A Project Report (16MBAPR407) A STUDY ON IMPACT OF FOREIGN CURRENCY FLUCTUATIONS ON INDIAN STOCK MARKET WITH REFERENCE TO NIFTY BY SOMASHEKHAR C (1AY16MBA77) SUBMITTED TO VISVESVARAYA TECHNOLOGICAL UNIVERSITY BELAGAVI In the fulfillment of the requirement for the award of the degree of MASTER OF BUSNIESS ADMINISTRATION Under the Guidance of INTERNAL GUIDE EXTERNAL GUIDE DR. PRAKASH B. YARAGOL Ms. RAHSMI RANJAN PADHI Professor Dept of MBA AIT Unit Head- Karnataka Department of MBA ACHARYA INSTITUTE OF TECHNOLOGY Soldevanahali, Hesaraghatta Main Road, Bangalore-107 May 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A Project Report

(16MBAPR407)

A STUDY ON IMPACT OF FOREIGN CURRENCY FLUCTUATIONS ON

INDIAN STOCK MARKET WITH REFERENCE TO NIFTY

BY

SOMASHEKHAR C

(1AY16MBA77)

SUBMITTED TO

VISVESVARAYA TECHNOLOGICAL UNIVERSITY

BELAGAVI

In the fulfillment of the requirement for the award of the degree of

MASTER OF BUSNIESS ADMINISTRATION

Under the Guidance of

INTERNAL GUIDE EXTERNAL GUIDE

DR. PRAKASH B. YARAGOL Ms. RAHSMI RANJAN PADHI Professor Dept of MBA AIT Unit Head- Karnataka

Department of MBA

ACHARYA INSTITUTE OF TECHNOLOGY Soldevanahali, Hesaraghatta Main Road, Bangalore-107

May 2018

....L.

Ji .

WEALTH . Br.IA CREATORS -- -- -- - -- -- -- ·-- -- - --Bui Id Ing Relattonahlpa . Crtallng Wealth BMA Wealth Creators Ltd.

CERTIFICATE

This is to certify that Mr. SOMASHEKHAR C USN I A Y l 6MBA 77 a student

of MBA studying at A CHARY A INSTITUTE OF TECHNOLOGY, Bangalore

has undergone the internship and has completed project titled as "A study on

Impact of Foreign Currency Fluctuation on Indian Stock Market With

Reference To Nifty" at BMA Wealth creators Ltd (Jayanagar Bangalore

Branch) from the period of 15thJanuary 2018 to 24th March 2018 in our

company under the guidance of Ms. RASHMI RAJAN P ADHI.

We wish to express our appreciation for his excellent work done and wish him

all the success in his new endeavour.

Place: Bangalore

Date: 24-March-2018

Ext'\')nal GHide

-~~\,\\i ' _.,.,..,-::: '}..,-'•

RASH~~ADID

Corporate Office:

Vishwakarma 2915A, Or. Ambedkar Sarani. Topsia Road,

Kolkata - 700046 PH : 033-400110099

Rogd Office 14/1 , Paul Mansion. 1st Floor, 6, Bishop Lefroy Rod, Kolkata 700020

I I

~

ACHARYA INSTITUTE OF TECHNOLOGY

(Affiliated to Visvesvaraya Technological University, Belagavi, Approved byAICTE, New Delhi and Accredited by NBA and NAAC)

25/05/2018

CERTIFICATE

This is to certify that Mr. Somashekhar C bearing USN

lA Y16MBA 77 is a bonafide student of Master of Business Administration

course of the Institute 2016-18 batch, affiliated to Visvesvaraya

Technological University, Belgaum. Project report on "A Study on Impact

of Foreign Currency Fluctuations on Indian Stock Market with

Reference to NIFTY at BMA Wealth Creators Ltd" Bangalore is

prepared by him under the guidance of Dr. Prakash B Yaragol in partial

fulfillment of the requirements for the award of the degree of Master of

Business Administration, Visvesvaraya Technological University, Belgaum,

Kamataka.

