Developing Natural Gas Infrastructure in the Americas: the Mexican case NARUC Committee on Gas Francisco Salazar Diez de Sollano Chairman, CRE July 17, 2007

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Developing Natural Gas Infrastructure in the Americas: the

Mexican case

NARUC Committee on Gas

Francisco Salazar Diez de SollanoChairman, CRE

July 17, 2007

Introduction: CRE

• CRE (Comisión Reguladora de Energía) was created in 1992 as a consulting body to the Secretary of Energy. Its objective was to prepare the rules that would regulate the relationship between the State’s utilities and the private investors in the power sector.

• In 1995, the Congress passed a reform opening the downstream activities in the natural gas sector. Then, CRE was also constituted as the formal regulator of the energy sector and was given operational and technical autonomy.

• CRE’s mandate is to promote the efficient development of the activities it regulates. In doing so, CRE looks for a balance between the interest of the consumers and that of the investors.

CRE’s regulation powers

Reserved to the State Open to private investment Regulated by CRE

Generation

CFE & LFC

National Transmission

Grid

Third Parties Others

ImportsImports / Exports

Power

Natural Gas Exploration

Marketing

Production

Processing.PMX Sales Transpo

rtStorage Distributio

n

LPG

Marketing

Production ProcessingPMX

Sales

Transmission

Generation Transmission

Distribution

PipelinePipeline

Distribution

Surface transport. Bottle Distribution

Storage

Natural gas demand

• According to the Ministry of Energy(1), natural gas demand was 6.549 bcfd in 2006 .

• 48% corresponded to the oil sector; 35.7% to the power sector; 14.6% to the industry (including Pemex Petrochemicals), and 1.6% to residential and other services.

• Natural gas demand is expected to increase at an overall annual rate of 3.9% over the next 10 years.

(1) Prospectiva del mercado de gas natural 2006-2015

Natural gas forecast 2005-2015

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MM

CFD

Demand

Supply

3.9 %

2.8 %

Source: SENER 2006 – 2015 Prospectiva del Mercado de Gas Natural

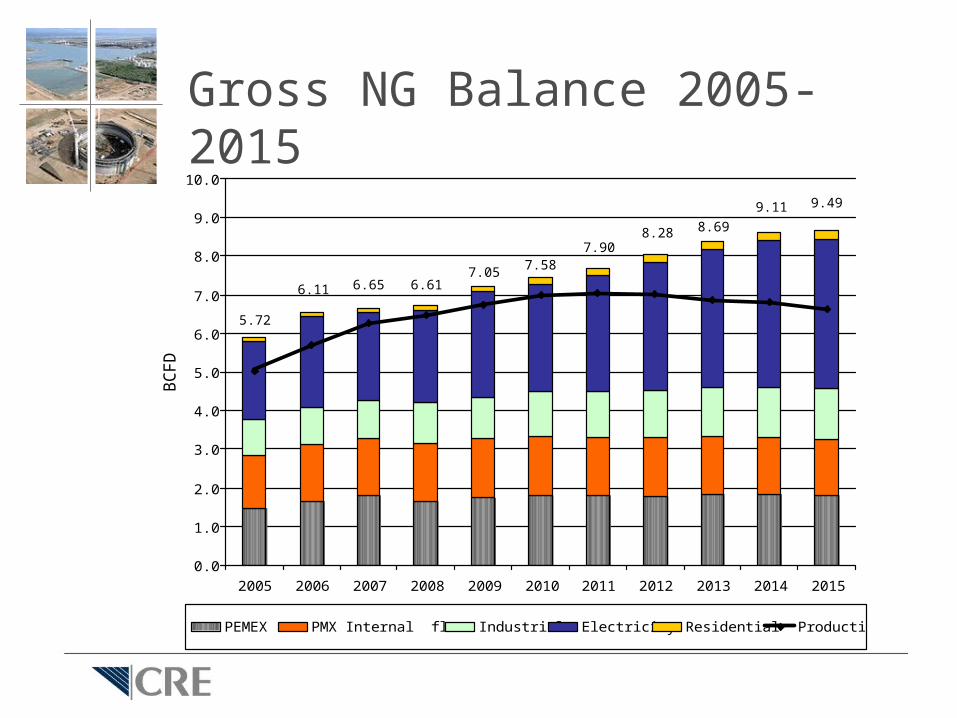

Gross NG Balance 2005-2015

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

BC

FD

PEMEX PMX Internal flows Industrial Electricity Residential Production

5.72

6.11 6.65 6.617.05 7.58

7.908.28 8.69

9.11 9.49

Natural gas for power plants

• Power forecasts 2005-2015– 4.8% annual demand growth rate from 191

TWh in 2005 to 305 TWh in 2015– 24 GW of new capacity required to meet

demand (approx. 49% of current capacity)– CFE will install 23,545 MW during the next

decade– Combined cycle power plants will grow from

33% to 51% of the total capacity by 2015• 7.3% average annual natural gas

growth over the next decade (for power)

