Debt Placement Note Sales Investment Sales Equity Placement and Joint Ventures Structured Finance Loan Servicing Capital Markets Presentation Real Estate Capital Markets Outlook for 2005: Themes and Key Ideas

Debt Placement Note Sales Investment Sales Equity Placement and Joint Ventures Structured Finance Loan Servicing Capital Markets Presentation Real Estate.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Debt Placement

Note Sales

Investment Sales

Equity Placementand Joint Ventures

Structured Finance

Loan Servicing

Capital Markets PresentationReal Estate Capital Markets Outlook for 2005: Themes and Key Ideas

Dynamics - Flow Forces• G-I-Normous capital flow into commercial

real estate continues to propel pricing amidst scarcity of supply of investment-grade product.– Rate and Spread Compression

– Unprecedented IRR Compression

– Historic High $PSF

– IO, Open Prepay, Pre-Sales at Stabilized Value: Get the Flow Out!

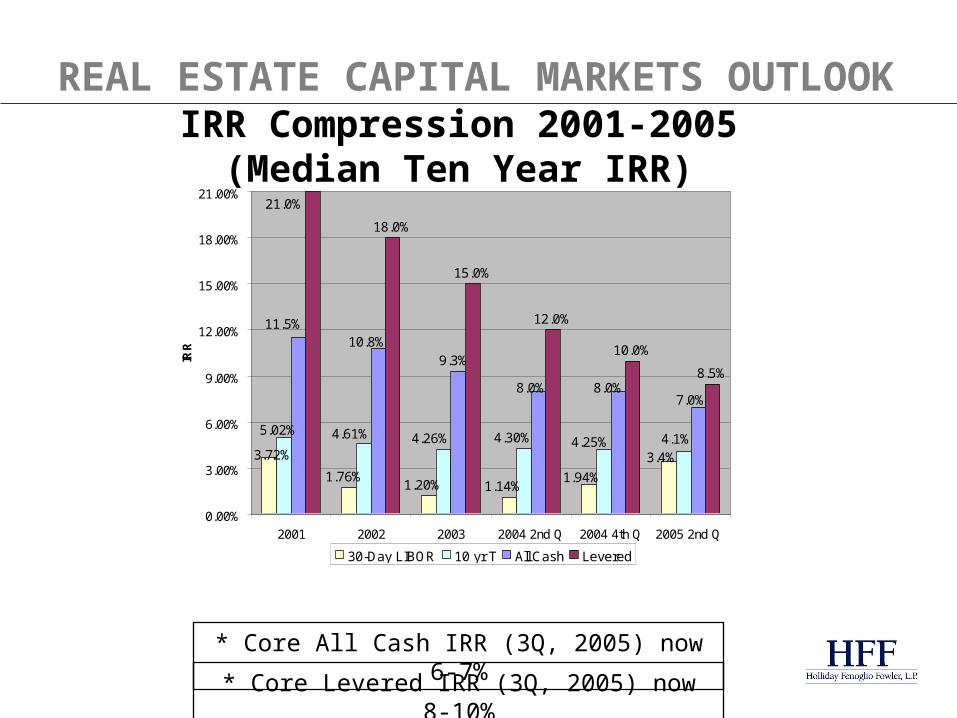

REAL ESTATE CAPITAL MARKETS OUTLOOK

IRR Compression 2001-2005(Median Ten Year IRR)

