Data Service Market Inquiry Dr. Onkokame Mothobi, Senior Researcher Research ICT Africa, South Africa Competition Commission, Pretoria, 17 October 2017 Competition Commssion, South Africa Pretoria 17 th October 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Data Service Market Inquiry

Dr. Onkokame Mothobi, Senior Researcher

Research ICT Africa, South Africa

Competition Commission,

Pretoria, 17 October 2017

Competition Commssion, South Africa

Pretoria 17th October 2018

Research ICT Africa- Evidence based policy

Research ICT Africa Mobile Pricing Index (RAMP)

• Voice/ SMS basket: the cost of 30 prepaid mobile voice

calls for a total of 50 minutes, distributed between

destinations and ‘peak’ periods, added to that of 100

SMSs, and divided by the subscription value for the

period of one month.

• Data baskets: the cost of 1 GB, 500 MB and 100 MB

prepaid mobile data bundles, valid for monthly, weekly

and daily periods.

Are data prices in South Africa high?

• The cost of cheapest of 1 GB of data is used to compare prices in

South Africa with other African countries

• South Africa performs poorly in the RAMP index, coming 35th of out of

49 African countries

• The cost of cheapest 1 GB of data in South Africa is USD 8.28 (ZAR

99) seven times higher the cost of 1 GB in Egypt (USD 1.13) and

nearly three times the cost of same data in Ghana, Kenya and Nigeria

SA ’s Cheapest 1GB data Compared to Africa ’s Top

Performers

USD 1.13

USD 1.25

USD 1.49

USD 2.08

USD 2.23

USD 2.23

USD 2.28

USD 2.37

USD 2.40

USD 2.46

USD 2.68

USD 2.75

USD 2.79

USD 8.28

0 2.25 4.5 6.75 9

Egypt

Namibia

Mozambique

Tunisia

Tanzania

Guinea

Sudan

Rwanda

Brundi

Kenya

Ghana

Uganda

Nigeria

South africa

FIGURE 4: SA’S CHEAPEST PREPAID MOBILE 1GB BASKETS COMPARED TO AFRICA’S TOP PERFORMERS (USD)

Source: RAMP Index, 2018

Benchmarking SA against large African Markets

Table 1: Benchmarking South Africa against Ghana, Kenya and Nigeria

AffordabilityComparison

averageTraffic Light

Country-level

indicatorSource

Mobile prepaid 1GB

basket (USD) 2,64 8,28 RIA, 2018

Dominant operator:

