DEVELOPING MACRO-STRESS TESTS SESSION 9 MINDAUGAS LEIKA 1

DEVELOPING MACRO-STRESS TESTS SESSION 9 MINDAUGAS LEIKA 1.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

DEVELOPING MACRO-STRESS TESTS

SESSION 9MINDAUGAS LEIKA

2

MACROPRUDENTIAL POLICY FRAMEWORK

I. Macroprudential policy definition, targets, policy transmission channels and relationships with other policies (Monday)

II. Institutional structure (Tuesday)

III. Policy tools (Tuesday)

IV. Risk identification and quantification: stress testing (This lecture)

AGENDA

What is macro stress testing?

Macro stress testing framework

Macro ST process

Use of stress tests

Did STs fail?

3

4

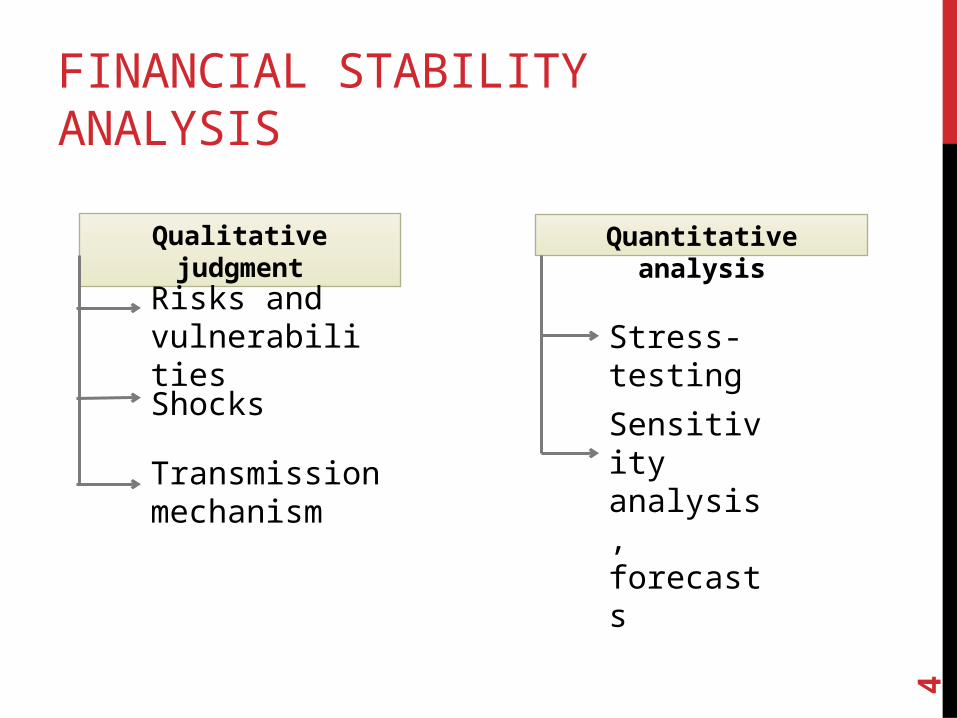

FINANCIAL STABILITY ANALYSIS

Quantitative analysisQualitative judgment

Risks and vulnerabilities

Shocks

Transmission mechanism

Stress-testing

Sensitivity analysis, forecasts

5

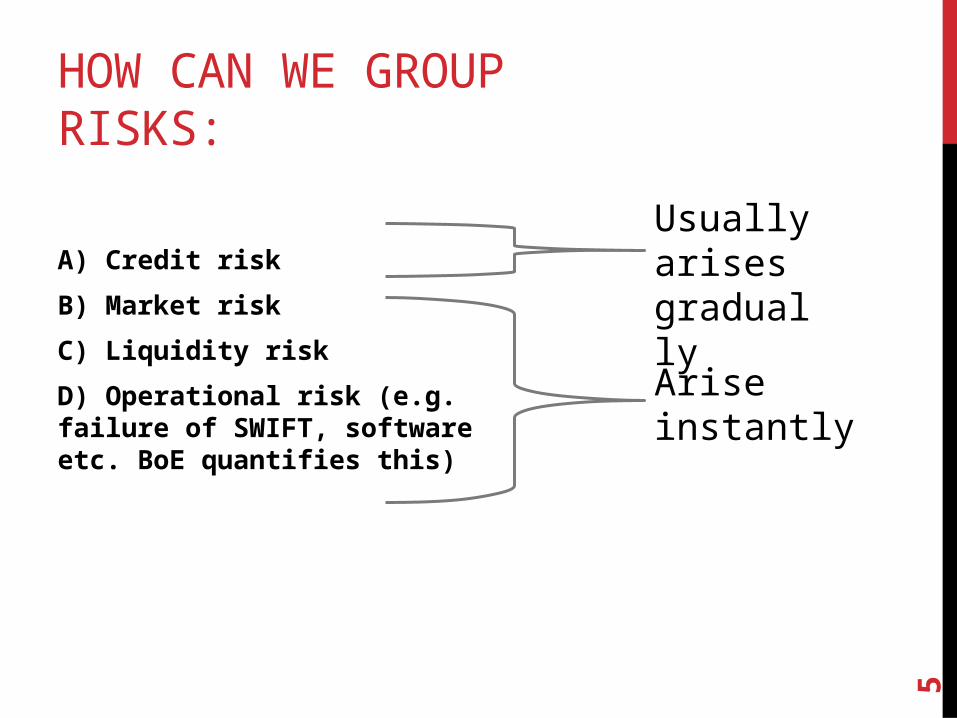

HOW CAN WE GROUP RISKS:

A) Credit risk

B) Market risk

C) Liquidity risk

D) Operational risk (e.g. failure of SWIFT, software etc. BoE quantifies this)

