Defining the AmerisourceBergen way. 2003 Annual Report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Defining the AmerisourceBergen way.

2003 Annual Report

Annual Report 2003AmerisourceBergen (NYSE:ABC) is the largest pharmaceutical services company

in the United States dedicated solely to the pharmaceutical supply channel. We work

with our branded, generic, and specialty pharmaceutical manufacturer customers

to distribute pharmaceutical products and services to America’s healthcare providers.

With more than $45 billion in operating revenue, the Company is headquartered

in Valley Forge, PA, and employs more than 14,000 people.

AmerisourceBergen is a leader in providing pharmaceuticals and related services

to the hospital systems/acute care market, physician’s offices, alternate care and

mail order facilities, independent community pharmacies, and regional chain

pharmacies. The Company is also a leader in the long term care pharmacy and

workers’ compensation fulfillment marketplaces. We provide logistical expertise,

contract packaging services, and product marketing assistance to our manufacturer

customers, and pride ourselves on our industry leading customer service. Our goal

is to help all of our customers improve their businesses and ultimately improve

the quality of healthcare in America.

www.amerisourcebergen.com

AmerisourceBergen is

committed to expanding

the value added services

we provide to our

customers along the

pharmaceutical supply

channel through

internal development

and through acquisition

of companies like

Anderson Packaging,

shown on the cover.

Defining the AmerisourceBergen way.

2003 Annual Report

2

6

4

1213

Financial

$45,5

R. David Yost, AmerisourceBergen’s

Chief Executive Officer, gives

an overview of fiscal year 2003

and the Company’s future outlook.

Robert E. Martini, Chairman of

AmerisourceBergen’s Board of

Directors, recaps Board activities

for fiscal year 2003 and gives

an update on the Company’s

Corporate Governance activities.

List of members of the Company’s Board

of Directors and AmerisourceBergen

Corporate Officers.

Defining the AmerisourceBergen Way: delivering

shareholder value through disciplined growth.

AmerisourceBergen Management’s

Discussion and Analysis of Financial

Condition and Results of Operations.

Contents

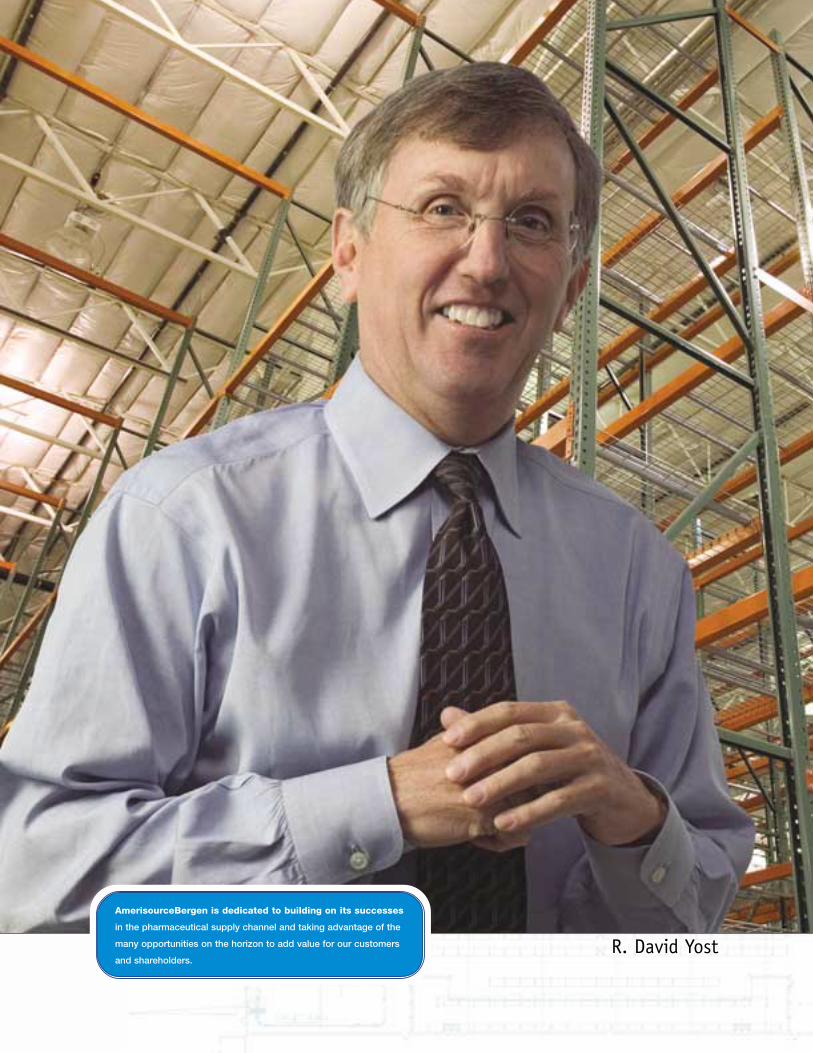

To Our

Shareholders:For fiscal 2003, the associates

of AmerisourceBergen promised to stay

focused on the pharmaceutical supply

channel and to deliver strong financial

results. It is my pleasure to report to

you that our promises were kept.

In fiscal year 2003, the Company

generated operating revenue of $45.5

billion, a 13% increase over fiscal 2002,

which when combined with a sharp

reduction in operating costs as a

percentage of revenue, produced a 28%

increase in net income over the prior

year. Earnings per share were $3.89,

a 23% increase over the previous year.

And that’s on top of a 50% increase

in earnings per share delivered in 2002.

Our strong financial results were

delivered while being disciplined in the

use of our capital, and generating over

$350 million in cash from operations.

We kept our receivables to 17 days,

the best in the industry, and produced

exceptional inventory productivity.

Besides solid financial performance,

our disciplined execution continues

to deliver on other commitments.

We are substantially ahead of schedule

in delivering $150 million in merger

related synergies promised by the end

of fiscal 2004. And, since the merger,

we have enhanced our role in the

pharmaceutical supply channel with

the investment of nearly $500 million

in five acquisitions that provide

AmerisourceBergen strong positions

in such important channel services

as pharmacy automation, contract

packaging, patient safety, and

physician education.

Underpinning these results

is the superior performance of

AmerisourceBergen associates.

They are building a collaborative

culture, centered on execution and

discipline, and it is my great pleasure

to work with them.

Disciplined Growth StrategyFocused on the pharmaceutical

supply channel, AmerisourceBergen

continues to execute our simple, two-part

growth strategy: Deliver “best in class”

pharmaceutical distribution and provide

“best in class” solutions and services to

the channel.

During 2003, we made outstanding

progress on our Optimiz program, which

is designed to create a world class

distribution network in our pharmaceutical

distribution business by 2007. During

the year, six more distribution centers

(DCs) were consolidated, and with 2002’s

seven consolidations, we now operate

38 distribution centers out of an original

51 DCs. When complete, the network

will have 30 distribution centers

including six new highly automated

“greenfield” facilities with approximately

300,000 square feet each. We now have

four of the new DCs under construction,

with the first scheduled to open in the

summer of 2004. We also remodeled

two DCs out of the seven planned,

and implemented our warehouse

management system, PkMS, in three

of our facilities, producing significant

productivity improvement and nearly

perfect order accuracy.

In our PharMerica segment, we

completed the migration of all long

term care pharmacy facilities to a

single operating system, and developed

plans to capture additional operating

efficiencies through automation.

We continue to add solutions and

services for our healthcare providers

and pharmaceutical manufacturer

customers. During the year we acquired

Our Optimiz program drives inventory accuracyto 99.99%, order accuracy to 99.94%, andimproves warehouse productivity by 40%.Pharmaceutical distribution continues

to be a very healthy business, withdouble digit growthforecasted well into the future.

Earnings per share increased23% in FY003, on top of a 50%increase in FY 2002.

2

Diluted EarningsPer ShareFY Ending September 30

1999 2000 2001 2002 2003

$1.

90

$1.

31

$2.

10

$3.

89

$3.

16

AmerisourceBergen is dedicated to building on its successes

in the pharmaceutical supply channel and taking advantage of the

many opportunities on the horizon to add value for our customers

and shareholders. R. David Yost

Anderson Packaging, a leading contract

packager for manufacturers; Bridge

Medical®, and its leading patient safety

software technology for the acute care

market; and U.S. Bioservices, which

provides reimbursement consulting and

the delivery of complex drug therapies

for manufacturers looking to bring new

products to market. Our acquisitions

since the beginning of fiscal 2002

have already collectively added to the

Company’s gross margin in FY 2003.

Fiscal 2004 will also be a active

building year for our Company. In the

pharmaceutical distribution segment,

we expect to have five greenfields

under construction and have planned

three consolidations, along with three

installations of PkMS, and one DC

remodeling. As we complete the

Optimiz program, we expect to deliver

cost savings well beyond fiscal 2004

and firmly establish ourselves as the

lowest cost service provider in the

industry. We have the ability to make

moderately sized acquisitions and expect

to continue our disciplined acquisition

activity with the right opportunities.

The FutureWe continue to view the

pharmaceutical supply channel as

a positive and stable environment.

The basic fundamental drivers of this

industry—demographics (the aging

of America) and the country’s demand

for new drugs—have not changed.

Our suppliers continue to invest tens

of billions of dollars developing the

products we will distribute in the

future. Pharmaceutical distribution

continues to be a good business to be

in, with double digit growth forecasted

far into the future.

Robert E. Martini

Fellow shareholders:

In our second full year of operations

AmerisourceBergen again delivered

outstanding operating performance while

achieving its aggressive plans in its network

consolidation and build-out process. The

Company also has thoroughly reviewed its

corporate governance structure and taken

measures to further strengthen its internal controls and reporting

mechanisms. AmerisourceBergen is fully compliant with corporate

governance requirements and the current New York Stock Exchange

listing standards.

Your Directors are actively engaged in the oversight and governance

of the Company, each lending his or her individual expertise and

fulfilling their responsibilities thoughtfully and completely. The

Governance and Nominating Committee conducted a formal

assessment of the Board and, while there were no deficiencies

noted, the Board adopted some enhancements to its oversight

and conduct procedures. In addition, the Board adopted Corporate

Governance Principles and modified the title and charters of its

committees to ensure compliance with the New York Stock Exchange’s

corporate governance rules. These corporate governance documents

are published in the 2004 proxy statement.

