Developing A New Crediting Method Jeff Hanschmann

Developing A New Crediting Method

Dec 31, 2015

Developing A New Crediting Method. Jeff Hanschmann. Why Develop a New Crediting Method?. Feedback and planned enhancements Options for customers Simplicity Innovation. Common Crediting Methods. Annual Point-to-Point Difference between ending and beginning annual values - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Developing A New Crediting Method

Jeff Hanschmann

Why Develop a New Crediting Method?

• Feedback and planned enhancements

• Options for customers

• Simplicity

• Innovation

2

Common Crediting Methods• Annual Point-to-Point

• Difference between ending and beginning annual values• Buy a call, sell a call.

• Monthly Average*• Difference between average and beginning annual value• Geometric Asian option

• Monthly Sum• Sum of monthly returns• Monthly cap (1%)

3

4

Other Crediting Methods• Rainbow Method*

• Weighted average of best performing indices• ING, American General

• Trigger Method*• Brand new to life insurance industry (Why hasn’t any company come

out with it before?)• Common in FIA industry

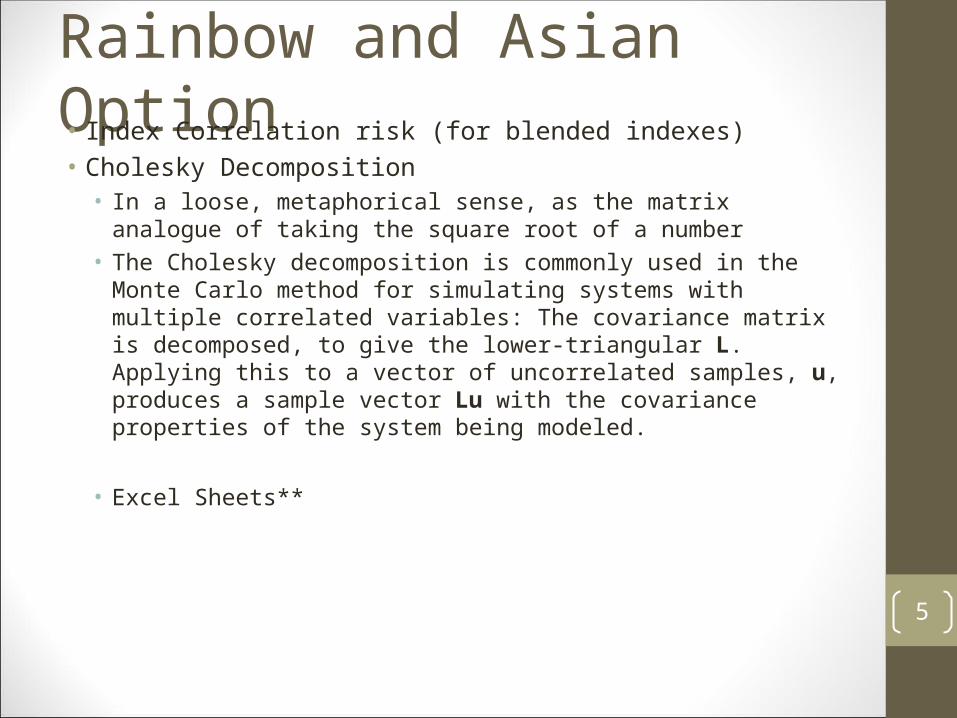

Rainbow and Asian Option• Index Correlation risk (for blended indexes)• Cholesky Decomposition

• In a loose, metaphorical sense, as the matrix analogue of taking the square root of a number

• The Cholesky decomposition is commonly used in the Monte Carlo method for simulating systems with multiple correlated variables: The covariance matrix is decomposed, to give the lower-triangular L. Applying this to a vector of uncorrelated samples, u, produces a sample vector Lu with the covariance properties of the system being modeled.

• Excel Sheets**

5

New Trigger Method

6

-2% 0% 2% 4% 6% 8% 10% 12% 14% 16%

Index Return

Pay

off

APP payoff (13% Cap)

Trigger payoff (10% Cap)

