WORKING TITLE: DIFFUSION OF THE BITCOIN INNOVATION Abstract This paper discusses the technological innovation known as the Bitcoin network; a distributed, peer-to-peer platform, within which a cryptographic currency protocol (also known as Bitcoin) enabling online digital payments, is presently prominent and attracting world-wide attention. A short introduction to the history and characteristics of Bitcoin is provided. Thereafter, the global awareness, acceptance and adoption of Bitcoin is examined through the prism of diffusion of innovations theory, as developed by American sociologist Everett Rogers. The S-shaped rate of adoption curve is utilized in reference to Bitcoin, enabling the potential evolution of the Bitcoin innovation beyond that of a medium of exchange, to be anticipated in general terms. Introduction to Bitcoin “Bitcoin is an exciting innovation that has the potential to greatly improve human welfare and jump-start beneficial and potentially revolutionary developments in payments, communications, and business.” (Brito & Castillo, 2013). Bitcoin is an open-source, digital currency protocol that operates on a distributed, peer-to-peer, global network and functions without a central authority (such as the Federal Reserve or the European Central Bank). Bitcoin became the 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WORKING TITLE: DIFFUSION OF THE BITCOIN INNOVATION

Abstract

This paper discusses the technological innovation known as the

Bitcoin network; a distributed, peer-to-peer platform, within

which a cryptographic currency protocol (also known as

Bitcoin) enabling online digital payments, is presently

prominent and attracting world-wide attention. A short

introduction to the history and characteristics of Bitcoin is

provided. Thereafter, the global awareness, acceptance and

adoption of Bitcoin is examined through the prism of diffusion

of innovations theory, as developed by American sociologist

Everett Rogers. The S-shaped rate of adoption curve is

utilized in reference to Bitcoin, enabling the potential

evolution of the Bitcoin innovation beyond that of a medium of

exchange, to be anticipated in general terms.

Introduction to Bitcoin

“Bitcoin is an exciting innovation that has the potential to greatly improve human

welfare and jump-start beneficial and potentially revolutionary developments in

payments, communications, and business.” (Brito & Castillo, 2013).

Bitcoin is an open-source, digital currency protocol that

operates on a distributed, peer-to-peer, global network and

functions without a central authority (such as the Federal

Reserve or the European Central Bank). Bitcoin became the

1

world’s first decentralized online payment system when it was

initiated in 2009 by a pseudonymous developer known as Satoshi

Nakamoto, who had previously released a white paper entitled

“Bitcoin: A Peer-to-Peer Electronic Cash System” (Nakamoto,

2008).

The Bitcoin protocol is revolutionary insofar as it provides a

solution to the long-standing “double-spending problem”

(Nakamoto, 2008) which had previously meant that digital

payment systems used by consumers required the participation

of a trusted third-party (such as a credit card processor) to

ensure that funds could not be spent twice and that fraud was

minimized between transacting entities.

Bitcoin circumvents the trusted third-party requirement by way

of its distributed ledger system known as a block chain. The

Bitcoin block chain is constantly updated with a time-stamped

record of all the transactions undertaken on the Bitcoin

network, which are verified to ensure that no double-spending

has occurred. Bitcoin ‘miners’ who contribute their computer

processing-power to verify the block chain ledger integrity,

by adding individually verified blocks to the chain, are paid

in small transaction fees and newly-created blocks of

bitcoins.

Incredibly, the Bitcoin network is the largest network of

distributed computing power ever created– in late 2013 it was

estimated that it was as 100 times as large as the 500 most

powerful super-computers on Earth, at more than 50,000

petaflops in size (The Economist, 2013).

2

Bitcoin’s monetary value against government-issued currencies

is determined by global exchanges on the open market and

denominated in all the major currencies of the world. In

January 2013, a unit of Bitcoin averaged at USD $13. By

December 2013, it had sky-rocketed to almost USD $1,200,

making the digital currency the best performing currency,

commodity or asset-class (debate is ongoing as to the precise

nature of Bitcoin) of the year. Presently, one unit fetches

USD $700 on global Bitcoin exchanges. These online enterprises

(e.g. Mt. Gox – https://www.mtgox.com/) enable the exchange of

fiat currency for Bitcoin and vice-versa.

Diffusion of Innovations

“Diffusion is the process in which an innovation is communicated through certain

channels over time among the members of a social system.” (Rogers, 2003, p.

5).

Rogers outlined four main elements to the diffusion of

innovations framework. The following sections will discuss the

diffusion model and make a preliminary attempt to relate it to

the Bitcoin innovation.

1. Innovation

An innovation is “an idea, practice, or object that is perceived

as new by an individual or other unit of adoption” (Rogers,

2003, p. 12).

Technology is seen as a “design for instrumental action that

reduces the uncertainty in the cause-effect relationship

3

involved in achieving a desired outcome” (Rogers, 2003, p.

13).

Technology usually consists of hardware and / or software, or

some combination of both. Bitcoin is an internet-based

innovation. It commenced its existence on the Internet, in

2009, as a “peer-to-peer version of electronic cash”

(Nakamoto, 2008) but it continues to evolve (as a protocol,

platform and network) and shows potential beyond that of a

mere currency.

Bitcoin relies on both hardware and software (Rogers, 2003, p.

13) for its continued survival and propagation,

notwithstanding the fact that it is possible to back-up

Bitcoin transactions offline, in hard-copy form, meaning that

Bitcoin could even, in theory, survive the destruction of the

Internet itself.

Rogers notes that technology clusters consist of “one or more

distinguishable elements of technology that are perceived as

being closely interrelated” (2003, p. 14). Subsequent to the

development of Bitcoin, multiple alternate crypto-currencies

(often referred to as ‘alt-coins’), have emerged.

Most of these alt-coins have used the Bitcoin open-source code

as their basis, with various modifications. For example,

Zerocoin, which is being developed by researchers at Johns

Hopkins University, was originally conceived as a

“cryptographic extension to Bitcoin that augments the protocol

to allow for fully anonymous currency transactions” (Garman et

4

al, 2013) but it is now being developed as a separate

currency.

In comparison to Bitcoin’s current market capitalization of

approximately USD $10 billion, these complements or

competitors to Bitcoin are much smaller, with Litecoin being

the second largest alt-coin at almost USD $600 million market

capitalization. Bitcoin at present has an entrenched first-

mover advantage as more and more businesses accept it as a

payment method.

Perceived attributes of innovation are important characteristics that

shed light on why innovations are adopted at different rates

(Rogers, 2003).

The relative advantage of an innovation is “the degree to which an

innovation is perceived as better than the idea it supersedes”

(Rogers, 2003, p. 13).

