSM003 Student ID: 089560855 Exam No: HH798 Email ID Date Submitted bs08309@qmul. ac.uk 1 st September 2009 Currency Crisis 1998 x Global Crisis 2008: The Brazilian Monetary and Fiscal Policies.

Dissertation Final BS08309-2

Aug 07, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

S c h o o l o f B u s i n e s s a n d M a n a g e m e n t , Q u e e n M a r y , U n i v e r s i t y o f L o n d o nM i l e E n d R o a d , L o n d o n – E 1 4 N S . P h : 0 2 0 7 7 8 2 5 5 5 5

Author: Leila Hsieh Course Title: MSc International Management with FinanceSubject Code: BUSM003Student ID: 089560855Exam No: HH798

Email IDDate Submitted

[email protected] September 2009

Currency Crisis 1998 x Global Crisis 2008: The Brazilian Monetary and Fiscal Policies.

2

Abstract

In 2007, a series of bank and insurance company failures triggered a financial crisis that

effectively halted global credit markets. Understanding what has caused one of the biggest

catastrophes and the intervention of government is the key to preventing a recurrence. This paper

will analyze the impact of current crisis at Brazilian market and how the authorizes responded to

it. Besides, making a comparison to the famous currency crisis happened at Brazil in 1998,

comprehending why Brazil did suffer a bigger impact back in that time. Hence, an interesting

question: what have changed in Brazilian economy and policy in 2008, that made Brazilian

market considerable strong to face the global financial crisis.

Literature Review

In the beginning of this work Soro (2008) and Cooper (2008) textbook and reports from the

Central Bank of Brazil- “Financial Stability” (2008) were very useful to have a deeper

knowledge about the current financial crisis and the present Brazilian economy situation,

therefore allowing me to initiate the introduction, set the scope of the research and provided

reliable sources. Consequently, the next step was the research on Baumann (2002), which was

especially important to study Brazil in the 1990s, the evolution and reforms at Brazilian market.

Moreover, Amann and Chang (2004) bring a slightly different standpoint in Brazilian market as

the current crisis happened at 1998, mentioning the causes and the consequences of its.

The useful research which analyzed the Brazilian economics and politics evolution and reform

were the textbook Kinzo and Dunkerley (2003) and Edwards (2007); and finally by Chadwick

(2008), the presentation published by Central Bank of Brazil- “Brazil and International Crisis”

(2009) and the article printed from City of London- “The Challenges and Opportunities for

3

Financial Services in Brazil” (2009), permitted me to comprehend the adverse impact from

global credit crunch at Brazilian market, therefore inducing me to the conclusion of my thesis.

Methodology

The research study followed here is secondary sources, which mainly refers to data already in

existence having been collected by governments, banks, statistics relating the economy and

textbooks. The reason of I have chosen this method is because it is suitable to my work, which

the analysis is based on what has already happened. The advantages of using this method are:

they have been scientifically collected; they give a wide-ranging picture of social phenomena

and the excellent comparative value in that they allow examination of trends over time.

4

Table of Contents

1 INTRODUCTION...............................................................................................................................................5

2 THE CURRENCY CRISIS IN BRAZIL, 1998.....................................................................13

2.1 THE BRAZILIAN ECONOMY IN 1990’S / POLICY REFORMS ............................................13

2.2 THE BRAZILIAN CRISIS OF 1998-99: ORIGINS AND CONSEQUENCES.........................18

2.3 THE BRAZILIAN MONETARY AND FISCAL POLICIES 1999-03..…...24

3 THE BRAZILIAN ECONOMY UNDER LULA’S GOVERNMENT.................29

3.1 LULA`S ORTHODOX ECONOMIC POLICIES AND THEIR EXPECTED RESULTS

………….30

3.2 GLOBAL FINANCIAL CRISIS 2007................................................................................................35

3.3 BRAZILIAN MARKET AND THE GLOBAL CRISIS ..................................................................37

4 CONCLUSION................................................................................................................................ 45

5 BIBIOGRAPHY..............................................................................................................................................48

5

1. Introduction

On August 2007 the world faced the biggest global financial crisis since Wall Street proved an

exceptional economic disaster in scale in 1929. The events that fuelled the current crisis and

actions by governments all around the world are presented chronologically from August 2007

until March 2009. The primary reason of the crisis is that it was initiated by Federal Reserve

maintenance of low interest rates and the US subprime home mortgage financing market. By

September 2008 this crisis spread through global markets with economic consequences for

several developed and developing economies. At the time of writing, the global crisis is ongoing.

Global growth rate projections have been revised downward in recent months. There is a general

feeling within the international economic scenarios that United States economy has shifted

towards period of reduced economic activity (Central Bank of Brazil 2009). Confirming this

conviction, it is assumable that new international market credits have become increasingly

difficult to obtain.

The large emerging economies have been able to weather the crisis relatively unscathed due to

their strong international reserve levels and robust macroeconomic fundamentals. Nonetheless,

the financial crunch may well impact the speed of international trade expansion. With the turmoil

triggered by the mortgage market crisis, Brazilian financial market indicators have shown that

has not adversely affect at economy, evidenced by significant increases in investment levels and

expansion of household consumption. This process has made it possible for investors to draw a

clear distinction among the different emerging countries, particularly impacts that did not affect

Brazil to a great extent.

6

Credit operations within Brazil have continued the process of expansion since December 2004,

while the ratio of these operations to GDP has gradually increased. It is important to emphasize

that bank credits have been subjected to special attention by the financial system supervisory

institution. This monitoring process has demonstrated that the volume of supplies set aside by the

system remains sufficient to cover possible losses caused by bad loans.

The financial instability often presented in emerging countries is originated as inevitable

consequences of Latin America policy mistakes (Thorp and Whitehead, 1987). This statement is

still accurate when the currency crises in Brazil happened in 1998, which started in Asia, made

their way first to Russia and finally affected Brazilian market. In that period, Brazilian economy

responded by raising interest rate, taxes were increased in order to save currency, and public

spending was necessary to be cut under strong pressure from the IMF (International Monetary

Fond), which caused vast adverse impacts at Brazilian market. Therefore, this thesis will

investigate what occurred at Brazilian monetary and fiscal policy at that time, and what caused

unfavorable situation to its economy; and meanwhile will compare the abovementioned crisis to

the current financial global crises explaining why the global financial crises did not strongly

impacted the Brazilian economy. Subsequently, we will investigate the efforts and actions that

Brazilian governments made at economic policy during these ten years period in order to turn

Brazilian market more resistant to financial turbulence.

Brazil, like most Latin American countries, experienced major economic reforms during the

1990s (Kinzo and Dunkerley, 2003). Although each country had its own plan, they shared a

similar core of reforms based on privatization, deregulation, lower trade tariffs, and efforts to

trim the state intervention, to seek macroeconomic stability and further economic growth.

However, these were in fact hard targets to those developing countries. Even though Brazil is a

7

wealth country in natural resources, its social instability, such as huge differences of standard of

living, high incidence of corruption from policies (governments), low rate of education and

elevated poverty represent a huge problem to reach economic stability.

FitzGerald and Thorp (2005) state that the economic doctrine certainly marked in Latin America

during 1980s, this change was characterized by a move away from industrialization, domestic

market expansion and public wealth provision as the basis for national economic development; it

was expressed as an explicit move from ‘developmentalism’1 to ‘neo-liberalism’; which

underpinned the re-establishment of democracy in one side, and spread of market institution in

the world economy.

For many years and up to 1994, high inflation rates were one of the main features of the

Brazilian economy. According to Kinzo and Bulmer-Thomas (1995), the high inflation of the

1980s led to various unsuccessful stabilization attempts, mostly through government intervention

and price freezes. Following the normalization of financial relations with the international

community and in step with the trade and financial liberalization movement of the early 1990s

the Real Plan (Plano Real), brought a sharp reduction in inflation, from an annual rate of over

5,000 percentages in June 1994 to less than 40 percentages in mid-1998. However, the frequency

of changes in the monetary policy generated intricacy at Brazilian economy development.

1 Term such structuralism and Keynisianism are often used by external observers of the region,

but not by Latin America themselves-where the most widely employed descriptor is perphas

‘desarrolismo’. We are indebted for this point to Jose Antonio Campos.

8

Velasco (2000) argued that although the result of the Real Plan was successful, adopting a new

and strong currency real, dropping inflation for the first time since the 1950s, there were few

signs of complication to the plan. Yet Brazil’s inflation had felt significantly; it was still higher

comparing to trade partner inflation. These facts leaded to concerns about currency overvaluation

and growing trade deficits; moreover, to increase competition in 1994 Brazil began to liberalize

not only foreign investment restrictions but also trade. As a result, budget and trade deficits

began to deteriorate, contributing to a growing sense of crisis, and pressures from financial

speculators increased.

Finance was another concern; the external deficits had been financed by strong foreign

investment (Gruben and Welch, 2000). By 1999, Brazil owed $244 billion or 46% of GDP to

foreign creditors. Analysing overall what has occurred at Brazilian economy we can affirm that

the statement of Basu (2002), “the policy of financial liberalization is unlikely to produce a

higher growth rate” is accurate and suitable to its situation because the process of liberalization

raises the interest rate, this will exacerbate imbalanced access to the loan market by increasing

bank’s credit standard requisite to borrowers; thus if these borrowers default on loans, this will

increase the possibility of financial catastrophe.