18.0%

15.0%

12.0%

10.0%

8.5%

3.4%

1.94%1.14%1.20%

1.76%

3.72%4.1%4.25%4.30%4.26%4.61%5.02%

10.8%11.5%

9.3%

7.0%8.0% 8.0%

21.0%

0.00%

3.00%

6.00%

9.00%

12.00%

15.00%

18.00%

21.00%

2001 2002 2003 2004 2nd Q 2004 4th Q 2005 2nd Q

IRR

30-Day LIBOR 10 yr T All Cash Levered

* Core All Cash IRR (3Q, 2005) now 6-7%

* Core Levered IRR (3Q, 2005) now 8-10%

REAL ESTATE CAPITAL MARKETS OUTLOOK

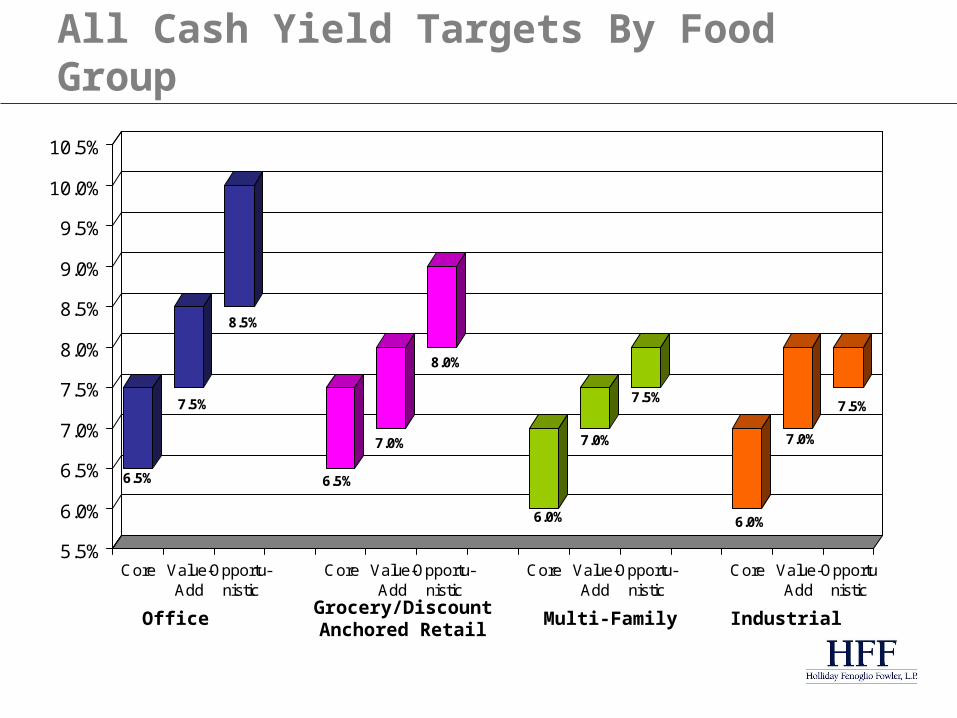

All Cash Yield Targets By Food Group

6.5%

7.5%

8.5%

6.5%

7.0%

8.0%

6.0%

7.0%

7.5%

6.0%

7.0%

7.5%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

Core Value-Add

Opportu-nistic

Core Value-Add

Opportu-nistic

Core Value-Add

Opportu-nistic

Core Value-Add

Opportunistic

7.5%

8.5%

10%

7.5%

8%

9%

7%

7.5%

8%

7%

8% 8%

OfficeGrocery/Discount Anchored Retail

Multi-Family Industrial

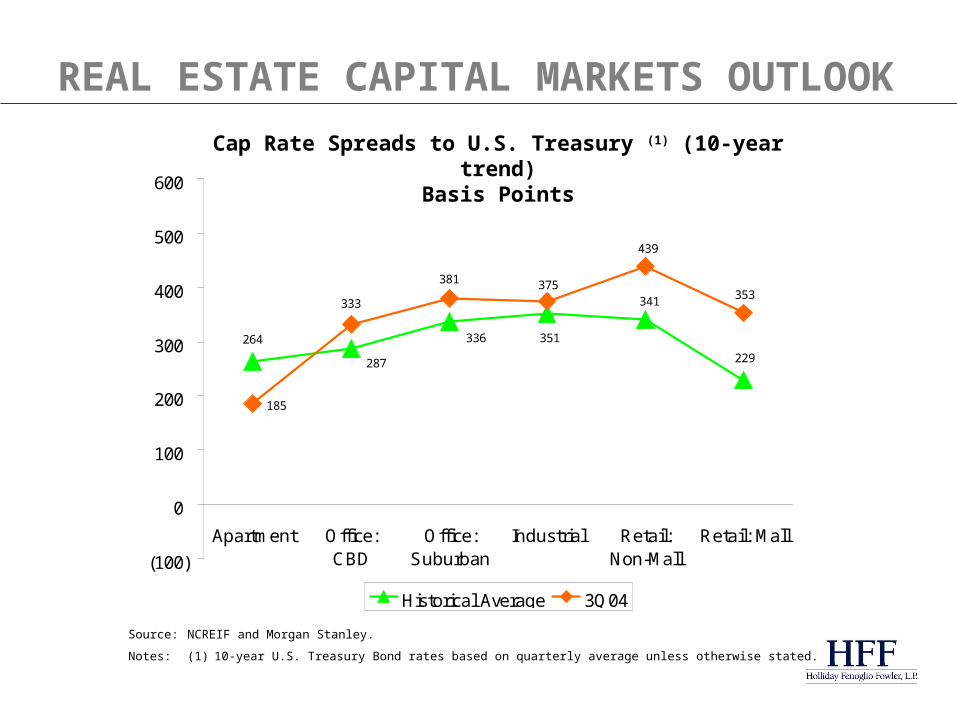

Cap Rate Spreads to U.S. Treasury (1) (10-year trend)Basis Points

185

229

341

351336

287

264

353

439

375381

333

(100)

0

100

200

300

400

500

600

Apartment Office:CBD

Office:Suburban

Industrial Retail:Non-Mall

Retail: Mall

Historical Average 3Q04

Source:NCREIF and Morgan Stanley.

Notes: (1)10-year U.S. Treasury Bond rates based on quarterly average unless otherwise stated.

REAL ESTATE CAPITAL MARKETS OUTLOOK

Exhib it 1 : Cap Rates Didn't Follow Treasuries Down, Why Would They Follow Them Up?

0%

2%

4%

6%

8%

10%

12%

Mar-93 Mar-94 Mar-95 Mar-96 Mar-97 Mar-98 Mar-99 Mar-00 Mar-01 Mar-02 Mar-03 Mar-04

Cap Rates and Interest Rates

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Vacancy RateImplied Office Cap Rate Ten-Year Treasury Rate Vacancy Rate

388 bps

135 bps247 bps

Sources: NCREIF; PPR

Office Cap Rates

Food Group Ranking

1.Retail

2.Trophy Office

2.Industrial

2.Multifamily

5.Office

6.Hotel

Food Group Ranking

1.Retail

2.Trophy Office

2.Industrial

2.Multifamily