All Directors and Company associates are required to comply with

AmerisourceBergen’s updated Code of Ethics and Business Conduct.

As required by the Sarbanes-Oxley Act of 2002, the CEO, CFO

and Controller also are subject to a Code of Ethics that complies

with Securities and Exchange Commission regulations. We have

implemented additional disciplines and will continue to monitor

and adopt policies and procedures as warranted.

We are most appreciative of the insight and guidance that we have

received from Francis G. “Buck” Rodgers, who will be retiring from

the Board after 22 years with the AmerisourceBergen and Bergen

Brunswig Boards, which he so dutifully served.

AmerisourceBergen prides itself on delivering shareholder value by

managing itself with integrity, reporting its financial results forthrightly,

and exceeding its customers’ expectations. This report outlines the

progress your management has made in the past year and the

opportunities ahead.

Thank you for your continued support.

Sincerely,

Robert E. Martini

Chairman of the Board

January 12, 2004

4

As always, there are changes ahead.

The new Medicare drug benefit, recently

signed into law, is expected to bring a

substantial increase in drug utilization

and revenue for AmerisourceBergen

in 2006. We will be ready and able to

leverage the added volume through our

highly efficient distribution centers.

On December 31, 2003 we lost the

Department of Veterans Affairs contract,

which represents more than $3 billion

in annual operating revenue and expires

March 31, 2004. While disappointing,

we expect to quickly move to take out

costs associated with this contract and

begin to re-deploy the associated capital

to replace lost earnings.

The U.S. Food and Drug

Administration (FDA) is seeking to

address reported incidents of counterfeit

merchandise in the channel. These are

rare in the context of the $200 billion

pharmaceutical industry. Nonetheless,

AmerisourceBergen and our peers, along

with pharmaceutical manufacturers, are

upgrading our safety procedures and

standards. The movement of product

from manufacturer to primary distributor

to healthcare provider continues to

be the “gold standard” of security and

reliability. Your Company will continue

to work closely with the FDA and

manufacturers, and will maintain our

leadership in this area.

The industry is continuing to evolve

from a model where pharmaceutical

distributors have the traditional

opportunity for earning profits from

speculating on price appreciation and

manufacturer deals, to one characterized

by incentives that more closely match

our inventory with the demand from

the healthcare provider. The industry

will be moving toward a fee-for-service

relationship with the brand name

pharmaceutical suppliers. Over time this

will result in a more efficient channel

with more product moving through

full-service distributors and more stable

and predictable earning power for

AmerisourceBergen. The change will be

positive for the Company in the long run.

Any temporary negative impact from this

change should impact AmerisourceBergen

less than its peers because we have run

with lower inventory and have been

historically the least dependent on

speculation profits and deals. Our cost

savings from the building of our world

class distribution network will also

help us smoothly manage this change.

In my 30 years in the industry, I have

experienced many changes and I am

confident that with continued discipline

AmerisourceBergen will adapt quickly and

well to any evolution in the marketplace.

I want to thank AmerisourceBergen

Director Francis G. “Buck” Rodgers

for his many years of service to

AmerisourceBergen as he retires from

the Board of Directors this year. The

Company and I have been well served

by his counsel and active participation

on the Board and I will miss his

unwavering optimism.

I also want to thank our many

associates. Their continuing daily efforts

in exceeding customer expectations

have allowed our Company to maintain

its leadership position in the industry.

GoalsAmerisourceBergen’s long-term

goals are to grow revenue with the

pharmaceutical market, which is

expected to expand 10% to 13%

between now and 2007; continue to

expand our operating margin; deliver

return on committed capital in excess

of 20%, and increase earnings per

share 15% or more annually, excluding

special items.

AmerisourceBergen is solidly on

track, and tracking in a solid industry.

Thank you for your continuing support.

R. David Yost

Chief Executive Officer

January 12, 2004

AmerisourceBergen has expanded its valueadded services portfolio to include additionalcapabilities that enable us to help ourcustomers improve the effectivenessand the efficiency of their businesses.

We are substantially ahead of schedule indelivering $150 million in merger related costsavings promised by the end of fiscal 2004.

5

Definingthe AmerisourceBergen Way.

Disciplined. Efficient. Innovative.

Successful. These are just some

of the words that help define the

AmerisourceBergen way of doing

business. We focus on delivering

outstanding service on a daily basis,

serving healthcare providers and

pharmaceutical manufacturers with

products and services to help them

improve their businesses and ultimately

improve the quality of healthcare

delivered in America. We operate in

a $200 billion industry that is growing

revenue at a double-digit rate. Fueled

by tens of billions of dollars in annual

drug research and development spending

and an aging population, the sale of

pharmaceutical products in the United

States will continue to expand through-

out the decade. AmerisourceBergen

is well positioned to benefit from this

organic growth in the pharmaceutical

supply channel in two ways: by delivering

pharmaceutical products and unique

services to the nation’s healthcare

providers, and by offering drug

manufacturers value added programs

and services to help them meet the

demands of the marketplace and preserve

the integrity of the pharmaceutical

supply channel. By leveraging our scale

and building upon the framework of our

essential role in the marketplace, we

are able to provide exceptional value to

our provider and manufacturer customers

as well as to our shareholders.

America’s healthcare providers

rely on AmerisourceBergen to deliver

pharmaceuticals and related products

on a just-in-time-basis and with nearly

100% order accuracy. In our business,

the standard is perfection. Whether

we are handling oral solid medications,

vaccines and other injectables, oncology

and other specialty drugs, or over the

counter products, our customers are

confident that the right product will

get to the right place at the right

time. AmerisourceBergen’s expertise

in handling the vast array of types

The new Sacramento, CA distribution center, one of four currently

under construction, is scheduled to open during the summer of 2004.

At over 300,000 square feet and equipped with the latest warehouse

management technology, it will be one of our largest and most efficient

facilities. When complete, all six “greenfield” facilities will be of

similar size and scope, and will utilize state-of-the-art technology.

As we complete our Optimiz program,we expect to continue to deliver costsavings well beyond fiscal 2004 andfirmly establish ourselves as the lowestcost service provider in the industry.

6

of pharmaceuticals available today is

unmatched in the industry. Our provider

customers include local retail pharmacies,

national and regional pharmacy chains,

regional food and drug store chains,

hospitals, long term care facilities,

clinics, physician offices, and prescription

mail order facilities. Our logistical

expertise in both traditional and

specialty product distribution and

in dispensing, combined with our

inventory management, reimbursement

consulting, packaging, pharmacy

automation, and other service offerings

make us a valuable partner in

providing healthcare today.

AmerisourceBergen is poised for

future growth through building the

“best in class” distribution network

and continuing to acquire and develop

“best in class” value added services to

our provider and manufacturer customers.

We continue to identify new market

opportunities across the pharmaceutical

supply channel, focusing on prospects

with attractive growth rates, EBIT

margins, return on committed capital

(ROCC), and a solid strategic fit with our

core business. The right services and

solutions include those that drive market

share, drive efficiency, and improve

patient care for our provider and manu-

facturer customers alike. We continue

to build our logistics and inventory

management capabilities and to create

innovative tools for preserving product

integrity. We recognize that healthcare

is delivered locally and healthcare capital

is precious, so we focus on open

architecture solutions that allow our

customers to preserve existing invest-

ments and allow us to have maximum

flexibility in meeting their needs.

AmerisourceBergen is investing in

the business for the long-term, utilizing

a strategy of disciplined execution that

rewards our customers, our associates,

and our shareholders. Our Optimiz

program is increasing the capacity of

our distribution network through facility

consolidations, new construction,

and expansions of existing facilities.

The Optimiz program also standardizes

and upgrades warehouse management

systems across the network, improving

warehouse productivity as much as 40

percent. Two years into the integration

The specialty pharmaceutical market is rapidly evolving,and with infrastructure already in place whichsupported nearly $4 billion in specialty pharmaceuticalsales in fiscal year 2003, AmerisourceBergen is uniquelypositioned to take advantage of the growing opportunities.

7

Kurt J. HilzingerPresident and Chief Operating Officer

Average Revenue Per Square Foot in PharmaceuticalDistribution CentersFY Ending September 30

1999 2000 2001 2002 2003

$4,

910

$4,

222 $

5,67

6

$8,

322

$7,

086

AmerisourceBergen is well positioned to benefit from organic growth in the pharmaceutical market in

two ways: by delivering pharmaceutical products and unique services to the nation’s healthcare providers,

and by offering drug manufacturers value added programs and services to help them meet the demands

of the marketplace and preserve the integrity of the pharmaceutical supply channel.

We recognize that healthcare isdelivered locally and healthcarecapital is precious, so we focuson open architecture solutionsthat allow our customers topreserve existinginvestments and allow us to have maximum flexibility in meeting their needs.

8

process, AmerisourceBergen remains on

schedule and on budget. We have already

captured substantial synergy savings

well ahead of schedule, and we will

continue to capture additional savings

as we work toward the completion of

the build out process in 2007.

DefiningValuethe AmerisourceBergen Way.

Most recently, AmerisourceBergen

has expanded its value added services

portfolio to include additional capabilities

that enable us to help our customers

improve the effectiveness and the

efficiency of their businesses. For

example, our pharmacy automation

unit, AutoMed, offers fully scalable

and integratable equipment designed

to help alleviate the three major issues

facing all pharmacies today: rising costs,

the shortage of pharmacists, and the

need to reduce medication errors.

AutoMed has products and work flow

solutions that can be applied to every

type of provider customer in our portfolio

of business to improve operating

efficiency, consumer satisfaction, and

safety. AutoMed’s automation equipment

is currently in use in the mail order

fulfillment centers of three of the four

largest pharmacy benefit managers, and

we’ve taken the expertise gleaned from

those installations and made it available

to the rest of our provider customer base.

