INSIDE THIS ISSUE DEBT LINE CALIFORNIA DEBT AND INVESTMENT ADVISORY COMMISSION BILL LOCKYER, CHAIRMAN 915 CAPITOL MALL, ROOM 400 SACRAMENTO, CA 95814 (916) 653-3269 WWW.TREASURER.CA.GOV/CDIAC A SOURCE OF CALIFORNIA DEBT AND INVESTMENT INFORMATION Not All Budget Deficits Are the Same 1 CDIAC Commission Meeting 2 Local BABs Activity for 2009 3 Mello-Roos and Mark-Roos Issuers: Local Agencies Must Report Defaults and Draws on Reserves 3 Upcoming CDIAC Seminars 4 Calendar of Issues 8 Vol. 29, No. 5, MAY 2010 Not All Budget Deficits Are the Same John Decker, Executive Director Barbara Tanaka, Deputy Executive Director Angelica Hernandez, Manager, Administration, Data and Education Units Not all deficits result from chronic fiscal conditions. A temporary budget deficit can open up from a “shock” to the state’s fiscal structure. Typically, this “shock” will be in the form of a temporary economic downturn. When this happens, General Fund revenues fall below the expected full-employment level. If the budget were narrowly balanced prior to the recession, expenditures might exceed revenues during a downturn – thereby cre- ating a deficit. See Figure 1. Figure 1 shows the effect on the budget balance resulting purely from an economic downturn. At full employment, revenues (displayed in the blue line) are above expen- ditures for the entire ten-year period. As- suming an economic slowdown in years 3 through 6, revenues fall below expenditures in years 3, 4, 5, and 6. By year 7, revenues return to the full-employment line when the economy recovers. e budget is un- balanced for a four year period during the economic downturn, but the effects on the budget are temporary. Cyclical downturns suppress revenues for two to five years. For example, the aerospace downturn that hit California in 1990 lasted until about 1993 or 1994. By 1995, state revenues had returned to their pre-1990 trendline (even after accounting for the tax increases approved in 1991.) (eoretically, a deficit could open up because expenditures unexpectedly rise. ough theoretically possible, this is not typical for California. Even after natural disasters, state General Fund costs do not rise so precipitously as to create major temporary deficits. Most temporary defi- cits are the result of the revenue effects of the business cycle.) e distinction between chronic and tem- porary deficits is not idle. If the budget deficit is chronic, the legislature may prefer to employ different budget-balancing solu- tions than it would use to address a three- year recession-driven deficit. FIGURE 1 COMPARISON OF EXPENDITURES AND REVENUES ASSUMING WITH FULL EMPLOYMENT AND WITH DOWNTURN (DOWNTURN IN YEARS 3 THROUGH 6) 1 2 3 4 5 6 7 8 9 10 $220 $190 $160 $130 $100 REVENUES (FULL EMPLOYMENT) EXPENDITURES REVENUES (DOWNTURN) Budget Deficits, page 2

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INS IDE TH IS ISSUE

D E B T L I N E

CALIFORNIA DEBT AND INVESTMENT ADVISORY COMMISSION BILL LOCKYER, CHAIRMAN915 CAPITOL MALL, ROOM 400 SACRAMENTO, CA 95814 (916) 653-3269 WWW.TREASURER.CA.GOV/CDIAC

A SOURCE OF CALIFORNIA DEBT AND INVESTMENT INFORMATION

Not All Budget Deficits Are the Same 1

CDIAC Commission Meeting 2

Local BABs Activity for 2009 3

Mello-Roos and Mark-Roos Issuers: Local Agencies Must Report Defaults and Draws on Reserves 3

Upcoming CDIAC Seminars 4

Calendar of Issues 8

Vol. 29, No. 5, MAY 2010

Not All Budget Deficits Are the SameJohn Decker, Executive Director

Barbara Tanaka, Deputy Executive Director

Angelica Hernandez, Manager, Administration, Data and Education Units

Not all deficits result from chronic fiscal conditions.

A temporary budget deficit can open up from a “shock” to the state’s fiscal structure. Typically, this “shock” will be in the form of a temporary economic downturn. When this happens, General Fund revenues fall below the expected full-employment level. If the budget were narrowly balanced prior to the recession, expenditures might exceed

revenues during a downturn – thereby cre-ating a deficit. See Figure 1.

Figure 1 shows the effect on the budget balance resulting purely from an economic downturn. At full employment, revenues (displayed in the blue line) are above expen-ditures for the entire ten-year period. As-suming an economic slowdown in years 3 through 6, revenues fall below expenditures in years 3, 4, 5, and 6. By year 7, revenues return to the full-employment line when the economy recovers. The budget is un-balanced for a four year period during the economic downturn, but the effects on the budget are temporary.

Cyclical downturns suppress revenues for two to five years. For example, the aerospace downturn that hit California in 1990 lasted until about 1993 or 1994. By 1995, state revenues had returned to their pre-1990

trendline (even after accounting for the tax increases approved in 1991.)

(Theoretically, a deficit could open up because expenditures unexpectedly rise. Though theoretically possible, this is not typical for California. Even after natural disasters, state General Fund costs do not rise so precipitously as to create major temporary deficits. Most temporary defi-cits are the result of the revenue effects of the business cycle.)

The distinction between chronic and tem-porary deficits is not idle. If the budget deficit is chronic, the legislature may prefer to employ different budget-balancing solu-tions than it would use to address a three-year recession-driven deficit.

FIGURE 1COMPARISON OF EXPENDITURES AND REVENUES ASSUMING WITH FULL EMPLOYMENT AND WITH DOWNTURN (DOWNTURN IN YEARS 3 THROUGH 6)

1 2 3 4 5 6 7 8 9 10

$220

$190

$160

$130

$100

REVENUES (FULL EMPLOYMENT)

EXPENDITURES

REVENUES (DOWNTURN)

Budget Deficits, page 2

2 DEBT LINE

Chairman:BILL LOCKYERCalifornia State Treasurer

Members:ARNOLD SCHWARZENEGGERGovernor

JOHN CHIANGState Controller

DAVE COXState Senator

CAROL LIUState Senator

ANNA CABALLEROAssemblymember

TED LIEUAssemblymember

JOSÉ CISNEROSTreasurer and Tax Collector City and County of San Francisco

JAY GOLDSTONEChief Operating Officer City of San Diego

Executive Director:JOHN DECKER

Debt Line is published monthly by the Califor-nia Debt and Investment Advisory Commission (CDIAC).

915 Capitol Mall, Room 400 Sacramento, CA 95814 P (916) 653-3269 F (916) 654-7440 [email protected] www.treasurer.ca.gov/cdiac

Debt Line publishes articles on debt financing and public fund investment that may be of in-terest to our readers; however, these articles do not necessarily reflect the views of the Commission.

Business correspondence and editorial com-ments are welcome.

All rights reserved. No part of this document may be reproduced without written credit giv-en to CDIAC. Permission to reprint with written credit given to CDIAC is hereby granted.

Budget Deficits, from page 1

“STRUCTURAL” VS. “ECONOMIC” DEFICITS. Public finance distinguishes be-tween a structural and an economic deficit.

A “structural” deficit arises when the budget is imbalanced even when the economy is running at “full employment.” In 2007, the State Treasurer made a long-term estimate of California’s General Fund budget, to de-termine if the state faced a “structural” im-balance. Staff calculated (a) General Fund revenues for a 20-year period, assuming the tax structure in place on January 1, 2007 and assuming a full-employment economy for the entire period, and (b) General Fund expenditures for the same period assuming spending patterns did not change from the 2007-08 budget. At that time, he estimat-ed that General Fund expenditures would exceed available resources by between 3.0 percent and 4.0 percent in each year begin-ning in about 2012. Because he assumed a full-employment economy, the 2007 Debt

Affordability Report labeled this chronic deficit a “structural” imbalance.

Since then, the economy has fallen off and revenues have fallen far below what staff assumed in their 2007 estimates. General Fund deficits have increased.

If you believe that the state’s economy will recover and revenues will return to the levels assumed by staff in the 2007 affordability re-port, then you would not apply permanent fiscal changes to fill the “economic” deficit. You would adopt temporary changes to rev-enues and expenditures to fill the difference.

If, however, you believe that the recession will permanently reduce revenues below what we assumed in 2007, then you would argue that the recession is creating a deeper “structural” deficit that requires permanent changes in spending or revenues.

A difficulty in budgeting during this period is cultivating how much of the state and General Fund deficit is “structural” and how much is “economic.” DL

CDIAC Commission Meeting

The California Debt and Investment Ad-visory Commission (CDIAC) will hold a public commission meeting on Monday, June 14, 2010, at 1:30 pm at the Jesse M. Unruh State Office Building, 915 Capitol Mall, Room 587, Sacramento, California. An agenda for this meeting will be post-

ed on CDIAC’s website (www.treasurer.

ca.gov/cdiac) and at its office at least ten days prior to the meeting. Questions regard-ing the meeting may be directed to CDIAC by calling (916) 653-3269 or by email to [email protected]. DL

