Decision-making of the firm- the RBV view Arto Lahti

Decision-making of the firm- the RBV view

Dec 30, 2015

Decision-making of the firm- the RBV view. Arto Lahti. Decision-making of the firm – the RBV view. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Decision-making of the firm- the RBV view

Arto Lahti

Decision-making of the firm – the RBV view

Alfred Marshall, the leading British economist at Cambridge between the 1890s and the 1920s wrote eight editions of his book Principles of Economics (Marshall 1920), where he exerted great influence on the development of economic thought of the time.

Marshall analyzed the relations between the firms and market(s). One of his major contributions was that he identified the internal and external economies of the firm. External economies depend on the firm’s adaptation to the industry development, while internal economies are dependent on the resources, organization and management efficiency. Marshall introduced into economic analysis the concept of Representative Firm that since Marshall’s contribution has been as the theoretical unit of analysis, instead of a real one. This kind of simplification makes possible to focus economists’ attention to the firms’ cost-minimizing adaptation, but inevitably excludes the behavior a real firm.

Marshall can be viewed as the father of managerialism. The resource-based view (RBV), initiated by Marshall, is targeted to deconstruct the black box of the economist’s production function into elementary components and interactions. The notion of firm-specific, knowledge-based or learning-based resource was developed by Edith Penrose in his book The Theory of the Growth of the Firm (1959).

Marshall became again popular in the 1950s, when Edith Penrose in her book The Theory of the Growth of the Firm reinvented Marshall’s theme of the development of knowledge in economic systems. Penrose founded what has now evolved into the’ approach in the modern microeconomics

Penrose highlighted a firm’s heterogeneity and proposed that the unique assets and capabilities of a firm are important giving rise to imperfect competition and the attainment of super-normal profits. Penrose continued Edward Chamberlin (1933) who identified the key capabilities of a firm as technical know-how, reputation, brand awareness, patents and trademarks, many of which have been revisited in management literature.

Penrose (1959) provides a detailed exposition of a resource-based (or knowledge) view that is at the heart of Schumpeterian innovation. Penrose reinvented the theme of Schumpeter and Marshall. Penrose founded what has later evolved into the dynamic capabilities of firms approach in the modern microeconomics. In Penrose’s thinking, opportunities rest on developed internal and external routines.

Penrose takes the boundedness of cognition for granted, as Schumpeter, but at the firm level instead of the economy. Penrose proposed that a firm’s rate of growth is limited by the growth of knowledge within it. Superior performance and a sustainable competitive position depend primarily on the heterogeneous resources available to the firm.

Penrose modernized the well-known writings of Alfred Marshall, and we use to talk about the Marshall-Penrose-paradigm. Marshall-Penrose-paradigm, resource-based (or knowledge) view, distinguished the theory of growth from the equilibrium models of price theory, and linked it with Schumpeter’s vision of the importance of knowledge at the heart of innovation. The idea of the ‘learning capacity of the firm’ is frequently used to embrace the resource development that leads to a carefully differentiated product strategy.

Penrose (1959, 31) provided a new, dynamic conceptualization of the firm - as ‘an administrative organization and as a collection of resources’ - designed to explain the firm level growth Penrose distinguished the firm’s tangible resources from services that these resources provide. While the firm’s tangible resources are finite, the resources from services these resources provide are mediated by the endless extensible body of managerial knowledge.

According to Penrose (1959, pp. 11-14) price theory tells nothing about the growth of the firm. Penrose reinvented Marshall’s theme of the development of knowledge in economic systems. However, when Simon, Chandler and Ansoff initiated a new paradigm Strategic planning, Marshall’s theme of the development of knowledge in economic systems was forgotten for decades.

Herbert Simon is a Nobel-prize winner. His pioneering book is The New Science of Management Decisions (1960). The New Science of Management Decisions As Simon insisted, human rationality is bounded. He believed that human beings are not good natural logicians or statisticians either. The premises for logical operations are often doubtful, and even more likely to be incomplete. Simon’s critique is justified like Penrose’s, as a distinction from the equilibrium models of price theory, but Simon’s intention was not to deny the usefulness of orthodox economic analysis.

Simon’s revolution in the concept of decision-making under uncertainty led far away from the rational man (homo economicus), often assumed in mainstream economics. Instead of maximal or optimal profits, Simon launched the concept of satisfying, i.e. setting an aspiration level which, if achieved, an individual will be happy enough with. In Simon’s thinking, the ‘rules of thumb’ are the best that economic agents, like entrepreneurs and business managers, can use in the ‘bounded’ and uncertain real world.

Simon’s writings are the foundation to the development of behavioral theory of the firm that can be interpreted as a complement of the mainstream theories. Richard Cyert and James March who published in 1963 their book Behavioral Theory of the Firm are the pioneers of the behavioral theory of the firm that is concerned with the day-to-day behavior of the firm. The fact that short-period objectives can be described, whereas long-period objectives apparently need to be advocated, has a significance of its own in explaining business behavior.

The inability of competitors to duplicate resource endowments is a central element of the RBV. Knowledge has been differentiated in terms of explicit vs. tacit, individual vs. collective, and common vs. context-specific. Tacit, context-specific knowledge is difficult to create, transfer, and integrate via markets. This type of knowledge, if valuable and unique, provides a competitive advantage because it is less imitable. A firm's ability to learn maintains it over time.

Iikujiro Nonaka and Hirotaka Takeuchi’s book The knowledge-creating company (1995) focuses on the transformation and communication of what is already known tacitly by employees. The resources that generate superior performance are those that are difficult to imitate and that are embedded as core competencies within the firm (Hamel and Prahalad, 1994). Such specialized resources are developed, not acquired, and have low mobility. Several overlapping explanations have been proposed:

ex-post limits to competition (Peteraf, Margaret (1993) The cornerstones of competitive advantage: A resource-based view, Strategic Management Journal. 14 (March), 179-191.)

isolating mechanisms (Rumelt, 1984) causal ambiguity (Reed, Richard and Robert DeFillippi J. (1990)

Causal ambiguity, barriers to imitation and sustainable competitive advantage, Academy of Management Review 15 (January), 88-102.).

Alfred Chandler, a famous economic historian, is named as the father of strategic management. In his book Strategy and Structure (1962), he wrote of the transformation of capitalism as a system between the 19th and 20th centuries due to the radical changes in communication and transportation technology and managerial systems. He combined historical investigation of some industrial firms with an in-depth theoretical analysis.

Chandler’ careful analysis revealed what Schumpeter had written. Big multinationals did not only passively adapt to prevailing markets. They grew to dominate sectors of the economy, and so doing, altered their structure and that of the economy as a whole.

Chandler found that technology clearly affects organization. For most of the 20th century, the large vertically integrated managerial corporation persisted because it was the appropriate solution for the capital-intensive industries to maintain minimum efficient scale of operations

Chandler advanced Penrose’s thinking in the sense that an effective managerial hierarchy, called an organization structure, becomes the driver of the firm’s (growth) strategy. Chandler’s generally accepted axiom is: a firm’s organizational structure and competencies must be suited to implement strategy (the product/market strategy). What, perhaps, nobody could image in beginning of the 1960s when Chandler published his results is that his axiom became the foundation for a totally new paradigm, the strategic planning or management paradigm and to an enormous industry of strategic consulting.

According to Igor Ansoff’s work Corporate Strategy (1965), strategic Management Models of strategic planning typically propose a rational process of setting objectives, followed by an internal appraisal of capabilities, an external appraisal of outside opportunities, and leading to decisions to expand or diversify based on the level of fit between existing products/ capabilities and investment prospects. Generally, the starting point of strategic management been to begin by assessing the firm’s strengths/weaknesses as part of a broader SWOT analysis.

In recent years, reservations have emerged regarding the SWOT. Top managers tend to emphasize financial strengths while middle and lower managers were more concerned about technical issues, suggesting a high potential for inconsistency. A SWOT analyzers tend to produce a fairly indiscriminate list of variables, leading to analyses without any internal logic (Hill, Charles W. and Gareth R. Jones. 1998. Strategic Management: An Integrated Approach. Boston, MA: Houghton Mifflin).

Later, the pursuit of sustainable competitive advantage has been at the heart of much of the strategic management. Understanding sources of sustained competitive advantage for firms has become a major area of research in the field of strategic management. A competitive advantage must, by definition, be scare, valuable and reasonably durable (Barney, J. (1991) Firm Resources and Sustained Competitive Advantage, Journal of. Management 17(1), pp. 99-120.)

