Management in Confidence MB2009.P.70 1 Dealing with Business Cases This guidance explains everything you need to do when producing a business case. Overview A business case is a formal document which explains the case for the investment of money or other resources in a project or programme of works. The business case is used to obtain management commitment and approval to invest resources, both money and people. It provides a framework for planning and managing the project as the ongoing viability of the project will be monitored against the approved business case. This guidance focuses on the production of the business case only – guidance on how to manage a project and the Houses‟ Gateway review process can be found under the project management section of the intranet. This guidance is intended for those managers that have either no or limited experience of preparing a business case. It is not anticipated that experienced, Prince 2 trained project managers will need to refer to this guidance other than to ensure all the key elements are included. Glossary FAQs Your role as a manager Types of Business Cases

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Management in Confidence MB2009.P.70

1

Dealing with Business Cases

This guidance explains everything you need to do when producing a business case.

Overview

A business case is a formal document which explains the case for the investment of money or other resources in a project or programme of works.

The business case is used to obtain management commitment and approval to invest resources, both money and people. It provides a framework for planning and managing the project as the ongoing viability of the project will be monitored against the approved business case.

This guidance focuses on the production of the business case only – guidance on how to manage a project and the Houses‟ Gateway review process can be found under the project management section of the intranet.

This guidance is intended for those managers that have either no or limited experience of preparing a business case. It is not anticipated that experienced, Prince 2 trained project managers will need to refer to this guidance other than to ensure all the key elements are included.

Glossary

FAQs

Your role as a manager

Types of Business Cases

Management in Confidence MB2009.P.70

2

Content of Business Cases

Checklist

Quick reference guides

Management in Confidence MB2009.P.70

3

Glossary

As this guidance is intended for both Houses of Parliament, the terminology used to describe roles, offices and processes has been altered to reflect the position in either House. The following glossary indicates these generic phrases and who or what they represent.

Terminology used House of Lords equivalent House of Commons equivalent

Central finance department Finance Department Financial Management Directorate (FMD)

Finance managers Finance Department Departmental finance managers

Budget-holder/Director General Budget Holder Director General

Finance Director Finance Director Director General (Resources)

Accounting Officer Clerk of the Parliaments Clerk of the House

PICT – AB (formerly JBSB) PICT – Advisory Board

PEB Parliamentary Estates Board

Management in Confidence MB2009.P.70

4

FAQs

Where do I go for help?

Your finance manager should be your first contact for help.

Why do we need business cases?

The business case is used to obtain management commitment and approval to invest the Houses‟ valuable resources: people and money, to complete a project.

When do I need to write a business case? If you work in either Estates or PICT you will need to produce an outline business case to obtain programme funding regardless of the value of the project. Once outline approval has been given then the total value of your project will determine which type of business case you will need to produce. If you do not work in the PED or PICT then you need to write a business case if you:

want to request additional budget, in excess of £50,000, for a scheme or initiative. For requests below £50,000, departments are expected to find the money from existing budgets. Please note, annual requests for changes to staffing levels are not covered by this guidance. Please refer to the staff planning guidance (HoC) or the Finance Department (HoL) in these cases

already have sufficient budget but the total cost of your project is in excess of £150,000 you will need to complete a formal business case

Please note that using business case disciplines are recommended even if your request does not need to be approved by the Finance Directors and are likely to be needed if the proposed expenditure could be deemed „novel or contentious‟. What is the difference between an outline and a detailed business case?

An outline business case is used at the start of the planning process to obtain senior management‟s „approval in principle‟ to a proposal. It focuses on WHY the project needs to be evaluated and can be a trigger for initial development funding where needed.

Management in Confidence MB2009.P.70

5

A detailed business is prepared after „approval in principle‟ is received and investigates HOW the proposal will be achieved.

Who needs to approve my business case?

Who approves your business case will depend on the total costs of the proposal and whether there is existing budgetary provision in place. Details of the approval process can be found in the annex to this guidance.

How do I know which strategy board to submit my business case to?

If your business case involves estates or ICT then you need to submit your outline business case to a strategy board. ICT related business cases are submitted to PICT-AB and estates related business cases are submitted to PEB. If your outline business case does not involve ICT or estates related work then you need to submit it directly to the Finance Directors. Please consult your finance managers for further guidance.

What is the deadline for submitting a business case?

ICT and estates outline business cases need to be submitted to:

Strategy boards by June

The Finance Directors by mid July (please note for estates, business cases need to be with the Finance Directors by June)

All other outline business cases need to be submitted to the Finance Directors by mid July.

When your outline business case has been approved, if the detailed business case requires approval by the Finance Directors then you need to submit your business case to them at least four months before the procurement procedure for the project concerned is due to start. If your business case only relates to one or other House then you should submit it to the Finance Director of that House. Most large projects are bi-cameral in nature and where that is the case you should submit your business case to both Finance Directors simultaneously, as they both need to approve it.

Urgent business cases can be submitted to the Finance Directors as they arise.

Management in Confidence MB2009.P.70

6

What is ‘strategic intent’?

Strategic intent is how, and to what extent, a project meets the corporate objectives or strategy. Providing evidence of this is an essential part of the outline business case.

Who do I need to consult?

Business cases can be very complex and cover a broad range of areas. For larger business cases that will involve a significant number of stakeholders, it is recommended that you consult as many people as possible to ensure that the business case is as comprehensive and robust as possible.

Who needs to be consulted will depend on the project or programme:

where a proportion or all of the costs will be shared between the Houses the proposal needs to be discussed and agreed with each House at an early stage.

where there are building works or changes in accommodation, you need to discuss this with estates or accommodation services.

changes to staff numbers which in turn will require changes to software and/or IT equipment need to be discussed with PICT

procurement of software or hardware need to be discussed with PICT during the planning stage.

I can’t think of any options, what do I do?

You need to be realistic about the options you propose – perhaps you have already thought of alternatives but have already disregarded them? If this is the case you still need to document them as possible options but then you need to explain why you disregarded them including the „do nothing‟ option.

Business cases offer senior management choices over whether, how, and when to invest. They need to be given a range of reasonable options from which to make a decision.

I don’t understand the financial appraisal template.

Contact your finance manager for help. If they are not available or you do not have one, contact your finance department.

Management in Confidence MB2009.P.70

7

Business case - Your role as a manager

“Manager” means the person who is responsible for producing the business case and managing the project.

you must ensure consultation takes place with all concerned parties

you must be realistic in your assumptions and achievements

you must ensure compliance with all appropriate House regulations and procedures

you must ensure the correct approvals are obtained before incurring any expenditure which is outside of your authority to incur

you must allow sufficient time for preparation and approval

Don‟t try to complete a business case independently, especially if you have never done one before. Consult as many people as possible to ensure all aspects have been covered.

When completing any business case, it is important to be CLEAR, CONCISE and FOCUSED. Don‟t waffle!

Your finance manager can help you with the production of a business case. However if you require more formal support, training seminars are provided by the Financial Management Directorate (HoC), and the Finance Department (HoL).

Management in Confidence MB2009.P.70

8

Types of Business cases

What is a business case?

Overview

Programmes and projects

Gateway Reviews

Stages of producing a Business Case

Business Planning Calendar

Outline business case

Detailed business cases

Management in Confidence MB2009.P.70

9

What is a business case?

Key

Points A business case is used to obtain management approval for projects requiring investment and to monitor ongoing viability.

Overview

When do I need to prepare a business case?

You will need to prepare a business case if you

want to request additional budget, in excess of £50,000, for a scheme or initiative. For requests below £50,000, departments are expected to find the money from existing budgets. You will need to discuss your requirements with your finance manager and Director General/ Budget-holder.

already have sufficient budget but the total cost of your project is in excess of £150,000 you will need to complete a formal business case anyway

have a contract that needs renewing whose value is expected to be in excess of £250,000 If you work in Estates, you need to produce a business case for:

each standalone project and

rolling maintenance programmes. Where the level of expenditure falls below these limits, it is recommended that business case disciplines are used. Please ask your finance manager for guidance. Full authorisation details can found towards the end of this guidance.

Management in Confidence MB2009.P.70

10

Who is responsible for preparing the business case?

The „client‟ project manager is responsible for preparing the business case. For example, if your project is the purchase of software for your department, although PICT will be involved significantly in its procurement and testing, you will need to prepare the business case.

What is the purpose of a business case?

The business case is used to obtain management commitment and approval to invest Parliament‟s valuable resources: people and money to complete a project, even if money is already available.

It provides a framework for planning the project or investment and is used to structure issues and actions in a logical fashion. The purpose of a business case is to:

identify the desired outcomes (including possible savings)

focus on deliverables (what users of the service want)

examine methods of delivery (for example, compare life-time costs and relative effectiveness)

identify scope of big changes (and manage big risks)

consider cross-cutting dependencies (for example, another office)

Once approved, the business case is then used to manage the progress of the project and monitor its ongoing viability. Some business cases can be completed quite easily whilst others will be complex and can take weeks or months to finish.

The main types of business case are:

outline business case.

detailed business case

Management in Confidence MB2009.P.70

11

Programmes and projects

The level of information and detail required for a business case will vary depending on whether the business case is for a stand-alone project or a programme which incorporates a number of projects.

