Dow.com 2014 In v estor Forum Andrew N. Liveris Chairman & Chief Executive Officer November 12, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 1/30

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 2/30

Some of our comments today include statements about our expectationfuture. Those expectations involve risks and uncertainties. Dow cannot gthe accuracy of any forecasts or estimates, and we do not plan to update

forward-looking statements if our expectations change. If you would likeinformation on the risks involved in forward-looking statements, please Annual Report and our SEC filings. In addition, some of our comments renon-GAAP financial measures. Where available, presentation of and recoto the most directly comparable GAAP financial measures and other assodisclosures are provided on the Internet at www.dow.com/investors.

SEC Disclosure Rules

™Trademark of The Dow Chemical Company or an affiliated company of Dow.“EBITDA” is defined as earnings (i.e., “Net Income”) before interest, income taxes, depreciation and amortization.“Adjusted EBITDA” is defined as EBITDA excluding the impact of Certain items.“Adjusted EBITDA margin” is defined as “Adjusted EBITDA” as a percentage of reported net sales.“Adjusted EPS” is defined as earnings per share excluding the impact of Certain items.“Net Debt” equals total debt (“Notes payable” plus “Long-term debt due within one year” plus “Long-Term Debt”) minus “Cash and cash equivalents.”“Net Debt to Total Capitalization” ratio is defined as “Net Debt” divided by “Net Capital.” “Net Capital” is defined as “Total Equity” + “Redeemable Noncontrolling “Net Debt to EBITDA” is defined as “Net Debt” divided by “Adjusted EBITDA.”“TTM” is defined as trailing twelve months.“Total Capital” is defined as total assets minus non-interest bearing liabilities.“Adjusted Return on Capital” is defined as TTM “Adjusted Net Operating Profit After Tax” divided by average “Total Capital.”“Adjusted Sales” for joint ventures is defined as sales for joint ventures less sales to Dow and/or other Dow joint ventures.“Net Debt” for joint ventures excludes debt owed to Dow and/or other Dow joint ventures.“Total Shareholder Return” is defined as stock price appreciation plus dividends paid.

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 3/30

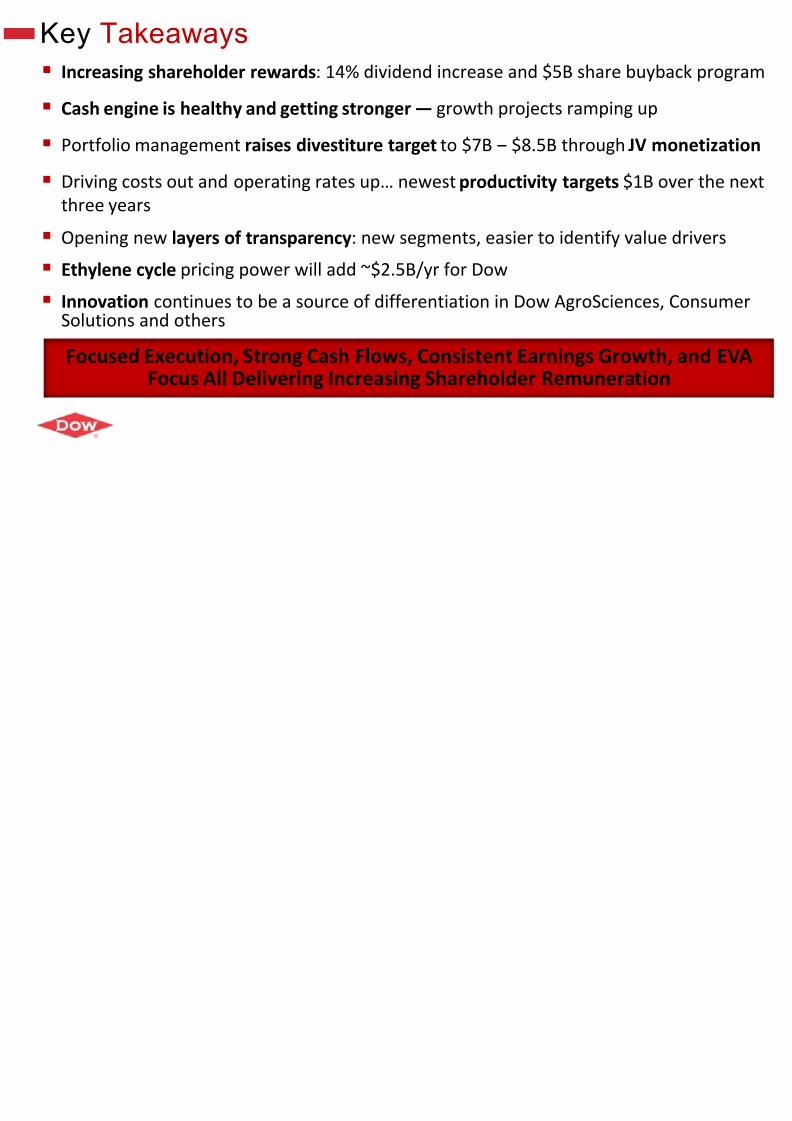

Key Takeaways

Increasing shareholder rewards: 14% dividend increase and $5B share b

Cash engine is healthy and getting stronger — growth projects ramping

Portfolio management raises divestiture target to $7B ‒ $8.5B through J

Driving costs out and operating rates up… newest productivity targets $

three years

Opening new layers of transparency: new segments, easier to identify v

Ethylene cycle pricing power will add ~$2.5B/yr for Dow

Innovation continues to be a source of differentiation in Dow AgroScienSolutions and others

Focused Execution, Strong Cash Flows, Consistent Earnings GroFocus All Delivering Increasing Shareholder Remunera

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 4/30

Our Agenda

Delivering Results Through Focused Execution

Consistent Strategy to Enhance Value, Drive R

Our Priorities Going Forward

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 5/30

0

1

2

3

4

5

6

7

8

9

10

$ B

10%

11%

12%

13%

14%

15%

16%

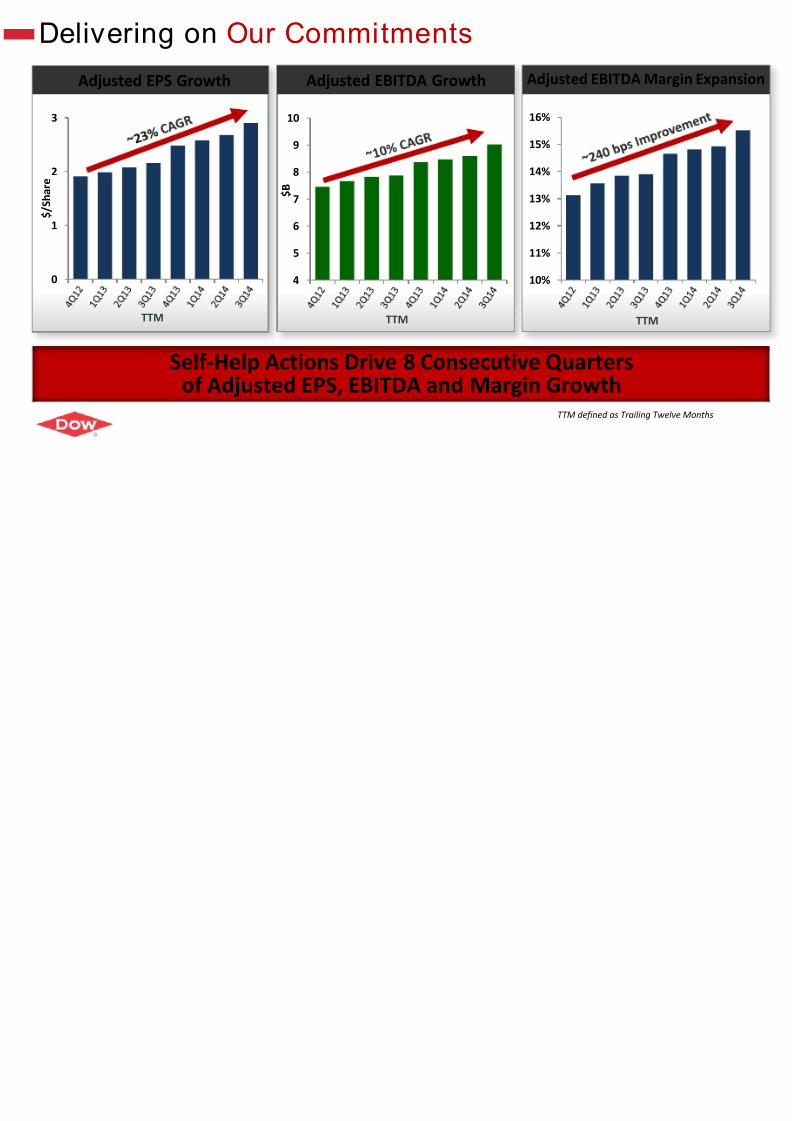

Delivering on Our Commitments

Self-Help Actions Drive 8 Consecutive Quartersof Adjusted EPS, EBITDA and Margin Growth