The resource-based and knowledge-based views are targeted attempts to deconstruct the black box of the economist’s production function into some more elemental components and interactions, and until we identify these we cannot be confident about what is useful to observe over time.

The resource-based view contends that the answer to this question lies in the possession of certain key resources, that is, resources that have characteristics such as value. A SCA (sustainable competitive advantage ) can be obtained if the firm effectively deploys these resources in its product-markets. Therefore, the RBV emphasizes strategic choice, charging the firm’s man-agement with the important tasks of identifying, developing and deploying key resources to maximise returns.

Valuable, and rare organizational resources can only be sources of sustained competitive advantage if firms that do not possesses these resources cannot obtain them. These firm resources are imperfectly imitable for one or combination of three reasons (]Dierickx, I. and Cool, K. (1989) Asset Stock Accumulation and sustained competitive advantage, Mangement Science, vol. 35, pp. 1504-1511.):

The ability of a firm to obtain a resource is dependent on unique historical conditions,

The link between the resource possessed by a firm and a firm’s sustained competitive advantage is causally ambiguous

The resource generating a firm’s sustained competitive advantage is socially complex.

Resource-based theory of the firm recognizes that knowledge or competence is a difficult concept to define, far from being one-dimensional. For example, knowledge has been differentiated in terms of (Spender, J-C., "Making Knowledge the Basis of a Dynamic Theory of the Firm", Strategic Management Journal, Vol. 17 (Winter Special Issue), 1996, pp. 45-62.)

explicit vs. tacit, individual vs. collective, and common vs. context-specific.

Tacit, collective, context-specific knowledge is difficult to create, transfer, or integrate via markets and, thus, provides a rationale for firms. The resource-based view similarly suggests that this type of knowledge, if valuable and unique, may provide a competitive advantage because it is less imitable. A firm's intellectual resources should support that capability today, and its ability to learn should maintain it over time.

Loasby (Loasby, Brian J. (1998) How do we know? In: Boehm, Stephan, Frowen, Stephen F., Pheby, John (eds) Economics as the Art of Thought: Essays in Memory of G. L. S. Shackle, Rutledge, London.) concludes:

The development of a specialized skill depends on a variety of experiences, but a variety that can be encompassed within a network of connections.

As Charles Hofer & Dan Schendel’s book, Strategy Formulation. Analytical Concepts (1978) suggested, the internal model of resource allocation has a lot of feedback and interactive mechanisms.

PhysicalResources

OrganizationalResources

TechnologicalResources

Product/MarketResources

FinancialResources

HumanResources

ExternalCapitalMarkets

Hofer & Schendel (1978) present an analytical concept of a firm’s resource stock that can also be expressed as the extended assets. The five types of resources and skills of an organization can be divided into groups based on their position in the strategic resource conversation cycle). Financial resources are the most basic and flexible, because they they are the only type of resource that is directly convertible into the other four of resources. Physical, human, and organizational resources are the next most flexible. Technological resources are the least flexible, although often the most important.

Referring to the standard books of strategic resource management, we might say that Hofer & Schendel (1978) present an analytical concept of a firm’s resource stock includes three processes of resource management:

1. Competence process that contain human and organizational resources - this process contains all activities that create knowledge, know-how, etc.

2. Technology process - that contain physical and technological resources – In Hofer & Schendel (1978) technology is a broad concept including both material and immaterial elements.

2. Capital process - this process contains all activities that are targeted to control the allocation of internal and external financial resources.

Entrepreneurial strategic market management The challenge of goodwill value and economic value-added that is called EVA (Economic Value Added)

The core content of entrepreneurial strategic market management can be found in the texts of famous Swedish economist. In his dissertation ’An Essay of Trade and Tranformation’, Bundestam Linder states that in the context of strategic market management an entrepreneur is doing what he or she perceives. The starting point of high value marketing strategy is entrepreneur’s vision of the future market prospects. These prospects actually consist of customer relations, product or service concept, agent relation, etc. They are goodwill value elements that through professional marketing can be used to earn

(1) ’abnormal’ profits through marketing processes and (2) ’temporary’ monopoly profis through market innovations

Abnormal’ profits and ’temporary’ monopoly profits are the key indicators behind the annual EVA improvements. In order to develop a model of strategic market management, we assume that the formula is valid.

GOODWILL VALUE = EVA

Formula 1: EVA as a proxy measure of goodwill

EVA is a residual income and not a new discovery. Alfred Marshall was the first that used residual income. He defined economic profit as total net gains less the interest on invested capital at the current rate. It is surprising how deeply Marshall could understand the theory of the firm.

EVA is a trademark registered by Stern Steward & Co that limits the use of it (Stewart, Bennet, The Quest For Value: the EVA™ management quide, Harper Business, New York. 1990).

Today, EVA is aimed to be a measure the wealth of shareholders. Whether a firm has positive or negative MVA (Market Value Added) depends on the level of rate of return compared to the cost of capital. A positive EVA means positive MVA and vice versa. The relation between EVA and MVA is simple

MVA= Present value of all future EVA measures (formula 2)

Market Value of Equity = Book Value of Equity + Present value of all future EVA measures (Formula 3)

The Balance Consulting Ltd in Finland is using the Market Value of Equity that corresponds the EVA™

The phenomenon with rate of return and MVA is in one sense similar to the relationship between the yield and market value of a bond. If the yield of a bond exceeds the current market interest rate (cost of capital) then the bond will sell at a premium (there is positive EVA and so the bond will sell at positive MVA). If the yield of a bond is lower than the current market interest rate then the bond will sell at discount (there is negative EVA and so the bond will sell at negative MVA).

If the net assets or "capital" in the EVA formula reflected the current value of a firm’s assets and if the "rate of return" reflected the true return, then there would not be much questioning about the theory between EVA and MVA. With MVA and EVA things are little bit more complicated. The "capital" does not reflect the current value of assets, because the capital is based on historical values. Nor does the "rate of return" reflect the true return of the company. All accounting based rate of returns like the ROI fail to assess the true or economic return of a firm, because they are based on the historical asset values.

The valuation formula of EVA (formula 3) gives always the right estimate of value (same as DCF and NPV) no matter what the original book value of equity is. This holds true even though capital is not an unbiased estimate of current value of assets and rate of return is not an unbiased estimate of the true return. That is because an increase in book value decreases the periodic EVA-figures.

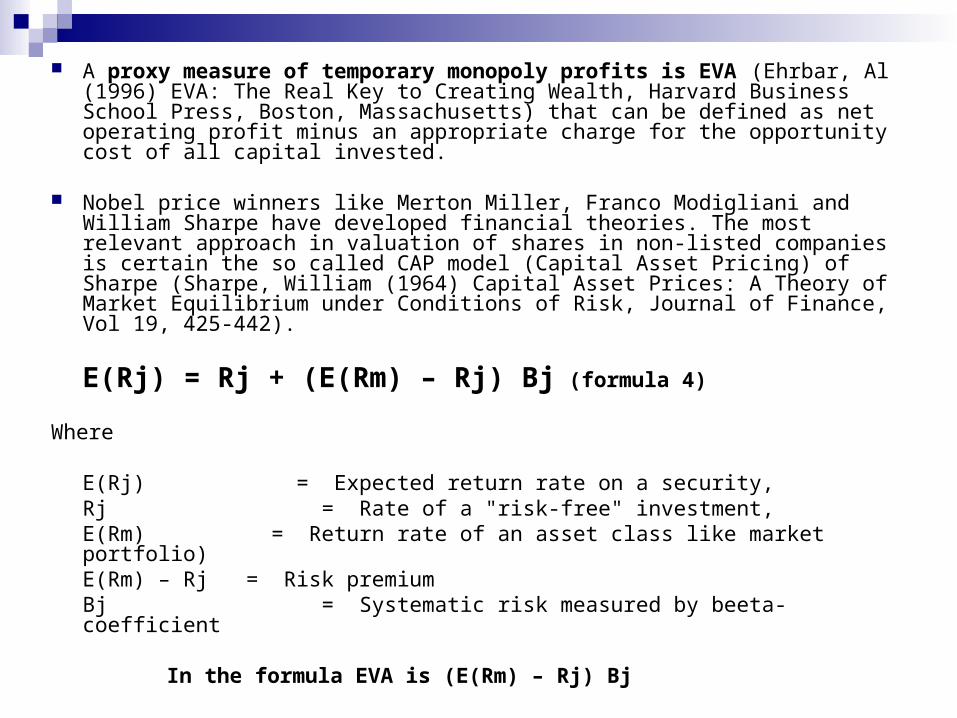

A proxy measure of temporary monopoly profits is EVA (Ehrbar, Al (1996) EVA: The Real Key to Creating Wealth, Harvard Business School Press, Boston, Massachusetts) that can be defined as net operating profit minus an appropriate charge for the opportunity cost of all capital invested.

