Depreciation Chapter 22 Accounting II

Depreciation Chapter 22 Accounting II. Current v. Long-term Assets Current Assets – Cash and other assets reasonably expected to be converted to cash.

Dec 30, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Depreciation

Chapter 22

Accounting II

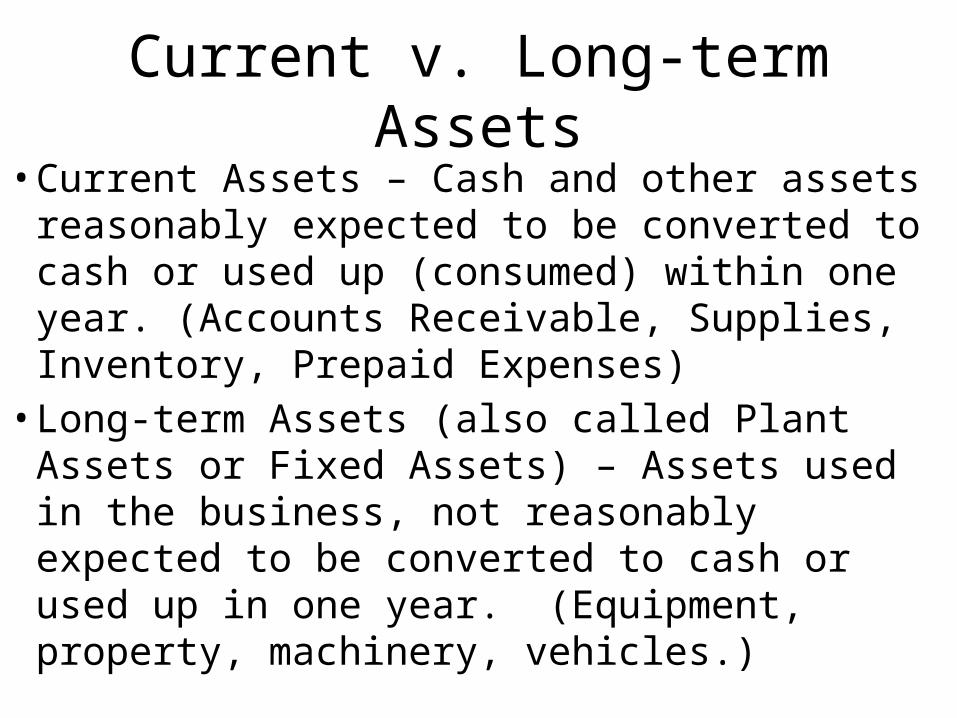

Current v. Long-term Assets• Current Assets – Cash and other assets

reasonably expected to be converted to cash or used up (consumed) within one year. (Accounts Receivable, Supplies, Inventory, Prepaid Expenses)• Long-term Assets (also called Plant Assets or

Fixed Assets) – Assets used in the business, not reasonably expected to be converted to cash or used up in one year. (Equipment, property, machinery, vehicles.)

Assets don’t last forever.

• The cost of a long-term asset must be expensed (proportionally) over the time period the asset is used.

• There are 3 methods used to pro-rate the cost of an asset over the asset’s “life.”

• The 3 methods are: depreciation, amortization, and depletion

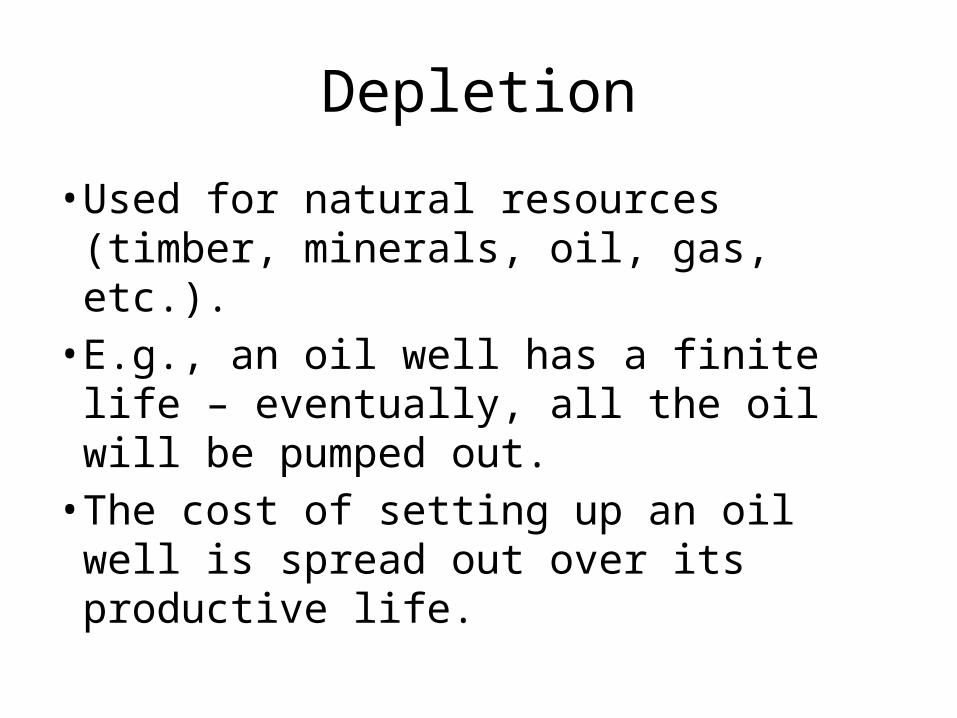

Depletion

• Used for natural resources (timber, minerals, oil, gas, etc.). • E.g., an oil well has a finite life –

eventually, all the oil will be pumped out.• The cost of setting up an oil well is

spread out over its productive life.

Amortization

• Used for intangible assets – assets that can’t be physically held (e.g., patents, copyrights, customer lists, software, etc.)

