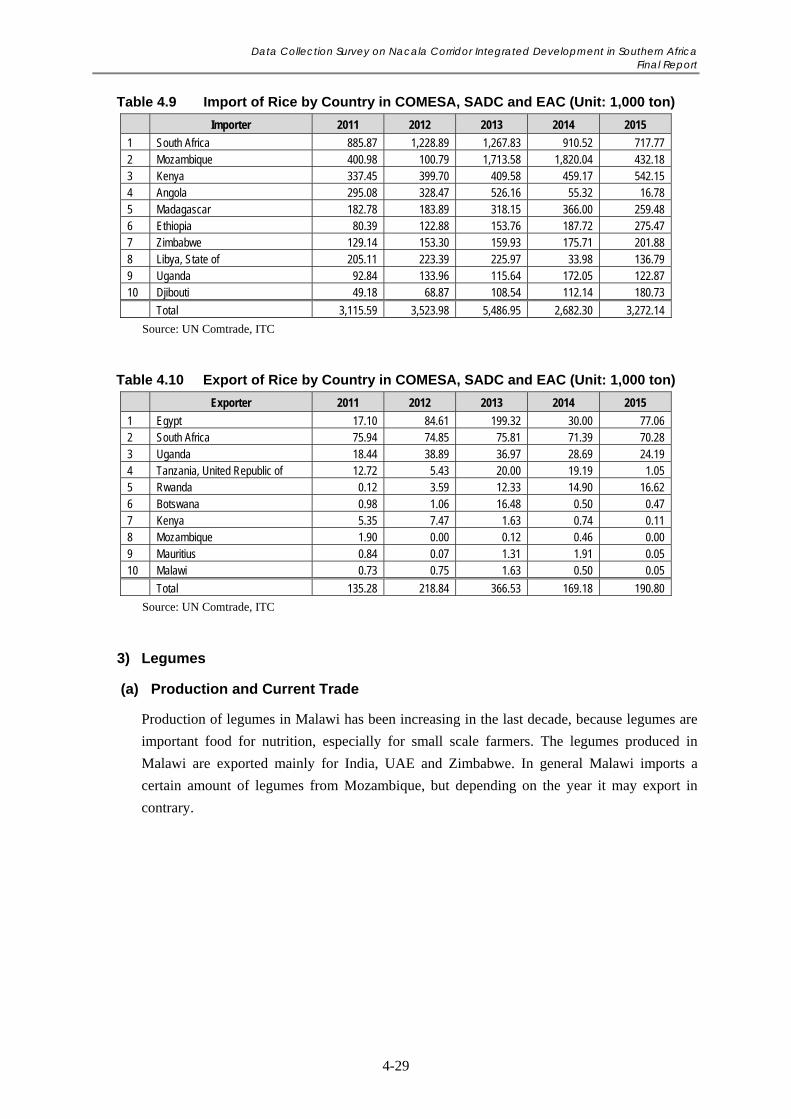

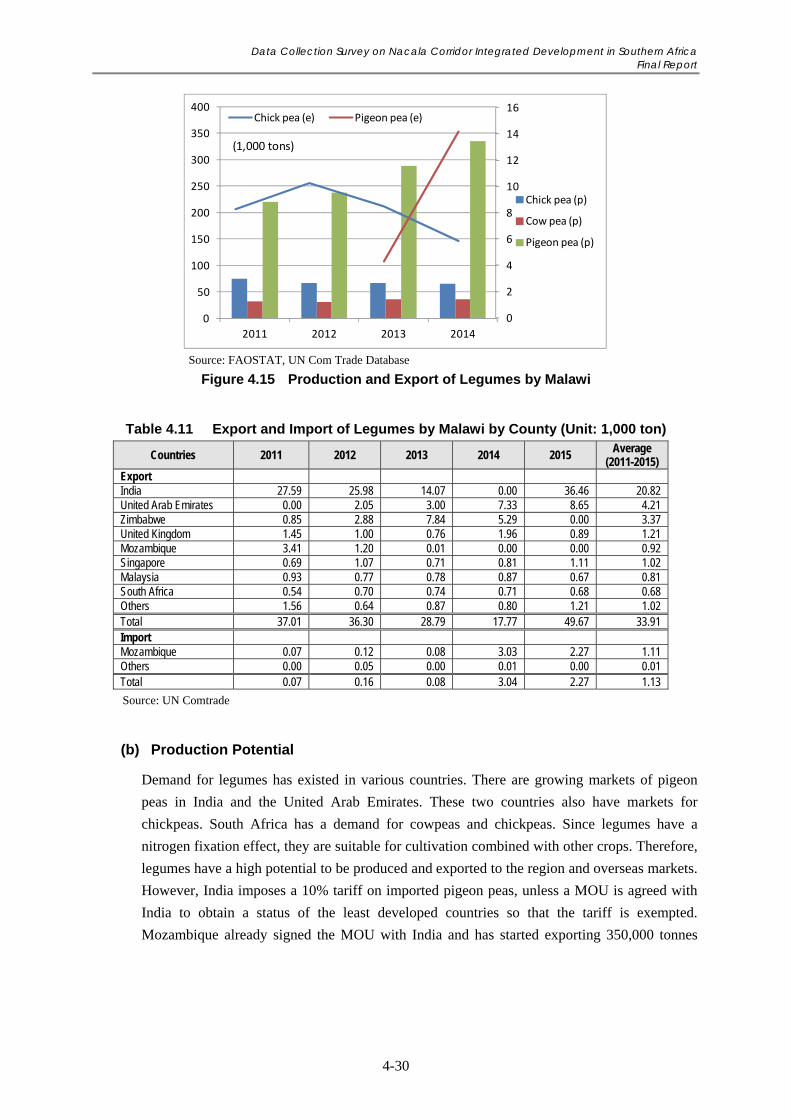

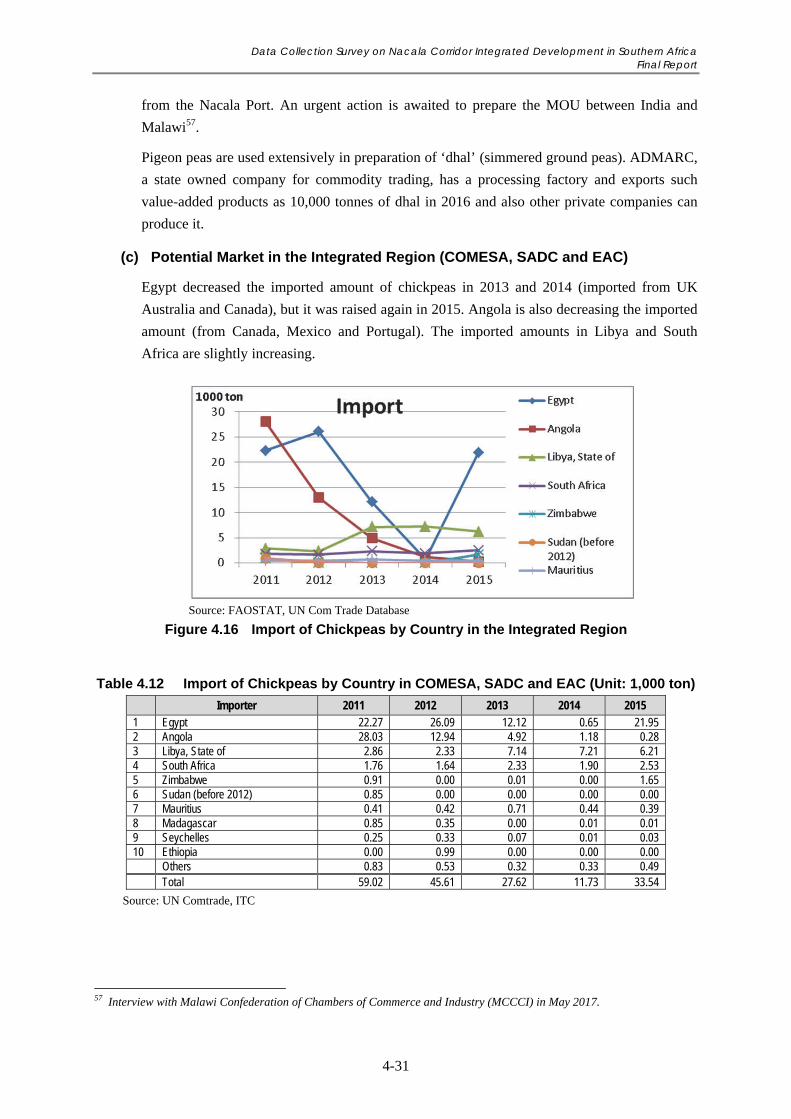

18 - 009 CR ( 3 ) 6R DATA COLLECTION SURVEY ON NACALA CORRIDOR INTEGRATED DEVELOPMENT IN SOUTHERN AFRICA FINAL REPORT MARCH 2018 JAPAN INTERNATIONAL COOPERATION AGENCY (JICA) ORIENTAL CONSULTANTS GLOBAL CO., LTD. MITSUBISHI UFJ RESEARCH AND CONSULTING CO.LTD. EIGHT-JAPAN ENGINEERING CONSULTANTS INC. REPUBLIC OF ZAMBIA REPUBLIC OF MALAWI

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

18-009CR (3)

6 R

DATA COLLECTION SURVEY ON

NACALA CORRIDOR INTEGRATED DEVELOPMENT

IN SOUTHERN AFRICA

FINAL REPORT

MARCH 2018

JAPAN INTERNATIONAL COOPERATION AGENCY (JICA) ORIENTAL CONSULTANTS GLOBAL CO., LTD.

MITSUBISHI UFJ RESEARCH AND CONSULTING CO.LTD.

EIGHT-JAPAN ENGINEERING CONSULTANTS INC.

REPUBLIC OF ZAMBIA REPUBLIC OF MALAWI

DATA COLLECTION SURVEY ON

NACALA CORRIDOR INTEGRATED DEVELOPMENT

IN SOUTHERN AFRICA

FINAL REPORT

MARCH 2018

JAPAN INTERNATIONAL COOPERATION AGENCY (JICA) ORIENTAL CONSULTANTS GLOBAL CO., LTD.

MITSUBISHI UFJ RESEARCH AND CONSULTING CO.LTD.

EIGHT-JAPAN ENGINEERING CONSULTANTS INC.

REPUBLIC OF ZAMBIA REPUBLIC OF MALAWI

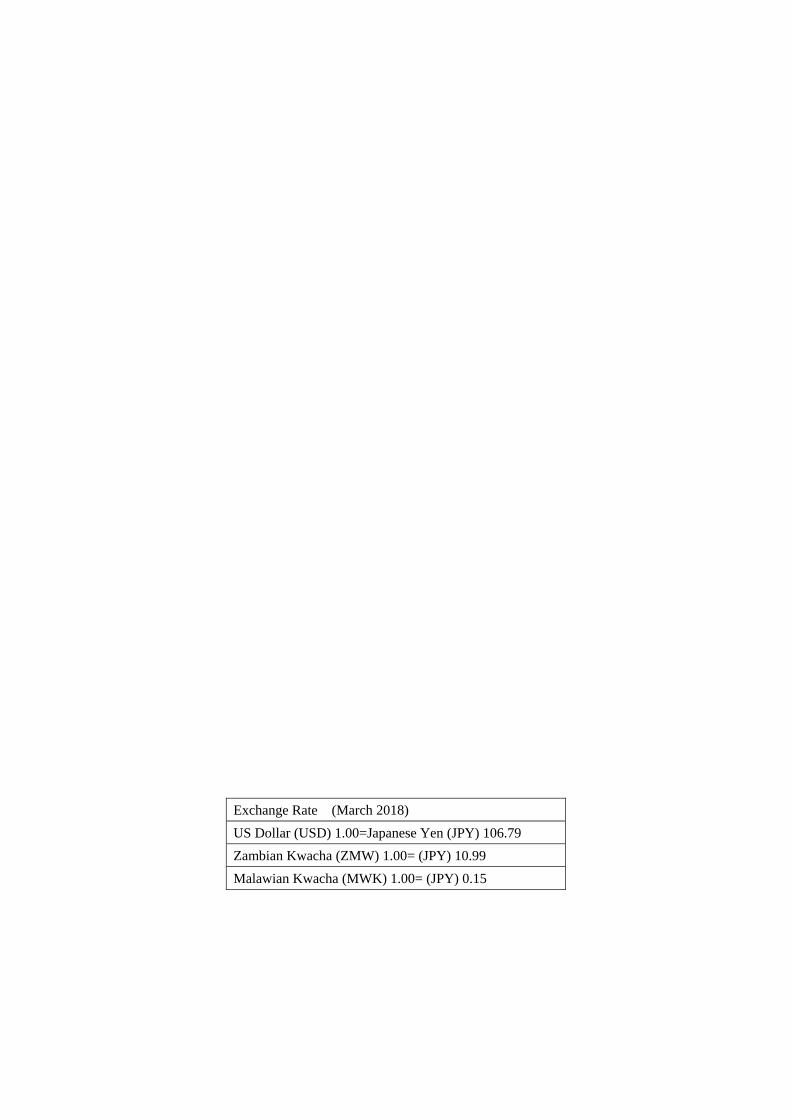

Exchange Rate (March 2018)

US Dollar (USD) 1.00=Japanese Yen (JPY) 106.79

Zambian Kwacha (ZMW) 1.00= (JPY) 10.99

Malawian Kwacha (MWK) 1.00= (JPY) 0.15

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

i

TABLE OF CONTENTS

Page

List of Tables .......................................................................................................................................... vi

List of Figures ........................................................................................................................................ xi

List of Abbreviations .............................................................................................................................. xv

Executive Summary

Chapter 1 Introduction ................................................................................................................. 1-1

1.1 Background of the Study .................................................................................................... 1-1

1.2 Objectives of the Study ...................................................................................................... 1-1

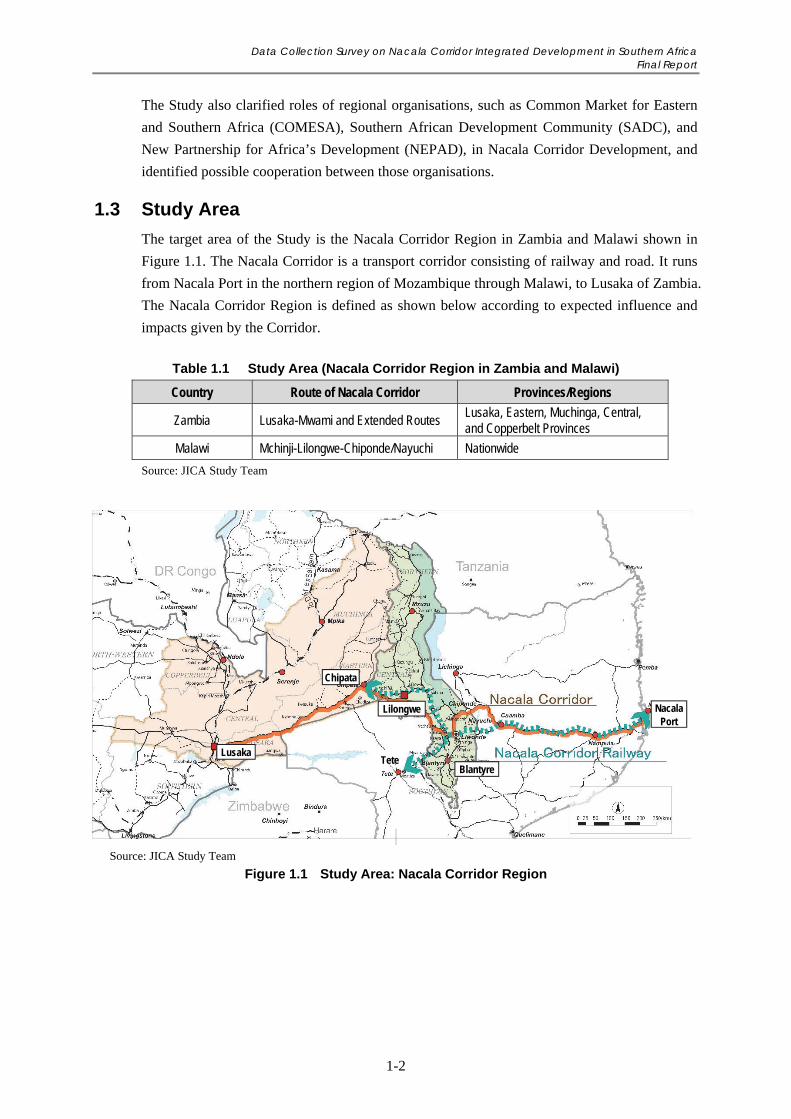

1.3 Study Area .......................................................................................................................... 1-2

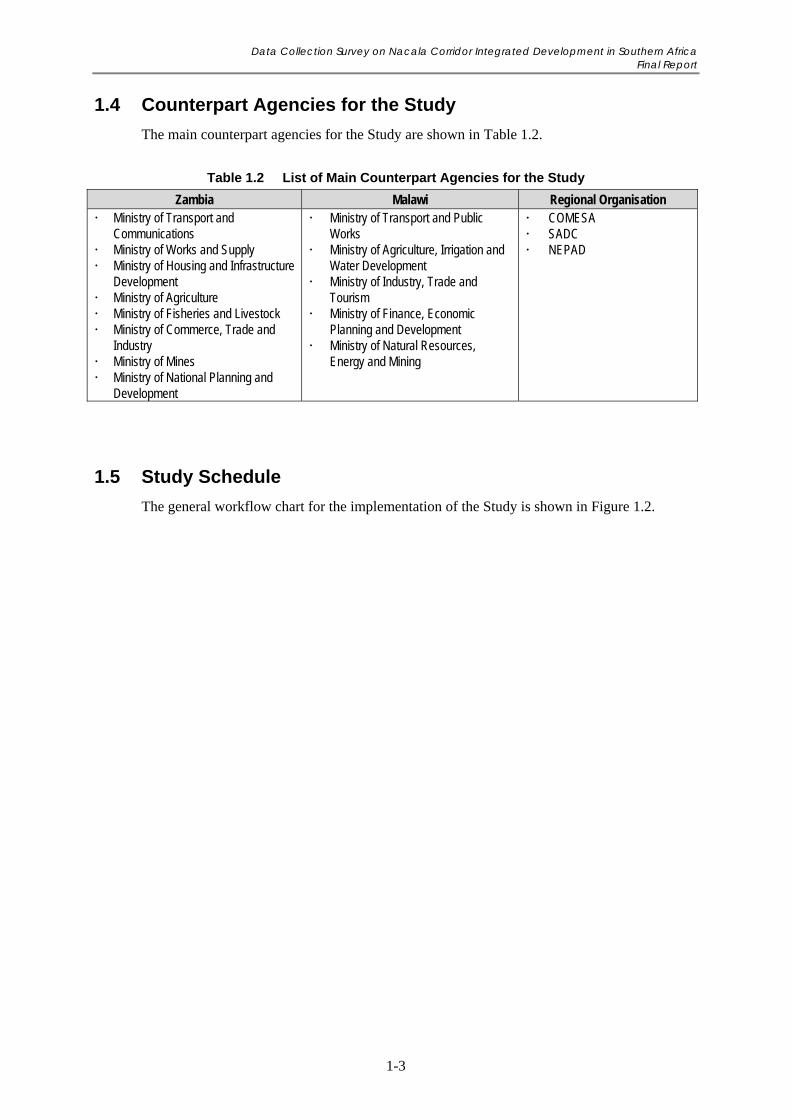

1.4 Counterpart Agencies for the Study ................................................................................... 1-3

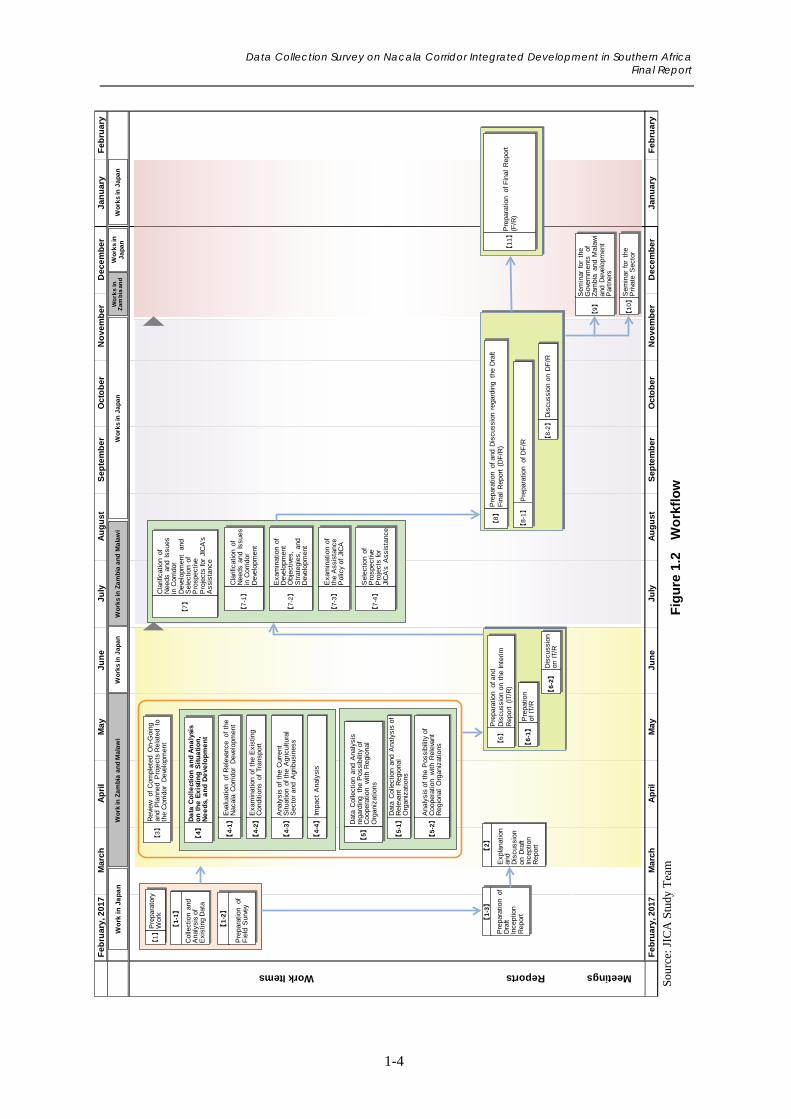

1.5 Study Schedule ................................................................................................................... 1-3

Chapter 2 Corridor Development in Zambia and Malawi and Current Status

of Nacala Corridor Development ............................................................................... 2-1

2.1 Clusters of Transport Corridors .......................................................................................... 2-1

2.1.1 Propulsion Frameworks: Transport Corridors as Economic Corridors ......................... 2-1

2.1.2 Transport Corridors Relevant to Malawi and Zambia ................................................... 2-3

2.1.3 Current Status of Major Transport Corridors Excluding Nacala Corridor .................... 2-5

2.1.4 Institutions for Transport Corridors ............................................................................... 2-6

2.2 Current Conditions and Status of Nacala Corridor ............................................................. 2-8

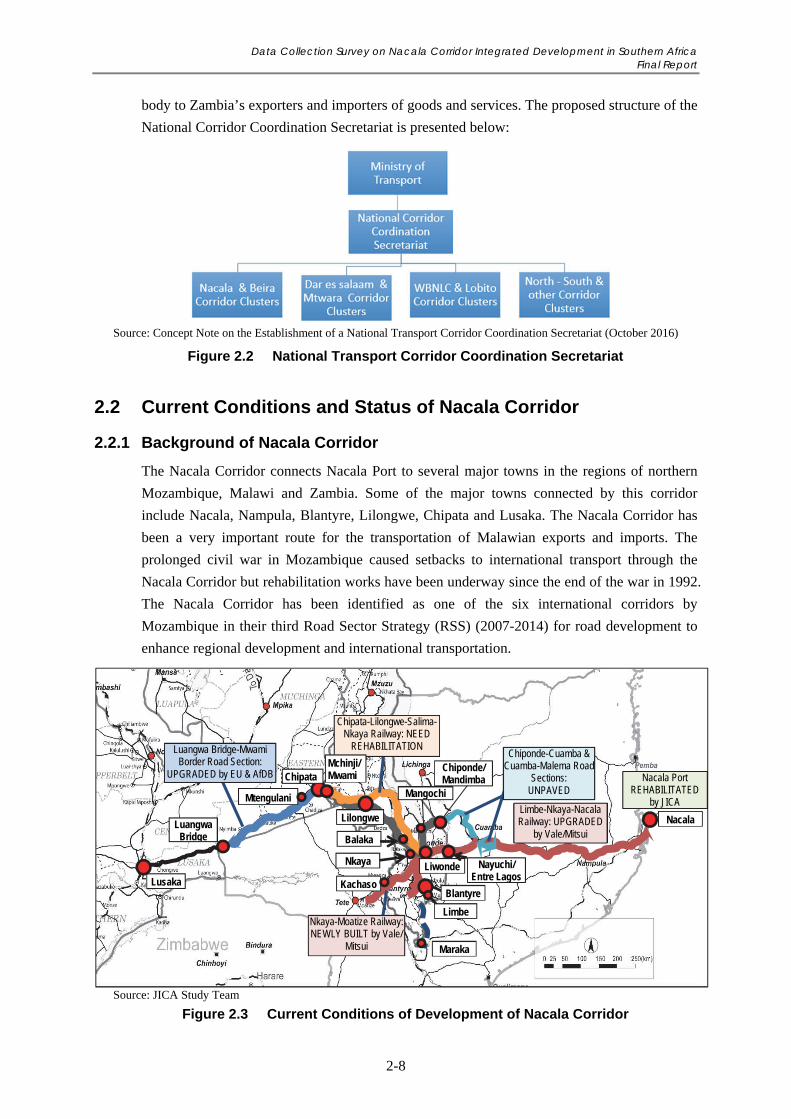

2.2.1 Background of Nacala Corridor .................................................................................... 2-8

2.2.2 Status and Conditions of Nacala Corridor ..................................................................... 2-9

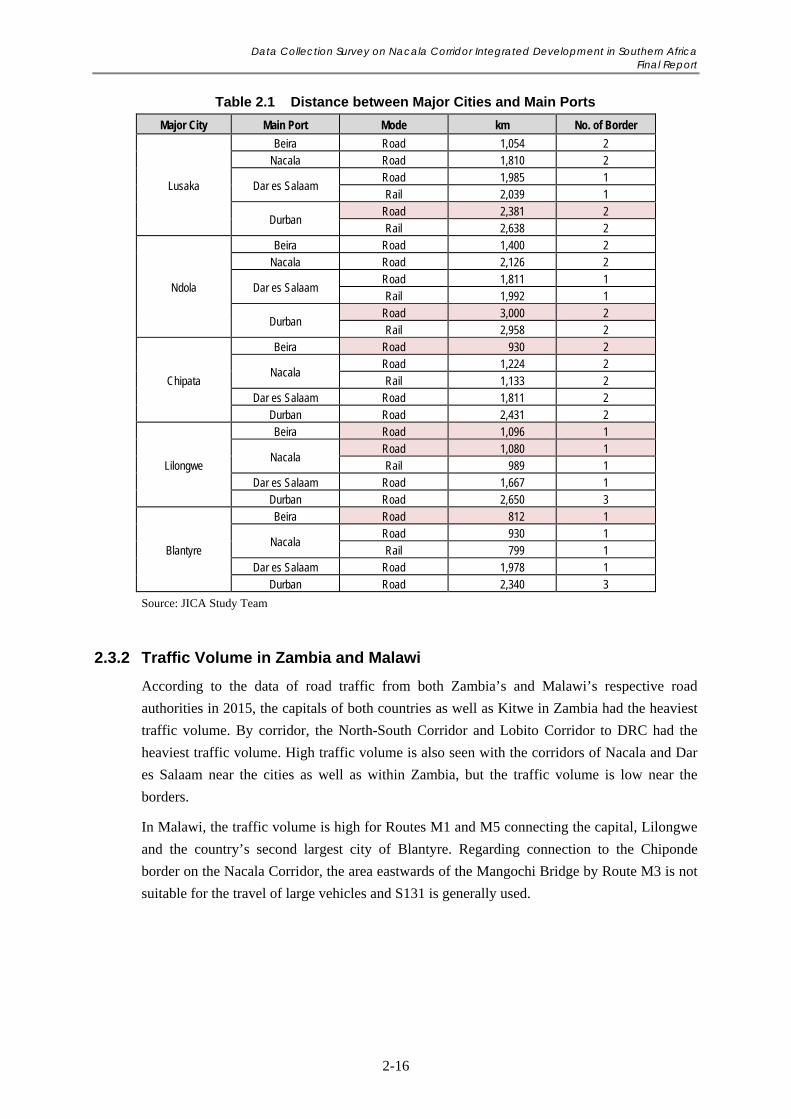

2.3 Current Usage of Nacala Corridor vis-a-vis Major Corridors .......................................... 2-15

2.3.1 Distance between Major Cities and Main Ports .......................................................... 2-15

2.3.2 Traffic Volume in Zambia and Malawi ....................................................................... 2-16

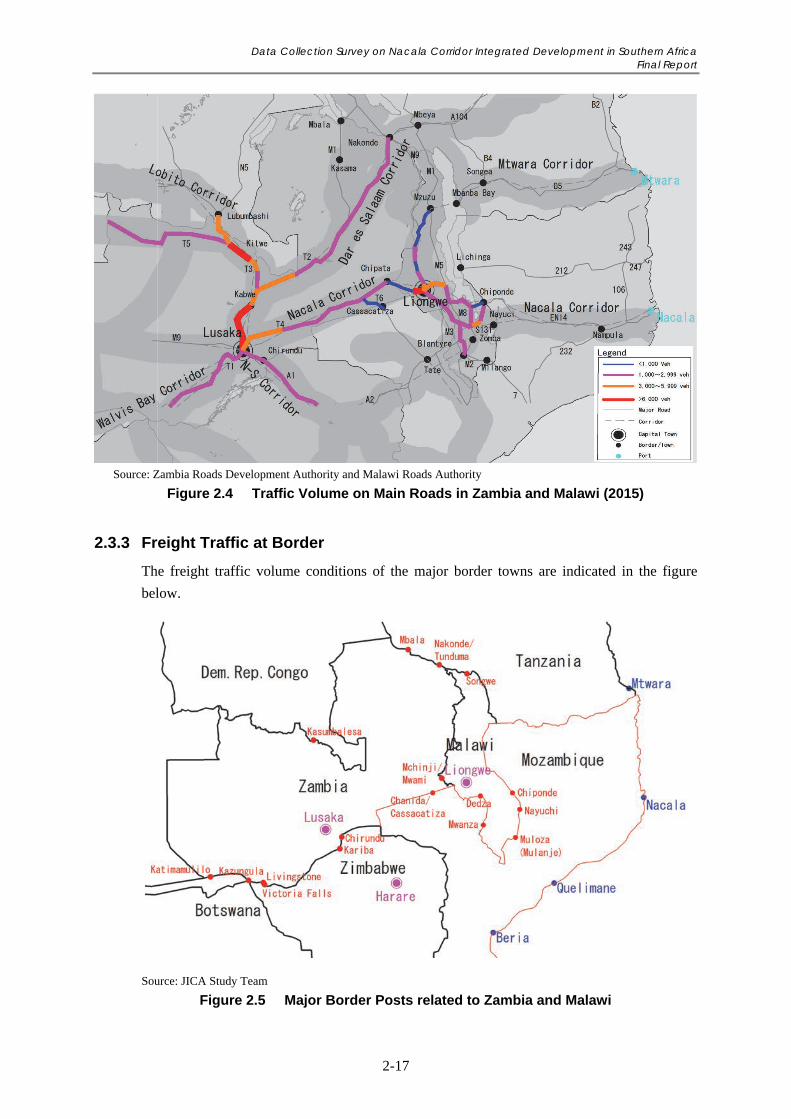

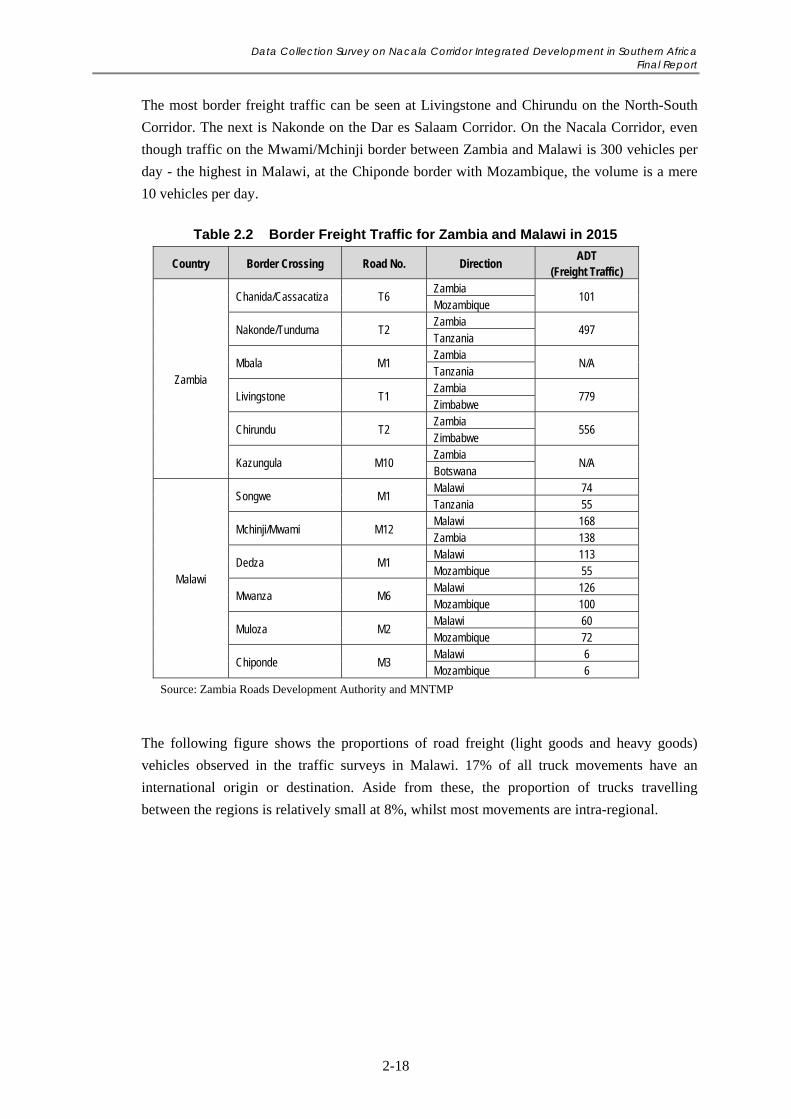

2.3.3 Freight Traffic at Border ............................................................................................. 2-17

