Paper to be presented at the Summer Conference 2010 on "Opening Up Innovation: Strategy, Organization and Technology" at Imperial College London Business School, June 16 - 18, 2010 DIVERSIFICATION BY YOUNG, SMALL FIRMS Rui Baptista Instituto Superior Tecnico, Technical University of Lisbon [email protected] Murat Karaöz Instituto Superior Tecnico, Technical University of Lisbon [email protected] João Leitão University of Beira Interior [email protected] Abstract: Young firm diversification is examined investigating the determinants of the timing of diversification and also whether diversifying firms have higher survival chances. Firms with a greater proportion of employees in managerial positions are more likely to diversify early, giving credence to resource-based views of diversification. Firms that enter volatile industries are more likely to diversify early, possibly due to entry mistakes. Firms born diversified are more likely to survive, suggesting that pre-entry capabilities play an important role in early diversification. Firms diversifying after birth are more likely to survive the older they are at the moment of diversification. JEL - codes: M13, L22, L25

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Paper to be presented at the Summer Conference 2010

on

"Opening Up Innovation:Strategy, Organization and Technology"

atImperial College London Business School, June 16 - 18, 2010

DIVERSIFICATION BY YOUNG, SMALL FIRMS

Rui BaptistaInstituto Superior Tecnico, Technical University of Lisbon

Murat KaraözInstituto Superior Tecnico, Technical University of Lisbon

João LeitãoUniversity of Beira [email protected]

Abstract:Young firm diversification is examined investigating the determinants of the timing of diversification and alsowhether diversifying firms have higher survival chances. Firms with a greater proportion of employees inmanagerial positions are more likely to diversify early, giving credence to resource-based views ofdiversification. Firms that enter volatile industries are more likely to diversify early, possibly due to entrymistakes. Firms born diversified are more likely to survive, suggesting that pre-entry capabilities play animportant role in early diversification. Firms diversifying after birth are more likely to survive the older theyare at the moment of diversification.

JEL - codes: M13, L22, L25

Diversification by Young, Small Firms Abstract: Young firm diversification is examined investigating the determinants of the timing of diversification and also whether diversifying firms have higher survival chances. Firms with a greater proportion of employees in managerial positions are more likely to diversify early, giving credence to resource-based views of diversification. Firms that enter volatile industries are more likely to diversify early, possibly due to entry mistakes. Firms born diversified are more likely to survive, suggesting that pre-entry capabilities play an important role in early diversification. Firms diversifying after birth are more likely to survive the older they are at the moment of diversification. Keywords: Diversification; Start-ups; Small Business; Resource-based View; Entry Mistakes J.E.L Codes: M13, L23, L25

1

1. Introduction

Since the 1980s, there has been a rise of research into entrepreneurship and small

business. Despite this renewed attention, diversification remains a relatively untapped

topic in studies focused on small firm growth (Davidsson, Achtenhagen and Naldi,

2006). Two well-known aspects of the entrepreneurship and industry dynamics

literatures are that start-ups are small and numerous, and that a significant percentage

exit the market in their early years (Romanelli, 1989; Mata and Portugal, 1994;

Bartelsman, Scarpetta and Schivardi, 2005). The factors distinguishing the ones that

survive from the ones that exit are studied in an extensive body of empirical research

(see Caves, 1998; and Carroll and Hannan, 2000 for reviews).

According to Audretsch (1995), one reason why so many new firms fail is that

their start-up size is smaller than the minimum efficient scale in the industry and they

experience a cost disadvantage vis-à-vis the most efficient firms in the market. The

larger the minimum efficient scale in an industry, the higher the cost of adjustment for

new firms. Mata, Portugal and Guimarães (1995) find that the probability of survival

of new firms improves over time as their size increases toward the minimum efficient

scale. It is then intuitive to perceive that the growth process of a small start-up firm

should be specialized while it adjusts its size to the requirements of the market. One

would expect additional resources acquired after start-up to be added back toward the

growth of the existing business in order to achieve more efficiency and, in this way,

ensure survival.

The fact remains, however, that some small firms choose to diversify early in their

lives. While a large majority of the research on corporate diversification focuses on

large firm diversification strategies and performance (see Ramanujam and

Varadarajan, 1989; Montgomery, 1994; and Palich, Cardinal and Miller, 2000 for

reviews), a range of studies indicate that diversification is a favored strategy among a

small proportion of young, small firms (Lynn and Reinsch, 1990; Kim and Kogut,

1996; Sandvig, 2000; Giarratana, 2004; Auerswald, 2008). In general, these studies

suggest that diversification might be a legitimate growth strategy for some young,

small firms. However, no study has specifically focused on two major questions:

i. Which factors determine the timing of diversification for start-ups; and

2

ii. How does diversification (and its timing) affect the probability of survival of

young firms?

This paper examines first-time diversification decisions by young firms. We

investigate the determinants of the timing of the diversification decision (i.e. how long

it takes from start-up to diversification) and also whether young firms diversifying

have significantly higher chances of survival than young firms that do not. We use

extensive longitudinal data containing information on firms’ characteristics and

environmental conditions, and their evolution over time.

The remainder of the paper is organized as follows. In the next section the

literature on the drivers of diversification is examined, discussing how it may apply to

the growth of new firms. The third section introduces the data used in the paper. The

fourth section examines the determinants of the timing of diversification, while the

fifth section looks at whether diversified young firms are more or less likely to

survive than non-diversified ones. The sixth section concludes.

2. Background

The empirical evidence supporting a “liability of smallness,” i.e. a negative

relationship between hazard rates and size (initial and/or current), is overwhelmingly

unambiguous. This result is found in samples of firms of all ages (Evans, 1987; Hall,

1987) and in samples of new firms (Mata and Portugal, 1994; Haveman, 1995;

Agarwal and Audretsch, 2001). Smaller entrants face lower barriers to exit (Sharma

and Kesner, 1996) and are more likely to lack the social legitimacy, relationships with

customers and suppliers, and productive routines that enhance the probability of

survival (Delmar and Shane, 2004). The probability of survival increases as firms

invest and grow their core business (Mata, Portugal and Guimarães, 1995; Sharma

and Kesner, 1996). Nevertheless, while diversification remains a growth strategy used

mainly by large firms, some young, small firms choose to grow through

diversification.

3

2.1. Drivers of Diversification

The diversification phenomenon is well studied within the context of large firms.

Montgomery (1994) examines three main perspectives of why large firms diversify:

the market power perspective; the managerial or agency perspective; and the resource

based perspective. The market power perspective argues that diversification yields

market power through anti-competitive practices (Edwards, 1955): cross-

subsidization, mutual forbearance, and reciprocal buying. The agency perspective

supposes that when managers hold little equity in the firm and shareholders are too

dispersed to enforce value maximization, corporate assets may be deployed to benefit

managers rather than shareholders (Marris, 1963, 1964).

The resource based perspective argues that rent-seeking firms diversify in response

to excess capacity in productive factors or resources that can be used in distinct

markets. These include factors the firm has purchased in the market, services the firm

created from those factors, and special knowledge (or technology) the firm has

accumulated over time (Penrose, 1959). Arguments originating from neoclassical and

evolutionary economics reinforce this view. Within the neoclassical theory of the

firm, the concept of ‘economies of scope’ (Panzar and Willig, 1981) provides a

rationale for diversification; Teece (1980; 1982) argues that diversification is a means

for firms to achieve economies of scope arising from the sharing of tangible and

intangible assets in the production of multiple products, resulting in lower joint costs

per unit of output. Evolutionary economic theory is concerned with firms as bundles

of resources which are organized in routines representing the organizational heritage

and knowledge base of the firm, shaping and bounding its path of further expansion

and new learning opportunities (Nelson and Winter, 1982). These arguments are

particularly relevant with regard to intangible assets. Many of a firm's skills and much

of its knowledge are not easily transferable since they are deeply embedded in the

human resources and routines of the firm. The transfer of these systemic resources

entails contracting problems due to information asymmetries (Wernerfelt, 1988) and

may require the transfer of organizational as well as individual knowledge (Teece,

1982), making diversification a superior strategy for growth.