In order to revamp Brazilian economy, an important event in the monetary policy occurred in

July of 1994, when a floating exchange rate regime was adopted replacing the decade-long

regime of fixed the real exchange rate. As a result, volatility of international reserves was

reduced and its impact on the monetary base; later on, Central Bank endowed with other

operating target short-term interest rates, which remained high during those years. Only from late

1995, following the phasing-out of credit controls, interest rates continuously trended down until

9

30th October 1997, when the Bank decided to raise the basic rates as a first line of defense

against the spreading crisis in the Asian financial markets. As pressures eased, the Bank was able

to progressively reduce its interest rates until the Russian crisis of mid-August 1998 again

precipitated a period of financial turmoil and rising interest rates.

To avoid the volatility of international markets, major changes have taken place in the operation

of monetary policy, such as the replacement of active reliance on open market interventions by

greater use of standing facilities as the primary policy tool of the Bank to steer interest rates.

The next stage of Brazilian economy begun at 2003, when several issues complicated the

election of presidency and transition of power (Kinzo and Dunkerley, 2003). The business

community, both domestic and international, had severe reservation about Luiz Inacio Lula da

Silva, concerning his limited international experience and his lack hand-on governing

experience. Sue and Kucinski (2003) claims that people were concerned about the future of

economic liberalization, the environment for foreign investment, the potential for default on

government debt and the role for free trade. Nonetheless, President Lula proved the opposite; he

fulfilled two most important posts for government credibility, the minister of finance and the

head of central bank, maintaining the moderation at interest rate and the currency strengthened,

by reflecting a highly supportive international environment, with strong demand for Brazilian

exports combined with high international commodities prices. These facts made him won second

round of election at 2006.

President Lula has experienced big revolution at international finance, characterized by

instability ingrained in the subprime mortgage market crisis in the United States, while is true

that the major emerging economies have been relatively intact by these events. With high level

10

of international reserves, these countries have become reigns on the financial markets of the

United State and Europe.

In the growth of default generated by the United States mortgage market and continuous

financial losses, the authorities with banking supervision clearly recognize that even in more

optimistic macroeconomic environment, a return to full operation and liquidity in the markets of

major financial assets is going to take a considerable amount of time.

The criteria governing credits in the mortgage at United States market were shown to be

excessively lenient, particularly when extending credits to individual with low credits

worthiness. Financial institutions which are responsible in transforming credits into negotiable

securities, failed to ensure that quality of credit underlying these securities would be sufficiently

clear. Banking institutions demonstrated that they were not sufficient awareness in assessing the

liquidity of markets and the adjustment of capital adequacy to regulatory rules (Central Bank of

Brazil, 2009).

Facing huge credit crunch, Brazil initiated immediately some measures to deflect the effects of

the financial crisis. President Lula broadened the authority of the Central Bank to appraise and

accept assets of distressed financial institutions and to grant foreign currency-denominated loans,

also imposes several reserve requirements on financial institutions to control liquidity within the

Brazilian financial system. By changing the requirements related to reserve ratios, the Central

Bank influenced the volume of funds available for financial institutions to lend, and

consequently, to make available on the market. The trade surplus at Brazil, jointly with a highly

sophisticated financial system, has acted as a cushion against external shocks, avoiding adverse

effects on the nation’s economic and financial stability.

11

In recent years, Brazil has developed into one of Latin America most thriving economy;

considered one of the largest natural resource production, high commodity price have

undoubtedly advantage for Brazilian economy; foreign direct investment is a cruel participant to

Brazilian economy, leading higher inflows into the country. The government has taken

advantages of this opportunity to pay all of its debts to international organizations, such as IMF

and the Paris Club.

The fundamentals of Brazilian economy were strong enough to weather severe turbulence in the

global credit market without major difficulties in 2007. Macroeconomic stability with low

inflation significantly boosted incomes and enabled the Central Bank to lower interest rates for a

long period, expanding the domestic credit market. These factors obliged strong expansion of

domestic demand, which led Brazilian economy growth by fuelling consumer spending,

increasing import and inducing vigorous growth of investment in local industry production.

Therefore, Brazil is in a position to perform better than the advanced economies, which are set to

experience a contraction of up to 1% in GDP. Its macroeconomic fundamentals have improved

significantly in recent years, steady growth combined with more optimistic future scenarios have

encouraged companies to invest in expanding industrial capacity, increasing income,

employment, total wages and credit have created favorable conditions to consumption, which has

made the domestic market a significant variable in underpinning GDP growth, expansion in the

middle class and the number of consumers generally.

Brazil’s overtook evolution from several angles, both macroeconomic and microeconomic –

although many improvements are still required – and has laid a foundation for a veritable surge

of investment in the last two years compared with the last two decades. Companies have been

encouraged, not only by the external demand, but also by the new dynamics of domestic demand,

12

believed in its consistency, and opted for expansion of production capacity in order to supply the

goods the new Brazilian consumers need. However, the reversal triggered by the global crisis

will interrupt this cycle, or at least put it on hold, and as a result we will see a substantial fall in

investment in 2009.

In section I of this dissertation, the causes of Brazilian currency crisis at 1998 will be explained,

focusing on the important facts during this calamity, and finally understanding what were the

impacts on Brazilian’s economy, identifying the monetary and fiscal policy applied in that time.

In section II, the events that fuelled the current crisis and actions by government will be

presented chronologically from August 2007 until today; the main idea is to identify the

differences in policy between 1998 and when Lula became President, the overall economic

reform and the collision from those facts at Brazilian market. Finally, a comparison on what

happened at the crises of 1998 and 2008 will be presented, bringing out the reasons why Brazil

did suffer a bigger impact back in 1998, and what have changed in Brazilian economy and policy

in 2008, that made Brazilian market considerable strong to face the global financial crisis.

13

2. THE CURRENCY CRISIS IN BRAZIL, 1998.

2.1 The Brazilian Economy in 1990’s / Policy reforms

Since the 1990s, Brazilian economy has undergone changes on an unprecedented scale,

transforming its structural characteristics and position in the global economy (Amann, 2000).

New perspectives for the economy and trade barriers have been lowered, markets have been

deregulated, privatizations implemented and more orthodox fiscal and monetary policies were

put into practice. With the domestic market opened to international trade and investment, the

performance characteristics of the economy have, in many senses, improved markedly. The

competitiveness of supply-side has advanced with a strong increase in productivity being

registered and Brazilian businesses being even more globally orientated. However, these

undoubted achievements on the other hand have made Brazilian economy more dependent on

foreign savings and on the persistence of highly uneven distributions of income, making the

market more susceptible to international influences.

In 1990, with the ascension of Fernando Collor de Melo to power, Brazil’s first directly elected

president for over 30 years, a change in consensus motivated a programme of economic reform,

the main elements of which remain in place up to this day. According to Bulmer (1994), the

reform programme was as follows:

(i) Trade Liberalisation

Given the need to improve industrial efficiency and export performance after years of intense

protection, the president Collor initiated a four-year rolling programme of trade reforms in 1990;

in these four years, average taxes were more than halved from 32 per cent to 14 per cent (figure

2.1); which constituted an enormous increase in competitive pressures on Brazilian businesses;

14

Figure:2.1 Nominal Tax Reductions in Brazil (1990-2006)/ Nominal Tax by Sectors (percent)

(ii) Privatisation

The process of privatisation began timidly under President Sarney in 1988. Nonetheless, under

President Collor it was accelerated substantially. In 1992 most of state owned steel and

petrochemical sectors had been transferred to private sectors. President Collor also developed

government plans to privatise further sectors including telecommunications and electrical

energy; known as the “Programa Nacional de Desestatizacao” (National State Divestment

Programme). Further, under President Fernando Henrique Cardoso in 1995, the privatization

programme has also embraced sectors such as banking and mining.

(iii) Market Deregulation

The main idea of President Collor’s government for the programme market deregulation was

designed to increase the competitiveness of domestic markets and to attract the much needed

foreign investment. However, this commitment had relatively little progress due to President

Collor’s removal from office in 1992. After that, under presidency of Fernando Henrique

15

Cardoso, the pace of market deregulation sharply accelerated. During his first year in office

(1995), the passage of legislation to open the oil, gas and mining sector to both domestic and

foreign private sector investors was succeeded.

(iv)Fiscal Reform

The persistence of high inflation facilitated policy-makers to artificially contain the expansion of

deficits through clever use of indexation mechanisms and the deliberate insertion of delays

between receipt and disbursement of revenues. With the end of high inflation following the

introduction of the revised Brazilian currency, the “real”, in July 1994, the weak state of public

finances was thrown into a sharper relief than ever before. As a consequence, the government of

Fernando Henrique Cardoso had been forced to redouble the efforts of earlier administrations to

bring about substantial reductions in the fiscal deficit. This effort involved measures such as

reduction of capital spending, whilst clamping down on expenditures and personnel costs.

The rapid introduction of structural microeconomic reforms were still very much constrained by

the hyper-inflation legacy of the 1970s and 1980s (Sallum Jr., 1999). President Collor

emphasized short-term monetary freezes and drastic spending cuts which both foreign and

domestic economic agents knew to be unsustainable in the long run; as a result, the plan only

worked temporarily to restrain inflation and then only at the cost of drastic reductions in output.

Thus, once the monetary freezes were removed, inflation rapidly returned with the credibility of

policy-makers further undermined.

According to Pinheiro (1994), the removal of President Collor from office in September 1992

and his replacement by the mercurial Itamar Franco could be considered one of the most

remarkable moments at Brazilian economy. Immediately, in May in 1993, Mr. Franco appointed

a former academic sociologist and formerly politically exiled, Fernando Henrique Cardoso, to

16

the office of Finance Minister. Besides that, Mr. Franco granted the newest member of his

cabinet a virtually free hand to assemble a new economic team and devise a radical new

macroeconomic policy agenda2.