mobile prepaid 1GB

basket (USD) 4,06 10,94 RIA, 2018

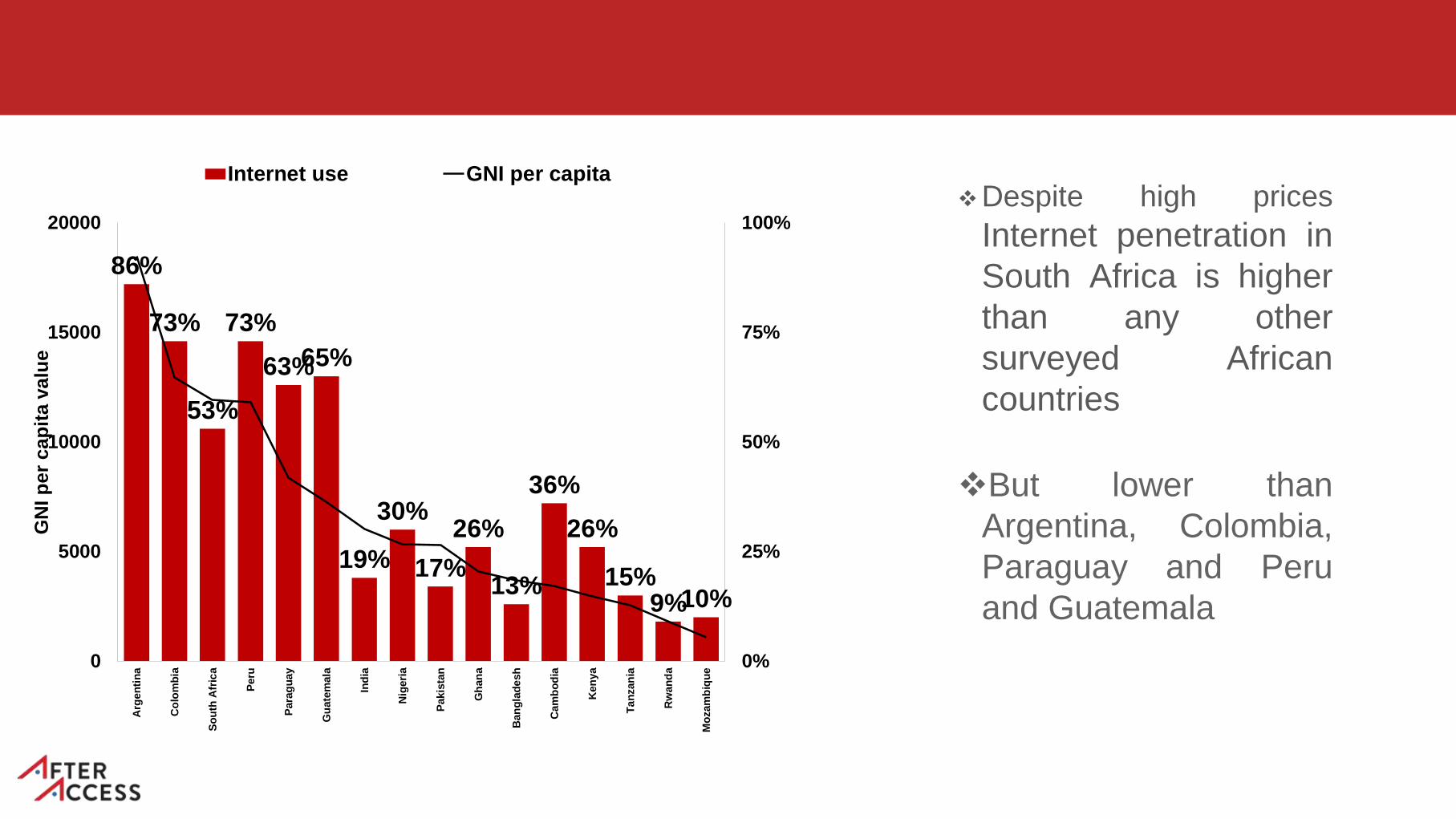

86%

73%

53%

73%

63%65%

19%

30%

17%

26%

13%

36%

26%

15%9%10%

0%

25%

50%

75%

100%

0

5000

10000

15000

20000

Arg

en

tin

a

Co

lom

bia

So

uth

Afr

ica

Peru

Para

gu

ay

Gu

ate

mala

Ind

ia

Nig

eri

a

Pakis

tan

Gh

an

a

Ban

gla

de

sh

Cam

bo

dia

Ken

ya

Ta

nzan

ia

Rw

an

da

Mo

zam

biq

ue

GN

I p

er

ca

pit

a v

alu

e

Internet use GNI per capita

Despite high prices

Internet penetration in

South Africa is higher

than any other

surveyed African

countries

But lower than

Argentina, Colombia,

Paraguay and Peru

and Guatemala

But Internet remains unaffordable to the low-income

earners

32

10

0 00

10

20

30

40

0 - 1 583 1 584 - 7 167 7 168 - 16 417 16 418 - 33 333

Pe

rce

nta

ge

The 2017 RIA After AccessSurvey shows that low-incomeearners pay a significantly highproportion of their disposableincome to accesstelecommunication services

The cost of Internet or theaffordability divide between thelow-income and high-incomeSouth Africans is creatingbarriers to connecting the low-income earners

The Survey shows that almost50% of South Africans do notuse the Internet and furtherthese 50% are those in thebottom of the pyramid

Cost drivers

• ~High rand-dollar exchange rate- Which affects equipment import required forthe constant upgrading of mobile network.