Of these perspectives, only the resource based one seems pertinent for young,

small firm diversification. Conglomerate power is a function of the firm's market

4

power in its individual markets (Gribbin, 1976). To wield power across markets, firms

must first have some measure of strength in its individual markets. A new small firm

with insignificant positions in a number of markets will not, in sum, have

conglomerate power. Arguments which link diversification and firm growth due to

agency problems are equally tied to the life cycle of the firm. Young businesses are

usually assumed to be formed of like-minded individuals with the same initial view

about the best course of action for the firm (Klepper, 2007).

According to the resource-based perspective (Barney, 1986, 1991; Peteraf, 1993),

firms accumulate tangible and intangible assets in the course of their activities in a

learning process that enables the accumulation of experience embedded in human

resources. These assets include product, process and industry-specific know-how and

human capital, customer and supplier ties, as well as marketing and distribution

channels. As the firm grows and becomes more efficient, the accumulated resources

may exceed the industry requirements. Idle resources induce owners or top managers

to redeploy and expand them into other industries or markets that require comparable

inputs and resources, thus leading to diversification.

2.2. Why do Young, Small Firms Diversify?

Since owner-managers and entrepreneurs may differ significantly in abilities and

growth orientation, reasons for diversification probably also vary widely and are

related to factors both internal and external to the firm (Carland et al., 1984). While

not attempting to provide a theoretical foundation for young firm diversification, the

sporadic research on the subject is examined in order to determine the main rationales

behind this phenomenon.

Following the resource-based logic, diversifying young firms may be looking for

synergies or the sharing of co-specialized innovative assets between different lines of

business. There are both competitive and cognitive reasons why young firms might

possess knowledge with potential application in multiple product markets. Pre-entry

resources and capabilities embodied in entrepreneurs (Helfat and Lieberman, 2002)

represent an important asset for new firms. Mosakowski (1998) defines

entrepreneurial resources as the propensity of individuals to behave creatively, act

with foresight, use intuition, and be alert to new opportunities. These entrepreneurial

5

resources can be dispersed among a team of individuals and combined into unique

capabilities (Tanriverdi and Venkatraman, 2005). Amit and Schoemaker (1993) define

capabilities to be information-based processes. Such information (or knowledge) may

be possessed by teams of founders prior to entry, enabling them to better recognize

opportunities (Shane, 2000) and making entrepreneurial start-ups a superior choice for

opportunity exploitation (Alvarez and Busenitz, 2001). Newly formed entrepreneurial

teams begin with a set of endowments (Levinthal and Myatt, 1994), including human

capital (knowledge, skills and experience), social capital (social ties within and

outside the team) and cognition (Helfat and Peteraf, 2003). While cognition enables

corporate managers to build up dynamic capabilities as firms and organizations evolve

(Adner and Helfat, 2003), human and social capital accrued by managers and

qualified personnel prior to start-up may also be an incentive to diversification. It is

therefore possible that, even in the very early stages of its life, firms may have the

resources and capabilities needed to deploy in multiple markets.

Diversification by young firms may also be associated with the specific nature of

small business entry in new markets. The growth of small firms is a particularly

erratic and risky phenomenon. Entry and failure rates of new firms are high,

regardless of the industry. Santarelli and Vivarelli (2007) highlight that, when dealing

with gross entry across all economic sectors, a huge multitude of ‘followers’ and very

few ‘real’ entrepreneurs are encountered. Instead, overconfidence and the ‘escape’

from unemployment are often key characteristics of new firms. Some influential

theoretical models in economics attempt to describe the chaotic process of small firm

growth (see, for instance, Hopenhayn, 1992; and Ericson and Pakes, 1995).

Diversification decisions in the young, small firm context may seek to reduce risk by

spreading resources across several industries, or correct an entry mistake by switching

resources from an industry where there is insufficient demand to a more promising

one.

2.2.1. Synergies and the Sharing of co-specialized and innovative assets

Synergistic diversification occurs when a venture or additional product line is

added in order to provide a direct benefit to the existing firm, either taking advantage

of economies of scope or reducing transactions costs (Teece, 1982). This may occur

6

through the use of excess capacity, stimulating demand in the original venture, or

through some other means of providing a cost or revenue advantage. Synergistic

diversification is often carried out into related industries, or in the form of vertical

integration.

Penrose (1959) conceptualizes the firm as a collection of resources, each of which

is a bundle of potential ‘productive services’ bounded together in an administrative

framework. Penrose’s fundamentally dynamic vision of firms holds that firm growth

is led by internal momentum generated by learning-by-doing. Managers and qualified

employees become more productive over time as they become accustomed to their

tasks. As managers gain experience, managerial talent can then be focused on growth

opportunities. Firms are therefore faced with incentives to grow because while the

knowledge possessed by a firm’s personnel tends to increase automatically with

experience, it is challenging to take full advantage of this valuable firm-specific

knowledge.

The notion of synergistic diversification is also central to Ansoff’s (1965) work.

Firms choosing to diversify can do it in one of three ways: by exporting the firm’s

traditional products or services into new markets, by diversifying according to

synergies of demand, or synergies of technology. These synergies may be due to

lower expected fixed costs of starting-up, or due to anticipated operating economies.

However, Ansoff (1965) advocates a prudent approach to diversification: firms should

only consider diversification when there are no other options to realize its growth

objectives; if a firm can discover growth opportunities by re-evaluating and re-

formulating its strategies within its present portfolio of activities, instead of expanding

the portfolio by commencing new activities, it should do so.

Synergistic diversification is likely to be found where the existing venture has high

barriers to entry and exit. Existing firms, which have incurred high sunk costs upon

entry, can increase gains by expanding into new sectors. This may happen in

particular in the absence of scale economies and/or where there is a natural upper

limit to growth in the original business (Giarratana, 2004). Also, firms whose value

chains contain weak links – such as a poor distribution system or an ineffective

maintenance service for a product or a technology – would likely undertake vertically

integrated diversification. Experienced entrepreneurs or owner-managers are more

7

likely to look for synergies in diversification since they have greater intra and inter-

industry knowledge (Lynn, 1998).

Innovative firms which employ transferrable technologies are likely to spawn

diversification which aids in capacity utilization, new product development, or

technology knowledge. Because technology-intensive industries are associated with

higher hazard rates due to faster obsolescence of initial endowments (Agarwal and

Gort, 2002), start-ups in these industries may need to implement a multi-product

strategy for survival and growth.

There are several studies of technology-based diversification behavior (see, for

example, Argyres, 1996; Silverman, 1999; Miller, 2004; 2006). Pavitt, Robson and

Townsend (1989) show considerable variation amongst firms of different sizes and

different principal activities in the nature, dynamics, and organization of their

technological activities. They find evidence of a general trend toward more

diversification resulting in large part from the growing interaction in the small

innovating firms amongst mechanical, instrument, and electrical-electronic

technologies. Kim and Kogut (1996) find that firms that originate in industrial fields

based on a platform technology (i.e. a core technology that is applicable to a wide set

of market opportunities) acquire the technological skills to diversify and to mimic the

branching of the underlying technological trajectory. A meta-analysis conducted by

Song et al. (2008) finds that market scope is a prominent success factor among newly

established technology ventures. Giarratana (2004) finds that innovation and product

differentiation, along with investments in co-specialized assets, are variables strongly

correlated with young firms’ probability of survival and growth in the encryption

software industry. Waves of specialized entrants increasing the mean level of firm

product specialization are followed by periods of market consolidation where

specialized firms leave the market, and companies with a broader product variety

survive.

Technological diversity seems to play an important role in small firm

diversification. In a study of resource sharing within and across large and small firm

product lines in technology-intensive industries, Stern and Henderson (2004) find that

within-business diversification matters a great deal, determining which start-ups

survive and which cope better with rapid environmental change. Miller (2006) finds

that multi-business firms create more value from technological diversity than do

8

single segment firms and diversified firms perform better as technological diversity

increases.

2.2.2. Risk Reduction and Entry Mistakes

Diversification may be a strategy for growth through the creation of a risk-reducing

portfolio of industries where the firm is present. Risk reduction strategies may lead to

unrelated diversification or to diversification into businesses that, even if related, do

not assist the original business directly in revenue generation or cost reduction. Such

diversification often occurs where the initial business is a high-risk enterprise, and is

directed toward sectors where minimal operational resource investments are required

for the new venture. Risk-reducing diversification may be particularly important if the

firm is concentrating its activities on a niche market with seasonal demand (Lynn and

Reinsch, 1990) or locally restrained (Rosa and Scott, 1999). If expansion is restrained

to one industry or region, the rate of return on additional investments diminishes with

the absence of growth in demand and/or technological efficiency gains (Sinha, 1999).