• The cost of an intangible asset is spread out over the asset’s useful life. (e.g., most patents are good for about 20 years; copyrights, for 70 years after the death of the author)

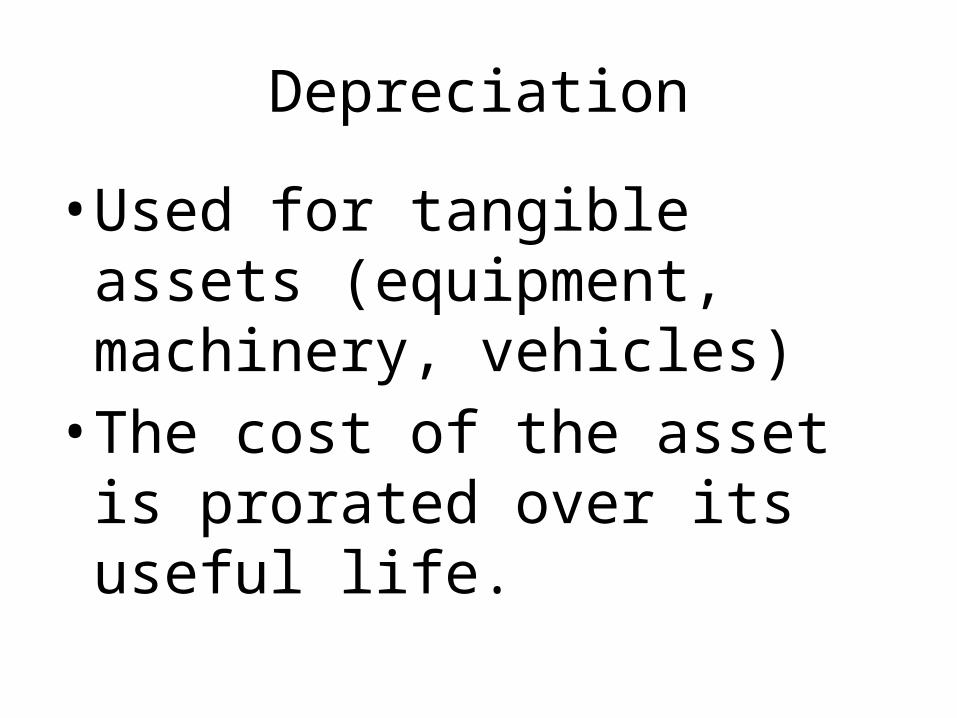

Depreciation

• Used for tangible assets (equipment, machinery, vehicles)• The cost of the asset is prorated

over its useful life.

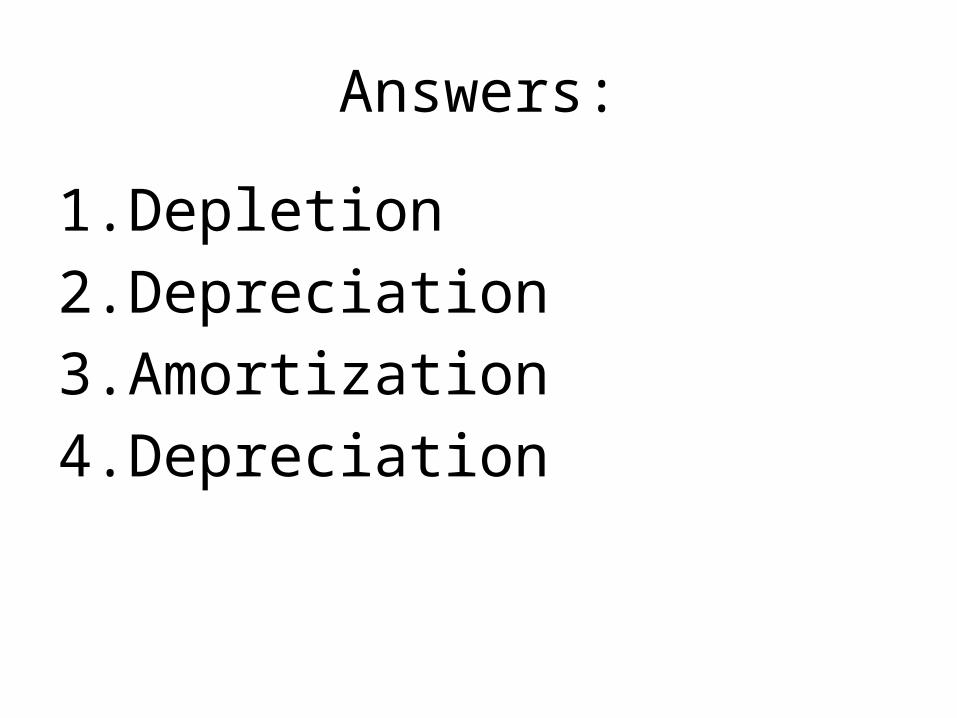

Quick QuizFor each of the following, name the method that would be used to apportion the asset’s cost over its useful life:1. A gold mine2. A building3. A customer list4. A truck used for deliveries

Answers:

1. Depletion2. Depreciation3. Amortization4. Depreciation

Buying Long-term assets

• When a business buys a long-term asset, it is recorded similarly to current assets• Debit the asset (increase) and

credit cash or accounts payable.

Using Long-term assets• A business buys long-term assets to earn

revenue• As the assets are used, and as time passes, they

decrease in value (e.g., newer models become available.

