2014 Momentum Webinar Series: Delivery Redirect Mapping Your Business to Changing Consumer Behavior Cornerstone Advisors, Inc. Digital Insight October 22, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2014 Momentum Webinar Series:Delivery RedirectMapping Your Business to Changing Consumer Behavior

Cornerstone Advisors, Inc.

Digital Insight

October 22, 2014

• Introduction

• Q/A

• Social Media: (#Diwebinar & @Digital_Insight)

• Post-webinar materials

Welcome

Introductions

Russell Lester - Senior Director, Strategy & Business Analytics, NCR Financial Services -Russell has over 15 years of experience in the financial services industry and presently leads the Analytics center of excellence for NCR Financial Services. In this role, Russell is responsible for managing a team of seasoned analysts that provide timely, accurate, relevant and pro-actively persuasive insights to internal stakeholders and customers. This team helps customers navigate the complex landscape of their diverse data assets to identify, quantify and prioritize areas of opportunity. Russell has spent much of his career interacting with financial institutions to understand their business challenges and identify ways in which insights can help inform their strategic plans. Prior to joining NCR, Russell was Vice President of Financial Planning and Analysis at Harland Clarke.

Dave Potterton - Research Director, Cornerstone Advisors - Dave is responsible for the

strategic direction of Cornerstone Advisor’s research and thought leadership efforts while building on the firm’s reputation and success. Previous to Cornerstone, Dave held thought leadership positions within a variety of financial services firms including Salesforce.com, IDC and JPMorgan. In addition to his experience as a practitioner, market researcher and consultant, David has been a speaker and facilitator at many financial services and technology conferences and authored numerous articles on technology in financial services. His Twitter handle is dpotterton.

Tim Daley - Senior Consultant, Cornerstone Advisors - Tim has more than a decade of

financial services experience in technology, business process analysis, project management, compliance and various information technology solutions. At Cornerstone, Tim focuses his efforts in the Strategic Technology Planning, Technology Assessments and Information Technology Organizational Assessments practice areas. Before joining Cornerstone, Tim led the integration of two online banking systems associated with the largest credit union merger in history. He also held key technology related positions at First Horizon National Corporation in Memphis, Tenn.

PRESENTED TO:

crnrstone.com gonzobanker.com480.423.2030

PRESENTED BY:

October 2014

Delivery Redirect – Mapping Your Business to Changing Consumer Behavior

David Potterton, Research Director

Tim Daley, Senior Consultant

Digital Insight Momentum Webinar

4

Ab

ou

t Co

rnersto

ne A

dviso

rsCornerstone at a Glance

National financial

services management

consulting firm

founded in 2002Specializing in mid-size

financial institutions with

$1-40 billion in assets

7 key

service

offerings

• Strategic Solutions

• Performance Solutions

• Technology Solutions

• Contract and Vendor Management Solutions

• Payment Solutions

• Channel Solutions

• Research and Knowledge Sharing

5

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

AGENDA

● What’s Happening With My Customers and the Marketplace?