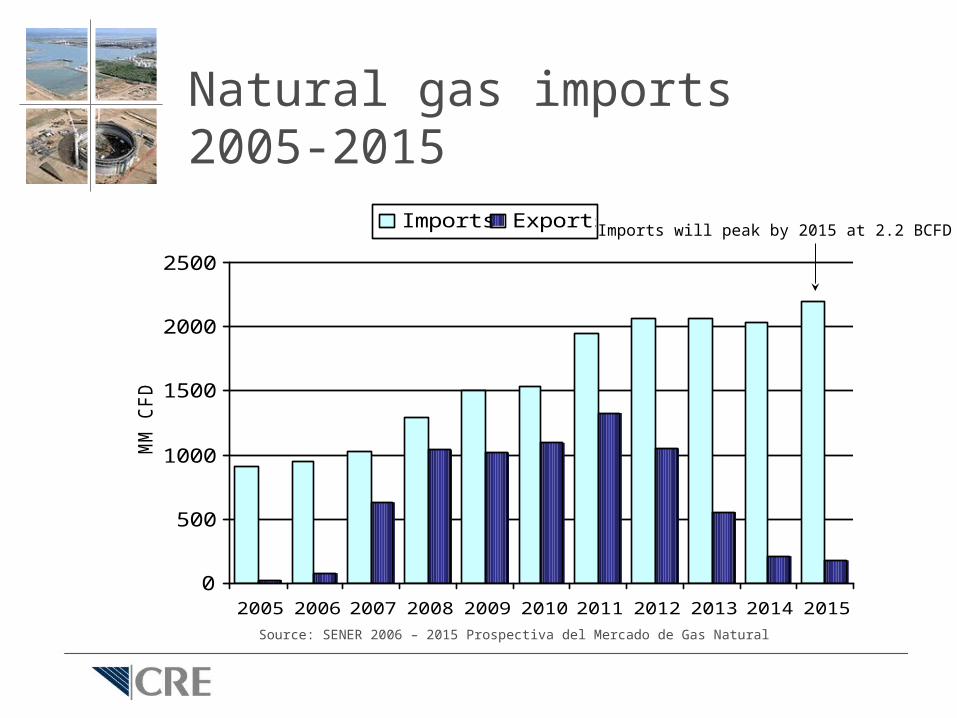

Natural gas imports 2005-2015

0

500

1000

1500

2000

2500

2005 20062007 2008 2009 20102011 2012 20132014 2015

MM

CFD

Imports Exports Imports will peak by 2015 at 2.2 BCFD

Source: SENER 2006 – 2015 Prospectiva del Mercado de Gas Natural

How to face increasing demand?

• Continue promoting private investment in– Development of LNG terminals along both

the Pacific and the Gulf coasts– Pipeline infrastructure both to strengthen

cross-interconnections and access to new LNG plants

• Start exploiting coal bed methane reserves• Focus Pemex’s investment in areas of

paramount interest such as exploration and production of oil and gas

CRE’s regulation objective

CRE’s regulation must:• Ensure technical engineering excellence through

modern standards and third-party auditing procedures

• Approve general terms of service that satisfy user’s needs and reflect current practice in industry

• Approve rates that are competitive and allow fair rates of return to investors

• Lead to predictable and stable regulatory conditions with adequate flexibility

Permits granted by CRE

Type Licenses Length (km)

Capital

Investment (MM USD)

