Connecting the world’s financial markets Debt Investor Update February 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Connecting the world’s financial markets

Debt Investor UpdateFebruary 2014

Connecting the world’s financial markets

Disclaimer

Disclaimer

Connecting the world’s financial markets 3

By reading the presentation slides, you agree to be bound by the following limitations.

This presentation has been prepared for information and background purposes only and the information contained herein (unless otherwise indicated) has been provided by ICAP Group Holdings plc (the “Company”). It is confidential and does not constitute or form part of, and should not be construed as, an offer or invitation to subscribe for, underwrite or otherwise acquire, any securities of the Company or any member of its group nor should it or any part of it form the basis of, or be relied on in connection with, any contract to purchase or subscribe for any securities of the Company or any member of its group (each and "Affiliate") or with any other contract or commitment whatsoever. This document does not constitute an offering document in whole or part and any decision to invest in the offering of any of the Company’s or any Affiliate's securities should be made solely on the basis of information to be contained in in any offering document, or prospectus expressly provided to you in connection with any such offering, and on an independent analysis of the information contained therein. Neither this presentation nor any part of it may be reproduced or redistributed, passed on, or the contents otherwise divulged, directly or indirectly, to any other person (excluding the recipient's professional advisers) or published in whole or in part for any purpose without the prior written consent of the Company.

This presentation does not purport to be all-inclusive or to contain all of the information that a person may require to make a full analysis of the matters referred to herein. None of the Company, and its Affiliates, advisers, connected persons or any other person accepts any liability for any loss howsoever arising, directly or indirectly, from this presentation or its contents.

Any assumptions, views or opinions (including statements, projections, forecasts or other forward-looking statements) contained in this presentation represent the assumptions, views or opinions of the Company as at the date indicated and are subject to change without notice. All information not separately sourced is from Company data.

This presentation includes forward looking statements within the meaning of the securities laws of certain applicable jurisdictions. These forward looking statements include, but are not limited to, all statements other than statements of historical facts contained in this presentation, including, without limitation, those regarding our future financial position and results of operations, our strategy, plans, objectives, goals and targets, future developments in the markets in which we participate or are seeking to participate or anticipated regulatory changes in the markets in which we operate or intend to operate. In some cases, you can identify forward looking statements by terminology such as “aim,” “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “plan,” “potential,” “predict,” “projected,” “should,” or “will” or the negative of such terms or other comparable terminology. By their nature, forward looking statements involve known and unknown risks, uncertainties and other factors because they relate to events and depend on circumstances that may or may not occur in the future. We caution you that forward looking statements are not guarantees of future performance and are based on numerous assumptions and that our actual results of operations, including our financial condition and liquidity and the development of the industry in which we operate, may differ materially from (and may be more negative than) those made in, or suggested by, the forward looking statements contained in

Connecting the world’s financial markets 4

this presentation. In addition, even if our results of operations, including our financial condition and liquidity and the development of the industry in which we operate, are consistent with the forward looking statements contained in this presentation, those results or developments may not be indicative of results or developments in subsequent periods. We undertake no obligation to update or revise any forward looking statement or risk factors, whether as a result of new information, future events or developments or otherwise. The forward looking statements speak only as at the date of this presentation. Each of the Company, other relevant group entities and their respective agents, employees and advisers, expressly disclaims any obligation or undertaking to update any forward looking statements contained herein.

This presentation is distributed only to and directed only at persons who are not, or are not capable of classification as, Retail Clients (as defined in the Markets in Financial Instruments Directive 2004/39/EC) or equivalent applicable local regulatory classification and should not be distributed to any Retail Clients; in the UK, is not being distributed to and must not be passed on to the general public, and may only be distributed to persons who are investment professionals within the meaning of Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) order 2005 (the “Order”), persons falling within Article 49(2)(a) to (d) of the Order, or persons to whom it may otherwise lawfully be communicated (all such persons being “Relevant Persons”), is directed only at Relevant Persons and must not be acted on or relied on by persons who are not Relevant Persons; in member states of the European Economic Area which have implemented the Prospectus Directive (Directive 2003/71/EC) as amended (the “Prospectus Directive”), is distributed only to, and directed only at, persons who are “qualified investors” within the meaning of the Prospectus Directive and pursuant to the relevant implementing rules and regulations adopted by each relevant member state (“Qualified Investors”).

