Dr. VICTORIANO MUÑOZ Chairman & CEO, ACERINOX Chairman, ISSF Dr. VICTORIANO MUÑOZ Dr. VICTORIANO MUÑOZ Chairman Chairman & CEO, & CEO, ACERINOX ACERINOX Chairman Chairman , ISSF , ISSF DEVELOPMENT IN THE GLOBAL STAINLESS STEEL INDUSTRY DEVELOPMENT IN THE DEVELOPMENT IN THE GLOBAL GLOBAL STAINLESS STEEL STAINLESS STEEL INDUSTRY INDUSTRY INFACON X 2 nd February, 2004 INFACON X INFACON X 2 2 nd nd February February , 2004 , 2004

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Dr. VICTORIANO MUÑOZChairman & CEO, ACERINOX

Chairman, ISSF

Dr. VICTORIANO MUÑOZDr. VICTORIANO MUÑOZChairman Chairman & CEO, & CEO, ACERINOXACERINOX

ChairmanChairman, ISSF, ISSF

DEVELOPMENT IN THE GLOBAL

STAINLESS STEEL INDUSTRY

DEVELOPMENT IN THE DEVELOPMENT IN THE GLOBAL GLOBAL

STAINLESS STEEL STAINLESS STEEL INDUSTRYINDUSTRY

INFACON X

2nd February, 2004

INFACON X INFACON X

22ndnd FebruaryFebruary, 2004, 2004

10101010thththth INTERNATIONAL FERROALLOYS CONGRESSINTERNATIONAL FERROALLOYS CONGRESSINTERNATIONAL FERROALLOYS CONGRESSINTERNATIONAL FERROALLOYS CONGRESSCape Town, 2Cape Town, 2Cape Town, 2Cape Town, 2----4 February 20044 February 20044 February 20044 February 2004

Ladies and gentlemen,

It is a privilege for me to have the opportunity to address this distinguished audience of ferroalloys producers, South African Associations, International Corporations and friends, in this plenary meeting of your INFACON-X Congress.

I recall now, not without some nostalgia, the first time that I participated in the first INFACON Congress in April 1974. I enjoyed it very much, not only for my ferrosilicon background, but also because it was the first time I visited this fascinating Country, that impressed me deeply from the very beginning. I took that opportunity to visit the already state-of-the-art ferroalloys facilities of South Africa and Zimbabwe and to establish the first ferrochrome contracts for our Gibraltar Camp melting shop, at that time in the final stage of construction.

The subject I have been asked to present to you by Dr. Barcza, “Development in the Global Stainless Steel Industry”, is dearest to me since its content actually involves my whole professional career of almost 43 years fully dedicated to the worldwide stainless steel business.

Before all, I would like to make the statement that I am very optimistic about the future of what is our “changing global stainless steel industry”.

Let me now offer you some parameters that support this optimistic view.

A CHANGING GLOBAL A CHANGING GLOBAL A CHANGING GLOBAL A CHANGING GLOBAL A CHANGING GLOBAL A CHANGING GLOBAL A CHANGING GLOBAL A CHANGING GLOBAL

STAINLESS STEEL INDUSTRYSTAINLESS STEEL INDUSTRYSTAINLESS STEEL INDUSTRYSTAINLESS STEEL INDUSTRYSTAINLESS STEEL INDUSTRYSTAINLESS STEEL INDUSTRYSTAINLESS STEEL INDUSTRYSTAINLESS STEEL INDUSTRY

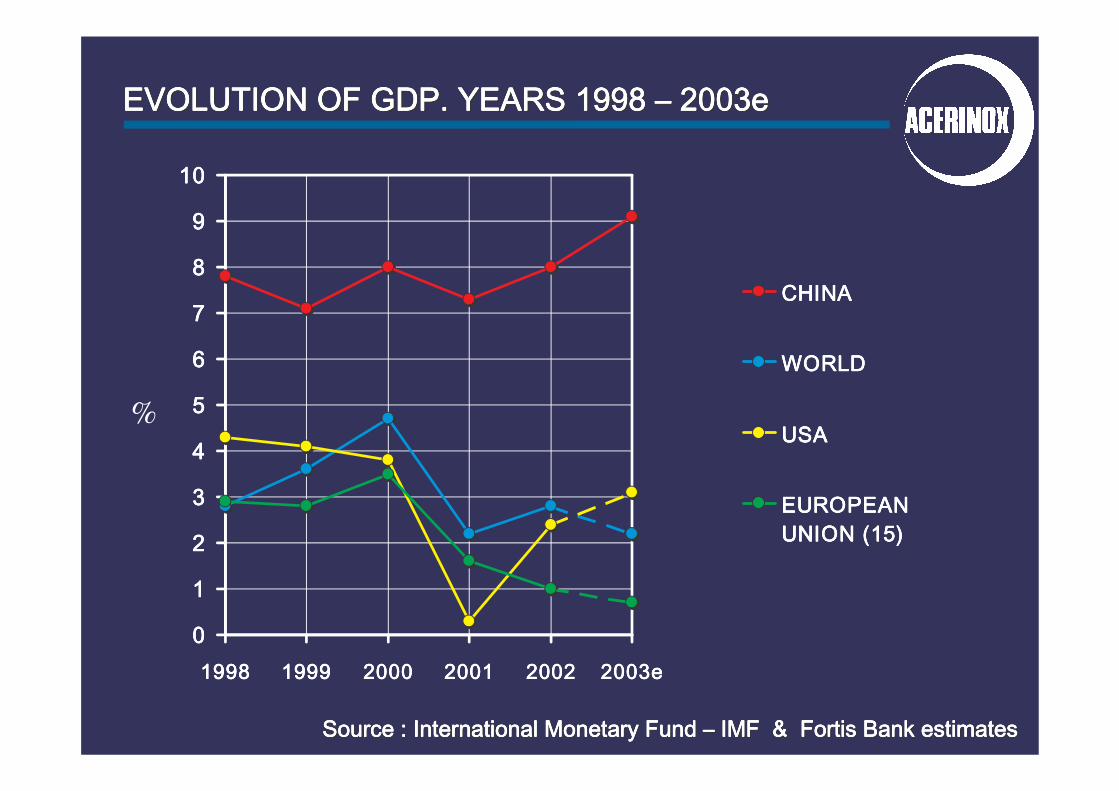

EVOLUTION OF GDP. YEARS 1998 EVOLUTION OF GDP. YEARS 1998 EVOLUTION OF GDP. YEARS 1998 EVOLUTION OF GDP. YEARS 1998 EVOLUTION OF GDP. YEARS 1998 EVOLUTION OF GDP. YEARS 1998 EVOLUTION OF GDP. YEARS 1998 EVOLUTION OF GDP. YEARS 1998 –––––––– 2003e 2003e 2003e 2003e 2003e 2003e 2003e 2003e

SourceSourceSourceSourceSourceSourceSourceSource : : : : : : : : International Monetary FundInternational Monetary FundInternational Monetary FundInternational Monetary FundInternational Monetary FundInternational Monetary FundInternational Monetary FundInternational Monetary Fund –––––––– IMF & IMF & IMF & IMF & IMF & IMF & IMF & IMF & Fortis Bank estimates Fortis Bank estimates Fortis Bank estimates Fortis Bank estimates Fortis Bank estimates Fortis Bank estimates Fortis Bank estimates Fortis Bank estimates

0000

1111

2222

3333

4444

5555

6666

7777

8888

9999

10101010

1998199819981998 1999199919991999 2000200020002000 2001200120012001 2002200220022002 2003e2003e2003e2003e

CHINACHINACHINACHINA

WORLDWORLDWORLDWORLD

USAUSAUSAUSA

EUROPEANEUROPEANEUROPEANEUROPEAN

UNION (15)UNION (15)UNION (15)UNION (15)

