PLATTS CRUDE OIL MARKETS ASIA 2013 Goodwood Park Hotel, Singapore September 18-19, 2013 Developing New Supply Opportunities with Russia: The Philippines’ Perspective ATTY. JOSE M. LAYUG, JR. Senior Partner , Puno & Puno Law Offices Philippine Energy Expert, University of the Philippines College of Law

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PLATTS

CR

UD

E OIL

MA

RK

ETS A

SIA

20

13

G

oodwood P

ark Hotel, S

ingapore S

eptember 1

8-1

9, 2

01

3

Developing New Supply Opportunities with Russia:

The Philippines’ Perspective ATTY. JOSE M. LAYUG, JR.

Senior Partner , Puno & Puno Law Offices Philippine Energy Expert, University of the

Philippines College of Law

1. Energy Supply and Demand Situation

2. Philippines’ Growth: Drivers of Oil Demand

3. The Downstream Oil Industry Framework

4. Tapping Russia as New Supply Center

5. Mitigating Measures

DISCUSSION OUTLINE

WHY THE PHILIPPINES?

ENERGY SUPPLY AND DEMAND SITUATION

PH

ILIPP

INES

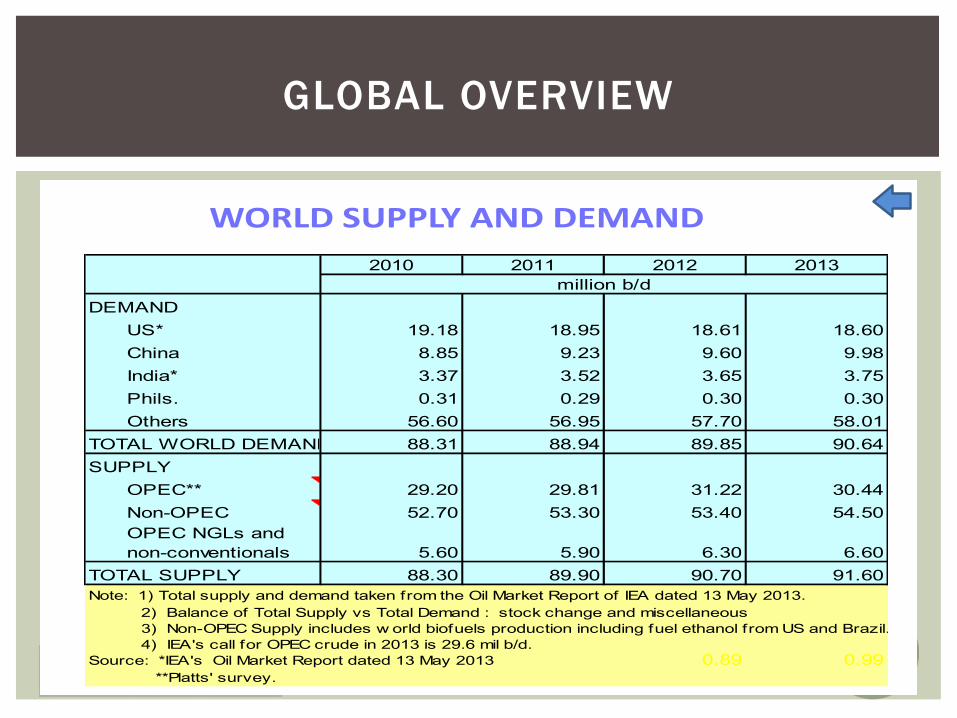

WORLD SUPPLY AND DEMAND 2010 2011 2012 2013

DEMANDUS* 19.18 18.95 18.61 18.60China 8.85 9.23 9.60 9.98India* 3.37 3.52 3.65 3.75Phils. 0.31 0.29 0.30 0.30Others 56.60 56.95 57.70 58.01

TOTAL WORLD DEMAND 88.31 88.94 89.85 90.64SUPPLY 0.01 0.01

OPEC** 29.20 29.81 31.22 30.44Non-OPEC 52.70 53.30 53.40 54.50OPEC NGLs and non-conventionals 5.60 5.90 6.30 6.60

TOTAL SUPPLY 88.30 89.90 90.70 91.60Note: 1) Total supply and demand taken from the Oil Market Report of IEA dated 13 May 2013. 2) Balance of Total Supply vs Total Demand : stock change and miscellaneous

3) Non-OPEC Supply includes w orld biofuels production including fuel ethanol from US and Brazil. 4) IEA's call for OPEC crude in 2013 is 29.6 mil b/d.

Source: *IEA's Oil Market Report dated 13 May 2013 0.89 0.99 **Platts' survey.

million b/d

GLOBAL OVERVIEW

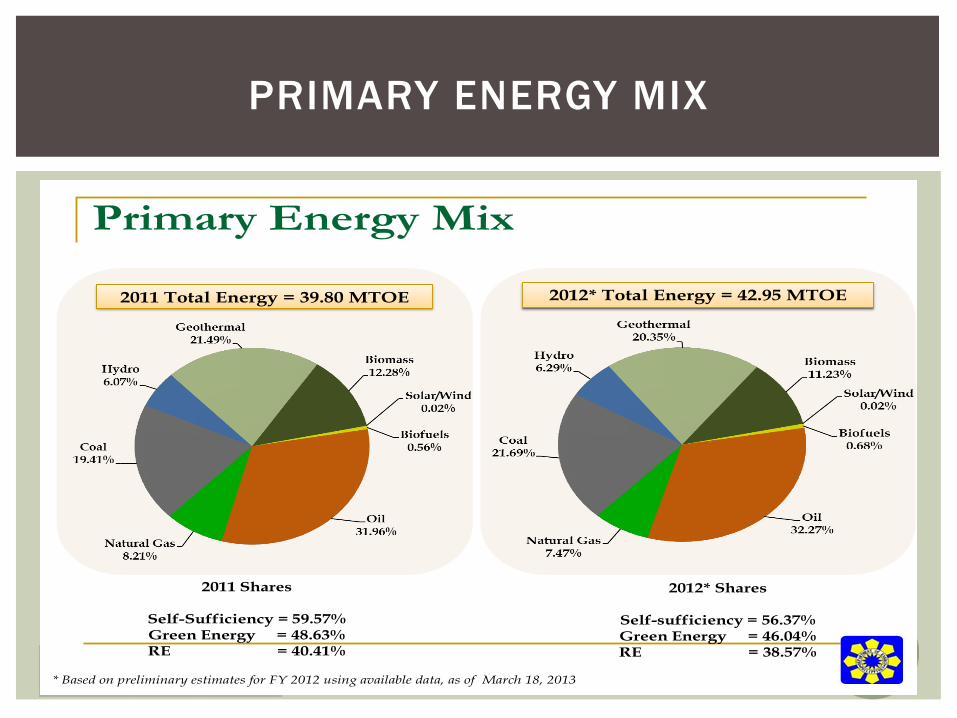

2011 Shares

Self-Sufficiency = 59.57% Green Energy = 48.63% RE = 40.41%

2011 Total Energy = 39.80 MTOE 2012* Total Energy = 42.95 MTOE

2012* Shares

Self-sufficiency = 56.37% Green Energy = 46.04% RE = 38.57%

* Based on preliminary estimates for FY 2012 using available data, as of March 18, 2013

Primary Energy Mix

PRIMARY ENERGY MIX

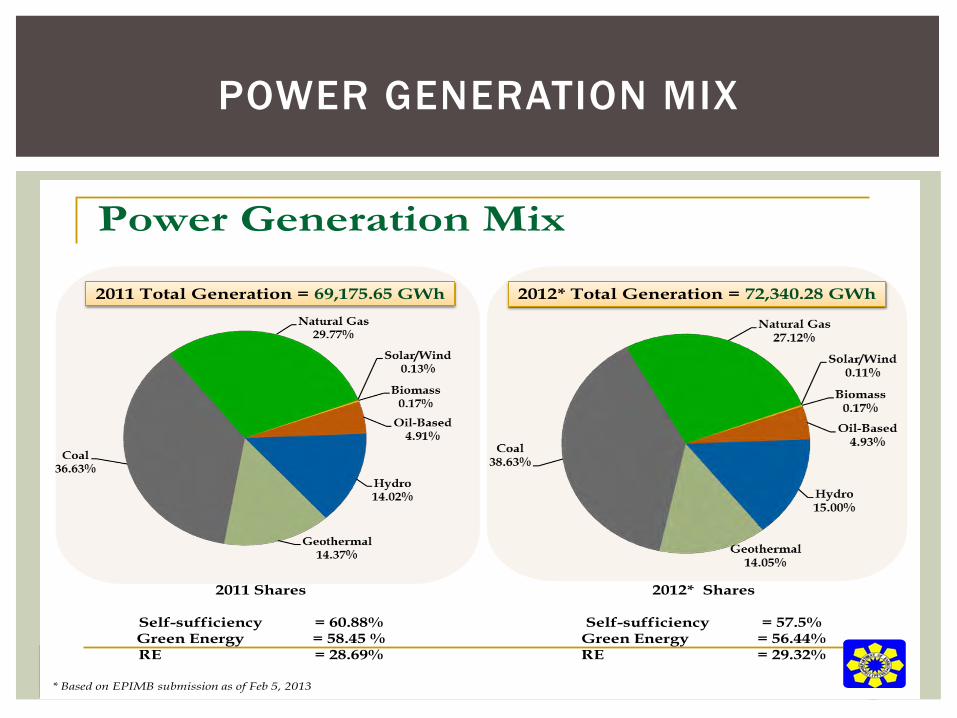

POWER GENERATION MIX

2011 Total Generation = 69,175.65 GWh 2012* Total Generation = 72,340.28 GWh

* Based on EPIMB submission as of Feb 5, 2013

2012* Shares

Self-sufficiency = 57.5% Green Energy = 56.44% RE = 29.32%

2011 Shares

Self-sufficiency = 60.88% Green Energy = 58.45 % RE = 28.69%

Power Generation Mix

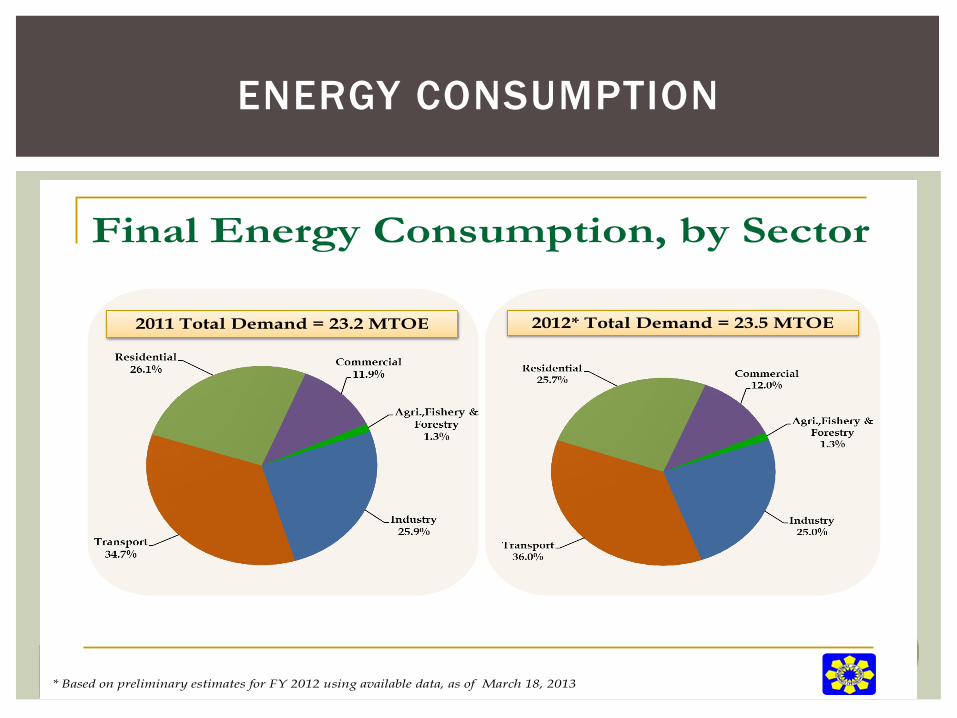

2011 Total Demand = 23.2 MTOE 2012* Total Demand = 23.5 MTOE

Final Energy Consumption, by Sector

* Based on preliminary estimates for FY 2012 using available data, as of March 18, 2013

