Discussion of “Financial Innovation, Macroeconomic Stability and Systemic Risk” Bill Nelson Federal Reserve Board November 17, 2006 Disclaimer: The views I express are not necessarily those of the Federal Reserve Board or its staff.

Discussion of “Financial Innovation, Macroeconomic Stability and Systemic Risk” Bill Nelson Federal Reserve Board November 17, 2006 Disclaimer: The views.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Discussion of “Financial Innovation, Macroeconomic Stability and Systemic Risk”

Bill NelsonFederal Reserve Board

November 17, 2006

Disclaimer: The views I express are not necessarily those of the Federal Reserve Board or its staff.

Outline of discussion

• Review the premises and conclusions of the paper.

• Evaluate the premises in terms of some empirical evidence.

• Discuss the issues raised from the perspective of a practitioner.

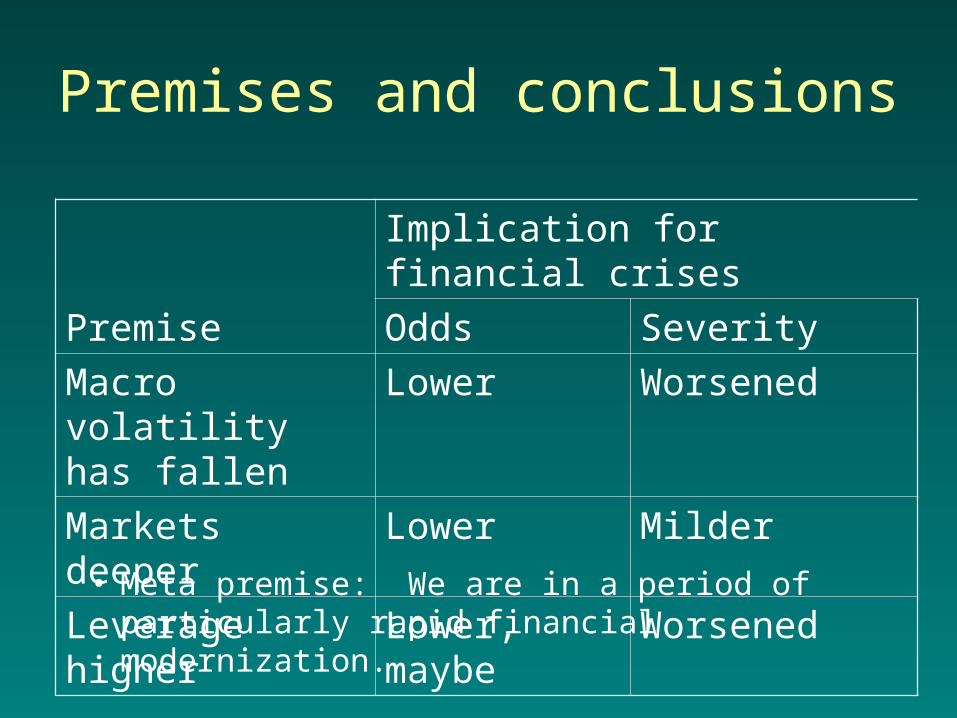

Premises and conclusions

• Meta premise: We are in a period of particularly rapid financial modernization.