%

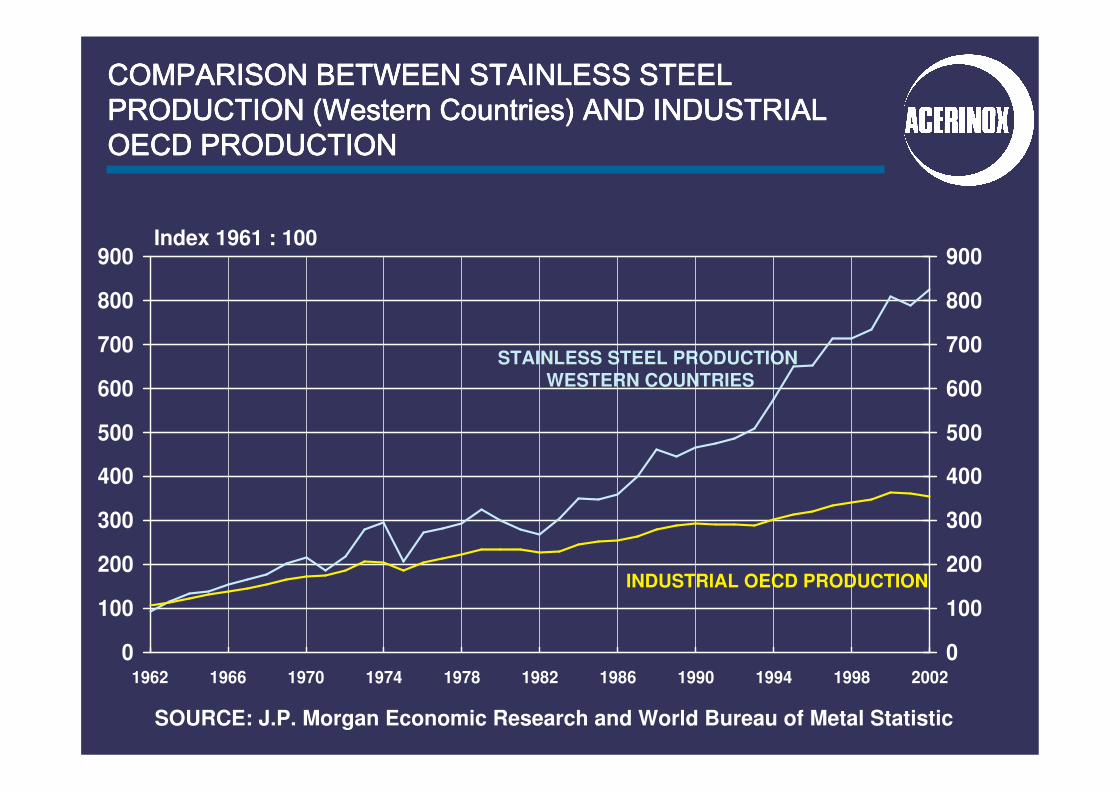

COMPARISON BETWEEN STAINLESS STEEL COMPARISON BETWEEN STAINLESS STEEL COMPARISON BETWEEN STAINLESS STEEL COMPARISON BETWEEN STAINLESS STEEL PRODUCTION (PRODUCTION (PRODUCTION (PRODUCTION (WesternWesternWesternWestern CountriesCountriesCountriesCountries) AND INDUSTRIAL ) AND INDUSTRIAL ) AND INDUSTRIAL ) AND INDUSTRIAL OECD PRODUCTIONOECD PRODUCTIONOECD PRODUCTIONOECD PRODUCTION

STAINLESS STEEL PRODUCTION STAINLESS STEEL PRODUCTION WESTERN COUNTRIESWESTERN COUNTRIES

INDUSTRIAL OECD PRODUCTIONINDUSTRIAL OECD PRODUCTION

SOURCE: J.P. Morgan Economic Research and World Bureau of Metal Statistic

Index 1961 : 100

0

100

200

300

400

500

600

700

800

900

1962 1966 1970 1974 1978 1982 1986 1990 1994 1998 20020

100

200

300

400

500

600

700

800

900

‘000 Mt

STAINLESS STEEL INGOT PRODUCTIONSTAINLESS STEEL INGOT PRODUCTIONSTAINLESS STEEL INGOT PRODUCTIONSTAINLESS STEEL INGOT PRODUCTIONWORLDWORLDWORLDWORLD, 1950 , 1950 , 1950 , 1950 –––– 2003e2003e2003e2003e

Compound Annual Compound Annual Compound Annual Compound Annual Growth Rate Growth Rate Growth Rate Growth Rate

1950195019501950----2003e: + 6.03%2003e: + 6.03%2003e: + 6.03%2003e: + 6.03%

0000

2.0002.0002.0002.000

4.0004.0004.0004.000

6.0006.0006.0006.000

8.0008.0008.0008.000

10.00010.00010.00010.000

12.00012.00012.00012.000

14.00014.00014.00014.000

16.00016.00016.00016.000

18.00018.00018.00018.000

20.00020.00020.00020.000

22.00022.00022.00022.000

24.00024.00024.00024.00024,00024,00024,00024,000

22,00022,00022,00022,000

20,00020,00020,00020,000

18,00018,00018,00018,000

16,00016,00016,00016,000

14,00014,00014,00014,000

12,00012,00012,00012,000

10,00010,00010,00010,000

8,0008,0008,0008,000

6,0006,0006,0006,000

4,0004,0004,0004,000

2,0002,0002,0002,000

00002003e50 60 70 80 90 00

1. 1. 1. 1. OIL OIL OIL OIL CRISISCRISISCRISISCRISIS

2. 2. 2. 2. OIL OIL OIL OIL CRISISCRISISCRISISCRISIS

GULF WARGULF WARGULF WARGULF WAR

ASIAN ASIAN ASIAN ASIAN CRISESCRISESCRISESCRISES

RECESSION 2001RECESSION 2001RECESSION 2001RECESSION 2001

22,50022,50022,50022,50022,50022,50022,50022,500

Doubling every Doubling every Doubling every Doubling every Doubling every Doubling every Doubling every Doubling every ten ten ten ten ten ten ten ten years on years on years on years on years on years on years on years on averageaverageaverageaverageaverageaverageaverageaverage

10.6 mill. Mt.10.6 mill. Mt.10.6 mill. Mt.10.6 mill. Mt.10.6 mill. Mt.10.6 mill. Mt.10.6 mill. Mt.10.6 mill. Mt.

63.3 %63.3 %63.3 %63.3 %63.3 %63.3 %63.3 %63.3 %

2.6 mill. Mt2.6 mill. Mt2.6 mill. Mt2.6 mill. Mt2.6 mill. Mt2.6 mill. Mt2.6 mill. Mt2.6 mill. Mt

15.2%15.2%15.2%15.2%15.2%15.2%15.2%15.2%

STAINLESS STEEL PRODUCT STRUCTURE. STAINLESS STEEL PRODUCT STRUCTURE. STAINLESS STEEL PRODUCT STRUCTURE. STAINLESS STEEL PRODUCT STRUCTURE. STAINLESS STEEL PRODUCT STRUCTURE. STAINLESS STEEL PRODUCT STRUCTURE. STAINLESS STEEL PRODUCT STRUCTURE. STAINLESS STEEL PRODUCT STRUCTURE. YEAR 2002YEAR 2002YEAR 2002YEAR 2002YEAR 2002YEAR 2002YEAR 2002YEAR 2002

Cold Cold Cold Cold Cold Cold Cold Cold rolled flatsrolled flatsrolled flatsrolled flatsrolled flatsrolled flatsrolled flatsrolled flats

Hot Hot Hot Hot Hot Hot Hot Hot rolled flatsrolled flatsrolled flatsrolled flatsrolled flatsrolled flatsrolled flatsrolled flats

Long productsLong productsLong productsLong productsLong productsLong productsLong productsLong products

BerlBerlBerlBerlBerlBerlBerlBerliiiiiiiin, May 2003n, May 2003n, May 2003n, May 2003n, May 2003n, May 2003n, May 2003n, May 2003

3.6 mill. Mt.3.6 mill. Mt.3.6 mill. Mt.3.6 mill. Mt.3.6 mill. Mt.3.6 mill. Mt.3.6 mill. Mt.3.6 mill. Mt.