ENERGY CONSUMPTION

2011 Total Demand = 23.2 MTOE 2012* Total Demand = 23.8 MTOE

Final Energy Consumption, by Fuel

* Based on preliminary estimates for FY 2012 using available data, as of March 18, 2013

ENERGY CONSUMPTION

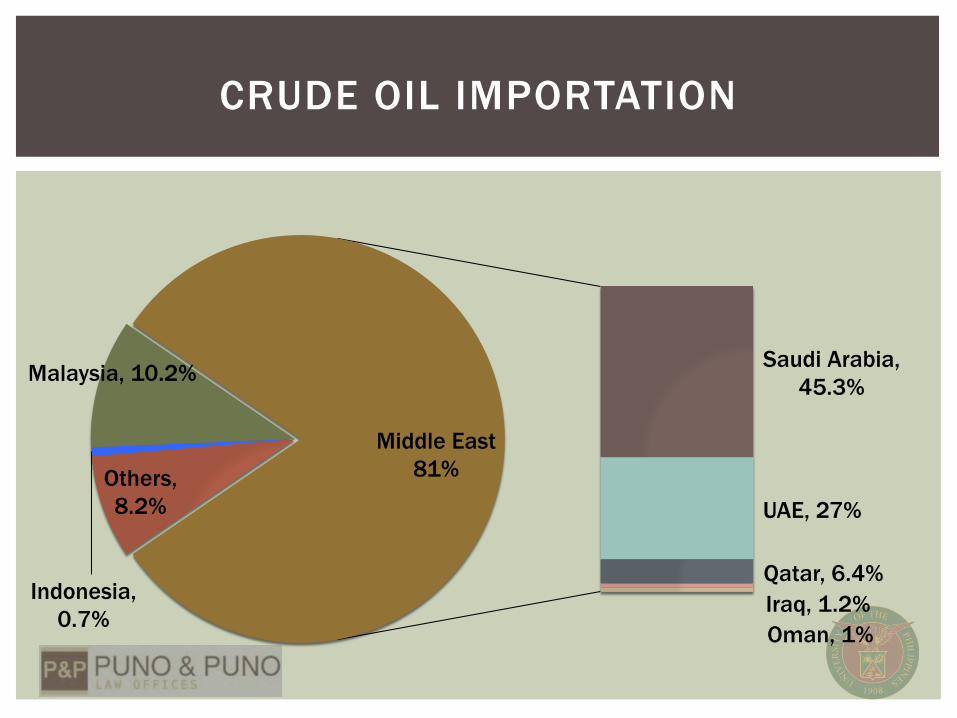

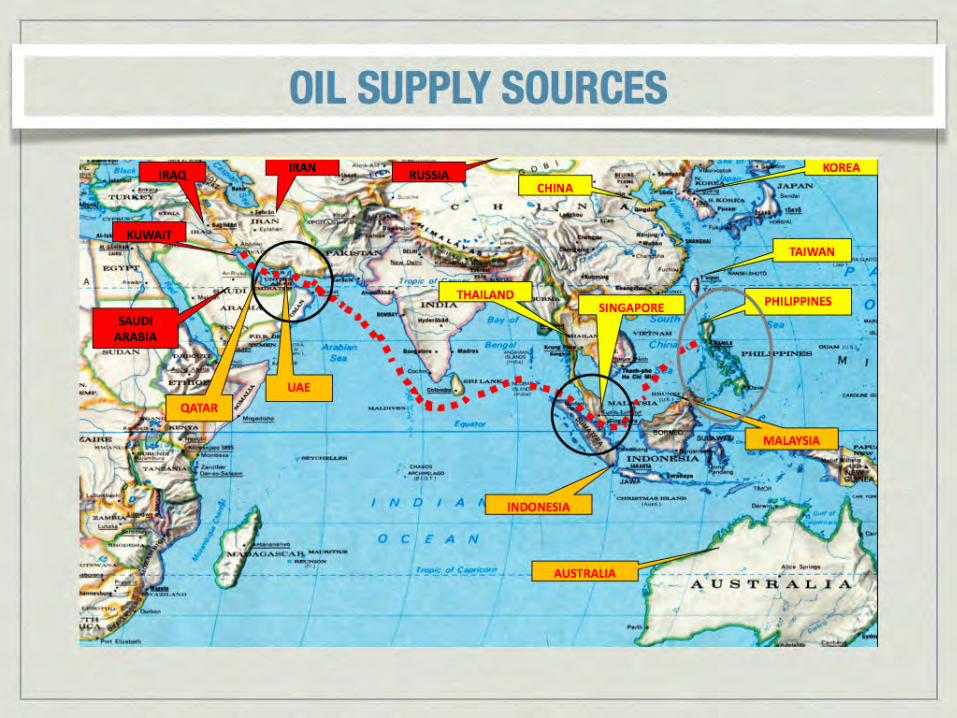

CRUDE OIL IMPORTATION

Others, 8.2%

Indonesia, 0.7%

Malaysia, 10.2% Saudi Arabia, 45.3%

UAE, 27%

Qatar, 6.4%

Oman, 1% Iraq, 1.2%

Middle East 81%

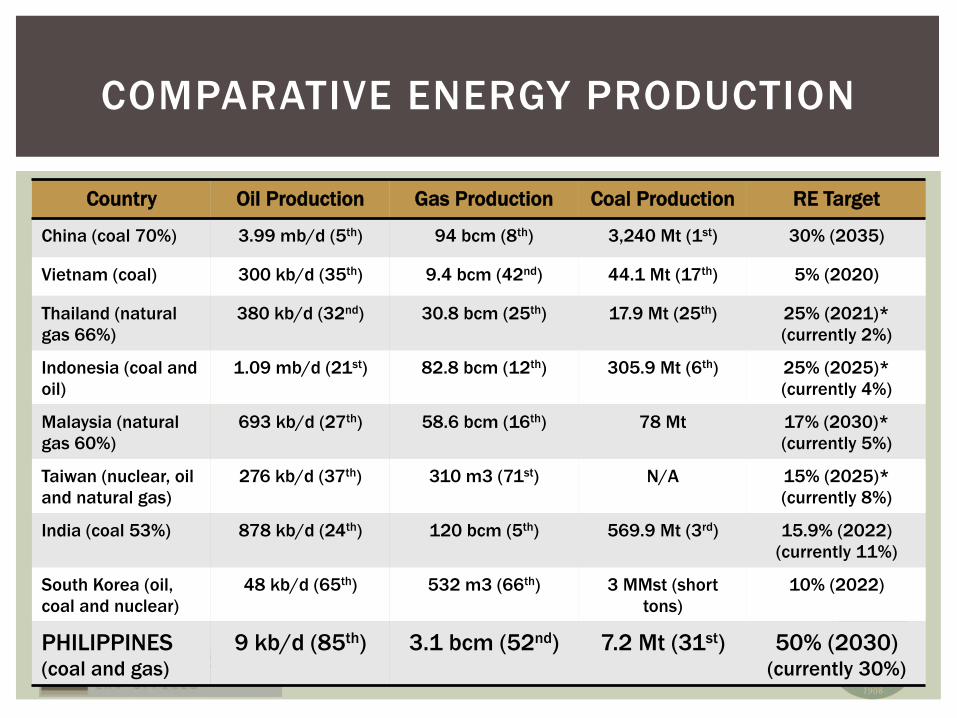

COMPARATIVE ENERGY PRODUCTION

Country Oil Production Gas Production Coal Production RE Target

China (coal 70%) 3.99 mb/d (5th) 94 bcm (8th) 3,240 Mt (1st) 30% (2035)

Vietnam (coal) 300 kb/d (35th) 9.4 bcm (42nd) 44.1 Mt (17th) 5% (2020)

Thailand (natural gas 66%)

380 kb/d (32nd) 30.8 bcm (25th) 17.9 Mt (25th) 25% (2021)* (currently 2%)

Indonesia (coal and oil)

1.09 mb/d (21st) 82.8 bcm (12th) 305.9 Mt (6th) 25% (2025)* (currently 4%)

Malaysia (natural gas 60%)

693 kb/d (27th) 58.6 bcm (16th) 78 Mt 17% (2030)* (currently 5%)

Taiwan (nuclear, oil and natural gas)

276 kb/d (37th) 310 m3 (71st) N/A 15% (2025)* (currently 8%)

India (coal 53%) 878 kb/d (24th) 120 bcm (5th) 569.9 Mt (3rd) 15.9% (2022) (currently 11%)

South Korea (oil, coal and nuclear)

48 kb/d (65th) 532 m3 (66th) 3 MMst (short tons)

10% (2022)

PHILIPPINES (coal and gas)

9 kb/d (85th) 3.1 bcm (52nd) 7.2 Mt (31st) 50% (2030) (currently 30%)

33

Enhanced Indigenous Energy Development

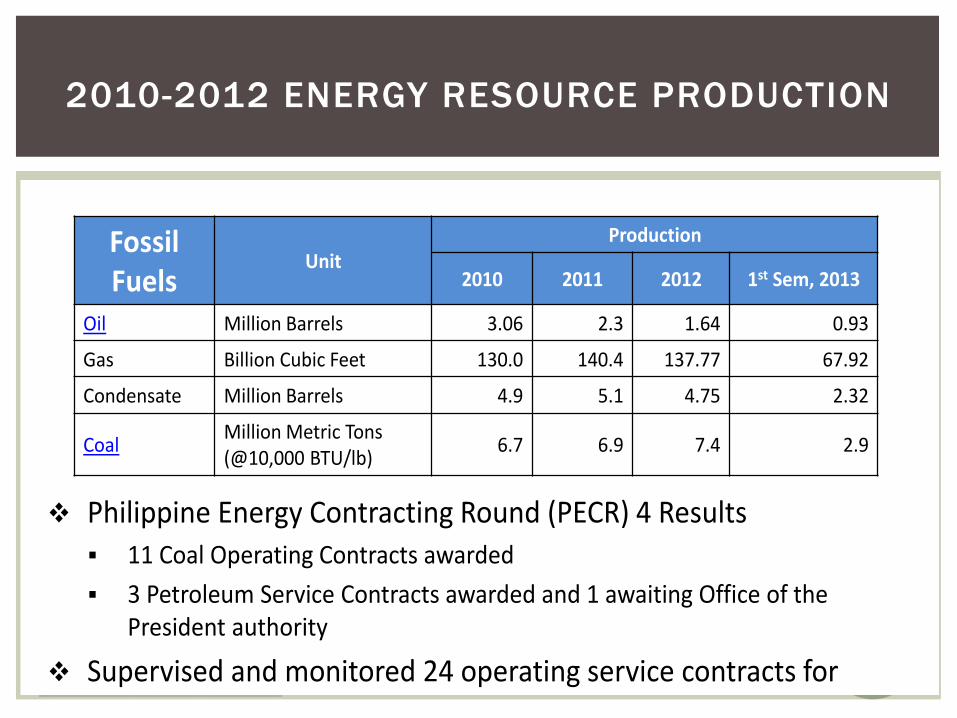

Fossil Fuels

Unit Production

2010 2011 2012 1st Sem, 2013

Oil Million Barrels 3.06 2.3 1.64 0.93

Gas Billion Cubic Feet 130.0 140.4 137.77 67.92

Condensate Million Barrels 4.9 5.1 4.75 2.32

Coal Million Metric Tons (@10,000 BTU/lb) 6.7 6.9 7.4 2.9

Philippine Energy Contracting Round (PECR) 4 Results 11 Coal Operating Contracts awarded 3 Petroleum Service Contracts awarded and 1 awaiting Office of the