Adjusted EPS Growth

TTM TTM

Adjusted EBITDA Growth Adjusted EBITD

TTM defined as Tra

$ / S h a r e

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 6/30

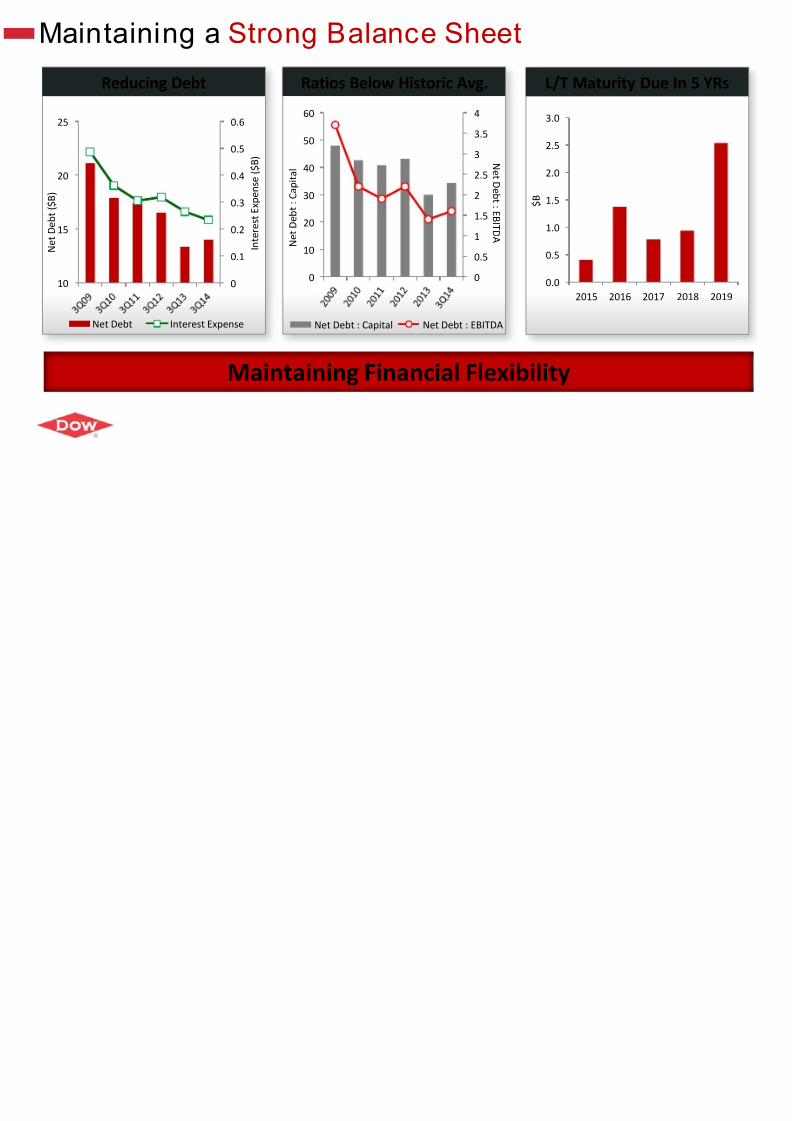

Maintaining a Strong Balance Sheet

0

0.1

0.2

0.3

0.4

0.5

0.6

10

15

20

25

I n t e r e s t E x p e n s e ( $ B )

N e t D e b t ( $ B )

Net Debt Interest Expense

Maintaining Financial Flexibility

Reducing Debt L/T MaturityRatios Below Historic Avg.