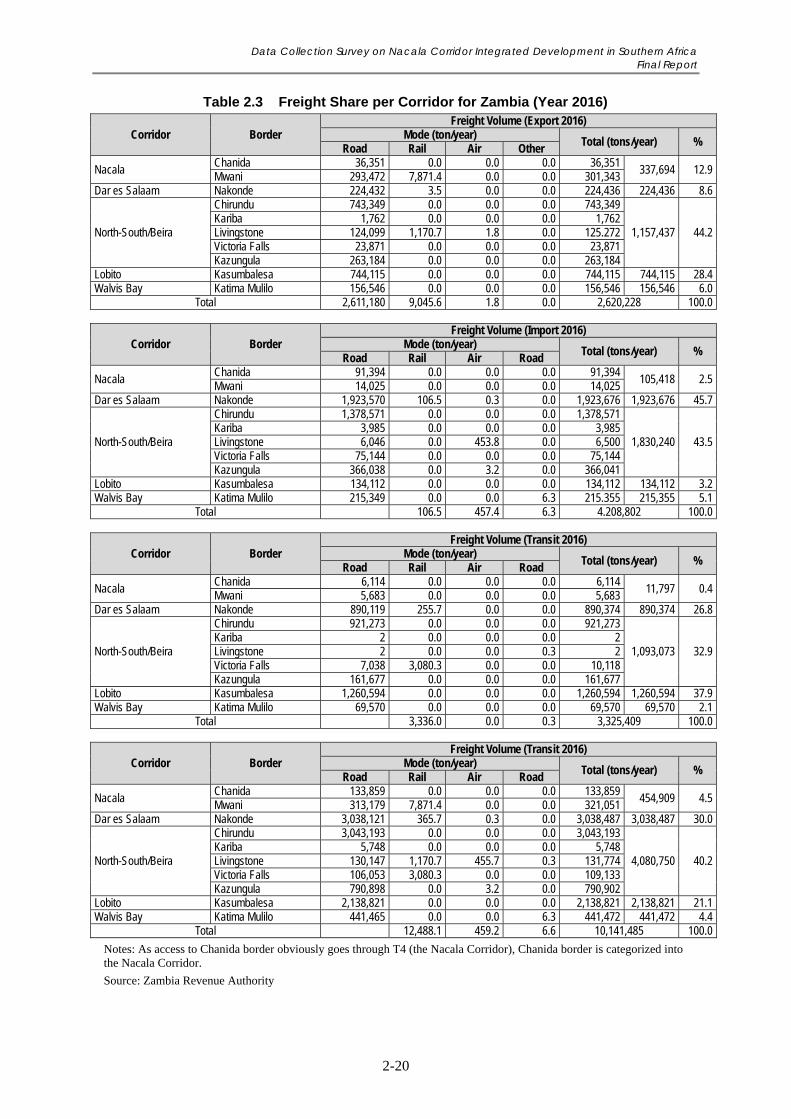

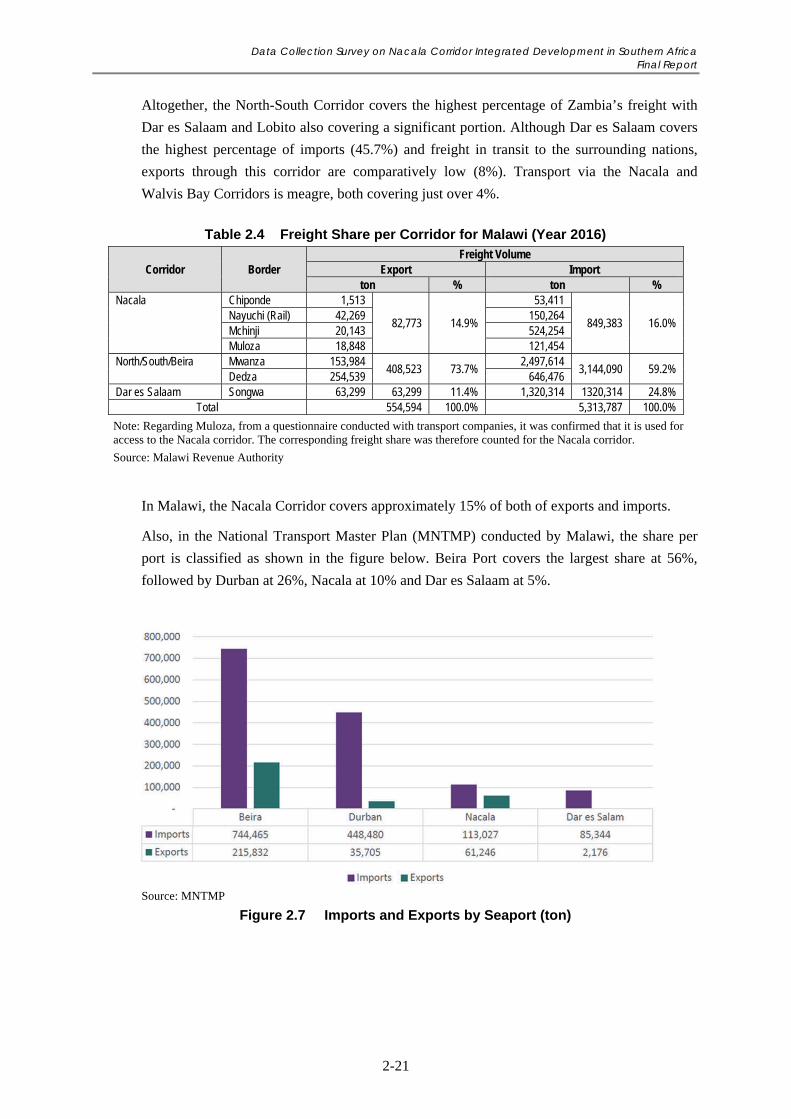

2.3.4 Freight Share per Corridor .......................................................................................... 2-19

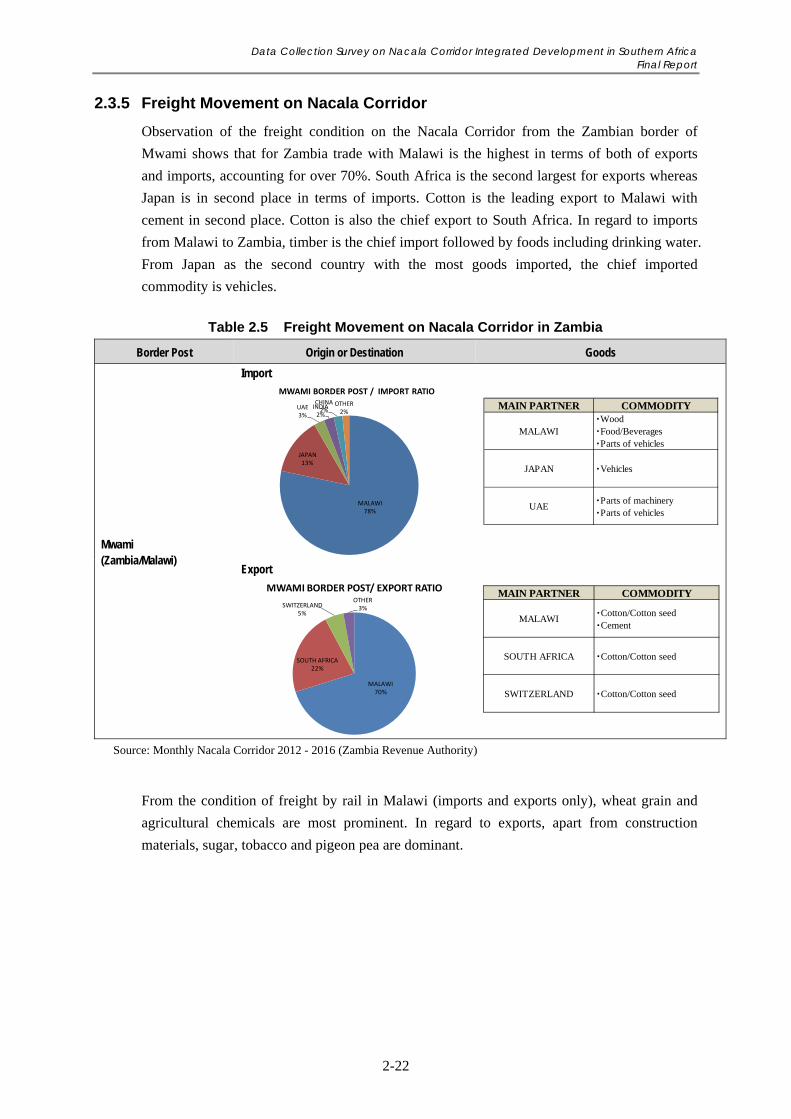

2.3.5 Freight Movement on Nacala Corridor ....................................................................... 2-22

2.3.6 Capacity of Major Ports .............................................................................................. 2-23

2.3.7 One Stop Border Posts (OSBPs) ................................................................................. 2-25

2.3.8 Transit Time and Cost ................................................................................................. 2-27

2.4 Comprehensive Evaluation of the Corridors .................................................................... 2-29

2.4.1 Hearing Survey Results on Nacala Corridor ............................................................... 2-29

2.4.2 Comprehensive Analysis on Transport Corridors Related to Zambia and Malawi ..... 2-31

Chapter 3 Present Condition of Zambia ..................................................................................... 3-1

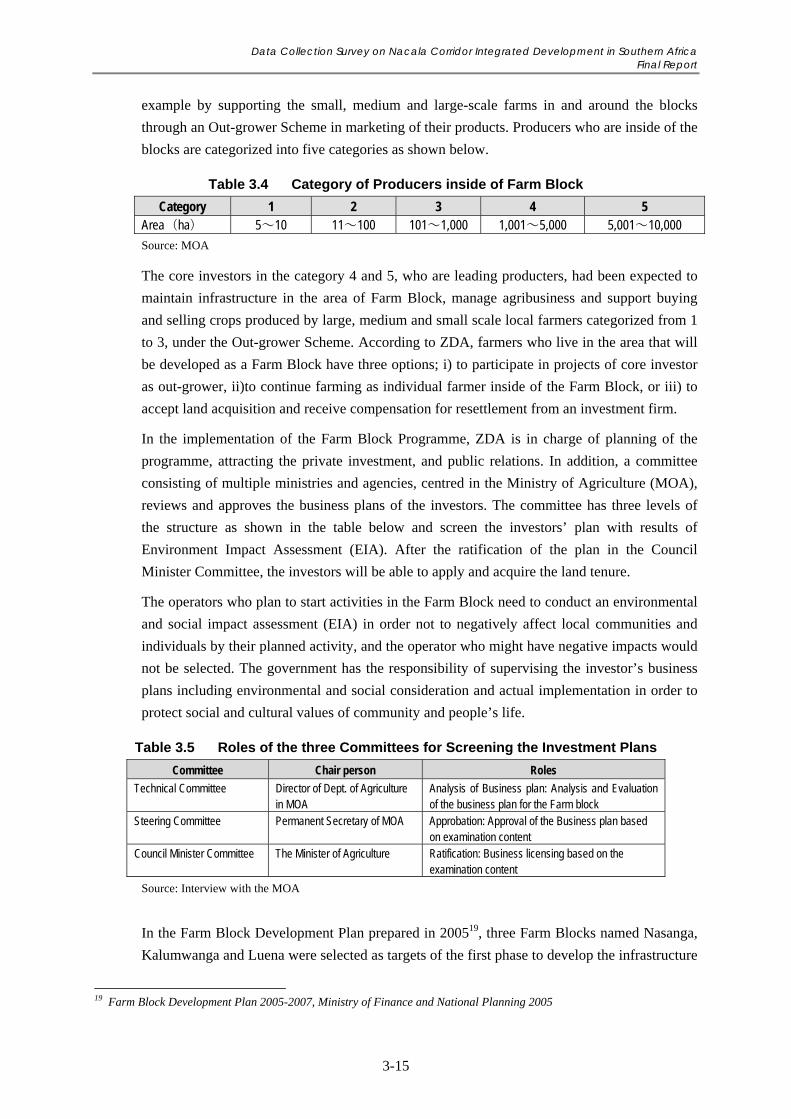

3.1 Agriculture.......................................................................................................................... 3-2

3.1.1 Overview of the Agriculture .......................................................................................... 3-2

3.1.2 Agriculture Condition ................................................................................................... 3-2

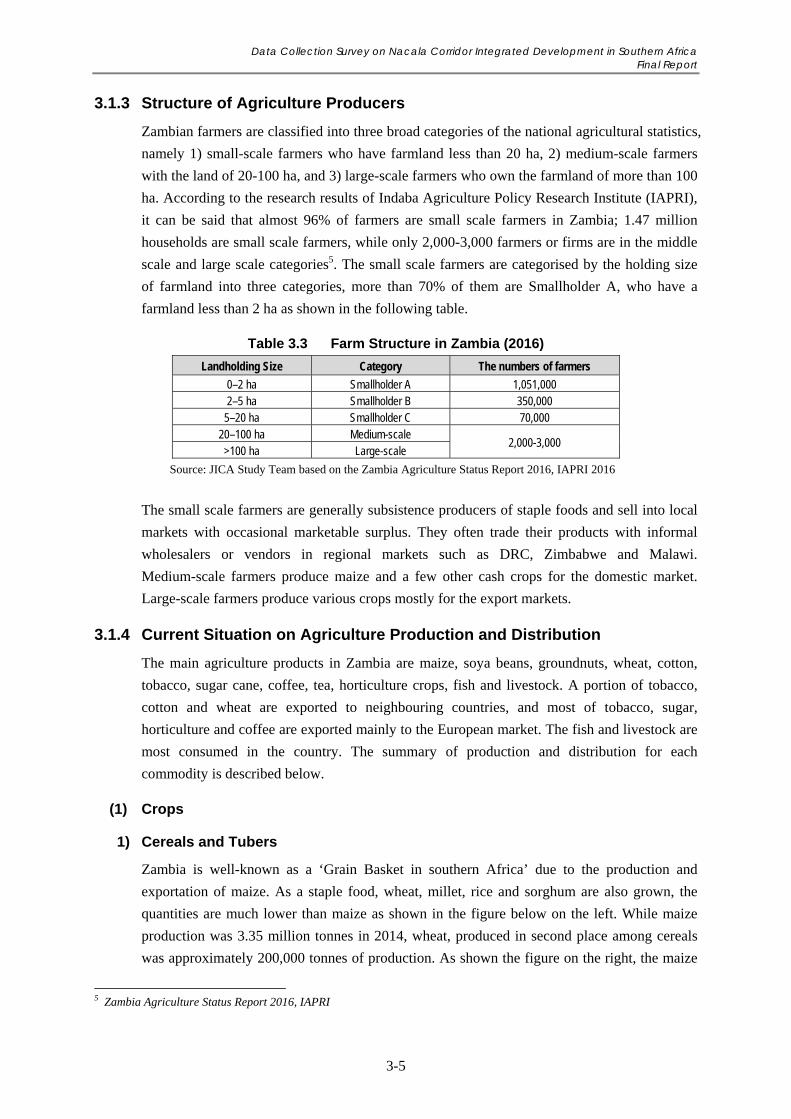

3.1.3 Structure of Agriculture Producers ................................................................................ 3-5

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

ii

3.1.4 Current Situation on Agriculture Production and Distribution ...................................... 3-5

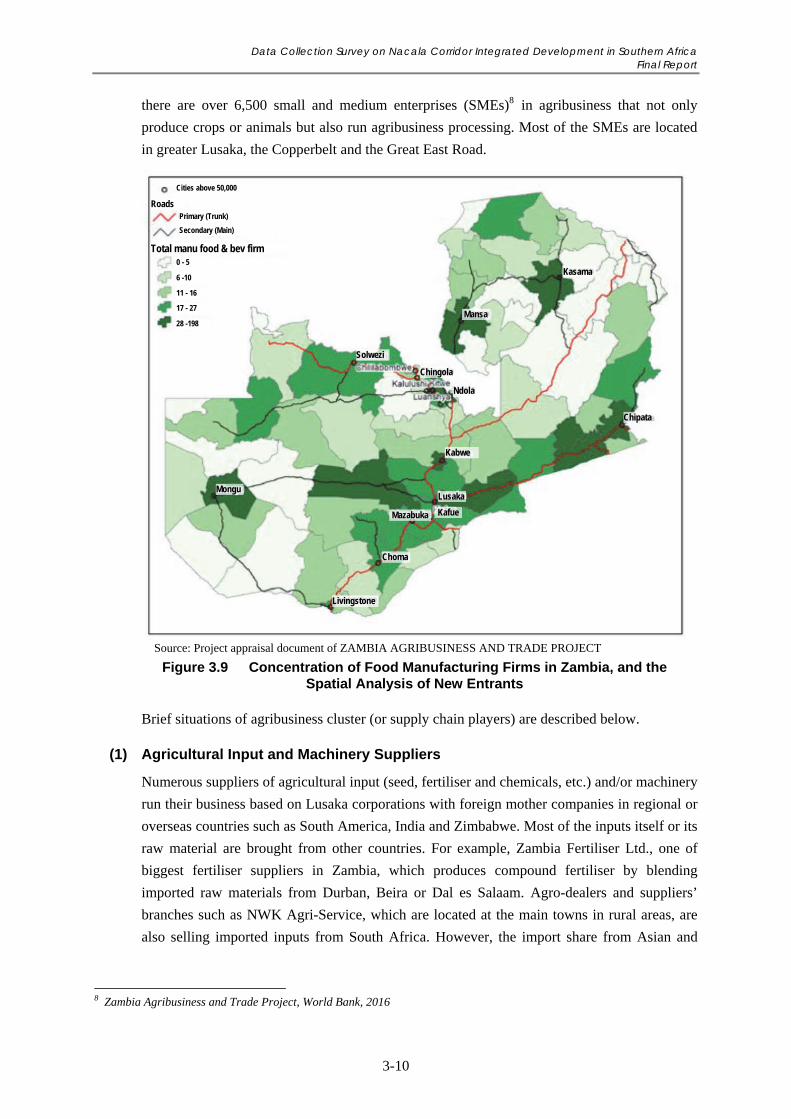

3.1.5 Agribusiness Clusters and Players ................................................................................ 3-9

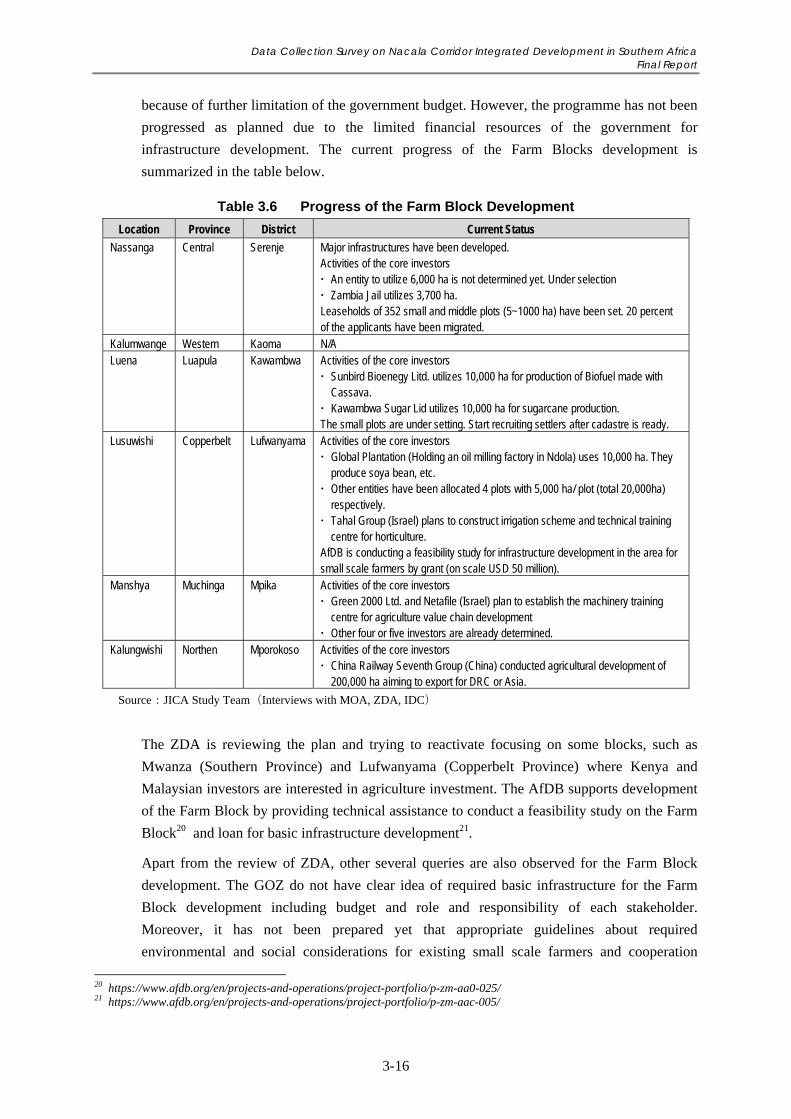

3.1.6 Related Policies, Programmes and Projects ................................................................ 3-13

3.1.7 Development Potential and Challenges of Agriculture and Agribusiness Sector ........ 3-19

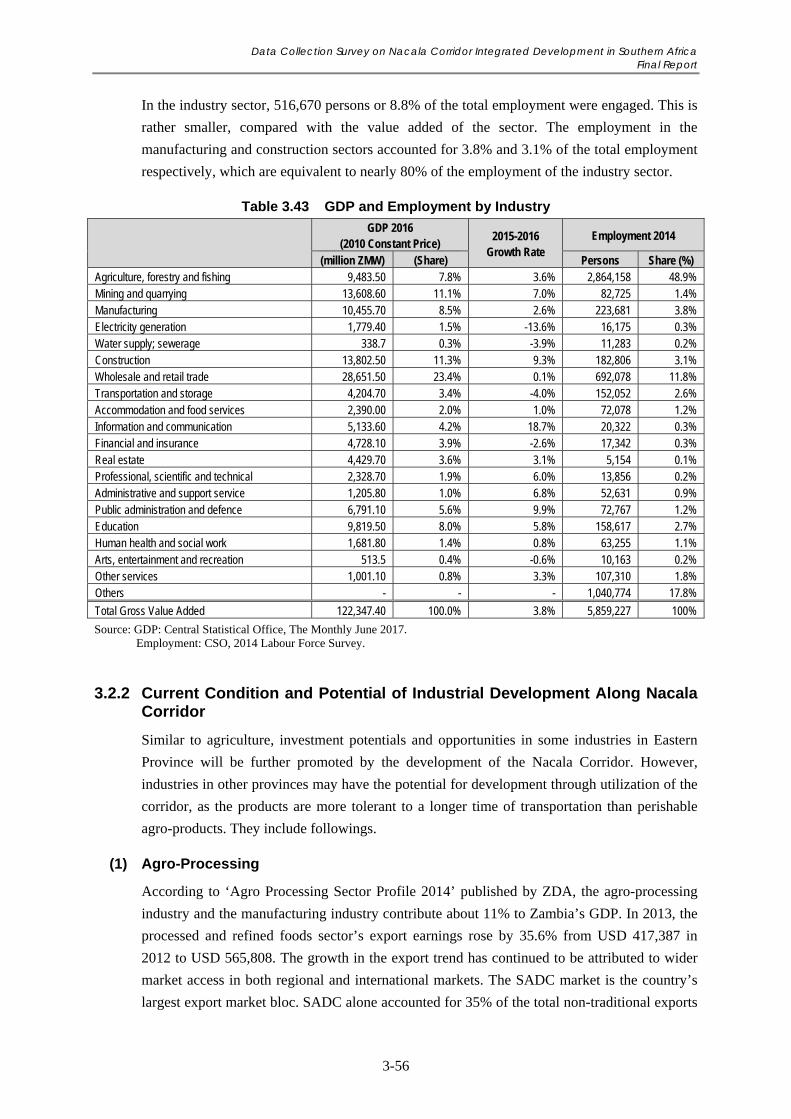

3.2 Industry ............................................................................................................................. 3-55

3.2.1 Overview of the Industry ............................................................................................. 3-55

3.2.2 Current Condition and Potential of Industrial Development Along Nacala

Corridor ....................................................................................................................... 3-56

3.3 Mining .............................................................................................................................. 3-58

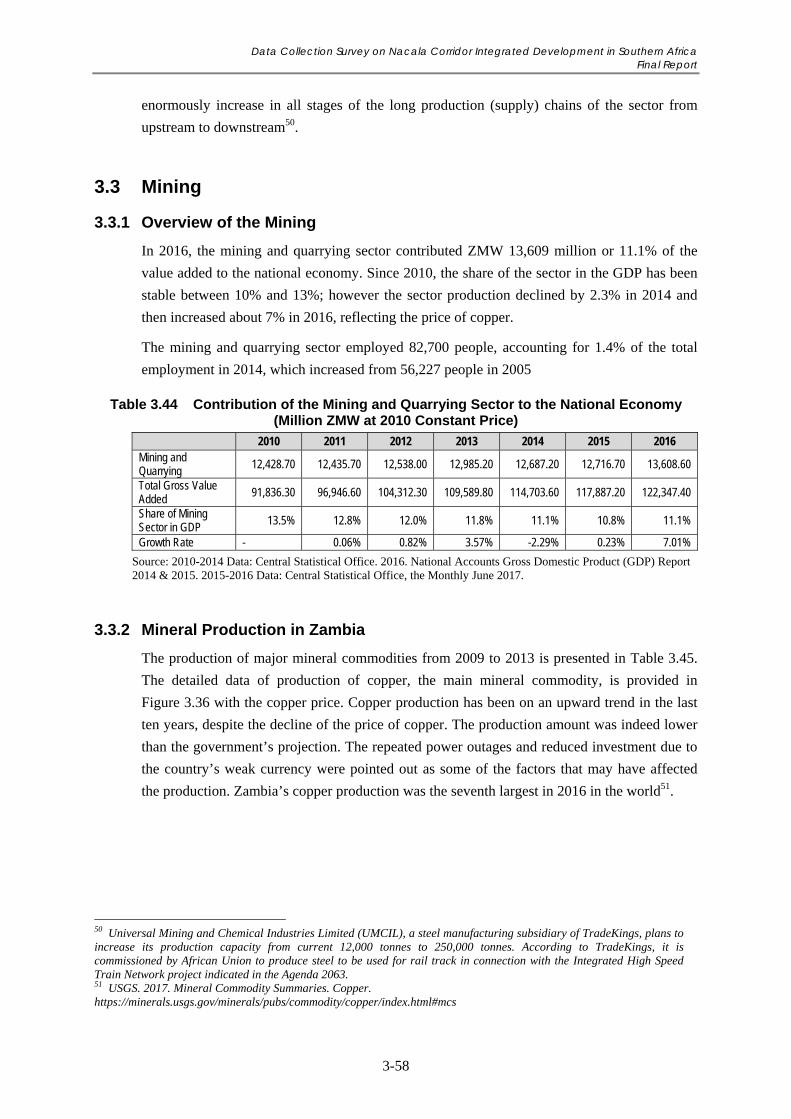

3.3.1 Overview of the Mining .............................................................................................. 3-58

3.3.2 Mineral Production in Zambia .................................................................................... 3-58

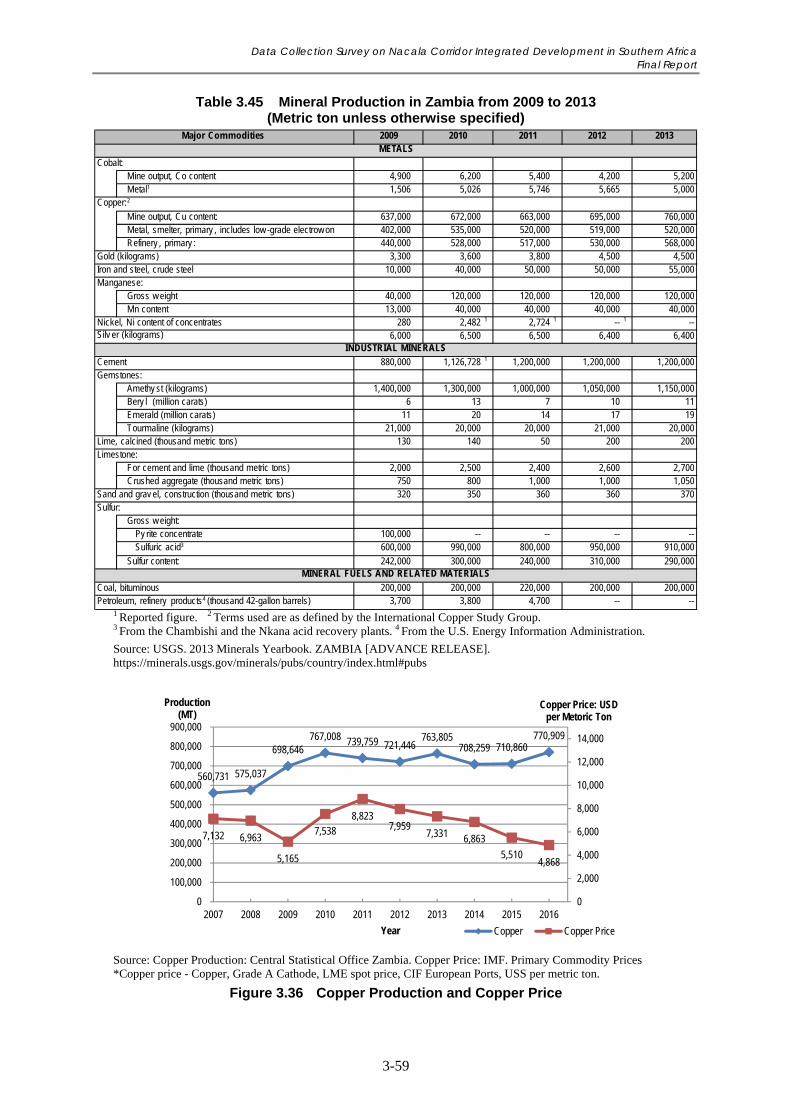

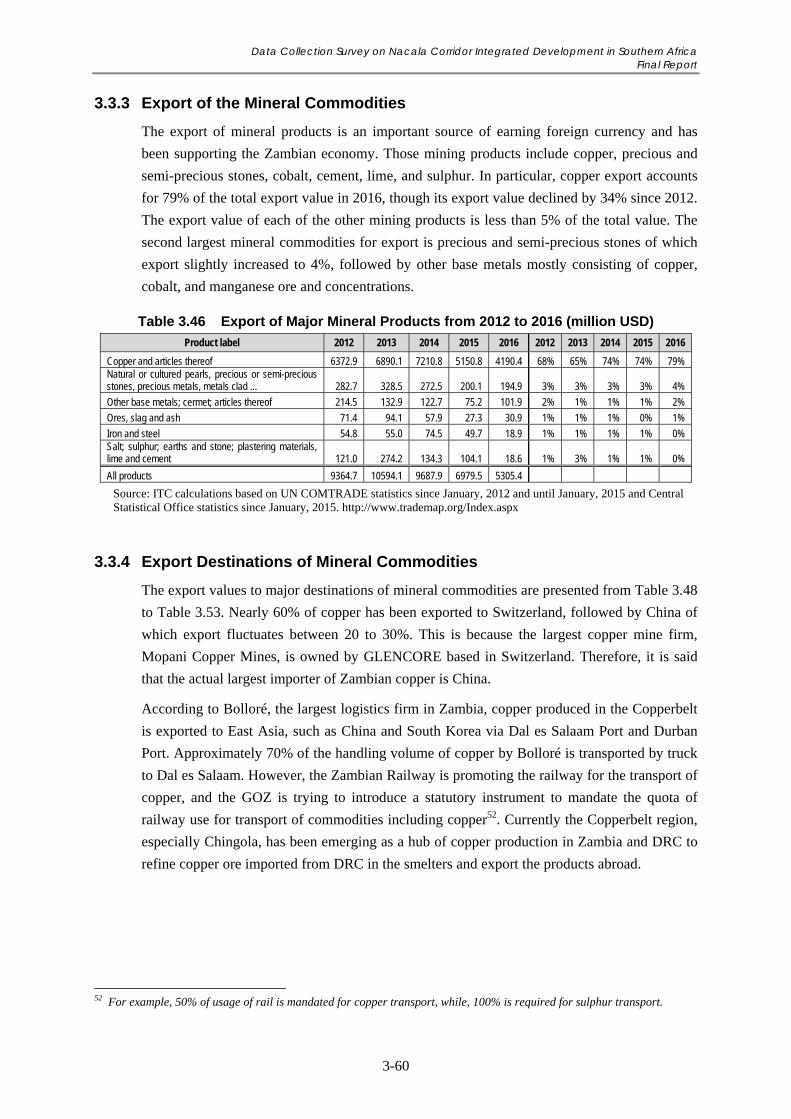

3.3.3 Export of the Mineral Commodities ............................................................................ 3-60

3.3.4 Export Destinations of Mineral Commodities ............................................................. 3-60

3.3.5 Government Policy of Mining Sector ......................................................................... 3-63

3.3.6 Development Potential of the Mining Sector in the Nacala Corridor Region ............. 3-64

3.4 Trade ................................................................................................................................. 3-64

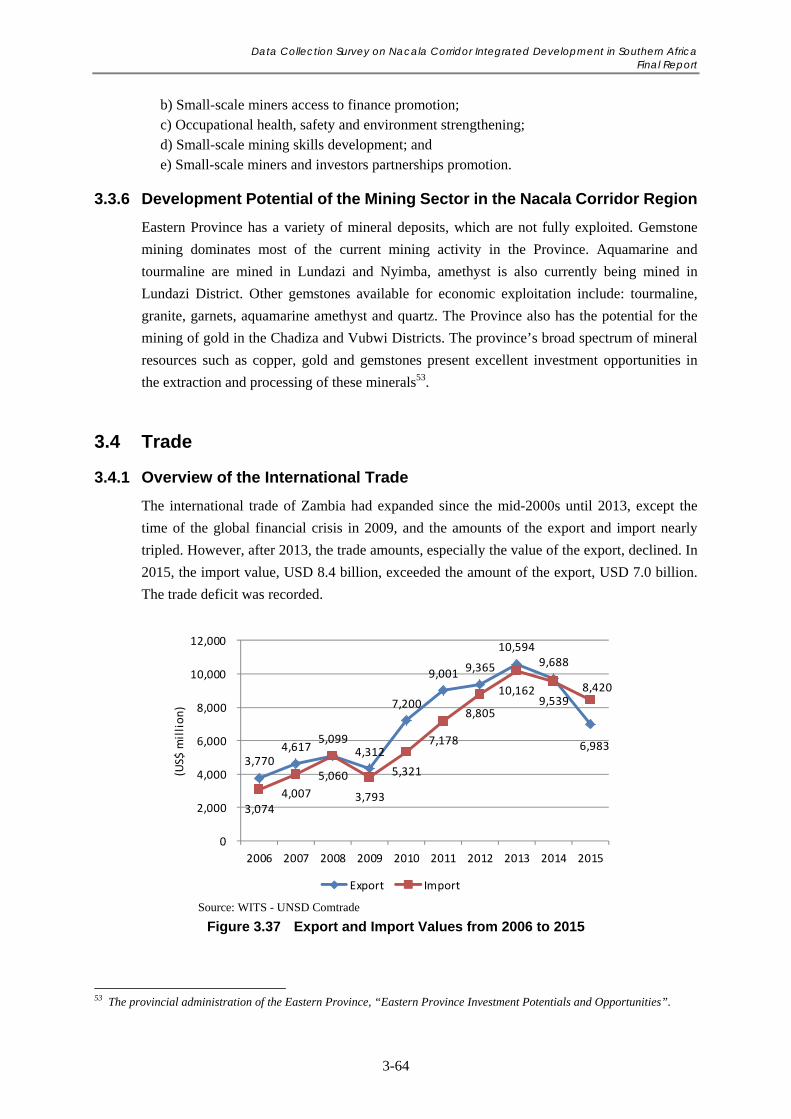

3.4.1 Overview of the International Trade ........................................................................... 3-64

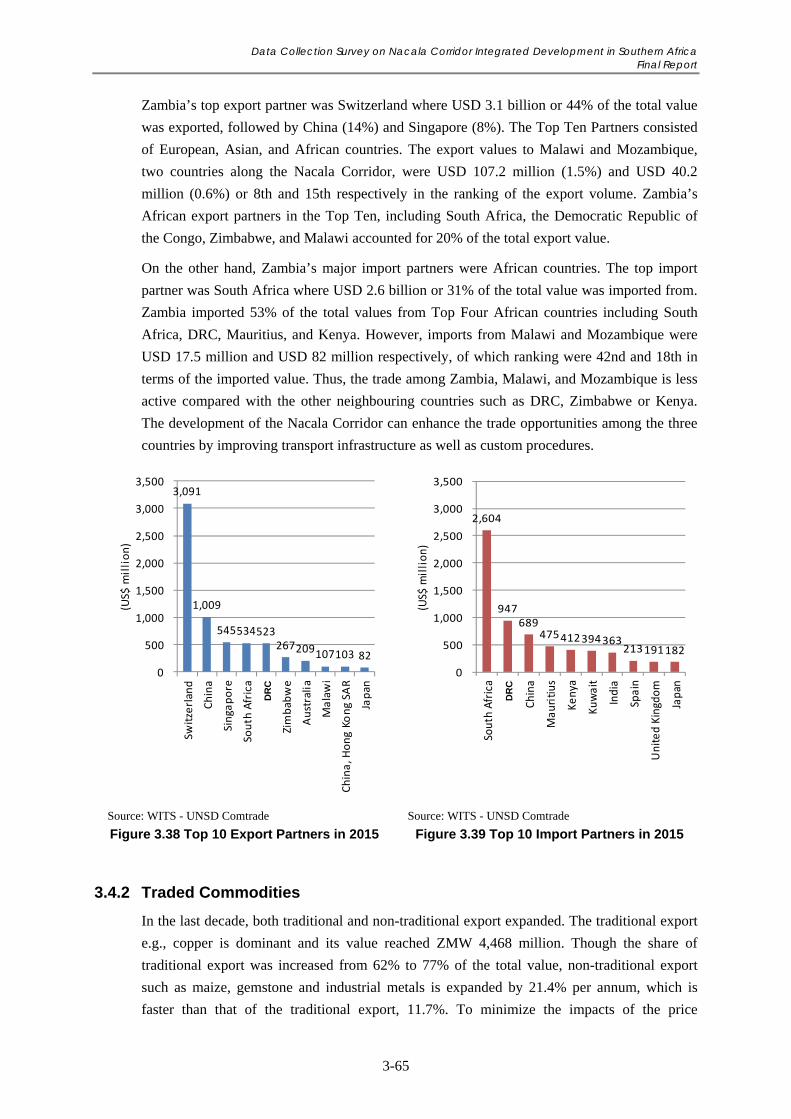

3.4.2 Traded Commodities ................................................................................................... 3-65