● Delivery Redirect and Potential Strategies

● Examples

● How to Begin the Journey

● Final Thoughts

6

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

It used to be all so simple

● Customers had a financial service need based on some life event -

college, getting a job, getting married, or needing a car or house

● Research would begin for a bank or credit union – more than likely

based on branch proximity and/or ads seen in traditional media such

as newspapers or television

● Ultimately they would decide if they wanted to accepted the terms,

fees, etc. to become a customer

7

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

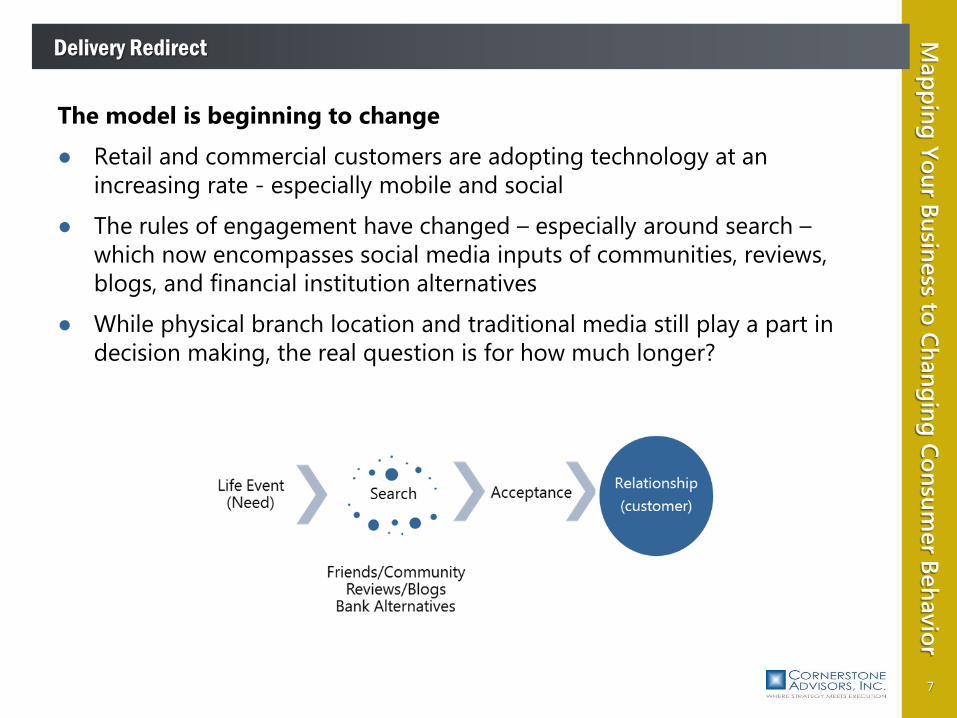

The model is beginning to change

● Retail and commercial customers are adopting technology at an

increasing rate - especially mobile and social

● The rules of engagement have changed – especially around search –

which now encompasses social media inputs of communities, reviews,

blogs, and financial institution alternatives

● While physical branch location and traditional media still play a part in

decision making, the real question is for how much longer?