0

0.5

1

1.5

2

2.5

33.5

4

0

10

20

30

40

50

60

N e t D e b t : E B I T D A N

e t D e b t : C a p i t a l

Net Debt : Capital Net Debt : EBITDA

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2015 2016

$ B

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 7/30

5 Year

3 Year

1 Year

Dow S&P 500 S&P Chemicals

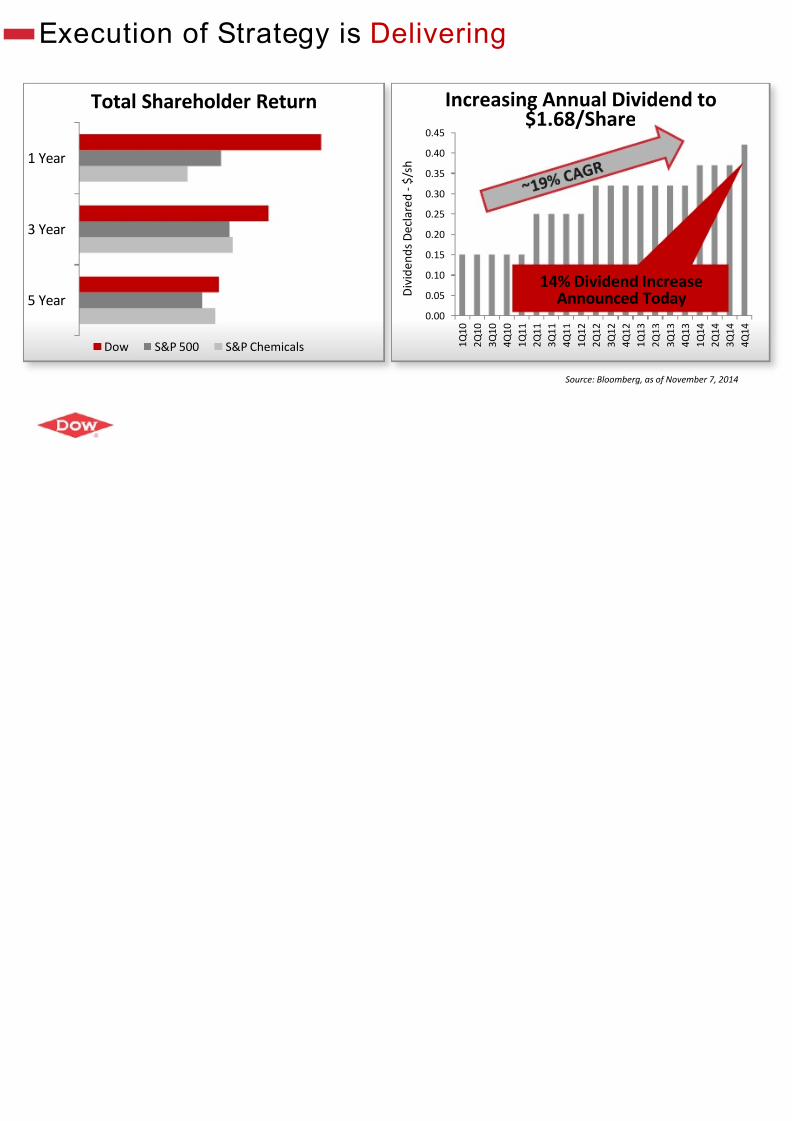

Execution of Strategy is Delivering

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

1 Q 1 0

2 Q 1 0

3 Q 1 0

4 Q 1 0

1 Q 1 1

2 Q 1 1

3 Q 1 1

4 Q 1 1

1 Q 1 2

2 Q 1 2

3 Q 1 2

4 Q 1 2

D i v i d e n d s D e c l a r e d - $ / s h

Increasing Annual Di$1.68/Share

Total Shareholder Return

14% DividenAnnounce

Source: Bloombe

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 8/30

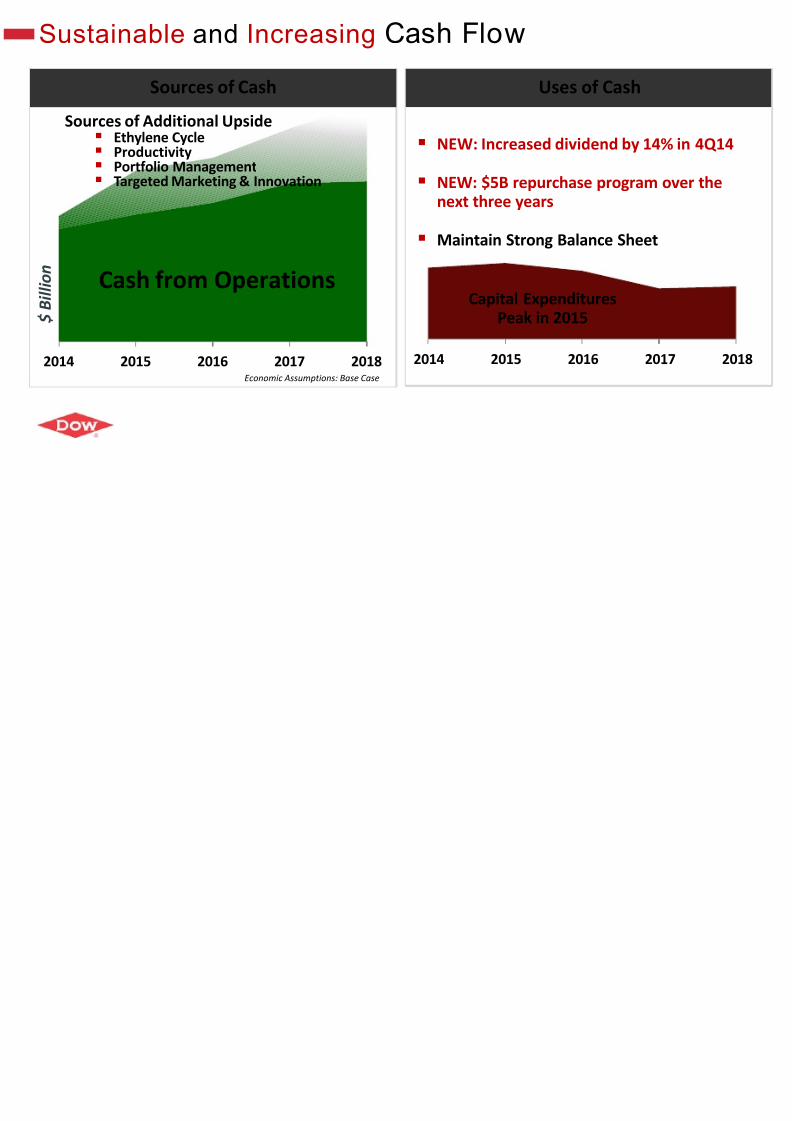

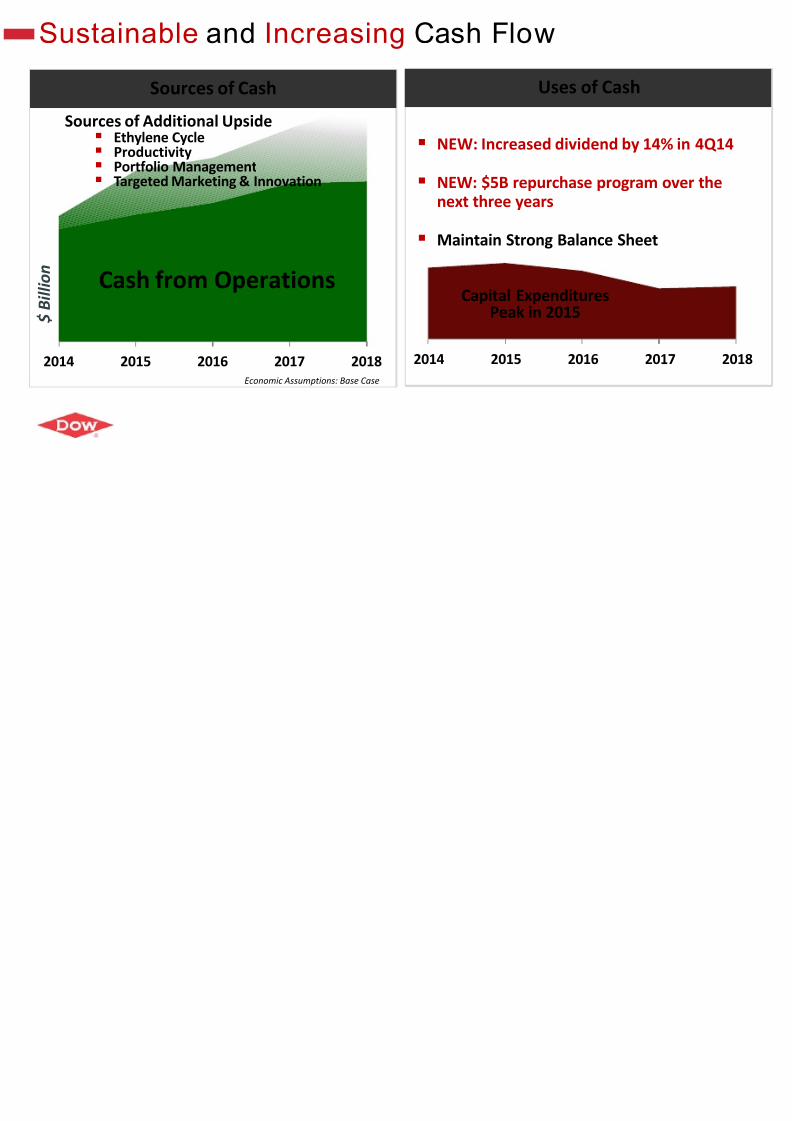

Sustainable and Increasing Cash Flow

2014 2015 2016

NEW: Increased dividend b

NEW: $5B repurchase prognext three years

Maintain Strong Balance Sh

2014 2015 2016 2017 2018

$

B i l l i o

n

Economic Assumptions: Base Case

Sources of Cash

Cash from Operations

Uses of Cas

Capital ExpendituresPeak in 2015

Sources of Additional Upside

Ethylene Cycle Productivity Portfolio Management Targeted Marketing & Innovation

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 9/30

0

1

2

3

4

5

6

78

9

10

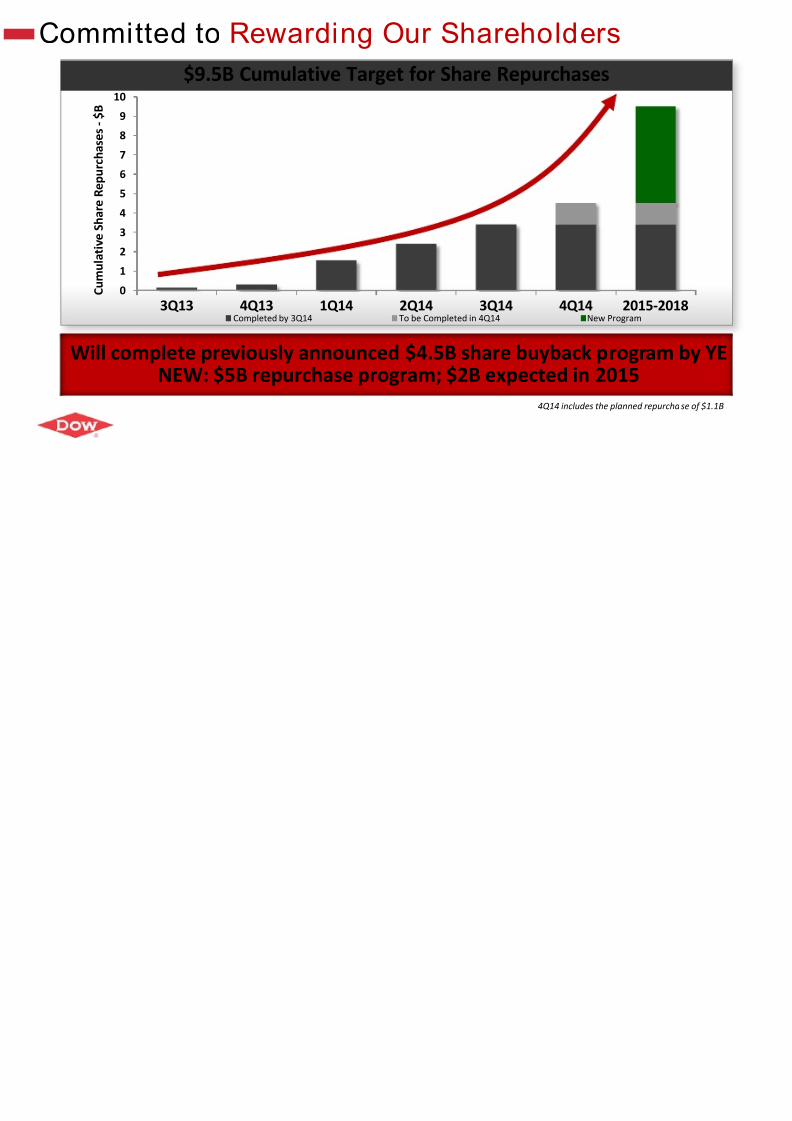

3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 2 C u m

u l a t i v e S h a r e R e p u r c h a s e

s - $ B

Completed by 3Q14 To be Completed in 4Q14 New Progr

Committed to Rewarding Our Shareholders

Will complete previously announced $4.5B share buyback progNEW: $5B repurchase program; $2B expected in 201

