THE DIRECT TAXES CODE, 2010 Bill No. 110 of 2010 PRESENTED BY :- SUPRIT SHARAN ARPITA SINGH

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

THE DIRECT TAXES CODE, 2010

Bill No. 110 of 2010

PRESENTED BY :-

SUPRIT SHARAN

ARPITA SINGH

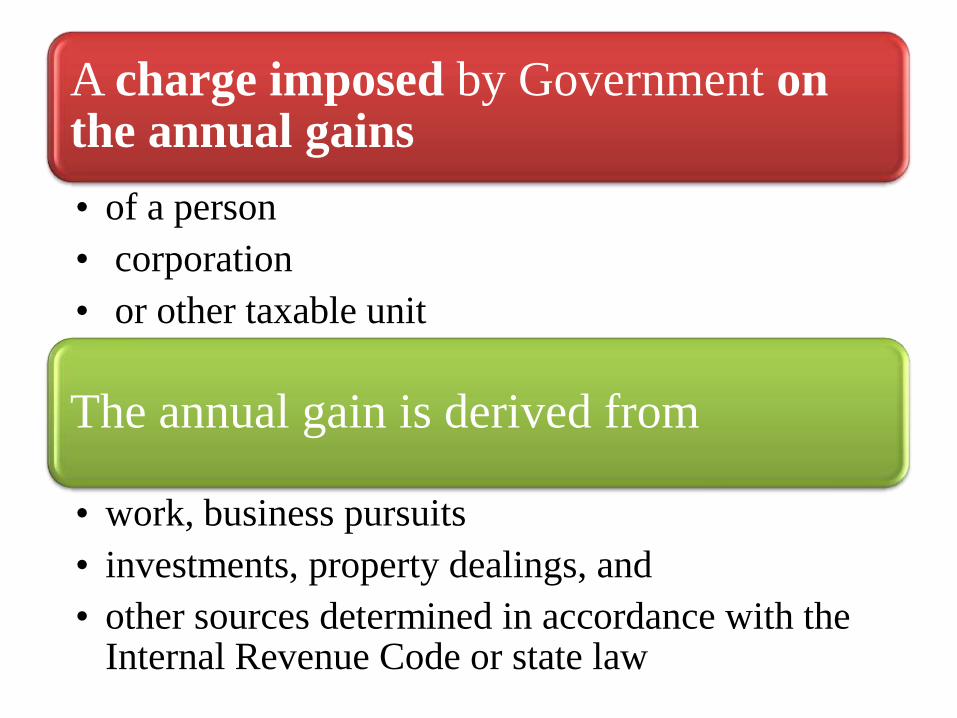

A charge imposed by Government on the annual gains

• of a person

• corporation

• or other taxable unit

The annual gain is derived from

• work, business pursuits

• investments, property dealings, and

• other sources determined in accordance with the Internal Revenue Code or state law

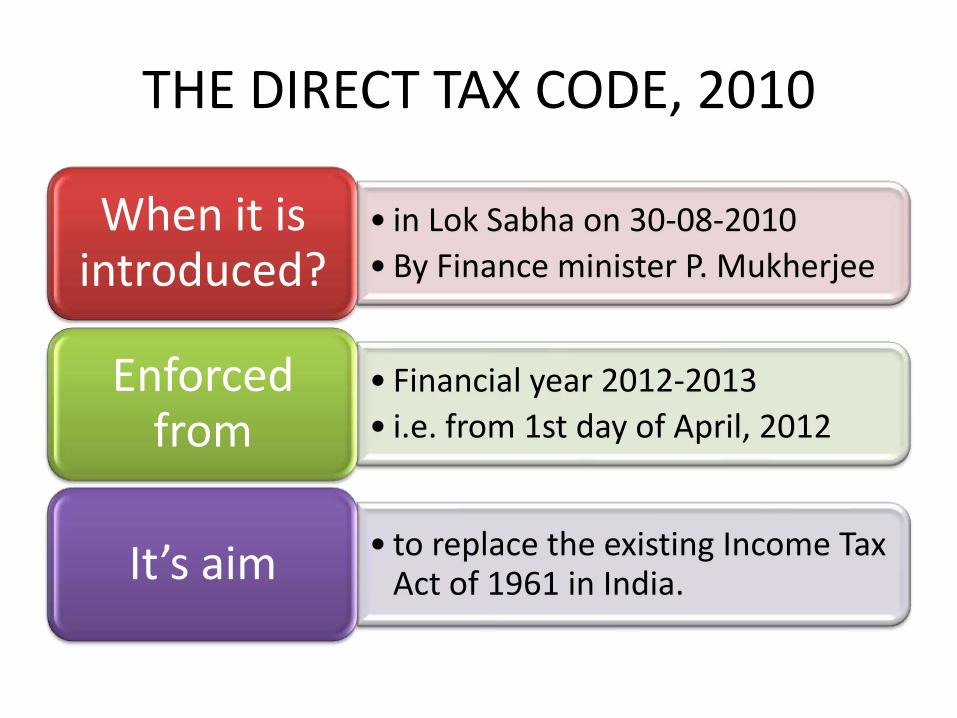

THE DIRECT TAX CODE, 2010

• in Lok Sabha on 30-08-2010

• By Finance minister P. Mukherjee

When it is introduced?

• Financial year 2012-2013

• i.e. from 1st day of April, 2012

Enforced from

• to replace the existing Income Tax Act of 1961 in India.It’s aim

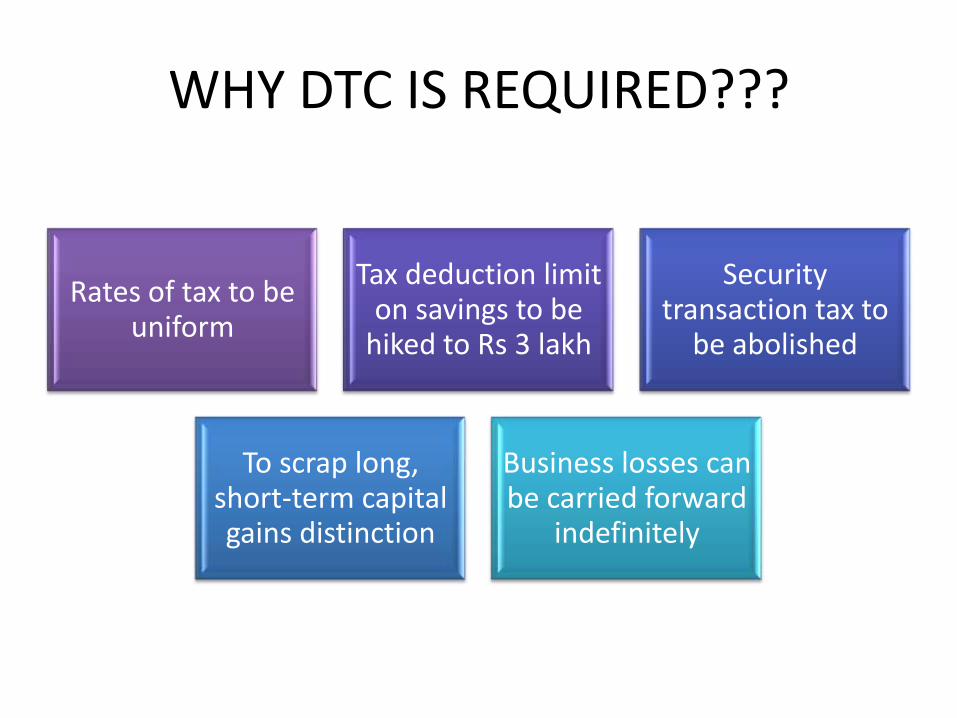

WHY DTC IS REQUIRED???

Rates of tax to be uniform

Tax deduction limit on savings to be

hiked to Rs 3 lakh

Security transaction tax to

be abolished

To scrap long, short-term capital gains distinction

Business losses can be carried forward

indefinitely

No tax deduction on interest payable on any Government security

Effective corporate tax rate at 30 %

Highest tax rate of 30% for individual of income over

Rs 25 lakh

AND…

TO PROMOTE THE

LONG-TERM INVESTMENT

BASIS OF CHARGE

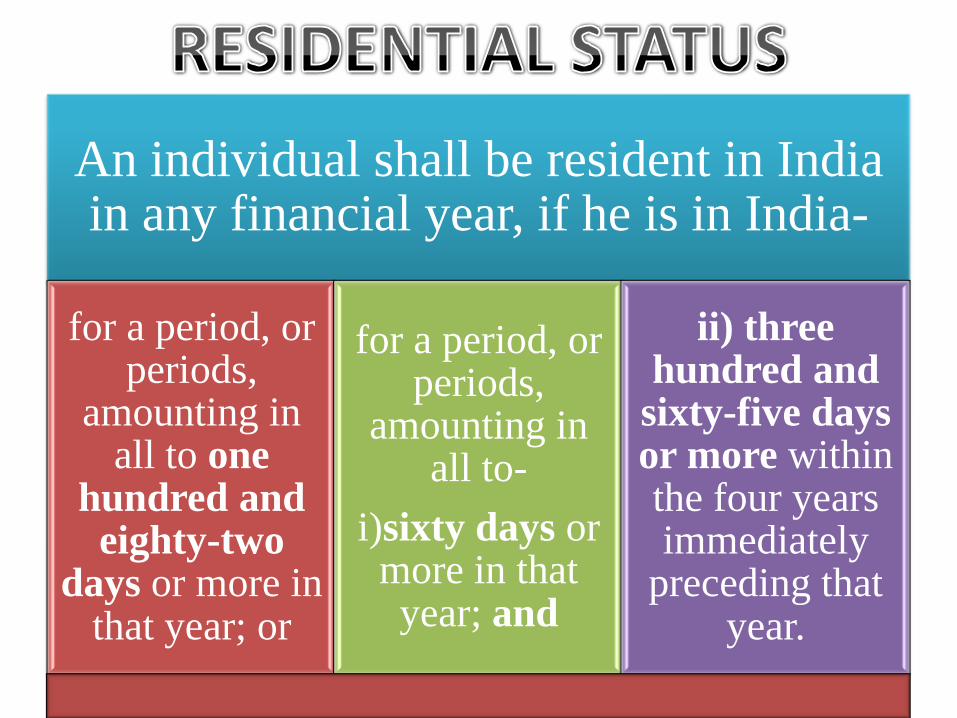

RESIDENTIAL STATUS

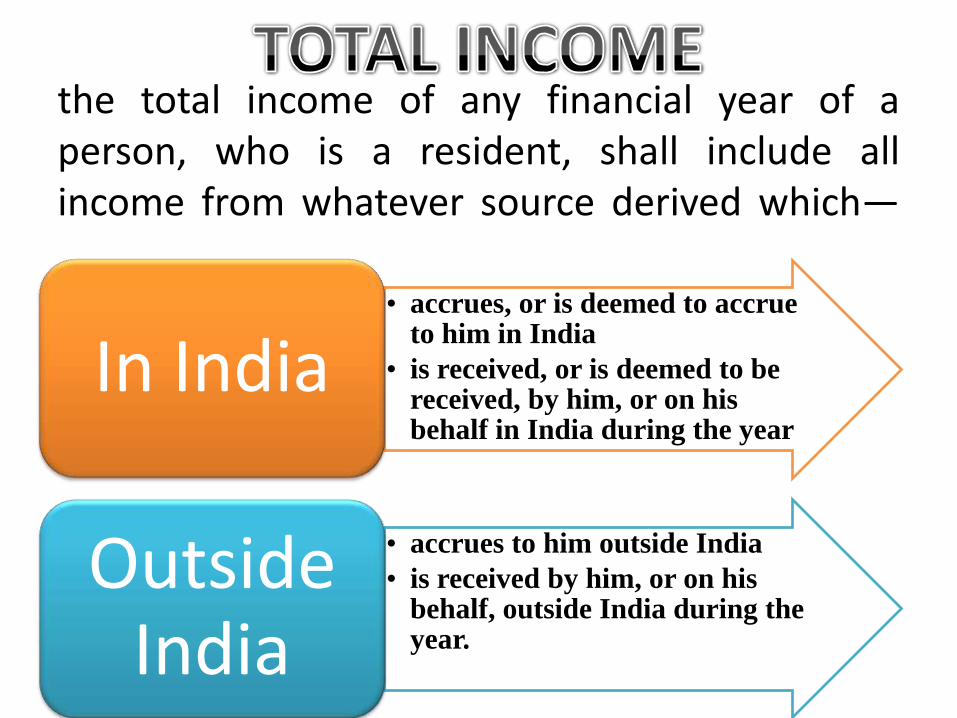

TOTAL INCOME

An individual shall be resident in India in any financial year, if he is in India-

for a period, or periods,

amounting in all to one

hundred and eighty-two

days or more in that year; or

for a period, or periods,

amounting in all to-

i)sixty days or more in that year; and

ii) three hundred and

sixty-five days or more within the four years immediately

preceding that year.