President authority

Supervised and monitored 24 operating service contracts for petroleum and 71 for coal exploration and development

2010-2012 ENERGY RESOURCE PRODUCTION

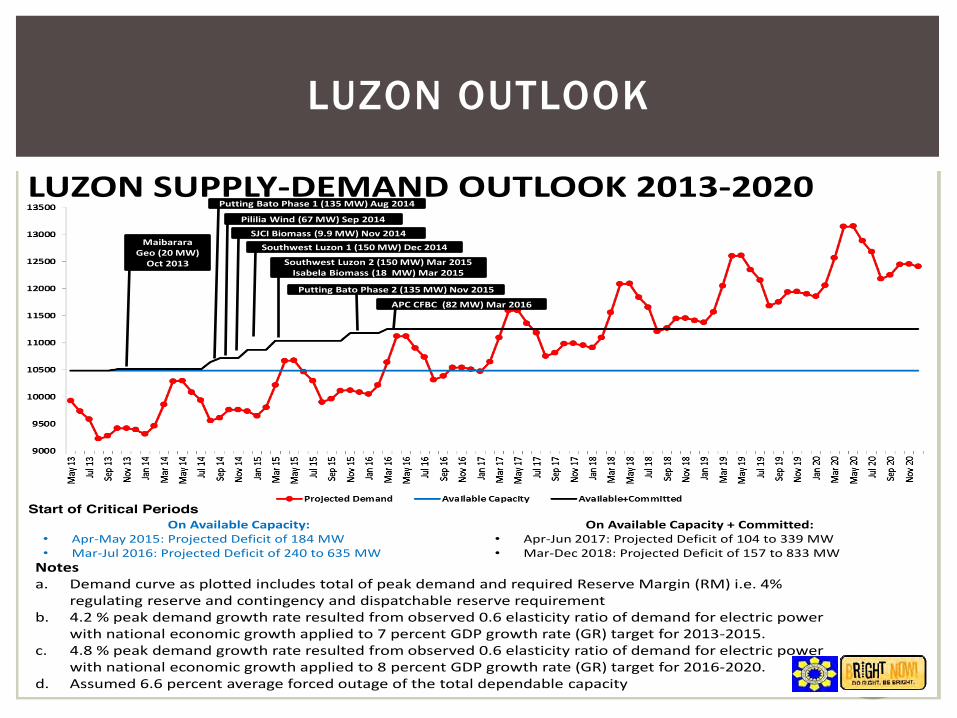

LUZON SUPPLY-DEMAND OUTLOOK 2013-2020

Notes a. Demand curve as plotted includes total of peak demand and required Reserve Margin (RM) i.e. 4%

regulating reserve and contingency and dispatchable reserve requirement b. 4.2 % peak demand growth rate resulted from observed 0.6 elasticity ratio of demand for electric power

with national economic growth applied to 7 percent GDP growth rate (GR) target for 2013-2015. c. 4.8 % peak demand growth rate resulted from observed 0.6 elasticity ratio of demand for electric power

with national economic growth applied to 8 percent GDP growth rate (GR) target for 2016-2020. d. Assumed 6.6 percent average forced outage of the total dependable capacity

On Available Capacity: • Apr-May 2015: Projected Deficit of 184 MW • Mar-Jul 2016: Projected Deficit of 240 to 635 MW

On Available Capacity + Committed: • Apr-Jun 2017: Projected Deficit of 104 to 339 MW • Mar-Dec 2018: Projected Deficit of 157 to 833 MW

Start of Critical Periods

Maibarara Geo (20 MW)

Oct 2013

Putting Bato Phase 1 (135 MW) Aug 2014

Pililia Wind (67 MW) Sep 2014 SJCI Biomass (9.9 MW) Nov 2014

Southwest Luzon 1 (150 MW) Dec 2014

Southwest Luzon 2 (150 MW) Mar 2015 Isabela Biomass (18 MW) Mar 2015

Putting Bato Phase 2 (135 MW) Nov 2015

APC CFBC (82 MW) Mar 2016

LUZON OUTLOOK

1600

1800

2000

2200

2400

2600

2800

3000

3200

May

13

Jul 1

3

Sep 1

3

Nov 1

3

Jan 14

Mar

14

May

14

Jul 1

4

Sep 1

4

Nov 1

4

Jan 15

Mar

15

May

15

Jul 1

5

Sep 1

5

Nov 1

5

Jan 16

Mar

16

May

16

Jul 1

6

Sep 1

6

Nov 1

6

Jan 17

Mar

17

May

17

Jul 1

7

Sep 1

7

Nov 1

7

Jan 18

Mar

18

May

18

Jul 1

8

Sep 1

8

Nov 1

8

Jan 19

Mar

19

May

19

Jul 1

9

Sep 1

9

Nov 1

9

Jan 20

Mar

20

May

20

Jul 2

0

Sep 2

0

Nov 2

0

Projected Demand Available Capacity Available+Committed

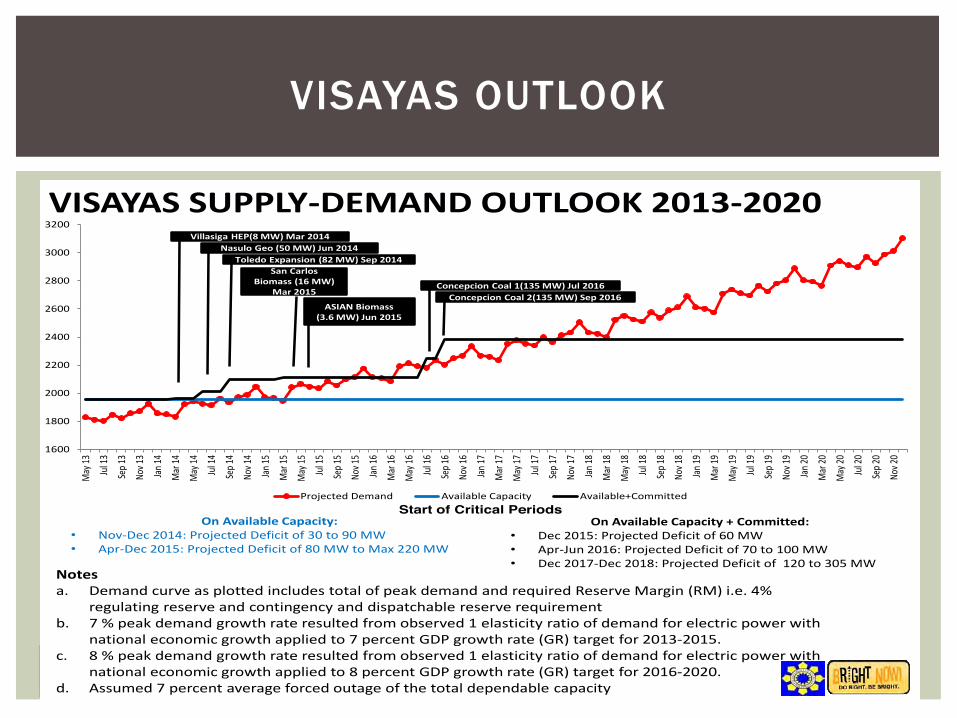

VISAYAS SUPPLY-DEMAND OUTLOOK 2013-2020

Notes a. Demand curve as plotted includes total of peak demand and required Reserve Margin (RM) i.e. 4%

regulating reserve and contingency and dispatchable reserve requirement b. 7 % peak demand growth rate resulted from observed 1 elasticity ratio of demand for electric power with

national economic growth applied to 7 percent GDP growth rate (GR) target for 2013-2015. c. 8 % peak demand growth rate resulted from observed 1 elasticity ratio of demand for electric power with

national economic growth applied to 8 percent GDP growth rate (GR) target for 2016-2020. d. Assumed 7 percent average forced outage of the total dependable capacity

On Available Capacity: • Nov-Dec 2014: Projected Deficit of 30 to 90 MW • Apr-Dec 2015: Projected Deficit of 80 MW to Max 220 MW

On Available Capacity + Committed: • Dec 2015: Projected Deficit of 60 MW • Apr-Jun 2016: Projected Deficit of 70 to 100 MW • Dec 2017-Dec 2018: Projected Deficit of 120 to 305 MW

Villasiga HEP(8 MW) Mar 2014 Nasulo Geo (50 MW) Jun 2014

Toledo Expansion (82 MW) Sep 2014

ASIAN Biomass (3.6 MW) Jun 2015

Concepcion Coal 1(135 MW) Jul 2016 Concepcion Coal 2(135 MW) Sep 2016

San Carlos Biomass (16 MW)

Mar 2015

Start of Critical Periods

VISAYAS OUTLOOK

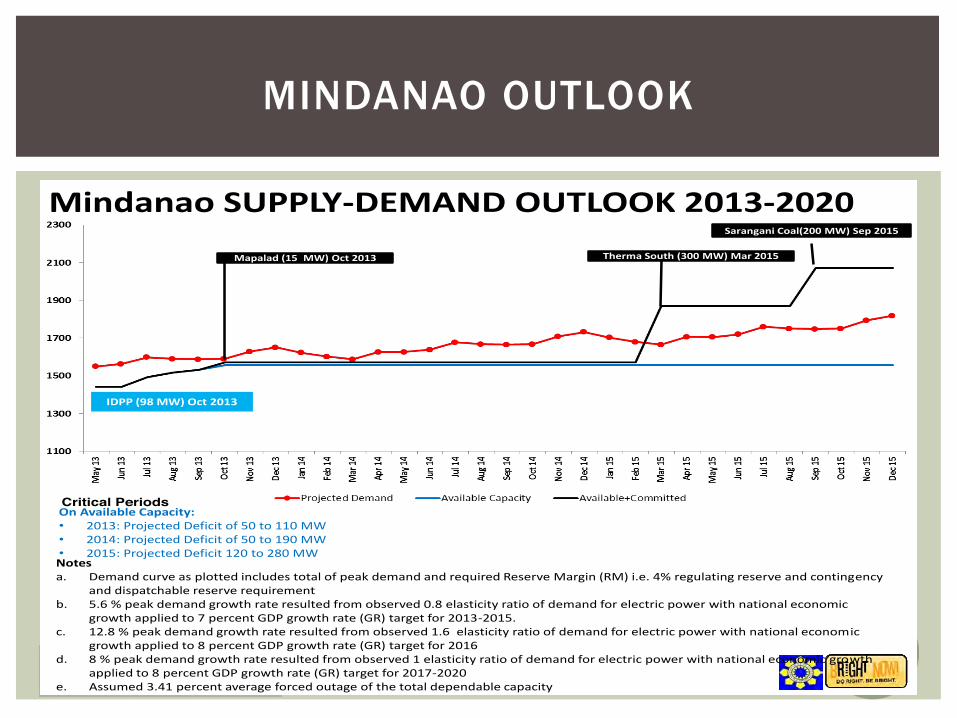

Mindanao SUPPLY-DEMAND OUTLOOK 2013-2020

Notes a. Demand curve as plotted includes total of peak demand and required Reserve Margin (RM) i.e. 4% regulating reserve and contingency

and dispatchable reserve requirement b. 5.6 % peak demand growth rate resulted from observed 0.8 elasticity ratio of demand for electric power with national economic

growth applied to 7 percent GDP growth rate (GR) target for 2013-2015. c. 12.8 % peak demand growth rate resulted from observed 1.6 elasticity ratio of demand for electric power with national economic

growth applied to 8 percent GDP growth rate (GR) target for 2016 d. 8 % peak demand growth rate resulted from observed 1 elasticity ratio of demand for electric power with national economic growth

applied to 8 percent GDP growth rate (GR) target for 2017-2020 e. Assumed 3.41 percent average forced outage of the total dependable capacity

On Available Capacity: • 2013: Projected Deficit of 50 to 110 MW • 2014: Projected Deficit of 50 to 190 MW • 2015: Projected Deficit 120 to 280 MW