What is the difference between a project and a programme?

A project

A project has definite start and finish dates, clearly defined outputs and benefits, defined finances and other resources. It will have, depending on the size, an outline business case (for planning purposes or seed corn funding) followed by a detailed business case, eg. School Transport Subsidies and the Big Ben Exhibition.

A programme

The Office of Government Commerce (OGC) states that a programme business case,

„…embraces the wider horizons of strategic benefits and outcomes from the programme‟s projects‟

In the simplest terms, a programme is „… a group of projects managed together for added benefit‟. It is about

managing groups of projects to achieve a desired outcome or benefit for an organisation, and

the structuring and control of those projects so they deliver effectively as a group.

A programme business case focuses on the strategic benefits and seeks management‟s commitment to adopt the recommended approach, eg. the cast iron roof programme and the Mechanical and Electrical Modernisation programme, both of which are long term programmes consisting of individual projects.

Management in Confidence MB2009.P.70

12

Gateway Reviews

What is a gateway review?

The OGC Gateway Process is the trademark name for the peer review process designed by the Office of Government Commerce, in which independent practitioners from outside the programme/project use their experience and expertise to examine the progress and likelihood of successful delivery of the programme or project.

The reviews use a series of interviews, reviews and experience to provide an additional perspective on the issues facing the project team, and an external challenge to the robustness of plans and processes.

When is a review needed?

The use of gateway reviews will depend on the assessment of potential risks of the programme or project. For low risk proposals health checks based on Gateway criteria and checkpoints will be sufficient. For medium or high risk proposals, you will need to arrange for a Gateway review to be carried out in accordance with OGC brand principles.

Timetable

Gateway Reviews for high risk, large schemes can take up to 12 weeks to complete. You will need to take this into account when planning your project or programme. In summary:

Stand alone project – gateway review needs to be completed prior to the submission of the detailed business case

Programme – initial gateway review needs to be completed prior to the submission of the outline business case. Subsequent interim reviews may need to be completed prior to the submission of the detailed business case.

Detailed guidance on the Gateway Review process can be found under the project management section of the intranet.

Management in Confidence MB2009.P.70

13

Stages of producing a business case

All major business cases should be related, as far as possible, to the annual planning cycle in both Houses. This is particularly important where funding needs to be secured. In some cases this may not be possible, eg if one or both Houses identify an urgent, in-year need.

The level of information and detail required for a business case will vary depending on the stage in the planning process.

Stage one: Planning Stage – ‘in principle’

Before the summer recess (May to July) for the financial year starting the following April, business units (departments and offices) will need to start the business planning process. At this stage if you are, or will be, responsible for a potential project or investment that will deliver an improvement to the business; you will need to complete an outline business case. This can then be used to judge the merits of taking forward a bid for your proposal in preference to other possible bids.

In the outline business case you will need to explain why the project needs to be considered. This is your opportunity to explain how the project or investment fits with the Houses‟ corporate objectives and why the project needs to be completed sooner rather than later.

You need to send your completed outline business case to your Director General (HoC) or Head of Office (HoL) so that they can submit all your departments‟ business cases to the Finance Directors as part of the business planning process. The business cases need to be submitted to the Finance Directors before the summer recess and according to the timescale set out in the annual guidance by the relevant House so that the appropriate authorisations can be obtained prior to each House submitting its budget request for future years.

For ICT and Estates related projects, these outline business cases will need to go to the relevant strategy boards ie PICT-AB and PEB prior to submitting to the Finance Directors. Ensure that you take this additional step into account when completing your business case. PICT need to be consulted from the outset in business-led business cases with ICT content.

Management in Confidence MB2009.P.70

14

When a satisfactory business case has been submitted to the Finance Directors, they will review, approve and where necessary pass it to the Accounting Officers for approval. It is the Senior Responsible Officer„s (SRO) responsibility to ensure the appropriate approvals are obtained.

Financial provision for the business cases which successfully complete this process and are approved will be included in the draft financial plan of the relevant Houses‟ budget request to the House Committee (HoL) or House of Commons Commission (HoC) in December. Once the House Committee and/or the House of Commons Commission approves the provision for inclusion in the Houses‟ budget for the following year, the proposed projects will have been approved „in-principle‟. In the case of the House of Lords a bid for funding will then be made to the Treasury, again in December.

However, at this stage you do not have the authority to incur any expense unless the approval of the outline business case provides funding for undertaking initial research or feasibility work for the project.

Stage two: Delivery Stage - detailed business case

Once you have approval for an outline business case, depending on the anticipated costs of the scheme, you will need to complete a detailed business case:

for project costs above £150,000 (non-Estates), £500,000 (Estates) where you have funding

for project costs above £50,000 where you are asking for funding.

Occasionally, a project is approved by one of the Houses‟ Committees (House of Lords House Committee, House of Commons Commission, Finance & Services). In these cases, an outline business case is not required and you can proceed directly to the full business case stage.

Management in Confidence MB2009.P.70

15

Business planning calendar

The business planning exercise starts in the spring/summer prior to the start of the following financial year (April):

April - June – outline business cases to the relevant strategy boards if applicable (PICT-AB, JEB) for priority ranking

May - mid July - to Finance Directors, for scrutiny over the summer recess and to start the approval process.

October – Business plans incorporating approved business cases presented to the Management Board.

November - December – Corporate business plan presented to the relevant House Committee.

The diagram on the next page illustrates the planning cycle for ICT related business cases in a pictorial format. Non-ICT related business cases will follow a similar timetable.

Occasionally, you will need to complete a business case for an urgent project. In these situations, business cases can be submitted to your Finance Directors outside of this timetable. Please discuss the situation with your finance manager.

Management in Confidence MB2009.P.70

16

Jan

Feb

Mar

Apr

MayJun

Jul

Aug

Sep

Oct

NovDec

JBSB

reviews

outline

business

cases

ICT ANNUAL BUSINESS CYCLE

JBSB

considers

overall ICT

planC & L

Management

Boards consider

overall business

plan including ICT

proposals

PICT budget

review and

deadline for

any last minute

bids (DPICT

and FD staff)

Trilateral

Finance

Ds/OCE/PICT

budget review

Submit Outline

business cases

to Finance

Directors

Programme

Governance

PICT

level

JBSB

level

Management

Board level

Key

C & L

Management

Boards agree

financial plan

options

Brief F&S and

House Cttees

House Committee

and Commission

consider outturn

and next year‟s

budget

Committee level

Finance &

Services

Cttee

considers

Estimate

bid

Commons and

Lords

Management

Boards set initial

strategy

Management in Confidence MB2009.P.70

17

Completing an outline business case

Key Points

Part of three year planning process. Leads to „approval in principle‟ only. The project may not be started at this point but initial research work can be undertaken if budgetary provision is available.

You will need to complete an outline business case in order to obtain ‘approval in principle’ if you want to start an improvement project which requires investment.

If a project has been approved by one of the Houses‟ Committees (House Committee, House of Commons Commission, Finance & Services Committee), then an outline business case is not required and you can proceed directly to the detailed business case stage.

If your project involves Estates/Accommodation Services or ICT, you will need to submit your outline business case to the relevant programme board (PICT-AB and PEB) prior to submission to the Finance Directors, to obtain an „in principle‟ decision regarding the direction and priority of programmes of work. Use this document to explain clearly and justify fully why the project should be considered in more detail. You need to ensure that the project achieves the Houses‟ objectives and that there is a clear benefit to the House. Approval of an outline business case is approval ‘in principle’ only. This means that the concept has been approved, but you will still need to complete a more detailed business case in order to gain approval to start the full project. However, you can use the outline business case to request funds to undertake detail research and feasibility studies.

Once „approval in principle‟ has been given, you will need to start producing a detailed business case.

Management in Confidence MB2009.P.70

18

Content of outline business case

The main areas to include in an outline business case are:

Executive Summary Summarise the key points and state clearly what is required from the approver.

Explanation of the strategic intent: Explains the problem or opportunity and why it needs to be addressed. The focus needs to be on how it meets the House‟s objectives including value for money (VFM).

Objectives, benefits and performance indictors:

Indicate the nature of the benefits to be gained and when they will be achieved

Initial risk assessment: Identifies and assesses the key risks and issues involved

Stakeholder interests: Identifies the key stakeholders

Resources: Provides a global estimate of the scale of the initiative – detailed costs are not required at this stage, although it would be beneficial to align resources to possible approaches that could be taken.

Next steps: Determines the priority of the actions required.

Management in Confidence MB2009.P.70

19

Completing a detailed business case

Key Points

Must be submitted at least four months before the start of the procurement procedure for the project is due to start.

The aim of the detailed business case is to obtain the Finance Directors approval to undertake a scheme including potentially novel or contentious schemes.

A scheme is potentially novel or contentious if it is likely to attract high levels of publicity, for example, a project which has been specifically requested by an MP or Peer may attract excessive attention. The Finance Directors must always be consulted if you are uncertain whether a scheme might be considered „novel or contentious‟.

