Decentralization and Segment Reporting Chapter 12

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Decentralization and

Segment Reporting

Chapter

12

12-2

© McGraw-Hill Ryerson Limited., 2001

LEARNING OBJECTIVES

1. Differentiate between a cost centre, profitcentre and investment centre and explainhow performance is measured in each.

2. Prepare a segmented income statementusing the contribution format, and explain thedifference between traceable fixed costs andcommon fixed costs.

3. Identify three business practices that hinderproper cost assignment.

4. Analyze variances from revenue targets.

After studying this chapter, you should be able to:

12-3

© McGraw-Hill Ryerson Limited., 2001

LEARNING OBJECTIVES

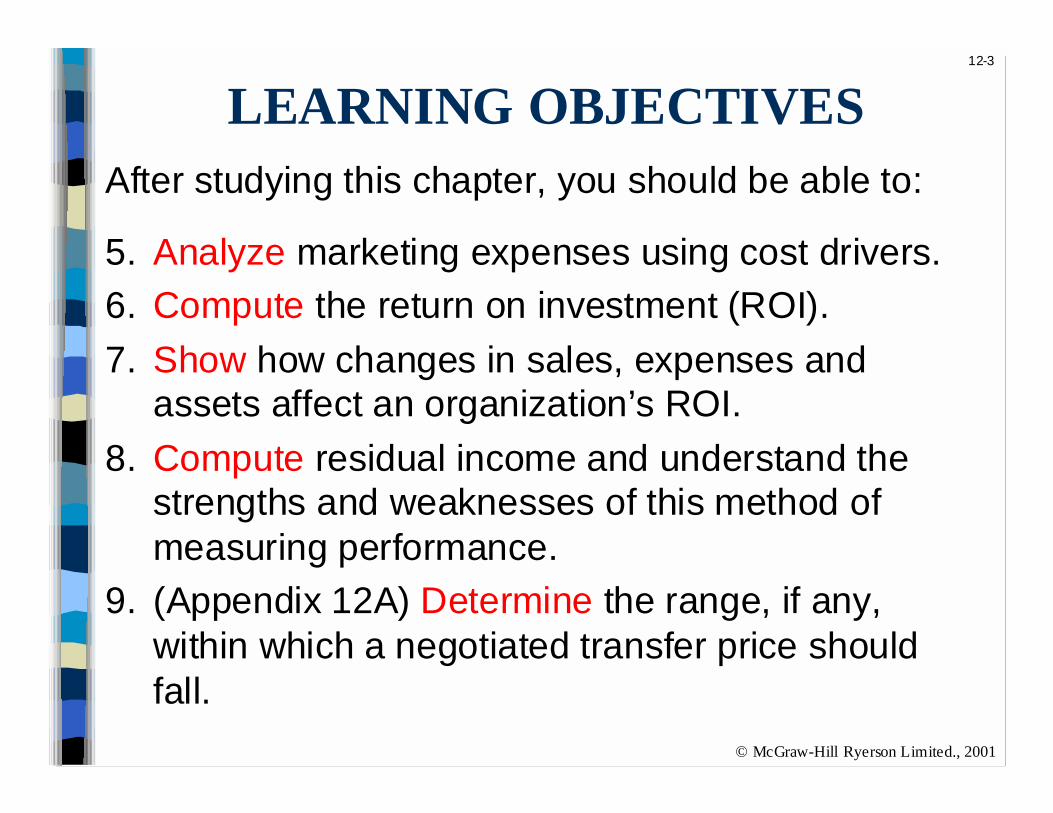

5. Analyze marketing expenses using cost drivers.

6. Compute the return on investment (ROI).

7. Show how changes in sales, expenses andassets affect an organization’s ROI.

8. Compute residual income and understand thestrengths and weaknesses of this method ofmeasuring performance.

9. (Appendix 12A) Determine the range, if any,within which a negotiated transfer price shouldfall.

After studying this chapter, you should be able to:

12-4

© McGraw-Hill Ryerson Limited., 2001

Decentralization in Organizations

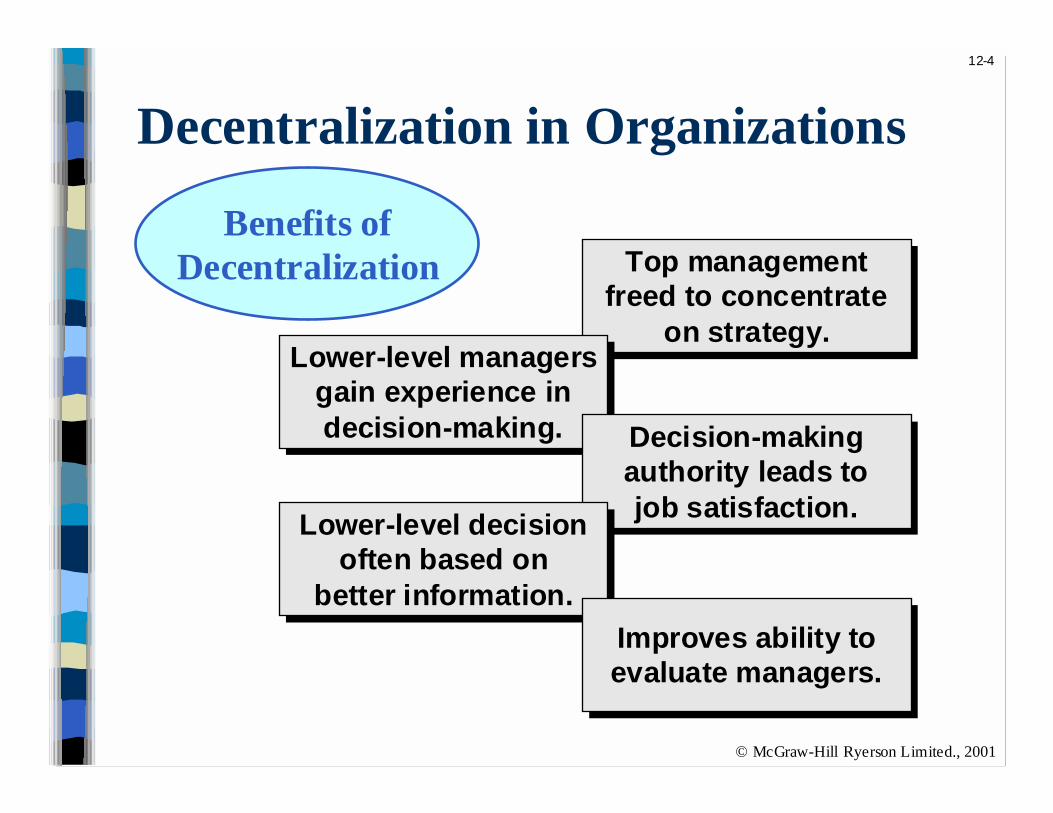

Benefits ofDecentralization Top management

freed to concentrateon strategy.

Top managementfreed to concentrate

on strategy.Lower-level managers

gain experience indecision-making.

Lower-level managersgain experience indecision-making. Decision-making

authority leads tojob satisfaction.

Decision-makingauthority leads tojob satisfaction.

Lower-level decisionoften based on

better information.

Lower-level decisionoften based on

better information.

Improves ability toevaluate managers.

Improves ability toevaluate managers.

12-5

© McGraw-Hill Ryerson Limited., 2001

Decentralization in Organizations

Disadvantages ofDecentralization

Lower-level managersmay make decisionswithout seeing the

“big picture.”

Lower-level managersmay make decisionswithout seeing the

“big picture.”

May be a lack ofcoordination among

autonomousmanagers.

May be a lack ofcoordination among

autonomousmanagers.

Lower-level manager’sobjectives may not

be those of theorganization.

Lower-level manager’sobjectives may not

be those of theorganization.

May be difficult tospread innovative ideas

in the organization.

May be difficult tospread innovative ideas

in the organization.