Since its inception Bitcoin has been popular with individuals

in society who are sometimes classified as ‘libertarians’.

Libertarianism is “a political philosophy advocating

protection or expansion of individual rights, especially those

connected with the operation of a free market, and

minimization of the role of the state” (OED, 2014).

In the world view of libertarians, governments in the

developed world have attempted, since 2008 (through various

fiscal and monetary policies of their central banks), to

inflate their way out of economic crises. Witness the

quantitative easing policy (QE3) of the Federal Reserve Bank

in the USA, which has injected USD $85 billion of liquidity

5

per month into the American economy since December 2012

(Federal Reserve, 2012).

“When Nakamoto’s paper came out in 2008, trust in the ability of

governments and banks to manage the economy and the money supply was

at its nadir.” (Wallace, 2011).

In this context, Bitcoin – which is not controlled by a

central authority (as the US dollar is by the Federal Reserve)

is seen by some as an improvement on traditional currencies

because it has an in-built deflationary bias (only 21 million

bitcoins will be created on a reducing scale until the year

2140) and it cannot be manipulated by governments with a

political and economic agenda.

Bitcoin has other perceived advantages over government-issued

fiat currencies. Transaction processing fees are significantly

lower than those that are charged by credit card companies

such as Visa and MasterCard, which include (some might say,

excessive) premiums in their rates to account for fraud

protection and to allow for eventualities such as customer

chargebacks. Bitcoin transactions are not reversible (caveat

emptor) and therefore negate the need for chargeback

facilitation, although entrepreneurial start-up businesses in

the Bitcoin space are presently devising various methods to

provide more protection to individuals (both buyers and

sellers) using Bitcoin to trade goods and services.

Additionally, firms that facilitate international remittances,

such as Western Union and MoneyGram also charge much higher

fees than Bitcoin to transfer money from one country to

6

another, especially from rich nations to the developing world.

Indeed, it is estimated that these firms make profits of USD

$70 billion on these remittances, from some of the poorest

people on the planet – money which could be used in the

developing world for societal improvement. Therefore from this

perspective the potential of Bitcoin seems apparent.

Compatibility is the “degree to which an innovation is perceived

as being consistent with the existing values, past

experiences, and needs of potential adopters” (Rogers, 2003,

p. 15).

Bitcoin has been associated in the public domain with illegal

activity, particularly in relation to the notorious online

market for illicit products and services, known as ‘The Silk

Road’ which was closed down by the FBI in late 2013. Despite

the fact that this event caused the price of Bitcoin on global

exchanges to temporarily dip by approximately 8% (Randewich,

2013), in most quarters the termination of the Silk Road

website was seen as a positive development for Bitcoin insofar

as it enabled the digital currency to distance itself from

such activity.

Moreover, it has also been argued by Bitcoin advocates and

even government officials that traditional cash remains the

most popular method of transacting the proceeds of criminal

enterprise. A representative named Jennifer Shasky Calvery,

from the Financial Crimes Enforcement Network (FinCEN) - a law

enforcement agency of the Treasury Department appeared at a

7

Senate hearing about Bitcoin on 18th Nov. 2013 and testified

that:

“Any financial institution could be exploited for money

laundering purposes. While of growing concern, to date,

virtual currencies have yet to overtake more traditional

methods to move funds internationally, whether for

legitimate or criminal purposes”.

Nevertheless, these negative associations do appear to persist

for the time being in the public consciousness and are at odds

with mainstream norms and values. Bitcoin and other alt-coins

will need to work hard to dispel such negative connotations in

order to achieve wider acceptance and adoption.

However, on the positive side from Bitcoin’s perspective,

public disillusionment with the role of banks in precipitating

the financial and economic crisis of the past 6 years, the

numerous scandals that banks have been involved in (e.g. LIBOR

interest rate-rigging scandal; HSBC laundering of Mexican drug

cartel money; JP Morgan involvement in the Madoff pyramid

scheme) and widespread anger at the ongoing and excessive

bonus culture of banking executives may have created an

environment where people might consider the adoption of

Bitcoin usage in place of using the services of discredited

banking institutions.

Complexity is “the degree to which an innovation is perceived as

difficult to understand and use” (Rogers, 2003, p. 16). The

simpler an innovation is, the more rapidly it will be adopted.

Bitcoin is perceived by many people as being too complicated

8

for them to understand, particularly because of its origins in

computer science and cryptography. However, in reality, the

operation of a Bitcoin account (referred to as an online

‘wallet’) is no more complex (and is in many ways simpler)

than the operation of an online banking account.

One prominent Bitcoin evangelist has dismissed the

innovation’s complicated nature, saying: “You don’t know how

every nut and bolt work on a car, but you can still drive”

(Sidel, 2014).

The same evangelist predicts that “2014 will be like the

Industrial Revolution for bitcoin” (Sidel, 2014).

In 2010, a ‘Consumer Billing and Payment Trends’ study

reported that almost 72.5 million American households used

online banking (McKenna, 2010) while in 2012 it was revealed

that 21% of mobile phone users in the USA accessed their bank

accounts through their mobile devices (Federal Reserve, 2012).

Therefore the potential market for Bitcoin adoption is

evidently gigantic. However, Bitcoin must improve and market

its public image, should understate its association with

computer science and should improve its customer-facing

features to become more user-friendly – all of which might

encourage wider adoption by the public.

Another concern that is frequently raised is the threat of

computer or phone hacking, which could be directed at

individual users’ desktop wallets (e.g. through the use of

malware) or at online wallet providers and Bitcoin exchanges.

Several high profile online thefts of Bitcoin have attracted

9

media attention and stoked public fears about security.

However, the Bitcoin protocol in its own right has withstood

security breaches and hacking attempts (Kaminsky, 2013).

Trialability is the “degree to which an innovation may be

experimented with on a limited basis” (Rogers, 2003, p. 16).

The adoption rate of an innovation will be faster if

individual users can try it out to a certain extent and learn

about its features and benefits by actually using it.

It is extremely easy to set up a Bitcoin wallet through one of

the numerous online providers (e.g. www.blockchain.info). The

prospective user is simply required to enter a valid email

address, a password and a captcha code (to verify the presence

of a real person as opposed to any form of automated software,

i.e. a ‘bot’). It is not even necessary to offer a physical

address or proof of identity – in contrast to online banking

stipulations.