Arise instantly

Usually arises gradually

6

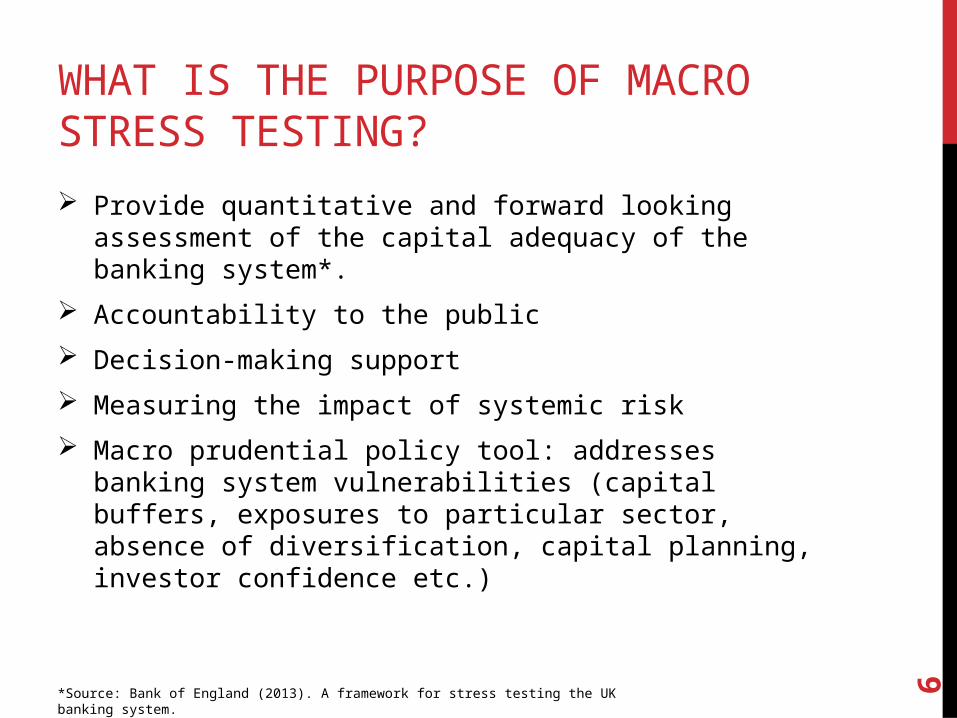

WHAT IS THE PURPOSE OF MACRO STRESS TESTING?

Provide quantitative and forward looking assessment of the capital adequacy of the banking system*.

Accountability to the public

Decision-making support

Measuring the impact of systemic risk

Macro prudential policy tool: addresses banking system vulnerabilities (capital buffers, exposures to particular sector, absence of diversification, capital planning, investor confidence etc.)

*Source: Bank of England (2013). A framework for stress testing the UK banking system.

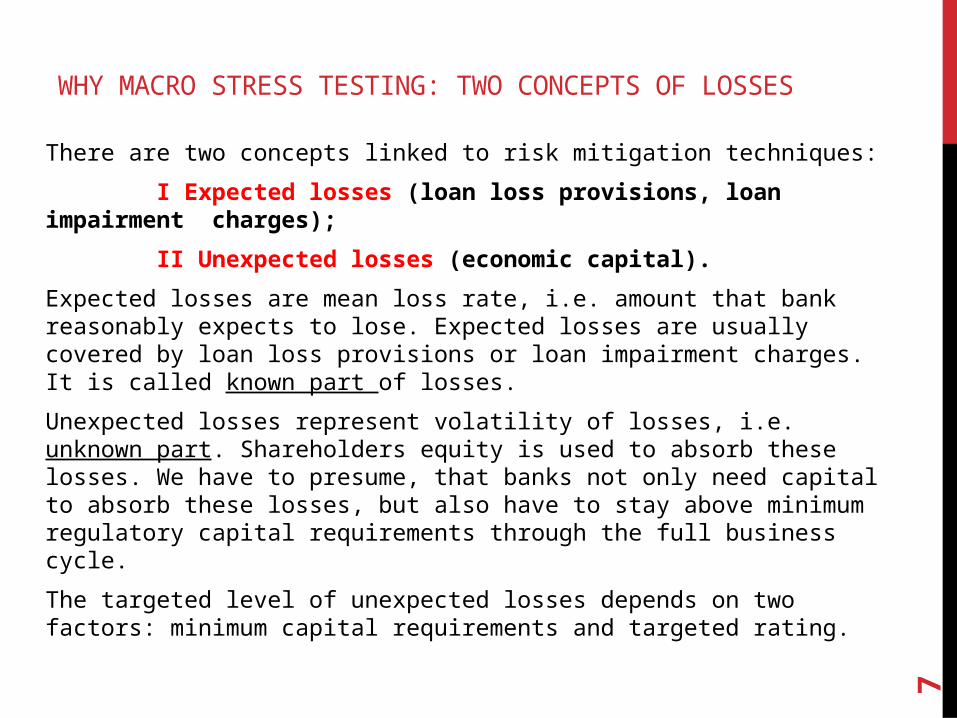

WHY MACRO STRESS TESTING: TWO CONCEPTS OF LOSSES

There are two concepts linked to risk mitigation techniques:

I Expected losses (loan loss provisions, loan impairment charges);

II Unexpected losses (economic capital).

Expected losses are mean loss rate, i.e. amount that bank reasonably expects to lose. Expected losses are usually covered by loan loss provisions or loan impairment charges. It is called known part of losses.

Unexpected losses represent volatility of losses, i.e. unknown part. Shareholders equity is used to absorb these losses. We have to presume, that banks not only need capital to absorb these losses, but also have to stay above minimum regulatory capital requirements through the full business cycle.

The targeted level of unexpected losses depends on two factors: minimum capital requirements and targeted rating.

7

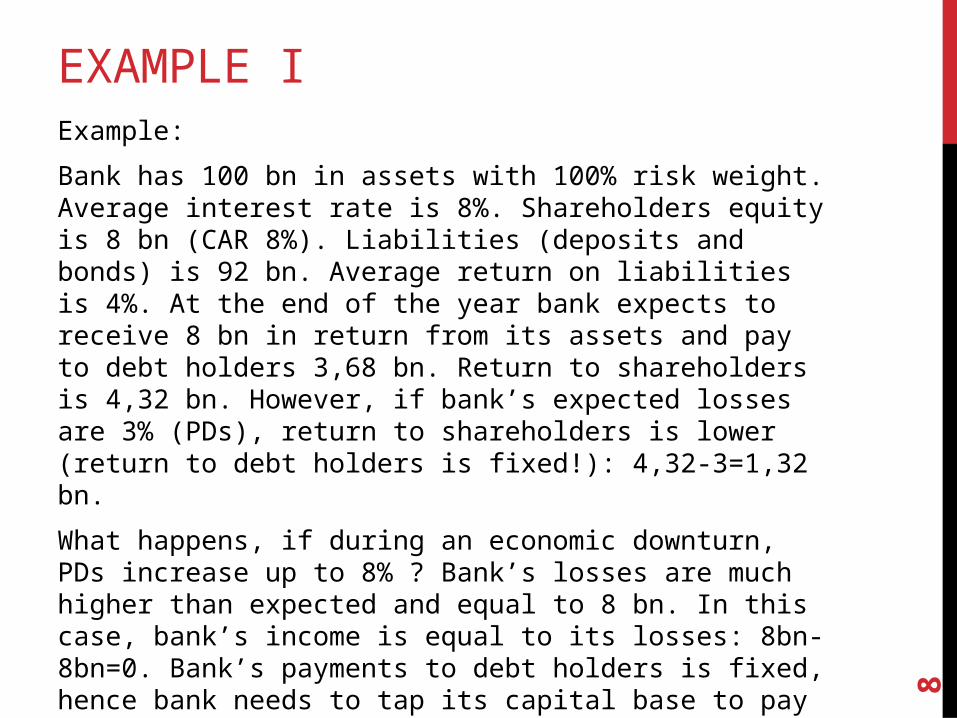

EXAMPLE IExample:

Bank has 100 bn in assets with 100% risk weight. Average interest rate is 8%. Shareholders equity is 8 bn (CAR 8%). Liabilities (deposits and bonds) is 92 bn. Average return on liabilities is 4%. At the end of the year bank expects to receive 8 bn in return from its assets and pay to debt holders 3,68 bn. Return to shareholders is 4,32 bn. However, if bank’s expected losses are 3% (PDs), return to shareholders is lower (return to debt holders is fixed!): 4,32-3=1,32 bn.

What happens, if during an economic downturn, PDs increase up to 8% ? Bank’s losses are much higher than expected and equal to 8 bn. In this case, bank’s income is equal to its losses: 8bn-8bn=0. Bank’s payments to debt holders is fixed, hence bank needs to tap its capital base to pay interest rate: 8-3,68=4,32 bn capital left. That’s below minimum CAR of 8%. Bank needs to be closed or recapitalized.

8

EXAMPLE II

How much additional capital bank needs to hold?

Bank provisions 3% for expected losses and needs additional reserves of 5 bn just to have zero profit. In this case return to its shareholders is 0.

To come up with the worst case scenario, and calculate additional reserves, we need to perform a stress test and model expected and unexpected losses.

Under Basel II IRB approach we have to model PDs, LGDs. EADs are given. Losses are expressed as:

Expected losses=PDs x LGDs x EADs

Under Basel II STD approach non IFRS and Basel I we model loan loss provisions (LLPs):

∆LLPs=∆NPLs x provisioning rate

Unexpected losses can be measured as a number of standard deviations from expected losses (VaR concept).

9

10

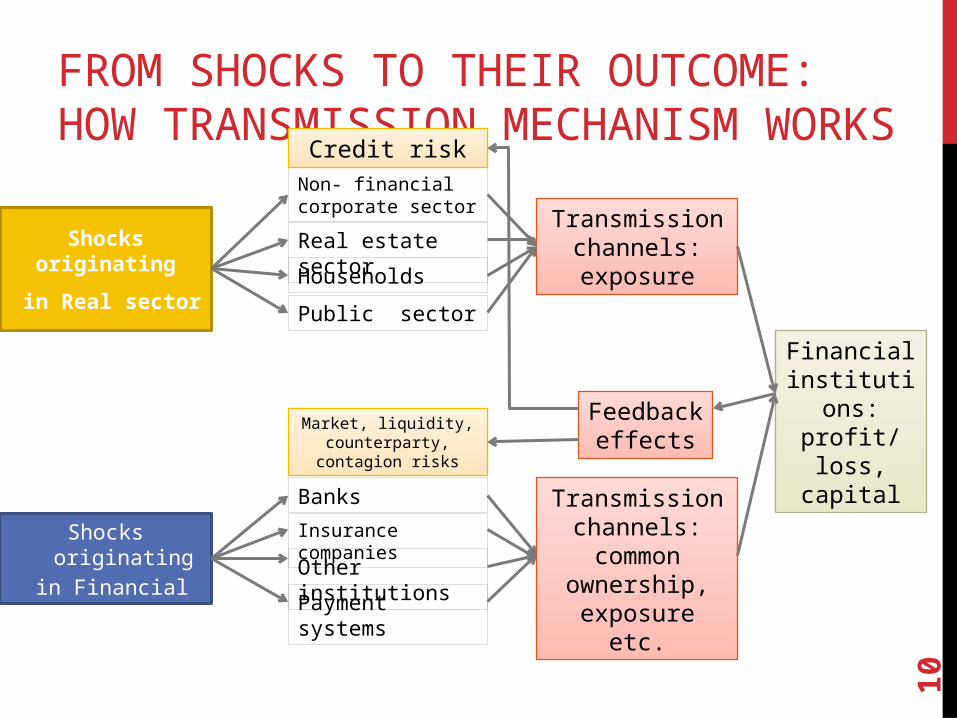

FROM SHOCKS TO THEIR OUTCOME: HOW TRANSMISSION MECHANISM WORKS

Shocks originating

in Real sector

Non- financial corporate sector

Households

Public sector

Real estate sectorTransmission

channels: exposure

Financial institutions:profit/loss,

capital

Credit risk

Shocks originating

in Financial sector

Banks

Insurance companies

Other institutions

Payment systems

Transmission channels: common

ownership, exposure etc.

Market, liquidity, counterparty, contagion

risks

Feedback effects

MACRO CREDIT RISK STRESS TESTING MODEL

Macroeconomic forecastsCB’s macro model

GDP, Housing prices, interest rates, FX rate, unemployment

Banking sector data

NPLs, provisions, credit growth

Short-term equations with AR(1) terms and/or ECM: NPLs depencence on selected macro variables

calculated for 1 to 4 quartersLong-term equations:

NPLs depencence on selected macro variables calculated up to 3 years

Equations on a bank-by-bank basis

Banking sector dataInterest income, expenses,

credit growth, doeposits, interest rate etc.