8

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

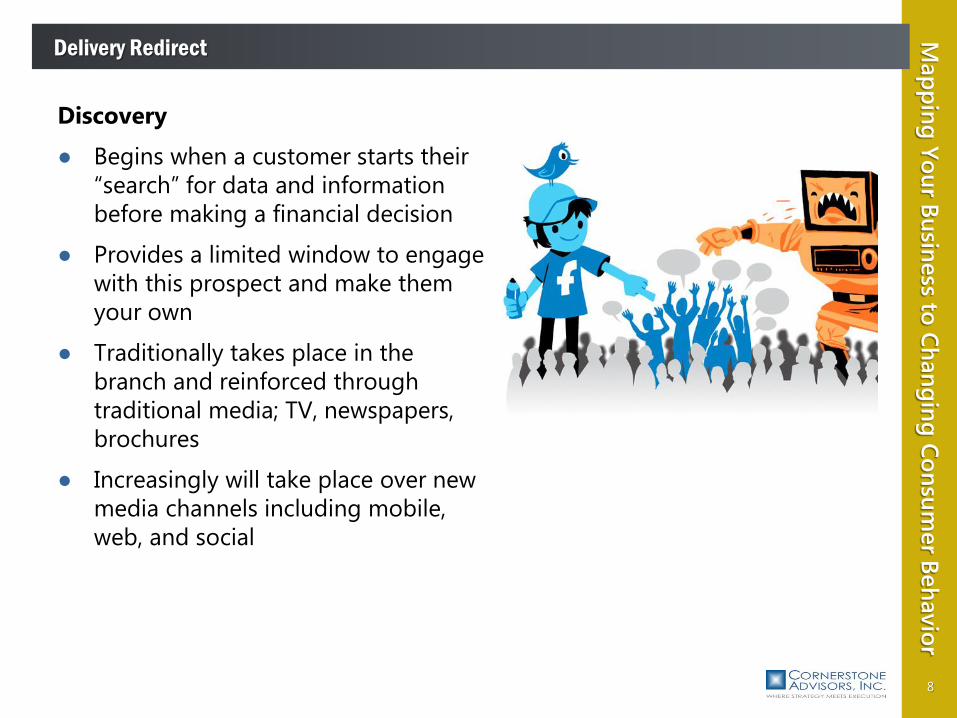

Discovery

● Begins when a customer starts their

“search” for data and information

before making a financial decision

● Provides a limited window to engage

with this prospect and make them

your own

● Traditionally takes place in the

branch and reinforced through

traditional media; TV, newspapers,

brochures

● Increasingly will take place over new

media channels including mobile,

web, and social

9

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Onboarding

● A critical interaction between the customer and financial institution

● Customers looking for fast fulfillment, timeliness, simplicity, and

convenience

● Unfortunately, the onboarding process is less than optimal at many

institutions creating a poor initial customer experience

● Essential information may also be overlooked which could generate

additional value for the customer and the organization

10

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Experience

● Is the process of customers using the financial products, services and

channels

● Includes customer service which is a key component in either a positive

or negative way

● Financial institutions need to measure and track satisfaction to

understand if they are providing the right level of products and

services for their customers

● This will help provide a consistent experience as well as relevant and

timely offers of additional services

11

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Advocacy

● Is the state that all financial institutions

should aspire to with their customers

● Customers become “advocates” of the

financial institution and its services within the

community (both social and physical)