In late 1993, the Real Plan was introduced by finance minister Cardoso, who devised a

comprehensive and innovative stabilization plan in order to transform the fortune of the Brazilian

economy. As a consequence of the success of the Real Plan and Cardoso’s popularity, he became

President of Brazil in January 1995. Paes de Barro (2000) point out some key elements of Real

Plan:

(i) Across the board spending cuts of US$ 7.5bn allied (around two per cent of total

expenditure) to a five per cent increase in tax rates, the latter delivering around seven per

cent increase in revenues.

(ii) The progressive abolition of the indexation system between mid 1993 and late 1994,

when both wage and price-indexing systems were abolished.

(iii) The introduction of the new currency pegged to US dollar at an initial rate of 1 to 1. The

beginning of a strong, dollar-pegged currency had a profound impact on relative prices in

all tradeable sectors and prices were forced down by import competition; over time the

price moderation forced on the tradeable sectors began to feed through into the non-

tradeable sectors as input costs for the latter fell.

(iv) The pursuit of a tight monetary policy, both to directly restrain demand side inflationary

pressures and to maintain the external value of the “real”.

2 The indexation system allowed an automatic price and wage increases to protect the “real” incomes of enterprises and workers. However, in propagating such increases on an automatic basis, the indexation system ensured that inflation was kept on the boil.

17

With the indexation system dismantled and with a dollar-linked currency driving down import

prices, inflation began a sharp decent with the result that between 1994 and 1995 accumulated

annual consumer price inflation declined from 916.46 percent to 22.41 percent. At the same time,

with actual incomes buoyed by the falling inflation, consumer spending rose sharply with the

result that GDP growth accelerated from 4.9 per cent to 5.9 per cent between 1993 and 1994

(Figure 2.2).

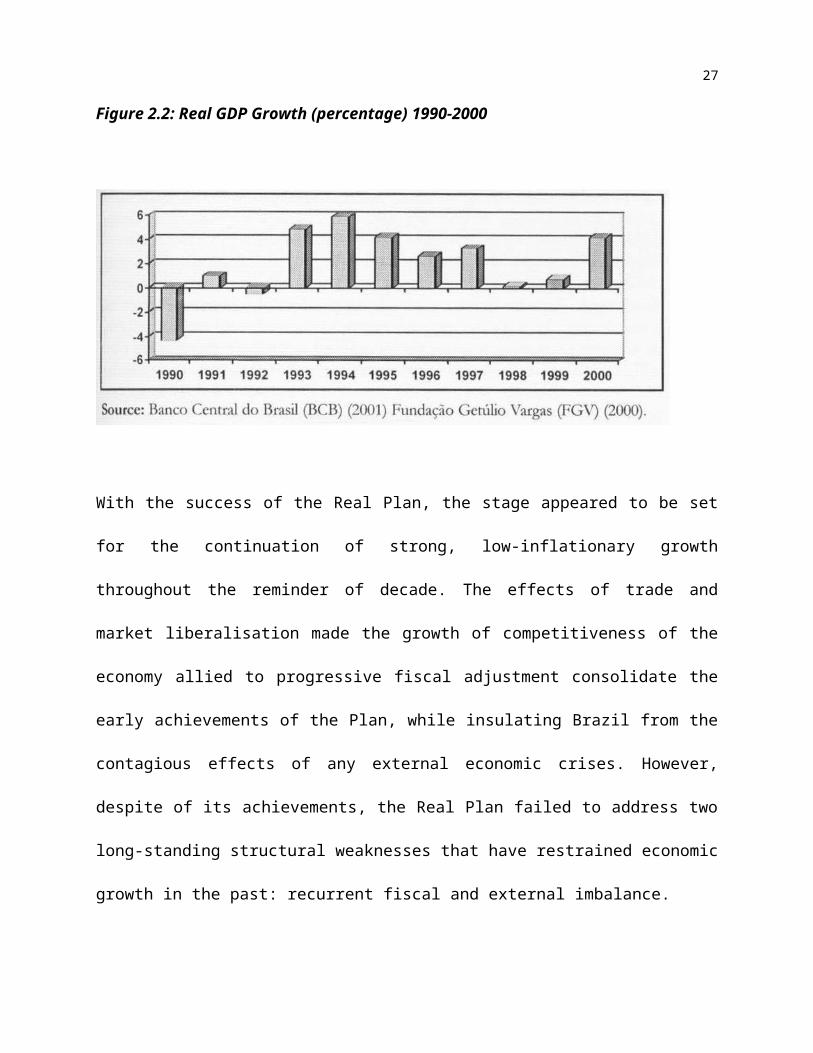

Figure 2.2: Real GDP Growth (percentage) 1990-2000

With the success of the Real Plan, the stage appeared to be set for the continuation of strong,

low-inflationary growth throughout the reminder of decade. The effects of trade and market

liberalisation made the growth of competitiveness of the economy allied to progressive fiscal

adjustment consolidate the early achievements of the Plan, while insulating Brazil from the

contagious effects of any external economic crises. However, despite of its achievements, the

Real Plan failed to address two long-standing structural weaknesses that have restrained

economic growth in the past: recurrent fiscal and external imbalance.

18

2.2 The Brazilian Crisis of 1998-99: Origins and consequences

In December 1994 a devaluation of currency by more than 50 percent in Mexico ocurrred. This

fact brought disastrous consequences in the following year. The pesos crisis commenced with an

enormous, yet unsustainably, large current account deficit which led to concern among

international investors surrounding the continuity of macroeconomic policy throughout the

region (Herscovitz, 2000). When in 1997 South Korea was forced to devaluate its currency,

inflation attained less than 10 percent and contraction at GDP dropped around 5 per cent. Finally

in the following year, in August 1998, Russia also suffered a currency crisis by misleading the

liberalisation of the market, which allowed foreign lenders and investors to leave the country

vulnerable to the risk against domestic market (Giambiagi 1999).

In the midst of financial turbulence around the world, Lins da Silva (2000) argued that in Brazil,

in order to maintain the external value of currency “real”, the authorities were forced to keep in

place a much tighter monetary policy; the exchange rate suffered a devaluation of seven to eight

percent in 1998, thus the “real” was allowed to fluctuate within a target band by Central Bank.

However, the tightness of it served only to enlarge the problem of public account, the operational

deficit (the inflation adjusted balance of total public sectors revenues and expenditures) rose

sharply after 1994 as the real cost of debt servicing increased tax reform initiatives faltered and

the government failed to tidy non-debt-expenditures (Figure 2.3 and 2.4).

Figure: 2.3 Inflation 1990-95 (percentage p.a.)

19

Figure: 2.4 Inflation 1995-2000 (percentage p.a)

Yet Baumann (2002) believes that there are two fundamental factors that explain the currency

crisis in Brazil. The first is the adverse shock of price index of primary and semi-manufacturing

goods exported by Brazil between January 1997 and 1999; it turned domestic product more

expensive in international market. The second is the closure of the international market for credit

after the Russian crisis in August 1998. In fact, Brazil assumed that the country would have time

to make necessary adjustment for economical stability while the world financed a temporally

20

elevated deficit on the current account however, the price shock aggravated this imbalance; the

Russian crisis, in turn, meant that the time allowed for this adjustment had expired.

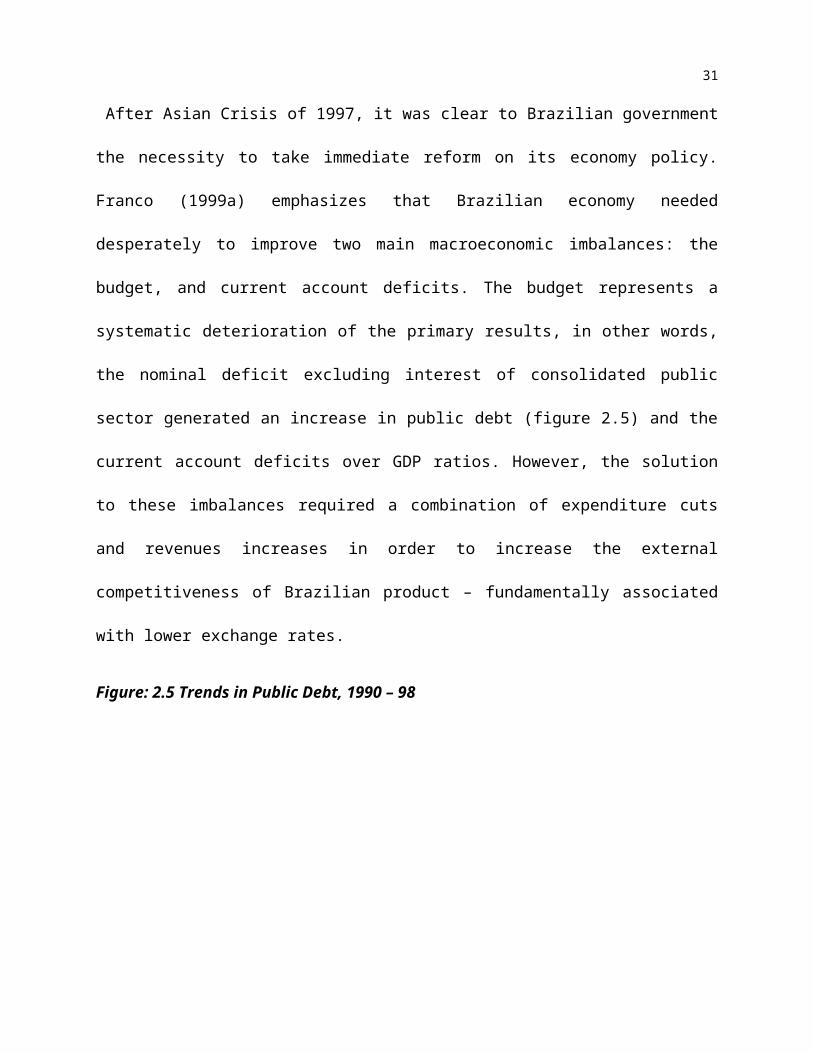

After Asian Crisis of 1997, it was clear to Brazilian government the necessity to take immediate

reform on its economy policy. Franco (1999a) emphasizes that Brazilian economy needed

desperately to improve two main macroeconomic imbalances: the budget, and current account

deficits. The budget represents a systematic deterioration of the primary results, in other words,

the nominal deficit excluding interest of consolidated public sector generated an increase in

public debt (figure 2.5) and the current account deficits over GDP ratios. However, the solution

to these imbalances required a combination of expenditure cuts and revenues increases in order

to increase the external competitiveness of Brazilian product – fundamentally associated with

lower exchange rates.