3MAY 2010

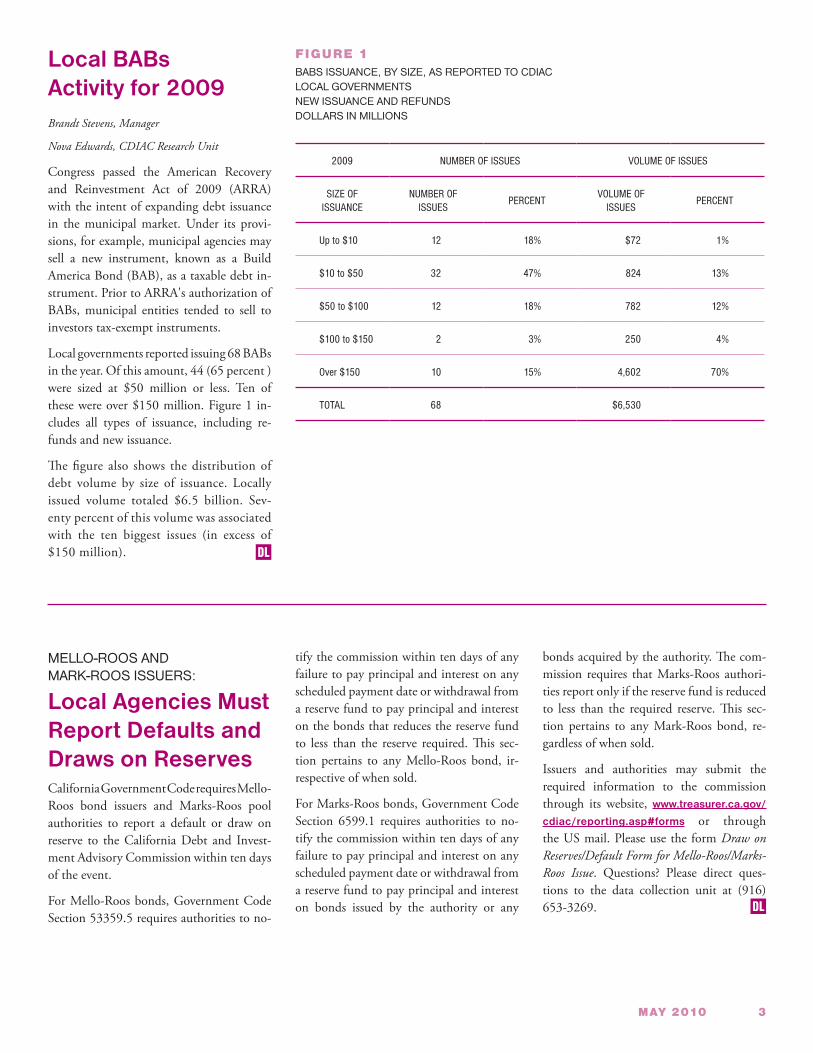

Local BABs Activity for 2009Brandt Stevens, Manager

Nova Edwards, CDIAC Research Unit

Congress passed the American Recovery and Reinvestment Act of 2009 (ARRA) with the intent of expanding debt issuance in the municipal market. Under its provi-sions, for example, municipal agencies may sell a new instrument, known as a Build America Bond (BAB), as a taxable debt in-strument. Prior to ARRA's authorization of BABs, municipal entities tended to sell to investors tax-exempt instruments.

Local governments reported issuing 68 BABs in the year. Of this amount, 44 (65 percent ) were sized at $50 million or less. Ten of these were over $150 million. Figure 1 in-cludes all types of issuance, including re-funds and new issuance.

The figure also shows the distribution of debt volume by size of issuance. Locally issued volume totaled $6.5 billion. Sev-enty percent of this volume was associated with the ten biggest issues (in excess of $150 million).

FIGURE 1BABS ISSUANCE, BY SIZE, AS REPORTED TO CDIAC LOCAL GOVERNMENTS NEW ISSUANCE AND REFUNDS DOLLARS IN MILLIONS

2009 NUMBER OF ISSUES VOLUME OF ISSUES

SIZE OF ISSUANCE

NUMBER OF ISSUES

PERCENTVOLUME OF

ISSUESPERCENT

Up to $10 12 18% $72 1%

$10 to $50 32 47% 824 13%

$50 to $100 12 18% 782 12%

$100 to $150 2 3% 250 4%

Over $150 10 15% 4,602 70%

TOTAL 68 $6,530

MELLO-ROOS AND MARK-ROOS ISSUERS:

Local Agencies Must Report Defaults and Draws on ReservesCalifornia Government Code requires Mello- Roos bond issuers and Marks-Roos pool authorities to report a default or draw on reserve to the California Debt and Invest-ment Advisory Commission within ten days of the event.

For Mello-Roos bonds, Government Code Section 53359.5 requires authorities to no-

tify the commission within ten days of any failure to pay principal and interest on any scheduled payment date or withdrawal from a reserve fund to pay principal and interest on the bonds that reduces the reserve fund to less than the reserve required. This sec-tion pertains to any Mello-Roos bond, ir-respective of when sold.

For Marks-Roos bonds, Government Code Section 6599.1 requires authorities to no-tify the commission within ten days of any failure to pay principal and interest on any scheduled payment date or withdrawal from a reserve fund to pay principal and interest on bonds issued by the authority or any

bonds acquired by the authority. The com-mission requires that Marks-Roos authori-ties report only if the reserve fund is reduced to less than the required reserve. This sec-tion pertains to any Mark-Roos bond, re-gardless of when sold.

Issuers and authorities may submit the required information to the commission through its website, www.treasurer.ca.gov/

cdiac/reporting.asp#forms or through the US mail. Please use the form Draw onReserves/Default Form for Mello-Roos/Marks-Roos Issue. Questions? Please direct ques-tions to the data collection unit at (916) 653-3269. DL

DL

4 DEBT LINE

Upcoming CDIAC Seminars

ated with investing in interim instruments. Part 2 is an introduction to municipal in-vestment. Running for one and one-half days, the seminar covers investment con-cepts, options and performance measure-ments. This seminar is the first in a two-part series on investments. Participants receive a copy of the commission’s investment guide-lines, a desktop reference for complying with California’s statutory laws.

DEBT SEMINAR 2: FROM INDENTURE DOCUMENTS TO SALE

February 3-4, 2011 Oakland Marriott Oakland, California

Speakers outline steps for evaluating debt capacity and establishing a debt manage-ment policy. The course discusses how to develop the bond documents. Panels ad-dress managing fund accounts, investing bond proceeds and administering the debt over the term of the instrument. This is the second of a three-course series on introduc-tory management, but participants can take classes in any sequence.

DEBT SEMINAR 3: ON-GOING DEBT ADMINISTRATION

April 8, 2011 CSU Pomona Kellogg Center Pomona, California

You’ve issued your debt—now what? This course describes the steps for managing debt over the next few decades. Speakers discuss the indenture documents and con-tinuing disclosure requirements associated with out-year administration. They describe the steps for managing bond proceeds, ar-bitrage and reserve accounts. Panels cover evaluating refunding options and managing

variable rate debt. This seminar is the last in a three-part series of seminars on debt issu-ance. Seminars in the series can be taken in any sequence.

IN THE KNOW ABOUT SCHOOL DEBT FINANCING

April 29, 2011 CSU Pomona Kellogg Center Pomona, California

This seminar is tailored to school offi-cials seeking an understanding of debt fi-nance—from planning the debt program to on-going administration and regula-tory compliance. The speakers present fis-cal management concepts, considerations before issuing debt, statutory requirements and out-year debt management strategies.

LAND-SECURED FINANCE: MELLO-ROOS DISTRICT AND ASSESSMENT DISTRICT FINANCING

March 18, 2011 Hotel Shattuck Berkeley, California

This seminar focuses on financing capital through special districts (Mello-Roos and assessment). Under what circumstances are these districts appropriate for your needs? How does a local agency form a district? How does the district issue debt and ad-minister the liens? Hear expert advice on how to comply with federal regulations and state law.

DEBT SEMINAR 1: FUNDAMENTALS OF DEBT FINANCING

September 23-24, 2010 Sheraton Park Anaheim, California

Experts explain concepts of structuring, marketing and pricing the deal, the rela-tionships between principal, interest, price and proceeds. Speakers address ways to evaluate types of interim and long-term municipal finance instruments. They dis-cuss how to use private expertise and how industry professionals can reduce costs. The seminar concludes with a discussion of is-suer responsibilities for initial and continu-ing disclosure. This seminar is the first of a three-part introductory debt issuance series.

DISCLOSURE IN MUNICIPAL SECURITIES

October 8, 2010 Renaissance Long Beach Long Beach, California

Proper and timely disclosure helps ensure access to the municipal finance market. Un-der what circumstances do issuers “talk to the market”? When they do, what are the federal disclosure rules? Speakers discuss the regulatory requirements for initial and con-tinuing disclosure. They also advise on ways to avoid common mistakes.

INVESTMENT SEMINAR 1: INTERIM FINANCING AND INVESTMENT BASICS

October 21-22, 2010 Concord Hilton Concord, California

This seminar has two distinct parts. Part 1, running for half a day, covers issues associ-

DL

CALIFORNIA DEBT AND INVESTMENT ADVISORY COMMISSION PRESENTS

DEBT SEMINAR 1: FUNDAMENTALS OF DEBT FINANCINGAN INTRODUCTION TO DEBT FINANCE

NAME TITLE

AGENCY

STREET ADDRESS

CITY STATE ZIP

PHONE FAX

ATTENDEE EMAIL

Please check here if you do not want CDIAC to use this email address for future seminar-related emails. CDIAC does not make its list available to other entities.

SEPTEMBER 23 -24 , 2010 | SHERATON PARK | ANAHE IM , C AL I F ORN IA

•Consideringwhethertoissuedebt?•Whatareyouroptionsforshort-andlong-

terminstruments?•Howcanprivateindustryprofessionalshelp

youreducecosts?•Howhaverecentmarketchangesaffected

yourabilitytoplacedebt?•Whatshouldyouknowaboutfederal

regulations?

Expertspeakersdiscusstheresponsibilitiesofbondcounsel,under-writers, trusteesand financialadvisors.Theydescribeandevaluatetypesof short- and long-term instruments available to your govern-ment.Apaneldetailshowtomarketandpriceanissue.Theseminarconcludeswithadiscussionofhowanissuercanmeetfederaldisclo-surerequirements.

CDIACstafffacilitatetheseminarsessions.Panelsfeaturelocalagen-cyofficialsandprivatesectorpractitioners.