5.Office

6.Hotel

Trophy Market Ranking

Washington, DC

NYC Metro

San Diego

“Edge” L.A.

Southern Florida

Trophy Market Ranking

Washington, DC

NYC Metro

San Diego

“Edge” L.A.

Southern Florida

Food Groups

Market Recovery

Seattle

Atlanta

St. Louis

Market Recovery

Seattle

Atlanta

St. Louis

REAL ESTATE CAPITAL MARKETS OUTLOOK

Dynamics - Flow Forces (Cont’d)• Mainstream Money Management- No

Longer Fringe Asset Class– Income-producing commercial real estate has

become favored risk-adjusted, fixed-income investment alternative.

– Lenders view real estate debt as attractive alternative to single-credit corporate paper.

– With better Corporate Junk Bonds yielding 6.5%, how is RE overpriced at 7%

REAL ESTATE CAPITAL MARKETS OUTLOOK

Dynamics - Flow Forces (Cont’d)• Allocation Trends Align with

Demographic Drivers– Retiree redemptions LOOM!! Most Important

Factor in All Investing for next Decade!

– Public and private joint venturing with tax-exempt institutions and foreign open-end funds to lever more purchasing power

– Surging syndicated equity drives pricing on the margin- Private REITs (INLAND as icon)

REAL ESTATE CAPITAL MARKETS OUTLOOK

Dynamics - Flow Forces (Cont’d)• Allocation Trends Align with Demographic

Drivers (Cont’d)Surging syndicated equity drives pricing on the margin

(Cont’d)

– Broker-dealer distribution and fee frenzy

– Hedge funds (Farollon – land spec in Mission Bay)

– Individual and Retirement Planning – RE as Standard Diversification Product (TIAA model)

REAL ESTATE CAPITAL MARKETS OUTLOOK

Dynamics - Flow Forces (Cont’d)• Commingled institutional equity rather

than separate account funding propels the tax-exempt fundraising.– More Co-Invest; More Discretion

– Many pension funds have raised RE allocations significantly

– Migration toward European model

REAL ESTATE CAPITAL MARKETS OUTLOOK

• Short-term capital (LIBOR-based) has been very stable.