For retail customers, introducing

effective automation into their stores

means that pharmacists can better

manage workload, leaving more time

for counseling patients and building

business. For institutional customers,

utilizing AutoMed’s barcode enabled

automation systems means that facilities

can accurately and cost effectively track

medications and the entire dispensing

process literally from the loading dock

to the patient’s bedside.

AmerisourceBergen’s Bridge Medical

bedside verification system completes

the process by tracking, on a patient-

by-patient basis, that the right drug

is given in the right dose at the right

time. Improved medication tracking

dramatically improves a facility’s

knowledge of its drug inventory,

and can streamline the patient billing

process, yielding cost savings and

greater operating efficiency. All of

our systems are designed in an open

architecture format to allow customers

to preserve existing capital investments

and seamlessly integrate with existing

systems. Our own Choice Systems® experts

facilitate the process of technology

installation and integration, a service

unmatched in the industry.

AmerisourceBergen has strengthened

its relationships with the leading

branded and generic pharmaceutical

manufacturers to not only provide

product distribution services, but to

also offer contract packaging, product

marketing assistance, and reimbursement

consulting. Our goal is to continue our

growth by offering additional services

in the supply channel to manufacturers

thereby enhancing our ability to add

value and to allow our manufacturer

customers to focus on their core

business of developing, manufacturing,

and marketing pharmaceuticals.

AmerisourceBergen’s Packaging Group

consists of American Health Packaging,

which focuses on packaging for

providers, and Anderson Packaging,

which is a leader in packaging for

manufacturers. Both operations include

FDA-compliant facilities and state-of-

the-art equipment and product safety

technology. The packaging group is a

leader in patient compliance packaging,

patient safety initiatives and developing

anti-counterfeiting technologies.

Packaging involves taking bulk shipments

of pharmaceuticals received directly

from the manufacturers and packaging

the medications into usable formats,

whether it be in bottles, unit dose form,

Scan-A-Dose form, foil packs, punch

cards, or packaged for commercial sale

or product sample distribution. In the

process, all packages are imprinted with

a bar code, which enables the medication

tracking capabilities of AutoMed, Bridge

Medical, and other barcode scanning

systems. In all, AmerisourceBergen’s

Packaging Group has over one million

AmerisourceBergen Packaging Group is a leader in patient compliance packaging,patient safety initiatives, and developinganti-counterfeiting technologies.

9

square feet of capacity and over 75

packaging lines.

As more biotech and other specialty

products enter the marketplace,

AmerisourceBergen is also well positioned

to offer value added services to specialty

drug manufacturers and providers.

Specialty pharmaceuticals typically fit

the following profile: expensive products

geared towards a small patient population;

injectable products requiring special

handling and dosing; special adminis-

tration and patient support requirements;

and complex reimbursement procedures.

Specialty pharmaceutical products include

traditional pharmaceuticals requiring

special handling, biopharmaceuticals

such as those created using genetic

engineering, and therapeutic blood

plasma products.

AmerisourceBergen’s Specialty

Group business model begins with

identifying products with great potential,

preparing the market through practice

management, and expanding access

by developing a reimbursement model.

From that point, we focus on building

a distribution model that serves both

the provider and the patient, linking

distribution and reimbursement.

We promote both the patient access

and clinical sides of our model in the

marketplace, support patient monitoring,

and help providers to effectively manage

the patient experience. The specialty

pharmaceutical market is rapidly evolving,

and AmerisourceBergen is uniquely

positioned to take advantage of the

growing opportunities with a $4 billion

footprint already in place today.

Another growing segment of the

pharmaceutical marketplace in which

we operate is long term care (LTC)

pharmacy. AmerisourceBergen’s

PharMerica operations offer long term

care providers safe, cost-effective

distribution systems, medication

management services, and regulatory

compliance assistance. PharMerica also

offers manufacturers opportunities to

drive market share through participating

in our Senior Select Formulary®, as well

as valuable data which helps measure

product efficacy, utilization, and

compliance in the elderly population.

PharMerica offers institutional pharmacies

integrated medication management

systems capable of handling unit dose

distribution and intravenous infusion

systems, helping to improve safety and

reduce medication errors. Going forward,

PharMerica will take advantage of

opportunities to partner with other

AmerisourceBergen resources, such as

the Company’s comprehensive generic

drugs program, automation technology

from AutoMed, and/or packaging

solutions from AmerisourceBergen

Packaging Group to offer its customers

a comprehensive and customized

solution for their LTC pharmacy needs.

the Futurethe AmerisourceBergen Way.

AmerisourceBergen is committed

to improving healthcare in America by

delivering the best customer service in

the industry and continuing to quickly

adapt to the ever changing market.

These are exciting times in our industry,

and we remain confident that the

investments we have made in technology,

new facilities, new value added services

and the like will carry us forward well

into the future. We will continue to

adapt to the changing needs of our

customers, finding innovative ways

to be rewarded for exceptional service.

AmerisourceBergen is dedicated to

building on its success in the pharma-

ceutical supply channel and taking

advantage of the many opportunities

on the horizon to add value for our

customers and shareholders.

We have lowered expenses bytaking costs out of ouroperations, capturing merger related synergies, and leveragingour financial position.

PharMerica’s integratedmedication management and formulary programsdrive both optimal patientoutcomes and market share for pharmaceuticalmanufacturers.

10

Operating Revenue(in millions)FY Ending September 30

1999 2000 2001* 2002 2003

*AmeriSource merged with Bergen Brunswig in August 2001.

$11

,610

$9,

760

$15

,823

$45

,537

$40

,241

Defining

By leveraging our scale and building upon the framework of our essential role in the marketplace,we are able to provide exceptionalvalue to our provider and manufacturer customersas well as to our shareholders.

11Michael D. DiCandiloSenior Vice President and Chief Financial Officer

Among AmerisourceBergen’s long-term goals are to grow

revenue with the market, and increase earnings per share 15% or

more annually, excluding special items. We have the ability to make

moderately sized acquisitions and expect to continue our disciplined

acquisition activity with the right opportunities.

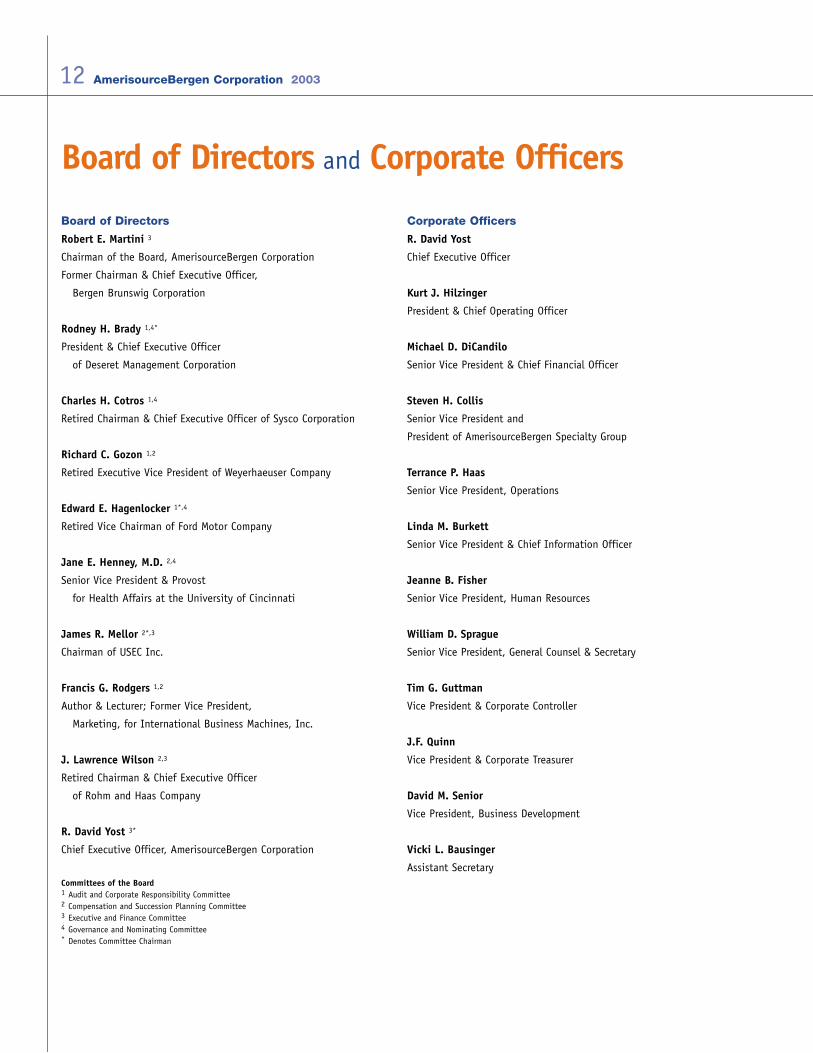

Board of Directors

Robert E. Martini 3

Chairman of the Board, AmerisourceBergen Corporation

Former Chairman & Chief Executive Officer,

Bergen Brunswig Corporation

Rodney H. Brady 1,4*

President & Chief Executive Officer

of Deseret Management Corporation

Charles H. Cotros 1,4

Retired Chairman & Chief Executive Officer of Sysco Corporation

Richard C. Gozon 1,2

Retired Executive Vice President of Weyerhaeuser Company

Edward E. Hagenlocker 1*,4

Retired Vice Chairman of Ford Motor Company

Jane E. Henney, M.D. 2,4

Senior Vice President & Provost

for Health Affairs at the University of Cincinnati

James R. Mellor 2*,3

Chairman of USEC Inc.

Francis G. Rodgers 1,2

Author & Lecturer; Former Vice President,

Marketing, for International Business Machines, Inc.

