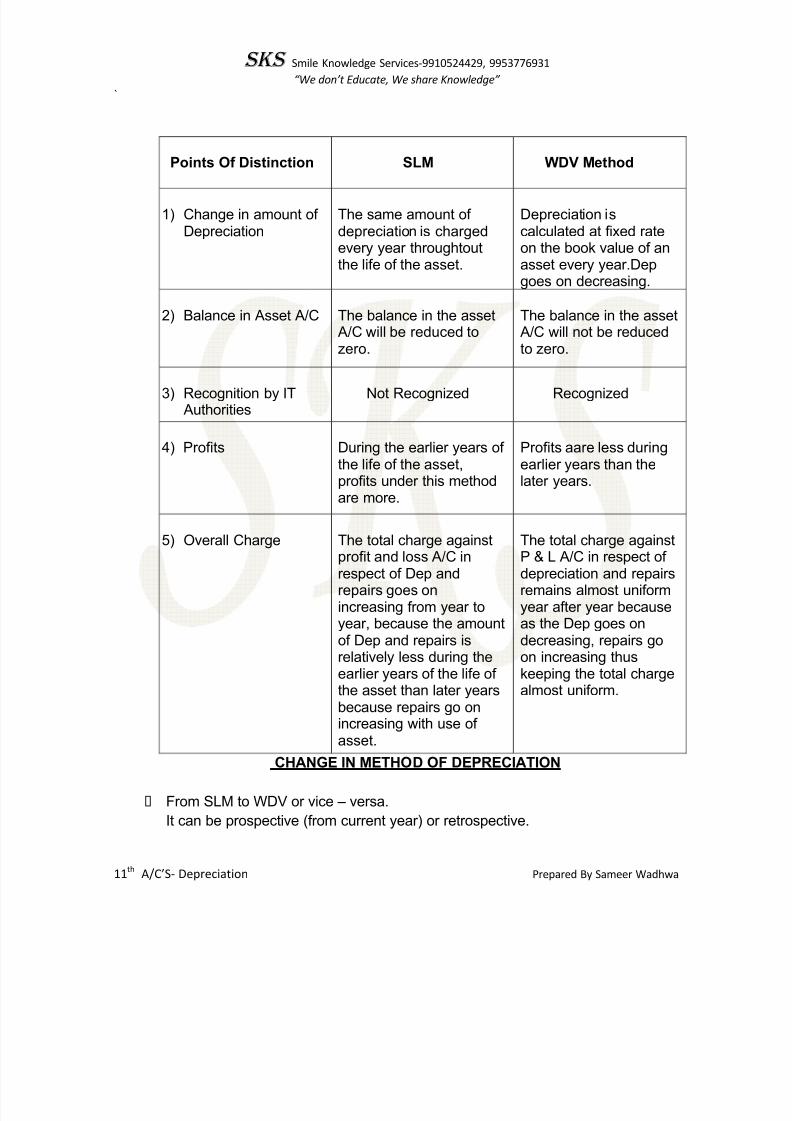

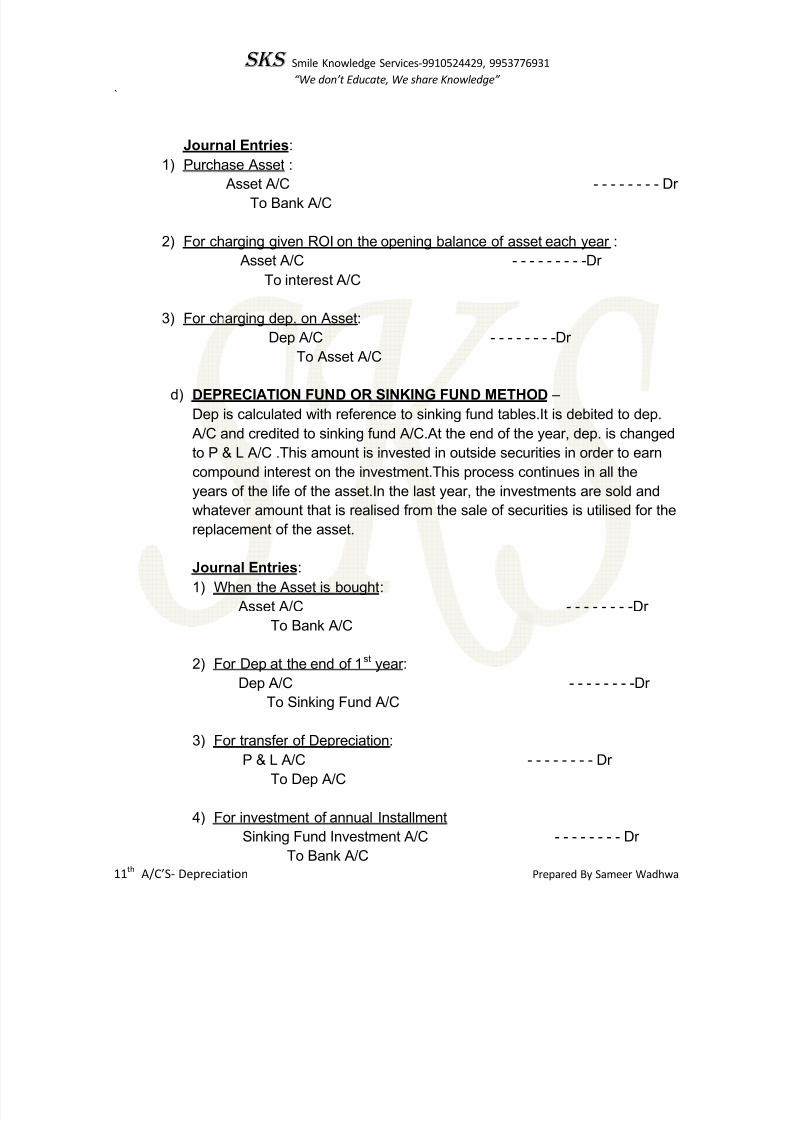

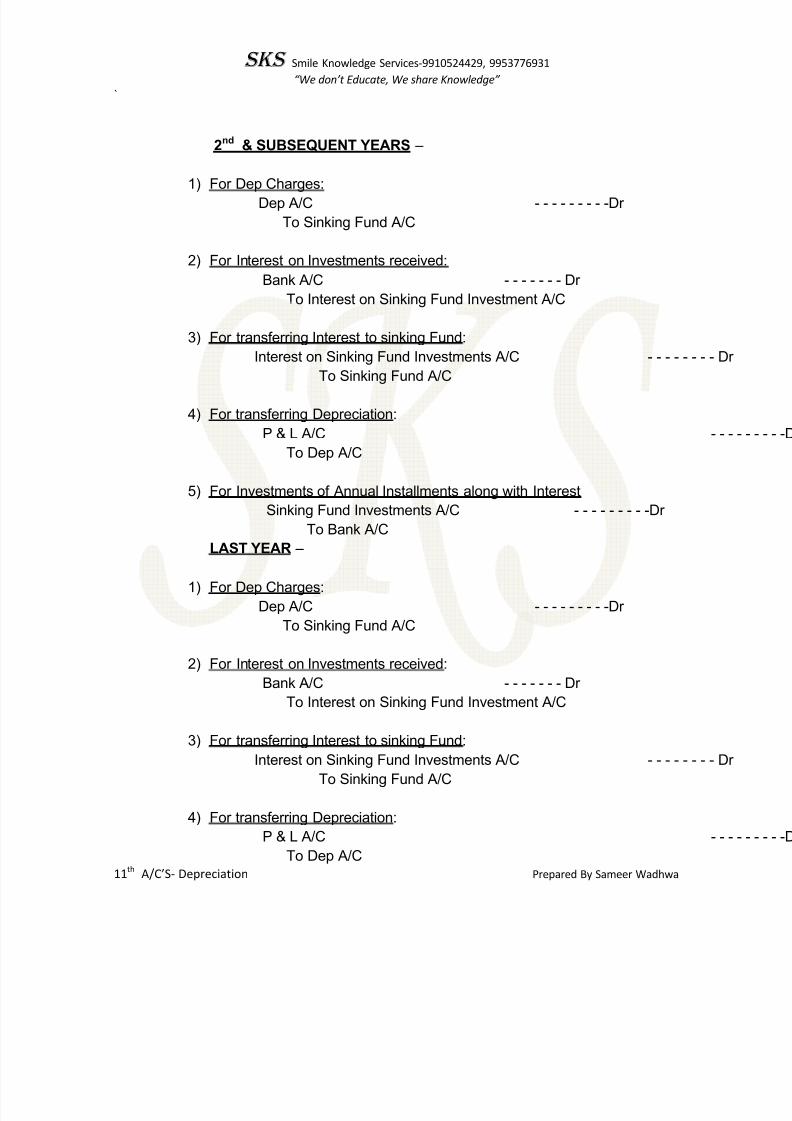

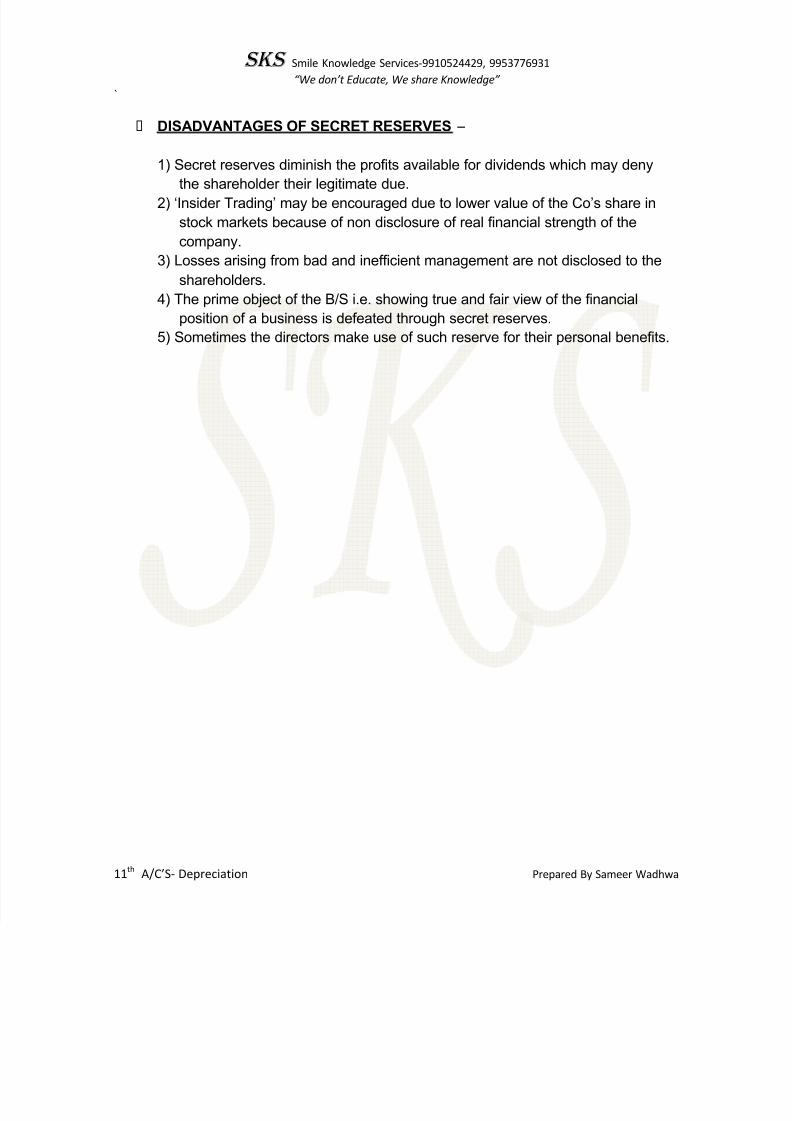

SKS Smile Knowledge Services-9910524429, 9953776931 We dont Educate, We share Knowledge ` 11 th A/CS- Depreciation Prepared By Sameer Wadhwa DEPRECIATION ACCOUNTING CONCEPT: Depreciation is the process of spreading the cost of fixed Asset over the different accounting periods which derive the benefit from their use. Eg.Of Assets ± M/C,Furniture,Buildings,Leases,etc. Land is a fixed Asset but not subject to depreciation because it has infinite lifetime. Meaning and Definition of Depreciation : Depreciation is a permanent decline in the value of an Asset.The gradual decrease, both in the value and usefulness of an Asset due to its nature and usage is termed as Depreciation. ³Depreciation is the measure of the exhaustion of the effective life of an Asset from any cause over a given period´. ICAI ³Depreciation is the measure of wearing out, consumption or other loss of value of a depreciable Asset arising from use, efflusion of time or obsolescence through technology and market changes´. IMPORTANT TERMS : 1) Depreciable Assets ± The A ssets whose lifetime can be estimated and used d uring two or more accounting periods in production or service activities of an organisation. 2) Useful Life ± It is the time during which the Ass et is helpful in the normal business activities of a firm.It can be less than the total lifetime of the Asset. 3) Depreciable Amount ± is the cost of acquisition and installation of an Asset after reducing any realisable value at the end of useful life. 4) Realisable Value ± This is the amount realisable at the end of the Asset¶s of an Asset as in the case of leased Assets. 5) Efflusion of Time ± is the passage of time irrespective of actual use of an Asset as in the case of leased Assets. 6) Obsoloscence ± refers to an A sset becoming out of date due to improved models or methods.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 1/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 2/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 3/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 4/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 5/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 6/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 7/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 8/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 9/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 10/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 11/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 12/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 13/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 14/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 15/16

8/7/2019 DEPRECIATION ACCOUNTING (Autosaved)

http://slidepdf.com/reader/full/depreciation-accounting-autosaved 16/16

Related Documents