COST (includesmealsandseminarmaterials):

$350(PublicSectorRepresentatives) $500(PrivateSectorRepresentatives)

REGISTRATION DEADLINE:

August10,2010oruntilfilled.Enrollmentislimited.Thisisoneof CDIAC’smostpopularseminars,sopleaseregisterpromptly.

TO REGISTER BY CREDIT CARD (VisaorMasterCard):

1. Gotowww.treasurer.ca.gov/cdiac/seminars.asp

2. Choosetheseminarandclick“RegisterOnline.”Thelinkdirectsyoutoasecurewebsite.Ifyouhavedifficultieswiththeweb-site,pleasecallReneeCashmereat(916)653-5318.

TO REGISTER BY CHECK:

1. Fillouttheattachedenrollmentform.Oneformisrequiredforeachparticipant.

2. Makethecheckpayableto: California Debt and Investment Advisory Commission.

3. Mailformandcheckto: SeminarPrograms,CDIAC 915CapitolMall,Room400, Sacramento,California95814.

For more information on this or other CDIAC seminars, pleasecheck the commission’s website, www.treasurer.ca.gov/cdiac orcall(916)653-3269.

CALIFORNIA DEBT AND INVESTMENT ADVISORY COMMISSION PRESENTS DISCLOSURE IN MUNICIPAL SECURITIES

WHAT YOU DON’T KNOW CAN HURT YOU

NAME TITLE

AGENCY

STREET ADDRESS

CITY STATE ZIP

PHONE FAX

ATTENDEE EMAIL

Please check here if you do not want CDIAC to use this email address for future seminar-related emails. CDIAC does not make its list available to other entities.

OCTOBER 8, 2010 | RENAISSANCE LONG BEACH | LONG BEACH, CALIFORNIA

•Isfederalregulatoryoversightchangingandmorestringent?

•Howshouldmyagencyrespond?

•Whataremyagency’sresponsibilitiesformeetingfederalrequirements?

•Towhatextentcanindividualsbeliableforregulatorysanctions?

Failuretocomplywithfederaldisclosureregulationscanhavecata-strophicconsequencesforindividualsandmunicipalities.Inthissemi-nar, expert speakers discuss the regulatory requirements for initialandcontinuingdisclosure.Theydiscusshowtomeetthecurrentfed-eralstandardsandcommonmistakesmadebystateandlocalagen-cies.Speakersdescribewhatinvestorsandthefinancialcommunityexpectfromlocalagencies.

CDIACstafffacilitatetheseminarsessions.Panelsfeaturelocalagen-cyofficialsandprivatesectorpractitioners.

COST:

$250(includesmealsandseminarmaterials)Open to public sector representatives only.

REGISTRATION DEADLINE:

September10,2010oruntilfilled.

TO REGISTER BY CREDIT CARD (VisaorMasterCard):

1. Gotowww.treasurer.ca.gov/cdiac/seminars.asp

2. Choosetheseminarandclick“RegisterOnline.”Thelinkdirectsyoutoasecurewebsite.Ifyouhavedifficultieswiththeweb-site,pleasecallReneeCashmereat(916)653-5318.

TO REGISTER BY CHECK:

1. Fillouttheattachedenrollmentform.Oneformisrequiredforeachparticipant.

2. Makethecheckpayableto: California Debt and Investment Advisory Commission.

3. Mailformandcheckto: SeminarPrograms,CDIAC 915CapitolMall,Room400, Sacramento,California95814.

For more information on this or other CDIAC seminars, pleasecheck the commission’s website, www.treasurer.ca.gov/cdiac orcall(916)653-3269.

CALIFORNIA DEBT AND INVESTMENT ADVISORY COMMISSION PRESENTS INVESTMENT SEMINAR 1:INTERIM FINANCING AND INVESTMENT BASICS

NAME TITLE

AGENCY

STREET ADDRESS

CITY STATE ZIP

PHONE FAX

ATTENDEE EMAIL

Part 1: Interim Financing Part 2: Investment Basics Both Parts Please check here if you do not want CDIAC to use this email address for future seminar-related emails. CDIAC does not make its list available to other entities.

OCTOBER 21-22, 2010 | CONCORD HILTON | CONCORD, CALIFORNIA

•Withcashflowissuesaffectingbudgetdiscussions,whatshouldyouknowaboutshort-termborrowing?

•Whatarethebasictermsandprocedures youshouldmasterformanagingyourinvestmentportfolio?

Thisseminarhastwodistinctparts.Part1,runningforhalfaday,covers issuesassociatedwith investing in interim(alsoknownas“short term”) instruments. Part 2 is an introduction to municipalinvestment.Runningforoneandone-halfdays,theseminarcoversinvestmentconcepts,optionsandperformancemeasurements.Thisseminaristhefirstinatwo-partseriesoninvestments.Participantsreceiveacopyofthecommission’sinvestmentguidelines,adesk-topreferenceforcomplyingwithCalifornia’sstatutorylaws.

CDIACstafffacilitatetheseminarsessions.Panelsfeaturelocalagen-cyofficialsandprivatesectorpractitioners.

COST (includesmealsandseminarmaterials):

$150forPart1(InterimFinancing) $300forPart2(InvestmentBasics) $400forbothparts Open to public sector representatives only.

REGISTRATION DEADLINE:

September23,2010oruntilfilled.Enrollmentisextremelylimitedforthisseminar,sopleaseregisterpromptly.

TOREGISTERBYCREDITCARD(VisaorMasterCard):

1. Gotowww.treasurer.ca.gov/cdiac/seminars.asp

2. Choosetheseminarandclick“RegisterOnline.”Thelinkdirectsyoutoasecurewebsite.Ifyouhavedifficultieswiththeweb-site,pleasecallReneeCashmereat(916)653-5318.

TO REGISTER BY CHECK:

1. Fillouttheattachedenrollmentform.Oneformisrequiredforeachparticipant.

2. Makethecheckpayableto: California Debt and Investment Advisory Commission.

3. Mailformandcheckto: SeminarPrograms,CDIAC 915CapitolMall,Room400, Sacramento,California95814.

For more information on this or other CDIAC seminars, pleasecheck the commission’s website, www.treasurer.ca.gov/cdiac or call(916)653-3269.

8D

EB

T L

INE

DEBT LINE CALENDAR LEGEND

CALIFORNIA

DEBT AND

INVESTMENT

ADVISORY

COMMISSION

CALENDAR AS OF APRIL 15, 2010

This calendar is based on information reported to the California Debt and Investment Advisory Commission on the Report of Proposed Debt Issuance and the Report of Final Sale or from sources considered reliable. Errors or omissions in the amount of a sale or financing participants will be corrected in a following issue. Cancelled issues are not listed in the calendar. The status of any

issue may be obtained by calling the Commission.

# Issue is newly reported in DEBT LINE. All other issues have been carried forward from previous calendars. + Issue has been republished to correct errata or list additional information. Additional or corrected items are underlined.

TYPE OF SALE/DATE OF SALE RATING AGENCIES CREDIT ENHANCEMENTComp Competitive S Standard & Poor's LOC Letter(s) of Credit (The date of the bid opening) M Moody's Investors Service Ins Bond Insurance Neg Negotiated or private placement F Fitch IBCA Oth Other third party enhancement (The date of the signing of the bond purchase agreement) NR Not rated SIP State Intercept

TAX STATUS REFUNDING PARTICIPANTSTaxable Interest is subject to federal and State taxation Issue is partially or fully for refunding. BC Bond Counsel Federally Taxable Interest is subject to federal taxation FA Financial Advisor State Taxable Interest is subject to State taxation UW Underwriter Subject to AMT Interest on this issue is a specific MATURITY TYPE(S) TR Trustee

preference item for the purpose of Serial Serial bonds EN Guarantor computing the federal alternative minimum tax. Term Term bond

Comb Serial and term bond, several term bonds or other types of structured financings

INTEREST COSTNIC Net Interest Cost The Interest Cost represents either the winning competitive NIC/TIC TIC True Interest Cost bid or the interest cost financing. The Net Interest Cost is calculated Var Rate pegged to an index by using the total scheduled interest payments plus the underwriter’s discount or minus the premium, divided by bond year dollars. Qualified Zone Academy Bonds (QZAB) carry little or no interest costs

SELECTED REPORTING REQUIREMENTS

Under existing law (California Government Code Section 8855(k)), "The issuer of any proposed new debt issue of State or local government (or public benefit corporation incorporated for the purpose of acquiring student loans) shall, not later than 30 days prior to the sale of any debt issue at public or private sale, give written notice of the proposed sale to the Commission, by mail, postage prepaid."

Under California Government Code Section 8855(l), "The issuer of any new debt issue of State or local government (or public benefit corporation for the purpose of acquiring student loans) shall, not later than 45 days after the signing of the bond purchase contract in a negotiated or private financing, or after the acceptance of a bid in a competitive offering, submit a report of final sale to the commission by mail, postage prepaid, or by any other method approved by the commission. A copy of the official statement for the issue shall accompany the report of final sale. The Commission may require information to be submitted in the report of final sale that is considered appropriate."

Under California Government Code Section 53583(c)(2)(B) if a "local agency determines to sell the (refunding) bonds at private sale or on a negotiated sale basis, the local agency shall send a written statement, within two weeks after the bonds are sold, to the California Debt and Investment Advisory Commission explaining the reasons why the local agency determined to sell the bonds at private sale or on a negotiated sale basis instead of at public sale."