Transport 155 12,354 1,979

Open Access

20 11,501 1,744

Non-Open Access

135 853 235

Distribution 22 35,494 1,669

LNG terminals 5 n.a.* 2,000

TOTAL 182 47,848 5,648

* LNG total storage capacity of 1,250,000 cubic metres

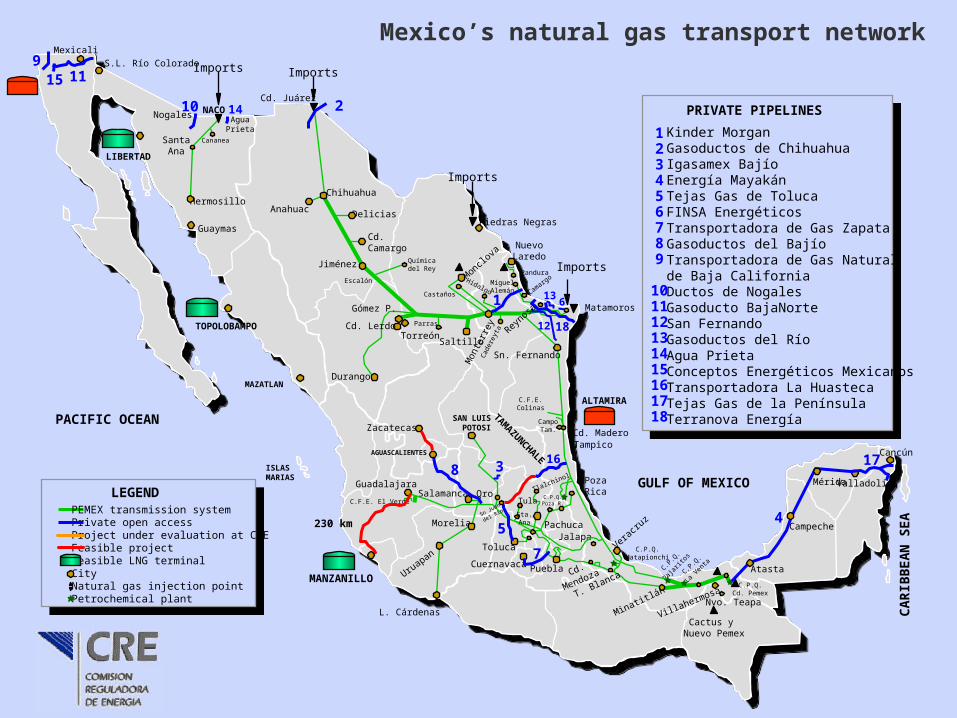

Mexico’s natural gas transport network

GULF OF MEXICO

CA

RIB

BEA

N S

EA

ISLASMARIAS

PACIFIC OCEAN

NACO

SantaAna

Hermosillo

Guaymas

Anahuac

Chihuahua

Delicias

Cd.Camargo

Jiménez Químicadel Rey

Monclo

va

SaltilloTorreón

Gómez P.

SAN LUISPOTOSI

SalamancaGuadalajara

Uruapan

Morelia

Toluca

Tula

Pachuca

Puebla

Jalapa

PozaRica

Verac

ruz

T. BlancaC.P

.Q.

Paja

ritos

Minatitlán

Nvo. TeapaVillahermosa

C.P.Q.Cd. Pemex

Atasta

Campeche

MéridaTlalchinol

Cactus y Nuevo Pemex

C.P.Q

.

La V

enta

Qro.

Cd. Juárez

Cd.

Mendoza

Cd. Lerdo

L. Cárdenas

Matamoros

Piedras Negras

S.L. Río ColoradoMexicali

NuevoLaredo

Imports Imports

Imports

Imports

Cd. MaderoTampico

Cuernavaca

Escalón

Durango

Castaños

Cad

erey

ta

Hidalgo

Parras

Camarg

oPandura

MiguelAlemán

Sn. Fernando

CampoTam.

C.F.E.Colinas

C.P.Q.Poza R.

C.P.Q.Matapionchi

C.F.E. El Verde

ALTAMIRA

MAZATLAN

911

10 2

1 6

3

5

7

8M

onte

rrey

Sta. Ana

Valladolid

4

PRIVATE PIPELINES

Kinder MorganGasoductos de ChihuahuaIgasamex BajíoEnergía MayakánTejas Gas de TolucaFINSA EnergéticosTransportadora de Gas ZapataGasoductos del BajíoTransportadora de Gas Naturalde Baja CaliforniaDuctos de NogalesGasoducto BajaNorteSan FernandoGasoductos del RíoAgua PrietaConceptos Energéticos MexicanosTransportadora La HuastecaTejas Gas de la PenínsulaTerranova Energía

123456789

101112131415161718

AGUASCALIENTES

Nogales

Sn Juan

del Río

Cancún

Cananea

AguaPrieta

13

14

12

TAMAZUN

CHALE16

15

17

TOPOLOBAMPO

LEGENDPEMEX transmission systemPrivate open access Project under evaluation at CREFeasible projectFeasible LNG terminalCityNatural gas injection pointPetrochemical plant

MANZANILLO

230 km

LIBERTAD

18Reyno

sa

Zacatecas

Developing LNG terminals

• LNG project solutions are varied – Having a predictable and transparent regulation

gives investors and developers the flexibility to structure their projects in a variety of ways

– Terminal Developers (TD) can participate in acquisition of LNG through different schemes

– TD can sign long-term contracts with utilities and shippers and/or assign all or a fraction of the terminal capacity to a marketing function

– Shippers can arrange for their LNG deliveries or have the terminal/marketer do it.