'k~ 1.-f]S /u ~

JjN~ ~~'ln;;;:~nt Signature of Internal Guide

<

Separ-tment of MBA Acharya Institute of Technology

J oldevanahtn, sa~r,?.1ore-560 io·,·

~~~ Signature of Principal

PRINCIPAL

'· ~ tQ\!f 'f·'C'"'l'rlJ'f': u···- T;. , 'Ol OGV ., .., ,~., ,H, i.) 1 1 t r .... \oo7 ,'i _

~;oldevanat1a!li Bangalure-550 1 o;

Acharya Or. Sarvepalli Aadhakrrshnan Road. Soladevanahalli, Acharya PO .. Bangalore 560 107, Karna1aka, lnd1a • www.acharya.ac.1n/ait/ • Ph: +91-80-225 555 55 Extn.: 2102 • Fax· +91-80-237 002 42 • E-mail: [email protected]

DECLARATION

I SOMASHEKAHR C hereby declare that internship report entitled "A STUDY ON IMPACT ,

OF FOREIGN CURRENCY FLUCTUATIONS ON INDIAN STOCK MARKET WITH

REFERENCE TO NIFTY" at BMA WEALTH CREATORS LTD, Bangalore prepared by

me under the guidance of DR. PRAKASH B Y ARAGOL, Professor of MBA Department,

Acharya Institute of Technology and external assistance by Ms. RASHMI RANJAN PADHI unit

head at BMA wealth creators ltd Bangalore.

I also declare this Internship work is towards the partial fulfillment of the university regulations

for the award of the degree of Master of Business Administration by Visvesvaraya Technological

University, Belgaum.

I have undergone a summer project for a period of TEN weeks. I further declare that this project

is based on the original study undertaken by me and has not been submitted for the award of any

degree/diploma from any other University Institution.

Place: Bangalore iomashekhar C. 1AY16MBA77

ACKNOWLEDGEMENT

I would like to thank all of those who have helped and supported me in completing this

project successfully.

Firstly I thank Dr.S.C.Pilli Principal,Dr.Mahesh Dean Academics and Dr.Nijaguna G.

Head of the department of MBA of Acharya Institution of Technology for giving

encouragement and support for completing the project.

I take this opportunity to thank our internal guide Dr. Prakash B Yaragolfor his constant

guidance in completing the project.

I wish to pay my heartfelt respect and regards to Ms.RASHMI RANJAN PADHI

Bangalore, for the cooperation and support, which helped me successfully to accomplish my

project work. Also, I am thankful to them for their valuable guidance given to me during the

course of my project.

Finally, it gives me great pleasure to extend my thanks to my Parents, Family, Friends and all

Teaching staff and Non-Teaching staff who have been instrumental either directly or

indirectly for this constant encouragement in carrying out this project successfully.

Place: BANGALORE SOMASHEKHAR C 1AY16MBA77

TABLE OF CONTENTS

Chapter

No.

Titles PAGE

NO

COMAPANY CERTIFICATE

COLLEGE CERTIFICATE

DECLARATION

AKNOWLEDMENT

LIST OS TABLES

LIST OF CHARTS

Executive summary 1

1

Introduction 2-3

1.1 Industry profile of Stock broking company 3-5

1.2 Company profile of BMA wealth creators 5

1.3 Nature of business of BMA 6

1.4 Management Team of BMA 6

1.5 Vision mission and quality policy 6-7

1.6 Products and Services of BMA 7-9

1.7 Area of operations of BMA 10

1.8 Infrastructure facilities 10

1.9 Competitors Information 10

1.10 SWOT Analysis of BMA 10-12

1.11 Future growth and prospects 12

2

Conceptual background and literature review

2.1 Introduction 13-16

2.2 Literature review 16-17

2.3 Research gap

17

3

Research Design

3.1 Statement of the problem 18

3.2 Need for the study 18

3.3 Objective of the study 18

3.4 Scope of study 18-19

3.5 Research methodology 19

Limitations of study 20

4

Data analysis and interpretation

4.1 Regression analysis of NIFTY 50 21-24

4.2 Regression analysis of NIFTY 100 25-28

4.3 Regression analysis of NIFTY 200 29-32

4.4 Regression analysis of NIFTY 500 33-36

4.5 Regression analysis of NIFTY NEXT 50 37-40

5

Summary of Finding , suggestions and Conclusion

5.1 Summary of findings 41-42

5.2 Suggestions 42

5.3 Conclusion 42-43

Bibliograpghy 43-45

LIST OF TABLES

TABLE

NO

TITLE OF TABLES

PAGE

NO

1.1 Tables showing Regression analysis of NIFTY 50 with

EURO 21

1.2 Tables showing Regression analysis of NIFTY 50 with

GBP 21

1.3 Tables showing Regression analysis of NIFTY 50 with

JYEN 22

1.4 Tables showing Regression analysis of NIFTY 50 with

USD 22

1.5 Tables showing Regression analysis of NIFTY 50 with all

4 currencies 23

1.6 Tables showing Regression analysis of NIFTY 100 with

EURO 25

1.7 Tables showing Regression analysis of NIFTY 100 with

GBP 25

1.8 Tables showing Regression analysis of NIFTY 100 with

JYEN 26

1.9 Tables showing Regression analysis of NIFTY 100with

USD 26

1.10 Tables showing Regression analysis of NIFTY 100with

all 4 currencies 27

1.11 Tables showing Regression analysis of NIFTY 200 with

EURO 29

1.12 Tables showing Regression analysis of NIFTY 200with

GBP 29

1.13 Tables showing Regression analysis of NIFTY 200with

JYEN

30

1.14 Tables showing Regression analysis of

NIFTY 200with USD

30

1.15 Tables showing Regression analysis of NIFTY 200 with

all 4 currencies

31

1.16 Tables showing Regression analysis of NIFTY 500with

EURO

33

1.17 Tables showing Regression analysis of NIFTY 500with

GBP

33

1.18 Tables showing Regression analysis of NIFTY 500with

JYEN

34

1.19 Tables showing Regression analysis of NIFTY 500with

USD

34

1.20 Tables showing Regression analysis of NIFTY 500with

all 4 currencies

35

1.21 Tables showing Regression analysis of NIFTY NEXT

50with EURO

37

1.22 Tables showing Regression analysis of NIFTY

NEXT50with GBP

37

1.23 Tables showing Regression analysis of NIFTY NEXT

50with JYEN

38

1.24 Tables showing Regression analysis of NIFTY NEXT

50with USD

38

1.25 Tables showing Regression analysis of NIFTY NEXT

50with all 4 currencies

39

LIST OF CHARTS

CHART NO

TITLE OF THE CHART

PAGE NO

1.1

Chart showing average return of NIFTY 50 for

the period of 5years

24

1.2

Chart showing average return of NIFTY 100 for

the period of 5years

28

1.3

Chart showing average return of NIFTY 200 for

the period of 5years

32

1.4

Chart showing average return of NIFTY 500 for

the period of 5years

36

1.5

Chart showing average return of NIFTY

NEXT 50 for the period of 5years

40

1

EXECUTIVE SUMMARY

This project gives the insight of the one of the oldest financial service providing firm BMA

Wealth Creators located in Kolkata. The project gives the complete information about the

organisation and the various kinds of services provided to the clients to satisfy to their needs,

the firm’s strengths, weakness, opportunities and threats are also analysed.

The economic development of the country mainly depends upon growth and efficiency of the

stock markets. The efficiency and growth of stock markets largely depends on various

macroeconomic factors. One of the main macroeconomic, external factors which have a

major impact on activities of stock market is FOREIGN EXCHANGE RATE. So, to find

whether the foreign currency fluctuation will affect the stock market of India or not and to

provide suggestions to the investors on the basis of the conclusion derived.

Stock market and foreign currency fluctuation are having a significant relationship. So, in

order to analyse these things we have taken closing prices of 5 NSE indices for 5years.

Choosing 4 major foreign exchange rates which deals in Indian securities exchange (USD,

GBP, EURO and JYEN) taking 5 years time span estimation of currencies against Indian

rupee. Based on these information we figured yearly return for indices, we computed

Regression analysis as a result we found that there is so significant relationship between

foreign currency fluctuation and Indian stock market. So according to the examination we

presume that effect of foreign currency fluctuation does not influence the Indian stock

market. Financial investors while making ventures does not consider the foreign currency

fluctuation as an indicator for analysing stock prices for making investment.

2

Chapter-1

INTRODUCTION

INTRODUCTION TO THE TOPIC

Day by day we go over news like Rupees' esteem slides to 69. We see levels of Indian Rupee

going up or tumbling down against US Dollar. Have you at any point wondered what happens

when estimation of a money acknowledge or deteriorate? All things considered, in this time

of globalization where a scarcest change in one perspective can influence the countries

identified with that viewpoint, we can't neglect the regular variances of foreign currency

fluctuation which puts an enormous effect on an economy of a country. The problem area

deals the same.

The effort has been made to find out the value of the currency, how foreign currency

fluctuation influence stock prices of various organizations. This examination is to look at the

time of effect of currency fluctuation on Indian securities exchange. In order to examine the

impact and it has US dollar (USD) EURO, JYEN, POUNDS, and currency fluctuation against

Indian rupee as independent factors and national stock index (NIFTY) as a dependent

variable. The examination has been led for the time of five years from 2012 to 2017.

Furthermore, carrying out regression analysis for the NSE indices with the different foreign

currencies to find the co-relation and the impact of currency on the nifty due to which the

nifty movement takes place. This investigation reasons that there is no impact of foreign

currency fluctuation on NIFTY. Today’s globalized economy and alternate monetary forms

and universal financial system the impact of macroeconomic elements were directing the

basics and details prevailing in the internal markets. In the current past, Indian securities

exchange have seen greatest crash of around some cross worth of investments have vanished

in a solitary day. So, it is felt that there is a need of inspecting the relative and the effect of

US dollar, Euro, Pounds and JYEN fluctuations on Indian securities exchange. So as to watch

the present economic situations and to reveal the actualities to the financial