• ~Increasing costs of key inputs – Have had an inflationary effects on dataprices

• ~In the absence of high-demand spectrum being released to operators for4G: high bandwidth services are also not being deployed in the cost-effectivemanner which further exacerbate the high cost of data.

• Regulatory issues: The failure of ICASA to put in place some mandatory andfoundational regulation means that the wholesale facility and service market,which is highly imperfect by nature, does not produce the intended competitiveresults

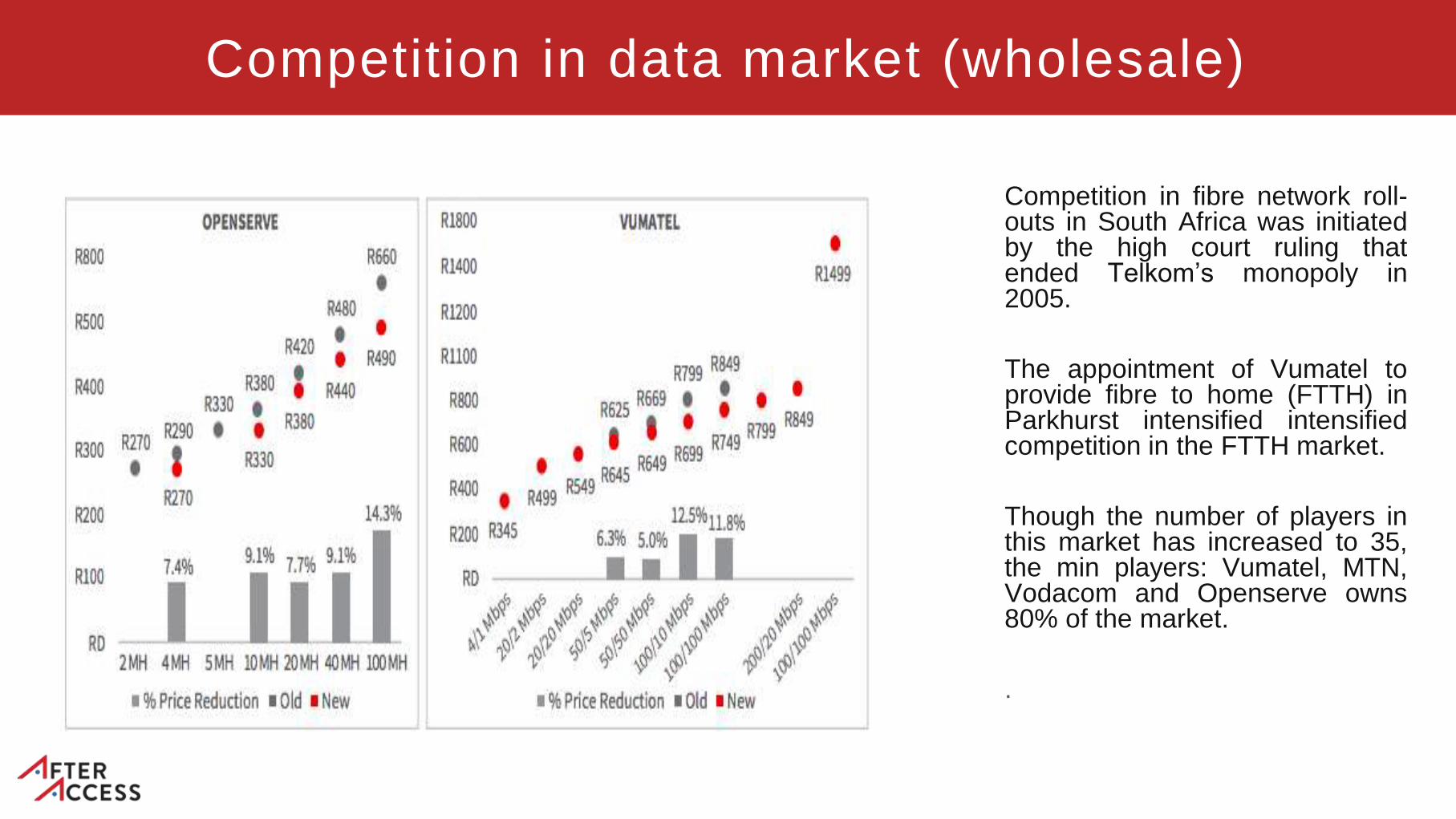

Competition in data market (wholesale)

Competition in fibre network roll-outs in South Africa was initiatedby the high court ruling thatended Telkom’s monopoly in2005.