Wallet holders then have three ways in which they can acquire

Bitcoin: (1) through Bitcoin mining which has become the

preserve of supercomputers or super networks of computers (so-

called ‘mining pools’), due to the large amount of processing

power needed to ‘discover’ new Bitcoin blocks; (2) by

receiving bitcoins from third parties as gifts, or as payment

for goods and services; and, (3) through buying bitcoins from

exchanges such as BitBargain (www.bitbargain.co.uk) or Eircoin

(www.eircoin.net) in Ireland. It is possible to buy Bitcoin up

to various monetary limits (depending on the particular

exchange) without supplying identification to the exchange;

10

however larger purchases and ‘cashing-out’ of Bitcoin by

selling do require identity verification steps.

Nevertheless individuals can easily set up as many Bitcoin

wallets as they want and a wallet can contain an unlimited

number of Bitcoin addresses (public keys) in the form of an

identifier of 27 - 34 alphanumeric characters (Bitcoin.org,

2014).

In terms of actually managing a Bitcoin wallet and processing

transactions, similarities can be founds with online banking,

as mentioned previously and should pose no major problem to

the modern consumer, while more and more user-friendly

features continue to be added to the Bitcoin network. Bitcoin

allows micropayments of as little as 1 cent which is a

convenient way for individuals to practice – they can even

send small amounts from one address to another in the same

Bitcoin wallet. Therefore the Bitcoin network appears to pass

the test of trialability - once the common initial reluctance

of individuals to try out new technology is overcome.

Observability is the “degree to which the results of an innovation

are visible to others” (Rogers, 2003, p. 16). Bitcoin has

attracted significant media attention in the past year. In

December 2013 the BBC News website reported the following:

“Searching for “bitcoin” across all English language news

brought up 2,631 articles in November. This is up from 41 in

January this year. In online media and in blogs, Bitcoin

came up 14,179 times in November in the US alone - up from

11

187 times in January, according to PR software company

Cision UK.” (Barford, 2013).

In addition to media coverage, Bitcoin has also propagated

through word of mouth, especially among members of the

technology community and this type of diffusion can be far

more impactful than mass media coverage, as will be discussed

below in a section on communication. Indeed, numerous friends

and acquaintances of this researcher have purchased small

amounts of Bitcoin in recent months.

Furthermore, local organizations have sprung up in cities

worldwide to promote the Bitcoin agenda. For example, in

Ireland the Irish Bitcoin Foundation

(http://www.bitcoinirl.ie/) and Bitcoin Dublin

(http://www.meetup.com/Bitcoin-Dublin/) hold regular events,

meetings and tutorial sessions which are advertised online and

are open to new members.

Reinvention is defined as the “degree to which an innovation is

changed or modified by a user in the process of adoption and

implementation” (Rogers, 2003, p. 17). Diffusion theory,

developed from empirical studies, has shown that the more

flexible an innovation is, the quicker its adoption will

occur.

Bitcoin’s source-code is open and freely available but it is

beyond the capabilities of most normal consumers to modify or

customize the software. However, many individuals with

programming experience have altered Bitcoin’s original code to

enable the development of other digital currencies (alt-

12

coins), as mentioned above. Some of these alt-coins may offer

genuine improvements on Bitcoin (for instance, QuarkCoin

boasts of being more secure with faster confirmation times)

while others are accused of being ‘pump-and-dump’ vehicles

attracting speculators looking for quick profits. Yet more

alt-coins appear to be nothing more than gimmicks – for

example, Dogecoin is named after a dog-related internet meme,

while Coinye West takes its name (without permission) from an

American rapper musician.

Taking the concept of reinvention a step further, in the near

future it is envisaged that the Bitcoin platform will evolve

beyond its current state as a currency (or asset, or

commodity) protocol to offer additional capabilities. Work has

already commenced on the development of overlay protocols

which utilise the ability of the Bitcoin network to enable the

achievement of consensus on a distributed ledger of assets.

Such a network would allow decentralized, distributed, peer-

to-peer management of a myriad of assets including bonds,

stocks, legal documents, other currencies and more. In this

sense the Bitcoin currency can be seen as merely the first

application (or ‘app’) on such an evolving network.

The spread of Bitcoin globally has also lead to secondary

innovation such as the development of Bitcoin ATMs (sometimes

referred to as ‘BTMs’) by a number of firms including

Robocoin, Lamassu and Genesis1. Another exciting potential use

for Bitcoin could be in spam prevention. Micropayments of a

hundredth of a cent or less, enabled by Bitcoin could be

initiated between the sender and receiver of an email. In this

13

way only those individuals who are willing to ‘pay’ to send

(or receive) email from other entities would be able to

transmit Bitcoin-verified emails. On a large scale this would

be an uneconomic option for mass spammers (who send tens of

millions of emails concurrently) and perhaps drive them out of

business.

2. Communication:

Communication is the “process by which participants create and

share information with one another in order to reach a mutual

understanding” (Rogers, 2003, p. 18).

Rogers describes a particular form of communication that is

known as diffusion –whereby information is exchanged that

relates to a new idea. He outlines the particular stages of

diffusion communication in detail.

Information relating to an innovation is transferred from one

entity (who has knowledge or experience of the innovation) to

another entity who does not, through one or more communication

channels, and this process is instrumental in deciding whether

or not the innovation will diffuse.

Although mass media communication channels such as newsprint

and TV can have relevance in terms of creating awareness of

innovations on a large scale, it has been shown by diffusion

studies that inter-personal channels are more effective in

encouraging individuals to actually accept a new idea.

In the age of the Internet this approach has been particularly

significant. For instance, social media platforms such as

14

Facebook, LinkedIn and others can exploit a vast amount of

personal data that they have accumulated in relation to their

users. This enables marketers on these websites to create

customized and highly-targeted advertisements which are

presented as recommendations and suggestions to users from

their own personal network of contacts, with resultant higher

rates of engagement and effectiveness as measured by social

media metrics.

Homophily and heterophily are opposing terms. The former refers to

the degree to which interacting people are similar in terms of

their background, education, socio-economic status, etc.,

while the latter is defined as the degree to which individuals

are different in these attributes.

Rogers (2003) has commented that communication is more likely

to be effective and rewarding when two or more individuals are

homophilous. This allows more information to be imparted from

one individual to another as they share common ground in terms

of location, education, interests or other variables.

Heterophilous communication is more difficult because two or

more entities may have trouble understanding each other.

However it is desirable that some degree of heterophily be

present, at least in relation to the innovation itself,

because this will allow an information exchange to take place

and the innovation to propagate.

Early adopters of Bitcoin have shown a high degree of

homophily.

15

“Bitcoin’s earliest adopters were libertarians, cryptographers, and coders attracted

by the idea of money that could operate without government oversight. They liked

the idea that people could exchange bitcoins without knowing or trusting one

another.”(Simonite, 2013).