FX risk, concentration risk, income/expense, duration gap models

Loan migration matrixProjected additional provisions

On a bank-by-bank basis

Projected net losses/profitCAR

Unexpected lossesMonte-carlo simulation

Number of banks that do not meet minimum CAR

Real estate prices: collateral value for LGD calculation

11

12

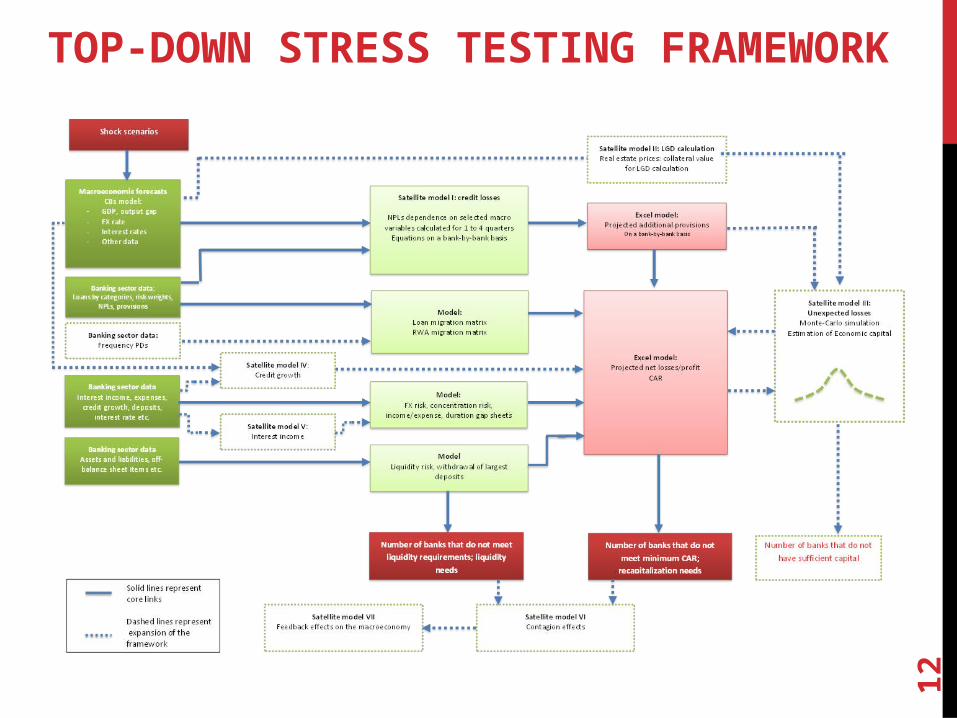

TOP-DOWN STRESS TESTING FRAMEWORK

THREE TYPES OF MODELS FOR MACRO STRESS TESTING

I Portfolio models (Credit Risk plus; Risk Metrics; Credit Portfolio View etc.)

II Balance sheet models (Cihak, Boss et all. and modifications).

III Market data based models (CCA).

First type of models dominate in private sector, second and third type dominate in regulatory institutions.

13

14

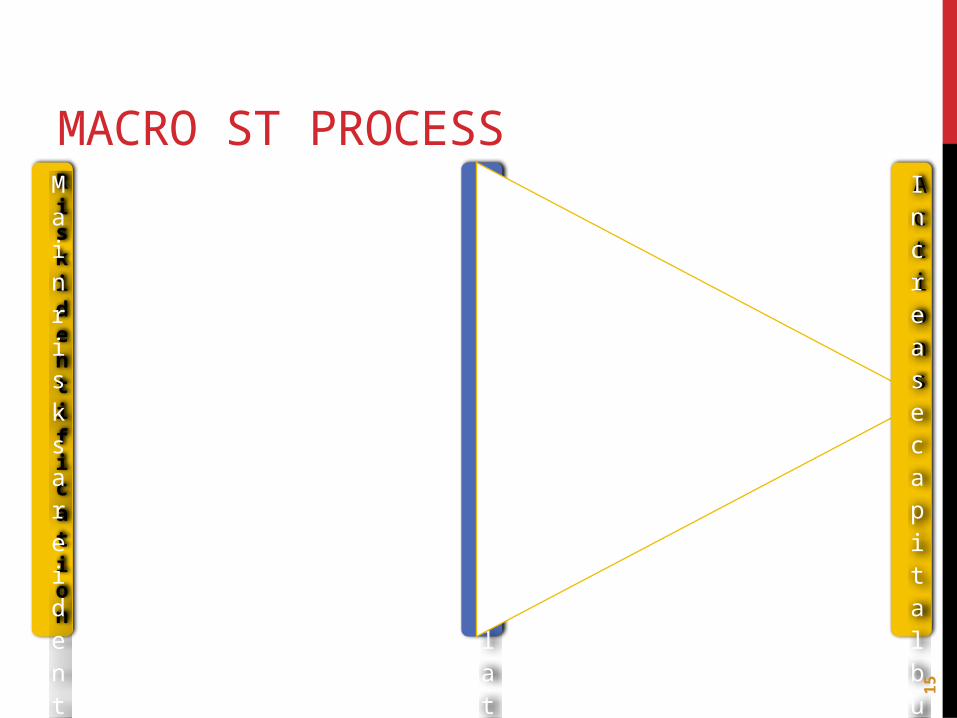

MACRO ST PROCESS

MACRO ST PROCESSRisk

identific

ation

Main risks are identified and scenarios constructed.III types of scenarios:I economic/industry downturnII market risk eventsIII liquidity crisis

Lo

ss calculation and

mapping

Losses are calculated using either sensitivity or scenario analysis or both approachesLosses in terms of CAR are presented

Actions

Increase capital buffersReduce RWAReduce exposureReview concentration limits etc.

15

UNDERSTANDING THE INCENTIVES

There are at least three stakeholders in the stress-testing process: financial institutions, regulators and the public/markets.

Usually they have different incentives: regulators want more data, more time, more extreme scenarios; financial institutions want to provide less data, use in-house models, usually less extreme scenarios. Regulators want to find the weakest components of the banking system, whereas institutions want to show resilience. Public wants “blood”- know institutions that fail the test.