This presentation is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation of such jurisdiction or which would require any registration or licensing within such jurisdiction. This presentation is not for publication, release or distribution in the United States, Australia, Canada or Japan. In particular these materials are not intended for distribution in the United States or to U.S. persons (as defined in Regulation S) under the United States Securities Act of 1933, as amended.

Connecting the world’s financial markets

Introduction

Connecting the world’s financial markets

Executive Summary

• Leading wholesale markets operator and provider of post-trade risk mitigation and information services

• Diversified business model

• Strong portfolio of technology assets acquired and developed over time

• Well positioned to seize opportunities from regulatory changes

• Consistent conversion of profits into free cash flow

• Robust balance sheet and modest gearing

• Investment grade rating

6

Connecting the world’s financial markets

An introduction to ICAP

ICAP is a leading global financial markets operator, providing broking, electronic execution, information and automated services simplifying operational workflow and reducing risk to market participants along the trade life cycle

A strong balance sheet, enabling flexibility to invest in organic growth through new product innovation and pioneering services into new markets

5,000employees in all major financial centres

Local presence in

32 countries,

with over 70locations worldwide

13% of revenue re-invested in technology and innovation

USD1.3 trillion ADV transacted through our platforms

4

Connecting the world’s financial markets

A diverse product offering

Broadest asset class coverage• Rates: Interest rate derivatives, government bonds, repos, cash products and financial futures• FX: Spot and forward exchange, options• Credit: Corporate bonds and credit derivatives• Commodities: Oil, natural gas, power, coal, iron ore, precious metals, shipping• Emerging markets: Latin America, Asia and Russia / Eastern Europe, especially BRIC countries• Equities: principally equity derivatives

Post Trade Risk and InformationServices• Help users of financial

products reduce operationaland system-wide risks

• Empower customers to make trading decisions with market information across key asset classes

• Simplify client workflow via automated advanced tools and Straight Through Processing

Global Broking• Provide access to global pools

of buyers/ sellers to create liquid markets and greater transparency

• Breadth and depth of our operation gives us a significant global footprint

Electronic Markets• Operate a number of fully

electronic platforms in a range of different asset classes and instruments

• Automated platforms allow execution of large deal volumes quickly and easily, with greater transparency

5

Connecting the world’s financial markets

Financial Performance

Connecting the world’s financial markets

Group profit for the year

FY121

£mFY132

£m

Revenue 1,681 1,472

Net operating expenses (1,309) (1,164)

Operating profit 372 308

Net finance charge (24) (29)

Associates 6 5

Profit before tax 354 284

Acquisition & disposal costs (137) (158)

Exceptional items - (60)

Profit before tax (statutory) 217 66

Operating profit margin 22% 21%

Group revenues by product

133 107

154108

167142

204

190

374

339

649

586

FY12 FY13

Rates

FX & MM

Commodities

Emerging mkts

Credit

Equities

£1,472m

£1,681m

7

1 – year ended 31 March 20122 – year ended 31 March 2013

Connecting the world’s financial markets

ICAP’s business mix

£1,172m£997m

£301m

£268m

£208m

£207m

FY12 FY13

Global Broking Electronic Markets Post Trade

£1,472m

£1,681m

Revenue by business Operating profit by business*

Operating profit margin by business*

£153m £105m

£127m£113m

£92m£90m

FY12 FY13Global Broking Electronic Markets Post Trade

£203m66%

£219m59%

13%

11%

42%

42%

44%

44%

0% 10% 20% 30% 40% 50%

FY12

FY13

* Excludes acquisition & disposal costs and exceptional items 8

Connecting the world’s financial markets

Diversified business model

Operating profit & margin*Revenues

76% 75% 72% 70% 68%

16% 16% 17% 18% 18%

8% 9% 11% 12% 14%

FY09 FY10 FY11 FY12 FY13

59%52%

46% 41%34%

24%28%

33%34%

37%

17% 20% 21% 25% 29%

FY09 FY10 FY11 FY12 FY13

£1,585m £1,472m£1,741m £1,681m£1,605m £365m23%

£354m22%

£372m22%

£375m22%

£308m21%

Global Broking Electronic Markets Post Trade

* Excludes acquisition & disposal costs and exceptional items

66%

41%

9

Connecting the world’s financial markets 13

FY12£m

FY13£m

Global Broking

Above analysis excludes acquisition and disposal costs and exceptional items.