● This can increase the visibility of the

organization’s brand and lead to other

potential customers

12

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

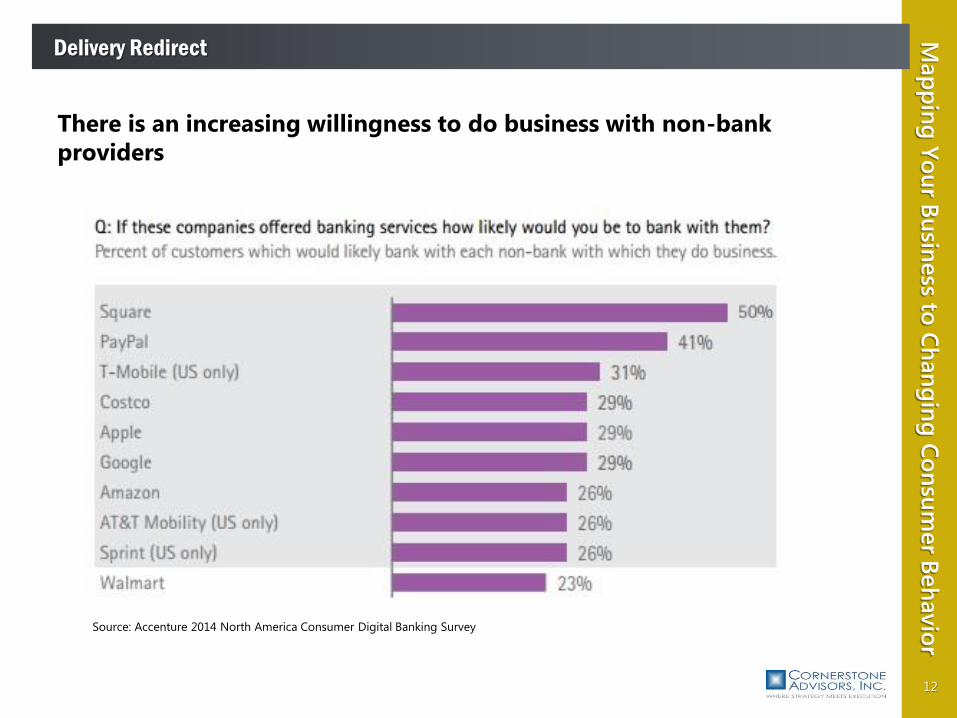

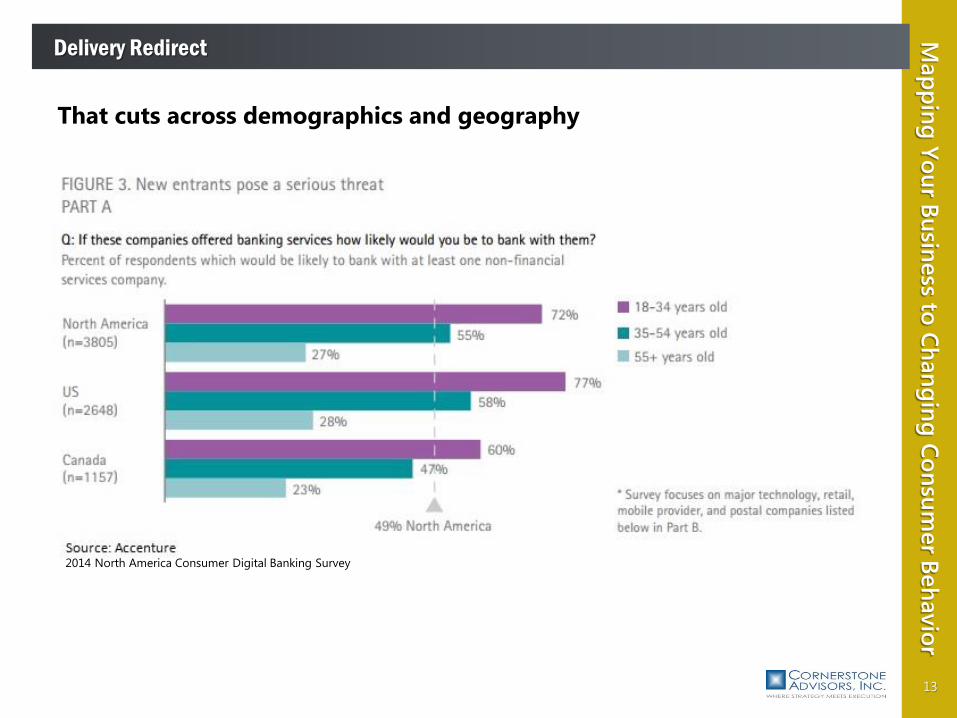

There is an increasing willingness to do business with non-bank

providers

Source: Accenture 2014 North America Consumer Digital Banking Survey

13

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

That cuts across demographics and geography

2014 North America Consumer Digital Banking Survey

14

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

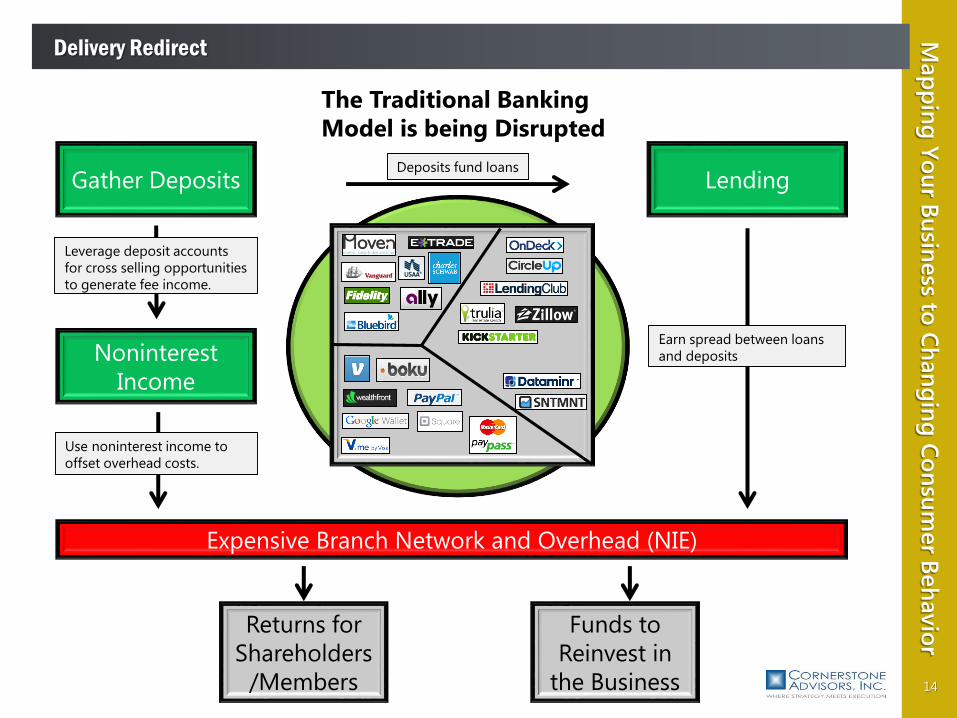

Gather Deposits Lending

Expensive Branch Network and Overhead (NIE)

Noninterest

Income

Deposits fund loans

Returns for

Shareholders

/Members

Earn spread between loans

and deposits

Leverage deposit accounts

for cross selling opportunities

to generate fee income.

Use noninterest income to

offset overhead costs.