16

MACRO STRESS TESTING STEPS

Determine the objective of the stress test

Design scenario

Perform stress test

Calculate stress losses

Report results

Determine actions

17

BASEL II/III

Pillar I

Minimum capital

Minimum capital requirement; point

in time assessment

Pillar II

Supervisory review

Individual capital guidance: Pilar I

risks+additional (bank specific) risksStress tests

Pillar III

Market discipline

ICAAP: Internal capital adequacy

assessment process;Calculation of

economic capital

18

19

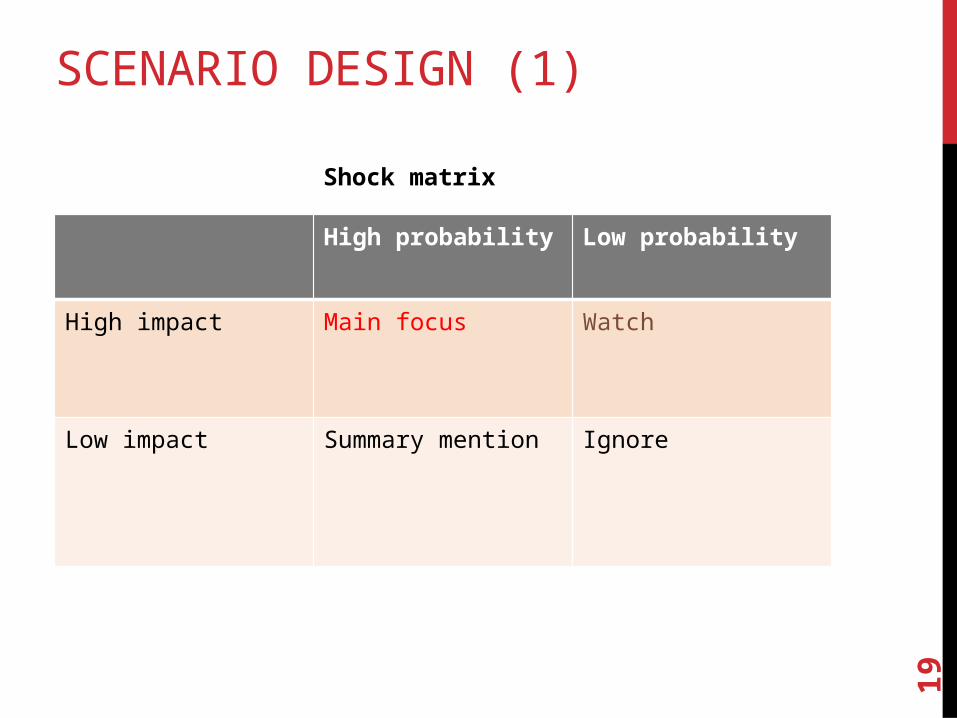

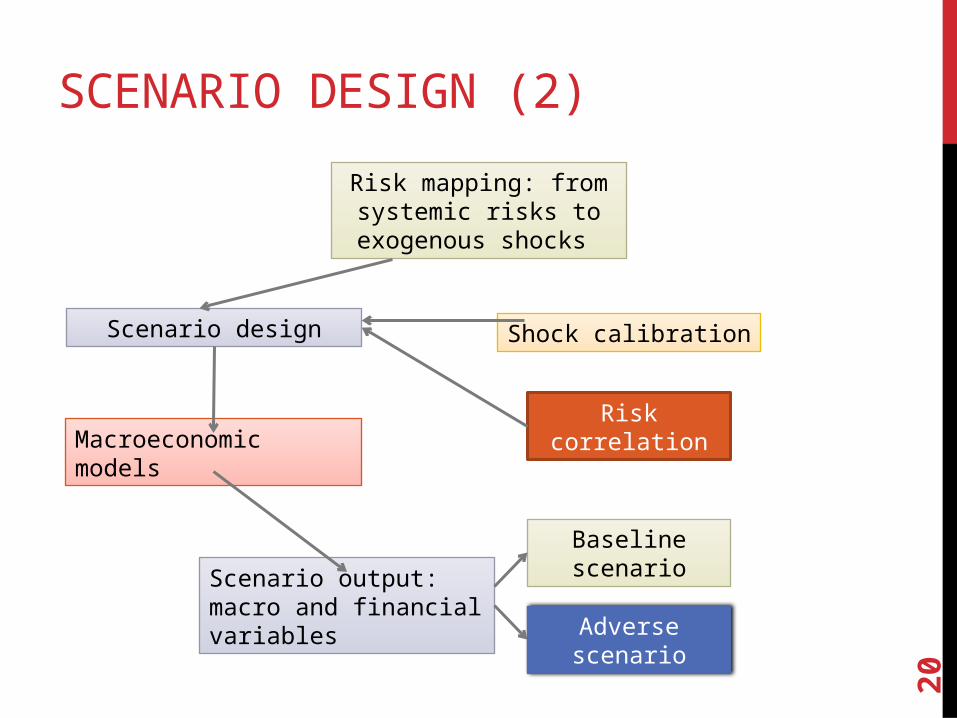

SCENARIO DESIGN (1)

High probability Low probability

High impact Main focus Watch

Low impact Summary mention Ignore

Shock matrix

20

SCENARIO DESIGN (2)

Risk mapping: from systemic risks to

exogenous shocks

Macroeconomic models

Scenario output: macro and financial variables

Risk correlation

Shock calibrationScenario design

Baseline scenario

Adverse scenario

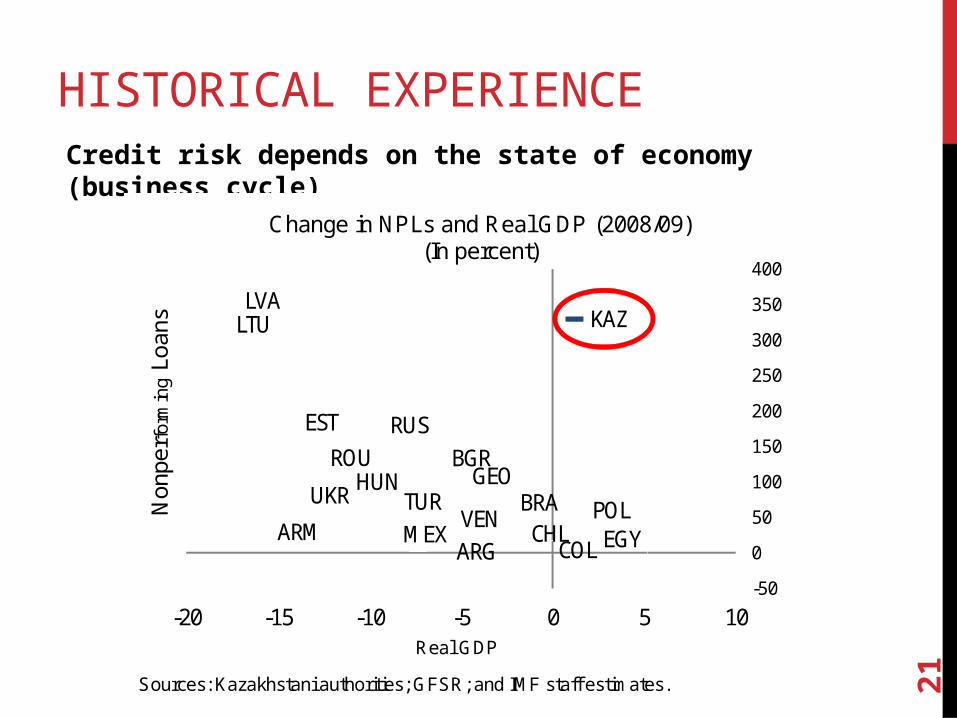

HISTORICAL EXPERIENCECredit risk depends on the state of economy (business cycle)

21

0

1

2

3

4

5

Aug-09 Apr-10

Kazakhstani banks' provisions to NPLs (90-day)(In percent)

ARG

BRACHL

COLMEX

VEN

BGR

EST

HUN

LVALTU

POL

ROURUS

TURUKR

ARM EGY

GEO

KAZ

-50

0

50

100

150

200

250

300

350

400

-20 -15 -10 -5 0 5 10Real GDP

Non

perf

orm

ing

Loan

s

Change in NPLs and Real GDP (2008/09)(In percent)

Sources: Kazakhstani authorities; GFSR; and IMF staff estimates.