specialists(investors). This investigation purposes to take in the dynamics and Effect of

fluctuations in the currency. Currency fluctuations are fundamentally the proceeding with

deviations between the relative ethics of the cash dispensed by one nation when compared to

various currencies. This effect of the various currencies every day It is these fluctuations that

3

investor in coinage trade exchanges appearance too carefully keeping in mind the end goal of

incurring incomes from their assets. Exchange rates among the most watched, explored and

legislatively operated economic measures.

1.01 INDUSTRY PROFILE

Stock Broking Company is a money related establishment which gives services like

purchasing and selling of financial securities to the purchaser and seller. Stock broking firm

generally trade with the assistance of specialists who help to manage investors money. They

for the most part do stock exchanging and bond exchanging with their clients. Stock breakage

additionally gives benefits like purchasing IPO, bonus shares etc. It is the registered

representative, in which the investor buys and sells stocks and other securities through a stock

market for a fee or commission. The employees of the stock broking company are entrusted

with the responsibility of carrying out research in the market to provide optimum information

to the investors, and in doing so they act as the pension fund managers and portfolio

managers alike. The firm provides loans for certain approved clients to purchase investments,

with applied terms and conditions.

The firm also provides up to date live stock prices and quotes. When the stock broking firm

does the trade for its own account, it is known as broker dealer.

BOMBAY STOCK EXCHANGE

In the nineteenth period of Indian history the business men called Premchan Roychan

established Bombay Stock Exchange (BSE). The primary stock exchange in India and oldest

most stock exchange in Asia. The BSE is the 11 the biggest stock exchanges. The market

capitalization of BSE as on July 2017 is $2 trillion.

BSE was framed with the assistance of 5 stock merchants. In the year 1957 the BSE was

perceived by Indian government under Securities Contracts Acts. Later on in the ear 1986 the

BSE created S&P BSE SENSEX. In the year 2000 the BSE utilized BSE SENSEX as device

to open derivative market trading with S&P BSE SENSEX future markets.

4

BSE in the year 2012 moved toward becoming accomplice trade of United Nations

Sustainable Stock Exchange activity.

NATIONAL STOCK EXCHANGE

“In the year 1992 the countries initially desalinated stock exchange was set up called National

Stock Exchange (NSE). NSE is just stock exchange which give completely mechanized,

screen based electronic exchanging framework. Vikram Limaye is present CEO and MD of

NSE. The aggregate market capitalization of NSE is $1.41 trillion.

NSE's NIFTY 50 came into drive on 1996 and reveals to us top 50 financial companies in

India and world. Nifty is managed by Indian Index and service Products (IISL).

NSE offers services like trading of securities, clearing and settlement process, trading of

derivatives etc. NSE is the twelfth biggest stock exchange in the world. The fundamental

companies of NSE are LIC, SBI, IFCI and IDBI Etc”1

SECURITIES AND EXCHANGE BOARD (SEBI)

“SEBI established in the year 1992, on April 12 according to the terms and conditions of

securities and exchange board of India Act 1992. It is the watchdog for all the transactions

carries out the security market in the market. The principle function of the SEBI is to

supervise activities in connection to all the monetary activities by giving guidelines. The

present CEO and chairman of SEBI is Ajay tyagi. It consists of 4 whole time directors and 4

part time directors. The major achievement of SEBI is making markets electronic and

paperless and introducing T+2 settlement system in April 2003. The SEBI is responsive to

3categories of people that is investors, issuer of securities (issuing companies), brokers or any

market intermediaries”2

5

INDIAN STOCK MARKET

Stock market is a very popular market where the company’s shares and securities are traded.

World’s first stock market was establishes in Belgium, later on many countries started their

own stock market.

MAJOR STOCK EXCHANGES IN INDIA

1. Bombay Stock Exchange.

2. Calcutta Stock Exchange.

3. National Stock Exchange.

4. Cochin Stock Exchange.

5. Over the Counter Stock Exchange (OTC).C

Capital market is a market for long term securities where the securities are bought and sold

for more than a year. It channels the wealth of investors to long term productive use, such as

companies or government making investments. There are importantly two types of capital

market

Primary Market

Secondary Market

Primary market is a market where the company’s issues shares for the first (initial) time. It

also called as new issue market. It issues shares in order to raise the capital from the public.

Secondary Market is market where securities which are already issued are traded. The shares

which are issued by primary market are traded in secondary market.

1.02 COMPANY PROFILE

BMA Wealth Creators is a firm which provides financial services to its clients. It was

established in the year 2000. Its net worth is over Rs2000crores. It has a 40 plus branches and

7000 plus business partners all over India. It provides the services like equity, Commodity,

mutual funds and Insurance. Its headquarters is located in Kolkata with over 1800 employees

who are working for the success of the company. It has a highly qualified research team that

6

is lead by industry stalwarts and experts who contribute massively to the day to day trends of

the market both in technical and fundamental parts.

It takes care of the dreams, needs, aspirations and concerns of its clients and builds a good

relationship with them.

1.03 NATURE OF BUSINESS CARRIED

BMA WC Ltd is one of the India’s leading stock brokerage companies. BMA WC Ltd also

provided online trading, stock marketing and investments to country. The important features

Providing Depository services

Providing advisory services

Opening trading account

Opening Demat accounts

Helps in online trading.

1.04 MANAGEMENT TEAM

CHAIRMAN AND MANAGING DIRECTOR:- Anubhav Bhatter

DIRECTOR:- Avinash Agarwalla

CEO:- Mrugesh Devashrayi

RESEARCH HEAD:- Dharmesh Rajdev

CHIEF HR OFFICER:- Sambit Kumar Ghosh

HEAD BROKING:- Sarat Murarka

KEY PERSON:- Asit kumar Ghosh and Shiv Kumar Damani

1.05 COMPANY VISSION AND MISSION

VISION

Aspire to be the global financial industry benchmark for providing integrated financial

services building investor wealth and confidence.

MISSION

Strive to be global premier financial supermarket providing integrated investment services to

our clients thereby partnering their aspirations and the growth of the society at large.

7

QUALITY POLICY

Our people: By promoting team work in the company, appreciating the talent, enhancing

leadership quality and acting in time and carrying out the work in pride and passion.

Our service: By becoming the financial consultant to its clients, delivering good products

and services to them and creating value.

Our technology: By trying unfaltering to deliver better technological platforms that enable

our stakeholders into deriving better business with us.

Our innovation: By continuously striving to innovate ways to better our service and enhance

the client connect experience.

Our conduct: By providing a good and safe work place, respecting the work environment,

caring for our communities and demonstrating high ethical standards.

1.06 BMA PRODUCTS AND SERVICES

BMA wealth creators provide various types of financial services to its clients. It provides

quality and superior services. Following are the areas in which BMA wealth creators render

services and satisfy its investors and clients:-

Equity Broking: The firm arrangements in value offers and subsidiaries. Offers are an

offer in an organization's offer capital. It is the littlest unit of an association's offer

capital. Open purchase shares and get profits as indicated by economic situations and

profit approach of the association

Derivative Broking: these are the instruments that derive from other securities, which

are referred to as underlying assets. The price, risk and function of the derivative

depend on underlying asset. When the underlying asset is affected the derivative is

affected. Commonly included underlying asset are stocks, commodities, bonds,

interest rates etc.

Life and General Insurance:

1. LIFE INSURANCE - Life is brimming with startling amazements.

Unpredictable occasions can strike abruptly and upset the smooth beat of life

whenever. Subsequently, one should dependably guarantee the monetary

security of his/her family. So BMA offers one of the best life insurance plans.

8

2. GENERAL INSURANCE – BMA WC oversees life covers as well as

person's life by and large. They have faith in avoiding potential risk and

remaining shielded from disasters which can happen whenever, wherever.

That is the reason BMA WC offers you a portion of the best designs

accessible in General Insurance fragment:

Motor Insurance

Health Insurance Program

Fire Insurance

Burglary Insurance

Travel Insurance

Depository Services: BMA WC is putting forth a large number of administrations

under one rooftop likewise incorporates unparalleled Depository Services. BMA WC

is an enrolled part/Depository Participant of both CDSL (Central Depository Services

Ltd.) and NSDL (National Securities Depository Ltd.), in this manner giving the

clients a choice to pick their storehouse benefits as well as the chance of exchanging

at one place.

Investment Advisory: BMA WC has an aptitude group who give venture counsel to

their customers relying upon the report put together by the exploration board of