Raffa, Zollo, and Caponi (1996) find that new firms based initially on technical

entrepreneurial know-how may expand their market abilities by acquiring new market

competencies through diversification of the entrepreneurial group’s activities.

Signals of weak or insufficient demand are likely to persuade the firm to search for

other industries to enter. This phenomenon is well established for declining industries

(Chandler, 1962; Miles, 1982): firms look for possible alternatives so that they can

gradually redeploy their assets and reorganize their businesses (Ghemawat and

Nalebuff, 1990; Anand and Singh, 1997). Sandvig (2000), and Filatotchev and Toms

(2003) study how small firms adjust to major declines in their core markets by

diversifying into related markets. However, diversification due to insufficient demand

is not exclusive to declining industries (MacDonald, 1984; Jovanovic, 1993). If the

firm enters a new industry where there is great uncertainty concerning the evolution of

demand, the risk of overestimating future growth is significant. Growing industries

usually experience highly volatile growth rates. This means that, while these

industries attract more entrants, they also experience greater market adjustments,

corresponding to an unstable environment where high rates of entry precede high rates

of exit. Audretsch (1995) uses a ‘revolving door’ to describe this phenomenon.

9

According to Kahneman and Lovallo (1993) individuals are susceptible to a type of

decision making bias in which their forecasts of future outcomes are often anchored

on plans and scenarios of success rather than being grounded in past experience and

are therefore overly optimistic. Camerer and Lovallo (1999) find that optimistic,

overconfident biases influence entry into competitive markets as potential entrants are

unrealistically confident about their chances. According to these authors, entry may

be viewed as an expensive lottery ticket with positively skewed returns: although

most entrants expect to lose money and fail, entry still maximizes expected profits

because the payoffs for success are very large.

Entry mistakes occur when a firm overestimates the market’s growth rate and/or its

own efficiency and enters the market with too large of a scale (Cabral, 1997; Vivarelli

and Audretsch, 1998; Vivarelli, 2004). Such mistakes may also happen due to

unexpected events such as the loss of a significant client or supplier. Under such

circumstances, while some firms may close, others may attempt to redeploy their

excess resources into other lines of business. Facing unexpected changes significant

enough to threaten it with serious operational or financial trouble, an established

venture may diversify by necessity rather than by strategy. Lynn (1998) calls it ‘crisis

diversification’, noting that it tends to be opportunistic and not synergistic.

3. Data Used in the Study

The present study uses the Quadros de Pessoal (QP) micro-data, a longitudinal

matched employer-employee data set built from mandatory information submitted

annually by all Portuguese firms with at least one wage-earner to the Ministry of

Labor and Social Security.1 Firms, establishments and individuals are fully cross-

referenced through the use of a unique identification number, thus allowing for the

recognition of both new entrants and exiting firms, as well as the opening and closure

of subsidiary establishments. For each firm, data are available for size (employment),

age, and number of establishments (including location, employment, and six-digit SIC

sector) for the years 1988-2000.

1 Recent studies using QP data include: Mata and Portugal (2000; 2002), Cabral and Mata (2003); and Varejão and Portugal (2007).

10

While the Portuguese economy is characterized by a small average firm size,

consistent with Portugal being a small open economy, this does not significantly

affect the validity of our results in comparison with other developed economies, as

much of the Portuguese data are consistent with other developed countries. In

particular, Cabral and Mata (2003) provide compelling evidence that the Portuguese

economy displays similar patterns to those of larger and more developed countries

with regard to the firm size distribution across industries.

The entry cohorts of 1988-1994 are followed up to the year 2000, registering all

events of survival and exit, as well as the occurrence of diversification for the first

time. A firm is assumed to exit when all its establishments disappear from the dataset

for at least two years in a row. Establishment, branch entry or acquisition are counted

in order to learn about firms’ diversification decisions. Diversification is defined as

the opening or acquisition of a new establishment (branch) in a different sector from

the start-up’s original one.2 Each firm is classified according to the six-digit sector of

industry aggregation. This provides unique detail, allowing for the identification of

product markets within more widely defined industries. Thus, the diversification

measure captures the emergence of new product lines based on competences and

resources similar to those required for the firm’s original product, as well as less

related forms of diversification. The moment of ‘first-time diversification’, the very

first event of diversification by a start-up, is at the core of the study. Diversification

may occur at birth if the firm enters several sectors simultaneously, or later in the

firm’s lifetime.

Table 1 presents the main characteristics of each entry cohort, including the

proportion of exiting firms and of related and unrelated diversifiers. A significant

proportion of the start-ups in each cohort exited during the period under analysis.

Over 63% of firms in the 1988 cohort exited in the first twelve years, while almost

45% of the 1994 cohort exited in the first six years. In total, 55% of all entrants in

1988-1994 had exited by 2000. These results are in line with the empirical literature

(Caves, 1998; Carroll and Hannan, 2000).

Unsurprisingly, only a very small portion of young firms diversify. About 2.6% of

the firms in the 1988 cohort had diversified after 12 years, while less than 1% of the

2 We are therefore considering diversification both through internal growth and through acquisition of an existing establishment.

11

1993 and 1994 cohorts had diversified by 2000. Entry within the same two-digit

sector is classified as related diversification, while entry into another two-digit sector

is classified as unrelated diversification. Unrelated diversification occurs more often

than related diversification. A total of 1783 firms engaged in unrelated diversification

while 981 diversified within the same two-digit sector. While the data enable the

differentiation between related and unrelated diversifiers, this path is not pursued in

the present study, as the number of events for each type of diversification are too few

to allow for substantial conclusions with regard to differences in diversification timing

and survival patterns between related and unrelated diversifiers.

4. The Timing of Diversification

In this section the factors influencing the time it takes for new firms to diversify

are examined. In order to do so a hazard model of time to diversification is estimated.

The proportional hazards model originally proposed by Cox (1972) is:

10( , ) ( )

p

i ii

X

h t X h t e

(1)

where 0 ( )h t is the baseline hazard function for the time t ; X is a vector of time-

varying covariates; and is a vector of corresponding coefficients to be estimated

(see Mata and Portugal, 2002 for an application).

4.1. Explanatory Variables

A set of explanatory variables accounting for the main firm-level and industry-

level determinants of diversification is developed based on the discussion in section 2.

The definitions and descriptive statistics for all the variables used in this paper are

shown in Table 2.3

The proportions of managers and qualified employees in the firm are used as

explanatory variables to account for the existence of resources and capabilities that

may be applied in a new industry. As previously discussed, Penrose (1959) argues that

3 Correlation matrices are omitted due to space restrictions but are available from the authors upon request.

12

managers become more productive over time thus allowing excess managerial talent

to focus on value-creating growth opportunities. The knowledge possessed by a firm’s

managers and qualified personnel represents a set of resources and capabilities that

may be deployed in new industries. Also as pointed out previously, newly formed

entrepreneurial teams begin with a set of pre-entry knowledge and resources

(Levinthal and Myatt, 1994; Alvarez and Busenitz, 2001) which can be used in a

variety of industries and serve as a basis for the accrual of dynamic capabilities. The

existence of such resources and capabilities from the onset of the firm may also be an

incentive to diversification. Data on business owners and employees for each firm and

establishment include their function (i.e. hierarchical level).4 We use this information

to compute the proportions of managers and qualified personnel; we expect that, as

these increase, diversification will become more likely.

Firm size and its relationship with the industry’s minimum efficient scale (MES)

are likely to be important determinants of diversification. As pointed out earlier, firms

smaller than the industry’s minimum efficient scale experience cost disadvantages vis-

à-vis larger firms (Audretsch, 1995). The larger the minimum efficient scale in an

industry, the longer it might take for a firm to achieve the required efficiency to be

competitive. The larger the size of the firm (or the lower the MES in the industry), the

more likely it is that it will have achieved a stable position in its original market and

may own excess assets and resources that may be used in expanding into a new

industry. We therefore expect that a firm will be more likely to diversify the greater

its size and the lower the industry MES.