DEFINING THRESHOLDS

22

Expected (mean losses)

E[x]=μ(x)

LossLoan loss provisions

Economic capital

Confidence interval is identical to default probability:

BBB0,1%

A0,07%

AA0,03%

AAA0,01%

Expected shortfall

P(X) Pass/Fail criteria and minimum capital requirements

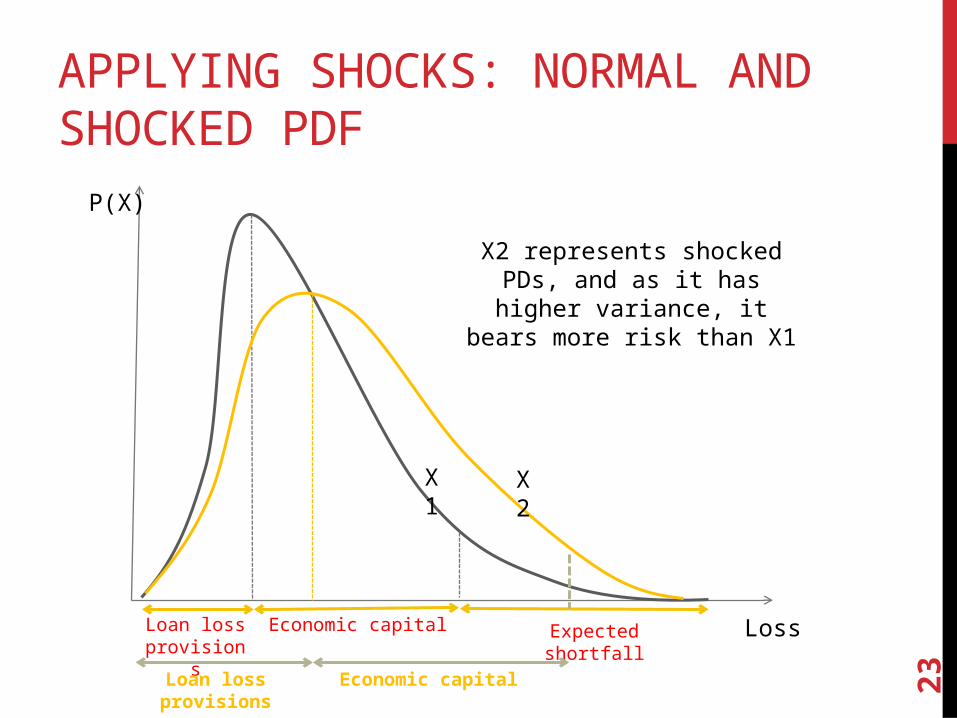

APPLYING SHOCKS: NORMAL AND SHOCKED PDF

23

LossLoan loss provisions

Economic capital Expected shortfall

X1 X2

X2 represents shocked PDs, and as it has higher variance, it bears

more risk than X1

Loan loss provisions Economic capital

P(X)

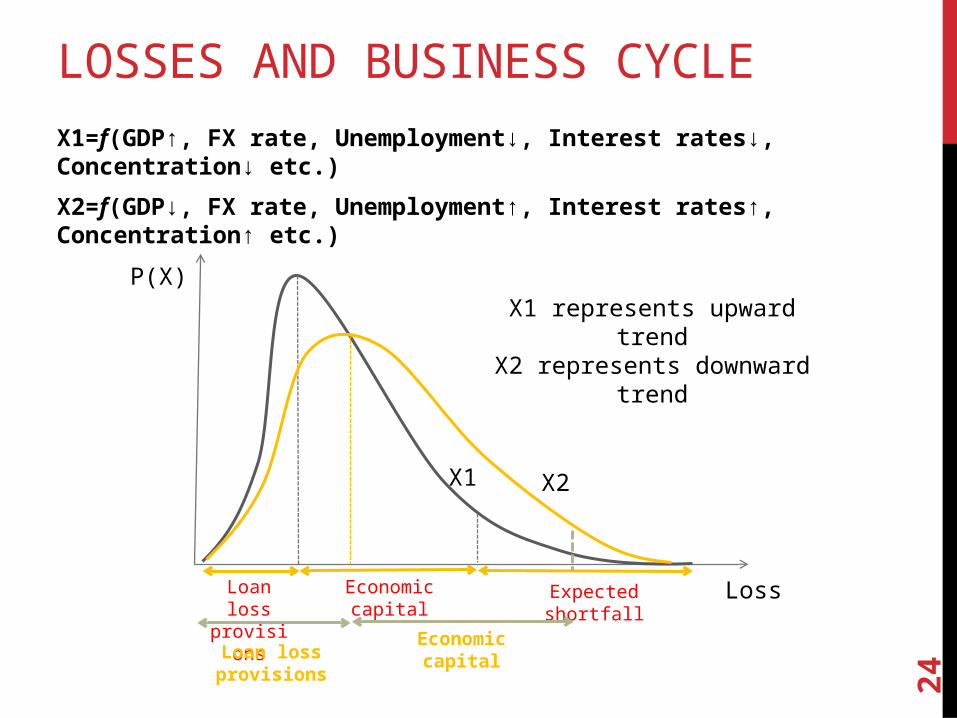

LOSSES AND BUSINESS CYCLEX1=f(GDP↑, FX rate, Unemployment↓, Interest rates↓, Concentration↓ etc.)

X2=f(GDP↓, FX rate, Unemployment↑, Interest rates↑, Concentration↑ etc.)

24

LossLoan loss provisions

Economic capital Expected shortfall

X1 X2

X1 represents upward trendX2 represents downward trend

Loan loss provisions

Economic capital

P(X)

CALCULATING LOSSES

25

26

CALCULATING CAR

Current Tier I and II capital (regulatory capital)

Net income before loan loss provisions; Forecasted from satellite income model

Loan loss provisions; Forecasted from satellite credit loss model

Loan loss provisions; Forecasted from satellite credit loss model

Migration matricesSatellite credit growth model

Current RWA for: credit, market and operational risks

27

USE OF STRESS TESTS

28

THEORETICAL USE OF STRESS TESTS

What answers stress tests should provide:

How much capital a bank needs to support its risk taking activities? (Forward looking)

Is the current level of capital adequate? (Present)

Lehman Brothers, Bear Stearns, Dexia, JP Morgan…. Did they do it right?

Capital that is available vs. Capital that is needed vs. Capital that regulators need.

