A THINK TANK for PRESTIGE BRANDS PHD Media PHARMA MAY 2010 Prepared By: Industry Partner: Ranking the digital competence of pharmaceutical brands © L2 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A THINK TANK for PRESTIGE BRANDS

PHD Media

PHARMAMAY 2010

Prepared By: Industry Partner:

Ranking the digital competence of pharmaceutical brands

© L2 2010

2© L2 2010

I. INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

II. METHODOLOGY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

III. RESULTS the rankings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

IV. DISCOVERIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

V. FINDINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

VI. OBSERVATIONS by disease state . . . . . . . . . . . . . . . . . . . . . . . . 25

ASTHMA & ALLERGY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

CARDIOLOGY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

GASTROINTESTINAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

NEUROLOGY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

PSYCHIATRY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

RHEUMATOLOGY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

UROLOGY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

WOMEN’S HEALTH . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

VII. TEAM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

© L2 2010

3

The Killer AppThe killer online app isn’t porn or social media, but med-ical advice. Arguably, no medium has so much influence over so much spending—one sixth of the nation’s GDP. In 2009, the number of Americans seeking pharmaceuti-cal information online reached 102 million1. Pharmaceu-tical companies continue to search for a voice that can rise above the digital cacophony. Although the emerg-ing direct-to-consumer relationship on the web allows for robust patient discovery and education, the online efforts have experienced fits and starts because the ambiguous regulatory environment leaves pharmaceuti-cal brands paralyzed.

The Innovator's DilemmaThe Food and Drug Administration’s Division of Drug Marketing, Advertising, and Communications (DDMAC) has expanded under the Obama Administration. As digital accelerates in new directions—mobile, geo-targeting, and healthcare information technology—the uncertainty surrounding regulation threatens to ham-string pharmaceutical companies and shift power to third-party portals and content sites. Brand managers are faced with a decision: take an aggressive approach and face possible regulatory wrath, or wait and lose ground to more innovative, risk-tolerant peers who are garnering skills, fans, and followers. When it comes to marketing and regulation, it may be heads the digital media win and tails digital wins again.

Despite the uncertain regulatory environment, some companies are innovating online and building a founda-tion for digital growth in anticipation of an unshackling. Robust branded sites, visibility in search, collabora-

1 Manhattan Research

tion with highly trafficked health portals, and forays onto Facebook and YouTube put brands like Gardasil and Viagra at the top of our ranking. However, the industry as a whole disappoints, as most brands offer obsolete technology, anemic site content, lack of search optimiza-tion, and scant social media programs. In sum, there are millions of unregulated conversations taking place online regarding prescription drugs, but the voice of the phar-maceutical companies is largely absent.

Our thesis is that digital aptitude will be a defining compe-tence that separates winners from losers in a medium too powerful to ignore. Key to managing and developing apti-tude is an actionable metric. This study quantifies the U.S. digital competence of 51 pharmaceutical brands across eight disease states and ranks them by their Digital IQ™. Our aim is to provide a robust tool to diagnose a brand's digital strengths and weaknesses relative to its peers to achieve greater return on incremental investment.

As in each L2 study, we brought in experts from aca-demia and industry to provide color and commentary on our findings. We were fortunate in this study to have insight from Peter Golder, professor of marketing at Dart-mouth's Tuck School of Business on innovation, Scott Hagedorn, U.S. CEO of PHD Media, on media trends in the industry, and Kristen Goelz of Flashlight interactive on web site messaging.

Scott Galloway

Clinical Associate Professor, NYU SternFounder, L2 (LuxuryLab)

INTRODUCTION

INTRODUCTION© L2 2010

4© L2 2010

METHODOLOGY

METHODOLOGY

Site Effectiveness: Reinforcement of core brand associations and values through aesthetics and interactivity. Also includes technology incorporation, navigation, consumer funnels, relevant content, and customer service.

PLATFORM - 40% • BRAND TRANSLATION • Aesthetics and Messaging • Interactivity

• SITE ELEMENTS• Technology Integration • User Interface • Customer Service • Content: Disease Education, Conversion, Community Content

Digital Marketing Efforts: Online advertising on and off consumer healthcare portals, mobile compatibility, email marketing, and other messaging.

OFF-PLATFORM MESSAGING - 25% • PORTAL AND OTHER ONLINE ADVERTISING • MOBILE• EMAIL MARKETING

Visibility: Organic and paid search visibility on popular search engines.

SEARCH ENGINE OPTIMIZATION (SEO) - 20% • TRAFFIC• KEYWORDS• WEB AUTHORITY• SEARCH ARCHITECTURE

Social Media Presence: Following, content, and influ-ence on major social media platforms, and buzz on blogs and other web 2.0 forums.

SOCIAL MEDIA - 15% • FACEBOOK• TWITTER• YOUTUBE• USER-GENERATED CONTENT

55

RESULTS

© L2 2010

The Digital IQ Index ranks brands according to their digital competence, with each falling into one of five categories:

GENIUSDigital competence is a point of competitive differentiation for these brands. Their sites are search optimized, aesthetically engaging, functional, interactive, and offer clear calls to action. These brands are highly visible advertisers on consumer health portals and elsewhere online and experiment on the edge of the network with social media content.

GIFTEDSites are crawlable, brand enhancing, and include calls to action. Brands typically advertise on health portals, are highly visible on top search engines, and offer email marketing.

AVERAGE Brand sites are functional yet predictable. Innovation efforts are uninspired and lack ambition. Boilerplate marketing online and in email.

CHALLENGEDThese brands offer little content online. Bare-bones sites provide only basic drug information. Engagement is limited to web property, and digital campaigns are an afterthought.

FEEBLE Brands have largely ignored the digital phenomenon. Sites lack basic functionality and navigability, and brands disregard digital marketing initiatives.

140+

110-139

90-109

70-89

<70

RESULTS: the rankings

6© L2 2010 RESULTS: the rankings

Rank Brand Parent Disease State IQ Label Comments

1 VIAGRA Pfizer Urology 149 Genius Site tech and interactivity are industry standouts; brand leverages iconic name in search and online buzz

2 NEXIUM AstraZeneca Gastrointestinal 143 Genius This social media maven offers best-in-class lifestyle support tools, including online access to dieticians

3 CHANTIX Pfizer Neurology (Smoking Cessation)

140 Genius Connects digitally with consumers both on and off site with email, short messaging service, and a dominant presence on health portals

4 ORTHO TRI-CYCLEN LO

Ortho-McNeil Janssen

Women’s Health (Birth Control)

137 Gifted Top in the competitive Women’s Health category; brand boasts interactive tools and desktop reminders

5 CRESTOR AstraZeneca Cardiology 135 Gifted Strong onsite tech integration and activity on portals and blogs elevates top brand in disappointing cardio category

6 GARDASIL Merck Women’s Health (Infectious Disease)

131 Gifted Rallies community online with pioneering Facebook page and strength in search

6 YAZ Bayer Women’s Health (Birth Control)

131 Gifted YAZXpress site offers interactive community content; brand also connects with users in mobile and email

8 SYMBICORT AstraZeneca Asthma & Allergy 130 Gifted Interactive video journey customizes site for best-in-category user experience

8 NUVARING Merck Women’s Health (Birth Control)

130 Gifted Brand boasts innovative web advertising and strength in search

10 LUNESTA Sepracor Neurology (Insomnia)

126 Gifted A YouTube channel coupled with strong off-platform efforts keeps brand awake online.

11 SEROQUEL AstraZeneca Psychiatry 124 Gifted Site provides strong educational content and community information

12 LIPITOR Pfizer Cardiology 121 Gifted Site branding and online advertising form the pulse of this brand’s digital efforts

12 LEVITRA Novartis Urology 121 Gifted Humorous multichannel In Bed video campaign generates online buzz

14 SEASONIQUE Teva (through Duramed)

Women’s Health (Birth Control)

120 Gifted Brand understands how to integrate digital content and user behavior

15 AMBIEN CR Sanofi-Aventis Neurology (Insomnia)

118 Gifted Site highlight is a downloadable tool that tracks and analyzes sleep patterns

16 CYMBALTA Eli Lilly Psychiatry 113 Gifted Strong visibility on WebMD portal

17 ORENCIA Bristol-Myers Squibb Rheumatology 111 Gifted Strong presence on health portals

17 ABILIFY Bristol-Myers Squibb Psychiatry 111 Gifted Impressive site funneling and substantial traffic raise brand’s profile

19 KAPIDEX Takeda Gastrointestinal 110 Gifted Strong branding and video content differentiate site

20 SYNVISC Genzyme Rheumatology 107 Average Search architecture and informative videos are brand strengths

PHARMACEUTICAL BRANDS RANKED BY DIGITAL IQ SCORE

7© L2 2010 RESULTS: the rankings

Rank Brand Parent Disease State IQ Label Comments

21 ADVAIR GlaxoSmithKline Asthma & Allergy 106 Average Asthma.com unbranded site incorporates education and technology

22 SINGULAIR Merck Asthma & Allergy 105 Average Site aesthetics, disease education and flash features are strengths; some presence on health portals

23 ZETIA Merck Cardiology 104 Average Presence on health portals and brand translation on site give IQ a boost

24 PLAN B Teva (through Duramed)

Women’s Health (Birth Control)