House of Lords ‘away-days’

The House of Lords also requires a business case to be completed for departmental „away-days‟. Specific guidance is available from the Human Resources Office and business cases need to be approved by the Finance Director to ensure VFM and to avoid reputational risk. The House of Lords has defined „away-days‟ as „to allow management and staff to discuss work related issues in an informal environment‟. If in doubt, please ask your finance manager.

As a general rule of thumb, if your business case needs to be approved by the Finance Directors, you will need to prepare a detailed business case.

Content: The main areas to include in a detailed business case are:

Executive summary

Objectives including benefits

Consultation

Risks/achievability

Options

Financial Consideration

Project plan and timetable

Management in Confidence MB2009.P.70

20

Conclusion

Appendices – option appraisals

Timetable

You will need to complete a detailed business case at least four months before the procurement procedure for the project concerned is due to start. If your business case only relates to one or other House then you should submit it to the Finance Director of that House. Most large projects are bi-cameral in nature and where that is the case you should submit you business case to both Finance Directors simultaneously, as they both need to approve it. This is to allow sufficient time for scrutiny and resolution of issues. If you do not meet this timetable the project may be rejected.

Remember: for medium or high risk projects, a Gateway Review must be completed before submission of the detailed Business Case.

Management in Confidence MB2009.P.70

21

Content of Business Cases

Executive Summary

Strategic Intent

Objectives and benefits

Benefits

Critical Success Factors

Consultation

Risks and achievability

Options

Option assessment

SWOT analysis

Financial Considerations

Capital Costs

Non-cash transactions

VAT

Project plan and timetable

Appendix: Investment Appraisal

Management in Confidence MB2009.P.70

22

Executive Summary

Key

Points An executive summary is used to highlight to the reader the KEY points in a business case. It should not include anything that has not been referred to in the main body of the report.

Content

Imagine yourself in the position of the PEB/PICT-AB or the finance director. What are the main aspects of the business case that you need to know? Ask yourself questions such as:

Why is this investment needed at all?

Why is it preferable to a different investment?

Why do it now as opposed to later?

Summarise your thoughts:

Why the scheme is being proposed

What the scheme will achieve

How it will be achieved – indicate the preferred option and why it is the preferred option

How much the preferred option will cost (including savings)

What are the main risks to non-achievement of the objective

Remember: keep it brief and to the point.

Management in Confidence MB2009.P.70

23

Strategic Intent

Key

Points To explain WHY the project is needed and why this project should take priority.

You will need to explain why the scheme or project is being proposed; this is referred to as the strategic intent and is the main focus of the outline business case. The strategic intent needs to explain clearly how the project meets the strategic objectives of the Houses of Parliament. If the justification for the scheme is not clear then the project may not be approved. In this section of the business case, you need to:

describe how or why this project is being proposed, for example is it due to a: o business change, (eg. the need to reduce costs) o technological developments (eg new software) or o regulatory or statutory change (eg health and safety legislation) o does it provide environmental benefits (eg reduction in carbon emissions)

explain how it contributes to the Houses‟ core tasks and objectives, including value for money (VFM)

consider whether it needs to be implemented now or whether it can be delayed

consider the implications if it is delayed

highlight the other partners involved who need to be, or have been, consulted, eg the House of Lords or the House of Commons

Include any research data of analysis to support the case you are making.

Management in Confidence MB2009.P.70

24

Objectives and Benefits

Key

Points In this section you need to identify clearly the objectives of the proposed project:

what are you trying to ACHIEVE?

when will you know you have achieve it – set TARGETS

are there DEGREES of success?

You need to be clear about what you are trying to achieve as this is one of the most important sections of a business case, yet tends to be the one that is completed the least effectively. Remember: in order to measure the achievement of an objective or benefit it is essential that you identify the starting point. You will need to explain the current, quantified position so that the senior manager approving your business case understands the extent of improvement projected. You must avoid using words like „improve‟, „optimise‟, „clarify, and „help‟ as they are vague and cannot be measured. Include details of the:

benefits the project will realise

how they will be measured

quantifiable targets

critical success factors You will also need to indicate the extent to which the targets need to be met in order for the project to be considered a SUCCESS, ie if the targets are not met fully, does that mean the project has failed? Is the scheme still considered to be successful if a target is only 80% achieved?

Management in Confidence MB2009.P.70

25

Benefits In this section you need to identify the benefits of the project; both financial and non-financial and how they will be measured. Where possible your business case needs to include quantifiable benefits, however it is recognised that some projects may only have qualitative benefits such as improved security or staff morale. Where you have identified financial benefits, these need to be included in the option appraisal section as these will reduce the cost of the project. Ensure the objectives are SMART – benefits should be specific, measurable, achievable, realistic and timely Important point to note: You need to identify clear benefits and indicate how you will know when they have been achieved otherwise this may cause delays approving your business case. Areas you should consider inlcude:

financial savings

value for money benefits o efficiency improvements eg. will it improve the workflow of a process or reduce waste (measure reduction in errors

or waste, or the time taken to complete an activity) o will costs be avoided eg. will the number of insurance claims be reduced or avoided or will it prevent penalties

being enforced?

reputational benefits: o will the project improve staff motivation (eg. can measure the reduction in sickness and recruitment and retention

targets) o sustainability agenda eg „green‟ agenda could measure reduction in CO2 emissions (energy usage), or

achievement of recycling targets.

compliance o with a statutory requirement if the Houses of Parliament adopt the relevant legislation (need to indicate what will

happen if the Houses were non-compliant) o Houses‟ objectives and policy commitments

Management in Confidence MB2009.P.70

26

Critical success factors

Critical Success Factors are the essential areas of activity that must be performed well if you are to achieve the project objectives. In large projects, so many issues can compete for your attention that it is often difficult to see the „wood for the trees‟. If you are managing a team, it can be extremely difficult to get everyone on the team pulling in the same direction and focusing on the true essentials. You will not need to identify critical success factors for small projects; only large projects need to consider this aspect. The following is an extract (only a few of the factors are listed) from the Access Control System business case (value >£5m). Although the business case detailed other benefits including the ability to integrate the system into all areas of the Palace and improved reliability, the main objectives which had to be achieved were the improved security aspects.

Improvement Priority Driver Consequence of not adopting

Alternatives Measurement of success

Improved Security to the Perimeter

Essential Operational and Security

Potential for harm to those on the estate

None No breaches of security to the perimeter

Improved Security between public and private areas

Essential Operational and Security

Potential for harm to those on the estate

None No internal breaches of security

The ability to monitor the movements to and from the estate

Essential Operational and Security and fire safety legislation

Non compliance None Entry and egress reports

Management in Confidence MB2009.P.70

27

Consultation

Key Points

Consult all interested parties including those who will be affected by the project as well as those who need to input into the project.

Stakeholders - Other departments in the House of Lords or the House of Commons (including PICT) You need to indicate in your business case the full range of consultation that has taken place, what is planned and the effects of the consultation. Many projects will involve other departments, the House of Lords, the House of Commons and/or third parties. It is important that you recognise the input of, or the impact the project has on, other departments. You will need to consult with stakeholders at an early stage regarding:

departments who need to contribute to the project eg is Estates, Accommodation Services or IT support required?

the procurement route to be followed, including timetable

the impact the delivered project will have on departments eg will other departments need additional training, support, guidance?

House of Lords and/or House of Commons - the full cost of the scheme needs to be identified along with the amount to be allocated to each party

Management in Confidence MB2009.P.70

28

Risks and achievability

Key

Points A realistic assessment and management of the risks that would prevent a successful outcome for the project.

In this section you need to consider any risks that may prevent the project from being successful. Once you have identified the risks you will need to indicate how you are going to manage them.

Risk Management Risk management is the identification and management of risks which could affect the success of your project. You need to consider two areas of risk in your business case:

those associated with the project as a whole irrespective of which option is selected; and

those associated with specific options Be realistic and:

identify the key risks

indicate how you are proposing to manage the risks

produce action plans to manage the risks Remember: where you have identified risks that are likely to occur and have a significant impact you must include the cost of managing these risks in the financial appraisal. You need to assess each risk in terms of its probability or likelihood of occurring and it potential impact. This is in line with the two Houses‟ corporate risk management policy guidance. Please see your House guidance. (HoC staff – see attached) When you have identified the risks you need to plot them on the „heat map‟.

Management in Confidence MB2009.P.70

29

The „heat map‟ assigns a traffic light colour to the risk: red, amber and green. You will need to indicate the action you are going to take to reduce the likelihood or impact of the risks that fall in the „amber and red zones‟ of the „heat map‟ methodology. Where this action requires resources these need to be included in the business case proposal. For example, if there is a high risk that the House may change the specification of a new build project the contract will need to be flexible enough to accommodate these additional costs and therefore may be more expensive. This type of additional cost needs to be included in the business case.

Risks to consider Potential risks to consider are

how changes in personnel will be managed

how changes in scope or objectives will be managed

how changes in budgetary requirements will be managed

management of business continuity issues

Note: if the scope or objectives of a project are altered, you will need to re-examine the business case. If the project changes significantly then the business case will need to be re-approved in accordance with the delegated authority limits as though it were a new project.

Dependencies You will also need to consider whether the project is dependent on any events or other projects and conversely whether any other projects are dependent on this one. What will happen if this dependency is not met?