4Q14 includes the plann

$9.5B Cumulative Target for Share Repurchases

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 10/30

Our Agenda

Delivering Results through Focused Execution

Consistent Strategy to Enhance Value, Drive R

Our Priorities Going Forward

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 11/30

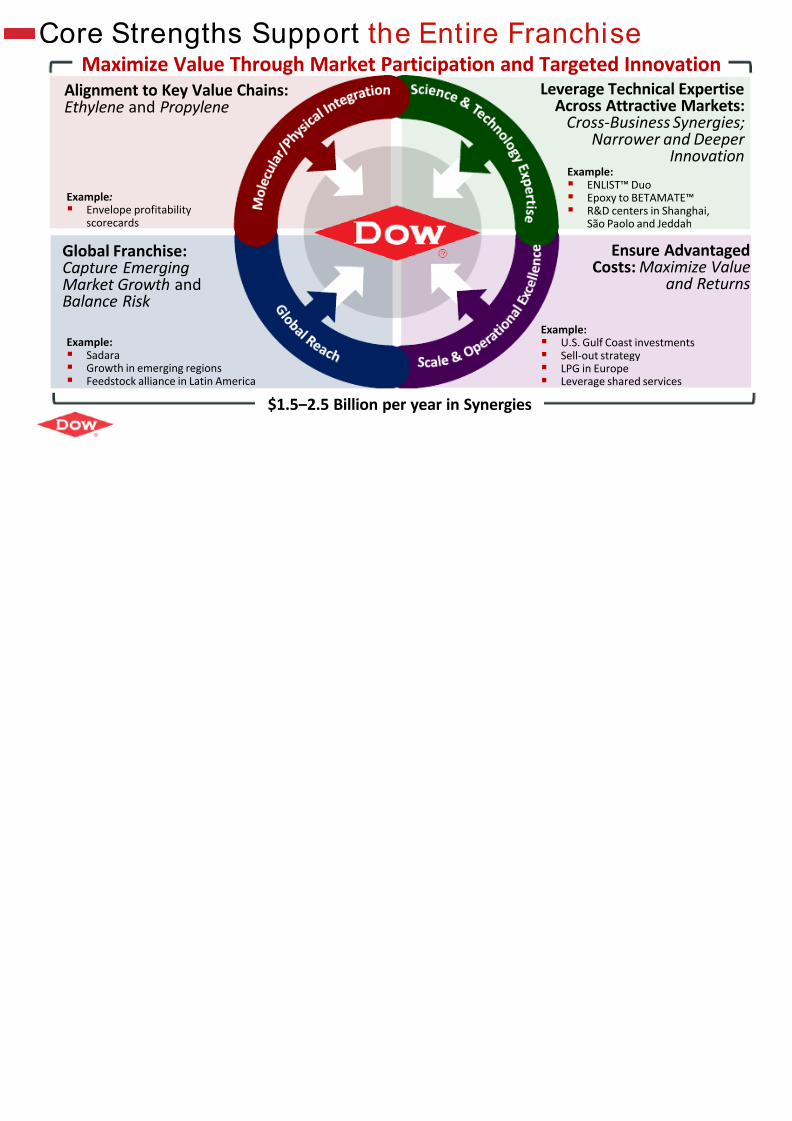

Core Strengths Support the Entire Franchise

INTEGRATION

Alignment to Key Value Chains:Ethylene and Propylene

Leverage TecAcross Attr

Cross-Bus

Narro

Global Franchise:Capture EmergingMarket Growth andBalance Risk

EnsCosts

Example: Envelope profitability

scorecards

Example: Sadara Growth in emerging regions Feedstock alliance in Latin America

Example: ENLIST™ Epoxy to R&D cent

São Paolo

Example: U.S. Gulf Coast Sell-out strate LPG in Europe Leverage share

$1.5‒2.5 Billion per year in Synergies

Maximize Value Through Market Participation and Targeted I

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 12/30

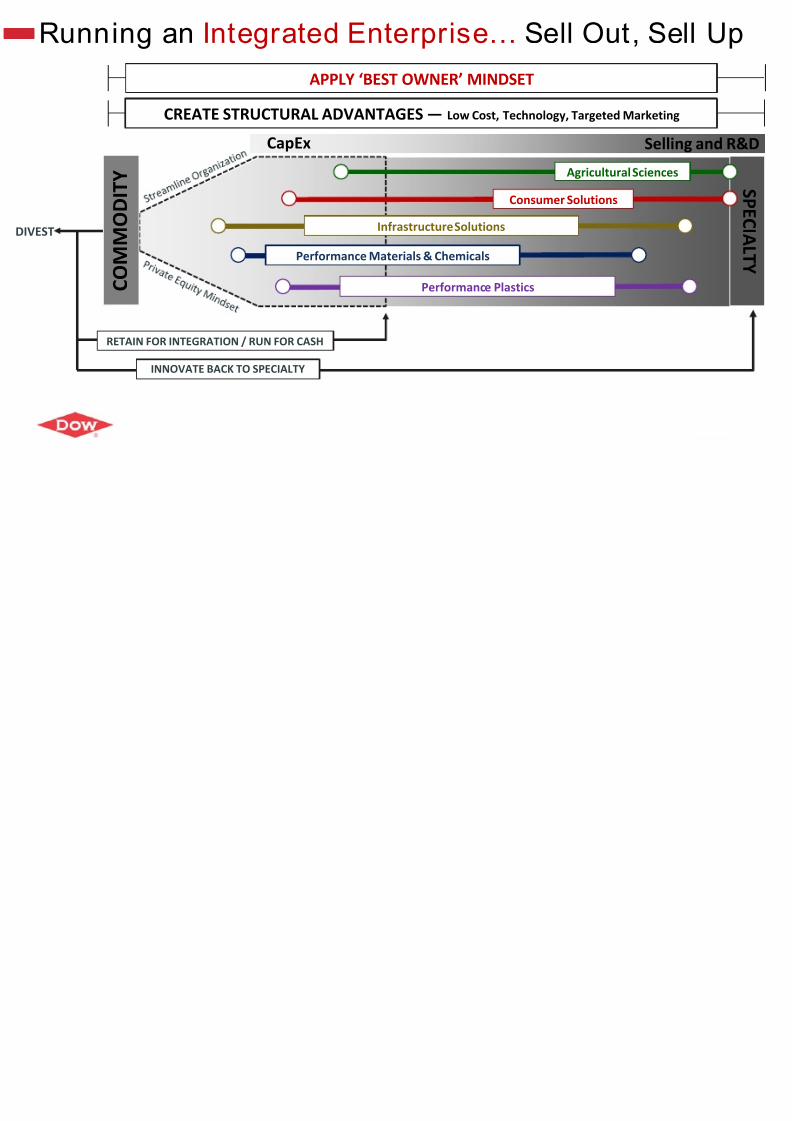

Running an Integrated Enterprise… Sell Out

DIVEST

RETAIN FOR INTEGRATION / RUN FOR CASH

CREATE STRUCTURAL ADVANTAGES — Low Cost, Technology, Targeted M

APPLY ‘BEST OWNER’ MINDSET

C O

M M O D I T Y

CapEx

Agricultural

Consumer Solutions

Infrastructure Solutions

Performance Materials & Chemicals

Performance Plastics

INNOVATE BACK TO SPECIALTY

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 13/30

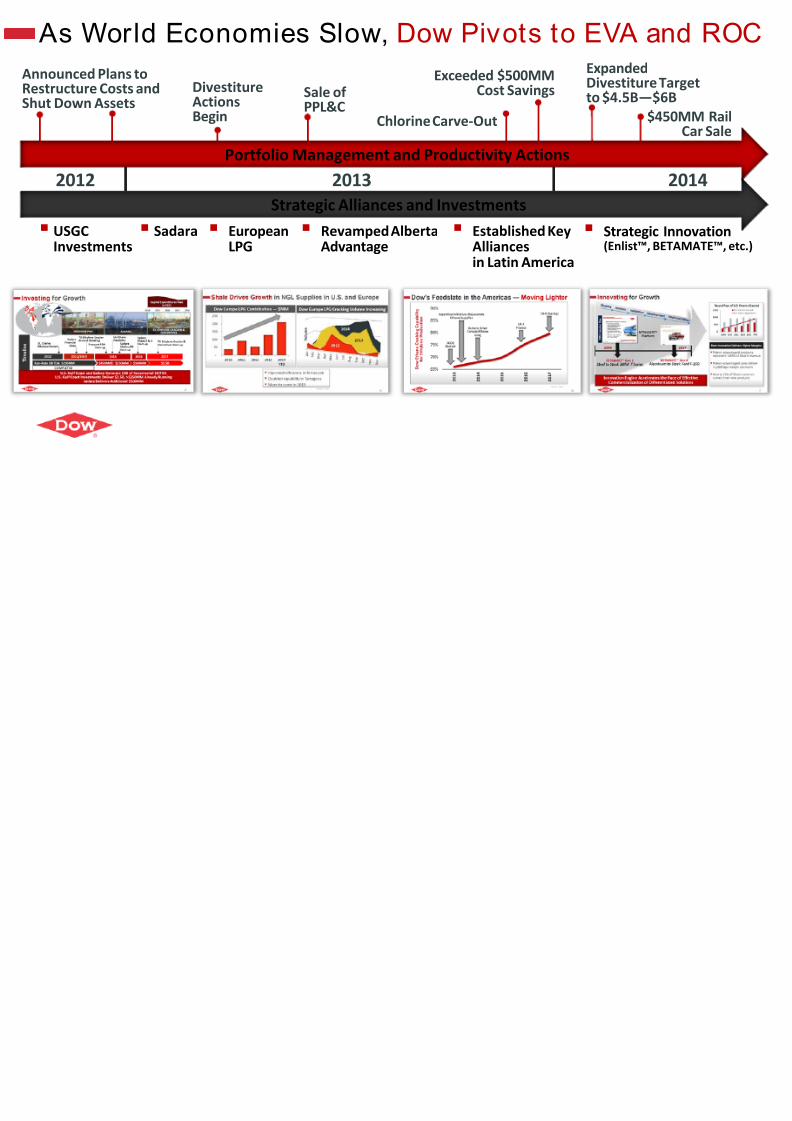