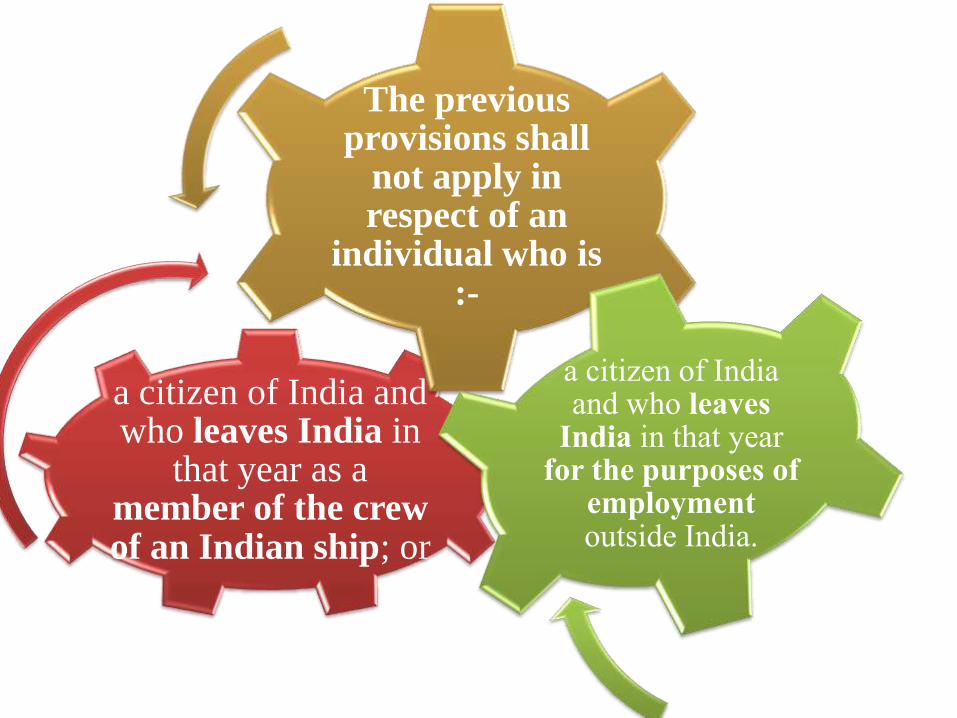

a citizen of India and who leaves India in

that year as a member of the crew of an Indian ship; or

The previous provisions shall

not apply in respect of an

individual who is :-

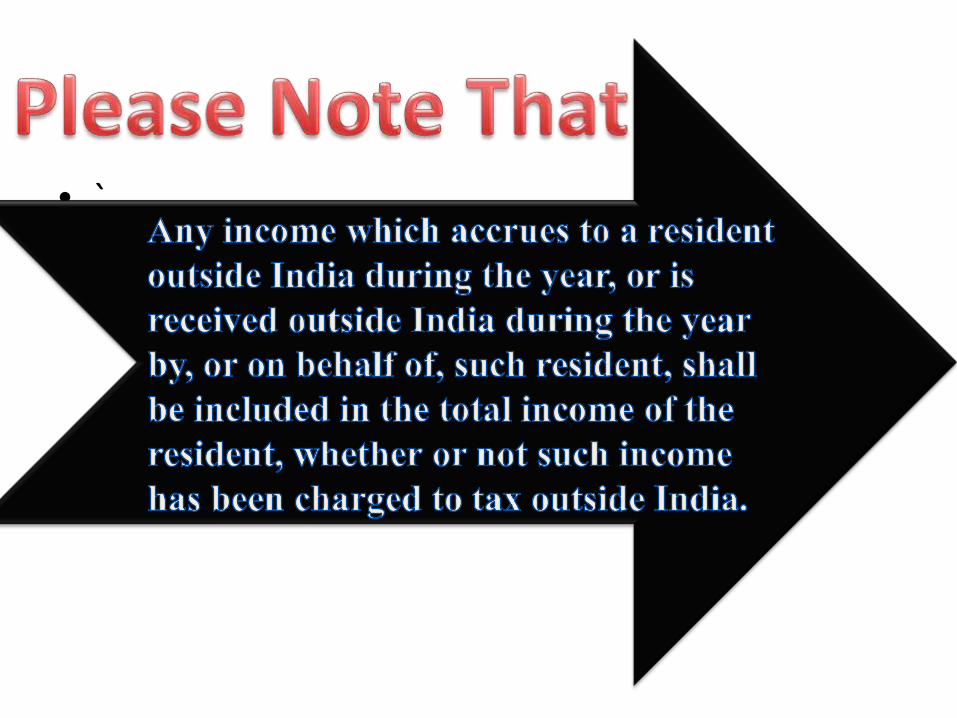

the total income of any financial year of aperson, who is a resident, shall include allincome from whatever source derived which—

• accrues, or is deemed to accrue to him in India

• is received, or is deemed to be received, by him, or on his behalf in India during the year

In India

• accrues to him outside India

• is received by him, or on his behalf, outside India during the year.

Outside India

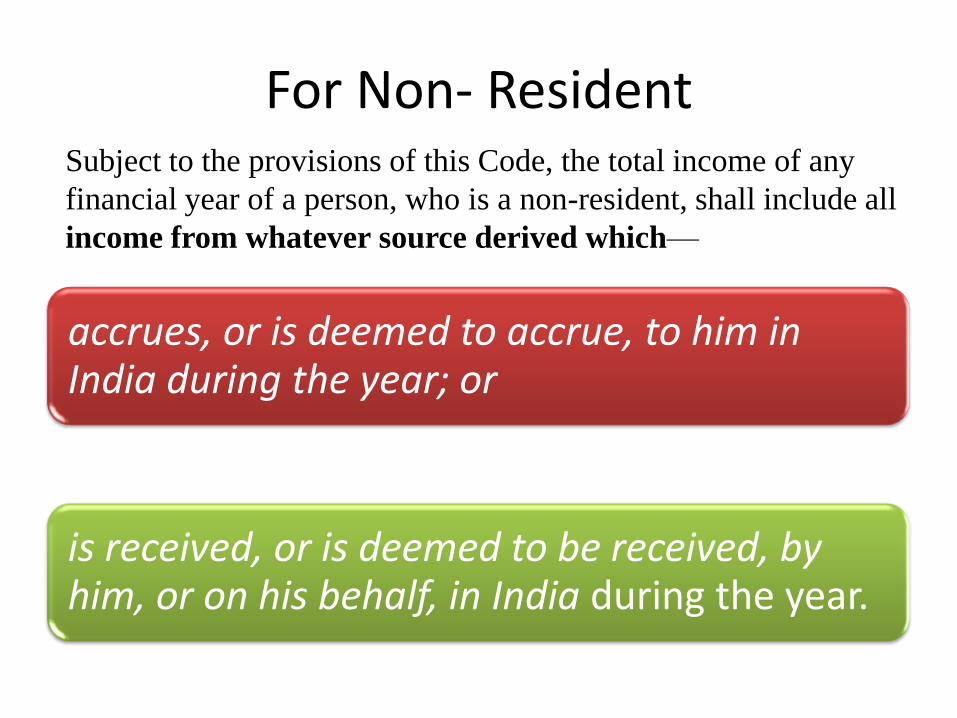

For Non- Resident

accrues, or is deemed to accrue, to him in India during the year; or

is received, or is deemed to be received, by him, or on his behalf, in India during the year.

Subject to the provisions of this Code, the total income of any

financial year of a person, who is a non-resident, shall include all

income from whatever source derived which—

• `

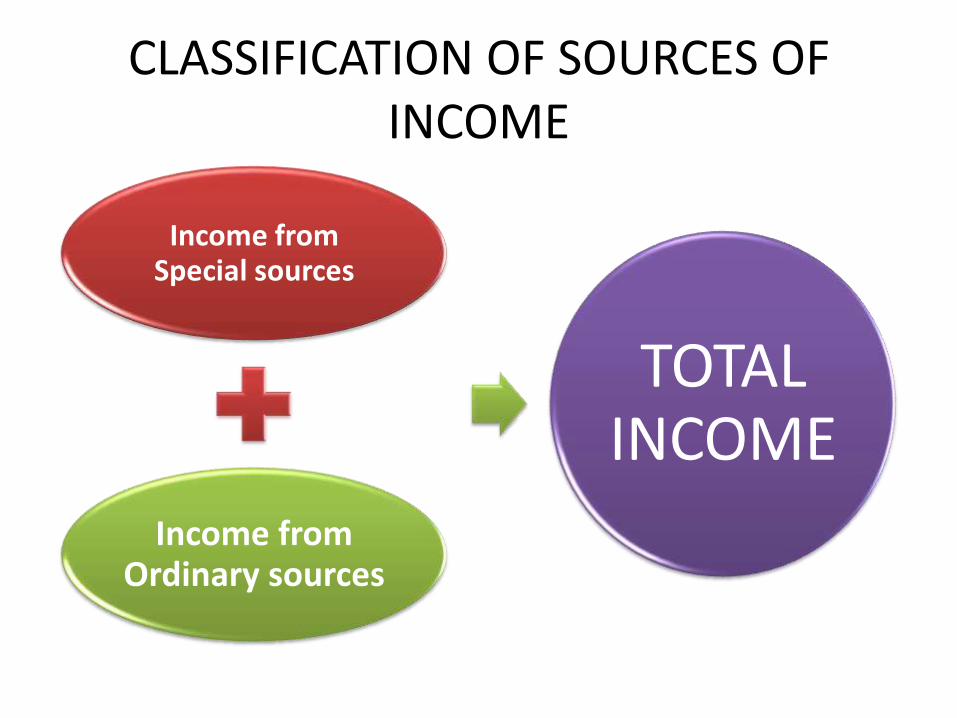

CLASSIFICATION OF SOURCES OF INCOME

Income from Special sources

Income from Ordinary sources

TOTAL INCOME

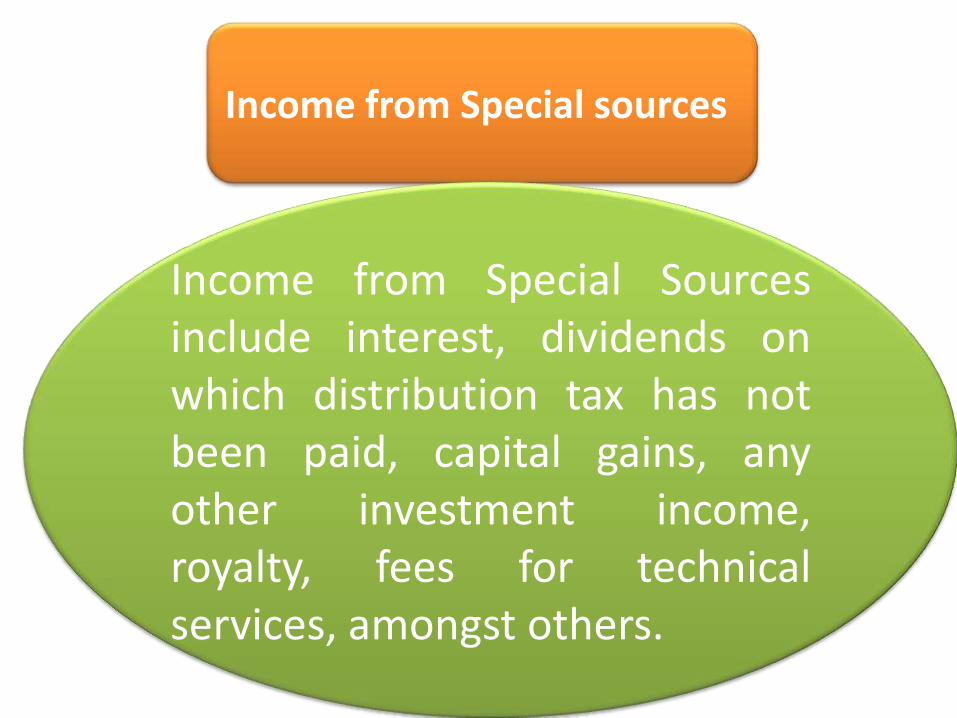

Income from Special sources

Income from Special Sourcesinclude interest, dividends onwhich distribution tax has notbeen paid, capital gains, anyother investment income,royalty, fees for technicalservices, amongst others.