Critical Periods

Mapalad (15 MW) Oct 2013 Therma South (300 MW) Mar 2015

Sarangani Coal(200 MW) Sep 2015

IDPP (98 MW) Oct 2013

MINDANAO OUTLOOK

PHILIPPINES GDP: DRIVERS OF OIL DEMAND

PH

ILIPP

INES

PHILIPPINES ECONOMIC GROWTH

PHILIPPINE ECONOMY

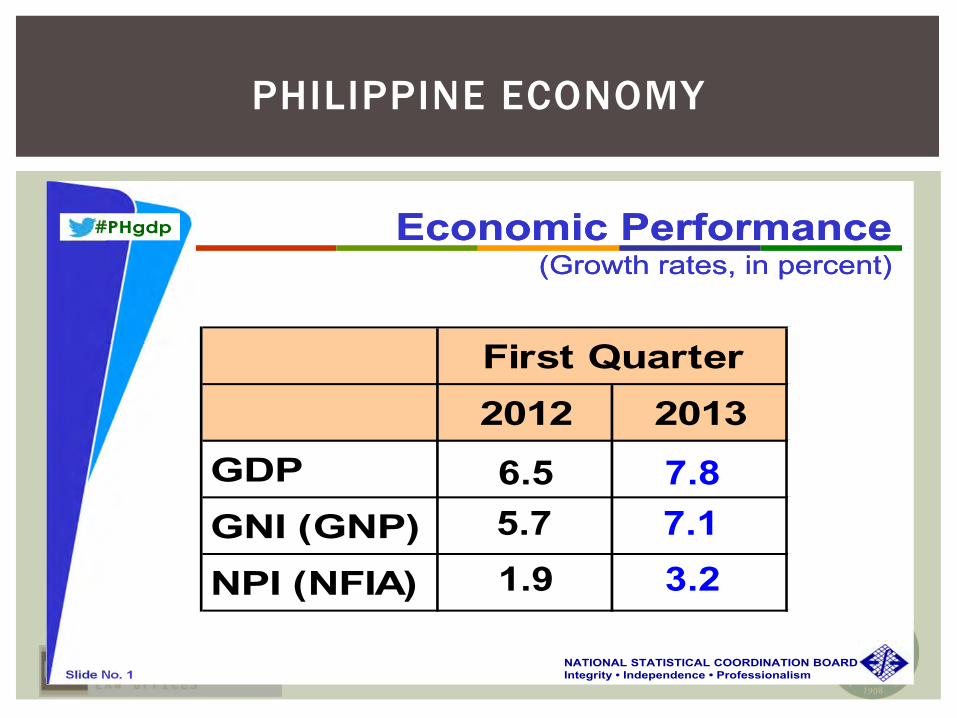

Slide No. 1NATIONAL STATISTICAL COORDINATION BOARDIntegrity • Independence • Professionalism

#PHgdp Economic Performance(Growth rates, in percent)

Economic Performance(Growth rates, in percent)

2012 2013GDPGNI (GNP)NPI (NFIA)

First Quarter

7.86.5

3.21.97.15.7

Slide No. 3NATIONAL STATISTICAL COORDINATION BOARDIntegrity • Independence • Professionalism

#PHgdp Per Capita GDP, GNI, HFCE(Growth rates, in percent)

Per Capita GDP, GNI, HFCE(Growth rates, in percent)

2013Q1 Q4 Q1

GDPGNI (GNP)HFCE (PCE)

2012

6.1

3.45.3

4.54.65.3

5.14.04.7

PHILIPPINE ECONOMY

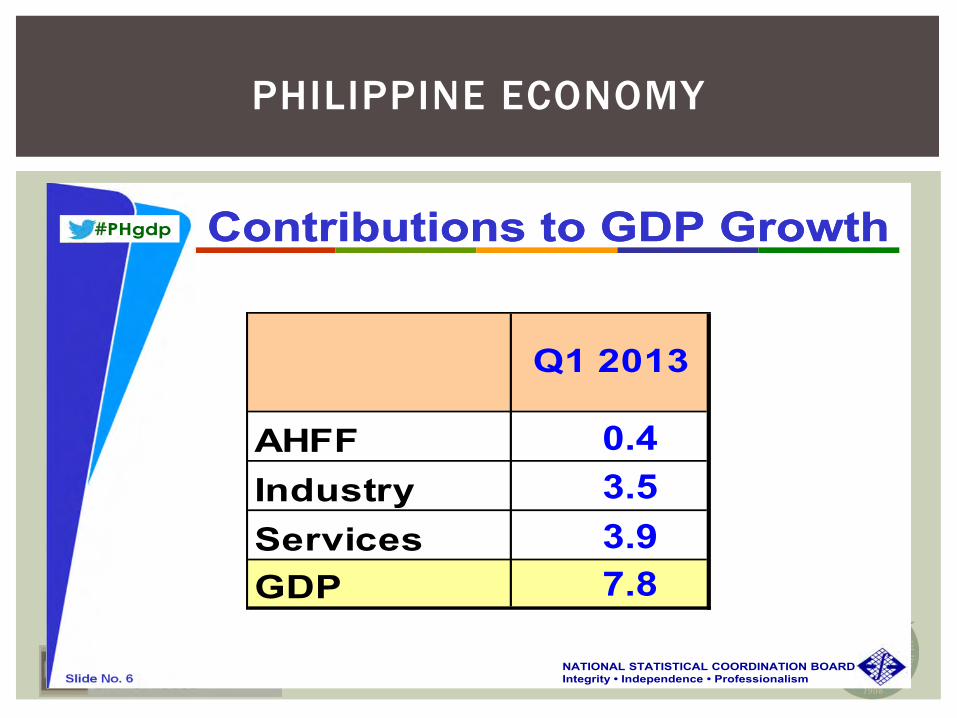

Slide No. 6NATIONAL STATISTICAL COORDINATION BOARDIntegrity • Independence • Professionalism

#PHgdp Contributions to GDP GrowthContributions to GDP Growth

AHFFIndustryServicesGDP

Q1 2013

3.9

0.43.5

7.8

PHILIPPINE ECONOMY

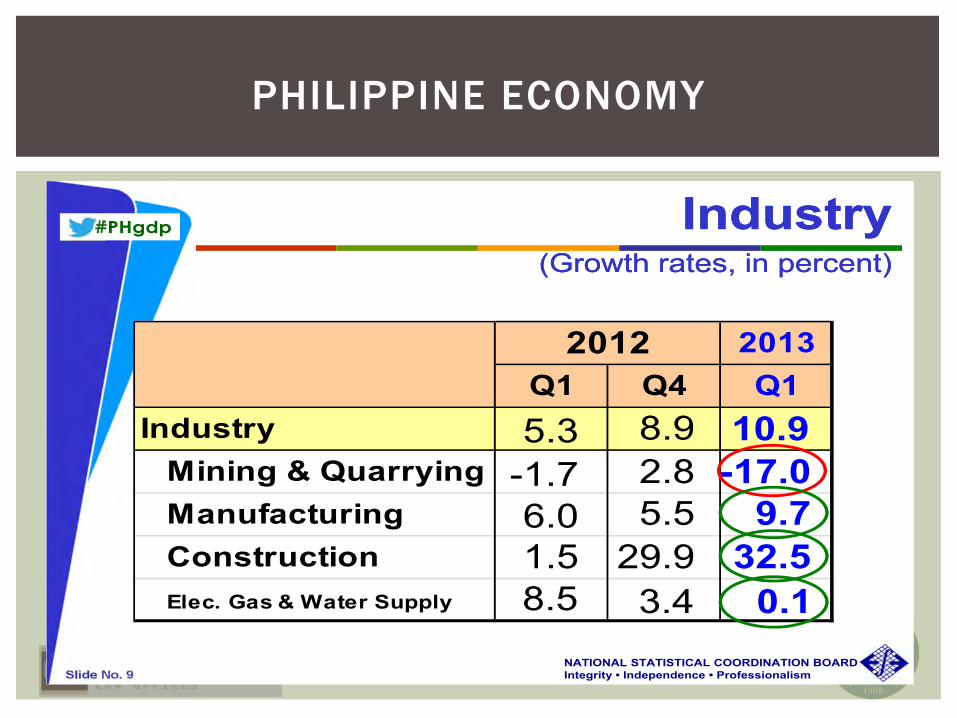

Slide No. 9NATIONAL STATISTICAL COORDINATION BOARDIntegrity • Independence • Professionalism

#PHgdp Industry(Growth rates, in percent)

Industry(Growth rates, in percent)

2013Q1 Q4 Q1

Industry Mining & Quarrying Manufacturing Construction Elec. Gas & Water Supply

2012

9.7

10.9-17.0

32.50.1

8.9

5.52.8

29.93.4

6.0

5.3-1.7

1.58.5

PHILIPPINE ECONOMY

Slide No. 11NATIONAL STATISTICAL COORDINATION BOARDIntegrity • Independence • Professionalism

#PHgdp

TOP CONTRIBUTORS TO GROWTH OF MFG.First Quarter 2013

Food Manufactures 5.1

Manufacturing(Contribution to Growth, in percentage point)

Manufacturing(Contribution to Growth, in percentage point)

Radio, television and communication equipment and apparatus 4.0Chemical & chemical products 1.0Basic metal industries 0.8Machinery and equipment except electrical 0.3

PHILIPPINE ECONOMY

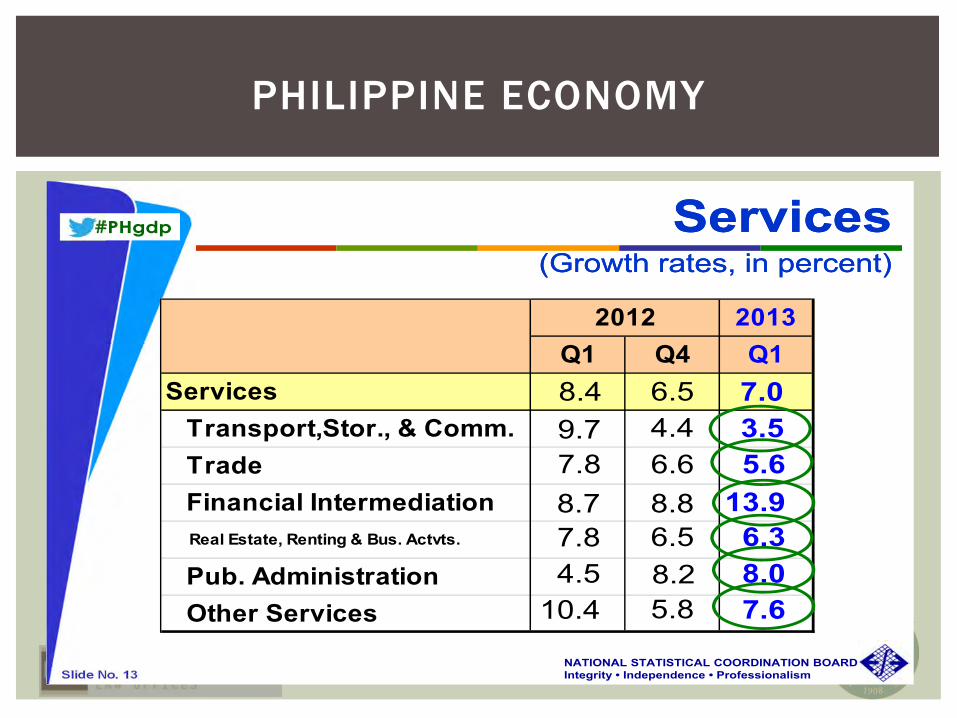

Slide No. 13NATIONAL STATISTICAL COORDINATION BOARDIntegrity • Independence • Professionalism

#PHgdp Services(Growth rates, in percent)

Services(Growth rates, in percent)

2013Q1 Q4 Q1

Services Transport,Stor., & Comm. Trade Financial Intermediation Real Estate, Renting & Bus. Actvts.

