Vola t ility Management of Equity Base d Ins ur ance Guarantees 2 9 th C B O E R i s k Management C o nf erence S tep hen Stone, FS A , C F A , FRM S VP, A IG L i fe a nd Re ti r ement Mar c h 5, 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 1/11

Volatility Management of EquityBased Insurance Guarantees

29 th CBOE Risk Management Conference

Stephen Stone, FSA, CFA, FRMSVP, AIG Life and Retirement

March 5, 2013

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 2/11

1

• Introduction to Equity Based Insurance Guaranteeso VA GM LBs: GMAB, GMWB, and GMIBo Index Annuities or Universal Life

• New VA GMLB embedded risk product designs:o Classic approacheso Recent direc tionso Current and Future direc tions

• How insurance companies manage volatility risko Vega profile of VA GMLBso Gamma

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 3/11

2

• VA is a Variable A nnuityo VA is an insurance product and a sec urityo Basket of mutual funds wrapped with insurance (life-contingent) guaranteeso Minimum guarantee is an annuitization rate for the Account Value (AV)o Insurance companies started competing with equity guarantees, first death and then living benefits

• GMWB, a Guaranteed Minimum Withdrawal Benefit, is the most popularo Series of lifetime income payments that are guaranteedo Income is funded from the AV until it is exhausted , then the insurer incurs a c laimso

Claim is equivalent to issuing an Immediate Life Annuityo Charges for the guarantee are deduc ted from the AVo Strike struc ture determined by the “Benefit Base” and the “Withdrawal Rate”

• The Embedded Derivativeo A type of “quanto-asian” put optiono Under certain restrictive c ond itions PDEs exist that can be solved to value a G MWBo Realistic situation adds rainbow, down-and-in barrier effec ts, and lookback effec tso Under realistic condition one needs to monte carlo