The firm’s growth rate is also an interesting indicator of its chances of

diversification. If the growth rate is slowing down, the firm may be approaching the

MES (Mata, Portugal and Guimarães, 1995) and therefore fewer investments are

required to achieve efficiency in its original industry. Hence, further investments may

be directed at other industries. Moreover, if the firm is not growing (or growing

slower than the market) it may be facing difficulties with competition – possibly

associated with an entry mistake – and should have a greater incentive to diversify.

4 The data have information about each individual’s occupational position and status within the firm coded using the International Standard Classification of Occupations (ISCO) and the International Classification by Status in Employment (ICSE).

13

We therefore expect that a firm will be more likely to diversify if its growth rate is

lower.5

As pointed out earlier, increased density or concentration in a market reduces

competitive pressure for incumbents and provides less scope for growth within the

industry (Hannan and Carroll, 1992; Bunch and Smiley, 1992). Firms in concentrated

industries may therefore have a greater incentive to diversify since they have both a

secure position and few opportunities for growth in their original industry. We control

for the effect of market concentration on the chance of diversification using the

logarithm of the Herfindahl concentration index for the firm’s original industry.

The overall size of the original industry and its growth rate also play a role in

stimulating (or slowing down) diversification. Large industries and industries

registering high growth rates afford young firms greater possibilities for growth,

making the opportunity cost of diversifying greater. It is therefore expected that firms

in larger and growing industries will be less likely to diversify. We include both the

logarithm of industry size and its growth rate as control variables in our study.

As discussed in section 2, industries registering high growth rates also register

higher rates of both entry and exit, due to uncertainty associated with high growth

volatility. Industries with volatile demand correspond to an unstable environment

where size adjustments by firms are recurrent and entry mistakes due to

overconfidence are frequent. It is expected that in such industries young firm

diversification carried out due to necessity associated with events that place the

venture in operational or financial trouble will be more likely to happen. We measure

volatility in industry growth using the logarithm of the standard deviation of the

growth rate of the firm’s original industry.

In order to capture effects associated with business cycles, a dichotomous variable

has been added, taking the value one in years when the unemployment rate decreases,

5 We measure firm size using the logarithm of the total number of employees. We follow Pashigian

(1969) in defining the MES as )/()/(

1AAnA i

n

i ii where A represents total employment in the

industry; iA denotes total employment in the i th firm size class; and in

denotes the number of firms

in the i th size class. Hence, the MES is computed as the sum of average firm sizes in all industry size classes, weighted by the proportion of employment accounted for by firms in each size class.

14

and the value zero otherwise. Cohort and industry sector dummies are also added to

the model, although their coefficients are not reported.

4.2. Estimation Results

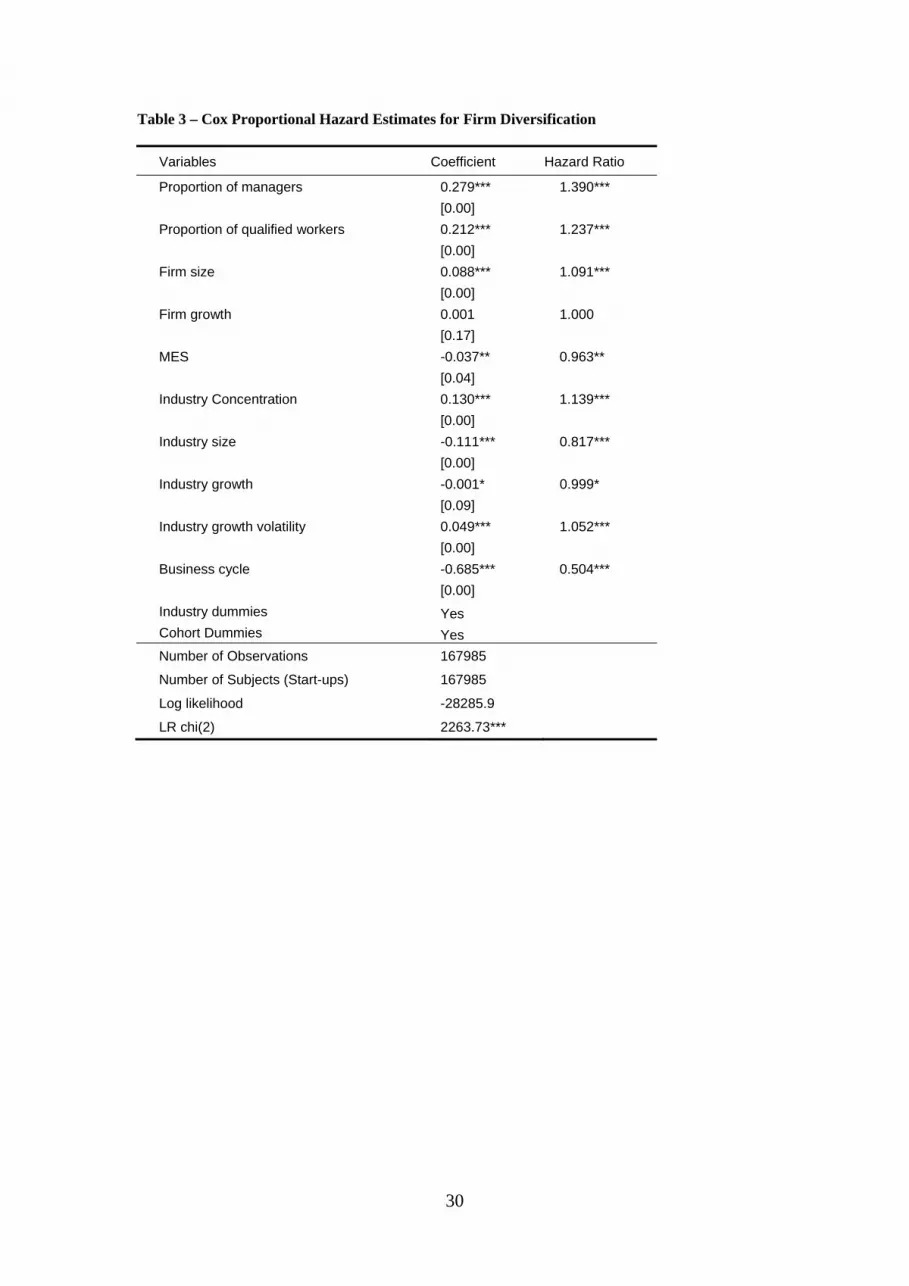

Estimates for the Cox model are presented in Table 3. Negative coefficients mean

that the explanatory variable has a negative impact on the likelihood of

diversification. Positive coefficients indicate that the explanatory variable has a

positive impact in the likelihood of diversification. In order to make interpretation of

the results clearer, rather than just presenting the coefficient estimates, we also present

the hazard ratios. The hazard ratio compares the effects of two different states of an

explanatory variable on the hazard rate, holding everything else constant; it is derived

by exponentiation of the estimated coefficient for an explanatory variable, holding all

other variables constant. If the hazard ratio equals one, it means that there is no impact

of the variable on the hazard of diversification. If the hazard ratio is larger than one,

higher values of the variable increase the hazard of diversification. If the hazard ratio

is lower than one, higher values of the variable decrease the hazard of diversification.

In general, the explanatory variables have the expected effects in light of the

observations presented in section 2. The proportion of managers and qualified

employees of the firm both have a positive impact on the likelihood of diversification.

This suggests that, if managerial and qualified human resources do indeed serve as

repositories of the firms’ knowledge and capabilities (regardless of whether these are

acquired pre- or post-entry) then having a greater proportion of such skilled human

resources provides a new firm with both the ability and the incentive to grow into new

industries where the routines and capabilities that are specific to the firm can be

deployed through these human resources.