The appointment of Vumatel toprovide fibre to home (FTTH) inParkhurst intensified intensifiedcompetition in the FTTH market.

Though the number of players inthis market has increased to 35,the min players: Vumatel, MTN,Vodacom and Openserve owns80% of the market.

.

Mobile Market

16 15 1619

23 23

17 17

37 37 3735 34 34 35

31

1 2 2 2 3 3 4 5

47 4745 44

40 4044

47

0

12.5

25

37.5

50

2010 2011 2012 2013 2014 2015 2016 2017

Cell MTN Telkom Vodacom The south African mobilemarket is dominated bytwo players: Vodacom andMTN.

Using the HHI the marketis found to be highlyconcentrated which nindex higher than 2500.

Despite smaller players(Cell C and Telkom)adopting a number ofcompetitive strategiesthey have failed to gainsubstantial market share.

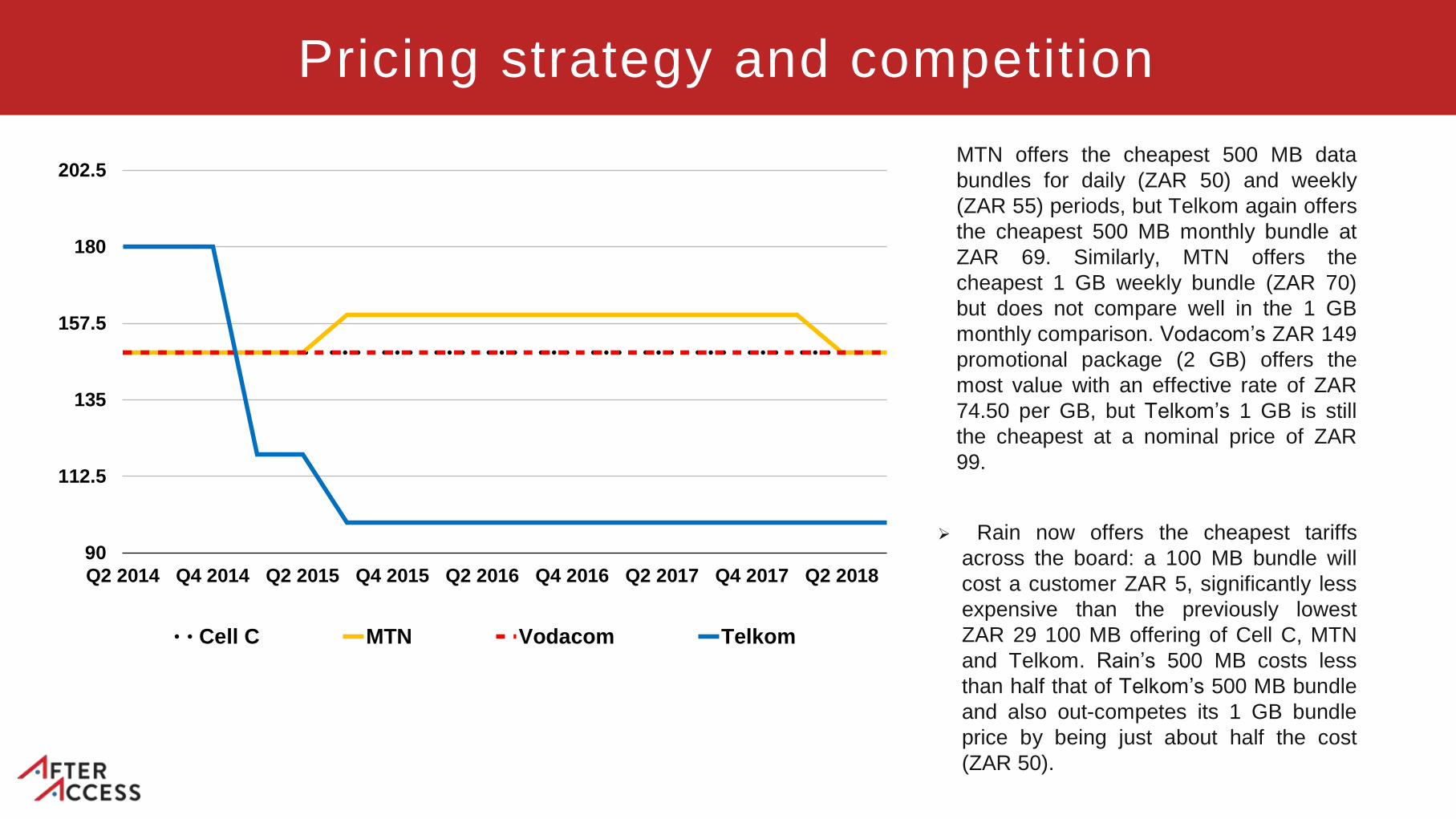

Pricing strategy and competition

90

112.5

135

157.5

180

202.5

Q2 2014 Q4 2014 Q2 2015 Q4 2015 Q2 2016 Q4 2016 Q2 2017 Q4 2017 Q2 2018

Cell C MTN Vodacom Telkom

MTN offers the cheapest 500 MB data

bundles for daily (ZAR 50) and weekly

(ZAR 55) periods, but Telkom again offers

the cheapest 500 MB monthly bundle at

ZAR 69. Similarly, MTN offers the

cheapest 1 GB weekly bundle (ZAR 70)

but does not compare well in the 1 GB

monthly comparison. Vodacom’s ZAR 149

promotional package (2 GB) offers the

most value with an effective rate of ZAR

74.50 per GB, but Telkom’s 1 GB is still

the cheapest at a nominal price of ZAR

99.

Rain now offers the cheapest tariffs

across the board: a 100 MB bundle will

cost a customer ZAR 5, significantly less

expensive than the previously lowest

ZAR 29 100 MB offering of Cell C, MTN

and Telkom. Rain’s 500 MB costs less

than half that of Telkom’s 500 MB bundle

and also out-competes its 1 GB bundle

price by being just about half the cost

(ZAR 50).

Quality adjusted prices

Represents the ratio between the1GB data basket and the averagedownload and upload speeds,shows that the two dominantoperators Vodacom and MTN offerhigher quality, respectively.

In the same period Telkom’s qualitywas the lowest. However, since Q12016, it seems that smalleroperators improved their quality,catching up with dominantoperators in Q2 2016 (in line withincreased network investments).Vodacom SA’s high prices areaccompanied by higher Internetspeeds, compared to MTN SA andCell C, which are performing lesswell on the measure based onaverage download/upload speed (inMbps) divided by 1GB basketcosts.

Quality and Coverage

South Africa is connected to six submarine cables.

