Detecting false financial statements using published data: some evidence from Greece Charalambos T. Spathis Aristotle University of Thessaloniki, Department of Economics, Division of Business Administration, Thessaloniki, Greece Introduction References to false financial statement (FFS) are increasingly frequent over the last few years. Falsifying financial statements primarily consists of manipulating elements by overstating assets, sales and profit, or understating liabilities, expenses, or losses. When a financial statement contains falsifications so that its elements no longer represent the true picture, we speak of fraud. Management fraud can be defined as ``deliberate fraud committed by management that injures investors and creditors through misleading financial statements’’ (Eliott and Willingham, 1980). For Wallace (1995), fraud is ``a scheme designed to deceive; it can be accomplished with fictitious documents and representations that support fraudulent financial statements’’. The International Federation of Accountants issued in 1982 the International Statement of Auditing (ISA) No. 11: Fraud and Error and explains that the characteristic which differentiates error from fraud is intent. Errors result from unintentional actions (Colbert, 2000). The American Institute of Certified Public Accountants (AICPA) (1983) in Statement on Auditing Standards (SAS) No. 47 notes that ``error refers to unintentional misstatements or omissions of amounts or disclosures in the financial statements’’. SAS No. 82 (AICPA, 1997) reiterates the idea that fraud is an intentional act, and fraud frequently includes the perpetrator(s) feeling pressure or having an incentive to commit fraud and also perceiving an opportunity to do so. Fraud and white-collar crime has reached epidemic proportions in the USA. Some estimates suggest that fraud costs US business more than $400 billion annually (Wells, 1997). In Greece, the issue of false financial statements has lately been brought more into the limelight in connection primarily with: the increase in the number of companies listed on the Athens Stock Exchange and the raising of capital through public offering; and attempts to reduce the level of taxation on profits. The year 2000 has been very difficult for the Greek stock market, which has suffered from stagnation both in terms of share prices and liquidity. This fact, along with the recent pervasive record of false financial statements, increased the interest of the authorities, stock market, Ministry of the Economy and the banking sector in early- warning systems. In this context, the absence of a Greek study on the subject is striking. This paper intends to address this need in the existing literature. For this purpose, univariate and multivariate statistical tools were employed to investigate the usefulness of publicly available variables for detecting FFS. A total of ten variables were found to be possible indicators of FFS. These include the ratios: debt to equity, sales to total assets, net profit to sales, accounts receivable to sales, net profit to total assets, working capital to total assets, gross profit to total assets, inventory to sales, total debt to total assets, and financial distress (Z-score). Using stepwise logistic regression, two models were developed with a high probability of detecting FFS in a sample. The models include the variables: the inventories to sales ratio, the ratio of total debt to total assets, the working capital to total assets ratio, the net profit to total assets ratio, and financial distress (Z-score). The paper is organised as follows: the second section reviews research on false financial statements carried out up to now. The third section underlines the methodologies employed, the variables, the method and the sample data used in the present study. The fourth section describes The current issue and full text archive of this journal is available at http://www.emeraldinsight.com/0268-6902.htm [179] Managerial Auditing Journal 17/4 [2002 ] 179±191 # MCB UP Limited [ISSN 0268-6902] [DOI 10.1108/0268690021042432 1] Keywords Financial statements, Fraud, Regression analysis, Greece Abstract This paper examines published data to develop a model for detecting factors associated with false financial statements (FFS). Most false financial statements in Greece can be identified on the basis of the quantity and content of the qualifications in the reports filed by the auditors on the accounts. A sample of a total of 76 firms includes 38 with FFS and 38 non-FFS. Ten financial variables are selected for examination as potential predictors of FFS. Univariate and multivariate statistica l techniques such as logistic regression are used to develop a model to identify factors associated with FFS. The model is accurate in classifying the total sample correctly with accuracy rates exceeding 84 per cent. The results therefore demonstrate that the models function effectively in detecting FFS and could be of assistance to auditors, both internal and external, to taxation and other state authorities and to the banking system.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Detecting false financial statements using publisheddata: some evidence from Greece

Charalambos T. SpathisAristotle University of Thessaloniki, Department of Economics,Division of Business Administration, Thessaloniki, Greece

Introduction

References to false financial statement (FFS)

are increasingly frequent over the last few

years. Falsifying financial statements

primarily consists of manipulating elements

by overstating assets, sales and profit, or

understating liabilities, expenses, or losses.

When a financial statement contains

falsifications so that its elements no longer

represent the true picture, we speak of fraud.

Management fraud can be defined as

`̀ deliberate fraud committed by management

that injures investors and creditors through

misleading financial statements’’ (Eliott and

Willingham, 1980). For Wallace (1995), fraud

is `̀ a scheme designed to deceive; it can be

accomplished with fictitious documents and

representations that support fraudulent

financial statements’’.

The International Federation of

Accountants issued in 1982 the International

Statement of Auditing (ISA) No. 11: Fraud

and Error and explains that the

characteristic which differentiates error

from fraud is intent. Errors result from

unintentional actions (Colbert, 2000). The

American Institute of Certified Public

Accountants (AICPA) (1983) in Statement on

Auditing Standards (SAS) No. 47 notes that

`̀ error refers to unintentional misstatements

or omissions of amounts or disclosures in the

financial statements’’. SAS No. 82 (AICPA,

1997) reiterates the idea that fraud is an

intentional act, and fraud frequently includes

the perpetrator(s) feeling pressure or having

an incentive to commit fraud and also

perceiving an opportunity to do so. Fraud

and white-collar crime has reached epidemic

proportions in the USA. Some estimates

suggest that fraud costs US business more

than $400 billion annually (Wells, 1997).

In Greece, the issue of false financial

statements has lately been brought more into

the limelight in connection primarily with:

the increase in the number of companies

listed on the Athens Stock Exchange and

the raising of capital through public

offering; and

attempts to reduce the level of taxation on

profits.

The year 2000 has been very difficult for the

Greek stock market, which has suffered from

stagnation both in terms of share prices and

liquidity. This fact, along with the recent

pervasive record of false financial

statements, increased the interest of the

authorities, stock market, Ministry of the

Economy and the banking sector in early-

warning systems. In this context, the absence

of a Greek study on the subject is striking.

This paper intends to address this need in the

existing literature. For this purpose,

univariate and multivariate statistical tools

were employed to investigate the usefulness

of publicly available variables for detecting

FFS. A total of ten variables were found to be

possible indicators of FFS. These include the

ratios: debt to equity, sales to total assets, net

profit to sales, accounts receivable to sales,

net profit to total assets, working capital to

total assets, gross profit to total assets,

inventory to sales, total debt to total assets,

and financial distress (Z-score). Using

stepwise logistic regression, two models were

developed with a high probability of

detecting FFS in a sample. The models

include the variables: the inventories to sales

ratio, the ratio of total debt to total assets, the

working capital to total assets ratio, the net

profit to total assets ratio, and financial

distress (Z-score).

The paper is organised as follows: the

second section reviews research on false

financial statements carried out up to now.

The third section underlines the

methodologies employed, the variables, the

method and the sample data used in the

present study. The fourth section describes

The current issue and full text archive of this journal is available at

http://www.emeraldinsight.com/0268-6902.htm

[ 179 ]

Managerial Auditing Journal17/4 [2002] 179±191

# MCB UP Limited[ISSN 0268-6902][DOI 10.1108/0268690021042432 1]

KeywordsFinancia l statements, Fraud,Regression analysis, Greece

AbstractThis paper examines publisheddata to develop a model for

detecting factors associated withfalse financia l statements (FFS).Most false financial statements in

Greece can be identified on thebasis of the quantity and contentof the qualification s in the reports

filed by the auditors on theaccounts. A sample of a total of76 firms includes 38 with FFS and

38 non-FFS. Ten financialvariables are selected forexamination as potential

predictors of FFS. Univariate andmultivariate statistica l techniques

such as logistic regression areused to develop a model to identifyfactors associated with FFS. The

model is accurate in classifyingthe total sample correctly with

accuracy rates exceeding 84 percent. The results thereforedemonstrate that the modelsfunction effectively in detecting

FFS and could be of assistance toauditors, both internal andexternal, to taxation and other

state authorities and to thebanking system.

the empirical results and discussion obtained

using univariate tests and multivariate

logistic regression analysis. Finally, in the

fifth section come the concluding remarks.