Pub. Administration Other Services

2012

7.0

5.63.5

8.06.3

7.6

13.9

6.5

6.64.4

8.86.58.25.8

8.49.77.88.77.84.5

10.4

PHILIPPINE ECONOMY

PHILIPPINE DOWNSTREAM OIL INDUSTRY FRAMEWORK

PH

ILIPP

INES

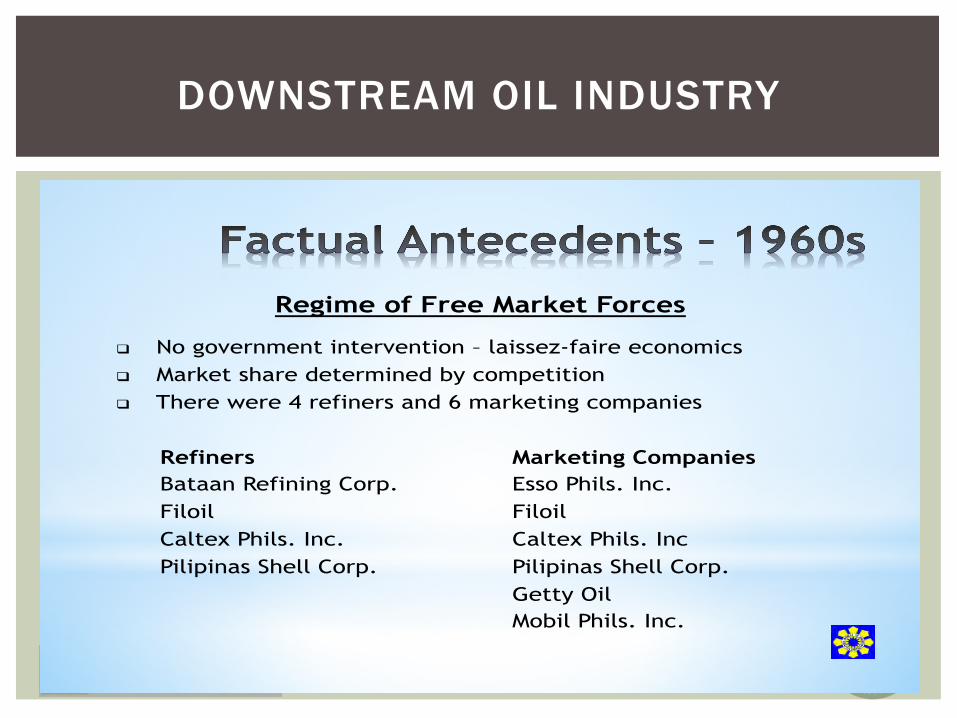

Regime of Free Market Forces

! No government intervention – laissez-faire economics

! Market share determined by competition

! There were 4 refiners and 6 marketing companies

Refiners Marketing Companies

Bataan Refining Corp. Esso Phils. Inc.

Filoil Filoil

Caltex Phils. Inc. Caltex Phils. Inc

Pilipinas Shell Corp. Pilipinas Shell Corp.

Getty Oil

Mobil Phils. Inc.

DOWNSTREAM OIL INDUSTRY

The Dawn of Regulation

! RA 6124 (1970) – created the Price Control Council to set

maximum selling prices of essential commodities

! RA 6173 (1971) – created the Oil Industry Commission (OIC); oil

price regulation was introduced

! PD 334 (1973) – formed the Philippine National Oil Company;

entry of the government in the oil industry

! PD 1206 (1977) – abolished OIC but created 2 separate agencies:

(1) Board of Energy to regulate domestic oil prices and (2) Dept.

of Energy, later renamed to Ministry of Energy, to formulate

energy policies and programs

DOWNSTREAM OIL INDUSTRY

The Subsidy Regime: CPEF and OPSF

! In 1979, a Consumer Price Equalization Fund (CPEF) was established to avoid frequent oil price movements; CPEF was abolished in June 1983

! PD 1956 (1984) – created the Oil Price Stabilization Fund (OPSF) to stabilize the domestic price of petroleum products

! Letter of Instruction No. 1441 (1984) – directed BOE, in consultation with MOE, to review and reset domestic oil prices every 2 months starting January 1985 to reflect prevailing price of crude oil and petroleum products

! Executive Order No. 172 – created the Energy Regulatory Board (ERB) to replace BOE

DOWNSTREAM OIL INDUSTRY

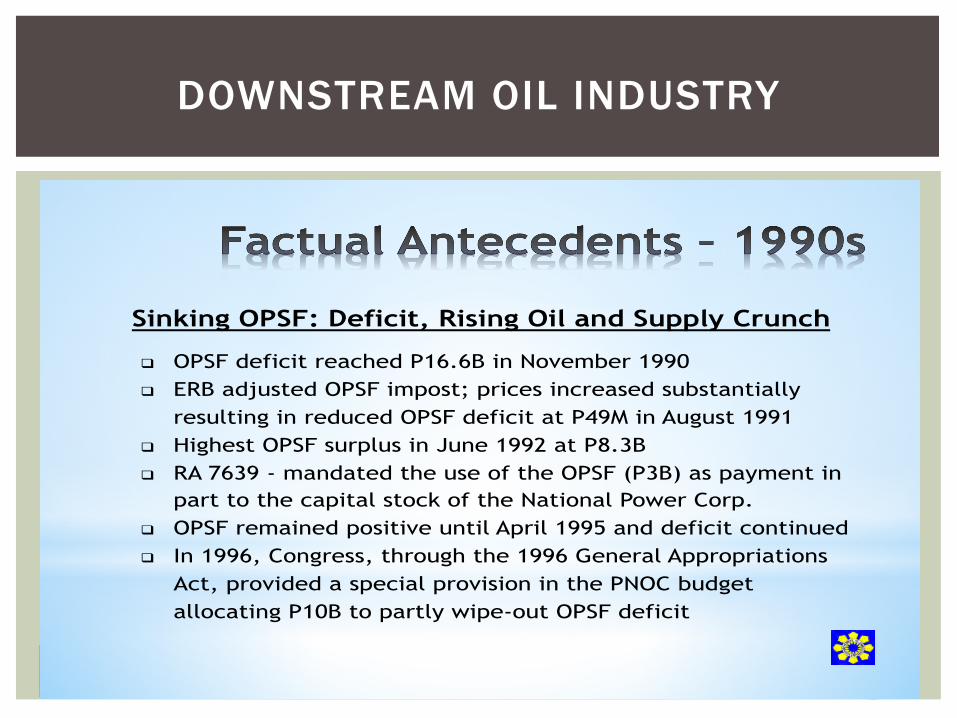

Sinking OPSF: Deficit, Rising Oil and Supply Crunch

! OPSF deficit reached P16.6B in November 1990 ! ERB adjusted OPSF impost; prices increased substantially

resulting in reduced OPSF deficit at P49M in August 1991 ! Highest OPSF surplus in June 1992 at P8.3B ! RA 7639 - mandated the use of the OPSF (P3B) as payment in

part to the capital stock of the National Power Corp. ! OPSF remained positive until April 1995 and deficit continued ! In 1996, Congress, through the 1996 General Appropriations

Act, provided a special provision in the PNOC budget allocating P10B to partly wipe-out OPSF deficit

DOWNSTREAM OIL INDUSTRY

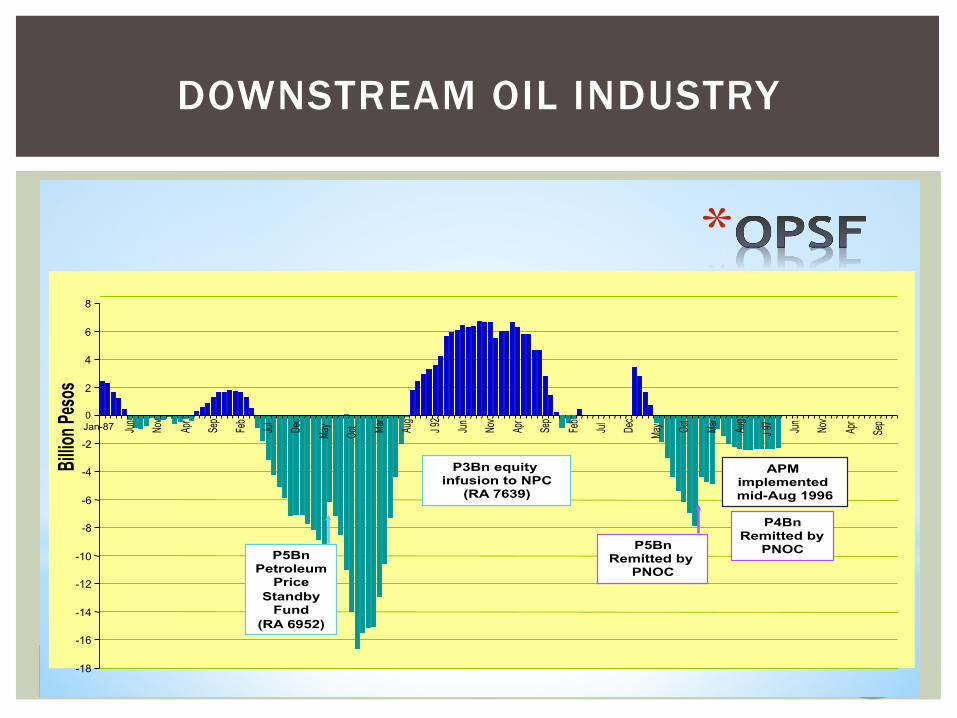

-18 -16 -14 -12 -10

-8 -6 -4 -2 0

2 4 6 8

Jan-87 Jun

Nov

Apr

Sep

Feb

Jul

Dec

May

Oct Ma

r

Aug

J 92

Jun

Nov

Apr

Sep

Feb

Jul

Dec

May Oc

t

Mar

Aug

J 97 Jun

Nov

Apr

Sep

Billio

n Pes

os

P5Bn Petroleum

Price Standby

Fund (RA 6952)

P3Bn equity infusion to NPC

(RA 7639)

P5Bn Remitted by

PNOC

P4Bn Remitted by

PNOC

APM implemented mid-Aug 1996

*

DOWNSTREAM OIL INDUSTRY

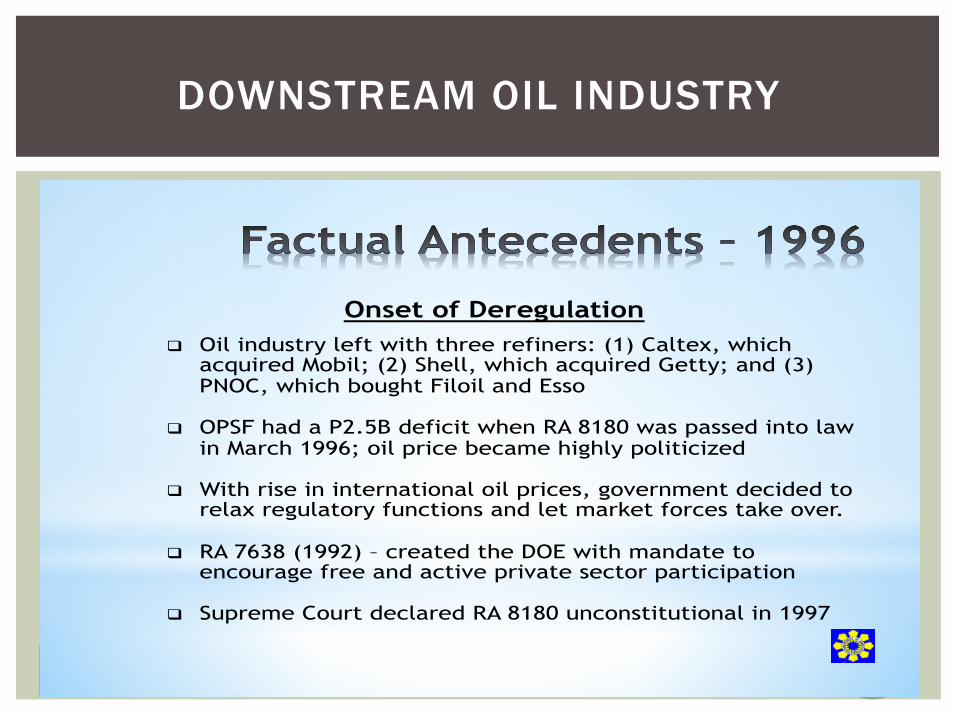

Onset of Deregulation

! Oil industry left with three refiners: (1) Caltex, which acquired Mobil; (2) Shell, which acquired Getty; and (3) PNOC, which bought Filoil and Esso

! OPSF had a P2.5B deficit when RA 8180 was passed into law in March 1996; oil price became highly politicized

! With rise in international oil prices, government decided to

relax regulatory functions and let market forces take over.