21.5 %21.5 %21.5 %21.5 %21.5 %21.5 %21.5 %21.5 %

Compound annual growthCompound annual growth 1993 1993 -- 20022002

+6.5 %+6.5 %+6.5 %+6.5 %+6.5 %+6.5 %+6.5 %+6.5 %

+3.2 %+3.2 %+3.2 %+3.2 %+3.2 %+3.2 %+3.2 %+3.2 %

+6.3 %+6.3 %+6.3 %+6.3 %+6.3 %+6.3 %+6.3 %+6.3 %

718718718718

506506506506420420420420

1,1111,1111,1111,1111,1171,1171,1171,1171,1971,1971,1971,197

1,9591,9591,9591,959

480480480480

2,2612,2612,2612,261

288288288288

0000

500500500500

1.0001.0001.0001.000

1.5001.5001.5001.500

2.0002.0002.0002.000

2.5002.5002.5002.500

3.0003.0003.0003.000

3.5003.5003.5003.500

Chi

na/HK

Chi

na/HK

Chi

na/HK

Chi

na/HK

Japan

Japan

Japan

Japan

USA

USA

USA

USA

Italy

Italy

Italy

Italy

Germ

any

Germ

any

Germ

any

Germ

any

Sout

h Kore

a

Sout

h Kore

a

Sout

h Kore

a

Sout

h Kore

a

Taiwan

Taiwan

Taiwan

Taiwan

France

France

France

France

Spai

n

Spai

n

Spai

n

Spai

n

India

India

India

India U

KU

KU

KU

K

Year 2002Year 2002Year 2002Year 2002 Year 1993Year 1993Year 1993Year 1993

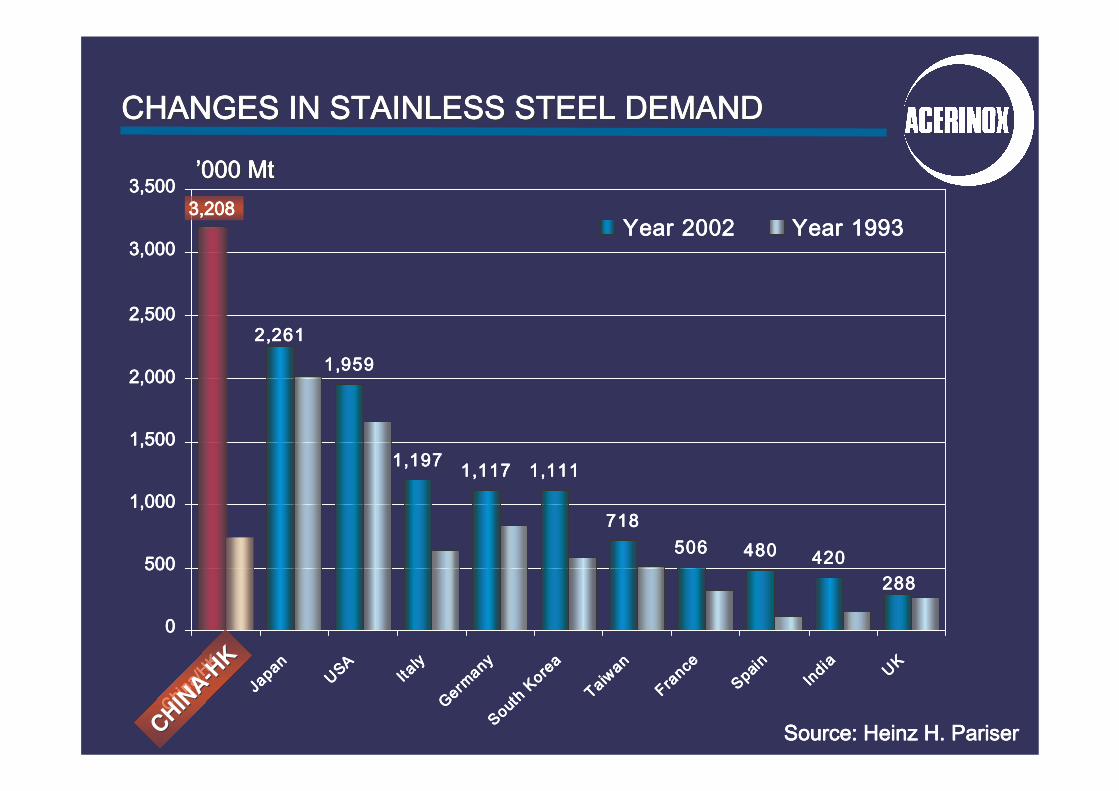

CHANGES IN STAINLESS STEEL DEMANDCHANGES IN STAINLESS STEEL DEMANDCHANGES IN STAINLESS STEEL DEMANDCHANGES IN STAINLESS STEEL DEMANDCHANGES IN STAINLESS STEEL DEMANDCHANGES IN STAINLESS STEEL DEMANDCHANGES IN STAINLESS STEEL DEMANDCHANGES IN STAINLESS STEEL DEMAND

’000 ’000 ’000 ’000 ’000 ’000 ’000 ’000 MtMtMtMtMtMtMtMt

SourceSourceSourceSource: : : : Heinz Heinz Heinz Heinz H. H. H. H. PariserPariserPariserPariser

3,2083,2083,2083,208

CHINA

CHINA--H

KHK

3,5003,5003,5003,500

3,0003,0003,0003,000

2,5002,5002,5002,500

2,0002,0002,0002,000

1,5001,5001,5001,500

1,0001,0001,0001,000

500500500500

0000

7%7%7%7%7%7%7%7%

0000

1.5001.5001.5001.500

3.0003.0003.0003.000

4.5004.5004.5004.500

6.0006.0006.0006.000

7.5007.5007.5007.500

9.0009.0009.0009.000

10.50010.50010.50010.500

12.00012.00012.00012.000

13.50013.50013.50013.500

1990199019901990 1995199519951995 1997199719971997 1998199819981998 1999199919991999 2000200020002000 2001200120012001 20022002200220022003(e)2003(e)2003(e)2003(e)

34%34%34%34%34%34%34%34%

18%18%18%18%18%18%18%18%

41%41%41%41%41%41%41%41%

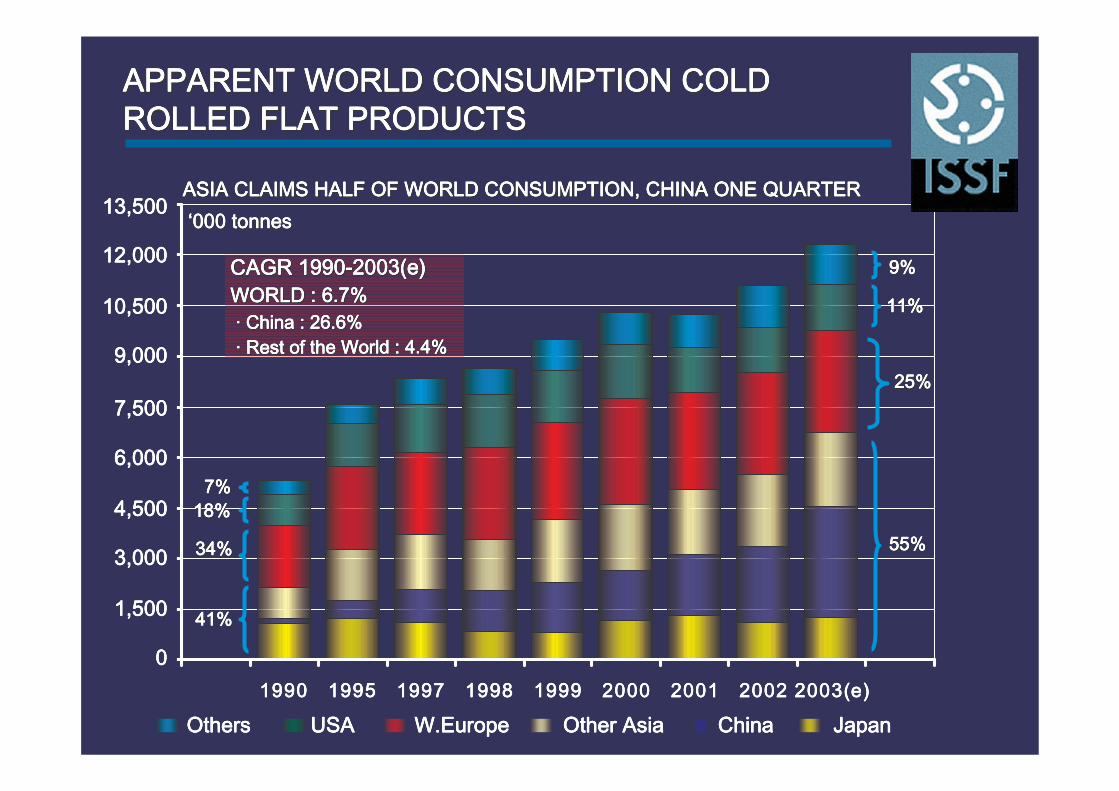

APPARENT APPARENT APPARENT APPARENT APPARENT APPARENT APPARENT APPARENT WORLD WORLD WORLD WORLD WORLD WORLD WORLD WORLD CONSUMPTION COLD CONSUMPTION COLD CONSUMPTION COLD CONSUMPTION COLD CONSUMPTION COLD CONSUMPTION COLD CONSUMPTION COLD CONSUMPTION COLD

ROLLED FLAT PRODUCTSROLLED FLAT PRODUCTSROLLED FLAT PRODUCTSROLLED FLAT PRODUCTSROLLED FLAT PRODUCTSROLLED FLAT PRODUCTSROLLED FLAT PRODUCTSROLLED FLAT PRODUCTS