Premise

Implication for financial crises

Odds Severity

Macro volatility has fallen

Lower Worsened

Markets deeper Lower Milder

Leverage higher Lower, maybe Worsened

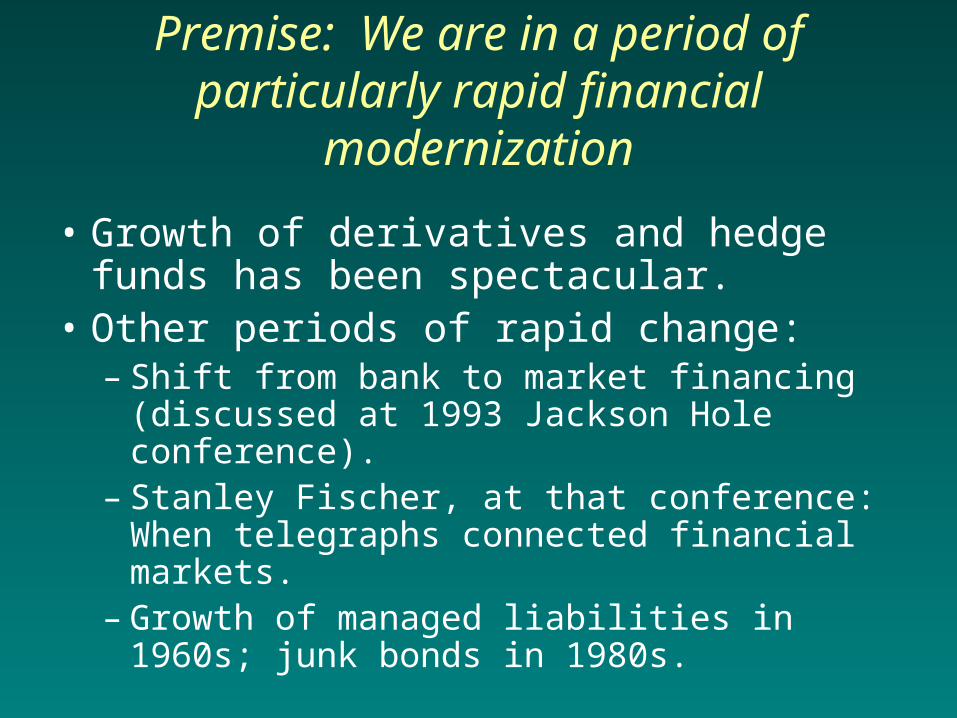

Premise: We are in a period of particularly rapid financial

modernization

• Growth of derivatives and hedge funds has been spectacular.

• Other periods of rapid change:– Shift from bank to market financing (discussed

at 1993 Jackson Hole conference).– Stanley Fischer, at that conference: When

telegraphs connected financial markets.– Growth of managed liabilities in 1960s; junk

bonds in 1980s.

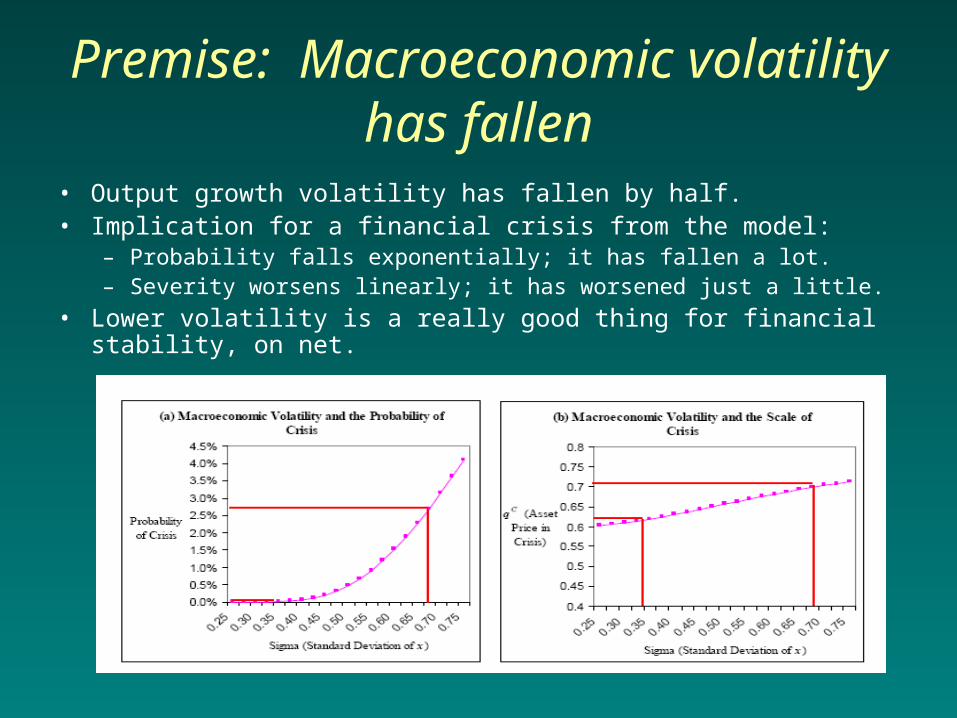

Premise: Macroeconomic volatility has fallen

• Output growth volatility has fallen by half.• Implication for a financial crisis from the model:

– Probability falls exponentially; it has fallen a lot.– Severity worsens linearly; it has worsened just a little.