trustees. The venture suggestions assist the financial specialists with making choice

and follow up on. They likewise furnish quality item and administrations with one of

the great research program offices.

Mutual funds: it is an investment vehicle that is made up of pool of funds from many

investors for the purpose of investing in the stocks, money market instruments and

various other assets. Mutual funds are operated by money managers who invest the

pooled funds in order gain capital gains. It is constructed in such a way that it matches

the investment objectives of the pooled investors.

Initial Public Offerings: At the point when shares are being offered by any

organization to open for acquiring in showcase out of the blue, it is known as IPO. An

IPO has a specific opening and shutting date. An IPO must be over 90% bought in of

what the firm has offered to people in general before the end date generally the entire

9

IPO gets wiped out and the cash so gathered must be returned back to the general

population.

Commodity Broking: Items like Gold, Silver and Copper and so on which are utilized

as a part of everyday life are additionally exchanged through a broking house. As a

matter of fact SEBI characterizes a great deal size of these items and that much

amount must be purchased by a speculator or in numerous of the part measure

characterized keeping in mind the end goal to buy a ware.

Bonds: An obligation instrument issued for a specific time of planned typically over a

year to raise capital. BMA WC gives a phase were the administration or corporate

organizations can pitch their securities to the overall population. The organization

ensures that the intrigue and singular amount sum is paid on the development.

Currency trading: Cash Derivatives are Future and Options contracts which you can

purchase or offer particular amount of a specific money match at a future date. It is

like the Stock Futures and Options however the fundamental happens to be money

match (i.e. USDINR, EURINR, JPYINR OR GBPINR) rather than Stocks

Fixed Deposits: A Fixed Deposits is a budgetary instrument given by Indian banks

which give financial specialists a higher rate of interest than a general investment

account, until the point when the given development dates. It could possibly require

the making of a different record. It is known as time deposit..

The characterizing standard for a fixed deposit is that the cash can't be pulled back

from the FD. Note that banks may offer lesser financing costs under unverifiable

monetary conditions. The financing cost fluctuates in the vicinity of 4 and 11 percent.

Organization Fixed Deposits are the settled stores plans offered by an organization

and it wins a settled rate of return over some stretch of time. Such stores are

additionally acknowledged by Financial Institutions and Non-Banking Finance

Companies (NBFCs). Organization Deposits offer higher rate of interests than typical

Fixed Deposits

1.07 AREA OF OPERATION

10

It has a 40 plus branches and 7000 plus business partners all over India. It provides the

services like equity, Commodity, mutual funds and Insurance. Its headquarters is located in

Kolkata with over 1800 employees who are working for the success of the company.

1.08 INFRASTRUCTURE FACILITIES

BMA provides good infrastructural facilities to their employee and company. They provide

the best environment and one of the best work place to their employee.

They provide a good place and clean environment for work for employee.

They also maintain good ventilation facilities in order have work efficiency.

They provide all office necessary (computer, tables, stationary, etc) to their employee.

They also internet facilities for employee all time for work need with speed network

connection.

They also provide quality product and services with one of the good research

program facilities.

1.09 COMPETITORS

BMA wealth creators are the main financial service provider in India. It has many

competitors in the field. The main competitors are

Angel Broking Ltd

Share khan Ltd

Motilal Oswal Securities Ltd

ICICI Securities Ltd

Religare Ltd

1.10 SWOT ANALYSIS

SWOT analysis is a method of recognising the strength and weakness of the organisation and

to forecast the opportunity and threat of the organisation. It is an effective way to run the

company.

It also provides information about the resources and capability of the company. It also helps

in formulation of strategy and policy of the company.

Strength-It is the internal capacity of the company.

11

Weakness- It is internal disadvantage of the company.

Opportunity- Provides external positive information which helps the company.

Threat- provides external negative information to take preventive measures.

1.11 SWOT ANALYSIS OF BMA WEALTH CREATORS

STRENGHTS

It has its branches located in more than 3000 locations all over the country.

They have a good reliability.

They provide both online and offline services.

They have a good brand image compared to other organisation.

They have good research expertise.

They provide excellent services to their clients.

They provide IPO and mutual fund facilities to their customers.

WEAKNESSES

They do not go for much of promotional activities like advertisement.

They carry high level of risk.

Entry of clients/investors to the business is less.

OPPOTUNITIES

Market development and Growth will play a positive picture in the minds of the

clients to contribute.

Flourishing monetary market in nation and also around the world.

Still there are people who have money in their pockets but they are unaware about

how market works or what are the complications

Exploring the new market.

THREATS

High level of competition in the industry.

A change in technology also affects the business.

A change in the policies of the capital market.

Competitors charge a less rate of brokerage which decreases the clients from BMA

WC.

12

1.12 FUTURE GROWTH AND PROSPECTUS

Company has a decent research group with better system in diversifying and it is

having better systems administration, quality research and customized

administrations.

It is as of now having more branches in south India and wanted to open more in north

India with speed web offices.

Within the coming 5-6years organization expects to become a market pioneer in

financial administrations.

With an intention of Development and Growth, It has dispatch IPOs in the year 2011.

13

CHAPTER 2

CONCEPTUAL BACKGROUND AND LITERATURE REVIEW

2.1 THEORETICAL BACKGROUND OF THE FOREX MARKET

Until the mid-1970s, due to the steady administration of the rate, foreign trade was

considered as a system only to make exchange shipments. With the fall of the Breton Woods

agreement and the rise of significant monetary standards, the conduct of foreign exchange

policy for the national banks was an extraordinary challenge as currency fluctuations opened

up tremendous opportunities for traders to exchange cash volatility in the borderless market

The market in India has been preserved since exchange rate controls have limited the

development of capital, and banks have been urged to continue to cover and keep the market

square.

Gradually, a request was made to allow banks in India to exchange FOREX. Due to this

request, the RBI allowed banks to try to exchange FOREX during the day in 1978, as a first

step. As a result, the determination of adherence to a square or near border location was

agreed to foreclosure every day. The rate of the position that has been detected overnight

(free position) and the limitations that traders have exchanged on the day have been selected

by the bank's management.

As profit opportunities began to appear, the major banks began offering bidirectional prices

against rupees even in currencies (rupees), and the volume of trades gradually began to

increase. This made it possible to fundamentally change the exchange rate regime in 1975,

when the rupees were divided by pounds of sterling and under a controlled floating

arrangement; the external value of the rupee was determined by the RBI in relation to the

weighted basket of currencies of India's main trading partners. Given the RBI's obligation to

buy and sell unlimited pound sterling (intervention currency) stemming from the Bank's

business transactions, its buy / sell quotations have effectively become the support around the

market.

As volumes grew, it was found that the desire to profit led to the observance of very different

procedures (some of which were irregular), dictated mainly by the size of the players, their

14

location, the expertise of the traders and the availability of means of communication. a set of

instructions relating to a whole range of transactions to be followed by banks dealing with

FOREX trading. Therefore, in 1981, "instructions for internal control of foreign exchange"

were created for admission by banks.

During the 1980s, the macroeconomic situation deteriorated, which eventually justified a

structural change in the exchange rate regime, which had an impact on the FOREX market.

Large and persisting external imbalances have been reflected in an increasing level of internal

indebtedness. Higher depreciation of the rupee could not offset the deepening of the inflation

gap between India and the rest of the world, and the rupee exchange rate was still overvalued.

The Gulf Problems of August 1990, due to the fragile state of the economy, caused an

unprecedented crisis of liquidity and trust. This unprecedented crisis has called for

extraordinary remedial action. At the same time, the country has taken adjustment measures

to stabilize the economy and start structural reforms that would restore the impetus for stable

growth.

As the initial phase towards this route, the RBI suffered a two-stage downward revision of

rupees in July 1991. At the same time, given the ultimate goal of providing a closer