As expected, larger young firms are more likely to diversify faster, possibly

because they have achieved sufficient efficiency gains from size increases. The

significant negative effect of the size of the industry MES on the likelihood of

diversification supports this finding – the larger the industry MES, the longer it should

take for the firm to achieve the required efficiency to be competitive, thus delaying

the investment of resources in a new industry. Larger young firms may also have an

incentive to diversify because they see fewer possibilities of further growth within the

15

same industry. However, the firm’s growth rate in the previous year has no significant

effect on the probability of diversification. This is not too surprising as we are dealing

with young, small firms whose yearly growth rates tend to fluctuate widely.6

Young firms in more concentrated markets are more likely to diversify early. This

result suggests that firms entering more concentrated markets are likely to find it

harder to achieve legitimacy and a stable market position, and may attempt to

diversify early in their lifetimes in order to correct an entry mistake or simply to

reduce the risk associated with entering a concentrated market. It can also be argued

that young firms which perceive they have achieved a secure position in a

concentrated industry may feel their position less threatened and be ready to use their

resources in a new industry, especially if the prospects for further growth are limited

in the native industry.

The overall size of the original industry and its growth rate have a negative impact

on the speed of diversification (although the effect for the industry growth rate is of

small magnitude and only weakly significant). This result suggests that larger and

growing industries may be seen by young, small firms has providing a favorable

environment for growth, making the opportunity cost of diversification higher and

leading them to invest all available resources into single-industry growth.

Entry into industries registering higher volatility in growth rates induces faster

diversification. The instability associated with demand volatility and uncertain

industry growth makes it more likely that entry mistakes and size adjustments will

occur. Diversification carried out by young firms is more likely to occur in these

industries due to unexpectedly low demand that may place the venture in operational

or financial trouble, or simply to reduce the risk associated with demand volatility.

Positive business cycles make young firm diversification less likely. This result

suggests that diversification by young, small firms has a significant necessity-based

component, associated with risk reduction and the correction of entry mistakes. When

the business cycle is positive, young firms may remain in their original industry due to

positive expectations of growth. When the business cycle is negative, young firms

have a greater incentive to look for their fortunes elsewhere.

6 Table 2 shows that the mean of firm yearly growth rates in about 42% while the standard deviation in over 730%.

16

5. Diversification and Survival

In this section we examine whether the pursuit of a diversification strategy – and

the timing of such diversification – influence the probability of survival for the start-

ups in our sample. We first adopt a non-parametric approach, examining the Kaplan-

Meier survivor functions for firms diversifying in different years in order to determine

whether there is a survival pattern associated with the timing of diversification. We

then estimate a semi-parametric hazard model with time-varying covariates, following

the procedure used for the analysis presented in section 4.

5.1. Non-parametric Analysis: Kaplan-Meier Survivor Functions

We first examine the Kaplan-Meier survivor functions for firms in our cohorts. The

diversification event separates diversified firms from non-diversified firms over time.

If a firm is born specialized (i.e. non-diversified) and remains so throughout the

period under analysis (or until it exits), it is in the non-diversified group. If a firm is

born diversified, it is on the diversified group during the whole period under analysis

(or until exit). If a firm is born specialized and, at time t, diversification occurs, the

firm switches from the non-diversified to the diversified group and remains so until

exit, or until the period under analysis ends.7

Figure 1 presents the survivor curves for diversified vs. non-diversified firms.

There appears to be a significant difference in survival patterns between diversified

and specialized firms in favor of diversification. This is confirmed by a long-rank

(LR) test, which registers a chi-square value of 44.49, significant at the 1% level.

Closer inspection of Figure 1 suggests that the significant differences in survival

patterns between the diversified and non-diversified groups are largely determined by

the proportion of firms exiting during the first year after start-up. After the first year,

the survivor curves show an approximately parallel slope, and the gap between

diversifiers and non-diversifiers does not widen significantly. We then examine the

Kaplan-Meier survivor functions for diversifiers and non-diversifiers according to the

7 Our data does not register events in which a diversified firm specializes, i.e. disinvests from one of its lines of business. All disinvestment events correspond to firm closures.

17

age of the firm at the time diversification occurs. For this, we create a set of eleven

binary variables. The first of these variables equals one for firms that are born

diversified and zero otherwise; the other ten variables each equal one for firms that

diversify between one and ten years after start-up, and zero otherwise. In this way, we

differentiate survivor curves according to the firm’s age when diversification occurs.8

Figure 2 presents the Kaplan-Meier survivor curves for firms diversified at birth

vs. all other firms. Figures 3-12 compare the survivor curves of firms that diversified

between one and ten years after start-up with non-diversifiers, given that non-

diversifiers had survived up to the year of diversification. It becomes clear that the

advantage of diversifiers over non-diversifiers is mostly associated with the greater

proportion of survivors among firms that were born diversified vs. firms that were

born specialized. For firms that were not diversified at start-up, the survival pattern

depends on the timing of diversification. Firms who diversify between the first and

fifth years of age register a significantly lower propensity to survive compared with

non-diversifiers. While there appears to be little difference in survival patterns

between firms who diversified in their sixth and seventh years and non-diversifiers,

firms who diversify in their eighth year or after register a clearly higher proportion of

survivors than non-diversified firms who had survived up to the year of

diversification.

These results suggest that a diversification strategy planned before start-up is likely

to be based on sufficient pre-entry resources and capabilities, taking advantage of

synergies and the sharing of co-specialized assets, representing a significant

advantage for firm survival. For firms that are not diversified at start-up,

diversification in the first years is likely to be more of a necessity associated with risk

reduction and entry mistakes than a strategy for growth. Firms likely overstretch their

resources and face a greater chance of failure. It appears however that, six to seven

years after start-up, some surviving firms may have acquired the necessary

experience, resources and capabilities essential for successful diversification as such a

strategy again enhances future survival chances. A more detailed analysis of the

determinants of survival is required to ascertain whether this is so.

8 We do not consider diversification in the 12th year as the data is left-censored and we would not be able to assess survival after that.

18

5.2. Semi-parametric Analysis: Proportional Hazards Model

We further examine survival of diversifying and non-diversifying firms by using a

Cox proportional hazards model, following the procedure used in section 4.

5.2.1. Explanatory Variables

In order to explain young firm survival, we use the set of eleven binary variables

differentiating firms according to their age when diversification occurs. To recap, the

first of these variables equals one for firms that are born diversified and zero

otherwise; the other ten variables each equal one for firms that diversify between one

and ten years after start-up, and zero otherwise. These binary variables switch from

zero to one the year in which the firm diversifies and remain equal to one afterwards.

In this way we can determine the effect of diversification on the probability of exit of

firms that diversified at different ages.

A set of control variables is used to account for firm-level and industry-level

determinants of survival, as well as the business cycle. As mentioned in section 4,

definitions and descriptive statistics for all the variables used in this paper are shown

in Table 2. The extant empirical evidence on firm survival points to a negative

relationship between hazard rates and size (Caves 1998; Carroll and Hannan, 2000).

This effect is independent of age. In addition to the logarithm of the firm’s current

size (measured by the number of employees), we include the firm’s growth rate as a

control variable. We expect growing firms to have a lower probability of exit. These

variables should provide an additional control to the effect of diversification on

survival. When a firm diversifies it is likely that it will employ more personnel. A

greater probability of survival may therefore be solely the result of the increase in size

and not of diversification itself.

Studies of survival have also addressed the effect of organizational characteristics

on survival probabilities. A number of authors have pointed out that a firm’s

knowledge resides in its human resources (Grant, 1996; Conner and Prahalad, 1996)

and it is the firm’s human capital that provides the basis for sustained competitive

advantage (Youndt et al., 1996; Teece, Pisano and Shuen, 1997; Eisenhardt and

Martin, 2000; Hitt et al., 2001). Mata and Portugal (2002) argue that the quantity (and

quality) of the education held by a firm’s workforce can be regarded as a measure,

19

albeit imperfect, of firm-specific resources and capabilities. We therefore control for

the level of education of the firms’ employees.

Studies conducted for a variety of countries and industries (reviewed in Caves,

1998) suggest that there are three main industry-level forces influencing survival: i)

economies of scale; ii) market concentration and barriers to entry; iii) industry growth.

The larger the MES in an industry, the higher is the cost of adjustment for new firms

(Audretsch, 1995). Hence, firms entering industries where the MES is larger face a

lower probability of survival. We therefore follow the same procedure as in section 4

in including the MES in the firm’s industry of origin as a control variable.