Previews research

Characteristics of FFSNo one knows how many business failures

are actually caused by fraud, but undeniably

lots of businesses, especially small firms, go

bankrupt each year due to fraud losses. In the

USA incidences of fraud cut across all

industries with greatest losses apparent

(fraud losses by industry) in real estate

financing, manufacturing, banking, oil and

gas, construction, and in health care (Wells,

1997). Losses can occur in almost any area,

certainly not just in cash areas. Losses in

cash actually represent the lowest level of

fraud. Accounts receivable, expenditures for

services, and inventory losses are each three

times higher than those in cash. Fraud is not

just a problem in large firms. Small

businesses with 1-100 employees are also

susceptible. This is a serious problem

because fraud in a small firm has a greater

impact, as the firm does not have the

resources to absorb the loss (Wells, 1997). In a

global economy and multinational trade, the

trend of international fraud affects all

countries (Vanasco, 1998).

A report by the Committee of Sponsoring

Organizations of the Treadway Commission

(COSO) compiled by Beasley et al. (1999)

examined fraudulent financial reporting

from 1987-1997 by US public companies. Some

of the most critical insights of the study are:

The companies committing fraud

generally were small, and most (78 per

cent of the sample) were not listed in the

New York or American Stock Exchanges.

Incidences of fraud went to the very top of

the organisations concerned. In 72 per

cent of the cases, the CEO appeared to be

associated with the fraud, and in 43 per

cent the CEO was associated with the

financial statement fraud.

The audit committees and boards of the

respective companies appeared to be

weak. Most audit committees rarely met,

and the companies’ boards of directors

were dominated by insiders and others

outsiders `̀ grey’’ directors, with

significant equity ownership and

apparently little experience of serving as

directors of other companies. A total of 25

per cent of the companies did not have an

audit committee.

The founders and board members owned a

significant portion of the companies. In

nearly 40 per cent of the companies,

authorizations for votes by proxy

provided evidence of family relationships

among the directors and/or officers. The

founder and current CEO were the same

person or the original CEO/President was

still in place in nearly half of the

companies.

Severe consequences resulted when

companies commit fraud, including

bankruptcy, significant changes in

ownership, and suspension from trading

in national exchanges.

Most techniques for manipulating profits can

be grouped into three broad categories ±

changing accounting methods, fiddling with

managerial estimates of costs, and shifting

the period when expenses and revenues are

included in results (Worthy, 1984). Other

false statements include manipulating

documents, altering test documents, and

producing false work reports (Comer, 1998).

For example, recording revenue on

shipments after year-end by backdating

shipment documents. Asset

misappropriation schemes include the theft

of company assets e.g. cash and inventory.

The study of Vanasco (1998) examines the

role of professional associations,

governmental agencies, and international

accounting and auditing bodies in

promulgating standards to prevent fraud in

financial statements and other white-collar

crimes. It also examines several fraud cases.

The cases examined show that the cash,

inventory, and related party transactions are

prone to fraud. Auditors assign a high-risk

index to the potential misappropriation of

inventory, cash defalcation, and conflict of

interest. Typical financial statement fraud

techniques involved the overstatement of

revenues and assets (Beasley et al., 1999).

Over half the frauds involved overstating

revenues by recording revenues prematurely

or fictitiously. Many of those revenue frauds

only affected transactions recorded right at

the end of significant financial reporting

periods (i.e. quarter-end or year-end). About

half the frauds also involved overstating

assets by understating allowances for

receivables, overstating the value of

inventory, property, plant and equipment

and other tangible assets, and recording

assets that did not exist.

Fraudulent statements are the most costly

schemes per case. In spite of being the most

common and the smallest loss per case, asset

misappropriation presents in total the largest

losses of the categories. Fraudulent

statements, on the other hand, have the

lowest total losses. Corporate falsification

[ 180]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

can also be classified as the committed by

insiders for the company (violation of

government regulations, i.e. tax, securities,

safety and environmental laws). Senior

managers might perpetrate financial

statement falsifications to deceive investors

and lenders or to inflate profits and thereby

gain higher salaries and bonuses. Higson

(1999) analysed the results of 13 interviews

with senior auditors/forensic accountants on

whether their clients report suspected fraud

to an external authority. Although some

companies do report it, quite a number seem

reticent about reporting. There appear to be

three contributing factors:

1 the imprecision of the word `̀ fraud’’;

2 the vagueness of directors’

responsibilities; and

3 the confusion over the reason for the

reporting of suspected fraud.

In 1997, the Auditing Standards Board issued

Statement on Auditing Standards (SAS)

No. 82: Consideration of Fraud in a Financial

Statement Audit (AICPA, 1997). This Standard

requires auditors to assess the risk of fraud

on each audit and encourages auditors to

consider both the internal control system and

management’s attitude toward controls,

when making this assessment (Caplan, 1999).

This SAS No. 82, which supersedes SAS

No. 53, clarifies but does not increase

auditors’ responsibilities to detect fraud

(Mancino, 1997). Risk factors `̀ red flags’’ that

relate to fraudulent financial reporting may

be grouped in the following three categories

(SAS No. 82):

1 Management’s characteristics and

influence over the control environment.

These pertain to management’s abilities,

pressures, style, and attitude relating to

internal control and the financial

reporting process. For example, strained

relationships between management and

the current or previous auditor.

2 Industry conditions. These involve the

economic environment in which the

entity operates. For example, a declining

industry with increasing business

failures.

3 Operating characteristics and financial

stability. These pertain to the nature and

complexity of the entity and its

transactions, the entity’s financial

condition, and its profitability. For

example, significant related-party

transactions not in the ordinary course of

business or with related entities not

audited or audited by another firm.

Moreover, similarly to the well-examined

area of bankruptcy prediction, research on

FFS has been minimal. In an important

study, Matsumura and Tucker (1992) discuss

an extensive theoretical foundation of

auditor/manager strategic interaction. This

study investigates the effects of the following

variables:

auditor’s penalty;

auditing standard requirements;

the quality of the internal control

structure; and

audit fee.

The interaction between manager and

auditor is examined with fraud as the focus.

The model encompasses all irregularities,

which it categorises into two types: fraud

(misrepresentation of fact) and defalcations

(misappropriation of assets). For a strategy

with reference to auditing and fraud, Morton

(1993) notes that auditors often use sampling

methods to audit probabilistically and the

probability of auditing is usually contingent

on information about that item. His model

for optional audit policy yields an exact

solution that can generate some useful

comparative statistics. As the audit cost

decreases, the audit region (or extent of the

sample) expands and the amount of

misreporting declines.

Bloomfield (1997) uses behavioural

laboratory experiments, which indicated

amongst other conclusions that auditors

have more trouble assessing fraud risk when

they face high legal liability for audit failure

and the firm they are auditing has strong

internal controls in place. Another study

examines how reliance on a mechanical

decision aid is effected by decision

consequences (Boatsman et al., 1997).

Experimental participants made planning

choices based on available input from actual

management fraud cases before and after

receiving the decision aid’s predictions of

fraud probability. The experiment

documents two types of nonreliance:

1 intentionally shifting the final planning

judgement away from the aid’s prediction

even through this prediction supports the

initial planning judgement; and

2 ignoring the aid when its prediction does

not support the initial planning

judgement.

The study of Bonner et al. (1998) examines

whether certain types of financial reporting

fraud result in a higher likelihood of

litigation against independent auditors and

develops a new taxonomy to document types

of fraud that includes 12 general categories.

They find that auditors are more likely to be

sued when the financial statement frauds are

of types that most commonly occur or when

the frauds arise from fictitious transactions.

Auditors’ sensitivity with respect to clients’

[ 181 ]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

ethical status and their assessment of the

likelihood of fraud is examined by

Abdolmohammadi and Owhoso (2000). The

results indicate that senior auditors were

sensitive to ethical information, e.g.

regarding clients’ service to the community,

in making their assessment of the likelihood

of fraud, deeming such clients less likely to

have committed fraud.

Detecting FFSStatement of Auditing Standards (SAS) No. 82

(AICPA, 1997) requires auditing firms to

detect management fraud. This increases the

need to detect management fraud effectively.

Detecting management fraud is a difficult

task using normal audit procedures (Porter

and Cameron, 1987; Coderre, 1999). First,

there is a shortage of knowledge concerning

the characteristics of management fraud.

Second, given its infrequency, most auditors

lack the experience necessary to detect it.

Finally, managers are deliberately trying to

deceive the auditors (Fanning and Cogger,

1998). For such managers, who understand

the limitations of an audit, standard auditing

procedures may be insufficient. These

limitations suggest the need for additional

analytical procedures for the effective

detection of management fraud.