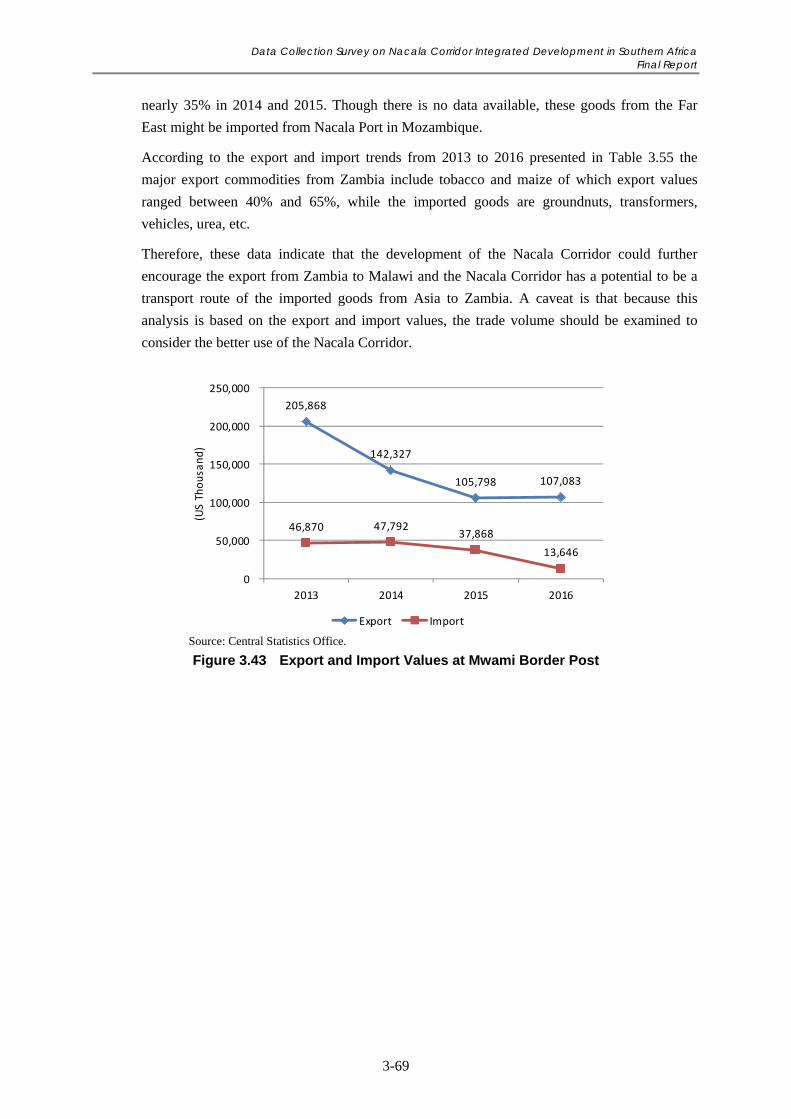

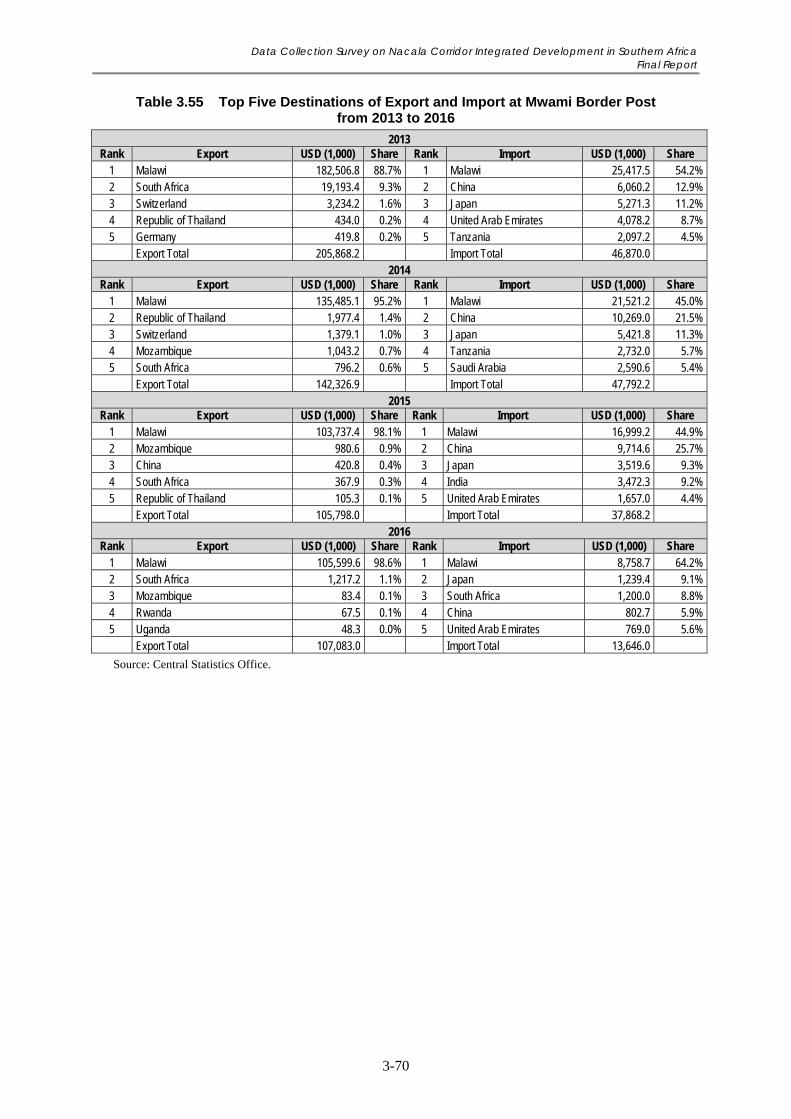

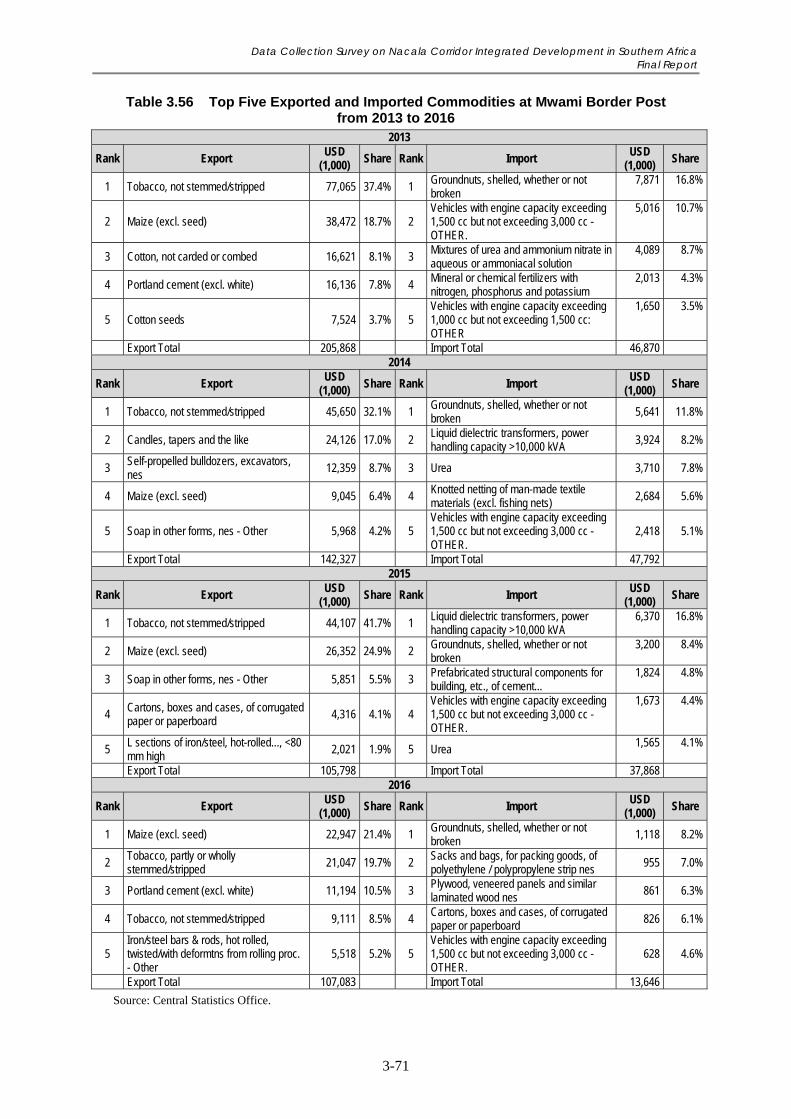

3.4.3 Trade Along Nacala Corridor ...................................................................................... 3-68

3.4.4 Development Potential and Challenges of the Trade Sector

in the Nacala Corridor Region .................................................................................... 3-72

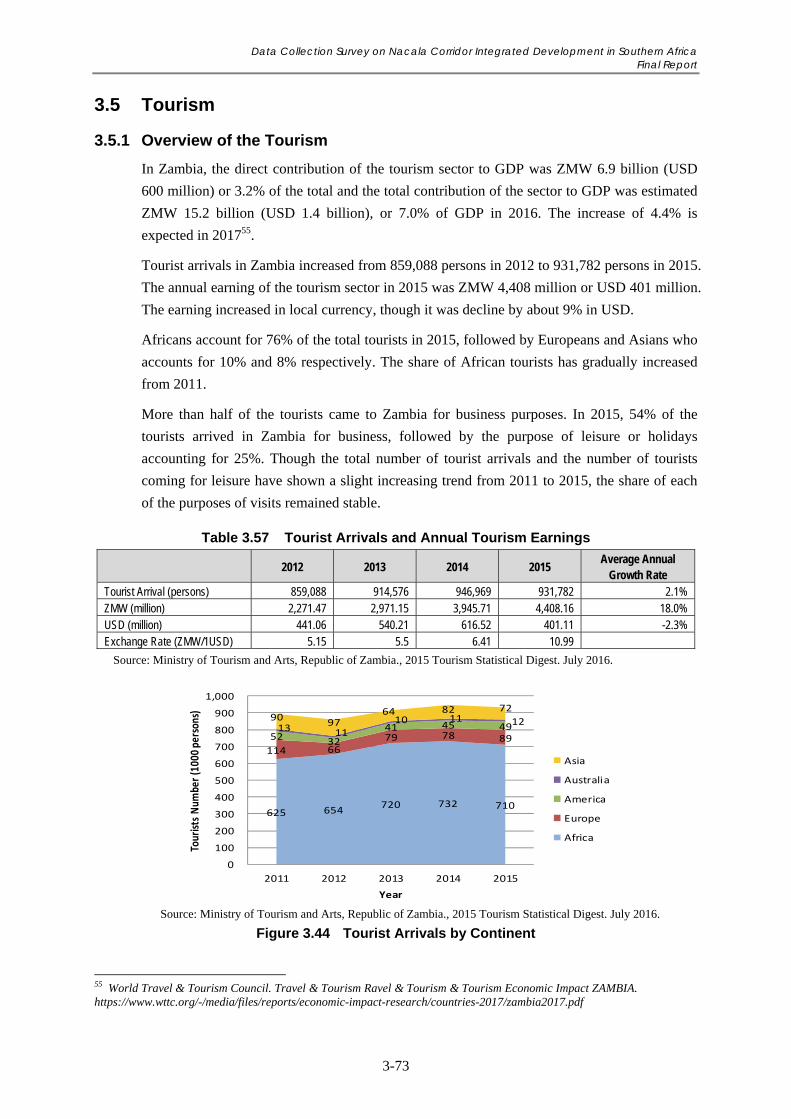

3.5 Tourism ............................................................................................................................. 3-73

3.5.1 Overview of the Tourism ............................................................................................. 3-73

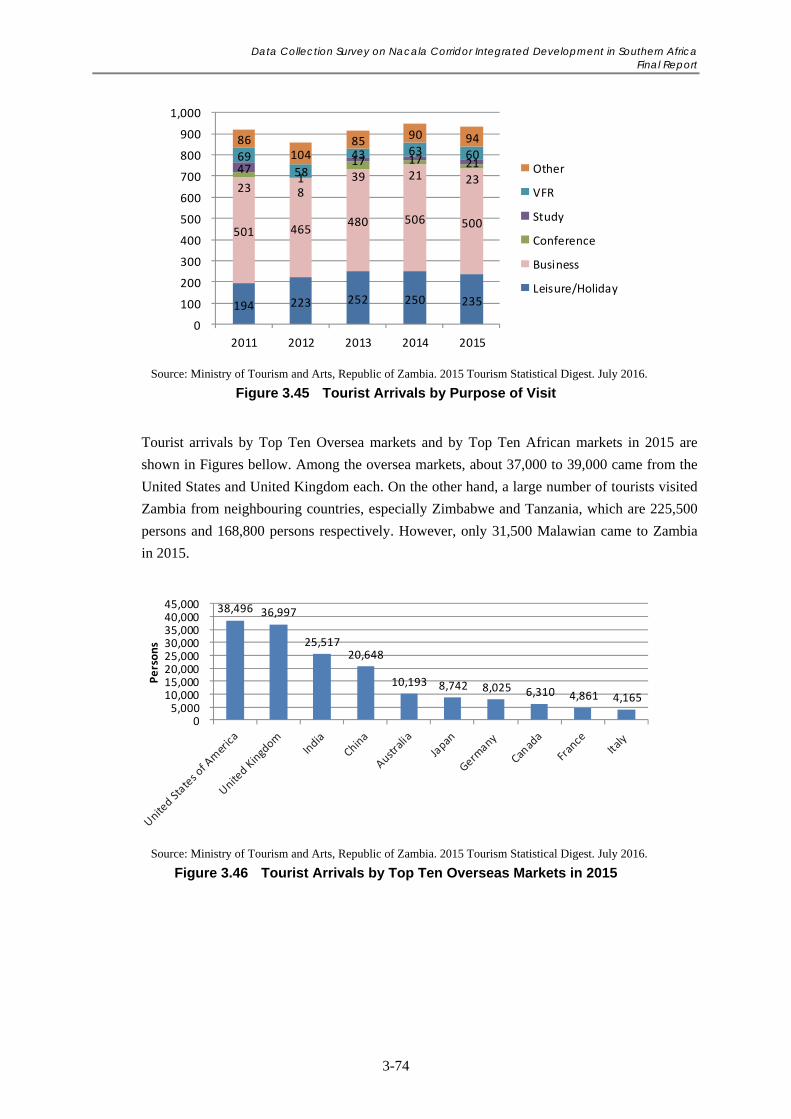

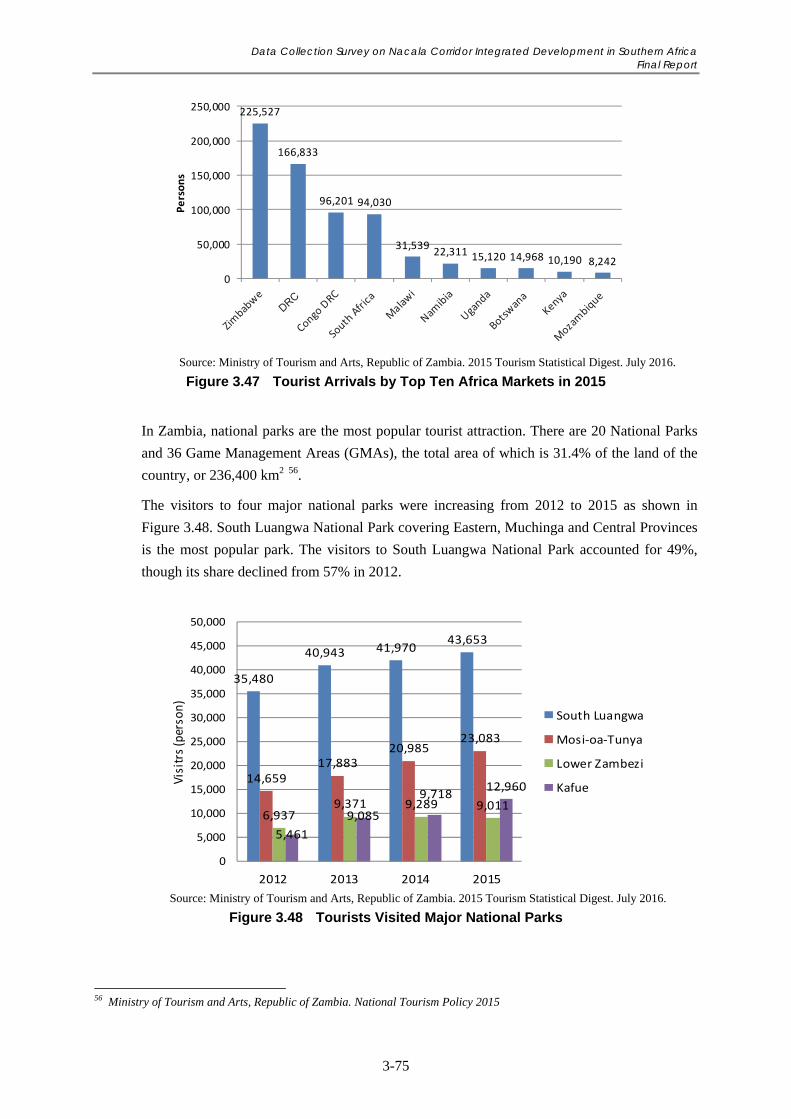

3.5.2 Tourism Sector of the Nacala Corridor Region ........................................................... 3-76

3.5.3 Policy Direction and Challenges of Tourism Sector ................................................... 3-78

3.5.4 Development Potential and Challenges of the Tourism Sector in the Nacala

Corridor Region .......................................................................................................... 3-79

3.6 Energy .............................................................................................................................. 3-80

3.6.1 Current Situations of the Electricity Sub-Sector ......................................................... 3-80

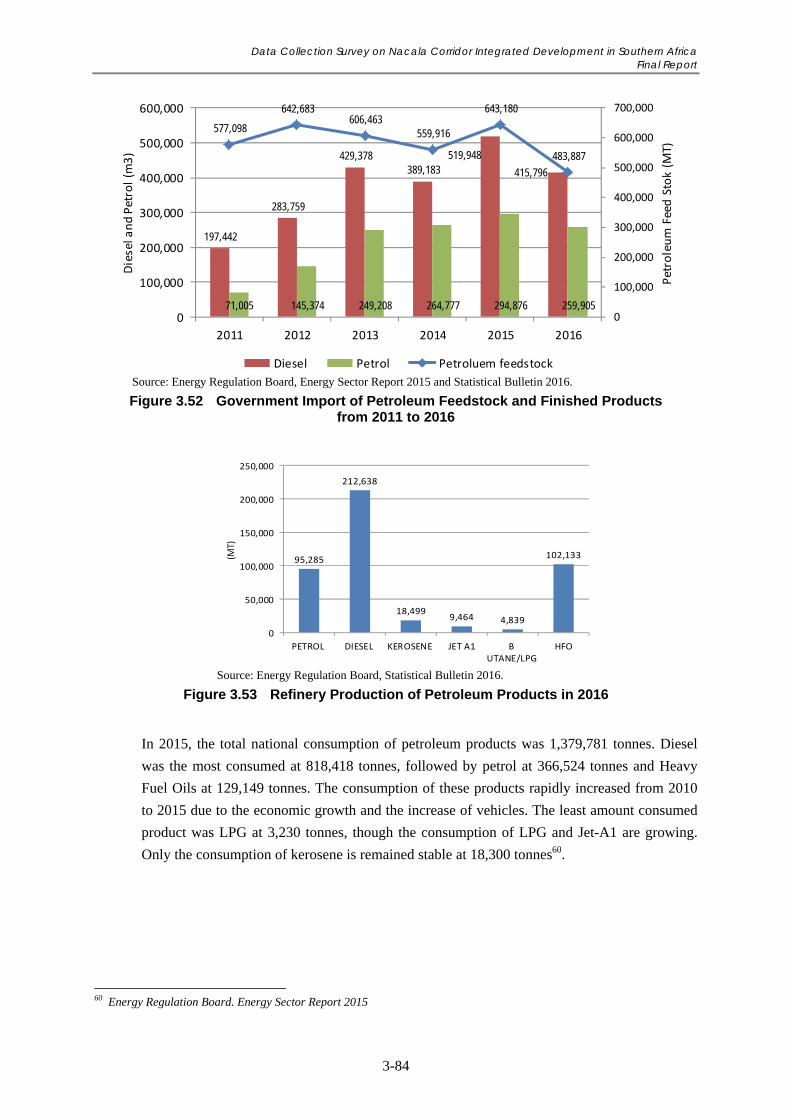

3.6.2 Current Situations of the Petroleum Sub-Sector ......................................................... 3-83

3.6.3 Development Potential and Challenges of the Energy Sector ..................................... 3-85

3.7 Foreign and Domestic Investment .................................................................................... 3-87

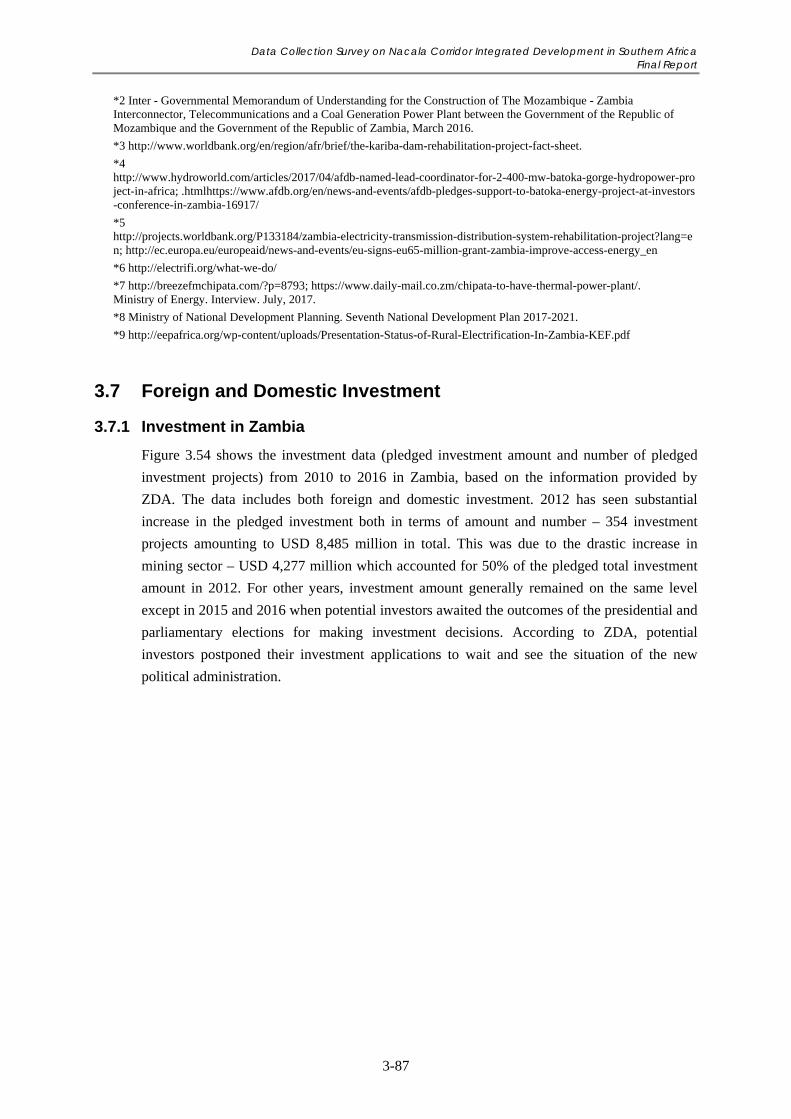

3.7.1 Investment in Zambia .................................................................................................. 3-87

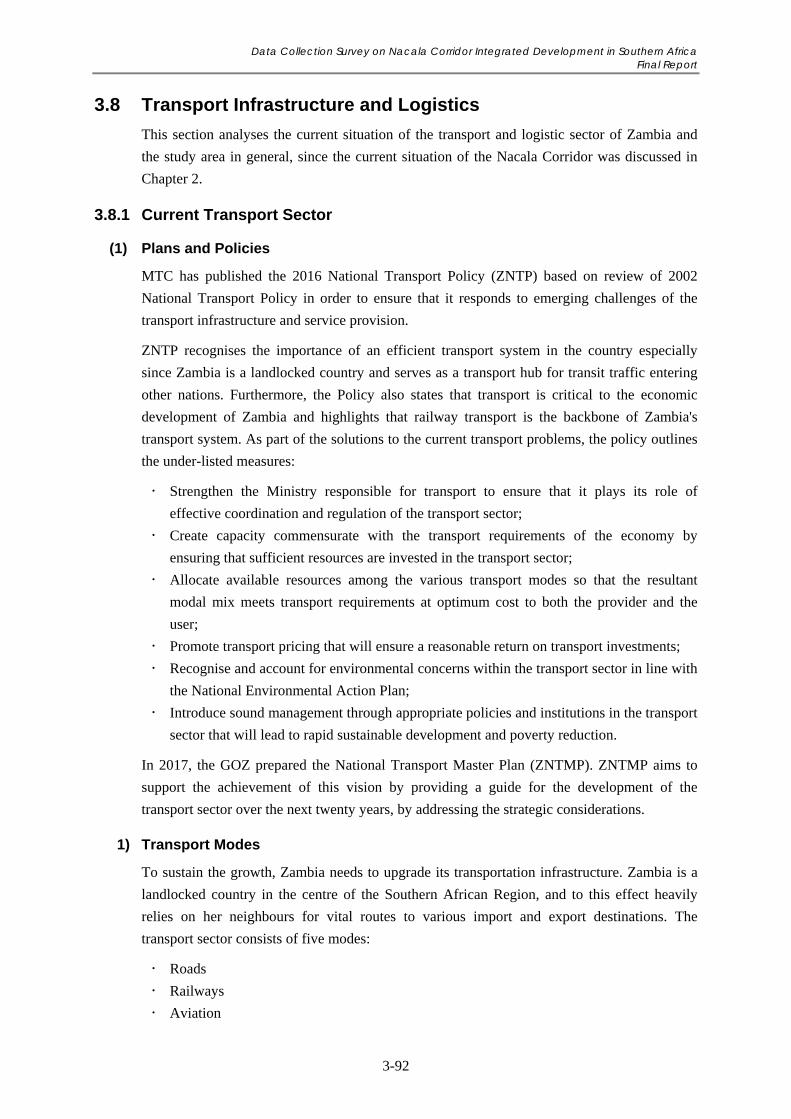

3.7.2 Investment in Eastern Province ................................................................................... 3-90

3.8 Transport Infrastructure and Logistics ............................................................................. 3-92

3.8.1 Current Transport Sector ............................................................................................. 3-92

3.8.2 Road Sub-Sector .......................................................................................................... 3-93

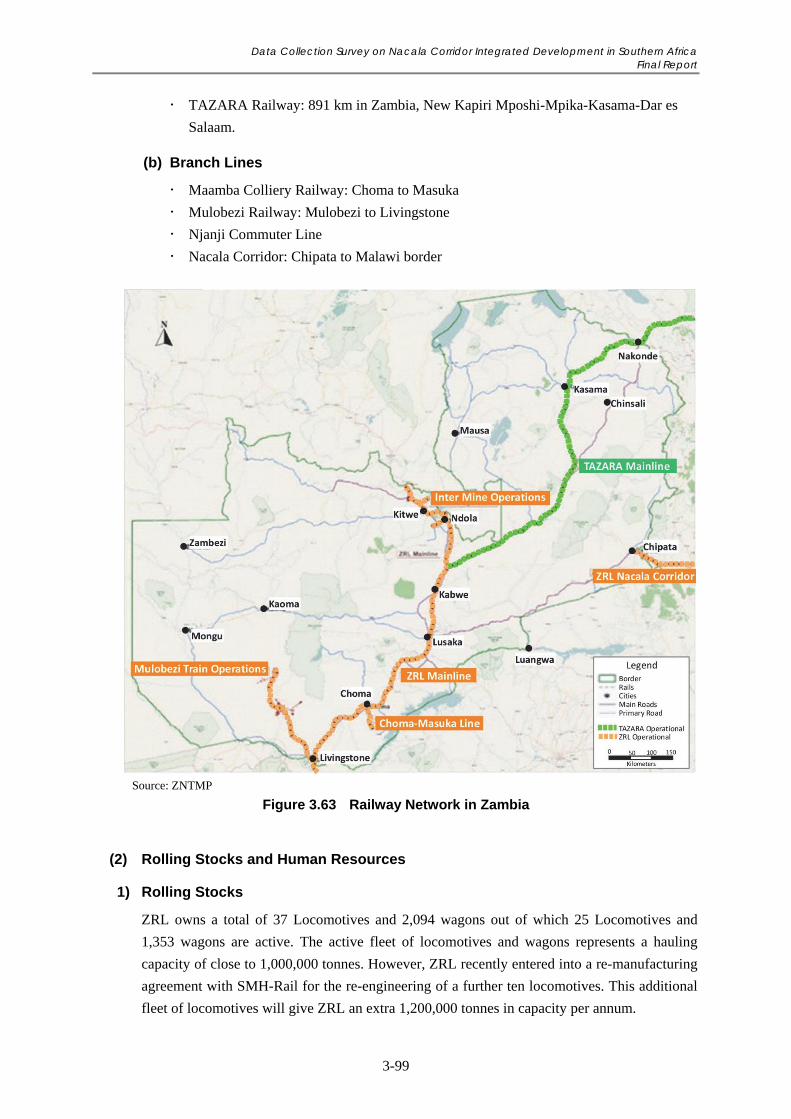

3.8.3 Rail Sub-Sector ........................................................................................................... 3-98

3.8.4 Aviation Sub-Sector .................................................................................................. 3-102

3.8.5 Waterway Sub-Sector ................................................................................................ 3-104

Chapter 4 Present Condition of Malawi ...................................................................................... 4-1

4.1 Agriculture.......................................................................................................................... 4-2

4.1.1 Overview of the Agriculture .......................................................................................... 4-2

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

iii

4.1.2 Agriculture Condition ................................................................................................... 4-2

4.1.3 Structure of Agriculture Producers ................................................................................ 4-5

4.1.4 Current Situation of Agriculture Production and Distribution ...................................... 4-6

4.1.5 Agribusiness Clusters and Players .............................................................................. 4-11

4.1.6 Related Policies, Programmes and Projects ................................................................ 4-13

4.1.7 Development Potential and Challenges of Agriculture and Agribusiness Sector ........ 4-20

4.2 Industry ............................................................................................................................. 4-43

4.2.1 Overview of the Industry ............................................................................................. 4-43

4.2.2 Current Condition and Potential of Industrial Development Along Nacala

Corridor ....................................................................................................................... 4-44

4.3 Mining .............................................................................................................................. 4-45

4.3.1 Overview of the Mining .............................................................................................. 4-45

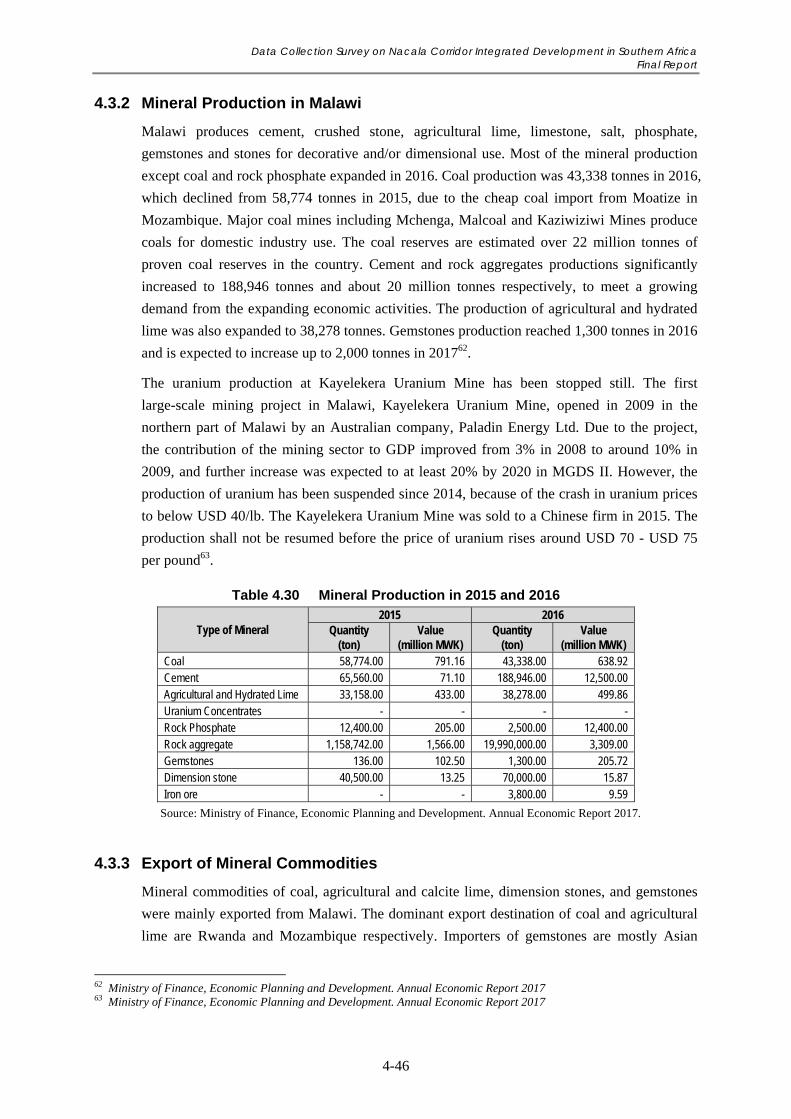

4.3.2 Mineral Production in Malawi .................................................................................... 4-46

4.3.3 Export of Mineral Commodities ................................................................................. 4-46

4.3.4 Government Policy of Mining Sector ......................................................................... 4-47

4.3.5 Increased Mining Projects in Recent Years ................................................................. 4-48

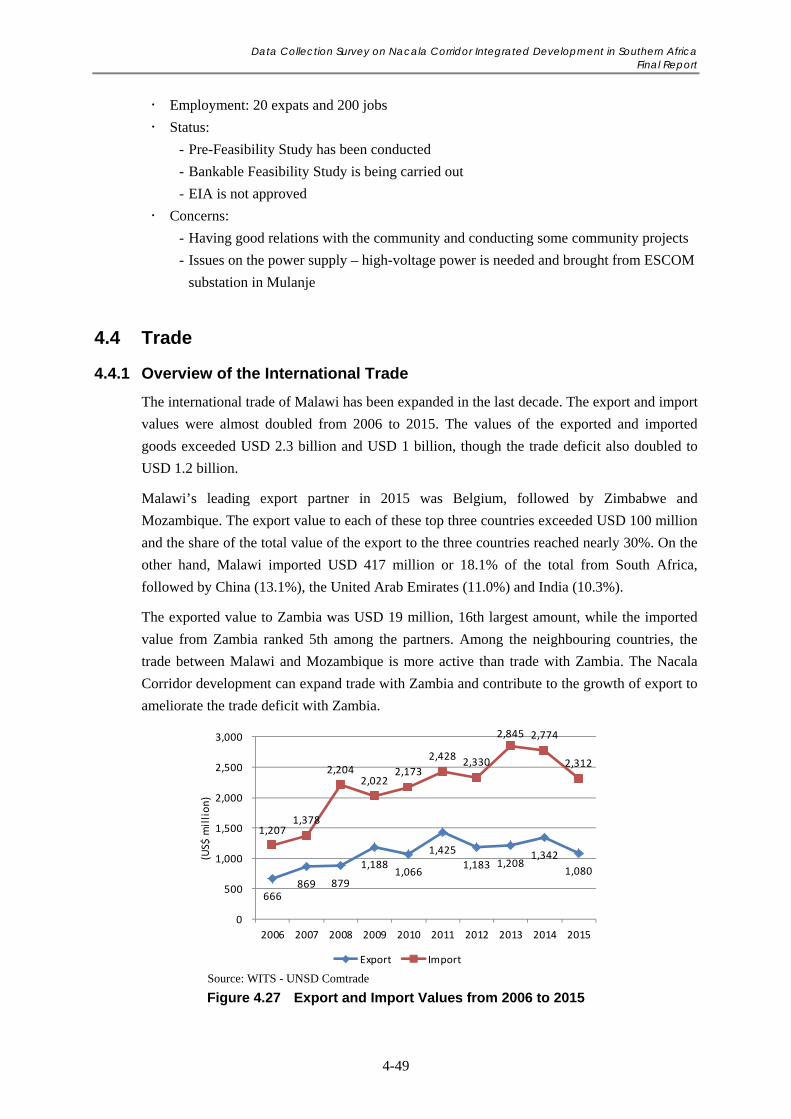

4.4 Trade ................................................................................................................................. 4-49

4.4.1 Overview of the International Trade ........................................................................... 4-49