Organizational ecologists (e.g. Hannan and Carroll, 1992) maintain that

competition is a force which increases mortality. When the number of firms in a

market is low, an increase in density (i.e. a decrease in market concentration) leads to

increased legitimacy and may favor survival; however, after a certain point, further

increases in the number of firms lead to increased competition and increased

mortality. Industrial economists argue that competitive (i.e. less concentrated) markets

exert a strong disciplinary effect and drive inefficient firms out of the market, while

high levels of concentration facilitate collusion, so in highly concentrated markets

incumbents are more likely to retaliate against entrants (Bunch and Smiley, 1992). We

control for the effect of market concentration on survival through the same procedure

used in section 4.

Larger industries and industries registering higher growth rates are likely to

provide an environment in which the probability of exit is lower. Large market size or

high growth might make survival easier. However, evidence shows that larger and

growing industries also register higher rates of both entry and exit, reflecting greater

intensity of competition (Agarwal and Gort, 1996). We control for these effects using

the same measures as in section 4. A variable accounting for the business cycle is also

included in the survival analysis. Cohort and industry sector dummies are also added

to the survival model, although their coefficients are not reported.

5.2.2. Estimation Results

Estimation results of the Cox proportional hazards model are presented in Table 4.

A coefficient with a negative sign indicates that the variable reduces the hazard of exit

20

thus having a positive effect on survival. Likewise, a positive sign indicates that the

variable increases the likelihood of exit, or has a negative effect on survival.

The hazard ratios are particularly useful for analyzing the effect of the

diversification timing variables on the probability of survival. Consider the case of the

binary variable taking the value one if the firm diversifies at birth and zero otherwise.

In our estimation, the hazard ratio for firms that were diversified at birth is significant

and equal to 0.78. This means that, all else equal, firms that were born diversified are

only 78% as likely to exit as firms who were not diversified at birth; another way of

expressing this result would be to say that firms who are diversified at birth are about

28% more likely to survive than firms who were not diversified at birth.9

While coefficients are not significant for firms who diversified during their first

year, hazard ratios for firms that diversified from the second to the fourth years after

start-up are significant and generally indicate that diversification this early in the

firms’ lifetimes hinders survival (i.e. hazard ratios are significantly greater than one).

A firm that diversifies in its fourth year is 26% more likely to exit afterwards than a

non-diversifier who has survived up to that year. After the fourth year, however,

circumstances change. While not significant, hazard ratios for firms who diversified in

the fifth year after start-up approach one. For diversification in the sixth year or later,

coefficients are significant and hazard ratios indicate that firms that diversify are more

likely to survive than the ones that do not. Hazard ratios are smaller than one and their

magnitudes diminish as diversification occurs later in the firms’ lifetimes. Firms that

diversify in their sixth year are only about 72% as likely to exit (i.e. about 38.9%

more likely to survive) as firms who survive up to the sixth year and did not diversify

then. Firms that diversify in their tenth year of age are only 26% as likely to exit (i.e.

almost four times more likely to survive) over the next two years as firms that, having

survived through ten years, do not diversify.

These results generally confirm the evidence shown by the Kaplan-Maier survivor

functions. Firms that are diversified at start-up seem to have the required resources

and capabilities to do it and may be taking advantage of synergies and co-specialized

and innovative assets across different industries. Therefore, such strategy has a

positive effect on the probability of survival. Firms who choose to diversify in the first

9 This result is achieved since 1/0.78 = 1.282.

21

years after start-up are more likely to be doing it out of necessity, to reduce the risk

associated with a volatile market or to correct an entry mistake. These firms are less

likely to own the resources and capabilities required by more than one industry and

may be overstretching the available capital and human resources. Such firms face a

higher chance of failure. However, from the sixth year of age onwards, diversification

again becomes a growth strategy enhancing survival probabilities. As the firm

becomes older, the contribution of diversification to enhance the chances of survival

increases. This may be because, having been in the market for some time, firms might

have acquired legitimacy, implemented routines, learned about their efficiency, and

obtained the necessary resources and capabilities to deploy in a new industry. Also, it

may be that chances for further growth in the original industry are exhausted and it is

appropriate for the firm to look for profitable opportunities elsewhere.

The control variables are significant and have, in general, the expected effects.

Larger firms and firms that are growing are less likely to exit at any time. Firm human

capital has a positive effect on survival, but of very low magnitude. Young, small

firms are more likely to exit from industries where the MES is large, due to their

efficiency disadvantages vis-à-vis the larger incumbents. Market concentration has a

positive effect on survival, possibly due to less intense competition in more

concentrated markets, while firms in larger industries are also more likely to survive.

Firms are more likely to exit when the business cycle is unfavorable. The only

somewhat unexpected result is the negative effect of the industry growth rate on

survival. This is likely because growing industries usually register higher levels of

both entry and exit. Growing industries attract large entry flows which signal a low

level of legitimation in the market and contribute to drive out recent entrants. The

empirical evidence from studies in industrial economics (Romanelli, 1989; Mata and

Portugal, 1994; Audretsch, 1995) supports this result.

6. Conclusions

This paper has examined the first-time diversification decision by young firms by

asking which factors determine the timing of diversification for a start-up, and how

does diversification affect the probability of survival of young firms.

22

Examining data for Portuguese firms in the period 1988-2000, we find that only a

very small proportion of young, small firms diversify in their first years. The

proportions of managers and qualified employees of the firm both have a positive

impact on the likelihood of diversification, supporting resource-based views about

diversification being used to deploy the firms’ managerial and qualified human

resources into new industries. If human resources embody the firm’s specific

knowledge, routines, and capabilities, then having a greater proportion of such

resources is likely to lead the firm to expand faster toward new industries where such

resources can be deployed. Young firms that entered highly concentrated industries

and/or industries with high growth rate volatility are more likely to diversify early in

their lifetimes, possibly due to necessity associated with correcting entry mistakes.

Start-ups entering industries where retaliation by concentrated incumbents is strong,

or where demand growth is lower than expected, may be forced to divert resources to

new industries in order to reduce risks and correct entry mistakes. The study therefore

finds support for the two main drivers of young firm diversification identified in the

literature.

Findings with respect to the effect of diversification on the probability of survival

of young firms are particularly striking. Results suggest that a diversification strategy

which is planned before start-up and implemented at the moment of entry represents a

significant advantage for firm survival, possibly because it is based on sufficient pre-

entry resources and capabilities, taking advantage of synergies and the sharing of co-

specialized assets. For firms that are not diversified at start-up, diversification in the

first four or five years significantly hinders survival. Such diversification is likely to

result more from necessity associated with risk reduction and entry mistakes than

from a deliberate growth strategy, likely overstretching resources. Circumstances

change significantly for firms diversifying in their sixth year of age and later: exit

probabilities diminish as the firm’s age at diversification increases. Diversification

again becomes a growth strategy enhancing survival chances. Firms may have

acquired legitimacy, implemented routines, learned about their efficiency, and

accumulated the necessary resources and capabilities to deploy in a new industry.

Such results again provide support for the importance of the two main drivers of

young firm diversification identified by the present study.

23

These results have obvious implications for managers and practitioners. While

diversification is a growth strategy applied by a very small subset of young, small

firms, it nevertheless seems to be a legitimate, survival-enhancing strategy when it is

planned based on resources and capabilities that are available to the entrepreneurial

team before entry occurs. When occurring after start-up, diversification in the very

early years of a firm’s lifetime is not a recommendable strategy for survival, and

seems more likely to occur as an ‘escape’ associated with intense competition and

demand fluctuations in the original market. The evidence suggests that it takes time –

on average at least six years – to build and acquire the resources, routines, assets and

capabilities that make diversification a successful, survival-enhancing strategy.

There are noteworthy limitations to this study. Firstly, the nature of our data, while

longitudinal and encompassing, does not cover a time span long enough to assess the

survival chances of firms who diversify after their tenth year. While the pattern of

results suggests that the hazard of exit goes further down the later the firm diversifies,

it is impossible to ascertain whether this pattern is inverted or remains constant after

the time span covered by the data. Secondly, the small proportion of diversifying

firms in the data does not allow for distinguishing the motivations and survival

performance of related and unrelated diversifiers. Finally, while the data available

provide significant information on firm and industry evolution, it does not contain

information on the specific technologies underlying different firms and industries. We

therefore assumed knowledge assets and capabilities to be embodied in the firms’

human resources. While this implication is supported by previous literature (Grant,

1996; Conner and Prahalad, 1996; Youndt et al., 1996; Teece, Pisano and Shuen,

1997; Eisenhardt and Martin, 2000; Hitt et al., 2001), the assessment of the role

played by synergies and the sharing of co-specialized and innovative assets as

motivators of young, small firm diversification is necessarily limited in our approach.