12-6

© McGraw-Hill Ryerson Limited., 2001

Decentralization and Segment Reporting

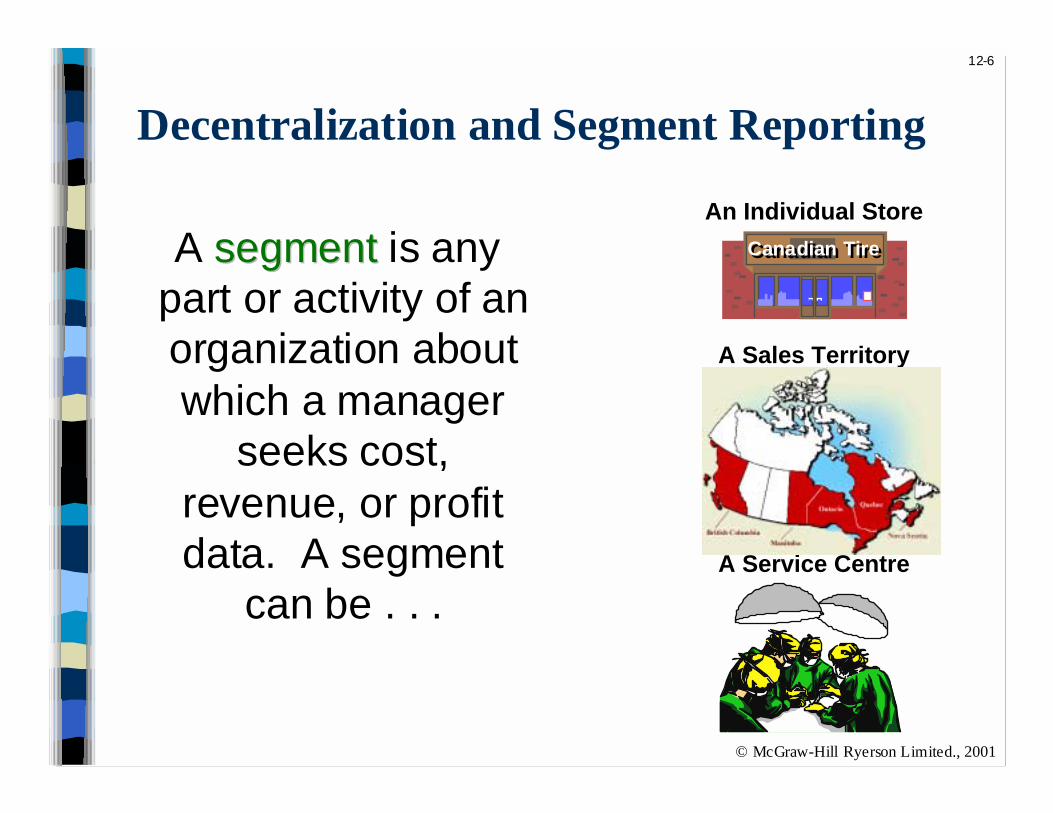

A segmentsegment is anypart or activity of anorganization aboutwhich a manager

seeks cost,revenue, or profitdata. A segment

can be . . .

Canadian TireCanadian Tire

An Individual Store

A Sales Territory

A Service Centre

12-7

© McGraw-Hill Ryerson Limited., 2001

Cost, Profit and Investment Centres

Cost Centre A segment whose

manager hascontrol over costs,

but not overrevenues or

investment funds. CostCost

Cost

12-8

© McGraw-Hill Ryerson Limited., 2001

Cost, Profit and Investment Centres

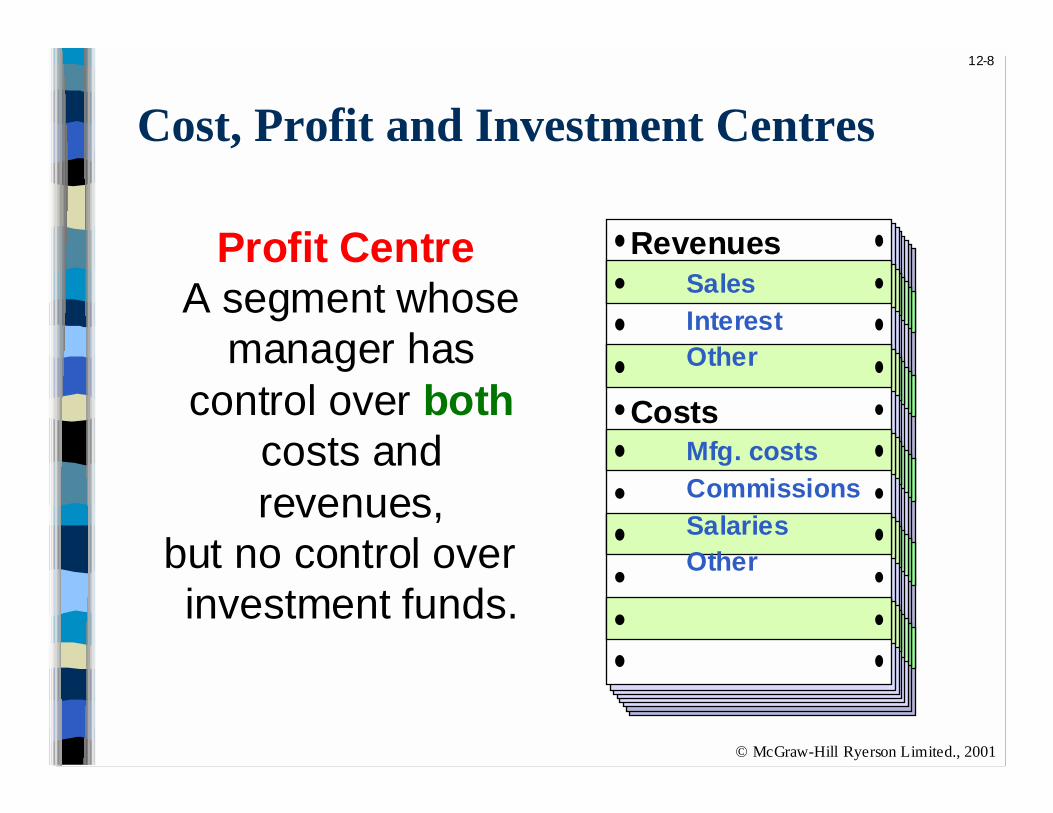

Profit Centre A segment whose

manager hascontrol over both

costs andrevenues,

but no control overinvestment funds.

RevenuesSales

InterestOther

CostsMfg. costs

Commissions

SalariesOther

12-9

© McGraw-Hill Ryerson Limited., 2001

Cost, Profit and Investment Centres

Investment Centre

A segment whosemanager has

control over costs,revenues, andinvestments in

operating assets.

Corporate Headquarters

12-10

© McGraw-Hill Ryerson Limited., 2001

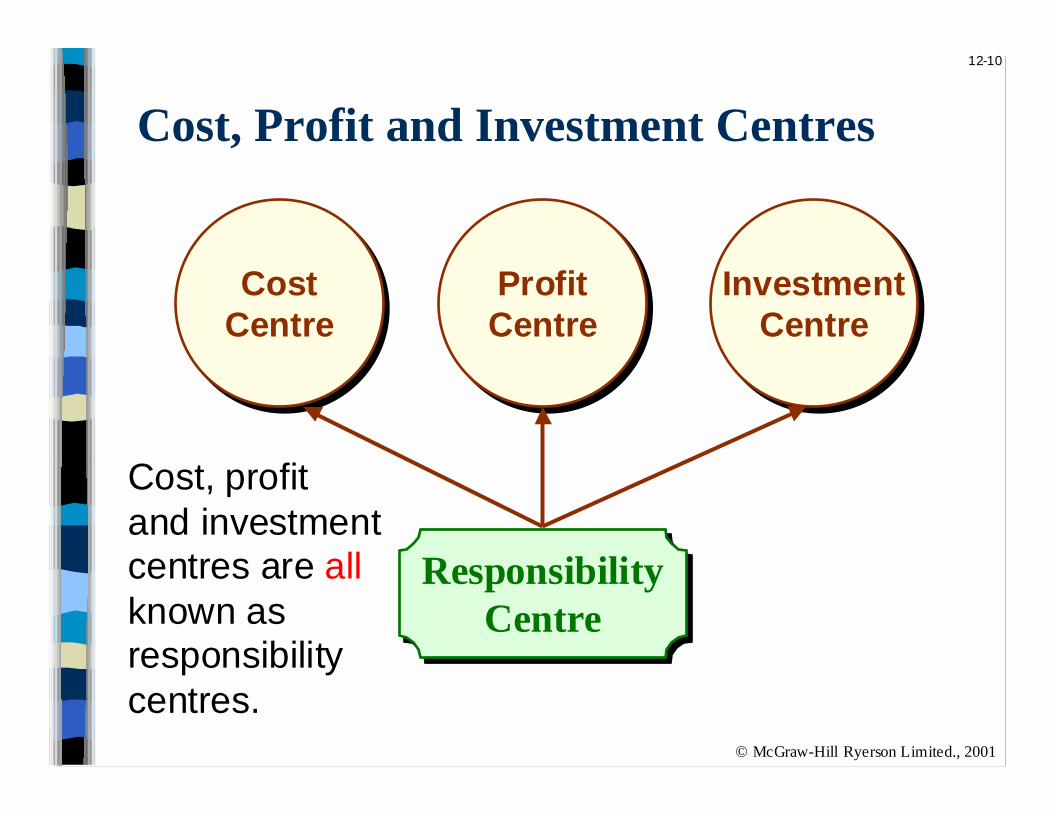

Cost, Profit and Investment Centres

ResponsibilityCentre

ResponsibilityCentre

CostCentreCost

CentreProfitCentreProfitCentre

InvestmentCentre

InvestmentCentre

Cost, profitand investmentcentres are allknown asresponsibilitycentres.