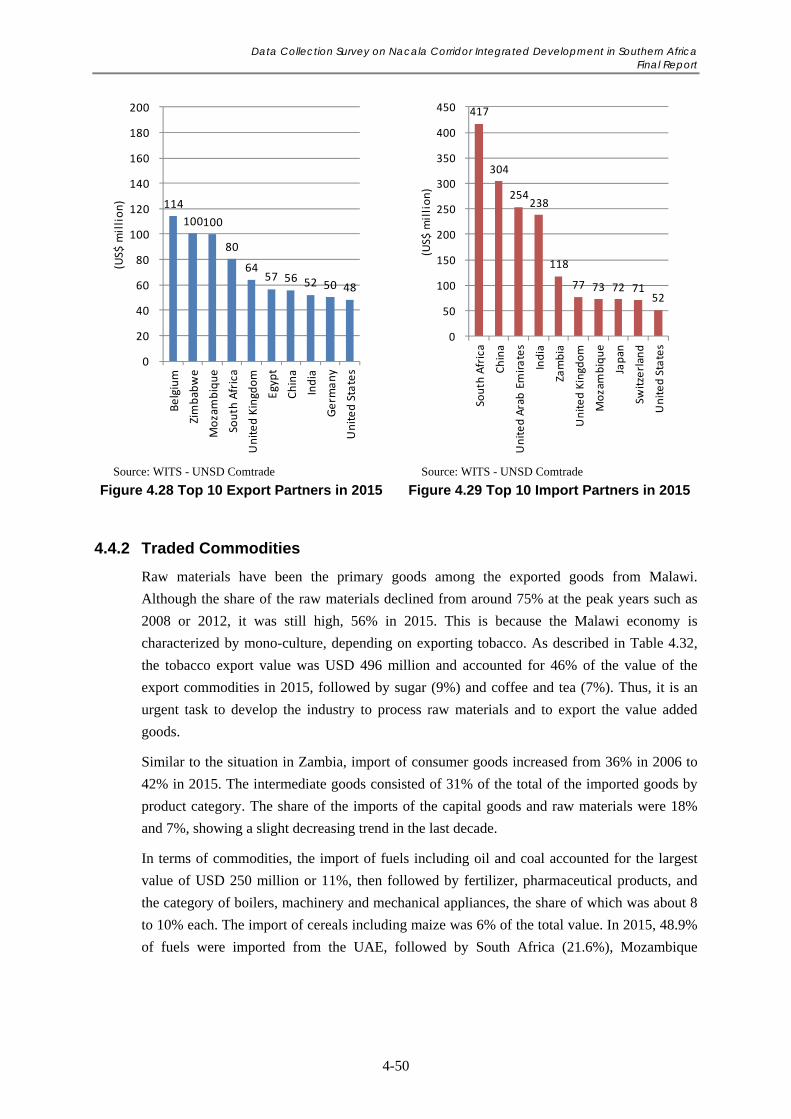

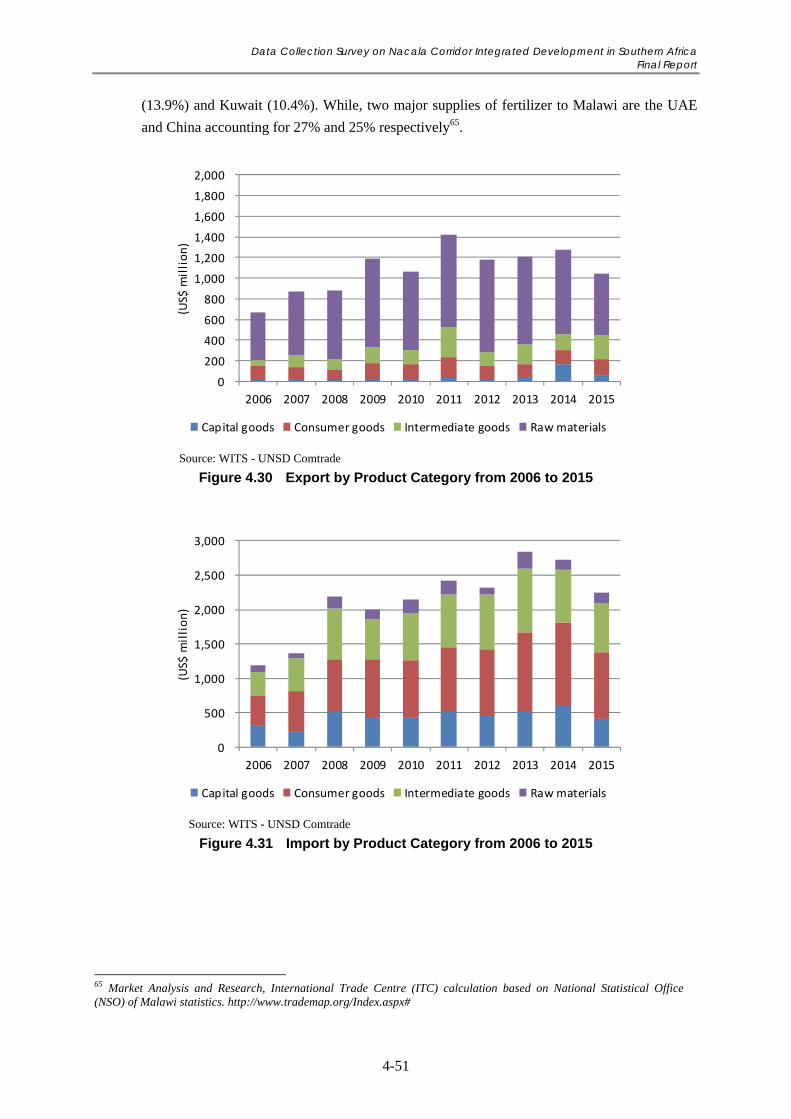

4.4.2 Traded Commodities ................................................................................................... 4-50

4.4.3 Development Potential and Challenges of the Trade Sector in the Nacala

Corridor Region .......................................................................................................... 4-53

4.5 Tourism ............................................................................................................................. 4-53

4.5.1 Overview of the Tourism ............................................................................................. 4-53

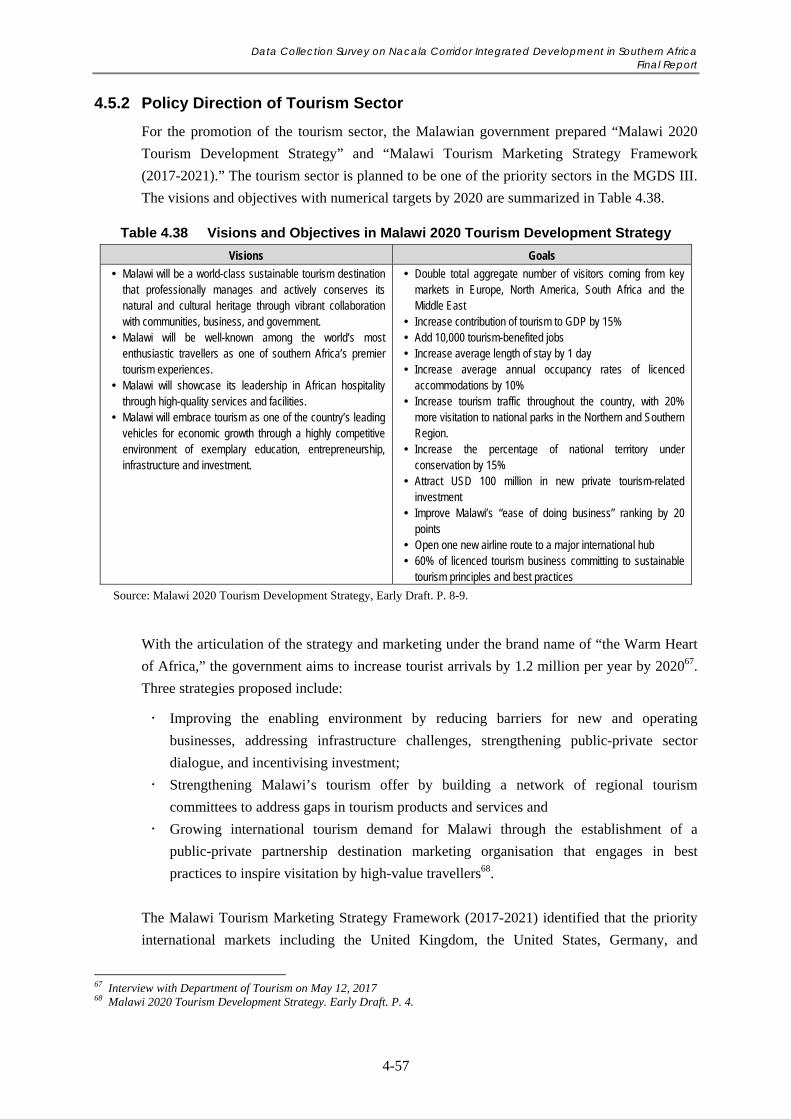

4.5.2 Policy Direction of Tourism Sector ............................................................................. 4-57

4.5.3 Development Potential and Challenges of the Tourism Sector in the Nacala

Corridor Region .......................................................................................................... 4-58

4.6 Energy .............................................................................................................................. 4-59

4.6.1 Current Situations of the Electricity Sub-Sector ......................................................... 4-59

4.6.2 Current Situations of the Liquid Fuel and Gas Sub-Sector ......................................... 4-61

4.6.3 Development Potential and Challenges of the Energy Sector ..................................... 4-63

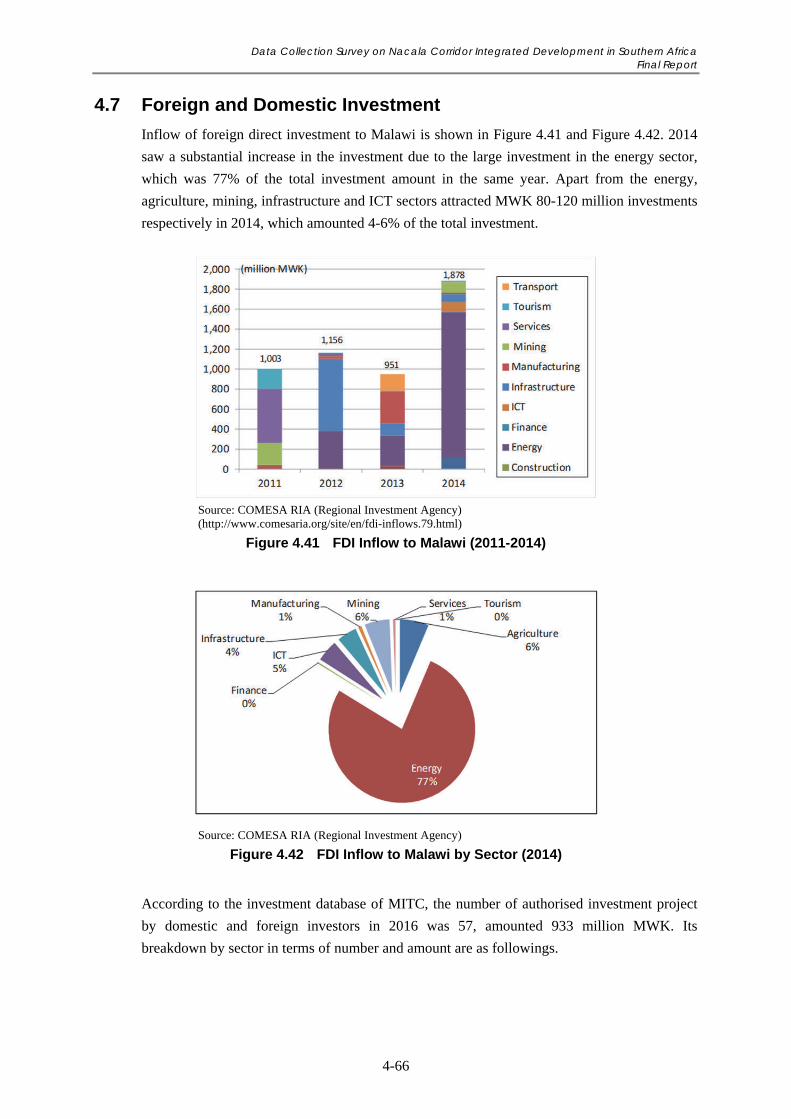

4.7 Foreign and Domestic Investment .................................................................................... 4-66

4.8 Transport Infrastructure and Logistics ............................................................................. 4-68

4.8.1 Current Transport Sector ............................................................................................. 4-68

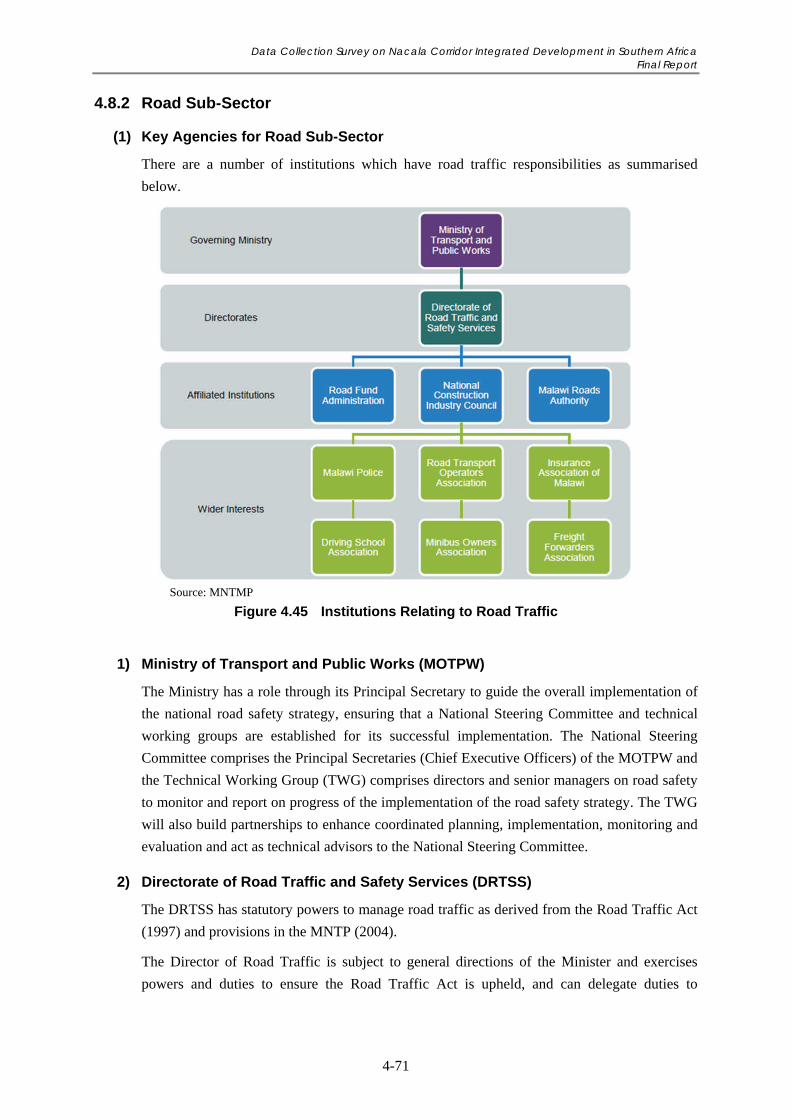

4.8.2 Road Sub-Sector .......................................................................................................... 4-71

4.8.3 Rail Sub-Sector ........................................................................................................... 4-77

4.8.4 Aviation Sub-Sector .................................................................................................... 4-83

4.8.5 Waterway Sub-Sector .................................................................................................. 4-84

Chapter 5 Overall Issues and Impact Analysis of Nacala Corridor Development .................. 5-1

5.1 Evaluation of Relevance of Nacala Corridor Development to Existing Policies

and Plans ............................................................................................................................ 5-1

5.1.1 Zambia’s National Development Plan and Nacala Corridor ......................................... 5-1

5.1.2 Zambia’s National Transport Policy (ZNTP) and Nacala Corridor ............................... 5-3

5.1.3 Zambia’s Budget Allocation Related Nacala Corridor Development ........................... 5-3

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

iv

5.1.4 Malawi Growth and Development Strategy (MGDS) III and Nacala Corridor ............ 5-6

5.1.5 Malawi’s National Transport Policy and Nacala Corridor ............................................ 5-7

5.1.6 Malawi’s National Transport Master Plan (MNTMP) and Nacala Corridor ................. 5-8

5.1.7 Malawi’s Budget Allocation Related Nacala Corridor Development ........................... 5-9

5.1.8 Regional Economic Integration Policy and Nacala Corridor ...................................... 5-12

5.2 Possible Driving Forces for Nacala Corridor Development ............................................. 5-14

5.2.1 Zambia ......................................................................................................................... 5-14

5.2.2 Malawi ......................................................................................................................... 5-20

5.3 Overall Issues on Nacala Corridor Development ............................................................. 5-24

5.3.1 Issues on Nacala Corridor Transport ........................................................................... 5-24

5.3.2 Issues on Economic Sectors ........................................................................................ 5-26

5.3.3 Issues on the Relationship Between Corridor Transport and Economic Sectors ........ 5-29

5.3.4 Issues on Regional Economic Integration ................................................................... 5-30

5.4 Impact Analysis ................................................................................................................ 5-31

5.4.1 Perspectives on Nacala Corridor Development ........................................................... 5-31

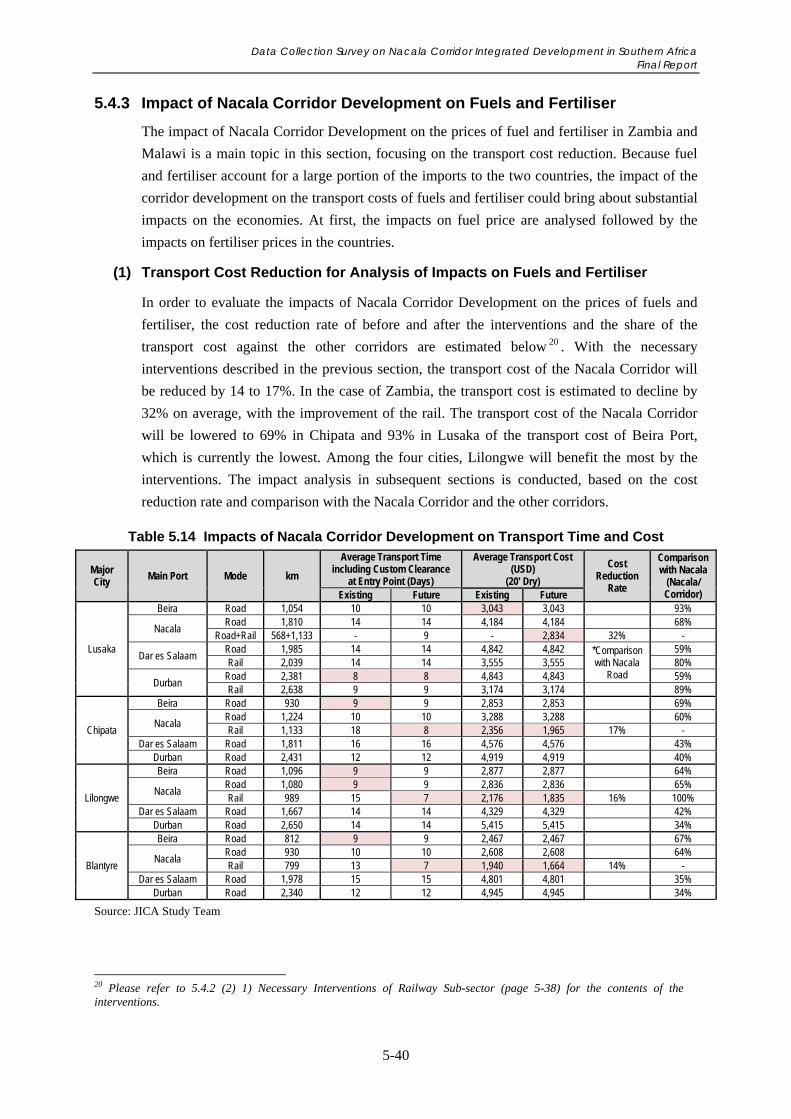

5.4.2 Impact of Railway Upgrading on Transport Cost ....................................................... 5-36

5.4.3 Impact of Nacala Corridor Development on Fuels and Fertiliser ............................... 5-40

5.4.4 Economic Impact on the Nacala Corridor Region ...................................................... 5-45

Chapter 6 Proposed Growth Scenarios of Zambia and Malawi Related

to Nacala Corridor Development .............................................................................. 6-1

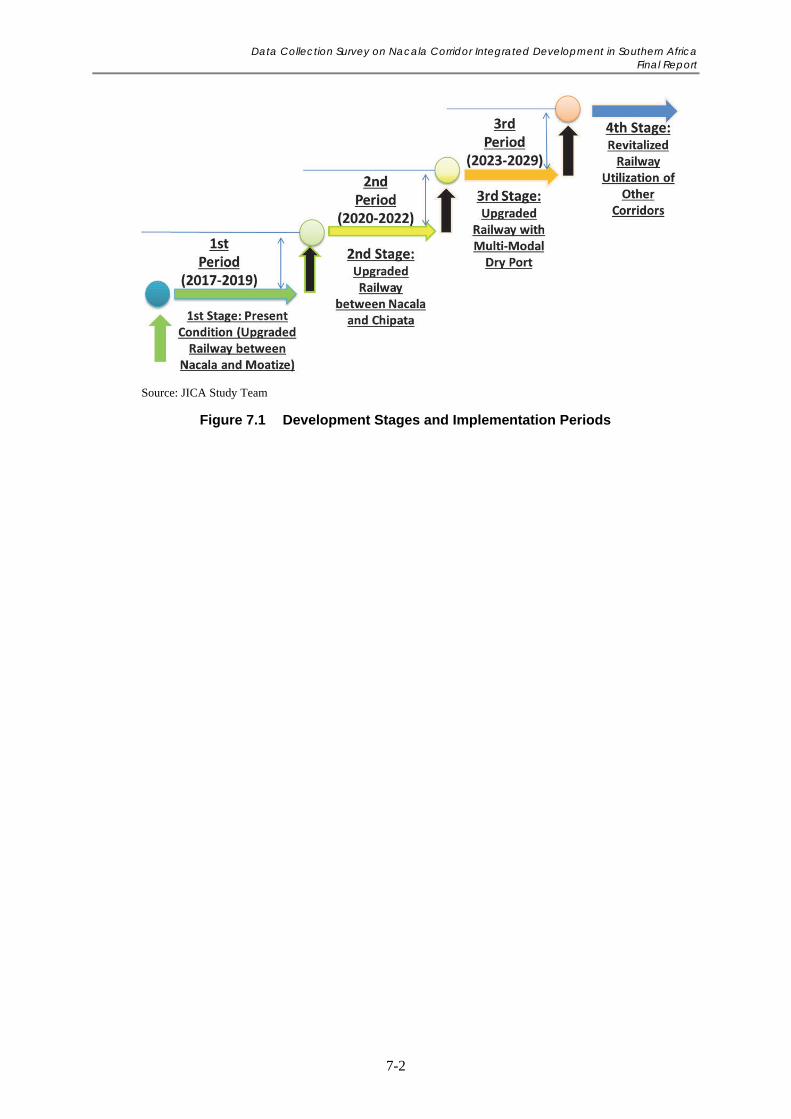

6.1 Introduction ........................................................................................................................ 6-1

6.2 Advantages of Nacala Corridor over Other Transport Corridors of Zambia

and Malawi ......................................................................................................................... 6-2

6.2.1 Emergence of Nacala Corridor as an Important Alternative Transport

Route ............................................................................................................................. 6-2

6.2.2 Advantages of Nacala Corridor over Other Transport Corridors

for Zambia and Malawi ................................................................................................. 6-3

6.2.3 Impact of Advantageous Nacala Corridor with Planned Interventions

on Development of Economic Sectors .......................................................................... 6-9

6.3 Proposed Vision for Nacala Corridor Development ......................................................... 6-10

6.3.1 Proposed Vision on Nacala Corridor Development for Zambia, Malawi

and Mozambique ......................................................................................................... 6-10

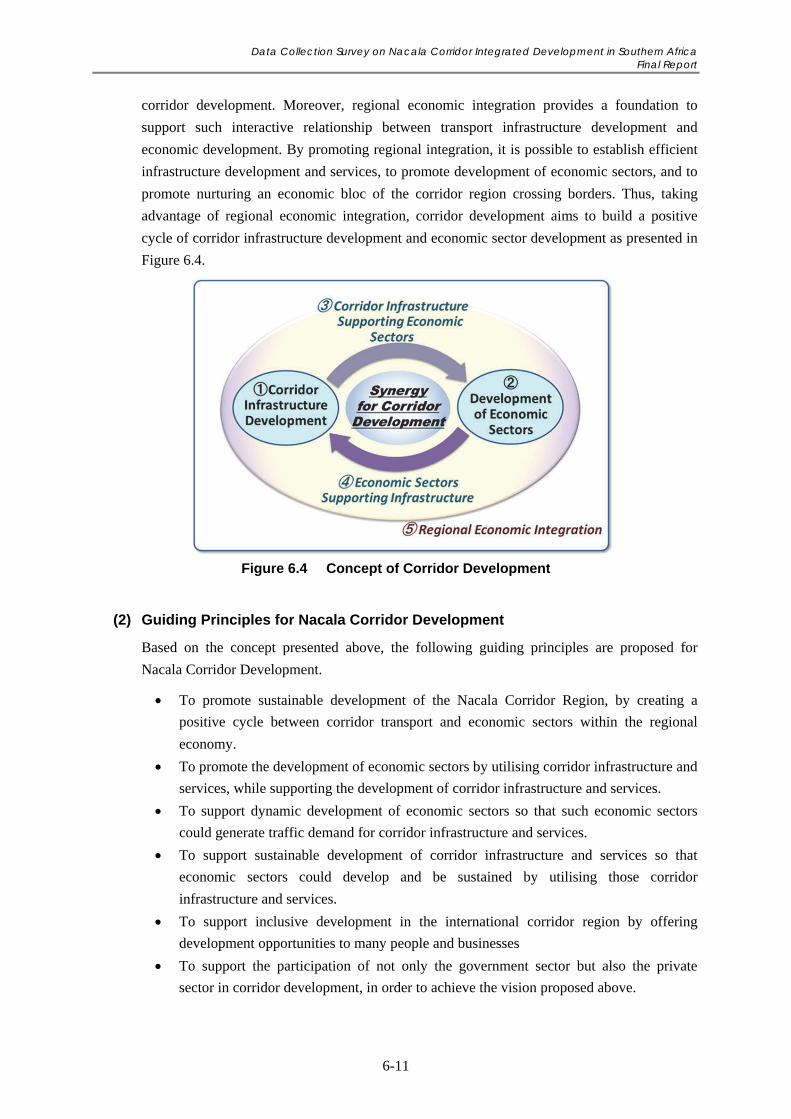

6.3.2 Nacala Corridor Development Concept and Guiding Principles ................................ 6-10

6.4 Basic Policies on the Utilisation of Nacala Corridor and Development

of Nacala Corridor Transport Infrastructure and Services ................................................ 6-12

6.4.1 Basic Policies on the Utilisation of Nacala Corridor .................................................. 6-12

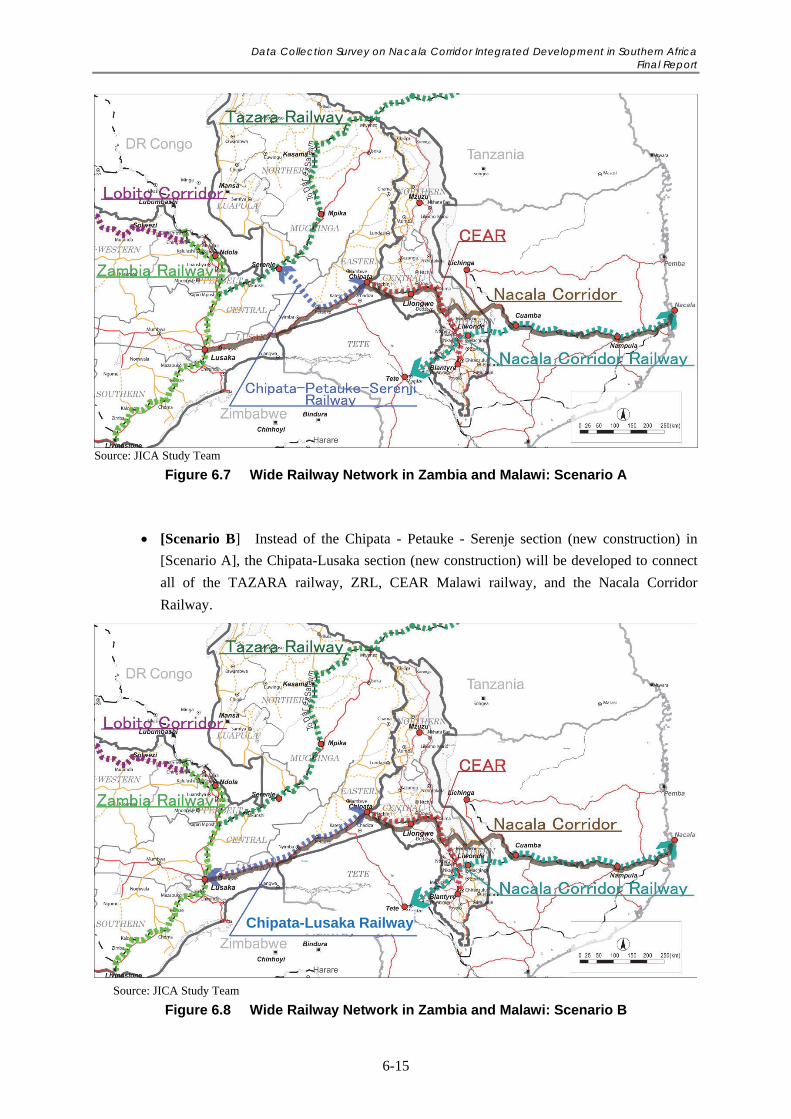

6.4.2 Selection of Development Scenario of Nacala Corridor Transport

Infrastructure and Services .......................................................................................... 6-14

6.5 Basic Policies on Priority Economic Sectors and Target Markets in Nacala

Corridor Development ...................................................................................................... 6-17

6.5.1 Increasing Importance of Regional Markets ............................................................... 6-17

6.5.2 Basic Policies for Development of Economic Sectors in Relation to the

Development of Nacala Corridor Transport Infrastructure ......................................... 6-17

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

v

6.5.3 Priority Economic Sectors to be Promoted in Relation to Nacala Corridor

Transport Infrastructure Development ........................................................................ 6-18

6.6 Strategies and Four Stages for Development of Nacala Corridor Transport

Infrastructure and Services ............................................................................................... 6-21

6.6.1 1st Stage (Present Situation) and 2nd Stage of Development of Nacala

Corridor Transport Infrastructure and Services ........................................................... 6-21

6.6.2 3rd Stage and 4th Stage of Development of Nacala Corridor Transport

Infrastructure and Services .......................................................................................... 6-21

6.7 Zambia’s Strategies for Promoting Development of Potential Economic Sectors

in Relation to Nacala Corridor Development ................................................................... 6-23

6.7.1 Zambia’s Strategies for Promoting Development of Potential Economic

Sectors by Taking Advantage of the Upgraded Nacala Corridor ................................ 6-23

6.7.2 Zambia’s Potential Economic Sectors Related to Nacala Corridor Development ...... 6-25

6.7.3 Description of Potential Economic Sectors of Zambia and Key Points

for Promoting Development of Potential Economic Sectors of Zambia ..................... 6-27

6.8 Malawi’s Strategies for Promoting Development of Potential Economic Sectors

in Relation to Nacala Corridor Transport Development ................................................... 6-32

6.8.1 Malawi’s Strategies for Promoting Development of Potential Economic

Sectors in Relation to Nacala Corridor Transport Development ................................. 6-32

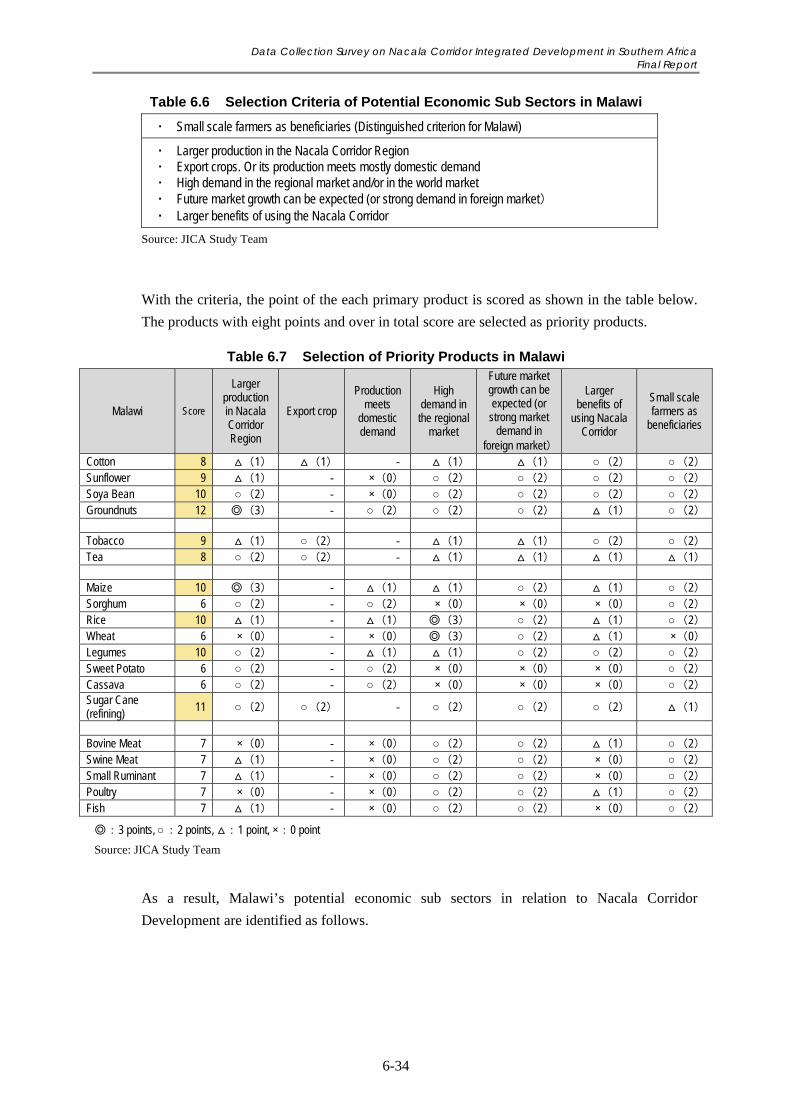

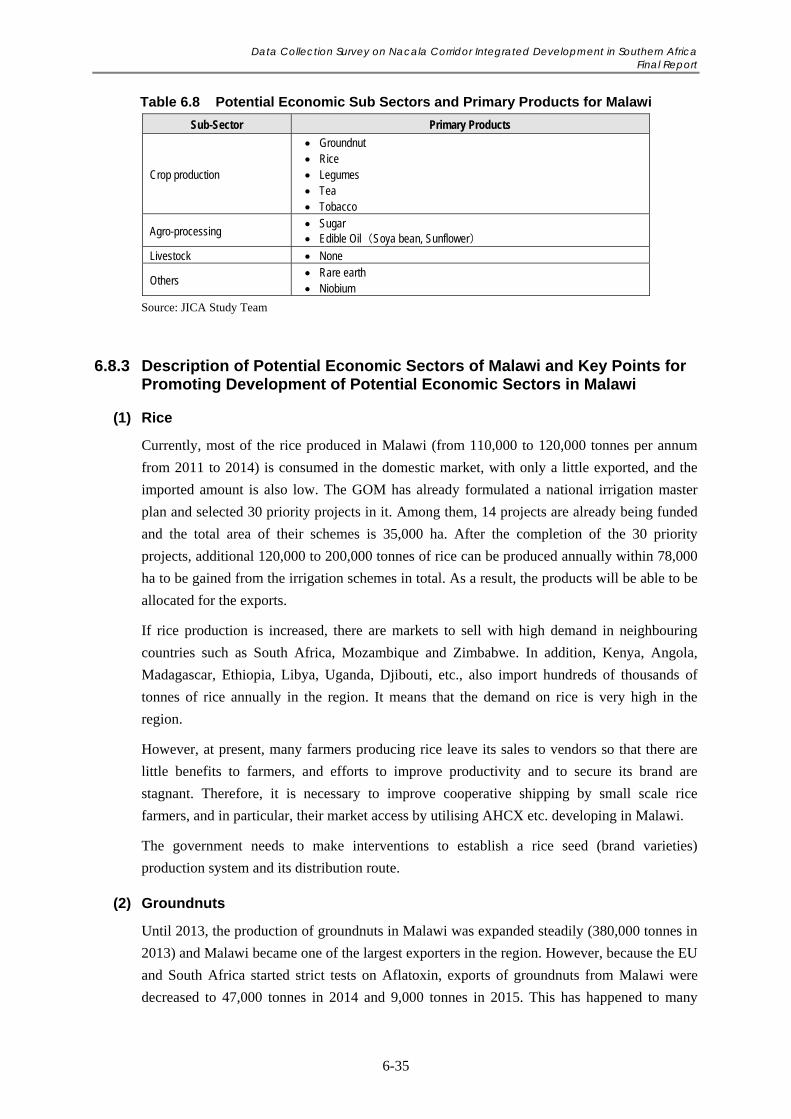

6.8.2 Malawi’s Potential Economic Sectors Related to Nacala Corridor Development ...... 6-33

6.8.3 Description of Potential Economic Sectors of Malawi and Key Points

for Promoting Development of Potential Economic Sectors in Malawi ..................... 6-35

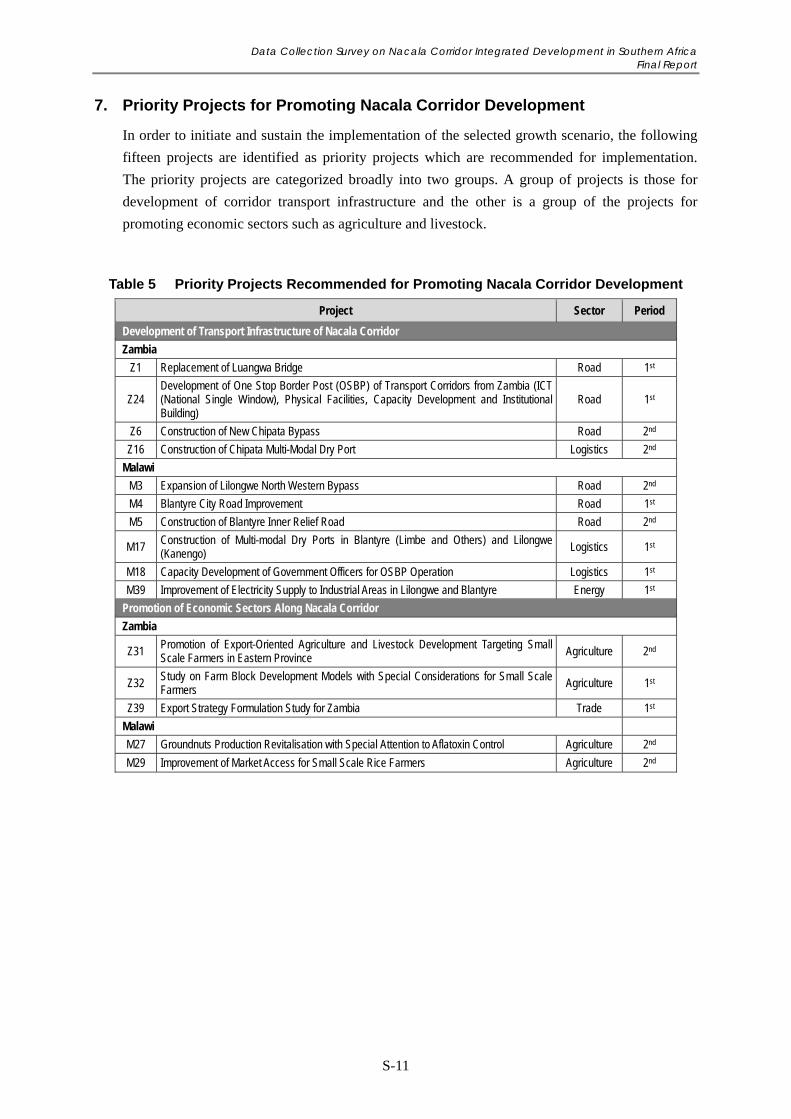

Chapter 7 Priority Projects Proposed for Promoting Nacala Corridor Development ............ 7-1