Management in Confidence MB2009.P.70

30

Options

Key

Points Identify reasonable alternative options for achieving your objective.

Options You need to consider the different options available for achieving your objective(s). Identify the criteria that you will use to evaluate each option and determine which is the most appropriate. You will need to complete a section for each option you consider. It is important that you are realistic in the options you put forward. Your business case will be delayed if you propose spurious options. For each option you need to provide:

a description of the option

an assessment of its strengths and weaknesses

an investment appraisal taking into account costs and savings over the full life-cycle (summarise the results in the main body of the report but attach the details as appendices)

an assessment of the risks and benefits associated with each option and how they will be managed if they have not already been covered by the earlier risk and benefits sections

Management in Confidence MB2009.P.70

31

Option assessment

Description and assessment You need to demonstrate in the business case that a reasonable range of options has been explored.

You will need to:

identify at least three reasonable options of which one option should be a „do minimum or do nothing‟ option.

(This option has caused confusion in the past; it does NOT mean that we cease any work we are currently undertaking but actually means we would „carry on as normal‟. For example, if an asset is currently being maintained then the „do nothing‟ option would be to continue with this maintenance.)

one option could be to increase maintenance rather than replace the asset.

consider new or innovative approaches to achieve the objective. Just because the Houses of Parliament have always purchased an asset or service in a certain way does not mean that it should continue to do so. The House may achieve substantial cost savings or service improvements by considering new and alternative ways to achieving the objective, for example: o outsourcing or franchising o partnership working o leasing o automation

You will need to complete an assessment of the strengths and weaknesses for each option – you may wish to use a SWOT analysis (alternative methodologies can be used – proper consideration of strengths and weaknesses including risks is more important than which methodology you use.)

Management in Confidence MB2009.P.70

32

SWOT analysis

SWOT analysis A SWOT analysis provides a structure for analysing the strengths, weaknesses, opportunities and threats for any scenario: Strengths Weaknesses Opportunities Threats It is one step in a process that helps you to

appreciate the strengths of a situation, which need to be built up on

define the weaknesses, which need to be minimised

make the most of opportunities that present themselves

recognise the possible threats and manage them in a planned and organised way. To help in completing a SWOT analysis for each of the options you have proposed, suggested questions have been provided below. Strengths & weaknesses

what are the advantages/disadvantages of the option?

is there an impact (good or bad) on the reputation of the Houses of Parliament?

what is the impact on resources: assets and people? o Do we have the resources and skills or do we need to buy-in? Could there be a problem with staff continuity? o How large is the budget? Is there a risk of significant overspend?

do we have the experience, knowledge and data to support the option?

do we already have or will we have the right processes, systems, IT and communications in place?

do we have or will we have the right cultural, attitudinal and behavioural attributes to ensure success of the option/project?

Management in Confidence MB2009.P.70

33

Opportunities and threats

are there opportunities for collaboration? (ie partnership working, timing of work to „piggy-back‟ other work)

are there any dependencies which would impact on the success of this option/project?

could political interference/support affect the scheme?

are there any environmental impacts which need to be considered?

would developments in IT assist in achieving the project‟s objectives?

how likely is the loss of key staff?

Management in Confidence MB2009.P.70

34

Financial Consideration

Key

Points The total cost of the project needs to be identified.

In this section, you need to consider whether the options you have proposed are affordable and how the Houses will fund the project. You need to identify the budget requirement that you are asking for.

You need to be explicit about what you are asking for:

how much funding are you asking for?

how much is coming from o existing budgets? o bids against central budgets? (in this case, you need to indicate why existing departmental budgets can not be

used) o is it bicameral and have they agreed? o other third parties?

what resource will be required? This includes staff and accommodation (not just budget)

what is the impact on other departments? Can they, and will they, support the scheme?

Highlight any financial benefits which may not be realised immediately, for example, freeing up accommodation for others to use or staff savings which will materialise over the long-term due to natural staff turnover. What is the difference between the budget requirement and the Net Present Value? The Net Present Value (NPV) is calculated using a technique called „Discounted Cash Flows‟ (DCF) as part of the investment appraisal and identifies, from a financial perspective, which option would provide the best value for money. DCFs use only cash items ie. those transactions that have an effect on cash such as a payment to a third party.

Management in Confidence MB2009.P.70

35

The budget requirement is the total cost of the project and needs to include non-cash items such as depreciation.

Management in Confidence MB2009.P.70

36

Capital costs

The costs that you can classify as capital are limited to those which comply with International Financial Reporting Standards. The guidance in this standard can be subject to interpretation but in general it refers to costs incurred as a result of long-term investment in assets both purchased and enhanced. You can capitalise costs associated with:

the purchase of, or improvement to, assets; and

project fees incurred in bringing those assets into use If in doubt about whether expenditure can be capitalised please ask your finance manager or the central finance department. When you capitalise expenditure, it creates revenue transactions called depreciation and cost of capital, sometimes referred to as „below the line‟ transactions. You will need to recognise these transactions in your budget requirement.

Management in Confidence MB2009.P.70

37

Non-cash (below the line) transactions If your project includes capital costs then you also need to recognise the associated „below the line‟ transactions. These are costs which do not result in a cash transaction – they are accounting transactions. These transactions include:

Depreciation

Capital charges (currently at 3.5%) Remember, if you are unsure please contact your finance manager for assistance. Depreciation When an asset is purchased the transaction is not shown in your department‟s revenue account (income and expenditure account). As the expenditure has been classified as capital the transaction only affects the balance sheet at this initial stage. As the asset is used and its value deteriorates because it is being used, a transaction needs to be put through the revenue account to represent this. This transaction is called depreciation and you calculate it as follows:

Cost of the asset – any residual value on disposal the life of the asset in years

For example, an asset costing £200,000 to acquire with an asset life of ten years and an expected residual value of £20,000 on disposal would create an annual depreciation charge of £18,000.

Cost of the asset – any residual value on disposal = 200,000 – 20,000 the life of the asset in years 10

The only exceptions to this are land, antiquarian library books, and heritage assets which are not depreciated. Depreciation starts in the year that the asset is brought into use. Please contact your finance department for details of asset lives.

Management in Confidence MB2009.P.70

38

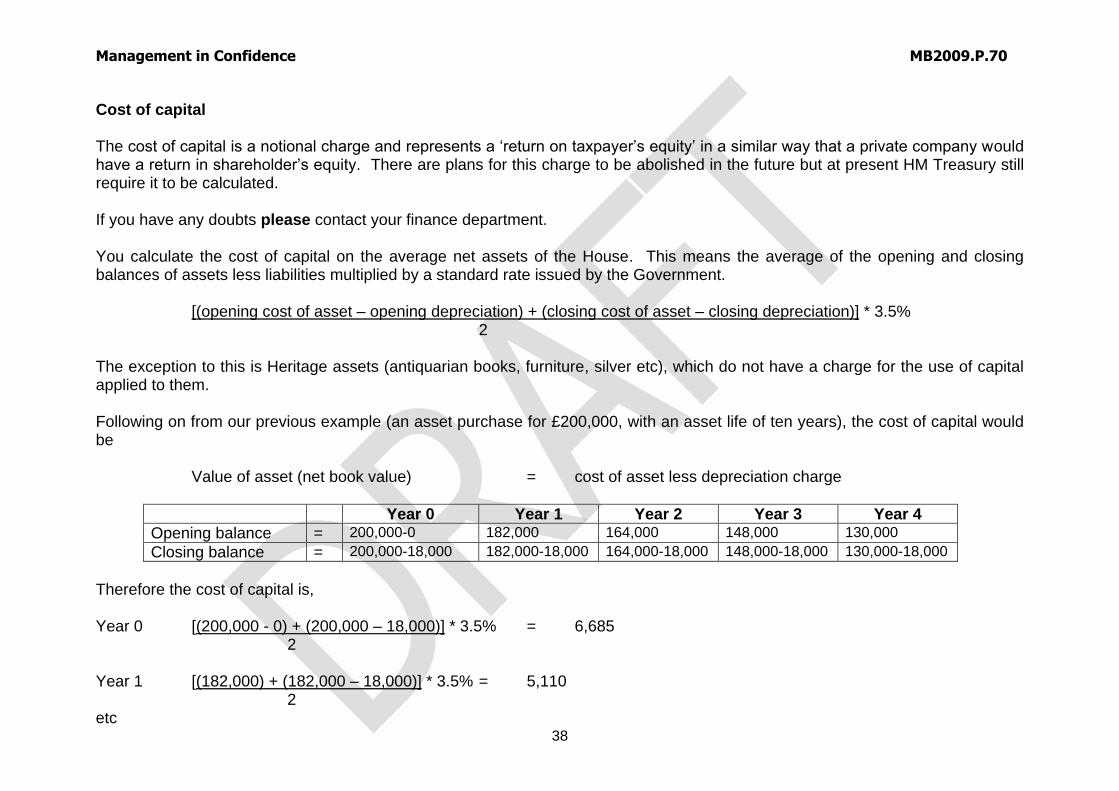

Cost of capital The cost of capital is a notional charge and represents a „return on taxpayer‟s equity‟ in a similar way that a private company would have a return in shareholder‟s equity. There are plans for this charge to be abolished in the future but at present HM Treasury still require it to be calculated. If you have any doubts please contact your finance department. You calculate the cost of capital on the average net assets of the House. This means the average of the opening and closing balances of assets less liabilities multiplied by a standard rate issued by the Government. [(opening cost of asset – opening depreciation) + (closing cost of asset – closing depreciation)] * 3.5% 2 The exception to this is Heritage assets (antiquarian books, furniture, silver etc), which do not have a charge for the use of capital applied to them. Following on from our previous example (an asset purchase for £200,000, with an asset life of ten years), the cost of capital would be Value of asset (net book value) = cost of asset less depreciation charge