12-11

© McGraw-Hill Ryerson Limited., 2001

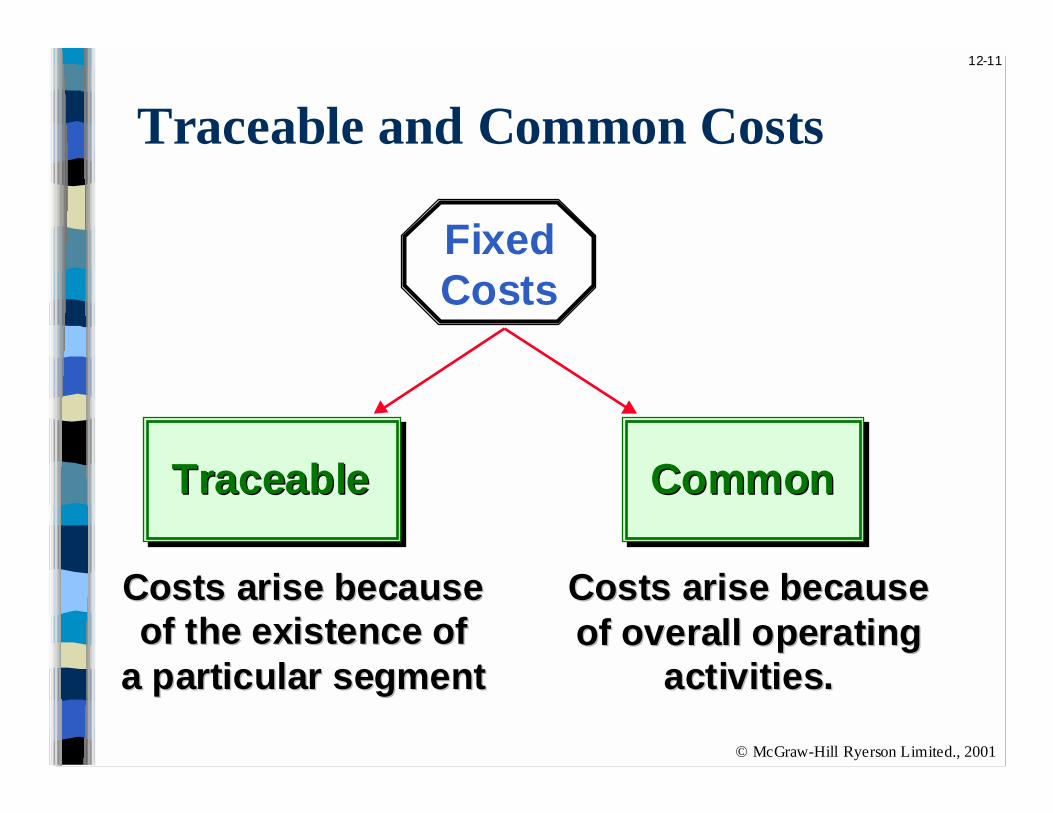

Traceable and Common Costs

FixedCosts

TraceableTraceable CommonCommon

Costs arise becauseCosts arise becauseof the existence ofof the existence of

a particular segmenta particular segment

Costs arise becauseCosts arise becauseof overall operatingof overall operating

activities.activities.

12-12

© McGraw-Hill Ryerson Limited., 2001

Traceable and Common Costs

FixedCosts

TraceableTraceable CommonCommon

Costs arise becauseCosts arise becauseof the existence ofof the existence of

a particular segmenta particular segment

Costs arise becauseCosts arise becauseof overall operatingof overall operating

activities.activities.

Don’t allocateDon’t allocatecommon costs.common costs.

12-13

© McGraw-Hill Ryerson Limited., 2001

Identifying Traceable Fixed Costs

Traceable costs would disappear overtime if the segment itself disappeared.

No computer No computer division means . . .division means . . .

No computerNo computerdivision manager.division manager.

12-14

© McGraw-Hill Ryerson Limited., 2001

Identifying Common Fixed Costs

Common costs arise because of overalloperation of the company and are not due to

the existence of a particular segment.

No computer No computer division but . . .division but . . .

We still have aWe still have acompany president.company president.

12-15

© McGraw-Hill Ryerson Limited., 2001

Levels of Segmented Statements

Let’s look more closely at the TelevisionDivision’s income statement.

Let’s look more closely at the TelevisionDivision’s income statement.

W ebber, Inc. has two divisions.

Computer Division Television Division

Webber, Inc.

12-16

© McGraw-Hill Ryerson Limited., 2001

Levels of Segmented Statements

Our approach to segment reporting uses thecontribution format.

Income StatementContribution Margin Format

Television DivisionSales 300,000$ Variable COGS 120,000 Other variable costs 30,000 Total variable costs 150,000 Contribution margin 150,000 Traceable fixed costs 90,000 Segment margin 60,000$

Cost of goodssold consists of

variable manufacturing

costs.

Cost of goodssold consists of

variable manufacturing

costs.

Fixed andvariable costsare listed in

separatesections.

Fixed andvariable costsare listed in

separatesections.

12-17

© McGraw-Hill Ryerson Limited., 2001

Levels of Segmented Statements

Our approach to segment reporting uses thecontribution format.

Income StatementContribution Margin Format

Television DivisionSales 300,000$ Variable COGS 120,000 Other variable costs 30,000 Total variable costs 150,000 Contribution margin 150,000 Traceable fixed costs 90,000 Segment margin 60,000$

Segment marginis Television’s

contributionto overall

operations.

Segment marginis Television’s

contributionto overall

operations.

12-18

© McGraw-Hill Ryerson Limited., 2001

Levels of Segmented Statements

Let’s see how the TelevisionLet’s see how the TelevisionDivision fits into Webber, Inc.Division fits into Webber, Inc.

12-19

© McGraw-Hill Ryerson Limited., 2001

Levels of Segmented Statements

Income Statem ent

Company Television Compute rSa les 300,000$ Va ria ble costs (150,000) CM 150,000 Tra ce a ble FC (90,000) Division ma rgin 60,000

Comm on costsNe t incom e

Let’s add the Com puterLet’s add the Com puterDivision’s num bers.Division’s num bers.

Segment margin has nowbecome division margin.

Segment margin has nowbecome division margin.

12-20

© McGraw-Hill Ryerson Limited., 2001

Levels of Segmented Statements

Income Statem ent

Company Television Compute rSa les 500,000$ 300,000$ 200,000$ Va ria ble costs (230,000) (150,000) (80,000) CM 270,000 150,000 120,000 Tra ce a ble FC (170,000) (90,000) (80,000) Division ma rgin 100,000 60,000 40,000

Comm on costsNe t incom e

12-21

© McGraw-Hill Ryerson Limited., 2001

Levels of Segmented Statements

Income Statem ent

Company Television Compute rSa les 500,000$ 300,000$ 200,000$ Va ria ble costs (230,000) (150,000) (80,000) CM 270,000 150,000 120,000 Tra ce a ble FC (170,000) (90,000) (80,000) Division ma rgin 100,000 60,000 40,000

Comm on costs (25,000) Ne t incom e 75,000$

Common costs arise because of overalloperating activities. ABC may be helpful

in the analysis of common costs.

Common costs arise because of overalloperating activities. ABC may be helpful

in the analysis of common costs.

12-22

© McGraw-Hill Ryerson Limited., 2001

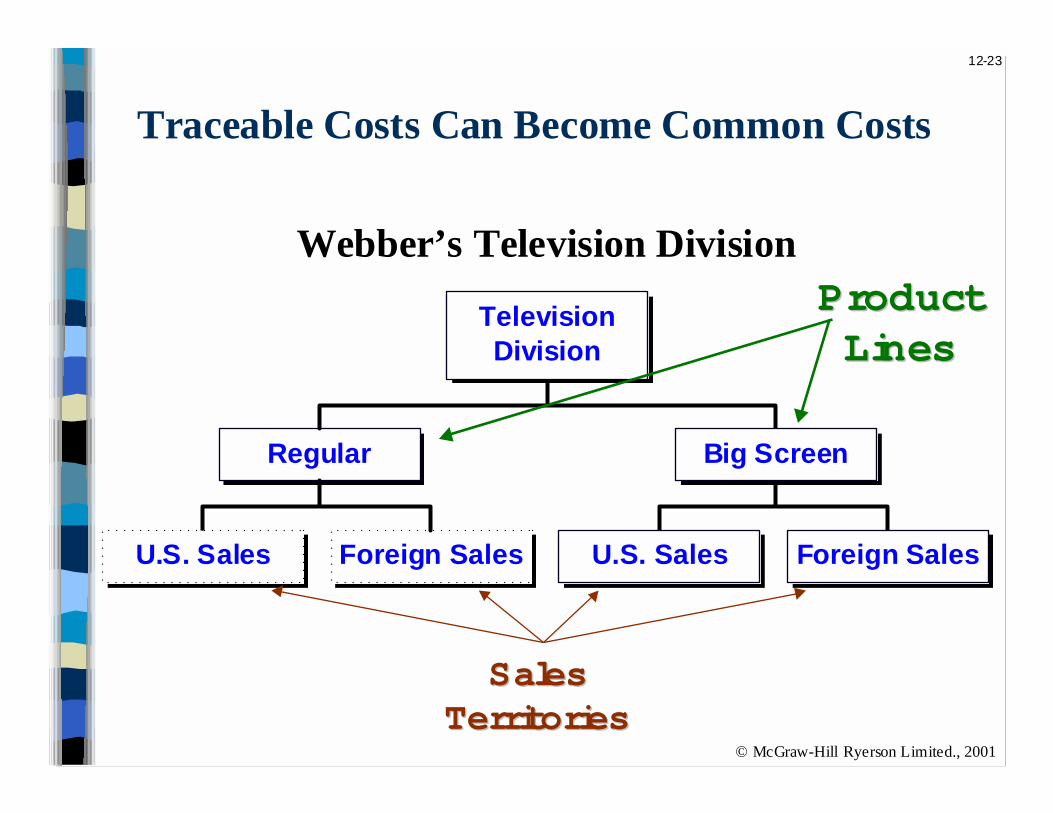

Traceable Costs Can Become Common Costs

Fixed costs that are traceable on onesegmented statement can become

common if the company is divided intosmaller smaller segments.