102 Average Site offers eligibility calculator and find-a-pharmacist feature

24 SPIRIVA Pfizer and Boehringer Ingelheim

Asthma & Allergy 102 Average Multichannel disease awareness campaign tests the waters on Twitter

26 VYTORIN Merck Cardiology 101 Average Strong site disease education and presence on top portals, but crippled by poor visibility

27 CIALIS Eli Lilly Urology 100 Average Although SEO is strong, customer relationship management program that directs users to PO Box shows digital failings

27 CELEBREX Pfizer Rheumatology 100 Average Status quo online advertising keeps this brand average

29 ACIPHEX Elsai and Ortho-McNeil Janssen

Gastrointestinal 98 Average Playful animation on site and strong keyword visibility

30 RITUXAN Biogen and Genentech

Rheumatology 94 Average Site incorporates elegant flash features, but efforts in search and online advertising get lost in the crowd

31 HUMIRA Abbott Rheumatology 93 Average MyHumira site for current brand users offers support for patients

32 ANDROGEL Solvay Urology 92 Average The Low Testosterone Lowdown sponsored content on WebMD has minimal visibility

32 ENBREL Amgen and Wyeth Rheumatology 92 Average Customer service standout offers find-a-doctor feature and toll-free phone access to nurses

32 MIRENA Bayer Women’s Health (Birth Control)

92 Average Trails strong Birth Control peers; interactive site elements are absent

32 PLAVIX Bristol-Myers Squibb and Sanofi-Aventis

Cardiology 92 Average Portal ads keep this brand in the middle of the pack

36 LOVAZA GlaxoSmithKline Cardiology 87 Challenged A strong site is brand’s only notable effort

37 AVODART GlaxoSmithKline Urology 86 Challenged Leverages GSK customer service features

37 NASONEX Schering-Plough Asthma & Allergy 86 Challenged Although “Don’t Blow It” game on Facebook disappoints, it scores points for social media effort

39 VERAMYST GlaxoSmithKline Asthma & Allergy 85 Challenged Allergyrewards email marketing program offers savings and tips

40 LYRICA Pfizer Rheumatology 84 Challenged Strong presence on WebMD, but site is poorly organized to reach users interested in newly approved Rheumatology indication

8© L2 2010 RESULTS: the rankings

Rank Brand Parent Disease State IQ Label Description

41 OMNARIS Sepracor Asthma & Allergy 82 Challenged Robust SEO

42 FLOMAX Astellas Pharma and Boehringer Ingelheim

Urology 71 Challenged Bare bones, text-heavy site with dated technology and no call-to-action

42 PRISTIQ Pfizer Psychiatry 71 Challenged A New Day patient support program has email marketing component; site is repurposed TV branding

44 LESCOL XL Novartis Cardiology 65 Feeble Obsolete site features newspaper-style cartoons

45 TRILIPIX Abbott Cardiology 63 Feeble Anemic site content, but ad presence includes spots on Hulu

46 CADUET Pfizer Cardiology 62 Feeble PDF downloads abound on this brand’s dated site

47 NIASPAN Abbott Cardiology 61 Feeble Brand fails to be brought to life on site and limited web advertising

48 PATANASE Alcon Asthma & Allergy 60 Feeble Worst in search; find-a-doctor feature is strongest element of site

49 TOPROL-XL AstraZeneca Cardiology 59 Feeble Mention on AstraZeneca’a YouTube channel is this brand’s lone social media effort

50 PULMICORT AstraZeneca Asthma & Allergy 52 Feeble Brand does little digitally beyond light display advertising

51 ASTEPRO Meda Asthma & Allergy 42 Feeble Miserable web site and absence from other digital media

9© L2 2010 DISCOVERIES

DISCOVERIES“Companies must

move beyond a DTC mentality and

adopt a DFC mentality (i.e., direct

from company). Instead of companies

pushing information to customers,

customers will pull information from

the company. An even better approach

is DFC + P2P, direct from company

plus peer-to-peer redistribution.”

“We often get

asked if social activation should play

a role in brand efforts. Our advice

is that it isn’t a matter of ‘if ’, it’s a

matter of ‘when’. It comes down to

mapping the brand introduction time-

line and knowing when to use social

and when not to in order to increase

impact while also mitigating risk.”

PETER GOLDERTuck School of Business at Dartmouth

SCOTT HAGEDORNPHD Media

The Tipping PointConsumer appetite for digital health content is voracious and grow-ing: the number of Americans accessing health information online is up 159% from 20041. Health portals including WebMD, Everyday Health, and About.com Health attract millions of unique visitors. In addition, traffic to branded pharmaceutical sites increased 82% last year, suggesting brands have a legitimate role in the online conversation. Disparity in the quality of the digital content produced by pharmaceutical brands leads discriminating con-sumers to vote with their browsers. While brands categorized as Genius or Gifted experienced average traffic growth of 175% from March 2009 to March 2010, 40% of the brands in the study realized negative traffic growth.

Anti-Social PharmaDespite hearings in November 2009, the FDA has remained silent about social media marketing regulation, restraining movement to platforms such as YouTube, Facebook, and Twitter. Although 80% of parent companies are starting to dip their toes into social media, only 19% of pharmaceutical brands maintain a presence on at least one site. Parent com-pany efforts lack sophistication, offering little more than glorified PR content and one-sided conversations. As a result, they have attracted few followers. Bright spots include Johnson & Johnson’s YouTube channel, viewed more than 1.6 million times, and Merck’s Gardasil human papillomavirus (HPV) awareness Facebook page, with more than 100,000 fans. Patient demand for online networking opportunities has been validated by the emergence and growth of condition-specific patient networking sites such as PatientsLikeMe, which doubled subscribers from December 2008 to December 2009, Juvena-tion, and Bayer’s MS-Gateway.

1 Manhattan Research

10

Mon

thly

Uni

que

Visi

tors

(tho

usan

ds)

Mar

ch 2

010

© L2 2010

Learn by DoingBrands with a higher Digital IQ demonstrate more risk tolerance when approaching digital marketing. Based on an assessment of regulatory compliance on branded sites, brands ranked Average and below err on the side of caution regarding FDA Web guidelines while brands ranked Genius and Gifted employ broader interpretations. Genius and Gifted brands have greater social media penetration: 37% are present on at least one platform, compared with 9% for Average and below brands. High IQ brands also returned to search marketing faster than their laggard peers: 89% of Gifted and above brands participate in paid search versus 59% of Average and below brands.

DISCOVERIES

20,000

18,000

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

WEBMD

EVERYDAY HEALTH

YAHOO! HEALTH

HEALTHGRADES

QUALITYHEALTH

REALAGE

HEALTHLINE

LIVESTRONG

HEALTHCENTRALNEXIUM

ORENCIALEVITRA

ABILIFYVIAGRA

Deserted Islands (Visibility)After the FDA submitted warning letters regarding paid search to more than 40 pharmaceutical brands in April 2009, most suspended search engine mar-keting. Although paid search has rebounded, and 70% of brands currently purchase search terms, many brand-ed sites are not optimized for organic search. As a result, site visibility on major search engines for upper-funnel disease-relevant terms lags that of such popular health portals as WebMD, Yahoo! Health, and HealthCentral.

HEALTH PORTAL AND BRANDED-SITE TRAFFIC

Monthly Unique Visitors to Health Portals and Branded Sites

Health Portals

Branded Sites

0% 10% 20% 30% 40% 50% 60% 70%

YouTube

SOCIAL MEDIA PENETRATION

Brands vs. Parent Companies

Brands

Parent Companies

11© L2 2010 DISCOVERIES

Innovation SilosThe average dispersion in brand-level Digital IQ among pharma-ceutical companies with more than one product in the study is 40 points. This large spread high-lights a silo mentality—digital com-petence within large companies sits isolated, with minimal shared learn-ing among brands. Although some companies leverage small econo-mies of scale (e.g., AstraZeneca sites are sometimes templated, and GlaxoSmithKline sites offer universal customer service tools), digital efforts appear largely uncoordinated. The lone exception is in social media, which is primarily deployed at the parent company level with little brand-level integration.

PETER GOLDERTuck School of Business at Dartmouth

“The results of

the Digital IQ studies present

companies with the triple threat of

innovation. First, with incremental

innovation, companies can upgrade

each of their own web sites to match

internal best practices. Second,

through radical innovation, com-

panies can adopt and improve upon

industrywide best practices. Third,

for truly breakthrough innovations,

companies can look to unrelated in-

dustries for inspiration in developing

completely new approaches to digital

communication.”

SCOTT HAGEDORNPHD Media

“Pharma is one

of the few remaining categories with

this level of disparity around ide-

ation. It is hard for vertical teams

structured around specific brands to

share best practices with other brand

teams. It is up to the agencies that

touch multiple brands to step up and

help replicate innovative best practices

across the client brand verticals.”