Nobel price winners like Merton Miller, Franco Modigliani and William Sharpe have developed financial theories. The most relevant approach in valuation of shares in non-listed companies is certain the so called CAP model (Capital Asset Pricing) of Sharpe (Sharpe, William (1964) Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk, Journal of Finance, Vol 19, 425-442).

E(Rj) = Rj + (E(Rm) – Rj) Bj (formula 4)

Where

E(Rj) = Expected return rate on a security,Rj = Rate of a "risk-free" investment,E(Rm) = Return rate of an asset class like market portfolio)E(Rm) – Rj = Risk premiumBj = Systematic risk measured by beeta-coefficient

In the formula EVA is (E(Rm) – Rj) Bj

The paradox with an innovative growth company is that its current market value in the moment of IPO consists almost totally of goodwill or goodwill value. If goodwill as a residual is 100 percent what is the relevance of substance. Is it possible that the traditional assets concept is old fashioned in the valuation of a company’s shares? Having relevant substance measures, it is possible that relation between substance and market value is more reasonable.

The measurement problem is relevant since the equity gap is still relevant in countries where we do not have well functioning stock market for small, innovative companies. Because of low asset value, the lack of reliability is a relevant constraint on the ability to rise external funding and under-capitalisation is a potential cause of business failure.

For the innovative companies having negative book value of assets, the only means for rising capital is to demonstrate high market value through proxy measures of goodwill. In the software industry, there are proxy measures of goodwill like scientific methods or algorithms used and sometimes even patents. These business-to-business industries that have access to relevant IRPs (immaterial property rights) have also succeeded in the stockmarkets like NASDAQ. The consumer-driven creative industries have been stuck in the dilemma of high valuation without any objective measures of goodwill.

In order to develop a model of strategic resource management for a company that has no or only spot information of efficient stock markets, we assume that the formula 5 is valid.

SUBSTANCE VALUE = CURRENT OPERATIONS VALUE (formula 5)

The substance value has many alternative measures. Having a narrow accountant view to substance value, we might define substance value as the capital assets. A more comprehensive view can be found in the strategic management literature. The most crucial substance element that should be added to comprehend the accountant view is competence.

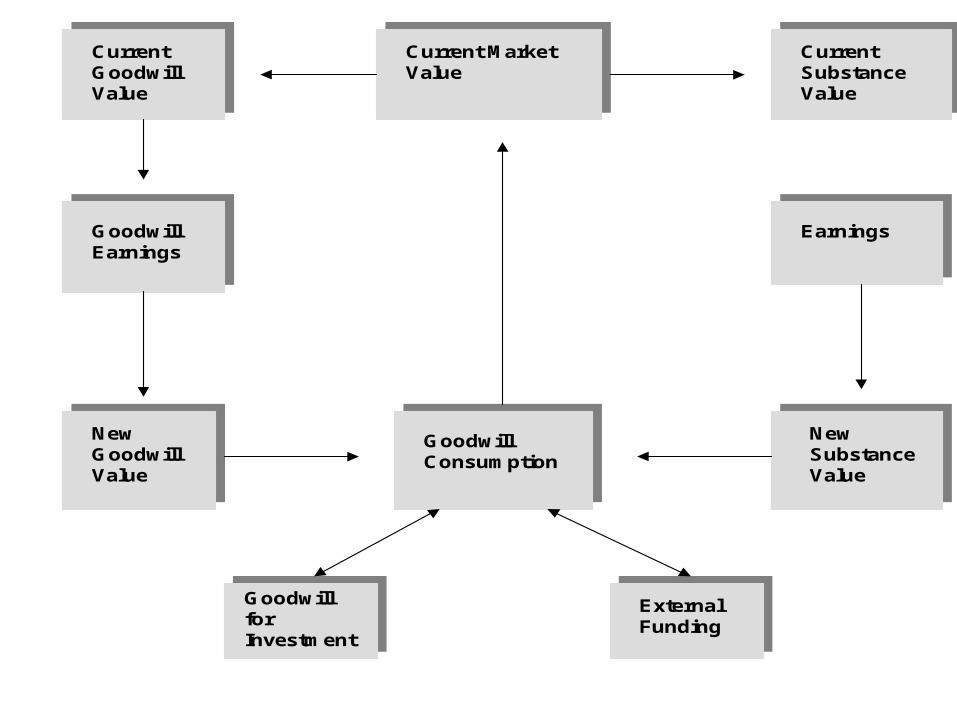

Referring to Hofer & Schendel (1978), we can develop our model of substance and goowill value further (summary in the next figure).

SUBSTANCE VALUE = CURRENT OPERATIONS VALUE = f(COMPENTENCE ASSETS , TECHNOLOGY ASSETS, CAPITAL ASSETS) (formula 6)

GOODWILL VALUE = EVA = f(DIFFERENTATION; DIFFERENTIAL ADVANTAGE; INNOVATIONS; MONOPOLY PROFITS) (formula 7)

CurrentGoodwillValue

Current MarketValue

CurrentSubstanceValue

GoodwillEarnings

NewGoodwillValue

GoodwillConsumption

NewSubstanceValue

Earnings

GoodwillforInvestment

ExternalFunding

Creative destructions in the markets provide opportunities to innovations and earnings of monopoly profits. Competition is a self-destructive mechanism that normalizes the profit level when the innovation effects are consumed. Therefore, a growth firm has to create innovations continuously. The long-term target is temporary monopoly profits through innovations. The key issue of these three well-known writers is that goodwill value is a function of differentiation plan, dífferential advantage, innovations and monopoly profits. We can develop our model of goodwill value further.

EVA has some value in that it makes obvious the need to earn returns in relation to the capital employed. The concept that equity capital has an opportunity cost and that the return on this is an important determinant of shareholder value is sensible, though nothing new. The present value of the EVA of a project over its life-time is exactly the same as the net present value (NPV) of the project. Thus, conceptually, EVA is no different from NPV. As long as assumptions made into the calculations are consistent, we would get exactly the same results for both EVA and NPV.

Luerman (1998) criticized the discount-cash-flow (DCF) valuation that is based on the assumption that an entrepreneur follows a predetermined plan, regardless of how events unfold. EVA estimates can be used only for a limited time space but, in principle, goodwill value can be utilized forever. Goodwill value as a residual will be materialized only in the moment of share exchange. Therefore, it is reasonable that goodwill value is measured through EVA estimates.

The formula 5 and 6 integrates the modern financial theories with strategic market management theories. Another relevant viewpoint to elaborate the goodwill value concept of ongoing innovative business venture is the competitive strategy viewpoint. The problem in the traditional marketing doctrine is that the researchers have developed a large number of sophisticated models but almost totally for secondary purposes. The primary focus of marketing is the goodwill value. In financial theories goodwill is above-market returns or abnormal return or monopoly profits. There are three classical writers that has conceptualized goodwill value in terms of market behavior:

(1) In his book ’The Theory of Monopolistic Competition’, Edward Chamberlin discussed about monopolistic competition that is a kind of mixture of competition and monopoly. Product differentiation attempts to create niches in the market through innovations, and it can be viewed as an attempt to create a quasi monopoly.

(2) In his book ’The Theory of Economic Development’, Joseph Schumpeter proposed that any kind of monopoly position is temporary. Competition is a self destructive mechanism; effective competition normalizes the profit level when the innovation effects have been utilized.

(3) In his book ’Marketing, Behavior and Executive Action’, Wroe Alderson argued that competition should not be defined in traditional market structure terms but the emphasis should be shifted to the creation of differential advantage by individual firms in their pursuit of markets.

Strategic market management or strategic marketing can be defined as a process of maintaining EVA prospects and establishing a sustainable competitive advantage, through differentiation plan, differential advantage, innovation and monopoly profits. How to develop a model to conceptualize the marketing processes behind a sustainable competitive advantage is a challenge, since for instance time to markets of a creative offering has shortened to months or weeks instead of years.