! RA 7638 (1992) – created the DOE with mandate to encourage free and active private sector participation

! Supreme Court declared RA 8180 unconstitutional in 1997

DOWNSTREAM OIL INDUSTRY

Transition Phase to Full Deregulation

! RA 8479 – New Downstream Oil Deregulation Law signed in

February 1998

! Automatic pricing mechanism - adjusted the wholesale posted prices of petroleum products based on the changes in Singapore Posted Prices. APM enabled adjustments in domestic prices to approximate closely and reflect promptly the movement of international prices of oil

! Executive Order No. 471 (1998) declared full deregulation of

the downstream oil industry

DOWNSTREAM OIL INDUSTRY

DUBAI CRUDE PRICES/FOREX March 1984 – MTD August 2011

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

M-84

J-85

N-85

S-86

J-87

M-88

M-89

J-90

N-90

S-91

J-92

M-93

M-94

J-95

N-95

S-96

J-97

M-98

M-99

J-00

N-00

S-01

J-02

M-03

M-04

J-05

N-05

S-06

J-07

M-08

M-09

J-10

N-10

S-11

0

5

10

15

20

25

30

35

40

45

50

55

60

Dubai US$/bbl Dubai P/li Forex P/1$

$/bbl P/$

I. Energy Reform Agenda II. Renewable Energy Resources

III. Upstream Oil and Gas Resources

IV. Coal Resources V. Downstream Oil and Gas Resources

DISCUSSION OUTLINE

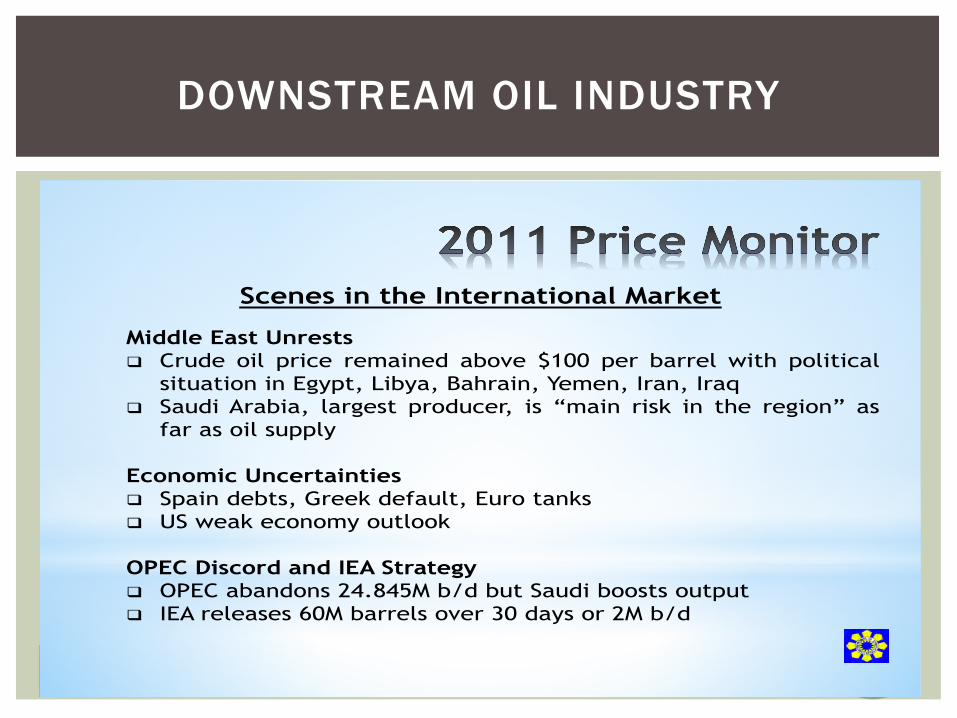

Scenes in the International Market

Middle East Unrests ! Crude oil price remained above $100 per barrel with political

situation in Egypt, Libya, Bahrain, Yemen, Iran, Iraq ! Saudi Arabia, largest producer, is “main risk in the region” as

far as oil supply

Economic Uncertainties ! Spain debts, Greek default, Euro tanks ! US weak economy outlook

OPEC Discord and IEA Strategy ! OPEC abandons 24.845M b/d but Saudi boosts output ! IEA releases 60M barrels over 30 days or 2M b/d

DOWNSTREAM OIL INDUSTRY

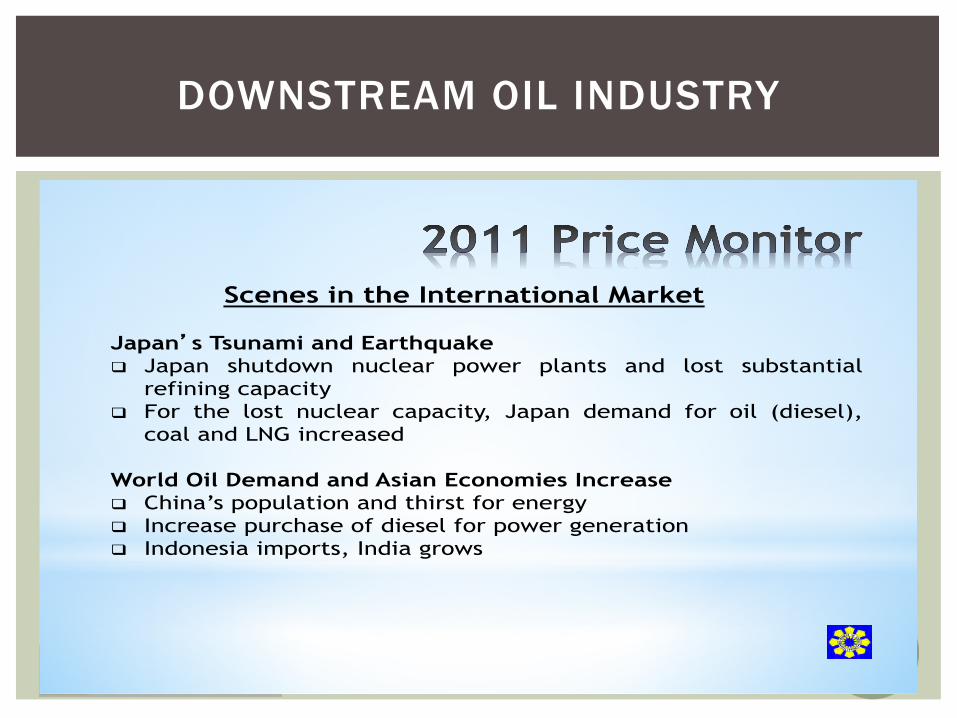

Scenes in the International Market Japan�s Tsunami and Earthquake ! Japan shutdown nuclear power plants and lost substantial

refining capacity

! For the lost nuclear capacity, Japan demand for oil (diesel),

coal and LNG increased

World Oil Demand and Asian Economies Increase ! China’s population and thirst for energy

! Increase purchase of diesel for power generation

! Indonesia imports, India grows

DOWNSTREAM OIL INDUSTRY

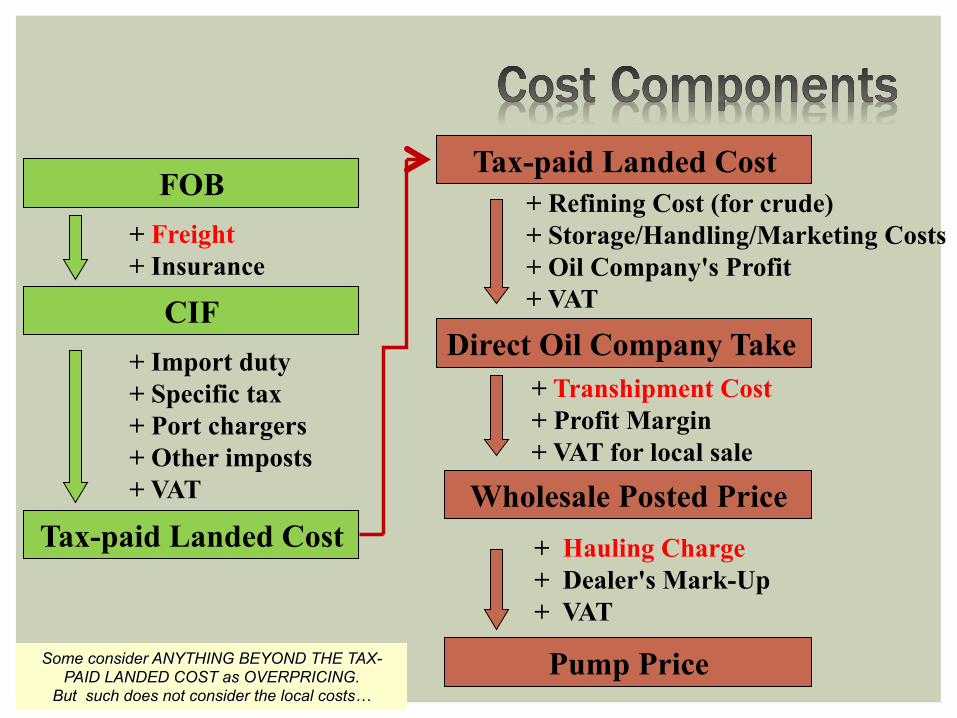

+ Refining Cost (for crude) + Storage/Handling/Marketing Costs + Oil Company's Profit + VAT

Wholesale Posted Price

Direct Oil Company Take

+ Hauling Charge + Dealer's Mark-Up + VAT

+ Transhipment Cost + Profit Margin + VAT for local sale

Pump Price

FOB

+ Freight + Insurance

+ Import duty + Specific tax + Port chargers + Other imposts + VAT Tax-paid Landed Cost

CIF

Tax-paid Landed Cost

Some consider ANYTHING BEYOND THE TAX-PAID LANDED COST as OVERPRICING.