However, in more recent months, it has been reported that

Bitcoin has been “gaining traction outside its existing

community of enthusiastic early adopters” (Simonite, 2013), a

development that is not always popular with them, as larger

investors and entrepreneurs become involved - but a necessary

step if the Bitcoin innovation is to realize its full

potential.

3. Time

Rogers (2003) states that the time dimension in an important

factor in the diffusion of an innovation through three

distinct processes. Firstly, the innovation-decision process

occurs when an individual learns of an innovation and decides

to adopt or reject it. Next, an entity’s propensity for

innovativeness is compared to other members by observing how

early or late an innovation is adopted. Finally, the communal

rate of adoption of an innovation over time is measured.

The Innovation Decision Process can be divided into five separate

stages: (1) knowledge; (2) persuasion; (3) decision; (4)

implementation; and (5) confirmation (Rogers, 2003).

As applied to Bitcoin, the following generalizations can be

made. Empirical work to validate these generalizations will be

required at a later date.

16

Knowledge of the Bitcoin innovation was very limited in its

early days. Its pseudonymous creator Satoshi Nakamoto was the

first person to mine a block of 50 bitcoins (the so-called

‘genesis block’) in early 2009 (Wallace, 2011).

“For a year or so, his creation remained the province of a tiny group of early

adopters” (Wallace, 2011).

However, as mentioned above, Bitcoin has now attracted

significant media attention, of both a positive and negative

nature. Overall though, the number of users remains low in

volume with enormous scope for further mass participation,

which leads many commentators to opine that Bitcoin is still

in the early adoption phase of the diffusion S-curve, although

this opinion has not been confirmed with academic rigour.

Persuasion occurs when an individual seeks out inter-personal

sources to appraise the advantages and disadvantages of an

innovation which will lead to a decision on whether to adopt

it or not. Mass-media information assumes less importance at

this stage because it is too general in scope and the

potential adopter usually wishes to receive specific details

from a trusted peer.

Adoption may then take place but this decision could later be

reversed (discontinuance) – sometimes with disastrous

consequences in the case of Bitcoin. For example, in 2013, it

was reported that a Welsh early-adopter had forgotten about

7,500 bitcoins mined in 2009 and had disposed of the computer

containing them in a landfill site. The bitcoins had then

appreciated in value to approximately GBP £4 million (Hern,

17

2013). The man had not followed through to the implementation

stage. Conversely a Norwegian man also forgot about his own

early-mined bitcoins but found they were worth nearly USD $1

million when he rediscovered them last year (Gibbs, 2013).

Here we would expect to see confirmation of the innovation-

decision process.

Innovativeness is “the degree to which an individual or other unit

of adoption is relatively earlier in adopting new ideas than

the other members of a system” (Rogers, 2003).

As illustrated previously, and established by diffusion

research, members of a system who have a similar background in

terms of socio-economic status, education and the like will

tend to fall into the same adopter categories, namely: (1)

innovators; (2) early adopters; (3) early majority; (4) late

majority; and (5) laggards.

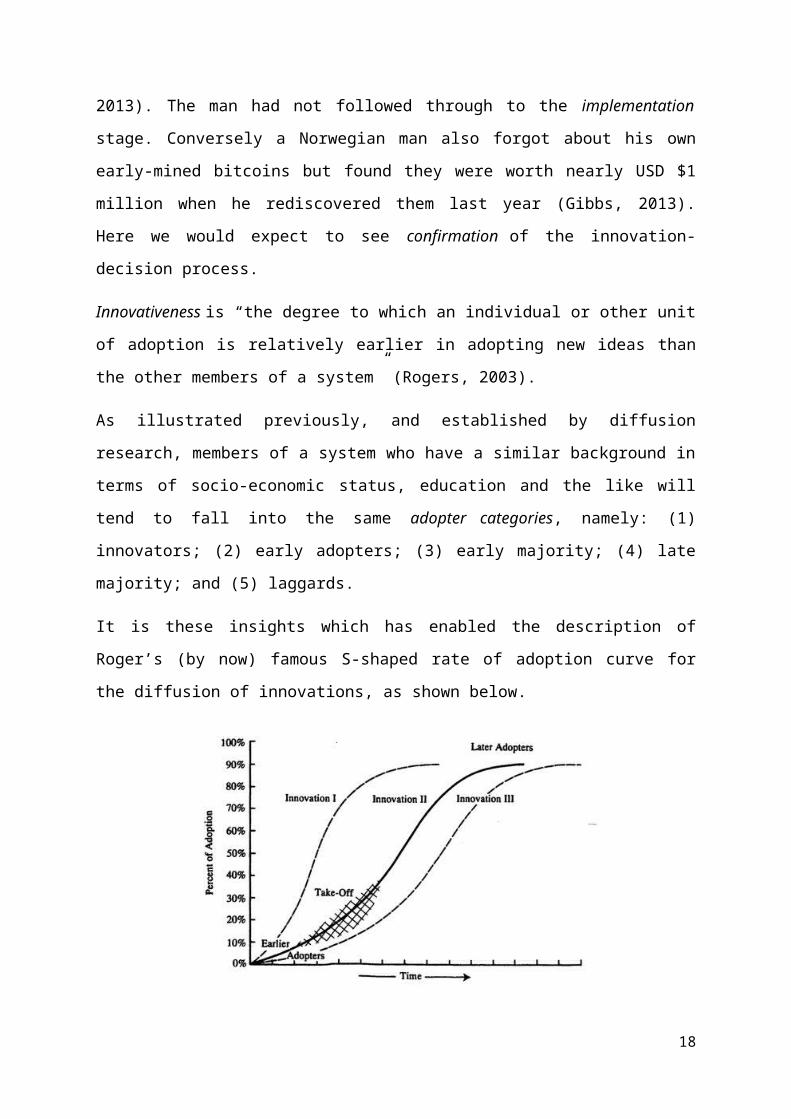

It is these insights which has enabled the description of

Roger’s (by now) famous S-shaped rate of adoption curve for

the diffusion of innovations, as shown below.

18

Figure 1. The Diffusion Process (Rogers, 2003)

A major part of this study in the future will involve

empirically testing as to whether Roger’s S-shaped curve can

indeed be applied to the diffusion of the Bitcoin innovation,

and, if it can, to subsequently establish with as much

precision as possible (by way of quantitative or qualitative

methods, where appropriate) the position that it occupies on

the S-shaped curve.