7.1 A Long List of Projects ...................................................................................................... 7-1

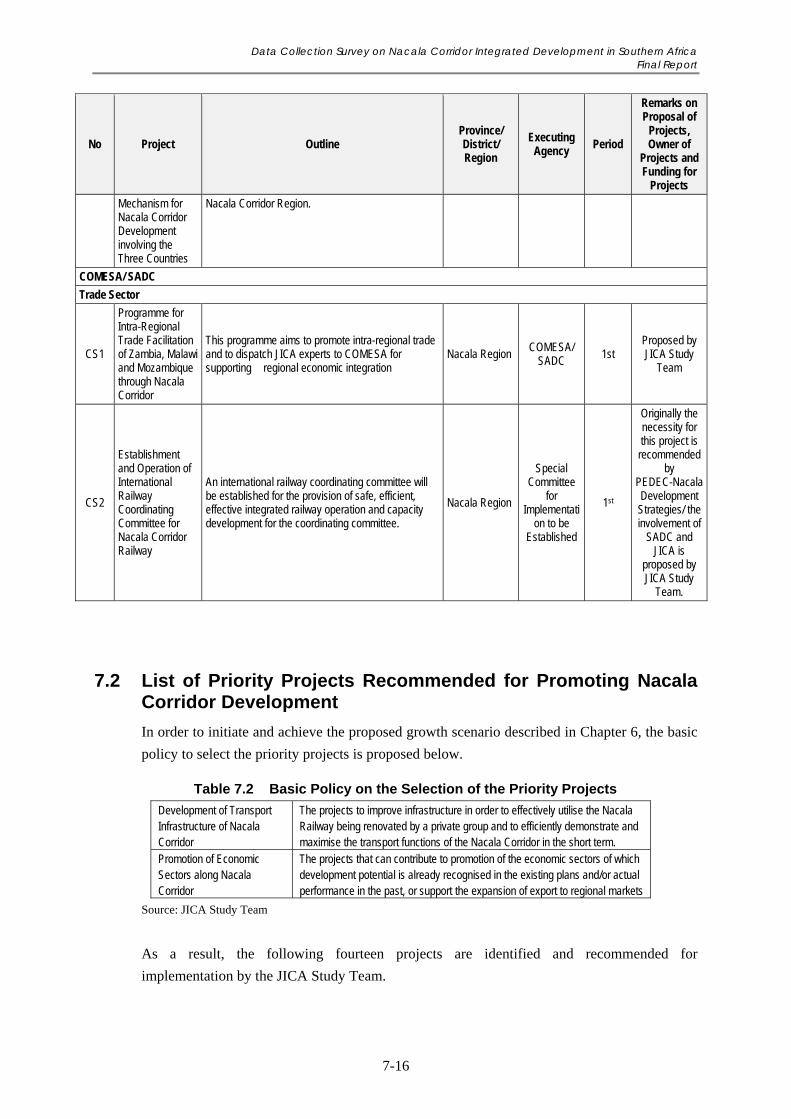

7.2 List of Recommended Priority Projects Promoting Nacala Corridor Development ........ 7-16

7.3 Brief Profiles of Priority Projects Recommended for Promoting Nacala

Corridor Development ...................................................................................................... 7-17

7.3.1 Development of Transport Infrastructure of Nacala Corridor ..................................... 7-17

7.3.2 Promotion of Economic Sectors Along Nacala Corridor ............................................ 7-27

Appendix for Chapter 7: Points to be Considered for Farming Plan .......................................... 7-36

ANNEX : Records of the Seminars

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

vi

LIST OF TABLES Page

Table 1.1 Study Area (Nacala Corridor Region in Zambia and Malawi) ............................................... 1-2

Table 1.2 List of Main Counterpart Agencies for the Study ................................................................... 1-3

Table 2.1 Distance between Major Cities and Main Ports .................................................................... 2-16

Table 2.2 Border Freight Traffic for Zambia and Malawi in 2015 ....................................................... 2-18

Table 2.3 Freight Share per Corridor for Zambia (Year 2016) ............................................................. 2-20

Table 2.4 Freight Share per Corridor for Malawi (Year 2016) ............................................................. 2-21

Table 2.5 Freight Movement on Nacala Corridor in Zambia ................................................................ 2-22

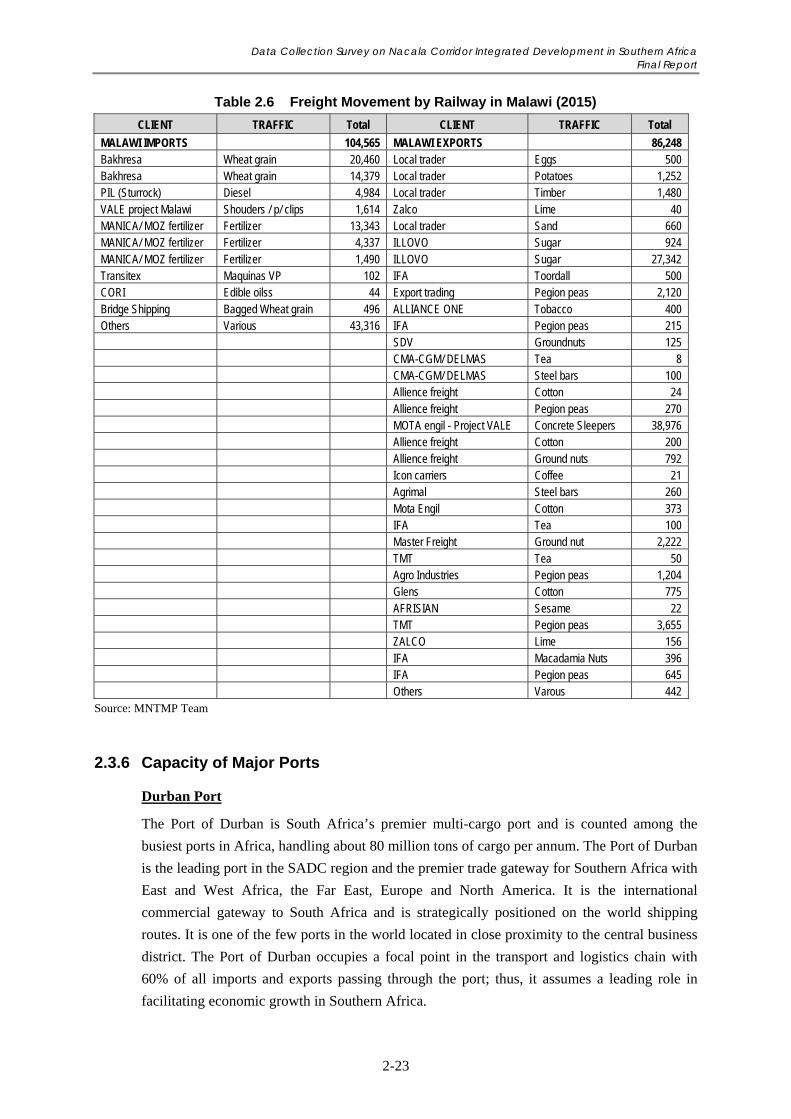

Table 2.6 Freight Movement by Railway in Malawi (2015) ................................................................ 2-23

Table 2.7 Outline of the Capacity of the Major Ports ........................................................................... 2-25

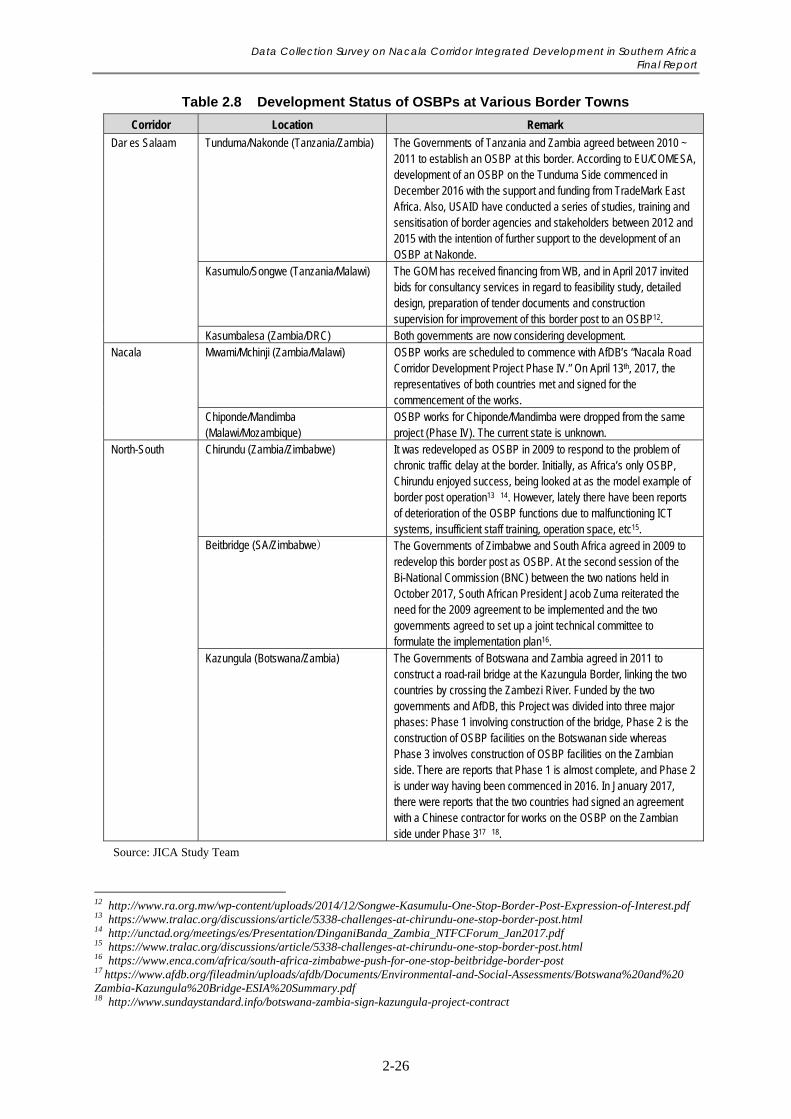

Table 2.8 Development Status of OSBPs at Various Border Towns .................................................... 2-26

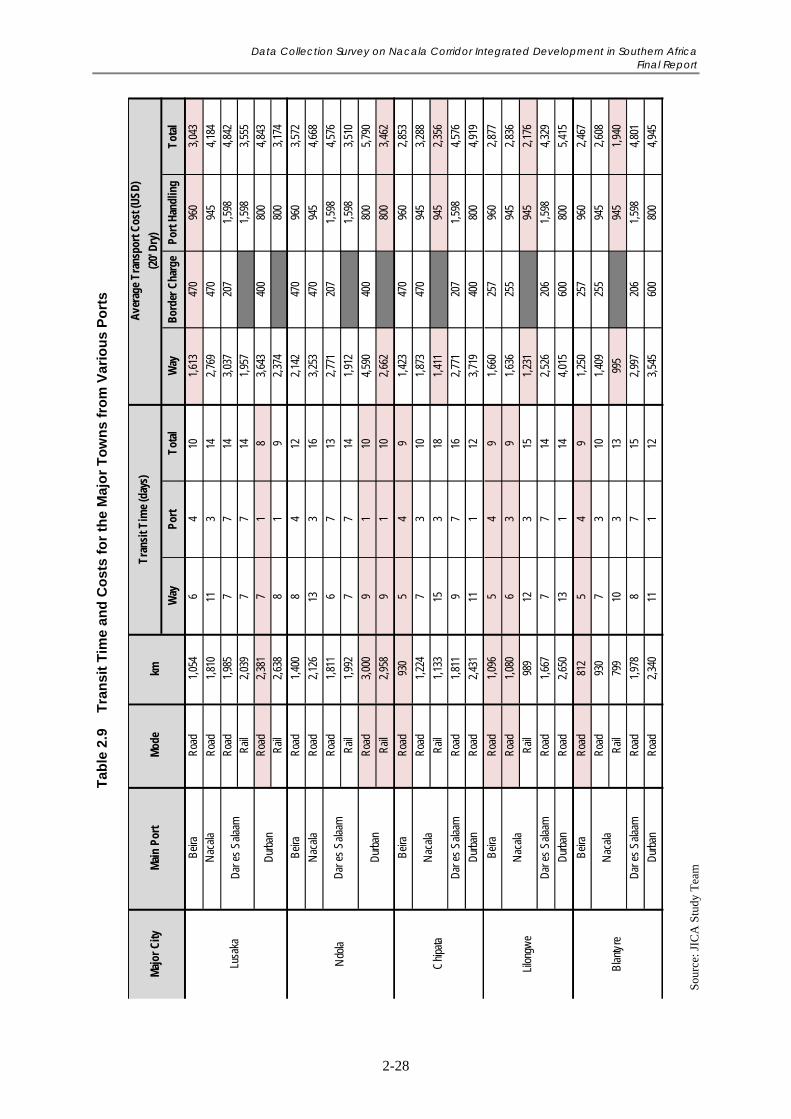

Table 2.9 Transit Time and Costs for the Major Towns from Various Ports ....................................... 2-28

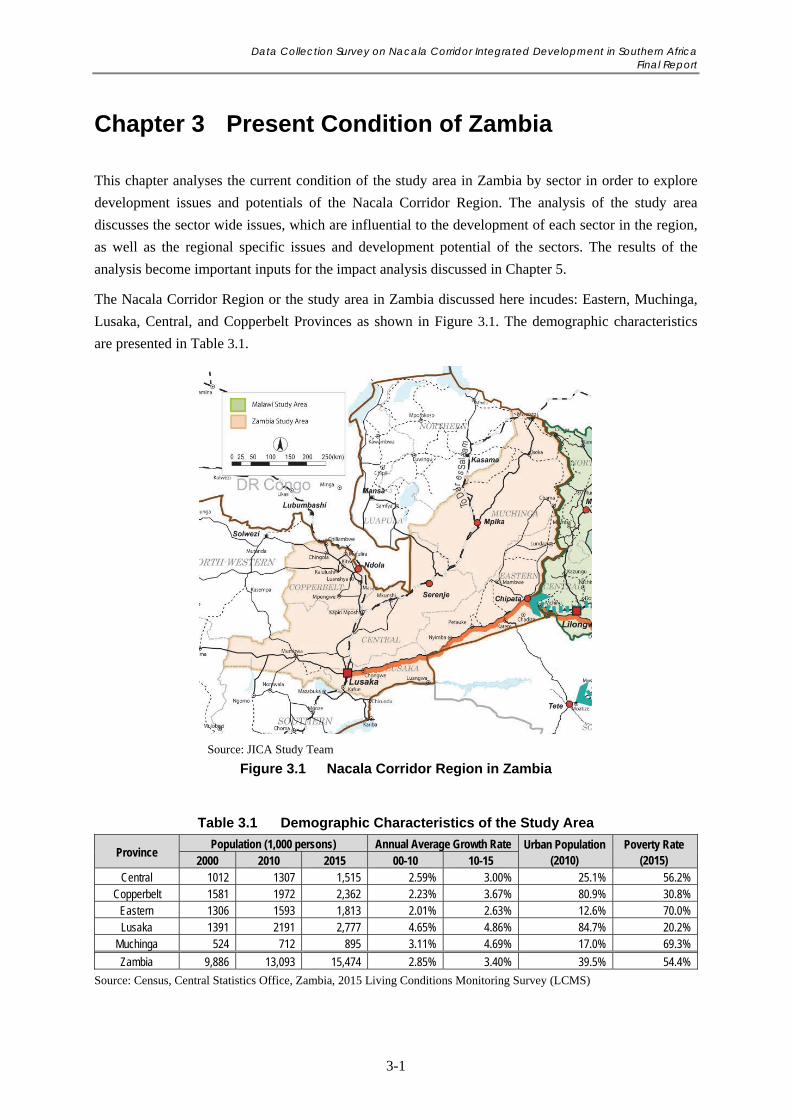

Table 3.1 Demographic Characteristics of the Study Area ..................................................................... 3-1

Table 3.2 Agriculture Products by Agro-ecological Region ................................................................... 3-3

Table 3.3 Farm Structure in Zambia (2016) ........................................................................................... 3-5

Table 3.4 Category of Producers inside of Farm Block ........................................................................ 3-15

Table 3.5 Roles of the three Committees for Screening the Investment Plans ..................................... 3-15

Table 3.6 Progress of the Farm Block Development ............................................................................ 3-16

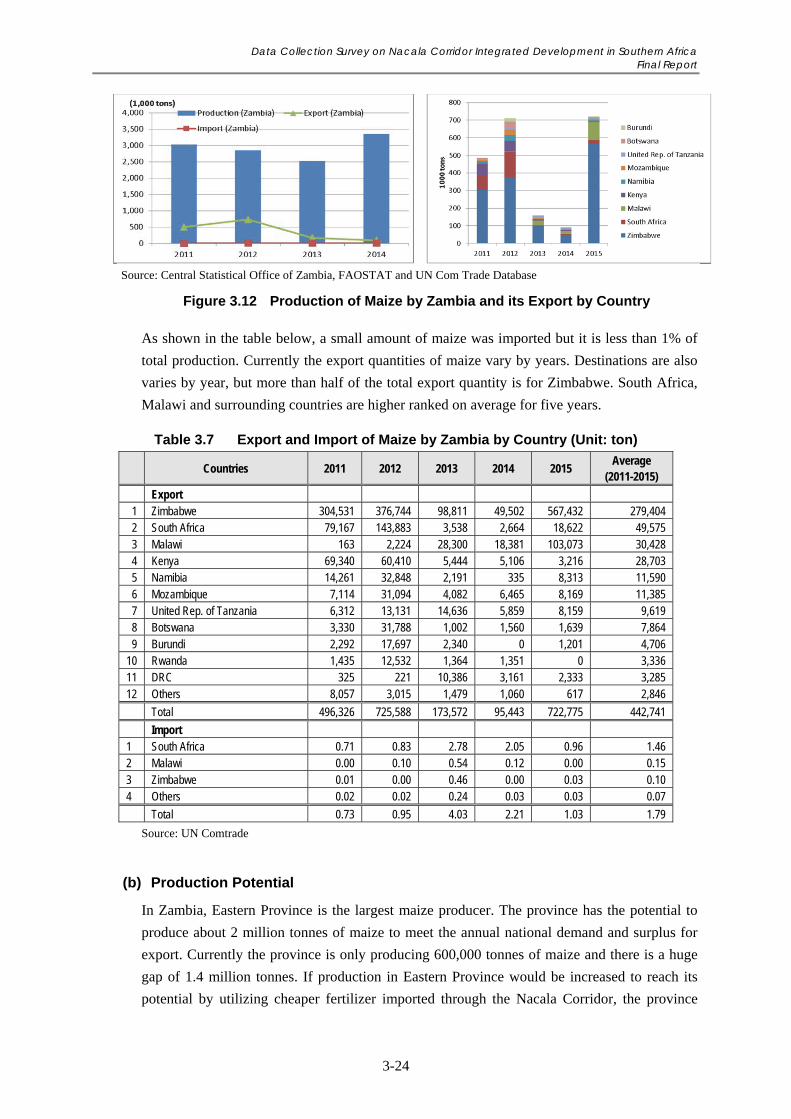

Table 3.7 Export and Import of Maize by Zambia by Country (Unit: ton) ........................................... 3-24

Table 3.8 Import of Maize by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ................... 3-26

Table 3.9 Export of Maize by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ................... 3-26

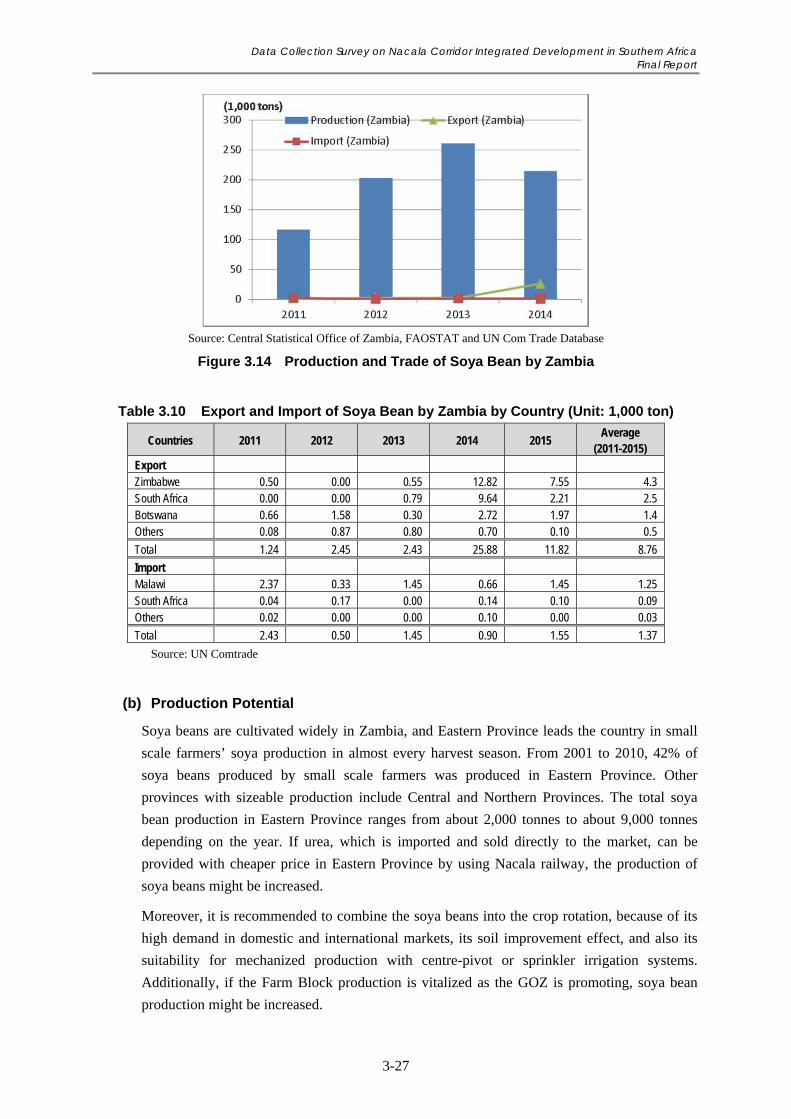

Table 3.10 Export and Import of Soya Bean by Zambia by Country (Unit: 1,000 ton) ......................... 3-27

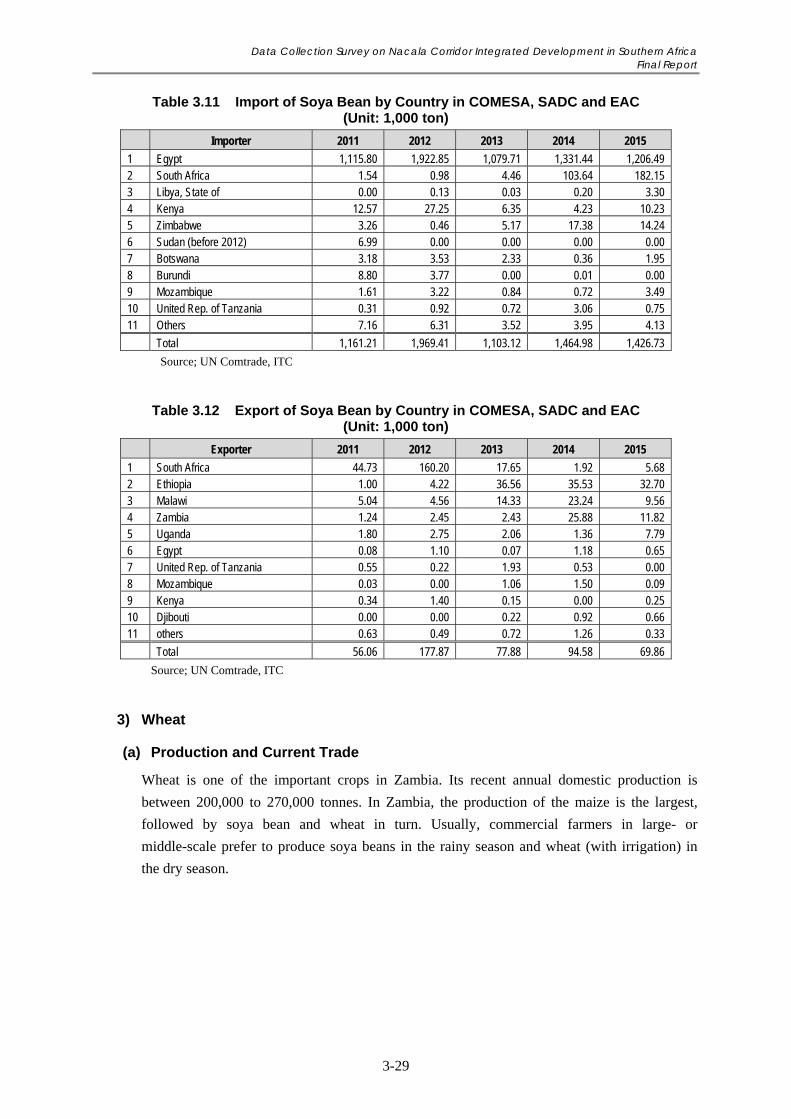

Table 3.11 Import of Soya Bean by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ............ 3-29

Table 3.12 Export of Soya Bean by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ............ 3-29

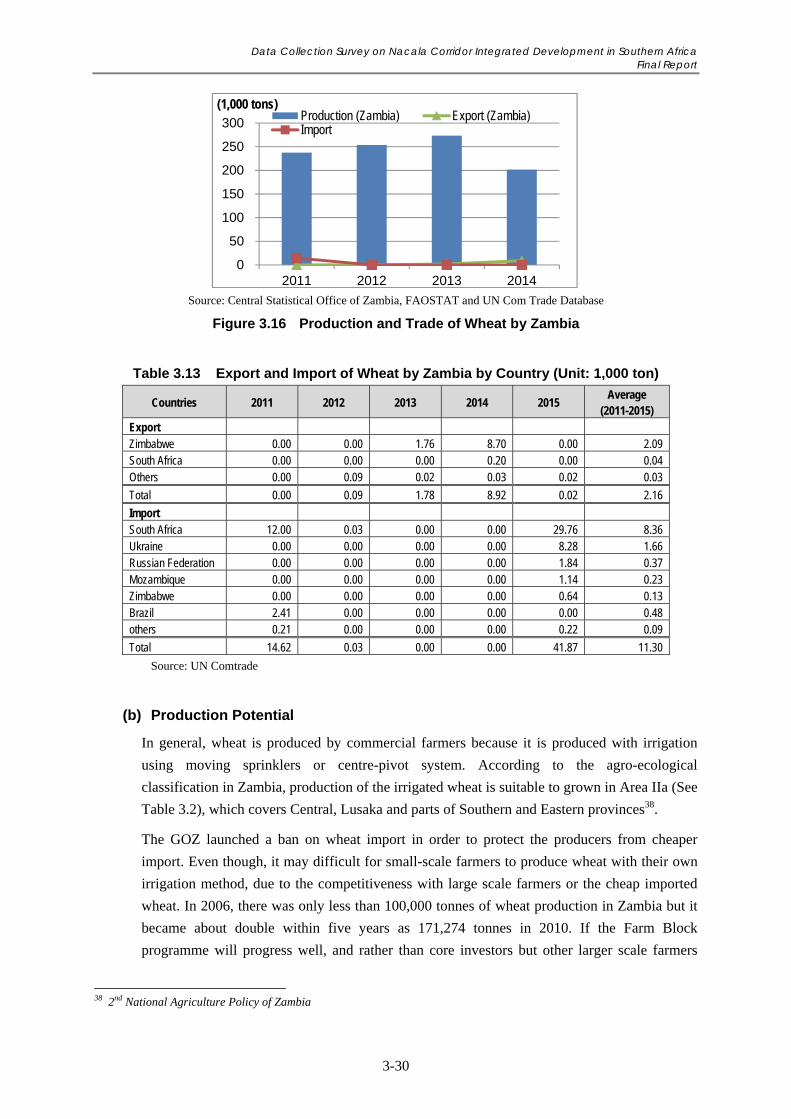

Table 3.13 Export and Import of Wheat by Zambia by Country (Unit: 1,000 ton) ................................ 3-30

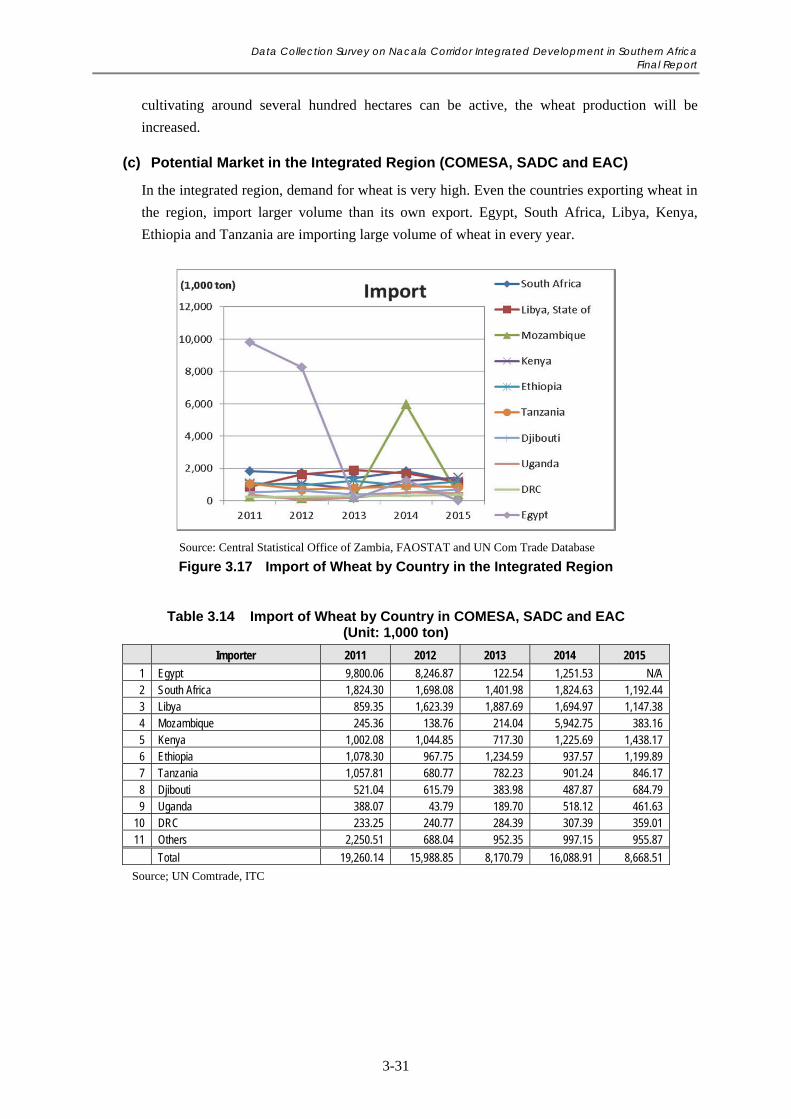

Table 3.14 Import of Wheat by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ................... 3-31

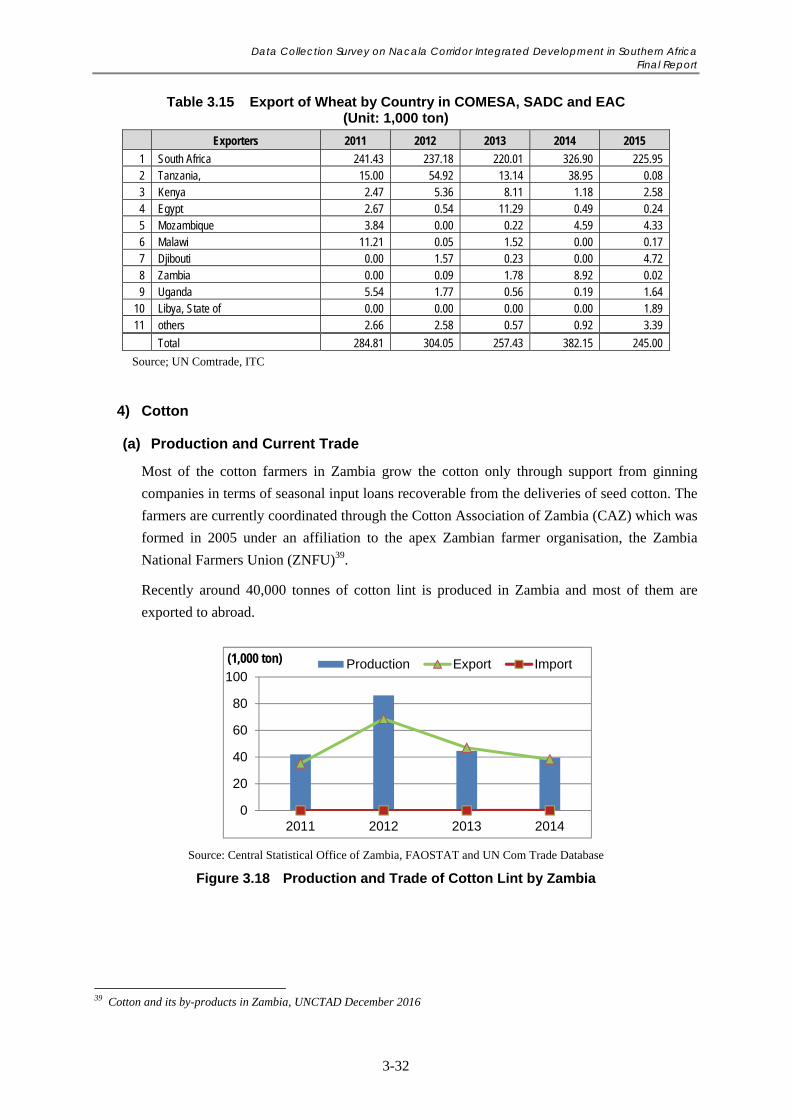

Table 3.15 Export of Wheat by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ................... 3-32

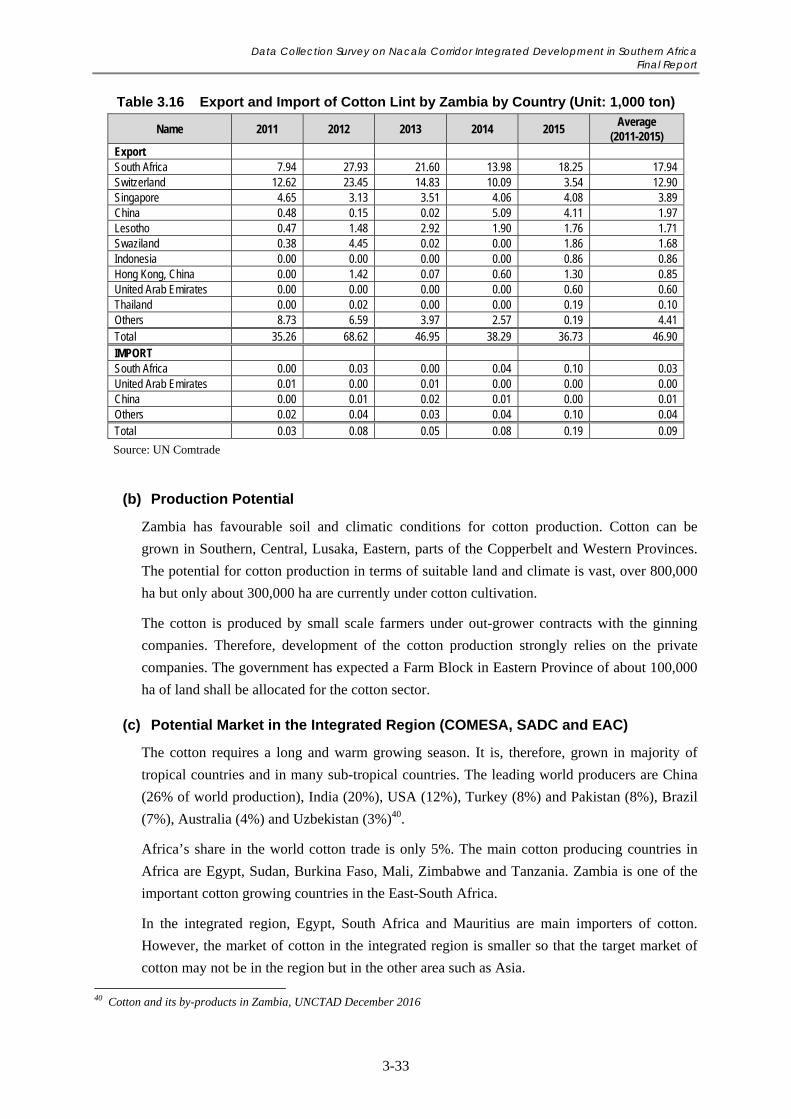

Table 3.16 Export and Import of Cotton Lint by Zambia by Country (Unit: 1,000 ton) ........................ 3-33