Figure: 2.5 Trends in Public Debt, 1990 – 98

The chosen solution was gradualism. Comparing data from 1997 and 1998, an improvement of

the primary fiscal result, together with real currency devaluation can be noted. These adjustments

21

took place especially in the second half of 1998, nevertheless this change was slow and delayed

and not enough to avoid collision with the external crisis.

This was the exact context in which Russia defaulted on its debts in August 1998. According to

Edwards (2007), contrary to what happened previously to Mexico and Asia, this time the

financial market closed almost completely, mainly the emerging market nations. The track

recorded devastating effects on Brazil; such as flow problem in 1999, in the sense that the

predicted current account deficit would be larger than the predicted capital inflow, generating

portfolio reallocation problem with economic agents in general. The emergence of this problem

was due to the need of agents to recover losses suffered with Russia, the fear of Brazilian default

or simple the pending likelihood of devaluation. Not surprisingly, this set of circumstances

provoked a massive capital flight (figure 2.6).

Figure: 2.6 Reserve & FDI

22

It was in this context that, a few weeks from presidential elections, government officially

announced the negotiation with IMF, by celebrating an agreement to rectify this situation.

Amann and Chang (2004) point out that the government based this agreement on four pillars: i) a

strong fiscal adjustment; ii) a tight monetary policy - the interest rate increased to approximately

40 percent again in mid September of 1998; iii) an external rescue package from IMF,

multilateral organizations and G7 countries – of US$ 42 billion; and iv) the maintenance of the

‘crawling peg’ exchange rate policy, where the currency with fixed exchange rate is allowed to

fluctuate within a band of rate3. The launch of this first adjustment, which was the announcement

of external aid and the confirmation of President Henrique Cardoso de Mello’s victory in the first

round of elections finally resulted on the drop of country risk levels and declined interest rate,

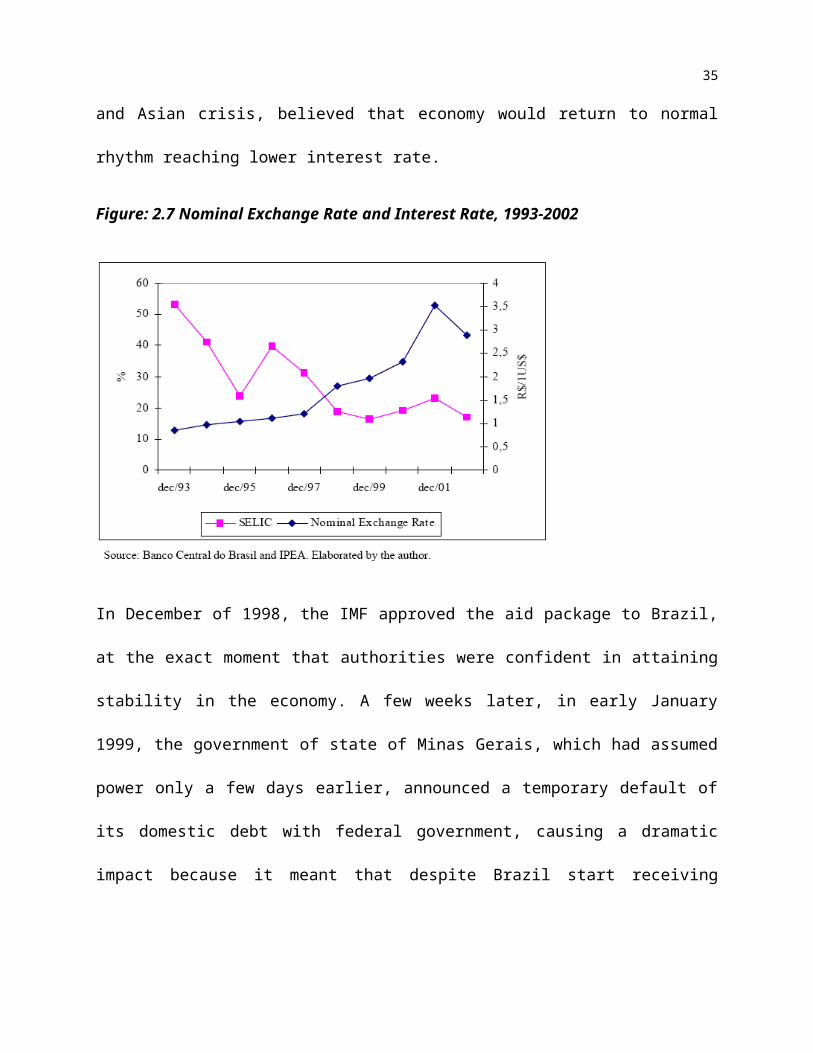

falling to around 30 per cent (Figure 2.7). The authorities, despite the loss in credibility due to

the successive traumatic and brusque changes in policy during Mexican and Asian crisis,

believed that economy would return to normal rhythm reaching lower interest rate.

Figure: 2.7 Nominal Exchange Rate and Interest Rate, 1993-2002

3 The par value of the stated currency is also adjusted frequently due to market factors such as inflation. This gradual shift of the currency's par value is done as an alternative to a sudden and significant devaluation of the currency.

23

In December of 1998, the IMF approved the aid package to Brazil, at the exact moment that

authorities were confident in attaining stability in the economy. A few weeks later, in early

January 1999, the government of state of Minas Gerais, which had assumed power only a few

days earlier, announced a temporary default of its domestic debt with federal government,

causing a dramatic impact because it meant that despite Brazil start receiving resources from

IMF it would fail to reach the fiscal target (Posthuma, 1999).

The government was losing autonomy in order to control its currency policy, reinforced by the

original agreement with the IMF, which requested as gross reserves minus the gross official

obligations an amount not less than US$ 20 billion Baumann (2002). The gross reserve was US$

40 billion in Brazil when IMF agreement was approved. By definition, the resources from

external loans do not affect the concept of net reserve; in fact, they increase gross reserve but

also the obligations. Therefore, the IMF agreement limited the Central Bank margin of

intervention at fortification of the currency policy; even worse, it may have stimulated the

24

demand for reserves, once it had undermined the strategy that the authorities had in order to react

to what was clearly becoming a speculative worry.

In the first days of January 1999 the reserve loss was dramatic; by the end of 1999 the controlled

exchange rate regime reserve losses approached US$ 1 billion a day (Central Bank of Brazil

1999). On January 13th, the government announced the replacement of Central Bank president

and the adoption of a band system, which represented a nine per cent of devaluation. This could

have been productive in other circumstances, but it was not viable, given the huge uncertainty

that prevailed at that time; consequently, the loss of reserve continued, and on the first days of

the band system, the exchange rate reached its ceiling. The new system lasted exactly 48 hours,

when finally, due to lack of alternatives, the Central Bank let the currency float4 , reaching

R$/US$ 2.16 at the exchange rate in March, compared with R$/US$ 1.21 before the currency

floated.

2.3 Brazilian Monetary and Fiscal Policies: 1999-2003

The replacement of the semi-pegged regimes and its over-valued exchange rate by a floating

exchange rate system and interest policy management succeeded in keeping monetary stability

and, after the 1999 stagnation, allowed GDP growth of four per cent in 2000 (Kinzo and

Dunkerley, 2003). However, IMF support was given and renewed in exchange for Brazil’s

commitment to a severe fiscal adjustment, aiming at huge yearly surplus in the public accounts

(interest owed was not included), large enough to be able to reduce the proportion of public debt

4 In the words of the Central Bank ex-president, Afonso Celso Pastore, the abandoning of the controlled currency policy represented an initial relief similar to that of a puncture. Once rid of the ‘infection’ that was causing the bleeding of reserves, it was necessary to put in place a wide series of measures so that the country could overcome the crisis. However, at that moment the feeling was that either the previous regimes were to be abandoned, or the country would be left with no reserves, or even that an external default would become inevitable.

25

in GDP. Further, during the 2001 and 2002 recession, the Argentine crisis and the political risk

connected to the 2002 presidential election produced additional economic constraints to

Cardoso’s policies, such as a reduction of FDI (Foreign Direct Investment flows to Brazil 2 and

it became difficult to rollover the external and internal debts. Therefore, once again Brazil’s

external dependency and economic fragility were revealed, despite the new floating exchange

policy.