Let’s see how this works!

12-23

© McGraw-Hill Ryerson Limited., 2001

U.S. Sales Foreign Sales

Regular

U.S. Sales Foreign Sales

Big Screen

TelevisionDivision

Traceable Costs Can Become Common Costs

ProductProductLinesLines

SalesSalesTerritoriesTerritories

Webber’s Television Division

12-24

© McGraw-Hill Ryerson Limited., 2001

Traceable Costs Can Become Common Costs

W e obtained the follow ing inform ation fromthe Regular and Big Screen segm ents.

Income Statement Television

Division Regular Big ScreenSales 200,000$ 100,000$ Variable costs (95,000) (55,000) CM 105,000 45,000 Traceable FC (45,000) (35,000) Product line margin 60,000 10,000

Common costsDivisional margin

12-25

© McGraw-Hill Ryerson Limited., 2001

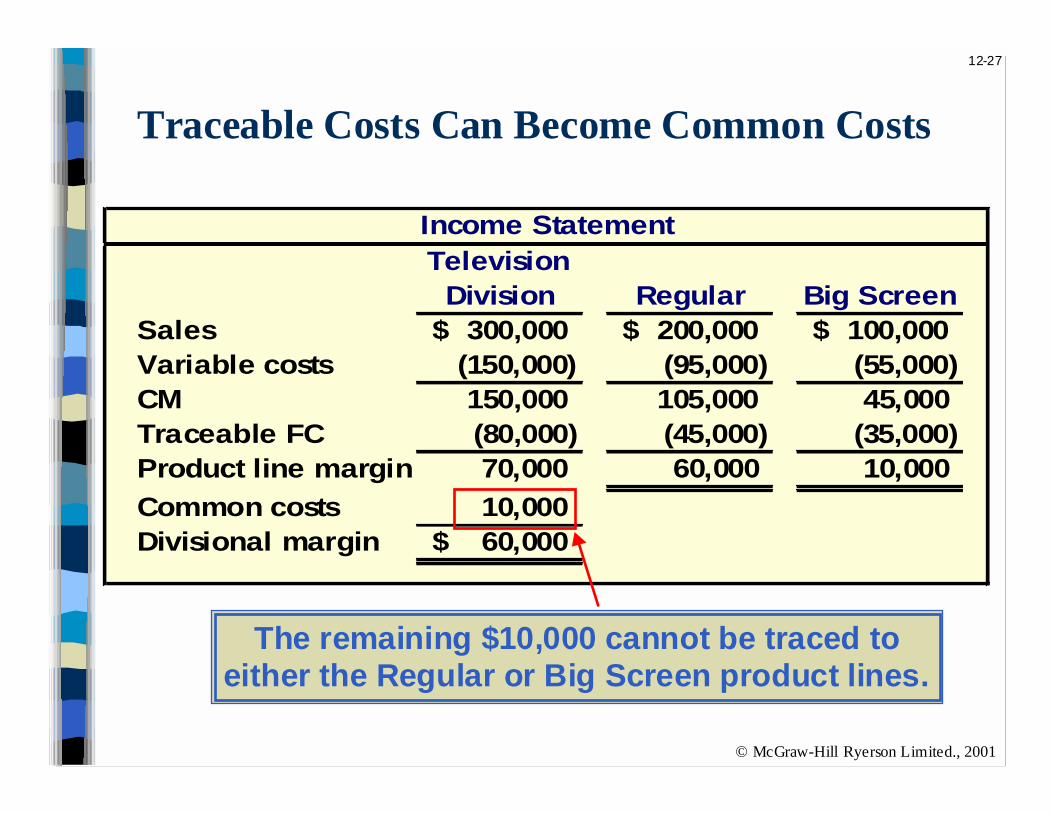

Income Statement Television

Division Regular Big ScreenSales 300,000$ 200,000$ 100,000$ Variable costs (150,000) (95,000) (55,000) CM 150,000 105,000 45,000 Traceable FC (80,000) (45,000) (35,000) Product line margin 70,000 60,000 10,000

Common costs 10,000 Divisional margin 60,000$

Traceable Costs Can Become Common Costs

Fixed costs directly tracedto the Television Division

$80,000 + $10,000 = $90,000

Fixed costs directly tracedto the Television Division

$80,000 + $10,000 = $90,000

12-26

© McGraw-Hill Ryerson Limited., 2001

Income StatementTelevision Division Regular Big Screen

Sales 300,000$ 200,000$ 100,000$ Variable costs (150,000) (95,000) (55,000) CM 150,000 105,000 45,000 Traceable FC (80,000) (45,000) (35,000) Product line margin 70,000 60,000 10,000

Common costs 10,000 Divisional margin 60,000$

Traceable Costs Can Become Common Costs

Of the $90,000 cost directly traced tothe Television Division, $45,000 istraceable to Regular and $35,000

traceable to Big Screen product lines.

12-27

© McGraw-Hill Ryerson Limited., 2001

Income StatementTelevision

Division Regular Big ScreenSales 300,000$ 200,000$ 100,000$ Variable costs (150,000) (95,000) (55,000) CM 150,000 105,000 45,000 Traceable FC (80,000) (45,000) (35,000) Product line margin 70,000 60,000 10,000

Common costs 10,000 Divisional margin 60,000$

Traceable Costs Can Become Common Costs

The remaining $10,000 cannot be traced toeither the Regular or Big Screen product lines.

12-28

© McGraw-Hill Ryerson Limited., 2001

Segment Margin

The segment margin is the best gauge best gauge ofthe long-run profitability of a segment.

TimeTime

Pro

fits

Pro

fits

12-29

© McGraw-Hill Ryerson Limited., 2001

Hindrances to Proper Cost Assignment

Three Problem sThree Problem s

Omission of some

costs in the

assignment process.

The use of inappropriate

methods for allocating

costs among segments.

Assignment of costs

to segments that are

really common costs of

the entire organization.

12-30

© McGraw-Hill Ryerson Limited., 2001

Omission of CostsCosts assigned to a segment should include all

costs attributable to that segment from thecompany’s entire value chainvalue chain.

Life cycle costingLife cycle costing focuses on all costs along thevalue chain that will be generated throughout

the entire life of the product.

Product Customer R&D Design Manufacturing Marketing Distribution Service

Business FunctionsBusiness FunctionsMaking Up TheMaking Up The

Value ChainValue Chain

12-31

© McGraw-Hill Ryerson Limited., 2001

Inappropriate Methods of AllocatingCosts Among Segments

Segment3

Segment4

FailureFailure to trace to tracecosts directlycosts directly

Arbitrarily dividingArbitrarily dividingcommon costscommon costs

among segmentsamong segmentsInappropriateInappropriate

allocation baseallocation base

Segment2

Segment1

12-32

© McGraw-Hill Ryerson Limited., 2001

Revenue Variance AnalysisConsider the following example for CardCo:

Budget Actual

Budget sales in units:

Deluxe cards 14,000 17,000

Standard cards 6,000 5,000

Budget price per unit:

Deluxe cards $18 $16

Standard cards $ 9 $10

Market volume expected:

Deluxe cards 75,000 85,000

Standard cards 95,000 90,000

Variable cost per unit:

Deluxe cards $ 8 $ 8

Standard cards $ 3 $ 3

12-33

© McGraw-Hill Ryerson Limited., 2001

Revenue Variance Analysis

Revenue: Deluxe (17,000x16) 272,000$ Standard (5,000x10) 50,000

322,000 Variable expenses: Deluxe (17,000x8) 136,000 Standard (5,000x3) 15,000

151,000 Contribution margin 171,000$

Actual Results Flexible Budget Master Budget

Actual results are based onthe actualactual quantity soldmultiplied by the actualactual

selling price or

variable cost

CardCo Actual and Budgeted Results

12-34

© McGraw-Hill Ryerson Limited., 2001

Revenue Variance Analysis

Revenue: Deluxe (17,000x16) 272,000$ (17,000x18) 306,000$ Standard (5,000x10) 50,000 (5,000x9) 45,000

322,000 351,000 Variable expenses: Deluxe (17,000x8) 136,000 (17,000x8) 136,000 Standard (5,000x3) 15,000 (5,000x3) 15,000