140

Viagra

Chantix

Lipitor

Celebrex

Lyrica

Pristiq

Caduet

Vytorin

NuvaRing

Gardasil

Zetia

Singulair Advair

LovazaAvodar t

Veramyst

Humira

Cymbalta

Ambien CR

Yaz

MirenaPlavix *

* in par tnership with Bristol-Myers Squibb

Cialis

Omnaris

Lunesta

Niaspan

Trilipix

Seroquel

Symbicor t

Crestor

Nexium

Toprol-XL

Pulmicor t

GENIUS

GIFTED

AVERAGE

CHALLENGED

FEEBLE

BAYER

SANOFI-AVENTIS

ELI LILLY

SEPRACORABBOTT

GLAXOSMITHKLINEMERCK

ASTRAZENECAPFIZER

104107

114

72

91

104 106 105

112110

90

70

DIGITAL IQ DISPERSION

Range of Brand Digital IQ Scores and Average Digital Score by Parent Company

12© L2 2010 DISCOVERIES

Younger “Age of Onset” Brands LeadAs one would expect, brands that market to younger consumers have higher Digital IQs. In an attempt to reach a generation raised on Google and Facebook, brand marketers in categories such as Birth Control, HPV and Psychiatry have worked to understand how to design informative and interac-tive web sites, incorporate community content and technology, attract users to branded sites, and test social media. Yet, this is a case of not seeing the forest from the trees as the vast majority of prescription drugs are consumed by older adults who are increasingly online— in the five-year period from 2004 to 2009 Internet usage increased by 55% to 17.5 million users2 for seniors. Furthermore, the fastest growing cohort on Facebook is boomer-age women.

2 Nielsen

SCOTT HAGEDORNPHD Media

“We’ve seen the

internet emerge as the medium all

segments of the population say they

could not live without. There is clear-

ly an opportunity for pharma brands

marketing to a senior population to

increase their web presence.”

PsychiatryPSY

RheumatologyRHM

CardiovascularCDV

Asthma & AllergyASM

UrologyURL

GastrointestinalGST

Birth ControlBCL

Human PapillomavirusHPV

140

110

90

70

GENIUS

GIFTED

AVERAGE

CHALLENGED

FEEBLE

CDV

HPV

BCL

PSY

ASM

RHM

URL

GST

AGE 80AGE 60

AGE 40AGE 20

DIGITAL IQ AND AGE OF ONSET

Average Digital IQ Score and Age of Disease Onset by Disease State Category

13© L2 2010 DISCOVERIES

Patent Cycle’s ImpactBrands categorized as Genius and Gifted have an average of 1.7 more years before patent expiry than brands categorized Average and below, suggesting digital marketing is correlated with the patent cycle.

Pharma brands typically invest heavily in online disease education and awareness efforts before FDA approval. Drugs also invest early in the patent cycle, one year after FDA approval, as they are building awareness for the brand. Brands new to the market have higher Digi-tal IQs, suggesting a greater digital investment and focus.

12

10

8

6

4

2

0

Genius Gifted

DIGITAL IQ

Average Challenged Feeble

YEAR

S

AVERAGE TIME TO PATENT EXPIRY

14© L2 2010 FINDINGS

Platform

QUICK STATS

Branded Sites:

• 85% offer a Doctor Discussion guide

• 62% offer little or no community content

• 57% offer savings for first-time prescriptions

• 47% have an unbranded site, typically devoted to disease education

• 45% offer a compliance tool, such as email, text reminders, or a downloadable PDF calendar

• 42% offer savings for current users

• 26% have no access to customer service

FINDINGS

Call to Action Message

“Quantitative

measures are most useful for bench-

marking and upgrading sites on

established performance criteria.

Qualitative insights are most use-

ful for generating and introducing

entirely new performance criteria.”

PETER GOLDERTuck School of Business at Dartmouth

Branded sites inform consumers and encourage patient compliance at different stages of the disease cycle. Sites for drugs with multiple indications face the ad-ditional challenge of tailoring content to different conditions. Because of the variety of patient audiences, clearly directing users and prospects to appropriate informa-tion is the hallmark of a strong site. Among branded sites, Symbicort and Abilify's are among the best at funneling visitors by condition and stage of diagnosis.

Although all sites offer basic drug information, the best include disease educa-tion, like Crestor’s scientific videos, and community content, like Nexium’s site with patient success-story videos and lifestyle tools. The biggest divergence among pharmaceutical sites is in the use of technology to amplify content. Although strong sites offer videos and interactive features with anatomic im-ages, doctor interviews, and patient testimonials, 55% fail to incorporate flash elements, popular for adding animation and interactivity to web content and a barometer of web sophistication, beyond the home page.

Every site aims to influence visitors to act through one or a combination of symptom assessment surveys, doctor discussion guides, coupons for a new or continuing prescription, and tools to encourage compliance with a prescription. Many of these tools are PDF documents, which in many cases is not the best way to leverage the speed and convenience of the digital medium. Exceptions include Spiriva and Synvisc, which offer to send assessment results via email.

60%

50%

40%

30%

20%

10%

0%

Visit Doctor New Rx Rx Savings Compliance

Freq

uen

cy

CALLS TO ACTION ON BRANDED SITES

1515© L2 2010

www.viagra.com

www.symbicort.com

FINDINGS

Forty-five percent of sites offer savings to current users, effectively diminishing the profitability of those sales, although there may be gains in market share when the drug is in a head-to-head battle with a major competitor.

The creation of unbranded education-oriented sites is a popular technique to market drugs before approval by the FDA. Once a drug is FDA-approved, the use of unbranded sites declines. Still, 47% of brands in the study maintain a microsite to comple-ment their branded site’s disease education content.

Comparatively, the unbranded site typically generates significantly fewer unique visitors than a branded site, even when offering better disease education information and technology integration. For example, Advair.com has more than 16 times as many visitors as its arguably superior un-branded counterpart, Asthma.com. Low traffic combined with the danger of competitive brands benefiting from other’s unbranded efforts, calls into question their longer-term value.

www.abilify.com

www.viagra.com

16

100%

80%

60%

40%

20%

0%

GASTROIN

TESTIN

AL

NEUROLO

GY

CARDIOLO

GY

PSYCHIATRY

RHEUMAT

OLOGY

UROLOGY

WOMEN’S H

EALT

H

ASTHMA &

ALLER

GY

Mar

ch 2

010

Mar

ch 2

010

BRANDS BY DISEASE STATE ON PAID SEARCH

© L2 2010

Search Engine OptimizationSearch engines are the primary tool consumers use to seek health infor-mation online, and search remains a digital priority for most pharmaceuti-cal brands1. Brands strive for search engine visibility, not only for consum-ers seeking specific drug information, but also for those learning about a condition. Generating awareness among upper-funnel consumers helps brands acquire diagnosed but untreated patients. Research has found that consumers who visit a brand’s site are three times more likely to request a drug by name2, and 44% of physicians prescribe a requested drug3. Weak search engine optimization by pharmaceuti-cal brands allows health portals to dominate in organic search visibility for every disease state.

In 2008, more than 30% of pharma-ceutical search engine traffic was directed from paid ads4. Because of space limitations and FDA regulation,

1 iCrossing2 Manhattan Research3 Kaiser4 Hitwise

pharmaceutical paid search advertising is primarily limited to two types of ads: brand-reminder and help-seeking. Brand-reminder ads incorporate a brand’s name and are restricted from explaining drug treatment uses and benefits; help-seeking ads tout the uses and benefits of a drug, but do not mention its name. Brands in the study strongly favor brand-reminder ads, particularly for patients further along the disease cycle using more specific, lower-funnel terms, and also because consumers may perceive help-seeking ads as con-fusing and potentially misleading. In November 2009, Google proposed two new types of ads: product-claim ads, which would link to a product site and explain drug benefits, and black-box ads, both of which link to full text black-box warnings. Yaz is the lone brand in the study to use black-box ads.

QUICK STATS

SEO:

• 70% of brands engage in paid search on Google or Bing

• 62% of brands engage in branded paid search on Google or Bing

• Google Page Rank average for branded pharmaceutical sites is 4.75

• Pharmaceutical sites have an average of 91 inbound links

Brand-Reminder Ad

Help-Seeking Ad

Black-Box Ad

{{

{

NEXIU

M

ORENCIA

LEVITR

A

ABILIFY

VIAGRA

PLAVIX

LIPITO

R

CYMBALTA

VYTORIN

NASONEX

NUVARING

ADVAIR

ENBREL

CHANTIX

RELATIVE TRAFFIC OF TOP BRANDED SITES

FINDINGS

17© L2 2010

SCOTT HAGEDORNPHD Media

“In addition to

shifting ad dollars, marketers are

re-examining their overall market-

ing investments. We see a shifting of

dollars to platforms that offer deeper

engagement with consumers. We be-

lieve this is driven in part by the richer

experiences that digital media offers.”

In 2009 pharmaceutical industry online advertising spend was up 31% year-on-year, to $117 million, while consumer ad spending overall remained virtually flat5. Digital spending represents about 4% of total DTC budgets. As online advertising becomes a larger part of pharmaceutical marketing bud-gets, brands are looking for innovative ways to reach consumers, however, most efforts remain focused on boilerplate ad offerings on highly trafficked consumer health portals, like WebMD or Quality Health.

Fifty-eight percent of brands in the study advertise on WebMD, Everyday Health, or About.com Health and 60% of these brands advertise on more than one of the portals. Branded presence on portal sites ranges from traditional display advertising to sponsored editorial content and diagnostic tools. The most effective advertising is highly visible on primary pages about a specific condition on the most popular sites. This coveted space sells out quickly, often relegating competing brands to less desirable pages. Notable advertis-ing initiatives beyond the portals are Cardiology drug Trilipix’s ads on video platform Hulu, HPV drug Gardasil on the CW TV Network’s site, and allergy brands' display advertising on AccuWeather and Weather.com.