9M

AY

20

10

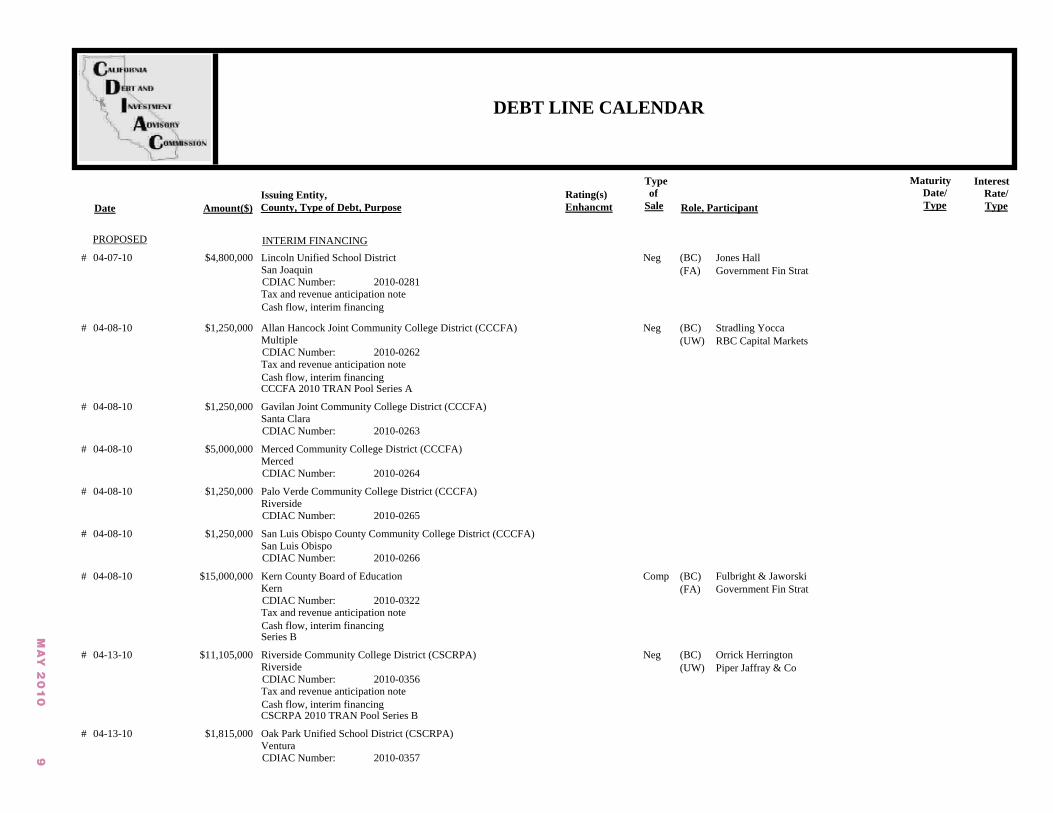

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

INTERIM FINANCING04-07-10

04-08-10

04-08-10

04-08-10

04-08-10

04-08-10

04-08-10

04-13-10

04-13-10

$4,800,000

$1,250,000

$1,250,000

$5,000,000

$1,250,000

$1,250,000

$15,000,000

$11,105,000

$1,815,000

Lincoln Unified School District

Allan Hancock Joint Community College District (CCCFA)

Gavilan Joint Community College District (CCCFA)

Merced Community College District (CCCFA)

Palo Verde Community College District (CCCFA)

San Luis Obispo County Community College District (CCCFA)

Kern County Board of Education

Riverside Community College District (CSCRPA)

Oak Park Unified School District (CSCRPA)

San Joaquin

Multiple

Santa Clara

Merced

Riverside

San Luis Obispo

Kern

Riverside

Ventura

2010-0281

2010-0262

2010-0263

2010-0264

2010-0265

2010-0266

2010-0322

2010-0356

2010-0357

CCCFA 2010 TRAN Pool Series A

Series B

CSCRPA 2010 TRAN Pool Series B

Tax and revenue anticipation note

Tax and revenue anticipation note

Tax and revenue anticipation note

Tax and revenue anticipation note

Neg

Neg

Comp

Neg

(BC)(FA)

(BC)(UW)

(BC)(FA)

(BC)(UW)

Jones HallGovernment Fin Strat

Stradling YoccaRBC Capital Markets

Fulbright & JaworskiGovernment Fin Strat

Orrick HerringtonPiper Jaffray & Co

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

#

#

#

#

PROPOSED

Cash flow, interim financing

Cash flow, interim financing

Cash flow, interim financing

Cash flow, interim financing

10

DE

BT

LIN

E

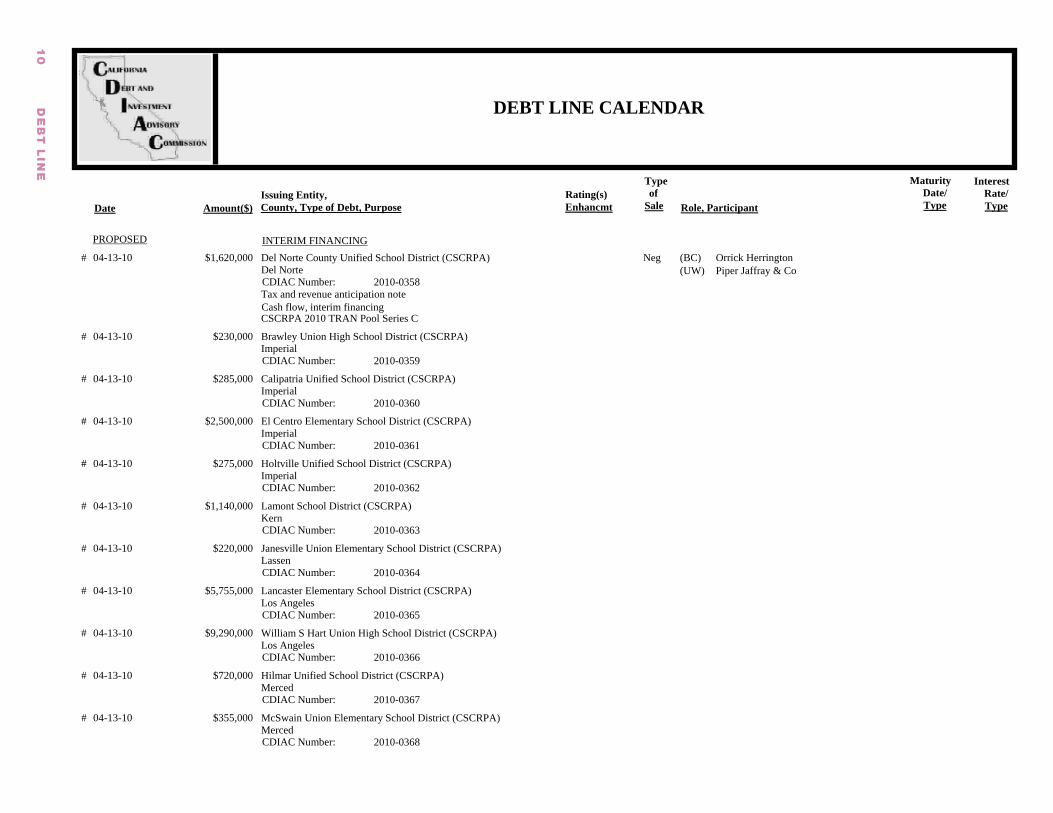

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

INTERIM FINANCING04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

$1,620,000

$230,000

$285,000

$2,500,000

$275,000

$1,140,000

$220,000

$5,755,000

$9,290,000

$720,000

$355,000

Del Norte County Unified School District (CSCRPA)

Brawley Union High School District (CSCRPA)

Calipatria Unified School District (CSCRPA)

El Centro Elementary School District (CSCRPA)

Holtville Unified School District (CSCRPA)

Lamont School District (CSCRPA)

Janesville Union Elementary School District (CSCRPA)

Lancaster Elementary School District (CSCRPA)

William S Hart Union High School District (CSCRPA)

Hilmar Unified School District (CSCRPA)

McSwain Union Elementary School District (CSCRPA)

Del Norte

Imperial

Imperial

Imperial

Imperial

Kern

Lassen

Los Angeles

Los Angeles

Merced

Merced

2010-0358

2010-0359

2010-0360

2010-0361

2010-0362

2010-0363

2010-0364

2010-0365

2010-0366

2010-0367

2010-0368

CSCRPA 2010 TRAN Pool Series C

Tax and revenue anticipation note

Neg (BC)(UW)

Orrick HerringtonPiper Jaffray & Co

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

#

#

#

#

#

#

PROPOSED

Cash flow, interim financing

11

MA

Y 2

01

0

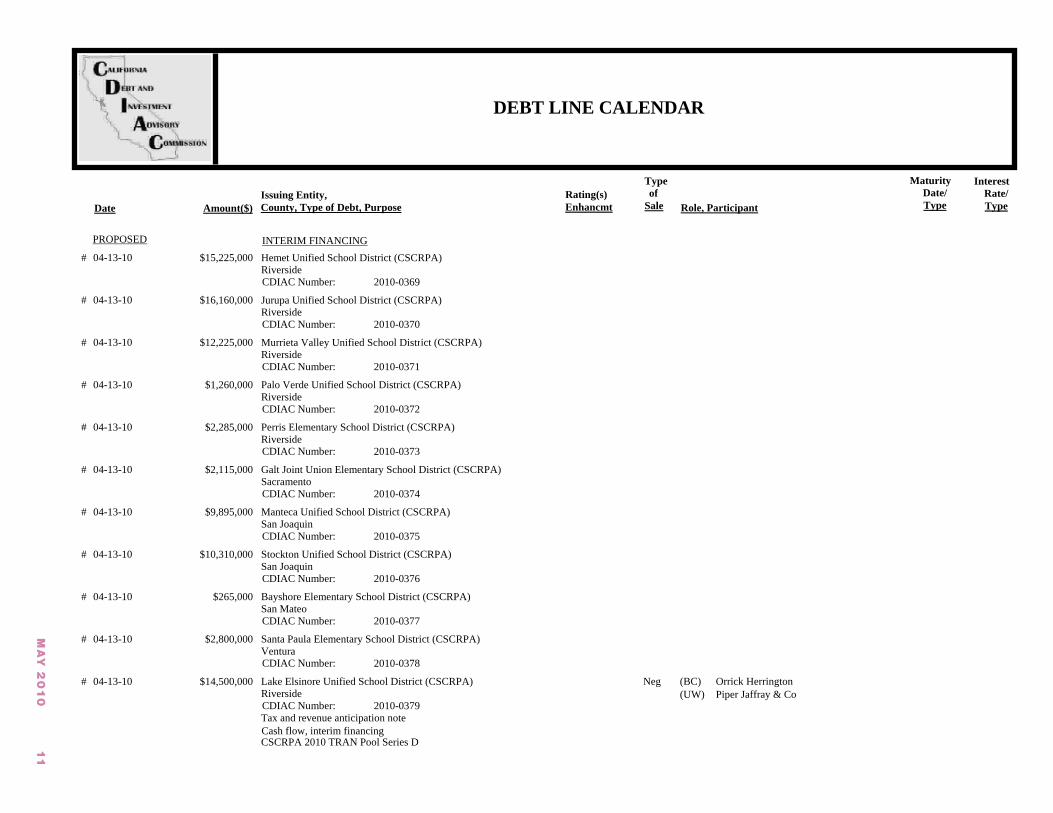

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

INTERIM FINANCING04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

$15,225,000

$16,160,000

$12,225,000

$1,260,000

$2,285,000

$2,115,000

$9,895,000

$10,310,000

$265,000

$2,800,000

$14,500,000

Hemet Unified School District (CSCRPA)