Income from Ordinary sources

Income from employment

Income from House

Property

Income from Business

Capital gainsIncome from

Residuary Sources

Income from employment

Gross salary, including the value of perquisites and profits in lieu of salary, to be taxed on due or receipt basis, whichever is earlier and to be reduced by permissible deductions

Permissible deductions to include professional tax, transport allowance, prescribed special allowance, compensation under voluntary retirement scheme, gratuity, commutation of pension, amongst others

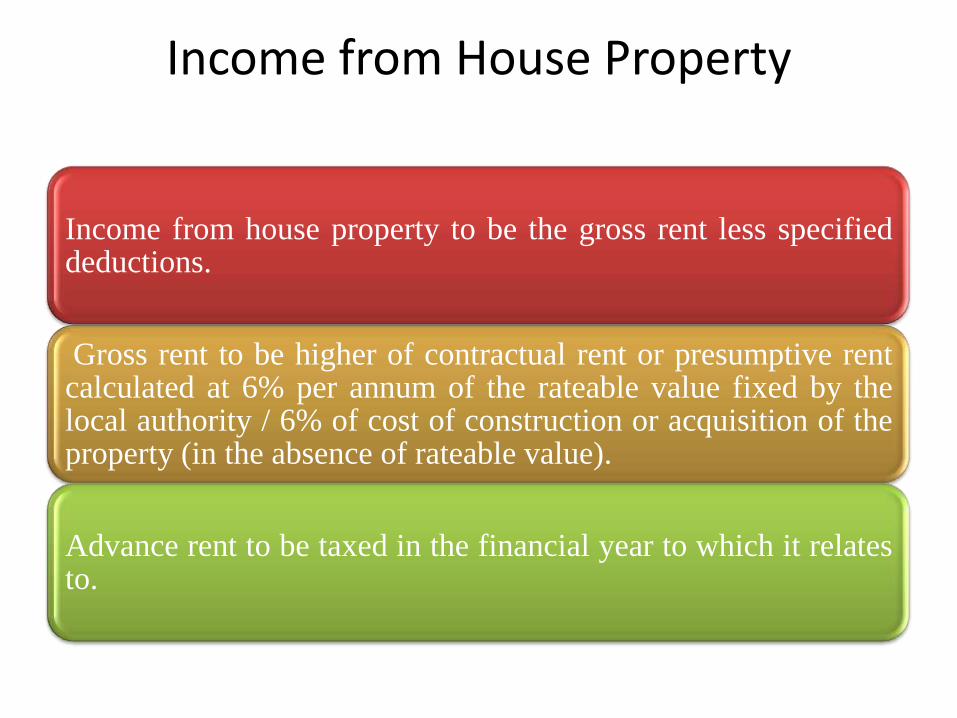

Income from House Property

Income from house property to be the gross rent less specifieddeductions.

Gross rent to be higher of contractual rent or presumptive rentcalculated at 6% per annum of the rateable value fixed by thelocal authority / 6% of cost of construction or acquisition of theproperty (in the absence of rateable value).

Advance rent to be taxed in the financial year to which it relatesto.

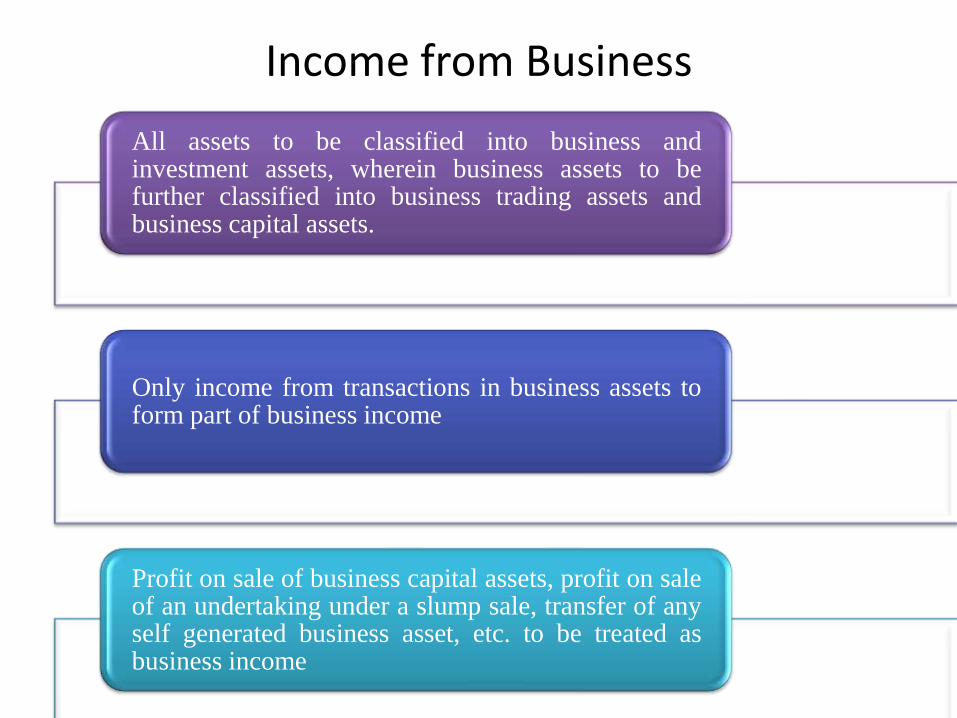

Income from Business

All assets to be classified into business andinvestment assets, wherein business assets to befurther classified into business trading assets andbusiness capital assets.

Only income from transactions in business assets toform part of business income

Profit on sale of business capital assets, profit on saleof an undertaking under a slump sale, transfer of anyself generated business asset, etc. to be treated asbusiness income

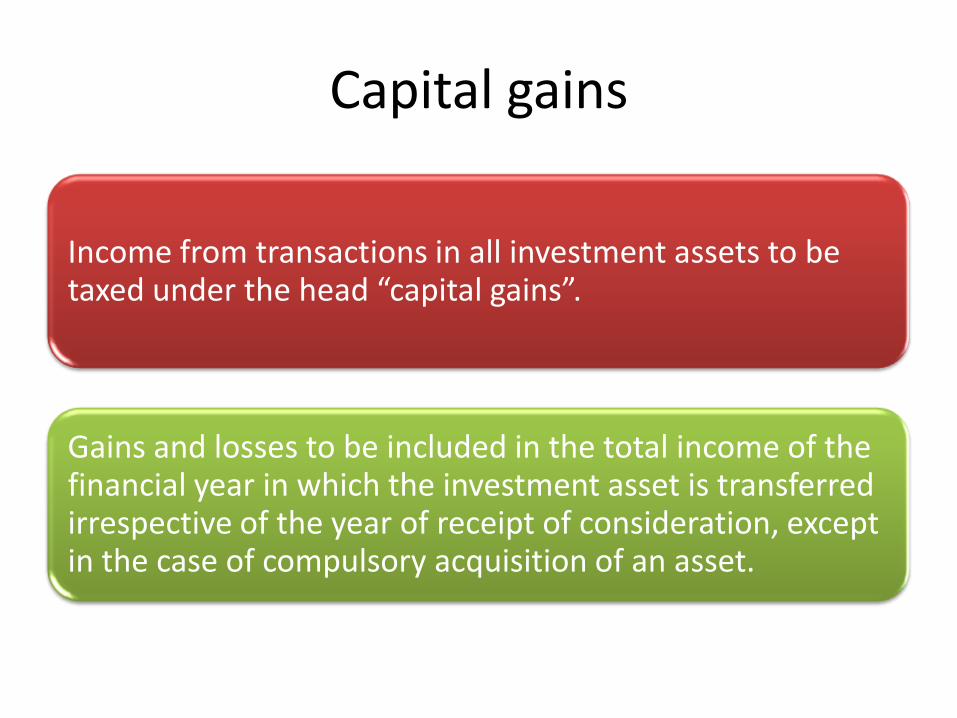

Capital gains

Income from transactions in all investment assets to be taxed under the head “capital gains”.

Gains and losses to be included in the total income of the financial year in which the investment asset is transferred irrespective of the year of receipt of consideration, except in the case of compulsory acquisition of an asset.

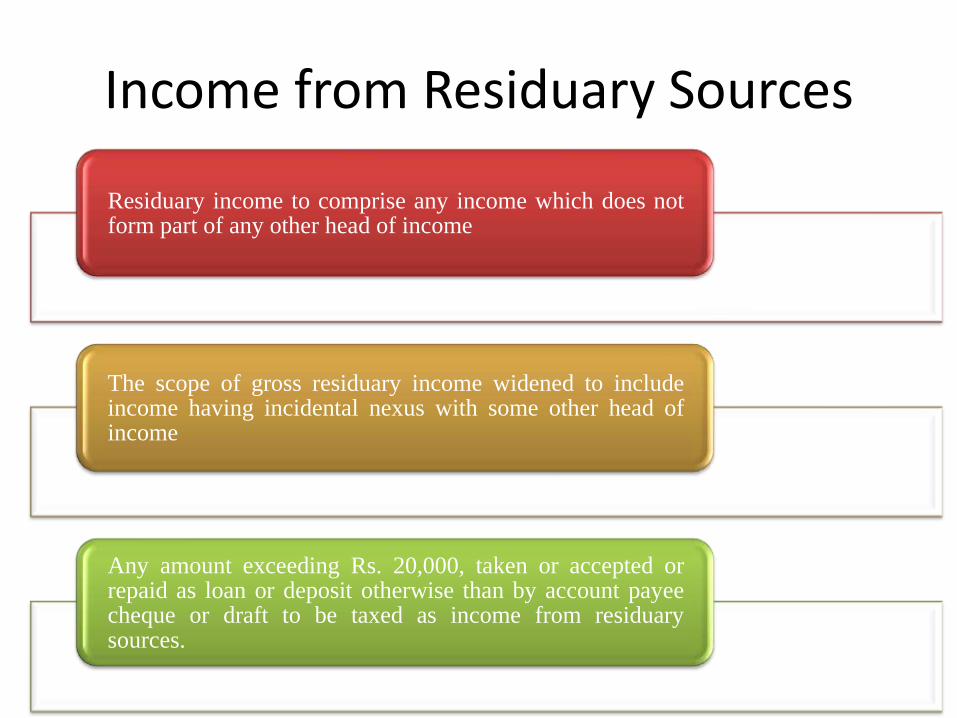

Income from Residuary Sources

Residuary income to comprise any income which does notform part of any other head of income

The scope of gross residuary income widened to includeincome having incidental nexus with some other head ofincome

Any amount exceeding Rs. 20,000, taken or accepted orrepaid as loan or deposit otherwise than by account payeecheque or draft to be taxed as income from residuarysources.

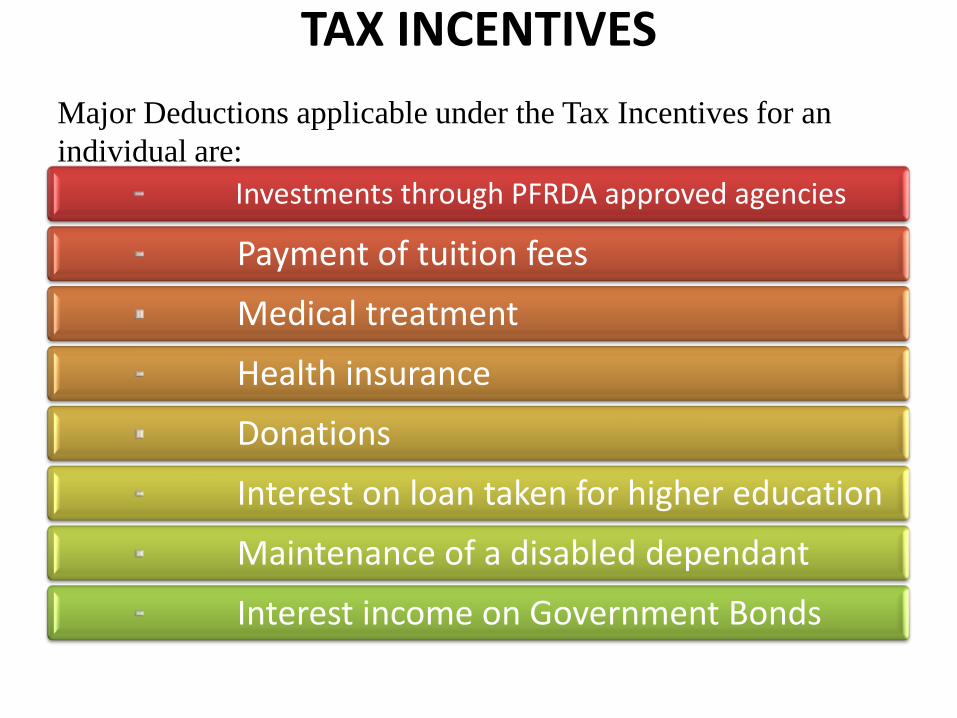

TAX INCENTIVES

Investments through PFRDA approved agencies

Payment of tuition fees

Medical treatment

Health insurance

Donations

Interest on loan taken for higher education

Maintenance of a disabled dependant

Interest income on Government Bonds

Major Deductions applicable under the Tax Incentives for an

individual are:

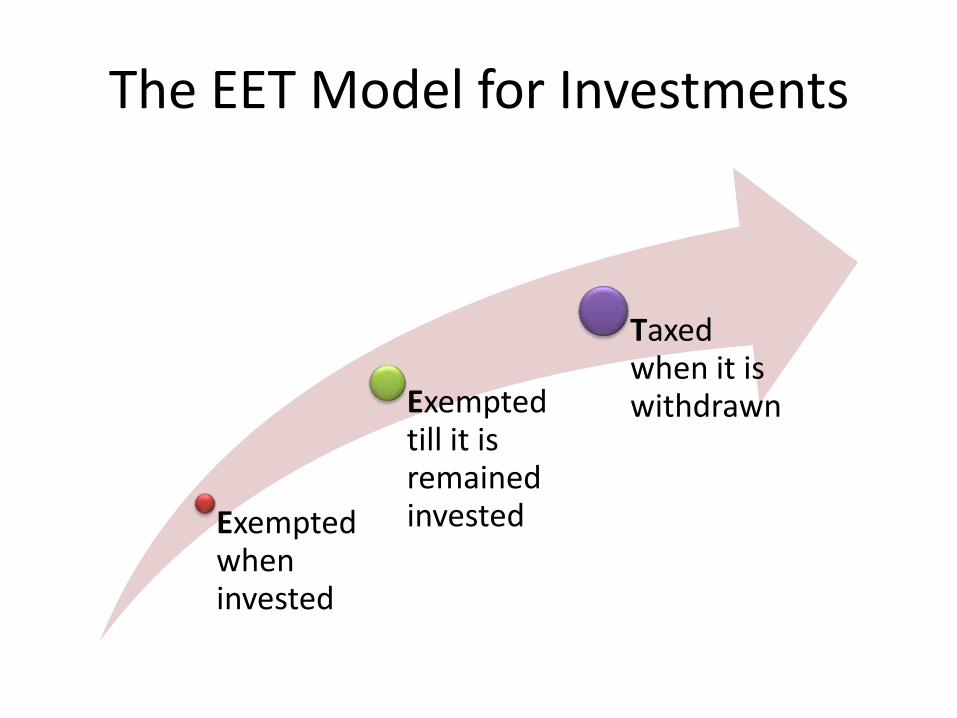

The EET Model for Investments

Exempted when invested

Exempted till it is remained invested

Taxed when it is withdrawn

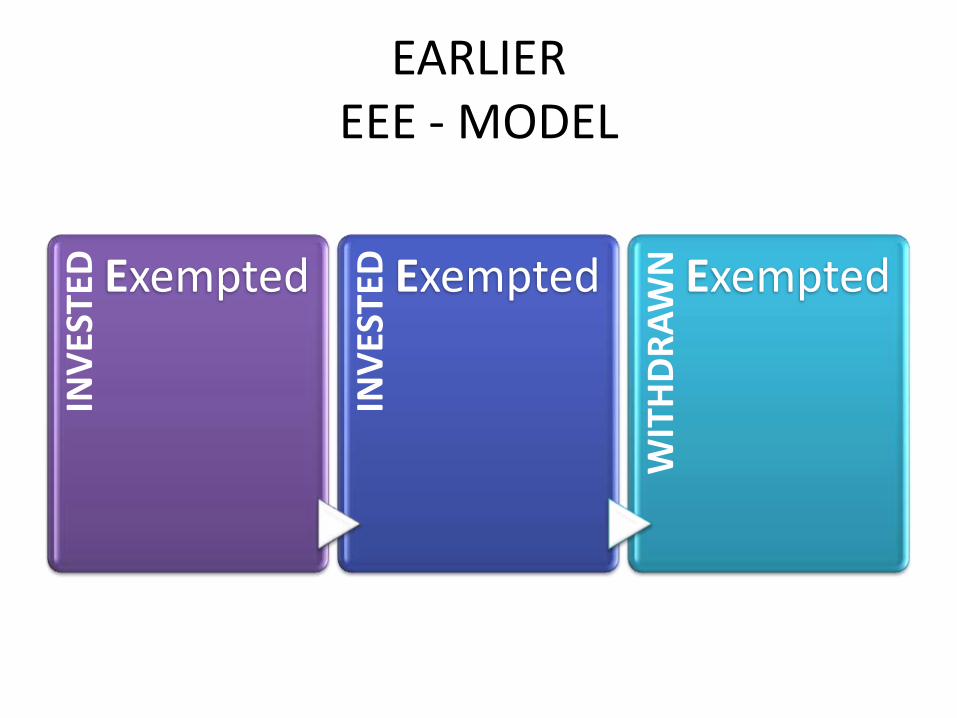

EARLIEREEE - MODEL

INV

ESTE

D Exempted

INV

ESTE

D Exempted

WIT

HD

RA

WN Exempted

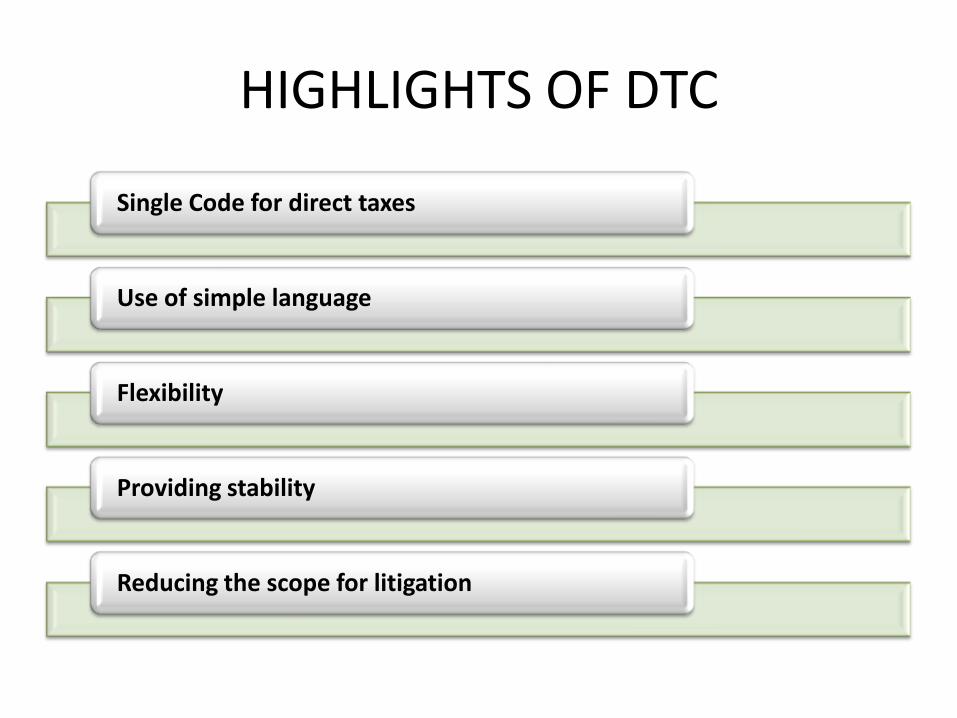

HIGHLIGHTS OF DTC

Single Code for direct taxes

Use of simple language

Flexibility

Providing stability

Reducing the scope for litigation

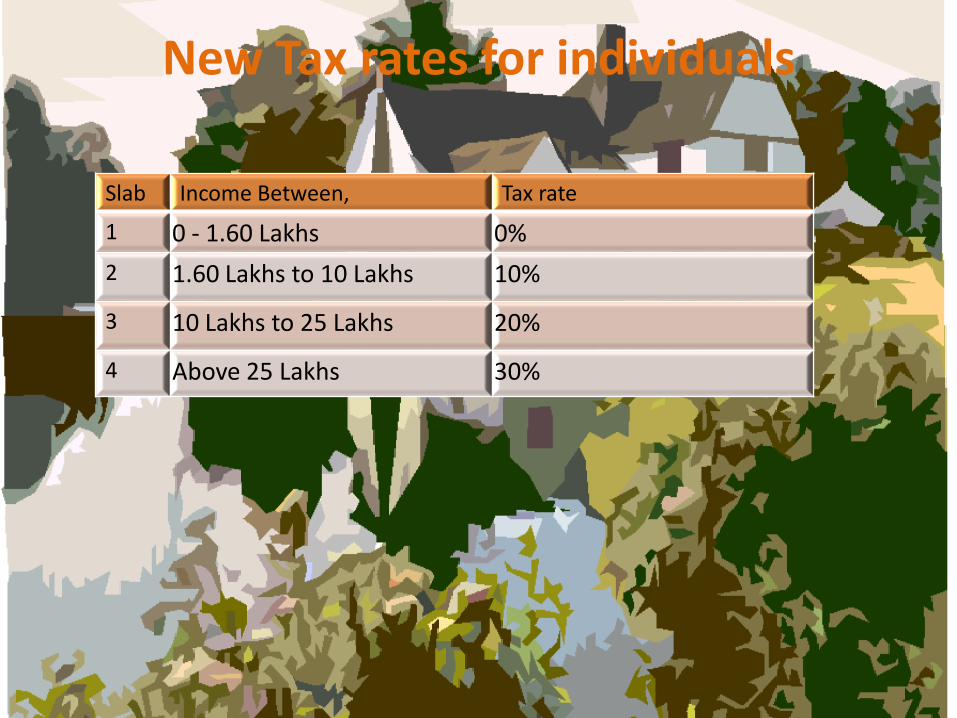

New Tax rates for individuals

Slab Income Between, Tax rate

1 0 - 1.60 Lakhs 0%

2 1.60 Lakhs to 10 Lakhs 10%

3 10 Lakhs to 25 Lakhs 20%

4 Above 25 Lakhs 30%

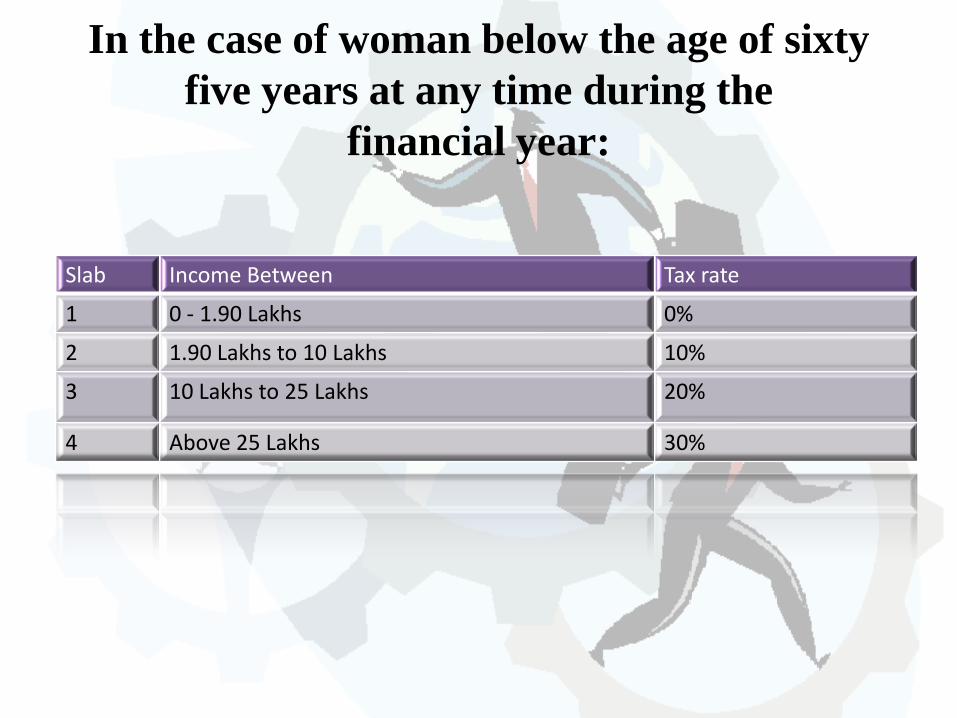

In the case of woman below the age of sixty

five years at any time during the

financial year:

Slab Income Between Tax rate

1 0 - 1.90 Lakhs 0%

2 1.90 Lakhs to 10 Lakhs 10%

3 10 Lakhs to 25 Lakhs 20%

4 Above 25 Lakhs 30%

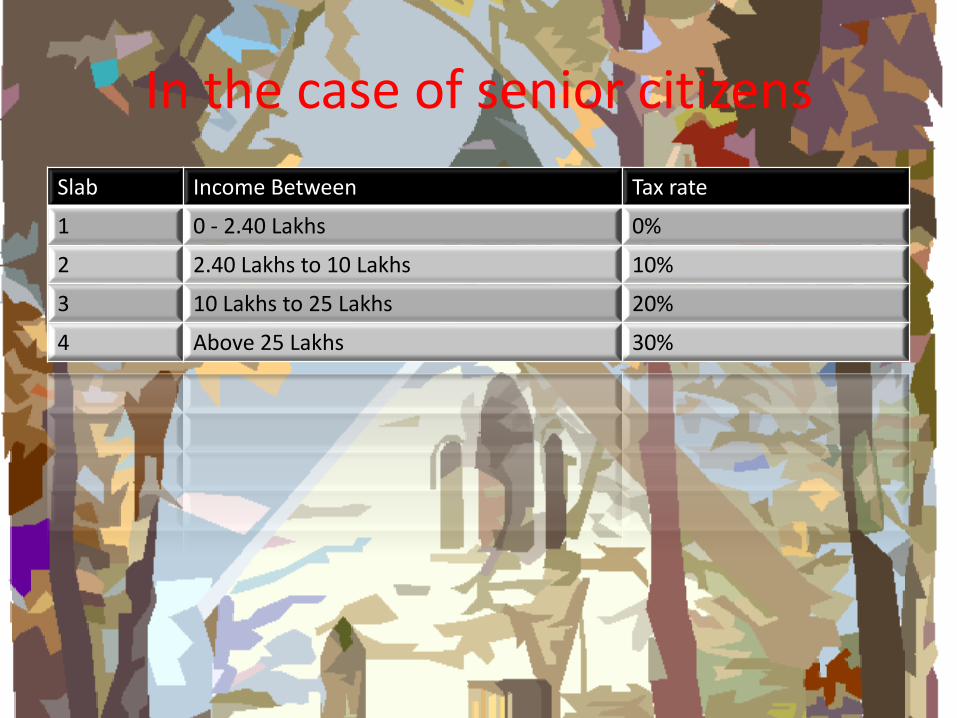

In the case of senior citizens

Slab Income Between Tax rate

1 0 - 2.40 Lakhs 0%

2 2.40 Lakhs to 10 Lakhs 10%

3 10 Lakhs to 25 Lakhs 20%

4 Above 25 Lakhs 30%

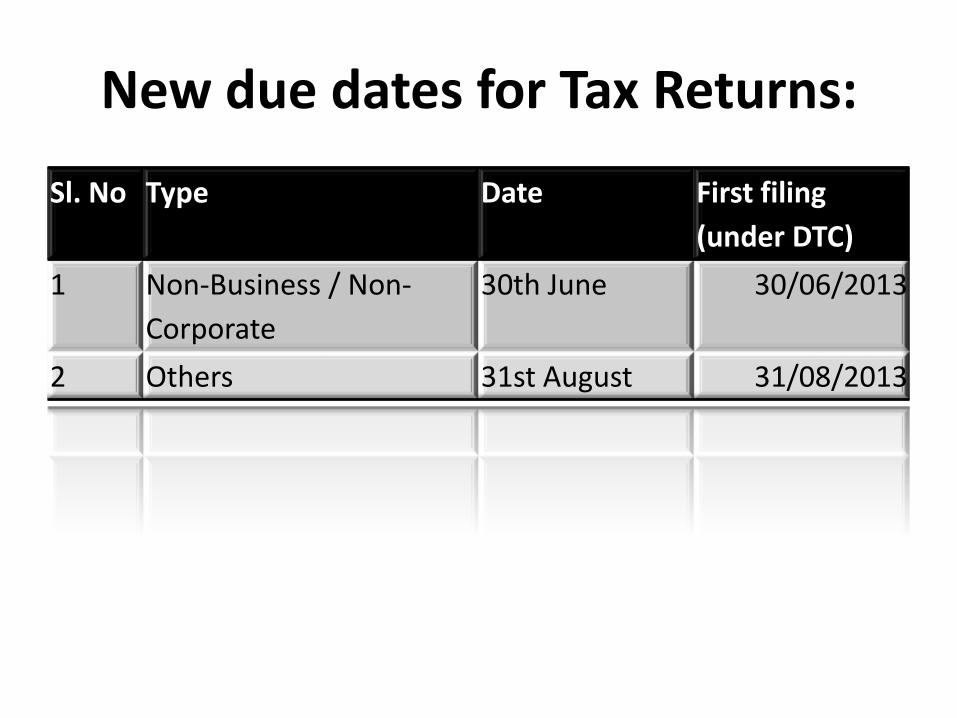

New due dates for Tax Returns:

Sl. No Type Date First filing

(under DTC)