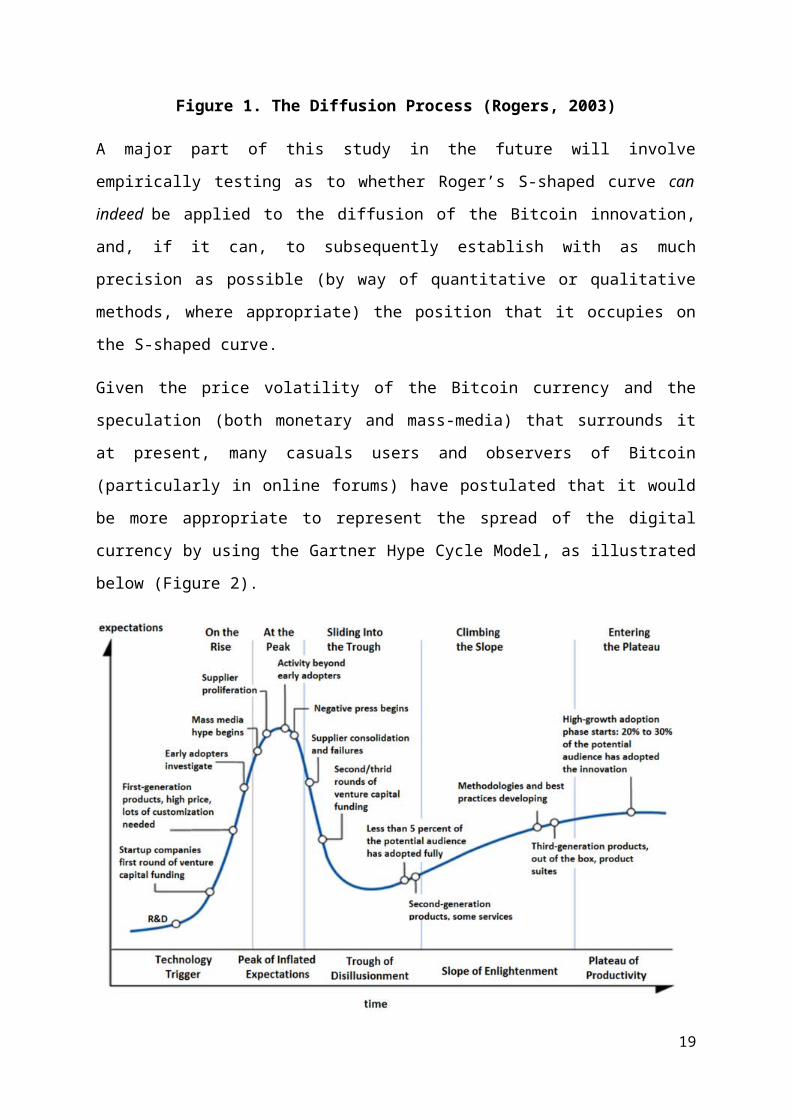

Given the price volatility of the Bitcoin currency and the

speculation (both monetary and mass-media) that surrounds it

at present, many casuals users and observers of Bitcoin

(particularly in online forums) have postulated that it would

be more appropriate to represent the spread of the digital

currency by using the Gartner Hype Cycle Model, as illustrated

below (Figure 2).

19

Figure 2. The Gartner Hype Cycle Model (Source: Wikipedia.com)

This model was developed by the Gartner firm and it envisages

the life cycle of a technological innovation through five

phases. At first a technological breakthrough occurs (e.g.

Nakamoto’s conceptualization of the double-spend solving block

chain) and stories of success and failure are evident (e.g.

the enrichment of early-adopters and the media frenzy over

Bitcoin). Some pioneering companies will adopt the new

technology (e.g. Overstock.com and Virgin Galactic) but others

will react with indifference or hostility (e.g. China

restricted the use of Bitcoin (Bloomberg, 2013) while Apple

Inc. removed Bitcoin applications from its AppStore (Stampler,

2013)).

Antecedent to the achievement of widespread acceptance

(applicable to Bitcoin presently) the Gartner Hype Cycle Model

anticipates disillusionment and decline (temporary or

terminal). Eventually, if the innovation survives and becomes

more widely understood, investment, enterprise and industry

expansion can occur leading to mainstream adoption. Bitcoin

may be entering this phase as venture capitalists begin to

invest (e.g. USD $25 million into Coinbase, an exchange

operator) and representatives from Silicon Valley and Wall

Street take notice.

It should be noted that the Gartner Hype Cycle Model has been

criticised for not being sufficiently scientific or academic

(Mortier, 2012) and further consideration and development of

20

the model, as well as additional analysis and theory would

appear to be required here.

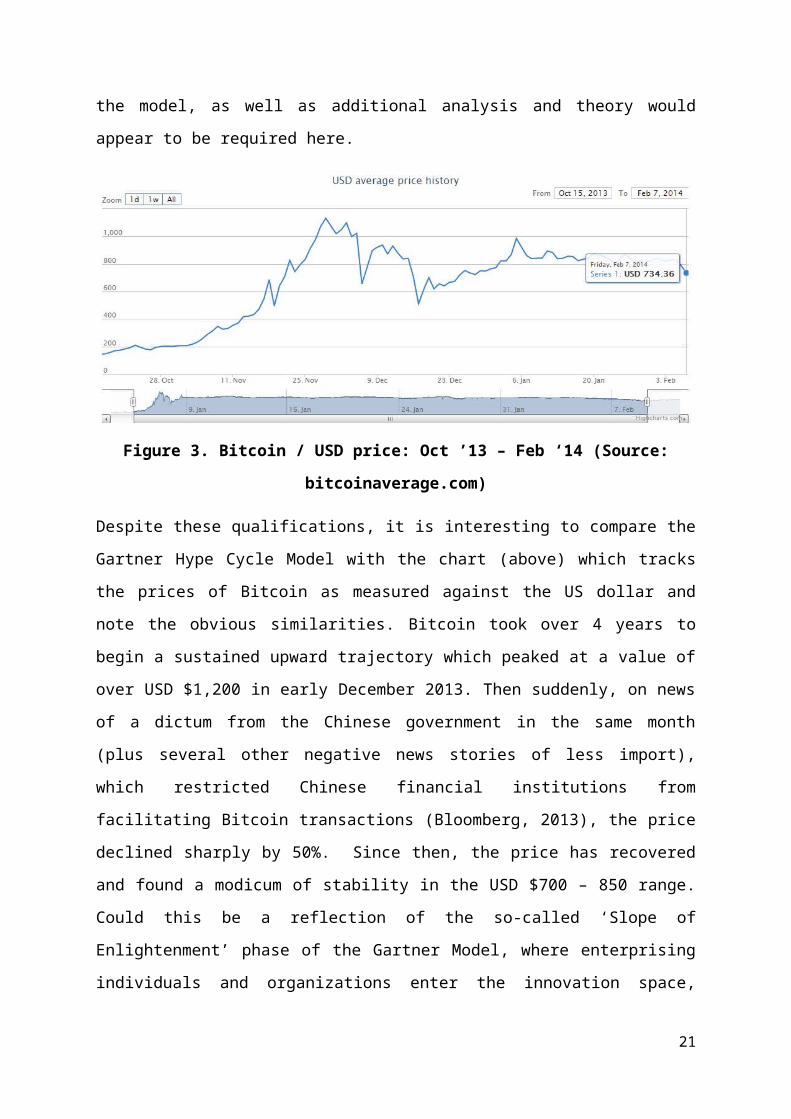

Figure 3. Bitcoin / USD price: Oct ’13 – Feb ‘14 (Source:

bitcoinaverage.com)