` ... Auditors using the expert system exhibited the ability todiscriminate better among situations with varying levels ofmanagement fraud risk and made more consistent decisionsregarding appropriate audit actions.... ’

Recent work has attempted to build models to

predict the presence of management fraud.

Results from logit regression analysis of 75

fraud and 75 no-fraud firms indicate that

no-fraud firms have boards with significantly

higher percentages of outside members than

fraud firms (Beasley, 1996). Hansen et al.

(1996) use a powerful generalized qualitative-

response model to predict management fraud

based on a set of data developed by an

international public accounting firm. The

model includes the probit and logit

techniques. An experiment was conducted to

examine the use of an expert system

developed to enhance the performance of

auditors (Eining et al., 1997). Auditors using

the expert system exhibited the ability to

discriminate better among situations with

varying levels of management fraud risk and

made more consistent decisions regarding

appropriate audit actions. Green and Choi

(1997) presented the development of a neural

network fraud classification model

employing endogenous financial data. A

classification model created from the learned

behaviour pattern is then applied to a test

sample. During the preliminary stage of an

audit, a financial statement classified as

fraudulent signals the auditor to increase

substantive testing during fieldwork.

Fanning and Cogger (1998) use an artificial

neural network (ANN) to develop a model for

detecting management fraud. Using publicly

available predictors of fraudulent financial

statements, they find a model of eight

variables with a high probability of

detection.

Summers and Sweeney (1998) investigate

the relationship between insider trading and

fraud. They find, with the use of a cascaded

logit model, that in the presence of fraud,

insiders reduce their holdings of company

stock through high levels of selling activity

as measured by either the number of

transactions, the number of shares sold, or

the dollar amount of shares sold. Beneish

(1999) investigates the incentives and the

penalties related to earnings overstatements

primarily in firms that are subject to

accounting enforcement actions by the

Securities and Exchange Commission (SEC).

He finds that the managers are likely to sell

their holdings and exercise stock

appreciation rights in the period when

earnings are overstated, and that the sales

occur at inflated prices. The evidence

suggests that the monitoring of managers’

trading behaviour can be informative about

the likelihood of earnings overstatement.

Eilifsen et al. (1999) and Hellman (1999)

analyse the link between the calculation of

taxable income and accounting income

influences on the incentive to manipulate

earnings, as well as the demand for

regulation and verification of both financial

statements and tax accounts. Abbot et al.

(2000) examine and measure the audit

committee independence and activity in

mitigating the likelihood of fraud. Using the

logistic regression analysis they find that

firms with audit committees which are

composed of independent directors and

which meet at least twice per year are less

likely to be sanctioned for fraudulent or

misleading reporting.

Prior work in this field has examined

several variables related to data from audit

work papers and from financial statements,

with various techniques, for their usefulness

in detecting management fraud (Fanning

et al., 1995). In this study, we examine in-

depth publicly available data from firms’

financial statements for detecting FFS.

Greece has entered the new millennium

with a very positive economic picture despite

some underlying structural inflation, and a

[ 182]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

stable social and political environment. In

June 2000, the leaders of the member states of

the European Union agreed to accept Greece

as a member of the Economic and Currency

Union. Greek enterprises continue to make

progress in profitability and efficiency. The

improvement in capital ratios, the increase

in investment, the significant increase in

profits and the return on capital are just

some of the indicators which make those

involved in Greek industries feel much more

optimistic than they did a few years ago. The

year 2000 has been very difficult for the

Greek Stock Market, which has suffered from

stagnation both in terms of share prices and

liquidity. This fact, along with the recent

pervasive record of false financial

statements, increased the interest of the

authorities, stock market, Ministry of the

Economy and the banking sector in early

warning systems.

In Greece, the issue of falsification of FS

has become of particular significance lately,

and this is due to the following:

Attempts to reduce the level of tax on

profits.

The increase in numbers of firms listed on

the Athens Stock Exchange, the large

increases in capital obtained by listed

companies, the extensive cooperation

achieved through takeovers and mergers

and the attempt by management to meet

the expectations of shareholders.

There is currently a backlog of companies

who are entering the Stock Exchange or

parallel market for the first time. The new

stock market (NEHA) for small and `̀ new

economy’’ enterprises will begin its operation

in 2001, and there is a strong interest in

listing. To avoid instances of false financial

statements being submitted by candidates

and other companies, examination by an

auditor is obligatory. Control by auditors is

also obligatory regarding the use of capital

raised through public floatation. The goal of

this research is to identify financial factors to

be used by auditors in assessing the

likelihood of FFS. The following section

discusses the methodology proposed to detect

FFS.

Methodology

SampleMost FFS in Greece can be identified on the

basis of the quantity and content of the

qualifications in the reports filed by the

auditors on accounts for: depreciation,

forecast payment defaults, forecast staff

severance pay, participation in other

companies, and fiddling of accounts for tax

purposes and other qualifications. The

classification of a financial statement as false

was based on:

the inclusion in the auditors’ reports of

opinions of serious doubt as to the

correctness of accounts;

the observations by the tax authorities

regarding serious taxation

intransigencies which seriously alter the

company’s annual balance sheet and

income statement;

the application of Greek legislation

regarding negative net worth;

inclusion of the company in the Athens

Stock Exchange categories of `̀ under

observation’’ and `̀ negotiation suspended’’

for reasons associated with falsification of

the company’s financial data; and

the existence of court proceedings

pending with respect to FFS or serious

taxation contraventions.

The sample of a total of 76 manufacturing

firms includes 38 with FFS and 38 with non-

FFS (the sample did not include financial

companies). For the non-FFS firms of the

sample, no published indication of FFS

behaviour was uncovered in a search of

databases and the relevant auditors’ reports.

It has to be noted that while the process of

ensuring that none of the considered non-FFS

firms had issued FFS was extensive, it cannot

guarantee that the financial statements in

this group of firms were not falsified. It only

guarantees that there was no publicly

available FFS information in the auditors’

reports and other sources, such as the Stock

Exchange and the Ministry of Finance. Since

this only covers information known to this

date, there is no guarantee that future

information will not prove that members of

the control group issue FFS.

Auditors check all the companies included

in the sample. All public limited companies

(socieÂteÂs anonymes) and limited liability

companies are obliged to submit to an

auditor’s control when they fulfil two of the

three following criteria:

1 total revenues are over 1 billion Greek

Drachmas (GRD) ($2,717 million, £1,852

million);

2 total assets are over 500 million GRD

($1.359 million, £926,000); and

3 the average number of employees is over

50 (Ballas, 1994; Caramanis, 1997).

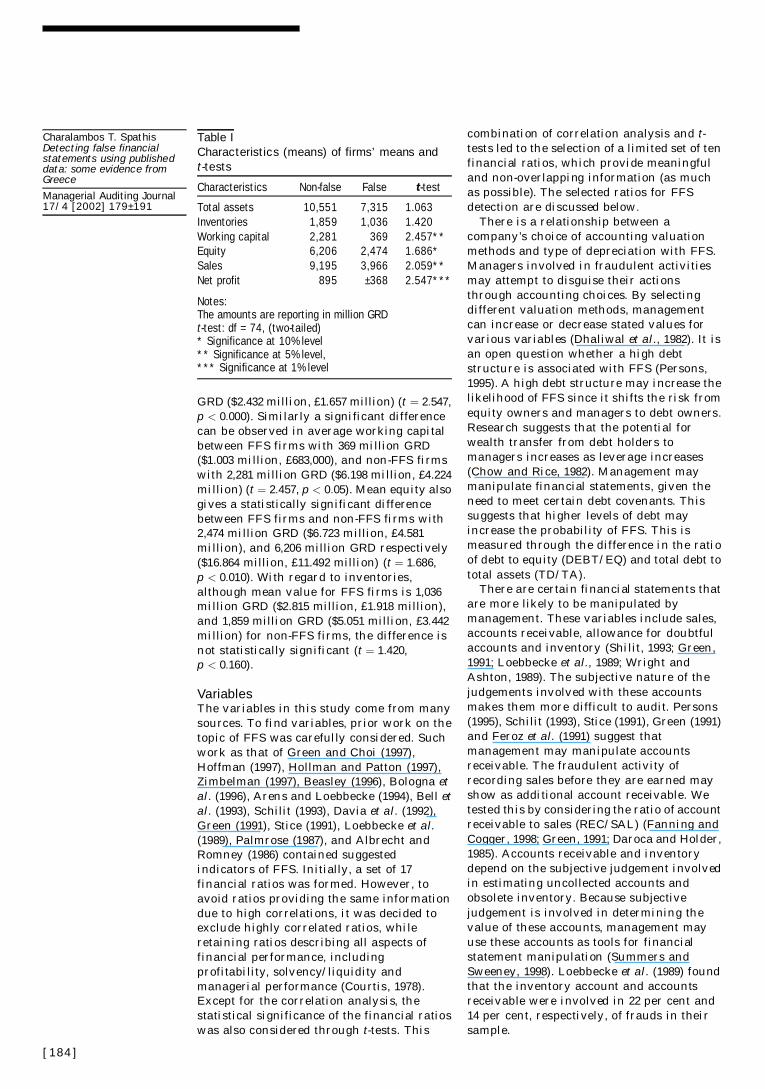

Some of the characteristics of the full sample

companies are presented in Table I.