– CRE has resolved all LNG applications in approximately 12 – 18 months

Developing LNG Terminals

• Leading times are currently very long for LNG projects

• Construction time is typically 3 years • There is an increasing demand of LNG

terminals, especially in North America • Costs of steel and concrete have

increased significantly • Additionally, liquefaction plants have

been delayed in several countries

LNG regasification plants

Cd. Pemex

Cd Juarez

Chihuahua

MonterreyReynosa

Cd Madero

TolucaD.F.

PR

MexicaliTijuana

Naco

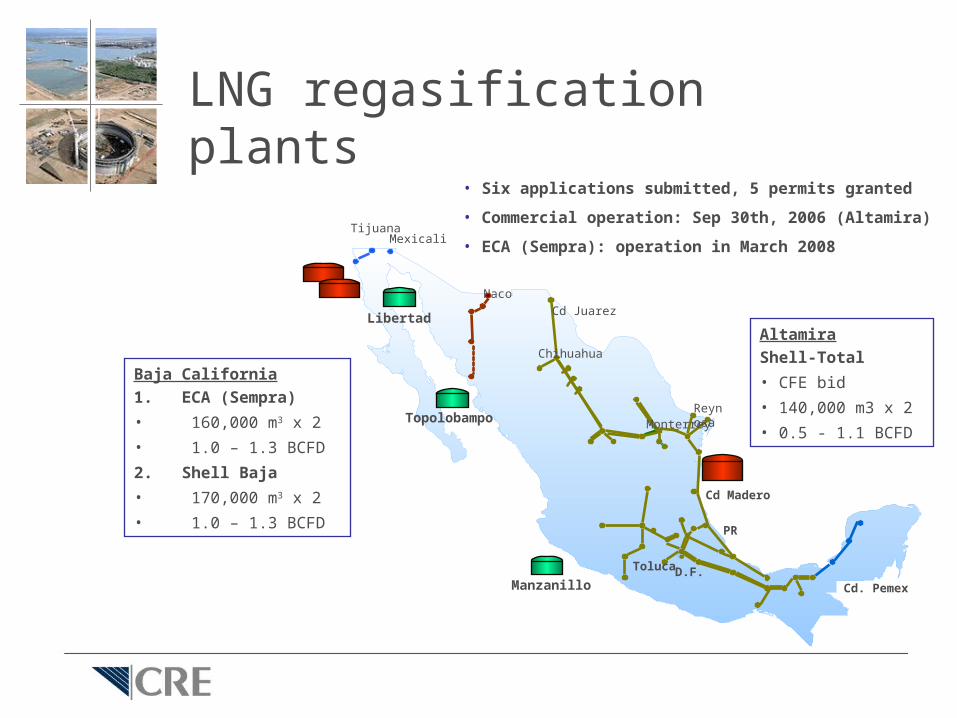

• Six applications submitted, 5 permits granted

• Commercial operation: Sep 30th, 2006 (Altamira)

• ECA (Sempra): operation in March 2008

Baja California1. ECA (Sempra)

• 160,000 m3 x 2

• 1.0 – 1.3 BCFD

2. Shell Baja

• 170,000 m3 x 2

• 1.0 – 1.3 BCFD

Manzanillo

AltamiraShell-Total

• CFE bid

• 140,000 m3 x 2

• 0.5 - 1.1 BCFD

Topolobampo

Libertad

Problems…

• Private projects associated to private industry and LDC’s have had limited success– Large consumers are reluctant to sign long term

contracts– Pemex’ supply and services are preferred– Competing fuels are priced with non-market criteria

• As a result, most transport and LNG infrastructure is tied to CFE’s need for CC generators and Pemex’ requirements

• Most of the new combined cycle power plants are located near Pemex’ transmission system or LNG terminals

• Both companies dominate the gas market

Towards a new transport model

• CRE is currently reviewing PEMEX SNG (national pipeline system) rates, the methodology to calculate them and the corresponding tariffs.

• The idea is prepare SNG to be the main part of a National Integrated Transport System (SNI)

• Issues being discussed include using a postage stamp instead of a mcf mile methodology, desired levels of central planning and expansion of the system, roll-in criteria, desired degree of competition, etc.

• Although SENER is responsible for energy policy and planning, CRE’s opinion is central in this issue.

Conclusions

• Natural gas foreseen demand’s growth in Mexico will require infrastructure to secure supply.

• So far, CRE has developed a predictable, transparent regulation that can accommodate flexibility to investors.

• Current infrastructure in Mexico has been mainly linked to CFE and PEMEX through long term contracts.

• New infrastructure to allow regional growth and active private participation in new projects poses regulatory challenges to the CRE.

Related Documents