arrangement between prices and imports, the EXIM plot was presented. The plan provides a

lift that transmits and with the experience gained in the plan was thought to regulate part of

the motivational power and pass it with a value tool while protecting basic imports from

money differences. In this way, with effect from 1 March 1992, the RBI initiated a double-

rate trading agreement under the Liberalized Exchange Rate Scheme (LERMS). For this

purpose, 40% of business revenue must be surrendered at the rate set by the RBI and RBI is

obliged to offer external trade only for imports of basic goods such as oil, fertilizers, life-

saving drugs and others. than the duty of general administration. Adaptation of 60% could be

changed in market-driven prices. The plan worked with an acceptable market set-up for its

developing part, and Rupee remained really stable, with the range between authority and

market rate of around 17%.

Even through a double frame for the exchange of degrees it worked admirably, it is, as far as

possible, derives a certain assessment of exporters and settlements. In addition, it avoided a

thorough division of property. LERMS was essentially a transitional system and in March

1993 two legs of the trade rates joined and started modified LERMS. He stipulated that form

15

on March 2, 1993; All the FOREX receipt could be changed in the exchange rates decided.

During the following eighteen months, the limitations on several other current record

exchanges were casual and on August 20, 1994, the Rupee became fully convertible for all

current record records and the nation formally recognized the commitments under Article

VIII of the Article of Agreement of the IMF

2.2 LITERATURE REVIEW

Seifert(1992.), investigated GARCH outline for day-to-day statistics as of the US, the U K,

Germans and Japanese, exposed that complete alterations in stocks earnings have optimistic

impact on exchange rates instability.

Maaysami Koh(2000.), studied influences of the interests rates and conversations rates of

stocks revenues and displayed that those exchanges rates and interests rates stay as the

elements in stock values.

Iqbal and Haider (2005) analysed that risk aspects rise from variations in certain important

monetary and commercial variable namely interest rate, price rises, existent commercial

movement, and argument rate between additional variables.

Abhayy. Pethee and Ajitt Kaarnik (2000.)analysed that inter – relationship flanked by

stock values and significant macro-economic variants, vice interchange rates against INR vis-

a-vis USD, main advancing rates, narrow money supply, and index of industrial production.

Solniks (1987.) studied outlook it shows adverse connection among stock market & native

currencies. Specify that the 1st and 2nd-order effect of conversation rates change

significantly affect differentiated selections in the US shares market.

Takeshi(2008) studied uni-directional connection from stock revenues to FII movements,

unrelated of the example historical in India whereas the opposite interconnection works only

post 2003.

Stone(2009) examine that in 2005, the rand was maintained by high product values, foreign

straight investment movements, and optimistic economic data for SA in spite of the rising

current account shortage. After left over relatively stable, the conversation rate encountered

devaluate on weights in 2006.

16

Edwards, Biscarri and Gracia, (2003), Huang and Yang , (2000),Jayasuriya,

(2005)Investigated the variability also lean towards to growth nearby some actions: earning

declarations, integration, gossips showed, etc. The result of the liberalization on the

unpredictability of the market is also substantial.

Mishras (2004.) examine, present is No theoretic agreement On the interface flanked by

stocks rates& exchanges rates.

BenassyQuere, Fontagné, and LahrecheRevil, (2001.)investigated interchange rates was 1

of more significant essentials in background fiscal rules in the developing states. Indeed,

conversation rates procedures play a main part to invite direct external investment and to

swallow the spread stages. The left over part of the work is controlled as follow. In the 2nd

section, we give a theoretic background of the relationships among Forex rate and stocks

revenues. In this 3rd sector, we gave an explanation of these data’s and method utilised.

Martins & Zdzienickas(2009.) examined lesser conversation rates unpredictability related

high development, high shares of FDI, high current accounts shortages, and high additional

acclaim.

Adjasis & Biekpes(2005.) examined in the large-Run interchange rates reduction indicates to

growth of stocks market value within certain nations & in the small-Run, conversation rates

devaluation decrease stock market yields.

Schnabl, G. (2007). Studied, in attendance not any Co-Integration among conversation rates

and the Malaysia’s stocks marketplaces among lengthy route, duo sage connection study

discloses Uni-directional causation happens interchange rates to those stocks markets with

small course.

Ndri Konans Leon.(2008.) studied the interests rate, it vital influence explanation stock

markets profit moderately with instability.

Engles & Rangels (2005.) were examined relation among those unqualified instability & a

no. of macro-economic variants. They incorporated macro-economic info in a straight line

estimate of such Garch methods. Was established the predictions of macro-economic variants

may be frequently combined with unpredictability calculations on shares indices yields.

Rizwan and Khan (2007) examined clarified variable reputation of local macro-economic

variants used clarifying connection in the middle of stocks earnings & instability in Karachi’s

stocks conversations. A weakening in conversation rates ambiguity although improves worth

clearness increasing effectiveness of amount machineries at global Phase.

Allayanis and Ofeks(2001.), Allayanis, Browns and Klaper,(2001.). Investigated the threat

organization in overall it decrease improbability around the commercial outcomes of those

17

company. These detail spirit shrivel the instability of those stocks yields. Consuming

equivocation tools also diminish infection flanked by marketplaces. Though these processes

were expensive can reduce efficiencies of the business.

Ma & KaoS (1990.) studied money gratefulness depressingly disturbs the local stocks

markets for Export-leading state and definitely influences the internal stocks marketplaces,

Import-Dominant states, looks to be reliable properties market place concept.

Schwerts (1990.) analysed actions of stocks yield instability everywhere, stocks market

places cracks & expose stocks market instability obstacles intensely throughout smash &

revenues to little Pre-Crashes stages fast.

Domelys & Sheehys (1996.) examine that contemporary connection among imported

argument rates and the market places price huge local or domestic vendors in their learning.

Khoo,S (1994.) analysed excavating firms financial experience by means of conversion rates,

Interest Rates & prices of Oils ,exposed the understanding of stocks revenues relating

difference rates undertaking, quantity of stocks profits clarified through Forex rate measure

were little.

2.3 RESEARCH GAP

Most of the studies have used regression analysis tool to examine the foreign

currency fluctuation impact on Indian stock market. In this study we have used

the regression tool for both individual currency and the multiple currencies.

The individual currency is taken up to analyse with the various Nifty indices

and also all the 4 currencies are taken up with the individual Nifty index to

examine the impact.

18

CHAPTER 3

RESEARCH DESIGN

3.1 STATEMENT OF THE PROBLEM

“A study on impact of foreign currency fluctuation on Indian stock market with

reference to Nifty”

3.2 NEED FOR THE STUDY

The study is undertaken in order to find out or examine the impact of foreign currency

fluctuation on the Indian stock market and the various macro economic factors which

influence the exchange rate by using 4 major foreign currencies. The study also helps in

suggesting the investor that the foreign exchange fluctuation does not influence the stock

prices and the investment can be made without any hesitation.

3.3 OBJECTIVE OF THE STUDY

To examine the impact of foreign currency fluctuations on volatility of the Indian

stock market with reference to Nifty.

To give the suggestions to the investors

3.4 SCOPE OF THE STUDY

The target of the examination is to comprehend those elements which influence foreign

exchange rates and how the exchange rates affects price of shares of various listed

organizations. The problem study deals with the different kinds of currencies like Dollar of

US, Pound of Britain, Euro of Europe, Yen of Japan and Indian Rupee. It additionally

manages how Indian Rupee's value has devalued throughout the years against all other

currencies said before.

The exchange rate volatility has an imperative association with Indian securities exchange for

this reason we have taken NSE records we have mainly 10 indices 5 from Broad based and 5

from Sector based indices separately, in those lists we taken every day closing price in

19

connection to this we taken Four major Foreign currency exchange rates USD, GBP, EURO

and JYEN day by day price against INR. Both Stock Indices and Exchange rates information

are gathered for a long time period to understand the macroeconomic variables.

3.5 RESEARCH METHODOLOGY

Data source: - The data is collected from the secondary source. The daily closing price of

NIFTY indices is collected form NSE official website (www.nseindia.com) and varying

currency values against Indian rupee is fetched from RBI official website (www.rbi.org.in)

Sample size: - The data is fetched for the period of 5years from 1/04/2012 to 30/03/2017.