There is a statistically significant

difference between average profits of FFS

firms, with losses averaging at 368 million

GRD ($1 million, £680,000), and non-FFS

companies averaging a profit of 895 million

[ 183 ]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

GRD ($2.432 million, £1.657 million) (t ˆ 2:547,

p < 0:000). Similarly a significant difference

can be observed in average working capital

between FFS firms with 369 million GRD

($1.003 million, £683,000), and non-FFS firms

with 2,281 million GRD ($6.198 million, £4.224

million) (t ˆ 2:457, p < 0:05). Mean equity also

gives a statistically significant difference

between FFS firms and non-FFS firms with

2,474 million GRD ($6.723 million, £4.581

million), and 6,206 million GRD respectively

($16.864 million, £11.492 million) (t ˆ 1:686,

p < 0:010). With regard to inventories,

although mean value for FFS firms is 1,036

million GRD ($2.815 million, £1.918 million),

and 1,859 million GRD ($5.051 million, £3.442

million) for non-FFS firms, the difference is

not statistically significant (t ˆ 1:420,

p < 0:160).

VariablesThe variables in this study come from many

sources. To find variables, prior work on the

topic of FFS was carefully considered. Such

work as that of Green and Choi (1997),

Hoffman (1997), Hollman and Patton (1997),

Zimbelman (1997), Beasley (1996), Bologna et

al. (1996), Arens and Loebbecke (1994), Bell et

al. (1993), Schilit (1993), Davia et al. (1992),

Green (1991), Stice (1991), Loebbecke et al.

(1989), Palmrose (1987), and Albrecht and

Romney (1986) contained suggested

indicators of FFS. Initially, a set of 17

financial ratios was formed. However, to

avoid ratios providing the same information

due to high correlations, it was decided to

exclude highly correlated ratios, while

retaining ratios describing all aspects of

financial performance, including

profitability, solvency/liquidity and

managerial performance (Courtis, 1978).

Except for the correlation analysis, the

statistical significance of the financial ratios

was also considered through t-tests. This

combination of correlation analysis and t-

tests led to the selection of a limited set of ten

financial ratios, which provide meaningful

and non-overlapping information (as much

as possible). The selected ratios for FFS

detection are discussed below.

There is a relationship between a

company’s choice of accounting valuation

methods and type of depreciation with FFS.

Managers involved in fraudulent activities

may attempt to disguise their actions

through accounting choices. By selecting

different valuation methods, management

can increase or decrease stated values for

various variables (Dhaliwal et al., 1982). It is

an open question whether a high debt

structure is associated with FFS (Persons,

1995). A high debt structure may increase the

likelihood of FFS since it shifts the risk from

equity owners and managers to debt owners.

Research suggests that the potential for

wealth transfer from debt holders to

managers increases as leverage increases

(Chow and Rice, 1982). Management may

manipulate financial statements, given the

need to meet certain debt covenants. This

suggests that higher levels of debt may

increase the probability of FFS. This is

measured through the difference in the ratio

of debt to equity (DEBT/EQ) and total debt to

total assets (TD/TA).

There are certain financial statements that

are more likely to be manipulated by

management. These variables include sales,

accounts receivable, allowance for doubtful

accounts and inventory (Shilit, 1993; Green,

1991; Loebbecke et al., 1989; Wright and

Ashton, 1989). The subjective nature of the

judgements involved with these accounts

makes them more difficult to audit. Persons

(1995), Schilit (1993), Stice (1991), Green (1991)

and Feroz et al. (1991) suggest that

management may manipulate accounts

receivable. The fraudulent activity of

recording sales before they are earned may

show as additional account receivable. We

tested this by considering the ratio of account

receivable to sales (REC/SAL) (Fanning and

Cogger, 1998; Green, 1991; Daroca and Holder,

1985). Accounts receivable and inventory

depend on the subjective judgement involved

in estimating uncollected accounts and

obsolete inventory. Because subjective

judgement is involved in determining the

value of these accounts, management may

use these accounts as tools for financial

statement manipulation (Summers and

Sweeney, 1998). Loebbecke et al. (1989) found

that the inventory account and accounts

receivable were involved in 22 per cent and

14 per cent, respectively, of frauds in their

sample.

Table ICharacteristics (means) of firms’ means andt-tests

Characteristics Non-false False t-test

Total assets 10,551 7,315 1.063Inventories 1,859 1,036 1.420Working capital 2,281 369 2.457**Equity 6,206 2,474 1.686*Sales 9,195 3,966 2.059**Net profit 895 ±368 2.547***

Notes:The amounts are reporting in million GRDt-test: df = 74, (two-tailed)* Significance at 10% level** Significance at 5% level,*** Significance at 1% level

[ 184]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

Many researchers such as Vanasco (1998),

Persons (1995), Schilit (1993) and Stice (1991)

also suggest that management may

manipulate inventories. The company may

not match sales with the corresponding cost

of goods sold, thus increasing gross margin,

net income and strengthening the balance

sheet. Another type of manipulation

involves reporting inventory at lower than

cost or market value. The company may

choose not to record the right amount of

obsolete inventory. Consequently, the ratio

of inventory to sales is considered (INV/

SAL). Another issue examined in this

research is whether higher or lower gross

margins are related to the issuing of FFS.

For this purpose, the ratio of gross profit to

total assets is used (GP/TA).

The profitability orientation is tempered

by the manager’s own utility maximization,

defined (partially) by job security.

Following this definition, the achievement

of stable or increasing earnings streams

maximizes the manager’s utility. This

approach is based on the expectation that

management will be able to maintain or

improve past levels of profitability,

regardless of what those levels were

(Summers and Sweeney, 1998). If this

expectation is not met by actual

performance, then it provides a

motivation for financial statement

falsification.

Loebbecke et al. (1989) found that profit

relative to industry was inadequate for 35 per

cent of companies with fraud in their sample.

In this research some other financial

statement red flag variables are examined,

such as the sales to total assets ratio (SAL/

TA), net profit to sales (NP/SAL), net profit to

total assets (NP/TA), working capital to total

assets (WC/TA), for their ability to predict

FFS. The sales to total assets ratio was a

significant predictor in prior research

(Persons, 1995).

Financial distress may be a motivation

for FFS (Bell et al., 1993; Stice, 1991;

Loebbecke et al., 1989; Kreutzfeldt and

Wallace, 1986). When the company is doing

poorly there is greater motivation to engage

in FFS. The results in Hamer (1983) suggest

that most models predict bankruptcy with

similar ability. Poor financial condition

(Bell et al., 1993; Loebbecke et al., 1989) may

motivate unethical insiders to take actions

intended to improve the appearance of the

company’s financial position, perhaps to

reduce the threat of loss of employment, or

to garner as many resources as possible

before termination. In addition to

motivating the commission of fraud, poor

financial condition may indicate a weak

control environment, a condition that

allows the perpetration of a fraud (AICPA,

1997). Loebbecke et al. (1989) found that 19

per cent of the fraud companies in their

sample were experiencing solvency

problems.

Therefore, we use the Altman (1968, 1983) Z-

score as a control variable to investigate the

association of FFS and financial distress. The

use of the Z-score is accompanied by some

limitations, as was its use 30 years ago to

develop a corporate failure prediction model

for the US manufacturing sector. It is

nevertheless still used today in many studies

(Summers and Sweeney, 1998). With regards

to Greek companies, despite the fact that a

number of researchers have looked at

bankruptcy, a generally accepted model has

not been established (Theodosiou, 1991;

Vranas, 1992; Negakis, 1995; Dimitras et al.,

1995). We measure this variable through the

difference in the Z-score in model (2) outlined

below as a control variable for differences in

financial condition between FFS and non-

FFS firms.

MethodThe statistical method selected was logistic

regression analysis (DeMaris, 1992;

Mendenhall and Sincish, 1993; Menard,

1995). The following logit model was

estimated using financial ratios from the

firms to see which of the ratios were related

to FFS. By including the data set of FFS and

non-FFS we may find out what factors

significantly influence the firms with FFS.

