Your State Association Presents Demystifying the New Liquidity Requirements Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the broadcast. Be sure to print enough copies for all listeners. Friday, February 27, 2015 Presenters: Colette Wagner & Philip Stalcup Technical Support (for faster service please submit inquiries via email or online): (Registration & Tech Support): Email- [email protected], Phone- (877)988-7526 FOR ADDITIONAL ASSISTANCE PLEASE REFER TO OUR FAQs

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Your State Association Presents

Demystifying the New Liquidity Requirements

Program Materials

Use this document to follow along with the live webinar

presentation. Please test your system before the broadcast.

Be sure to print enough copies for all listeners.

Friday, February 27, 2015 Presenters: Colette Wagner

& Philip Stalcup

Technical Support (for faster service please submit inquiries via email or online): (Registration & Tech Support): Email- [email protected], Phone- (877)988-7526 FOR ADDITIONAL ASSISTANCE PLEASE REFER TO OUR FAQs

1

Demystifying the New Liquidity Requirements

Course Agenda:

Liquidity Risk Management

BCBS (“Basel”) Liquidity Framework Overview

New Terminology Explained

Liquidity Coverage Ratio (LCR)

High Quality Liquid Assets (HQLA)

Net Stable Funding Ratio (NSFR)

Applicability of New Regulatory Guidance for Liquidity

Liquidity Governance Concepts

Liquidity Contingency Funding Plans

2

Liquidity Contingency Funding Plans

Liquidity Monitoring and Stress Testing

Liquidity Buffers

Tips for What You Can Do Next

2

Liquidity

Basel Guidance, 2008:

Liquidity is the ability of a bank to fund increases in assets and meet q y yobligations as they come due, without incurring unacceptable losses

Interagency Guidance, 2010

Liquidity is a financial institution’s capacity to meet its cash and collateral obligations at a reasonable cost. Maintaining an adequate level of liquidity depends on the institution’s ability to efficiently meet both expected and unexpected cash flows and collateral needs without adversely affecting either d il ti th fi i l diti f th i tit ti

3

daily operations or the financial condition of the institution.

In the 2007 crisis, many financial institutions did not:

Have an adequate framework to account for liquidity risks posed by individual products and business lines – business incentives were not

li d ith ll i k t laligned with overall risk tolerance

Consider the amount of liquidity they might need to satisfy contingent obligations as they viewed funding of these obligations to be highly unlikely

View severe and prolonged liquidity disruptions as plausible, and did not conduct stress tests that considered the possibility of market wide strain or the severity or duration of the disruptions.

Contingency funding plans (CFPs) were not always appropriately linked to

4

Contingency funding plans (CFPs) were not always appropriately linked to stress test results and sometimes failed to take account of the potential closure of some funding sources.

3

Liquidity Risk Management

Basel 2008

Liquidity risk management is important for every financial institution, because a liquidity shortfall at a single institution can have system-wide repercussions.

Financial market developments in the past decade have increased the complexity of liquidity risk and its management.

Interagency Guidance 2010

Liquidity risk is the risk that an institution’s financial condition or overall safety and soundness is adversely affected by an inability (or perceived inability) to meet its obligations.

Changes in economic conditions or exposure to credit market operation

5

Changes in economic conditions or exposure to credit, market, operation, legal, and reputation risks also can affect an institution’s liquidity risk profile and should be considered in the assessment of liquidity and asset/liability management.

Because of the critical importance to the viability of the institution, liquidity risk management should be fully integrated into the institution’s risk management processes.

Basel Committee on Banking Supervision

Liquidity Framework Overview

6

4

BCBS updated BCBS updated guidance forguidance forguidance for guidance for liquidity risk liquidity risk management after management after the 2007 liquidity the 2007 liquidity crisis, realizing that crisis, realizing that previous guidance previous guidance (2000) was not (2000) was not sufficient.sufficient.

7

www.bis.org/publ/bcbs144.htm

Built on 17 principles for managing and supervising liquidity risk

Principles for Sound Liquidity Risk Management (Basel)Principle 1 (Fundamental principle):

A bank is responsible for the sound management of liquidity risk. A bank h ld t bli h b t li idit i k t f k th t it

Remaining Principles

should establish a robust liquidity risk management framework that ensures it maintains sufficient liquidity, including a cushion of unencumbered, high quality liquid assets, to withstand a range of stress events, including those involving the loss or impairment of both unsecured and secured funding sources. Supervisors should assess the adequacy of both a bank's liquidity risk management framework and its liquidity position and should take prompt action if a bank is deficient in either area in order to protect depositors and to limit potential damage to the financial system.