ASIA CLAIMS HALF OF ASIA CLAIMS HALF OF ASIA CLAIMS HALF OF ASIA CLAIMS HALF OF ASIA CLAIMS HALF OF ASIA CLAIMS HALF OF ASIA CLAIMS HALF OF ASIA CLAIMS HALF OF WORLD WORLD WORLD WORLD WORLD WORLD WORLD WORLD CONSUMPTION, CHINA ONE QUARTERCONSUMPTION, CHINA ONE QUARTERCONSUMPTION, CHINA ONE QUARTERCONSUMPTION, CHINA ONE QUARTERCONSUMPTION, CHINA ONE QUARTERCONSUMPTION, CHINA ONE QUARTERCONSUMPTION, CHINA ONE QUARTERCONSUMPTION, CHINA ONE QUARTER

9%9%9%9%9%9%9%9%

11%11%11%11%11%11%11%11%

25%25%25%25%25%25%25%25%

55%55%55%55%55%55%55%55%

‘000 ‘000 ‘000 ‘000 ‘000 ‘000 ‘000 ‘000 tonnestonnestonnestonnestonnestonnestonnestonnes

Others Others Others Others USA W.USA W.USA W.USA W.Europe Other Europe Other Europe Other Europe Other Asia China Asia China Asia China Asia China JapanJapanJapanJapan

CAGR 1990CAGR 1990CAGR 1990CAGR 1990CAGR 1990CAGR 1990CAGR 1990CAGR 1990--------2003(e)2003(e)2003(e)2003(e)2003(e)2003(e)2003(e)2003(e)

WORLD WORLD WORLD WORLD WORLD WORLD WORLD WORLD : 6.7%: 6.7%: 6.7%: 6.7%: 6.7%: 6.7%: 6.7%: 6.7%

· China : 26.6%· China : 26.6%· China : 26.6%· China : 26.6%· China : 26.6%· China : 26.6%· China : 26.6%· China : 26.6%

· · · · · · · · Rest ofRest ofRest ofRest ofRest ofRest ofRest ofRest of thethethethethethethethe World : 4.4%World : 4.4%World : 4.4%World : 4.4%World : 4.4%World : 4.4%World : 4.4%World : 4.4%

13,50013,50013,50013,500

12,00012,00012,00012,000

10,50010,50010,50010,500

9,0009,0009,0009,000

7,5007,5007,5007,500

6,0006,0006,0006,000

4,5004,5004,5004,500

3,0003,0003,0003,000

1,5001,5001,5001,500

0000

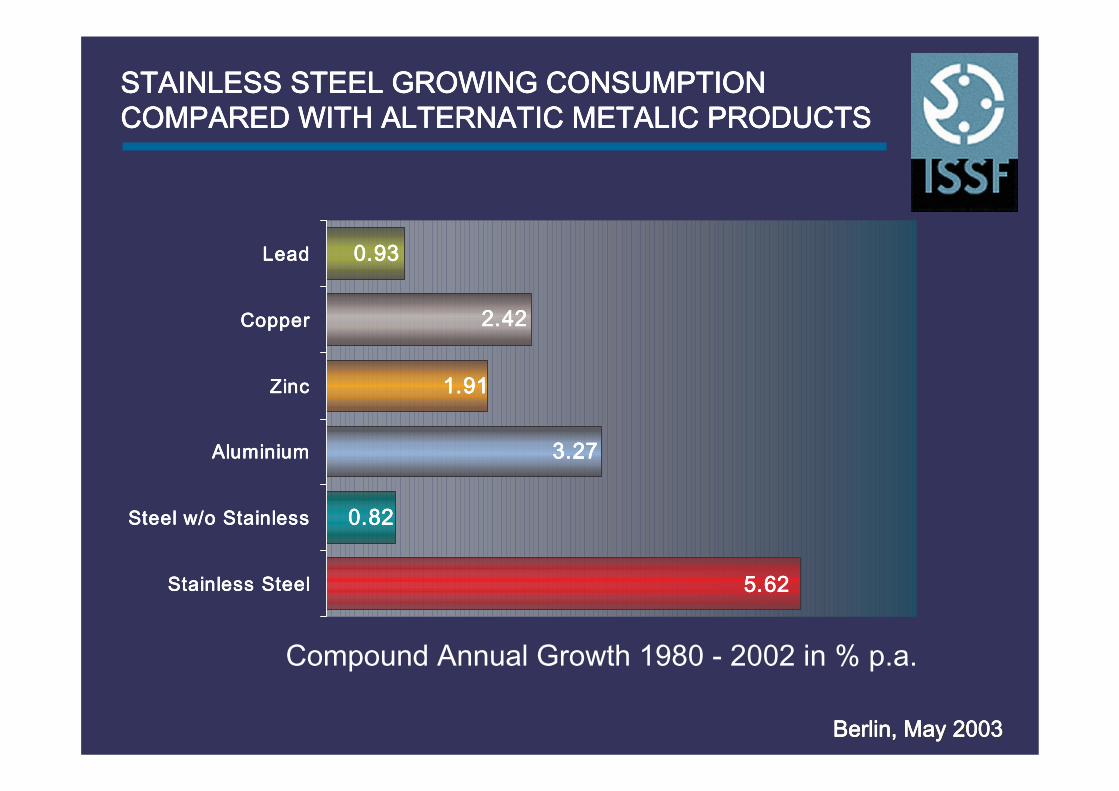

STAINLESS STEEL GROWING CONSUMPTION STAINLESS STEEL GROWING CONSUMPTION STAINLESS STEEL GROWING CONSUMPTION STAINLESS STEEL GROWING CONSUMPTION COMPARED WITH ALTERNATIC METALIC PRODUCTSCOMPARED WITH ALTERNATIC METALIC PRODUCTSCOMPARED WITH ALTERNATIC METALIC PRODUCTSCOMPARED WITH ALTERNATIC METALIC PRODUCTS

BerlinBerlinBerlinBerlinBerlinBerlinBerlinBerlin, May 2003, May 2003, May 2003, May 2003, May 2003, May 2003, May 2003, May 2003

Compound Annual Growth 1980 - 2002 in % p.a.

0.930.930.930.93

2.422.422.422.42

1.911.911.911.91

3.273.273.273.27

0.820.820.820.82

5.625.625.625.62

LeadLeadLeadLead

CopperCopperCopperCopper

ZincZincZincZinc

AluminiumAluminiumAluminiumAluminium

Steel w/o StainlessSteel w/o StainlessSteel w/o StainlessSteel w/o Stainless

Stainless SteelStainless SteelStainless SteelStainless Steel

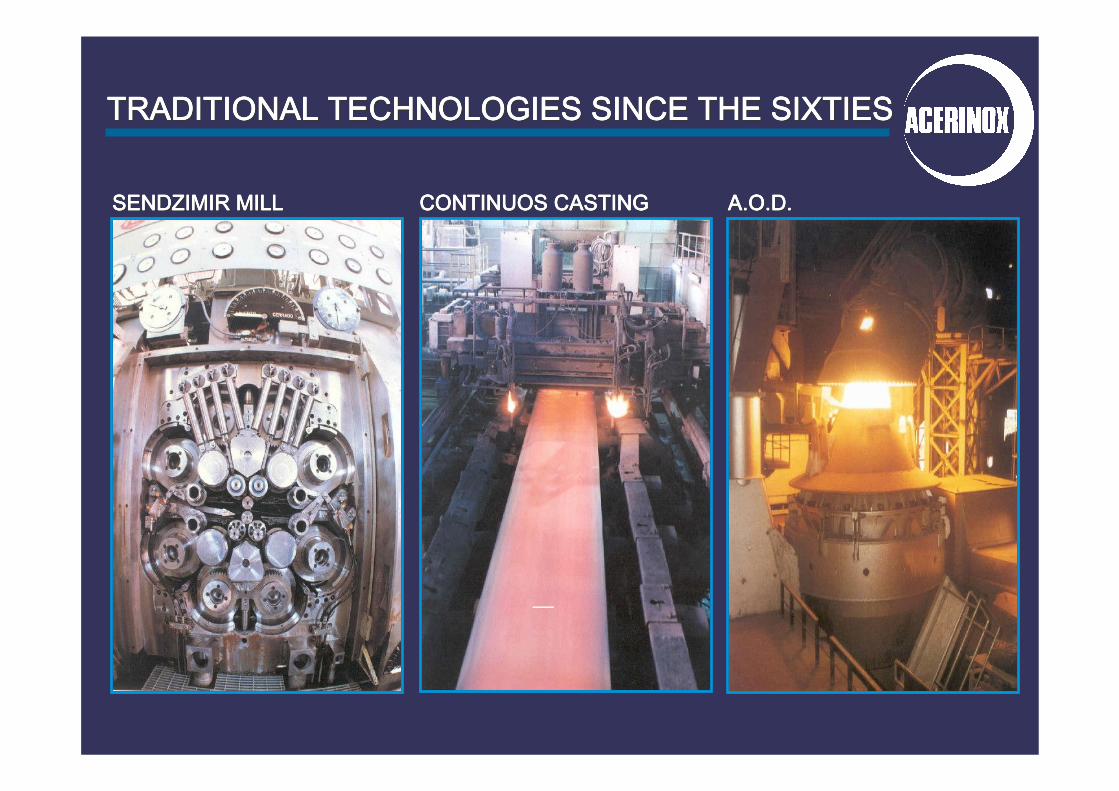

NEW TECHNOLOGIES NEW TECHNOLOGIES NEW TECHNOLOGIES NEW TECHNOLOGIES NEW TECHNOLOGIES NEW TECHNOLOGIES NEW TECHNOLOGIES NEW TECHNOLOGIES