151,000 151,000 Contribution margin 171,000$ 200,000$

Actual Results Flexible Budget Master Budget

Flexible budget results arebased on the actualactual quantity

sold multiplied by the budgetedbudgetedselling price

orvariable cost

CardCo Actual and Budgeted Results

12-35

© McGraw-Hill Ryerson Limited., 2001

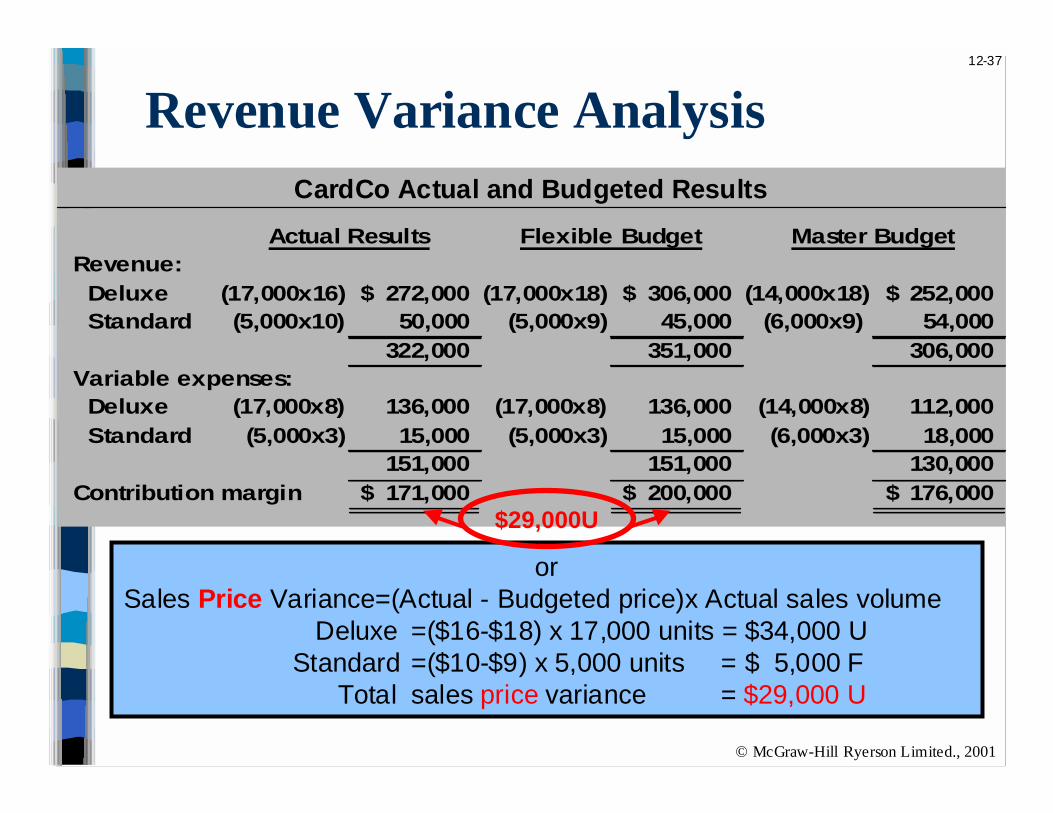

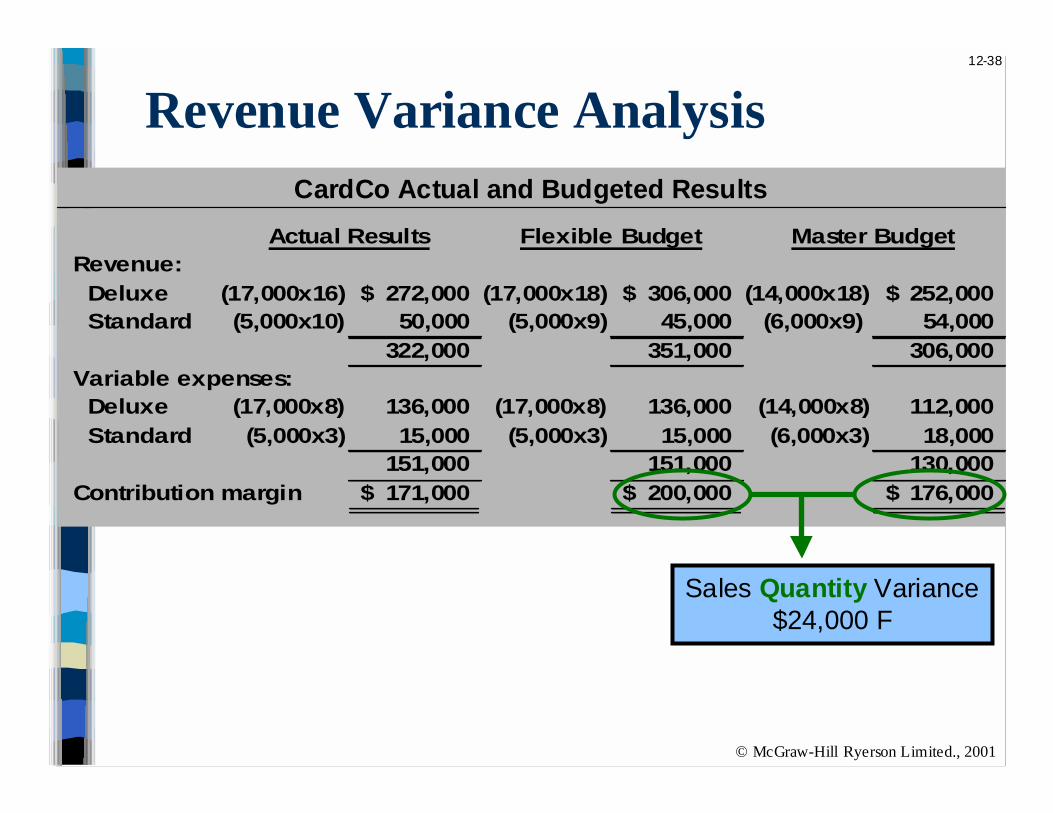

Revenue Variance Analysis

Revenue: Deluxe (17,000x16) 272,000$ (17,000x18) 306,000$ (14,000x18) 252,000$ Standard (5,000x10) 50,000 (5,000x9) 45,000 (6,000x9) 54,000

322,000 351,000 306,000 Variable expenses: Deluxe (17,000x8) 136,000 (17,000x8) 136,000 (14,000x8) 112,000 Standard (5,000x3) 15,000 (5,000x3) 15,000 (6,000x3) 18,000

151,000 151,000 130,000 Contribution margin 171,000$ 200,000$ 176,000$

Actual Results Flexible Budget Master Budget

Master budget results arebased on the budgetedbudgeted quantitysold multiplied by the budgetedbudgeted

selling price or

variable cost

CardCo Actual and Budgeted Results

12-36

© McGraw-Hill Ryerson Limited., 2001

Revenue Variance Analysis

Revenue: Deluxe (17,000x16) 272,000$ (17,000x18) 306,000$ (14,000x18) 252,000$ Standard (5,000x10) 50,000 (5,000x9) 45,000 (6,000x9) 54,000

322,000 351,000 306,000 Variable expenses: Deluxe (17,000x8) 136,000 (17,000x8) 136,000 (14,000x8) 112,000 Standard (5,000x3) 15,000 (5,000x3) 15,000 (6,000x3) 18,000

151,000 151,000 130,000 Contribution margin 171,000$ 200,000$ 176,000$

Actual Results Flexible Budget Master Budget

Sales Price Variance$29,000 U

CardCo Actual and Budgeted Results

12-37

© McGraw-Hill Ryerson Limited., 2001

Revenue Variance Analysis

Revenue: Deluxe (17,000x16) 272,000$ (17,000x18) 306,000$ (14,000x18) 252,000$ Standard (5,000x10) 50,000 (5,000x9) 45,000 (6,000x9) 54,000

322,000 351,000 306,000 Variable expenses: Deluxe (17,000x8) 136,000 (17,000x8) 136,000 (14,000x8) 112,000 Standard (5,000x3) 15,000 (5,000x3) 15,000 (6,000x3) 18,000

151,000 151,000 130,000 Contribution margin 171,000$ 200,000$ 176,000$

Actual Results Flexible Budget Master Budget

orSales Price Variance=(Actual - Budgeted price)x Actual sales volume

Deluxe =($16-$18) x 17,000 units = $34,000 U Standard =($10-$9) x 5,000 units = $ 5,000 F

Total sales price variance = $29,000 U

$29,000U

CardCo Actual and Budgeted Results

12-38

© McGraw-Hill Ryerson Limited., 2001

Revenue Variance Analysis

Revenue: Deluxe (17,000x16) 272,000$ (17,000x18) 306,000$ (14,000x18) 252,000$ Standard (5,000x10) 50,000 (5,000x9) 45,000 (6,000x9) 54,000

322,000 351,000 306,000 Variable expenses: Deluxe (17,000x8) 136,000 (17,000x8) 136,000 (14,000x8) 112,000 Standard (5,000x3) 15,000 (5,000x3) 15,000 (6,000x3) 18,000