Funds to

Reinvest in

the Business

The Traditional Banking

Model is being Disrupted

15

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Delivery Redirect is about

facing up to the tough choices

concerning resources, the sales

force, and new organizational

capabilities that financial

institutions must address in

order to be viable in 2020 and

beyond

16

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Delivery Redirect is not about

just migrating transactions but

REVENUE PRODUCTION –

the optimal mix of channels and

resources to successfully

influence the buying behavior

of current and future members

to drive new and cross

sell/upsell revenue

17

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

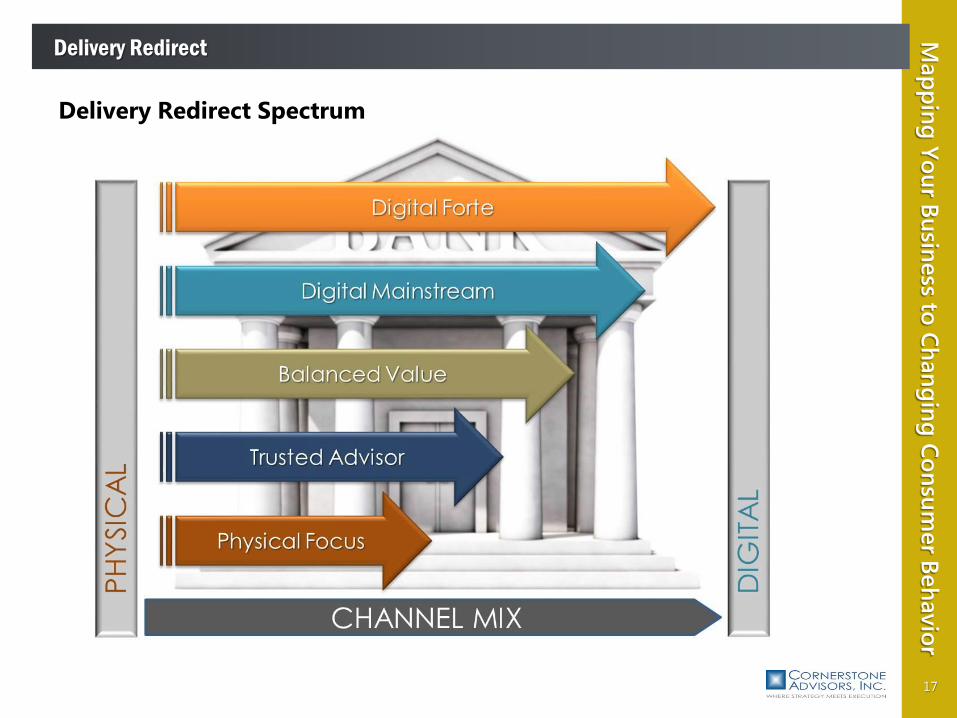

Delivery Redirect Spectrum

18

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Physical Focus

● Institutions that operate in less technical, cash heavy markets such as

under banked segments, rural markets, etc.