1 Non-Business / Non-

Corporate

30th June 30/06/2013

2 Others 31st August 31/08/2013

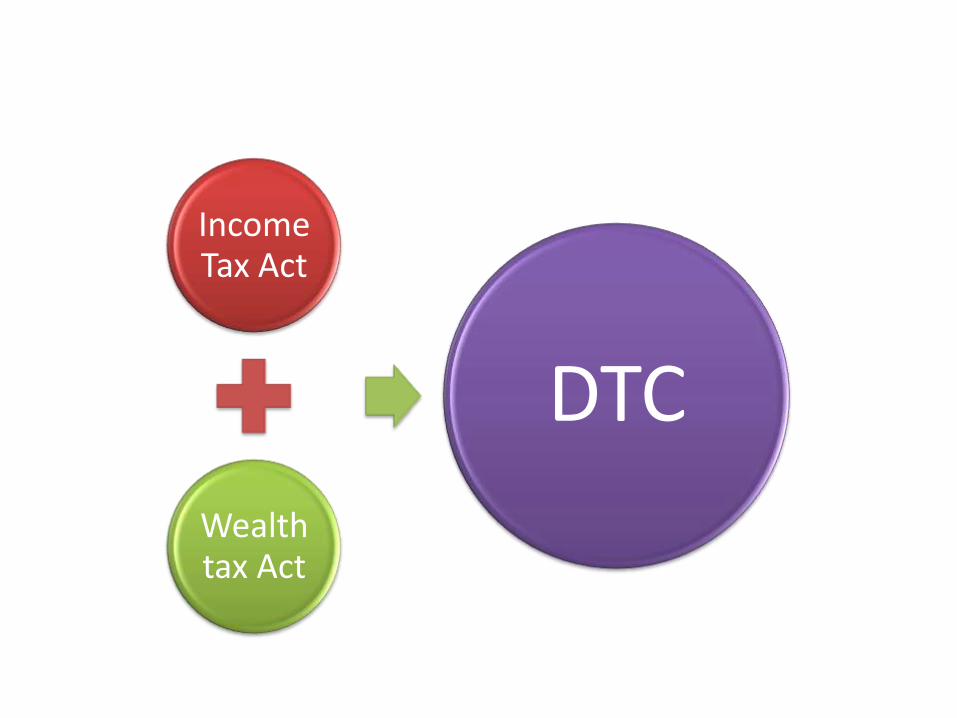

Income Tax Act

Wealth tax Act

DTC

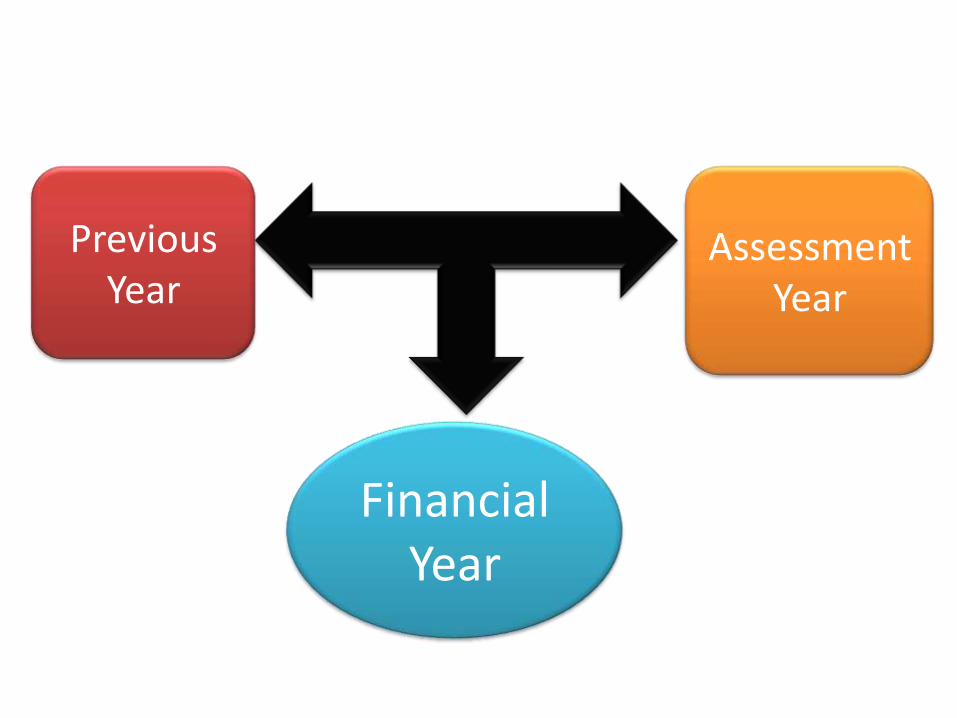

Previous Year

Assessment Year

Financial Year

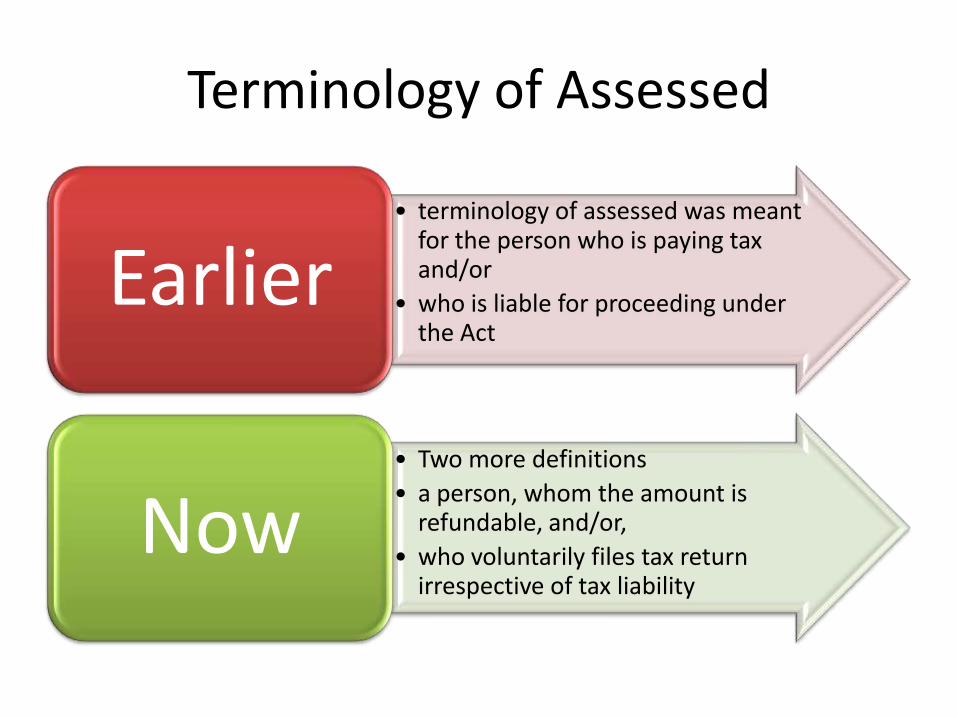

Terminology of Assessed

• terminology of assessed was meant for the person who is paying tax and/or

• who is liable for proceeding under the Act

Earlier

• Two more definitions

• a person, whom the amount is refundable, and/or,

• who voluntarily files tax return irrespective of tax liability

Now

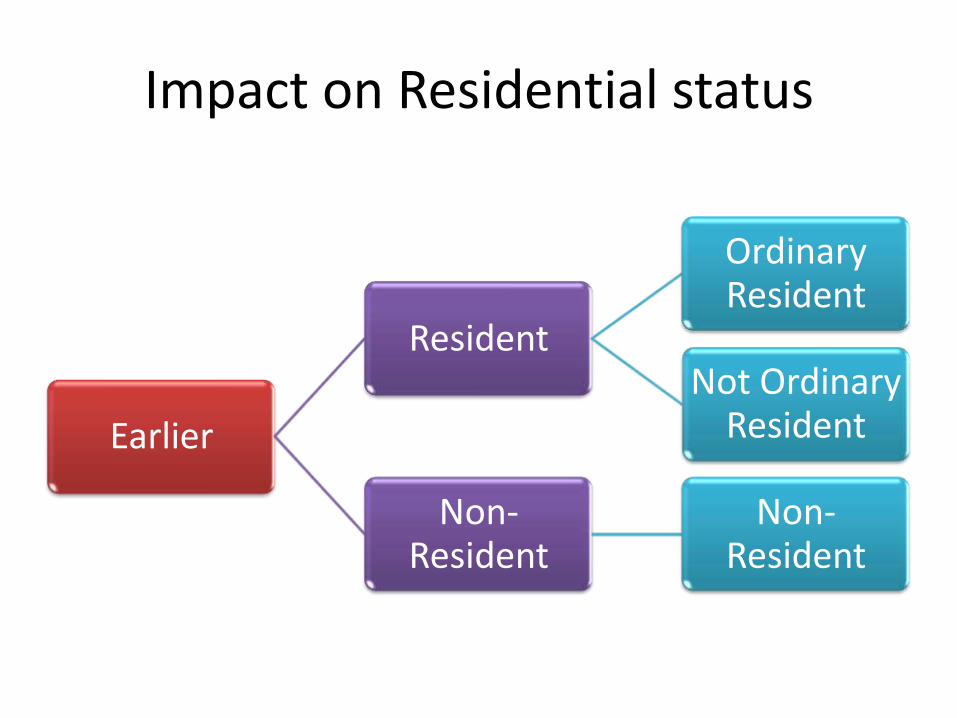

Impact on Residential status

Earlier

Resident

Ordinary Resident

Not Ordinary Resident

Non-Resident

Non-Resident

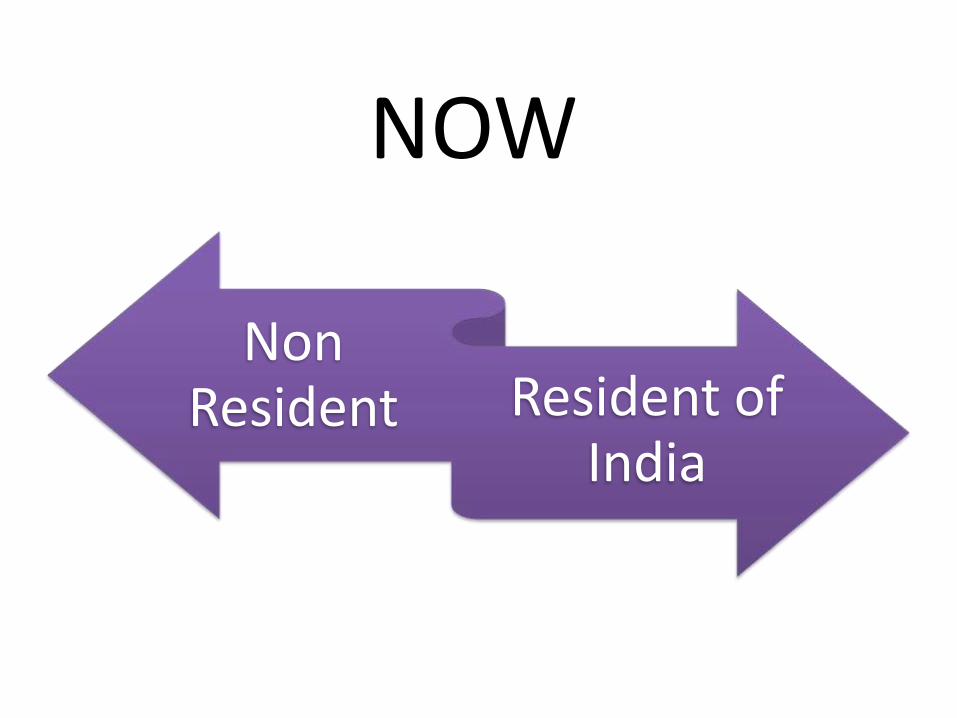

Non Resident Resident of

India

NOW

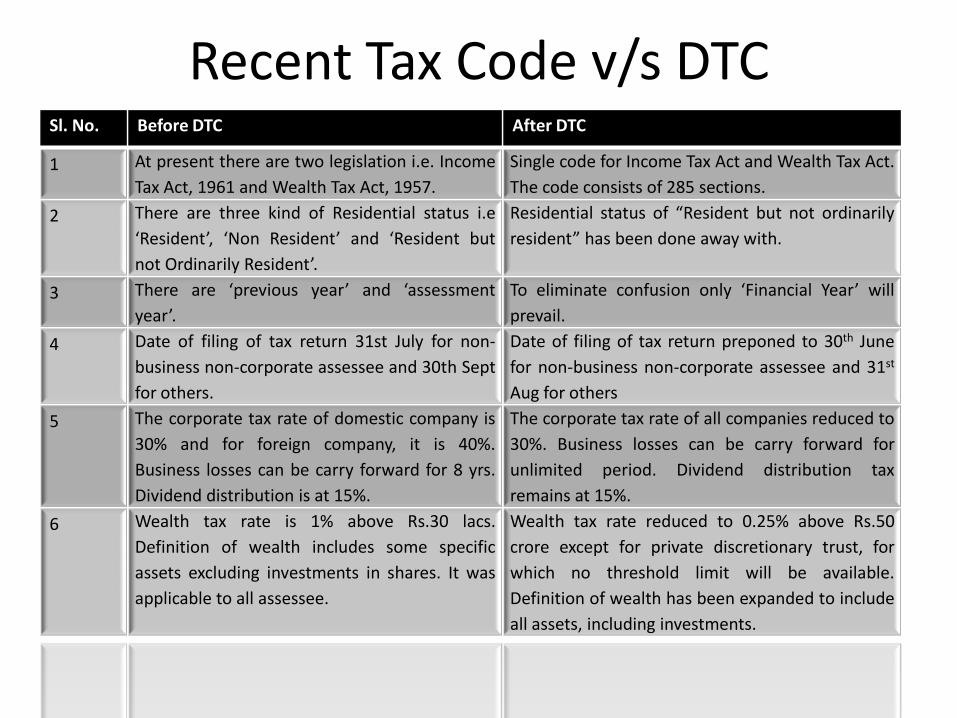

Recent Tax Code v/s DTCSl. No. Before DTC After DTC

1 At present there are two legislation i.e. Income

Tax Act, 1961 and Wealth Tax Act, 1957.

Single code for Income Tax Act and Wealth Tax Act.

The code consists of 285 sections.

2 There are three kind of Residential status i.e

‘Resident’, ‘Non Resident’ and ‘Resident but

not Ordinarily Resident’.

Residential status of “Resident but not ordinarily

resident” has been done away with.

3 There are ‘previous year’ and ‘assessment

year’.

To eliminate confusion only ‘Financial Year’ will

prevail.

4 Date of filing of tax return 31st July for non-

business non-corporate assessee and 30th Sept

for others.

Date of filing of tax return preponed to 30th June

for non-business non-corporate assessee and 31st

Aug for others

5 The corporate tax rate of domestic company is

30% and for foreign company, it is 40%.

Business losses can be carry forward for 8 yrs.

Dividend distribution is at 15%.

The corporate tax rate of all companies reduced to

30%. Business losses can be carry forward for

unlimited period. Dividend distribution tax

remains at 15%.

6 Wealth tax rate is 1% above Rs.30 lacs.

Definition of wealth includes some specific

assets excluding investments in shares. It was

applicable to all assessee.

Wealth tax rate reduced to 0.25% above Rs.50

crore except for private discretionary trust, for

which no threshold limit will be available.

Definition of wealth has been expanded to include

all assets, including investments.

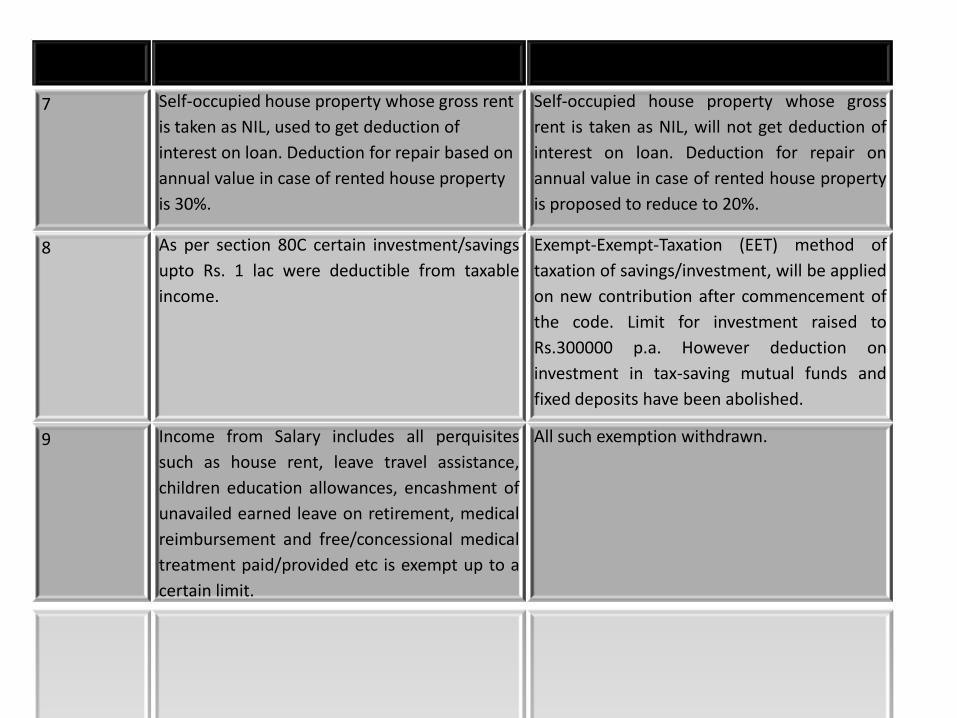

7 Self-occupied house property whose gross rent

is taken as NIL, used to get deduction of

interest on loan. Deduction for repair based on

annual value in case of rented house property

is 30%.

Self-occupied house property whose gross

rent is taken as NIL, will not get deduction of

interest on loan. Deduction for repair on

annual value in case of rented house property

is proposed to reduce to 20%.

8 As per section 80C certain investment/savings

upto Rs. 1 lac were deductible from taxable

income.

Exempt-Exempt-Taxation (EET) method of

taxation of savings/investment, will be applied

on new contribution after commencement of

the code. Limit for investment raised to

Rs.300000 p.a. However deduction on

investment in tax-saving mutual funds and

fixed deposits have been abolished.

9 Income from Salary includes all perquisites

such as house rent, leave travel assistance,

children education allowances, encashment of

unavailed earned leave on retirement, medical

reimbursement and free/concessional medical

treatment paid/provided etc is exempt up to a

certain limit.

All such exemption withdrawn.