151,000 151,000 130,000 Contribution margin 171,000$ 200,000$ 176,000$

Actual Results Flexible Budget Master Budget

Sales Quantity Variance$24,000 F

CardCo Actual and Budgeted Results

12-39

© McGraw-Hill Ryerson Limited., 2001

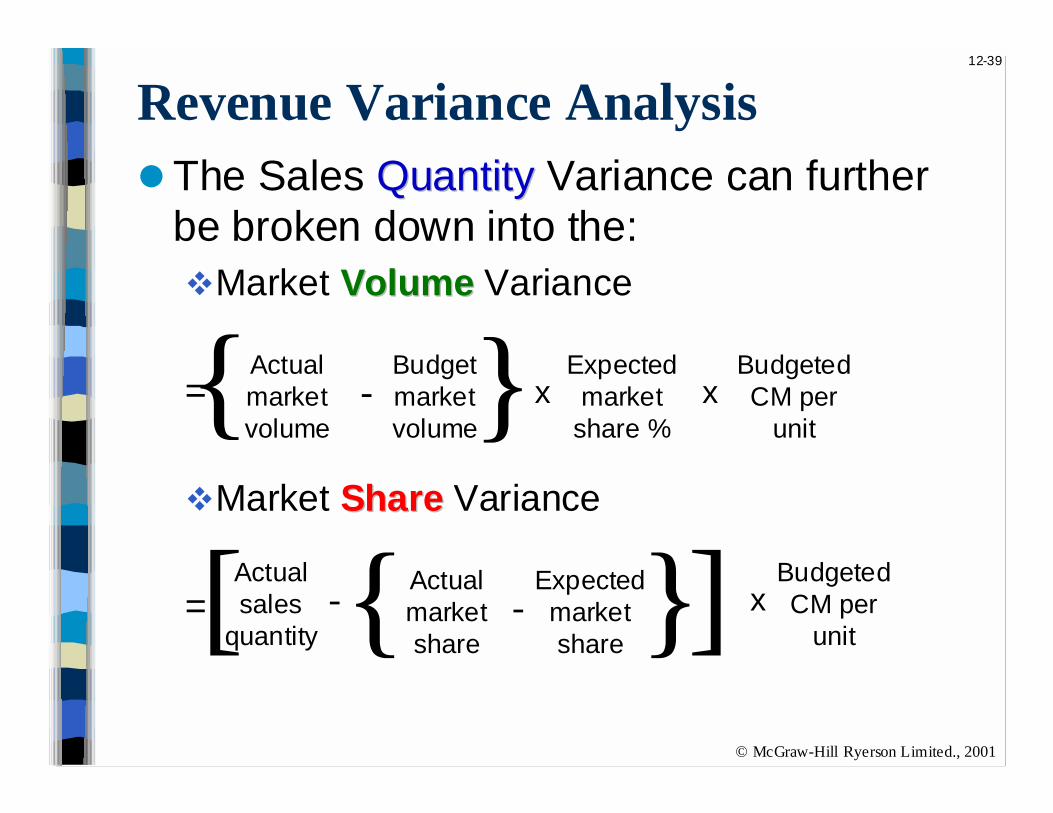

!The Sales QuantityQuantity Variance can furtherbe broken down into the:"Market VolumeVolume Variance

=

"Market ShareShare Variance

=

Revenue Variance Analysis

BudgetedCM per

unit

Actualmarketvolume

Budgetmarketvolume

-{ } x

BudgetedCM per

unitx

Actualmarketshare

-Expectedmarketshare }{

xExpectedmarket

share %

Actualsales

quantity-[ ]

12-40

© McGraw-Hill Ryerson Limited., 2001

!For CardCo, the Sales QuantityQuantity Varianceof $24,000 F breakdown further as follows:"Market VolumeVolume VarianceDeluxe=(85,000-75,000) x (14,000/75,000) x (18-8)=18,667 F

Standard=(90,000-95,000) x (6,000/95,000) x (9-3)= 1,895 U

Total Market Volume Variance ❶ =16,772 F16,772 F

"Market ShareShare VarianceDeluxe=[17,000-(85,000 x 14,000/75,000)] x (18-8) =11,333 F

Standard=[5,000-(90,000 x 6,000/95,000)] x (9-3) = 4,105 U

Total Market Share Variance = 7,228 F7,228 F

Sales QuantityQuantity Variance = ❶ + ❷ =24,000 F

Revenue Variance Analysis

❷

12-41

© McGraw-Hill Ryerson Limited., 2001

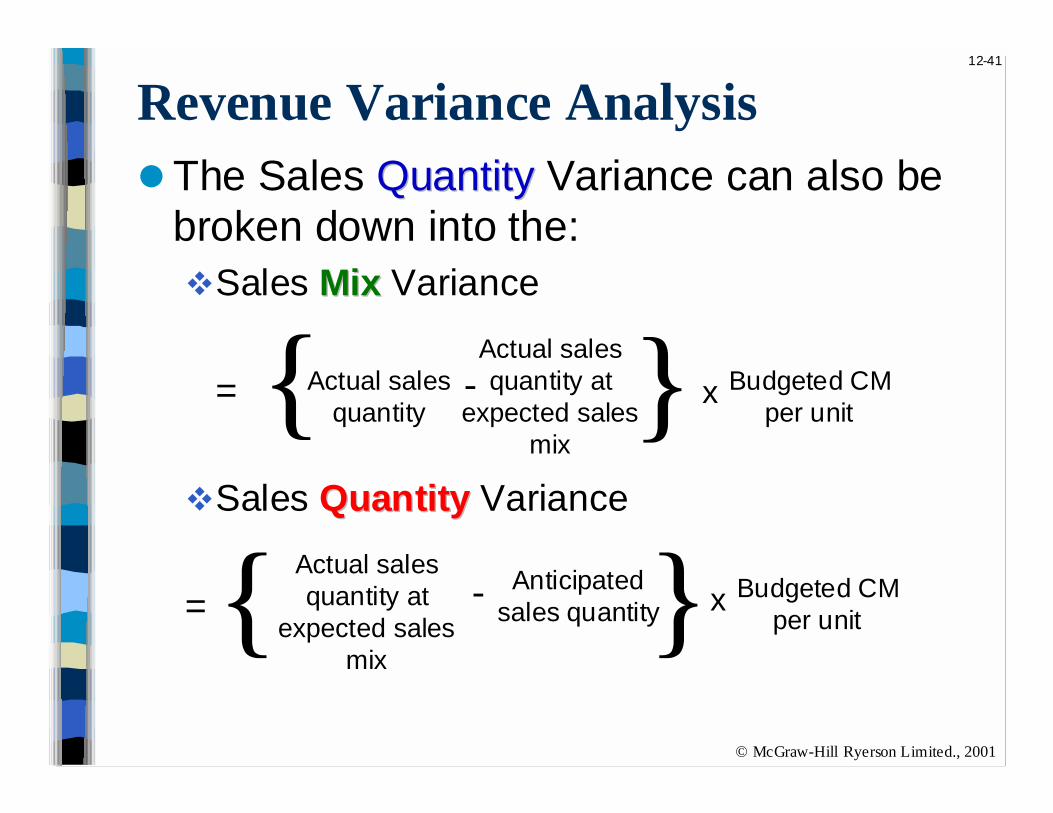

!The Sales QuantityQuantity Variance can also bebroken down into the:"Sales MixMix Variance

=

"Sales QuantityQuantity Variance

=

Revenue Variance Analysis

Actual salesquantity

Actual salesquantity at

expected salesmix

Budgeted CMper unit

-{ } x

Actual salesquantity at

expected salesmix

- Anticipatedsales quantity} Budgeted CM

per unitx{

12-42

© McGraw-Hill Ryerson Limited., 2001

!For CardCo, the Sales QuantityQuantity Varianceof $24,000F is made up of:"Sales MixMix VarianceDeluxe=[17,000-(22,000 x14/20)] x (18-8) =16,000 F

Standard=[(5,000-22,000 x 6/20)] x (9-3) = 9,600 U

Total Sales Mix Variance ❶ = 6,400 F6,400 F

"Sales QuantityQuantity VarianceDeluxe=[(22,000 x 14/20)-14,000] x (18-8) =14,000 F