Year 0 Year 1 Year 2 Year 3 Year 4

Opening balance = 200,000-0 182,000 164,000 148,000 130,000

Closing balance = 200,000-18,000 182,000-18,000 164,000-18,000 148,000-18,000 130,000-18,000

Therefore the cost of capital is, Year 0 [(200,000 - 0) + (200,000 – 18,000)] * 3.5% = 6,685 2 Year 1 [(182,000) + (182,000 – 18,000)] * 3.5% = 5,110 2 etc

Management in Confidence MB2009.P.70

39

VAT You should include VAT when it is not recoverable from HMRC (Her Majesty‟s Revenue & Customs). As a general rule, VAT is not recoverable on goods or services which can not be provided in-house. A current list of account codes /expenditure types where VAT is recoverable is provided at „standard data‟ document 2. [include HoL list]

Management in Confidence MB2009.P.70

40

Project plan and timetable

Key Points

Indicate the key deadlines and significant dependencies.

Deliverables You need to provide details of the proposed timetable and project plan, indicating the completion dates for key deliverables, such as the procurement timetable. You also need to indicate how the project will be delivered. This could include:

internally or externally

through outsourcing

if externally procured, the type of procurement procedure are you proposing.

Management in Confidence MB2009.P.70

41

Appendix - Investment Appraisal

Investment Appraisal

Content of Financial Analysis

Full Life-cycle costs

Discounted cash flow

Sensitivity Analysis

Management in Confidence MB2009.P.70

42

Investment Appraisal

Key

Points In this section you need to identify the true cost of each option.

An investment appraisal identifies the cash flows for each option in order to ascertain which, from a financial perspective, would provide the best value for money. It is a „cost-benefit‟ analysis of the „before and after‟ situation. The current financial situation needs to be known and understood at the start of the process otherwise the true cost and savings can not be identified. Remember, the decision to select one option over another is not always about the cost. Non-financial benefits will also play a significant part in the selection of the preferred option. You need to prepare an investment appraisal for each of the options you have identified and attach them as annexes to the business case. A template is provided to assist you in providing the key information required. Sensitivity Analysis You will need to prepare a sensitivity analysis to ensure that the chosen option is still the preferred one even if some of the assumptions change.

Management in Confidence MB2009.P.70

43

Content of financial analysis When you complete an investment appraisal of each option, you will need to include:

the full life-cycle costs

all the financial years of the project, not just the initial set-up

all the cash items divided into:

initial acquisition or development

on-going running/operating costs

capital and non-capital costs

contributions from third parties

savings (if applicable) You can use the template provided in this guidance. You need to ensure that all costs are included, such as:

other departmental costs (if the project needs input from facilities (eg estates or accommodation services), PICT or any other department then these costs need to be shown clearly, this will mean early consultation with other departments)

VAT but only if it is not recoverable When you have identified all the costs and savings, the results should be discounted to reflect the value of future cash flows. If you are using existing budgets then this should be shown clearly. This is particularly relevant if you are preparing a Facilities or a ICT related business case. You do not need to include adjustments for inflation.

Management in Confidence MB2009.P.70

44

Full life-cycle costs

Full life-cycle costs refer to the total costs of a scheme over its entire life; not just its initial set-up costs but its running costs throughout its life, including maintenance. For example, if the project you are proposing is for the purchase of an asset which has a life of 10 years, then your appraisal should also cover 10 years. When you use full life-cycle costs, your appraisal may indicate that the cheapest project to purchase initially is not necessarily the most economical one. For example, asset A may be cheaper to buy initially compared to asset B, but asset B may have lower maintenance and running costs. Therefore, when considering the cost of the asset over its life, asset B may represent better value for money. i.e. Asset A, purchase price £50,000, no maintenance costs Asset B purchase price £20,000, with annual maintenance costs of £10,000 p.a. Over the life of the asset (say five years), Asset A would represent the better value for money.

Management in Confidence MB2009.P.70

45

Discounted cash flows

You do not need to make any adjustments to the figures in the business case to reflect inflation. The costs you produce should be provided at the current day price. Discount Factors If your project is going to last longer than one year then you will need to discount its future cash flows to reflect the current year value, ie £1 today will not have a value of £1 in five years time. The longer the project, the more important it is to obtain the true cost of the scheme, for example, If you were comparing two pieces of equipment, say a boiler, and both boilers incurred the same total costs, £5,500 over their useful life (10 years), but boiler A incurred more costs at the beginning of its life, whereas boiler B incurred costs towards the end of its life. When a discount factor of 3.5% is applied, Boiler B is the most economic boiler to purchase; boiler B costs £4,490, whereas boiler A costs £4.978.

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Total

Before discounting

Boiler A 1000 900 800 700 600 500 400 300 200 100 5500

Boiler B 100 200 300 400 500 600 700 800 900 1000 5500

Apply discount factor to cash flows

Boiler A 1000 870 747 631 523 421 325 236 152 73 4978

Boiler B 100 193 280 361 436 505 569 629 683 734 4490

The „financials‟ templates provided with this guidance will automatically adjust your figures for you. HM Treasury has set the cost of capital at 3.5% (as at 2008/09 – please check with finance to ensure that this has not changed). For details of rates see „standard data‟ document 3.

Management in Confidence MB2009.P.70

46

Sensitivity Analysis

Sensitivity Analysis You will need to undertake sensitivity analysis to ensure that the chosen option is still the preferred one even if some of the assumptions made when selecting it, change. Sensitivity analysis tests the vulnerability of options to changes in assumptions (variables). It assesses how changes in assumptions or inputs will impact on the results and highlights at what stage a proposal may cease to be beneficial to the House. For example, if the proposal is very sensitive to changes in demand where a change in demand has a disproportionate impact on the cost of the proposal, then the House may consider a different option. You will need to replicate the financial appraisal for different scenarios such as a „worst case or pessimistic‟ scenario to compare with the proposed option. For more complex business cases, you will need to consider at least three different scenarios. Suggested variations to consider are:

changes in demand, eg. in a catering contract, a change in projected sales of say 10%, may affect the profitability of the proposal

changes in specification , eg. a change in the specification for the refurbishment of a room from the „top of the range‟ standard to a more publicly acceptable standard may affect which contractor is used

changes in personnel numbers, eg. an accommodation project may recommend a different option if the numbers of staff involved changes

changes in contract prices (how realistic is the price indicated in the business case? Is it a quote or a best guess?)