But such does not consider the local costs…

2011 PRICE MONITOR The ERB Formula

AUTOMATIC PRICING MECHANISMComputation of the estimated adjustment for the week

LANDED COST (Product) Past Week Present WeekUS$ PER BARREL

FOB (MOPS*) a1 a2

FREIGHT PLUS b1 b2

CIF c1 = a1+b1 c2 = a2+b2

EXCHANGE RATE d1 d2

PESO LANDED COST

CIF e1 = c1*d1 e2 = c2*d2

DUTY: f1 = e1*__% f2 = e2*__%

OCEAN LOSS g1 = e1*0.5% g2 = e2*0.5%

TOTAL (Without VAT) h1 = e1+f1+g1 h2 = e2+f2+g2

TOTAL (With VAT) i1 = h1 * 1.12 i2 = h2 * 1.12

PESO LANDED COST, P/li j1 = i1/159 j2 = i2/159

DIFFERENCE

Peso/barrel k2 = i2 - i1

Peso/liter l2 = k2/159

* MOPS of ULG, Diesel, IFO or LPG (Contract Price, CP)

Note: The value appearing in l2 is the estimated adjustment in the price

of the product for the monthWPP = Landed Cost + Oil company Margin + Specific Tax + VATPP = WPP + Dealers/Haulers Margin

1. Energy Supply and Demand Situation

2. Philippines GDP: Drivers of Oil Demand

3. The Downstream Oil Industry

4. Tapping Russia as New Supply Center

5. Next Steps

DOWNSTREAM OIL INDUSTRY

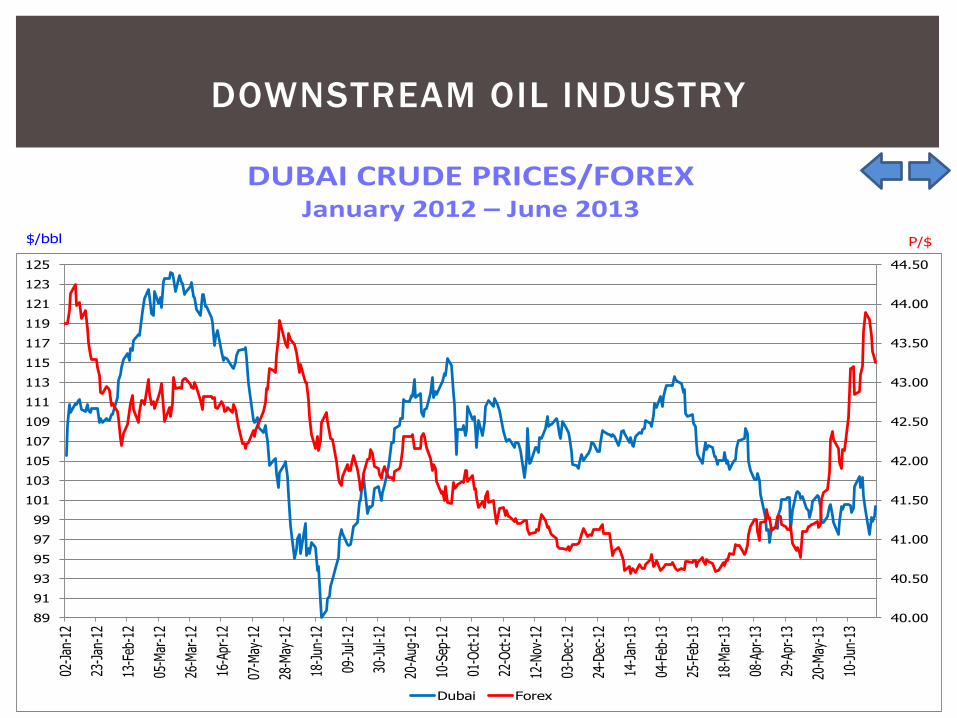

DUBAI CRUDE PRICES/FOREX January 2012 – June 2013

$/bbl P/$

40.00

40.50

41.00

41.50

42.00

42.50

43.00

43.50

44.00

44.50

89

91

93

95

97

99

101

103

105

107

109

111

113

115

117

119

121

123

125

02-Ja

n-12

23-Ja

n-12

13-F

eb-1

2

05-M

ar-1

2

26-M

ar-1

2

16-A

pr-1

2

07-M

ay-1

2

28-M

ay-1

2

18-Ju

n-12

09-Ju

l-12

30-Ju

l-12

20-A

ug-1

2

10-S

ep-1

2

01-O

ct-12

22-O

ct-12

12-N

ov-1

2

03-D

ec-1

2

24-D

ec-1

2

14-Ja

n-13

04-F

eb-1

3

25-F

eb-1

3

18-M

ar-1

3

08-A

pr-1

3

29-A

pr-1

3

20-M

ay-1

3

10-Ju

n-13

Dubai Forex

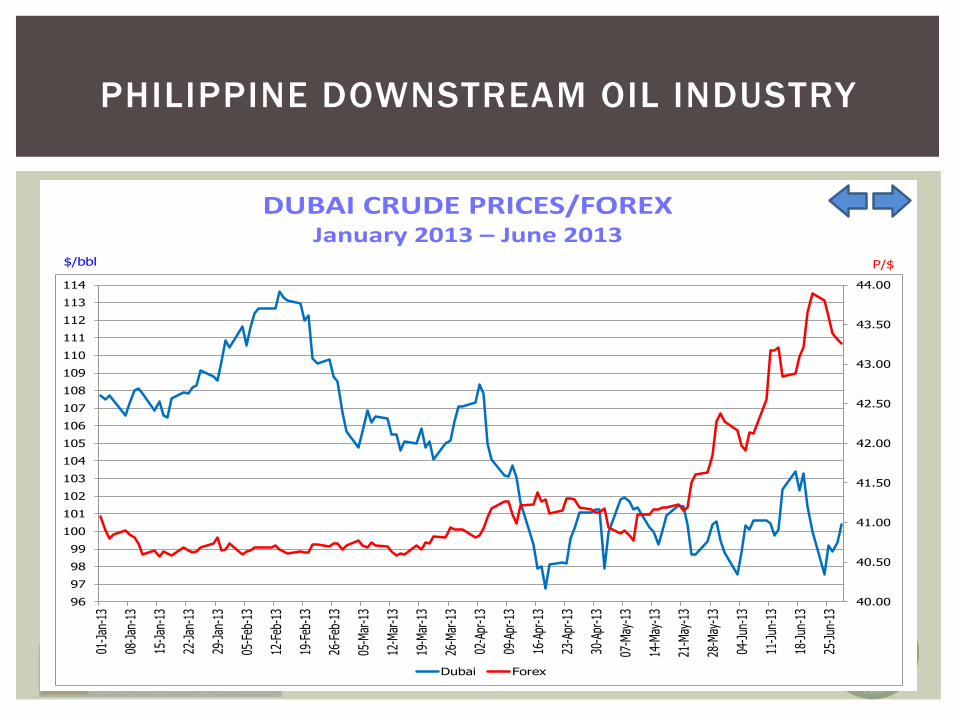

DUBAI CRUDE PRICES/FOREX January 2013 – June 2013

$/bbl P/$

40.00

40.50

41.00

41.50

42.00

42.50

43.00

43.50

44.00

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

01-Ja

n-13

08-Ja

n-13

15-Ja

n-13

22-Ja

n-13

29-Ja

n-13

05-F

eb-1

3

12-F

eb-1

3

19-F

eb-1

3

26-F

eb-1

3

05-M

ar-1

3

12-M

ar-1

3

19-M

ar-1

3

26-M

ar-1

3

02-A

pr-1

3

09-A

pr-1

3

16-A

pr-1

3

23-A

pr-1

3

30-A

pr-1

3

07-M

ay-1

3

14-M

ay-1

3

21-M

ay-1

3

28-M

ay-1

3

04-Ju

n-13

11-Ju

n-13

18-Ju

n-13

25-Ju

n-13

Dubai Forex

PHILIPPINE DOWNSTREAM OIL INDUSTRY

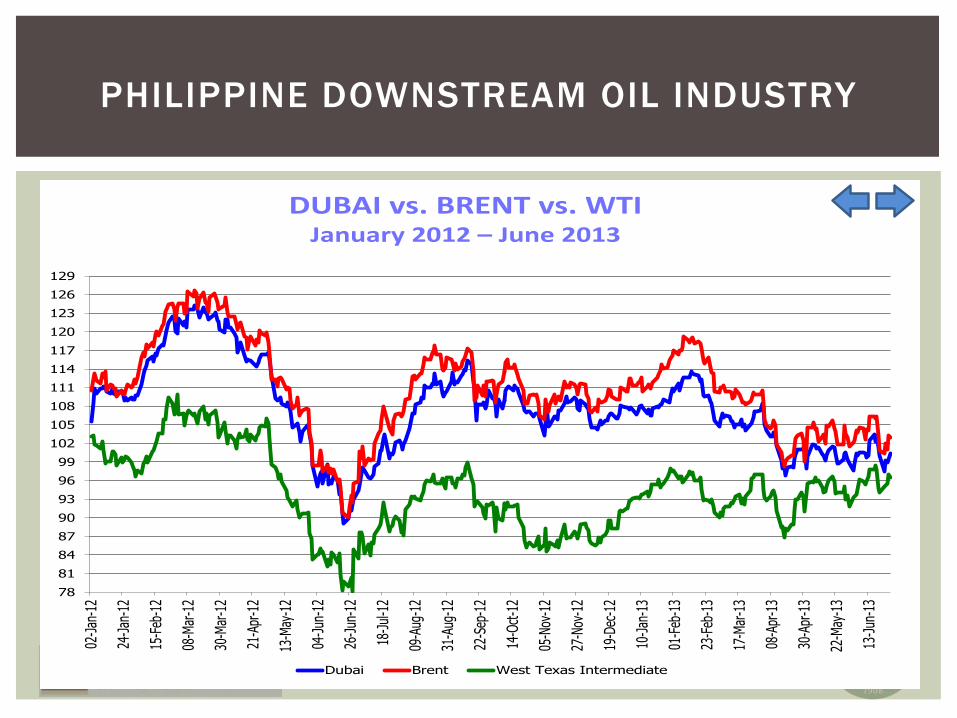

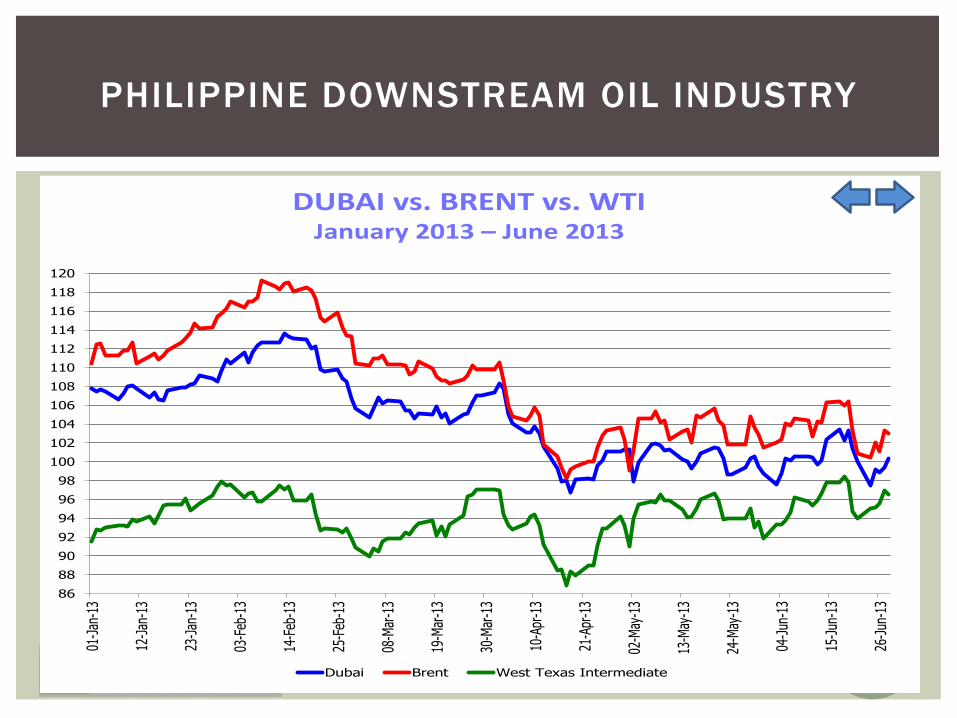

DUBAI vs. BRENT vs. WTI January 2012 – June 2013

$/bbl

78

81

84

87

90

93

96

99

102

105

108

111

114

117

120

123

126

129

02-Ja

n-12

24-Ja

n-12

15-F

eb-1

2

08-M

ar-1

2

30-M

ar-1

2

21-A

pr-1

2

13-M

ay-1

2

04-Ju

n-12

26-Ju

n-12

18-Ju

l-12

09-A

ug-1

2

31-A

ug-1

2

22-S

ep-1

2

14-O

ct-12

05-N

ov-1

2

27-N

ov-1

2

19-D

ec-1

2

10-Ja

n-13

01-F

eb-1

3

23-F

eb-1

3

17-M

ar-1

3

08-A

pr-1

3

30-A

pr-1

3

22-M

ay-1

3

13-Ju

n-13

Dubai Brent West Texas Intermediate

PHILIPPINE DOWNSTREAM OIL INDUSTRY

DUBAI vs. BRENT vs. WTI January 2005 – MTD September 2013

$/bbl

35

45

55

65

75

85

95

105

115

125

135

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Dubai Brent West Texas Intermediate