Despite these qualifications, it is interesting to compare the

Gartner Hype Cycle Model with the chart (above) which tracks

the prices of Bitcoin as measured against the US dollar and

note the obvious similarities. Bitcoin took over 4 years to

begin a sustained upward trajectory which peaked at a value of

over USD $1,200 in early December 2013. Then suddenly, on news

of a dictum from the Chinese government in the same month

(plus several other negative news stories of less import),

which restricted Chinese financial institutions from

facilitating Bitcoin transactions (Bloomberg, 2013), the price

declined sharply by 50%. Since then, the price has recovered

and found a modicum of stability in the USD $700 – 850 range.

Could this be a reflection of the so-called ‘Slope of

Enlightenment’ phase of the Gartner Model, where enterprising

individuals and organizations enter the innovation space,

21

while more conservative entities remain cautious? At present

this question cannot be answered with any degree of certainty

and requires further study.

The rate of adoption of an innovation is “the relative speed with

which an innovation is adopted by members of a social system”

(Rogers, 2003, p. 23).

Rogers and others have observed that most innovations, across

many disciplines, follow the S-shaped curve of adoption as

discussed above. Different innovations propagate at different

rates and the speed of adoption is influenced by many factors.

The rate of adoption of the Bitcoin innovation is unclear and

any estimate of same is based on the frequency and volume of

mass-media coverage as well as anecdotal evidence. Little

academic work has been undertaken to date but will be required

in the near future.

4. Social System

Rogers defines a social system as “a set of inter-related

units that are engaged in joint problem solving to accomplish

a common goal” (2003, p. 23).

In studying the Bitcoin system, analysis can be undertaken of

individual units who might accept and use the innovation –

potentially 5 billion + people (excluding small children) on a

global scale. Additionally it is conceivable that millions of

organizational entities such as governments, corporations and

private businesses will also use the protocol in the future.

22

Bitcoin is a decentralized system: it is not controlled by a

central authority. In order for changes or additions to be

made to the protocol (by a small group of lead developers) or

for agreement on the rules and transaction history of the

network, the consensus of the Bitcoin community is required

(Felten, 2013). This is unusual as compared to many systems

where structures and boundaries are more clearly defined. The

nature of structures and boundaries has an impact on how

diffusion occurs within a system and more work is required

here in relation to Bitcoin.

Rogers defines structure as “the patterned arrangements of the

units in a system” (2003, p. 24) and notes that structures can

be formal (e.g. such as the Irish Bitcoin Foundation, of which

this researcher is a member) or informal in terms of

interpersonal relationships where diffusion in a network is a

social process affected by the strength of ties between

members (e.g. homophilous friends recommending Bitcoin to one

another).

Norms are the “established behaviour patterns for the members

of a social system” (Rogers, 2003, p. 26) and it has been

shown in diffusion studies that they have an important

influence on the rate of adoption of innovations. There has

been little academic investigation into the norms of the

Bitcoin system and its sub-systems. Presently, political and

regulatory institutions are considering whether and how they

should become involved in regulating the Bitcoin economy.

23

From the point of view of individuals, honesty is an important

norm that is generally practised – for example, because

Bitcoin transactions are irreversible, the principle of caveat

emptor (buyer beware) prevails (although a buyer can at least

try asking for a refund if dissatisfied). However, there have

also been numerous reported instances of Bitcoin fraud, theft

etc. where norms have been broken. More research is required

here.

Opinion leadership is the “degree to which an individual is able to

influence other individuals’ attitudes or overt behaviour

informally in a desired way with relative frequency” (Rogers,

2003, p. 27). Opinion leaders are not appointed in a formal

sense but their professional and social skills, as well as

their networked connections enable them to lead or oppose the

diffusion of an innovation. Words including ‘evangelist’ and

‘proselytizer’ are frequently invoked to describe prominent

Bitcoin enthusiasts who have been involved since the early

days in promotion of the innovation. These individuals may not

actually be the most innovative original devotees because that

type of person tends to be viewed as too specialist in the

public perception (Rogers, 2003).

In the wider global debate around Bitcoin several well-known

public figures have expressed strong opinions on either side.

In November 2013, Richard Branson, the influential founder of the

Virgin Group announced in a very positive blog post that the

Virgin Galactic arm of his empire would begin accepting

bitcoins for payment on its proposed low level space flights

(Virgin, 2013).

24

Early in 2014, American firm Overstock, with an annual

turnover of USD $1.3 billion became the largest online

retailer to implement Bitcoin as a payment option. The CEO of

Overstock, Patrick Byrne, an enthusiastic Bitcoin believer, was

the inspiration behind this move. The company realized sales

of approximately USD $130,000 in bitcoins from 840 new

customers on the first day of trading. Byrne later suggested

that larger online enterprises such as Amazon will ultimately

have to integrate Bitcoin into their business models

(Weisenthal, 2014).

Many conventional economists are opponents of Bitcoin and

consider the digital currency component of the platform to be

nothing more than a pyramid or ‘Ponzi’ scheme. For instance

New York Times columnist Paul Krugman wrote an article in

January 2013 with the headline “Bitcoin is Evil” (Krugman,

2013) while former Chairman of the Federal Reserve Alan

Greenspan has called Bitcoin a “speculative bubble with no

intrinsic value” (Tadeo, 2013). It should be pointed out that

Krugman was the economist who commented in 1998 that “By 2005

or so, it will become clear that the Internet's impact on the

economy has been no greater than the fax machine” (Krugman,

1998).

A change agent is “an individual who influences clients’

innovation-decisions in a direction deemed desirable by a

change agency”. These individuals will typically have a

technical background which may cause communication issues

people who are recently exposed to a new innovation but this

obstacle may be overcome by the use of a change aide who will

25

help to translate the innovation’s message to enable wider

understanding and use (Rogers, 2003).

Presently, computer security expert Andreas Antonopolous is

viewed by many people as the most high-profile and effective

change agent for Bitcoin in the world. He travels the world

constantly to attend conferences, appear on broadcasts and to

meet devotees and businesses that are interested in Bitcoin.