29

ACTUAL USE OF STRESS TESTS DURING THE CRISIS

Stress tests popped out as a tool to address loss in public confidence

Confidence was boosted by disclosing individual banks’ results, scenarios and data about exposures

SCAP (US) vs. EBA (EU).

30

STS BEFORE AND AFTER CRISIS

Before After

Very little public disclosure, usually : “All banks are adequately capitalized, however challenges remain, thus we will be vigilant”

Comprehensive analysis, data available on a bank by bank basis. Not all banks pass tests, capital shortfalls are public

Static analysis Dynamic analysis

Usually single shocks, VaR based Macro based, multiple scenarios, dependency among various risk factors, CoVaR

In most cases solo, individual entity based Consolidated at the parent (group) level

Simple models, usually for credit and market risk separately

Comprehensive models: credit, market, liquidity risks and lost income

Not necessarily linked to CAR Linked to CAR

No macroprudential measures or capital conservation plans

Macroprudential measures (system wide) and capital conservation plans (individual)

31

CAN STRESS TESTS DETECT SYSTEMIC RISKS?

In theory, macroprudential STs should unveil the sources of systemic risk (see IMF (2012)

In practice, sources indeed were identified correctly (e.g housing market in the US, contagion from Greece in the EU etc).

Magnitude of shocks and subsequently their impact was miscalculated

32

DID STS FAIL?

33

WHY STRESS TESTS CAN FAIL? (1)

We can find many “wrongs”:

Wrong models: too complex

Wrong (absence of) data: where risks were “parked”?

Wrong scenarios: underestimation of tail risk events and contagion effects

Wrong incentives: no need to rock the boat, public will not understand

Wrong scale: “shadow institutions” escaped

Wrong policy measures

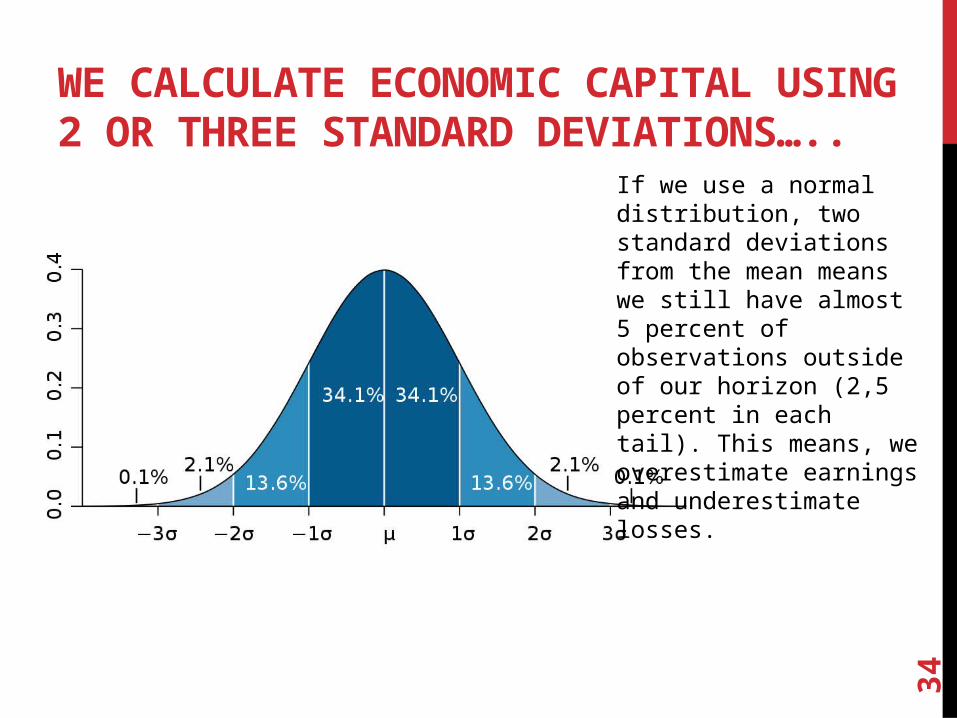

WE CALCULATE ECONOMIC CAPITAL USING 2 OR THREE STANDARD DEVIATIONS…..

34

If we use a normal distribution, two standard deviations from the mean means we still have almost 5 percent of observations outside of our horizon (2,5 percent in each tail). This means, we overestimate earnings and underestimate losses.

HOWEVER DURING THIS GLOBAL FINANCIAL CRISIS VOLATILITY WAS MUCH HIGHER…..

In August 2007, the Chief Financial Officer of Goldman Sachs, David Viniar, commented to the Financial Times:

“We are seeing things that were 25-standard deviation moves, several days in a row”.

As Andrew Haldane, executive director at the bank of England noticed:

“Assuming a normal distribution, a 7.26-sigma daily loss would be expected to occur once every 13.7 billion or so years. That is roughly the estimated age of the universe. A 25-sigma event would be expected to occur once every 6 x 10124 lives of the universe.”

35

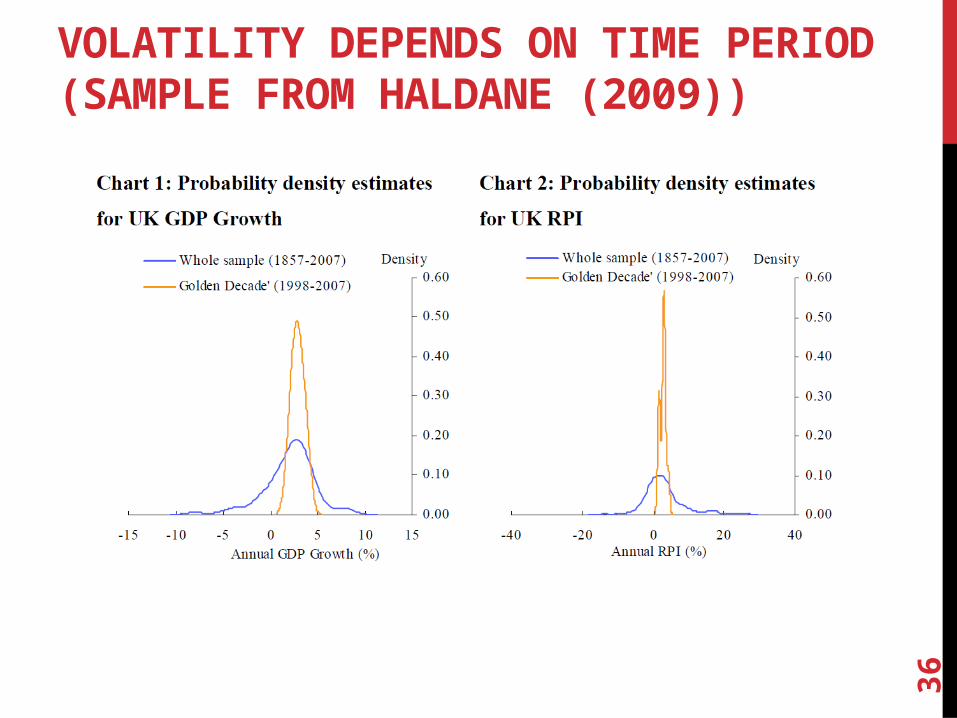

VOLATILITY DEPENDS ON TIME PERIOD (SAMPLE FROM HALDANE (2009))