Revenues by region

Revenue 1,172 997

Operating profit 153 105

Margin 13% 11%

Number of brokers 2,347 2,195

562479

131

1,172

488397

112

997

-

£200m

£400m

£600m

£800m

£1,000m

£1,200m

EMEA Americas Asia Pacific Total

FY12 FY13

Cost savings by region

Staff costs as % of revenue

£21m

£27m

£16m

£20m

£5m

£5m

0 10 20 30 40 50 60

FY12

FY13

EMEA Americas Asia Pacific

£52m

£42m

57%

63%

55%

59%58%

61%

57%59%

57%

60%

51%

57%

45%

50%

55%

60%

65%

EMEA Americas Asia Pacific Global BrokingFY12 FY13 H1 FY14

Connecting the world’s financial markets

FY12£m

FY13£m

US Treasuries – Average Daily Volumes

14

Electronic Markets

Revenue mix

Spot FX – Average Daily Volumes

Above analysis excludes acquisition & disposal costs and exceptional items

Revenue 301 268Revenue - constant rate 305 266

Operating profit 127 113Operating profit – constant rate 128 111

Margin 42% 42%

Headcount 542 512

FY13FY12

137121

10

£301m 155131

15

50

100

150

200

250

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar$bn/day FY12 FY13 FY14

FY12: $130bn/day

FY13: $119bn/day

FY14 (10 mths): $156bn/day

50

100

150

200

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar$bn/day FY12 FY13 FY14

FY12: $152bn/day FY13:

$116bn/day

FY14 (10 mths): $95bn/day

£268m

EBS

BrokerTec

Other

Connecting the world’s financial markets 15

FY12£m

FY13£m

Post Trade Risk & Information

Revenue mix

Traiana – FX volumes triResolve – number of customers

Revenue 208 207Revenue – constant rate 207 207

Operating profit 92 90Operating profit – constant rate 91 91

Margin 44% 44%

Headcount 459 521

31%

53

4337

75

£208m

47

44

43

73

Reset & ReMatch

TriOptima

Traiana

Information

£207m

Above analysis excludes acquisition & disposal costs and exceptional items

FY13

3647

-5

101520253035404550

H1 FY13 H1 FY14

FY12

200

300

400

500

600

700

800

900

Oct 12 Jan 13 Apr 13 Jul 13 Oct 13 Jan 14

207%

Avg monthly transactions(millions)

Connecting the world’s financial markets 16

Net operating expenses

Net operating expenses by type Net operating expenses reconciliation

Headcount Cost savings

Above analysis excludes acquisition & disposal costs and exceptional items

960 824

159136

190204

-

£250m

£500m

£750m

£1,000m

£1,250m

£1,500m

FY12 FY13

Other

IT

Employee

£1,164m£1,309m

5,1234,976 4,885

24712738

6236

4,600

4,800

5,000

5,200 5%

£20m

£60m

£5m

FY12

FY13

FY14

Achieved in year Annualised Total

£80m

£25m

11%

1,309

1,164

6074 11

£1,000m

£1,100m

£1,200m

£1,300m

Connecting the world’s financial markets

Efficient conversion to cash

17

£233m £228m£260m £259m

£211m

£296m£264m

£210m

£268m £274m

FY09 FY10 FY11 FY12 FY13

Profit after tax Ongoing free cash flow

CashConversion 127% 116% 81% 103% 130%

Acquisitions(net of cash acquired) £200m £149m £29m £27m £12m

Dividends paid £106m £92m £135m £135m £145m

Movement in net debt £(67)m £(22)m £68m £79m £107m

Above analysis excludes acquisition & disposal costs and exceptional items

Two year moving average of 101%

conversion

Connecting the world’s financial markets

Gross and net debt

18

Gross debt / EBITDA* 1.4 1.7 1.3 1.4 1.6

Net debt / EBITDA* 0.5 0.6 0.4 0.2 n/a

(750)

(600)

(450)

(300)

(150)

-

150

300

450

600

FY09 FY10 FY11 FY12 FY13

£m

Cash and cash equivalents Gross debt Net debt

* Excludes acquisition & disposal costs and exceptional items

Connecting the world’s financial markets

Current outlook

19

Interim management statement on 5 Feb 2014.....Management’s expectations for PBT (before acquisition and disposal costs andexceptional items) for the full year remain unchanged, on a constant currency basis…..