He is also writing ‘The Bitcoin Book’.

Types of innovation-decisions also have an influence on the diffusion

of an innovation and they fall into four categories as

outlined below.

An optional innovation-decision is “made by an individual

independent of the decisions of the other members of the

system” (Rogers, 2003, p. 28). It is estimated that there are

approximately 1 million + users of Bitcoin worldwide

(McMillan, 2013) although precise statistics in the public

domain do not exist at this juncture. These users have made

their own choices to adopt the innovation, whether that be

through mining activity, by offering exchange services, for

speculation as an asset-class, as a store of value, as a

medium of exchange or by setting up their businesses to accept

it as a payment method. Nevertheless, as has been discussed,

the individual adopter will be influenced by others in the

social system in making the decision to adopt.

Collective innovation-decisions are made in a system by consensus

among its members. Some small enterprises may have privately

26

made this type of decision in regard to adopting Bitcoin (or

not) but it has not been evidenced on a large scale to date.

Authority innovation-decisions are made by individuals in

positions of power, status or technical expertise (Rogers,

2003) and are imposed on the rest of the members of a system

or sub-system. These types of decisions have been mainly

negative so far in relation to Bitcoin. For instance, Apple

Inc. has unilaterally restricted its users from installing

Bitcoin applications on their iPhones without consultation

(Stampler, 2013) while China ordered financial institutions in

that country to refrain from facilitating Bitcoin transactions

after the Chinese New Year 2014 (Bloomberg, 2013).

Finally, a contingent innovation-decision is a combination of two

or more of the innovation decisions outlined, which occur in a

sequential fashion (Rogers, 2003). For example, some firms are

currently planning to introduce an option for their employees

to be paid in Bitcoin. Indeed, a recent survey indicated that

more than 50% of IT professionals would be interested in

having such an option (Casey, 2014).

Consequences of innovations are “the changes that occur to an

individual or to a social system as a result of the adoption

or rejection of an innovation (Rogers, 2003, p. 30).

Rogers outlines three types of consequences that might be

realized through the adoption of an innovation. A desirable

consequence of Bitcoin would to reduce the cost and to

increase the ease of making international transfers, while an

undesirable one would improve the potential ability of money

27

launderers to move illicit funds around the globe (although

such a consequence is mere speculation – it has not been

proved or disproved to date).

A direct consequence is an immediate response to the adoption of

an innovation – for example, users of Bitcoin, including this

researcher, have lessened their usage of traditional banking

services as the Bitcoin economy has expanded. In the longer

terms indirect consequences of such behaviour might induce a

reallocation of employment resources in the wider economy

should the hegemony of large banks be permanently altered by

Bitcoin.

Anticipated consequences of an innovation are those which are

expected and planned for, while unanticipated consequences emerge

over time and cannot be predicted in advance. It is expected

that crypto-currencies will not disappear and will continue to

have a disruptive effect on the global economy, however the

long-term future of Bitcoin itself is simply unknown at this

point. Analysis, explanation and prediction is urgently

required here.

Conclusion

The Bitcoin network has the potential to be a truly disruptive

innovation. Most of what has been written about the innovative

potential of Bitcoin to date has been published in the mass

media – in-depth analysis from the academic perspective is

severely lacking. It is hoped that this initial attempt in

using Roger’s diffusion of innovations framework is a

28

constructive place to begin in unravelling the intricacies of

Bitcoin, and will lead to further insight as the innovation

continues its seemingly inexorable exponential growth and

evolution.

Bitcoin is more than a mere currency – it is a technological

and social network and Metcalfe’s law in relation to

telecommunications networks (which also invokes the S-shaped

curve of adoption dynamics) states that “the value of a

network goes up as the square of the number of users” (Shapiro

and Varian, 1999, p. 184). Again, this indicates to an

exponential increase in the value of the Bitcoin network as

the rate of awareness, acceptance and adoption increase over

time. A USD $10 billion market capitalization for Bitcoin may

seem trivial to what can be expected in the near future.

Malcom Gladwell, in his book ‘The Tipping Point’ (2000) has

spoken of the point at which an innovation reaches a ‘critical

mass – where beyond a certain point in time, mass adoption of

an innovation occurs and major behavioural changes are

observed in a social system, with consequences that are both

anticipated and unforeseen. Many would argue that the Bitcoin

innovation is fast approaching that point considering the

amount of public and media interest and the level of

investment that is currently being directed into the Bitcoin

space.

Most of the analysis of Bitcoin so far – both academic and

non-academic has focused on its properties from either a

technological point of view (computer science and

29

cryptography, etc.) or as a currency with volatile properties,

attracting speculation from investors. The full potential of

the Bitcoin network as a platform for innovation has yet to

explored, although many entrepreneurial individuals and firms

are currently working feverishly behind the scenes to bring

these new Bitcoin-centric goods and services to the market.

The additional capabilities of the Bitcoin protocol, beyond

its use as a medium of exchange are arguably the most

important and exciting. These involve using the protocol to

achieve consensus on a distributed ledger of assets, allowing

decentralized, distributed, peer-to-peer management of a

myriad of assets – a development that would impact many

industries including financial services, law, and accountancy.

It is anticipated by this researcher, and many others, that

these innovations will have a profound effect on the way we do

business in the modern global economy and academia should be

poised and ready to take advantage of the research

opportunities that will imminently be offered.

30

REFERENCES

1. Barford, V. (2013). Bitcoin: Price v hype. BBC News

[online]. Available at:

<http://www.bbc.co.uk/news/magazine-25332746> [Accessed

on 03 Feb. 2014].

2. Bitcoin (2014). How does Bitcoin work? Bitcoin.org [online].

Available at: <https://bitcoin.org/en/how-it-works>

[Accessed on 03 Feb. 2014].

3. Brito, J. & Castillo, A. (2013). Bitcoin: A Primer for

Policymakers. Mercatus Center. George Mason University

[online]. Available at:

<http://mercatus.org/sites/default/files/Brito_BitcoinPri

mer.pdf> [Accessed on 04 Feb. 2014].

4. Bloomberg (2013). China Bans Financial Companies From

Bitcoin Transactions. Personal Finance [online]. Available

at: <http://www.bloomberg.com/news/2013-12-05/china-s-

pboc-bans-financial-companies-from-bitcoin-

transactions.html> [Accessed on 08 Feb. 2013].

5. Casey, M. J. (2014). Pay Me in Bitcoin, IT Professionals

Say. The Wall Street Journal, 27 Jan. [online]. Available at

<http://blogs.wsj.com/moneybeat/2014/01/27/pay-me-in-

bitcoin-it-professionals-say/> [Accessed on 09 Feb.