• Lower volatility is a really good thing for financial stability, on net.

Premise: Asset markets have become deeper.

• Not clear if the assertion in the paper is that the resale market for physical or financial assets has become deeper.

• Growth of CDS and syndicated loan market have made it easer to resell corporate liabilities.

• Measures of liquidity in these markets are scarce and don’t go back in time very far.

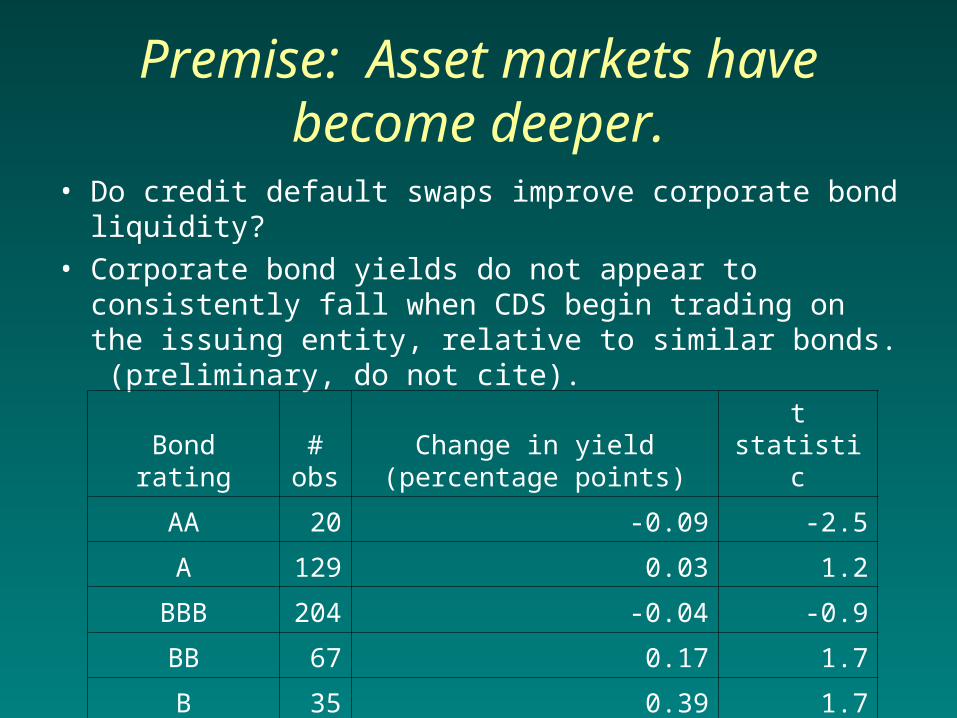

Premise: Asset markets have become deeper.

• Do credit default swaps improve corporate bond liquidity?

• Corporate bond yields do not appear to consistently fall when CDS begin trading on the issuing entity, relative to similar bonds. (preliminary, do not cite).

Bond rating#

obsChange in yield (percentage

points) t statistic

AA 20 -0.09 -2.5

A 129 0.03 1.2

BBB 204 -0.04 -0.9

BB 67 0.17 1.7

B 35 0.39 1.7

Premise: Leverage has increased

• Not clear in the paper whose leverage has supposedly increased, nonfinancial corporations or financial intermediaries. – In the model, financial intermediaries own the

means of production.

• Regardless, leverage appears to have fallen, not risen, in all the relevant sectors, at least in the U.S.

Premise: Leverage has increased

• Leverage of U.S. nonfinancial corporations has trended down for a decade.