Michael Spencer, Group Chief Executive Officer, said: “Trading activity across many marketswas down in the third quarter, compared to the prior year, with a slower December than weanticipated. Although market conditions remain difficult, we saw a modest improvement inactivity in January as the on-going debate about the Federal Reserve quantitative easingprogramme continued.

“Innovation is vital for our success and our strong cash generation allows us to continue toinvest in our future growth. The launch of the ICAP SEF was a very important project. Wehave had tremendous feedback from customers to our SEF and I am pleased that it is themarket leader in interest rate swaps. We are also seeing the tangible benefits of ourinvestments in post trade, as the regulatory push for risk mitigation drives demand for oursolutions.”

Connecting the world’s financial markets

Current Environment

Connecting the world’s financial markets

Wholesale markets are evolving

21

Impacts

Regulation• Increased importance of e-trading capabilities• Blocks and less liquid instruments harder to trade• Increased compliance cost

Customers• Growing importance of buy-side• Bank deleveraging not fully complete• Expect increased intermediation of OTC activity

Competition• New players emerging e.g. exchanges• New technology-driven trading venues – will need

liquidity for success

Products

• Banks are scaling back from capital intensive products

• Mandate for pre/post-trade transparency and reporting

Structural changes

Increased electronic trading

A new competitive landscape and a wider customer base

Intermediation of trade volumes on to SEFs

Bank deleveraging and shift from structured to flow products

Mandatory centralised OTC clearing and potential futurisation

Increased demand for post-trade risk mitigation services

1

2

3

4

5

Key change drivers

6

Connecting the world’s financial markets

Swap Execution Facility (“SEF”)

• Launched Oct 2013 in response to Dodd Frank Act for transparent OTC derivatives market per G20 objectives from 2009

• Opportunities– expanded customer footprint– electronic trading of interest rate derivatives on iSwap– expansion of Traiana in pre-trade screening

• Mandatory execution and clearing started 17 Feb 2014– certain interest rate and credit default swaps– gradual expansion to include other derivatives– softer launch with EU agreement and ruling for ‘packaged’ trades

22

Connecting the world’s financial markets

TraianaMarket leader in post trade processing • Network of 500+ clients from banks,

brokers, platforms and buyside• Global presence – New York, Chicago,

London, Hong Kong, Tokyo, Singapore• Processes average $1.5trn daily and 3m

messages

Solutions for new regulatory world• CCP Connect

Matching FX derivative trades cleared through LCH

• TR ConnectReporting OTC trades to repositories in Europe (EMIR), US (Dodd Frank) and Asia Pacific

• CreditLinkPre/post-trade credit screening and limit management across multiple venues (SEFs)

23

Connecting the world’s financial markets

TriOptima

triReduce• major multilateral compression to

remove unnecessary OTC trades• 200+ regular clients and $350 trn+

value compressed since 2003• reduces client Basel III capital costs

and helps improve leverage ratio

triResolve• reconciling OTC derivatives – regular

volume of 7m trades• 800 clients and 265,000 reconciliations

weekly• real-time reporting and exception

resolution for clients to avoid disputes and margin calls

24

Confidence, product & support

Award winning, market leader in risk mitigation and termination solutions

Connecting the world’s financial markets

EBS Direct

• Development of EBS platform (acquired 2006) – largest liquidity source in spot FX market

• Allows custom pricing for spot FX to disclosed clients

• Provides alternative for banks without own platform

• Average daily volume of $2bn in Jan

• Opportunity to extend to other asset classes

25

Confidence, product & support

Distribution, liquidity & best execution

Relationships & trust

Ecosystem & liquidityoptimization

Confidence, product & support

0

20

40

60

80

100

120

140

Apr 13 May 13 Jun 13 Jul 13 Aug 13 Sep 13 Oct 13 Nov 13 Dec 13 Jan 14

No.

of u

niqu

e co

unte

rpar

ties

EBS Direct Beta Post-launch

Avg Daily Volume ($m) Unique counterparties

EBS Direct is bringing new customers to EBS.Approximately 50 new customers in 2013.