Product differentiation and differential advantage are relevant concepts in any kind of creative business, in which competence is an isolation mechanism like Rumelt (Rumelt, R., 'Towards a Strategic Theory of the Firm', in Lamb, R., (ed.) Competive Strategicv Manangement, Englewood Cliffs, Prentice-Hall, 1984.) conceptualizes it. Rumelt’s isolation mechanism (like causal ambiguity, team-embodied skills or special information) provides a basis to isolate a company or company group from the keenly competitive market arena. Rumelt actually identifies competence based differentiation or differential advantage or temporary monopoly position.

The clue of an innovative, entrepreneurial company is the goodwill value. Goodwill value is in a way a residual in the valuation of a company’s shares. The body of the traditional accounting literature seems to define the goodwill value as the difference between the market value and the substance value. In the accountant view, the goodwill value will be materialized only in the transactions where more or less company shares are sold. The RBV is always applicable (see figure)

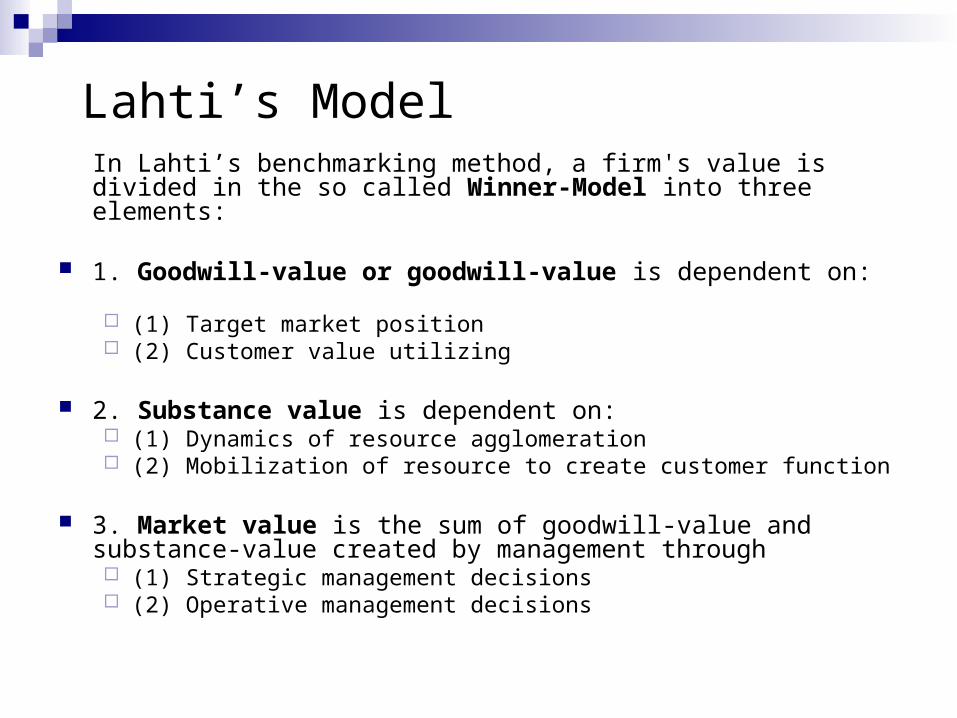

Lahti’s ModelIn Lahti’s benchmarking method, a firm's value is divided in the so called Winner-Model into three elements:

1. Goodwill-value or goodwill-value is dependent on: (1) Target market position (2) Customer value utilizing

2. Substance value is dependent on: (1) Dynamics of resource agglomeration (2) Mobilization of resource to create customer function

3. Market value is the sum of goodwill-value and substance-value created by management through (1) Strategic management decisions (2) Operative management decisions

Edward Chamberlin: forgotten but influential Harvard professor Edward Chamberlin, who also opposed the neoclassical Walras-

Marshall price theory that solely relied on two theoretical models of competition (perfect competition and monopoly) and excluded the reality of imperfect, monopolistic competition.

Chamberlin contributed the concept of differentiation that is a parallel concept of Joseph Schumpeter’s concept of innovation. Chamberlin’s work can be considered revolutionary, in the sense that he conceptualizes a market structure characterized by both competitive and monopoly elements, and that is the point that makes his work so important to the modern microeconomic theory.

Differentiation through innovativeness (economies of scope) is an entrepreneur’s best strategy in competition against the market power of multinationals (economies of scale).

Chamberlin, Edward (1933) The Theory of Monopolistic Competition, Harvard University Press, Cambridge.

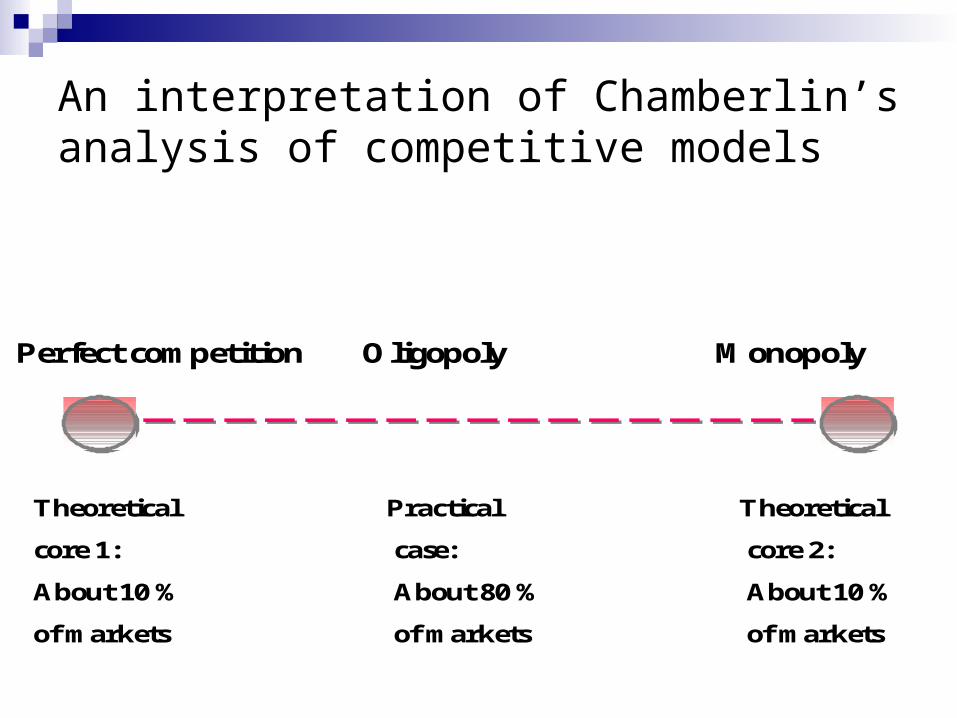

An interpretation of Chamberlin’s analysis of competitive models

Perfect competition Oligopoly Monopoly

Theoretical Practical Theoretical

core 1: case: core 2:

About 10 % About 80 % About 10 %

of markets of markets of markets

An interpretation of Chamberlin’s analysis of competitive models (continues)

For Chamberlin, perfect competition, per se, is an abstraction, because the real behavior of firms is not like pure price competition. Chamberlin’s contribution to microeconomics is that he offered product differentiation as the explanation for a downward falling demand curve of an individual product. Chamberlin proposed that the demand of an individual product depends on the quality of the product and selling activities. Chamberlin insisted on the claim that at an individual product level, there are two basically different kinds of competition:

1. Price competition2. Non-price competition

The problem with the neoclassical microeconomics is the exclusion of non-price competition that through differentiation of products is the major means of firms to earn monopoly profits. Both kinds of competition can be keen but for various reasons. Another dimension of competitive models is the number of competitive firms in the markets. There are three types: perfect competition, oligopoly and monopoly.

A more realistic classification of competitive models, modifying Chamberlin’s thinking

One competitor Few competitors Many competitors

HETEROGENEUSOLIGOPOLY

MONOPOLISTICCOMPETITITON

MONOPOLYHOMOGENEOUS

OLIGOPOLYPERFECT

COMPETITION

differentiated products/open competition

homogeneous products/close competition

typical transfer untypical transfer

The distinction between monopolistic competition and heterogeneous oligopoly can be visualized in the ICT-industries

In Chamberlin’s (1933) classification of competitive models, the ICT-cluster is an excellent example of the transfer from the closed/ homogenous domestic markets (perfect competition) to the open/ differentiated markets (next figure).

This is also called deregulation. The competitive models that are relevant in the Finnish ICT-cluster are a unique combination of heterogeneous oligopoly and monopolistic competition.

1. The big multinational or global companies are assumed to dominate the areas of heterogeneous oligopoly.

2. In the monopolistic industries, the market structure is fragmented and there are continuous changes in the rules of the game.