J. Lawrence Wilson 2,3

Retired Chairman & Chief Executive Officer

of Rohm and Haas Company

R. David Yost 3*

Chief Executive Officer, AmerisourceBergen Corporation

Committees of the Board1 Audit and Corporate Responsibility Committee2 Compensation and Succession Planning Committee3 Executive and Finance Committee4 Governance and Nominating Committee* Denotes Committee Chairman

Corporate Officers

R. David Yost

Chief Executive Officer

Kurt J. Hilzinger

President & Chief Operating Officer

Michael D. DiCandilo

Senior Vice President & Chief Financial Officer

Steven H. Collis

Senior Vice President and

President of AmerisourceBergen Specialty Group

Terrance P. Haas

Senior Vice President, Operations

Linda M. Burkett

Senior Vice President & Chief Information Officer

Jeanne B. Fisher

Senior Vice President, Human Resources

William D. Sprague

Senior Vice President, General Counsel & Secretary

Tim G. Guttman

Vice President & Corporate Controller

J.F. Quinn

Vice President & Corporate Treasurer

David M. Senior

Vice President, Business Development

Vicki L. Bausinger

Assistant Secretary

Board of Directors and Corporate Officers

12 AmerisourceBergen Corporation 2003

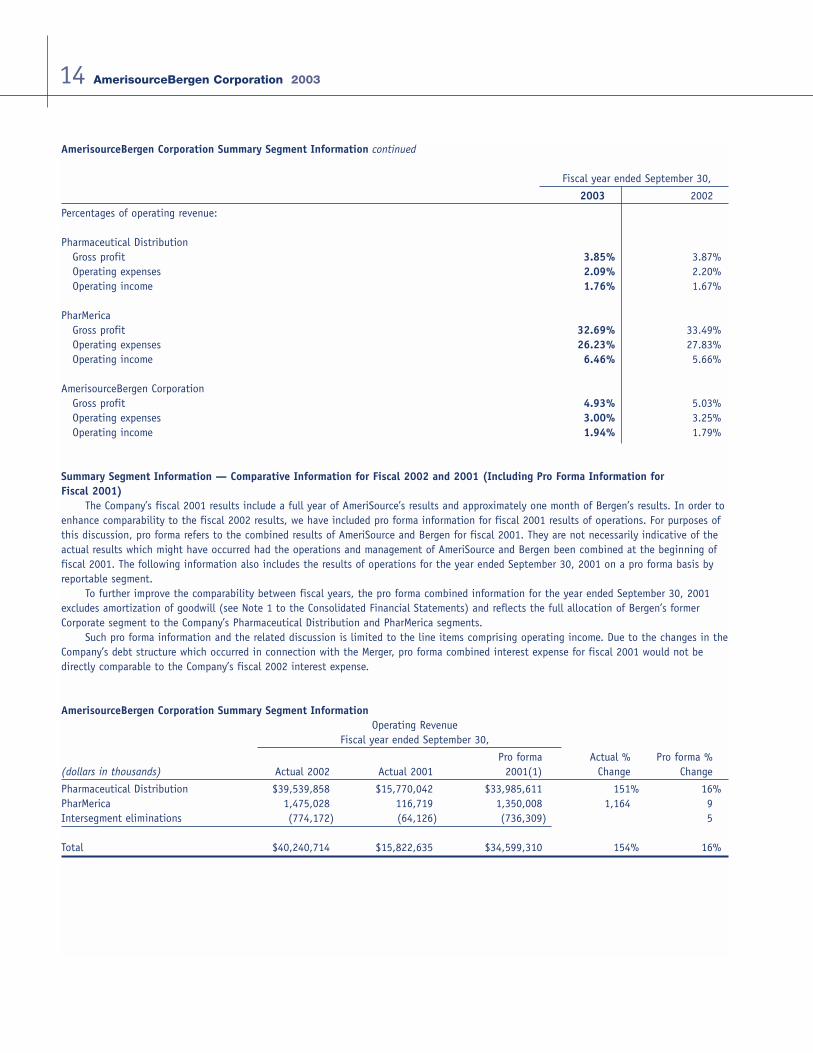

Summary Segment Information — Comparative Information for Fiscal 2003 and 2002

AmerisourceBergen Corporation Summary Segment Information

Operating RevenueFiscal year ended September 30,

(dollars in thousands) 2003 2002 Change

Pharmaceutical Distribution $44,731,200 $39,539,858 13%PharMerica 1,608,203 1,475,028 9Intersegment eliminations (802,714) (774,172) (4)

Total $45,536,689 $40,240,714 13%

Operating IncomeFiscal year ended September 30,

(dollars in thousands) 2003 2002 Change

Pharmaceutical Distribution $788,193 $659,208 20%PharMerica 103,843 83,464 24Facility consolidations and employee severance

and merger costs (“special items”) (8,930) (24,244) 63

Total $883,106 $718,428 23%

Management’s Discussion and Analysisof Financial Condition and Results of Operations

The following discussion should be read in conjunction with theConsolidated Financial Statements and notes thereto contained herein.

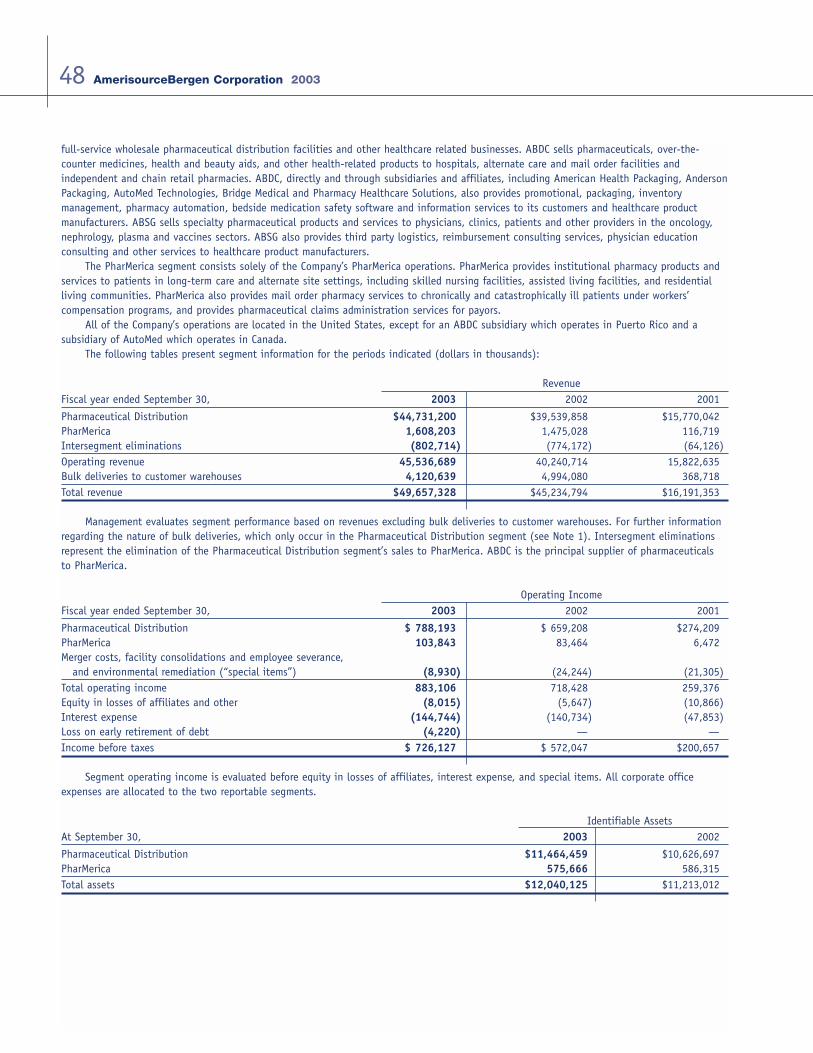

The CompanyAmerisourceBergen Corporation (the “Company”) is a leading

national wholesale distributor of pharmaceutical products and relatedhealthcare services and solutions with $45.5 billion in annual operat-ing revenue. The Company was formed in connection with the mergerof AmeriSource Health Corporation (“AmeriSource”) and BergenBrunswig Corporation (“Bergen”) on August 29, 2001 (the “Merger”).

The Company is organized based upon the products and servicesit provides to its customers. The Company’s operating segments havebeen aggregated into two reportable segments: PharmaceuticalDistribution and PharMerica.

The Pharmaceutical Distribution segment includesAmerisourceBergen Drug Corporation (“ABDC”) and AmerisourceBergenSpecialty Group (“ABSG”). ABDC includes the full-service wholesalepharmaceutical distribution facilities and other healthcare relatedbusinesses. ABDC sells pharmaceuticals, over-the-counter medicines,health and beauty aids, and other health-related products to hospi-

tals, alternate care and mail order facilities and independent andchain retail pharmacies. ABDC, directly and through subsidiaries andaffiliates, including American Health Packaging, Anderson Packaging,AutoMed Technologies, Bridge Medical and Pharmacy HealthcareSolutions, also provides promotional, packaging, inventory manage-ment, pharmacy automation, bedside medication safety software andinformation services to its customers and healthcare product manu-facturers. ABSG sells specialty pharmaceutical products and servicesto physicians, clinics, patients and other providers in the oncology,nephrology, plasma and vaccines sectors. ABSG also provides thirdparty logistics, reimbursement consulting services, physician educationconsulting and other services to healthcare product manufacturers.

The PharMerica segment consists solely of the Company’sPharMerica operations. PharMerica provides institutional pharmacyproducts and services to patients in long-term care and alternate sitesettings, including skilled nursing facilities, assisted living facilities,and residential living communities. PharMerica also provides mailorder and on-line pharmacy services to chronically and catastrophi-cally ill patients under workers’ compensation programs, and providespharmaceutical claims administration services for payors.

132003 AmerisourceBergen Corporation

AmerisourceBergen Corporation Summary Segment Information continued

Fiscal year ended September 30,

2003 2002

Percentages of operating revenue:

Pharmaceutical DistributionGross profit 3.85% 3.87%Operating expenses 2.09% 2.20%Operating income 1.76% 1.67%

PharMericaGross profit 32.69% 33.49%Operating expenses 26.23% 27.83%Operating income 6.46% 5.66%

AmerisourceBergen CorporationGross profit 4.93% 5.03%Operating expenses 3.00% 3.25%Operating income 1.94% 1.79%

Summary Segment Information — Comparative Information for Fiscal 2002 and 2001 (Including Pro Forma Information for Fiscal 2001)

The Company’s fiscal 2001 results include a full year of AmeriSource’s results and approximately one month of Bergen’s results. In order toenhance comparability to the fiscal 2002 results, we have included pro forma information for fiscal 2001 results of operations. For purposes ofthis discussion, pro forma refers to the combined results of AmeriSource and Bergen for fiscal 2001. They are not necessarily indicative of theactual results which might have occurred had the operations and management of AmeriSource and Bergen been combined at the beginning offiscal 2001. The following information also includes the results of operations for the year ended September 30, 2001 on a pro forma basis byreportable segment.