5 Medical, Marketing & Media

Off-Platform Messaging

QUICK STATS

Portal Collaboration:

• 58% of brands advertised on WebMD, Everyday Health or About.com Health in February 2010

• 42% of brands had a noticeable presence on WebMD

• 47% of brands had a noticeable presence on Everyday Health

• 13% of brands had a noticeable presence on About.com Health

• All Psychiatry and Rheumatology brands were visible on top health portals

www.webmd.comwww.qualityhealth.com

FINDINGS

18© L2 2010

EmailEmail is a low-cost way to engage patients and ensure they stay current on their drug regimen. More than 80% of brands offered opt-in email from the branded site, although less than 60% of these brands corresponded in a six-week period. Often a brand email effort is touted as a support program and is complemented by an offline effort, including direct mail.

The number one reason consumers opt in to email programs is to receive coupons6, and 30% of email programs specifically offered savings. The purpose and content of email campaigns ranged from calls to action (75%) to branded-drug-specific information: (75%), disease education (50%) and community content (30%).

In the best cases, emails were customized and personalized like Pristiq’s A New Day support messages. Some brands, including Ortho Tri-Cyclen Lo, Yaz, Humira, and Lovaza, offer patient reminder emails to support compli-ance.

6 Epsilon

QUICK STATS

Email:

• 72% of email programs contain a clear call to action to prompt doctor discussion or prescription fills.

• 70% of branded programs personalize emails.

• All Cardiology brands have email marketing programs.

• All Neurology brands have email marketing programs with clear calls to action.

Lescol XL email

Pristiq emailHumira email

FINDINGS

19© L2 2010

Mobile Pharmaceutical branded mobile activity is scant with the exception of SMS reminder alerts sent by 15% of brands. Third-party companies are also offering reminder and compliance apps, including the “Pill Phone” and “PillBoxer.”

None of the brands in the study have applications available in iTunes, however many iPhone apps exist for both general and specific disease management purposes. Notable in the general category is WebMD’s app, “WebMD Mobile,” which pro-vides information about symptoms, drugs, and first aid. Apps are com-mon for disease state management for conditions such as smoking ces-sation, insomnia, allergies, rheuma-tology, and cardiovascular disease.

MOBILE APPLICATION

Disease State

Customer Rating Comments

Chronic Pain Tracker Rheumatology 3/5

Enhanced $5.99 version allows users to log, track, and analyze pain and download data into PDF for healthcare provider discussion

iHeart-Pulse Reader Cardiovascular 5/5$4.99 app allows users to monitor and track their pulse over time

PureSleep AmbiScience Insomnia 3.5/5$0.99 app offers customizable audio programs to promote sleep

Live Happy Psychiatry 3/5$0.99 app provides tools to track mood and exercises to promote happiness

QuitterSmoking Cessation 3/5

Free app tracks number of smoke-free days and cost savings

Pink Reminder Women’s Health 3/5 $0.99 app reminds users to take medication

NOTABLE DISEASE MANAGEMENT APPS

QUICK STATS

Mobile:

• Merck and Sanofi-Aventis are the only pharmaceutical parent com- panies with iPhone apps. No brands have iPhone apps

i-Heart Pulse Reader App

ThePill.com App

Livehappy.com App

FINDINGS

20© L2 2010

PORTAL Description

Unique Monthly Visitors (millions) Key Advertising Tools

Advertising Brands include

Educational content, expert commentary, medical reviews, community services, and health management tools.

Content includes information about conditions, a drug database, healthy living advice, and news.

Message boards and newsletters serve as a precursor to its upcoming Health Exchange community site.

17.4 • Banner ads

• Sponsored editorial

• Sponsored “health checks”

• Technology superior to other

sites

Chantix

Cymbalta

Enbrel

NuvaRing

Viagra

Educational health content for more than 100 health categories ranges from information about common health conditions to interactive symptom checkers to nutritional and exercise tips.

Community section incorporates 2.0 tools, including blogs, personal profiles, and photos, to promote interaction among site visitors.

6.4 • Banner ads with flash and video

• Sponsored editorial

• Custom email campaigns

Abilify

Chantix

Lipitor

Orencia

Plavix

Seroquel

Viagra

Vytorin

Content organized by condition centers with information on the condition, symptoms, treatment options, and support resources.

The site also features healthcare news, videos, interactive symptom checkers, and community content in the form of health newsletters and such social media tools as blogs, chat rooms, and forums.

No data

• Banner ads

• Video ads

Cymbalta

Kapidex

Seasonique

Zetia

Offers news, videos, tips, drug guides, and interactive health tools across a number of disease-specific categories.

Social media tools are integrated to promote community, and offer condition-specific groups, message boards, and expert advice blogs.

Editorial content and videos often courtesy of third-party health content providers.

6.3 • Banner ads

• Video ads

Cialis

Lunesta

NuvaRing

Pristiq

Provides educational health content across more than 45 disease categories, with information on causes, symp-toms, and treatments.

The portal offers videos, news, expert advice, drug guides, and interactive tools, including symptom checkers and quizzes. 2.0 tools include blogs and support groups.

2.9 • Banner ads with flash

• Video ads

• Sponsorship of health centers

• Sponsored editorial

Cymbalta

Kapidex

Vytorin

Features informative health and fitness content, interac-tive tools, resources, expert advice, videos, specialized reports, and community content across more than 50 disease centers.

Disease centers include content in line with that of other portals, such as news, information on symptoms, and treat-ment options. Partners with third-party content providers.

2.8 • Banner ads with flash

• Video features

Chantix

Enbrel

Lipitor

Lyrica

NuvaRing

Pristiq

Viagra

SELECTED HEALTH PORTALS

FINDINGS

21

monials to educational pieces. The corporate Twitter account retweets and converses with users, while the company’s Facebook page features wall postings of varied and interest-ing content.

Some companies are experimenting with sponsored communities tailored to patients of specific disease states. Bayer’s MS-Gateway forum for multiple sclerosis boasts more than 12,000 members and 200,000 posts. Other interesting efforts include Novo Nordisk’s Voices of Diabetes community and Novartis’s CML Earth, an elegantly designed platform for leukemia patients.

As social media platforms experi-ence double- and triple-digit user growth, the pharmaceutical industry is missing a key opportunity to con-nect with consumers. According to Manhattan Research, more than 80 million Americans use social media for health-related issues. Brands often

© L2 2010

Social NetworkingOnly 19% of pharmaceutical brands are on at least one major social media platform: Facebook, You-Tube, or Twitter. Standouts Gardasil and Nexium maintain pages with rich media content and have at-tracted thousands of fans despite prohibiting wall postings to avoid adverse-event reporting. On Twitter, the Purple Pill listens to custom-ers and direct messages an 800 number in response to tweets about the drug. The only other brand ac-tive on Twitter is Spiriva, with five Twitter handles, four from celebrity spokespeople, conversing about the Drive4COPD campaign.

Eighteen percent of brands have a presence on YouTube ranging from dedicated YouTube channels (Yaz and Lunesta) to videos on parent

QUICK STATS

Social Media:

• 48% of parent companies have a presence on Facebook

• 28% of branded sites have Facebook as a top-5 referral site

• Facebook is a top-5 referral site for all Women’s Health brands

• 60% of parent companies have a presence on Twitter, with an average growth in followers of 31% from February to March 2010

• 36% of parent companies have a presence on YouTube

• According to Manhattan Research, almost 50% of con- sumers seeking health informa- tion watched health videos online in 2009

Yaz YouTube

Gardasil Facebook

FINDINGS

company channels (Ambien and Toprol-XL). Videos range from offer-ing specific information about a drug, its benefits and side effects, to playful content about a disease state, as in the case of Levitra’s InBed videos featuring a cartoon couple dealing with erectile dysfunction.

On the flip side, parent company social media adoption tops 80%. The disparity in participation be-tween parent company and brands highlights the effect of the current regulatory limbo concerning social media. However, most company efforts are little more than PR or human resources tools. Johnson & Johnson is a notable exception; the company maintains an engaging presence on all three major plat-forms. Its YouTube channel features videos ranging from patient testi-

22FINDINGS

cite regulations about adverse-event reporting as the reason for their hesi-tation to embrace social media. Yet, a November 2009 Nielsen study found that only one in 500 online postings, or 0.2%, incorporate the criteria re-quired for adverse-event reporting.

Third-party patient communities are proliferating, like PatientsLikeMe, with over 50,000 members, but they seldom offer brand advertising. Con-sumer health portals are also moving into the social networking space. In March 2010, WebMD announced the launch of Health Exchange, a new health social networking platform, to grab share from already entrenched third-party social media communi-ties. Well-known destination sites are also strong on Twitter, Facebook, and YouTube: LIVESTRONG’s CEO tweets, retweets, and direct mes-sages with some 1 million followers, and Mayo Clinic’s YouTube channel has generated more than 1.7 million views.