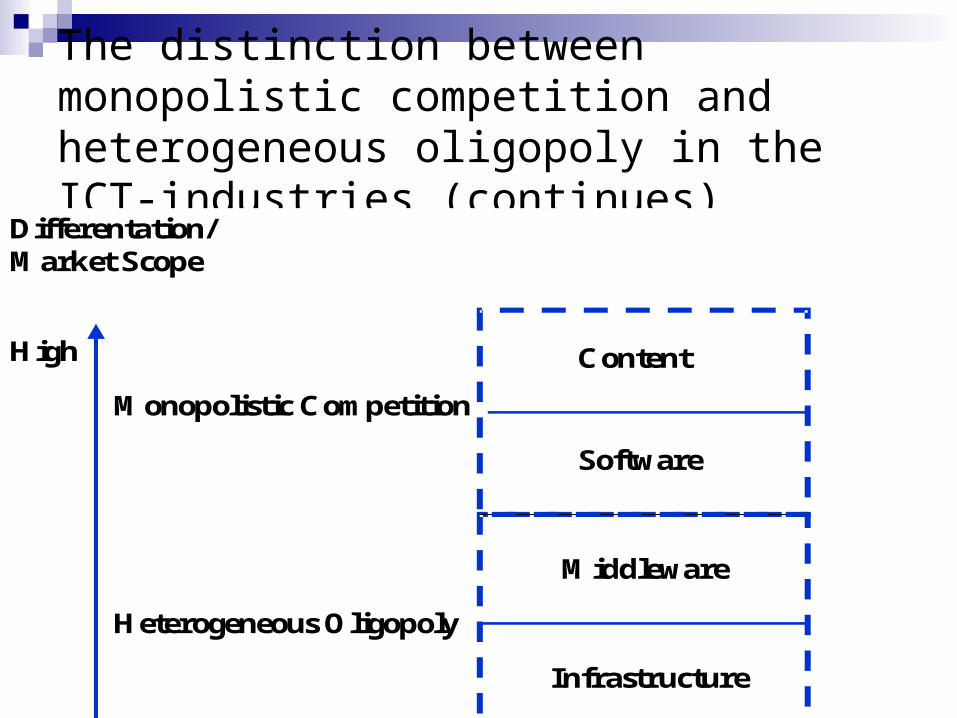

The distinction between monopolistic competition and heterogeneous oligopoly in the ICT-industries (continues)

High

Low

Differentation/Market Scope

Content

Infrastructure

Monopolistic Competition

Heterogeneous Oligopoly

Middleware

Software

The distinction between monopolistic competition and heterogeneous oligopoly can be visualized in the ICT-industries

In Chamberlin’s (1933) classification of competitive models, the ICT-cluster is an excellent example of the transfer from the closed/ homogenous domestic markets (perfect competition) to the open/ differentiated markets (next figure).

This is also called deregulation. The competitive models that are relevant in the Finnish ICT-cluster are a unique combination of heterogeneous oligopoly and monopolistic competition.

1. The big multinational or global companies are assumed to dominate the areas of heterogeneous oligopoly.

2. In the monopolistic industries, the market structure is fragmented and there are continuous changes in the rules of the game.

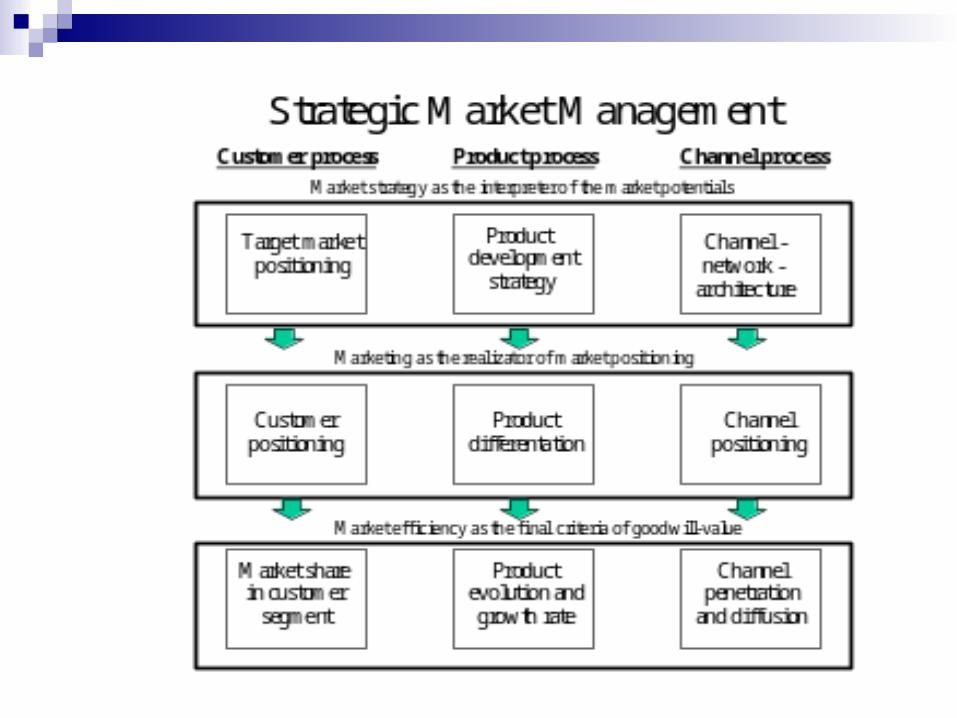

The model presented divides marketing into three processes (Customer, Product and Channel) that have mutual dependence. Further, there are inherent dynamics inside each of the processes. The starting point of the process is strategic competition where the focus is in market prospects.

The operative competition issue is marketer's basic selection of realization of market prospects. The final criterion of success is a composition measure of three variables (market share, product evolution or growth rate and channel penetration or diffusion). The critical processes behind a sustainable competitive advantage is supposed to be:

Customer process - this process contains all activities in the customer interface

Product process - this process contains all activities that are targeted to create customer functions or attributes.

Channel process - this process contains all activities that are targeted to control channels between the firm and the customers.

Chamberlin is an economist and the father of marketing. Therefore, the theoretical underpinning of marketing is economics. Marketing itself has borrowed more heavily from the economic theory than from any other discipline (Bartels, Robert (1988) The History of Marketing Thought, Columbus, Publishing Horizons).

This means that on the issue of exchanges between the firm and its markets, economic more than social or political has the primary emphasis with an assumption of rationality in marketing decisions. Nevertheless, the potential benefits of integration with these traditions should not be ignored as is demonstrated by recent contributions that combines institutional theory and the resource-based view in an analysis of sustainable competitive advantage (Oliver, Christine (1997) Sustainable competitive advantage: Combining institutional and resource-based views, Strategic Management Journal, 18 (October), 697-713.).

Later, the topics of strategic marketing are adapted including strategic analysis, positioning and international marketing. The current tradition is built on the work of industrial economists and has been growing in popularity in the strategy literature since the mid-1980s. More than one firm in a given market can have a competitive advantage. Specificity is the idea that transactions within the firm and with its external constituents are idiosyncratic to individual firms (Williamson, Oliver (1985) The Economic Organization. Firms, market and policy control, Wheatsheaf Books.).

George Day (Day, George S. (1990) Market-Driven Strategy: Processes for Creating Value. New York: Free Press) argues that winners are guided by a shared strategic vision and are driven to be responsive to market requirements. There are no standard formulas on how to cope in chaotic environment. As Day (1990) emphasizes there is distinctive features of successful responses to the chaotic market environment.

One of them is external orientation, an adaptive planning process, a continuous creation and renewal of new sources of competitive advantage. Strategic marketing emphasizes that strategy development needs to be externally oriented – towards customers, competitors, the market and the market’s environment. David Aaker (Aaker, David (1988) Strategic market management (2nd ed.). New York: John Wiley. & Sons) stresses the need for a system that provides assistance in an inherently complex decision making, sensitive enough to be applied in a variety of situations.

International marketing strategy is likely to be particularly enriched by perspectives from the resource-based view of the firm. Geographic nearness to markets was found to influence investment decisions while the role of cultural proximity or psychic distance was proposed as a key variable by Reijo Luostarinen. the role of industry effects in observed performance levels which is evident in the ongoing debate on the relative importance of both firm and industry factors (Henderson, Rebecca & Will, Mitchell (1997) The interactions of organisational and competitive influences on strategy and performance, Strategic Management Journal 18 (Summer Special Issue) 5-14).