8

Remaining Principles

Principles 2 - 4 Governance of Liquidity Risk Management

Principles 5 – 12 Measurement and Management of Liquidity Risk

Principle 13 Public Disclosure

Principles 14 – 17 Role of Supervisors

5

Principles 2, 3, & 4: Governance

2. Articulate risk tolerance

3. Develop strategy, policy and procedures and monitor continuouslyp gy p y p y

4. Assess liquidity costs and benefits for all activities and lines of business

Liquidity Liquidity risk tolerance, which risk tolerance, which should define should define the level of the level of liquidity risk that the bank is willing to assume, liquidity risk that the bank is willing to assume, should be set should be set considering business considering business objectivesobjectives, strategic , strategic direction and direction and overall risk appetite. overall risk appetite.

The The tolerance should ensure that the tolerance should ensure that the firm manages firm manages its its liquidity strongly in normal times in such a way that it is able liquidity strongly in normal times in such a way that it is able t ith t dt ith t d l dl d i d f ti d f t

9

to withstand to withstand a prolonged a prolonged period of stress. period of stress.

There There are are a variety a variety of of ways ways in which a bank can express its in which a bank can express its risk tolerance. risk tolerance. For exampleFor example, a bank may quantify its liquidity , a bank may quantify its liquidity risk tolerance in terms of the level of risk tolerance in terms of the level of unmitigated funding unmitigated funding liquidity risk the bank decides to take under normal and liquidity risk the bank decides to take under normal and stressed stressed business conditionsbusiness conditions..

Principles 5-12: Measurement and Management of Liquidity Risk

5. Sound measurement and monitoring framework

F t re cash flo s Future cash flows

Sources of contingent demand and triggers

6. Monitor and control risk within and across legal entities, considering limitations on transferability

7. Diversified funding sources

Maintain market relationships and presence

Test funding sources

10

8. Intraday liquidity positions under normal and stress conditions

9. Manage collateral positions (encumbered vs. unencumbered assets)

10. Conduct regular stress tests that inform contingency plans

11. Establish formal contingency funding plan (CFP)

12. Maintain a cushion of unencumbered, high quality liquid assets

6

Interagency Policy Statement on Funding and Liquidity Risk Management (March 2010)

Note consistency of focus Note consistency of focus between Basel andbetween Basel andbetween Basel and between Basel and Interagency GuidanceInteragency Guidance

11

Additionally, note Additionally, note consistency of focus with consistency of focus with Supervisory ApproachSupervisory Approach

12

www.occ.gov/publications/publications-by-type/comptrollers-handbook/liquidity.pdf

7

Liquidity Guidance

Basel guidance is similar to I tInteragency Guidance You are already implementing

While some of the newly implemented requirements are complex they

13

complex, they don’t apply to community and mid-tier banks.

LCR, HQLA, and NSFR Explained

14

8

http://www.bis.org/publ/bcbs238.htm

Includes Includes some tools some tools that may that may be usefulbe useful

15

Liquidity Coverage RatioAn adequate stock of unencumbered high-quality liquid assets (HQLA) that q g q y q ( )can be converted easily into cash immediately in private markets with minimal deterioration of asset values to meet liquidity needs for a 30 calendar day liquidity stress scenario.

Stock of HQLA’s≥ 100%

Total net cash outflows over

16

Total net cash outflows overnext 30 calendar days

9

HQLAHQLA includes three categories of assets with decreasing levels of quality, subject to haircuts and g g q y jinclusion limits. The “HQLA Stock” can be calculated as follows:

Asset Level Examples of Included Assets Haircut

Level 1Highest quality/most

liquid assets

• FRB balances• Foreign withdrawable resources• U.S. government securities• Certain sovereign and multinational organization

securities

None

Level 2A Relatively stable and

• Certain claims on/guaranteed by a U.S. GSE, sovereign entity or multilateral development bank

15%

17

significant sources of liquidity

• Certain covered bonds • Certain corporate debt securities

15%

Level 2B Lesser degree of liquidity and more

volatility

• Certain publically traded stocks• Corporate securities• Lower-rated corporate bonds• Mortgage backed securities

50%

• HQLA Stock must not include more than 40% of Level 2 (2A+2B) Assets.• HQLA Stock must not include more than 15% of Level 2B Assets.