Reacting to these facts, the Central Bank took measures to deepen fiscal adjustment, raise

interest rates and sign new agreements with the IMF- though protection of Brazilian financial

solvency reduced the 2001 and 2002 GDP growth to less than two per cent a year (Central Bank

of Brazil, 1999)5.

The new macroeconomic management implied some changes in State / economic branch

relations: non-financial activities tended to gain greater importance and government stimulated

in different ways those economic branches which could help to produce a surplus in external

trade.

According to Venturi (2000), these changes can be seen as a sign of a political transformation

with the hegemonic bloc, which leaned sporadically towards the liberal-developmentalist model.

This model has come to be known as ‘The New Consensus Macroeconomics’-NCM, which the

main features and highlight of its policy implications are the following:

(i) Inflation targeting is a monetary policy framework whereby public announcement of official

inflation targets (figure 2.8), which is undertaken along with explicit acknowledgement that price

stability, meaning low and stable inflation, is monetary policy’s primary long-term objective.

The focus is on price stability, along with three objectives: credibility (the framework should

5 The FDI was US $33.3 billion in 2000; it fell to US$20 billion in 2001 and to US$ 16.6 billion in 2002.

26

command trust); flexibility (the framework should allow monetary policy to react optimally to

unanticipated shocks); and legitimacy (the framework should attract public and parliamentary

support);

(ii) The level of economic activity fluctuates around a supply-side equilibrium, which

corresponds to a zero output gap or to NAIRU (non-accelerating inflation rate of

unemployment), a supply-side phenomenon closely related to the workings of the labor market.

The source of domestic inflation (relative to the expected rate of inflation) is seen to arise from

unemployment falling below the NAIRU, and inflation is postulated to accelerate if

unemployment is held below the NAIRU. However, in the long run there is no trade-off between

inflation and unemployment, and the economy has to operate (on average) at the NAIRU if

accelerating inflation is to be avoided (Bernanke, 1999);

(iii) In this framework, monetary policy is taken as the main instrument of macroeconomic

policy. Fiscal policy is no longer viewed as a powerful macroeconomic instrument (in any case it

is hostage to the slow and uncertain legislative process); in this way, “monetary policy moves

first and dominates, forcing fiscal policy to align with monetary policy” (Mishkin, 2000). Indeed,

monetary policy is viewed as the most direct determinant of inflation, so much so that in the long

run the inflation rate is the only macroeconomic variable that monetary policy can affect;

(iv) A mechanism for openness, transparency and accountability should be in place with respect

to monetary policy formulation. Openness and transparency in the conduct of monetary policy

improve credibility. In the context of inflation targeting, central banks publish inflation reports

that might include not only an outlook for inflation, but also output and other macroeconomic

variables, along with an assessment of economic conditions;

27

(v) In the case of inflation targeting an open economy, exchange rate considerations are of

crucial importance, and we highlight this aspect in the case of emerging countries, and Brazil in

particular in what follows in this paper. They transmit both certain effects of changes in the

policy instrument, interest rates, and various foreign shocks. Given this critical role of the

exchange rate in the transmission process of monetary policy, excessive fluctuations in interest

rates can produce excessive fluctuations in output by inducing significant changes in exchange

rates. This may suggest exchange rate targeting. However, the experience of a number of

developing countries, which pursued exchange rate targeting but experienced financial crises

because their policies were not perceived as credible, is relevant to the argument. The adoption

of inflation targeting, by contrast, may lead to a more stable currency since it signals a clear

commitment to price stability in a freely floating exchange rate system.

Fugure: 2.8

Therefore, although with the implementation of principles at economic policies, in the second

term of Cardoso presidency, he lost much of his prestige, mainly because the government broke

28

its word and devaluated the currency in January 1999, stimulating the fear of inflation. At the

same time the government could not punctually fulfill its promise of renewing economic growth.

In that time, high inflation did not return and economic activity started to grow after a little more

than one year, but even so the president did not recover the leadership of his first term. Therefore

the government political coalition lost discipline, making more difficult to get approval of law in

Congress and in defining specific policies, allowing the opposition parties to get stronger.

The 2002 electoral fight for presidency expressed the changes occurring in the hegemonic bloc

well, the debility of its political coalition and the ideological shift of the main opposition parties.

No presidential candidate stood for liberal fundamentalism, the whole set of political tendencies

tried to represent the establishment left wing, which meant that all of them advocated for more

state control over the market, more state incentives to productive activities and more state

protection to poorest without breaking the liberal framework, molding the sociopolitical coalition

in power. In 2003, Worker’s Party (PT), represented by the candidate Luiz Inacio Lula da Silva,

won the election. Against all the rumors, this government did not break with the liberal

hegemony established years before. Indeed, the new government agenda is a liberal

developmentalist one: its aim is not to rebuild the entrepreneurial national State but to reform the

State so that it might push private development and social equality6.

6 It is important to stress that in Brazil and in most Latin American countries economic liberalism was not against the Welfare State but opposed to the Entrepreneur State and in favor of social policies.

3 THE BRAZILIAN ECONOMY UNDER LULA’S GOVERNMENT

This section seeks to assess President Luiz Inácio Lula da Silva’s economic policies and their

impacts on the Brazilian economy. Furthermore, we will analyze how Brazilian economy is

29

facing the current global finance crisis. The result and the economic policies turned out to be

surprisingly different from those that most members and electoral supporters of the Workers’

Party – Partido dos Trabalhadores (PT) – might have ever expected.

In mid 2002, the situation changed when financial markets finally realized that Lula’s leading

position in the presidential run was probably unshakeable (Oreiro and Paula 2007). As it had

been expected, capital flight pushed down the exchange rate and a large segment of financial

investors refrained from purchasing public securities maturing after January 1st, 2003, when the

new presidential term would begin. Facing the possibility of Lula’s victory, a number of events

followed, which may not have been unrelated to that expectation: (i) capital outflows intensified

and, as a result, foreign reserves fell from US$ 42.0 billion in June 2002 to US$ 35.6 billion in

November 2002; (ii) the “real” weakened from R$ 2.38 per US dollar in January 2002 to R$

3.81 in October 2002; (iii) as a result mainly of the effects of the exchange devaluation on

domestic prices, the monthly inflation rate increased from 0.5% in January 2002 to 1.3% in

October 2002, equivalent to around 17 percent on an annual basis,; and (iv) the demand for

Brazilian securities decreased rapidly, as a consequence, the ‘Brazil risk’, measured by J.P.

Morgan, increased by almost 600 basis points, at the beginning of the year, to about 2,400 basis

points by October 2002.

30

In this framework, two important related developments took place. A new rescue package from

the International Monetary Fund (IMF) was sought and Lula faced a very heavy pressure to show

his support for it; and the pressure led Lula’s advisors to prepare a ‘Letter to the Brazilian

People’, which, although in very vague terms, the candidate assured the financial markets of his

willingness to abide by the rules set by these markets (Prates, 2006).

3.1 Lula`s orthodox economic policies and their expected results

According to Sicsu, Oreiro and Paula (2003), mid 2002 was an important moment to show

wealth-owners in Brazil the extension of their power over the new government. President Lula

focused on the theoretical economic policies based on the NCM argued earlier, nominated

Antonio Palocci, an unknown politician from the right-wing of the PT, for the Ministry of

Finance. The President also appointed Henrique Meirelles, a former chair of BankBoston in

Latin America, and elected congressman by Cardoso’s political party (Brazilian Social

Democratic Party - PSDB), as chairman of the Brazilian Central Bank. Antonio Palocci’s team

and BCB’s direction were constituted mostly by neo-liberal economists and/or economists that

were working in some big banks in Brazil. As a result, the economic policies have been marked

by the continuation, and in some aspects radicalization, of Cardoso’s economic policies,

implemented during his second term, 1999-2002.

31

As the main item of the Brazilian exports are commodities, such as soy, steel and iron, the

increase in the price of most of the commodities exported by Brazil explained why trade balance

arose from US$ 24.9 billion in 2003 to US$ 44.8 billion in 2005, although the real exchange rate

was continuously appreciating since 2003 (Prates, 2006). Net exports were the main source of

growth for the Brazilian economy from 2002 to 2005 and allowed the BCB to increase exchange

reserves from US$ 37.8 billion in 2002 to US$ 53.8 billion in 2005 (Figure 3.1). In fact, the

commodity boom explains the entirety of Brazilian 'success' and how it avoided defaults on its

external debt obligations.