Johnson & Johnson YouTube channel and Facebook page

Patientslikeme.com

© L2 2010 FINDINGS

23© L2 2010

Company Twitter FollowersFollower Growth*

Total Tweets

**Tweet

Growth*Re-

tweets? Comments

Pfizer pfizer_news 5,146 14.1% 99 11.2% N Mostly PR, some pharmaceutical news and links to blogs and social media news

Novartis Novartis 4,652 ND 150 4.2% N Information about the company, products, links to other social media and technology. Company also appears to own protected handle Novartis Trials

GlaxoSmithKline GSKUS 3,426 ND 254 13.9% Y Links to GSK blog posts, news, other links; glaxo-smithkline also appears to be occupied by com-pany, but no tweets

Johnson & Johnson

JNJComm 3,201 ND 744 7.2% Y Highly personalized content; retweets and converses; provides color on industry and more general news

Roche Roche.com 3,193 ND 661 7.1% Y Conversations and news about company

Genentech genentechnews 2,754 6.6% 81 11.0% N PR news, information, links; brand also occupies genentech handle but no tweets

Amgen Amgen 2,124 8.4% 101 4.1% N Corporate PR and financial news

Sanofi-Aventis Durbaniak 1,677 ND 1,484 ND Y Vice president for innovation tweets about pharmaceutical social media

AstraZeneca AstraZeneca 1,287 17.4% 107 16.% Y PR information, including comments from CEO

Sanofi-Aventis sanofiaventisTV 924 6.3% 132 6.5% N French-language handle

Bristol-Myers Squibb

bmsnews 785 31.5% 4 ND N Mostly business news. First tweet March 1, 2010

Merck merckcareers1 669 8.6% 1,056 10.0% N Posts job openings. Company also appears to occupy Merck handle but account is protected

Bayer BayerHealthCare 556 143.9% 48 ND N German and English bilingual account tweets news

AstraZeneca AstraZenecaJobs 481 12.4% 888 13.6% N Tweets about available jobs

Genzyme genzymecorp 397 26.0% 0 0.0% N No content; unsure if official

Pfizer RayKerins 362 ND 31 3.3% Y Retweets Pfizer content and other pharmaceutical posts. Updates about FDA approvals and other industry news

Lilly Eli Lilly 205 9.6% 0 0.0% N No content; unsure if official

Novartis NVSOncoCareers 128 ND 58 141.7% N Links to job postings

Amgen AmgenFoundation 61 103.3% 2 NA N First tweet late February about Amgen’s foundation and philanthropic efforts

Galaderma galaderma 38 18.8% 0 0.0% N No content; unsure if official

TOP PARENT COMPANY TWITTER EFFORTS

FINDINGS

* February-March 2010 ** As of March 2010

24© L2 2010

Company Facebook Page Name Fans Comments

Novartis Novartis 3,615 Active fan wall engagement and photo uploads, including from employees and bloggers, a few links from company

Pfizer Pfizer 3,344 Launched in late February, offers links to news, corporate info (annual report, corporate social responsibility initiatives), Twitter, blogs, company posts, links, and videos on various topics

GlaxoSmithKline GlaxoSmithKline 2,739 PR communications from company, fan engagement in postings, unmoderated discussion board

Johnson & Johnson Johnson & Johnson Network

2,471 Links to news, history, stories, videos of patients, and caregiver stories about various conditions

Boehringer Ingelhelm Boehringer Ingelhelm 1,669 Unclear if page is official, mostly employees connecting from all over the world

AstraZeneca AstraZeneca US Community Connections

1,613 Highlights corporate social responsibility efforts and policies, wall postings, videos, and forum for moderated discussion, although no fan engagement

TOP PARENT COMPANY FACEBOOK EFFORTS

Company YouTube ChannelTotal

Views**Viewer

Growth* Comments

Johnson & Johnson Johnson & Johnson Health Channel

174,510 ND Videos on a number of procedures from hair transplants to coronary stent implants. Links to other J&J digital properties including blog

GlaxoSmithKline GSK Vision 20,682 3.4% General PR content from GSK

AstraZeneca AstraZenecaPharma 11,815 ND Video response to Men’s Health article that include two AstraZen-eca drugs: http://www.astrazeneca-us.com/?itemId=3311003

Boehringer Ingelheim boeringeringelheim 11,770 ND Disclaimer on site that states that it is not intended for views in U.S. Videos feature disease education: Parkinson’s, anticoagulation, etc.

Novartis Novartis 9,402 ND Patient testimonials, employee interviews, advertisements, demonstrations of social networking sites for gastrointestinal tumor (GIST) and chronic myelogenous leukemia (CML Earth)

Abbott AbbottChannel 6,167 6.2% Site content about the Abbot Fund, a nonprofit organization wholly supported by Abbott Laboratories

AstraZeneca AZ Careers 3,082 9.2% Content for recruiting and job seekers

Genentech Genentech 2,732 7.4% Testimonials from Genentech employees about work

Sanofi-Aventis Sanofi-Aventis Pharma’s Channel

1,922 1.4% Video of Ambien rooster commercial

Bayer Bayer AG 1,196 17.5% Videos about innovative company efforts

AstraZeneca AZ Business Channel 774 ND Interviews with management

TOP PARENT COMPANY YOUTUBE EFFORTS

FINDINGS

* February-March 2010 ** As of March 2010

25© L2 2010

8 1 SYMBICORT AstraZeneca 5 3 1 2 130 Gifted

21 2 ADVAIR GlaxoSmithKline 3 3 2 3 106 Average

22 3 SINGULAIR Merck 3 3 2 3 105 Average

24 4 SPIRIVAPfizer and Boehringer Ingelheim 2 2 1 5 102 Average

37 5 NASONEX Schering-Plough 2 0 3 3 86 Challenged

39 6 VERAMYST GlaxoSmithKline 3 2 1 0 85 Challenged

41 7 OMNARIS Sepracor 1 1 4 1 82 Challenged

48 8 PATANASE Alcon 2 0 0 1 60 Feeble

50 9 PULMICORT AstraZeneca 0 2 0 1 52 Feeble

51 10 ASTEPRO Meda 0 0 1 0 42 Feeble

OVERALL

RANK

CATEG

ORY RANK

DRUGPA

RENT

PLATF

ORM

OFF-P

LATF

ORM

SEO SOCIAL MED

IA

DIGITA

L IQ

CLASS

Brands in the Asthma & Allergy category demonstrate the lowest average IQ of the eight disease states.

Sites in the category suffer from poor traffic, weak content, and do little to build community or prompt user action. AstraZeneca’s Symbi-cort is the lone bright spot, scoring IQ points for its innovative advertis-ing presence on healthcare portal Everyday Health, and for a site that incorporates an intuitive interface with interactive disease education.

Singulair and Spiriva are the only other brands that demonstrate an active ad presence on top health portals. Spiriva boasts the category’s strongest social media effort with a rare pharmaceutical multichannel digital campaign, Drive4COPD.

>> 67% of brands in the category offer coupons for new prescriptions. <<

ASTHMA & ALLERGY

ASTHMA & ALLERGY

0

5

10

15

20

ASTEPRO

PULMICORT

PATANASE

VERAMYST

OMNARISSPIRIVA

NASONEXADVAIR

SINGULAIR

SYMBICORT

SITE CONTENT BY BRAND

Enhance Brand

Building Community

Conversion

Disease Education

26© L2 2010

FLASH OF GENIUS

DRIVE4COPD

A rare multichannel effort is Spiriva’s Drive4COPD campaign, which recruited five celebrities to drive across the U.S. to host screening events for chronic obstructive pulmonary disease (COPD). A dedicated microsite serves as mission control for social media tools used to promote Drive4COPD, including a live Twitter feed, links to Flickr photos, YouTube videos, and a dedicated Facebook page. The site also hosts a screening tool so that users can participate virtually.

>> 60% of Allergy & Asthma brands have an email marketing program. <<

ASTHMA & ALLERGY

COMPARATIVE TRAFFIC

Relative Site Traffic Among Asthma & Allergy Brands

0

10

20

30

40

50

PULMICORT PATANASESINGULAIRSPIRIVAVERAMYSTASTEPROOMNARISSYMBICORTADVAIRNASONEX

Paid Search

No Paid SearchRE

LATI

VE S

ITE

TRAF

FIC

27© L2 2010

>> 40% of Allergy & Asthma brands engage in paid search. <<

ASTHMA & ALLERGY

SPOTLIGHT ON SOCIAL MEDIAMISSED OPPORTUNITY

In addition to Spiriva’s efforts on Twitter, YouTube, Facebook, and Flickr, other brands in the Asthma & Allergy category dabble with social media.

AstraZeneca’s Symbicort launched a YouTube channel, My Asthma Story, in February 2009, featuring testimonials by users about their experiences with the drug. The site was no longer on YouTube as of March 2010.

PULMICORT

Pulmicortflexhaler.com is a limited site that is best described as brochure ware. For example, the “Just Ask Sara” section recaps a conversation between a patient and physician in text without employing media or graphics to bring the content to life. The user does not have a reason to return to the site and is left feeling like the web is an afterthought for the brand.