Analytical research: - In Analytical Research, the researcher need to use actualities or data

effectively accessible, and examine them to make a assessment of the collected information.

It includes the inside and out examination and assessment of accessible data trying to clarify

complex marvel. In other words it uses the available information to evaluate the critical

problems and under goes in depth study.

Tools and Techniques used:-

Regression analysis

Return of indices

HYPOTHESIS

The following hypothesis is used to find the relationship between the foreign currency

fluctuation and stock price.

H0: There is a no significant relationship between NIFTY and currency fluctuations.

H1: US Dollar has a significant relationship on NIFTY

H2: Euro has a significant relationship on NIFTY

H3: Japanese YEN has a significant relationship on NIFTY.

H4: Pound Sterling has a significant relationship on NIFTY

20

LIMITATIONS

Only few currency exchange rates were taken into consideration against Indian rupee.

There are other currencies which can affect the stock price of the Indian stock market.

Only 5 NSE indices were considered for the analysis and computation.

The data is collected for only 5years for the analysis.

The authenticity of the data while doing the calculations can be a limitation.

The statistical tool regression analysis is only used for the examination/finding

conclusion to the study.

The company has the limitation to disclose their financial details , so a detailed

analysis of financial performance of the company is not possible

21

CHAPTER- 4

DATA ANALYSIS AND INTERPRETATION

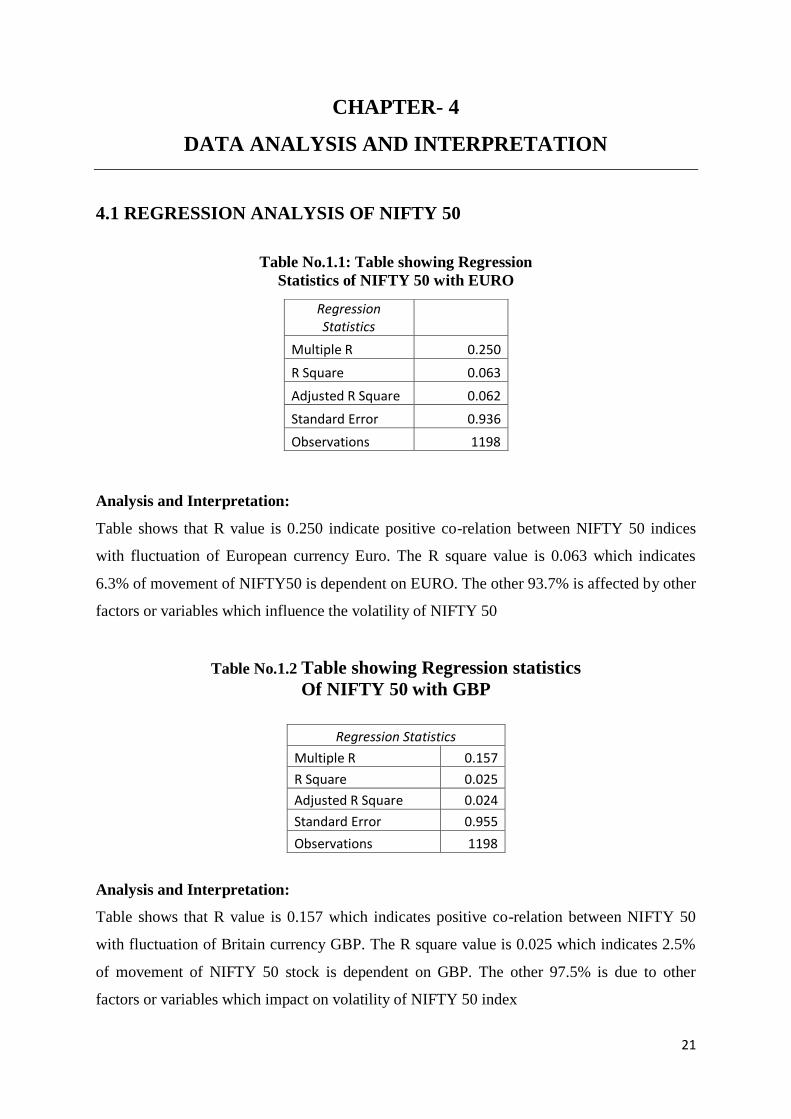

4.1 REGRESSION ANALYSIS OF NIFTY 50

Table No.1.1: Table showing Regression

Statistics of NIFTY 50 with EURO

Analysis and Interpretation:

Table shows that R value is 0.250 indicate positive co-relation between NIFTY 50 indices

with fluctuation of European currency Euro. The R square value is 0.063 which indicates

6.3% of movement of NIFTY50 is dependent on EURO. The other 93.7% is affected by other

factors or variables which influence the volatility of NIFTY 50

Table No.1.2 Table showing Regression statistics

Of NIFTY 50 with GBP

Analysis and Interpretation:

Table shows that R value is 0.157 which indicates positive co-relation between NIFTY 50

with fluctuation of Britain currency GBP. The R square value is 0.025 which indicates 2.5%

of movement of NIFTY 50 stock is dependent on GBP. The other 97.5% is due to other

factors or variables which impact on volatility of NIFTY 50 index

Regression Statistics

Multiple R 0.250

R Square 0.063

Adjusted R Square 0.062

Standard Error 0.936

Observations 1198

Regression Statistics

Multiple R 0.157

R Square 0.025

Adjusted R Square 0.024

Standard Error 0.955

Observations 1198

22

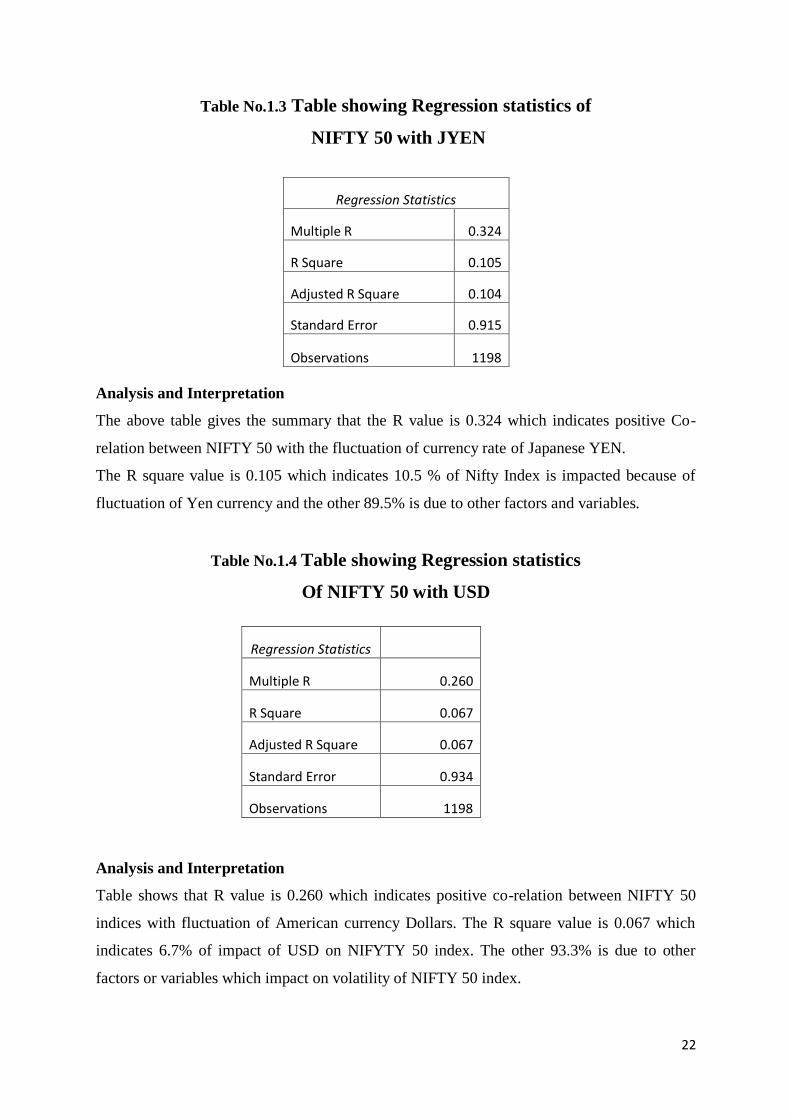

Table No.1.3 Table showing Regression statistics of

NIFTY 50 with JYEN

Analysis and Interpretation

The above table gives the summary that the R value is 0.324 which indicates positive Co-

relation between NIFTY 50 with the fluctuation of currency rate of Japanese YEN.

The R square value is 0.105 which indicates 10.5 % of Nifty Index is impacted because of

fluctuation of Yen currency and the other 89.5% is due to other factors and variables.

Table No.1.4 Table showing Regression statistics

Of NIFTY 50 with USD

Analysis and Interpretation

Table shows that R value is 0.260 which indicates positive co-relation between NIFTY 50

indices with fluctuation of American currency Dollars. The R square value is 0.067 which

indicates 6.7% of impact of USD on NIFYTY 50 index. The other 93.3% is due to other

factors or variables which impact on volatility of NIFTY 50 index.

Regression Statistics

Multiple R 0.324

R Square 0.105

Adjusted R Square 0.104

Standard Error 0.915

Observations 1198

Regression Statistics

Multiple R 0.260

R Square 0.067

Adjusted R Square 0.067

Standard Error 0.934

Observations 1198

23

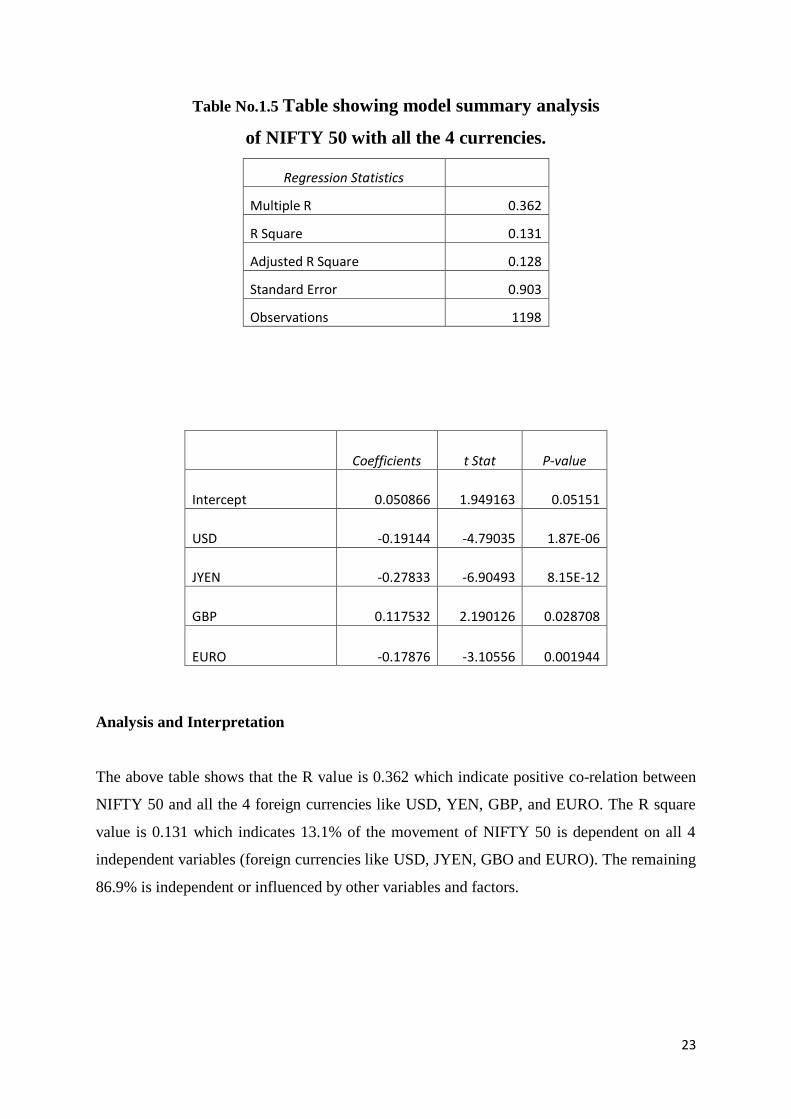

Table No.1.5 Table showing model summary analysis

of NIFTY 50 with all the 4 currencies.

Regression Statistics

Multiple R 0.362

R Square 0.131

Adjusted R Square 0.128

Standard Error 0.903

Observations 1198

Analysis and Interpretation

The above table shows that the R value is 0.362 which indicate positive co-relation between

NIFTY 50 and all the 4 foreign currencies like USD, YEN, GBP, and EURO. The R square

value is 0.131 which indicates 13.1% of the movement of NIFTY 50 is dependent on all 4

independent variables (foreign currencies like USD, JYEN, GBO and EURO). The remaining

86.9% is independent or influenced by other variables and factors.

Coefficients t Stat P-value

Intercept 0.050866 1.949163 0.05151

USD -0.19144 -4.79035 1.87E-06

JYEN -0.27833 -6.90493 8.15E-12

GBP 0.117532 2.190126 0.028708

EURO -0.17876 -3.10556 0.001944

24

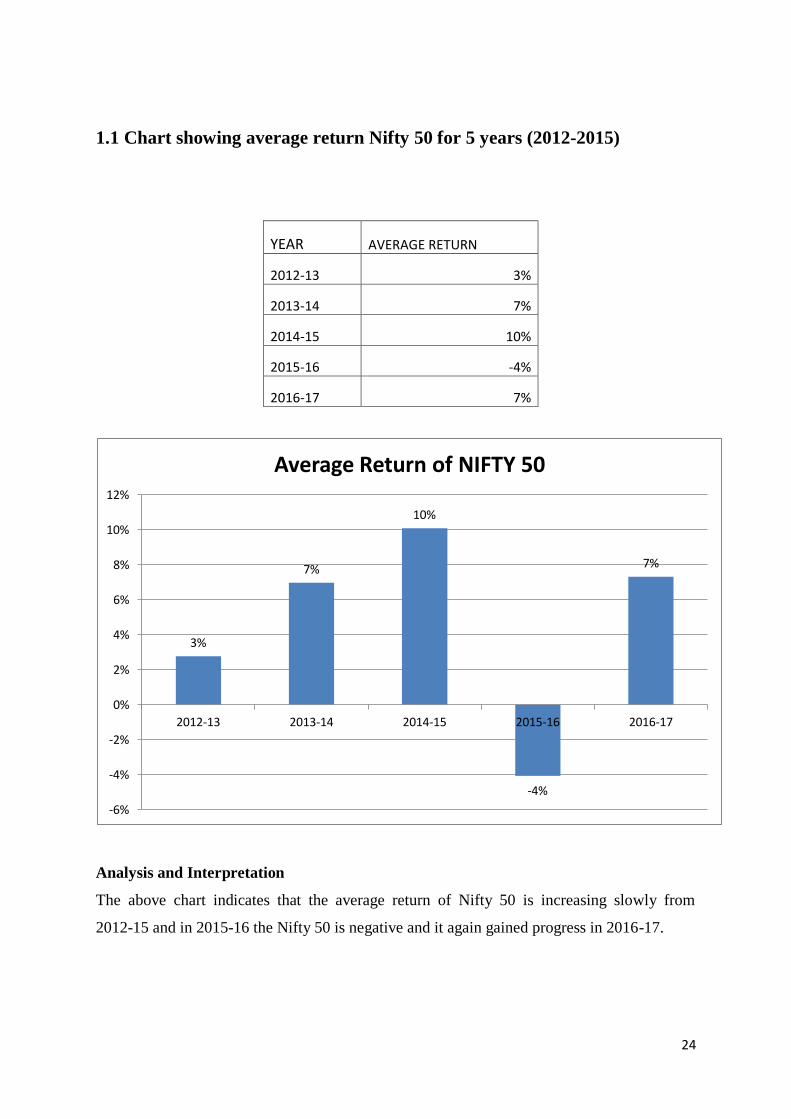

1.1 Chart showing average return Nifty 50 for 5 years (2012-2015)

YEAR AVERAGE RETURN

2012-13 3%

2013-14 7%

2014-15 10%

2015-16 -4%

2016-17 7%

Analysis and Interpretation

The above chart indicates that the average return of Nifty 50 is increasing slowly from

2012-15 and in 2015-16 the Nifty 50 is negative and it again gained progress in 2016-17.

3%

7%

10%

-4%

7%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2012-13 2013-14 2014-15 2015-16 2016-17

Average Return of NIFTY 50

25

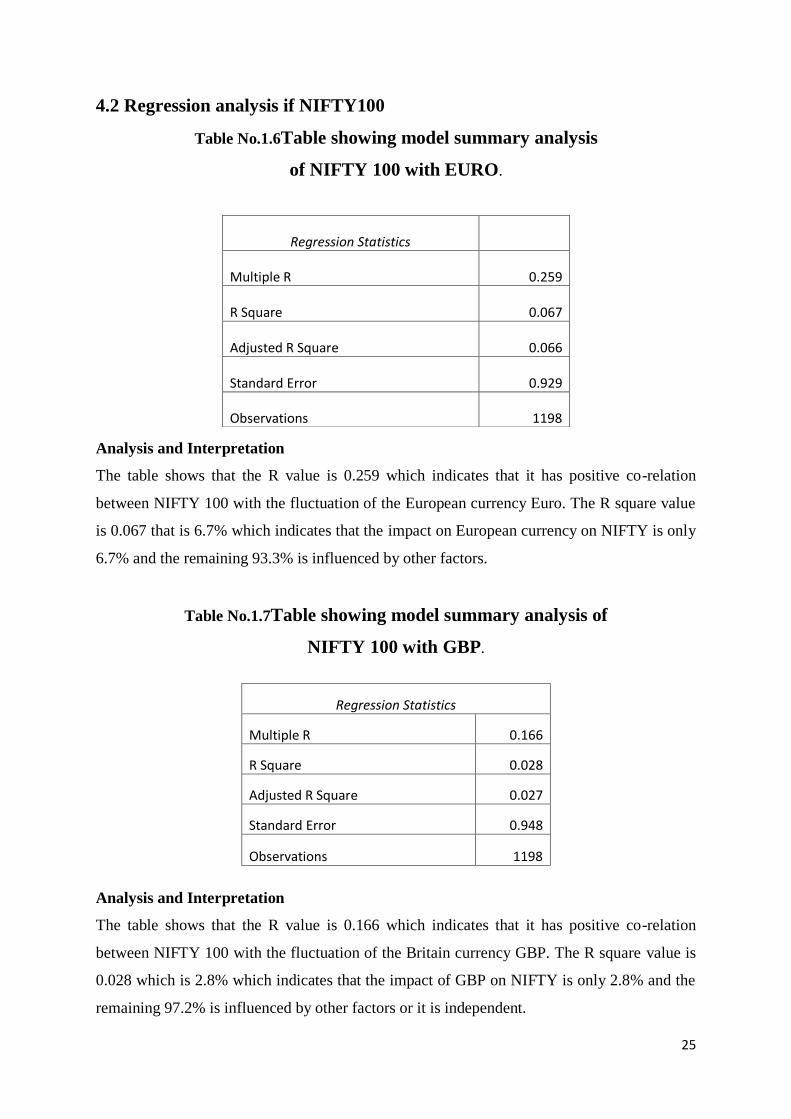

4.2 Regression analysis if NIFTY100

Table No.1.6Table showing model summary analysis

of NIFTY 100 with EURO.

Analysis and Interpretation

The table shows that the R value is 0.259 which indicates that it has positive co-relation

between NIFTY 100 with the fluctuation of the European currency Euro. The R square value

is 0.067 that is 6.7% which indicates that the impact on European currency on NIFTY is only

6.7% and the remaining 93.3% is influenced by other factors.

Table No.1.7Table showing model summary analysis of

NIFTY 100 with GBP.

Analysis and Interpretation

The table shows that the R value is 0.166 which indicates that it has positive co-relation

between NIFTY 100 with the fluctuation of the Britain currency GBP. The R square value is

0.028 which is 2.8% which indicates that the impact of GBP on NIFTY is only 2.8% and the

remaining 97.2% is influenced by other factors or it is independent.

Regression Statistics

Multiple R 0.259

R Square 0.067

Adjusted R Square 0.066

Standard Error 0.929

Observations 1198

Regression Statistics

Multiple R 0.166

R Square 0.028

Adjusted R Square 0.027

Standard Error 0.948

Observations 1198

26

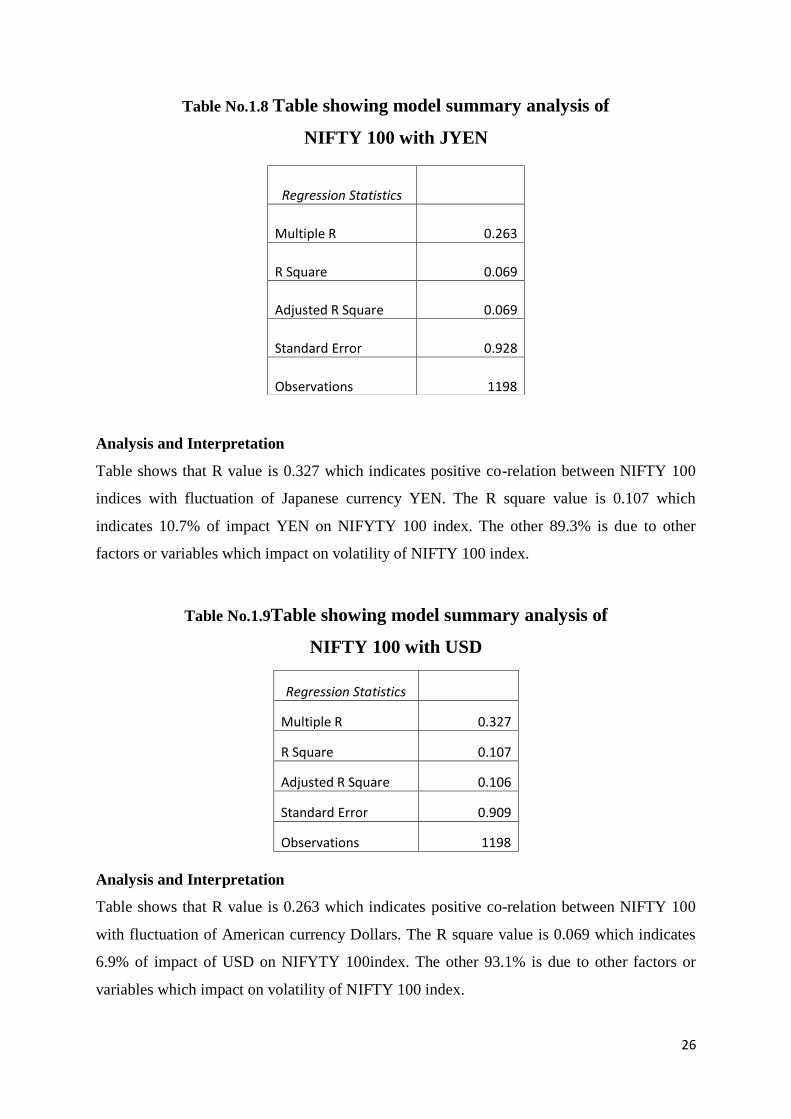

Table No.1.8 Table showing model summary analysis of

NIFTY 100 with JYEN

Analysis and Interpretation

Table shows that R value is 0.327 which indicates positive co-relation between NIFTY 100

indices with fluctuation of Japanese currency YEN. The R square value is 0.107 which

indicates 10.7% of impact YEN on NIFYTY 100 index. The other 89.3% is due to other

factors or variables which impact on volatility of NIFTY 100 index.

Table No.1.9Table showing model summary analysis of

NIFTY 100 with USD

Analysis and Interpretation

Table shows that R value is 0.263 which indicates positive co-relation between NIFTY 100

with fluctuation of American currency Dollars. The R square value is 0.069 which indicates

6.9% of impact of USD on NIFYTY 100index. The other 93.1% is due to other factors or

variables which impact on volatility of NIFTY 100 index.

Regression Statistics

Multiple R 0.263

R Square 0.069

Adjusted R Square 0.069

Standard Error 0.928

Observations 1198

Regression Statistics

Multiple R 0.327

R Square 0.107

Adjusted R Square 0.106

Standard Error 0.909

Observations 1198

27

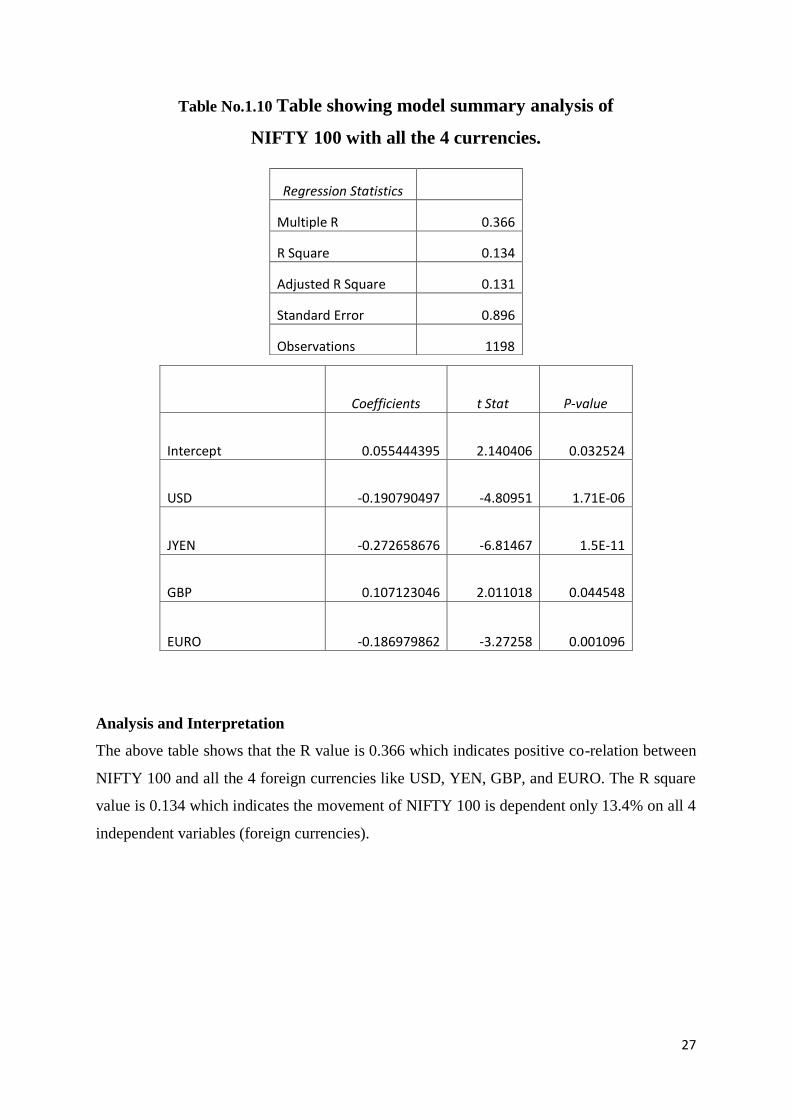

Table No.1.10 Table showing model summary analysis of

NIFTY 100 with all the 4 currencies.

Analysis and Interpretation

The above table shows that the R value is 0.366 which indicates positive co-relation between

NIFTY 100 and all the 4 foreign currencies like USD, YEN, GBP, and EURO. The R square

value is 0.134 which indicates the movement of NIFTY 100 is dependent only 13.4% on all 4

independent variables (foreign currencies).

Regression Statistics

Multiple R 0.366

R Square 0.134

Adjusted R Square 0.131

Standard Error 0.896

Observations 1198

Coefficients t Stat P-value

Intercept 0.055444395 2.140406 0.032524

USD -0.190790497 -4.80951 1.71E-06

JYEN -0.272658676 -6.81467 1.5E-11

GBP 0.107123046 2.011018 0.044548

EURO -0.186979862 -3.27258 0.001096

28

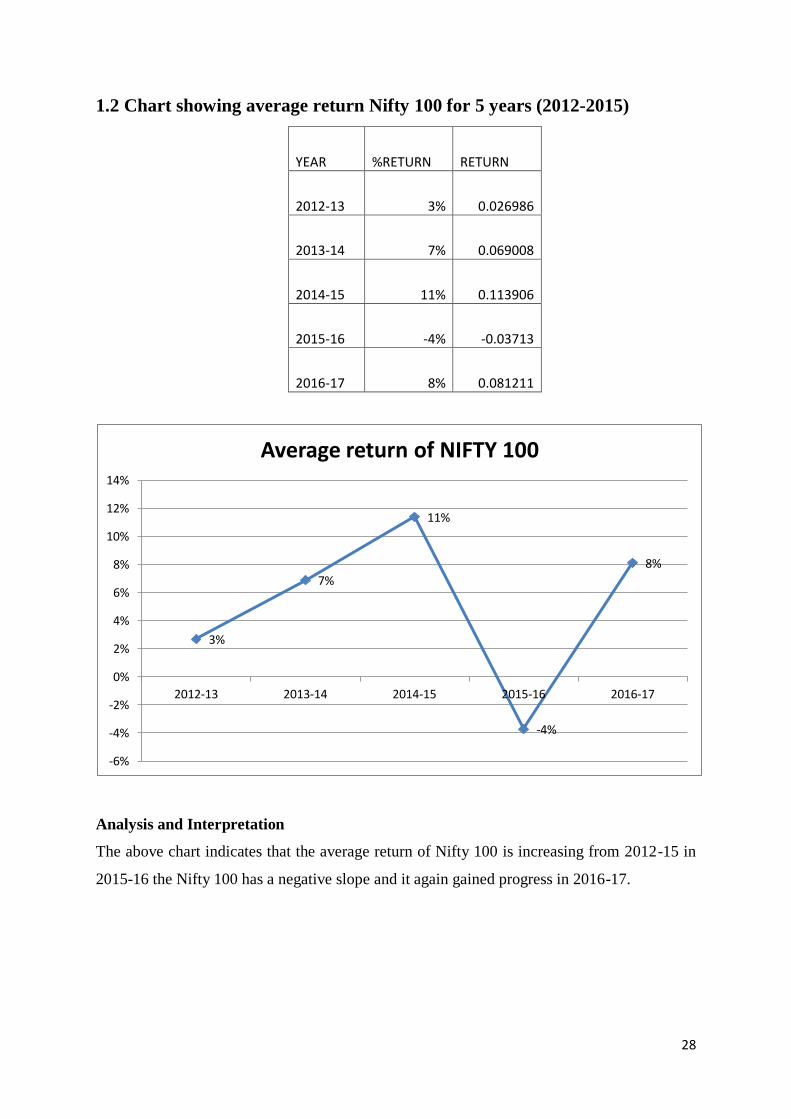

1.2 Chart showing average return Nifty 100 for 5 years (2012-2015)

YEAR %RETURN RETURN

2012-13 3% 0.026986

2013-14 7% 0.069008

2014-15 11% 0.113906

2015-16 -4% -0.03713

2016-17 8% 0.081211

Analysis and Interpretation

The above chart indicates that the average return of Nifty 100 is increasing from 2012-15 in

2015-16 the Nifty 100 has a negative slope and it again gained progress in 2016-17.

3%

7%

11%

-4%

8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2012-13 2013-14 2014-15 2015-16 2016-17

Average return of NIFTY 100

29

4.3 Regression analysis of NIFTY 200

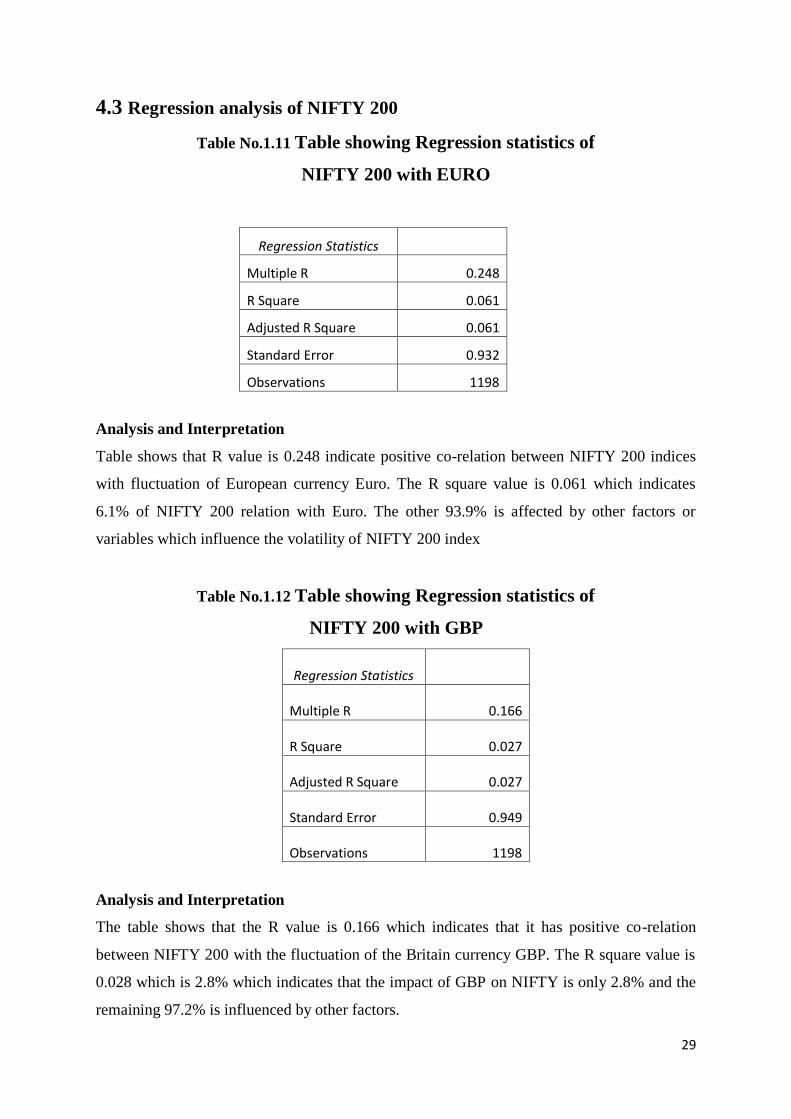

Table No.1.11 Table showing Regression statistics of

NIFTY 200 with EURO

Regression Statistics

Multiple R 0.248

R Square 0.061

Adjusted R Square 0.061

Standard Error 0.932

Observations 1198

Analysis and Interpretation

Table shows that R value is 0.248 indicate positive co-relation between NIFTY 200 indices

with fluctuation of European currency Euro. The R square value is 0.061 which indicates

6.1% of NIFTY 200 relation with Euro. The other 93.9% is affected by other factors or

variables which influence the volatility of NIFTY 200 index

Table No.1.12 Table showing Regression statistics of

NIFTY 200 with GBP

Regression Statistics

Multiple R 0.166

R Square 0.027