Demographic

● Customers are generally not technology savvy and depend on

traditional physical channels – branches and ATMs

● Heavy check cashing volume, particularly at on certain days of the

week/month

● Small business and commercial accounts, especially for proximity

businesses. Limited/no social media interest

Strategy

● Focus on physical channels – specifically branches – in areas of highest

concentration of customers

● Offer digital (mobile, Web) for those who want but not a leader as far

as digital service offerings. Limited/no social media presence

19

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Trusted Advisor

● More sophisticated commercial and wealth-focused banks that drive

revenue from high valued relationships

Demographic

● Similar to Physical Focus customers but more technology knowledge

and use including social media

● Physical channels still important but less so

● Mix of small business and commercial accounts

Strategy

● Keep focus on physical channels and proximity, but less so

● Look to differentiate service offering and marketing within branches

● Offer digital services with increased functionality and create minimal

social media presence

20

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Balanced Value

● Large national players and progressive community and regional

institutions

Demographic

● Even mix between retail and commercial customers with full range of

tech and non-tech sophistication

● Use of both physical and digital channels. Social media usage

medium/high

Strategy

● More balanced customer mix necessitates broader channel support

depending on who is utilizing the channel

● Technology solutions available for those customers who want

● Present broad and deep functionality across all channels and maintain

good social media presence and outreach

21

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Digital Mainstream

● Players that blend digital focus with a limited office presence, similar to

major mutual funds/brokerage houses nationwide

Demographic

● Higher level of technology sophistication and usage for customers

whose preference runs to digital channels

● Retail versus commercial concentration

● High reliance on self-service. Social media usage very high

Strategy

● Lead with technology and capabilities but still maintain a

representative physical presence which makes use of smaller footprints

and innovative technology

● Be very active in social media

22

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Digital Forte

● Category killers who leverage digital and contact center channels

Demographic

● Customer preference runs to digital channels

● High level of technology knowledge and usage

● Retail versus commercial concentration

● High reliance on self-service. Social media usage very high

Strategy

● Very limited to no physical presence – predominately remote and

mobile

● Lead with technology capabilities and innovation. Extremely active in

social media

23

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Digital Forte Example - USAA

● $59 billion in deposits and more than 10 million

customers

● One physical branch for many years

● On average, members utilize four USAA products

● Deposit growth of 21% for latest quarter

● From the beginning have focused on alternate, online

and mobile channels

● They are one of the few retail financial institutions

allowing people to rate and review products online

● Have approximately 28,000 followers on Twitter and

232,440 ‘Likes’ on Facebook leading all other financial

institutions in social channels

24

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

The Situation

● BECU has spent 15 years architecting a delivery system that is

aligned with changes in technology and consumer behavior

and can drive strong value for members

– The credit union experimented with cashless branches very early

– A bold entry into Safeway stores dramatically increased their

footprint and brand awareness

– Investments in online and call center channels have leveraged a

tech-friendly Puget Sound area population base

– More than 500,000 checking accounts serviced by less than 100

tellers drives incredible delivery efficiency

Delivery channels can’t just be

additive. Credit unions need to

make bold and deliberate plans

to redirect their investments

and capabilities.

The Lesson

25

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

The Situation

● Wright Patt is a strong and growing credit union with one of

the highest Net Promoter scores in the country (73% Relational)

● The credit union recently expanded into the Columbus market,

but decided to try something new

● Columbus will be used as the living lab for technology driven

branches (NCR uGenius) with more universal associate

positions

● Direct marketing and branding experiments will also be done in

this new market

Use a weakness to create a future

strength. A new market is a great

place to take new risks without

alienating your core member base.

Test and learn!

The Lesson

26

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

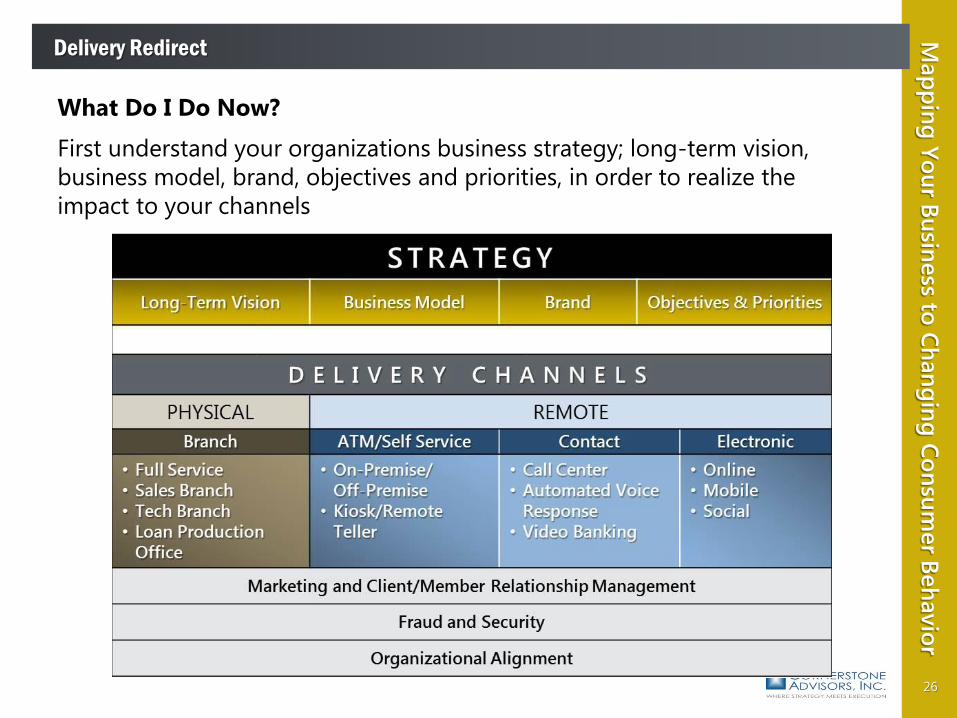

What Do I Do Now?