COMPARATIVE BRAND BUZZ

Relative Volume & Sentiment of Commentary on Blogs

+7

+6

+5

+4

+3

+2

+1

-1

-2

-3

-4

-5

-6

-7

0

ADVAIR

SINGULAIR

SYMBICORT

NASONEX

SPIRIVA

PULMICORT

VERAMYST

ASTEPRO

OMNARISPATANASE

Pos

itive

Neutral

RELATIVE VOLUME

Neg

ativ

e

RELA

TIVE

SEN

TIM

ENT

BRANDED SOCIAL MEDIA PRESENCE

Advair - - -

Astepro - - •Nasonex - - -

Omnaris - - -

Patanase - - -

Pulmicort - - -

Singulair - - -

Spiriva • • •Symbicort - - •Veramyst - - -

KRISTIN GOELZFlashlight Interactive

28© L2 2010

5 1 CRESTOR AstraZeneca 5 3 2 4 137 Gifted

12 2 LIPITOR Pfizer 4 4 2 3 124 Gifted

23 3 ZETIA Merck 2 4 2 3 106 Average

26 4 VYTORIN Merck 2 4 2 3 103 Average

32 5 PLAVIXBristol-Myers Squibb and Sanofi-Aventis 1 4 2 3 94 Average

36 6 LOVAZA GlaxoSmithKline 4 0 1 1 88 Challenged

44 7 LESCOL XLSchering-Plough and GlaxoSmithKline 1 1 2 0 66 Feeble

45 11 TRILIPIX Abbott 0 0 0 2 63 Feeble

46 8 CADUET Pfizer 1 1 1 0 63 Feeble

47 10 NIASPAN Abbott 0 0 0 1 61 Feeble

49 9 TOPROL-XL AstraZeneca 0 1 0 2 60 Feeble

OVERALL

RANK

CATEG

ORY RANK

DRUGPA

RENT

PLATF

ORM

OFF-P

LATF

ORM

SEO SOCIAL MED

IA

DIGITA

L IQ

CLASS

Cardiology, the largest category in the study (as defined by the number of brands included), disappoints. This group boasts more Feeble brands than any other disease state.

Gifted brands Crestor and Lipitor lead online category efforts with interac-tive, brand-enhancing sites that substantially outperform peers in the space. Although 82% of Cardiology brands engage in paid search, aver-age traffic to branded sites was 27% below the study average, and not one cardiovascular brand has established a beachhead in social media. Toprol-XL is the only brand with web 2.0 presence: a video on AstraZeneca’s YouTube Channel. More than 60% of sites offer discounts for new prescrip-tions and more than half offer savings for current users.

Although every Cardiology brand engages in email marketing, brand sites were the least likely among all categories to offer compliance tools such as Crestor’s cholesterol tracker and Lovaza’s email, text, and voicemail reminders. In addition to site efforts, most differentiation in the space occurs across off-platform messaging. Aggressive online adver-tising both on and off consumer health portals supports Gifted brand Lipitor. Zetia, Vytorin, and Plavix also shine in the space.

>> Four of the brands in this category have dedicated unbranded disease education sites, with Niaspan offering three separate sites: www.forheartrisk.com | www.knowyourhdl.com | www.knowyourtrigs.com <<

CARDIOLOGY

CARDIOLOGY

TRILIPIX

TOPROL-XL

NIASPANCADUET

LESCOL XLPLAVIX

VYTORINLOVAZA

ZETIALIPITOR

CRESTOR

SITE CONTENT BY BRAND

Enhance Brand

Building Community

Conversion

Disease Education

29© L2 2010

FLASH OF GENIUS

KRISTIN GOELZFlashlight Interactive CRESTOR: Online Tools

Crestor.com is made for the masses. It is built for technophobes as well as technophiles. The content-heavy site gives users control of their experience with the choice to read or watch product or disease state explanations. The online tools encourage repeat visits and clearly emphasize the need to speak to a physician about treatment options.

LIPITOR: NavigationLipitor.com does a great job connecting disease state and brand information. The fun navigational tools accentuate the breadth of content on the site and allow easy access to key areas. The site satisfies the regulatory constraints of the pharmaceutical industry while still engaging patients by allowing

them to share stories.

>> Vytorin leads all cardiology brands in site traffic, boasting over 100,000 unique monthly visitors. <<

CARDIOLOGY

30© L2 2010

>> Niaspan’s site offers a dedicated customer service phone number available 24/7. <<

CARDIOLOGY

LESCOL XLTOPROL-XLCADUETLOVAZANIASPANTRILIPIXCRESTORPLAVIXLIPITORZETIAVYTORIN

MISSED OPPORTUNITY

NIASPAN.COMThe small print filling the primary entry page of Niaspan.com makes for an intimidating first impression. The site reinforces this by repeating words such as “side effects” and “safety information” (11 times on the home page alone), as well as using content filled with legalese. Consumers searching for clear information will have trouble deciphering phrases such as, “NIASPAN, along with diet and a bile acid binding resin.”

KRISTIN GOELZFlashlight Interactive

COMPARATIVE TRAFFIC

Relative Site Traffic Among Cardiology BrandsPaid Search

No Paid Search

RELA

TIVE

SIT

E TR

AFFI

C

31© L2 2010

>> Lescol XL’s site offers phone, mail, and email contact information, with a promise to return email messages within 24 hours. <<

CARDIOLOGY

SPOTLIGHT ON SOCIAL MEDIA

AstraZeneca’s YouTube channel includes a short video featuring a doctor discussing Toprol-XL and its treatment of high blood pressure. As of March 2010, the video had only 320 views since its upload in October 2009—though not setting the world on fire, the effort is to be applauded.

Cardiology brands benefit from an average buzz score three times the study’s average, with blog topics ranging from FDA news and medical study results to business news and side effects.

COMPARATIVE BRAND BUZZ

Relative Volume & Sentiment of Commentary on Blogs

+7

+6

+5

+4

+3

+2

+1

0

-1

-2

-3

-4

-5

-6

-7

TOPROL-XL

LOVAZA

LESCOL XLPLAVIX

VYTORIN

ZETIA

CRESTOR

NIASPAN CADUET

LIPITOR

TRILIPIX

Pos

itive

Neutral

RELATIVE VOLUME

Neg

ativ

e

RELA

TIVE

SEN

TIM

ENT

BRANDED SOCIAL MEDIA PRESENCE

Caduet - - -

Crestor - - -

Lescol XL - - -

Lipitor - - -

Lovaza - - -

Niaspan - - -

Plavix - - -

Vytorin - - -

Zetia - - -

Toprol-XL - - •Trilipix - - -

32© L2 2010

2 1 NEXIUM AstraZeneca 5 3 3 5 143 Genius

19 2 KAPIDEX Takeda 3 5 3 0 110 Gifted

29 3 ACIPHEXElsai & Ortho-McNeil-Janssen (PriCara)

3 0 4 2 98 Average

OVERALL

RANK

CATEG

ORY RANK

DRUGPA

RENT

PLATF

ORM

OFF-P

LATF

ORM

SEO SOCIAL MED

IA

DIGITA

L IQ

CLASS

Genius Nexium leads the small but relatively strong Gastrointestinal category.

AstraZeneca’s purple pill stood out as an industry leader with the top-trafficked site and is the only brand with both a Twitter and Facebook presence, the latter offering an inter-active poll and links to coupons.

The Nexium site possesses an intuitive user interface and practi-cal lifestyle tools for managing diet, exercise, and sleep. The brand also has a prominent advertising pres-ence on healthcare portals including WebMD and Everyday Health.

Takeda’s Kapidex leads category online advertising efforts, with spon-sored editorial and video content on WebMD. Along with Aciphex, Kapidex offers email communica-tion; however, limited online adver-tising and a flat brand site prevents Kapidex from keeping up with digitally adept gastrointestinal peers. All brands in the category participate in paid search.

>> Aciphex leads Gastrointestinal brands in mentions on blogs and online comments. <<

GASTROINTESTINAL

GASTROINTESTINAL

0

3

6

9

12

15

KAPIDEXACIPHEX

NEXIUM

SITE CONTENT BY BRAND

Enhance Brand

Building Community

Conversion

Disease Education

0

10

20

30

40

50

60

ACIPHEXKAPIDEXNEXIUM

COMPARATIVE TRAFFIC

Relative Site Traffic Among Gastrointestinal Brands

Paid Search

No Paid Search

RELA

TIVE

SIT

E TR

AFFI

C

33© L2 2010

FLASH OF GENIUS

NEXIUM: Lifestyle Tools

Nexium’s site offers customized health management tools and dietician’s advice via email. Tools include the Trigger Checker, a searchable database of acid-reflux trigger ingredients and suggestions for milder substitutes; the Meal Planner, a weekly menu builder with heartburn-preventing recipes; and the Personal Fitness Planner, a tool that creates customized exercise plans designed by a virtual fitness trainer that can be saved on site.

>> Nexium leads all brands in traffic with more than 900,000 unique monthly visitors. <<

GASTROINTESTINAL

34© L2 2010

>> Nexium is the only brand in this category with an unbranded disease education site with a separate URL: www.gerd.com. <<

GASTROINTESTINAL

SPOTLIGHT ON SOCIAL MEDIA

Nexium is the only gastrointestinal brand with a presence on both Facebook and Twitter. With more than 2,000 fans, Nexium’s Facebook page promotes purplepill.com’s health tools, patient success stories, and FAQs. The page features moderated discussions, user polls, and links to a printable savings card.

Nexium’s Twitter handle has 152 followers and grew by almost one third month-on-month from February to March 2010. In addition, the AZhelps handle, maintained by par-ent company AstraZeneca, responds to comments and complaints about Nexium via direct messages and offers a toll-free number for users to follow up.