• Page 3: Example of a single path

• Page 4: Example of average over a full monte carlo simulation

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 4/11

3

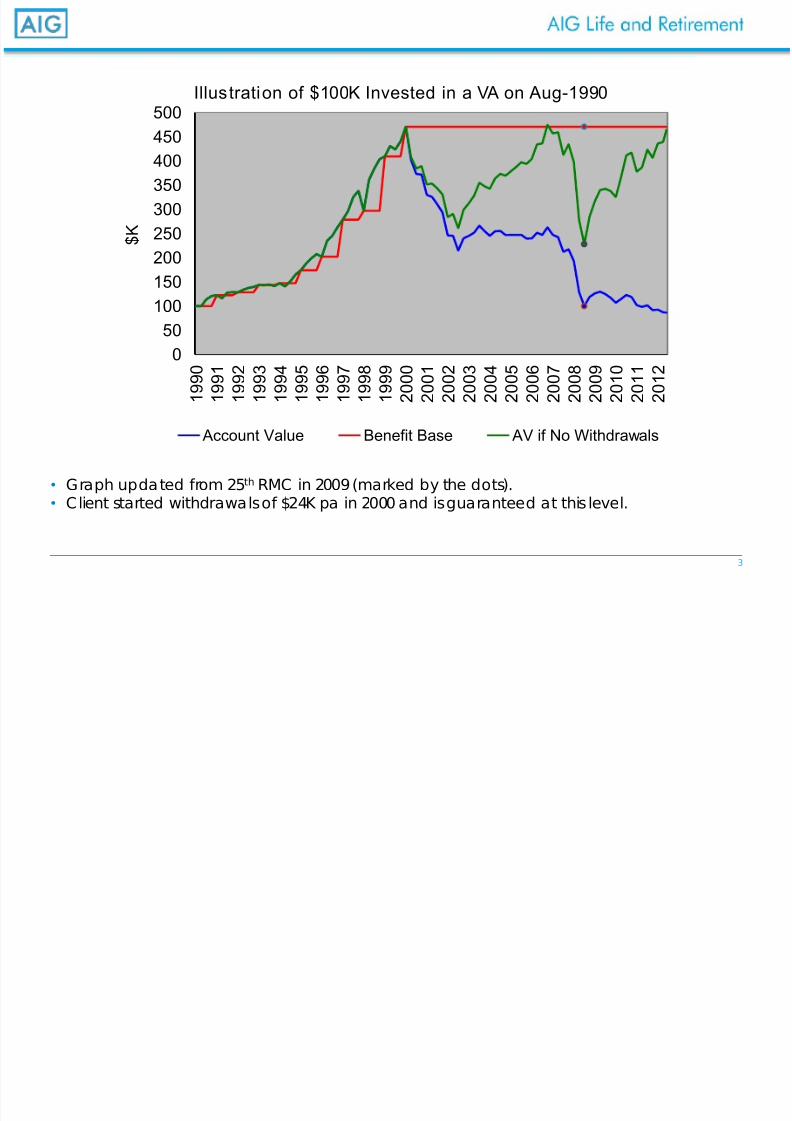

• Graph upda ted from 25 th RMC in 2009 (marked by the dots).• Client started withdrawals of $24K pa in 2000 and is guaranteed at this level.

050

100150200250300350400450

500

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

$ K

Illustration of $100K Invested in a VA on Aug-1990

Account Value Benefit Base AV if No Withdrawals

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 5/11

4

• Slide was presented at the 25 th RMC in 2009• Though a long-tailed contract due to the life annuity component, that does not result in 60