assumptions about the transfer of risk

Management in Confidence MB2009.P.70

47

Templates and flow charts

Checklist

Quick Reference

Management in Confidence MB2009.P.70

48

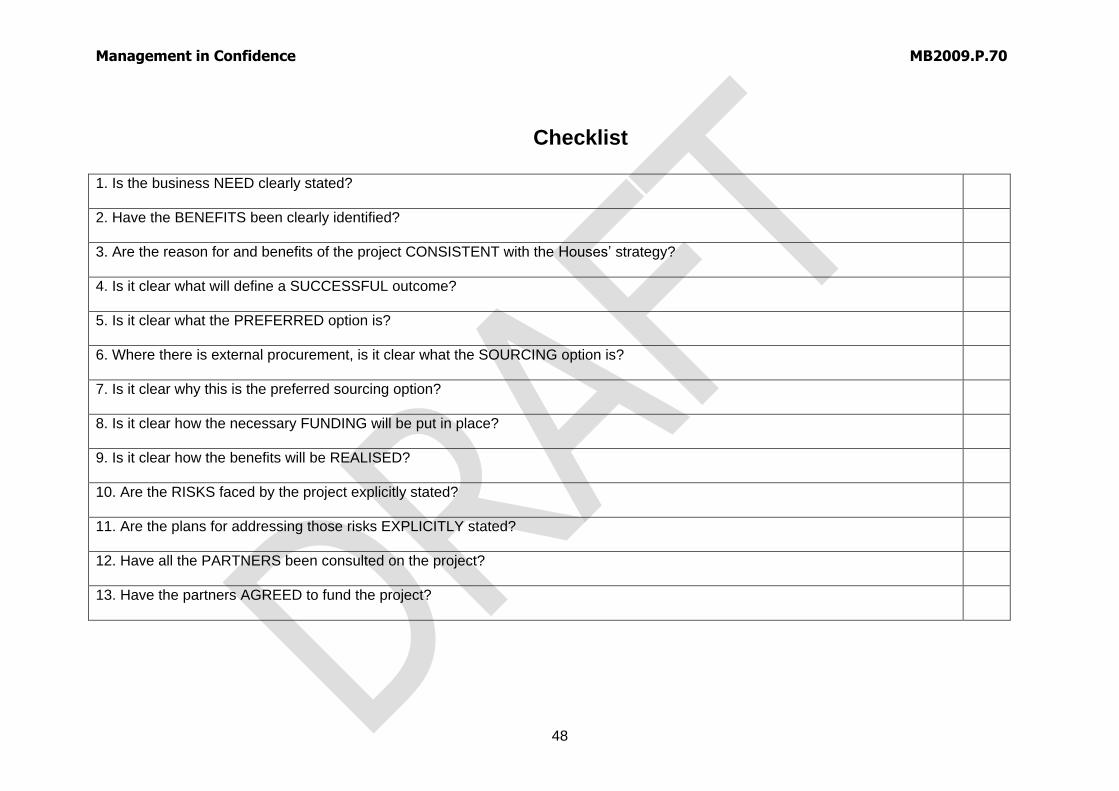

Checklist

1. Is the business NEED clearly stated?

2. Have the BENEFITS been clearly identified?

3. Are the reason for and benefits of the project CONSISTENT with the Houses‟ strategy?

4. Is it clear what will define a SUCCESSFUL outcome?

5. Is it clear what the PREFERRED option is?

6. Where there is external procurement, is it clear what the SOURCING option is?

7. Is it clear why this is the preferred sourcing option?

8. Is it clear how the necessary FUNDING will be put in place?

9. Is it clear how the benefits will be REALISED?

10. Are the RISKS faced by the project explicitly stated?

11. Are the plans for addressing those risks EXPLICITLY stated?

12. Have all the PARTNERS been consulted on the project?

13. Have the partners AGREED to fund the project?

Management in Confidence MB2009.P.70

1

Quick reference guides

Templates – important information

Informal templates or quick reference guides have been provided to assist in the preparation of business cases. These are attached as annexes to this guidance. Please note: these templates are not blank documents for completion; they advise on the structure that can be used and include brief guidance (taken from the main guidance) for preparing a business case. Every project is different and will inevitably require you to think about the details relevant to the circumstances. The template provides the MINIMUM level of information that is required. If the project is complex, the information needed before managers will approve the business case will increase.

1 Outline business case guidance

2 Full Business case guidance

3 Option Appraisal work sheet (separate document)

Management in Confidence MB2009.P.70

2

Outline Business Case Brief Guidance Notes

Remember: this is the document that needs to justify why the House needs to undertake this project.

You need to ensure that it is clear and focused otherwise the project may not proceed to the next stage.

EXCUTIVE SUMMARY You need to explain BRIEFLY:

Why the scheme is being proposed

What the scheme will achieve

The potential impact in other departments in the House

How much it will cost (outline costs)

STRATEGIC INTENT In this section you need to explain why we need to undertake this project.

The outline business case needs to justify why the House needs to undertake this project.

The subsequent full and short-form business cases investigate how the project will be

implemented.

Explain the problem/opportunity and why it needs to be addressed:

how does it contribute to the House’s core tasks and objectives

does it need to be implemented now or can it be delayed?

what are the implications if it is delayed?

are there any other partners involved eg the House of Lords, House of Commons?

Include any research data of analysis to support the case you are making.

OBJECTIVES and benefits In this section you need to explain what it is you are trying to achieve.

Explain what the proposal aims to achieve.

Are there any known critical success factors at this stage? Does it need to be linked

with another piece of work?

Is this part of a larger scheme or programme?

Identify the benefits in terms of financial (those which will reduce the cost of the

project) and non-financial benefits:

OPTIONS You need to outline the potential options that will be considered in detail in the full or

short-form business case. Remember to consider different procurement options:

Partnership working

Outsourcing etc

Risks In this section you need to outline the key risks to the project that may need to be managed.

STAKEHOLDER INTERESTS

Management in Confidence MB2009.P.70

3

In this section you need to identify all the potential stakeholders:

who needs to be consulted,

who will be impacted by the project?

Consider Estates, PICT, House of Lords, House of Commons, 3rd

parties.

Indicate if anyone has already been consulted and what their response was (were they

supportive?). NOTE, if this scheme involves the other House it is essential that they are

consulted early in the process to ensure they also obtain the potential funding necessary to

complete the project.

Cost and Timescale Give an indication of when the costs are likely to be incurred, such as

Will they be spread evenly over the project or weighted in the first year,

What is the split between capital and revenue,

Will temporary resources be brought in and if so, when?

How will the services/asset be purchased? Proper procurement procedures will take

time to complete.

Use the full business case finance template as a guide to identify the main components,

although the same level of detail is not required at this stage.

NEXT STEPS Be clear about what is required next:

Are you requesting monies to complete a feasibility study? If yes, state what you

need and what will be achieved with it.

If ‘approval in principle’ is given, when will a full business case be produced?

Management in Confidence MB2009.P.70

4

Detailed Business Case Brief Guidance Notes Remember: the main difference between the short-form and full business case is the level of detail

provided reflecting the higher risk generally associated with large scale projects.

EXECUTIVE SUMMARY You need to explain BRIEFLY:

Why the scheme is being proposed

What the scheme will achieve

How it will achieve it – indicate the preferred option

What the main risks are

How much it will cost and when will it start

OBJECTIVES and benefits 1.1 Objectives

The justification for undertaking the project should have been made in the OUTLINE

business case. However, you should refer back to it to remind the reader.

You need to include details of the:

Objectives to be achieved

Benefits the project will realise

Quantifiable targets

Critical success factors including any assumptions made.

Identify the benefits in terms of financial (those which will reduce the cost of the project)

and non-financial benefits.

Avoid using words such as ‘improve, optimise, clarify, and help’ as they are vague and

subjective.

1.2 Financial benefits

You need to give details of the financial benefits of the project in monetary terms. For

example:

Improved cash flow.

Reduced stock levels.

Explain how the value of the benefits will be measured.

1.3 Non-Financial benefits

You need to describe any other benefits of the project. For example:

Improved image/reputation.

Improved staff morale.

Improved response times.

Explain how the non-monetary value of the benefits is to be measured. For example:

Satisfaction survey.

Reduced staff turnover.

Management in Confidence MB2009.P.70

5

CONSULTATION You need to provide details of who has already been consulted and who needs to be

consulted. Consider stakeholders:

Whose input is required to complete the project eg PICT, Estates

Who will be affected by the completion of the project

Who will be expected to contribute towards the cost of the project eg the other House

Risks and ACHIEVABLILTY In this section you need to

outline the key risks to the project and assess their impact on the success of the

project

detail how they will be managed and what contingency plans are in place.

OPTIONS You need to provide details of all the options being considered – there should be at least

three of which is a ‘do nothing’ or ‘do minimum’ option. See the OPTION

ASSESSMENT section in the main guidance for further information.

For each provide details of:

the proposed option

its strengths and weakness

a summary of its costs

any additional risks or benefits specific to that option.

Financial appraisals should be attached as annexes to the business case.

FINANICAL CONSIDERATION (affordability) Provide CLEAR details of

the total cost of the preferred option – refer to the details in the annex

how it will be funded. If existing budgets/programme budgets are being used please

state this clearly.

What other resources are needed and when

A summary of any sensitivity analysis undertaken (for projects over [£500,000])

PrOject PLan and Timescale Provide details of the proposed timescale for the project:

the proposed milestones

key deliverables

details of the delivery arrangements eg procurement procedures that will need to be

completed.