Jurupa Unified School District (CSCRPA)

Murrieta Valley Unified School District (CSCRPA)

Palo Verde Unified School District (CSCRPA)

Perris Elementary School District (CSCRPA)

Galt Joint Union Elementary School District (CSCRPA)

Manteca Unified School District (CSCRPA)

Stockton Unified School District (CSCRPA)

Bayshore Elementary School District (CSCRPA)

Santa Paula Elementary School District (CSCRPA)

Lake Elsinore Unified School District (CSCRPA)

Riverside

Riverside

Riverside

Riverside

Riverside

Sacramento

San Joaquin

San Joaquin

San Mateo

Ventura

Riverside

2010-0369

2010-0370

2010-0371

2010-0372

2010-0373

2010-0374

2010-0375

2010-0376

2010-0377

2010-0378

2010-0379

CSCRPA 2010 TRAN Pool Series D

Tax and revenue anticipation note

Neg (BC)(UW)

Orrick HerringtonPiper Jaffray & Co

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

#

#

#

#

#

#

PROPOSED

Cash flow, interim financing

12

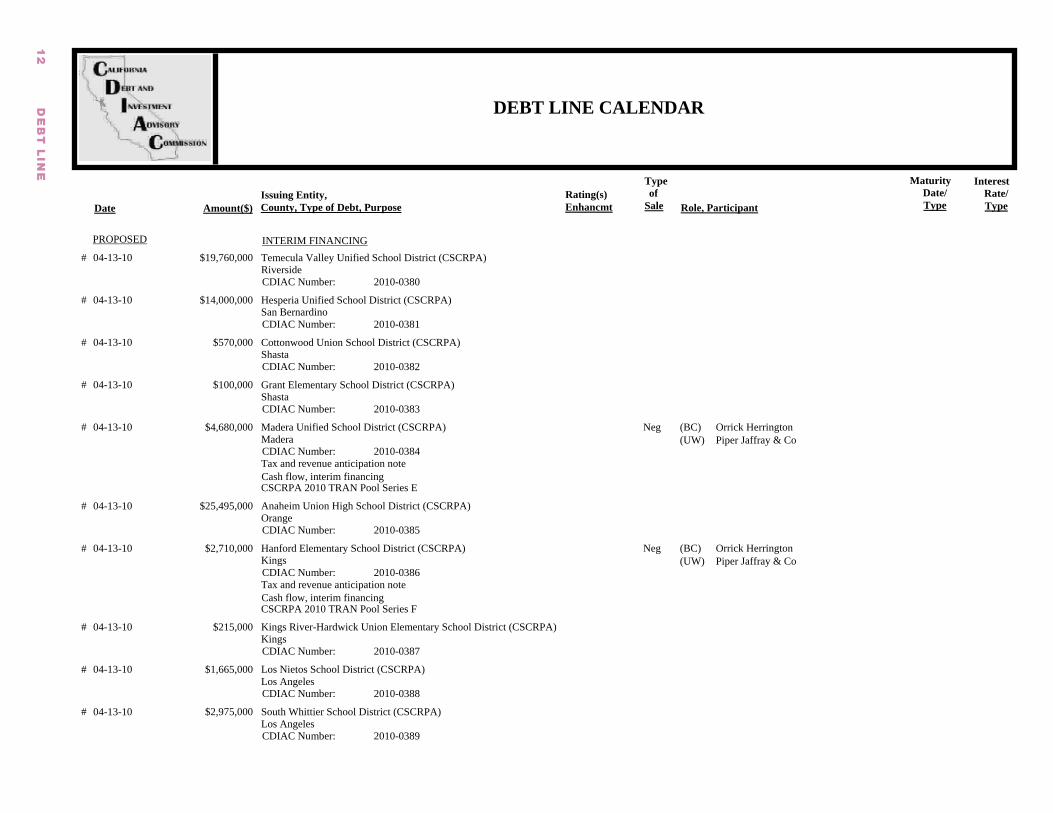

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

INTERIM FINANCING04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

$19,760,000

$14,000,000

$570,000

$100,000

$4,680,000

$25,495,000

$2,710,000

$215,000

$1,665,000

$2,975,000

Temecula Valley Unified School District (CSCRPA)

Hesperia Unified School District (CSCRPA)

Cottonwood Union School District (CSCRPA)

Grant Elementary School District (CSCRPA)

Madera Unified School District (CSCRPA)

Anaheim Union High School District (CSCRPA)

Hanford Elementary School District (CSCRPA)

Kings River-Hardwick Union Elementary School District (CSCRPA)

Los Nietos School District (CSCRPA)

South Whittier School District (CSCRPA)

Riverside

San Bernardino

Shasta

Shasta

Madera

Orange

Kings

Kings

Los Angeles

Los Angeles

2010-0380

2010-0381

2010-0382

2010-0383

2010-0384

2010-0385

2010-0386

2010-0387

2010-0388

2010-0389

CSCRPA 2010 TRAN Pool Series E

CSCRPA 2010 TRAN Pool Series F

Tax and revenue anticipation note

Tax and revenue anticipation note

Neg

Neg

(BC)(UW)

(BC)(UW)

Orrick HerringtonPiper Jaffray & Co

Orrick HerringtonPiper Jaffray & Co

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

#

#

#

#

#

PROPOSED

Cash flow, interim financing

Cash flow, interim financing

13

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

INTERIM FINANCING04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-13-10

04-26-10

$5,000,000

$2,325,000

$2,805,000

$9,225,000

$1,050,000

$1,250,000

$905,000

$1,005,000

$1,670,000

$400,000,000

Merced City School District (CSCRPA)

Buena Park Elementary School District (CSCRPA)

Center Unified School District (CSCRPA)

Tracy Joint Unified School District (CSCRPA)

Roseland School District (CSCRPA)

Corning Union Elementary School District (CSCRPA)

Red Bluff Union Elementary School District (CSCRPA)

Burton Elementary School District (CSCRPA)

Fruitvale School District (CSCRPA)

Los Angeles County Capital Asset Leasing Corporation

Merced

Orange

Sacramento

San Joaquin

Sonoma

Tehama

Tehama

Tulare

Kern

Los Angeles

2010-0390

2010-0391

2010-0392

2010-0393

2010-0394

2010-0395

2010-0396

2010-0397

2010-0398

2010-0354

CSCRPA 2010 TRAN Pool Series G

Tax and revenue anticipation note

Commercial paper

Neg

Neg

(BC)(UW)

(BC)(FA)

Orrick HerringtonPiper Jaffray & Co

Nixon PeabodyPRAG

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

#

#

#

#

#

PROPOSED

Refunding

Cash flow, interim financing

Project, interim financing

14

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

INTERIM FINANCING04-27-10

04-27-10

04-27-10

05-05-10

05-05-10

05-05-10

05-05-10

$15,000,000

$10,000,000

$1,940,000

$40,000,000

$10,000,000

$40,000,000

$10,000,000

Baldwin Park Unified School District (LACS)

Walnut Valley Unified School District (LACS)

Wilsona School District (LACS)

San Francisco City & County

San Francisco City & County

San Francisco City & County

San Francisco City & County

Los Angeles

Los Angeles

Los Angeles

San Francisco

San Francisco

San Francisco

San Francisco

2010-0317

2010-0318

2010-0319

2010-0285

2010-0286

2010-0287

2010-0288

LACS 2010 TRAN Pool Series F

Series 1

Series 1-T

Series 2

Series 2-T

Tax and revenue anticipation note

Commercial paper

Commercial paper

Commercial paper

Commercial paper

Neg

Neg

Neg

Neg

Neg

(BC)(UW)

(BC)(FA)

(BC)(FA)

(BC)(FA)

(BC)(FA)

Hawkins DelafieldRBC Capital Markets

Jones HallKNN Public Finance

Jones HallKNN Public Finance

Jones HallKNN Public Finance

Jones HallKNN Public Finance

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

#

#

PROPOSED

Federally Taxable

Federally Taxable

Cash flow, interim financing

Project, interim financing

Project, interim financing

Project, interim financing

Project, interim financing

15

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

INTERIM FINANCING

EDUCATION

05-05-10

05-05-10

03-04-10

03-05-10

03-31-10

04-07-10

$100,000,000

$12,500,000

$12,000,000

$500,000

$3,000,000

$14,500,000

Alameda County Joint Powers Authority

Panama-Buena Vista Union School District

Mt Diablo Unified School District

Fairfax

Riverside Unified School District CFD No 20

California Infrastructure & Economic Development Bank

Alameda

Kern

Contra Costa

Marin

Riverside

State of California

2010-0320

2010-0355

2009-1299

2010-0258

2010-0238

2010-0259

Series A

Series A

King City Jt UnHSD

Commercial paper

Tax and revenue anticipation note

Tax and revenue anticipation note

Tax and revenue anticipation note

Limited tax obligation bond

Public lease revenue bond

S:SP-1+

NR

Neg

Neg

Neg

Neg

Neg

Neg

10-01-10

04-23-10

Term

Term

.550

4.000

TIC

TIC

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(UW)