• For example – cars decrease in value as soon as they are driven off the lot:

http://www.edmunds.com/car-buying/how-fast-does-my-new-car-lose-value-infographic.html

Long-term assets

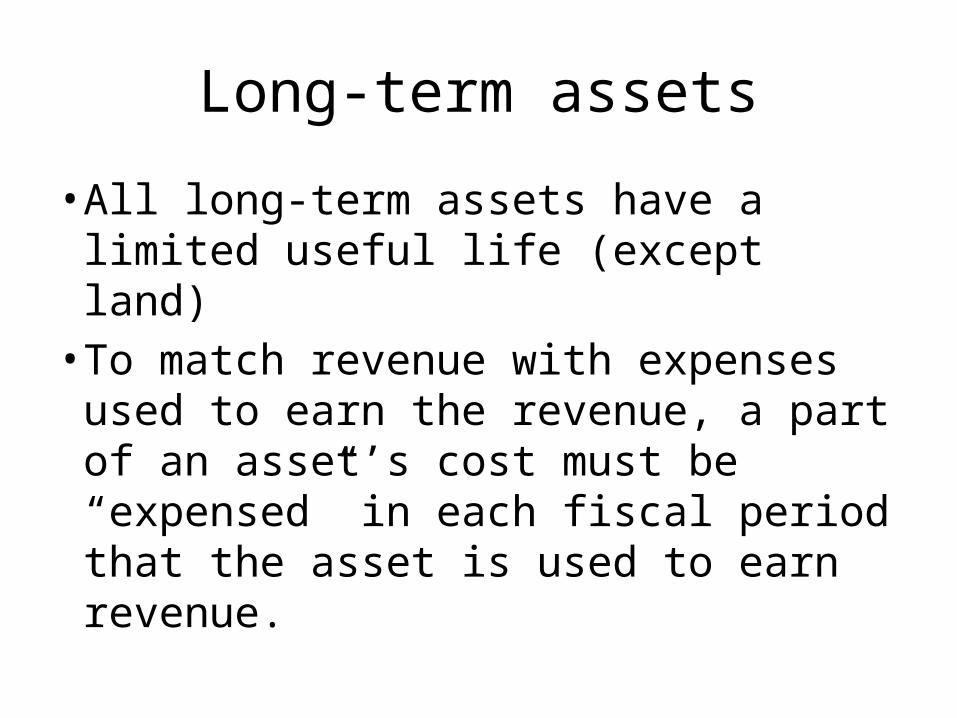

• All long-term assets have a limited useful life (except land)• To match revenue with expenses

used to earn the revenue, a part of an asset’s cost must be “expensed” in each fiscal period that the asset is used to earn revenue.

Expensing Long-term assets

• Businesses use an account called “Depreciation Expense” • Depreciation Expense – the part of

a long-term asset’s cost that is transferred to an expense account each fiscal period over the asset’s useful life.

Depreciation

• Depreciation expense does not represent the actual decline in value of an asset.• It tries to allocate the asset’s cost

over several fiscal periods• Never depreciate below salvage

value

Calculating Depreciation Expense

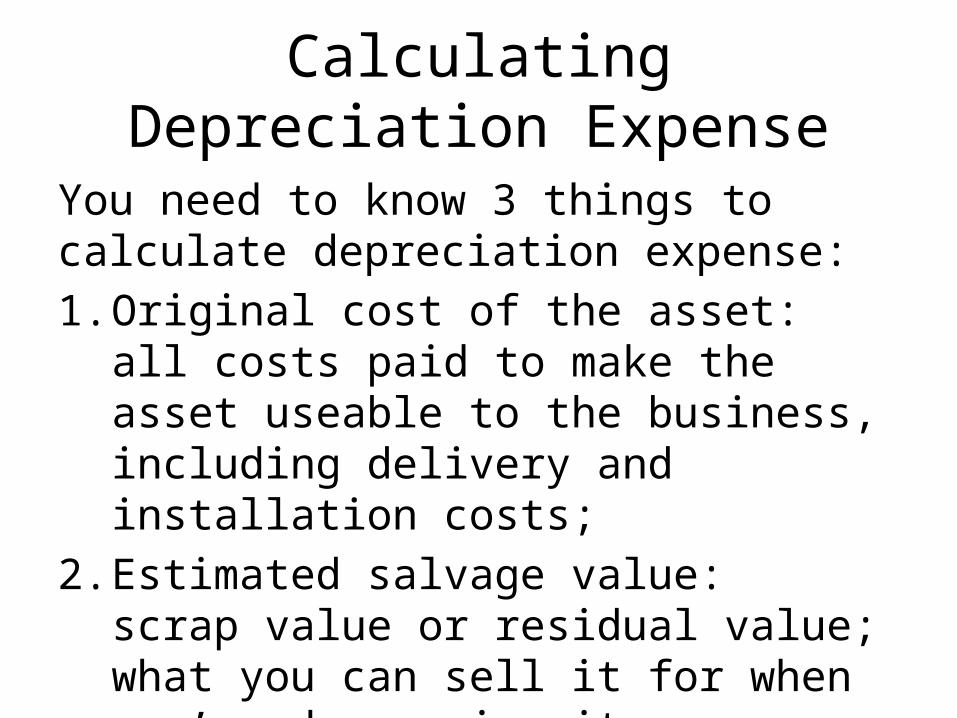

You need to know 3 things to calculate depreciation expense:1. Original cost of the asset: all costs paid to

make the asset useable to the business, including delivery and installation costs;

2. Estimated salvage value: scrap value or residual value; what you can sell it for when you’re done using it

Calculating Depreciation Expense, continued

3. Estimated useful life – the number of years the asset will be used (based on previous experience, and guidelines available from the I.R.S. and trade associationshttp://www.irs.gov/pub/irs-pdf/p946.pdfhttp://www.accountingtools.com/questions-and-answers/what-is-macrs-depreciation.html

Calculating Useful Life:

Two factors affect a long-term asset’s useful life:1. Physical depreciation -- wear and tear on the

asset; an asset may deteriorate due to aging and weathering

2. Functional depreciation – an asset becomes inadequate or obsolete – can no longer perform as needed. Obsolete means a newer machine can operate more efficiently or produce better service

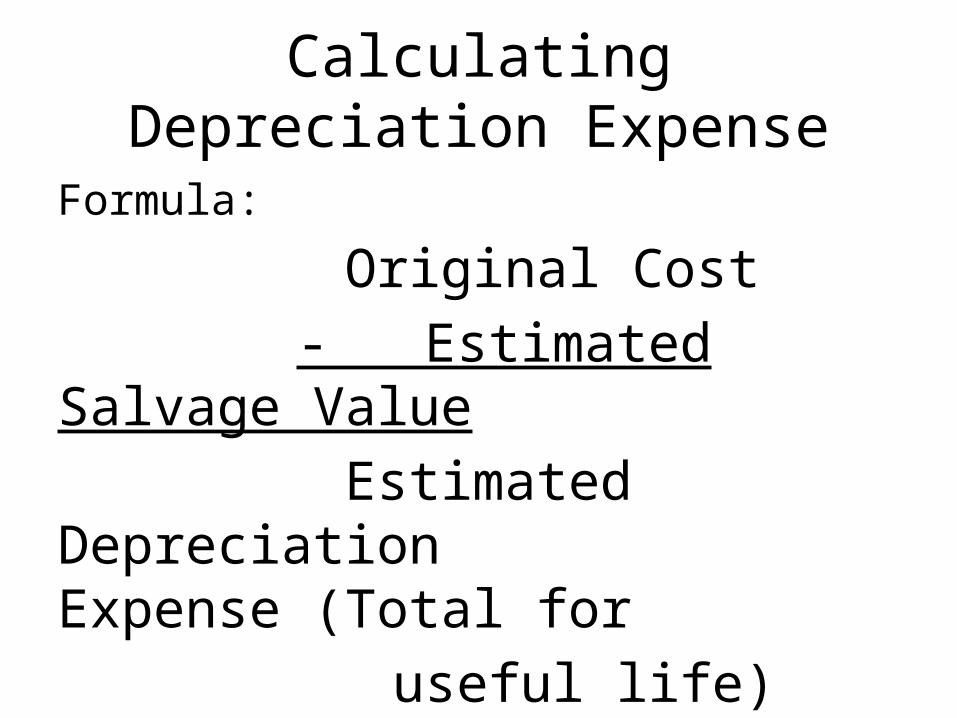

Calculating Depreciation Expense

Formula:

Original Cost - Estimated Salvage Value

Estimated Depreciation

Expense (Total for useful

life)

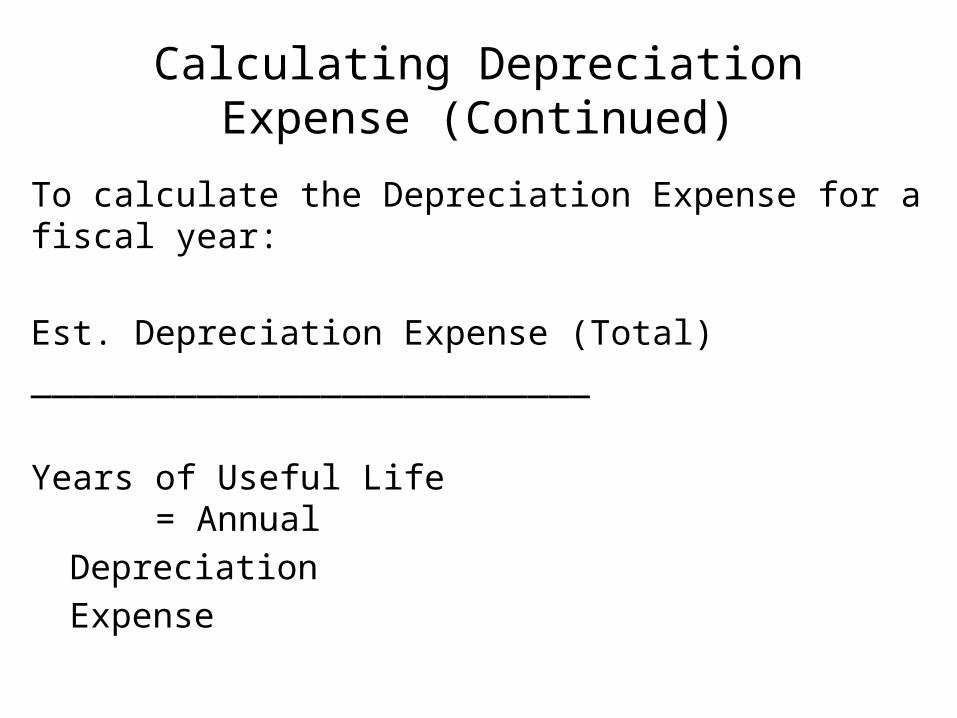

Calculating Depreciation Expense (Continued)

To calculate the Depreciation Expense for a fiscal year:

Est. Depreciation Expense (Total)___________________________

Years of Useful Life = AnnualDepreciationExpense

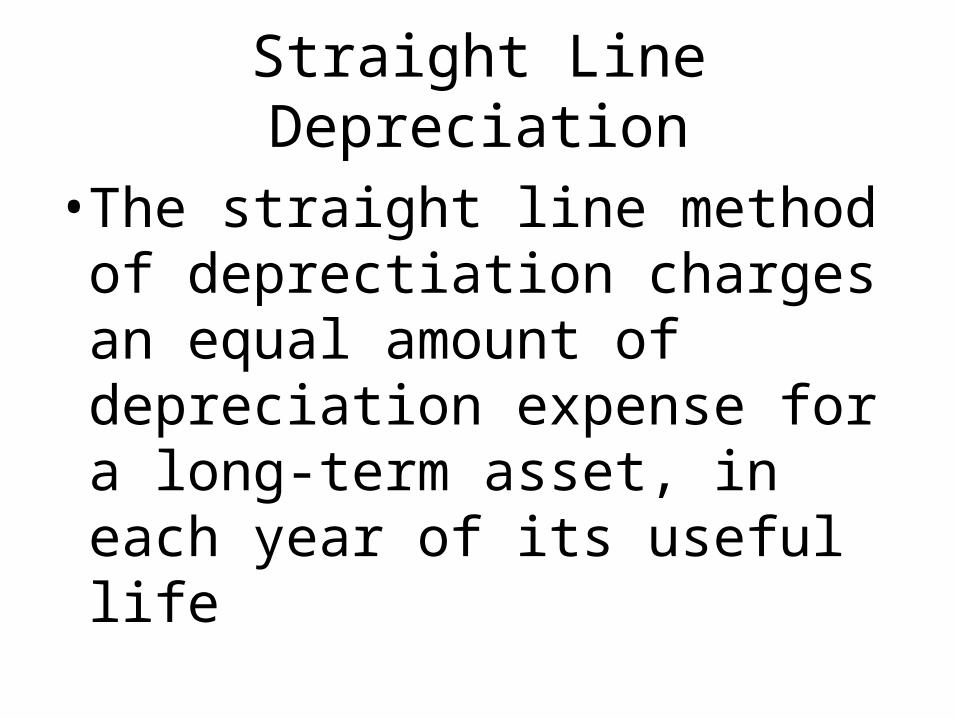

Straight Line Depreciation

• The straight line method of deprectiation charges an equal amount of depreciation expense for a long-term asset, in each year of its useful life

Example:

A business buys a piece of machinery that costs $800 plus $20 for installation costs.The estimated salvage value is $100.Original Cost = $820Minus Estimated salvage value ($100) = Estimated Depreciation Expense (Total) $820 - $100 = $720; useful life is 5 years:

$720 / 5 = $144 per year

Another Example

A business buys a truck for $30,000. What is its useful life? 5 yearsIt has a salvage value of $15,000.What is the annual depreciation expense, using

straight line depreciation?($30,0000 – 15,000) / 5 = $3,000 /year

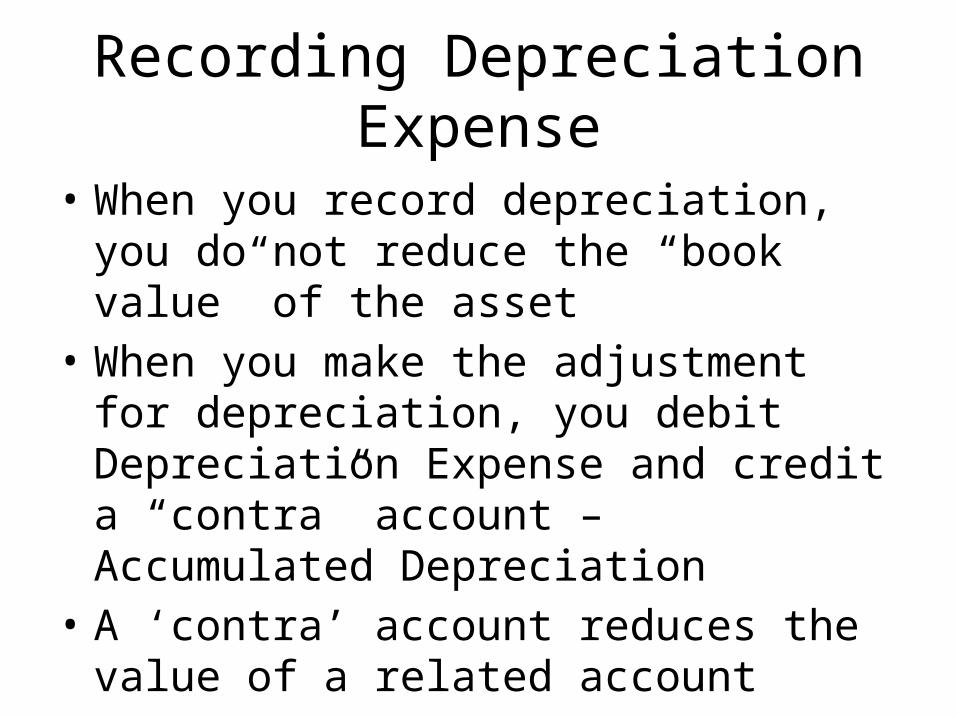

Recording Depreciation Expense

• When you record depreciation, you do not reduce the “book value” of the asset

• When you make the adjustment for depreciation, you debit Depreciation Expense and credit a “contra” account – Accumulated Depreciation

• A ‘contra’ account reduces the value of a related account

Asset Records

• Most businesses keep a separate record for each long-term asset.

• Sometimes called a “Plant Asset Record.”• Includes the date bought, information about

the asset (e.g., model / serial no.) the original cost, estimated useful life, estimated salvage value, book value, and accumulated depreciation.

“Book Value”

Book value is what an asset is worth according to the books of the business. It is the difference between original cost and accumulated depreciation.

“Basis”

The “basis” of an asset is another name for “original cost” – it includes the original price of the asset, plus shipping and installation and anything else needed to place the asset in service.

Recording Depreciation ExpenseTo record depreciation expense

(adjusting entries):Dr. Depreciation Expense

Cr. Accumulated DepreciationThe book value of the asset does not

change when depreciation is recorded.

Disposing of Long-Term Assets

When a business can no longer use a long-term asset, it disposes of it by selling it, trading it, or discarding it.