Connecting the world’s financial markets 26

Ongoing priorities

• Leverage our comparative advantage

• Seize opportunities from regulatory developments – transparency, risk reduction, resilience and auditability

• Continue to deliver innovative solutions in changing market environment

• Improve the efficiency and cost discipline of the organisation

• Reinforce cultural values and best practices

Connecting the world’s financial markets

Debt Considerations

Connecting the world’s financial markets

Debt profile at 30 Sep 2013

Gross debt by currency

Gross debt interest exposure

22%

34%

44%

Fixed

USD

GBP

EUR

Floating

Note: 5Y €300m notes shown under EUR although swapped into GBP.

28

Financing Maturities

-

£50m

£100m

£150m

£200m

£250m

£300m

£350m

£400m

£450m

FY15 FY16 FY17 FY18 FY19 …… FY24

GBP50m term loan EUR300m notes USD193m PP notes

GBP425m RCF GBP125m retail bond EUR15m note

57%

43%

Connecting the world’s financial markets

Corporate structure

ICAP plc

ICAP Group Holdings plc Intercapital Limited

ICAP America Investments

Limited

ICAP Holdings (Asia Pacific)

Limited

ICAP Holdings Limited

ICAP Europe Limited

ICAP ElectronicBroking LLC

Reset PrivateLimited

EBS Service Company Limited

ICAP Securities USA LLC

TriOptima AB ICAP Brokers Pty Limited

Principal subsidiary (>5% EBITDA)

Holding company

29

Connecting the world’s financial markets 30

Credit ratings

• Coverage initiated in 2009 with Moody’s and Fitch

• Current position:

– Moody’sLT rating of Baa2 with negative outlookOpinion last updated on 7 Jan 2014Lead analyst: Michael Eberhardt ([email protected])

– FitchLT rating of BBB with stable outlookResearch report issued on 7 Jan 2014Lead analyst: Erwin van Lumich ([email protected])

Connecting the world’s financial markets

Appendices

Connecting the world’s financial markets 32

Global Executive Management Group

Duncan WalesGroup General Counsel

Iain TorrensGroup Finance Director

John NixonGroup Executive Director

Americas

David CastertonCEO

Global Broking

Gil MandelzisCEO EBS

Executive Chairman Traiana

Seth Johnson Co-CEO BrokerTec

CEO ISDX

Ken PigagaGroup Chief Operating

Officer

= Board Member

Michael SpencerGroup CEO

Laurent Paulhac

Hugh GallagherCEO

Asia Pacific

Connecting the world’s financial markets

• Board of directors oversees risk, control and compliance functions

• Clear division of roles and responsibilities between Chairman and Group CEO

• Day-to-day business delegated to Global Executive Management Group – three Board and eight business leaders