(BC)(FA)(UW)

Nixon PeabodyPRAGBarclays Capital Inc

Goodwin ProcterFieldman RolappStone & Youngberg

Quint & ThimmigGovernment Fin StratContra Costa CoStone & Youngberg

Quint & ThimmigWulff Hansen & CoMarin CoTiburon

Best Best & KriegerW J Fawell CoPiper Jaffray & Co

Stradling YoccaKNN Public FinancePiper Jaffray & Co

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

PROPOSED

SOLD

PROPOSED

Federally Taxable

Project, interim financing

Cash flow, interim financing

Cash flow, interim financing

Cash flow, interim financing

K-12 school facility

K-12 school facility

16

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

EDUCATION04-15-10

04-15-10

04-15-10

04-19-10

04-28-10

05-06-10

$6,185,000

$7,500,000

$45,000,000

$4,320,000

$8,000,000

$30,000,000

Tustin Unified School District CFD No 06-1

Willits Unified School District

Gilroy Unified School District

Salida Union School District

Snowline Joint Unified School District

Saugus/Hart School Facilities Financing Authority

Orange

Mendocino

Santa Clara

Stanislaus

San Bernardino

Los Angeles

2009-1088

2009-1329

2010-0329

2010-0344

2010-0270

2010-0119

Measure P

Series A & Taxable C Build America Bonds

Limited tax obligation bond

Certificates of participation/leases

Bond anticipation note

Certificates of participation/leases

Certificates of participation/leases

Public lease revenue bond

Neg

Neg

Neg

Neg

Neg

Neg

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(UW)

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)(UW)

Bowie Arneson WilesRBC Capital MarketsUBS Securities

Jones HallCaldwell FloresStone & Youngberg

Orrick HerringtonGeorge K Baum

Quint & ThimmigCapitol Public Fin GroupSouthwest Securities

Quint & ThimmigSchool Fac FinanceChilton & Assoc

Bowie Arneson WilesFieldman RolappStone & Youngberg

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

PROPOSED

Federally Taxable

Refunding

Refunding

K-12 school facility

K-12 school facility

K-12 school facility

K-12 school facility

K-12 school facility

K-12 school facility

17

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

EDUCATION05-06-10

05-06-10

05-06-10

05-15-10

05-15-10

06-01-10

$11,715,000

$11,715,000

$18,450,000

$1,400,000

$5,000,000

$3,600,000

Saugus/Hart School Facilities Financing Authority

Saugus/Hart School Facilities Financing Authority

Saugus/Hart School Facilities Financing Authority

Mt Diablo Unified School District

California Municipal Finance Authority

Menifee Union School District CFD No 2004-6

Los Angeles

Los Angeles

Los Angeles

Contra Costa

Multiple

Riverside

2010-0185

2010-0186

2010-0187

2010-0274

2010-0331

2009-0999

Series A

Series B Build America Bonds

Series C

School Buses

American Film Institute

Cameo Homes

Public lease revenue bond

Public lease revenue bond

Public lease revenue bond

Certificates of participation/leases

Conduit revenue bond

Limited tax obligation bond

Neg

Neg

Neg

Comp

Neg

Neg

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)(UW)

(FA)

(BC)(FA)(UW)

(BC)(UW)

Bowie Arneson WilesFieldman RolappStone & Youngberg

Bowie Arneson WilesFieldman RolappStone & Youngberg

Bowie Arneson WilesFieldman RolappStone & Youngberg

Government Fin Strat

Ronald E LeePop Lazic & CoCity National Bank

Rutan & TuckerStone & Youngberg

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

PROPOSED

Federally Taxable

K-12 school facility

K-12 school facility

K-12 school facility

Other, multiple educational uses

Other, multiple educational uses

K-12 school facility

18

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

EDUCATION02-11-10

02-26-10

03-01-10

03-08-10

03-10-10

03-10-10

$4,180,000

$6,875,000

$4,156,630

$65,185,000

$24,998,007

$34,525,000

Castaic Union School District

Ocean View School District

California Municipal Finance Authority

California Educational Facilities Authority

Poway Unified School District

California Educational Facilities Authority

Los Angeles

Orange

Multiple

State of California

San Diego

State of California

2010-0093

2010-0138

2010-0184

2010-0141

2010-0094

2010-0201

Northlake Hills ES

Spring View MS

Our Lady Queen of Angels School

Loyola Marymount Univ, Westchester Campus Ctr Series A

ID No 2007-1

Carnegie Institution of Washington Series A

Certificates of participation/leases

Certificates of participation/leases

Conduit revenue bond

Conduit revenue bond

Bond anticipation note

Conduit revenue bond

S:AAA/A

S:AAA/A+

NR

S:AA+

M:A2

M:MIG1

M:Aaa

Ins

Ins

Neg

Neg

Neg

Neg

Neg

Neg

09-01-33

03-01-22

04-01-20

10-01-40

12-01-11

07-01-40

Comb

Serial

Serial

Comb

Term

Term

4.975

3.494

4.528

1.972

4.568

NIC

TIC

VAR

TIC

TIC

NIC

(BC)(FA)(EN)(TR)(UW)

(BC)(FA)(EN)(TR)(UW)

(BC)(FA)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

Orrick HerringtonFieldman RolappAssured Guaranty CorpUS Bank Natl AssocPiper Jaffray & Co

Stradling YoccaClean Energy AdvocatesAssured Guaranty CorpUS Bank Natl AssocWedbush Morgan Sec

Squire SandersCatholic Finance CorpFarmers & Merchants Bank

Orrick HerringtonPFMUS Bank Natl AssocMorgan Stanley

Orrick HerringtonCA Financial ServiceZions First Natl BkStone & Youngberg

Orrick HerringtonPFMUS Bank Natl AssocBarclays Capital Inc

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

SOLD

Refunding

Refunding

Refunding

Refunding

K-12 school facility

K-12 school facility

K-12 school facility

College, university facility

K-12 school facility

College, university facility

19

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

EDUCATION03-17-10

03-17-10

03-18-10

03-18-10

03-19-10

03-19-10

$146,950,000

$205,145,000

$7,875,000

$42,875,000

$19,670,000

$188,000,000

Trustees of the California State University

Trustees of the California State University

Huntington Beach Union High School District

Kern Community College District

California Infrastructure & Economic Development Bank

California Infrastructure & Economic Development Bank

State of California

State of California

Orange

Multiple

State of California

State of California

2010-0230

2010-0339

2009-0516

2010-0148

2010-0036

2010-0330

Systemwide Series A

Systemwide Series B Build America Bonds

Coast HS Adult Education

Bakersfield Comm College Campus

UCSF Neurosciences Bldg 19A Series A

UCSF Neurosciences Bldg 19A Series B Build America Bonds

Public enterprise revenue bond

Public enterprise revenue bond

Certificates of participation/leases

Certificates of participation/leases

Conduit revenue bond

Conduit revenue bond

S:A+

S:A+

S:AAA/A

S:SP-1+

S:AA-

S:AA-

M:Aa3

M:Aa3

M:Aa2

M:Aa2

Ins

Neg

Neg

Neg

Neg

Neg

Neg

11-01-31

11-01-41

09-01-39

04-01-14

05-15-25

05-15-49

Serial

Comb

Comb

Term

Serial

Term

3.626

6.446

5.156

3.257

3.958

4.216

NIC

NIC

NIC

NIC

NIC

NIC

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(EN)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

Orrick HerringtonKNN Public FinanceState TreasurerBarclays Capital Inc

Orrick HerringtonKNN Public FinanceState TreasurerBarclays Capital Inc

Orrick HerringtonCA Financial ServiceAssured Guaranty CorpUS Bank Natl AssocPiper Jaffray & Co

Jones HallDale Scott & Co IncWells Fargo BankE J De La Rosa

Orrick HerringtonPFMThe Bank of NY MellonBarclays Capital Inc

Orrick HerringtonPFMThe Bank of NY MellonBarclays Capital Inc

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

SOLD

Federally Taxable

Federally Taxable

Refunding

Refunding

College, university facility

College, university facility

Other, multiple educational uses

College, university facility

College, university facility

College, university facility

20

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

EDUCATION03-23-10

03-25-10

03-30-10

03-31-10

03-31-10

$38,500,000

$93,295,000

$8,885,432

$75,395,000

$10,100,000

California Educational Facilities Authority

California Statewide Communities Development Authority

Washington Unified School District

The Regents of the University of California

The Regents of the University of California

State of California

Multiple

Yolo

State of California

State of California

2010-0142

2010-0174

2010-0275

2010-0217

2010-0218

Loyola Marymount Univ Series B

Aspire Public Charter Schools

Qualified School Construction Bonds

Series S

Series T

Conduit revenue bond

Conduit revenue bond

Certificates of participation/leases

Public enterprise revenue bond

Public enterprise revenue bond

NR

S:AA

S:AA

F:BBB

M:A2

M:Aa1

M:Aa1

LOC

Neg

Neg

Neg

Neg

Neg

10-01-15

07-01-46

03-15-26

05-15-40

05-15-35

Term

Comb

Term

Comb

Comb

6.338

1.420

3.820

5.856

VAR

TIC

TIC

NIC

NIC

(BC)(FA)(TR)(UW)

(BC)(EN)(TR)(UW)

(BC)(FA)(UW)

(BC)(TR)(UW)

(BC)(TR)(UW)