We therefore formulated the following

equation:

E…y† ˆ exp…bo ‡ b1x1 ‡ b2x2 ‡ . . . ‡ bkxk†1 ‡ exp…bo ‡ b1x1 ‡ b2x2 ‡ . . . ‡ bkxk†

Where

y ˆ 1 if FFS firm occurs

y ˆ 0 if non-FFS firm occurs

E…y† ˆ p (FFS firms occurs) ˆQ

Qˆ denotes the probability that

y ˆ 1

bo ˆ the intercept term

b1; b2; . . . ; bk ˆ the regression coefficients of

independent variables

x1; x2; . . . ; xk ˆ the independent variables

The models are presented as:

FFS ˆbo ‡ b1…DET=EQ† ‡ b2…SAL=TA†‡ b3…NP=SAL† ‡ b4…REC=SAL†‡ b5…NP=TA† ‡ b6…WC=TA†‡ b7…GP=TA† ‡ b8…INV=SAL†‡ b9…TD=TA† ‡ e

…1†

Where FFS ˆ 1 if FFS discovered group, 0

otherwise.

[ 185 ]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

FFS ˆbo ‡ b1…DEBT=EQ† ‡ b2…SAL=TA†‡ b3…NP=SAL† ‡ b4…REC=SAL†‡ b5…NP=TA† ‡ b6…WC=TA†‡ b7…GP=TA† ‡ b8…INV=SAL†‡ b9…TD=TA† ‡ b10…Z† ‡ e

…2†

For model (2) the variable Z was added into

the above model (1).

The Z-score (Altman, 1968, 1983) was used

to investigate the association of FFS and

financial distress:

Z ˆ1:2 …working capital=total assets†‡ 1:4 …retained earnings=total assets†‡ 3:3 …earnings before interest and taxes=

total assets†‡ 0:06 …market value of equity=

book value of total debt†‡ 1:0 …sales=total assets†:

The models will classify firms into FFS and

non-FFS categories based upon financial

statement ratios that have been documented

as diagnostic in prior studies.

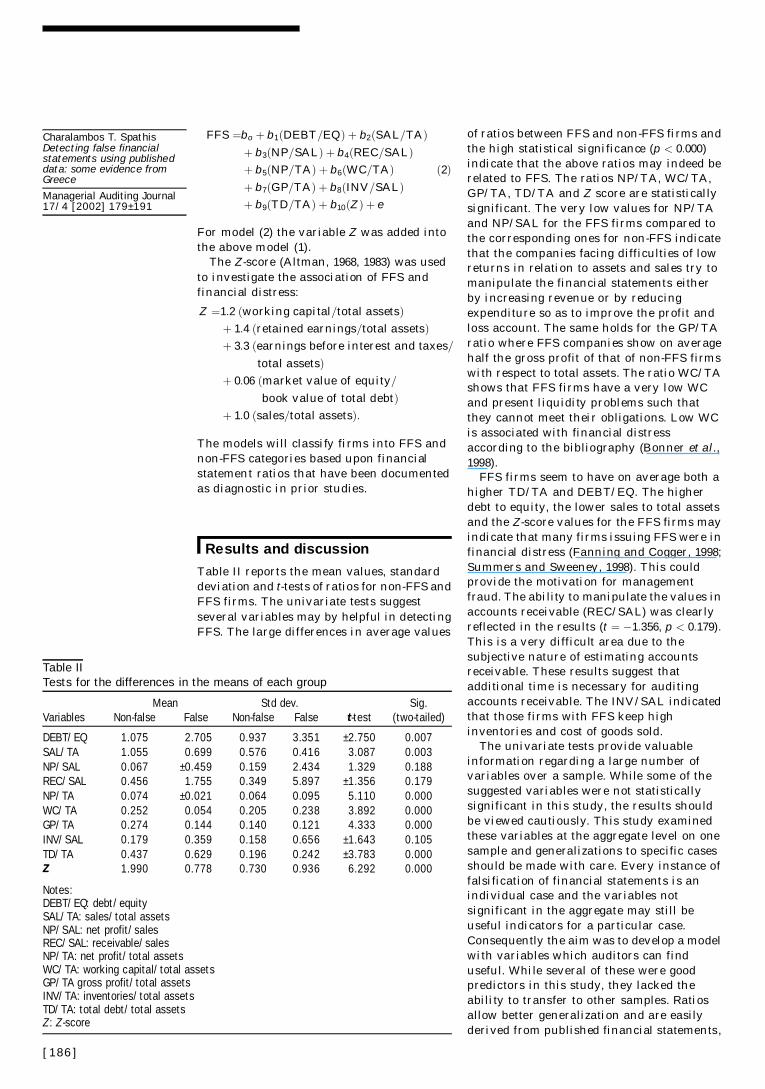

Results and discussion

Table II reports the mean values, standard

deviation and t-tests of ratios for non-FFS and

FFS firms. The univariate tests suggest

several variables may by helpful in detecting

FFS. The large differences in average values

of ratios between FFS and non-FFS firms and

the high statistical significance (p < 0:000)

indicate that the above ratios may indeed be

related to FFS. The ratios NP/TA, WC/TA,

GP/TA, TD/TA and Z score are statistically

significant. The very low values for NP/TA

and NP/SAL for the FFS firms compared to

the corresponding ones for non-FFS indicate

that the companies facing difficulties of low

returns in relation to assets and sales try to

manipulate the financial statements either

by increasing revenue or by reducing

expenditure so as to improve the profit and

loss account. The same holds for the GP/TA

ratio where FFS companies show on average

half the gross profit of that of non-FFS firms

with respect to total assets. The ratio WC/TA

shows that FFS firms have a very low WC

and present liquidity problems such that

they cannot meet their obligations. Low WC

is associated with financial distress

according to the bibliography (Bonner et al.,

1998).

FFS firms seem to have on average both a

higher TD/TA and DEBT/EQ. The higher

debt to equity, the lower sales to total assets

and the Z-score values for the FFS firms may

indicate that many firms issuing FFS were in

financial distress (Fanning and Cogger, 1998;

Summers and Sweeney, 1998). This could

provide the motivation for management

fraud. The ability to manipulate the values in

accounts receivable (REC/SAL) was clearly

reflected in the results (t ˆ ¡1:356, p < 0:179).

This is a very difficult area due to the

subjective nature of estimating accounts

receivable. These results suggest that

additional time is necessary for auditing

accounts receivable. The INV/SAL indicated

that those firms with FFS keep high

inventories and cost of goods sold.

The univariate tests provide valuable

information regarding a large number of

variables over a sample. While some of the

suggested variables were not statistically

significant in this study, the results should

be viewed cautiously. This study examined

these variables at the aggregate level on one

sample and generalizations to specific cases

should be made with care. Every instance of

falsification of financial statements is an

individual case and the variables not

significant in the aggregate may still be

useful indicators for a particular case.

Consequently the aim was to develop a model

with variables which auditors can find

useful. While several of these were good

predictors in this study, they lacked the

ability to transfer to other samples. Ratios

allow better generalization and are easily

derived from published financial statements,

Table IITests for the differences in the means of each group

Mean Std dev. Sig.(two-tailed)Variables Non-false False Non-false False t-test

DEBT/EQ 1.075 2.705 0.937 3.351 ±2.750 0.007SAL/TA 1.055 0.699 0.576 0.416 3.087 0.003NP/SAL 0.067 ±0.459 0.159 2.434 1.329 0.188REC/SAL 0.456 1.755 0.349 5.897 ±1.356 0.179NP/TA 0.074 ±0.021 0.064 0.095 5.110 0.000WC/TA 0.252 0.054 0.205 0.238 3.892 0.000GP/TA 0.274 0.144 0.140 0.121 4.333 0.000INV/SAL 0.179 0.359 0.158 0.656 ±1.643 0.105TD/TA 0.437 0.629 0.196 0.242 ±3.783 0.000Z 1.990 0.778 0.730 0.936 6.292 0.000

Notes:DEBT/EQ: debt/equitySAL/TA: sales/total assetsNP/SAL: net profit/salesREC/SAL: receivable/salesNP/TA: net profit/total assetsWC/TA: working capital/total assetsGP/TA gross profit/total assetsINV/TA: inventories/total assetsTD/TA: total debt/total assetsZ: Z-score

[ 186]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

and they have been used in the model

development.

There were ten possible variables in this

study with the results of the univariate tests.