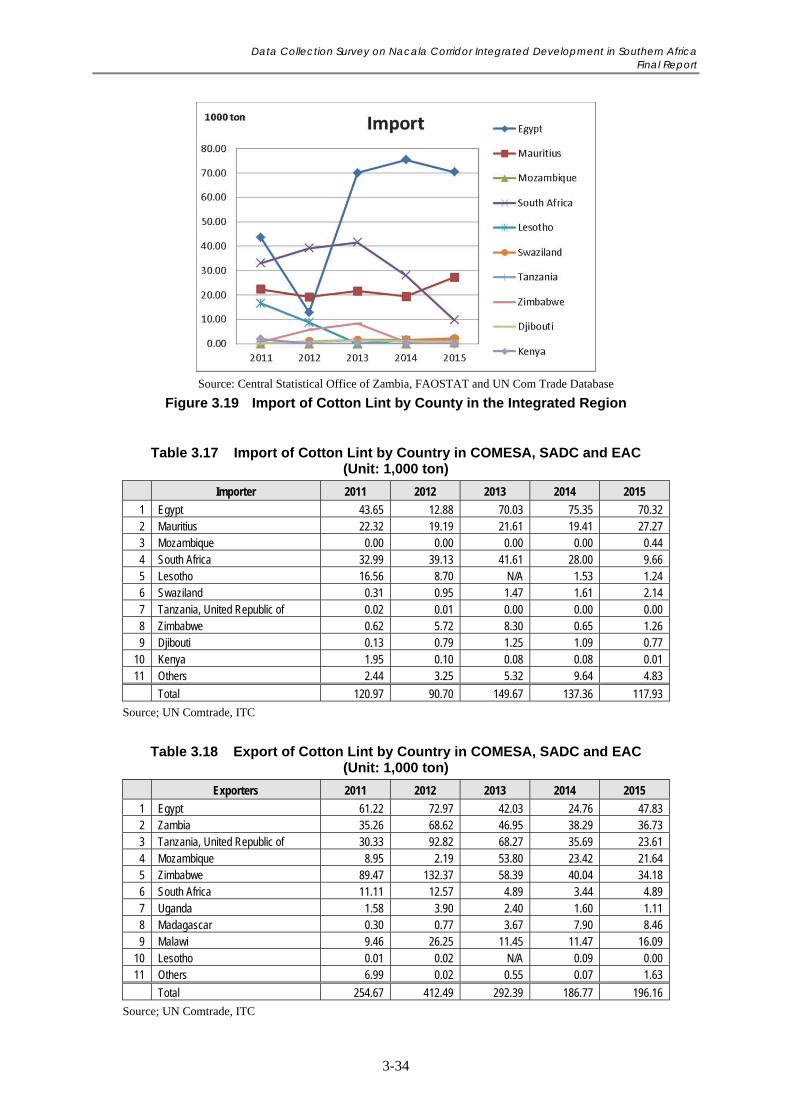

Table 3.17 Import of Cotton Lint by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ........... 3-34

Table 3.18 Export of Cotton Lint by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ........... 3-34

Table 3.19 Export and Import of Bovine Meat by Zambia by Country (Unit: ton) ................................ 3-36

Table 3.20 Export and Import of Live Bovine Animal by Zambia by Country (Unit: ton) .................... 3-36

Table 3.21 Export and Import of Live Goats and Sheep and Sheep Meat by Zambia

by Country (Unit: ton) .......................................................................................................... 3-37

Table 3.22 Export and Import of Meat and Edible Offal of Poultry by Zambia

by Country (Unit: ton) .......................................................................................................... 3-38

Table 3.23 Export and Import of Live Poultry by Zambia by Country (Unit: ton) ................................ 3-38

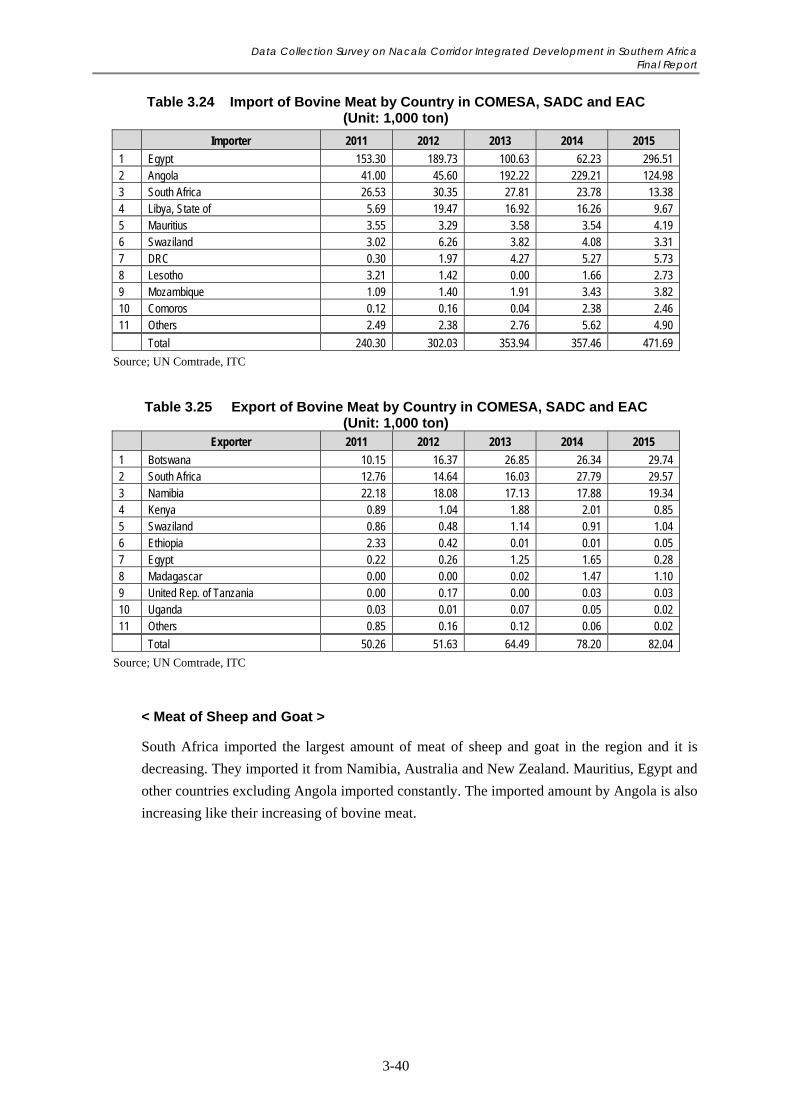

Table 3.24 Import of Bovine Meat by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ......... 3-40

Table 3.25 Export of Bovine Meat by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ......... 3-40

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

vii

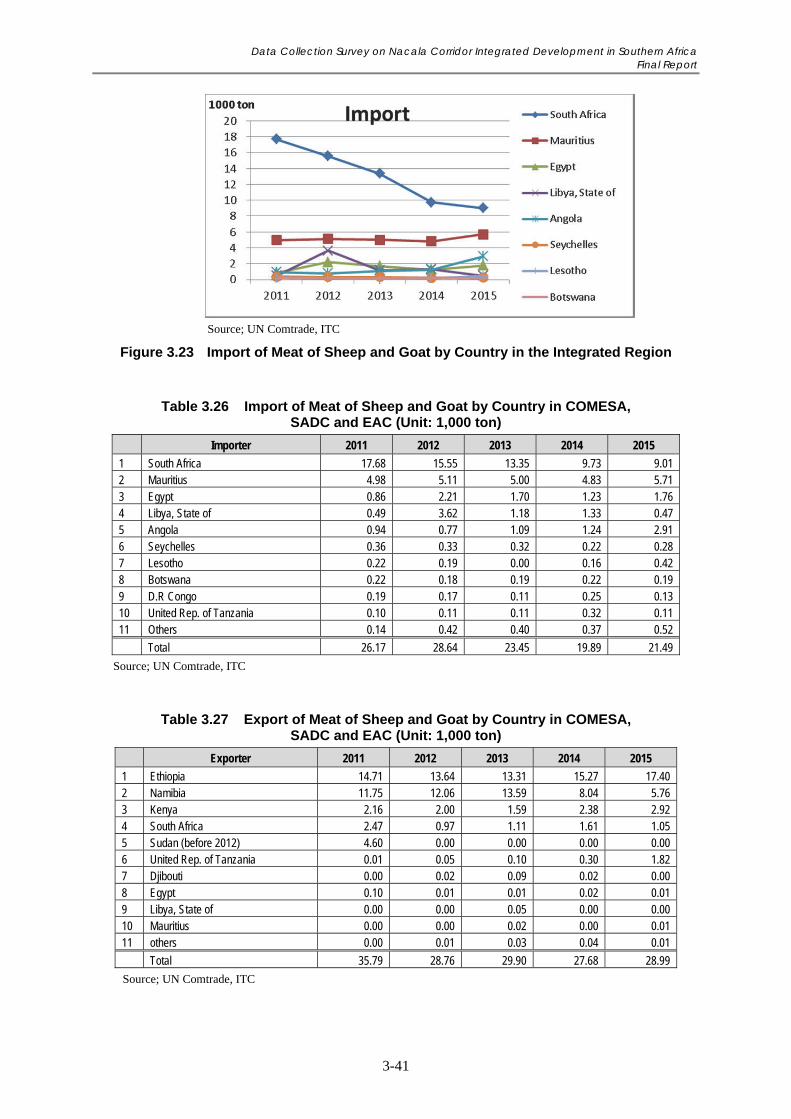

Table 3.26 Import of Meat of Sheep and Goat by Country in COMESA, SADC and EAC

(Unit: 1,000 ton) ................................................................................................................... 3-41

Table 3.27 Export of Meat of Sheep and Goat by Country in COMESA, SADC and EAC

(Unit: 1,000 ton) ................................................................................................................... 3-41

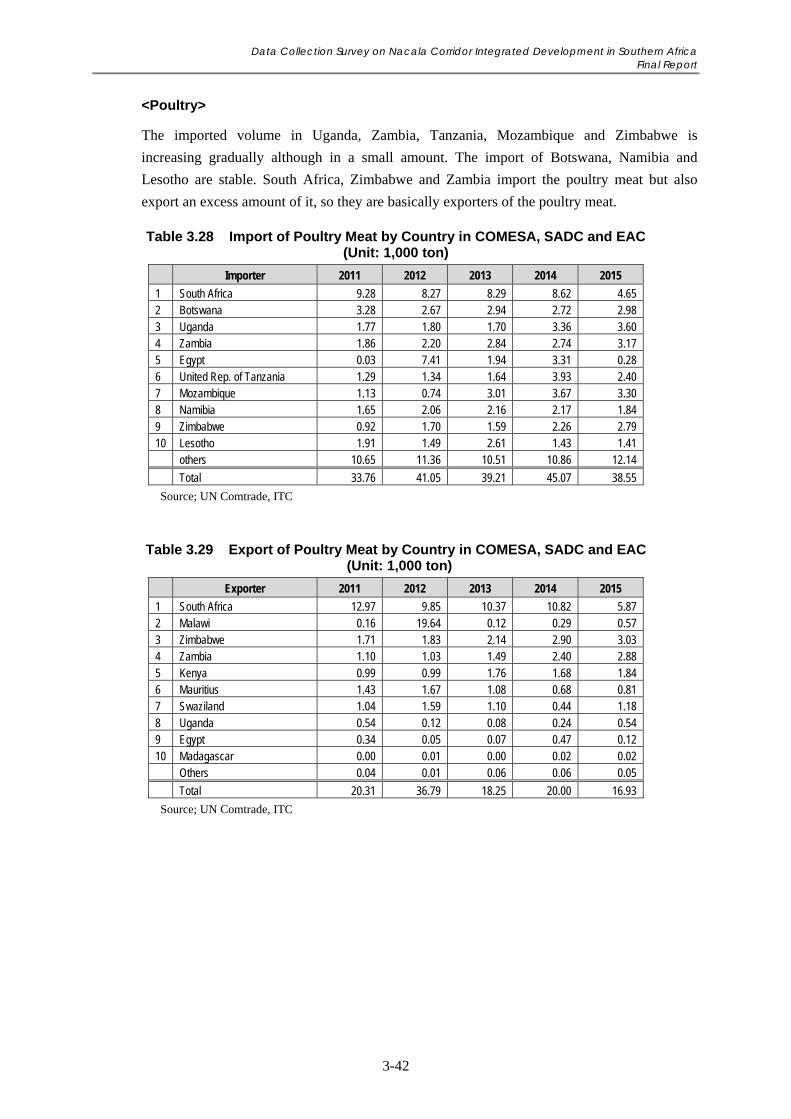

Table 3.28 Import of Poultry Meat by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ........ 3-42

Table 3.29 Export of Poultry Meat by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ........ 3-42

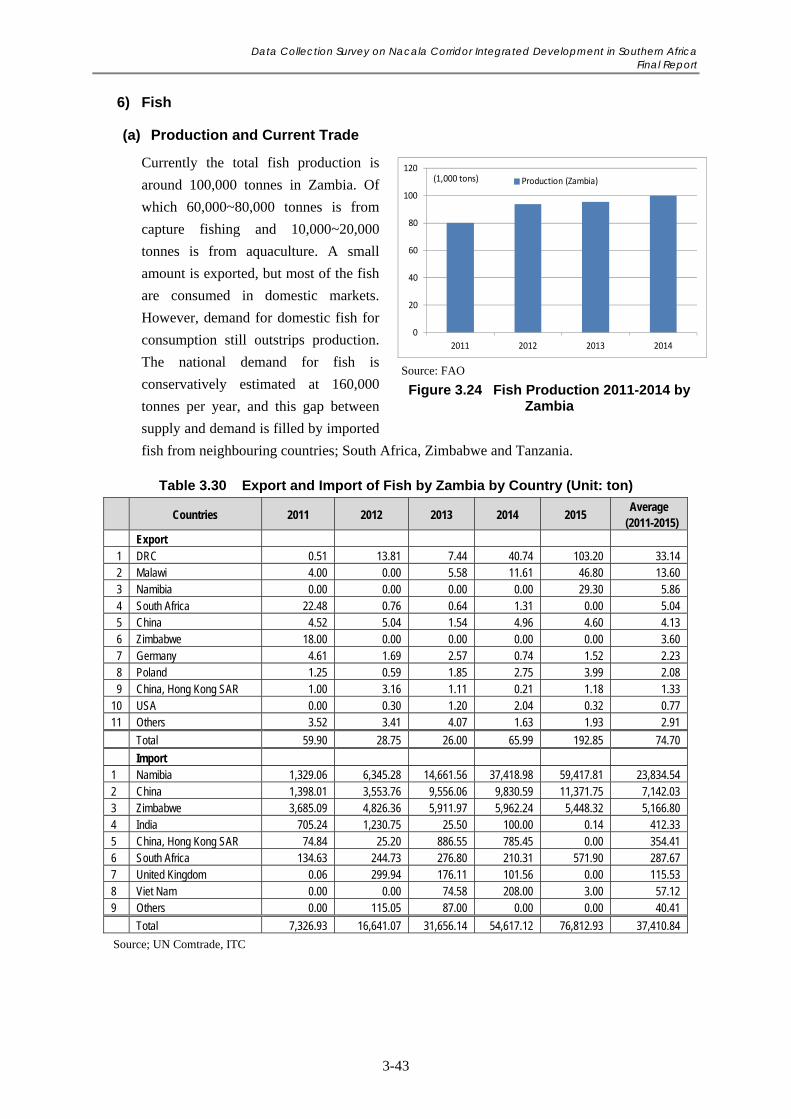

Table 3.30 Export and Import of Fish by Zambia by Country (Unit: ton) .............................................. 3-43

Table 3.31 Import of Fish by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...................... 3-45

Table 3.32 Export of Fish by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...................... 3-45

Table 3.33 Export and Import of Soya Bean Oil by Zambia by Country (Unit: 1,000 ton) ................... 3-46

Table 3.34 Export and Import of Sunflower Oil by Zambia by Country (Unit: 1,000 ton) .................... 3-46

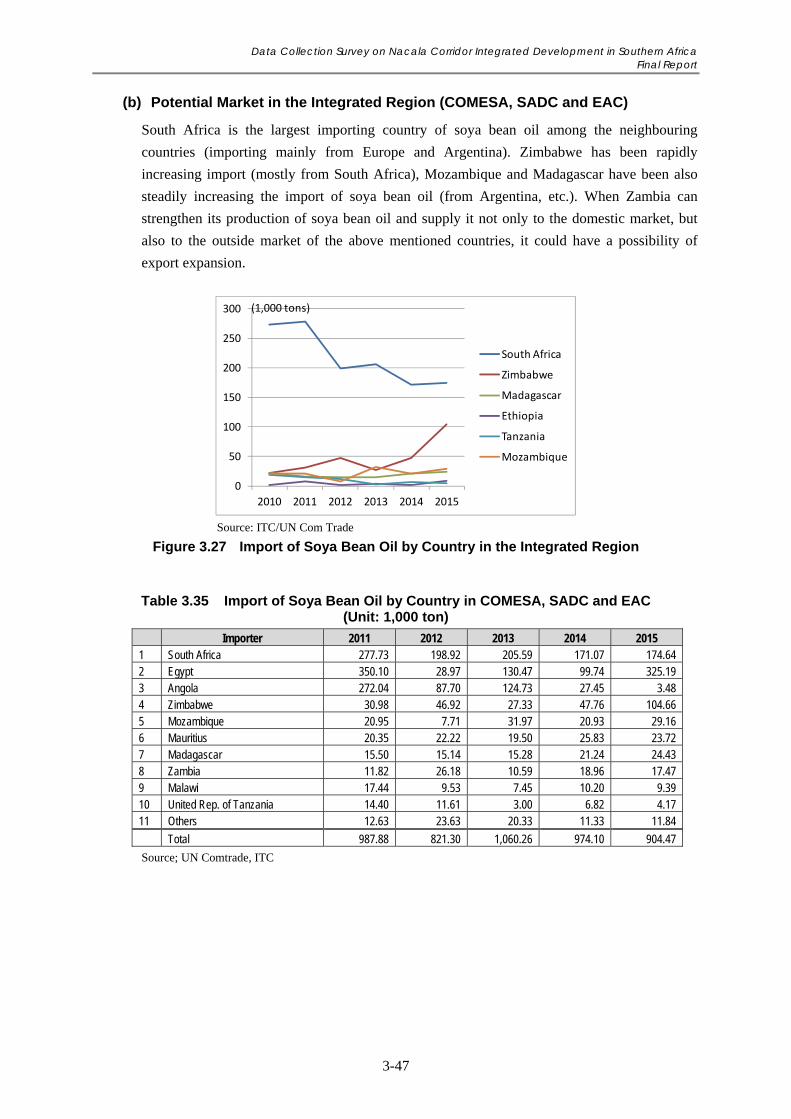

Table 3.35 Import of Soya Bean Oil by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...... 3-47

Table 3.36 Export of Soya Bean Oil by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...... 3-48

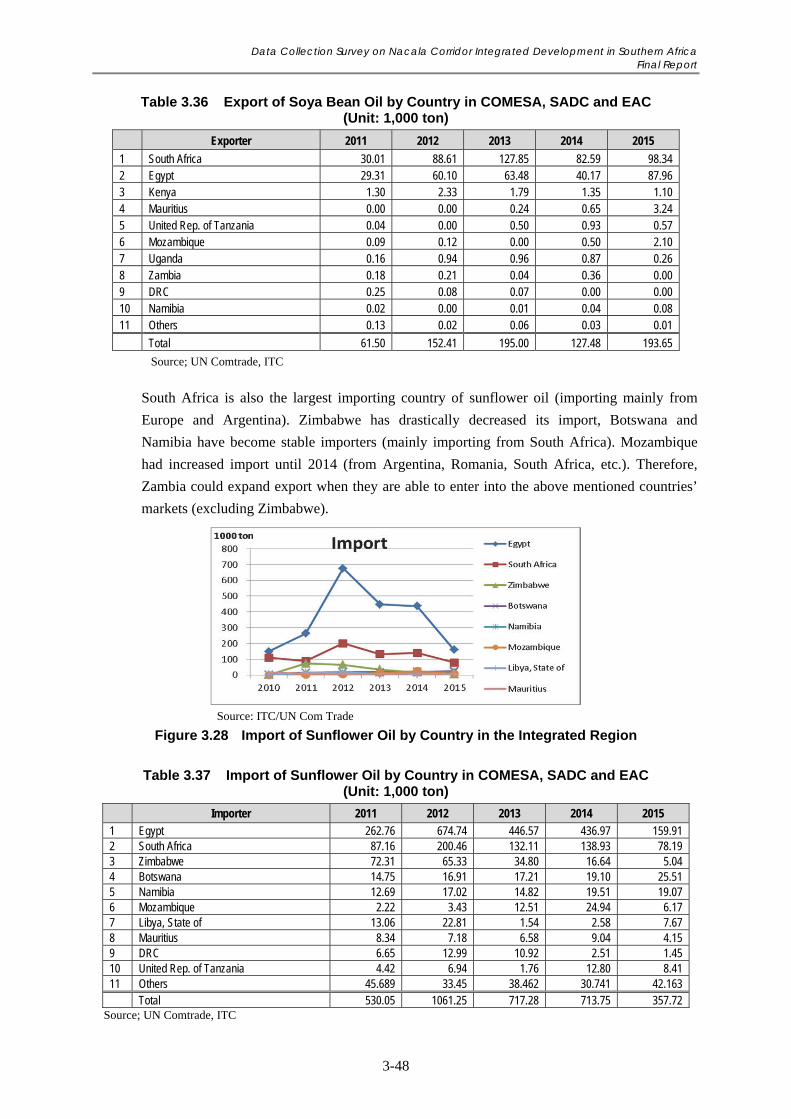

Table 3.37 Import of Sunflower Oil by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ....... 3-48

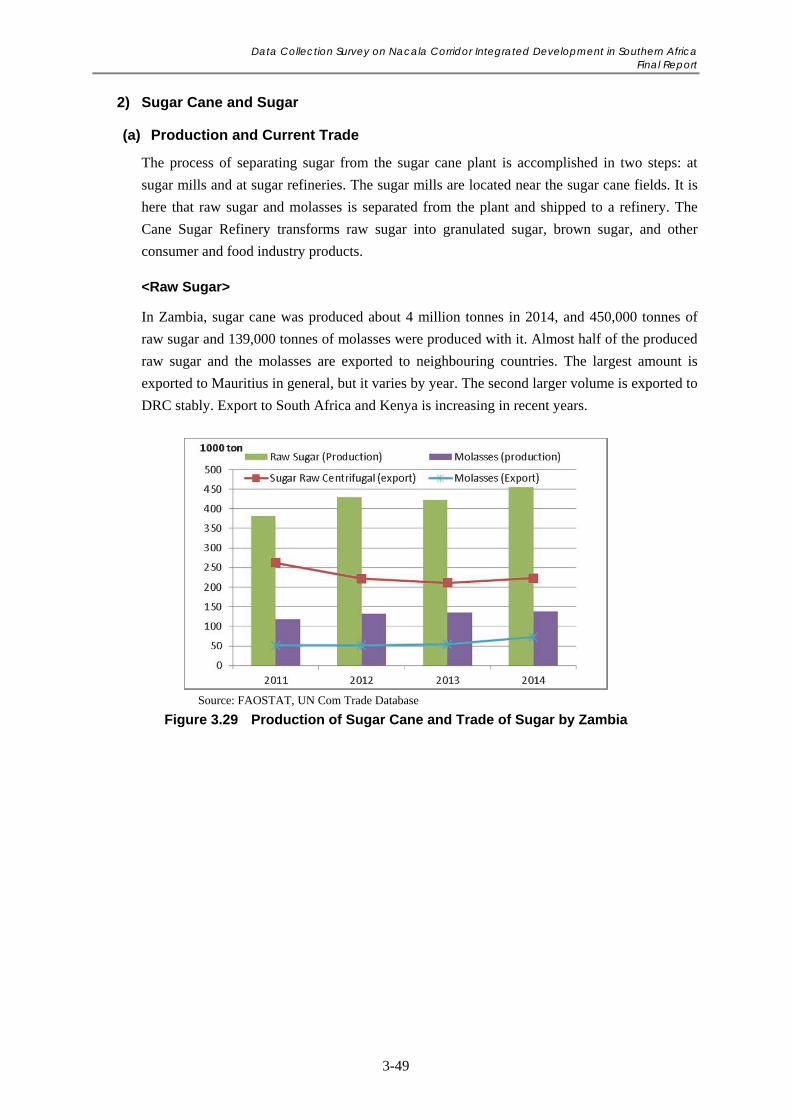

Table 3.38 Export and Import of Raw Sugar by Zambia by Country (Unit: 1,000 ton) ......................... 3-50

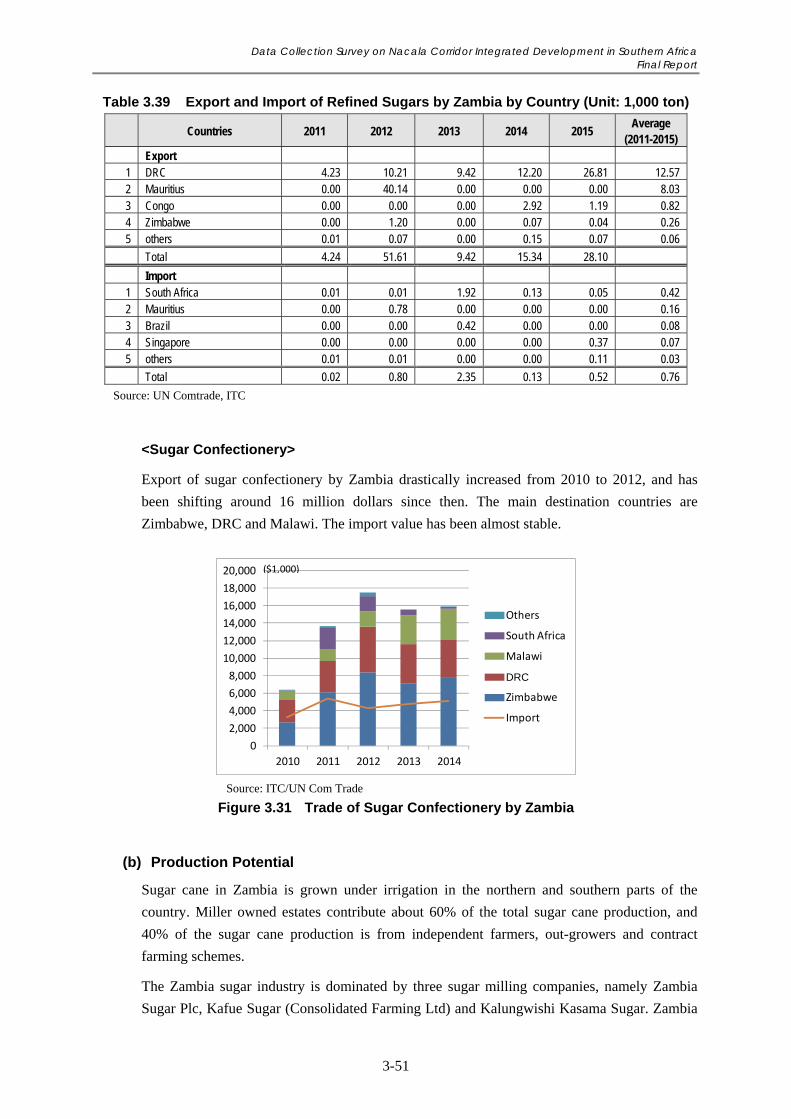

Table 3.39 Export and Import of Refined Sugars by Zambia by Country (Unit: 1,000 ton) .................. 3-51

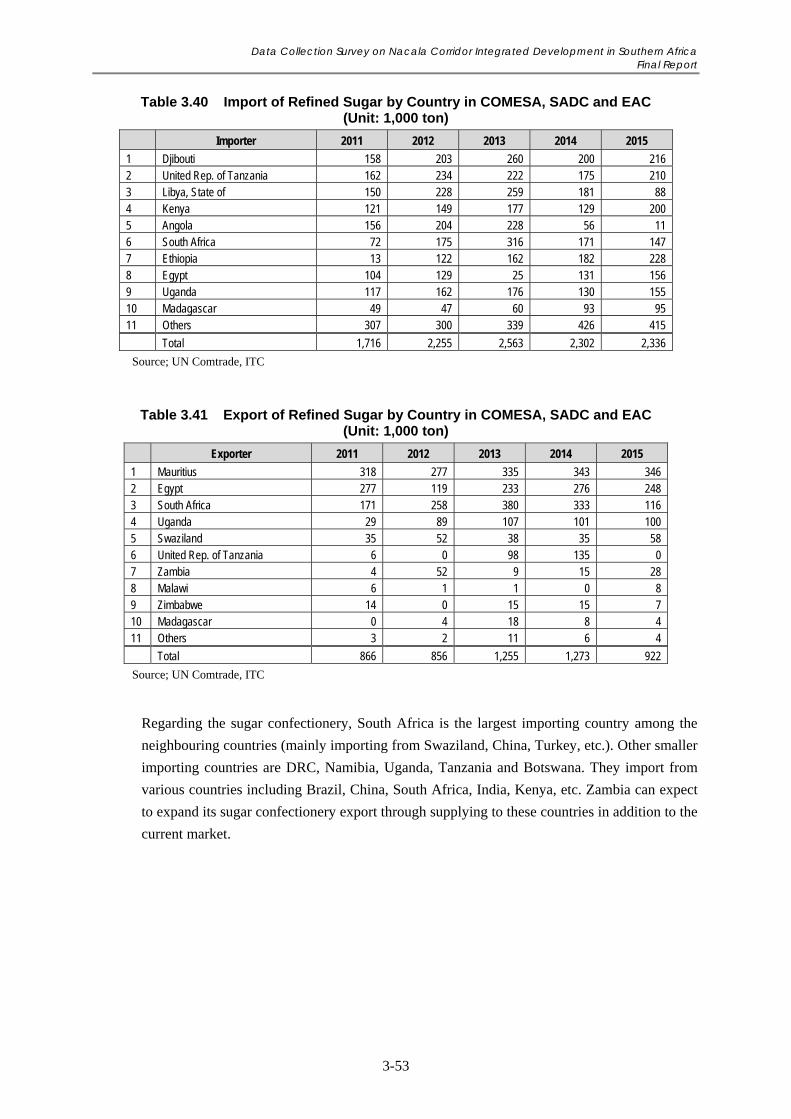

Table 3.40 Import of Refined Sugar by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...... 3-53

Table 3.41 Export of Refined Sugar by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...... 3-53

Table 3.42 Import of Soap and Detergent by Country in COMESA, SADC and EAC

(Unit: 1,000 ton) ................................................................................................................... 3-55

Table 3.43 GDP and Employment by Industry ....................................................................................... 3-56

Table 3.44 Contribution of the Mining and Quarrying Sector to the National Economy

(Million ZMW at 2010 Constant Price) ................................................................................ 3-58

Table 3.45 Mineral Production in Zambia from 2009 to 2013 (Metric ton unless otherwise

specified) .............................................................................................................................. 3-59

Table 3.46 Export of Major Mineral Products from 2012 to 2016 (million USD) ................................. 3-60

Table 3.47 Export Value and Destinations of Copper from 2011 to 2015 (million USD) ..................... 3-61

Table 3.48 Export Value and Destinations of Precious Stones and Semi-Precious Stones in 2015 ....... 3-62

Table 3.49 Export Value and Destinations of Cement in 2015............................................................... 3-62

Table 3.50 Export Value and Destinations of Lime in 2015 .................................................................. 3-62

Table 3.51 Export Value and Destinations of Cobalt in 2015 ................................................................ 3-62

Table 3.52 Export Value and Destination of Sulphur in 2015 ................................................................ 3-62

Table 3.53 Export Value and Destination of Manganese in 2016 .......................................................... 3-62

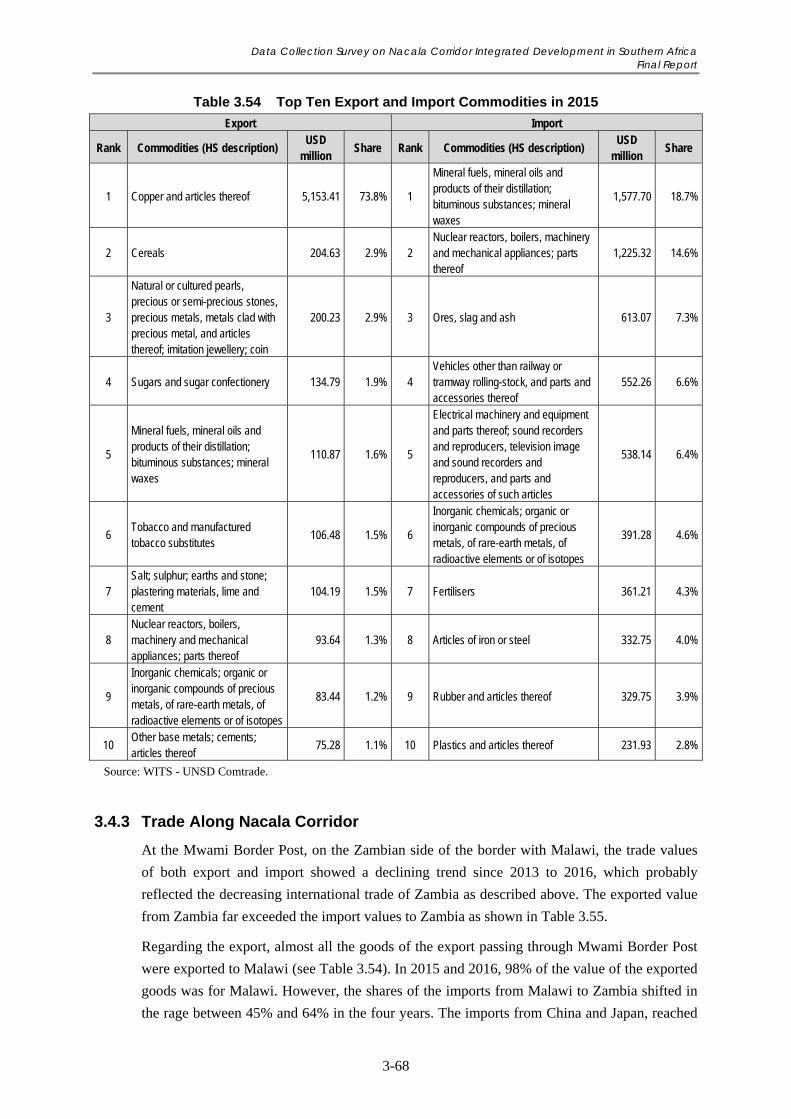

Table 3.54 Top Ten Export and Import Commodities in 2015 ............................................................... 3-68

Table 3.55 Top Five Destinations of Export and Import at Mwami Border Post from 2013

to 2016 .................................................................................................................................. 3-70

Table 3.56 Top Five Exported and Imported Commodities at Mwami Border Post from 2013

to 2016 .................................................................................................................................. 3-71

Table 3.57 Tourist Arrivals and Annual Tourism Earnings .................................................................... 3-73