years of vega exposure

Expected Cash Flows fo r $100K of a GMWB Issu ed to a 55 year old

-3,000

-2,500

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

0 5 10 15 20 25 30 35 40 45 50 55 60

Years from Issue

Expected Fees Collected Expected Claims Paid Total Expected Cash Flow

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 6/11

5

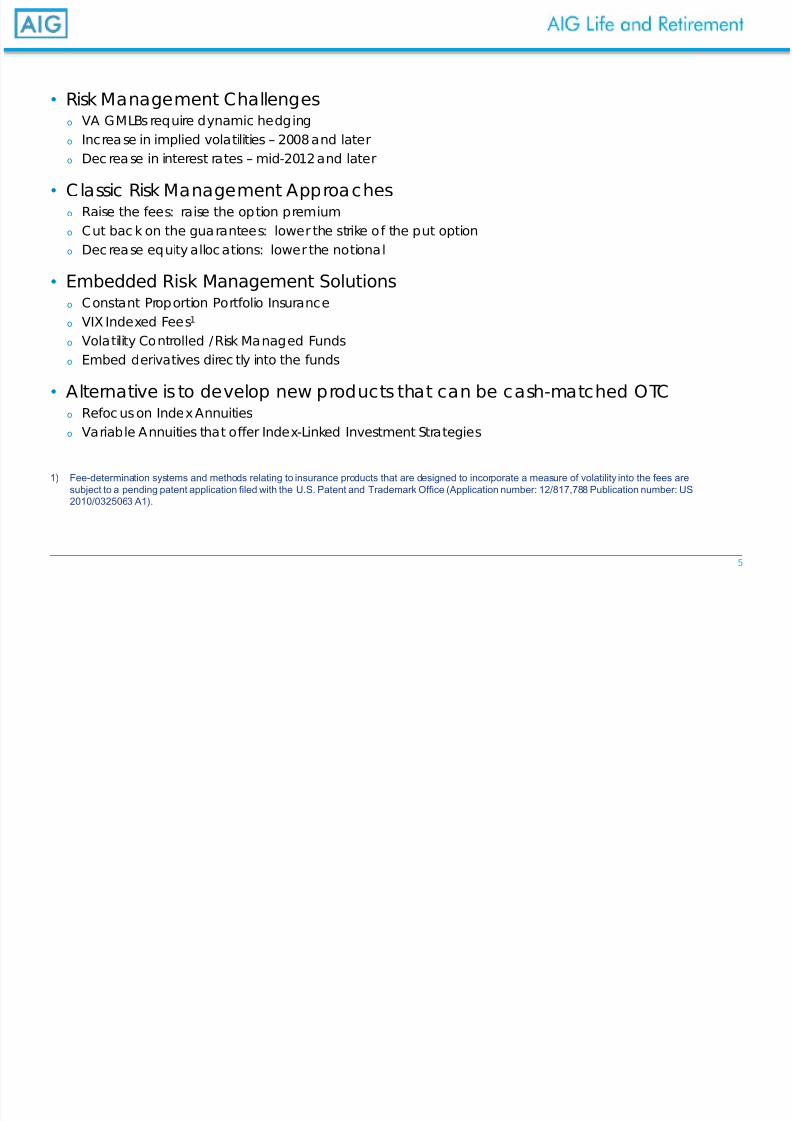

• Risk Management Challengeso VA GMLBs require dynamic hedgingo Increa se in implied volatilities – 2008 and latero Dec rea se in interest rates – mid-2012 and later

• Classic Risk Management Approacheso Raise the fees: raise the option premiumo Cut bac k on the gua rantees: lower the strike of the put optiono Dec rease equity alloc ations: lower the notiona l

• Embedded Risk Management Solutionso Constant Proportion Portfolio Insuranceo VIX Indexed Fees 1

o Volatility Controlled /Risk Managed Fundso Embed derivatives direc tly into the funds

• Alternative is to develop new products that can be cash-matched OTCo Refoc us on Index Annuitieso Variable Annuities that offer Index-Linked Investment Strategies

1) Fee-determination systems and methods relating to insurance products that are designed to incorporate a measure of volatility into the fees aresubject to a pending patent application filed with the U.S. Patent and Trademark Office (Application number: 12/817,788 Publication number: US2010/0325063 A1).