References

Adner R, Helfat CE. 2003. Corporate effects and dynamic managerial capabilities. Strategic Management Journal 24: 1011-1025.

Agarwal R, Audretsch DB. 2001. Does entry size matter? The impact of the life cycle and technology on firm survival. Journal of Industrial Economics 49: 21-43.

24

Agarwal R, Gort M. 1996. The evolution of markets and entry, exit and survival of firms. Review of Economics and Statistics 78: 489-498.

Agarwal R, Gort M. 2002. Firm and product life cycles and firm survival. The American Economic Review 92(2): Papers and Proceedings, 14th AEA Meeting, 184-190.

Alvarez SA, Busenitz LW. 2001. The entrepreneurship of resource-based theory. Journal of Management 27: 755-775.

Amit R, Schoemaker PJH. 1993. Strategic assets and organizational rent. Strategic Management Journal 14: 33-46.

Anand J, Singh H. 1997. Asset redeployment, acquisitions and corporate strategy in declining industries. Strategic Management Journal 18: 99-118.

Ansoff I. 1987 [1965]. Corporate Strategy. Revised Edition, Penguin Books, Harmondsworth, England.

Argyres N. 1996. Capabilities, technological diversification, and divisionalization. Strategic Management Journal 17(5): 395–410.

Audretsch DB. 1995. Innovation and Industry Evolution. MIT Press: Cambridge MA.

Auerswald PE. 2008. Entrepreneurship in the theory of the firm. Small Business Economics 30: 111-126.

Barney JB. 1986. Strategic factor markets: expectations, luck, and business strategy. Management Science 32: 1512-1514.

Barney J. 1991. Firm resources and sustained competitive advantage. Journal of Management 27(1): 99-120.

Bartelsman E, Scarpetta S, Schivardi F. 2005. Comparative analysis of firm demographics and survival: evidence from micro-level sources in OECD countries. Industrial and Corporate Change 14: 365-91.

Cabral LMB. 1997. Entry Mistakes. Centre for Economic Policy Research Discussion Paper No. 1729. CEPR: London.

Cabral LMB, Mata J. 2003. On the evolution of the firm size distribution: facts and theory. American Economic Review 93(4): 1075-1090.

Camerer C, Lovallo D. 1999. Overconfidence and excess entry. American Economic Review 89(1): 306-18.

Carland JW, Hoy F, Foulton WR, Carland JAC. 1984. Differentiating entrepreneurs from small business owners: A conceptualization. Academy of Management Review 9(2): 354-359

Carroll GR, Hannan MT. 2000. The Demography of Corporations and Industries. Princeton University Press: Princeton.

25

Caves RE. 1998. Industrial organization and new findings on the turnover and mobility of firms. Journal of Economic Literature 36: 1947-1982.

Chandler A. 1962. Strategy and Structure. MIT Press: Cambridge MA.

Conner KR, Prahalad CK. 1996. A resource based theory of the firm: knowledge versus opportunism. Organization Science 7(5): 477-501.

Cox D. 1972. Regression models and life-tables. Journal of the Royal Statistical Society Series B 34: 187- 202.

Davidsson P, Achtenhagen L, Naldi L. 2006. What do we know about small Firm growth? In The Life Cycle of Entrepreneurial Ventures, International Handbook Series on Entrepreneurship. Ed. Parker S. Springer: New York, NY.

Delmar F, Shane S. 2004. Legitimating first: organizing activities and the survival of new ventures. Journal of Business Venturing 19: 385–410.

Edwards CD. Conglomerate Bigness as a Source of Power. National Bureau Committee for Economic Research, Business Concentration and Price Policy. Princeton University Press: Princeton.

Eisenhardt KM, Martin JS. 2000. Dynamic capabilities: what are they? Strategic Management Journal 21: 1105-1121.

Ericson R, Pakes A. 1995. Markov-perfect industry dynamics: a framework for empirical work. Review of Economic Studies 62: 53-82.

Evans DS. 1987. The relationship between firm growth, size and age: estimates for 100 manufacturing industries. Journal of Industrial Economics 35: 567-581.

Filatotchev L, Toms S. 2003. Corporate governance, strategy and survival in a declining industry: A study of UK cotton textile companies. Journal of Management Studies 40: 895-920.

Ghemawat P, Nalebuff B. 1990. The devolution of declining industries. Quarterly Journal of Economics 105(1): 167-186.

Giarratana M. 2004. The birth of a new industry: entry by start-ups and the drivers of firm growth the case of encryption software. Research Policy 33: 787-806.

Grant R. 1996. Toward a knowledge-based theory of the firm. Strategic Management Journal 17: 109–122.

Gribbin JD. 1976. The conglomerate merger. Applied Economics 8: 19-35.

Hall B. 1987. The relationship between firm size and firm growth in the United States manufacturing sector. Journal of Industrial Economics 35: 583–606.

Hall R. 1992. The strategic analysis of intangible resources. Strategic Management Journal 13(2): 135-144

26

Haveman H. 1995. The demographic metabolism of organizations: industry dynamics, turnover, and tenure distributions. Administrative Science Quarterly 40: 586–618.

Helfat CE, Lieberman MB. 2002. The birth of capabilities: market entry and the importance of pre-history. Industrial and Corporate Change 11(4): 725-760.

Helfat CE, Peteraf MA. 2003. The dynamic resource-based view: capability lifecycles. Strategic Management Journal 24: 997-1010.

Hitt M, Bierman L, Shimizu K, Kochhar R. 2001. Direct and moderating effects of human capital on strategy and performance in professional service firms: a resource-based perspective. Academy of Management Journal 44:13-28.

Hopenhayn H. 1992. Entry, exit, and firm dynamics in long run equilibrium, Econometrica 60(5): 1127-1150.

Jensen MC. 1986. Agency costs of free cash flow, corporate finance, and takeovers. American Economic Review 76: 323-29.

Jovanovic B. 1993. The diversification of production. Brookings Papers on Economic Activity - Microeconomics 1: 197-247.

Kahneman D, Lovallo D. 1993. Timid choices and bold forecasts: a cognitive perspective on risk taking. Management Science 39: 17-31.

Kim D, Kogut B. 1996. Technological platforms and diversification. Organization Science 7(3): 283-300.

Klepper S. 2007. Disagreements, spinoffs, and the evolution of Detroit as the capital of the U.S. automobile industry. Management Science 53(4): 616-631.

Levinthal D, Myatt J. 1994. Co-evolution of capabilities and industry: the evolution of mutual fund processing. Strategic Management Journal 15: 45-62.

Lynn M. 1998. Patterns of micro-enterprise diversification in transitional Eurasian economies. International Small Business Journal 16(2): 34-49.

Lynn M, Reinsch NL. 1990. Diversification patterns among small businesses. Journal of Small Business Management 28: 60-70.

MacDonald J. 1984. Diversification, market growth, and concentration in U.S. manufacturing. Southern Economic Journal 50(4): 1098-1111.

Marris R. 1963. A model of the ‘managerial’ enterprise. Quarterly Journal of Economics 77(2): 185-209.

Marris R. 1964. The Economic Theory of Managerial Capitalism. Macmillan: London.

Mata J, Portugal P. 1994. Life duration of new firms. Journal of Industrial Economics 42(3): 227-245.

27

Mata J, Portugal P. 2002. The survival of new domestic and foreign-owned firms. Strategic Management Journal 23: 323-343.

Mata J, Portugal P, Guimarães P. 1995. The Survival of new plants: entry conditions and post-entry evolution. International Journal of Industrial Organization 13: 459-482.

Miles R. 1982. Coffin Nails and Corporate Strategies. Prentice Hall: Engelwood Cliffs NJ.

Miller DJ. 2004. Firms’ Technological resources and the performance effects of diversification a longitudinal study. Strategic Management Journal 25: 1097-1119.