The contextual challenge of strategic marketing is to balance between Serve or Create. ‘To ‘Serve’ is nowadays referred as market orientation and contends that the key to the attainment of organizational goals is identifying the needs and wants of the target market and delivering products and services that satisfy these needs. ‘To Create’ or innovation orientation or knowledge orientation refers to issues such as technological superiority or inventing superior products.

Since the 50s when Drucker (Drucker, Peter (1954). The Principles of Management. New York, NY HarperCollins Publishers) stated that the sole purpose of a firm is to create and keep customers, customer orientation has been the trend. In Theodor Levitt’s (Levitt, Theodor (1975) Marketing Myopia, Harvard Business Review, October-November) thinking, the key issue is ‘to run the business, not customers’. In the 90s, parallel with the globalization, the customer orientation is subsumed under the idea of market orientation.

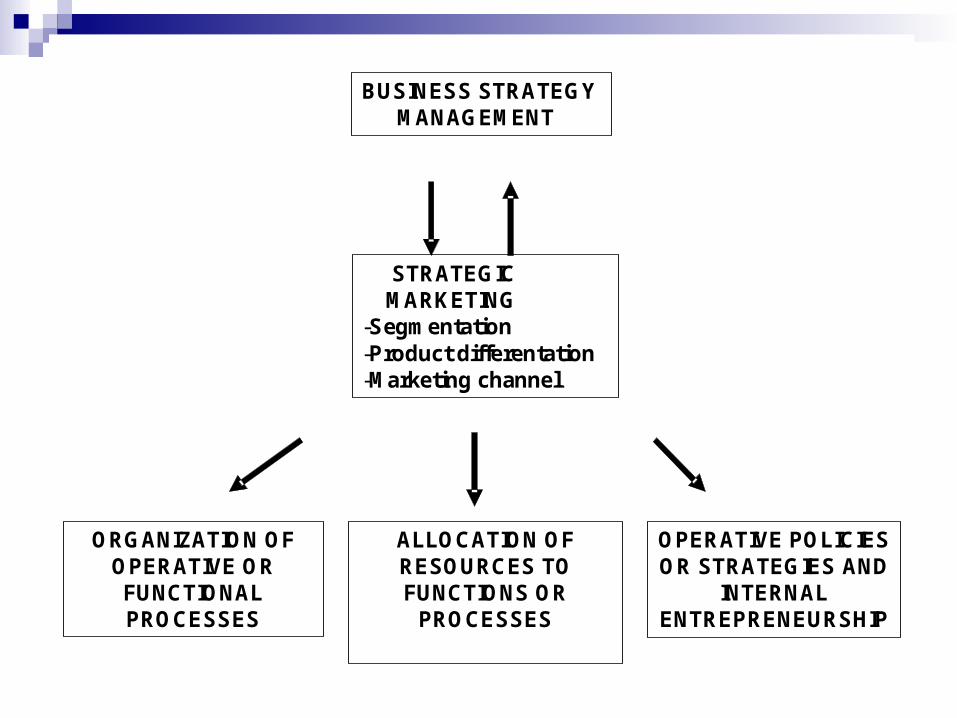

Having creative entrepreneurs in mind, the key challenge is to move from the simple expert model towards models that allows practical benchmarking. The key findings of benchmarking might be useful to analyse because benchmarking is a bit more collaborating than the ‘PIMS principles’. Lahti’s Strategic Marketing model is developed for SME benchmarking (figure).

BUSINESS STRATEGY MANAGEMENT

STRATEGIC MARKETING

-Segmentation-Product differentation-Marketing channel

ORGANIZATION OF OPERATIVE OR FUNCTIONAL PROCESSES

ALLOCATION OF RESOURCES TO FUNCTIONS OR

PROCESSES

OPERATIVE POLICIES OR STRATEGIES AND

INTERNAL ENTREPRENEURSHIP

The key issue is knowledge based product differentiation and differential advantage. Like Rumelt (1984) conceptualizes, the isolation mechanism (like causal ambiguity, team-embodied skills or special information) provides a basis to isolate a company or a company group from the keenly competitive market arena.

The dominant model of global competence competition is monopolistic competition which is a mixture of competition and monopoly. Product differentiation attempts to create niches in the market through innovations, and it can be viewed as an attempt to create a quasi‑monopoly. Global firms have huge marketing budgets that allow them to differentiate their offerings through mass-customization their offerings and to utilize location and ownership advantages in all continents (Dunning, John (1993) The Globalization of Business, London).

Knowledge-intensive, growth firms have another differentiation strategy, the customer-specific differentiation. It is a strong capability, since global giants cannot combine large-scaled marketing and logistics with customer-specific strategies. The mobility barriers of medium-sized firms have much to do with operative business strategies (marketing and logistics).

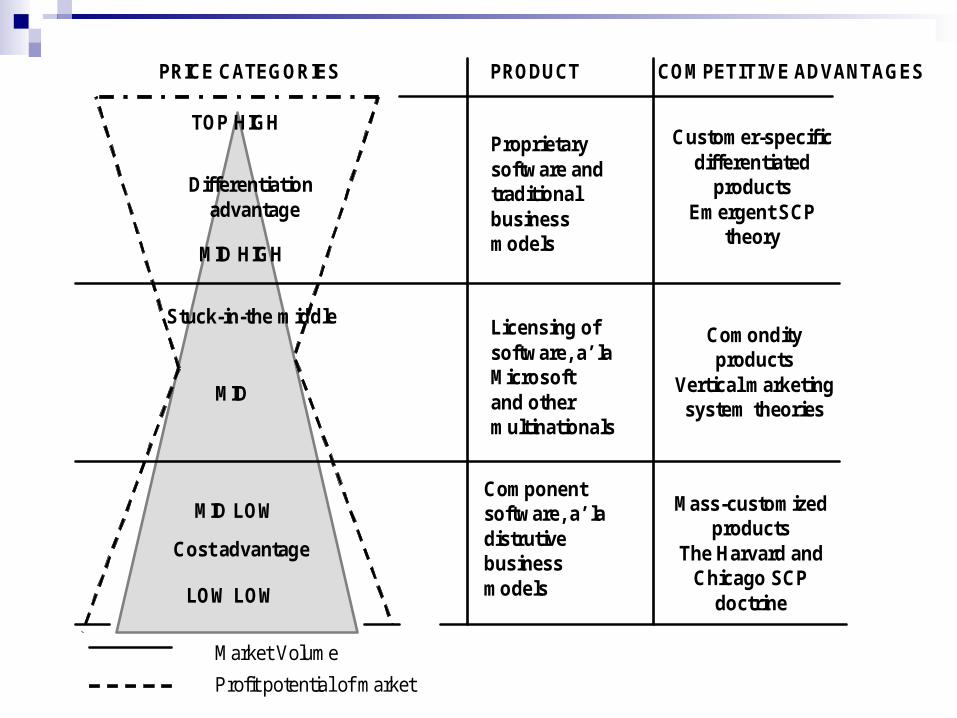

In figure an application of Chamberlin’s positioning model by Alfred Sloan in the GM was one of the first managers that utilized Chamberlin’s product differentiation model positioning GM’s five car brands in five price categories. (Sloan, Alfred (1963) My Work With General Motors, Doubleday, New York) is shown, modified for the software industry).

PRICE CATEGORIES PRODUCT COMPETITIVE ADVANTAGES

Stuck-in-the middle

Cost advantage

Licensing of software, a’ la Microsoft and other multinationals

Proprietary software andtraditional business models

Componentsoftware, a’ la distrutive business models

Differentiationadvantage

Customer-specificdifferentiated

productsEmergent SCP

theory

Comondityproducts

Vertical marketingsystem theories

Mass-customizedproducts

The Harvard and Chicago SCP

doctrine

Market Volume

Profit potential of market

TOP HIGH

MID

MID LOW

MID HIGH

LOW LOW

The customer-focused marketing concepts, such as segmentation, positioning and the product-life cycle, have also influenced thinking in strategic management (Day, George (1992) Marketing’s contribution to the strategy dialogue, Journal of the Academy of Marketing Science 10 (May) 323-329.)

Product/brand positioning is a core strategic marketing activity and firms can seek to adopt a number of distinct positions in the marketplace. These may involve positions based on price, premium quality, superior service and innovativeness. The resource-based view of the firm focuses attention on the ability of the firm to deliver on its desired positioning strategy.