Adjusted R Square 0.027

Standard Error 0.949

Observations 1198

Analysis and Interpretation

The table shows that the R value is 0.166 which indicates that it has positive co-relation

between NIFTY 200 with the fluctuation of the Britain currency GBP. The R square value is

0.028 which is 2.8% which indicates that the impact of GBP on NIFTY is only 2.8% and the

remaining 97.2% is influenced by other factors.

30

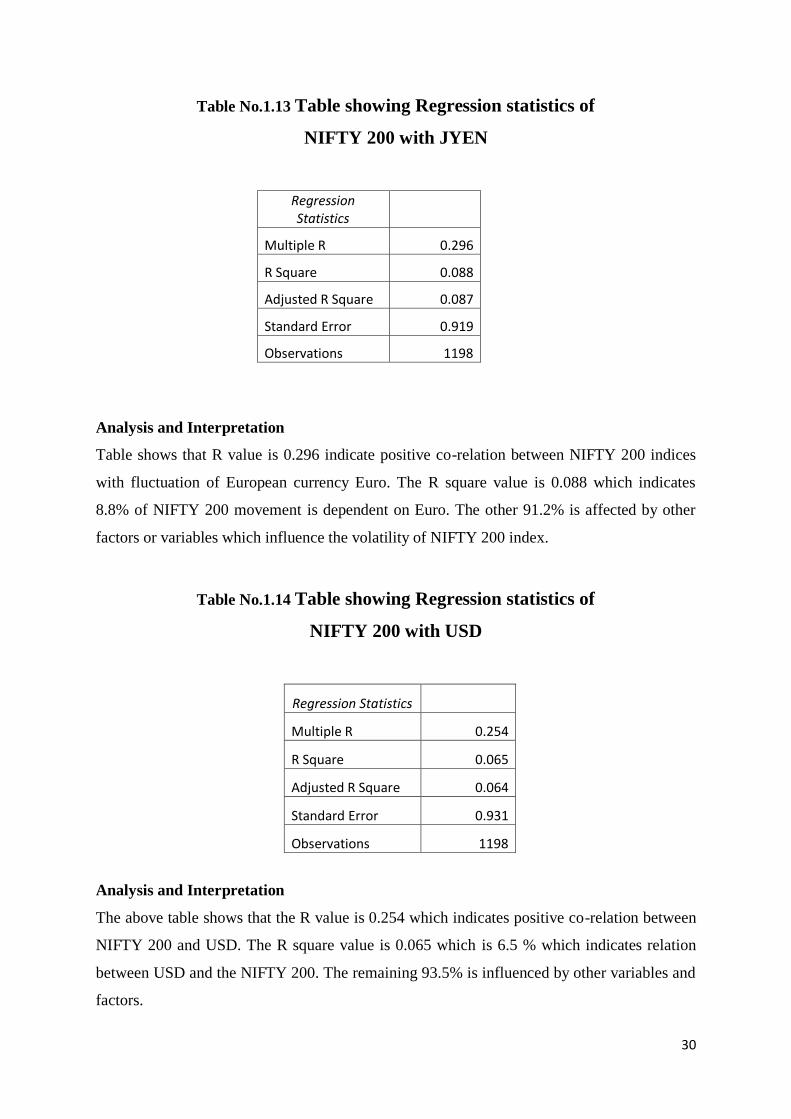

Table No.1.13 Table showing Regression statistics of

NIFTY 200 with JYEN

Regression Statistics

Multiple R 0.296

R Square 0.088

Adjusted R Square 0.087

Standard Error 0.919

Observations 1198

Analysis and Interpretation

Table shows that R value is 0.296 indicate positive co-relation between NIFTY 200 indices

with fluctuation of European currency Euro. The R square value is 0.088 which indicates

8.8% of NIFTY 200 movement is dependent on Euro. The other 91.2% is affected by other

factors or variables which influence the volatility of NIFTY 200 index.

Table No.1.14 Table showing Regression statistics of

NIFTY 200 with USD

Regression Statistics

Multiple R 0.254

R Square 0.065

Adjusted R Square 0.064

Standard Error 0.931

Observations 1198

Analysis and Interpretation

The above table shows that the R value is 0.254 which indicates positive co-relation between

NIFTY 200 and USD. The R square value is 0.065 which is 6.5 % which indicates relation

between USD and the NIFTY 200. The remaining 93.5% is influenced by other variables and

factors.

31

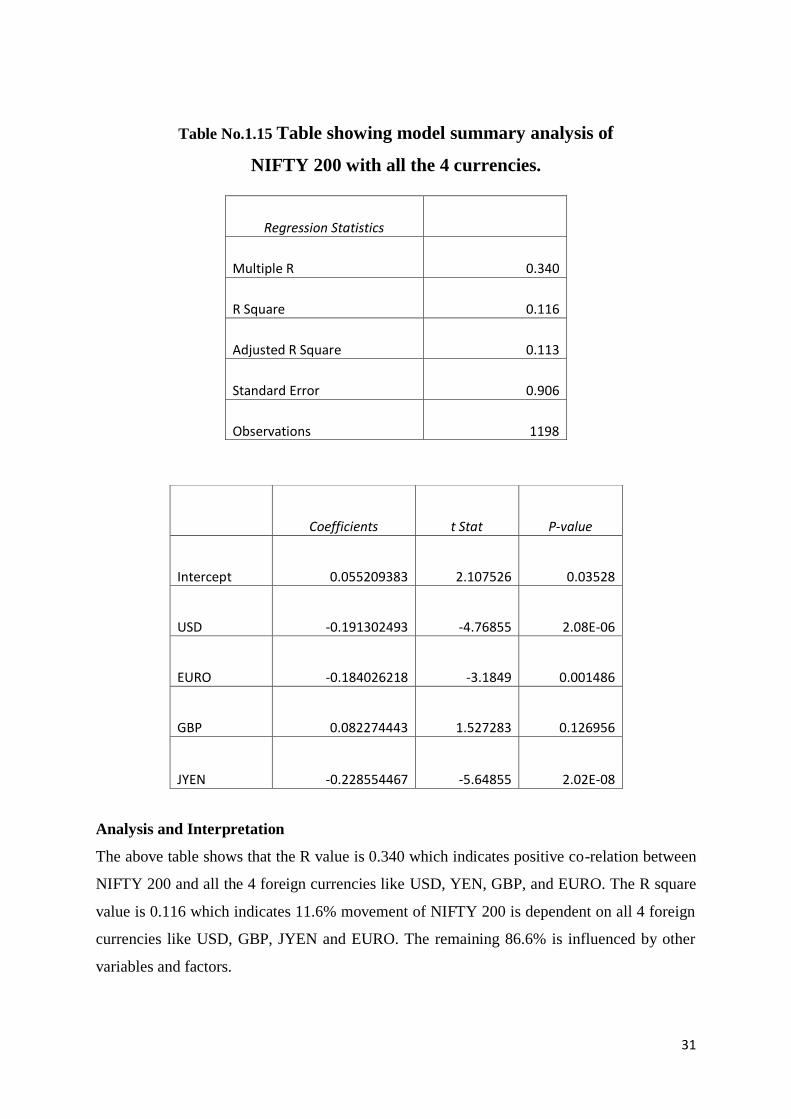

Table No.1.15 Table showing model summary analysis of

NIFTY 200 with all the 4 currencies.

Analysis and Interpretation

The above table shows that the R value is 0.340 which indicates positive co-relation between

NIFTY 200 and all the 4 foreign currencies like USD, YEN, GBP, and EURO. The R square

value is 0.116 which indicates 11.6% movement of NIFTY 200 is dependent on all 4 foreign

currencies like USD, GBP, JYEN and EURO. The remaining 86.6% is influenced by other

variables and factors.

Regression Statistics

Multiple R 0.340

R Square 0.116

Adjusted R Square 0.113

Standard Error 0.906

Observations 1198

Coefficients t Stat P-value

Intercept 0.055209383 2.107526 0.03528

USD -0.191302493 -4.76855 2.08E-06

EURO -0.184026218 -3.1849 0.001486

GBP 0.082274443 1.527283 0.126956

JYEN -0.228554467 -5.64855 2.02E-08

32

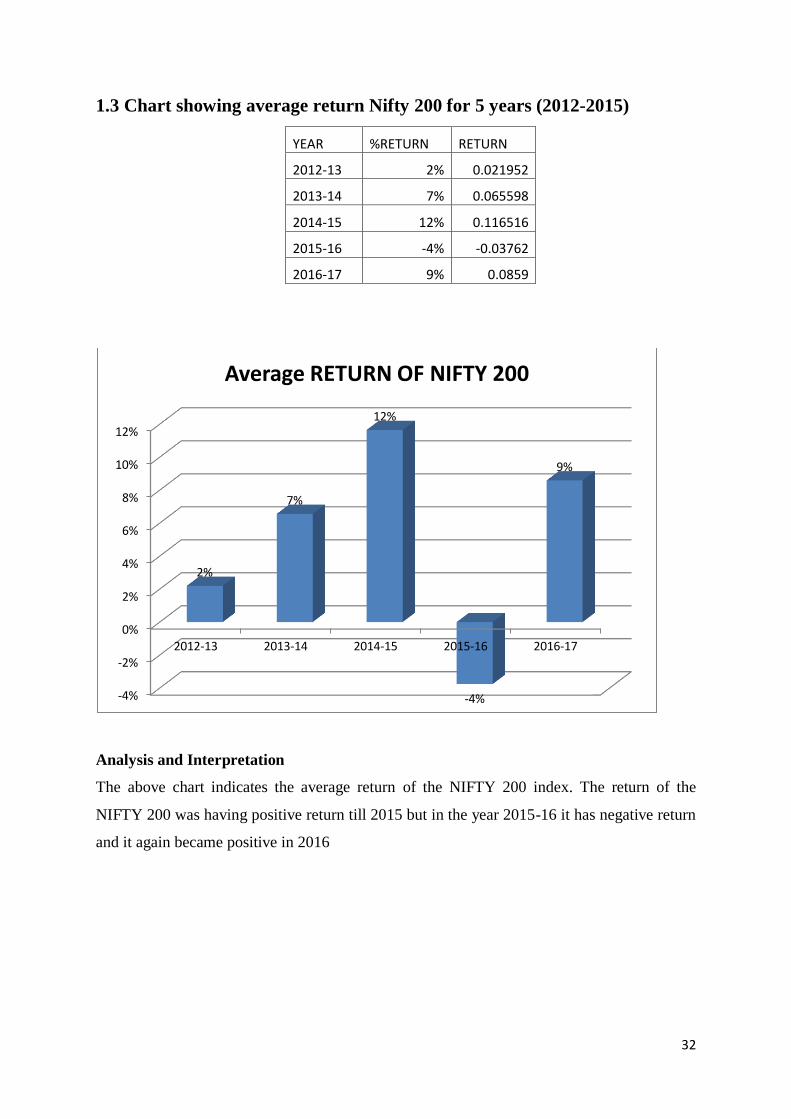

1.3 Chart showing average return Nifty 200 for 5 years (2012-2015)

YEAR %RETURN RETURN

2012-13 2% 0.021952

2013-14 7% 0.065598

2014-15 12% 0.116516

2015-16 -4% -0.03762

2016-17 9% 0.0859

Analysis and Interpretation

The above chart indicates the average return of the NIFTY 200 index. The return of the

NIFTY 200 was having positive return till 2015 but in the year 2015-16 it has negative return

and it again became positive in 2016

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2012-13 2013-14 2014-15 2015-16 2016-17

2%

7%

12%

-4%

9%

Average RETURN OF NIFTY 200

33

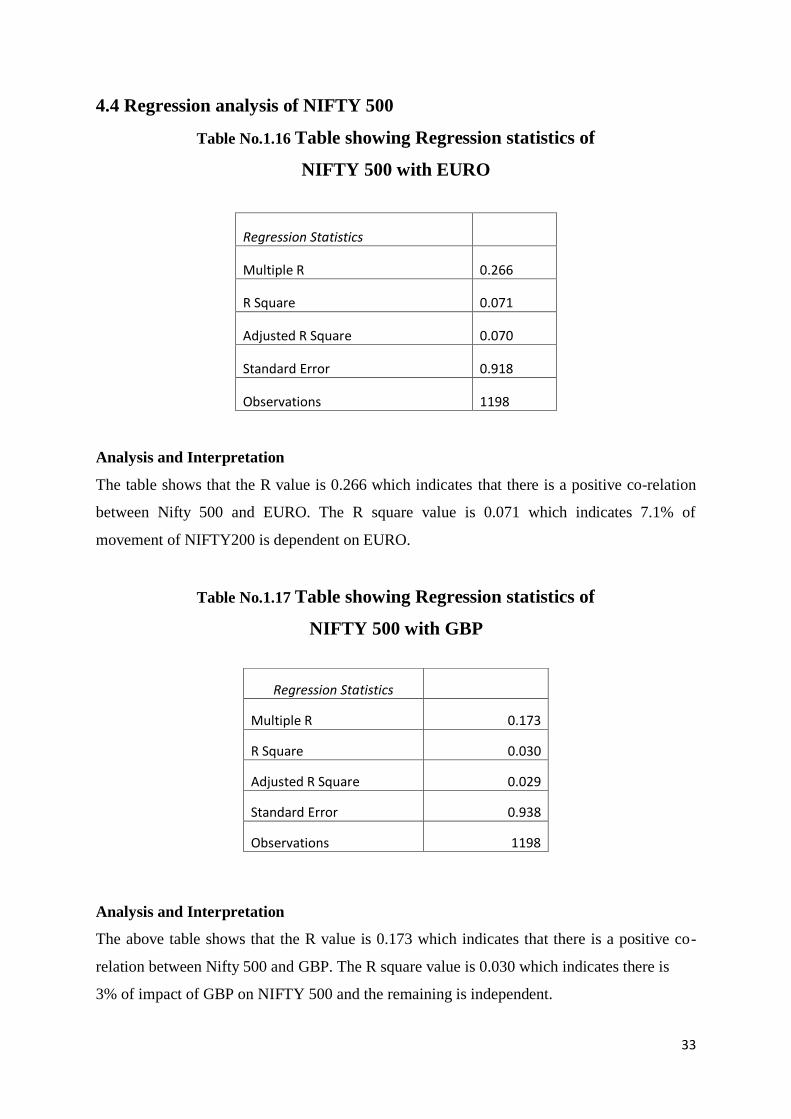

4.4 Regression analysis of NIFTY 500

Table No.1.16 Table showing Regression statistics of

NIFTY 500 with EURO

Analysis and Interpretation

The table shows that the R value is 0.266 which indicates that there is a positive co-relation

between Nifty 500 and EURO. The R square value is 0.071 which indicates 7.1% of

movement of NIFTY200 is dependent on EURO.

Table No.1.17 Table showing Regression statistics of

NIFTY 500 with GBP

Analysis and Interpretation

The above table shows that the R value is 0.173 which indicates that there is a positive co-

relation between Nifty 500 and GBP. The R square value is 0.030 which indicates there is

3% of impact of GBP on NIFTY 500 and the remaining is independent.

Regression Statistics

Multiple R 0.266

R Square 0.071

Adjusted R Square 0.070

Standard Error 0.918

Observations 1198

Regression Statistics

Multiple R 0.173

R Square 0.030

Adjusted R Square 0.029

Standard Error 0.938

Observations 1198

34

Table No.1.18 Table showing Regression statistics of

NIFTY 500 with JYEN.

Analysis and Interpretation

Table shows that R value is 0.330 indicate positive co-relation between NIFTY 500 indices

with fluctuation of YEN. The R square value is 0.109 which indicates 10.9% of NIFTY 500

movement is dependent with YEN. The other 89.1% is affected by other factors or variables

which influence the volatility of NIFTY 500 index.

Table No.1.19 Table showing Regression statistics of

NIFTY 500 with USD.

Regression Statistics

Multiple R 0.266

R Square 0.071

Adjusted R Square 0.070

Standard Error 0.918

Observations 1198

Analysis and Interpretation

The above table shows that the R value is 0.266 which indicates positive co-relation between

NIFTY 500 and USD. The R square value is 0.071 which is 7.1 % which indicates relation

between USD and the NIFTY 500. The remaining 92.9% is influenced by other variables and

factors.

Regression Statistics

Multiple R 0.330

R Square 0.109

Adjusted R Square 0.108

Standard Error 0.899

Observations 1198

35

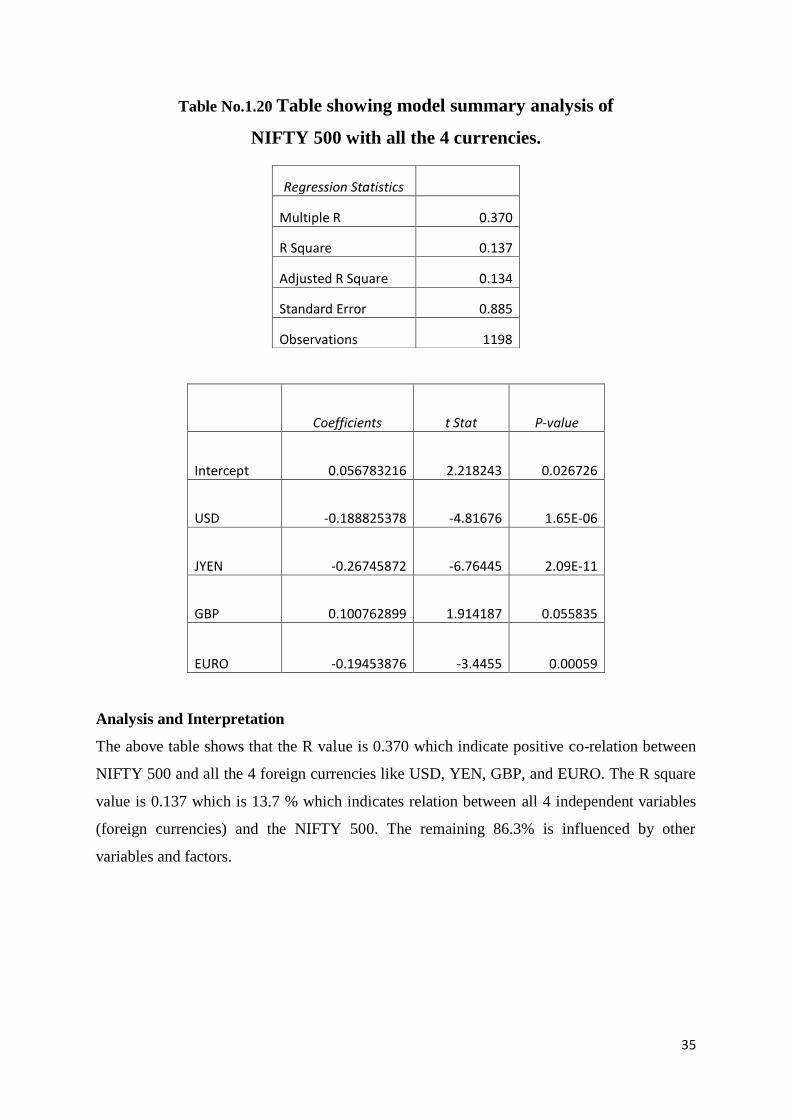

Table No.1.20 Table showing model summary analysis of

NIFTY 500 with all the 4 currencies.

Analysis and Interpretation

The above table shows that the R value is 0.370 which indicate positive co-relation between

NIFTY 500 and all the 4 foreign currencies like USD, YEN, GBP, and EURO. The R square

value is 0.137 which is 13.7 % which indicates relation between all 4 independent variables

(foreign currencies) and the NIFTY 500. The remaining 86.3% is influenced by other

variables and factors.

Regression Statistics

Multiple R 0.370

R Square 0.137

Adjusted R Square 0.134

Standard Error 0.885

Observations 1198

Coefficients t Stat P-value

Intercept 0.056783216 2.218243 0.026726

USD -0.188825378 -4.81676 1.65E-06

JYEN -0.26745872 -6.76445 2.09E-11

GBP 0.100762899 1.914187 0.055835

EURO -0.19453876 -3.4455 0.00059

36

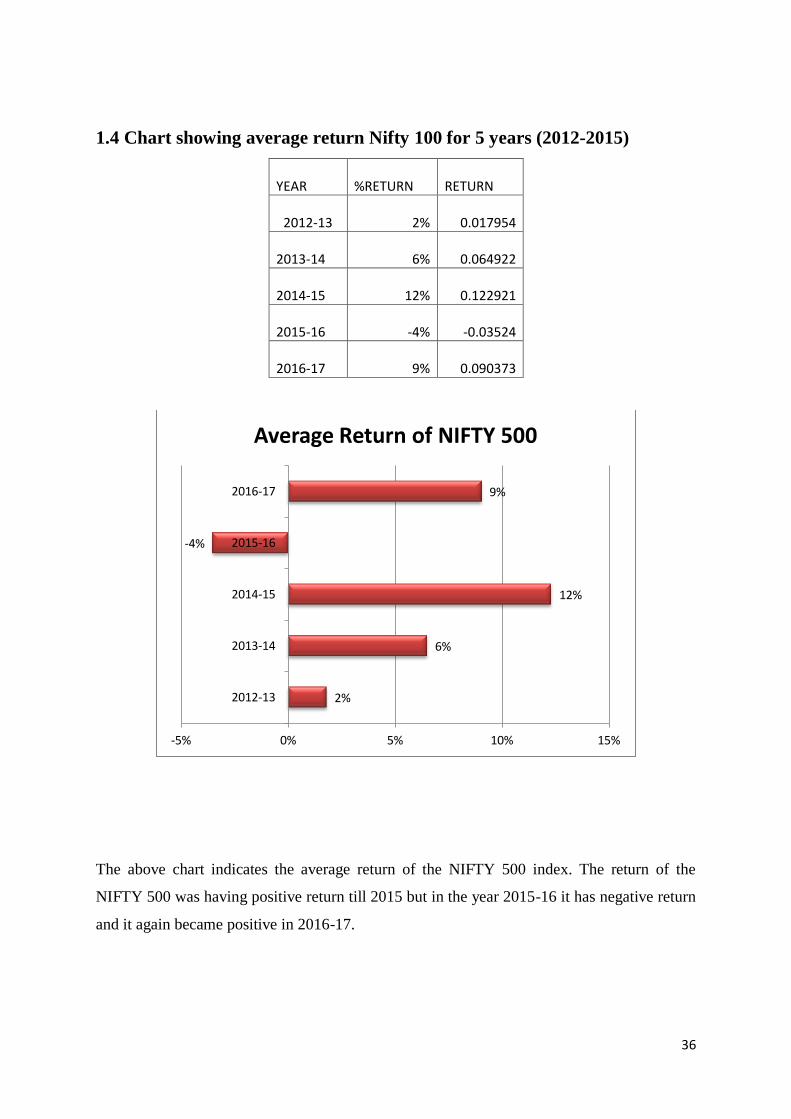

1.4 Chart showing average return Nifty 100 for 5 years (2012-2015)

YEAR %RETURN RETURN

2012-13 2% 0.017954

2013-14 6% 0.064922

2014-15 12% 0.122921

2015-16 -4% -0.03524

2016-17 9% 0.090373

The above chart indicates the average return of the NIFTY 500 index. The return of the

NIFTY 500 was having positive return till 2015 but in the year 2015-16 it has negative return

and it again became positive in 2016-17.

2%

6%

12%

-4%

9%

-5% 0% 5% 10% 15%

2012-13

2013-14

2014-15

2015-16

2016-17

Average Return of NIFTY 500

37

4.5 Regression analysis of NIFTY NEXT 50

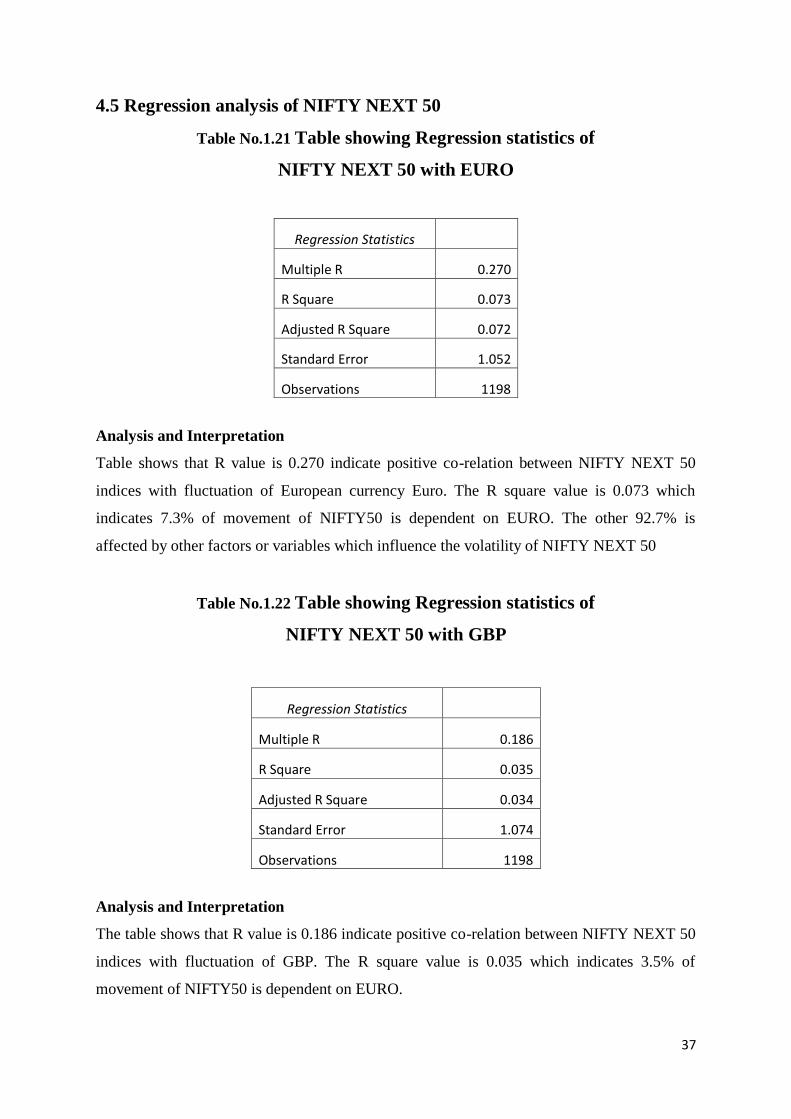

Table No.1.21 Table showing Regression statistics of

NIFTY NEXT 50 with EURO

Regression Statistics

Multiple R 0.270

R Square 0.073

Adjusted R Square 0.072

Standard Error 1.052

Observations 1198

Analysis and Interpretation

Table shows that R value is 0.270 indicate positive co-relation between NIFTY NEXT 50

indices with fluctuation of European currency Euro. The R square value is 0.073 which

indicates 7.3% of movement of NIFTY50 is dependent on EURO. The other 92.7% is

affected by other factors or variables which influence the volatility of NIFTY NEXT 50

Table No.1.22 Table showing Regression statistics of

NIFTY NEXT 50 with GBP

Regression Statistics

Multiple R 0.186

R Square 0.035

Adjusted R Square 0.034

Standard Error 1.074

Observations 1198

Analysis and Interpretation

The table shows that R value is 0.186 indicate positive co-relation between NIFTY NEXT 50

indices with fluctuation of GBP. The R square value is 0.035 which indicates 3.5% of

movement of NIFTY50 is dependent on EURO.

38

Table No.1.23 Table showing Regression statistics of

NIFTY NEXT 50 with JYEN

Analysis and Interpretation

Table shows that R value is 0.304 indicate positive co-relation between NIFTY NEXT 50

indices with fluctuation of Japanese currency JYEN. The R square value is 0.092 which

indicates 9.2% of movement of NIFTY50 is dependent on JYEN. The other 90.8% is affected

by other factors or variables which influence the volatility of NIFTY NEXT 50

Table No.1.24 Table showing Regression statistics of

NIFTY NEXT 50 with USD

Analysis and Interpretation

Table shows that R value is 0.252 indicate positive co-relation between NIFTY NEXT 50

indices with fluctuation of US Dollars. The R square value is 0.063 which indicates 6.3% of

movement of NIFTY50 is dependent on USD. The other 93.7% is affected by other factors or

variables which influence the volatility of NIFTY NEXT 50

Regression Statistics

Multiple R 0.304

R Square 0.092

Adjusted R Square 0.092

Standard Error 1.041

Observations 1198

Regression Statistics

Multiple R 0.252

R Square 0.063

Adjusted R Square 0.063

Standard Error 1.058

Observations 1198

39

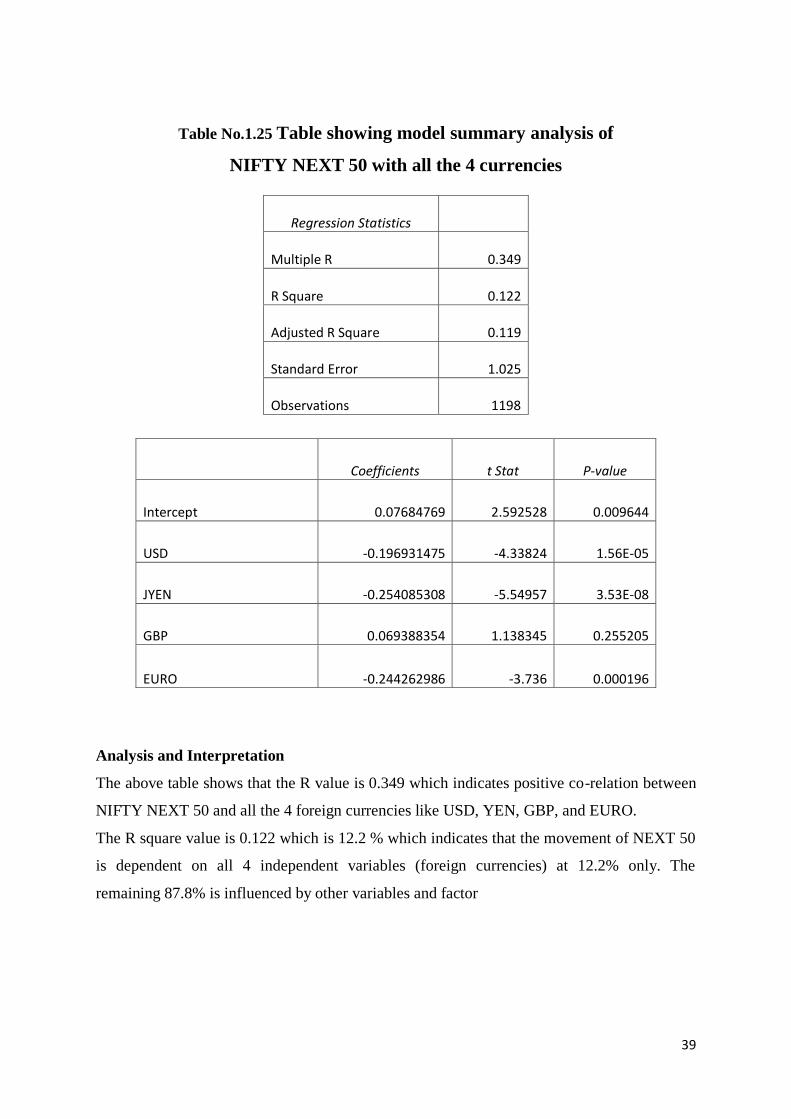

Table No.1.25 Table showing model summary analysis of

NIFTY NEXT 50 with all the 4 currencies

Analysis and Interpretation

The above table shows that the R value is 0.349 which indicates positive co-relation between

NIFTY NEXT 50 and all the 4 foreign currencies like USD, YEN, GBP, and EURO.

The R square value is 0.122 which is 12.2 % which indicates that the movement of NEXT 50

is dependent on all 4 independent variables (foreign currencies) at 12.2% only. The

remaining 87.8% is influenced by other variables and factor

Regression Statistics

Multiple R 0.349

R Square 0.122

Adjusted R Square 0.119

Standard Error 1.025

Observations 1198

Coefficients t Stat P-value

Intercept 0.07684769 2.592528 0.009644

USD -0.196931475 -4.33824 1.56E-05

JYEN -0.254085308 -5.54957 3.53E-08

GBP 0.069388354 1.138345 0.255205

EURO -0.244262986 -3.736 0.000196

40

1.5 Chart showing average return Nifty Next 50 for 5 years (2012-2015)

Analysis and Interpretation

The above chart indicates the average return of the NIFTY 500 index. The return of the

NIFTY 500 was having positive return till 2015 but in the year 2015-16 it has negative return