To further improve the comparability between fiscal years, the pro forma combined information for the year ended September 30, 2001excludes amortization of goodwill (see Note 1 to the Consolidated Financial Statements) and reflects the full allocation of Bergen’s formerCorporate segment to the Company’s Pharmaceutical Distribution and PharMerica segments.

Such pro forma information and the related discussion is limited to the line items comprising operating income. Due to the changes in theCompany’s debt structure which occurred in connection with the Merger, pro forma combined interest expense for fiscal 2001 would not bedirectly comparable to the Company’s fiscal 2002 interest expense.

AmerisourceBergen Corporation Summary Segment InformationOperating Revenue

Fiscal year ended September 30,

Pro forma Actual % Pro forma %(dollars in thousands) Actual 2002 Actual 2001 2001(1) Change Change

Pharmaceutical Distribution $39,539,858 $15,770,042 $33,985,611 151% 16%PharMerica 1,475,028 116,719 1,350,008 1,164 9Intersegment eliminations (774,172) (64,126) (736,309) 5

Total $40,240,714 $15,822,635 $34,599,310 154% 16%

14 AmerisourceBergen Corporation 2003

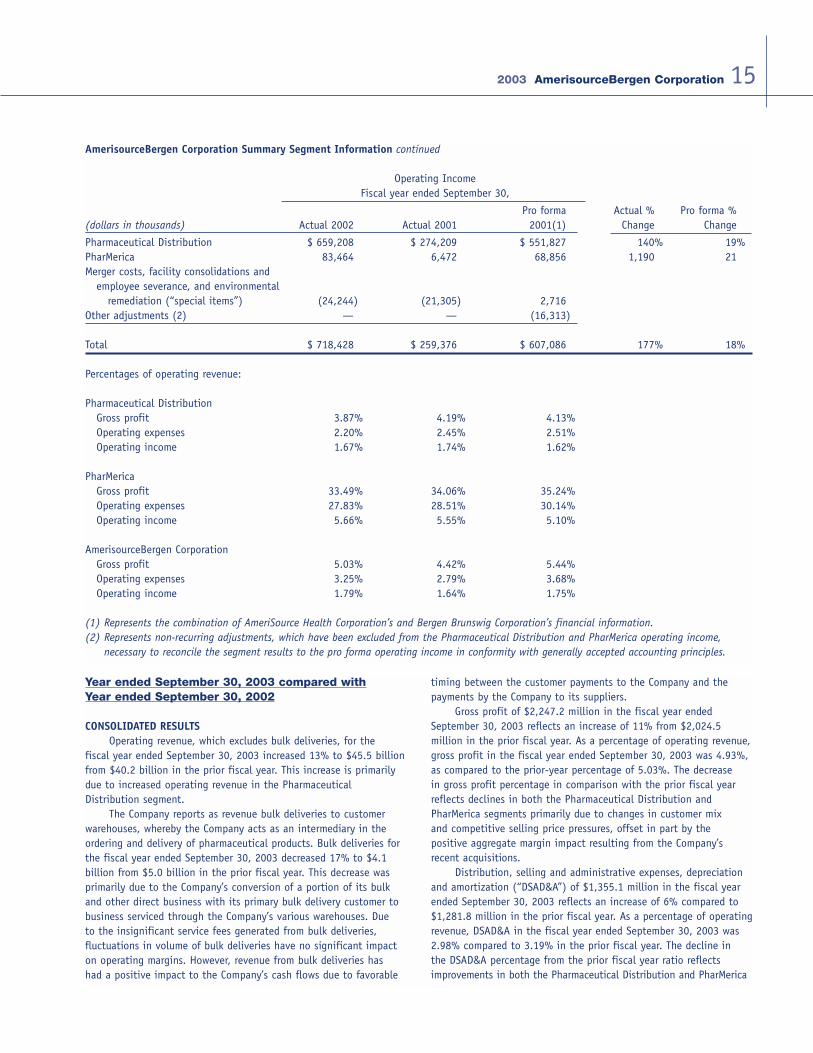

AmerisourceBergen Corporation Summary Segment Information continued

Operating IncomeFiscal year ended September 30,

Pro forma Actual % Pro forma %(dollars in thousands) Actual 2002 Actual 2001 2001(1) Change Change

Pharmaceutical Distribution $ 659,208 $ 274,209 $ 551,827 140% 19%PharMerica 83,464 6,472 68,856 1,190 21Merger costs, facility consolidations and

employee severance, and environmental remediation (“special items”) (24,244) (21,305) 2,716

Other adjustments (2) — — (16,313)

Total $ 718,428 $ 259,376 $ 607,086 177% 18%

Percentages of operating revenue:

Pharmaceutical DistributionGross profit 3.87% 4.19% 4.13%Operating expenses 2.20% 2.45% 2.51%Operating income 1.67% 1.74% 1.62%

PharMericaGross profit 33.49% 34.06% 35.24%Operating expenses 27.83% 28.51% 30.14%Operating income 5.66% 5.55% 5.10%

AmerisourceBergen CorporationGross profit 5.03% 4.42% 5.44%Operating expenses 3.25% 2.79% 3.68%Operating income 1.79% 1.64% 1.75%

(1) Represents the combination of AmeriSource Health Corporation’s and Bergen Brunswig Corporation’s financial information.(2) Represents non-recurring adjustments, which have been excluded from the Pharmaceutical Distribution and PharMerica operating income,

necessary to reconcile the segment results to the pro forma operating income in conformity with generally accepted accounting principles.

152003 AmerisourceBergen Corporation

Year ended September 30, 2003 compared withYear ended September 30, 2002

CONSOLIDATED RESULTSOperating revenue, which excludes bulk deliveries, for the

fiscal year ended September 30, 2003 increased 13% to $45.5 billionfrom $40.2 billion in the prior fiscal year. This increase is primarilydue to increased operating revenue in the PharmaceuticalDistribution segment.

The Company reports as revenue bulk deliveries to customerwarehouses, whereby the Company acts as an intermediary in theordering and delivery of pharmaceutical products. Bulk deliveries forthe fiscal year ended September 30, 2003 decreased 17% to $4.1 billion from $5.0 billion in the prior fiscal year. This decrease wasprimarily due to the Company’s conversion of a portion of its bulkand other direct business with its primary bulk delivery customer tobusiness serviced through the Company’s various warehouses. Due to the insignificant service fees generated from bulk deliveries, fluctuations in volume of bulk deliveries have no significant impacton operating margins. However, revenue from bulk deliveries has had a positive impact to the Company’s cash flows due to favorable

timing between the customer payments to the Company and the payments by the Company to its suppliers.

Gross profit of $2,247.2 million in the fiscal year endedSeptember 30, 2003 reflects an increase of 11% from $2,024.5 million in the prior fiscal year. As a percentage of operating revenue,gross profit in the fiscal year ended September 30, 2003 was 4.93%,as compared to the prior-year percentage of 5.03%. The decrease in gross profit percentage in comparison with the prior fiscal yearreflects declines in both the Pharmaceutical Distribution andPharMerica segments primarily due to changes in customer mix and competitive selling price pressures, offset in part by the positive aggregate margin impact resulting from the Company’srecent acquisitions.

Distribution, selling and administrative expenses, depreciationand amortization (“DSAD&A”) of $1,355.1 million in the fiscal yearended September 30, 2003 reflects an increase of 6% compared to$1,281.8 million in the prior fiscal year. As a percentage of operatingrevenue, DSAD&A in the fiscal year ended September 30, 2003 was2.98% compared to 3.19% in the prior fiscal year. The decline in the DSAD&A percentage from the prior fiscal year ratio reflectsimprovements in both the Pharmaceutical Distribution and PharMerica

segments due to customer mix changes, operational efficiencies andcontinued benefits from the merger integration effort.