The next step in securing a model was the

application of multivariate testing with

stepwise logistic regression. The univariate

results were informative but there was the

question of whether the association was a

direct association or whether there was a

joint correlation with a third variable. A

univariate test does not allow detection of

interaction effects which multivariate tests

may find. This study used model (1) with nine

variables (without Z scores) and model (2)

with ten variables, Z score included.

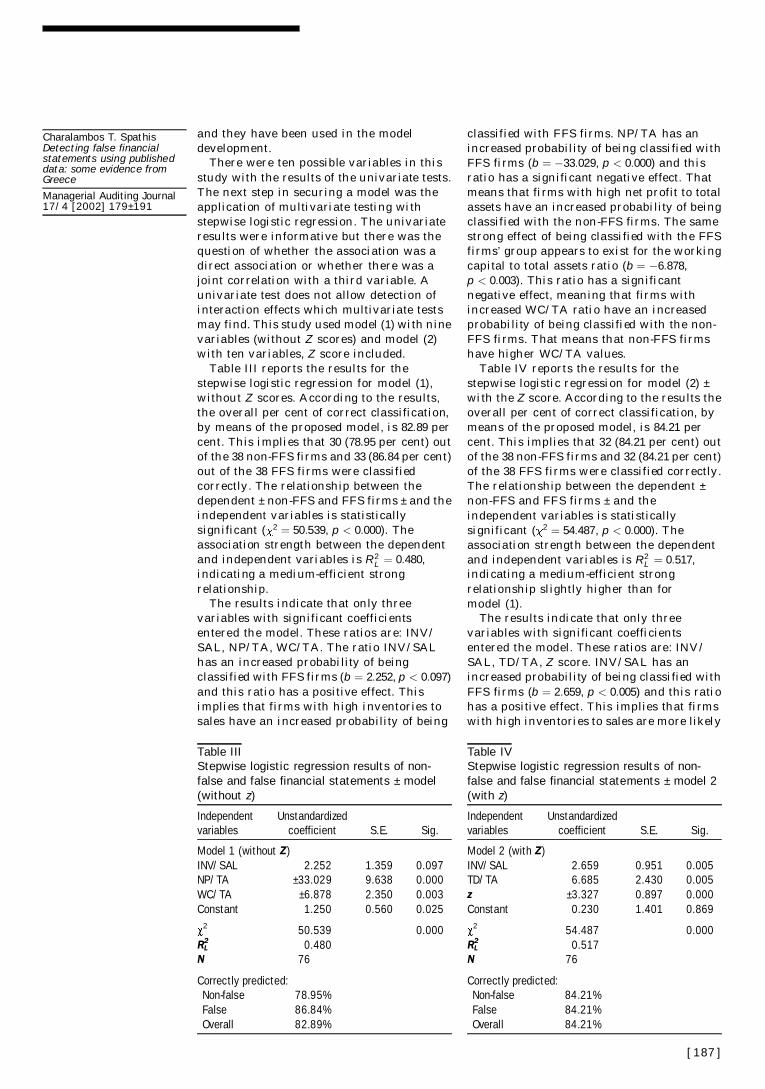

Table III reports the results for the

stepwise logistic regression for model (1),

without Z scores. According to the results,

the overall per cent of correct classification,

by means of the proposed model, is 82.89 per

cent. This implies that 30 (78.95 per cent) out

of the 38 non-FFS firms and 33 (86.84 per cent)

out of the 38 FFS firms were classified

correctly. The relationship between the

dependent ± non-FFS and FFS firms ± and the

independent variables is statistically

significant ( 2 ˆ 50:539, p < 0:000). The

association strength between the dependent

and independent variables is R2L ˆ 0:480,

indicating a medium-efficient strong

relationship.

The results indicate that only three

variables with significant coefficients

entered the model. These ratios are: INV/

SAL, NP/TA, WC/TA. The ratio INV/SAL

has an increased probability of being

classified with FFS firms (b ˆ 2:252, p < 0:097)

and this ratio has a positive effect. This

implies that firms with high inventories to

sales have an increased probability of being

classified with FFS firms. NP/TA has an

increased probability of being classified with

FFS firms (b ˆ ¡33:029, p < 0:000) and this

ratio has a significant negative effect. That

means that firms with high net profit to total

assets have an increased probability of being

classified with the non-FFS firms. The same

strong effect of being classified with the FFS

firms’ group appears to exist for the working

capital to total assets ratio (b ˆ ¡6:878,

p < 0:003). This ratio has a significant

negative effect, meaning that firms with

increased WC/TA ratio have an increased

probability of being classified with the non-

FFS firms. That means that non-FFS firms

have higher WC/TA values.

Table IV reports the results for the

stepwise logistic regression for model (2) ±

with the Z score. According to the results the

overall per cent of correct classification, by

means of the proposed model, is 84.21 per

cent. This implies that 32 (84.21 per cent) out

of the 38 non-FFS firms and 32 (84.21 per cent)

of the 38 FFS firms were classified correctly.

The relationship between the dependent ±

non-FFS and FFS firms ± and the

independent variables is statistically

significant ( 2 ˆ 54:487, p < 0:000). The

association strength between the dependent

and independent variables is R2L ˆ 0:517,

indicating a medium-efficient strong

relationship slightly higher than for

model (1).

The results indicate that only three

variables with significant coefficients

entered the model. These ratios are: INV/

SAL, TD/TA, Z score. INV/SAL has an

increased probability of being classified with

FFS firms (b ˆ 2:659, p < 0:005) and this ratio

has a positive effect. This implies that firms

with high inventories to sales are more likely

Table IIIStepwise logistic regression results of non-false and false financial statements ± model(without z)

Independentvariables

Unstandardizedcoefficient S.E. Sig.

Model 1 (without Z)INV/SAL 2.252 1.359 0.097NP/TA ±33.029 9.638 0.000WC/TA ±6.878 2.350 0.003Constant 1.250 0.560 0.025

2 50.539 0.000RL

2 0.480N 76

Correctly predicted:Non-false 78.95%False 86.84%Overall 82.89%

Table IVStepwise logistic regression results of non-false and false financial statements ± model 2(with z)

Independentvariables

Unstandardizedcoefficient S.E. Sig.

Model 2 (with Z)INV/SAL 2.659 0.951 0.005TD/TA 6.685 2.430 0.005z ±3.327 0.897 0.000Constant 0.230 1.401 0.869

2 54.487 0.000RL

2 0.517N 76

Correctly predicted:Non-false 84.21%False 84.21%Overall 84.21%

[ 187 ]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

to be classified as FFS. The ratio TD/TA has

an increased probability of being classified

with FFS firms (b ˆ 6:685, p < 0:005) and this

ratio has a significant positive effect. That

means that firms with high total debt to total

assets values have an increased probability

of being classified with the FFS group. The

same strong effect of being classified with

FFS firms appears to be attributed to the Z

score (b ˆ ¡3:327, p < 0:000). This ratio has a

significant negative effect, meaning that

firms with increased Z score values have

increased probability of being classified with

the non-FFS firms. That means that non-FFS

firms have higher Z scores.

In both models, the ratio indicated as an

important variable is INV/SAL,

demonstrating that FFS firms keep higher

stocks, indicating a lower stock turnover

with respect to sales. The coefficients of

WC/TA, NP/TA, and Z score have negative

signs. This is consistent with the hypothesis

that an improvement in the liquidity

position of a firm, an improvement in the

profitability of the firm, or an improvement

in the Z score of the firm will have a negative

effect on the probability of FFS.

` ... The analysis shows that higher TD/TA may indicate that manyfirms issuing FFS were in financial distress . . . This could providethe motivation for management fraud ... ’

The coefficient of the debt ratio TD/TA and

INV/SAL ratio has a positive sign, which

conforms to the hypothesis that more

leverage and large inventories make the firm

more vulnerable to FFS. The analysis shows

that higher TD/TA may indicate that many

firms issuing FFS were in financial distress

(Persons, 1995; Fanning and Cogger, 1998;

Summers and Sweeney, 1998). This could

provide the motivation for management

fraud. On the other hand, the identification of

INV/SAL as a crucial factor agrees with the

results of previous studies in this field. The

inventory is likely to be manipulated by

management (Loebbecke et al., 1989; Schilit,

1993; Summers and Sweeney, 1998). SAS

No. 47, Audit Risk and Materiality in

Conducting and Audit (AICPA, 1983) states

that any account that requires subjective

judgement in determining its value increases

audit risk. Inventory is noted as such an

account due to the subjective judgement

involved in estimating obsolete inventory. A

further examination indicates that firms

with FFS were less profitable (lower NP/TA)

since they get less profit for the same total

assets. This result agrees with the existing

research (Loebbecke et al., 1989; Summers

and Sweeney, 1998; Beasley et al., 1999).