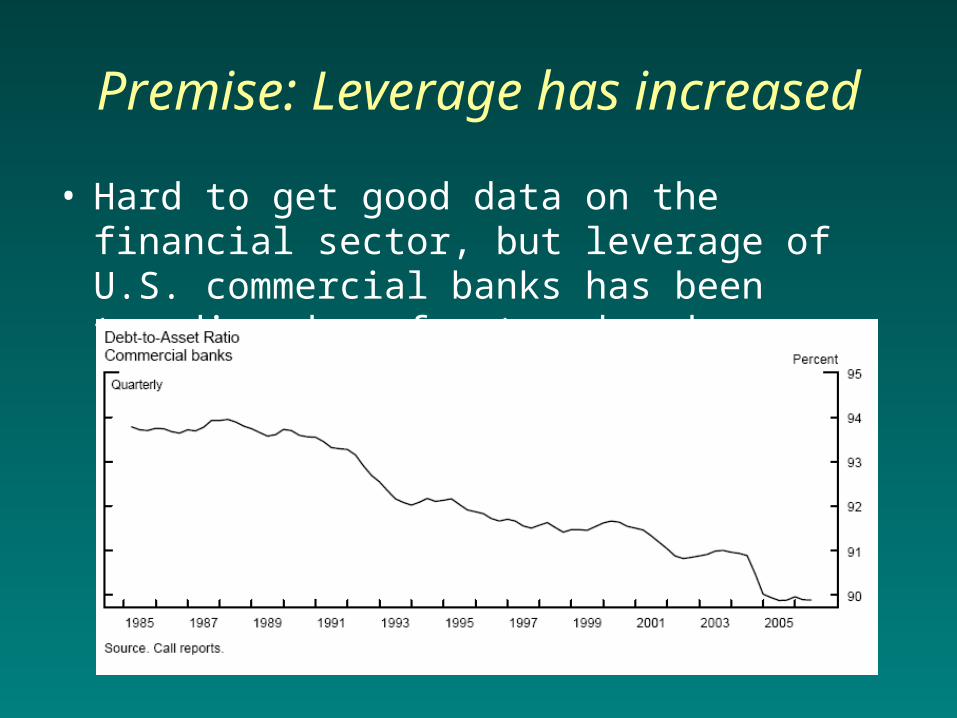

Premise: Leverage has increased

• Hard to get good data on the financial sector, but leverage of U.S. commercial banks has been trending down for two decades.

Premise: Leverage has increased

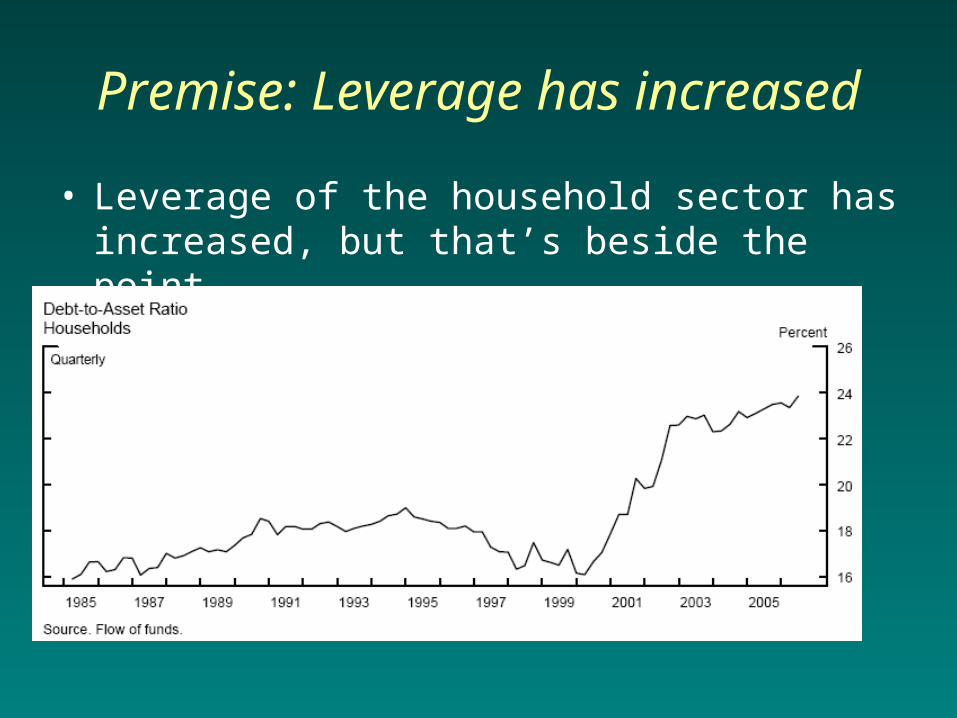

• Leverage of the household sector has increased, but that’s beside the point.