DUBAI vs. BRENT vs. WTI January 2013 – June 2013

$/bbl

86

88

90

92

94

96

98

100

102

104

106

108

110

112

114

116

118

120

01-Ja

n-13

12-Ja

n-13

23-Ja

n-13

03-F

eb-1

3

14-F

eb-1

3

25-F

eb-1

3

08-M

ar-1

3

19-M

ar-1

3

30-M

ar-1

3

10-A

pr-1

3

21-A

pr-1

3

02-M

ay-1

3

13-M

ay-1

3

24-M

ay-1

3

04-Ju

n-13

15-Ju

n-13

26-Ju

n-13

Dubai Brent West Texas Intermediate

PHILIPPINE DOWNSTREAM OIL INDUSTRY

METRO MANILA PRICING Gasoline P/li

30323436384042444648505254565860626466

2/2-

6

4/13

-17

6/22

-26

8/31

-9/4

11/9

-13

1/18

-22

3/29

-4/2

6/7-

11

8/16

-20

10/2

5-29

1/3-

7/11

3/14

-18

5/23

-27

8/1-

5

10/1

0-14

12/1

9-23

2/27

-3/2

5/7-

11

7/16

-20

9/24

-28

12/3

-7

2/11

-15

4/22

-26

Calculated Based on Adviced Adjustments (Suggested Retail Price)

Calculated from Mean of Platts Singapore

Common Price Metro Manila

PHILIPPINE DOWNSTREAM OIL INDUSTRY

PHILIPPINE DOWNSTREAM OIL INDUSTRY

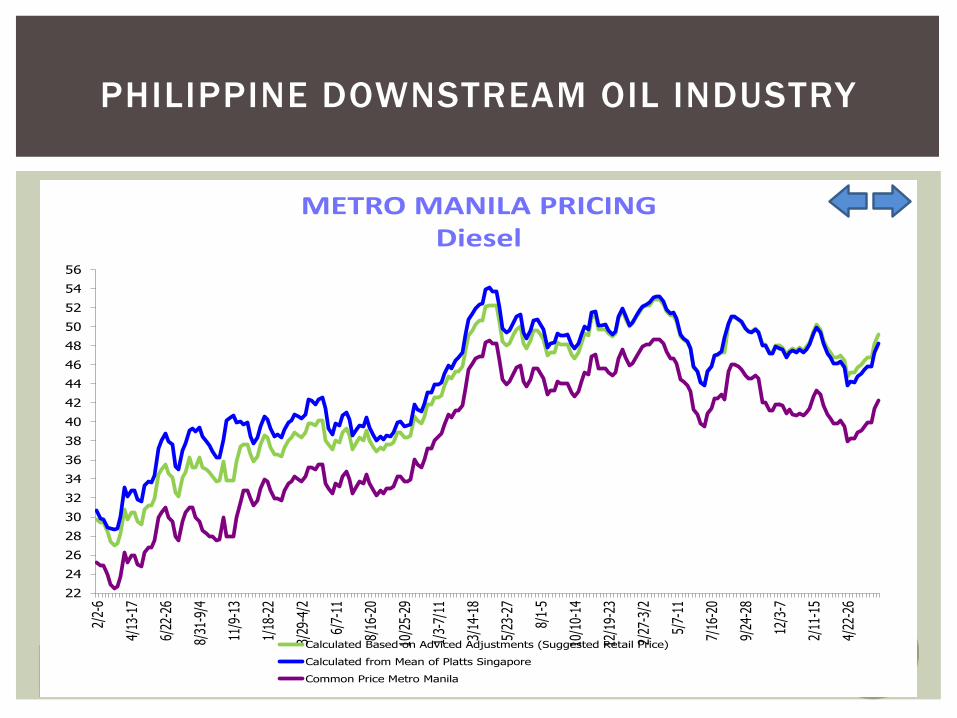

METRO MANILA PRICING Diesel P/li

22

24

26

28

30

32

34

36

38

40

42

44

46

48

50

52

54

56

2/2-

6

4/13

-17

6/22

-26

8/31

-9/4

11/9

-13

1/18

-22

3/29

-4/2

6/7-

11

8/16

-20

10/2

5-29

1/3-

7/11

3/14

-18

5/23

-27

8/1-

5

10/1

0-14

12/1

9-23

2/27

-3/2

5/7-

11

7/16

-20

9/24

-28

12/3

-7

2/11

-15

4/22

-26

Calculated Based on Adviced Adjustments (Suggested Retail Price)

Calculated from Mean of Platts Singapore

Common Price Metro Manila

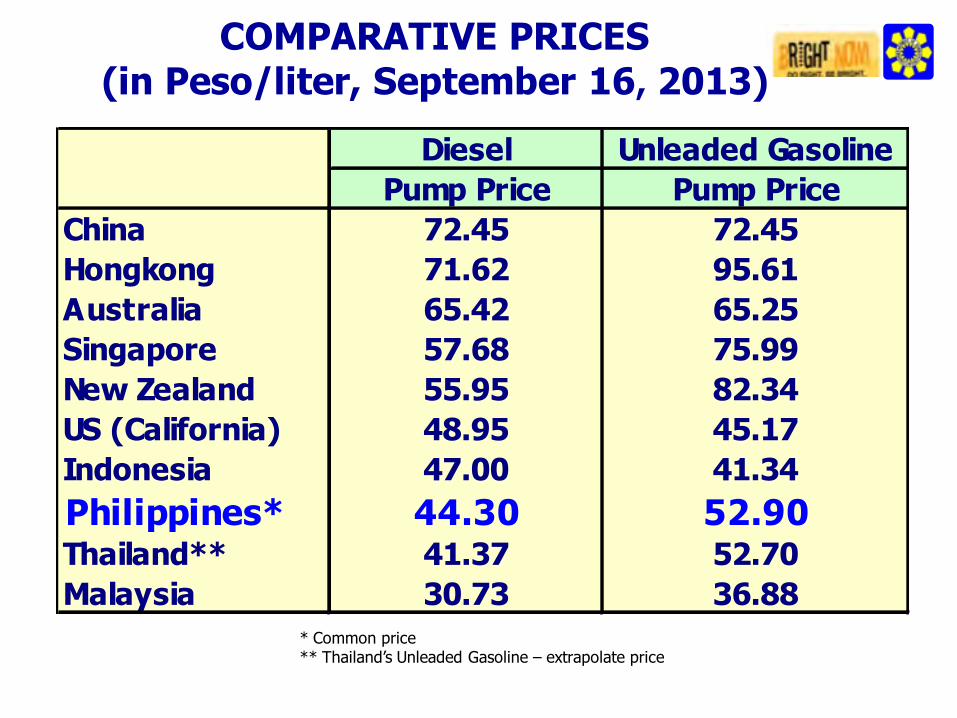

COMPARATIVE PRICES (in Peso/liter, September 16, 2013)

* Common price** Thailand’s Unleaded Gasoline – extrapolate price

Diesel Unleaded GasolinePump Price Pump Price

China 72.45 72.45Hongkong 71.62 95.61Australia 65.42 65.25Singapore 57.68 75.99New Zealand 55.95 82.34US (California) 48.95 45.17Indonesia 47.00 41.34Philippines* 44.30 52.90Thailand** 41.37 52.70Malaysia 30.73 36.88

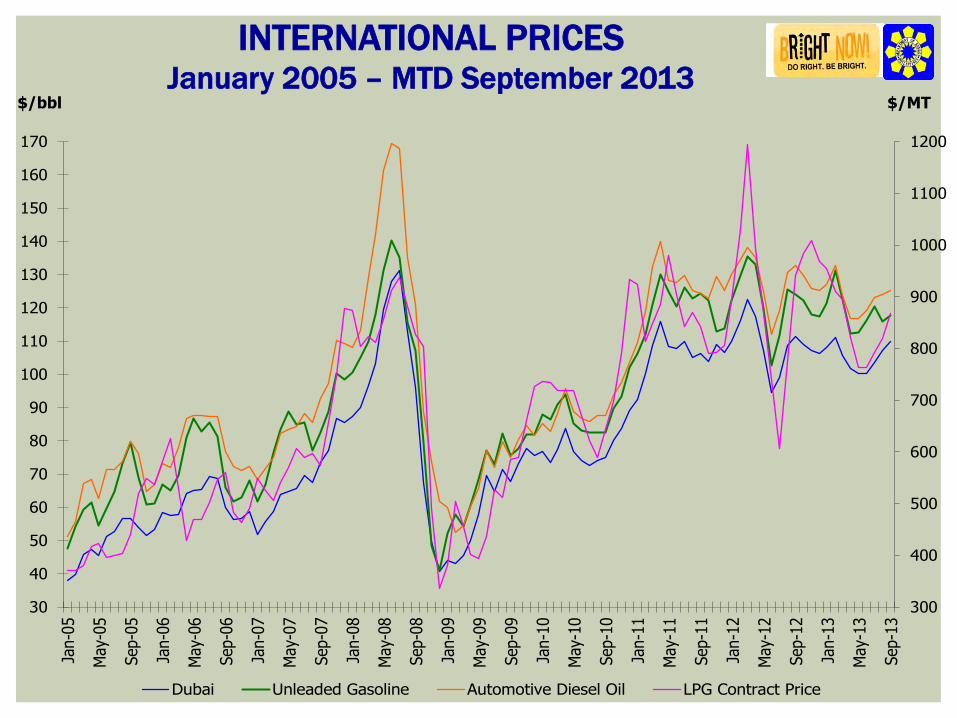

INTERNATIONAL PRICES

January 2005 – MTD September 2013 $/bbl $/MT

300

400

500

600

700

800

900

1000

1100

1200

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Dubai Unleaded Gasoline Automotive Diesel Oil LPG Contract Price

TAPPING RUSSIA AS MAJOR SUPPLY SOURCE

PH

ILIPP

INES

CRUDE OIL IMPORTATION

Country of Origin 2008 2009 2010 2011 2012 1H 2103

Saudi Arabia 46,603 22,578 30,359 30,795 29,784 8,197

Iran 1,915 819 5,874 0 0

UAE 13,054 10,144 18,088 14,730 16,230 5,145

Qatar 0 8,372 4,273 1,551 5,018 3,730

Middle East 61,572 42,243 54,232 52,955 51,032 18,122

ASEAN (Malaysia, Indonesia, Brunei, Singapore, Vietnam

6,121 5,168 7,335 2,341 3,176 1,159

Russia 180 2,782 5,207 14,318 9,508 6,540

¡ Less vulnerability to oil price fluctuation in Middle East (lower price)

¡ Supply security (3rd largest after US and out-produced Saudi Arabia by 1.15 million barrels per day in 2013)

¡ Multiple sources: Rosneft, Lukoil, Gazprom, Tatneft, etc.)

¡ Stable energy strategy and reserves § 17.8 billion tonnes of proven oil reserves § 48.8 trillion cubic meters of gas

¡ Russian energy policy shift to Asia and China

TAPPING RUSSIA AS SUPPLIER

DEPARTMENT OF ENERGY PROGRAMS

RESOURCE DEVELOPMENT

AYALA ECONOMIC BRIEFING August 23, 2011

POLITICAL ISSUES

DEPARTMENT OF ENERGY PROGRAMS

RESOURCE DEVELOPMENT

AYALA ECONOMIC BRIEFING August 23, 2011

PLATTS

CR

UD

E OIL

MA

RK

ETS A

SIA

20

13

G

oodwood P

ark Hotel, S

ingapore S

eptember 1

8-1

9, 2

01

3

Developing New Supply Opportunities with Russia:

The Philippines’ Perspective ATTY. JOSE M. LAYUG, JR.

Senior Partner , Puno & Puno Law Offices Philippine Energy Expert, University of the

Philippines College of Law

Related Documents