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 7/11

6

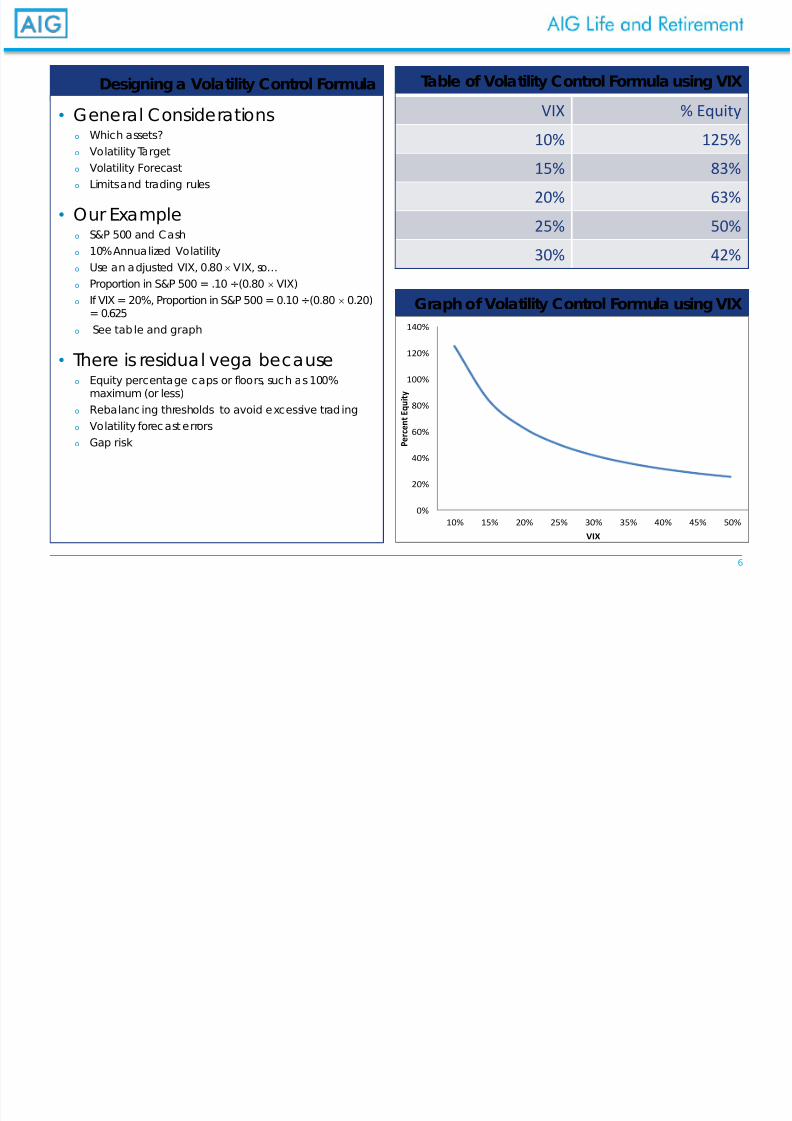

Designing a Volatility Control Formula

1-YearFixed Account*

*Minimum guaranteedinterest rate of 1%; renewsannually

A Choice ofRequired Asset

Allocation Models

Models (fund offunds) contain adiversified mix ofprofessionallymanaged investmentportfolios

All models have avolatility controlfunction that reduceequity exposure inresponse to marketvolatility

20% 80%

• General Considerationso Which assets?o Volatility Targeto Volatility Forecasto Limits and trading rules

• Our Exampleo S&P 500 and Casho 10% Annua lized Volatilityo Use an adjusted VIX, 0.80 × VIX, so…o Proportion in S&P 500 = .10 ÷(0.80 × VIX)o If VIX = 20%, Proportion in S&P 500 = 0.10 ÷(0.80 × 0.20)

= 0.625o See tab le and graph

• There is residual vega becauseo Equity percentage caps or floors, such as 100%

maximum (or less)o

Rebalanc ing thresholds to avoid excessive trad ingo Volatility forec ast errorso Gap risk