Figure: 3.1 Some Macroeconomic Indicators of Brazilian Economy

32

33

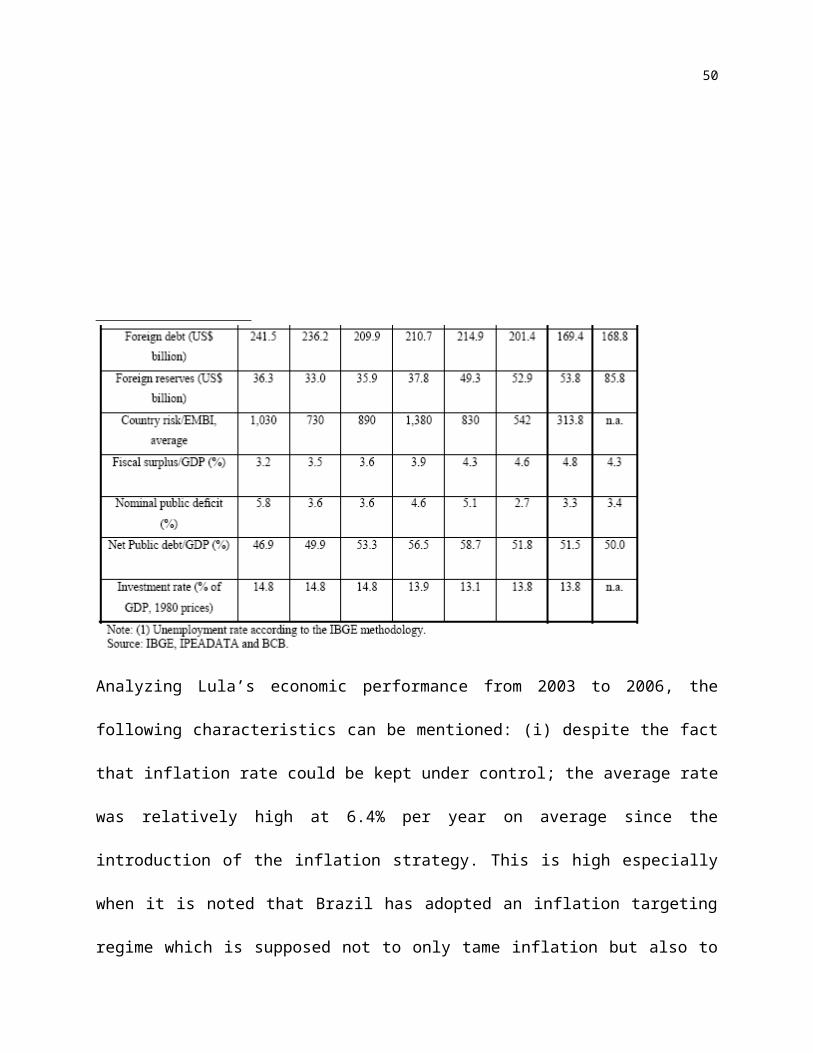

Analyzing Lula’s economic performance from 2003 to 2006, the following characteristics can be

mentioned: (i) despite the fact that inflation rate could be kept under control; the average rate

was relatively high at 6.4% per year on average since the introduction of the inflation strategy.

This is high especially when it is noted that Brazil has adopted an inflation targeting regime

which is supposed not to only tame inflation but also to ‘lock-in’ inflation rates to low levels; (ii)

the annual nominal interest rate was around 18.4%, while the average real interest rate reached

11.2%; and (iii) the average annual growth rate of GDP was only 2.6%. Finally, it is important to

emphasize that the course and results of Lula’s economic policies, based on inflation targeting,

primary fiscal surplus and flexible exchange rate regime, did not perform as well as might be

34

expected by conventional wisdom, although some indicators have improved recently.

3.2 Global Financial Crisis 2007

The world’s economy is currently beset by more macroeconomic uncertainty than at any time in

the last 25 years. The financial crisis that started in the summer of 2007 and was intensified in

September 2008 has remade Wall Street; financial giants such as Bear-Stearns, Lehman

Brothers,Merrill-Lynch, AIG, FannieMae, FreddieMac, and Citigroup have either disappeared or

been rescued through large government bailouts. Goldman-Sachs and Morgan-Stanley converted

to bank holding companies in late September, perhaps marking the end of investment banking in

the United States.

While the U.S. economy initially appeared surprisingly resilient to the financial crisis that is

clearly no longer the case. The crisis that began on Wall Street has migrated to Main Street. The

National Bureau of Economic Research, the semi-official organization that dates recessions,

determined that a recession began in December 2007. By the beginning of 2009, the

unemployment rate had risen to 7.6%, before the current recession started of 4.4%. Forecasters

expect this rate to rise to 9% or even higher by 2010(figure 3.2), and it seems likely that this will

go down in history as the worst recession since the Great Depression of the 1930s.

Figure: 3.2 Unemployment rate

35

The controversial question of who to blame for the economic crisis is a strong debate and often

merely reflect a social need to determine a scapegoat during a time of panic. The treasury

secretary of the US Fed believes that the root cause of the crisis was the housing correction

which resulted in illiquid mortgage assets stemming off the flow of credit so vital to the economy

whilst others argue global imbalances played a central role (Figure 3.3). Academic literature

reveals and most commentators argue that Alan Greenspan’s administration of maintaining very

low interest rates for several years caused a housing boom, which in turn led to the sub-mortgage

crisis then sparked off the subsequent crisis around the world.

36

Figure 3.3: USA Noncurrent Mortgage (Percentage by mortgage category)

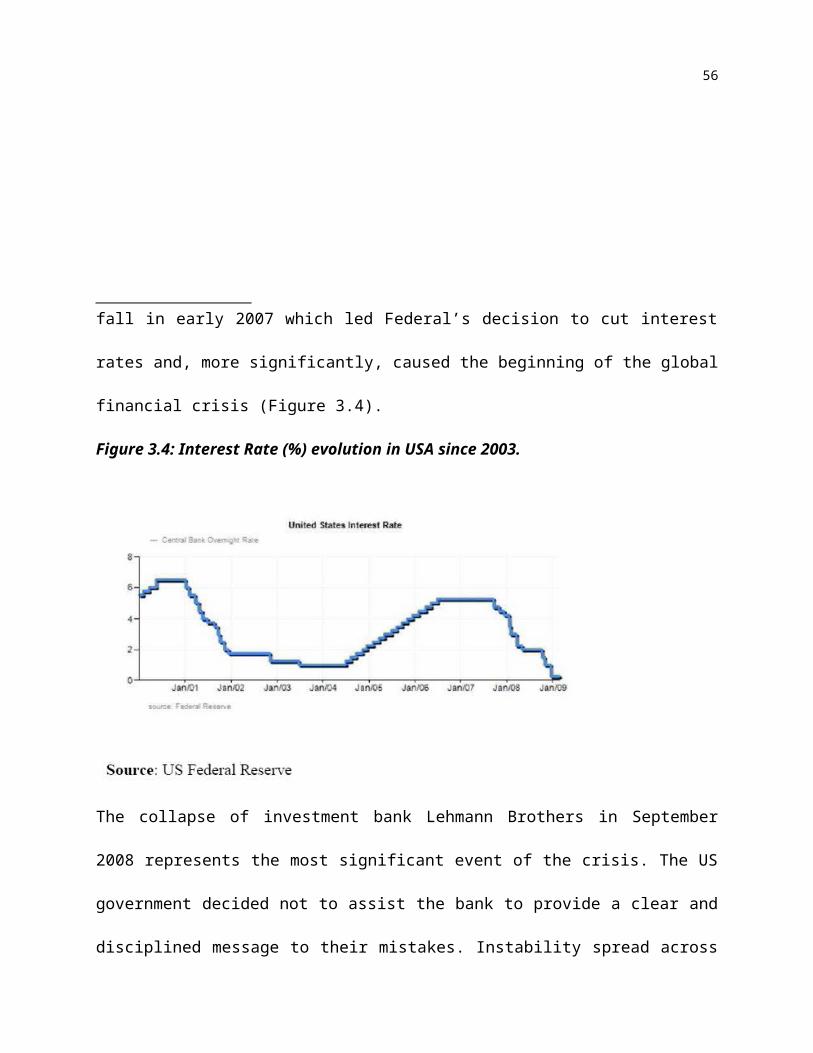

The U.S. housing boom began in late 1990s, gaining momentum as monetary easing after the I.T

bubble’s collapse sparked residential investment. Home ownership ratio surged from 65% in the

late 1990s to peak 70% in 2005. Residential investment grew as a ratio of nominal GDP, peaking

in 2005 after the Federal Reserve Bank initiated interest rate hikes in 2004. U.S. home prices

surged in early 2003 gradually decelerated as interest rate hikes curbed residential investment.

Home prices began to fall in early 2007 which led Federal’s decision to cut interest rates and,

more significantly, caused the beginning of the global financial crisis (Figure 3.4).

Figure 3.4: Interest Rate (%) evolution in USA since 2003.

37

The collapse of investment bank Lehmann Brothers in September 2008 represents the most

significant event of the crisis. The US government decided not to assist the bank to provide a

clear and disciplined message to their mistakes. Instability spread across markets and banks

worldwide stopped lending money to each other (LSE Panel Discussion, 2009). Lack of liquidity

in the derivatives market was exposed and governments had to intervene to prevent the collapse

of the entire financial system.

At the same time, banks in Europe faced problems related to subprime assets, but the

consequences were more apparent. French bank BNP Paribas and Britain’s Northern Rock

received an injection of €204 billion from the ECB to cover debts. In December 2008, Swiss

bank UBS reported losses caused by subprime assets of € 3.4 billion and followed soon after,

38

corporations reported mortgage related losses. Consequently, the Dow Jones index experienced

the biggest fall since 9/11 by January 2008. The Fed reacted by sharply cutting interest rates and

injected $700 billion in October and similar actions were taken in China, in the UK and in other

European countries (figure 3.5 and 3.6).

Figure: 3.5: Key stock markets value decline: Aug/07 – Feb/09

The figure 3.5 demonstrates the domino effect these occurrences had on the rest of the world

revealing the interdependence of global markets and what essentially began as US crisis

expanding into a global crisis.

Figure: 3.6 Economic slowdown, real GDP growth 2008-2010 forecast (US$ billion).

39

In the financial market, prices in commodities such as gold have risen as the stock prices are

unstable for investment. Safe bonds like treasury bills from the government become more

expensive as they became a safe haven. If people do not buy stocks, money may flow to safe

zero risk bonds and this will push up prices due to demand and reduce yields. If government

lowers interest rates, value of the bond goes up. The reason for that is that interest rates and

inflation go up and down together (Mishkin 2007) and policy makers have to tackle the economy

accurately.