As World Economies Slow, Dow Pivots to EVA

2012 2013

Announced Plans toRestructure Costs andShut Down Assets

Chlorine Carve-Out

Exceeded $500MMCost SavingsDivestiture

ActionsBegin

ExpandDivestito $4.5

Strategic Alliances and Investments

Portfolio Management and Productivity Actions

Established KeyAlliancesin Latin America

Revamped AlbertaAdvantage

EuropeanLPG

Sadara

Sale ofPPL&C

USGCInvestments

Strat(Enlis

Portfolio Management and Productivity Actions

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 14/30

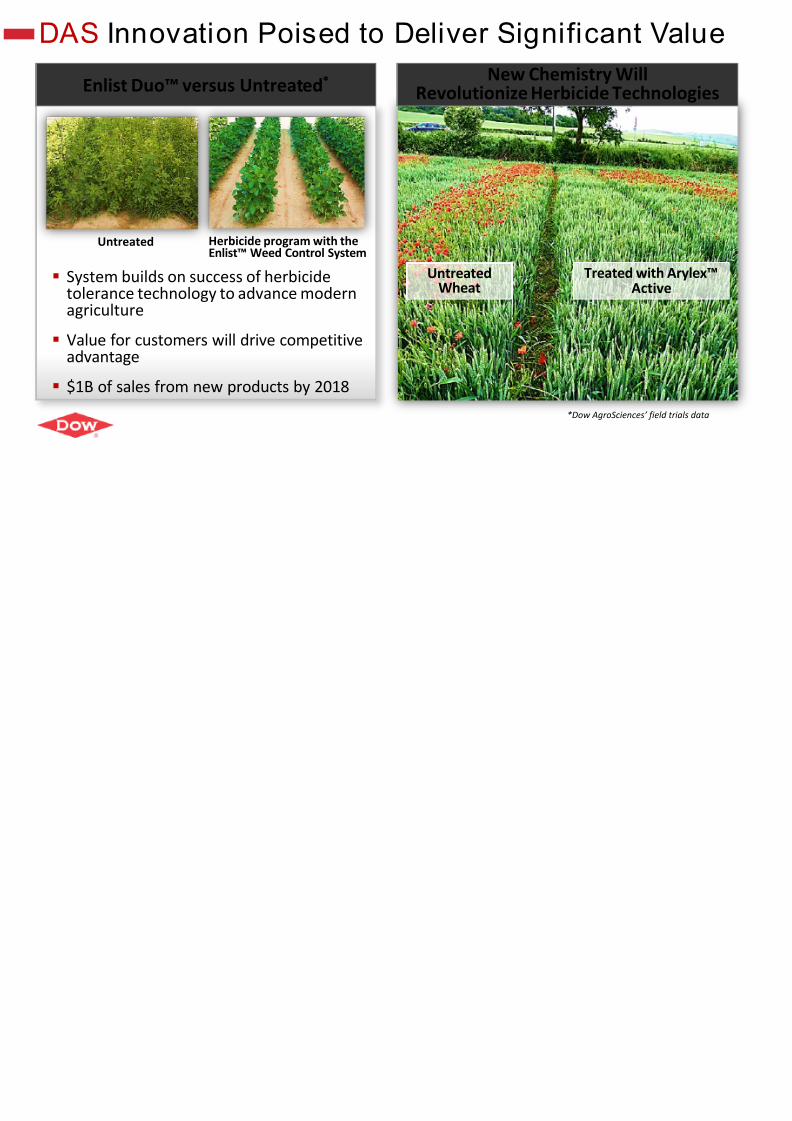

DAS Innovation Poised to Deliver Significan

UntreatedWheat

New Chemistry WRevolutionize Herbicide Te

Untreated Herbicide program with theEnlist™ Weed Control System

Enlist Duo™ versus Untreated*

Treated System builds on success of herbicidetolerance technology to advance modernagriculture

Value for customers will drive competitiveadvantage

$1B of sales from new products by 2018

*Dow AgroScien

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 15/30

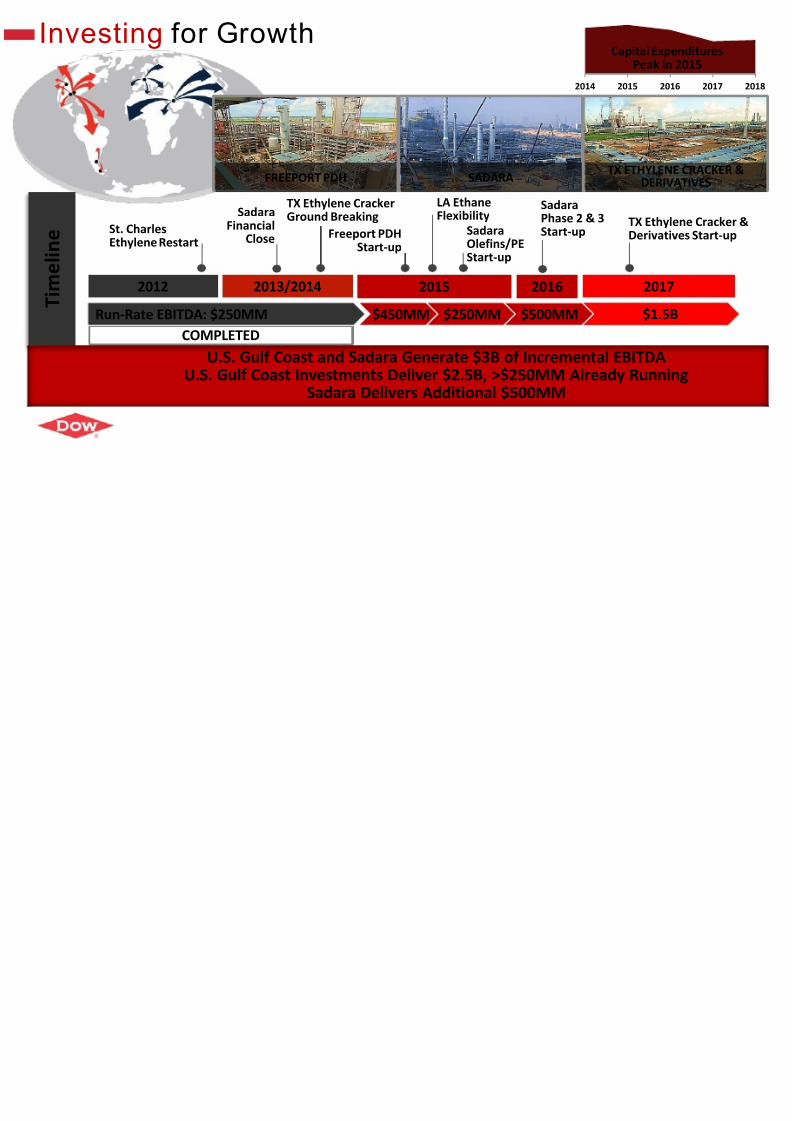

2014 201

Investing for Growth

T i m

e l i n e

COMPLETED

2012 2013/2014 2015

St. CharlesEthylene Restart

Freeport PDHStart-up

TX Ethylene CrackerGround Breaking

SadaraOlefins/PEStart-up

LA EthaneFlexibility

TD

Run-Rate EBITDA: $250MM $450MM $250MM $500MM

SadaraFinancial

Close

2016

SadaraPhase 2 & 3Start-up

SADARAFREEPORT PDHTX E

U.S. Gulf Coast and Sadara Generate $3B of Incremental EBU.S. Gulf Coast Investments Deliver $2.5B, >$250MM Already