CONCLUSION AND RECOMMENDATIONS

Management in Confidence MB2009.P.70

6

ANNEXES

Management in Confidence MB2009.P.70

7

Standard Data

1 Authorisation limits

2 VAT – accounts codes where VAT is recoverable (separate document)

3 Discounted cash flows rates

4 HoC – Risk Measurement

Management in Confidence MB2009.P.70

8

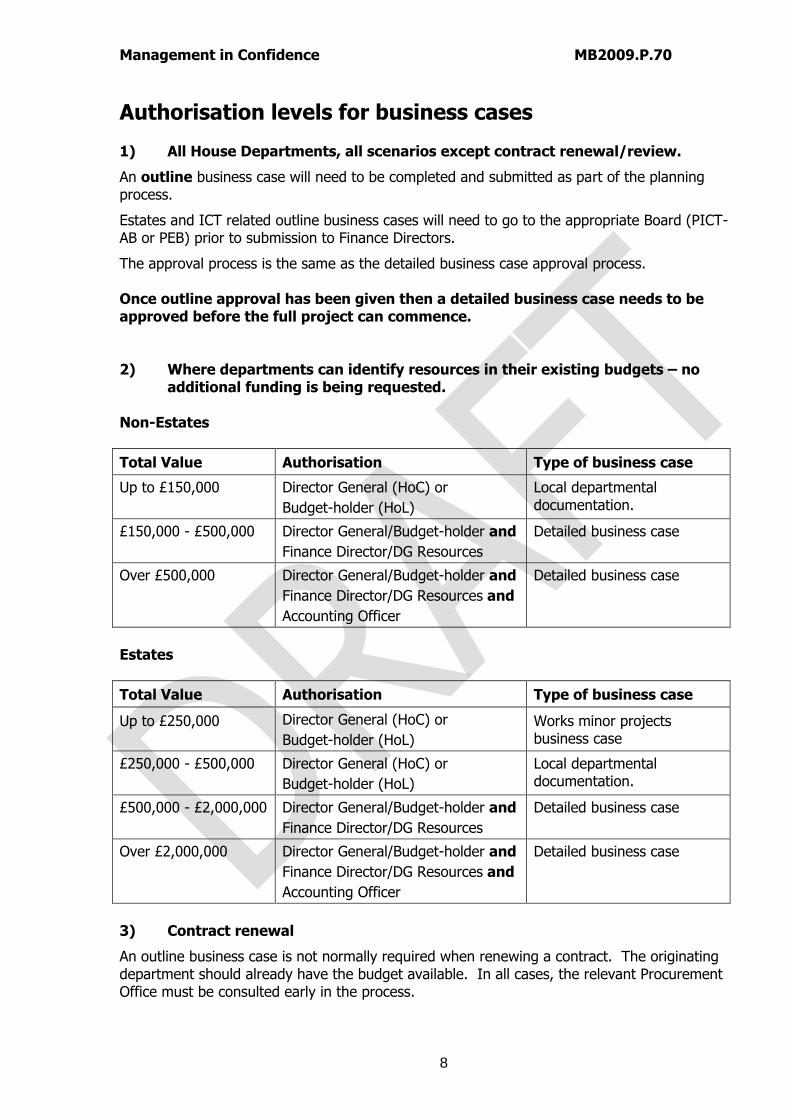

Authorisation levels for business cases 1) All House Departments, all scenarios except contract renewal/review.

An outline business case will need to be completed and submitted as part of the planning process.

Estates and ICT related outline business cases will need to go to the appropriate Board (PICT-AB or PEB) prior to submission to Finance Directors.

The approval process is the same as the detailed business case approval process. Once outline approval has been given then a detailed business case needs to be approved before the full project can commence. 2) Where departments can identify resources in their existing budgets – no

additional funding is being requested. Non-Estates

Total Value Authorisation Type of business case

Up to £150,000 Director General (HoC) or

Budget-holder (HoL)

Local departmental documentation.

£150,000 - £500,000 Director General/Budget-holder and

Finance Director/DG Resources

Detailed business case

Over £500,000 Director General/Budget-holder and

Finance Director/DG Resources and

Accounting Officer

Detailed business case

Estates

Total Value Authorisation Type of business case

Up to £250,000 Director General (HoC) or

Budget-holder (HoL)

Works minor projects business case

£250,000 - £500,000 Director General (HoC) or

Budget-holder (HoL)

Local departmental documentation.

£500,000 - £2,000,000 Director General/Budget-holder and

Finance Director/DG Resources

Detailed business case

Over £2,000,000 Director General/Budget-holder and

Finance Director/DG Resources and

Accounting Officer

Detailed business case

3) Contract renewal

An outline business case is not normally required when renewing a contract. The originating department should already have the budget available. In all cases, the relevant Procurement Office must be consulted early in the process.

Management in Confidence MB2009.P.70

9

Total Value Authorisation Type of business case

Up to £250,000 Director General (HoC) or

Budget-holder (HoL)

Procurement agreed document

£250,000 - £1,000,000 Director General/Budget-holder and

Finance Director/DG Resources

Detailed business case

Over £1,000,000 Director General/Budget-holder and

Finance Director/DG Resources and

Accounting Officer

Detailed business case

4) Where additional funding is requested.

Once outline approval has been given then a detailed business case needs to be approved before authority to incurred expenditure is given.

Total Value Authorisation Type of business case

Up to £50,000 Director General/ Budget-holder – Departments are expected to fund these projects from existing funds

Local documentation*

£50,000 - £500,000 Director General/Budget-holder and

Finance Director/DG Resources

Detailed business case

Over £500,000 Director General/Budget-holder and

Finance Director/DG Resources and

Accounting Officer

Detailed business case

5) Overspends on approved projects

Value of overspend Authorisation Type of business case

Up to 5% of approved **total costs up to a maximum of £100,000

Director General (HoC) or Budget-holder (HoL) and

Director of FMD (HoC)/Head of Finance (HoL)

Revised budget forecast – use financial appraisal document.

Over 5% of **total costs or over £100,000

Director General (HoC) or Budget-holder (HoL) and

Finance Director/DG Resources

Revised budget forecast – using financial appraisal document.

If the scheme overspends by more than £1,000,000

Director General (HoC) or Budget-holder (HoL) and

Finance Director/DG Resources and

Accounting Officer

Revised full business case

**total costs are based on the original approved business case.

Management in Confidence MB2009.P.70

10

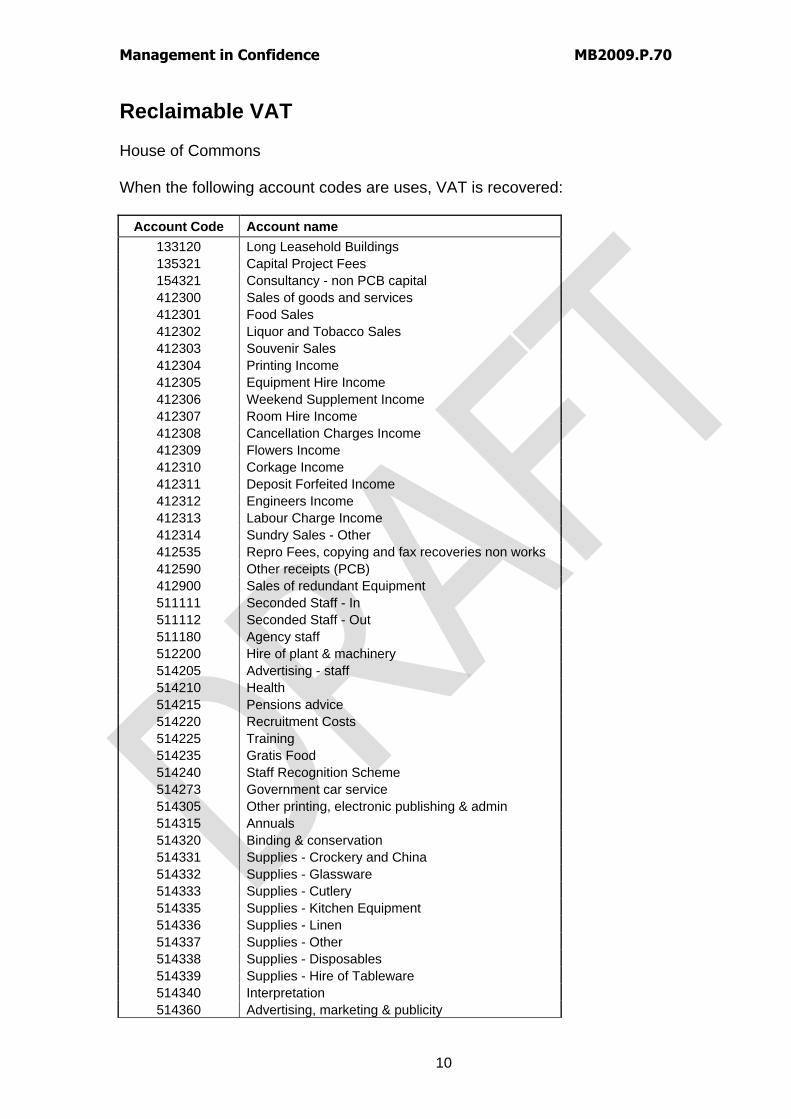

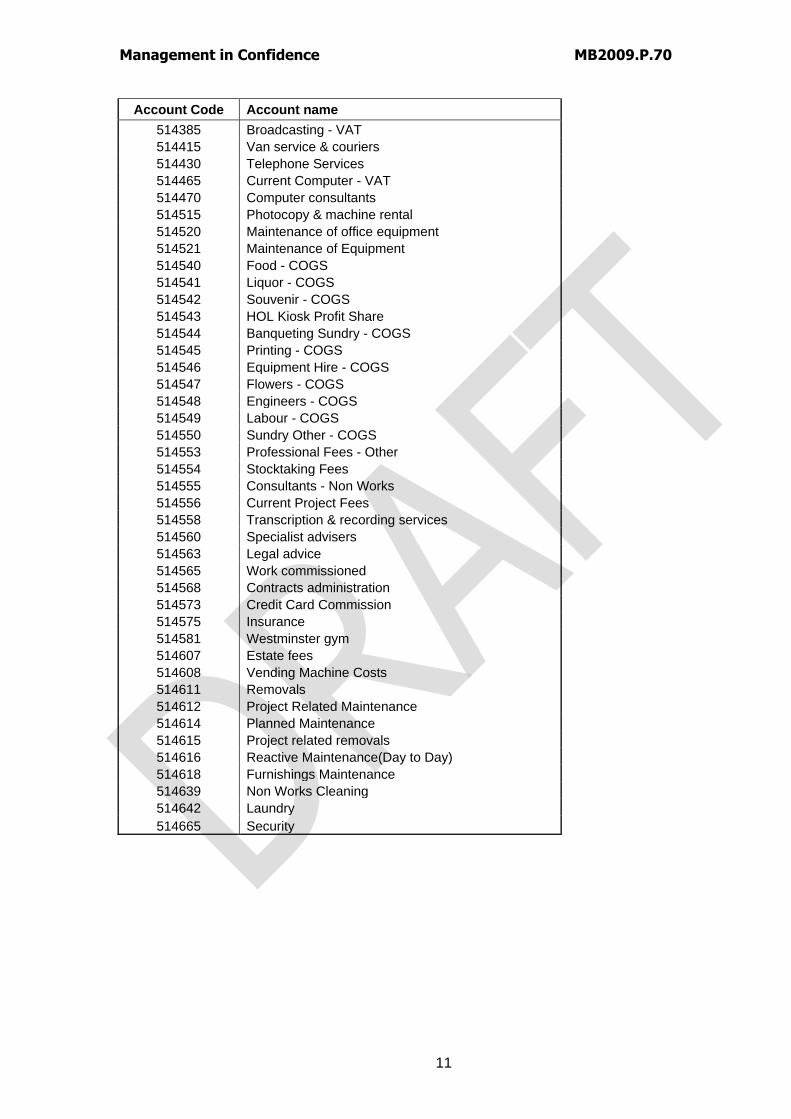

Reclaimable VAT

House of Commons When the following account codes are uses, VAT is recovered:

Account Code Account name

133120 Long Leasehold Buildings

135321 Capital Project Fees

154321 Consultancy - non PCB capital

412300 Sales of goods and services

412301 Food Sales

412302 Liquor and Tobacco Sales

412303 Souvenir Sales

412304 Printing Income

412305 Equipment Hire Income

412306 Weekend Supplement Income

412307 Room Hire Income

412308 Cancellation Charges Income

412309 Flowers Income

412310 Corkage Income

412311 Deposit Forfeited Income

412312 Engineers Income

412313 Labour Charge Income

412314 Sundry Sales - Other

412535 Repro Fees, copying and fax recoveries non works

412590 Other receipts (PCB)

412900 Sales of redundant Equipment

511111 Seconded Staff - In

511112 Seconded Staff - Out

511180 Agency staff

512200 Hire of plant & machinery

514205 Advertising - staff

514210 Health

514215 Pensions advice

514220 Recruitment Costs

514225 Training

514235 Gratis Food

514240 Staff Recognition Scheme

514273 Government car service

514305 Other printing, electronic publishing & admin

514315 Annuals

514320 Binding & conservation

514331 Supplies - Crockery and China

514332 Supplies - Glassware

514333 Supplies - Cutlery

514335 Supplies - Kitchen Equipment

514336 Supplies - Linen

514337 Supplies - Other

514338 Supplies - Disposables

514339 Supplies - Hire of Tableware

514340 Interpretation

514360 Advertising, marketing & publicity

Management in Confidence MB2009.P.70

11

Account Code Account name

514385 Broadcasting - VAT

514415 Van service & couriers

514430 Telephone Services

514465 Current Computer - VAT

514470 Computer consultants

514515 Photocopy & machine rental

514520 Maintenance of office equipment

514521 Maintenance of Equipment

514540 Food - COGS

514541 Liquor - COGS

514542 Souvenir - COGS

514543 HOL Kiosk Profit Share

514544 Banqueting Sundry - COGS

514545 Printing - COGS

514546 Equipment Hire - COGS

514547 Flowers - COGS

514548 Engineers - COGS

514549 Labour - COGS

514550 Sundry Other - COGS

514553 Professional Fees - Other

514554 Stocktaking Fees

514555 Consultants - Non Works

514556 Current Project Fees

514558 Transcription & recording services

514560 Specialist advisers

514563 Legal advice

514565 Work commissioned

514568 Contracts administration

514573 Credit Card Commission

514575 Insurance

514581 Westminster gym

514607 Estate fees

514608 Vending Machine Costs

514611 Removals

514612 Project Related Maintenance

514614 Planned Maintenance

514615 Project related removals

514616 Reactive Maintenance(Day to Day)

514618 Furnishings Maintenance

514639 Non Works Cleaning

514642 Laundry

514665 Security

Management in Confidence MB2009.P.70

12

Discount factors HM Treasury set the cost of capital for the public sector. This factor is used to adjust future cash flows to current day values. At present the discount factor is 3.5% so the cash flow for each year needs to be multiplied by the following amounts:

Year Multiple

0 1.0000

1 0.9662

2 0.9335

3 0.9019

4 0.8714

5 0.8420

6 0.8135

7 0.7860

8 0.7594

9 0.7337

10 0.7089

11 0.6849

12 0.6618

13 0.6394

14 0.6178

15 0.5969

16 0.5767

17 0.5572

18 0.5384

19 0.5202

20 0.5026

21 0.4856

22 0.4692

23 0.4533

24 0.4380

25 0.4231

Management in Confidence MB2009.P.70

13

Risk Measurement

Risk Measurement You need to assess risk using a combination of:

the probability or likelihood of the risk occurring; and

the impact it will have if its does occur. To make comparisons between risks possible, a scoring system is used. We use the 5x5 matrix which uses scores of between one and five, with one being low and five being high, so Probability - A risk which is unlikely to occur would score one; conversely a risk that is likely to occur (expected) would be a five. Impact – If the risk occurs but it does not have a significant impact on achieving the project goals then it will score one; conversely a risk that will have a significant, detrimental effect on achieving the project goals will score five. When each risk has been assessed in terms of probability and impact, you will need to calculate the „score‟ which is derived from multiplying the two criteria PROBABILITY x IMPACT These scores will give you an indication of whether the risk is tolerable or whether you need to take additional action to reduce the risk. It may help to use a risk log:

Risk ref Description Impact Probability Mitigation Owner

Management in Confidence MB2009.P.70

14

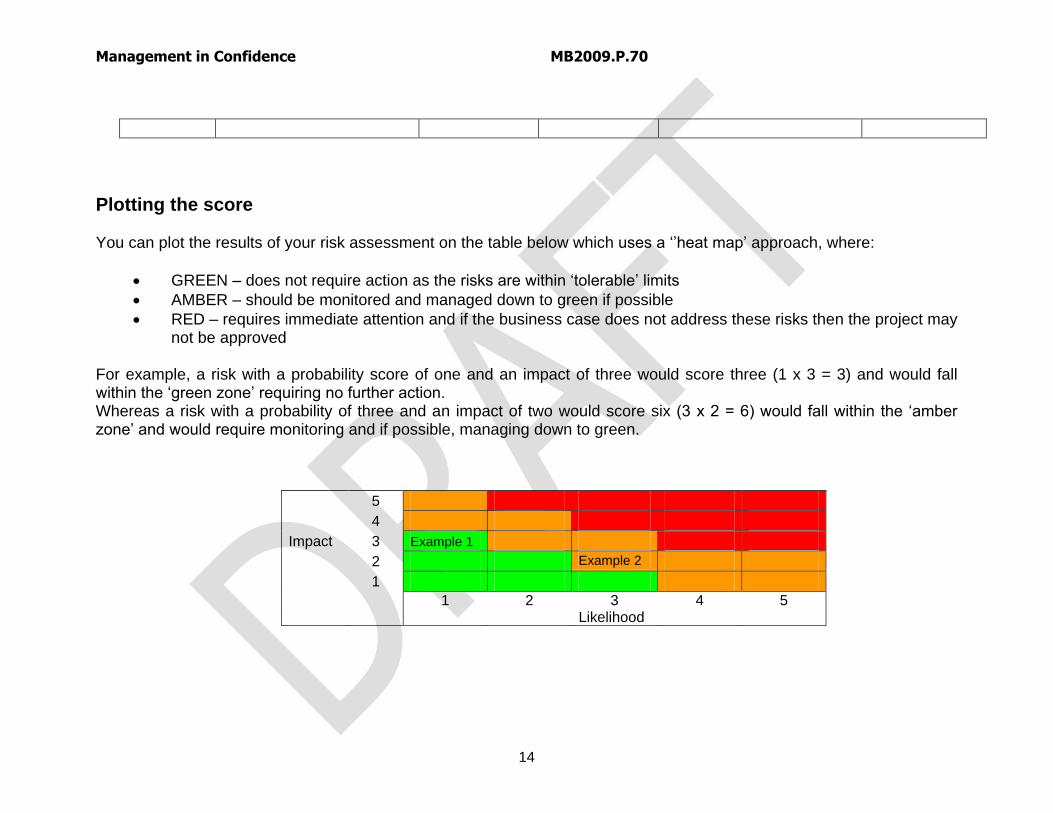

Plotting the score You can plot the results of your risk assessment on the table below which uses a „‟heat map‟ approach, where:

GREEN – does not require action as the risks are within „tolerable‟ limits

AMBER – should be monitored and managed down to green if possible

RED – requires immediate attention and if the business case does not address these risks then the project may not be approved

For example, a risk with a probability score of one and an impact of three would score three (1 x 3 = 3) and would fall within the „green zone‟ requiring no further action. Whereas a risk with a probability of three and an impact of two would score six (3 x 2 = 6) would fall within the „amber zone‟ and would require monitoring and if possible, managing down to green.

5

4

Impact 3 Example 1

2 Example 2

1

1 2 3 4 5 Likelihood

Related Documents