First understand your organizations business strategy; long-term vision,

business model, brand, objectives and priorities, in order to realize the

impact to your channels

27

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

● Align Your Delivery Channel Strategy with Your Corporate Strategy

● Develop a formal Delivery Channel Road Map

● Transform Marketing and Relationship Management

● Enhance Fraud and Security

● Upgrade the Organization to Meet New Competitive Realities

28

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

In developing your specific redirect action plans for each channel, keep

the following in mind:

● How Much Do Customers Value The Channel? – Your transaction

data, channel usage metrics, and available survey metrics should help

you answer this question

● How Cost Effective Is The Channel? – Compare your direct cost (staff,

facility, other unallocated) to your deposits as well as your direct cost

to non-interest income plus funding credit

● How Is The Channel Contributing To Sales? – Understand your

open/close ratios, number of new accounts overall and by type (e.g.

checking), value of direct consumer/small business loan production as

well as investment and mortgage referrals

29

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

Final Thoughts

● Drive customer experience management from the top – Customer

experience is a C- level accountability and therefore executive

leadership and channel management needs to be aligned and

supported

● Don’t let legacy systems spell doom – All institutions have them, but

look beyond the systems and don’t let them be your anchor

● Remember, today’s shareholder value means nothing– Take a look

at the disrupters in financial services – how many more of them will

there be in 2020? Do people really need financial institutions?

● We’ve met the enemy and it is us. Don’t let the past dictate how

your institution will respond to the changing financial services

landscape and don’t be lolled into a false sense of security

30

Map

pin

g Y

ou

r Bu

siness to

Ch

an

gin

g C

on

sum

er B

eh

avio

rDelivery Redirect

START NOW … RIGHT NOW (WE MEAN IT)!

Getting started

With increasingly diverse interaction—it’s critical to think holistically

• The market often views channels in silos.

• In reality, there’s a consumer at the end of each channel, and most consumers use multiple channels.

• It’s more important than ever to maximize the value of every touch point: Branch, ATM, Online, Mobile . . .

The result is experiences that your end users love—and your revenue reflects.

As interactions change, it’s important to keep the economics of these changes in mind

Examine the primary moving parts of profit optimization potential:

• Evaluate current channel footprint

• Capabilities? Consistency across channels? Gaps?

• Demand? Transaction volumes? Throughput?

• Costs to support? (Include opportunity costs.)

• Existing levels of: account ownership, retention, balances and fee income

• Likely future direction – What is your demographic shifting towards? What are their expectations? What technology will it require?