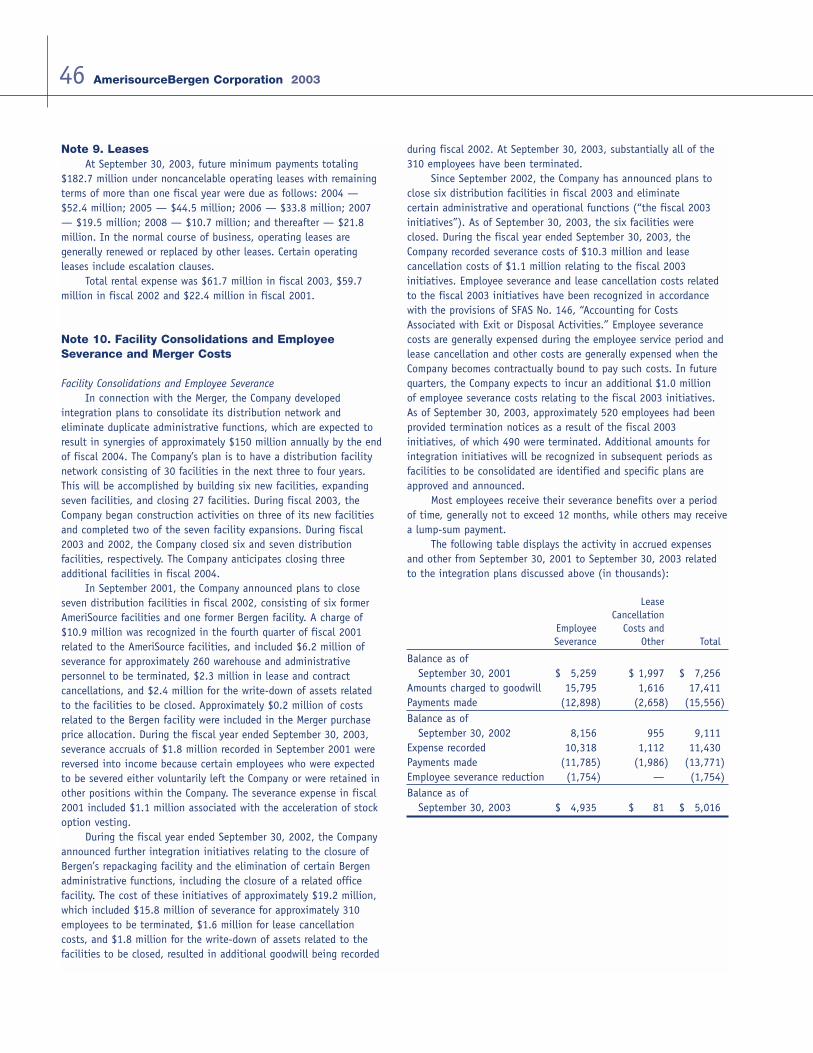

In connection with the Merger, the Company developed integration plans to consolidate its distribution network and eliminate duplicate administrative functions, which are expected toresult in synergies of approximately $150 million annually by the endof fiscal 2004. The Company’s plan is to have a distribution facilitynetwork consisting of 30 facilities in the next three to four years.This will be accomplished by building six new facilities, expandingseven facilities, and closing 27 facilities. During fiscal 2003, theCompany began construction activities on three of its new facilitiesand completed two of the seven facility expansions. During fiscal2003 and 2002, the Company closed six and seven distribution facilities, respectively. The Company anticipates closing three additional facilities in fiscal 2004.

In September 2001, the Company announced plans to closeseven distribution facilities in fiscal 2002, consisting of six formerAmeriSource facilities and one former Bergen facility. A charge of$10.9 million was recognized in the fourth quarter of fiscal 2001related to the AmeriSource facilities, and included $6.2 million ofseverance for approximately 260 warehouse and administrative personnel to be terminated, $2.3 million in lease and contract cancellations, and $2.4 million for the write-down of assets relatedto the facilities to be closed. Approximately $0.2 million of costsrelated to the Bergen facility were included in the Merger purchaseprice allocation. During the fiscal year ended September 30, 2003,severance accruals of $1.8 million recorded in September 2001 werereversed into income because certain employees who were expectedto be severed either voluntarily left the Company or were retained inother positions within the Company.

During the fiscal year ended September 30, 2002, the Companyannounced further integration initiatives relating to the closure ofBergen’s repackaging facility and the elimination of certain Bergenadministrative functions, including the closure of a related officefacility. The cost of these initiatives of approximately $19.2 million,which included $15.8 million of severance for approximately 310employees to be terminated, $1.6 million for lease cancellationcosts, and $1.8 million for the write-down of assets related to thefacilities to be closed, resulted in additional goodwill being recordedduring fiscal 2002. At September 30, 2003, substantially all of the310 employees have been terminated.

Since September 2002, the Company has announced plans toclose six distribution facilities in fiscal 2003 and eliminate certainadministrative and operational functions (“the fiscal 2003 initia-tives”). As of September 30, 2003, the six facilities were closed.During the fiscal year ended September 30, 2003, the Companyrecorded severance costs of $10.3 million and lease cancellationcosts of $1.1 million relating to the fiscal 2003 initiatives. Employeeseverance and lease cancellation costs related to the fiscal 2003 initiatives have been recognized in accordance with the provisions of Statement of Financial Accounting Standards (“SFAS”) No. 146,“Accounting for Costs Associated with Exit or Disposal Activities.”Employee severance costs are generally expensed during the employ-ee service period and lease cancellation and other costs are generallyexpensed when the Company becomes contractually bound to paysuch costs. In the future, the Company expects to incur an additional$1.0 million of employee severance costs relating to the fiscal 2003

initiatives. As of September 30, 2003, approximately 520 employeeshad been provided termination notices as a result of the fiscal 2003initiatives, of which 490 were terminated. Additional amounts forintegration initiatives will be recognized in subsequent periods asfacilities to be consolidated are identified and specific plans areapproved and announced.

The Company paid a total of $13.8 million and $15.6 million foremployee severance and lease and contract cancellation costs in thefiscal years ended September 30, 2003 and 2002, respectively, related to the aforementioned integration plans. Remaining unpaidamounts of $5.0 million for employee severance and lease cancella-tion costs are included in accrued expenses and other in the accompanying consolidated balance sheet at September 30, 2003.Most employees receive their severance benefits over a period oftime, generally not to exceed 12 months, while others may receive a lump-sum payment.

During the fiscal year ended September 30, 2002, the Companyexpensed approximately $24.2 million of merger costs, primarilyrelated to integrating the operations of AmeriSource and Bergen.Such costs were comprised primarily of consulting fees, whichamounted to $16.6 million. The merger costs also included a $2.1million adjustment to the Company’s fourth quarter 2001 charge of$6.5 million relating to the accelerated vesting of AmeriSource stockoptions. Effective October 1, 2002, the Company converted its merger integration office to an operations management office.Accordingly, the costs of the operations management office areincluded within distribution, selling and administrative expenses inthe Company’s consolidated statements of operations.

Operating income of $883.1 million for the fiscal year endedSeptember 30, 2003 reflects an increase of 23% from $718.4 millionin the prior fiscal year. Special items reduced the Company’s operat-ing income by $8.9 million in the fiscal year ended September 30,2003 and by $24.2 million in the prior fiscal year. The Company’soperating income as a percentage of operating revenue was 1.94% inthe fiscal year ended September 30, 2003 compared to 1.79% in theprior fiscal year. The improvement was primarily due to the loweramount of special items and the aforementioned DSAD&A expensepercentage reduction.

The Company recorded equity in losses of affiliates and other of $8.0 million and $5.6 million during the fiscal years endedSeptember 30, 2003 and 2002, respectively. These amounts primarily consisted of impairment charges relating to investments in technology companies.

During the fiscal year ended September 30, 2003, the Companyrecorded a $4.2 million loss resulting from the early retirement ofdebt (see Note 5 of “Notes to Consolidated Financial Statements”).

Interest expense increased 3% in the fiscal year endedSeptember 30, 2003 to $144.7 million from $140.7 million in theprior fiscal year. Average borrowings, net of invested cash, under theCompany’s debt facilities during the fiscal year ended September 30,2003 were $2.3 billion as compared to average borrowings, net of invested cash, of $2.0 billion in the prior fiscal year. Average borrowing rates under the Company’s debt facilities decreased to5.6% in the current fiscal year from 6.1% in the prior fiscal year. Theincrease in average borrowings, net of invested cash, was primarily a result of additional merchandise inventories on hand during thecurrent fiscal year compared to the prior fiscal year. The decrease in

16 AmerisourceBergen Corporation 2003

average borrowing rates resulted from lower percentages of fixed-ratedebt outstanding to total debt outstanding in the current fiscal yearcompared to the prior fiscal year, as well as lower market interestrates on variable-rate debt.

Income tax expense of $284.9 million in the fiscal year endedSeptember 30, 2003 reflects an effective tax rate of 39.2%, versus39.7% in the prior fiscal year. The Company has been able to lowerits effective tax rate during the current fiscal year by implementingtax planning strategies.

Net income of $441.2 million for the fiscal year endedSeptember 30, 2003 reflects an increase of 28% from $344.9 millionin the prior fiscal year. Diluted earnings per share of $3.89 in thefiscal year ended September 30, 2003 reflects a 23% increase ascompared to $3.16 per share in the prior fiscal year. Special itemsand the loss on early retirement of debt had the effect of decreasingnet income by $8.0 million and reducing diluted earnings per shareby $0.07 for the fiscal year ended September 30, 2003. Special items had the effect of decreasing net income by $14.6 million and reducing diluted earnings per share by $0.13 for the fiscal yearended September 30, 2002. The growth in earnings per share wassmaller than the growth in net income for the fiscal year endedSeptember 30, 2003 due to the issuance of Company common stockin connection with the acquisitions described in Note 2 to theCompany’s consolidated financial statements and in connection with the exercise of stock options.

SEGMENT INFORMATION

Pharmaceutical Distribution SegmentPharmaceutical Distribution operating revenue of $44.7 billion

for the fiscal year ended September 30, 2003 reflects an increase of13% from $39.5 billion in the prior fiscal year. The Company’s recentacquisitions contributed less than 0.5% of the segment’s operatingrevenue growth for the fiscal year ended September 30, 2003. Duringthe fiscal year ended September 30, 2003, 56% of operating revenuewas from sales to institutional customers and 44% was from retailcustomers; this compares to a customer mix in the prior fiscal yearof 53% institutional and 47% retail. In comparison with the prior-year results, sales to institutional customers increased 20% primarilydue to (i) the previously mentioned conversion of bulk delivery andother direct business with the Company’s primary bulk delivery customer to business serviced through the Company’s various warehouses, which contributed 4% of the total operating revenuegrowth; (ii) above market rate growth of the ABSG specialty pharma-ceutical business; and (iii) higher revenues from customers engagedin the mail order sale of pharmaceuticals. Sales to retail customersincreased by 5% in comparison to the prior fiscal year. The growthrate of sales to retail customers has declined during fiscal 2003 compared to the fiscal 2002 growth primarily due to lower growthtrends in the retail market and the below market growth of certain of the Company’s large regional chain customers. Additionally, retailsales in the second-half of fiscal 2003 were adversely impacted bythe loss of a large customer. This segment’s growth largely reflectsU.S. pharmaceutical industry conditions, including increases in prescription drug utilization and higher pharmaceutical prices offset,in part, by the increased use of lower priced generics. The segment’sgrowth has also been impacted by industry competition and changes

in customer mix. Industry growth rates, as estimated by industrydata firm IMS Healthcare, Inc., are expected to be between 10% and13% over the next four years. Future operating revenue growth willcontinue to be driven by industry growth trends, competition withinthe industry and customer consolidation.