COMPARATIVE BRAND BUZZ

Relative Volume & Sentiment of Commentary on Blogs

+7

+6

+5

+4

+3

+2

+1

-1

-2

-3

-4

-5

-6

-7

-8

-9

-10

0

ACIPHEX

NEXIUM

KAPIDEX

Pos

itive

Neutral

RELATIVE VOLUME

Neg

ativ

e

RELA

TIVE

SEN

TIM

ENT

BRANDED SOCIAL MEDIA PRESENCE

Aciphex - - -

Kapidex - - -

Nexium • • -

35© L2 2010

3 1 CHANTIX Pfizer 4 5 4 3 140 Genius

10 2 LUNESTA Sepracor 3 5 3 5 126 Gifted

15 3 AMBIEN CR Sanofi-Aventis 4 2 5 4 118 Gifted

OVERALL

RANK

CATEG

ORY RANK

DRUGPA

RENT

PLATF

ORM

OFF-P

LATF

ORM

SEO SOCIAL MED

IA

DIGITA

L IQ

CLASS

The small Neurology category features three of the most ubiquitous pharma-ceutical brands and some of the strongest digital innovation in the industry.

Pfizer’s smoking cessation drug, Chantix, earns a spot in the Genius ranks boasting an intuitive, customer- oriented site and a sponsored re-source center on WebMD.

Lunesta takes home the digital crown among sleep aids, with a YouTube channel featuring patient success stories. The Sepracor brand also scores points for effective email marketing and digital advertising on health portals.

Although Ambien CR finished below its sleep-aid rival, its site is a delight, with playful videos that explore the embarrassing outcomes of sleep de-privation. The brand site also features polls that allow users to compare their sleep habits with those of the local and national population, and interactive sleep trackers.

>> All Neurology brands engage in paid search. <<

RELA

TIVE

SIT

E TR

AFFI

C

NEUROLOGY

NEUROLOGY

0

3

6

9

12

15

LUNESTA

CHANTIX

AMBIEN CR

SITE CONTENT BY BRAND

Enhance Brand

Building Community

Conversion

Disease Education

01020304050607080

AMBIEN CRLUNESTACHANTIX

COMPARATIVE TRAFFIC

Relative Site Traffic Among Neurology Brands

Paid Search

No Paid Search

36© L2 2010

FLASH OF GENIUS

KRISTIN GOELZFlashlight Interactive CHANTIX: Online Advertising

The Pfizer superstar stands out for its widespread and innovative online advertis-ing across major portals including WebMD, Everyday Health, and About.com Health. Chantix’s sponsored resource center on WebMD features brand-created content, including video testimonials from successful quitters, instant polls, and articles on smok-ing cessation.

A second resource center, Proven Strategies

to Quit Smoking When You’re Ready to Get

Serious, is funded by parent company Pfizer and features editorial content as well as banner ads.

>> Lunesta is the only Neurology brand that does not maintain an unbranded disease education site; relative newcomer Chantix maintains three separate sites, and Ambien CR supports one. <<

NEUROLOGY

37© L2 2010

>> All Neurology brands offer compliance tools on their branded sites. Ambien CR’s site receives more than twice as much traffic as Lunesta’s. <<

NEUROLOGY

SPOTLIGHT ON SOCIAL MEDIA

Both major insomnia brands have a social media presence: Lunesta hosts a dedicated YouTube chan-nel, and Ambien CR posts its famed rooster commercial on parent Sanofi-Aventis’s channel, with more than 8,500 upload views to date. Lunesta’s channel features patient stories that are also streamed on its site, but is plagued by limited views.

On the heels of great earned media from the “Silence Your Rooster” campaign, Ambien CR leads Neurol-ogy brands in mentions on online blogs and comments.

COMPARATIVE BRAND BUZZ

Relative Volume & Sentiment of Commentary on Blogs

+7

+6

+5

+4

+3

+2

+1

-1

-2

-3

-4

-5

-6

-7

0

AMBIEN CR

CHANTIX

LUNESTA

Pos

itive

Neutral

RELATIVE VOLUME

Neg

ativ

e

RELA

TIVE

SEN

TIM

ENT

BRANDED SOCIAL MEDIA PRESENCE

Ambien CR - - •Chantix - - -

Lunesta - - •

38© L2 2010

11 1 SEROQUEL AstraZeneca 4 4 3 4 124 Gifted

16 2 CYMBALTA Lilly 1 5 4 3 113 Gifted

17 3 ABILIFY Bristol-Myers Squibb 3 2 5 3 111 Gifted

42 4 PRISTIQ Pfizer 0 4 0 1 71 Challenged

OVERALL

RANK

CATEG

ORY RANK

DRUGPA

RENT

PLATF

ORM

OFF-P

LATF

ORM

SEO SOCIAL MED

IA

DIGITA

L IQ

CLASS

Psychiatry’s strength as a category is in off-platform messaging, and most brands advertise on top consumer health portals and other digital properties.

All brands but Cymbalta engage in email marketing programs. Annual traffic growth to branded Psychiatry sites tops 130%—second only to Urology in this study—driven largely by triple-digit growth to Abilify and Cymbalta’s sites.

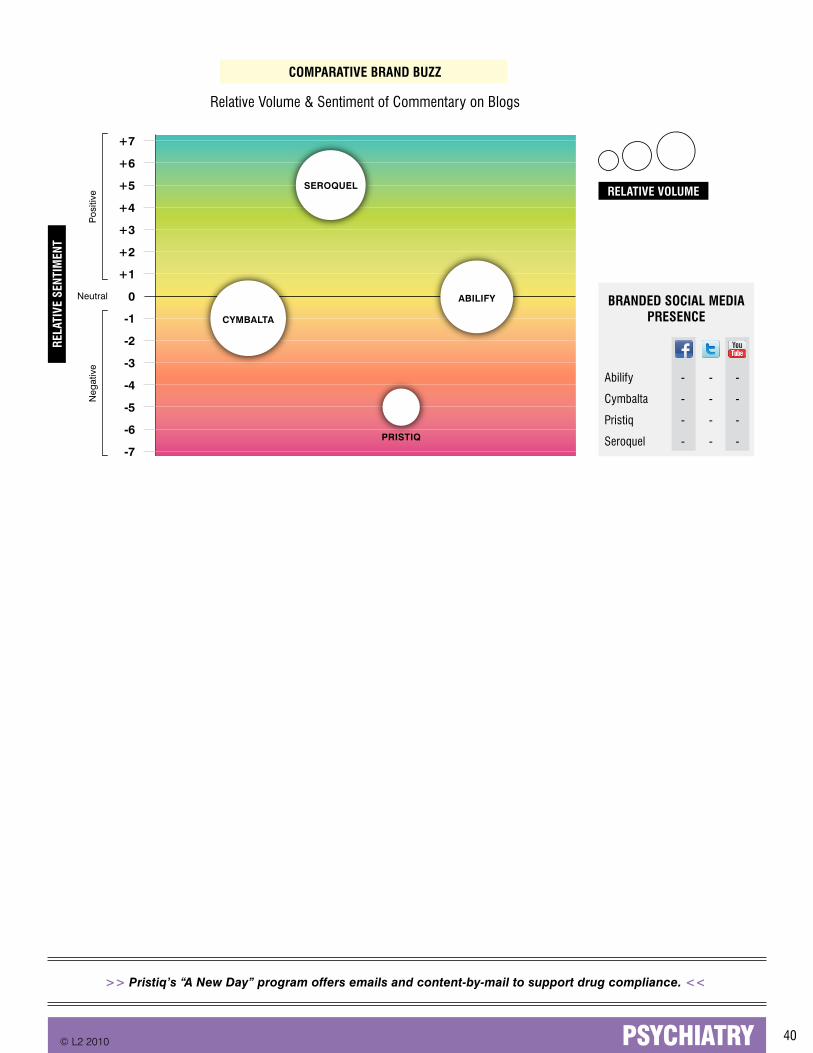

All brands participate in paid search except for Pristiq. Not one brand in the category has an official social media presence, however Psychiatry brands are popular conversation topics in the blogosphere. Category leader Seroquel is the only brand with net positive attention, largely be-cause of recent legal liability victories.

Sites in the category vary greatly, from Seroquel’s easy-to-navigate, tech-savvy platform with strong education and community content to Pristiq’s dated efforts overwhelmed by repurposed TV content. Overall, education information and conver-sion tools are weak across the category. Abilify’s site offers various tools intended to prompt doctor discussion, including a Depression Inventory questionnaire, Doctor Discussion guide, and side effects checklist.

>> Seroquel and Cymbalta are the only Psychiatry brands with unbranded disease education sites. <<

PSYCHIATRY

PSYCHIATRY

0

3

6

9

12

15

PRISTIQ

CYMBALTA

SEROQUELABILIFY

SITE CONTENT BY BRAND

Enhance Brand

Building Community

Conversion

Disease Education

SPOTLIGHT ON SOCIAL MEDIA

None of the Psychiatry brands currently participate in social media. Cymbalta, Abilify, and Seroquel all earn high blog buzz scores with content ranging from brand news and discussions of efficacy to side effects and compliance.

39© L2 2010

FLASH OF GENIUS

SEROQUEL: Video & Portraits Of Bipolar Depression

Seroquel integrates video throughout its site featuring dramatized stories and patient testimonials. The “Portraits of Bi-Polar” section offers ten short, high-resolution dramatizations that explain the challenges of Bi-Polar disorder to patients and those who support them. The nine patient testimonials address the impact of bi-polar disorder on inter-personal relationships and provide disease information.