Central Banks buy gilts, now ranges of assets to ensure that the supply of money will grow at

some rate to keep inflation target and restart economic growth. Central Banks aim to increase

supply of money to bring liquidity to all markets. There is an ongoing massive fiscal and

monetary stimulus in many countries but a new policy design to restore the financial sector

stability is also required (EIU, 2008; LSE Panel Discussion, 2009). On the other hand, there is a

40

threat of protectionism in the global trade and geopolitical changes that might occur (LSE Panel

Discussion, 2009). Indeed, global policy coordination will be vital to minimize the impact of the

crisis and prevent losses from ‘push-backs’ in the globalisation process and free trade gains

conquered in the previous decades. Moreover, the capitalist model is once again at risk but its

ability to reinvent itself shall prevail (The Guardian Debate, 2009).

3.3 Brazilian Market and the Global Crisis

“Brazil is in a markedly different place today than it was even five years ago. The global crisis

will no doubt hurt Brazil, but investors are likely to be rewarded for hanging on in difficult

times” (Chadwick 2008). Financial and political stress are not unusual to Brazil, indeed, over the

last thirty years, the country has endured debt crises, extended hyperinflation, currency crashes,

seven currency changes, economic recession, unemployment, the transition from military to

civilian government, presidential resignation to avoid impeachment, banking failures, and, more

recently, a period of rapid domestic and export growth that broke completely with traditional

experience. Therefore, we can argue that the consistent theme throughout these challenging years

has made Brazil resilient at both economic and social fields.

The current economic recession is very different from past crises, such as the Asian crisis of

1997, the 1998 Russian crisis and the crisis in the run-up to the Brazilian presidential election in

41

late 2002, as discussed before. In intervening years, President Lula has used the solid global

demand, surging commodity prices and elevated liquidity to lower external indebtedness. Neither

the private sectors nor public ones are heavily indebted in foreign currency and at the same time

currency and interest rate dynamics improved - Grinfeld (2009). Massive capital inflows have

allowed foreign exchange reserves to grow to around USD 208.795 billion at 2008(Figure 3.7),

which is equivalent to around a year worth of import, and Brazil has become a net international

creditor for the first time in its history (Bank of Brazil, 2009).

Figure: 3.7 Brazilian International Reserve

42

Source: Central Bank of Brazil

The strength of Brazil’s international payments position provides comfort to investors as well as

policy-makers, as it practically rules out the destructive dynamics of past currency crisis.

Nowadays, monetary policy can and is being used effectively as a counter-cyclical tool to protect

the fall in economic growth and to maintain the functioning of the country’s large domestic

market for goods and services.

OECD (2008) believes that the global crisis hit Brazil economy after the collapse of Lehman

Brothers in September 2008. The fall in GDP in the Q4/08 (Figure 3.8) was due not only to a

2.9% decline in exports but also to a 3.8% fall in domestic demand (a 2% drop in consumption)

and a 9.8% contraction in investment. Aggregate consumption will likely fall by 1% this year

and the unemployment rate will rise to around 10.5%, from 7.5% in September 2008.

Figure: 3.8 Brazil, real GDP growth

43

Source: IGBE

Before the crisis, strong global growth and rapid expansion in domestic credit sustained

economic expansion. Up to Q3/08, Brazil’s economic growth was strong, up by 6.8% year on

year. Investment, consumption and real wages were all rising rapidly. This cycle turned abruptly

in October as highlighted in the in the figure 3.9 and 4.0.

Figure: 3.9 Investment index, 1995=100, seasonally adjusted

44

Figure: 4.0 Household consumption index, 1995=100, seasonally adjusted

45

Prior to this recession in activities, there were already signs of overheating, especially in 2007

and 2008. For instance, the Brazilian currency “real” appreciated sharply as a result of improved

terms of trade, increased risk appetite on the part of investors and abundant global liquidity. In

addition, the current account deficit remained manageable through high commodity prices.

Private sector companies took advantage of this currency appreciation as well as low interest

rates abroad, at this time to hike dollar borrowings, both locally (through derivatives) and

abroad. These operations resulted in losses once crisis-induced depreciation of the real began in

September 2008 (Bank of Brazil 2008).

46

The rise of commodities price in 2008, affected by some means the inflation, originated a

tightening of domestic monetary policies in the second half of the year (Figure 4.1). Fiscal policy

remained expansionary, with current government spending growing one-to-one with taxation.

The result was that global excesses led to local ones. But the key factor associated with previous

crises, namely excessive foreign borrowing was large avoided. Companies mostly borrowed

locally in domestic currency and the public sector used favourable international conditions to

accumulate foreign exchange reserves and to move into a net creditor position in foreign

currency.

Figure: 4.1 Commodity Prices Indices (Total, Food and Energy)

47

Source: IMF

The initial impact of the crisis on the Brazilian economy was a reduced availability of credit: the

drying up of foreign funding meant that local banks provided less domestic credit as foreign

liabilities were repaid. This credit stringency was also driven by falling demand for exports and

diminished consumer expectations. These factors meant that local credit-dependent segments,

such as automobiles and consumer durables, suffered most.

The response of Brazilian monetary authorities to the crisis included measures to provide the

financial market with increased liquidity and permit the Central Bank of Brazil to take a more

48

proactive position. President Lula, under Provisional Measure No. 442 of October 6, 2008 (“MP

442/08”), broadened the authority of the Central Bank to appraise and accept assets of distressed

financial institutions and to grant foreign currency-denominated loans. Finally, on October 21st,

2008, President Lula also enacted Provisional Measure No. 443 (“MP 443/08”) in order to

increase the role of the Public Sector in the Brazilian Financial System (Mello and Betzios,

2008).

At the same period, the Central Bank imposes several reserve requirements on financial

institutions to control liquidity within the Brazilian financial system. By changing the

requirements related to reserve ratios, Central Bank influences the volume of funds available for

financial institutions to lend, and consequently, to make available on the market. According to

Central Bank of Brazil (2008), one of the primary objectives of these changes was to reduce the

reserve requirements referring to time deposits, which requested financial institutions the

obligation of deposit a reserve ratio of 15% of their average daily time deposits.

The expansion of public sector in Brazilian Financial System, by purchasing Assets from

financial institutions and extending foreign currency played an important role at monetary

policy. According to what occurred in the United States and Europe, in Brazil the authority for

the Central Bank to assist the Brazilian financial institutions that face cash shortages was

extended, allowing this authority to acquire credit portfolios institutions and to grant foreign

49

currency loans to Brazilian financial institutions to finance Brazilian foreign trades.

Finally, the authorities imposed on the financial institution the following measures, among others

deemed suitable by the Central Bank: (i) require additional funds to cover the risks to which the

financial institution is exposed; (ii) adopt more restrictive operating limits; (iii) restrict the

performance of certain transactions or operational modes; (iv) reestablish the liquidity levels

required from the institution; (v) suspend the distribution of any results beyond the minimum

limits prescribed by law or the bylaws or articles of association, when compliance with the

minimum standards for paid in capital, net worth or equity requirements are threatened by the

level of exposure of such institution; (vi) prohibit any acts that imply an increase in the

compensation of officers or other members of corporate bodies; (vii) prohibit development of a

new line of business; and (viii) sale of assets/divestiture.

50

4. CONCLUSION

To conclude my work, I have decided to make a comparison on what happened at the crises of

1998 and 2008, pointing out the reasons why Brazil did suffer an adverse impact back in 1998,

and what have changed in Brazilian economy and policy in 2008, which made Brazilian market

considerable strong to face the global financial crisis.

51

As mentioned at section I, Brazil went through into economy reform in 1990s and one of the

most remarkable fact was the start of Real Plan, which pegged the currency to the U.S. dollar on

a gradual schedule, breaking the inertia of inflationary expectations and introduced the new

currency “Real”. In its first years, the Real Plan’s implementation involved fiscal, monetary and

economic reforms, including privatization of some major state-run companies, which in turn led

to renewed interest on the part of foreign investors. But this progress was abruptly halted by the

1998 Asian crisis and Russian default. In the midst of this turbulent economic chapter, Brazil

redoubled its inflation-fighting efforts and adopted a floating exchange rate policy. These

measures — which included policy rates that hit 45% at one point — helped quell panicky

devaluation of the currency and bought the nation some time to instill confidence in a stricter

fiscal policy.

Right after the Brazilian currency crisis happened in 1998, the Brazilian market was given an aid

package from the IMF which renewed confidence in the economy, a temporary default from

domestic debt occurred with federal government. However, in the time of currency crisis some

important fact was implemented which became extremely important for later on at Brazilian

monetary and fiscal policy, such as floating exchange rate breaking with decades of exchange

rate manipulation and repression by the government.

52

Brazil’s newfound fiscal integrity stems from a number of initiatives. For example, the 2000 Fis-

cal Responsibility Act can impose severe penalties on elected officials at federal, state and local

levels who exceed budget constraints. Debt issued by Brazilian states has been renegotiated. Fur-

ther, federal debt has been restructured on more favorable terms by eliminating currency-indexed

bonds, reducing inflation-indexed debt and enlarging the fixed-rate component. The bottom line

is that foreign exchange depreciation does not cause sovereign solvency problems anymore.

These developments are reflected in the upgrades to investment grade status that Brazil’s debt

has achieved over the past year.

There is no doubt that the world is currently experiencing an extremely difficult time. But it is

also true that Brazil is among the countries that are better prepared to cope with the effects of the

global financial crisis – a fact pointed out by several organizations in many occasions, such as

the last issue of the OECD composite leading indicators, a survey encompassing 35 countries.