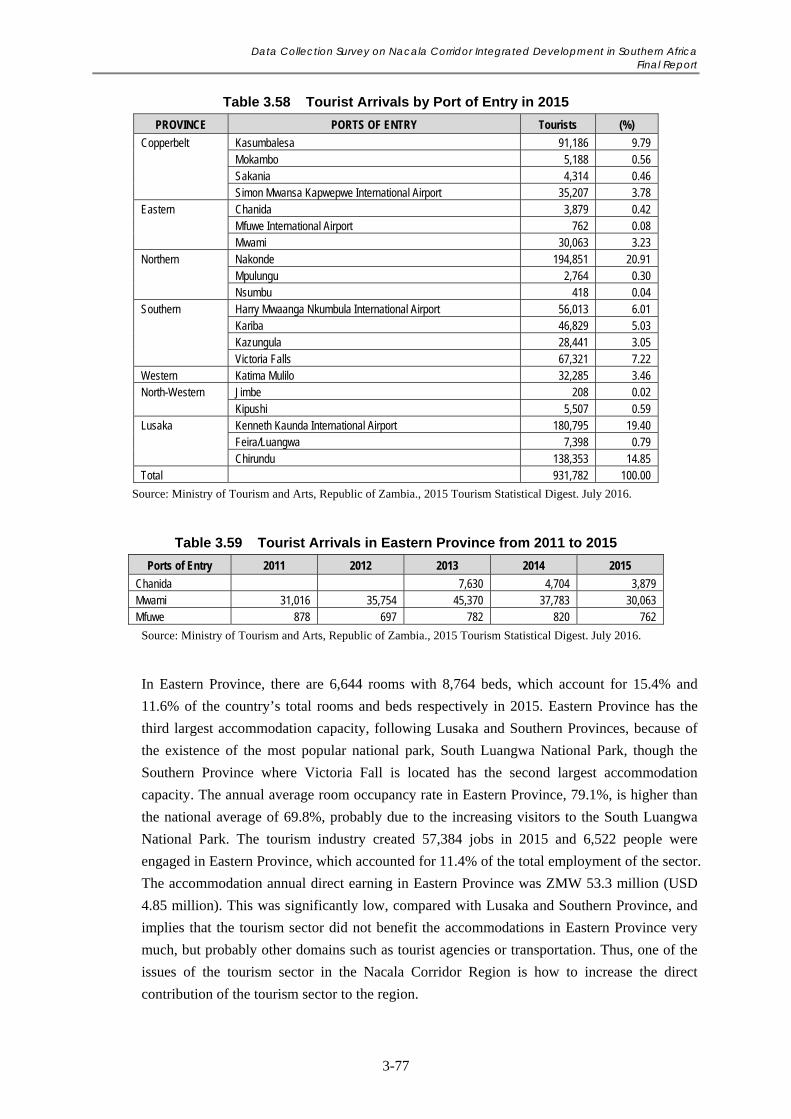

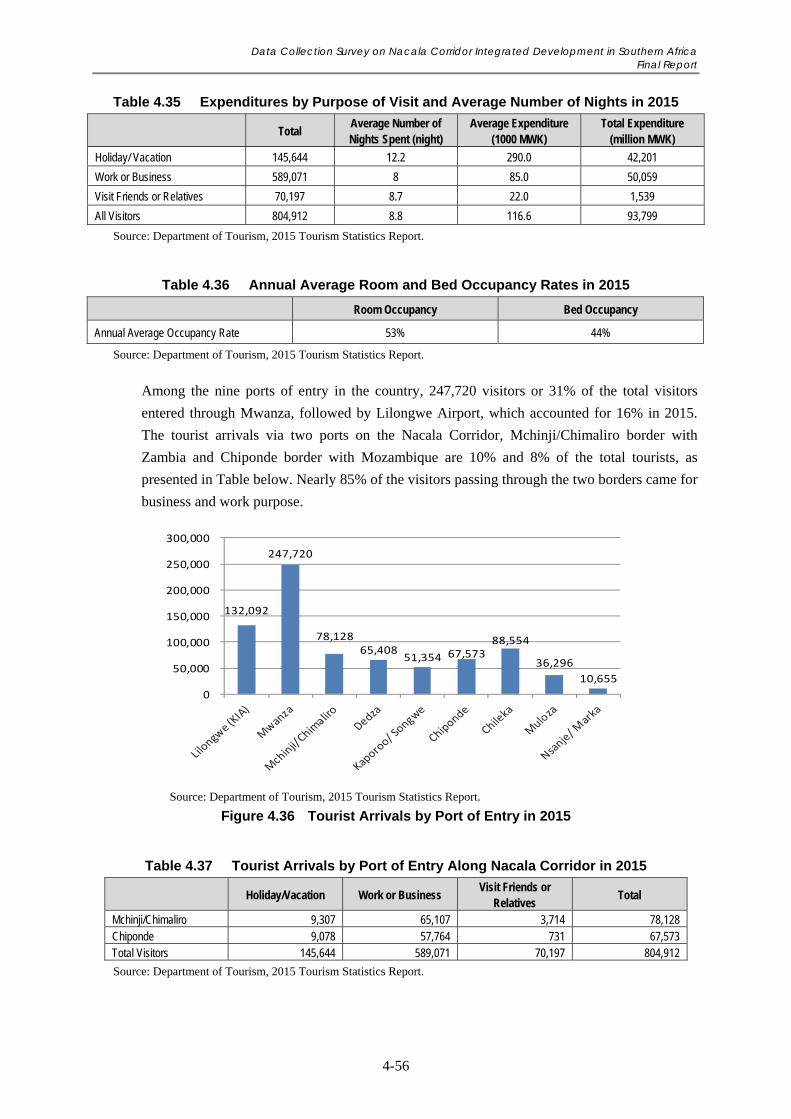

Table 3.58 Tourist Arrivals by Port of Entry in 2015 ............................................................................. 3-77

Table 3.59 Tourist Arrivals in Eastern Province from 2011 to 2015 ...................................................... 3-77

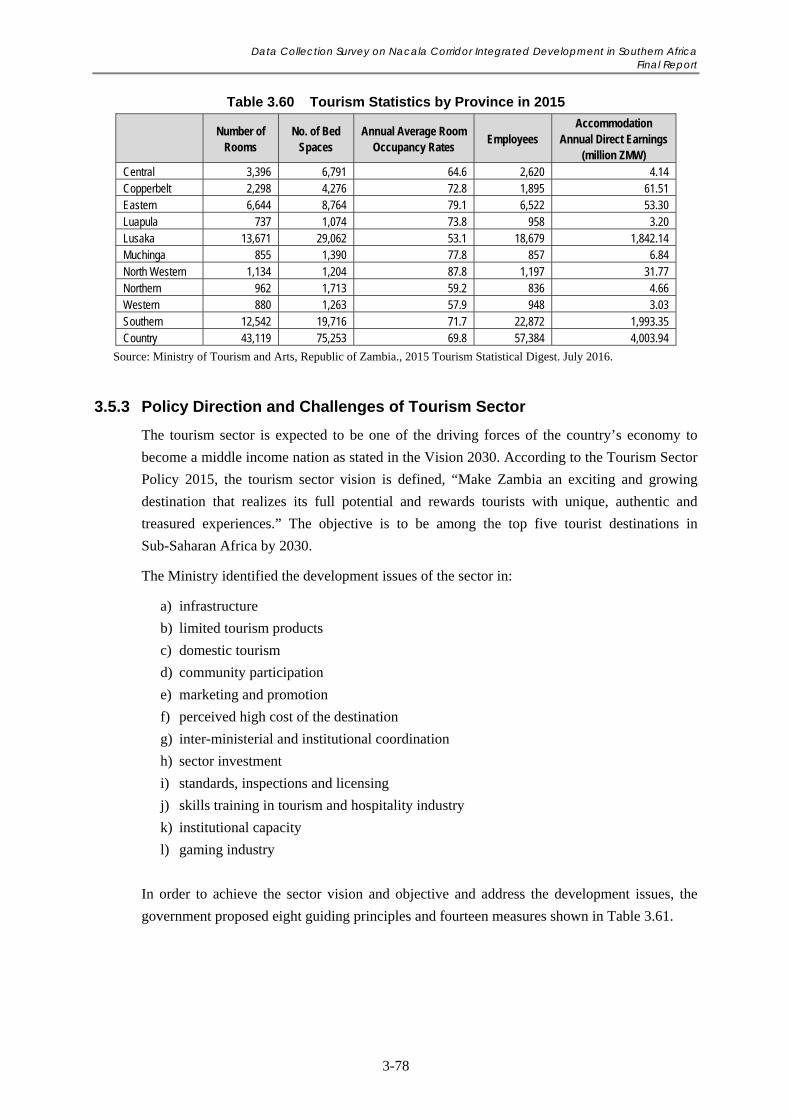

Table 3.60 Tourism Statistics by Province in 2015 ................................................................................ 3-78

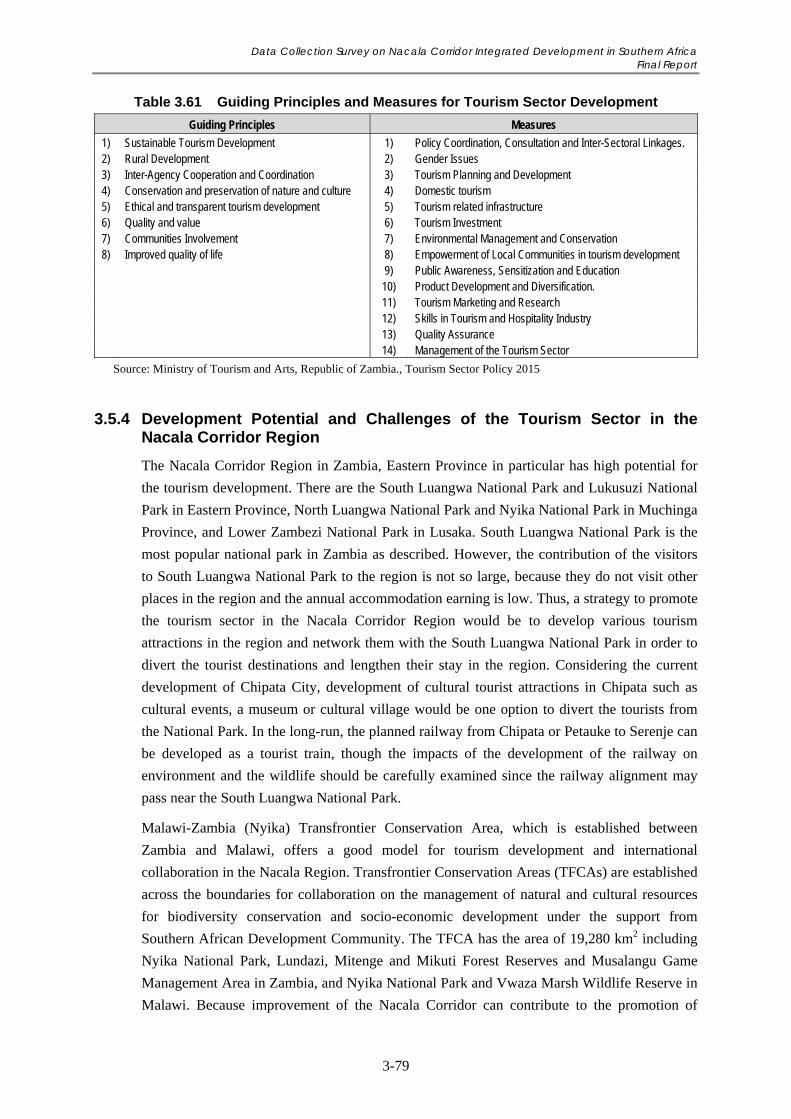

Table 3.61 Guiding Principles and Measures for Tourism Sector Development .................................... 3-79

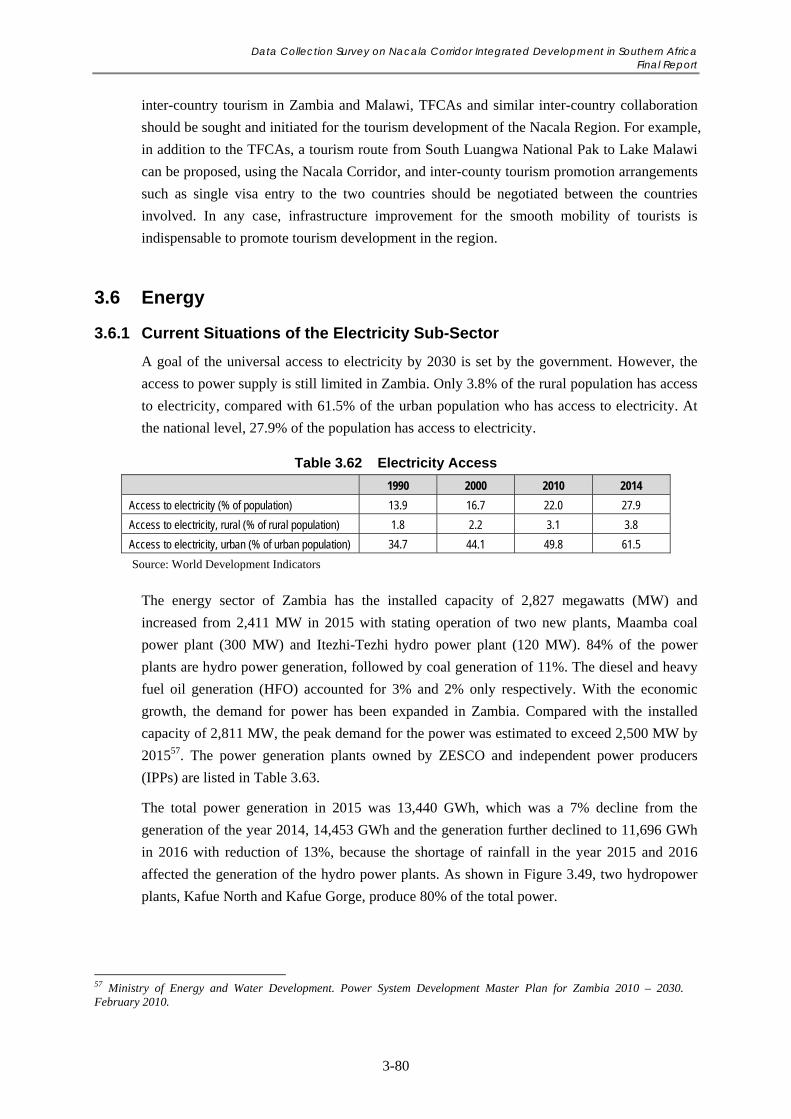

Table 3.62 Electricity Access ................................................................................................................. 3-80

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

viii

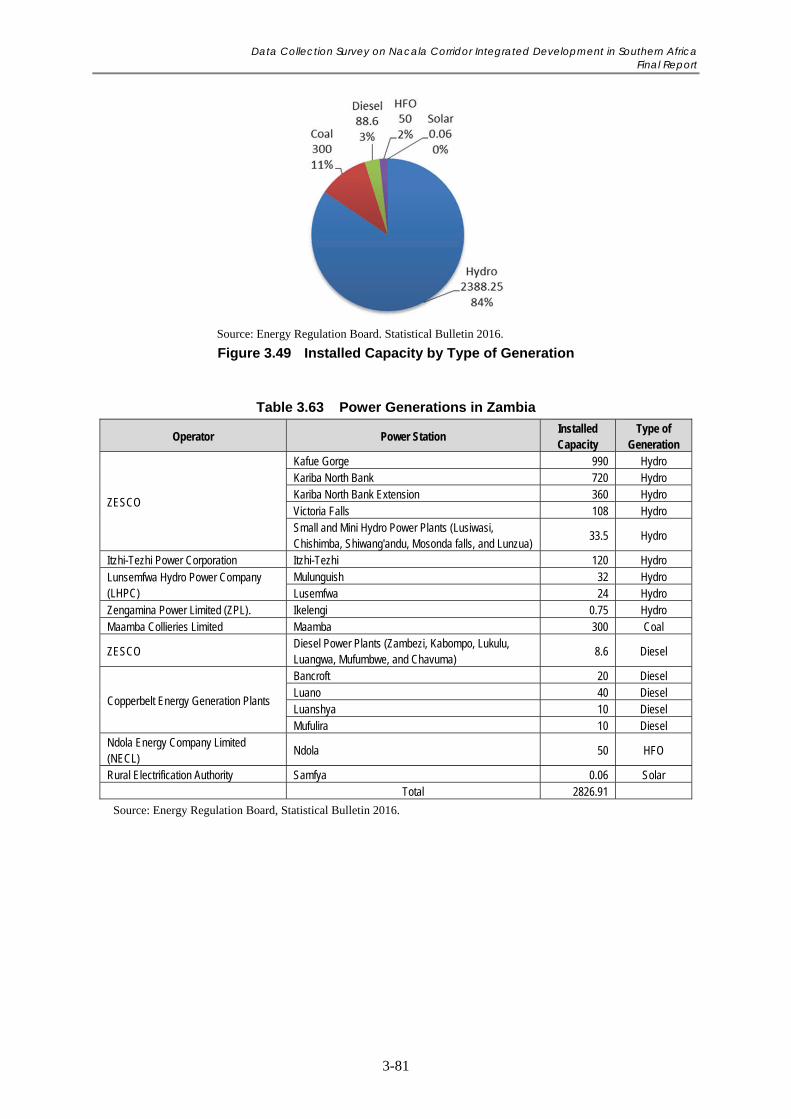

Table 3.63 Power Generations in Zambia ............................................................................................... 3-81

Table 3.64 Consumption of Power by Sector in 2015 ............................................................................ 3-82

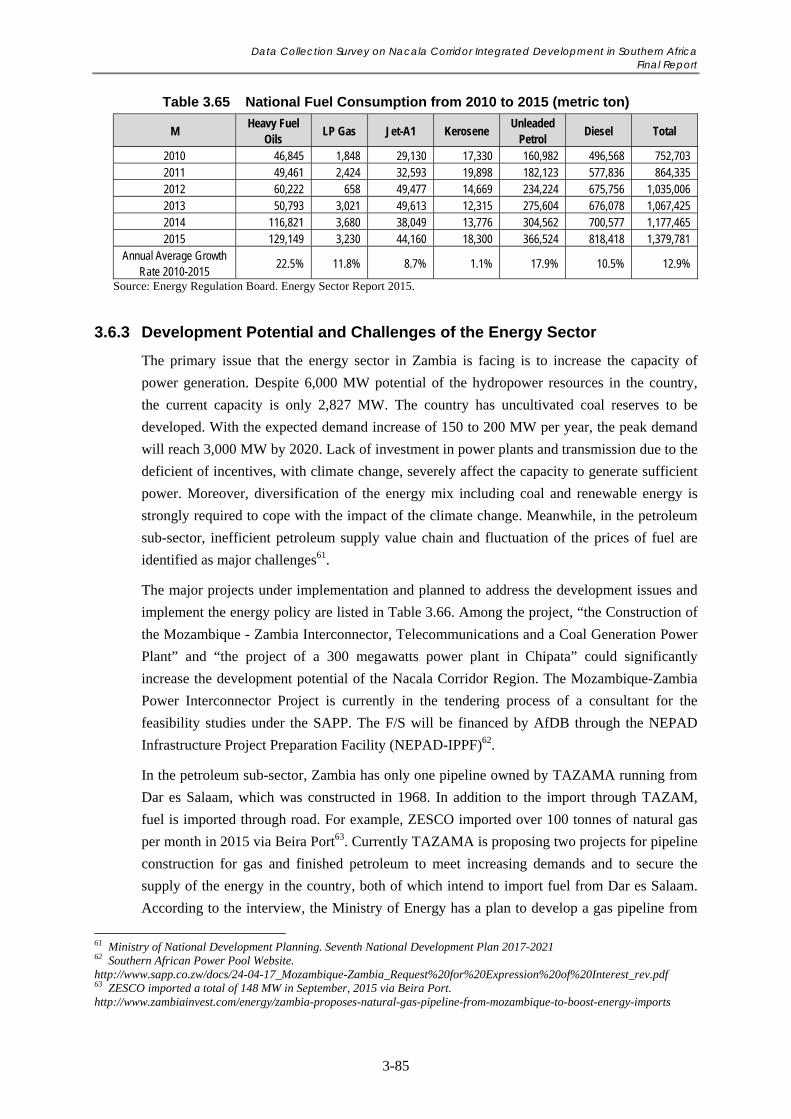

Table 3.65 National Fuel Consumption from 2010 to 2015 (metric ton) ............................................... 3-85

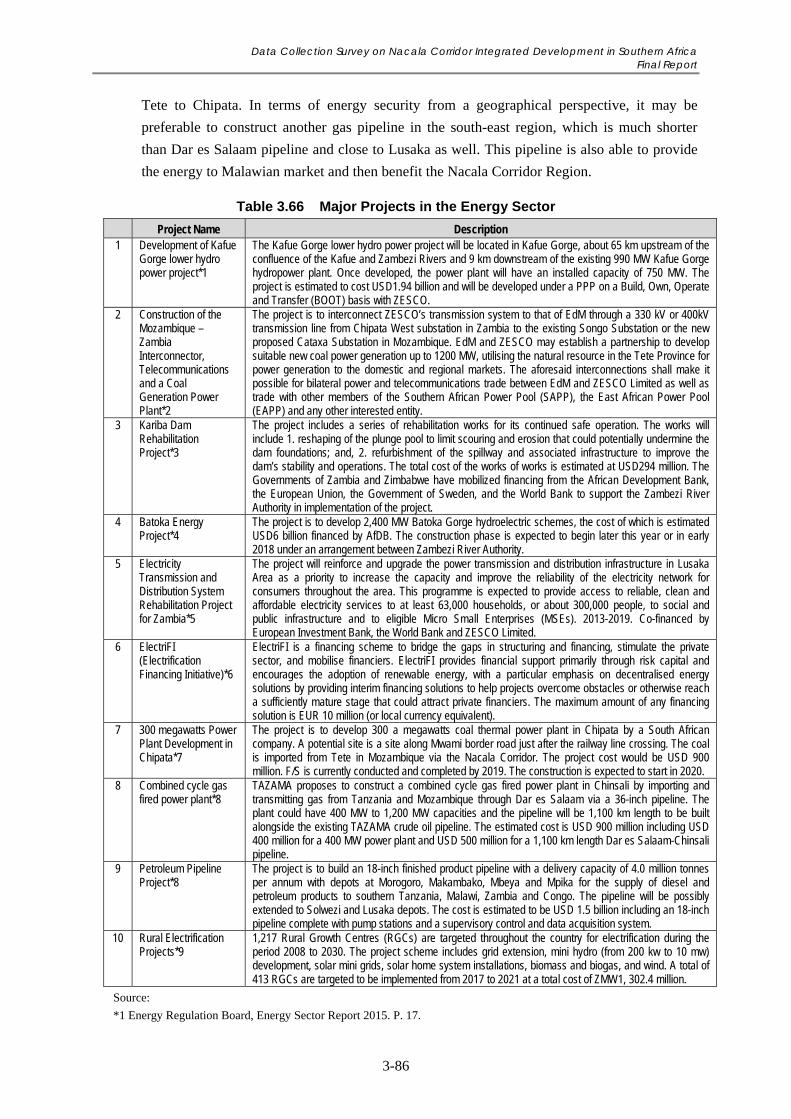

Table 3.66 Major Projects in the Energy Sector ..................................................................................... 3-86

Table 3.67 Investment in Eastern Province in Comparison with the Whole Country

(Pledged base, 2010-2016) ................................................................................................... 3-91

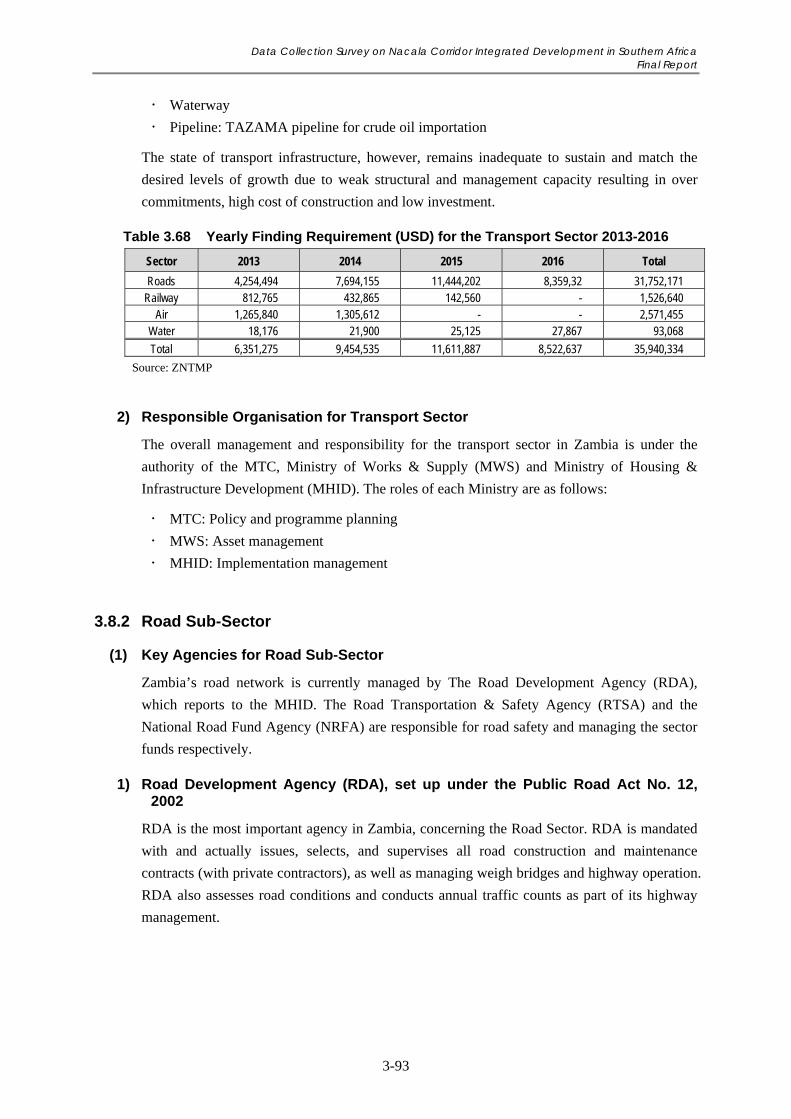

Table 3.68 Yearly Finding Requirement (USD) for the Transport Sector 2013-2016 ............................ 3-93

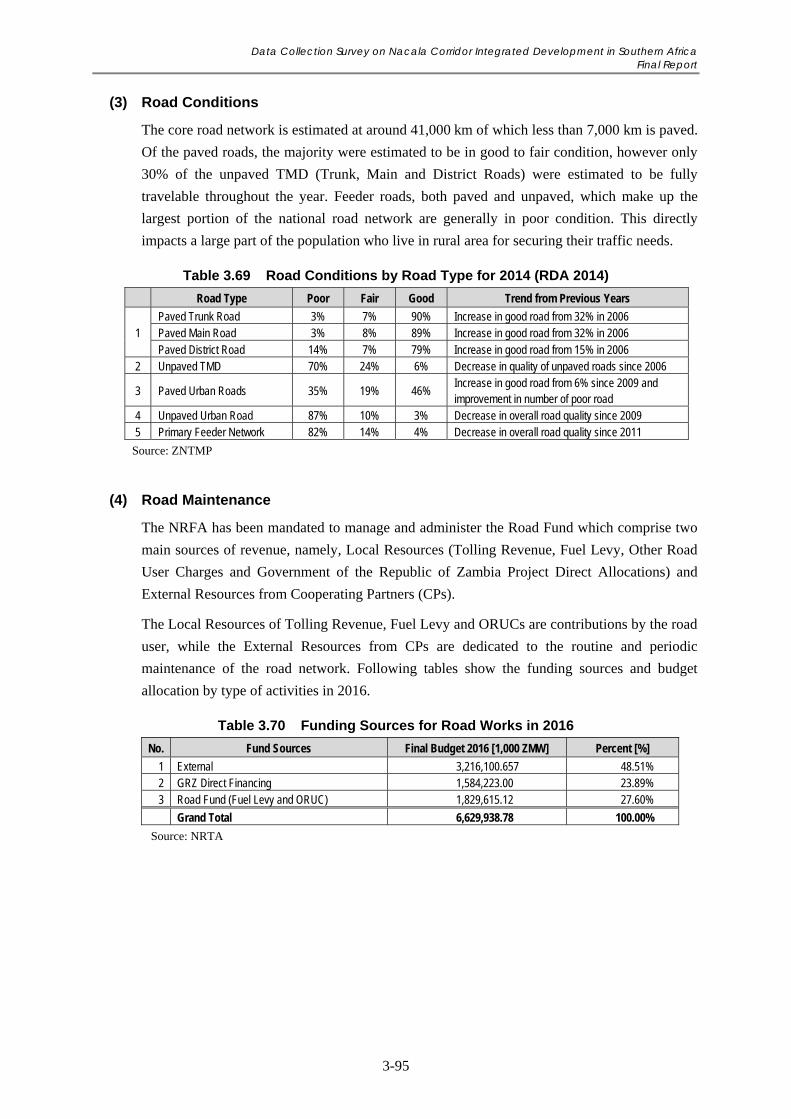

Table 3.69 Road Conditions by Road Type for 2014 (RDA 2014) ........................................................ 3-95

Table 3.70 Funding Sources for Road Works in 2016 ............................................................................ 3-95

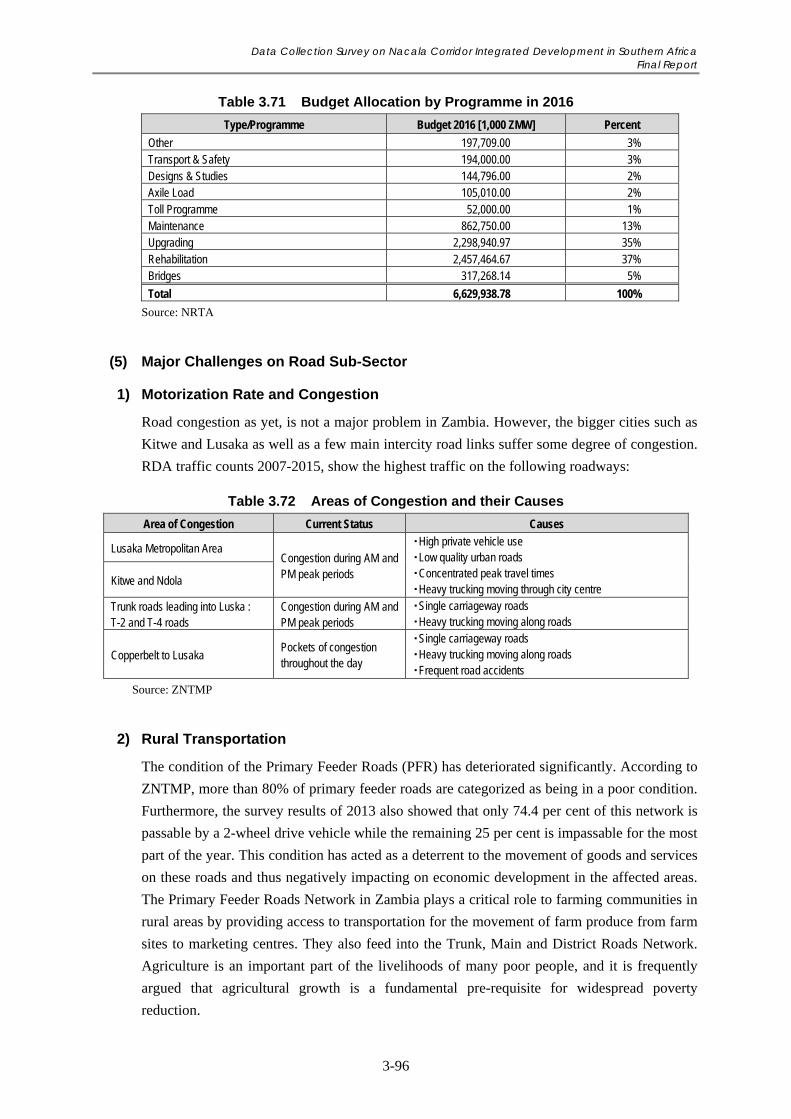

Table 3.71 Budget Allocation by Programme in 2016 ........................................................................... 3-96

Table 3.72 Areas of Congestion and their Causes .................................................................................. 3-96

Table 3.73 ZRL Market Share in 2013 ................................................................................................. 3-100

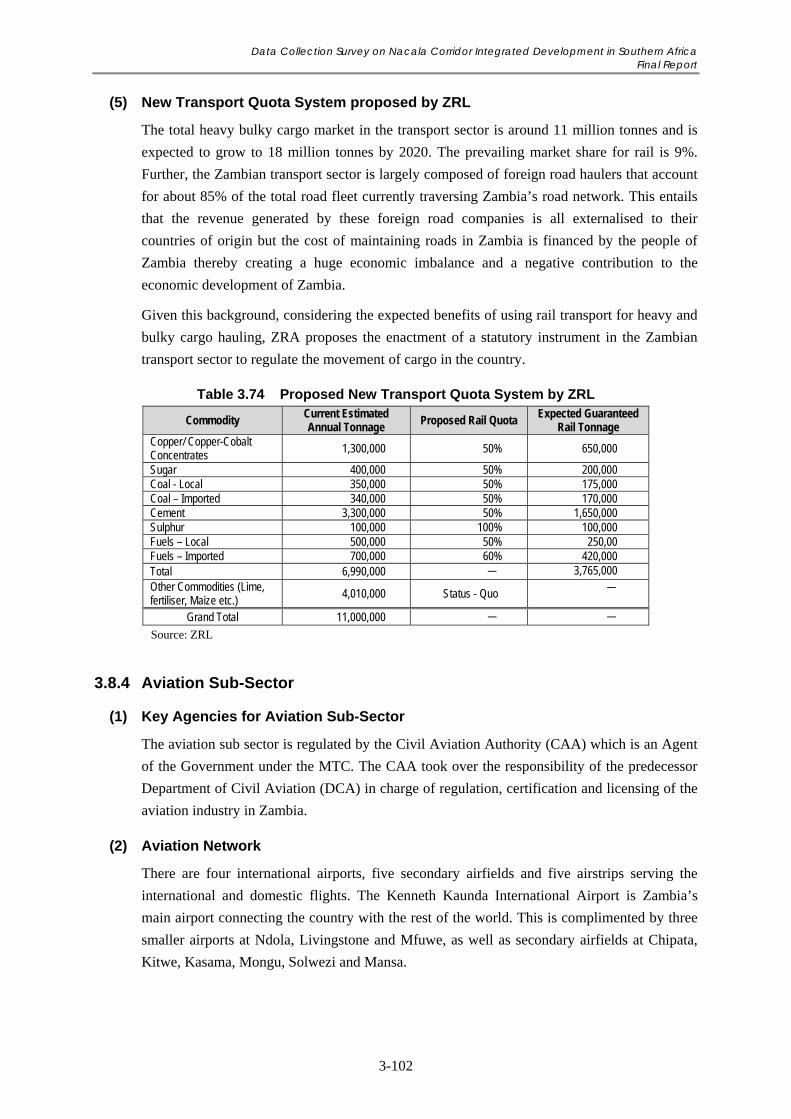

Table 3.74 Proposed New Transport Quota System by ZRL ............................................................... 3-102

Table 3.75 Dry Port and ICD Facilities and Select Information ........................................................... 3-105

Table 4.1 Demographic Characteristics .................................................................................................. 4-1

Table 4.2 Distribution of Landholdings and Cultivated Area by Farm Size ........................................... 4-6

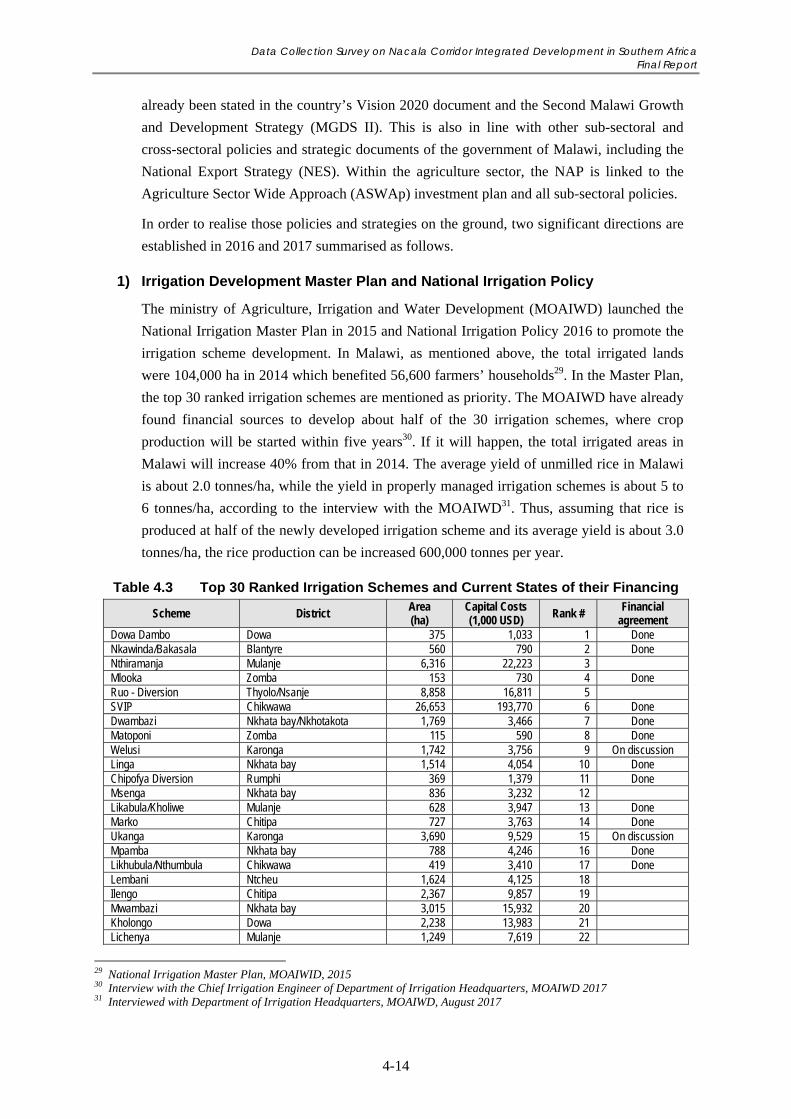

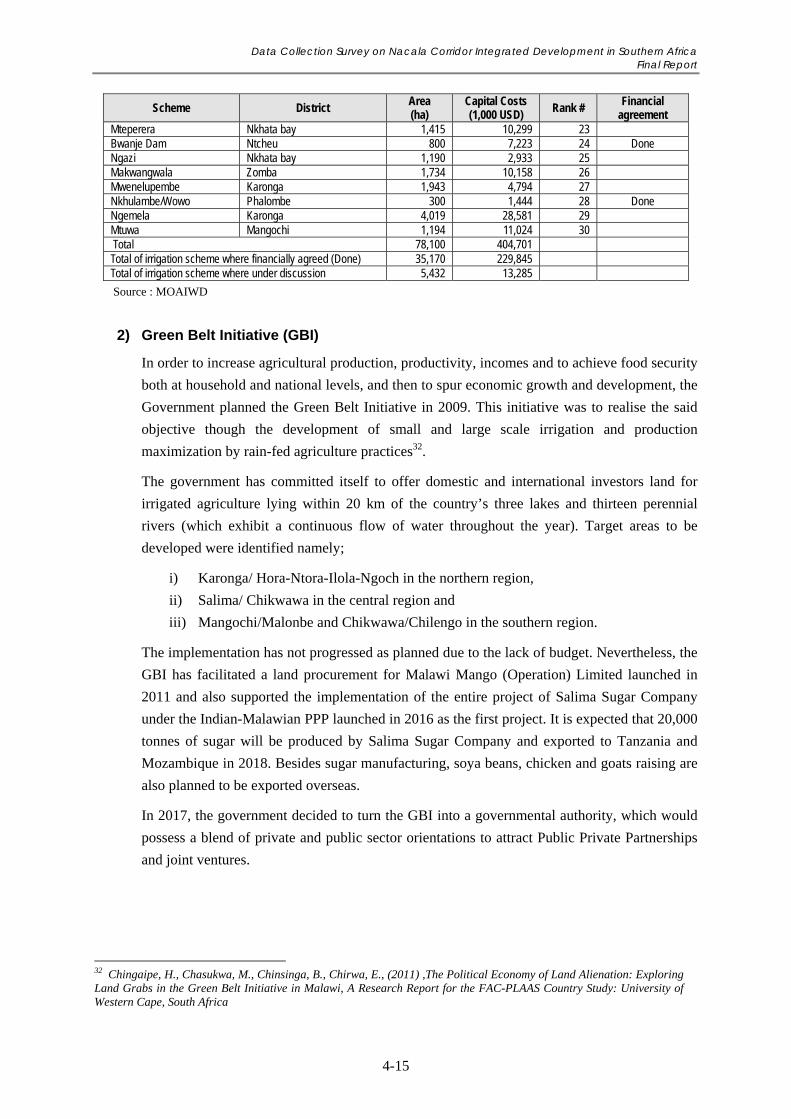

Table 4.3 Top 30 Ranked Irrigation Schemes and Current States of their Financing ........................... 4-14