Disposing of Long-Term Assets

A journal entry is needed to: (1) remove the asset and its accumulated depreciation from the books; (2) recognize any cash or other (new) assets received for the old asset; and (3) recognize the gain or loss (if there is any) on the disposal of the asset.

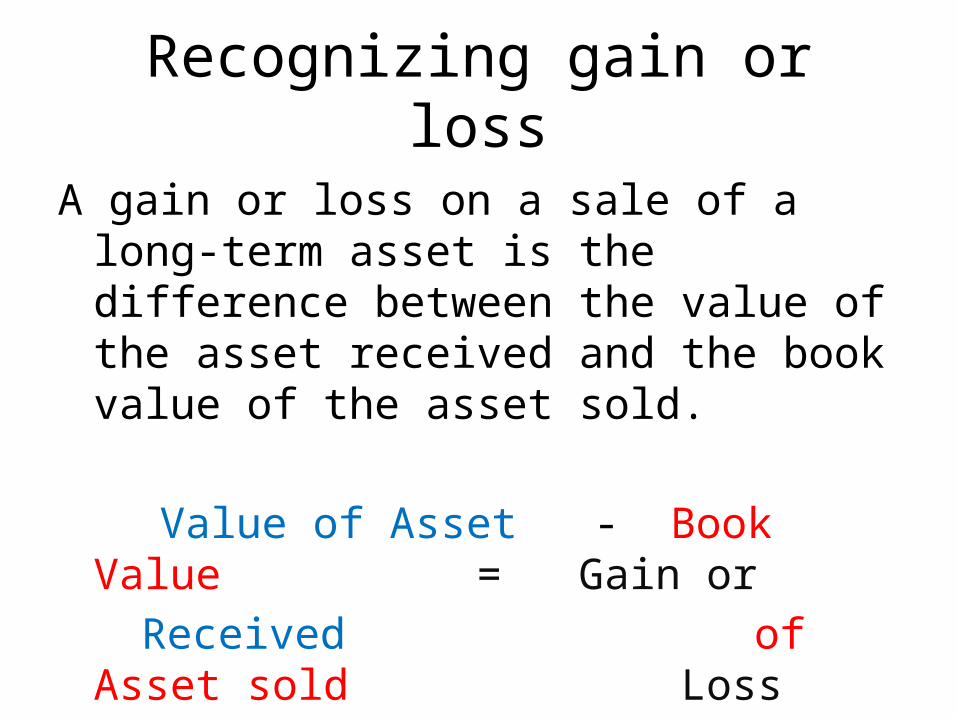

Recognizing gain or loss

A gain or loss on a sale of a long-term asset is the difference between the value of the asset received and the book value of the asset sold.

Value of Asset - Book Value = Gain orReceived of Asset sold

Loss

Example:

A business buys a printer for $820. Its estimated salvage value is $100, so it can depreciate the asset down to $100, and then no further.

Total Depreciation = original - salvage valueExpense cost

$720 = $820 - $100

Example, continued

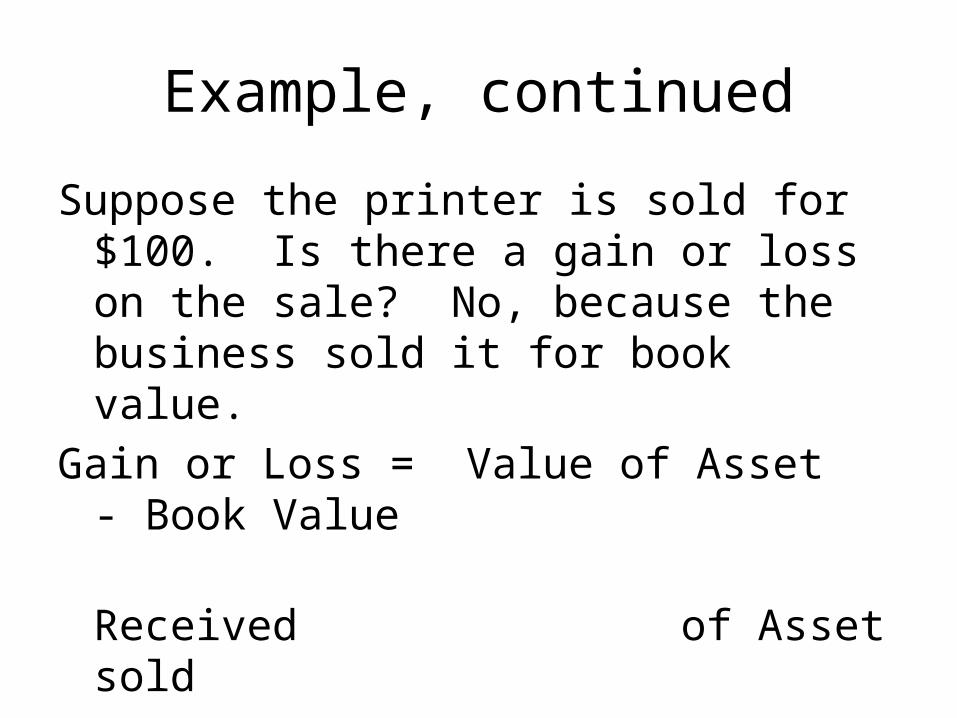

Suppose the printer is sold for $100. Is there a gain or loss on the sale? No, because the business sold it for book value.