Concluding remarks

The primary objective of this study has been

the development of a reliable false financial

statement detection model for Greek firms. In

order to achieve this goal we used a sample of

FFS and non-FFS firms. We used univariate

and multivariate statistical techniques such

as logistic regression to develop a model to

identify factors associated with FFS. A total

of ten financial ratios are selected for

examination as potential predictors of FFS.

These variables appeared to be important in

prior research and constitute ratios derived

from published financial statements. The

variables selected by the above techniques as

possible indicators of FFS are: the

inventories to sales ratio, the ratio of total

debt to total assets, the working capital to

total assets ratio, the net profit to total assets

ratio, and financial distress (Z-score). Both

models are accurate in classifying the total

sample correctly with accuracy rates

exceeding 84 per cent. The results of these

models suggest there is potential in detecting

FFS through analysis of publicly available

financial statements. In general the

indicators selected are associated with FFS

firms. Companies with high inventories with

respect to sales, high debt to total assets, low

net profit to total assets, low working capital

to total assets and low Z scores are more

likely to falsify financial statements

according to the results of the stepwise

logistic regression.

Alternative methods for FFS detection can

be used, such as discriminant analysis,

adaptive logit networks, neural networks and

multicriteria analysis. There were several

publicly available variables that remain for

future study. These variables include

standing within industries and long-term

trends. Industry standing probably would

provide additional valuable information in

the growth and financial distress variables. A

further possibility would be to examine

variables other than those in financial

statements, such as the number of members

of the board of directors, the rate of turnover

of the financial manager, the type of auditor

used and the frequency with which they are

changed, auditors’ opinions, the size of the

company, the existence of company

branches, inventory evaluation methods,

depreciation methods. This study did not use

a holdout sample to validate the model that is

presented. Further research with larger

[ 188]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

samples will be necessary to validate these

results.

The results are encouraging in that we

have developed a reliable model for assessing

the likelihood of false financial statements of

businesses in Greece. The use of the proposed

methodological framework could be of

assistance to auditors, both internal and

external, to taxation and other state

authorities, individual and institutional

investors, stock exchanges, law firms,

economic analysts, credit scoring agencies

and to the banking system. For the auditing

profession, moving to address its

responsibility to detect FFS, the results of

this study should be beneficial. The auditors

can provide this model as effective expert

witness testimony and computer litigation

support regarding FFS at a low cost to

auditor and client. The auditors with suitable

software will be able to apply it to scan

financial statements posted on Internet Web

sites and analyse the differences between

trends of the company’s reports. It also

identifies `̀ red flags’’ that substantially differ

from the norms of the industry. Therefore,

the present study contributes to auditing and

accounting research by examining the

suggested variables to identify those that can

best discriminate cases of FFS. This study

suggests certain variables from publicly

available information to which auditors

should be allocating additional audit time.

With more improved statistical techniques

and a greater number of variables it is

possible to develop a more powerful

analytical tool for the detection of FFS.

ReferencesAbbot, J.L., Park, Y. and Parker, S. (2000), `̀ The

effects of audit committee activity and

independence on corporate fraud’’,

Managerial Finance, Vol. 26 No. 11, pp. 55-67.

Abdolmohammadi, J.M. and Owhoso, D.V. (2000),

`̀ Auditors’ ethical sensitivity and the

assessment of the likelihood of fraud’’,

Managerial Finance, Vol. 26 No. 11, pp. 21-32.

Albrecht, S. and Romney, M. (1986), `̀ Red-flagging

management: a validation’’, Advances in

Accounting, Vol. 3, pp. 323-33.

Altman, E. (1968), `̀ Financial ratios, discriminant

analysis, and the prediction of corporate

bankruptcy’’, Journal of Finance, September,

pp. 589-609.

Altman, E. (1983), Corporate Financial Distress: A

Complete Guide to Predicting, Avoiding, and

Dealing with Bankruptcy, John Wiley,

New York, NY.

AICPA (1983), Auditing Risk and Materiality in

Conducting an Audit, Statement on Auditing

Standards No. 47, American Institute of

Certified Public Accountants, New York, NY.

AICPA (1997), Consideration of Fraud in a

Financial Statement Audit, Statement on

Auditing Standards No. 82, American

Institute of Certified Public Accountants,

New York, NY.

Arens, A. and Loebbecke, J. (1994), Auditing: An

Integrated Approach, 6th ed., Prentice-Hall,

Englewood Cliffs, NJ.

Ballas, A. (1994), `̀ Accounting in Greece’’, The

European Accounting Review, Vol. 3 No. 1,

pp. 107-21.

Beasley, M. (1996), `̀ An empirical analysis of the

relation between board of director

composition and financial statement fraud’’,

The Accounting Review, Vol. 71 No. 4,

pp. 443-66.

Beasley, S.M., Carcello, J.V. and Hermanson, D.R.

(1999), Fraudulent Financial Reporting: 1987-

1997: An Analysis of US Public Companies,

Research Report, COSO.

Bell, T., Szykowny, S. and Willingham, J. (1993),

`̀ Assessing the likelihood of fraudulent

financial reporting: a cascaded logic

approach’’, Working Paper, KPMG Peat

Marwick, Montvale, NJ.

Beneish, M.D. (1999), `̀ Incentives and penalties

related to earnings overstatements that

violate GAAP’’, The Accounting Review,

Vol. 74 No. 4, pp. 425-57.

Bloomfield, R.I. (1997), `̀ Strategic dependence and

the assessment of fraud risk: a laboratory

study’’, The Accounting Review, Vol. 72 No. 4,

pp. 517-38.

Boatsman, J.R., Moeckel, C. and Pei, B.K.W.

(1997), `̀ The effects of decision consequences

on auditors’ reliance on decision aids in audit

planning’’, Organizational Behavior and

Human Decision Processes, Vol. 71 No. 2,

pp. 211-47.

Bologna, G., Lindquist, R. and Wells, J. (1996), The

Accountant’s Handbook of Fraud and

Commercial Crime, John Wiley,

New York, NY.

Bonner, S.E., Palmrose, Z.V. and Young, S.M.

(1998), `̀ Fraud type and auditor litigation. An

analysis of SEC accounting and auditing

enforcement releases’’, The Accounting

Review, Vol. 73 No. 4, pp. 503-32.

Caplan, D. (1999), `̀ Internal controls and the

detection of management fraud’’, Journal of

Accounting Research, Vol. 37 No. 1, pp. 101-17.

Caramanis, V.C. (1997), `̀ The enigma of the Greek

auditing profession: some preliminary results

concerning the impact of liberalization on

auditor behavior’’, The European Accounting

Review, Vol. 6 No. 1, pp. 85-108.

Chow, C. and Rice, S. (1982), `̀ Qualified audit

opinions and share prices: an investigation’’,

Auditing: A Journal of Practice and Theory,

Vol. 1, pp. 35-53.

Coderre, G.D. (1999), Fraud Detection. Using Data

Analysis Techniques to Detect Fraud, Global

Audit Publications, Vancover.

[ 189 ]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

Colbert, L.J. (2000), `̀ International and US

standards: error and fraud’’, Managerial

Auditing Journal, Vol. 15 No. 3, pp. 97-107.

Comer, J.M. (1998), Corporate Fraud, 3rd ed.,

Gower Publishing, Aldershot.

Courtis, J.K. (1978), `̀ Modelling a financial ratios

categoric framework’’, Journal of Business

Finance and Accounting, Vol. 5 No. 4,

pp. 371-86.

Daroca, F. and Holder, W. (1985), `̀ The use of

analytical procedures in renew and audit

engagements’’, Auditing: A Journal of Practice

and Theory, Vol. 4, pp. 80-92.

Davia, H., Coggins, P., Wideman, J. and

Kastantin, J. (1992), Management

Accountant’s Guide to Fraud Discovery and

Control, John Wiley, New York, NY.

DeMaris, A. (1992), Logit Modeling, Sage

University Paper Series on Quantitative

Applications in the Social Sciences, CA.

Dhaliwal, D., Salamon, G. and Smith, E. (1982),

`̀ The effect of owner versus management

control on the choice of accounting methods’’,

Journal of Accounting and Economics, Vol. 4,

pp. 41-53.

Dimitras, A.I., Zopounidis, C. and Hurson, Ch.