Risk governance

Board

Group Chief Executive Officer

Global Executive Management Group

Group Chief Operating Officer

Group General Counsel

Global Operating Committee Internal Audit

Group Risk and Capital

Committee

Audit and Risk Committees

External Audit

33

Group Chief Risk Officer

Group Head of Compliance

Direct reporting authority

Delegated authority

Connecting the world’s financial markets

Three Lines of Defence

34

Connecting the world’s financial markets 35

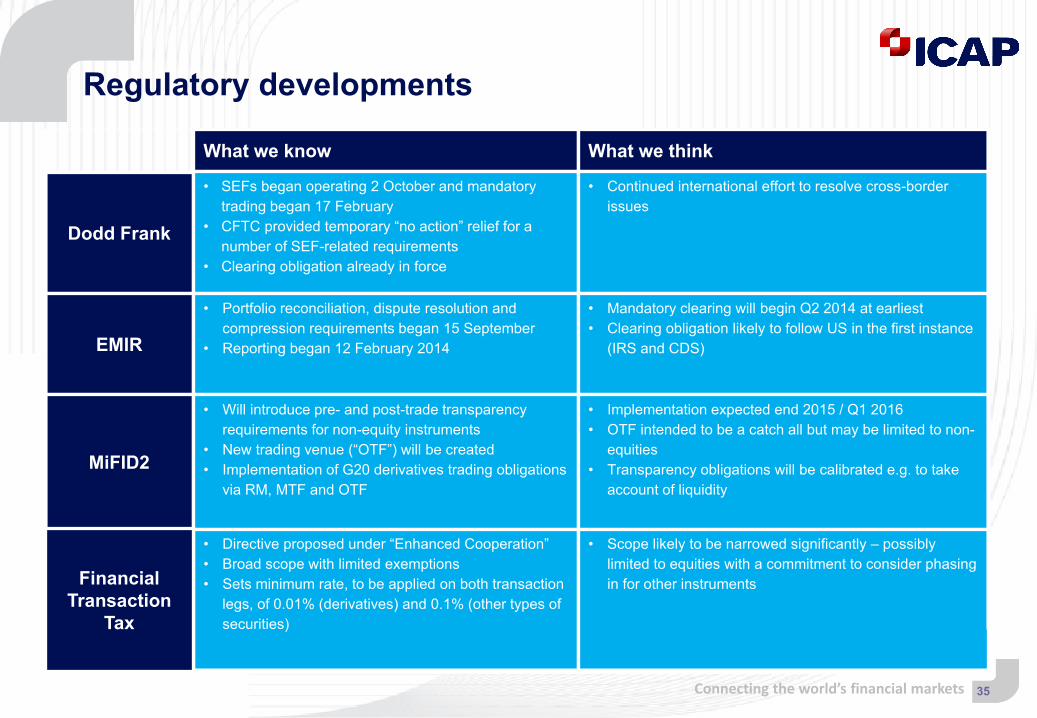

Regulatory developments

Dodd Frank

What we know What we think

• SEFs began operating 2 October and mandatory trading began 17 February

• CFTC provided temporary “no action” relief for a number of SEF-related requirements

• Clearing obligation already in force

• Continued international effort to resolve cross-border issues

EMIR

• Portfolio reconciliation, dispute resolution and compression requirements began 15 September

• Reporting began 12 February 2014

• Mandatory clearing will begin Q2 2014 at earliest• Clearing obligation likely to follow US in the first instance

(IRS and CDS)

MiFID2

• Will introduce pre- and post-trade transparency requirements for non-equity instruments

• New trading venue (“OTF”) will be created• Implementation of G20 derivatives trading obligations

via RM, MTF and OTF

• Implementation expected end 2015 / Q1 2016• OTF intended to be a catch all but may be limited to non-

equities• Transparency obligations will be calibrated e.g. to take

account of liquidity

• Directive proposed under “Enhanced Cooperation”• Broad scope with limited exemptions• Sets minimum rate, to be applied on both transaction

legs, of 0.01% (derivatives) and 0.1% (other types of securities)

• Scope likely to be narrowed significantly – possibly limited to equities with a commitment to consider phasing in for other instrumentsFinancial

TransactionTax

Connecting the world’s financial markets 36

Central committed financing

Facility Borrower Issue Date Amount Maturity Purpose

Term loan facility ICAP Group Holdings plc Sep 2013 GBP50m Sep 2014 General corporate purposes

Syndicated revolving credit facility including USD 200m swingline

ICAP Group Holdings plc Jun 2013 GBP425m Dec 2016 General corporate purposes

Programme Issuer Issue Date Amount Maturity Cusip / ISIN No

Global MTN ICAP Group Holdings plc Jul 2009 EUR300m Jul 2014 XS0441744645

US Private Placement Intercapital Limited [1] Jun 2005 USD193m Jun 2015 n/a

Global MTN ICAP plc [2] Jul 2012 GBP125m Jul 2018 XS0805454872

Global MTN ICAP plc [2] May 2013 EUR15m May 2023 XS0935766674

Bank Facilities

Issued Notes

1 – Guaranteed on subordinated basis by ICAP plc2 – Guaranteed by ICAP Group Holdings plc

ICAP plc2 Broadgate, London EC2M 7UR+44 (0) 20 7000 5000www.icap.com

Connecting the world’s financial markets

Related Documents