For example, if the firm seeks to become a customer service leader in an industry, it needs to develop the resources that are necessary to enable it to try to attain such a position. Among its distinctive capabilities are a customer-focused organisational culture and an obsession with detail at every level of the organisation (Day, George (1994) The capabilities of market-driven organizations, Journal of Marketing. 58 (October) 37-52.)

Many researchers referring to Porter’s generic strategies have misunderstood the intelligent notions of Joseph Schumpeter and Alfred Marshall and their followers.

The paradoxies of generic strategies are explained in the following figure.

An interpretation of Porters generic strategies

Mar

ket s

cope

Competitive advantage

Differentiation Costs leadership

Customerstrategy

Marketstrategy

MultinationalsHarvard-method

GrowthfirmsEmergenttheory

During the 1980s, the most influential writer was Michael Porter with his book Competitive Strategy. In a short time, Porter's writings on mobility barriers or generic strategies became broadly used in teaching, consultation, and research projects. Porter divided a company’s market scope in two ones: industry wide and particular segment only. Anyone who has read Porter’s dissertation could recognize that this is the same division into big (industry wide) and small (particular segment only) companies. This is not very much more than what any policy-maker or business manager already knows.

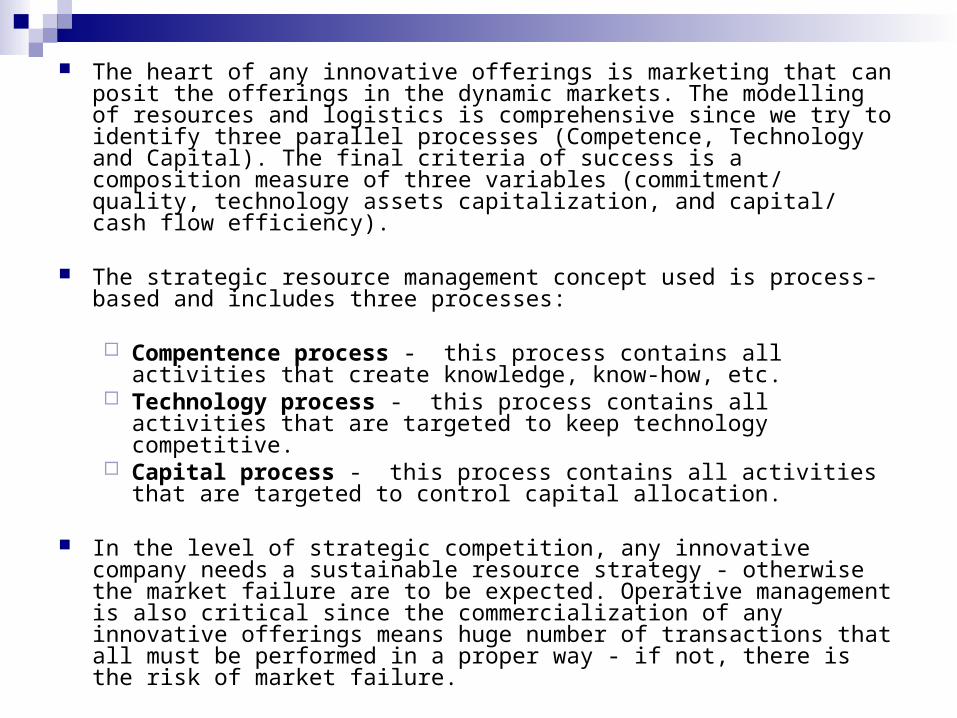

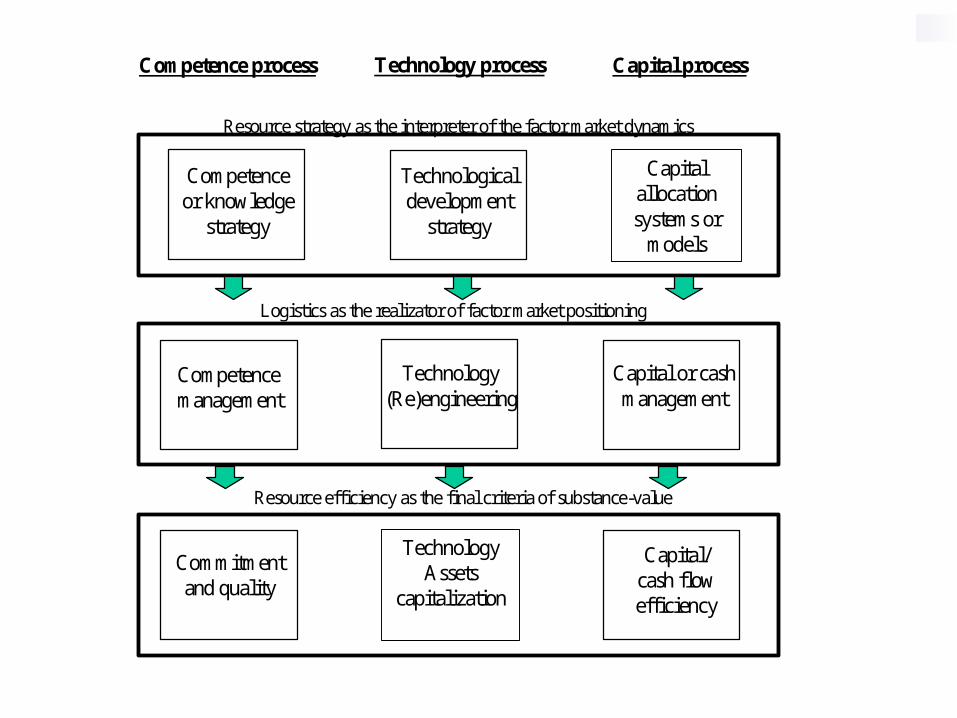

The heart of any innovative offerings is marketing that can posit the offerings in the dynamic markets. The modelling of resources and logistics is comprehensive since we try to identify three parallel processes (Competence, Technology and Capital). The final criteria of success is a composition measure of three variables (commitment/ quality, technology assets capitalization, and capital/ cash flow efficiency).

The strategic resource management concept used is process-based and includes three processes:

Compentence process - this process contains all activities that create

knowledge, know-how, etc. Technology process - this process contains all activities that are

targeted to keep technology competitive. Capital process - this process contains all activities that are targeted

to control capital allocation.

In the level of strategic competition, any innovative company needs a sustainable resource strategy - otherwise the market failure are to be expected. Operative management is also critical since the commercialization of any innovative offerings means huge number of transactions that all must be performed in a proper way - if not, there is the risk of market failure.

o

Logistics as the realizator of factor market positioning

Competence process Technology process Capital process

Resource strategy as the interpreter of the factor market dynamics

Resource efficiency as the final criteria of substance-value

Competenceor knowledge

strategy

Technologicaldevelopment

strategy

Capital allocationsystems or

models

Competencemanagement

Technology(Re)engineering

Capital or cashmanagement

Commitmentand quality

TechnologyAssets

capitalization

Capital/cash flowefficiency

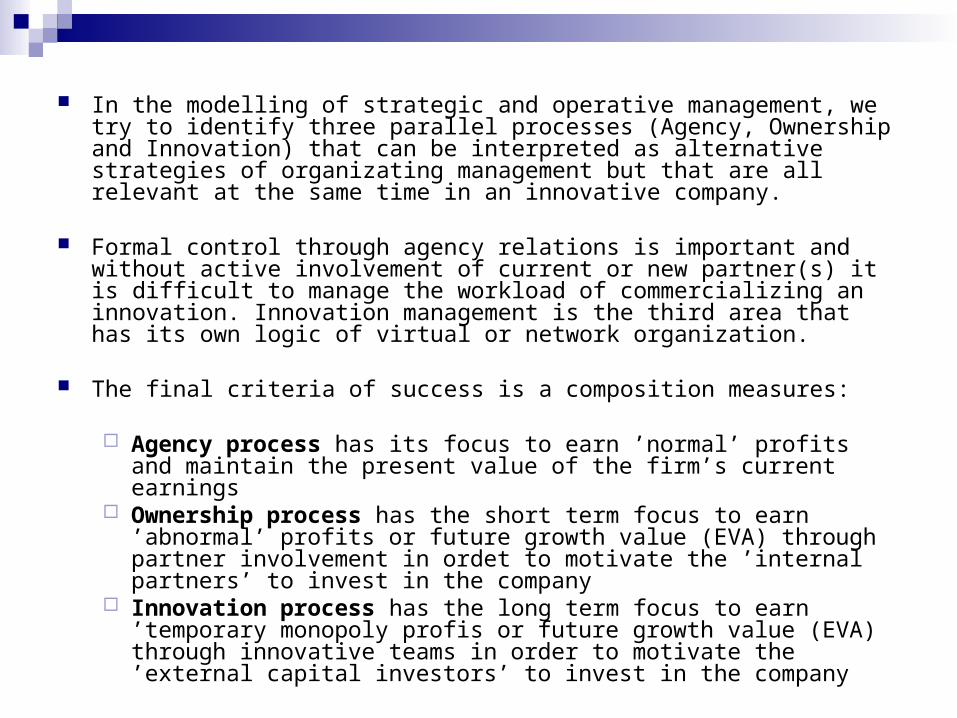

In the modelling of strategic and operative management, we try to identify three parallel processes (Agency, Ownership and Innovation) that can be interpreted as alternative strategies of organizating management but that are all relevant at the same time in an innovative company.