and it again became positive in 2016-17.

2%

7%

16%

-1%

12%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2012-13 2013-14 2014-15 2015-16 2016-17

Average Return NIFTY NEXT 50 RETURN

YEAR %RETURN RETURN

2012-13 2% 0.024797

2013-14 7% 0.066889

2014-15 16% 0.158443

2015-16 -1% -0.01499

2016-17 12% 0.12424

41

CHAPTER 5

SUMMARY OF FINDINGS, SUGGESTIONS AND CONCLUSION

SUMMARY OF FINDINGS

From the examination it is discovered that, the co-effective of INR_USD, INR_GBP,

INR_EURO, and INR_JYEN were discovered insignificant for all the chosen stock

indices of National Stock Exchange (NSE). The above statements disclose that as per

above estimations of study it clearly indicates that there is no Influence of FOREIGN

CURRENCY fluctuation on the Indian Stocks Market.

From the above amalgamated regression table we effortlessly found that the effect of

foreign currency volatility does not influence the not even a single NSE stock index in

the course of 5 years. The 5 NSE indices for example, nifty50, nifty100, nifty200,

nifty 500, nifty next 50 with the examination of four principle Exchange rates in

connection to INR, for example, USD, GBP, EURO and JYEN individually were

altogether observed to be significant so we can easily analyse that foreign currency

fluctuation will won't influence the Indian stock market.

The co-relation of all the 4 currencies for NIFTY50 is 0.362 which indicates that there

is no much movement of NIFTY50 due to foreign currency fluctuation

The co-relation of all the 4 currencies for NIFTY 100 is 0.366 which indicates there is

positive correlation and for NIFTY 200 is 0.340, nifty 500 and nifty next50 is 0.370

and 0.349 respectively.

From the above analysis only NIFTY next 50 is affected to the most as it has a

positive correlation of 0.370. It is because it contains only few stocks, hence it is

affected the most than any other.

From all the most significant than 4 currencies only GBP has a positive coefficient

which states that GBP price are the most significant than EURO, JYEN and USD.

42

From the above return analysis of the NSE indices it is found that the return of all the

indices is negative in the year 2015-16 due to impact of various other factors other

than foreign currency fluctuation.

The average return of the NIFTY indices indicated the state of economy of the

country as most of the top companies are under the NIFTY index and hence it can be

found that it has a positive growth from 2012-2015 but in 2015-16 it has a negative

growth due to various reasons.

SUGGESTIONS

As indicated by the above investigation in the wake of all the pertinent approaches and its

examination clearly tells that foreign currency fluctuation does not influence the Stock

market of India. Since there was no effect of volatility of exchange rates to Indian capital

market/securities exchange of India. We can give important exhortation to the general

population who are keen on making investment in stock market, we will recommend to all the

investors while they are investing, if there is volatility in the exchange rates it won't impact

the Stock market. So don't consider foreign currency volatility as an important factor as factor

to invest in Indian securities exchange.

As the currency fluctuations do not influence the Indian stock market, the investors can also

go for FOREX trade separately. This includes trading of currencies were the currency of one

nation is traded or exchanged for a value with another nation currency. The investor can also

make gains through FOREX trade.

CONCLUSION

Under this examination we can undoubtedly comprehend that foreign currency fluctuation

doesn't influence money markets. According to the regression analysis carried out we found

that fluctuation of trade rates against INR, for example, USD, GBP, EURO and JYEN

separately. These don't have any effect on the Indian securities exchange in the course of the

last 5years. So Investors while making interest in the share trading system don't consider the

foreign currency fluctuation as a factor of budgetary pointer or instrument.

43

The examination covers important indices of the NSE and it can be used for taking decisions.

There are lot other stocks or indices which might be affected by the foreign currency

fluctuation but most of the top rated companies which are under NSE indices are included in

NIFTY.

From the above amalgamated regression table we effortlessly found that the effect of foreign

currency volatility does not influence the not even a single NSE stock index in the course of 5

years. The 5 NSE indices for example, nifty50, nifty100, nifty200, nifty 500, nifty next 50

with the examination of four principle Exchange rates in connection to INR, for example,

USD, GBP, EURO and JYEN individually were altogether observed to be significant so we

can easily analyse that foreign currency fluctuation will won't influence the Indian stock

market.

44

BIBLIOGRAPHY

Iqbal, J., & Haider, A. (2005). Arbitrage Pricing Theory: Evidence from an Emerging Stock

Market. The Lahore Journal of Economics, 10,123-139

Maysami, R., & Koh, T. (2000). A Vector Error Correction Model of the Singapore Stock

Market. International Review of Economics and Finance, 9:1, 79-96.

Seifert, B. (1992). Volatility of exchange rates, interest rates, and stock returns. Journal of

Multinational Financial Management, 2, 1-19.

Ajayi, R. A., & Mougoue, M. (1996). On the dynamic relation between stock prices and

Exchange Rates. Journal of Financial Research, 19 , 193-207.

V.Murinde, & Abdalla, I. S. (1997). Exchange rate and stock price interactions in emerging

financial markets: Evidence on India, Korea, Pakistan and the Philippines. Applied Financial

Economics, 25-35.

Pethe, A., & Karnik, A. (2000). Do Indian Stock Markets matter? Stock Market Indices and

Macro Economic Variables. Economic and Political Weekly, 35: 5, 349-356.

Morley, B., & Pentecost, E. (2000). Common Trends and Cycles in G-7 Countries Exchange

Rates and Stock Prices. Applied Economic Letters, 7, 7-10.

Ozair, A. (2006). Causality Between Stock prices and Exchange Rates: A Case of The United

States. Florida Atlantic University, Master of Science Thesis.

Vygodina, A. V. (2006). Effects of size and international exposure of the US firms on the

realtionship between stock prices and exchange rates. Global Finance Journal, 17, 214-223.

Takeshi, I. (2008, November). The causal relationships in mean and variance between stock

returns and Foreign institutional investment in India. IDE Paper Discussion, No. 180.

Stone(2009). Using financial prices to test exchange rate models: A note. Journal of Finance,

42 (1), pp. 141-149.

Allayannis, G., G. Brown, and L. Klapper, 2003, Capital structure and financial risk:

Evidence from foreign debt use in East Asia, Journal of Finance, 58, 2667- 2709.

Allayannis, G., and O. Ofek, 2001, Exchange rate exposure, hedging, and the use of foreign

currency derivatives, Journal of International Money and Finance 20, 273296

Edwards, S., and R., Susmel, 2001, Volatility dependence and contagion in emerging equity

markets, Journal of Development Economics, 66, 505-532.

Edwards, S., J., Biscarri, and P., Gracia, 2003, Stock market cycles, financial liberalization

and volatility, Journal of International Money and Finance, 22, 925955.

Huang, B.N., and C.W., Yang, 2000, The impact of financial liberalization on stock price

volatility in emerging markets, Journal of Comparative Economics 28, 321-339.

45

Jayasuriya, S., 2005, Stock market liberalization and volatility in the presence of favorable

market characteristics and institutions, Emerging Markets Review 6, 170191.

Bekaert, G., and C., Harvey, 2003, Emerging Markets Finance, Journal of Empirical Finance

10, 3-55.

Bénassy-Quéré A., L., Fontagné, and A., Lahreche-Revil 2001, Exchange Rate Strategies in

the Competition for Attracting Foreign Direct Investment, Journal of the Japanese and

International Economies 15, 178-198.

Mishra K.A (2004) Stock market and foreign Exchange market in India. Are they related?

South Asia Economic Journal, 5:2, Sage Publications, New Delhi.

Solnik, B. (1987). Using financial prices to test exchange rate models- A note. Journal of

Finance, 42, 141-149.

Benita, G., and B. Lauterbach. (2004), Policy Factors and Exchange Rate Volatility: Panel

Data Verses a Specific Country Analysis,Research Unit, Foreign Exchange Activity

Department, Bank of Israel, Jerusalem.

Mishkin, F. S (2001). The Economics of Money, Banking and Financial Markets. New York:

Addison Wesley.

Schnabl, G. (2007). Exchange Rate Volatility and Growth in Small Open economies at the

EMI Periphery. ECB Working Paper, No.773.

N.dri. Konan, L. (2008) “The Effects of Interest Rates Volatility on Stock Returns and

Volatility: Evidence from Korea”, International Research Journal of Finance and

Economics, Issue 14, 285-290

Engle, R.F and J.G.Rangel (2005) The SPLINE GARCH model for unconditional volatility

and its global microeconomic causes, Mimeo, presented at the world congress of the

Econometric Society, London August, 2005

Rizwan, M.F and Khan, S. U. (2007). “Stock Return Volatility in Emerging Equity Market

(Kse): The Relative Effects of Country and Global Factors”, International Review of

Business Research Papers, Vol.3, No.2, pp. 362 – 375

Schwert, W. (1990), Stock Returns and Real Activity: A Century of Evidence, Journal of

Finance, 45, pp.1237-1257.

. Mao, C. K. G., and W. Kao. (1990), On Exchange Rate Changes and Stock Price Reactions,

Journal of Business Finance and Accounting, 17 (3), pp.441-449.

Donnelly, R., and E. Sheeby. (1996), The Share Price Reaction of UK Exporters to Exchange

Rate Movements: An Empirical Study, Journal of International Business Studies, 27(1): 157–

65.

Adjasi, C. K.D., and B.N. Biekpe. (2005), Stock Market Returns and Exchange Rate