Sadara Delivers Additional $500MM

Cap

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 16/30

Our Agenda

Delivering Results Through Focused Execution

Consistent Strategy to Enhance Value, Drive R

Our Priorities Going Forward

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 17/30

Dow Vision 2020

Optimize long-term value per share

Strategy

Vision

Integrated manufacturing positions in chemicals, plasti

and agriculture Low cost in all product and asset positions, leveraging

Presence in all growing geographic markets

Growing downstream specialties for value add to low c

Will be in some commodities to achieve low cost for ouwill run these for maximum cash to re-invest in:

1) Specialty positions (integrated Plastics)

2) Value-add specialties (Electronics & Agriculture)

3) Reward our shareholders via share buybacks and

Combination of Low-Cost and Value-Add Products EnSuperior Value Creation Throughout the Cycle

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 18/30

Our Priorities Going Forward

Maintain strong focus on rewarding shareholde

Fully capitalize on growth levers

Make further strategic choices: Go deeper andnarrower to drive the next level of long-term gr

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 19/30

Announcing New Segments Aligned to Dow’s St

Foundation of Core Strengths Support the Entire Franch Cost Advantaged Feedstocks in Every Region Scale & Operational Excellence Molecular and Physical Integration

Global Reach ― Marketing, Busines Expertise in Science & Technology Strong Brand Value

Performance Materials& ChemicalsAgricultural Sciences Consumer Solutions Infrastructure Solutions

Revenue: $14.9BAdj. EBITDA: $2.1B

Revenue: $4.6BAdj. EBITDA: $1.0B

3Q14 Trailing Twelve Months Revenue an

Chlor Alkali and Vinyl

Chlorinated Organics

Epoxy

Industrial Solutions

Polyurethanes

Crop Protection

Seeds

Consumer Care

Dow AutomotiveSystems

Dow ElectronicMaterials

Dow Building &Construction

Dow Coating Materials

Energy & WaterSolutions

Performance Monomers

Revenue: $7.2BAdj. EBITDA: $0.9B

Revenue: $8.5BAdj. EBITDA: $1.1B

G

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 20/30

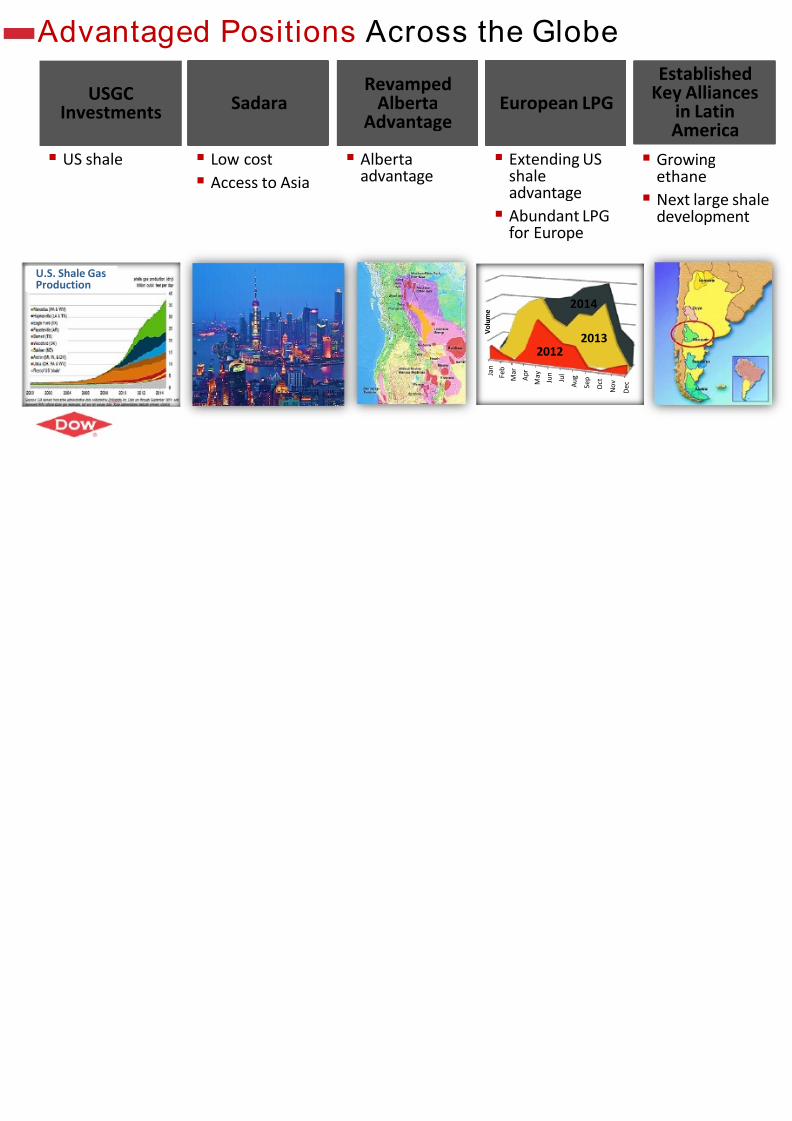

Advantaged Positions Across the Globe

USGCInvestments

US shale Low cost

Access to Asia

Albertaadvantage

Sadara European LPGRevamped

AlbertaAdvantage

Extending USshaleadvantage

Abundant LPGfor Europe

J a n

F e b

M a r

A p r

M a y

J u n

J u l

A u g

S e p

O c t

N o v

D e c

V o l u m e

20122013

2014

U.S. Shale GasProduction

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 21/30

0

5

10

15

20

25

30

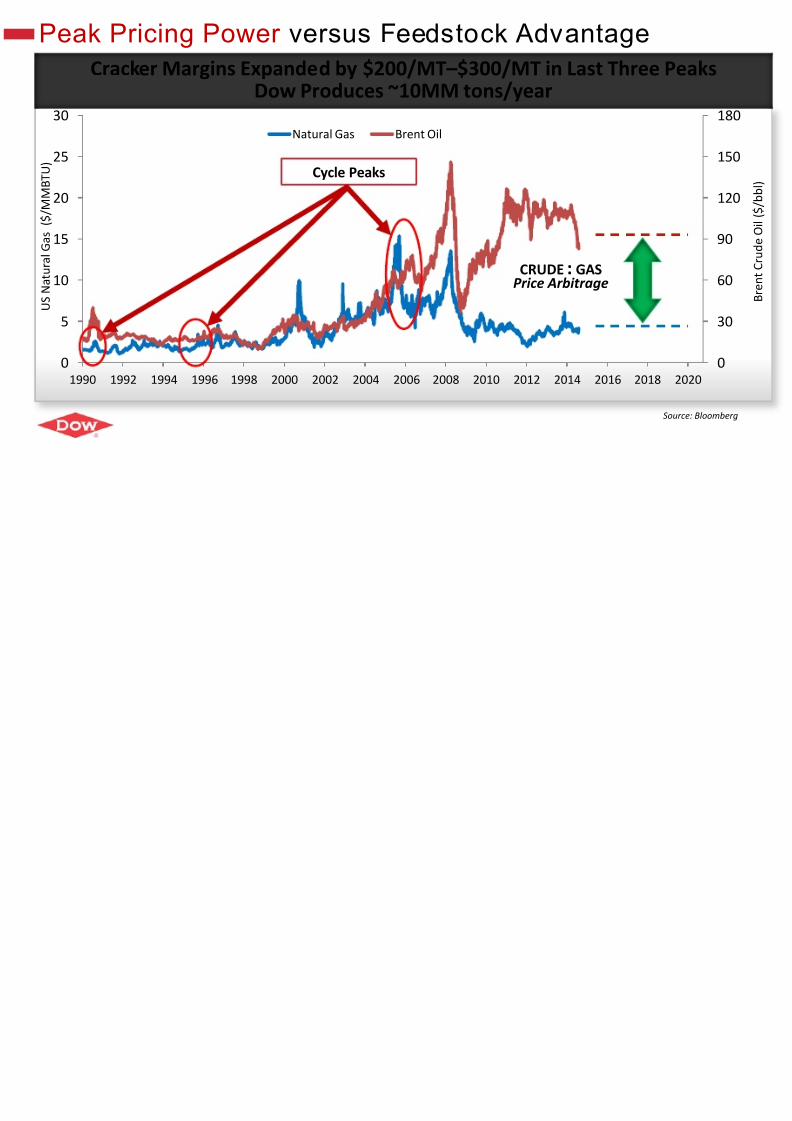

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Natural Gas Brent Oil

Peak Pricing Power versus Feedstock Advantag

Cracker Margins Expanded by $200/MT–$300/MT in Last ThDow Produces ~10MM tons/year