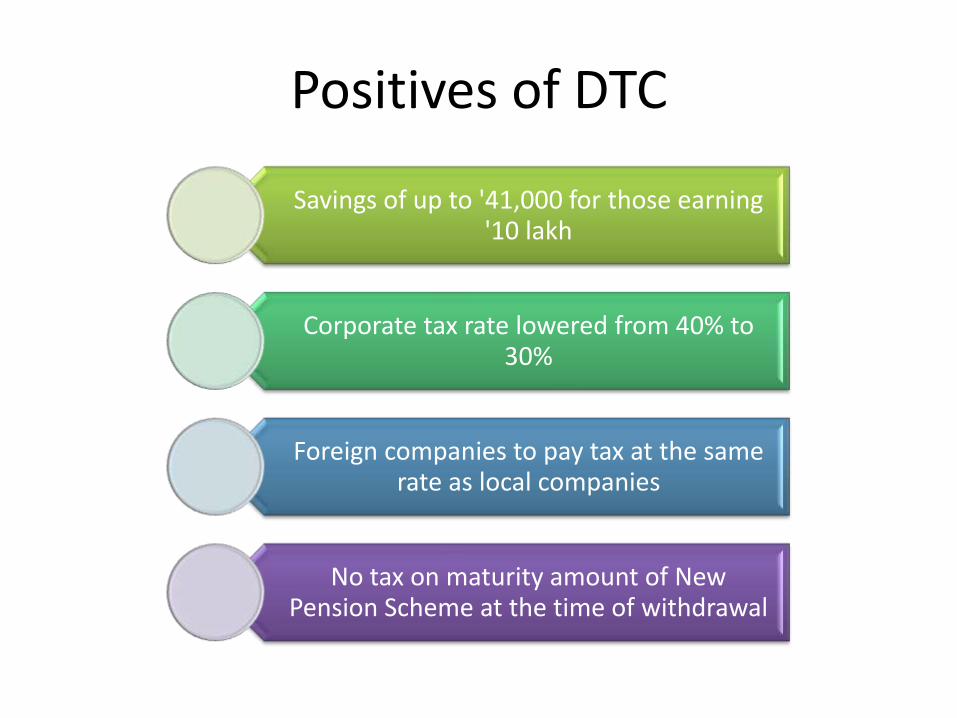

Positives of DTC

Savings of up to '41,000 for those earning '10 lakh

Corporate tax rate lowered from 40% to 30%

Foreign companies to pay tax at the same rate as local companies

No tax on maturity amount of New Pension Scheme at the time of withdrawal

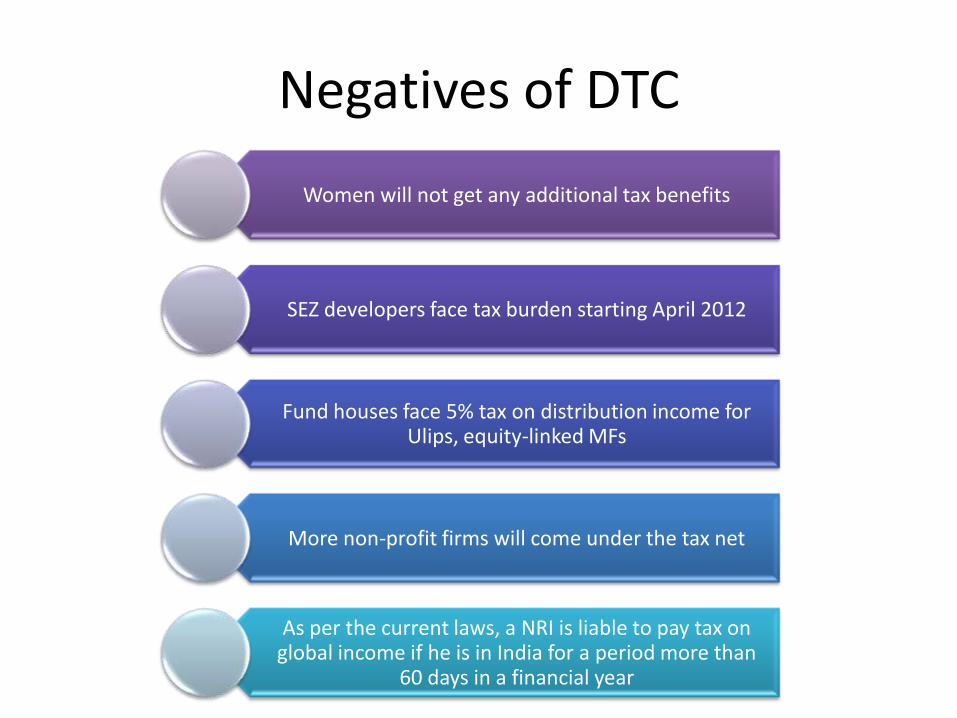

Negatives of DTC

Women will not get any additional tax benefits

SEZ developers face tax burden starting April 2012

Fund houses face 5% tax on distribution income for Ulips, equity-linked MFs

More non-profit firms will come under the tax net

As per the current laws, a NRI is liable to pay tax on global income if he is in India for a period more than

60 days in a financial year

How insurance gets impacted:

Under DTC, to be eligible for taxdeduction, a policy should give life coverof at least 20 times the annual premium

If this condition is not met, you will not getany tax deduction on the premium andeven the income from the policy will betaxable

Right now income received from insurancepolicies is free.

Impact on Pension Funds:

Under the DTC, most of current tax saving investment will not be eligible for deduction

An Annuity is an investment that gives out a regular income of the investor.

DTC has proposed to make annuity income exempt from taxation which makes them good tax saving instrument

The New Pension scheme is low cost pension fund which an investor can consider.

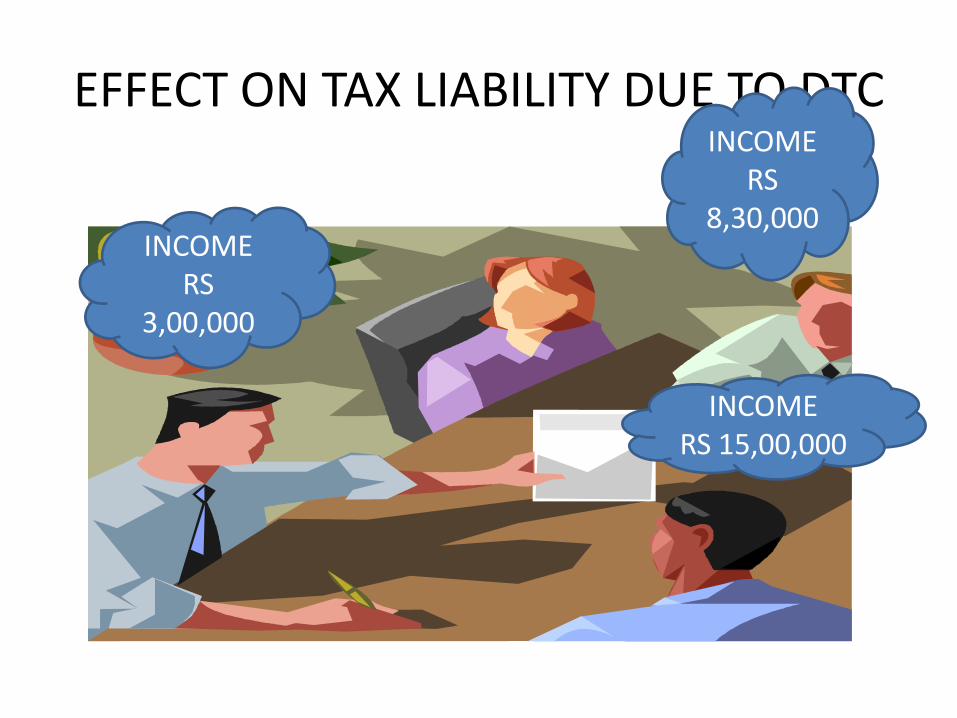

EFFECT ON TAX LIABILITY DUE TO DTC

INCOME RS

3,00,000

INCOME RS

8,30,000

INCOME RS 15,00,000

EFFECT ON TAX LIABILITY DUE TO DTC

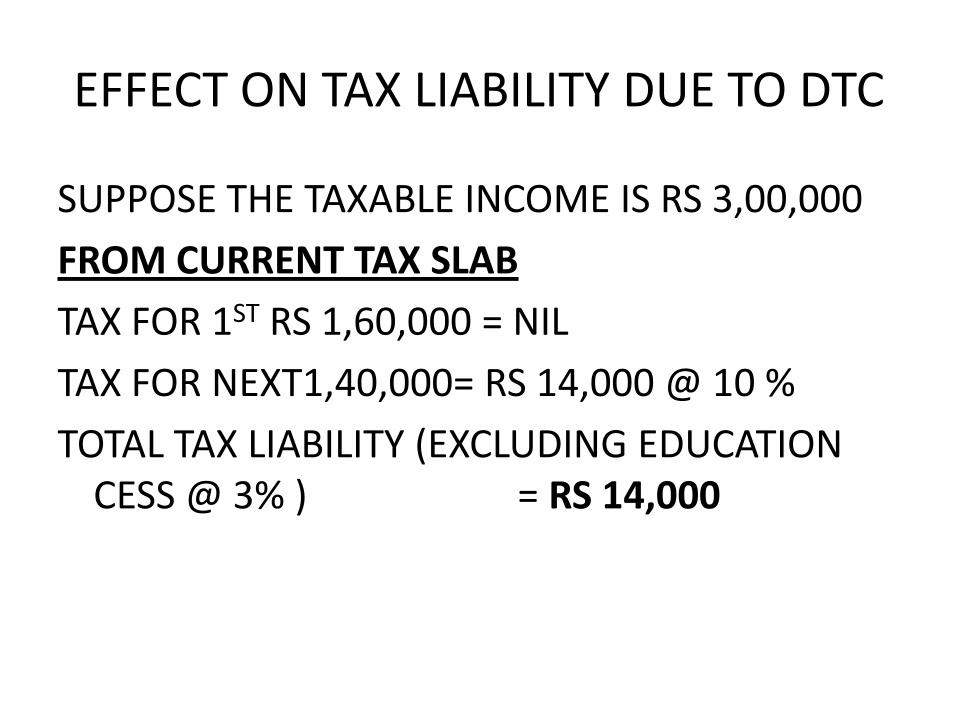

SUPPOSE THE TAXABLE INCOME IS RS 3,00,000

FROM CURRENT TAX SLAB

TAX FOR 1ST RS 1,60,000 = NIL

TAX FOR NEXT1,40,000= RS 14,000 @ 10 %

TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS @ 3% ) = RS 14,000

NOW, AFTER DTC

TAXABLE INCOME = RS 3,00,000

TAX FOR 1ST RS1,60,000 = NIL

TAX FOR NEXT RS 1,40,000 = RS 14,000@ 10%

TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS @ 3%) = RS 14,000

TOTAL SAVING = RS ( 14,000 – 14,000)

= RS 0

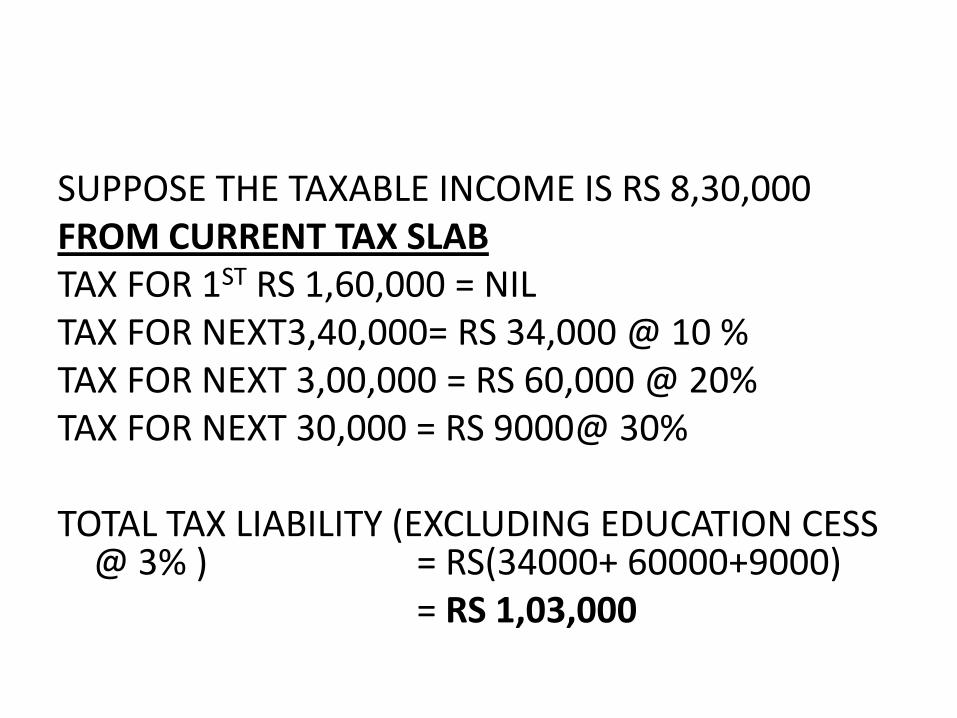

SUPPOSE THE TAXABLE INCOME IS RS 8,30,000FROM CURRENT TAX SLABTAX FOR 1ST RS 1,60,000 = NILTAX FOR NEXT3,40,000= RS 34,000 @ 10 %TAX FOR NEXT 3,00,000 = RS 60,000 @ 20%TAX FOR NEXT 30,000 = RS 9000@ 30%

TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS @ 3% ) = RS(34000+ 60000+9000)