*

** *10%

13%

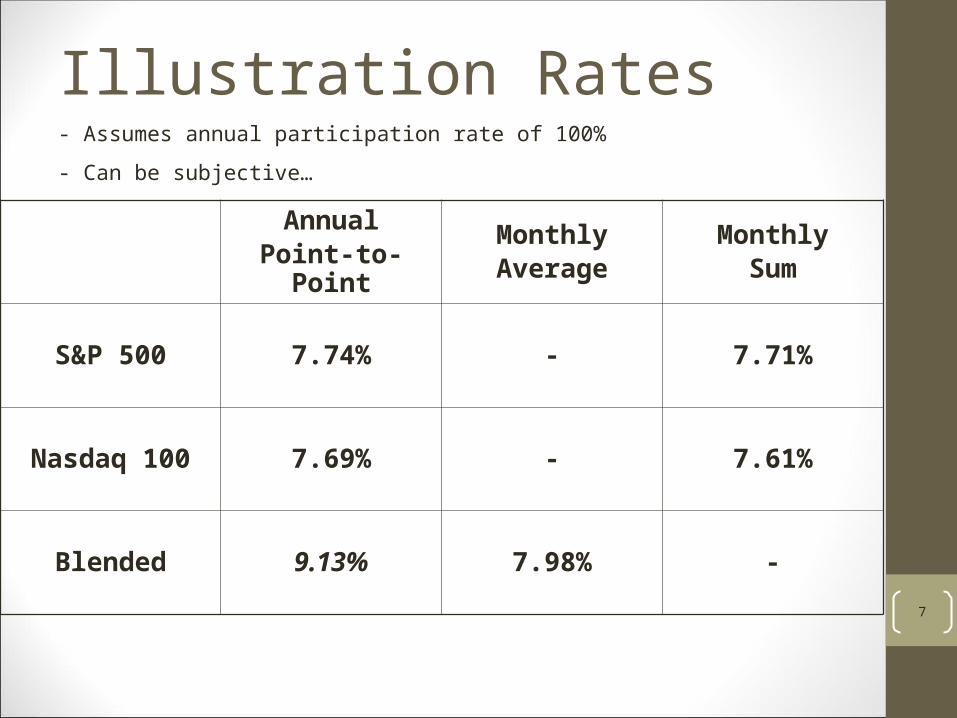

Illustration Rates

AnnualPoint-to-Point

MonthlyAverage

MonthlySum

S&P 500 7.74% - 7.71%

Nasdaq 100 7.69% - 7.61%

Blended 9.13% 7.98% -

7

- Assumes annual participation rate of 100%

- Can be subjective…

Illustrations• What initial cap are we able to provide?• Why do we need to blend current and long term if we statically

hedge? • Avoid fluctuating caps!• Estimate bank “mark-up”

8

Challenges• What’s the story?

• Growing vs. stable market• No more 0% returns than APP

• Hedging• Static vs. Dynamic hedge• What are advantages and

disadvantages?• High Tracking error when delta

hedged daily (10,000 sims)*

• IT costs• Implementation costs are high• Down to last indexing space• Modification will increase costs

Year Trigger (10% Cap) APP (13% CAP)

2001 0.00% 0.00%

2002 0.00% 0.00%

2003 10.00% 13.00%

2004 10.00% 8.99%

2005 10.00% 3.00%

2006 10.00% 13.00%

2007 10.00% 3.53%

2008 0.00% 0.00%

2009 10.00% 13.00%

2010 10.00% 12.78%

9

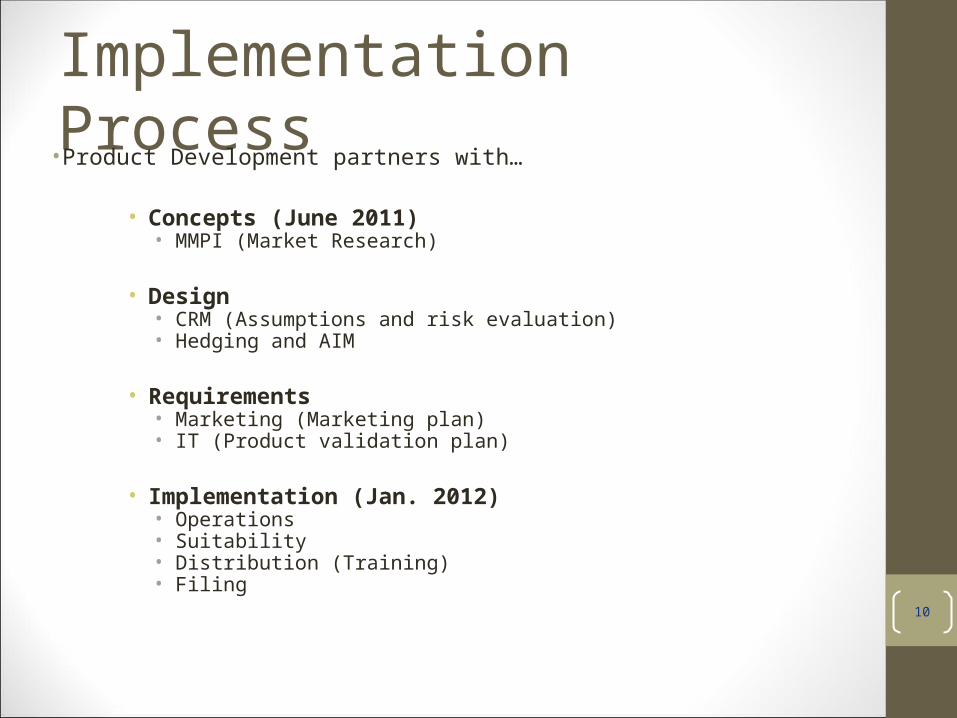

Implementation Process•Product Development partners with…

• Concepts (June 2011)• MMPI (Market Research)

• Design• CRM (Assumptions and risk evaluation)• Hedging and AIM

• Requirements• Marketing (Marketing plan)• IT (Product validation plan)

• Implementation (Jan. 2012)• Operations• Suitability• Distribution (Training)• Filing

10

Q/A•Thank you!

Related Documents