(1995), `̀ A multicriteria decision aid method

for the assessment of business failure risk’’,

Foundations of Computing and Decision

Sciences, Vol. 20 No. 2, pp. 99-112.

Eilifsen, A., Knivsfla, K.H. and Soettem, F. (1999),

`̀ Earnings manipulation: cost of capital

versus tax’’, The European Accounting

Review, Vol. 8 No. 3, pp. 481-91.

Eining, M.M., Jones, D.R. and Loebbecke, J.K.

(1997), `̀ Reliance on decision aids: an

examination of auditors’ assessment of

management fraud’’, Auditing: A Journal of

Practice and Theory, Vol. 16 No. 2, pp. 1-19.

Elliot, R. and Willingham, J. (1980), Management

Fraud: Detection and Deterrence, Petrocelli,

New York, NY.

Fanning, M.K. and Cogger, K.O. (1998), `̀ Neural

detection of management fraud using

published financial data’’, International

Journal of Intelligent Systems in Accounting,

Finance and Management, Vol. 7 No. 1,

pp. 21-41.

Fanning, K., Cogger, K. and Srivastava, R. (1995),

`̀ Detection of management fraud: a neural

network approach’’, International Journal of

Intelligent Systems in Accounting, Finance

and Management, Vol. 4 No. 2, pp. 113-26.

Feroz, E., Park, K. and Pastens, V. (1991), `̀ The

financial and market effects of the SEC’s

accounting and auditing enforcement’s

releases’’, Journal of Accounting Research,

Vol. 29, pp. 107-42.

Green, B. (1991), `̀ Identifying management

irregularities through preliminary analytical

procedures’’, unpublished doctoral

dissertation, Kent State University, Kent, OH.

Green, B.P. and Choi, J.H. (1997), `̀ Assessing the

risk of management fraud through neural-

network technology’’, Auditing: A Journal of

Practice and Theory, Vol. 16 No. 1, pp. 14-28.

Hamer, M. (1983), `̀ Failure prediction: sensitivity

of classification accuracy to alternative

statistical methods and variable sets’’,

Journal of Accounting and Public Policy,

Vol. 2 No. 4, pp. 289-307.

Hansen, J.V., McDonald, J.B., Messier, W.F. and

Bell, T.B. (1996), `̀ A generalized qualitative-

response model and the analysis of

management fraud’’, Management Science,

Vol. 42 No. 7, pp. 1022-32.

Hellman, N. (1999), ``Earnings manipulation: cost

of capital versus tax. A commentary’’, The

European Accounting Review, Vol. 8 No. 3,

pp. 493-7.

Higson, A. (1999), `̀ Why is management reticent to

report fraud? An exploratory study’’, 22nd

Annual Congress of European Accounting

Association, Bordeaux.

Hoffman, V.B. (1997), `̀ Discussion of the effects of

SAS No. 82 on auditors attention to fraud risk-

factors and audit planning decisions’’,

Journal of Accounting Research, Vol. 35 No. 5,

pp. 99-104.

Hollman, V.P. and Patton, J.M. (1997),

`̀ Accountability, the dilution effect and

conservatism in auditors fraud judgments’’,

Journal of Accounting Research, Vol. 35 No. 2,

pp. 227-37.

International Federation of Accountants (1982),

Fraud and Error, International Statements on

Auditing (ISA) No. 11.

Kreutzfeldt, R. and Wallace, W. (1986), `̀ Error

characteristics in audit populations: their

profile and relationship to environment

factors’’, Auditing: A Journal of Practice and

Theory, Vol. 6, pp. 20-43.

Loebbecke, J., Eining, M. and Willingham, J.

(1989), `̀ Auditor’s experience with material

irregularities: frequency, nature, and

detectability’’, Auditing: A Journal of Practice

and Theory, Vol. 9, pp. 1-28.

Mancino, J. (1997), `̀ The auditor and fraud’’,

Journal of Accountancy, April, pp. 32-6.

Matsumura, E. and Tucker, R.R. (1992), `̀ Fraud

detection ± a theoretical foundation’’, The

Accounting Review, Vol. 67 No. 4, pp. 753-82.

Menard, S. (1995), Applied Logistic Regression

Analysis, Sage University Papers, Series on

Quantitative Applications in the Social

Sciences, Thousand Oaks, CA.

Mendenhall, W. and Sincish, T. (1993), A Second

Course in Business Statistics: Regression

Analysis, 4th ed., Macmillan, New York, NY.

Morton, S. (1993), `̀ Strategic auditing for fraud’’,

The Accounting Review, Vol. 68 No. 4,

pp. 825-39.

Negakis, C. (1995), `̀ Robustness of Greece

business failure prediction models’’,

International Review of Economics and

Business, Vol. 42 No. 3, pp. 203-15.

Palmrose, Z. (1987), `̀ Litigation and independent

auditors: the role of business failures and

[ 190]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

management fraud’’, Auditing: A Journal of

Practice and Theory, Vol. 6 No. 2, pp. 90-102.

Persons, O. (1995), `̀ Using financial statement

data to identify factors associated with

fraudulent financing reporting’’, Journal of

Applied Business Research, Vol. 11 No. 3,

pp. 38-46.

Porter, B. and Cameron, A. (1987), `̀ Company

fraud ± what price the auditor?’’, Accountant’s

Journal, December, pp. 44-7.

Schilit, H. (1993), Financial Shenanigans: How to

Detect Accounting Gimmicks and Fraud in

Financial Reports, McGraw-Hill,

New York, NY.

Stice, J. (1991), `̀ Using financial and market

information to identify pre-engagement

market factors associated with lawsuits

against auditors’’, The Accounting Review,

Vol. 66 No. 3, pp. 516-33.

Summers, S.L. and Sweeney, J.T. (1998),

`̀ Fraudulently misstated financial statements

and insider trading: an empirical analysis’’,

The Accounting Review, Vol. 73 No. 1,

pp. 131-46.

Theodosiou, P. (1991), `̀ Alternative models for

assessing the financial condition of business

in Greece’’, Journal of Business Finance and

Accounting, Vol. 18 No. 5, pp. 697-720.

Vanasco, R. R. (1998), `̀ Fraud auditing’’,

Managerial Auditing Journal, Vol. 13 No. 1,

pp. 4-71.

Vranas, A.S. (1992), `̀ The significance of financial

characteristics in predicting business failure:

an analysis in the Greek context’’,

Foundations of Computing and Decision

Sciences, Vol. 17 No. 4, pp. 257-75.

Wallace, W.A. (1995), Auditing, South-Western

College Publishing, Cincinnati, OH.

Wells, J.T. (1997), Occupational Fraud and Abuse,

Obsidian Publishing, Austin, TX.

Worthy, F.S. (1984), `̀ Manipulating profits: how

it’s done?’’, Fortune, Vol. 25, pp. 50-4.

Wright, A. and Ashton, R. (1989), `̀ Identifying

audit adjustments with attention-direction

procedures’’, The Accounting Review, Vol. 64

No. 4, pp. 79-83.

Zimbelman, M.F. (1997), `̀ The effects of SAS No. 82

on auditors attention to fraud risk-factors and

audit planning decisions’’, Journal of

Accounting Research, Vol. 35 No. 5, pp. 75-9.

Early versions of this paperwere presented at the 23rdCongress of the EuropeanAccounting Association heldin Munich, Germany 29-31March, 2000) and at the9th Annual Meeting of theEuropean FinancialManagement Associationheld in Athens, Greece28 June1 July, 2000). The

author wishes to thank theparticipants for constructivecomments and criticismsthat resulted in significantimprovements in thepresent version.

[ 191 ]

Charalambos T. SpathisDetecting false financialstatements using publisheddata: some evidence fromGreece

Managerial Auditing Journal17/4 [2002] 179±191

Related Documents

![v P ] v X } u [Digital Electronics for IBPS IT-Officer 2014] Input Output A B C False False False False True False True False False True True True Symbol for And gate: Also C= A.B](https://static.cupdf.com/doc/110x72/5aad019c7f8b9aa9488db79d/v-p-v-x-u-digital-electronics-for-ibps-it-officer-2014-input-output-a-b-c.jpg)

![Detecting Carbon Monoxide Poisoning Detecting Carbon ...2].pdf · Detecting Carbon Monoxide Poisoning Detecting Carbon Monoxide Poisoning. Detecting Carbon Monoxide Poisoning C arbon](https://static.cupdf.com/doc/110x72/5f551747b859172cd56bb119/detecting-carbon-monoxide-poisoning-detecting-carbon-2pdf-detecting-carbon.jpg)