Standard=[(22,000 x 6/20)-6,000] x (9-3) = 3,600 F

Total Sales Quantity Variance ❷ = 17,600F17,600F

Sales QuantityQuantity Variance = ❶ + ❷ = 24,000F

Revenue Variance Analysis

12-43

© McGraw-Hill Ryerson Limited., 2001

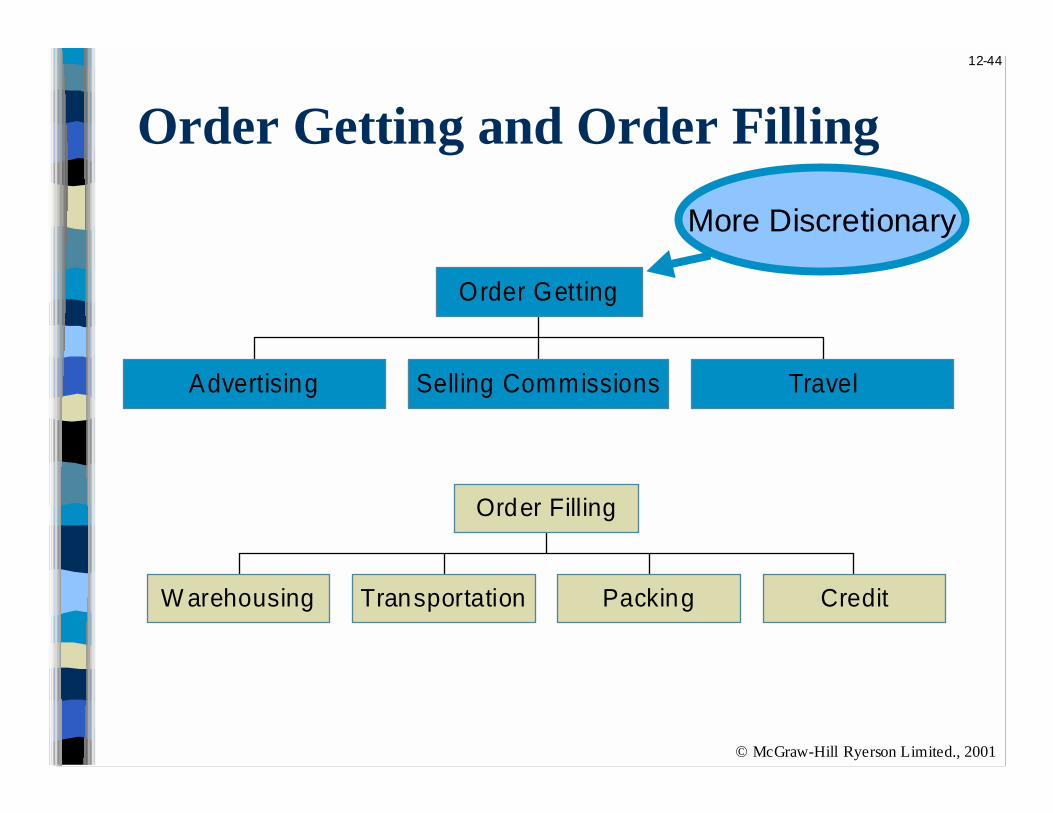

Costs factors to consider inmarketing strategy:

Marketing Strategy

Transport Warehousing

SellingAdvertising

Credit

12-44

© McGraw-Hill Ryerson Limited., 2001

Order Getting and Order Filling

Advertising Selling Commissions Travel

Order Getting

W arehousing Transportation Packing Credit

Order Filling

More Discretionary

12-45

© McGraw-Hill Ryerson Limited., 2001

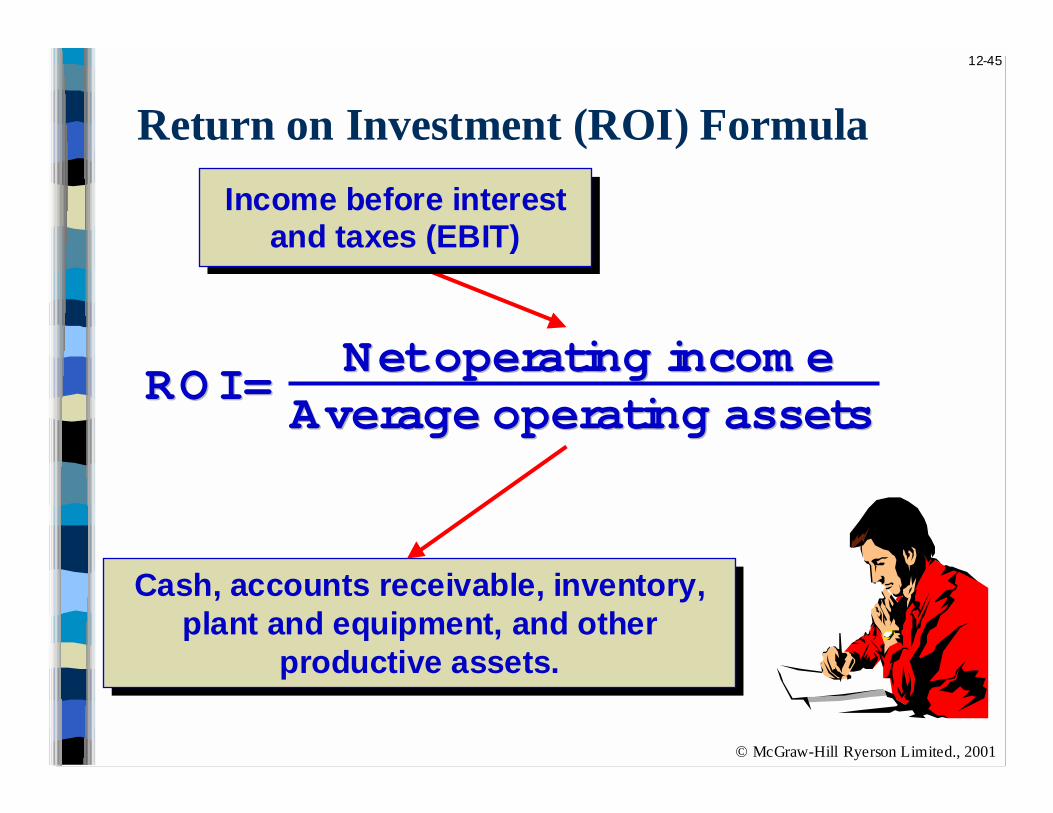

Return on Investment (ROI) Formula

ROI = ROI = Net operating incom eNet operating incom e

Average operating assets Average operating assets

Cash, accounts receivable, inventory,plant and equipment, and other

productive assets.

Cash, accounts receivable, inventory,plant and equipment, and other

productive assets.

Income before interestand taxes (EBIT)

Income before interestand taxes (EBIT)

12-46

© McGraw-Hill Ryerson Limited., 2001

Return on Investment (ROI) Formula

Regal Company reports the following:Regal Company reports the following:

Net operating income $ 30,000Net operating income $ 30,000

Average operating assets $ 200,000 Average operating assets $ 200,000

Sales $ 500,000 Sales $ 500,000

$30,000 $200,000

= 15%15%RO I =

12-47

© McGraw-Hill Ryerson Limited., 2001

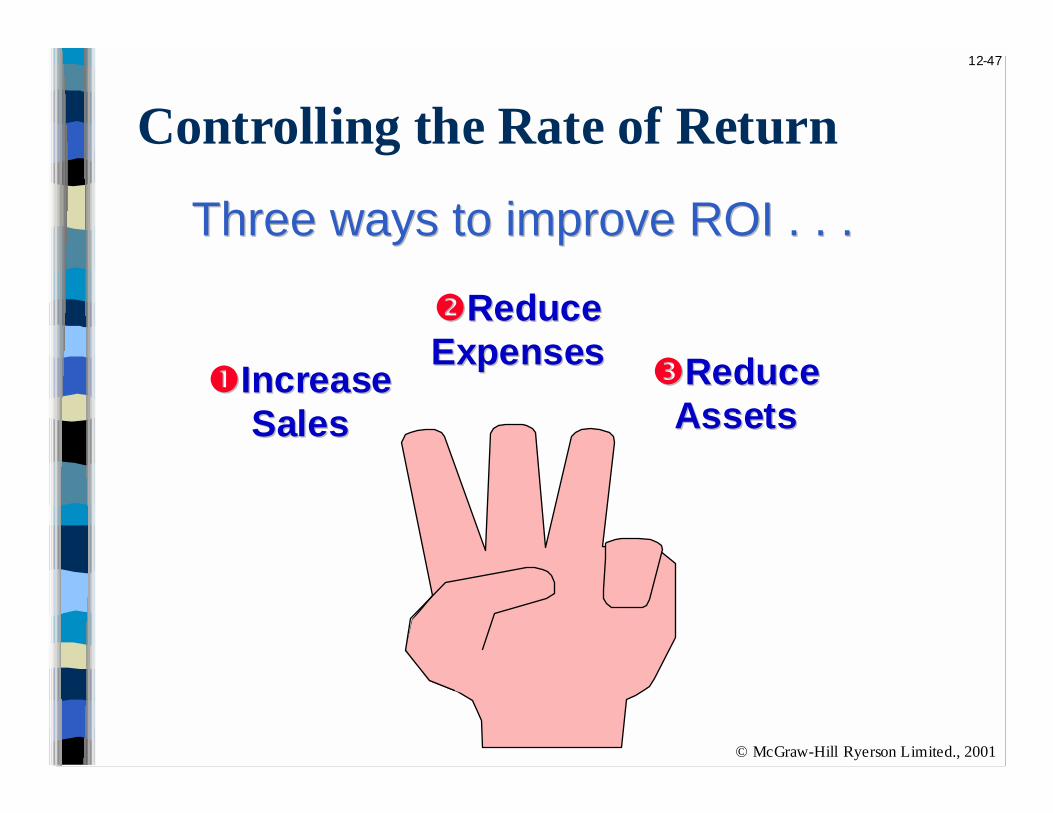

Controlling the Rate of Return

Three ways to improve ROI . . .Three ways to improve ROI . . .

##IncreaseIncreaseSalesSales

$$ReduceReduceExpensesExpenses

%%ReduceReduceAssetsAssets

12-48

© McGraw-Hill Ryerson Limited., 2001

Controlling the Rate of Return

!Regal’s manager was able to increasesales to $600,000 which increased netoperating income to $42,000.

!There was no change in the averageoperating assets of the segment.

Let’s calculate the new ROI.Let’s calculate the new ROI.