Miller DJ. 2006. Technological diversity, related diversification, and firm performance. Strategic Management Journal 27: 601–619

Montgomery CA. 1994. Corporate diversification. Journal of Economic Perspectives 8: 163-178.

Mosakowski E. 1998. Entrepreneurial resources, organizational choices, and competitive outcomes. Organization Science 9(6): 625-643

Nelson RR, Winter SG. 1982. An Evolutionary Theory of Economic Change. The Belknap Press of Harvard University Press: Cambridge.

Palich LE, Cardinal LB, Miller CC. 2000. Curvilinearity in the diversification-performance linkage: an examination over three decades of research. Strategic Management Journal 21(2): 155-174.

Panzar JC, Willig RD. 1981. Economies of scope. American Economic Review 71: 268-72.

Pashigian P. 1969. The effect of market size on concentration. International Economic Review 10(3): 291-314.

Pavitt K, Robson M, Townsend J. 1989. Technological accumulation, diversification and organization in UK companies, 1945-1983. Management Science 35(1): 81-99.

Penrose ET. 1959. The Theory of the Growth of the Firm. Basil Blackwell: Oxford.

Peteraf M. 1993. The cornerstones of competitive advantage, Strategic Management Journal 14(3): 179-191.

Raffa M, Zollo G, Caponi R. 1996. The development process of small firms. Entrepreneurship and Regional Development 8(4): 359-372.

Ramanujam V, Varadarajan P. 1989. Research on corporate diversification: a synthesis. Strategic Management Journal 10(6): 523-551.

Romanelli E. 1989. Environments and strategies at startup: effects on early survival. Administrative Science Quarterly 34: 369-387.

28

Rosa P, Scott M. 1999. Entrepreneurial diversification, business-cluster formation, and growth, Environment and Planning C: Government and Policy, 17: 527-547.

Santarelli E, Vivarelli M. 2007. Entrepreneurship and the process of firms’ entry, survival and growth. Industrial and Corporate Change, 16(3): 455-488.

Sandvig J. 2000. The role of technology in small firm diversification. Journal of Technology transfer 25: 157-168.

Shane S. 2000. Prior knowledge and the discovery of entrepreneurial opportunities. Organization Science 11: 448-469.

Sharma A, Kesner I. 1996. Diversifying entry: some ex ante explanations for post-entry survival and growth. Academy of Management Journal 39: 635-677.

Silverman BS. 1999. Technological resources and the direction of diversification: toward an integration of the resource-based view and transaction cost economics. Management Science 45: 1109–1124.

Sinha D. 1999. On conglomerate diversification, Anthology. Atlantic Economic Journal 27(1): 115.

Song M, Podoynitsyna K, van der Bij H, Hamlan J. 2008. Success factors in new ventures: A meta-analysis, Journal of Product Innovation Management 25: 7-27.

Stern I, Henderson AD. 2004. Within-business diversification in technology-intensive industries. Strategic Management Journal 25: 487–505.

Tanriverdi H, Venkatraman N. 2005. Knowledge relatedness and the performance of multibusiness firms. Strategic Management Journal 26(2): 97-119.

Teece DJ. 1980. Economics of scope and the scope of the enterprise. Journal of Economic Behavior and Organization 1: 223-47.

Teece DJ. 1982. Towards an economic theory of the multiproduct firm. Journal of Economic Behavior and Organization 3(1): 39-63.

Teece DJ. 1998. Capturing value from knowledge assets: The new economy, markets for know-how, and intangible assets. California Management Review 40(3): 55-79.

Teece DJ, Pisano G, Shuen A. 1997. Dynamic capabilities and strategic management. Strategic Management Journal 18: 509-533.

Vivarelli M. 2004. Are all the potential entrepreneurs so good? Small Business Economics 23(1): 41-49.

Vivarelli M, Audretsch DB. 1998. The link between the entry decision and post-entry performance: Evidence from Italy. Industrial and Corporate Change 7(3): 485-500.

Youndt M, Snell S, Dean J, Lepak D. 1996. Human resource management, manufacturing strategy and firm performance. Academy of Management Journal 39: 836-866.

29

Table 1 – Entry Cohorts

Entry Cohort

Cohort Size

Follow-up Period Total Exits

Related Diversified Firms

Unrelated Diversified

Firms

Total Diversified

Firms

Period Number (%) Number (%) Number (%) Number (%) 1988 22821 1989-2000 14522 63.6 198 0.87 430 1.88 601 2.63

1989 26336 1990-2000 16180 61.4 170 0.65 345 1.31 481 1.83

1990 22735 1991-2000 13530 59.5 127 0.56 260 1.14 368 1.62

1991 24676 1992-2000 13891 56.3 118 0.48 202 0.82 305 1.24

1992 24649 1993-2000 13544 54.9 101 0.41 174 0.71 266 1.08

1993 24620 1994-2000 12531 50.9 103 0.42 146 0.59 238 0.97

1994 39451 1995-2000 17727 44.9 164 0.42 226 0.57 378 0.96

Total 185288 101925 55.0 981 0.53 1783 0.96 2637 1.42

Table 2 – Variable Definitions and Descriptive Statistics

Variable Description Mean Std. Dev. Min Max

Proportion of managers

Proportion of firm employees in managerial positions x 100 18.00 26.20 0.00 100.00

Proportion of qualified workers

Proportion of firm employees in qualified and highly qualified worker

positions x 100 38.00 36.50 0.0 100.00

Firm size Logarithm of firm’s number of employees in the previous year 1.31 1.12 0.02 10.31

Firm growth Firm growth rate in previous year x 100 42.81 733.73 -99.0 1487.64

Firm human capital

Proportion of employees with college degree x 100 6.50 14.20 0.00 100.00

MES Logarithm of minimum efficient scale in the industry where the firm entered (six

digit sector) 2.04 0.73 0.05 6.14

Industry concentration

Logarithm of industry Herfindahl index x 100 (six digit sector) 3.62 1.40 1.00 9.23

Industry size Proportion of industry employment in

total employment x 100 (six digit sector)

0.02 0.04 0.0 0.54

Industry growth Employment growth rate in the industry x 100 (six digit sector) 3.74 83.81 -53.44 16038.42

Industry growth volatility

Logarithm of standard deviation of employment growth rates in the

industry (six digit sector) 7.98 9.36 0.00 11.69

Business cycle Dummy variable equal to one when yearly unemployment rate decreases 0.13 0.33 0.00 1.00

30

Table 3 – Cox Proportional Hazard Estimates for Firm Diversification

Variables Coefficient Hazard Ratio

Proportion of managers 0.279*** 1.390***

[0.00]

Proportion of qualified workers 0.212*** 1.237***

[0.00]

Firm size 0.088*** 1.091***

[0.00]

Firm growth 0.001 1.000

[0.17]

MES -0.037** 0.963**

[0.04]

Industry Concentration 0.130*** 1.139***

[0.00]

Industry size -0.111*** 0.817***

[0.00]

Industry growth -0.001* 0.999*

[0.09]

Industry growth volatility 0.049*** 1.052***

[0.00]

Business cycle -0.685*** 0.504***

[0.00]

Industry dummies Yes

Cohort Dummies Yes

Number of Observations 167985

Number of Subjects (Start-ups) 167985

Log likelihood -28285.9

LR chi(2) 2263.73***

31

Table 4 – Cox Proportional Hazard Estimates for Firm Survival

Variables Coefficient Hazard Ratio

Born diversified -0.250*** 0.781***

[0.01]

Diversified year 1 -0.021 0.982

[0.82]

Diversified year 2 0.151** 1.159**

[0.03]

Diversified year 3 0.163** 1.172**

[0.03]

Diversified year 4 0.230** 1.261**

[0.04]

Diversified year 5 0.080 1.084

[0.55]

Diversified year 6 -0.332** 0.723**

[0.03]

Diversified year 7 -0.663 0.509

[0.02]

Diversified year 8 -0.633** 0.532**

[0.01]

Diversified year 9 -0.744*** 0.478***

[0.01]

Diversified year 10 -1.378** 0.262**

[0.05]

Firm size -0.401*** 0.672***

[0.00]

Firm human capital -0.004*** 0.991***

[0.00]

Firm growth -0.061*** 0.941***