Brazilian fundamentals not only enable us to face the current environment in better conditions

than most countries, but also in a much better shape than in the past.

One of the distinguishing features of the Brazilian economy is its prudential regulatory

framework. The vigilant stance of the Central Bank prevented the development of disequilibria

and excesses that emerged in several other economies; not allowing the markets adopt risk taking

attitudes that led to the losses and problems that many countries are facing today. In fact, the

53

Brazilian framework is considered a model for prudential regulation and regarded as an example

to be followed by other regulatory authorities. However, this fact does not mean that Brazil is not

being hit or suffering the impacts of the financial turmoil. But the Brazilian government is

prepared to react and take all the necessary measures to tackle the crisis.

Ironically, President Luiz Inácio Lula da Silva, who currently enjoys sky-high popularity for his

handling of the financial crisis, was once viewed as a potential roadblock on the country’s path

to economic modernization. In 2002, when he first emerged as a candidate, the market was

suspicious of his blue collar origins and affiliation with the left-wing PT (Workers’ Party). But

such fears proved unfounded, as the Lula administration kept Cardoso’s main economic policy

orientation and restored market confidence. To underscore its commitment, the new government

increased its target for the primary budget surplus and upheld the Brazilian Central Bank’s

(BCB) operational autonomy

The recovery of the global economy since 2001, due to American economic growth and mainly

to Chinese economic growth, provoked an increase in both demand and prices of commodities in

the international trade. Consequently, the positive international conditions in that time included

both greater economic growth and increase of the liquidity of the Brazilian financial markets.

The implementation of consistent macroeconomic policies also fostered record inflows of

54

currencies to the country, while the performance of exporting companies and the dynamics of

global growth resulted in exports, trade balance and current account record highs. The

conjunction of these effects allowed significant improvement of external sustainability

indicators, which, in several cases, stand at the best levels of the historical series.

In 2007, Brazil recorded the fifth consecutive yearly current account surplus. This paramount

series in the economic history of the country was mainly driven by the significant trade results in

the period, which breached US$40 billion from 2005 to 2007, more than offsetting the increase

in net remittances of services and income; and about 200 billion dollars of credit in reserve in

2008. Therefore, with the credit crunch happened in 2007 did not presented large adverse impact

at Brazilian economy.

Finally, the case for “Brazil is a strong one”, we saw that Brazilian market has shown remarkable

resilience, setting it apart from many others countries, is due from the benefits from a set of con-

ditions very different from those of previous crises. The world’s hunger for commodities, despite

the current cyclical slowdown, is likely to increase in coming years. In the developing world, this

hunger stems from infrastructure investment, global population growth and increasing per capita

income. Demand from the developed world should also increase markedly in the near term, as

government bailout programs fund an unprecedented wave of infrastructure projects. Brazil has

55

proven itself capable of fundamental economic transformation and worthy of optimism about the

country’s ability to meet the challenges of the global crisis and further reform. The maturation of

its capital markets has been driven by sustained macroeconomic stability, declining real interest

rates, better corporate governance and management practices, and the steady growth of its mid-

dle class consumer sector. These attractive fundamentals — which have endured despite the

world’s market meltdown — make the country a very attractive opportunity for global investors.

(9853 Words)

5. BIBLIOGRAPHY

Amann, E. (2000). “Economic Liberalization and Industrial Performance in Brazil”. Oxford and

New York: Oxford University Press.

56

Amann, E. and Baer, W. (2000). “The Illusion of Stability: The Brazilian Economy under

Cardoso”, World Development, vol.28, no.10.

Amann, E. and Chang, H.J. (2004). “Brazil and South Korea: Economic Crisis and

Restructuring”. Institute of Latin America Studies. University of London 2004.

Aresti, P. and Filho, F. F. (2007). “Assessing the Economic Policies of President Lula da Silva in

Brazil: Has Fear Defeated Hope?”. Federal University of Rio Grande do Sul and CNPq, Rio

Grande do Sul, Brazil.

BANCO CENTRAL DO BRASIL. www.bcb.gov.br. Access in 2009.

Basu, S. (2002), “Financial Liberalization and Intervention: A New Analysis of Credit

Rationing”, Cheltenham, UK and Northamption, MA, USA: Edward Elgar.

Baumann, R. (2002). “Brazil in The 1009s An Economy in Transition”. PALGRAVE,

Houndmills, Basingstoke, Hampshire RG21 6XS. ISBN 0-333092196-8.

57

BERNANKE, B.S.; GERTLER, M.; GILCHRIST, S. (1999), “The financial accelerator in a

quantitative business cycle framework”. In: TAYLOR, J.; WOODFORD, M. (ed),

Handbook of Macroeconomics, Volume 1, Amsterdam: North Holland.

Branford, S. and Kucinski, B. (2003). “Politics Transformed: Lula and the Workers’ Party in

Brazil”. Latim America Bureau. ISBN 1 899365 61 3.

Bulmer, T. V. (1994). “An Economic History of Latin America since Independence”. Cambridge:

Cambridge University Press.

City of London (2009). “The Challenges and Opportunities for Financial Services in Brazil”.

Trusted Sources, Research & Networks.

Cooper, G. (2008). “The Origin of Financial Crises: Central Bank, credit bubbles and the

efficient market fallacy.” Great Britain. British Library Cataloguing in Publication Data.

Chadwick, B. (2008). “Surfing the Tsunami: Brazilian Markets and The Global Crisis”. The

Journal of The New York Society of Security Analysis, The Investment Professional

58

(November).

Edwards, L. (2007). “Brazil”. www.abc-clio.com. ABC-CLIO. ISBN 1-800368-6868.

FitzGerald, V. and Thorp, R. (2005) “Economic Doctrines in Latin America: Origins,

Embedding and Evolution”. Published by Macmillan, P. editors Valpy FitzGerald, Rosemary

Thord. P.cm. – (St. Antony’s series) “In association with St. Antony’s College.” Includes

bibliographical references and index. ISBN 1-4039-9749-7.

Franco, G. (1999a). “O Desafio Brasileiro- Ensaio Sobre Desenvolvimento, Globalizacao e

Moeda”. Sao Paulo: Editora 34.

Giambiagi, F. et al. (1999). “A Economia Brasileira nos anos 90”. BNDES

Gruben,W.C. and Welch, J.H. (2000). “Banking and Currency Crisis Recovery: Brazil’s

Turnaround of 1999”. Federal Reserve of Bank of Dallas, 2000.

59

Herscovitz, H. (2000). “Social and Institutional Influences on New Values and Routines in

Brazil: From Military Rule to Democracy”, paper presented at the 50th Annual Conference of the

International Communication Association, Acapulo, Mexico, June 1-5.

Kinzo, M.D. and Bulmer-Thomas,V. (1995). “Growth and Development in Brazil: Cardoso’s

Real Challenge”. Institute of Latin America Studies, 1995. British Library Catalogue-in-

Publication Data. ISBN 0 901145 96 3.

Kinzo, M.D and Dunkerley,J.( 2003). “Brazil since 1985 Economy, Polity and Society”. Institute

of Latin America Studies, School of Advanced Study University of London. British Library

Catalogue-in-Publication Data. ISBN1 900039 53 2

Lins da Silva, C. E. (2000). “Journalism and Corruption in Brazil”, in Joseph Tulchin and Ralph

Espach (eds.), Combating Corruption in Latin America (Baltimore: Woodrow Wilson Centre

Press), pp. 173-92.

Mello, J. L. H and Betzios, A. (2008). “Government Measure to Stave off the Effects of the

Financial Crisis in Brazil”. Attachment Biblioteca Informa, numero 2029. (October)

60

MISHKIN, F.S. (2000), “What should central banks do?”. Federal Reserve Bank of St.

Louis Review, 82(6), 1-13.

OECD (2008). “Brazil: Strengthening Governance for Growth”. (June)

OREIRO, J.L.; PAULA, L.F. (2007), “Strategy for economic growth in Brazil: a Post

Keynesian approach”. In: ARESTIS, P.; BADDELEY, M.; MCCOMBIE, J. (ed.).

Economic Growth: New Directions in Theory and Policy. Cheltenham, Edward

Elgar (Forthcoming).

Paes de Barro, R. et. al. (2000) “A estabilidade inaceitavel: desigualdade e pobreza no Brasil”,

in Ricardo Henriques (ed.), Desigualdade e Pobreza no Brazil (IPEA).

Pinheiro, P. S. (1994). “The legacy of authoritarianism in Democratic Brazil”, in Stuart S. Nagel

(ed.), Vigilantism and the State in Morden Latin America Development and Public Policy (New

York: St Martins Press).

61

Posthuma, A. (1999). “Introducao: transformacoes do emprego no Brasil na decada de 90”, in

Abertura e ajuste do mercado de trabalho o Brasil (Editora 34 Ltda).

Prates, D. (2006), “A inserção externa da economia brasileira no governo Lula”. In:

Política Econômica em Foco. Campinas: IE/UNICAMP.

Rochon, L. P and Rossi, S. (2006). “Monetary and Exchange Rate Systems: A Global View of

Financial Crises”. Edward Elgar Publishing Limited. Cheltenham, UK. Northampton, MA,

USA.

Sallum Jr. B. (1999). “O Brasil sob Cardoso: neoliberalismo e desenvolvimentismo”. Tempo

Social. Revista de Sociologia da USP, Sao Paulo, vol. 11. Numero 2, pp 23-47 (October).