Telkom, Liquid Telecom South Africa (previously

Neotel) and Broadband Infraco have made considerable

backbone and backhaul investment over the past

decade, giving South Africa the most extensive

coverage in the continent

Supplemented by recent expansion of fibre networks in

larger metropolitan areas

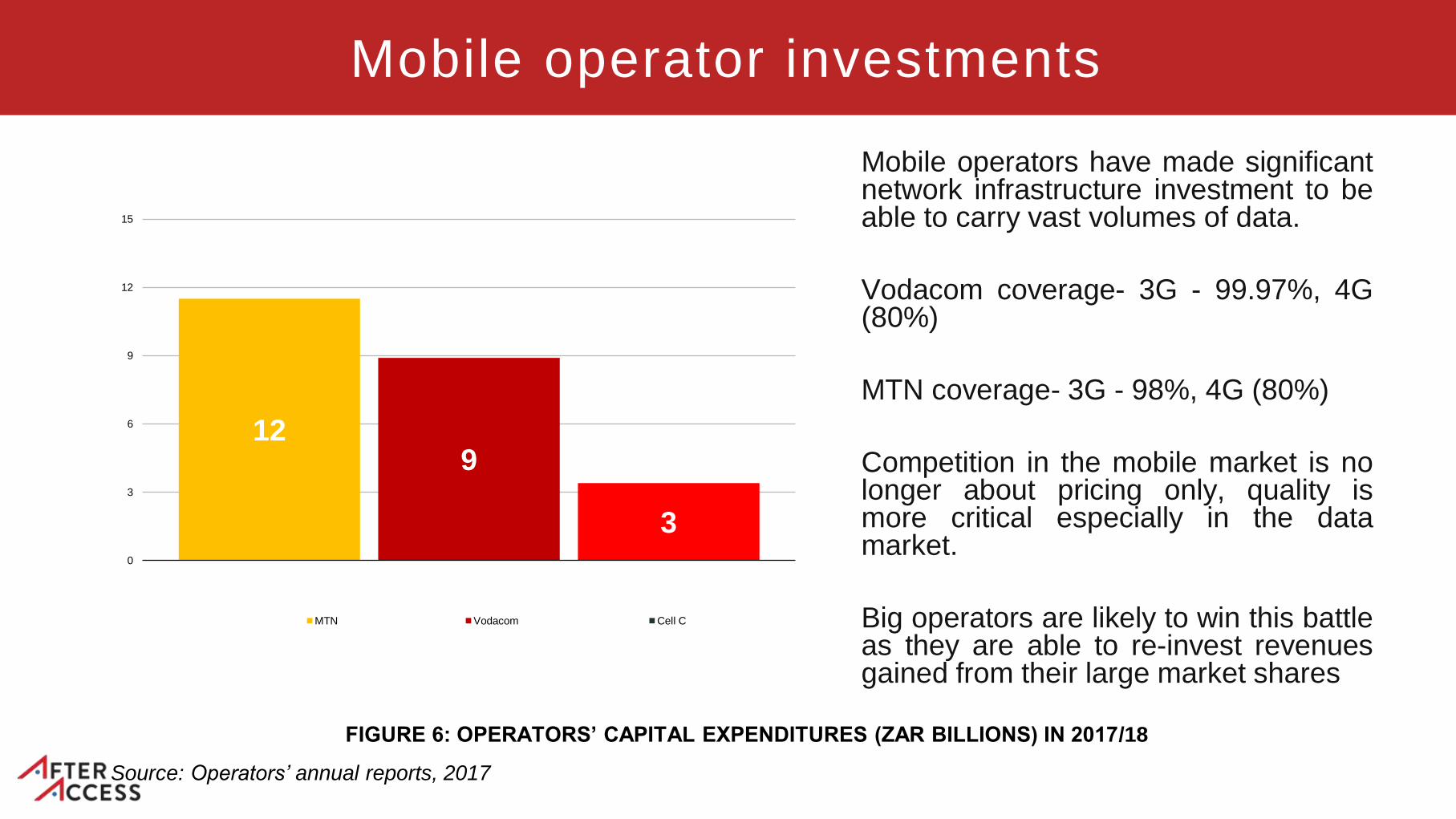

Mobile operator investments

FIGURE 6: OPERATORS’ CAPITAL EXPENDITURES (ZAR BILLIONS) IN 2017/18

Source: Operators’ annual reports, 2017

129

30

3

6

9

12

15

MTN Vodacom Cell C

Mobile operators have made significantnetwork infrastructure investment to beable to carry vast volumes of data.

Vodacom coverage- 3G - 99.97%, 4G(80%)

MTN coverage- 3G - 98%, 4G (80%)

Competition in the mobile market is nolonger about pricing only, quality ismore critical especially in the datamarket.

Big operators are likely to win this battleas they are able to re-invest revenuesgained from their large market shares

Download speed in ZA vs Rest of the World

(Speedchecker)

South Africa performs well in

comparison to other African

countries.

download speeds in South

Africa have been improving

due to innovations and

technological developments.

A development which can

be associated with

investments by

telecommunication

Related Documents