U S N a

t u r a l G a s ( $ / M M B T U )

CRUDE : GAS

Price Arbitrage

Cycle Peaks

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 22/30

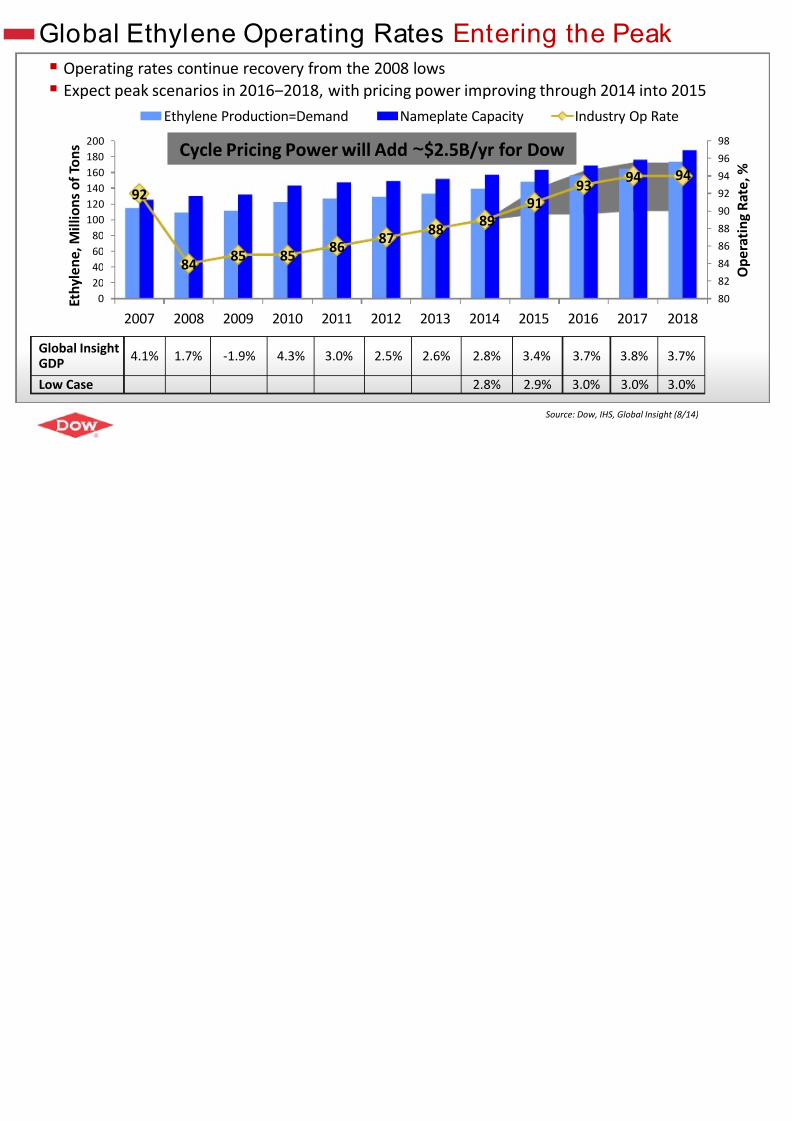

Global Ethylene Operating Rates Entering the P

Source: Dow, IHS, Glo

Operating rates continue recovery from the 2008 lows

Expect peak scenarios in 2016‒2018, with pricing power improving through 2014

92

8485 85

8687

8889

9193

9

020

40

60

80

100

120

140

160

180 200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20 E t h y

l e n e , M i l l i o n s o f T o n s

Ethylene Production=Demand Nameplate Capacity Industry

Global InsightGDP

4.1% 1.7% -1.9% 4.3% 3.0% 2.5% 2.6% 2.8% 3.4% 3.7% 3.

Low Case 2.8% 2.9% 3.0% 3.

Cycle Pricing Power will Add ~$2.5B/yr for Dow

O P i iti G i F d

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 23/30

Our Priorities Going Forward

Maintain strong focus on rewarding shareholde

Fully capitalize on growth levers

Make further strategic choices: Go deeper andnarrower to drive the next level of long-term gr

C t t P d ti it F

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 24/30

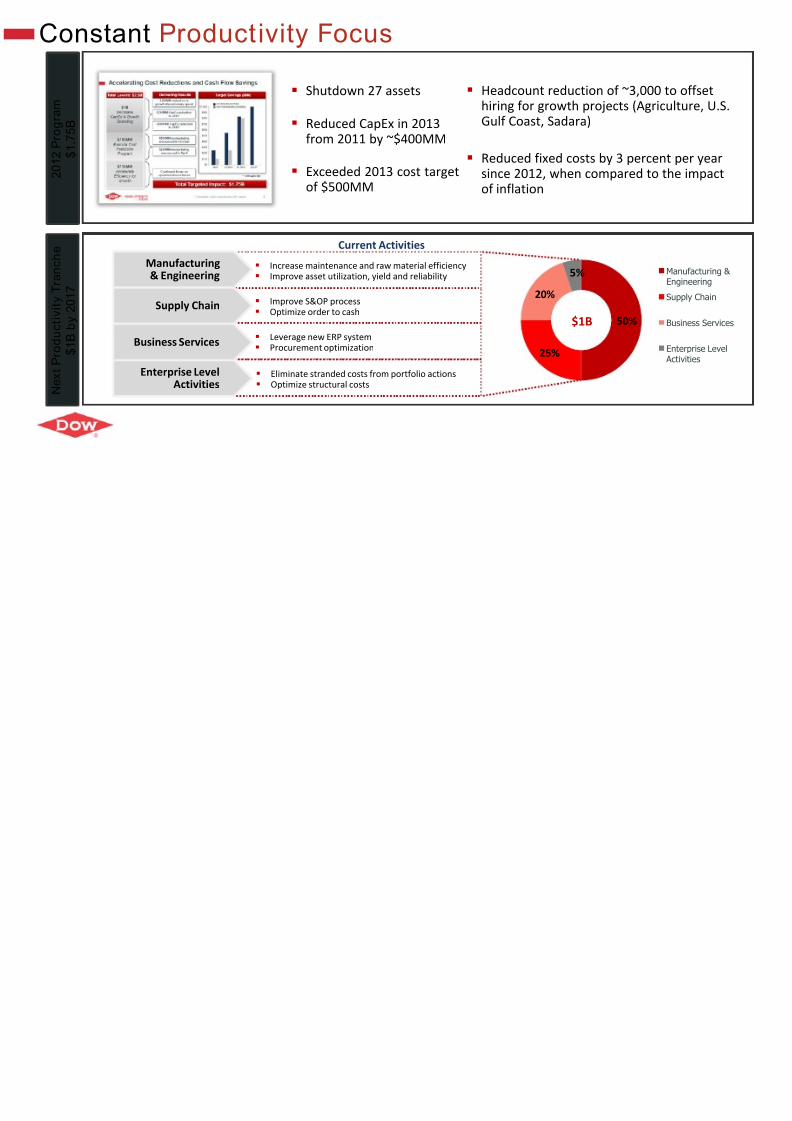

50%

25%

20%

5%

Improve S&OP process Optimize order to cash

Eliminate stranded costs from portfolio actions Optimize structural costs

Leverage new ERP system Procurement optimization

Current Activities

Manufacturing& Engineering

Supply Chain

Enterprise LevelActivities

Business Services

$1B

Increase maintenance and raw material efficiency Improve asset utilization, yield and reliability

N e x t P r o d u c t i v i t y T r a n c h e

$ 1 B

b y 2 0 1 7

Shutdown 27 assets

Reduced CapEx in 2013

from 2011 by ~$400MM

Exceeded 2013 cost targetof $500MM

2 0 1 2 P

r o g r a m

$ 1 . 7

5 B

Headcount reduction of ~hiring for growth projects Gulf Coast, Sadara)