− Low volatility beta over last 4 years.

− Sophisticated borrowers arbing LIBOR vs. Treasury, “Spread Investing”.

− 50% of securitized debt is unhedged and floating according to HFF data.

REAL ESTATE CAPITAL MARKETS OUTLOOK

• Mezz, Mezz, Mezz!!! Structured finance, especially mezzanine debt and preferred equity, booming. New niches like larger loans, longer-term mezz and aggressive, clubbed A-B packages. “Loan to Own” raiders on the loose.

– Who ISN’T Doing Mezz

– Compressed yields

REAL ESTATE CAPITAL MARKETS OUTLOOK

• Foreign investment capital, with weakening dollar, expanding in 2005

– German funds under scrutiny for yield performance

– Israeli and Middle East investors are very active and aggressive

– Japanese capital returning

REAL ESTATE CAPITAL MARKETS OUTLOOK

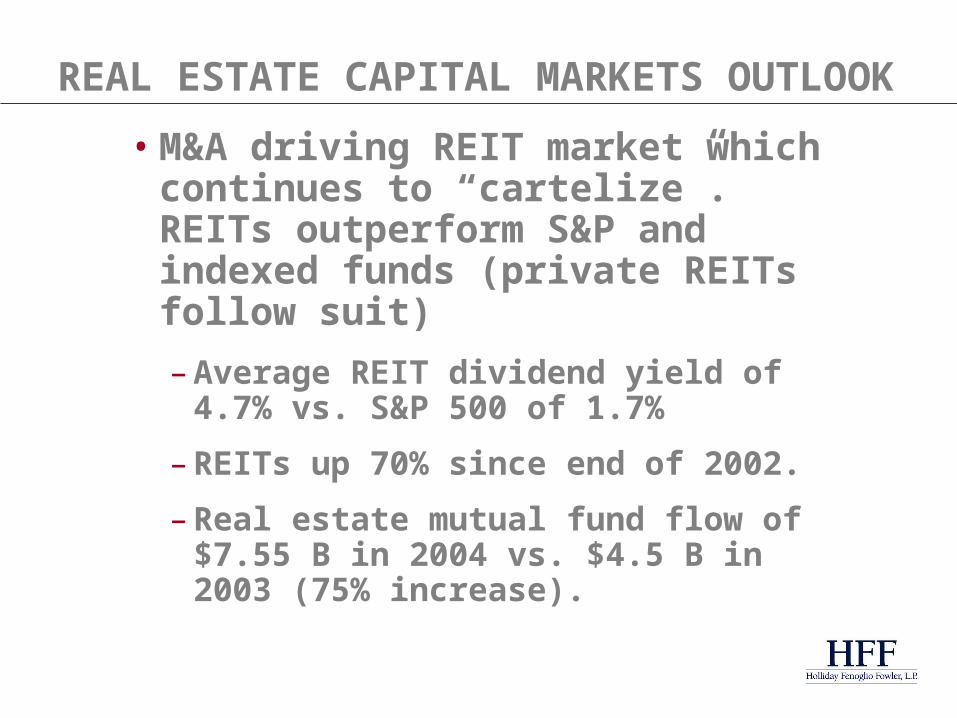

• M&A driving REIT market which continues to “cartelize”. REITs outperform S&P and indexed funds (private REITs follow suit)

– Average REIT dividend yield of 4.7% vs. S&P 500 of 1.7%

– REITs up 70% since end of 2002.

– Real estate mutual fund flow of $7.55 B in 2004 vs. $4.5 B in 2003 (75% increase).