Premise: Leverage has increased

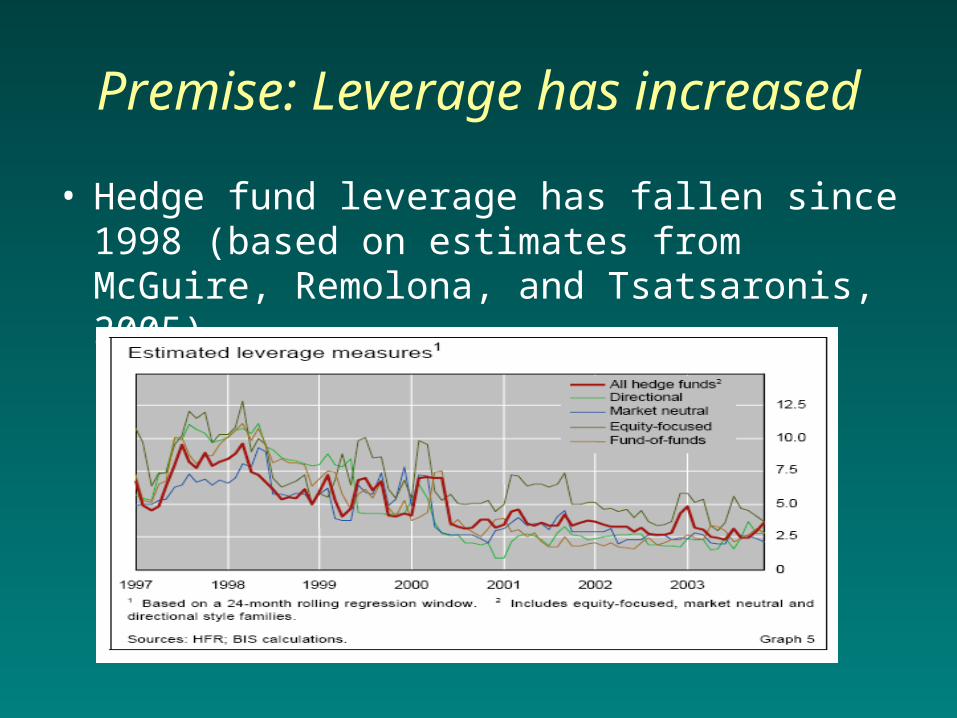

• Hedge fund leverage has fallen since 1998 (based on estimates from McGuire, Remolona, and Tsatsaronis, 2005).

Premise: Leverage has increased

• Perhaps the point is that hedge funds’ share of financial intermediation has risen.– But hedge funds appear to be less, not more,

levered than banks.– In risk adjusted terms, maybe hedge funds

are more levered. • They do seem to fail more frequently.

Premise: Leverage has increased

• A quibble with the analysis.

• Risk of crisis highest for middle-income financial systems.

• But model isn’t estimated, or even really calibrated.

• Hard to know what part of the curve we are on.