2014].

31

6. Federal Reserve (2012). Consumers and Mobile Financial Services

[online]. Available at:

<http://www.federalreserve.gov/econresdata/mobile-

devices/2012-current-use-mobile-banking-payments.htm>

[Accessed on 02 Feb. 2014].

7. Federal Reserve (2012). Press Release [online]. Available

at:

<http://www.federalreserve.gov/newsevents/press/monetary/

20121212a.htm> [Accessed on 02 Feb. 2014].

8. Felten, E. (2013). How Consensus Drives Bitcoin. Freedom

To Tinker blog [online], 4 Jun. Available at:

<https://freedom-to-tinker.com/blog/felten/how-consensus-

drives-bitcoin/> [Accessed on 07 Feb. 2014].

9. Garman, C., Green, M., Miers, I. & Rubin, A. (2013).

Zerocoin: Anonymous Distributed e-Cash from Bitcoin. In

IEEE Symposium on Security and Privacy (Oakland).

10. Gibbs, S. (2013). Man buys $27 of bitcoin, forgets

about them, finds they’re now worth $886k. The Guardian

[online]. Available at

<http://www.theguardian.com/technology/2013/oct/29/bitcoi

n-forgotten-currency-norway-oslo-home> [Accessed on 07

Feb. 2014].

11. Gladwell, M. (2000). The Tipping Point. New York: Little

Brown & Co.

32

12. Hern, A. (2013). Missing: hard drive containing

Bitcoins worth £4m in Newport landfill site. The Guardian

[online]. Available at

<http://www.theguardian.com/technology/2013/nov/27/hard-

drive-bitcoin-landfill-site> [Accessed on 07 Feb. 2014].

13. Kaminsky, D. (2013). Let’s Cut Through the Bitcoin

Hype: A Hacker-Entrepreneur’s Take. Wired [online].

Available at <http://www.wired.com/opinion/2013/05/lets-

cut-through-the-bitcoin-hype/> [Accessed on 05 Feb.

2014].

14. Krugman, P. (2013). Bitcoin Is Evil. The New York Times,

blog [online]. Available at

<http://krugman.blogs.nytimes.com/2013/12/28/bitcoin-is-

evil/> [Accessed on 08 Feb. 2014].

15. Krugman, P. (1998). Why most economists’ predictions

are wrong. The Red Herring, June [online]. Available at

<http://web.archive.org/web/19980610100009/www.redherring

.com/mag/issue55/economics.html [Accessed on 10 Feb.

2014].

16. McKenna, A. (2010). More Consumers Embracing Online

Banking, Bill Pay. American Banker [online]. Available at

<http://www.americanbanker.com/bulletins/-1020520-1.html>

[Accessed on 02 Feb. 2014].

17. McMillan, R. (2014). Apple Yanks World’s Most

Popular Bitcoin Wallet From App Store. Wired [online].

33

Available at:

<http://www.wired.com/wiredenterprise/2014/02/blockchain_

apple/> [Accessed on 08 Feb. 2013].

18. Mourdoukoutas, P. (2013). What Will It Take For

Bitcoin To Cross The Tipping Point? Forbes.com, 27 Nov.

[online].

<http://www.forbes.com/sites/panosmourdoukoutas/2013/11/2

7/what-will-it-take-for-bitcoin-to-cross-the-tipping-

point/> [Accessed on 03 Feb. 2014].

19. Mortier, S. (2012). Bitcoin: entre économie

dangereuse et nouveau. Sécurité Globale, Issue 20, pp.115-

134.

20. OED Online (2010). Oxford English Dictionary [online].

Available at: <http://dictionary.oed.com/> [Accessed on

10 Feb. 2014].

21. Randewich, N. (2013). Bitcoin sinks in value after

FBI busts Silk Road drug market. Reuters [online].

Available at

<http://www.reuters.com/article/2013/10/08/net-us-crime-

silkroad-bitcoin-idUSBRE99113A20131008> [Accessed on 02

Feb. 2014].

22. Rogers, E. (2013). Diffusion of Innovations, 5th ed. New

York, USA: Free Press.

34

23. Shapiro, C. & Varian, H. (1999). Information Rules: A

Strategic Guide to the Network Economy. Boston, USA: Harvard

Business Review Press.

24. Sidel, R. (2014). Hard Times for a Bitcoin

Evangelist. The Wall Street Journal, 5 Feb. [online]. Available

at

<http://online.wsj.com/news/articles/SB100014240527023044

50904579365201803918312?mg=reno64-wsj&url=http://

online.wsj.com/article/

SB10001424052702304450904579365201803918312.html>

[Accessed on 07 Feb. 2014].

25. Simonite, T. (2013). Bitcoin Hits the Big Time, to

the Regret of Some Early Boosters. MIT Technology Review

[online]. Available at

<http://www.technologyreview.com/news/515061/bitcoin-

hits-the-big-time-to-the-regret-of-some-early-boosters/>

[Accessed on 05 Feb. 2014].

26. Stampler, L. (2013). Apple Kills Last Bitcoin App.

Time Magazine, Business & Money [online]. Available at

<http://business.time.com/2014/02/06/apple-bitcoin-

blockchain-app-store/> [Accessed on 07 Feb. 2014].

27. Tadeo, M. (2013). Alan Greenspan blasts Bitcoin as

Beijing moves to ban the virtual currency. The Independent

[online]. Available at:

<http://www.independent.co.uk/news/business/news/alan-

35

greenspan-blasts-bitcoin-as-beijing-moves-to-ban-the-

virtual-currency-8984738.html> [Accessed on 08 Feb.

2014].

28. The Economist (2013). Bitcoin under pressure.

Technology Quarter, Q4 2013, Nov. 30 [online]. Available at

<http://www.economist.com/news/technology-quarterly/21590

766-virtual-currency-it-mathematically-elegant-

increasingly-popular-and-highly> [Accessed on 04 Feb.

2014].

29. Virgin Galactic (2013). Bitcoins in space. Virgin.com

[online]. Available at: <http://www.virgin.com/richard-

branson/bitcoins-in-space> [Accessed on 08 Feb. 2014].

30. Wallace, B. (2011). The Rise and Fall of Bitcoin.

Wired [online]. Available at

<http://www.wired.com/magazine/2011/11/mf_bitcoin/>

[Accessed on 05 Feb. 2014].

31. Weisenthal, J. (2014). OVERSTOCK CEO: Amazon Will Be

Forced To Start Accepting Bitcoin. Business Insider [online].

Available at: <http://www.businessinsider.com/overstock-

bitcoin-2014-1> [Accessed on 08 Feb. 2014].

36

Related Documents