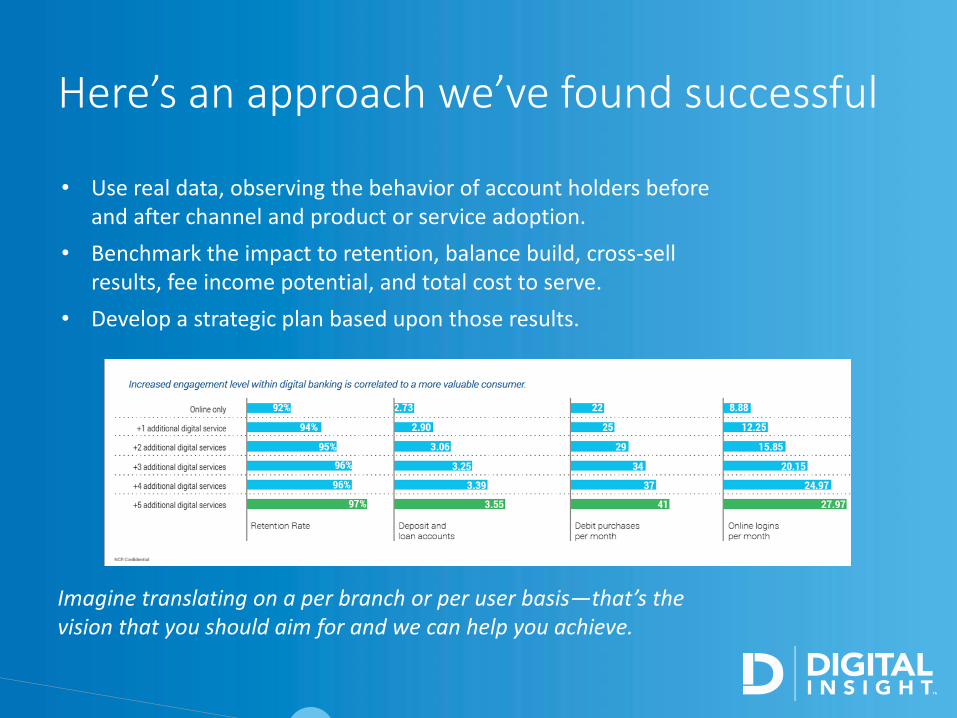

Here’s an approach we’ve found successful

• Use real data, observing the behavior of account holders before and after channel and product or service adoption.

• Benchmark the impact to retention, balance build, cross-sell results, fee income potential, and total cost to serve.

• Develop a strategic plan based upon those results.

Imagine translating on a per branch or per user basis—that’s the vision that you should aim for and we can help you achieve.

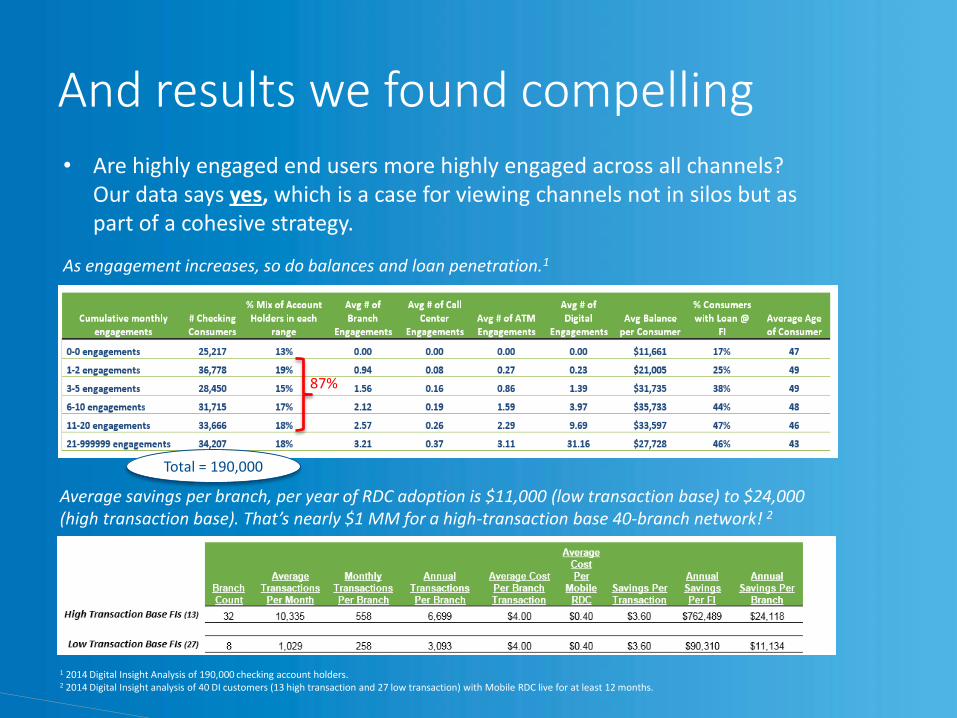

And results we found compelling

• Are highly engaged end users more highly engaged across all channels? Our data says yes, which is a case for viewing channels not in silos but as part of a cohesive strategy.

As engagement increases, so do balances and loan penetration.1

1 2014 Digital Insight Analysis of 190,000 checking account holders. 2 2014 Digital Insight analysis of 40 DI customers (13 high transaction and 27 low transaction) with Mobile RDC live for at least 12 months.

Average savings per branch, per year of RDC adoption is $11,000 (low transaction base) to $24,000 (high transaction base). That’s nearly $1 MM for a high-transaction base 40-branch network! 2

87%

Total = 190,000

www.digitalinsight.com

Thank you!

Visit Digital Insight:

We value your feedback. Take the survey

after today’s call and let us know:

1. How we did

2. If you would like follow-up information

Join the conversation: #DIwebinar

Visit Cornerstone Advisors: www.crnrstone.com

Related Documents