Graph of Volatility Control Formula using VIX

Table of Volatility Control Formula using VIX

VIX % Equity

10% 125%15% 83%

20% 63%

25% 50%

30% 42%

0%

20%

40%

60%

80%

100%

120%

140%

10% 15% 20% 25% 30% 35% 40% 45% 50%

P e r c e n t E

q u

i t y

VIX

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 8/11

7

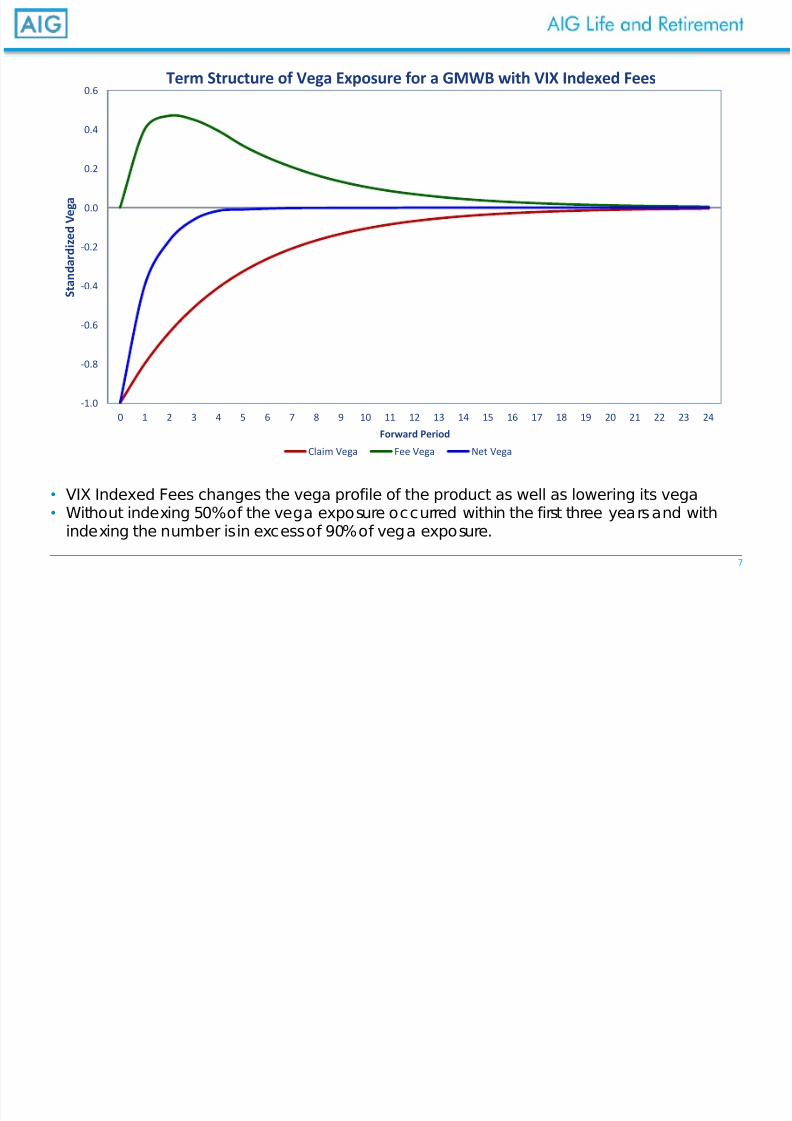

• VIX Indexed Fees changes the vega profile of the product as well as lowering its vega• Without indexing 50% of the vega exposure occurred within the first three years and with

indexing the number is in excess of 90% of vega exposure.

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

S t a n d a r d i z e d V e g a

Forward Period

Term Structure of Vega Exposure for a GMWB with VIX Indexed Fees

Claim Vega Fee Vega Net Vega

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 9/11

8

• Volatility Control Funds tend to lower the vega profile across the term structure

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

S t a n d a r d i z e d V e g a

Forward Period

Term Structure of Vega Exposure for a GMWB with VCF

Claim Vega without VCF Fee Vega Claim Vega with VCF

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 10/11

9

• GMWB without embedded risk management features would require a bout $7B of ATM puts to hedge $15Bof GMWBs, concentrated mostly in the 5 to 10 year range

• VIX Indexed Fees changes the vega profile of the product as well as lowering its vega• GMWB with VIX Indexed Fees require about $3.4B of ATM puts, mostly in years 1 to 3

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1 2 3 5 10 15 20 25 30

$ M M

Maturity of Put Option

Notional Amount of SPX Puts to Hedge $15B of GMWB

GMWB without Risk Control GMWB with VCF GMWB with Indexed Fees

8/12/2019 Day3 Session2B Stone

http://slidepdf.com/reader/full/day3-session2b-stone 11/11

10

• Insurer Volatility Risk Management Prac ticeso Vary greatly from firm to firmo Prior to the c risis some firms were not even hedging deltao Some products are accounted for under SOP 03-01 and don’t mark to volatility market for GAAPo Even under FAS 157 mark volatility to model after some horizon when the options market is less liquido Statutory guidance doesn’t mark to volatility market

• VIX Indexed Feeso Volatility risks (vega and gamma) of claims are the same as classic GMWBso Fees adjust so that the premium charged for the guarantee is appropriateo Variable fee adjusts in loc k-step with options prices to fund ga mma hedging

• Volatility Controlled Fundso Instead of c hanging fees to fund the c laims in a given volatility environment the c laims are c hangedo Volatility risks of c laims dramatically reduced and a lteredo Gamma can be significantly impacted as well as vega if changes in the asset mix are appropriately

considered ib the “shocks” to calculate gamma

Related Documents