36

37

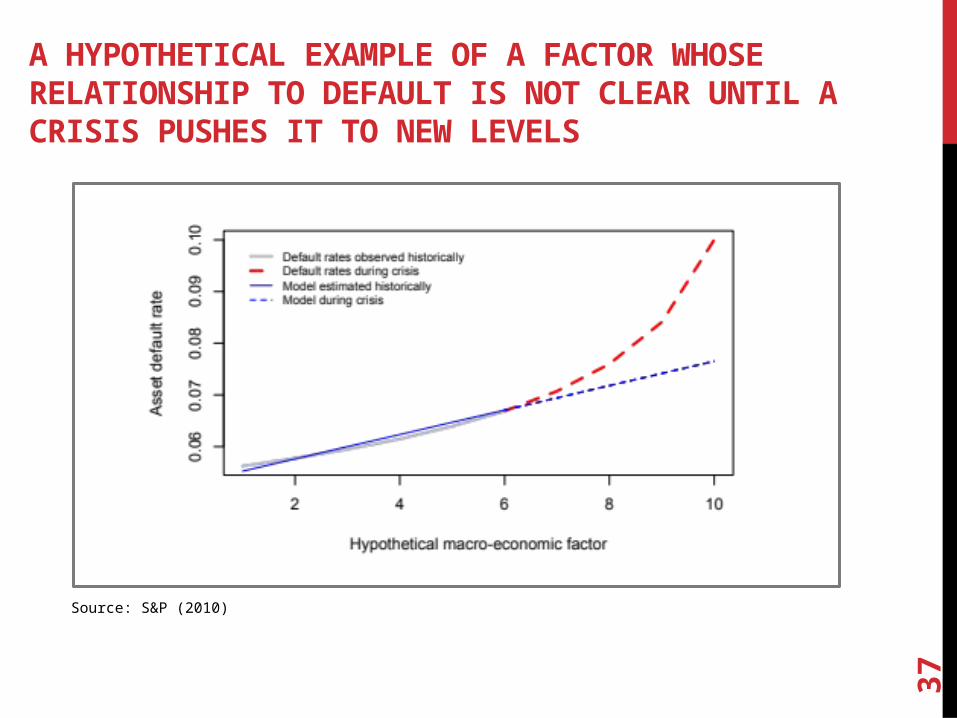

A HYPOTHETICAL EXAMPLE OF A FACTOR WHOSE RELATIONSHIP TO DEFAULT IS NOT CLEAR UNTIL A CRISIS PUSHES IT TO NEW LEVELS

Source: S&P (2010)

38

BIMODAL NATURE OF RATING TRANSITIONS

Source: Moody’s (2013) Stress Testing of Credit Migration. A Macroeconomic approach.

39

WHY STRESS TESTS CAN FAIL? (2)

Underestimated probability of adverse outcomes (disaster myopia)

Reluctance to include severe scenarios Willingness to hold capital under less extreme scenario only Postponement of crisis Reverse engineering: scenarios are such, that bank never

violates minimum CAR Short time series in emerging market countries Data quality issues We usually never look beyond economic capital! Historical scenarios are based on historical data. We can not

test anything new using data from the past only

40

REDUCED FORM VS. FULL-SCALE STRESS TESTS

Most of the stress tests banks do are reduced form stress tests

Reduced form – Monte Carlo simulation

Full scale – links with macro variables. Correlations

Why reduced form? If probabilities are unknown, we face uncertainty. In this case randomization is an answer.

41

WHY REDUCED FORM IS NOT SUITABLE FOR MACRO STS

Reduced form does depend on assumptions about distribution. Beta distribution has fatter tails than the normal one

Reduced form ST has very little connection with macro variables

Is opaque

Is good, once we deal with random, uncorrelated price movements or volatilities. Is not suitable, once we deal with systemic events or highly correlated movements

42

THE WAY AHEADHow to incorporate balance sheet adjustments into core models?

How to avoid modeling partial equilibrium situations only, i.e. include feedback effects and adjustments in broader sectors of economy?

How to model nonlinearities?

System’s stability is most vulnerable then nobody anticipates shocks, i.e. risks are underpriced, real estate prices are at their peaks, GDP and credit grows fast. How to model aggressive risk taking and rapid build-up of imbalances?

How to model financial innovations and market liberalization (historical data are not available at all or structural breaks emerge)?

How to extend stress tests to other (non-bank) financial institutions?

43

IMPORTANCE FOR MACROPRUDENTIAL POLICY

Based on Borio, Drehmann and Tstatsaronis (2012) objective of the stress tests is to support crisis management and resolution. Drilling down we can formulate this objective more precisely:

a) calculation of how much capital should be injected into the system to prevent credit crunch;

b) Identification of weakest financial institutions;

c) signaling to the market about losses and restoring confidence in the banking system;

d) Improve risk management practices, models and data collection;

e) Story telling: use stress tests to describe shocks, transmission channels and possible impact on financial system and broader economy.

44

SEVEN BEST PRACTICE PRINCIPLES PROPOSED BY THE IMF1. Define appropriately the institutional perimeter for the

tests.

2. Identify all relevant channels of risk propagation.

3. Include all material risks and buffers.

4. Make use of the investors’ viewpoint in the design of stress tests.

5. Focus on tail risks.

6. When communicating stress test results, speak smarter, not just louder.

7. Beware of the “black swan.”

Source: Macrofinancial Stress Testing—Principles and Practices (2012)

45

WHAT TO DO? Do not constrain yourselves with historical experience and

scenarios (it is not contrary to the “this time is different” syndrome, i.e. one should think that worst crisis might repeat again or my country is not necessarily too much different from the ones that experienced crisis earlier)

Use judgmental adjustments in scenarios

Use reverse stress testing more often to find break-even points (especially important in liquidity stress-testing)

Make it simple. Last CCAR (2013) emphasized simplicity. Simplicity means no complicated “black box”: executives should be able to understand and supervisors to verify

In the end, follow the advise by J.M. Keynes: “It is better to be roughly right than precisely wrong”

Related Documents