REAL ESTATE CAPITAL MARKETS OUTLOOK

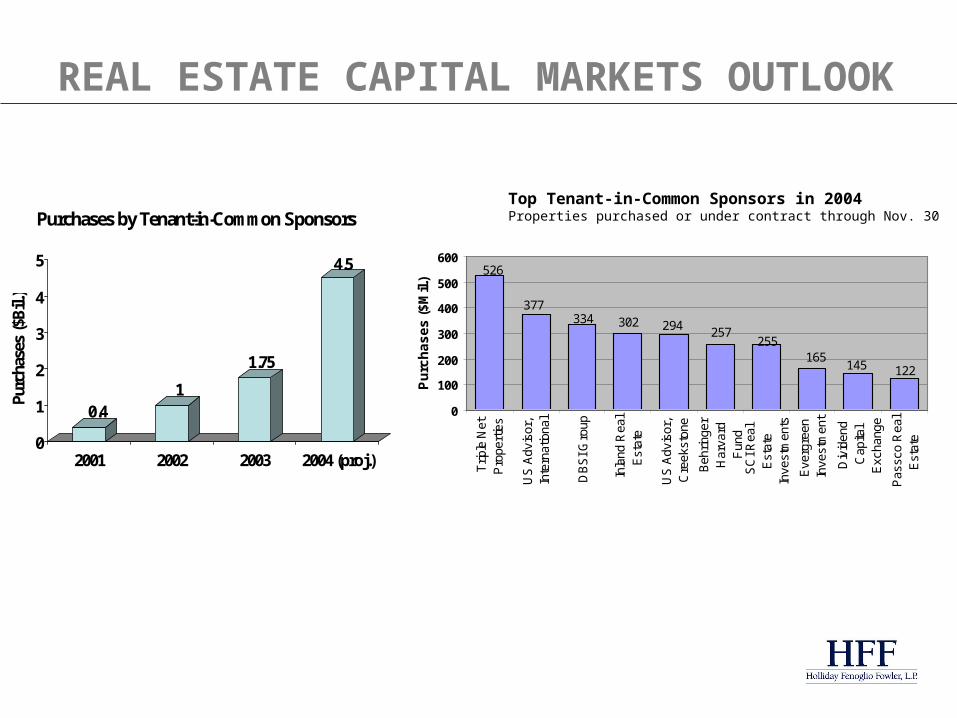

0.41

1.75

4.5

0

1

2

3

4

5

Purc

hase

s ($

Bil.

)

2001 2002 2003 2004 (proj.)

Purchases by Tenant-in-Common Sponsors

526

377334 302 294 257

255165

145 122

0

100

200

300

400

500

600

Trip

le N

etP

rope

rtie

s

US

Adv

isor

,In

tern

atio

nal

DB

SI G

roup

Inla

nd R

eal

Est

ate

US

Adv

isor

,C

reek

ston

e

Beh

ringe

rH

arva

rdF

und

SC

I Rea

lE

stat

eIn

vest

men

ts

Eve

rgre

enIn

vest

men

t

Div

iden

dC

apita

lE

xcha

nge

Pas

sco

Rea

lE

stat

e

Pu

rch

as

es

($

Mil.

)

Top Tenant-in-Common Sponsors in 2004Properties purchased or under contract through Nov. 30

REAL ESTATE CAPITAL MARKETS OUTLOOK

• TIC TAC DOUGH and Fund of Funds = New Drivers

• Improving Fundamentals Too

REAL ESTATE CAPITAL MARKETS OUTLOOK

Pricing• “Stagress” – Stagnant real job

growth (part-time vs. core) yet real economic progress holds down rates. – Oil price increase lags 12-15 months.