>> Cymbalta’s site had over 130,000 unique visitors in February 2010. <<

RELA

TIVE

SIT

E TR

AFFI

C

PSYCHIATRY

COMPARATIVE TRAFFIC

Relative Site Traffic Among Psychiatry Brands

01020304050607080

PRISTIQCYMBALTA SEROQUELABILIFY

Paid Search

No Paid Search

40© L2 2010

>> Pristiq’s “A New Day” program offers emails and content-by-mail to support drug compliance. <<

PSYCHIATRY

COMPARATIVE BRAND BUZZ

Relative Volume & Sentiment of Commentary on Blogs

+7

+6

+5

+4

+3

+2

+1

-1

-2

-3

-4

-5

-6

-7

0

CYMBALTA

ABILIFY

SEROQUEL

PRISTIQ

Pos

itive

Neutral

RELATIVE VOLUME

Neg

ativ

e

RELA

TIVE

SEN

TIM

ENT

BRANDED SOCIAL MEDIA PRESENCE

Abilify - - -

Cymbalta - - -

Pristiq - - -

Seroquel - - -

41© L2 2010

17 1 ORENCIA Bristol-Myers Squibb 3 4 2 1 111 Gifted

20 2 SYNVISC Genzyme 4 2 3 2 107 Average

27 3 CELEBREX Pfizer 2 3 2 4 100 Average

30 4 RITUXAN Biogen and Genetech 3 2 1 1 94 Average

31 5 HUMIRA Abbott 3 1 2 1 93 Average

32 6 ENBREL Amgen and Wyeth 2 3 2 2 92 Average

40 7 LYRICA Pfizer 1 3 3 2 84 Challenged

OVERALL

RANK

CATEG

ORY RANK

DRUGPA

RENT

PLATF

ORM

OFF-P

LATF

ORM

SEO SOCIAL MED

IA

DIGITA

L IQ

CLASS

Rheumatology brand efforts are functional yet predictable and stifled by limited risk-taking.

Bristol-Myers Squibbs’ Orencia tops the rankings, scoring IQ points from its advertising presence on WebMD and Everyday Health and its email marketing initiatives. Celebrex, En-brel, and Lyrica also boast a strong advertising presence on health portals. Lyrica, which received multi-indication approval for fibromyalgia in 2007, takes a hit for its site, which is difficult to navigate and fails to incorporate technology, although a disease education site improves the quality of Lyrica’s digital information.

No Rheumatology brand participates in social media, although Enbrel’s 24-hour nurse hotline allows for two-way communication between a patient and the brand.

>> Lyrica leads all Rheumatology brands in traffic, with more than 165,000 unique visitors per month. <<

RHEUMATOLOGY

RHEUMATOLOGY

0

3

6

9

12

15

LYRICAHUMIRA

CELEBREXENBREL

RITUXAN

ORENCIA

SYNVISC

SITE CONTENT BY BRAND

Enhance Brand

Building Community

Conversion

Disease Education

SPOTLIGHT ON SOCIAL MEDIA

No Rheumatology brands participate in social media. Celebrex leads the category in mentions on online blogs and commenting and is sixth overall among all brands in the study.

42© L2 2010

FLASH OF GENIUS

SYNVISC: Disease EducationSynvisc boasts nine videos throughout its site, including patient testimonials and descriptive pieces featuring the site physician, Dr. Nicholas DiNubile. Video content is supplemented by information on living with knee pain, links to related organizations, and other lifestyle content. In addition, Synvisc’s Knee Pain Assessment tool is accessible from most education-related pages on the brand site. The assessment can be emailed to the user or printed and is accom-panied by a doctor locator tool prompting a clear call to action.

>> Six of the seven Rheumatology brands maintain an unbranded disease education site with a separate URL; Lyrica is the exception. <<

RHEUMATOLOGY

COMPARATIVE TRAFFIC

Relative Site Traffic Among Rheumatology Brands

0

10

20

30

40

50

RITUXANHUMIRASYNVISC ORENCIAENBRELCELEBREXLYRICA

Paid Search

No Paid SearchRE

LATI

VE S

ITE

TRAF

FIC

43© L2 2010

>> 85% of Rheumatology brands offer email marketing programs; 65% of which include clear calls to action in email. <<

RHEUMATOLOGY

MISSED OPPORTUNITY

LYRICAThe section of Lyrica.com created for epilepsy is small with limited content. Given the strong offline campaign for the brand, visitors expect more from the site, which has no interactive features and provides external links for most resources.

KRISTIN GOELZFlashlight Interactive

COMPARATIVE BRAND BUZZ

Relative Volume & Sentiment of Commentary on Blogs

+7

+6

+5

+4

+3

+2

+1

-1

-2

-3

-4

-5

-6

-7

0

CELEBREX

ENBREL

LYRICA

HUMIRA

ORENCIA

SYNVISC

RITUXAN

Pos

itive

Neutral

RELATIVE VOLUME

Neg

ativ

e

RELA

TIVE

SEN

TIM

ENT BRANDED SOCIAL MEDIA

PRESENCE

Celebrex - - -

Enbrel - - -

Humira - - -

Lyrica - - -

Orencia - - -

Rituxan - - -

Synvisc - - -

44© L2 2010

1 1 VIAGRA Pfizer 5 4 5 4 149 Genius

12 2 LEVITRA Novartis 2 4 3 5 121 Gifted

27 3 CIALIS Eli Lilly 1 3 4 4 100 Average

32 4 ANDROGEL Solvay 4 2 1 0 92 Average

37 5 AVODART GlaxoSmithKline 1 1 3 3 86 Challenged

42 6 FLOMAXAstellas and Boehringer Ingelheim 1 1 1 3 71 Challenged

OVERALL

RANK

CATEG

ORY RANK

DRUGPA

RENT

PLATF

ORM

OFF-P

LATF

ORM

SEO SOCIAL MED

IA

DIGITA

L IQ

CLASS

Digital aptitude varies significantly across the heavily marketed Urology category.

Most brand sites introduce con-version tools to facilitate initial patient-doctor discussion but place little emphasis on community. The category has a significant presence on top consumer health portals, and many brands, not surprisingly, generate a disproportionate amount of buzz on pharmaceutical blogs.

Genius Viagra offers quality and consistency across platforms and boasts a dominant online advertis-ing presence, considerable site traffic, and interactive video on its brand site. Well-conceived email marketing initiatives and a YouTube channel (the lone category social media presence) earned Levitra a spot among the Gifted ranks.

Cialis scores well in blog mentions and search engine strength, but its text-heavy site lacks strong branding beyond the home page. AndroGel’s otherwise underwhelming digital footprint is buttressed by a strong disease education site that supple-ments its Is It LowT? campaign. Challenged brands Avodart and Flomax struggle to overcome their outdated sites.

>> Viagra’s site was second only to Nexium’s in unique page visitors. <<

UROLOGY

UROLOGY

0

5

10

15

20

FLOMAX

AVODARTCIALIS

LEVITRA

ANDROGELVIAGRA

SITE CONTENT BY BRAND

Enhance Brand

Building Community

Conversion

Disease Education

45© L2 2010

FLASH OF GENIUS

VIAGRA.COMIn addition to an excellent user interface, Viagra’s site displays an impressive use of flash and video to create an interactive user experience. The “Start the talk” and “Hear from real guys” videos incorporate buttons that direct users to relevant content, includ-ing a simulated patient-doctor conversation. Viagra’s video content packages informa-tion in digestible, informative bits, a strong contrast to the text-heavy, brochure-ware common to sites in the category.

>> Levitra and AndroGel are the only brands in the category with unbranded disease education sites. <<

UROLOGY

COMPARATIVE TRAFFIC

Relative Site Traffic Among Urology Brands

01020304050607080

ANDROGELFLOMAXAVODARTLEVITRACIALISVIAGRA

Paid Search

No Paid Search

RELA

TIVE

SIT

E TR

AFFI

C

46© L2 2010

>> Cialis, Viagra, and Levitra are the top three brands generating blog postings and comments in the study. <<

UROLOGY

SPOTLIGHT ON SOCIAL MEDIA

LEVITRA: In Bed CampaignBuzz on blogs is a categorywide strength for Urology brands, but Levitra’s multichannel In

Bed campaign is a standout industry success on YouTube.

Although a disclaimer indicates that the content is intended for audiences outside the U.S. and the U.K., two brand channels feature videos from the campaign. With more than 135,000 views, the Inbedstory channel unspools a series of nine short episodes following the disease awareness and treatment process of an “ordinary bloke” who suffers from erectile dysfunction (ED).

A second channel, Inbeddr, with almost 2,000 views, offers educational content on ED with 60 videos featuring advice from a doctor.

COMPARATIVE BRAND BUZZ

Relative Volume & Sentiment of Commentary on Blogs

+7

+6

+5

+4

+3

+2

+1

-1

-2

-3

-4

-5

-6

-7

0 CIALIS

VIAGRALEVITRA

FLOMAX

AVODARTANDROGEL

Pos

itive

Neutral

RELATIVE VOLUME

Neg

ativ

e

RELA

TIVE

SEN

TIM

ENT

BRANDED SOCIAL MEDIA PRESENCE

AndroGel - - -

Avodart • - -

Cialis - - -

Flomax - - -

Levitra - - •Viagra - - -

47

WOMEN’S HEALTH

WOMEN’S HEALTH© L2 2010

4 1 ORTHO TRI-CYCLEN LO

Ortho-McNeil Janssen 5 4 4 4 137 Gifted

6 2 GARDASIL Merck 5 1 5 5 131 Gifted