CONTRIBUTION TO THE STAINLESS CONTRIBUTION TO THE STAINLESS CONTRIBUTION TO THE STAINLESS CONTRIBUTION TO THE STAINLESS CONTRIBUTION TO THE STAINLESS CONTRIBUTION TO THE STAINLESS CONTRIBUTION TO THE STAINLESS CONTRIBUTION TO THE STAINLESS

STEEL DEVELOPMENTSTEEL DEVELOPMENTSTEEL DEVELOPMENTSTEEL DEVELOPMENTSTEEL DEVELOPMENTSTEEL DEVELOPMENTSTEEL DEVELOPMENTSTEEL DEVELOPMENT

TRADITIONAL TECHNOLOGIES SINCE THE SIXTIESTRADITIONAL TECHNOLOGIES SINCE THE SIXTIESTRADITIONAL TECHNOLOGIES SINCE THE SIXTIESTRADITIONAL TECHNOLOGIES SINCE THE SIXTIESTRADITIONAL TECHNOLOGIES SINCE THE SIXTIESTRADITIONAL TECHNOLOGIES SINCE THE SIXTIESTRADITIONAL TECHNOLOGIES SINCE THE SIXTIESTRADITIONAL TECHNOLOGIES SINCE THE SIXTIES

SENDZIMIR MILLSENDZIMIR MILLSENDZIMIR MILLSENDZIMIR MILLSENDZIMIR MILLSENDZIMIR MILLSENDZIMIR MILLSENDZIMIR MILL A.O.D.A.O.D.A.O.D.A.O.D.A.O.D.A.O.D.A.O.D.A.O.D.CONTINUOS CASTINGCONTINUOS CASTINGCONTINUOS CASTINGCONTINUOS CASTINGCONTINUOS CASTINGCONTINUOS CASTINGCONTINUOS CASTINGCONTINUOS CASTING

NEW GENERATION STECKEL MILLS NEW GENERATION STECKEL MILLS NEW GENERATION STECKEL MILLS NEW GENERATION STECKEL MILLS NEW GENERATION STECKEL MILLS NEW GENERATION STECKEL MILLS NEW GENERATION STECKEL MILLS NEW GENERATION STECKEL MILLS (YEAR 1985)(YEAR 1985)(YEAR 1985)(YEAR 1985)(YEAR 1985)(YEAR 1985)(YEAR 1985)(YEAR 1985)

NEW DEVELOPMENTS 21NEW DEVELOPMENTS 21NEW DEVELOPMENTS 21NEW DEVELOPMENTS 21NEW DEVELOPMENTS 21NEW DEVELOPMENTS 21NEW DEVELOPMENTS 21NEW DEVELOPMENTS 21stststststststst CENTURYCENTURYCENTURYCENTURYCENTURYCENTURYCENTURYCENTURY

THIN SLABTHIN SLABTHIN SLABTHIN SLABTHIN SLABTHIN SLABTHIN SLABTHIN SLAB STRIPSTRIPSTRIPSTRIPSTRIPSTRIPSTRIPSTRIP CASTERCASTERCASTERCASTERCASTERCASTERCASTERCASTER

R.A.P.R.A.P.R.A.P.R.A.P.R.A.P.R.A.P.R.A.P.R.A.P.

Uncoilers

Welding machine

Pretreatment

Tandem mill

Looper 2

Annealingfurnace Cooling

-Scalebreaker

Shot-Shot-

blasting

-

Looper 3

Looper 4

Coilers

Decreasing

Skin pass/reduction

Levelling

Looper 1

Electrolyticpickling

Mixed-acidpickling

Uncoilers

Welding machine

Pretreatment

Tandem mill

Looper 2

Annealingfurnace Cooling

-Scalebreaker

Shot-Shot-

blasting

-

Looper 3

Looper 4

Coilers

Decreasing

Skin pass/reduction

Levelling

Looper 1

Electrolyticpickling

Mixed-acidpickling

SourceSourceSourceSourceSourceSourceSourceSource: OUTOKUMPU: OUTOKUMPU: OUTOKUMPU: OUTOKUMPU: OUTOKUMPU: OUTOKUMPU: OUTOKUMPU: OUTOKUMPU

SourceSourceSourceSourceSourceSourceSourceSource: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER SourceSourceSourceSourceSourceSourceSourceSource: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER: EUROFER

Transfer Transfer Transfer Transfer

ladleladleladleladle

TundishTundishTundishTundish

UncoilerUncoilerUncoilerUncoiler

60 60 60 60 to to to to 90 mm90 mm90 mm90 mm

Pressing rollsPressing rollsPressing rollsPressing rolls

Tunnel furnaceTunnel furnaceTunnel furnaceTunnel furnace

ShearShearShearShear

20 20 20 20 to to to to 40 mm40 mm40 mm40 mm

Roughing standsRoughing standsRoughing standsRoughing stands

CoilerCoilerCoilerCoiler

1 mm (mini)1 mm (mini)1 mm (mini)1 mm (mini)

CoilerCoilerCoilerCoiler20 20 20 20 to to to to 40 mm40 mm40 mm40 mm

Scale breakerScale breakerScale breakerScale breakerFinishing standsFinishing standsFinishing standsFinishing stands Cooling spraysCooling spraysCooling spraysCooling sprays Teeming ladle Teeming ladle Teeming ladle Teeming ladle = 10t= 10t= 10t= 10t

((((maximum capacity maximum capacity maximum capacity maximum capacity = 90 t)= 90 t)= 90 t)= 90 t)

Extractor Extractor Extractor Extractor rollsrollsrollsrollsPinch rollsPinch rollsPinch rollsPinch rolls

TundishTundishTundishTundish

WaterWaterWaterWater----coled nickelcoled nickelcoled nickelcoled nickel----plated cooper casting rollsplated cooper casting rollsplated cooper casting rollsplated cooper casting rolls((((diameter diameter diameter diameter = 1200 mm, = 1200 mm, = 1200 mm, = 1200 mm, width width width width = 1330 mm)= 1330 mm)= 1330 mm)= 1330 mm)

1,6 1,6 1,6 1,6 to to to to 5,0 mm5,0 mm5,0 mm5,0 mm

StripStripStripStrip((((widthwidthwidthwidth:860 :860 :860 :860 to to to to 1300 mm)1300 mm)1300 mm)1300 mm)

AccumulatorAccumulatorAccumulatorAccumulator----tensiontensiontensiontensionregulatorregulatorregulatorregulator

Rolling millRolling millRolling millRolling mill CoilerCoilerCoilerCoilerCasting speedCasting speedCasting speedCasting speed::::

20 20 20 20 to to to to 130 m/130 m/130 m/130 m/minminminmin

CONSOLIDATION OF STAINLESS CONSOLIDATION OF STAINLESS CONSOLIDATION OF STAINLESS CONSOLIDATION OF STAINLESS CONSOLIDATION OF STAINLESS CONSOLIDATION OF STAINLESS CONSOLIDATION OF STAINLESS CONSOLIDATION OF STAINLESS

STEEL INDUSTRYSTEEL INDUSTRYSTEEL INDUSTRYSTEEL INDUSTRYSTEEL INDUSTRYSTEEL INDUSTRYSTEEL INDUSTRYSTEEL INDUSTRY

CONSOLIDATING STAINLESS STEEL INDUSTRYCONSOLIDATING STAINLESS STEEL INDUSTRYCONSOLIDATING STAINLESS STEEL INDUSTRYCONSOLIDATING STAINLESS STEEL INDUSTRY