REAL ESTATE CAPITAL MARKETS OUTLOOK

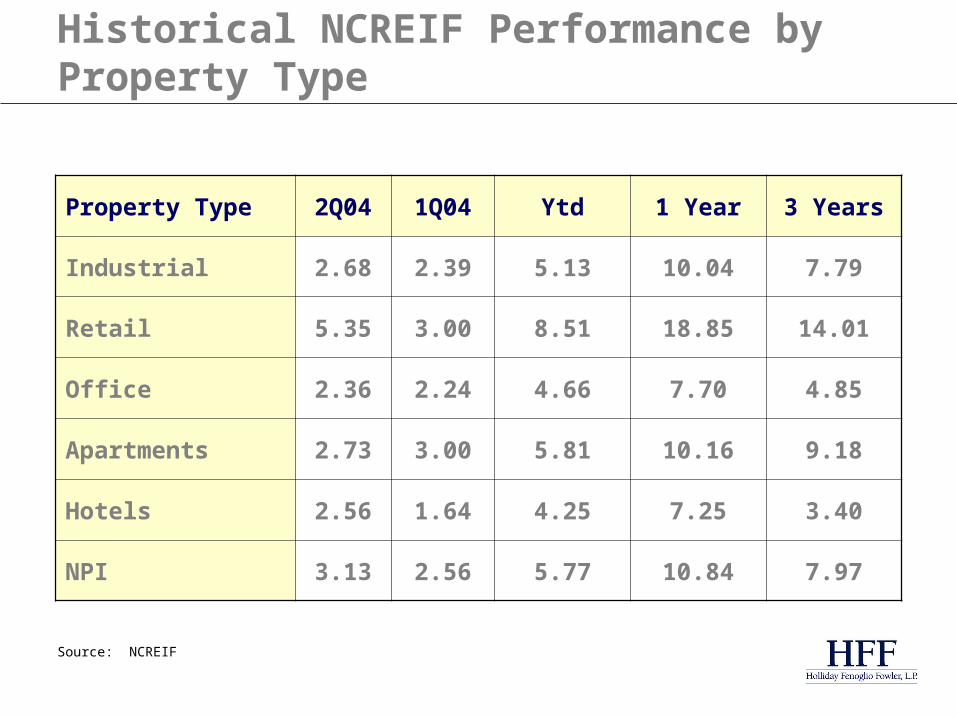

Property Type 2Q04 1Q04 Ytd 1 Year 3 Years

Industrial 2.68 2.39 5.13 10.04 7.79

Retail 5.35 3.00 8.51 18.85 14.01

Office 2.36 2.24 4.66 7.70 4.85

Apartments 2.73 3.00 5.81 10.16 9.18

Hotels 2.56 1.64 4.25 7.25 3.40

NPI 3.13 2.56 5.77 10.84 7.97

Historical NCREIF Performance by Property Type

Source: NCREIF

• Heyday for “infill” and “edge city” locations.

• Fortress mall cap rates fall to lows near 5%. (back to mid 1980s)

• Power centers command premium (all cash IRR of 7.0-7.5, flat returns) for income stability and lease term.

Food GroupsREAL ESTATE CAPITAL MARKETS OUTLOOK

Retail TrendsMajor Retail Segments

Cap Rate* Compression 2001-2005(Median Capitalization Rates)

8.8%

11.0%

10.0%10.5%

10.0%

9.0%

6.50%

5.5%6.0%

8.5%8.0%

7.25%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

FortressMall

SecondaryMall

PowerCenter

LifestyleCenter

CommunityCenter

NeighborhoodCenter

2001

2005

• Secondary office market sales activity bringing new liquidity to this large segment.

• Large industrial properties are oversubscribed and trade at trophy premium.

• Multifamily, despite economic vacancy, still command pricing power.

Food GroupsREAL ESTATE CAPITAL MARKETS OUTLOOK

• Development sites with entitlements “red hot” as entrepreneurs often with institutional capital, seek higher returns.– Condo conversion mania

• Net lease purchasing at historic highs driven by RELPs, syndicated equity and 1031 exchange capital.

Food GroupsREAL ESTATE CAPITAL MARKETS OUTLOOK

• Land Spec: Fast Growing and Institutionally Driven (JPMF in Inland Empire)

• Note Sales, “Loan To Own”, Partner Recaps: Any Opportunity, Stupid!

Food GroupsREAL ESTATE CAPITAL MARKETS OUTLOOK

• Recognition of True Reproduction Costs and Valuation

• Global acquisitions/M&A

– Mills/Scotland malls

– GEPT Canada

– Blackstone model/precedent

– Galileo/New Plan

– Simon/China JVs

Next

REAL ESTATE CAPITAL MARKETS OUTLOOK

• Foreign capital surge (esp. Debt)

• New Megabank Equity

– Direct /Co-Invest

*Citicorp

• Fractionalization

• Mutual Fund R.E. (evolution from private syndicates; 401K)

Next

REAL ESTATE CAPITAL MARKETS OUTLOOK

• Blowoffs: – Rates above 5.5% and LIBOR spike

*Business Week Survey of Corporate/Wall Street Experts = 5.1% T-10 Consensus

–Condo conversion, presales at Stabilized Value

–Master leases

Next

REAL ESTATE CAPITAL MARKETS OUTLOOK

Related Documents