Orrick HerringtonPFMUS Bank Natl AssocMorgan Stanley

Orrick HerringtonPCSD Guaranty Pool I LLCUnion Bank NARBC Capital Markets

Quint & ThimmigGovernment Fin ServJP Morgan Chase Bk

Orrick HerringtonThe Bank of NY MellonM R Beal & Co

Orrick HerringtonThe Bank of NY MellonM R Beal & Co

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

SOLD

Federally Taxable

Federally Taxable

Refunding

Refunding

Refunding

Refunding

College, university facility

K-12 school facility

K-12 school facility

College, university facility

College, university facility

21

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

EDUCATION

HOUSING

04-07-10

03-31-10

03-31-10

03-31-10

04-15-10

04-15-10

$3,997,019

$11,266,695

$30,243,785

$53,033,682

$33,850,000

$5,600,000

Orland Unified School District

California Housing Finance Agency

California Housing Finance Agency

California Housing Finance Agency

Compton Community Redevelopment Agency

California Statewide Communities Development Authority

Multiple

State of California

State of California

State of California

Los Angeles

Multiple

2010-0268

2010-0282

2010-0283

2010-0284

2010-0202

2010-0204

Series A

Mountain View Apts Series D

Bond anticipation note

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Tax allocation bond

Conduit revenue bond

S:SP-1+ Neg

Neg

Neg

Neg

Neg

Neg

04-01-12Comb

2.464TIC

(BC)(FA)(TR)(UW)

(BC)(UW)

(BC)(UW)

(BC)(UW)

(BC)(FA)(UW)

(BC)(UW)

Dannis Woliver KelleyDale Scott & Co IncThe Bank of NY MellonPiper Jaffray & Co

Orrick HerringtonCitibank

Orrick HerringtonCitibank

Orrick HerringtonCitibank

Richards WatsonFieldman RolappGrigsby & Assoc

Orrick HerringtonDougherty & Co LLC

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

SOLD

PROPOSED

Federally Taxable

Subject to Alternative Minimum Tax

Refunding

Refunding

Refunding

Refunding

K-12 school facility

Multifamily housing

Multifamily housing

Multifamily housing

Multifamily housing

Multifamily housing

22

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

HOUSING04-15-10

04-23-10

04-27-10

04-29-10

05-11-10

06-15-10

$7,000,000

$2,713,424

$4,560,000

$2,808,171

$9,500,000

$11,000,000

California Statewide Communities Development Authority

California Municipal Finance Authority

California Statewide Communities Development Authority

California Statewide Communities Development Authority

California Enterprise Development Authority

California Municipal Finance Authority

Multiple

Multiple

Multiple

Multiple

Sacramento

Multiple

2010-0205

2010-0332

2010-0253

2010-0216

2009-1251

2010-0292

Desert Palms Apts Series C

Oakridge Apts Series A-1 & Sub A-2

Rolling Hills Estate

Orange Villas Series G

San Diego Christian Foundation Inc

Garvey Ct

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Neg

Neg

Neg

Neg

Neg

Neg

(BC)(UW)

(BC)(UW)

(BC)

(BC)(UW)

(BC)(FA)(UW)

(BC)

Orrick HerringtonDougherty & Co LLC

Orrick HerringtonJP Morgan Securities

Jones Hall

Orrick HerringtonWells Fargo Bank

Kutak RockGrowth CapitalComerica Bank

Jones Hall

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

PROPOSED

Refunding

Multifamily housing

Multifamily housing

Multifamily housing

Multifamily housing

Multifamily housing

Multifamily housing

23

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

HOUSING07-15-10

02-26-10

03-02-10

03-25-10

03-29-10

$28,000,000

$11,990,000

$11,410,000

$15,910,000

$19,537,631

Poway

California Municipal Finance Authority

Vista Community Development Commission

La Habra

California Municipal Finance Authority

San Diego

Multiple

San Diego

Orange

Multiple

2009-1315

2010-0080

2010-0055

2010-0154

2009-1418

Royal Mobile Home Park

Regency Towers Series A

Vista Area Low & Moderate Income Housing

Park La Habra & Viewpark Mobile Home Pks Series A

St Joseph's Sr Apts Series A-1 & 2

Certificates of participation/leases

Conduit revenue bond

Tax allocation bond

Certificates of participation/leases

Conduit revenue bond

NR

S:A-

S:AAA/A

NR

M:Aa3

Ins

Neg

Neg

Neg

Neg

Neg

04-01-35

09-01-37

09-01-40

02-01-32

Term

Comb

Comb

Comb

8.441

5.504

VAR

TIC

TIC

VAR

(BC)(FA)(UW)

(BC)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(EN)(TR)(UW)

(BC)(TR)(UW)

Richards WatsonPFMSpelman & Co

Jones HallUS Bank Natl AssocCiti Community Capital

Jones HallMagis AdvisorsUS Bank Natl AssocPiper Jaffray & Co

Kutak RockDavid Paul Rosen & AssocAssured Guaranty CorpThe Bank of NY MellonChilton & Assoc

Quint & ThimmigUS Bank Natl AssocUS Bank Natl Assoc

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

PROPOSED

SOLD

Federally Taxable

Refunding

Refunding

Single-family housing

Multifamily housing

Multifamily housing

Single-family housing

Multifamily housing

24

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

HOUSING

COMMERCIAL AND INDUSTRIAL DEVELOPMENT

03-30-10

03-31-10

03-31-10

03-30-10

05-04-10

$18,300,000

$2,300,000

$14,800,000

$50,000,000

$29,000,000

Los Angeles

California Statewide Communities Development Authority

California Statewide Communities Development Authority

California Infrastructure & Economic Development Bank

California Pollution Control Financing Authority

Los Angeles

Multiple

Multiple

State of California

State of California

2009-1374

2010-0014

2010-0015

2010-0276

2010-0098

MacArthur Park Metro Apts Series C

Broadway Studios Apts Series A-T

Broadway Studios Apts Series A

Pacific Gas & Electric Co Series E

BLT Enterprises of Fremont LLC Series A

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

NR

S:AAA/A-1+

S:AAA/A-1+

LOC

LOC

Neg

Neg

Neg

Neg

Neg

04-01-42

04-01-50

04-01-50

Term

Term

Term

VAR

VAR

VAR

(BC)(FA)(TR)(UW)

(BC)(EN)(TR)(UW)

(BC)(EN)(TR)(UW)

(BC)(UW)

(BC)(FA)(UW)

Kutak RockCSG AdvisorsUS Bank Natl AssocBanc of Am Pub Cap Corp

Orrick HerringtonEast West BankWells Fargo BankHutchinson Shockey

Orrick HerringtonEast West BankWells Fargo BankHutchinson Shockey

Sidley Austin LLPJP Morgan Securities

Orrick HerringtonAndrew S RoseWesthoff Cone

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

SOLD

PROPOSED

Federally Taxable

Refunding

Refunding

Multifamily housing

Multifamily housing

Multifamily housing

Pollution control

Pollution control

25

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

HOSPITAL AND HEALTH CARE FACILITIES03-15-10

05-05-10

05-11-10

05-11-10

06-30-10

01-14-10

$265,000,000

$62,000,000

$39,665,000

$20,000,000

$30,600,000

$54,310,000

California Health Facilities Financing Authority

California Infrastructure & Economic Development Bank

California Statewide Communities Development Authority

Sierra View Local Hospital District

Antelope Valley Healthcare District

ABAG Finance Authority for Nonprofit Corporations

State of California

State of California

Multiple

Tulare

Los Angeles

Multiple

2010-0405

2010-0334

2010-0277

2010-0399

2010-0333

2009-1330

Children's Hosp Los Angeles

Sanford Consortium Series A

Univ Retirement Community at Davis

Casa de las Campanas Inc

Conduit revenue bond

Conduit revenue bond

Conduit revenue bond

Public enterprise revenue bond

Conduit revenue bond

Conduit revenue bond

S:A-

F:BBB+

Ins

Neg

Neg

Neg

Neg

Neg

Neg 09-01-37Comb

6.824NIC

(BC)(FA)(UW)

(BC)(UW)

(BC)(UW)

(BC)(FA)(UW)

(BC)(FA)

(BC)(EN)(TR)(UW)

Orrick HerringtonShattuck HammondBank of America Merrill

Orrick HerringtonBarclays Capital Inc

Orrick HerringtonCain Brothers

Quint & ThimmigG L Hicks FinancialEdward D Jones & Co

Meyers NaveGE Capital Markets Inc

Holland & KnightOSHPDUS Bank Natl AssocCain Brothers

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

PROPOSED

SOLD

Refunding

Refunding

Refunding

Refunding

Hospital

Other, multiple health care purposes

Health care facilities

Health care facilities

Health care facilities

Health care facilities

26

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

HOSPITAL AND HEALTH CARE FACILITIES

CAPITAL IMPROVEMENTS AND PUBLIC WORKS

03-01-10

03-11-10

03-11-10

04-14-10

04-15-10

04-15-10

$5,000,000

$2,040,000

$3,024,486

$12,400,000

$750,000

$3,000,000

California Health Facilities Financing Authority

California Health Facilities Financing Authority

California Enterprise Development Authority

Brea

Lindsay Financing Authority

Brea

State of California

State of California

Sacramento

Orange

Tulare

Orange

2010-0220

2010-0025

2010-0096

2010-0349

2010-0229

2010-0348

Citrus Vly Med Ctr Inc & Foothill Hosp - Morris L Johnston Memorial

Valley Community Clinic Series A

Orange Co ARC

Solar & Energy Efficiency

Library

Solar & Energy Efficiency

Other note

Conduit revenue bond

Conduit revenue bond

Public enterprise revenue bond

Certificates of participation/leases

Public lease revenue bond

NR

S:A-

NR

Oth

Neg

Neg

Neg

Neg

Neg

Neg

04-01-15

04-01-40

03-01-20

Serial

Comb

Serial

4.820

6.066

TIC

TIC

VAR

(BC)(TR)(UW)