Reduced fixed costs by 3 psince 2012, when compareof inflation

Constant Productivity Focus

J i t V t P tf l i A ti

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 25/30

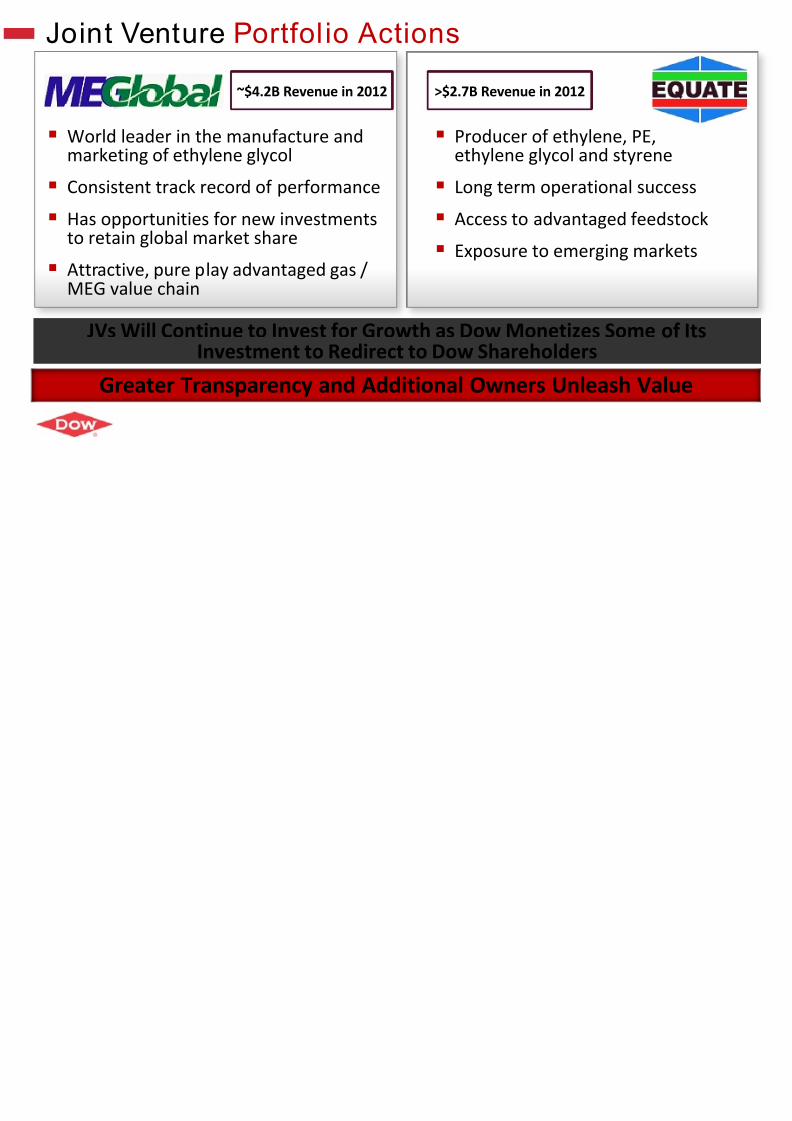

Joint Venture Portfol io Actions

World leader in the manufacture andmarketing of ethylene glycol

Consistent track record of performance

Has opportunities for new investmentsto retain global market share

Attractive, pure play advantaged gas /MEG value chain

~$4.2B Revenue in 2012

JVs Will Continue to Invest for Growth as Dow Monetizes SomInvestment to Redirect to Dow Shareholders

>$2.7B Revenue in 2012

Greater Transparency and Additional Owners Unleash

Producer of ethylene, ethylene glycol and sty

Long term operational

Access to advantaged

Exposure to emerging

O i P ti P tf li M t

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 26/30

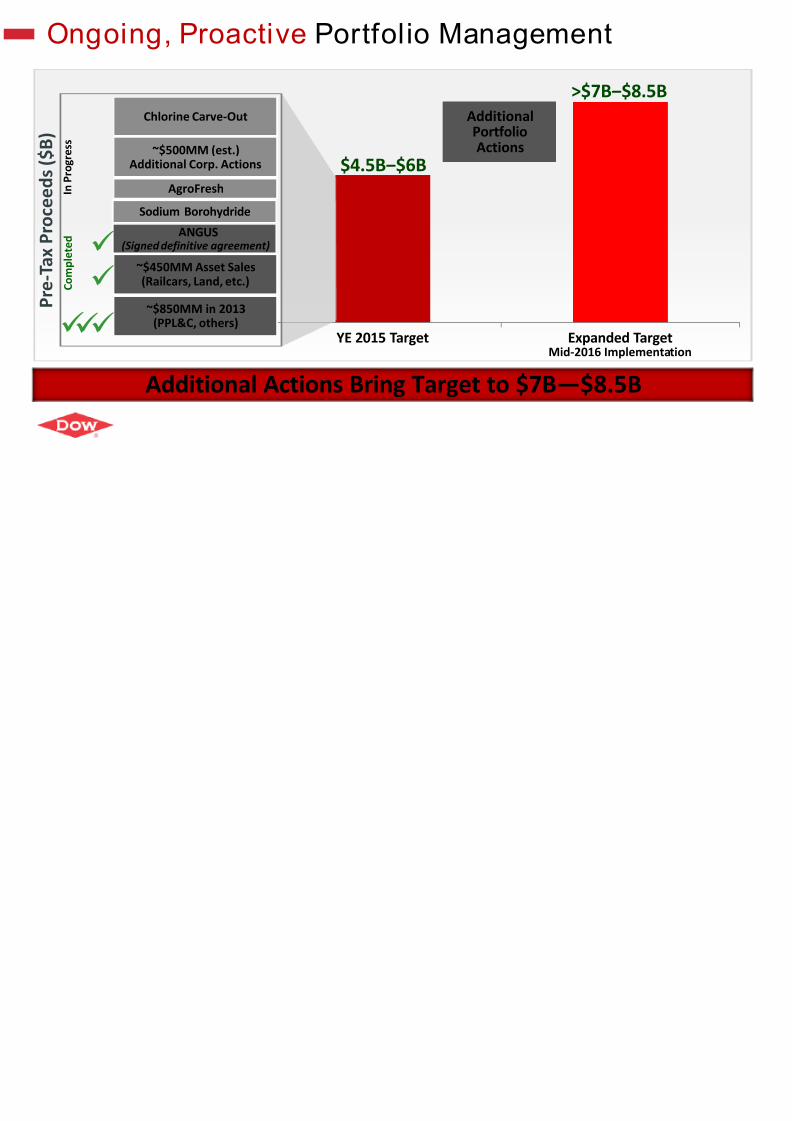

Ongoing, Proactive Portfolio Management

YE 2015 Target Expanded

~$850MM in 2013(PPL&C, others)

Chlorine Carve-Out

~$450MM Asset Sales

(Railcars, Land, etc.)

AgroFresh

~$500MM (est.)Additional Corp. Actions $4.5B‒$6B

P r e - T a x P r o c e e d s ( $ B

)

C o

m p l e t e d

I n P r o g r e s s

AdditionalPortfolio

Actions

>$7B‒$

Additional Actions Bring Target to $7B―$8.5B

Mid-2016 Imple

Sodium Borohydride

ANGUS

(Signed definitive agreement)

O r Priorities Going For ard

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 27/30

Our Priorities Going Forward

Fully capitalize on growth levers

Make further strategic choices: Go deeper and nar

drive the next level of long-term growth

Maintain strong focus on rewarding shareholders

Sustainable and Increasing Cash Flow

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 28/30

2014 2015 2016 2017 2018 2014 2015 2016

NEW: Increased dividend b

NEW: $5B repurchase prognext three years

Maintain Strong Balance Sh

$

B i l l i o n

Economic Assumptions: Base Case

Sources of Cash

Cash from Operations

Uses of Cas

Capital ExpendituresPeak in 2015

Sources of Additional Upside Ethylene Cycle

Productivity Portfolio Management Targeted Marketing & Innovation

Sustainable and Increasing Cash Flow

We Are an Integrated Chemical Company that Is Del

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 29/30

We Are an Integrated Chemical Company that Is Del

Cash and growth engines are simultaneously ramping

New projects are gearing up (USGC, Sadara, ENLIST™ launch)

The ethylene cycle is upon us — pricing power will add ~$2.5B/y

Extending our continuing dedication to Productivity ― $1B

JV optimization driving divestiture targets even higher

Fulfilling our commitments to shareholders ― 14% dividend inc$5B share buyback program

Driving to Higher Cash Flows, More Consistent EarningIncreased Shareholder Remuneration

8/10/2019 Day1 2014InvestorForum Final

http://slidepdf.com/reader/full/day1-2014investorforum-final 30/30

Related Documents