Market share of top Market share of top Market share of top Market share of top 5 5 5 5 producersproducersproducersproducers ---- 1997199719971997 Market share of top Market share of top Market share of top Market share of top 5 5 5 5 producersproducersproducersproducers ---- 2000200020002000

Market share of top Market share of top Market share of top Market share of top 5 5 5 5 producersproducersproducersproducers –––– 2003e2003e2003e2003e SOURCE: Deutsche Bank

0%0%0%0%

20%20%20%20%

40%40%40%40%

60%60%60%60%

80%80%80%80%

100%100%100%100%

Pla

tin

um

Pla

tin

um

Pla

tin

um

Pla

tin

um

Dia

mo

nd

sD

iam

on

ds

Dia

mo

nd

sD

iam

on

ds

Iro

n r

reIr

on

rre

Iro

n r

reIr

on

rre

Nic

ke

lN

ick

el

Nic

ke

lN

ick

el

Sta

inle

ss

Sta

inle

ss

Sta

inle

ss

Sta

inle

ss

Ste

el

Ste

el

Ste

el

Ste

el

Co

op

er

Co

op

er

Co

op

er

Co

op

er

Th

erm

al

Th

erm

al

Th

erm

al

Th

erm

al

co

al

co

al

co

al

co

al

Zin

cZ

inc

Zin

cZ

inc

Alu

min

ium

Alu

min

ium

Alu

min

ium

Alu

min

ium

Go

ldG

old

Go

ldG

old

Pa

pe

rP

ap

er

Pa

pe

rP

ap

er

Ca

rbo

nC

arb

on

Ca

rbo

nC

arb

on

ste

el

ste

el

ste

el

ste

el

RAW MATERIALSRAW MATERIALSRAW MATERIALSRAW MATERIALSRAW MATERIALSRAW MATERIALSRAW MATERIALSRAW MATERIALS

16,61016,61016,61016,610

Ending Ending Ending Ending

2003200320032003

3,0003,0003,0003,000

5,0005,0005,0005,000

7,0007,0007,0007,000

9,0009,0009,0009,000

11,00011,00011,00011,000

13,00013,00013,00013,000

15,00015,00015,00015,000

17,00017,00017,00017,000

19,00019,00019,00019,000

OFFICIAL NICKEL PRICE IN L.M.E.OFFICIAL NICKEL PRICE IN L.M.E.OFFICIAL NICKEL PRICE IN L.M.E.OFFICIAL NICKEL PRICE IN L.M.E.OFFICIAL NICKEL PRICE IN L.M.E.OFFICIAL NICKEL PRICE IN L.M.E.OFFICIAL NICKEL PRICE IN L.M.E.OFFICIAL NICKEL PRICE IN L.M.E.((((((((MonthlyMonthlyMonthlyMonthlyMonthlyMonthlyMonthlyMonthly AverageAverageAverageAverageAverageAverageAverageAverage ValuesValuesValuesValuesValuesValuesValuesValues)))))))) JanJanJanJanJanJanJanJan 1980 1980 1980 1980 1980 1980 1980 1980 –––––––– DecDecDecDecDecDecDecDec 20032003200320032003200320032003

80 81 82 83 84 85 86 87 88 89 90 91 80 81 82 83 84 85 86 87 88 89 90 91 80 81 82 83 84 85 86 87 88 89 90 91 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 0392 93 94 95 96 97 98 99 00 01 02 0392 93 94 95 96 97 98 99 00 01 02 0392 93 94 95 96 97 98 99 00 01 02 03

US$/US$/US$/US$/US$/US$/US$/US$/MtMtMtMtMtMtMtMt. Ni.. Ni.. Ni.. Ni.. Ni.. Ni.. Ni.. Ni.

7,1107,1107,1107,110

Beginning Beginning Beginning Beginning

2003200320032003

2% SUPPLY2% SUPPLY2% SUPPLY2% SUPPLY2% SUPPLY2% SUPPLY2% SUPPLY2% SUPPLY--------DEMAND DEFICIT DOES NOTDEMAND DEFICIT DOES NOTDEMAND DEFICIT DOES NOTDEMAND DEFICIT DOES NOTDEMAND DEFICIT DOES NOTDEMAND DEFICIT DOES NOTDEMAND DEFICIT DOES NOTDEMAND DEFICIT DOES NOTJUSTIFY SUCH EXTREME PRICE INCREASEJUSTIFY SUCH EXTREME PRICE INCREASEJUSTIFY SUCH EXTREME PRICE INCREASEJUSTIFY SUCH EXTREME PRICE INCREASEJUSTIFY SUCH EXTREME PRICE INCREASEJUSTIFY SUCH EXTREME PRICE INCREASEJUSTIFY SUCH EXTREME PRICE INCREASEJUSTIFY SUCH EXTREME PRICE INCREASE

0,000,000,000,00

0,200,200,200,20

0,400,400,400,40

0,600,600,600,60

0,800,800,800,80

1,001,001,001,00

1,201,201,201,201.201.201.201.20

1.001.001.001.00

0.800.800.800.80

0.600.600.600.60

0.400.400.400.40

0.200.200.200.20

0000

FERROCHROME PRICE (FERROCHROME PRICE (FERROCHROME PRICE (FERROCHROME PRICE (FERROCHROME PRICE (FERROCHROME PRICE (FERROCHROME PRICE (FERROCHROME PRICE (MetalMetalMetalMetalMetalMetalMetalMetal BulletinBulletinBulletinBulletinBulletinBulletinBulletinBulletin))))))))

89 90 91 92 93 94 95 96 97 98 99 00 089 90 91 92 93 94 95 96 97 98 99 00 089 90 91 92 93 94 95 96 97 98 99 00 089 90 91 92 93 94 95 96 97 98 99 00 01 02 031 02 031 02 031 02 03

USD / Lb. Cr.USD / Lb. Cr.USD / Lb. Cr.USD / Lb. Cr.USD / Lb. Cr.USD / Lb. Cr.USD / Lb. Cr.USD / Lb. Cr.

0.570.570.570.57

Ending Ending Ending Ending 2003200320032003

0.340.340.340.34

Beginning Beginning Beginning Beginning 2003200320032003

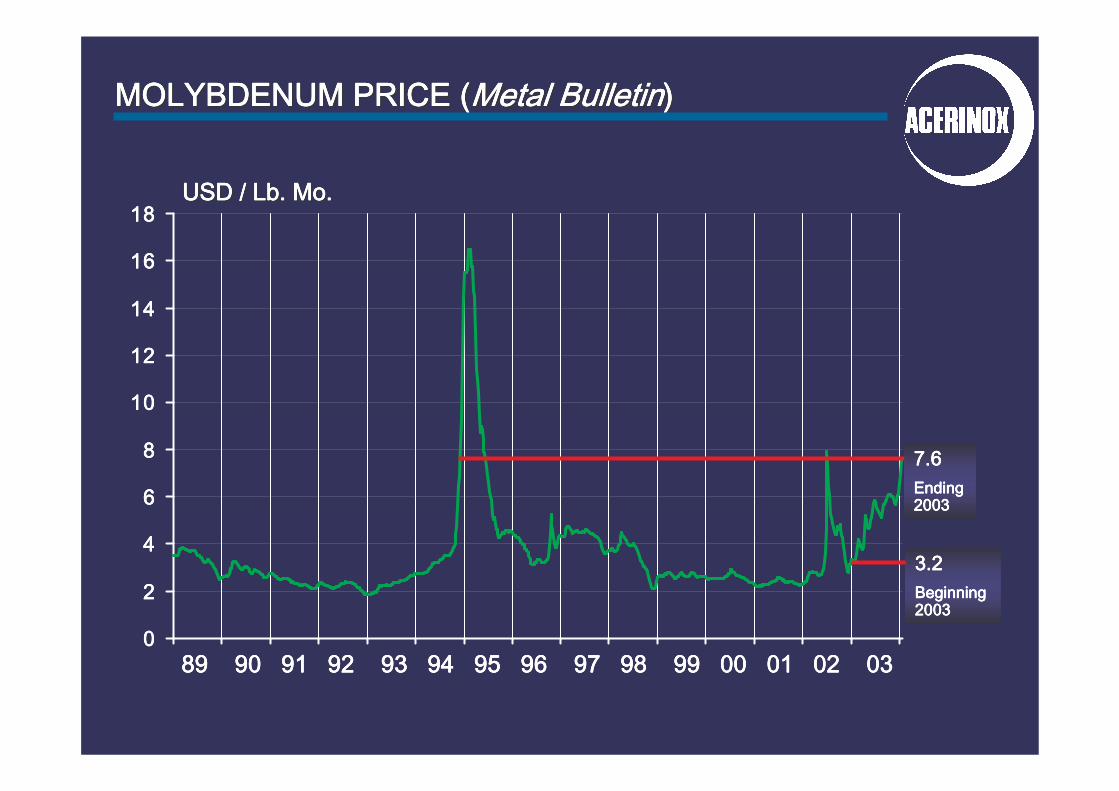

MOLYBDENUM PRICE (MOLYBDENUM PRICE (MOLYBDENUM PRICE (MOLYBDENUM PRICE (MOLYBDENUM PRICE (MOLYBDENUM PRICE (MOLYBDENUM PRICE (MOLYBDENUM PRICE (Metal Metal Metal Metal Metal Metal Metal Metal BulletinBulletinBulletinBulletinBulletinBulletinBulletinBulletin))))))))

USD / Lb. USD / Lb. USD / Lb. USD / Lb. USD / Lb. USD / Lb. USD / Lb. USD / Lb. MoMoMoMoMoMoMoMo........