Gain or Loss = Value of Asset - Book Value Received of Asset sold

$0 = $100 - $100

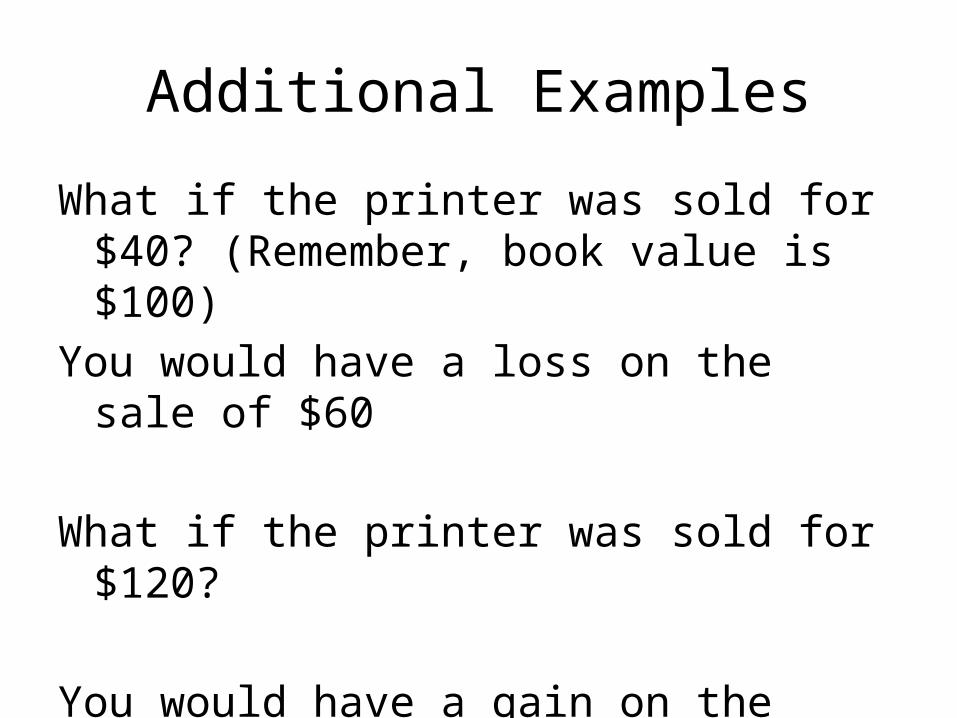

Additional Examples

What if the printer was sold for $40? (Remember, book value is $100)

You would have a loss on the sale of $60

What if the printer was sold for $120?

You would have a gain on the sale of $20

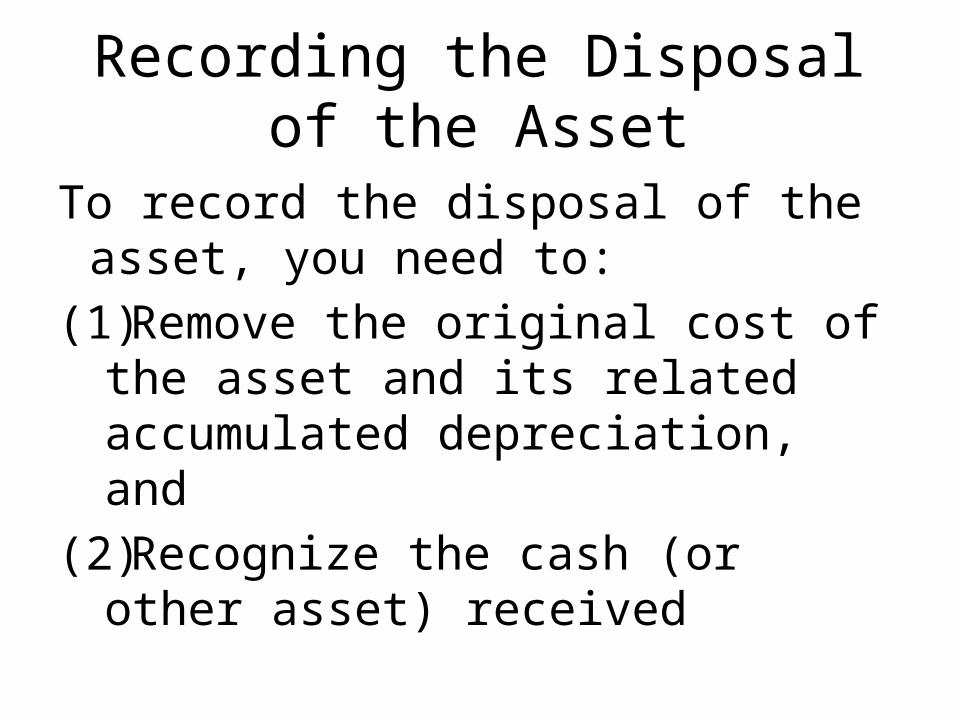

Recording the Disposal of the Asset

To record the disposal of the asset, you need to:

(1)Remove the original cost of the asset and its related accumulated depreciation, and

(2)Recognize the cash (or other asset) received

Journal Entries:Before disposing of the printer, the accounts look like

this: Printer Accumulated Depreciation

$820 $720

Entries to dispose of the printer for $100: Printer Accumulated Depreciation Cash $820 $820 $720 $720 $100

Sell asset at a gain:Before selling the printer for $120: ($100 salvage value)

Printer Accumulated Depreciation

$820 $720

Entries to dispose of the printer for $120: Printer Accumulated Depreciation Cash Gain on Plant

$820 $820 $720 $720 $100 $20 Decrease Increase

Assets

Sell asset at a loss:Before selling the printer for $60: ($100 salvage value)

Printer Accumulated Depreciation

$820 $720

Entries to dispose of the printer for $60: Printer Accumulated Depreciation Cash Loss on Plant

$820 $820 $720 $720 $60 $40 Increase Decrease

Assets

Accelerated Depreciation

• Most assets do not depreciate the same amount each year. Most assets depreciate / lose value faster in the first few years they are owned, and less in later years.

• For these assets, more depreciation should be charged in the early years than the later years

Accelerated Depreciation

• Declining balance method – multiply the book value (original cost – accumulated depreciation) by the same amount each year – a constant depreciation rate. • Because the book value is the highest in

the first year, that year will have the highest depreciation expense.