Formal control through agency relations is important and without active involvement of current or new partner(s) it is difficult to manage the workload of commercializing an innovation. Innovation management is the third area that has its own logic of virtual or network organization.

The final criteria of success is a composition measures:

Agency process has its focus to earn ’normal’ profits and maintain the present value of the firm’s current earnings

Ownership process has the short term focus to earn ’abnormal’ profits or future growth value (EVA) through partner involvement in ordet to motivate the ’internal partners’ to invest in the company

Innovation process has the long term focus to earn ’temporary monopoly profis or future growth value (EVA) through innovative teams in order to motivate the ’external capital investors’ to invest in the company

Management

Operative management as the realizator of competitive advantage

Agency process Ownership process Innovation process

Strategic management as the interpreter of synergy

Profitability as the final criteria of market value

Executiverecrutingstrategy

Partnershipstrategy

Architecture ofinnovationnetworks /ventures

Operative

annual planning

Partnermobilization

planning

Virtualcompanyutilization

ROI or profit margin

Extra profitsthroughpartner

involvement

Monopolyprofits through

innovations

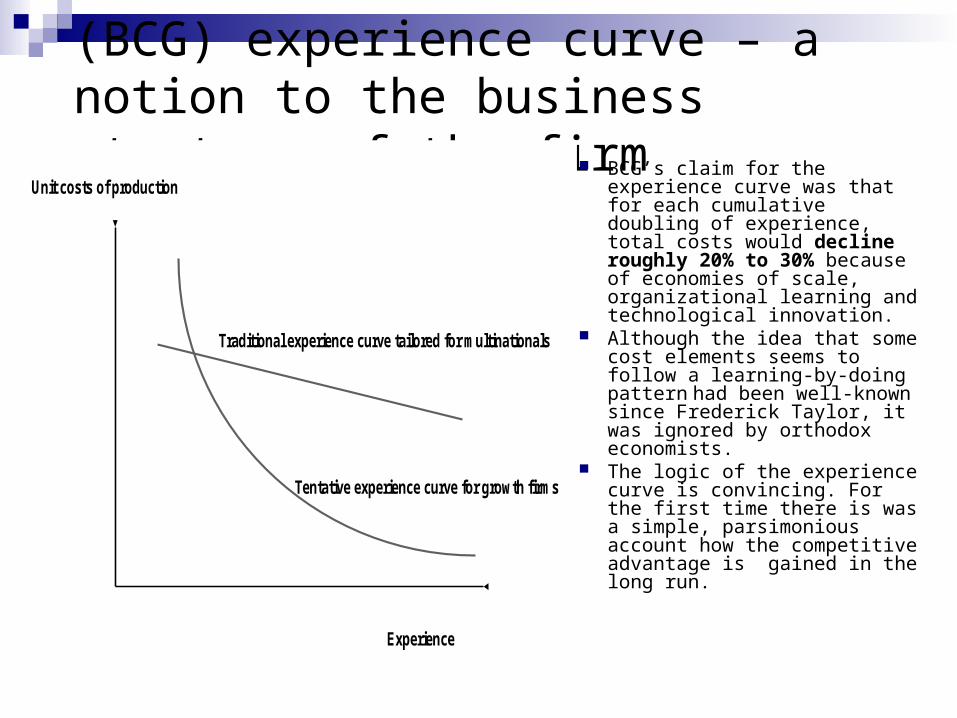

(BCG) experience curve – a notion to the business strategy of the firm

BCG’s claim for the experience curve was that for each cumulative doubling of experience, total costs would decline roughly 20% to 30% because of economies of scale, organizational learning and technological innovation.

Although the idea that some cost elements seems to follow a learning-by-doing pattern had been well-known since Frederick Taylor, it was ignored by orthodox economists.

The logic of the experience curve is convincing. For the first time there is was a simple, parsimonious account how the competitive advantage is gained in the long run.

Unit costs of production

Experience

Traditional experience curve tailored for multinationals

Tentative experience curve for growth firms

What is relevant experience?

Experience curve consists of two elements: 1. Scale economies: One of the key idea of modern microeconomics is that

a production unit, like a factory has its a) mimimum efficient scale of operation and b) optimal size depending the technology of product and production.

2. Learning curve: In the beginning of the past century, Frederick Taylor, the famous US work researcher, wrote his book Scientific Management in which he claimed that specialization inside the factory is critical to minimize the unit costs of a product produced.

Scale econonomies depend on general industrial infrastructure and distance to the target markets. If the industrial infrastructure is weakly developed, it is practically impossible to build up and maintain big, integrated production units to be efficient enough for international exchange. When a company is producing goods and services for international markets, its mimimum efficient scale of operation is much bigger than when it is serving only local makets and so do the optimal scale.

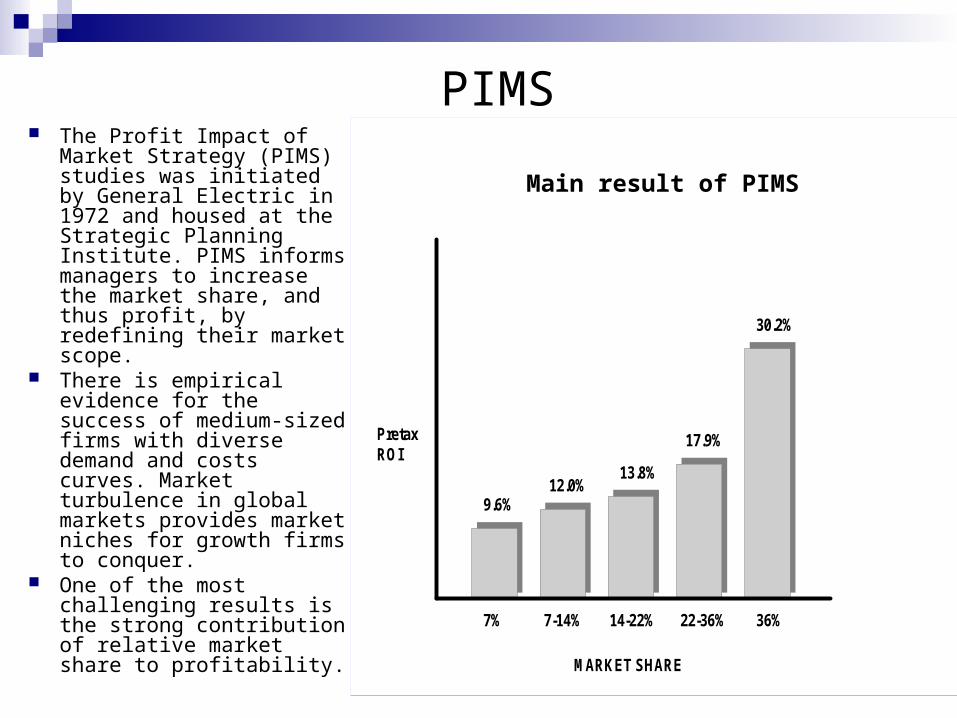

PIMS The Profit Impact of

Market Strategy (PIMS) studies was initiated by General Electric in 1972 and housed at the Strategic Planning Institute. PIMS informs managers to increase the market share, and thus profit, by redefining their market scope.

There is empirical evidence for the success of medium-sized firms with diverse demand and costs curves. Market turbulence in global markets provides market niches for growth firms to conquer.

One of the most challenging results is the strong contribution of relative market share to profitability.

PretaxROI

9.6%12.0%

13.8%

17.9%

30.2%

7% 7-14% 14-22% 22-36% 36%

MARKET SHARE

Main result of PIMS

Related Documents