= RS 1,03,000

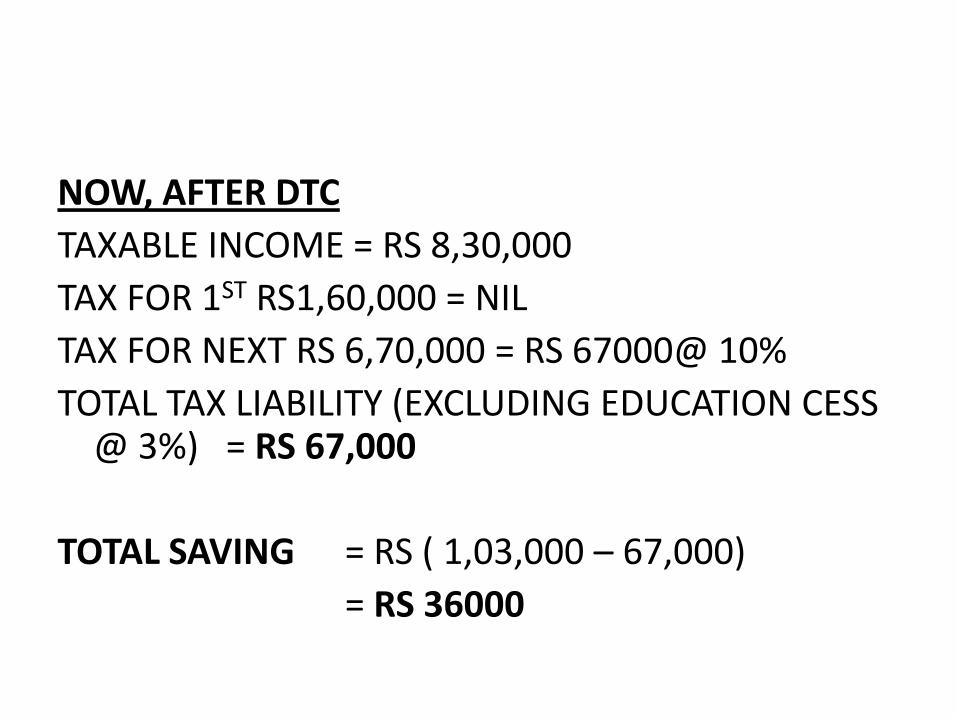

NOW, AFTER DTC

TAXABLE INCOME = RS 8,30,000

TAX FOR 1ST RS1,60,000 = NIL

TAX FOR NEXT RS 6,70,000 = RS 67000@ 10%

TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS @ 3%) = RS 67,000

TOTAL SAVING = RS ( 1,03,000 – 67,000)

= RS 36000

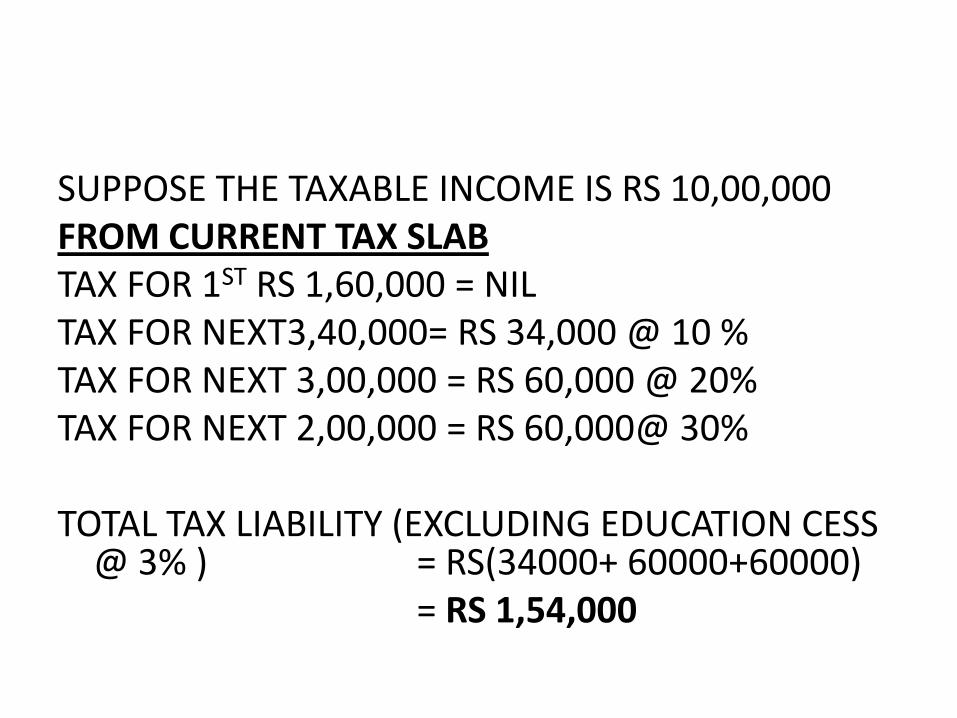

SUPPOSE THE TAXABLE INCOME IS RS 10,00,000FROM CURRENT TAX SLABTAX FOR 1ST RS 1,60,000 = NILTAX FOR NEXT3,40,000= RS 34,000 @ 10 %TAX FOR NEXT 3,00,000 = RS 60,000 @ 20%TAX FOR NEXT 2,00,000 = RS 60,000@ 30%

TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS @ 3% ) = RS(34000+ 60000+60000)

= RS 1,54,000

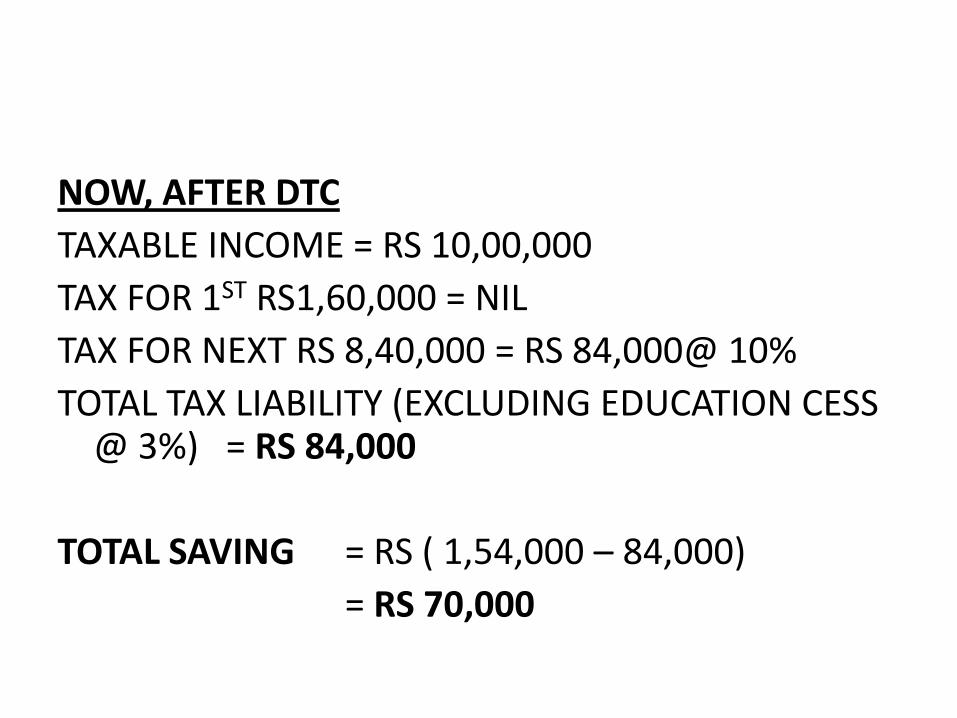

NOW, AFTER DTC

TAXABLE INCOME = RS 10,00,000

TAX FOR 1ST RS1,60,000 = NIL

TAX FOR NEXT RS 8,40,000 = RS 84,000@ 10%

TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS @ 3%) = RS 84,000

TOTAL SAVING = RS ( 1,54,000 – 84,000)

= RS 70,000

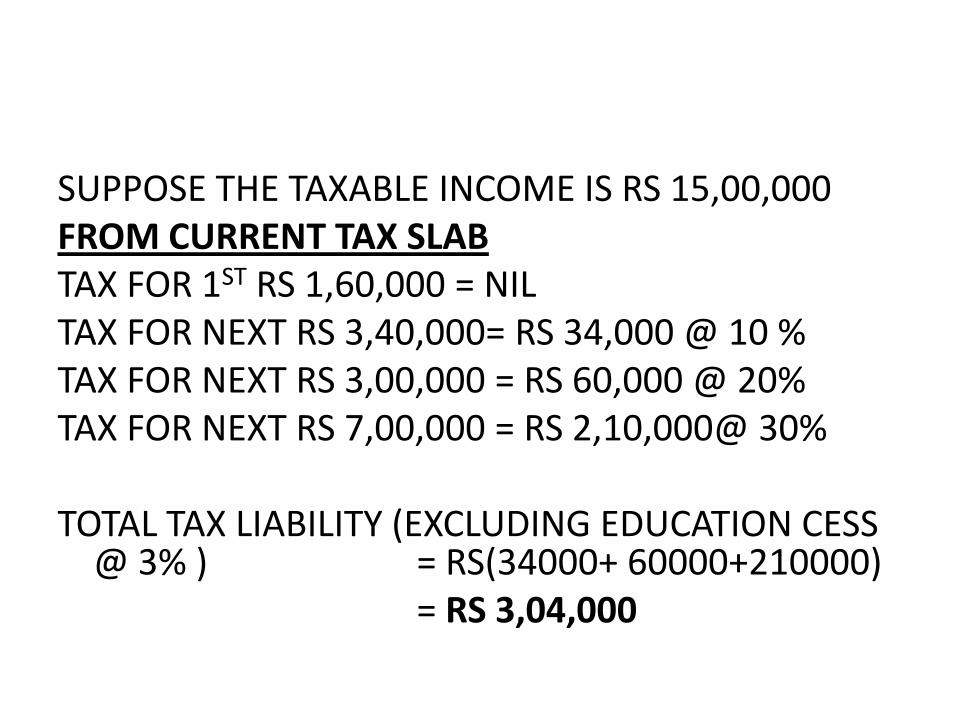

SUPPOSE THE TAXABLE INCOME IS RS 15,00,000FROM CURRENT TAX SLABTAX FOR 1ST RS 1,60,000 = NILTAX FOR NEXT RS 3,40,000= RS 34,000 @ 10 %TAX FOR NEXT RS 3,00,000 = RS 60,000 @ 20%TAX FOR NEXT RS 7,00,000 = RS 2,10,000@ 30%

TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS @ 3% ) = RS(34000+ 60000+210000)

= RS 3,04,000

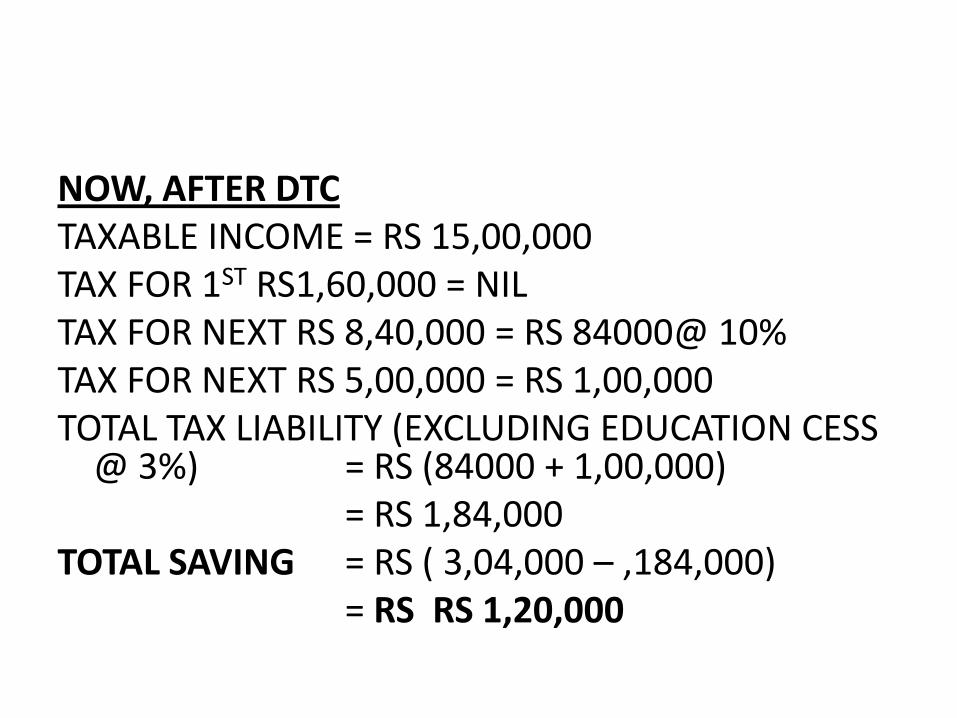

NOW, AFTER DTCTAXABLE INCOME = RS 15,00,000TAX FOR 1ST RS1,60,000 = NILTAX FOR NEXT RS 8,40,000 = RS 84000@ 10%TAX FOR NEXT RS 5,00,000 = RS 1,00,000TOTAL TAX LIABILITY (EXCLUDING EDUCATION CESS

@ 3%) = RS (84000 + 1,00,000)= RS 1,84,000

TOTAL SAVING = RS ( 3,04,000 – ,184,000)= RS RS 1,20,000

Related Documents