Double Declining Balance Method

• A method of accelerated depreciation• The book value declines each

year at twice the straight-line rate, multiplied by the book value.

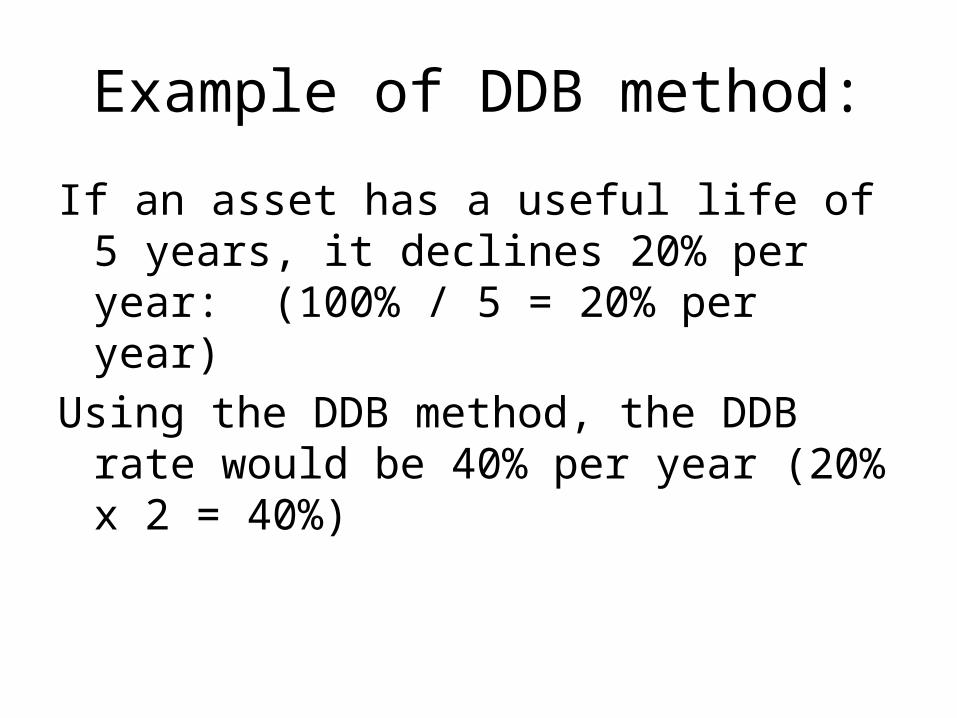

Example of DDB method:

If an asset has a useful life of 5 years, it declines 20% per year: (100% / 5 = 20% per year)

Using the DDB method, the DDB rate would be 40% per year (20% x 2 = 40%)

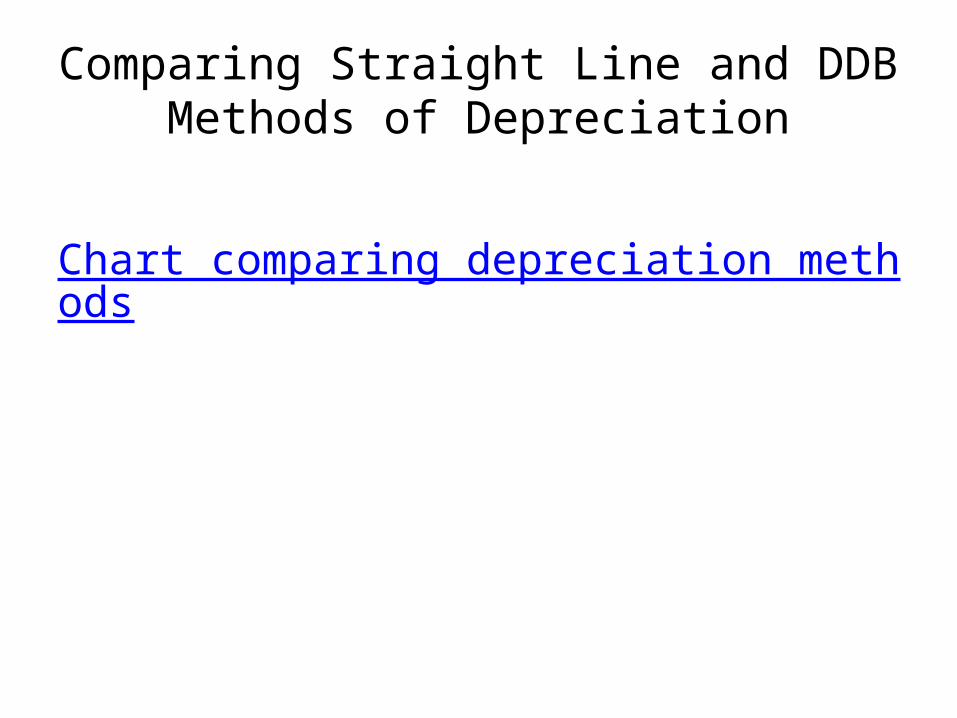

Straight-Line Method Double Declining Balance Method

Year BeginningBookValue

AnnualDeprec.

EndingBook Value

Beginning Book Value

Annual Deprec.

EndingBook Value

1 $20,000 $3,600 $16,400 $20,000 $8,000 $12,000

2 16,400 3,600 12,800 12,000 4,800 7,200

3 12,600 3,600 9,200 7,200 2,880 4,320

4 9,200 3,600 5,600 4,320 1,728 2,592

5 5,600 3,600 2,000 2,592 592 2,000

Total Depr. 18,000 18,000

Original cost: $20,000; useful life: 5 years; Salvage Value: $2,000

Comparing Straight Line and DDB Methods of Depreciation

Chart comparing depreciation methods

Related Documents