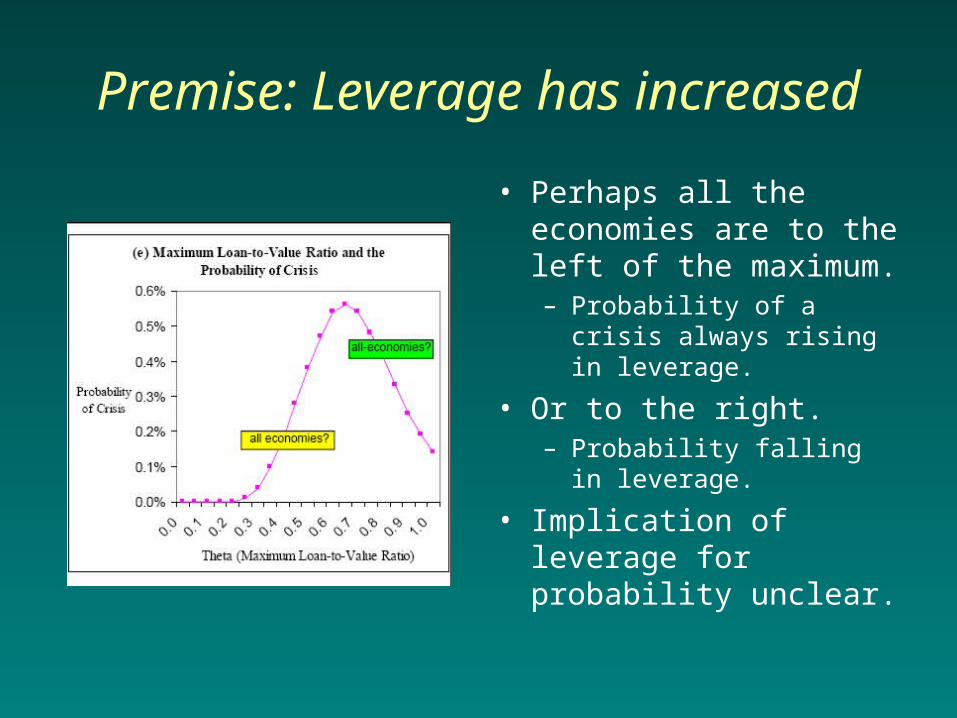

Premise: Leverage has increased

• Perhaps all the economies are to the left of the maximum.– Probability of a crisis

always rising in leverage.

• Or to the right.– Probability falling in

leverage.

• Implication of leverage for probability unclear.

Has financial modernization made crises less likely?

• While Russia/LTCM resulted in a financial crisis (maybe), subsequent shocks, (stock market crash, 9/11, Enron, Ford and GM, Amaranth) have not.

• Financial sector seems resilient, importantly because of low leverage.– At odds with the paper.

• But also increased market depth and role of market participants that will buy when positions are liquidated.– In accord with the paper.

Has financial modernization made crises less likely?

• LTCM lost $2 billion. – FRBNY coordinated a private-sector bailout.– Market liquidity fell and there was a broad pullback

from risk taking.– The FOMC eased policy three times to cushion the

blow on the economy.

• Amaranth lost $6 billion.– Citadel and JPMC acquired the portfolio.– There was barely a ripple in financial markets.– But financial institutions healthier.

Would crises be worse?

• Maybe, it’s hard to say.• Lot’s of clever people think so.

– Counterpart Risk Management Policy Group (Corrigan report); President Geithner (as quoted); Bill White at the BIS.

• A couple of key questions:– How would hedge funds and their counterparties act

in a crisis?– How would financial markets respond to a major

economic downturn?

How would hedge funds and their counterparties act in a crisis?

• Hedge funds are important providers of liquidity.• In a crisis, increased volatility could lead to

higher VaRs, leading counterparties to raise collateral requirements, potentially resulting in a sharp reduction in market liquidity.

• Hedge funds are new so their behavior is less certain.

• Banks have more stable funding sources, maybe.

How would hedge funds and their counterparties act in a crisis?

• Supervisory effort are underway to understand better how hedge funds and their counterparties manage risk.

• My colleagues and I are examining if hedge funds are likely to be heading for the exits simultaneously (preliminary, do not cite).

How would financial markets respond to a major economic

downturn?

• Market for credit risk has become more complex.• However:

– The CDS market has worked through some large failures and downgrades.

– FRBNY has led a successful effort to strengthen CDS infrastructure.

• Still, it is unclear how the CDS market would cope with a widespread deterioration in credit quality.

• In addition, financial institutions could be weakened and so less resilient.

What additional research would be most valuable?

• Financial crises require– A shock.– Propagation.

• Can we predict shocks? – Probably not promising.

• How will market participants respond to a shock?– When could simultaneous risk management actions

result in a reduction in market liquidity?

• How do asset prices behave in crises?

What additional research would be most valuable?

• Can we get better measures of financial system resilience?– Does increased financial fragility, investor

skittishness, leave a measurable imprint?

• What policies are most effective for preventing or responding to a financial crisis?– Including ex ante policies designed to increase

resilience.– And ex post policies such as providing liquidity.

Discussion of “Financial Innovation, Macroeconomic Stability and Systemic Risk”

Bill NelsonFederal Reserve Board

November 17, 2006

Related Documents