Pharmaceutical Distribution gross profit of $1,721.5 million inthe fiscal year ended September 30, 2003 reflects an increase of 12%from $1,530.5 million in the prior fiscal year. As a percentage ofoperating revenue, gross profit in the fiscal year ended September30, 2003 was 3.85%, as compared to 3.87% in the prior fiscal year.The slight decline in gross profit as a percentage of operating revenue was the net result of the negative impact of a change incustomer mix to a higher percentage of large institutional, mail order and chain accounts, and the continuing competitive pricingenvironment, offset primarily by the positive aggregate impact ofrecently-acquired companies, which amounted to 15 basis points inthe fiscal year ended September 30, 2003. Downward pressures onsell-side gross profit margin are expected to continue and there canbe no assurance that the inclusion of additional businesses that generate higher margins or that increases in the buy-side componentof the gross margin, including increases derived from manufacturerprice increases, negotiated deals and secondary market opportunities,will be available in the future to fully or partially offset the antici-pated decline of the sell-side margin. The Company expects that buy-side opportunities may decrease in the future as pharmaceuticalmanufacturers increasingly seek to control the supply channelthrough product allocations that limit the inventory the Companycan purchase and through the imposition of inventory managementand other agreements that prohibit or severely restrict the Company’sright to purchase inventory from secondary source suppliers.Although the Company seeks in any such agreements to obtainappropriate compensation from pharmaceutical manufacturers forforegoing buy-side opportunities, there can be no assurance that theagreements will function as intended and replace any or all lost profitopportunities. The Company’s cost of goods sold includes a last-in,first-out (“LIFO”) provision that is affected by changes in inventoryquantities, product mix, and manufacturer pricing practices, whichmay be impacted by market and other external influences.

Pharmaceutical Distribution operating expenses of $933.3 million in the fiscal year ended September 30, 2003 reflects anincrease of 7% from $871.3 million in the prior fiscal year. As a percentage of operating revenue, operating expenses in the fiscalyear ended September 30, 2003 were 2.09%, as compared to 2.20%in the prior fiscal year. The decrease in the expense percentagereflects the changing customer mix described above, efficiencies of scale, the elimination of redundant costs through the merger integration process, the continued emphasis on productivity through-out the Company’s distribution network and a reduction of bad debtexpense, offset, in part, by higher expense ratios associated with theCompany’s recent acquisitions.

Pharmaceutical Distribution operating income of $788.2 millionin the fiscal year ended September 30, 2003 reflects an increase of20% from $659.2 million in the prior fiscal year. As a percentage ofoperating revenue, operating income in the fiscal year endedSeptember 30, 2003 was 1.76%, as compared to 1.67% in the priorfiscal year. The improvement over the prior-year percentage was dueto a reduction in the operating expense ratio in excess of the decline

172003 AmerisourceBergen Corporation

in gross margin, which was partially the result of the Company’s ability to capture synergy cost savings from the Merger. While management historically has been able to lower expense ratios and expects to continue to do so, there can be no assurance thatreductions will occur in the future, or that expense ratio reductionswill exceed possible declines in gross margins. Additionally, there canbe no assurance that merger integration efforts will proceed asplanned or result in the desired cost savings.

PharMerica SegmentPharMerica’s operating revenue increased 9% for the fiscal

year ended September 30, 2003 to $1,608.2 million compared to$1,475.0 million in the prior fiscal year. This increase is principallyattributable to the growth in PharMerica’s workers’ compensationbusiness, which has grown at a faster rate than its long-term carebusiness. During the second-half of fiscal 2003, the growth rate ofthe workers’ compensation business began to slow down, partiallydue to the loss of a significant customer. The slow down in the workers’ compensation business is expected to continue in fiscal2004 and as a result, the operating revenue growth rate in fiscal2004 for the PharMerica segment is expected to be in the mid-singledigits. The future operating revenue growth rate will be impacted bycompetitive pressures, changes in the regulatory environment andthe pharmaceutical inflation rate.

PharMerica’s gross profit of $525.6 million for the fiscal yearended September 30, 2003 increased 6% from gross profit of $494.0million in the prior fiscal year. PharMerica’s gross profit margindeclined slightly to 32.69% for the fiscal year ended September 30,2003 from 33.49% in the prior fiscal year. This decrease is primarilythe result of a change in the sales mix, with a greater proportion of PharMerica’s current year revenues coming from its workers’ compensation business, which has lower gross profit margins andlower operating expenses than its long-term care business. In addition, industry competitive pressures continue to adversely affect gross profit margins.

PharMerica’s operating expenses of $421.8 million for the fiscalyear ended September 30, 2003 increased from $410.5 million in theprior fiscal year. As a percentage of operating revenue, operatingexpenses were reduced to 26.23% in the fiscal year ended September30, 2003 from 27.83% in the prior fiscal year. The percentage reduc-tion was primarily due to the continued improvements in operatingpractices, the aforementioned shift in customer mix towards theworkers’ compensation business and a reduction in bad debt expense.

PharMerica’s operating income of $103.8 million for the fiscalyear ended September 30, 2003 increased by 24% from $83.5 millionin the prior fiscal year. As a percentage of operating revenue, operatingincome in the fiscal year ended September 30, 2003 was 6.46%, ascompared to 5.66% in the prior fiscal year. The improvement was due to the aforementioned reduction in the operating expense ratio,which was greater than the reduction in gross profit margin. Whilemanagement historically has been able to lower expense ratios andexpects to continue to do so, there can be no assurance that reductions will occur in the future, or that expense ratio reductionswill exceed possible further declines in gross margins.

Intersegment EliminationsThese amounts represent the elimination of the Pharmaceutical

Distribution segment’s sales to PharMerica. AmerisourceBergen DrugCompany is the principal supplier of pharmaceuticals to PharMerica.

Year ended September 30, 2002 compared withYear ended September 30, 2001

CONSOLIDATED RESULTSOperating revenue, which excludes bulk deliveries, for the fiscal

year ended September 30, 2002 increased 154% to $40.2 billionfrom $15.8 billion in the prior fiscal year. This increase is primarilydue to increased operating revenue in the PharmaceuticalDistribution segment as a result of the Merger. Operating revenueincreased 16% from $34.6 billion in the prior fiscal year on a proforma combined basis. This increase is primarily due to the 16%increase in the Pharmaceutical Distribution segment.

The Company reports as revenue bulk deliveries to customerwarehouses, whereby the Company acts as an intermediary in theordering and delivery of pharmaceutical products. As a result of theMerger, bulk deliveries increased to $5.0 billion in the fiscal yearended September 30, 2002 compared to $368.7 million in the priorfiscal year. Revenue from bulk deliveries increased 10% from $4.5billion in the prior fiscal year on a pro forma combined basis. Due tothe insignificant service fees generated from these bulk deliveries,fluctuations in volume have no significant impact on operating margins. However, revenue from bulk deliveries has a positive impactto the Company’s cash flows due to favorable timing between thecustomer payments to us and the payments by us to our suppliers.

Gross profit of $2,024.5 million in the fiscal year endedSeptember 30, 2002 reflects an increase of 189% from $700.1 million in the prior fiscal year on a historical basis and an increaseof 8% from $1,880.7 million in the prior fiscal year on a pro formacombined basis. As a percentage of operating revenue, gross profit inthe fiscal year ended September 30, 2002 was 5.03%, as comparedto prior-year percentages of 4.42% on a historical basis and 5.44%on a pro forma combined basis. The increase in the gross profit percentage from prior fiscal year historical results was primarily dueto the inclusion of PharMerica in the current year. PharMerica, due tothe nature of its prescription fulfillment business, has significantlyhigher gross margins and operating expense ratios than theCompany’s Pharmaceutical Distribution segment. The decrease ingross profit percentage in comparison with the prior fiscal year pro forma combined percentage reflects declines in both thePharmaceutical Distribution and PharMerica segments due to changes in customer mix and competitive selling price pressures.

Distribution, selling and administrative expenses, depreciationand amortization (“DSAD&A”) of $1,281.8 million in the fiscal yearended September 30, 2002 reflects an increase of 206% compared to$419.4 million in the prior fiscal year on a historical basis and anincrease of less than 1% compared to $1,276.4 million in the priorfiscal year on a pro forma combined basis. As a percentage of operating revenue, DSAD&A in the fiscal year ended September 30,2002 was 3.19%, as compared to prior fiscal year percentages of2.65% on a historical basis and 3.69% on a pro forma combined

18 AmerisourceBergen Corporation 2003

basis. The increases in the DSAD&A percentage from the prior fiscalyear historical results were primarily due to the inclusion ofPharMerica in the current year, as explained above. The decrease inthe DSAD&A percentage from the prior fiscal year pro forma combinedratio reflects improvements in both the Pharmaceutical Distributionand PharMerica segments due to customer mix changes, operationalefficiencies and benefits from the merger integration effort.

In connection with the Merger, the Company developed integration plans to consolidate its distribution network and eliminate duplicate administrative functions, which are expected toresult in synergies of approximately $150 million annually by the endof fiscal 2004. The Company’s plan is to have a distribution facilitynetwork consisting of 30 facilities in the next three to four years.This will be accomplished by building six new facilities, expandingseven facilities, and closing 27 facilities. During 2002, the Companyclosed seven distribution facilities.

In September 2001, the Company announced plans to closeseven distribution facilities in fiscal 2002, consisting of six formerAmeriSource facilities and one former Bergen facility. A charge of$10.9 million was recognized in the fourth quarter of fiscal 2001related to the AmeriSource facilities, and included $6.2 million ofseverance for approximately 260 warehouse and administrative personnel to be terminated, $2.3 million in lease and contract cancellations, and $2.4 million for the write-down of assets relatedto the facilities to be closed. Approximately $0.2 million of costsrelated to the Bergen facility were included in the Merger purchaseprice allocation.