Phase-In by US Regulators Faster than Basel

Minimum LCR 2015 2016 2017 2018 2019

Threshold will be a minimum requirement in normal times. During a period of stress, banks would be expected to use their pool of liquid assets thereby temporarily falling below the minimum requirement

Requirements

Basel 60% 70% 80% 90% 100%

US Interagency 80% 90% 100% 100% 100%

18

assets, thereby temporarily falling below the minimum requirement.

10

Reporting Requirements for Large Banks are Onerous

Frequency of Calculation 2015 2016

.

q y

Jan 1 –June 30

July 1 –Dec 31

Jan 1 –June 30

July 1 –Dec 31

Full LCR Monthly Daily Daily Daily

Modified LCR n/a n/a Monthly Monthly

Community Banks n/a n/a n/a n/a

19

Full LCR Modified LCR

$250 billi i t B t $50 billi

Applicability is Limited

>$250 billion in assets>$10 billion in foreign exposures>$10 billion asset subsidiary of above

Between $50 billion and $250 billion in assetsDoes NOT apply to subsidiaries of above

Not Required

<$50 billion in assets

20

11

Applicability The final rule focuses on large, internationally active banking organizations

with $250 billion or more in total consolidated assets or $10 billion or more in total on balance sheet foreign exposure because of their complexityin total on-balance sheet foreign exposure because of their complexity, funding profiles, and potential risk to the financial system.

The Board is separately adopting a modified minimum liquidity coverage

ratio requirement for most financial institutions that have more than $50 billion in total consolidated assets but that are not internationally active.

The agencies do not intend to apply the final rule to community banks.

21

g pp y y

However, the concepts are still useful and could be considered as part of However, the concepts are still useful and could be considered as part of the overall liquidity monitoring and reporting process.the overall liquidity monitoring and reporting process.

www.occ.gov/publications/publications-by-type/comptrollers-handbook/liquidity.pdf

Tools to help visualize concepts:Tools to help visualize concepts:Do I have good shortDo I have good short--term coverageterm coverage

22

12

www.occ.gov/publications/publications-by-type/comptrollers-handbook/liquidity.pdf

Tools to help visualize concepts:Tools to help visualize concepts:How much of a buffer do I need?How much of a buffer do I need?

23

NSFR

• Net Stable Funding Ratio is designed to improve incentives for using more

Another BaselAnother Basel--proposed proposed liquidity monitoring ratio liquidity monitoring ratio –– the the NSFR has not been agreed and NSFR has not been agreed and adopted to dateadopted to date

Net Stable Funding Ratio is designed to improve incentives for using more stable forms of funding. The NSFR is intended to limit overreliance on short-term wholesale funding, to encourage better assessment of funding risks across all on- and off-balance sheet items, and to promote funding stability.

• The BCBS is in the process of reviewing the NSFR that was included in the Basel III Liquidity Framework when it was first published in 2010.

• The agencies anticipate a separate rulemaking regarding the NSFR once the BCBS adopts a final international version of the NSFR

24

the BCBS adopts a final international version of the NSFR.

Available stable funding≥ 100%

Required amount of stable funding

13

Beyond Ratios

Liquidity Governance Concepts

25

Governance – Roles and Responsibilities

Board should:

Set liquidity risk tolerance and communicate effectively

Establish liquidity management strategy

Stay informed about the risk profile

Establish requirements for management to monitor, measure, and control liquidity risk.

Assess CFP

Approve policies annually

26

Senior Management should

Establish supporting processes and procedures to implement policy.

Enforce compliance with policy

Monitor and report liquidity position throughout the business.

14

Governance

Risk tolerance well-articulated

Pro forma cash flo s identif cash flo mismatches or gaps Pro-forma cash flows identify cash flow mismatches or gaps