(BC)(EN)(TR)(UW)

(BC)(FA)(UW)

(BC)(UW)

(BC)(UW)

(BC)(UW)

Orrick HerringtonMarshall & Ilsley TrustGE Government Fin

Quint & ThimmigOSHPDUS Bank Natl AssocPiper Jaffray & Co

Kutak RockGrowth CapitalCity National Bank

Jones HallStone & Youngberg

Stradling YoccaUSDA

Jones HallStone & Youngberg

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

SOLD

PROPOSED

Refunding

Other, multiple health care purposes

Health care facilities

Health care facilities

Power generation/transmission

Public building

Power generation/transmission

27

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

CAPITAL IMPROVEMENTS AND PUBLIC WORKS04-15-10

04-29-10

04-29-10

04-29-10

05-01-10

05-03-10

$14,475,000

$400,000,000

$5,500,000

$4,800,000

$35,000,000

$150,000,000

Castaic Lake Water Agency

Long Beach

Lancaster Redevelopment Agency

Jurupa Community Services District CFD No 38

San Joaquin County CFD No 2009-2

San Francisco Bay Area Rapid Transit District

Los Angeles

Los Angeles

Los Angeles

Riverside

San Joaquin

Multiple

2010-0404

2010-0226

2010-0257

2010-0267

2009-0754

2010-0178

Santa Clarita Water Division Series B

Series B

Eastvale IA No 2 Series A

Vernalis Interchange

Certificates of participation/leases

Public enterprise revenue bond

Public lease revenue bond

Limited tax obligation bond

Limited tax obligation bond

Sales tax revenue bond

Neg

Neg

Neg

Neg

Neg

Comp

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)

(BC)(FA)

Stradling YoccaFieldman RolappCitigroup Global Markets

Kutak RockPRAGE J De La Rosa

Stradling YoccaUrban FuturesWedbush Morgan Sec

Best Best & KriegerFieldman RolappPiper Jaffray & Co

Nossaman LLPWedbush Morgan Sec

Orrick HerringtonKNN Public Finance

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

PROPOSED

Subject to Alternative Minimum TaxRefunding

Refunding

Refunding

Water supply, storage, distribution

Ports, marinas

Multiple capital improvements, public works

Multiple capital improvements, public works

Street construction and improvements

Public transit

28

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

CAPITAL IMPROVEMENTS AND PUBLIC WORKS05-04-10

05-04-10

05-04-10

05-04-10

05-05-10

05-05-10

$6,750,000

$11,000,000

$2,500,000

$3,195,000

$1,500,000,000

$6,000,000

Santa Cruz Public Financing Authority

Garden Grove Public Financing Authority

Garden Grove Public Financing Authority

Garden Grove Public Financing Authority

California Department of Water Resources

Hercules Public Financing Authority

Santa Cruz

Orange

Orange

Orange

State of California

Contra Costa

2010-0347

2010-0351

2010-0352

2010-0353

2010-0321

2010-0327

Series A

Series B Build America Bonds

Recovery Zone Series C

Series L

Electric Substation

Public lease revenue bond

Public enterprise revenue bond

Public enterprise revenue bond

Public enterprise revenue bond

Public enterprise revenue bond

Public enterprise revenue bond

Neg

Neg

Neg

Neg

Neg

Neg

(BC)(FA)

(BC)(FA)

(BC)(FA)

(BC)(FA)

(BC)(FA)(UW)

(BC)(UW)

Jones HallNorthcross Hill Ach

Stradling YoccaSequoia Financial Group

Stradling YoccaSequoia Financial Group

Stradling YoccaSequoia Financial Group

Hawkins DelafieldMontague DeRoseJP Morgan Securities

Fulbright & JaworskiChilton & Assoc

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

#

PROPOSED

Federally Taxable

Federally Taxable

Refunding

Refunding

Parking

Water supply, storage, distribution

Water supply, storage, distribution

Water supply, storage, distribution

Power generation/transmission

Power generation/transmission

29

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

CAPITAL IMPROVEMENTS AND PUBLIC WORKS05-11-10

05-11-10

05-11-10

05-18-10

05-18-10

05-20-10

$10,000,000

$33,000,000

$80,000,000

$45,000,000

$30,000,000

$15,730,000

California Statewide Communities Development Authority

Marin Municipal Water District Financing Authority

Orange County Sanitation District

Sunnyvale

Sunnyvale

Los Gatos

Multiple

Marin

Orange

Santa Clara

Santa Clara

Santa Clara

2009-1431

2010-0271

2010-0328

2010-0402

2010-0403

2010-0289

Aerojet

Series A

Series A Build America Bonds

Library

Conduit revenue bond

Public enterprise revenue bond

Certificates of participation/leases

Public enterprise revenue bond

Public enterprise revenue bond

Certificates of participation/leases

Neg

Neg

Comp

Neg

Neg

Comp

(BC)(UW)

(BC)(UW)

(BC)(FA)

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)

Kutak RockChatsworth Securities Inc

Quint & ThimmigE J De La Rosa

Fulbright & JaworskiPRAG

Jones HallRoss FinancialE J De La Rosa

Jones HallRoss FinancialE J De La Rosa

Jones HallE Wagner & Assoc

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

#

#

#

#

#

PROPOSED

Federally Taxable

Federally Taxable

Refunding

Refunding

Power generation/transmission

Water supply, storage, distribution

Wastewater collection, treatment

Wastewater collection, treatment

Water supply, storage, distribution

Public building

30

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

CAPITAL IMPROVEMENTS AND PUBLIC WORKS06-01-10

06-15-10

01-21-10

01-21-10

01-26-10

$42,855,000

$57,000,000

$98,495,000

$526,135,000

$875,000

Orange CFD No 06-1

Chino Basin Regional Financing Authority

San Diego County Water Authority Financing Agency

San Diego County Water Authority Financing Agency

Kanawha Water District

Orange

San Bernardino

San Diego

San Diego

Glenn

2009-1087

2010-0153

2010-0022

2010-0254

2010-0005

Del Rio

Inland Empire Utilities Agency Series A

Cap Imp Program Series A

Cap Imp Program Series B Build America Bonds

Limited tax obligation bond

Public enterprise revenue bond

Public enterprise revenue bond

Public enterprise revenue bond

Revenue bond (Pool)

S:AA+

S:AA+

NR

F:AA

F:AA

M:Aa3

M:Aa3

Neg

Neg

Neg

Neg

Neg

05-01-27

05-01-49

10-01-16

Serial

Term

Serial

4.246

6.163

4.210

NIC

NIC

TIC

(BC)(FA)(UW)

(BC)(FA)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

Quint & ThimmigFieldman RolappStone & Youngberg

Stradling YoccaPFMCitigroup Global Markets

Orrick HerringtonWedbush Securities IncUS Bank Natl AssocCitigroup Global Markets

Orrick HerringtonWedbush Securities IncUS Bank Natl AssocCitigroup Global Markets

Weist Law FirmSutter SecuritiesKanawha WDKanawha-Glide PFA

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

PROPOSED

SOLD

Federally Taxable

Refunding

Refunding

Refunding

Multiple capital improvements, public works

Wastewater collection, treatment

Water supply, storage, distribution

Water supply, storage, distribution

Water supply, storage, distribution

31

MA

Y 2

01

0

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

CAPITAL IMPROVEMENTS AND PUBLIC WORKS01-26-10

02-03-10

02-03-10

02-25-10

02-26-10

$670,000

$8,025,000

$101,260,000

$37,935,000

$765,545

Glide Water District

Northern California Power Agency

Northern California Power Agency

Central Basin Municipal Water District

Yolo County

Glenn

Multiple

Multiple

Los Angeles

Yolo

2010-0006

2009-1308

2009-1309

2009-1184

2010-0085

Hydroelectric No 1 Series B

Hydroelectric No 1 Series A

Southeast Water Reliability Series A

Justice Ctr Solar

Revenue bond (Pool)

Public enterprise revenue bond

Public enterprise revenue bond

Certificates of participation/leases

Certificates of participation/leases

NR

S:A

S:A

S:AAA/AA/AA

NR

F:A

F:A

M:A2

M:A2

M:Aa3/A1/A1

Ins

Neg

Neg

Neg

Neg

Neg

10-01-14

07-01-13

07-01-23

08-01-39

09-16-15

Serial

Serial

Serial

Comb

Term

4.071

3.079

3.901

4.516

4.750

TIC

NIC

TIC

TIC

TIC

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(TR)(UW)

(BC)(FA)(EN)(TR)(UW)

(BC)(FA)(TR)(UW)

Weist Law FirmSutter SecuritiesGlide WDKanawha-Glide PFA

Orrick HerringtonPFMUS Bank Natl AssocMorgan Stanley

Orrick HerringtonPFMUS Bank Natl AssocMorgan Stanley

Stradling YoccaKNN Public FinanceAssured Guaranty CorpUnion Bank NAStone & Youngberg

Jones HallMuniBond FinancialDeutsche Bank Natl TrustBanc of Am Pub Cap Corp

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

CDIAC Number:

SOLD

Federally Taxable

Refunding

Refunding

Refunding

Refunding

Water supply, storage, distribution

Power generation/transmission

Power generation/transmission

Water supply, storage, distribution

Power generation/transmission

32

DE

BT

LIN

E

Date Amount($)Issuing Entity, County, Type of Debt, Purpose

Rating(s) Enhancmt

Type of Sale Role, Participant

Maturity Date/ Type

Interest Rate/ Type

DEBT LINE CALENDAR

CAPITAL IMPROVEMENTS AND PUBLIC WORKS02-26-10

02-26-10

03-03-10

03-03-10

03-05-10

03-10-10

$2,000,000

$2,019,214

$23,375,000

$1,525,000

$12,980,000

$8,460,000

Yolo County

Yolo County

Gilroy

Moraga