During the fiscal year ended September 30, 2002, the Companyannounced further integration initiatives relating to the closure ofBergen’s repackaging facility and the elimination of certain Bergenadministrative functions, including the closure of a related officefacility. The cost of these initiatives of approximately $19.2 million,which included $15.8 million of severance for approximately 310employees to be terminated, $1.6 million for lease cancellationcosts, and $1.8 million for the write-down of assets related to thefacilities to be closed, resulted in additional goodwill being recordedduring fiscal 2002.

In connection with the Merger, the Company expensed mergercosts in the fiscal year ended September 30, 2002 of $24.2 million,consisting primarily of integration consulting fees of $16.6 million.The merger costs also included a $2.1 million increase to theCompany’s fourth quarter fiscal 2001 charge of $6.5 million relatingto the accelerated vesting of AmeriSource stock options. Total mergercosts in fiscal 2001 amounted to $13.1 million, primarily consistingof consulting fees and the accelerated stock option vesting charge.

Operating income of $718.4 million for the fiscal year endedSeptember 30, 2002 reflects an increase of 177% from $259.4 millionin the prior fiscal year. Special items had the effect of reducing theCompany’s operating income in the fiscal year ended September 30,2002 and 2001 by $24.2 million and $21.3 million, respectively. The Company’s operating income as a percentage of operating revenue was 1.79% in the fiscal year ended September 30, 2002, ascompared to prior-year percentages of 1.64% on a historical basisand 1.75% on a pro forma combined basis. The improvements aredue to the aforementioned DSAD&A expense percentage reductionsmore than offsetting the reductions in gross margin.

Equity in losses of affiliates and other was $5.6 million and$10.9 million in fiscal 2002 and fiscal 2001, respectively. The fiscal2002 amount principally reflects an impairment of the Company’sinvestment in a healthcare technology company. The majority of the fiscal 2001 amount represents the impact of the Company’sinvestment in Health Nexus, LLC, which was accounted for on theequity method. The Company’s percentage ownership in the successorto Health Nexus, LLC fell below 20% in November 2001, and thisinvestment is now accounted for using the cost method.

Interest expense, which includes the distributions on preferredsecurities of a subsidiary trust, increased 194% in the fiscal yearended September 30, 2002 to $140.7 million compared to $47.9 million in the prior fiscal year, primarily as a result of the Merger.Average borrowings, net of invested cash, under the Company’s debtfacilities during the fiscal year ended September 30, 2002 were $2.0billion as compared to average borrowings, net of invested cash, of$696 million in the prior fiscal year. Average borrowing rates underthe Company’s variable-rate debt facilities decreased to 3.5% in thecurrent fiscal year from 6.2% in the prior fiscal year, due to lowermarket interest rates.

Income tax expense of $227.1 million in the fiscal year endedSeptember 30, 2002 reflects an effective tax rate of 39.7% versus38.3% in the prior fiscal year. The tax rate for fiscal 2002 was higherthan the prior fiscal year’s tax rate as a result of the Merger.

Net income of $344.9 million for the fiscal year endedSeptember 30, 2002 reflects an increase of 179% from $123.8 million in the prior fiscal year. Diluted earnings per share of $3.16 inthe fiscal year ended September 30, 2002 reflects a 50% increase ascompared to $2.10 per share in the prior fiscal year. Special itemshad the effect of reducing net income and diluted earnings per sharefor the fiscal year ended September 30, 2002 by $14.6 million and$0.13, respectively, and for the fiscal year ended September 30,2001 by $13.1 million and $0.21, respectively. Diluted earnings per share for the fiscal year ended September 30, 2002 reflects the full-year impact of the shares issued to effect the Merger.

SEGMENT INFORMATION

Pharmaceutical Distribution SegmentPharmaceutical Distribution operating revenue of $39.5 billion

for the fiscal year ended September 30, 2002 increased 151% from$15.8 billion in the prior fiscal year on a historical basis andincreased 16% from $34.0 billion in the prior fiscal year on a proforma combined basis. During the fiscal year ended September 30,2002, 53% of operating revenue was from sales to institutional customers and 47% was from retail customers; this compares to acustomer mix in the prior fiscal year of 53% institutional and 47%retail on a historical basis and 52% institutional and 48% retail on a pro forma combined basis. In comparison with prior fiscal year proforma combined results, sales to institutional customers increased by 19% primarily due to higher revenues from mail order facilities,ABSG’s specialty pharmaceutical business and alternate site facilities.Sales to retail customers increased 14% over the prior fiscal year ona pro forma combined basis, principally due to higher revenues fromregional drug store chains, including the pharmacy departments ofsupermarkets. This segment’s growth largely reflects national industry

192003 AmerisourceBergen Corporation

economic conditions, including increases in prescription drug usageand higher pharmaceutical prices. Operating revenue increased 18%in the first half of the year and 14% in the second half of the yearwhen compared to the same periods in the prior year on a pro formacombined basis as the Company reached the April 2002 anniversarydate of the addition of a large mail order customer.

Pharmaceutical Distribution gross profit of $1,530.5 million inthe fiscal year ended September 30, 2002 increased 132% from$660.4 million in the prior fiscal year on a historical basis andincreased 9% from $1,405.0 million in the prior fiscal year on a proforma combined basis. As a percentage of operating revenue, grossprofit in the fiscal year ended September 30, 2002 was 3.87%, ascompared to prior fiscal year percentages of 4.19% on a historicalbasis and 4.13% on a pro forma combined basis. The year-to-yeardeclines reflect the net impact of a number of factors, including thechange in customer mix to a higher percentage of large institutional,mail order and chain accounts, and the continuing competitive pricing environment, offset, in part, by higher buy-side margins than in the prior year.

Pharmaceutical Distribution operating expenses of $871.3 million in the fiscal year ended September 30, 2002 increased 126%from $386.2 million in the prior fiscal year on a historical basis andincreased 2% from $853.1 million in the prior fiscal year on a proforma combined basis. As a percentage of operating revenue, operating expenses in the fiscal year ended September 30, 2002 were 2.20%, as compared to prior-year percentages of 2.45% on ahistorical basis and 2.51% on a pro forma combined basis. Thesedecreases in expense percentages reflect the changing customer mix described above, efficiencies of scale, the elimination of redundant costs through the merger integration process and the continued emphasis on productivity throughout the Company’s distribution network.

Pharmaceutical Distribution operating income of $659.2 millionin the fiscal year ended September 30, 2002 increased 140% from$274.2 million in the prior fiscal year on a historical basis andincreased 19% from $551.8 million in the prior fiscal year on a pro forma combined basis. As a percentage of operating revenue,operating income was 1.67% in the fiscal year ended September 30,2002, as compared to prior-year percentages of 1.74% on a historicalbasis and 1.62% on a pro forma combined basis. The improvementover the prior-year pro forma combined percentage was due to areduction in the operating expense ratio, which was greater than thereduction in gross profit margin. The reduction of the operatingexpense ratio was partially due to the Company’s ability to capturesynergy cost savings from the Merger.

PharMerica SegmentThe PharMerica segment was acquired in connection with

the Merger and the historical amounts for the fiscal year endedSeptember 30, 2001 are comprised of only one month of PharMerica’soperating results. Accordingly, the discussion below focuses all comparisons with the prior-year on a pro forma combined basis.

PharMerica’s operating revenue increased 9% for the fiscal yearended September 30, 2002 to $1.48 billion compared to $1.35 billion in the prior fiscal year. This increase is principally attributableto growth in PharMerica’s workers’ compensation business, which has

grown at a faster rate than its long-term care business.PharMerica’s gross profit of $494.0 million for the fiscal year

ended September 30, 2002 increased 4% from gross profit of $475.8million in the prior fiscal year. PharMerica’s gross profit margindeclined to 33.49% for the fiscal year ended September 30, 2002from 35.24% in the prior fiscal year. This decrease is primarily theresult of a change in the sales mix, with a greater proportion of PharMerica’s current year revenues coming from its workers’ compensation business, which has lower gross profit margins and lower operating expenses than its long-term care business.

PharMerica’s operating expenses of $410.5 million for the fiscalyear ended September 30, 2002 increased 1% from operating expensesof $406.9 million in the prior fiscal year. As a percentage of operatingrevenue, operating expenses were reduced to 27.83% in the fiscal year ended September 30, 2002 from 30.14% in the prior fiscal year.The percentage reduction is due to several factors, including the aforementioned shift in customer mix towards the workers’ compensa-tion business, consolidation of technology platforms, the consolidationor sale of several pharmacies, and a reduction in bad debt expense.

PharMerica’s operating income of $83.5 million for the fiscalyear ended September 30, 2002 increased 21% compared to operatingincome of $68.9 million in the prior fiscal year. As a percentage ofoperating revenue, operating income was 5.66% in the fiscal yearended September 30, 2002, an increase of 56 basis points from5.10% in the prior fiscal year. The year-to-year improvement in the operating income percentage was due to the aforementionedreductions in the operating expense ratio, which were greater thanthe reductions in gross profit margin.

Intersegment EliminationsThese amounts represent the elimination of the Pharmaceutical

Distribution segment’s sales to PharMerica. AmerisourceBergen DrugCompany is the principal supplier of pharmaceuticals to PharMerica.

Critical Accounting PoliciesCritical accounting policies are those accounting policies that

can have a significant impact on the Company’s financial positionand results of operations that require the use of complex and subjective estimates based upon past experience and management’sjudgment. Because of the uncertainty inherent in such estimates,actual results may differ from these estimates. Below are those policies applied in preparing the Company’s financial statements thatmanagement believes are the most dependent on the application ofestimates and assumptions. For additional accounting policies, seeNote 1 of “Notes to Consolidated Financial Statements.”

Allowance for Doubtful AccountsTrade receivables are primarily comprised of amounts owed to

the Company through its pharmaceutical service activities and arepresented net of an allowance for doubtful accounts. In determiningthe appropriate allowance, the Company considers a combination offactors, such as industry trends, its customers’ financial strength andcredit standing, and payment and default history. The calculation ofthe required allowance requires a substantial amount of judgment asto the impact of these and other factors on the ultimate realizationof its trade receivables.

20 AmerisourceBergen Corporation 2003

Merchandise InventoriesInventories are stated at the lower of cost or market. Cost for