89 90 91 92 93 94 95 96 97 98 99 00 89 90 91 92 93 94 95 96 97 98 99 00 89 90 91 92 93 94 95 96 97 98 99 00 89 90 91 92 93 94 95 96 97 98 99 00 01 02 0301 02 0301 02 0301 02 030000

2222

4444

6666

8888

10101010

12121212

14141414

16161616

18181818

7.67.67.67.6

Ending Ending Ending Ending 2003200320032003

3.23.23.23.2

BeginningBeginningBeginningBeginning2003200320032003

EVOLUTION OF THE STAINLESS EVOLUTION OF THE STAINLESS EVOLUTION OF THE STAINLESS EVOLUTION OF THE STAINLESS EVOLUTION OF THE STAINLESS EVOLUTION OF THE STAINLESS EVOLUTION OF THE STAINLESS EVOLUTION OF THE STAINLESS

STEEL PRICESSTEEL PRICESSTEEL PRICESSTEEL PRICESSTEEL PRICESSTEEL PRICESSTEEL PRICESSTEEL PRICES

USA

GERMANY

HONG KONG

1995 1996 1997 1998 1995 1996 1997 1998 1995 1996 1997 1998 1995 1996 1997 1998 1999 2000 2001 2002 1999 2000 2001 2002 1999 2000 2001 2002 1999 2000 2001 2002 2003200320032003

STAINLESS STEEL SHEET PRICESSTAINLESS STEEL SHEET PRICESSTAINLESS STEEL SHEET PRICESSTAINLESS STEEL SHEET PRICESAISI. 304 2,0 mm AISI. 304 2,0 mm AISI. 304 2,0 mm AISI. 304 2,0 mm ((((JanuaryJanuaryJanuaryJanuary 95 95 95 95 –––– DecemberDecemberDecemberDecember 03)03)03)03)

SOURCE: Metal Bulletin

Research “Stainless Steel

Monthly”

US$/Mt, final price, alloy surcharge included

1.000

1.250

1.500

1.750

2.000

2.250

2.500

2.750

3.000

3.250

3.500

3.7503,7503,7503,7503,750

3,5003,5003,5003,500

3,2503,2503,2503,250

3,0003,0003,0003,000

2,7502,7502,7502,750

2,5002,5002,5002,500

2,2502,2502,2502,250

2,0002,0002,0002,000

1,7501,7501,7501,750

1,5001,5001,5001,500

1,2501,2501,2501,250

1,0001,0001,0001,000

SUBSTITUTIONSUBSTITUTIONSUBSTITUTIONSUBSTITUTIONSUBSTITUTIONSUBSTITUTIONSUBSTITUTIONSUBSTITUTION

USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL

PROPERTIESPROPERTIESPROPERTIESPROPERTIESPROPERTIESPROPERTIESPROPERTIESPROPERTIES

BUTANE GAS CYLINDER

USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL USE OF STAINLESS STEEL FOR THEIR MECHANICAL

PROPERTIES IN THE AUTOMOTIVE SECTORPROPERTIES IN THE AUTOMOTIVE SECTORPROPERTIES IN THE AUTOMOTIVE SECTORPROPERTIES IN THE AUTOMOTIVE SECTORPROPERTIES IN THE AUTOMOTIVE SECTORPROPERTIES IN THE AUTOMOTIVE SECTORPROPERTIES IN THE AUTOMOTIVE SECTORPROPERTIES IN THE AUTOMOTIVE SECTOR

BRIDGE IN MONTANA STATE, USA

STAINLESS STEEL REBARSTAINLESS STEEL REBARSTAINLESS STEEL REBARSTAINLESS STEEL REBARSTAINLESS STEEL REBARSTAINLESS STEEL REBARSTAINLESS STEEL REBARSTAINLESS STEEL REBAR

COMPETITORS ON THE RISE AS WELLCOMPETITORS ON THE RISE AS WELLCOMPETITORS ON THE RISE AS WELLCOMPETITORS ON THE RISE AS WELLCOMPETITORS ON THE RISE AS WELLCOMPETITORS ON THE RISE AS WELLCOMPETITORS ON THE RISE AS WELLCOMPETITORS ON THE RISE AS WELL

12 12 12 12 12 12 12 12 monthmonthmonthmonthmonthmonthmonthmonth LME LME LME LME LME LME LME LME Aluminium Aluminium Aluminium Aluminium Aluminium Aluminium Aluminium Aluminium cash cash cash cash cash cash cash cash price price price price price price price price In MT In MT In MT In MT In MT In MT In MT In MT vs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventory

12 12 12 12 12 12 12 12 monthmonthmonthmonthmonthmonthmonthmonth LME LME LME LME LME LME LME LME CooperCooperCooperCooperCooperCooperCooperCooper cash cash cash cash cash cash cash cash price price price price price price price price In MT In MT In MT In MT In MT In MT In MT In MT vs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventoryvs Inventory

1,5501,5501,5501,550

1,5251,5251,5251,525

1,5001,5001,5001,500

1,4751,4751,4751,475

1,4501,4501,4501,450

1,4251,4251,4251,425

1,4001,4001,4001,400

1,3751,3751,3751,375

1,3501,3501,3501,350

1,3251,3251,3251,325

1,3001,3001,3001,300

1,2751,2751,2751,275

2,3002,3002,3002,300

2,2002,2002,2002,200

2,1002,1002,1002,100

2,0002,0002,0002,000

1,9001,9001,9001,900

1,8001,8001,8001,800

1,7001,7001,7001,700

1,6001,6001,6001,600

1,5001,5001,5001,500

1,4001,4001,4001,400

12/9 1/8 2/27 4/14 5/27 12/9 1/8 2/27 4/14 5/27 12/9 1/8 2/27 4/14 5/27 12/9 1/8 2/27 4/14 5/27 6/26 8/5 9/9 10/17 11/116/26 8/5 9/9 10/17 11/116/26 8/5 9/9 10/17 11/116/26 8/5 9/9 10/17 11/11

900900900900

850850850850

800800800800

750750750750

700700700700

650650650650

600600600600

550550550550

500500500500

450450450450

MT

(00

0’s

)M

T (

00

0’s

)M

T (

00

0’s

)M

T (

00

0’s

)

1,4001,4001,4001,400

1,3501,3501,3501,350

1,3001,3001,3001,300

1,2501,2501,2501,250

1,2001,2001,2001,200

1,1501,1501,1501,150

1,1001,1001,1001,100

MT

(00

0’s

)M

T (

00

0’s

)M

T (

00

0’s

)M

T (

00

0’s

)

12/16 1/21 2/11 3/12 4/15 6/3 12/16 1/21 2/11 3/12 4/15 6/3 12/16 1/21 2/11 3/12 4/15 6/3 12/16 1/21 2/11 3/12 4/15 6/3 7/10 8/4 9/3 9/30 11/10 7/10 8/4 9/3 9/30 11/10 7/10 8/4 9/3 9/30 11/10 7/10 8/4 9/3 9/30 11/10

Pri

ce

P

rice

P

rice

P

rice

US

$U

S$

US

$U

S$

Pri

ce

P

rice

P

rice

P

rice

US

$U

S$

US

$U

S$

PricesPricesPricesPrices

InventoryInventoryInventoryInventory

MetalpricesMetalpricesMetalpricesMetalprices....comcomcomcom

• Intensified informal cooperation (2002 - )

(Co-ordination of messages to the market)