Encumbered assets are segregated, at least on paper

Metrics are used to identify unstable liabilities

Funding is diversified

Contingent liabilities are quantified and well-understood

Assumptions are reasonable

27

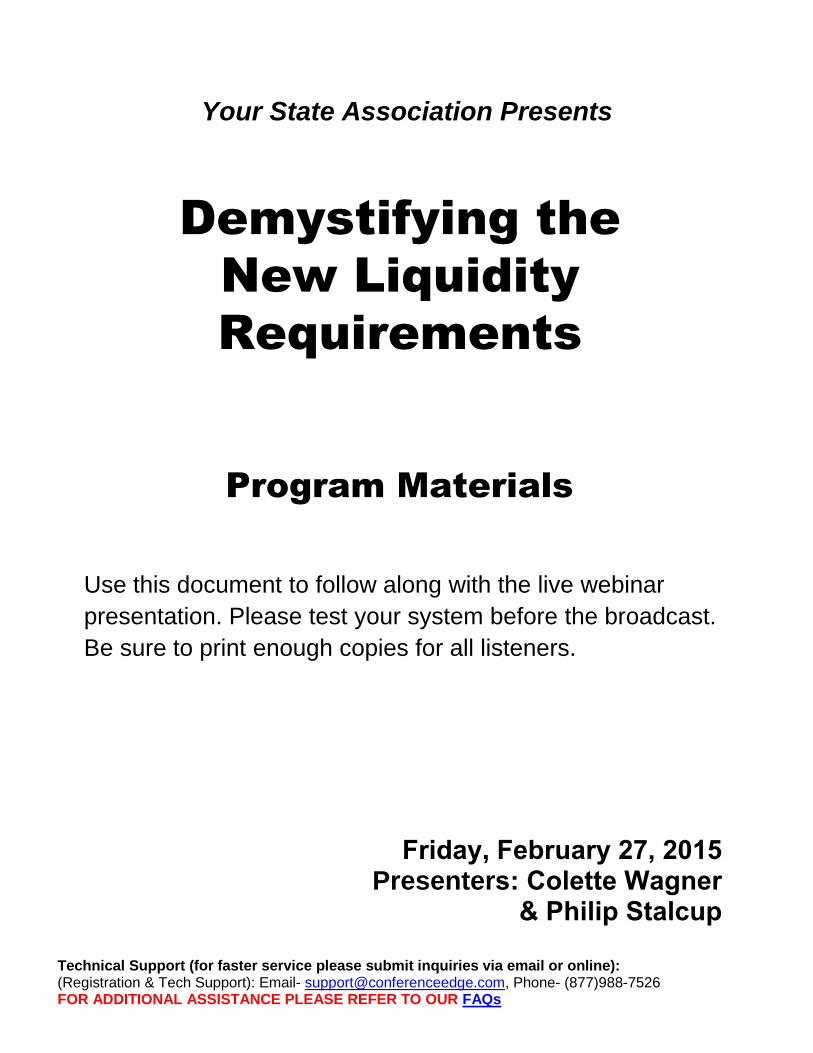

Governance – Stress Test Reporting

Stress cash flow projections should:

Cover at least one year

Accurately reflect

Stress scenarios

Assumptions about sources and uses of funds

For each stress scenario, should identify discrete and cumulative funding

mismatches or gaps over the stressed time horizon.

Contingent liquidity risk = peak cumulative net outflow difference over stress period

28

g q y p p

15

Stress Test Reporting

Documentation for each scenario:

Assumptions used p

Peak cumulative net outflow difference over a stress period that exceeds the minimum liquidity cushion

Action plan to address instances where the peak cumulative net outflow exceeds the minimum liquidity cushion

29

Measurement and Monitoring Systems

Liquidity Risk Reports

Cash flow projections

Critical assumptions

Cash flow gaps

Dashboard

Asset and funding concentrations

Key early warning risk indicators

Available contingent funding

Collateral usage

30

Collateral usage

16

Reporting – Dashboards For More Effective Communication

Example for Illustrative PurposesExample for Illustrative Purposes

31

Liquidity Monitoring and Stress Testing

32

17

Measurement and Monitoring Systems

Operational Cash Flow Forecasting

1+ year Projections

30+ day Gaps

Assumptions

Document, including their development

Identify key assumptions (those that strongly impact results.

Liquidity Models should be Liquidity Models should be subject to sound Model Risk subject to sound Model Risk

33

Management PrinciplesManagement Principles

Measurement and Monitoring Systems

Assumptions are inherently inaccurate, so develop a sense of the reliability of your estimates:

Perform sensitivity tests to see the impact of assumption errors

Isolate key assumptions

Use operational daily cash flow projections

Run multiple scenarios changing a single assumption (e.g., ±20%).

34

18

Measurement and Monitoring Systems

AssumptionError Risk

=Peak Cumulative Net Outflow Difference Over 30-day Backtest Period

35

Measurement and Monitoring Systems

Back-Test to Understand Forecast Error Risk

Determine key drivers of differences between actual and forecast over a given period.

Forecast setup?

Forecast assumptions?