12-49

© McGraw-Hill Ryerson Limited., 2001

Return on Investment (ROI) Formula

Net operating incom e Sales

Sales Average operating assets

×RO I =

$42,000 $600,000

×$600,000$200,000

21%21%

We can modify our original formula slightly:

RO I =

RO I =

We increased ROI from 15% to 21%We increased ROI from 15% to 21%

Margin Turnover×

12-50

© McGraw-Hill Ryerson Limited., 2001

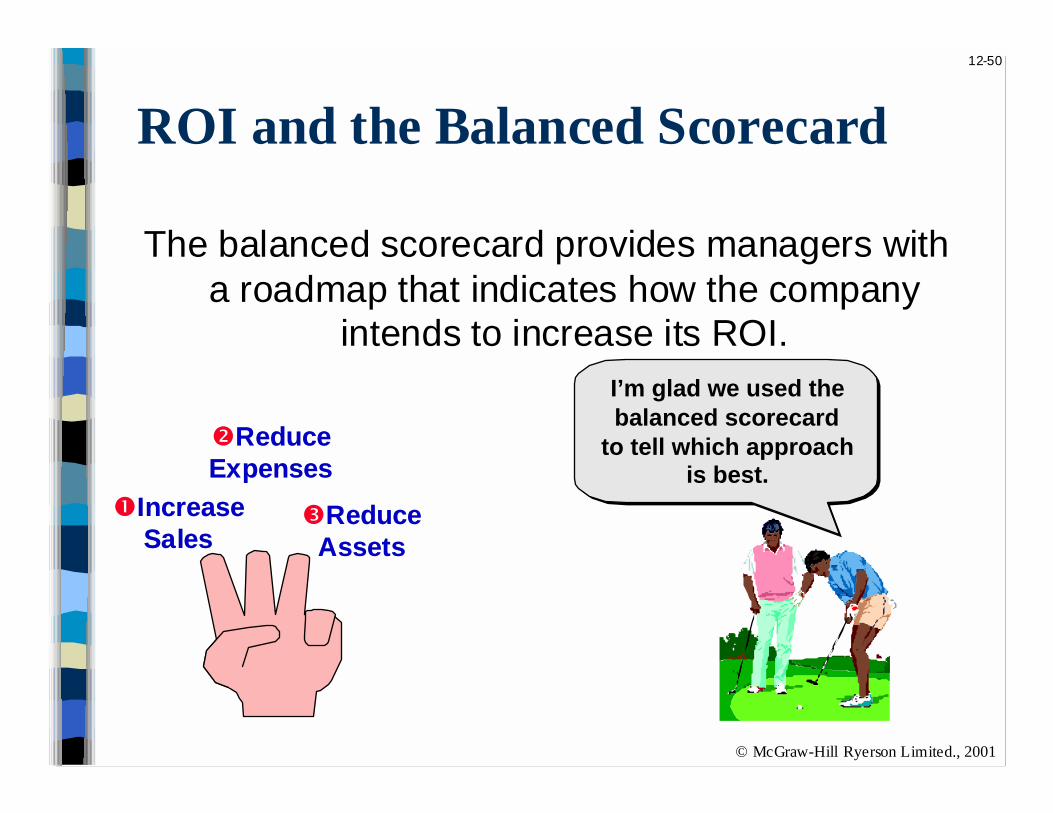

ROI and the Balanced Scorecard

The balanced scorecard provides managers witha roadmap that indicates how the company

intends to increase its ROI.

##IncreaseIncreaseSalesSales

$$ReduceReduceExpensesExpenses

%%ReduceReduceAssetsAssets

I’m glad we used thebalanced scorecard

to tell which approachis best.

I’m glad we used thebalanced scorecard

to tell which approachis best.

12-51

© McGraw-Hill Ryerson Limited., 2001

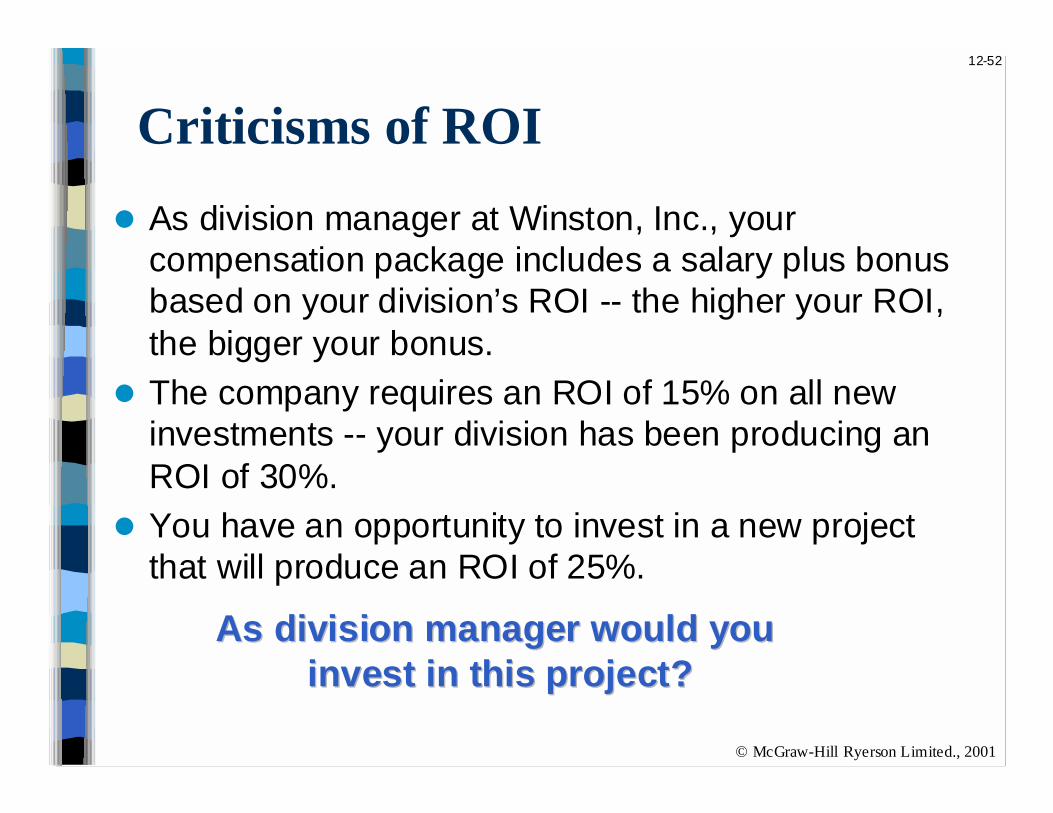

Criticisms of ROI

In the absence of the balancedscorecard, management may

not know how to increase ROI.

Managers often inherit manycommitted costs over which

they have no control.

Managers evaluated on ROImay reject profitable

investment opportunities.

12-52

© McGraw-Hill Ryerson Limited., 2001

Criticisms of ROI

! As division manager at Winston, Inc., yourcompensation package includes a salary plus bonusbased on your division’s ROI -- the higher your ROI,the bigger your bonus.

! The company requires an ROI of 15% on all newinvestments -- your division has been producing anROI of 30%.

! You have an opportunity to invest in a new projectthat will produce an ROI of 25%.

As division manager would you As division manager would you invest in this project?invest in this project?

12-53

© McGraw-Hill Ryerson Limited., 2001

Criticisms of ROI

As division manager,I wouldn’t invest in

that project becauseit would lower my pay!

12-54

© McGraw-Hill Ryerson Limited., 2001

Criticisms of ROI

Gee . . .I thought we were

supposed to do what was best for the

company!

12-55

© McGraw-Hill Ryerson Limited., 2001

Residual Income - Another Measure ofPerformance

Net operating incomeabove some minimum

return on operatingassets

12-56

© McGraw-Hill Ryerson Limited., 2001

Residual Income

!A division of Zepher, Inc. has averageoperating assets of $100,000 and isrequired to earn a return of 20% on theseassets.

! In the current period the division earns$30,000.

Let’s calculate residual incom e.Let’s calculate residual incom e.

12-57

© McGraw-Hill Ryerson Limited., 2001

Residual Income

Operating assets 100,000$ Required rate of return × 20%Required return 20,000$

Operating assets 100,000$ Required rate of return × 20%Required return 20,000$

Actual return 30,000$ Required return (20,000) Residual income 10,000$

Actual return 30,000$ Required return (20,000) Residual income 10,000$

12-58

© McGraw-Hill Ryerson Limited., 2001

Motivation and Residual Income

Residual incom e encourages m anagers to Residual incom e encourages m anagers to m ake profitable investm ents that w ouldm ake profitable investm ents that w ouldbe rejected by m anagers using RO I.be rejected by m anagers using RO I.

Transfer Pricing

Appendix

12A

12-60

© McGraw-Hill Ryerson Limited., 2001

Transfer Pricing

!Fundamental Objective:" Setting transfer prices to motivate the

managers to act in the

“best interest of the overall company”“best interest of the overall company”

12-61

© McGraw-Hill Ryerson Limited., 2001

Three Common Approaches:

Managers negotiatetheir own transfer price

❶

Set transfer price using either:1. Variable Cost, or2. Full (Absorption) Cost

❷

Set transfer price atmarket price

❸

12-62

© McGraw-Hill Ryerson Limited., 2001

Let’s get to workLet’s get to workon m y ROI . . .on m y ROI . . .

End of Chapter 12

Related Documents