• Heavy focus on Health & Environment

• New priorities: - joint statistical work

- joint market development

• Joint ISSF - NiDI Board meetings since 2000

• Joint ISSF Board – ICDA Council meetings will

start 2004

TEAM STAINLESS (ICDA TEAM STAINLESS (ICDA TEAM STAINLESS (ICDA TEAM STAINLESS (ICDA TEAM STAINLESS (ICDA TEAM STAINLESS (ICDA TEAM STAINLESS (ICDA TEAM STAINLESS (ICDA –––––––– NiDINiDINiDINiDINiDINiDINiDINiDI –––––––– IMOA IMOA IMOA IMOA IMOA IMOA IMOA IMOA –––––––– ISSF)ISSF)ISSF)ISSF)ISSF)ISSF)ISSF)ISSF)

SOUTH AFRICAN STAINLESS STEEL SOUTH AFRICAN STAINLESS STEEL SOUTH AFRICAN STAINLESS STEEL SOUTH AFRICAN STAINLESS STEEL SOUTH AFRICAN STAINLESS STEEL SOUTH AFRICAN STAINLESS STEEL SOUTH AFRICAN STAINLESS STEEL SOUTH AFRICAN STAINLESS STEEL

MARKET AND INDUSTRYMARKET AND INDUSTRYMARKET AND INDUSTRYMARKET AND INDUSTRYMARKET AND INDUSTRYMARKET AND INDUSTRYMARKET AND INDUSTRYMARKET AND INDUSTRY

80808080

90909090

100100100100

110110110110

120120120120

130130130130

140140140140

150150150150

160160160160

1996 1997 1998 1999 2000 2001 2002 2003e

SOUTH AFRICAN APPARENT STAINLESS STEEL SOUTH AFRICAN APPARENT STAINLESS STEEL SOUTH AFRICAN APPARENT STAINLESS STEEL SOUTH AFRICAN APPARENT STAINLESS STEEL SOUTH AFRICAN APPARENT STAINLESS STEEL SOUTH AFRICAN APPARENT STAINLESS STEEL SOUTH AFRICAN APPARENT STAINLESS STEEL SOUTH AFRICAN APPARENT STAINLESS STEEL CONSUMPTIONCONSUMPTIONCONSUMPTIONCONSUMPTIONCONSUMPTIONCONSUMPTIONCONSUMPTIONCONSUMPTION

‘000 ‘000 ‘000 ‘000 ‘000 ‘000 ‘000 ‘000 MtMtMtMtMtMtMtMt

Compound Annual Growth Rate

Compound Annual Growth Rate

Compound Annual Growth Rate

Compound Annual Growth Rate: +

7.7%: +

7.7%: +

7.7%: +

7.7%

MIDDELBURG FACTORY IN 2002 (MIDDELBURG FACTORY IN 2002 (MIDDELBURG FACTORY IN 2002 (MIDDELBURG FACTORY IN 2002 (MIDDELBURG FACTORY IN 2002 (MIDDELBURG FACTORY IN 2002 (MIDDELBURG FACTORY IN 2002 (MIDDELBURG FACTORY IN 2002 (South AfricaSouth AfricaSouth AfricaSouth AfricaSouth AfricaSouth AfricaSouth AfricaSouth Africa))))))))

+24.6%+24.6%+24.6%+24.6%+24.6%+24.6%+24.6%+24.6%

COLUMBUS STAINLESS PRODUCTIONCOLUMBUS STAINLESS PRODUCTIONCOLUMBUS STAINLESS PRODUCTIONCOLUMBUS STAINLESS PRODUCTIONCOLUMBUS STAINLESS PRODUCTIONCOLUMBUS STAINLESS PRODUCTIONCOLUMBUS STAINLESS PRODUCTIONCOLUMBUS STAINLESS PRODUCTION

100100100100

200200200200

300300300300

400400400400

500500500500

600600600600

700700700700

800800800800

2001200120012001 2002200220022002 2003200320032003 2004(e)2004(e)2004(e)2004(e) 2005(e)2005(e)2005(e)2005(e)

MeltingMeltingMeltingMelting

Hot rollingHot rollingHot rollingHot rolling

Cold rollingCold rollingCold rollingCold rolling

‘000 ‘000 ‘000 ‘000 ‘000 ‘000 ‘000 ‘000 MtMtMtMtMtMtMtMt

+22.8%+22.8%+22.8%+22.8%+22.8%+22.8%+22.8%+22.8%

NEW SENDZIMIR ZNEW SENDZIMIR ZNEW SENDZIMIR ZNEW SENDZIMIR ZNEW SENDZIMIR ZNEW SENDZIMIR ZNEW SENDZIMIR ZNEW SENDZIMIR Z--------MILL 3 (ZRMILL 3 (ZRMILL 3 (ZRMILL 3 (ZRMILL 3 (ZRMILL 3 (ZRMILL 3 (ZRMILL 3 (ZR--------21BN21BN21BN21BN21BN21BN21BN21BN--------63) HOUSING FOR 63) HOUSING FOR 63) HOUSING FOR 63) HOUSING FOR 63) HOUSING FOR 63) HOUSING FOR 63) HOUSING FOR 63) HOUSING FOR

COLUMBUS STAINLESS IN PRECOLUMBUS STAINLESS IN PRECOLUMBUS STAINLESS IN PRECOLUMBUS STAINLESS IN PRECOLUMBUS STAINLESS IN PRECOLUMBUS STAINLESS IN PRECOLUMBUS STAINLESS IN PRECOLUMBUS STAINLESS IN PRE--------ASSEMBLY, NOVEMBER ASSEMBLY, NOVEMBER ASSEMBLY, NOVEMBER ASSEMBLY, NOVEMBER ASSEMBLY, NOVEMBER ASSEMBLY, NOVEMBER ASSEMBLY, NOVEMBER ASSEMBLY, NOVEMBER

20032003200320032003200320032003

CONCLUSIONCONCLUSIONCONCLUSIONCONCLUSIONCONCLUSIONCONCLUSIONCONCLUSIONCONCLUSION

CONCLUSION:CONCLUSION:CONCLUSION:CONCLUSION:

I am more optimistic than ever about the future of stainless steel under only two conditions:

1.- World economy grows normally.2.- Reasonable behaviour of raw materials.

All of us, raw materials suppliers, stainless steel producers and transformers, are in the same boat and it is very important to avoid all kind of speculations like those suffered last year, especially with the LME nickel prices. How? This is a difficult question but you will agree with me that they are affecting the wonderful 6% growth rate of the stainless steel of last 53 years, that could even be higher due, on top of its life cycle and maintenance free, to its superior mechanical properties than other competitive materials.

Will the growth depend in a big extent of China? Yes, but not exclusively, because in all the remaining geographic areas it will continue growing too, even if certain transforming industries, intensive in man power, will move not only to China but also to Taiwan, South Korea, Malaysia, Vietnam, etc., and why not to South Africa, provided that the Rand would recover soon a reasonable parity with the US Dollar?. Such unavoidable displacements will be compensated with new applications. I also strongly believe in the recovery of the North American market, now that its economy is doing well and its stainless steel industries are becoming competitive and in consequence the market prices have been already aligned with those of other areas.

The past experience is that “when a country reaches a certain GDP level, the stainless steel consumption always takes off spectacularly” and I think this moment has already arrived for China, and you can imagine what can happen in a Country with 1.3 billion population ready to work. If GDP of China continues growing not at between 7 and 9% p.a. like last years, but even at a little lower pace, the stainless steel consumption will rise at two digits figures. If so, China will reduce rather fast its cold rolled coils imports but will continue importing hot coils and also special cold rolled grades during all this decade.

When the analysts talk about overcapacity, they often forget that the more sophisticated the new equipments are, the longer time is necessary for the start up since it takes many months until the full capacity is reached. Besides that, the recent mergers of heavy machinery makers, with the inherent early retirement of experienced engineers, has caused delays in important projects, not to mention about the possible financial dangers, specially in the tight moments of the cycle.

Even if the new investments are undertaken in a reasonable manner and timing, there will be a fierce competition in our very globalized market, and consequently the profit margins will continue narrowing more and more. The importance of the integrated process in the plants, with a minimal size of about 1 million tons, will be decisive. The location of production close to the customers and raw materials will become another important factor. Nevertheless, due to our product excellence it will not exist a big global overcapacity, except for certain short periods of time, as it happened cyclically in the past. The consolidation of the stainless steel industry will continue, as it has already been accomplished in Europe, but not enough yet in other continents and most especially in Asia, that should digest its very big and outstanding fast expansion.

I hope that these personal views about stainless steel industry will be helpful for your discussions in this Ferroalloys Congress and I am at your disposal for replying your questions.

Many thanks.

Related Documents