Methodology

Use prior period operational daily cash flow projections

Compare actual daily net cash inflow/outflow to projections

36

19

Measurement and Monitoring Systems

ForecastError Risk

=Peak Cumulative Net Cash Outflow Difference Over 30-day Backtest Period

37

Measurement and Monitoring Systems

Use the results of Assumption SensitivityAnalysis and Back-Testing to determinethe amount of liquidity cushion needed.

38

20

Liquidity Buffers

39

Liquidity Buffer

Reg YY – Enhanced Prudential Standards requires BHC’s with total consolidated assets of $50 billion or more to:

Establish and maintain robust liquidity management practices

Perform internal stress tests for determining liquidity adequacy

Maintain a buffer of highly liquid assets sufficient to cover net cash outflows based on a 30 day stress test cycle under various scenarios.

40

Project Cash Flows

Stress Tests

Determine Liquidity Buffer

21

Liquidity Buffer

Reg YY Guidance for liquidity risk management is generally consistent with Basel guidance and the 2010 Interagency Guidance.

Pro forma cash flow projections and stress testing are already expected at most larger community and mid-tier financial institutions.

While the minimum (30 day stress) buffer requirements do not apply to these institutions, the conceptual approach may offer value in developing a contingency funding plan

41

Project Cash Flows Stress Tests

Develop Contingency Funding Plan

Liquidity Contingency Funding Planning

Contingent Liquidity Risks

Reduced borrowing capacityg p y

Increased collateral haircuts

Off-balance sheet exposure

Depreciated assets become harder to sell

Asset quality affects cash flows

Interest Rate Risk

Bad publicity and rumors

42

22

Liquidity Contingency Funding Planning

Establish clear lines of responsibility and escalation procedures

Identify liquidity stress event triggersy q y gg

Multiple liquidity events

At least one where subject to PCA

Consider the short-, intermediate-, and long-term liquidity profile

Articulate assumptions about sources and uses of funds in a liquidity event

Articulate plans under various and increasing levels of liquidity stress

43

Liquidity Contingency Funding Planning

Projection and evaluation of expected cash flows under increasing stress scenarios:

Quantitative, not just judgments

Assumptions should be reasonable for each source and use of cash based on uniqueness:

Insured vs. uninsured deposits

Public vs. retail deposits

Borrowing lines by provider reflecting collateral and collateral haircuts

Renewing vs. new loans

44

g

23

Liquidity Contingency Funding Planning

What about Interest Rate Risk?

Are assumptions affected by a rapid long-term increase in interest rates?p y p g

Increase in non-maturity deposit decay rates?

Increase in time deposit early withdrawals?

Decrease in loan prepayment speeds?

Decrease in investment prepayment speeds?

45

What Should You Do Next?

46

24

Management of Funding and Liquidity Risk

Liquidity as a Strategy

Liquidity Cushionq y

Diversification of Funding Sources

Risk Measurement and Monitoring Systems

Contingency Planning

Stress Testing

47

Liquidity as a Strategy

Balance sheet structure for liquid asset quality

Strategic planning to diversify funding sourcesg p g y g

Liquidity risk measurement and monitoring system

48

25

Balance Sheet Structuring

49

How Much On-Balance Sheet Liquidity?

Other considerations

Cash-flow volatilityy

Uninsured deposit concentrations

Deteriorating asset quality

Predictability of cash flow mismatches

Credit rating with the FHLB

50

26

How Much On-Balance Sheet Liquidity?

Sized to stress tests and maximum liquidity outflow over survival period, supported by:

Stress tests

Forecast error

Risk profile

Risk tolerance

51

Diversification of Funding Sources

52

27

Diversification of Funding Sources

Considerations

Limited number of borrowing sourcesg

Concentration of credit line availability

Deteriorating asset quality

Predictability of cash flow mismatches

Credit rating with the FHLB

53

Actions for more robust liquidity risk management

Assess systems and tools used to monitor and measure liquidity

Assess whether your monitoring and reporting are sufficient for assessing liquidity position.

Check your contingency funding plan (CFP) to make sure it can cope with the outcomes from your stress tests.

Check your assumptions – will you be able to execute your contingency plans in the face of a crisis?

Make your liquidity risk management process dynamic to reflect the changing environment and financial position of the company

A i t f li idit ti fit bilit

54

Assess impact of liquidity actions on profitability

Set correct incentives to align liquidity strategy with business objectives

Think broadly in liquidity stress testing – could a low probability/high impact situation sink the ship?

28

Questions

55

Related Documents