Table 4.4 Recent Implemented Projects Related to Aflatoxins Control ............................................... 4-19

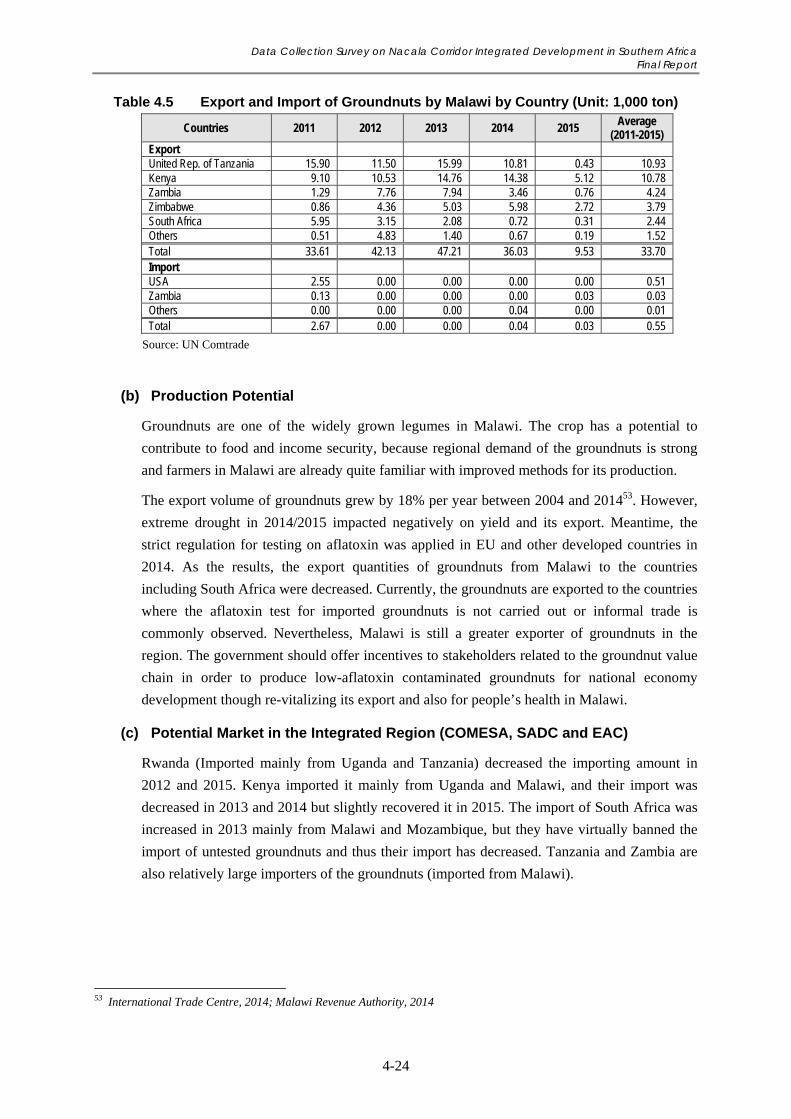

Table 4.5 Export and Import of Groundnuts by Malawi by Country (Unit: 1,000 ton) ........................ 4-24

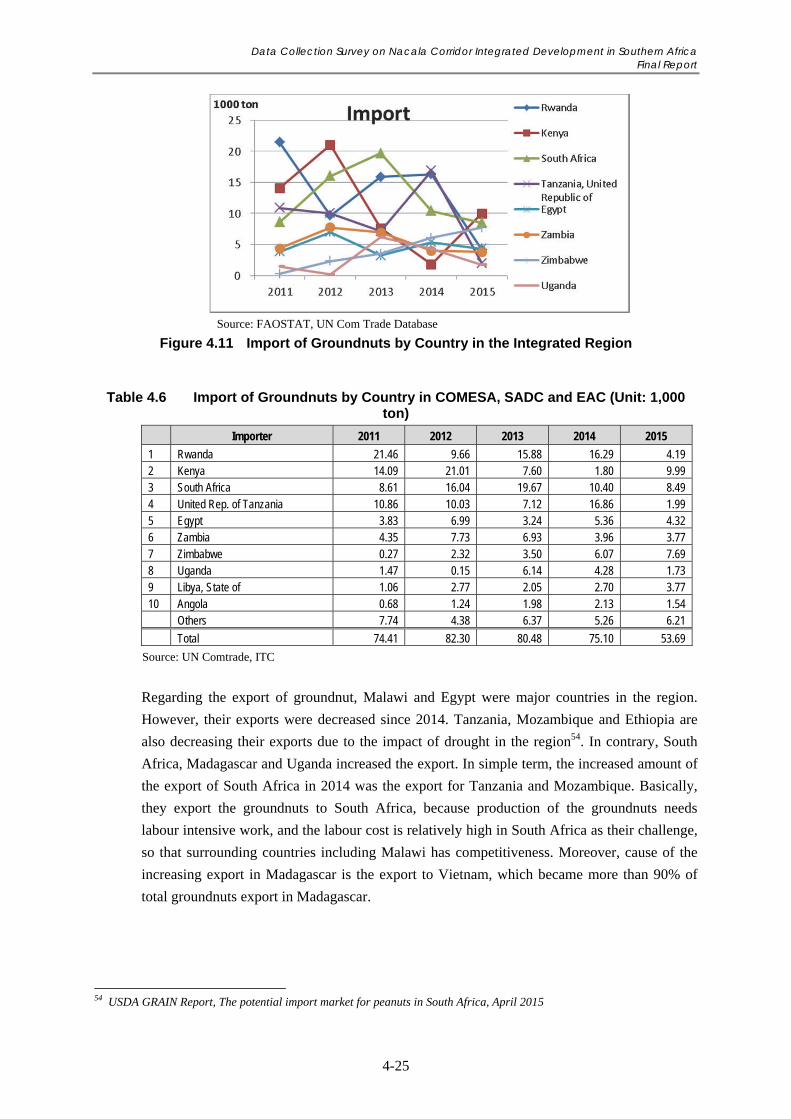

Table 4.6 Import of Groundnuts by Country in COMESA, SADC and EAC (Unit: 1,000 ton) .......... 4-25

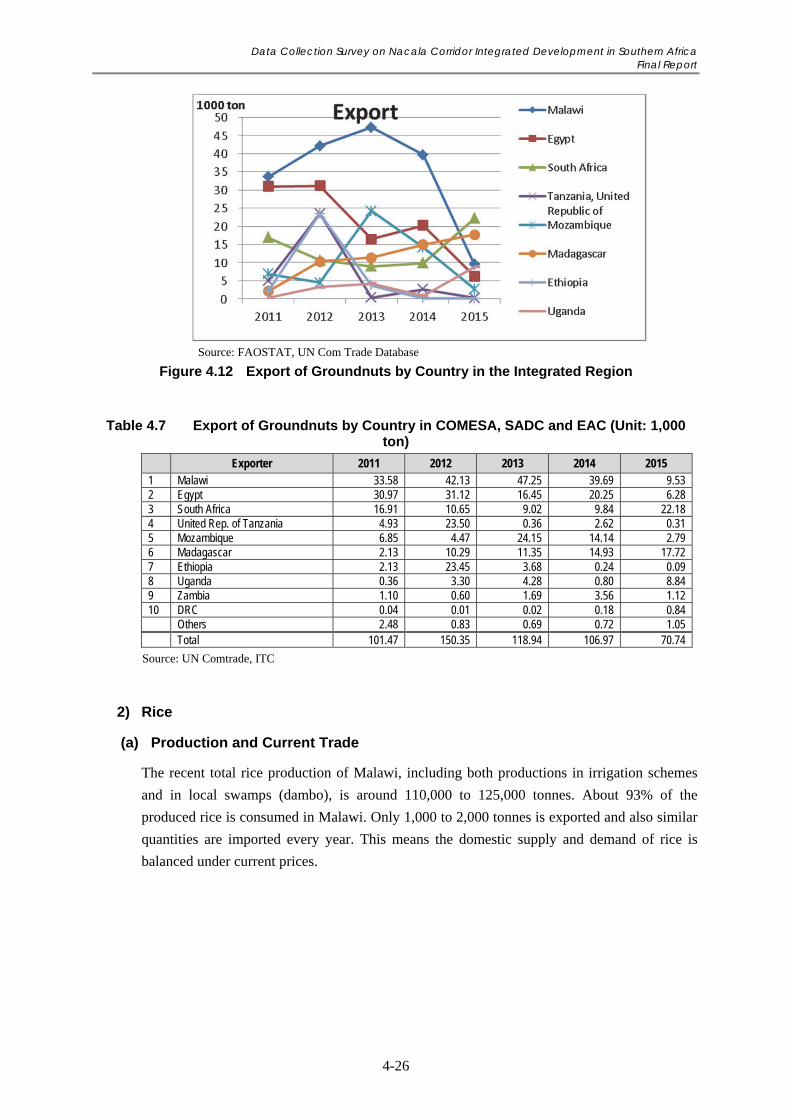

Table 4.7 Export of Groundnuts by Country in COMESA, SADC and EAC (Unit: 1,000 ton) .......... 4-26

Table 4.8 Export and Import of Rice by Malawi by Country (Unit: 1,000 ton) ................................... 4-27

Table 4.9 Import of Rice by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...................... 4-29

Table 4.10 Export of Rice by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ...................... 4-29

Table 4.11 Export and Import of Legumes by Malawi by County (Unit: 1,000 ton) ............................. 4-30

Table 4.12 Import of Chickpeas by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ............. 4-31

Table 4.13 Export of Chickpeas by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ............. 4-32

Table 4.14 Export of Pigeon Pea by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ........... 4-32

Table 4.15 Import of Pigeon Pea by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ........... 4-32

Table 4.16 Export of Cotton Lint by Malawi by Country (Unit: 1,000 tons) ......................................... 4-33

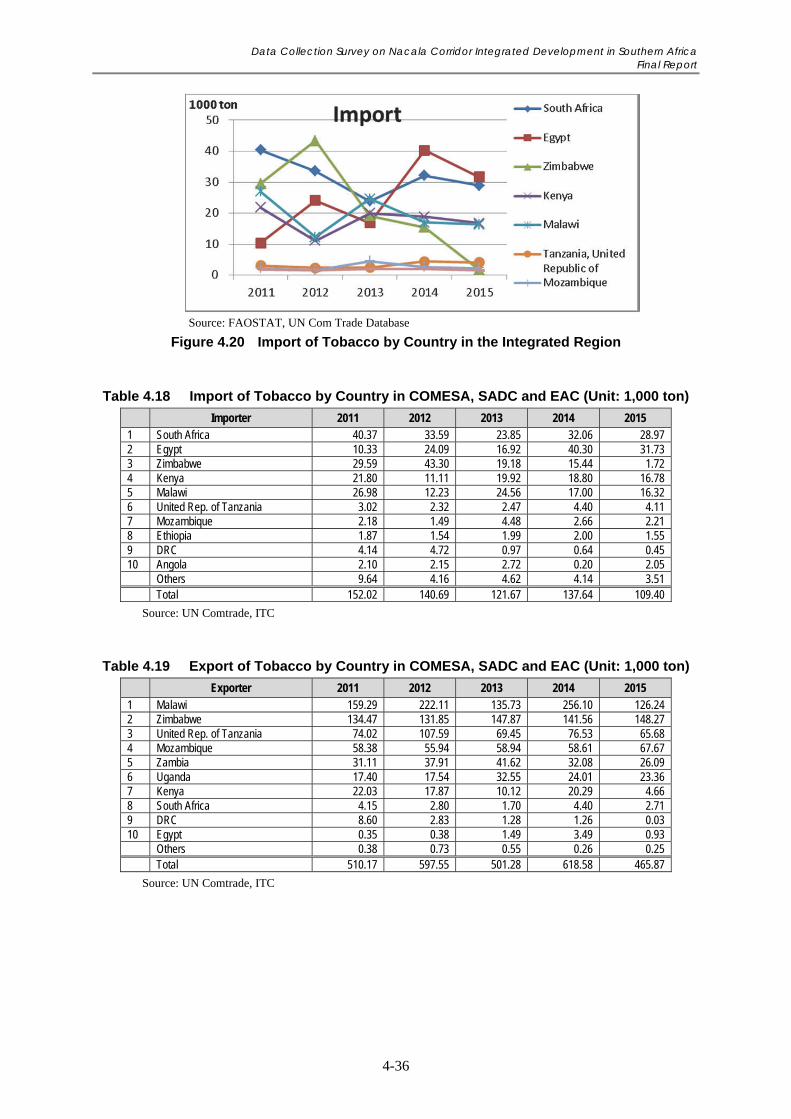

Table 4.17 Export and Import of Tobacco by Malawi by Country (Unit: 1000 tons) ............................ 4-35

Table 4.18 Import of Tobacco by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ................ 4-36

Table 4.19 Export of Tobacco by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ................ 4-36

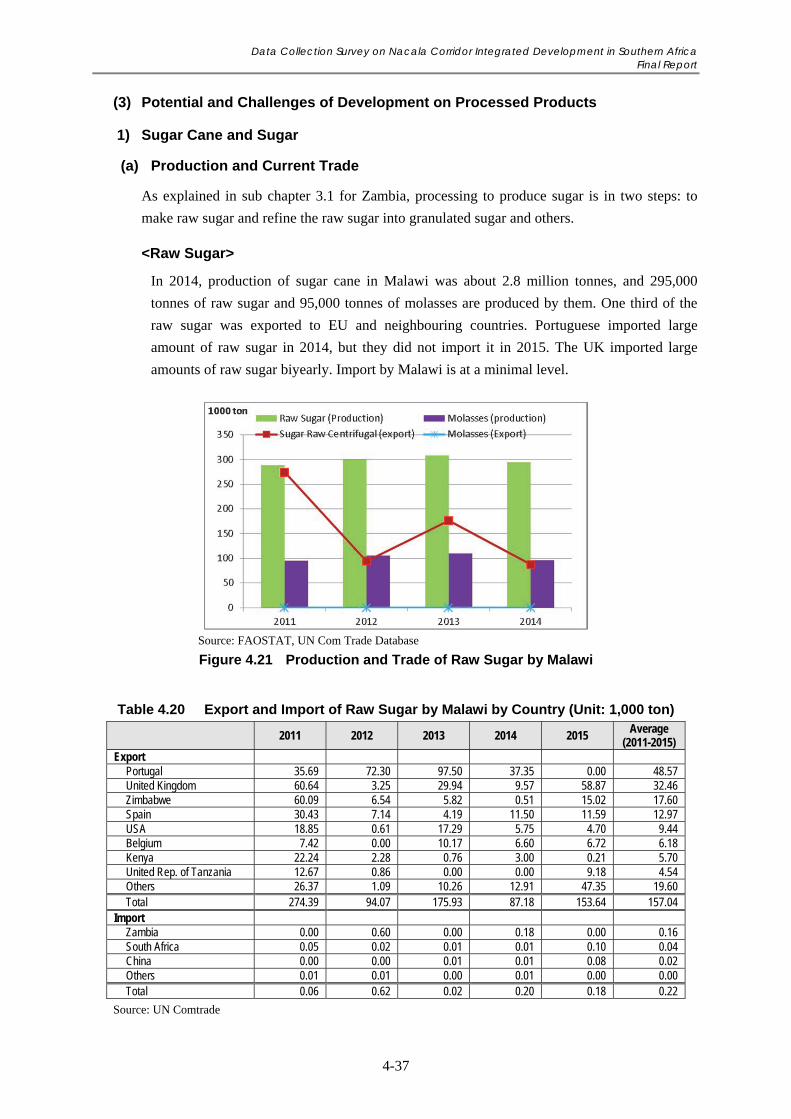

Table 4.20 Export and Import of Raw Sugar by Malawi by Country (Unit: 1,000 ton) ......................... 4-37

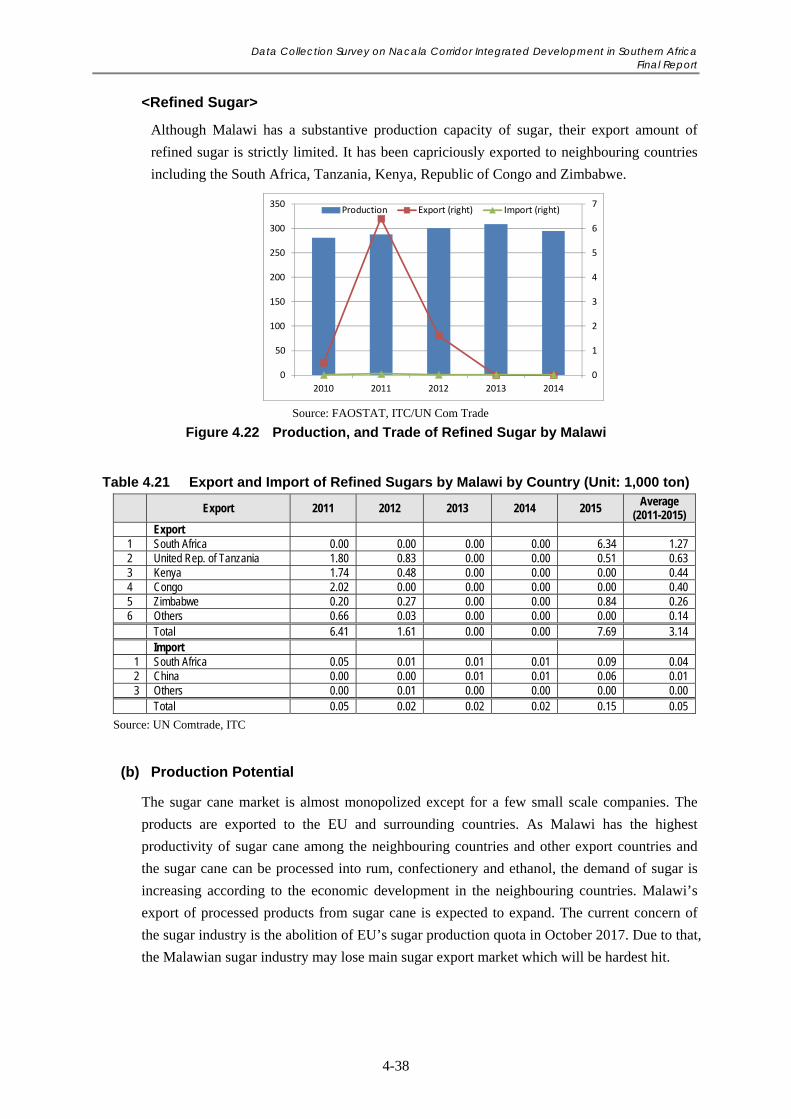

Table 4.21 Export and Import of Refined Sugars by Malawi by Country (Unit: 1,000 ton) .................. 4-38

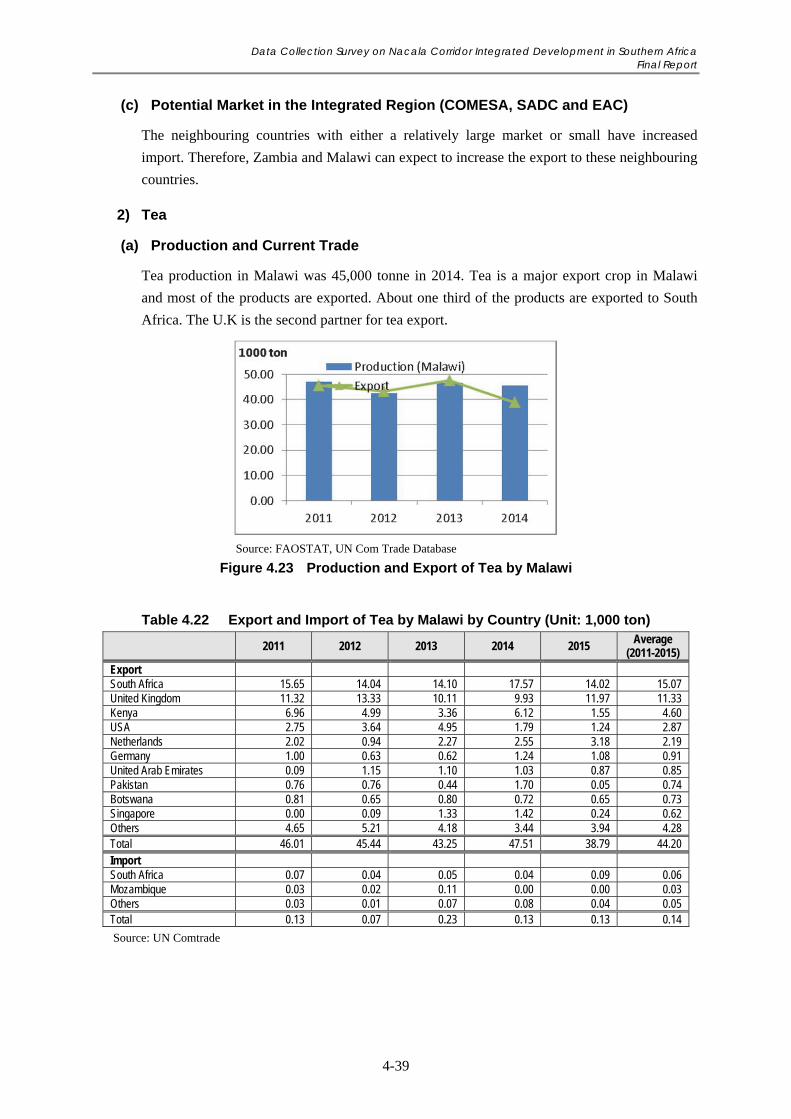

Table 4.22 Export and Import of Tea by Malawi by Country (Unit: 1,000 ton) ..................................... 4-39

Table 4.23 Import of Tea by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ....................... 4-40

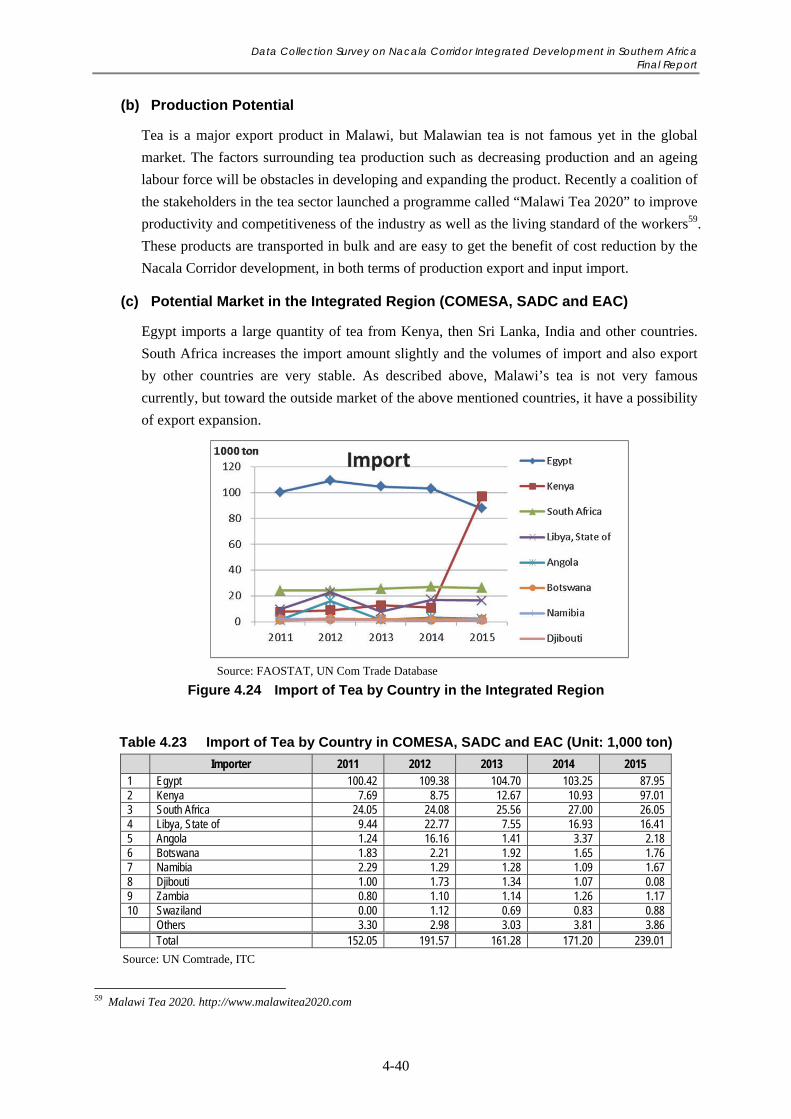

Table 4.24 Export of Tea by Country in COMESA, SADC and EAC (Unit: 1,000 ton) ....................... 4-41

Table 4.25 Export and Import of Soya Beans by Malawi by Country (Unit: 1,000 ton) ........................ 4-42

Table 4.26 Import of Soya Bean Oil by Malawi by Country (Unit: 1,000 ton) ...................................... 4-42

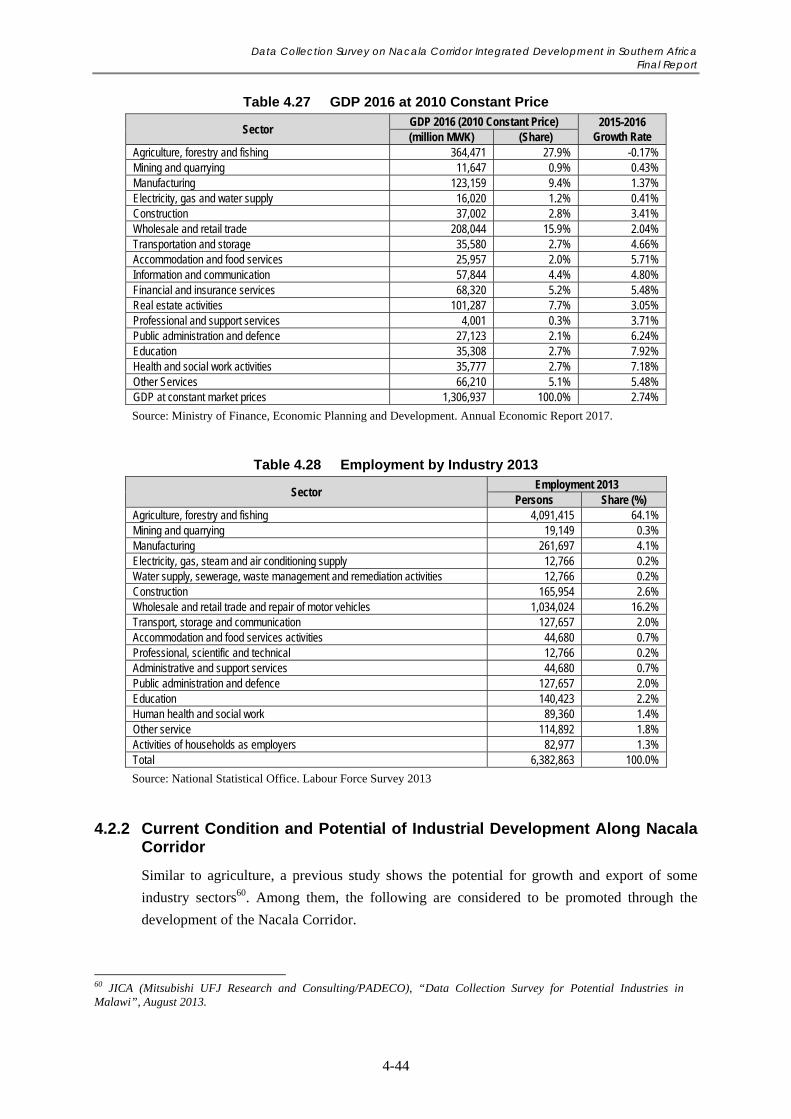

Table 4.27 GDP 2016 at 2010 Constant Price ........................................................................................ 4-44

Table 4.28 Employment by Industry 2013 ............................................................................................. 4-44

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

ix

Table 4.29 Contribution of Mining and Quarrying Sector to the National Economy

(Million MWK at 2010 Constant Price) ............................................................................... 4-45

Table 4.30 Mineral Production in 2015 and 2016 .................................................................................. 4-46

Table 4.31 Mineral Export in 2015 and 2016 ......................................................................................... 4-47

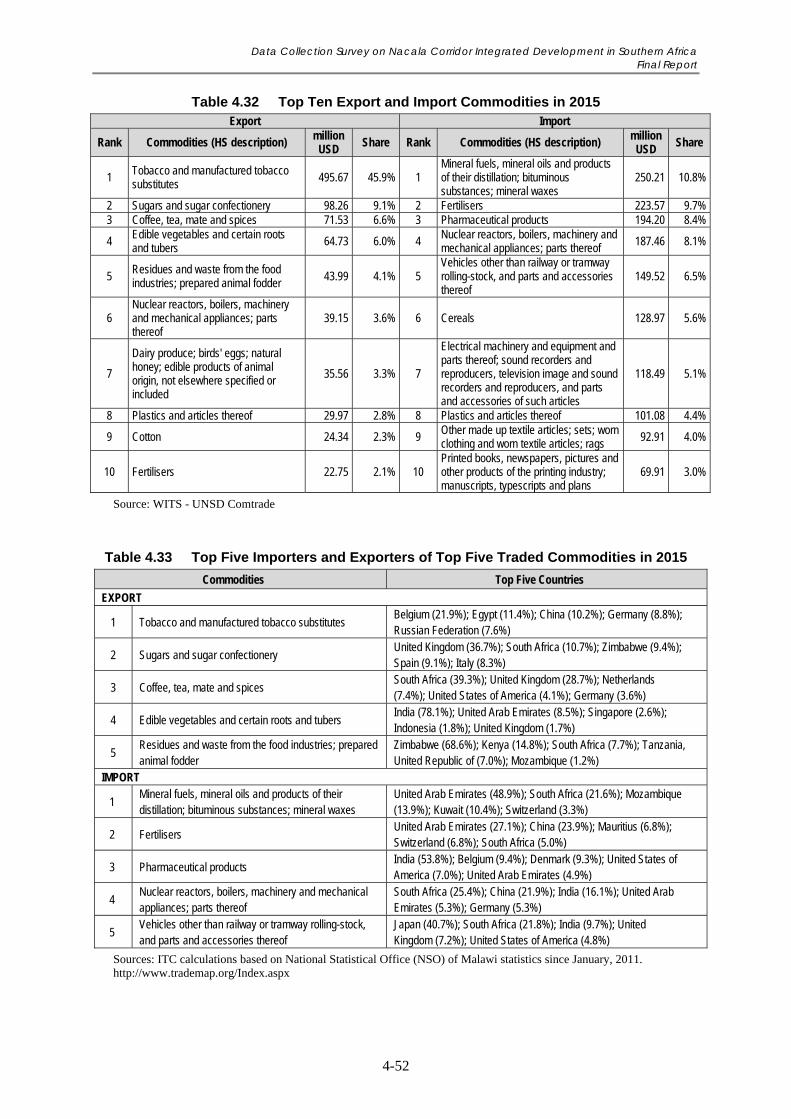

Table 4.32 Top Ten Export and Import Commodities in 2015 ............................................................... 4-52

Table 4.33 Top Five Importers and Exporters of Top Five Traded Commodities in 2015 ..................... 4-52

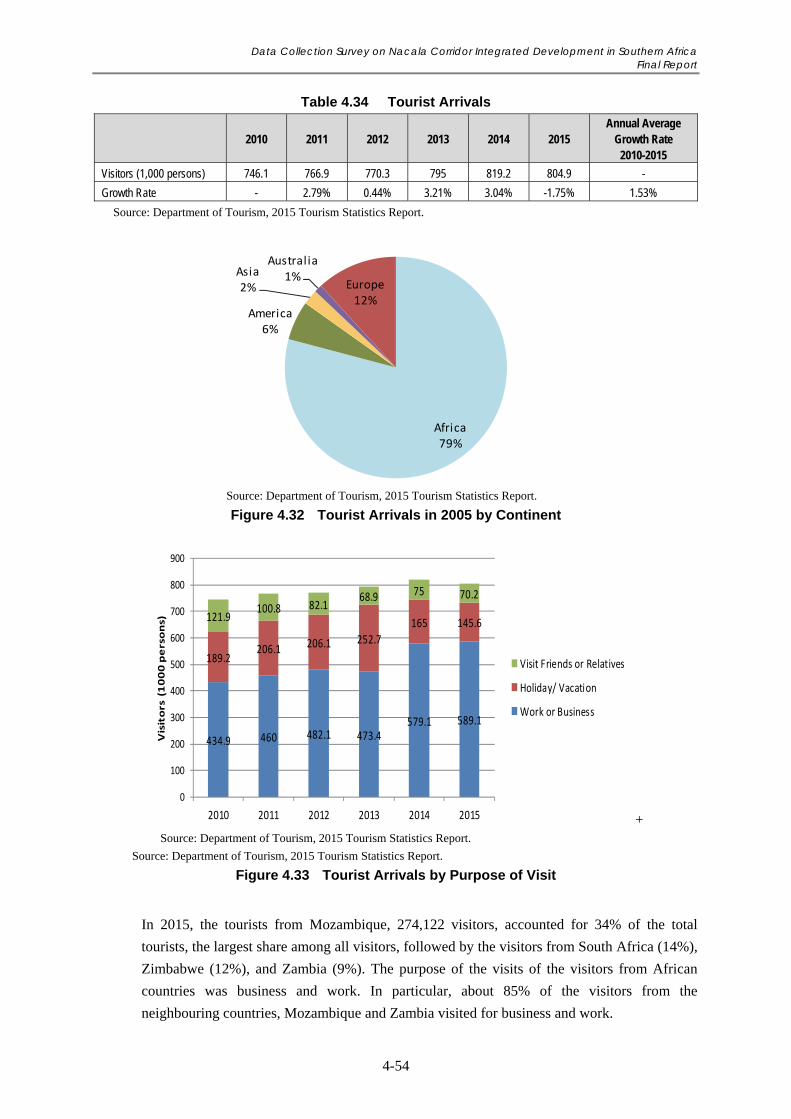

Table 4.34 Tourist Arrivals ..................................................................................................................... 4-54

Table 4.35 Expenditures by Purpose of Visit and Average Number of Nights in 2015 ......................... 4-56

Table 4.36 Annual Average Room and Bed Occupancy Rates in 2015 ................................................. 4-56

Table 4.37 Tourist Arrivals by Port of Entry Along Nacala Corridor in 2015 ....................................... 4-56

Table 4.38 Visions and Objectives in Malawi 2020 Tourism Development Strategy ............................ 4-57

Table 4.39 Challenges to the Tourism Sector ......................................................................................... 4-58

Table 4.40 Access to Electricity ............................................................................................................. 4-59

Table 4.41 Installed Capacity and Peak Demand from 2007 to 2016 ..................................................... 4-59

Table 4.42 Existing Power Stations ........................................................................................................ 4-59

Table 4.43 Peak Demand Forecast.......................................................................................................... 4-60

Table 4.44 Stand-by Power Supply Installation, Electricity Generation and Demand by Industry

in 2012 .................................................................................................................................. 4-61

Table 4.45 Fuel Import from 2000 to 2016 ............................................................................................. 4-62

Table 4.46 Fuel Import by Corridor from 2000 to 2016 (Thousand Litres) ........................................... 4-63

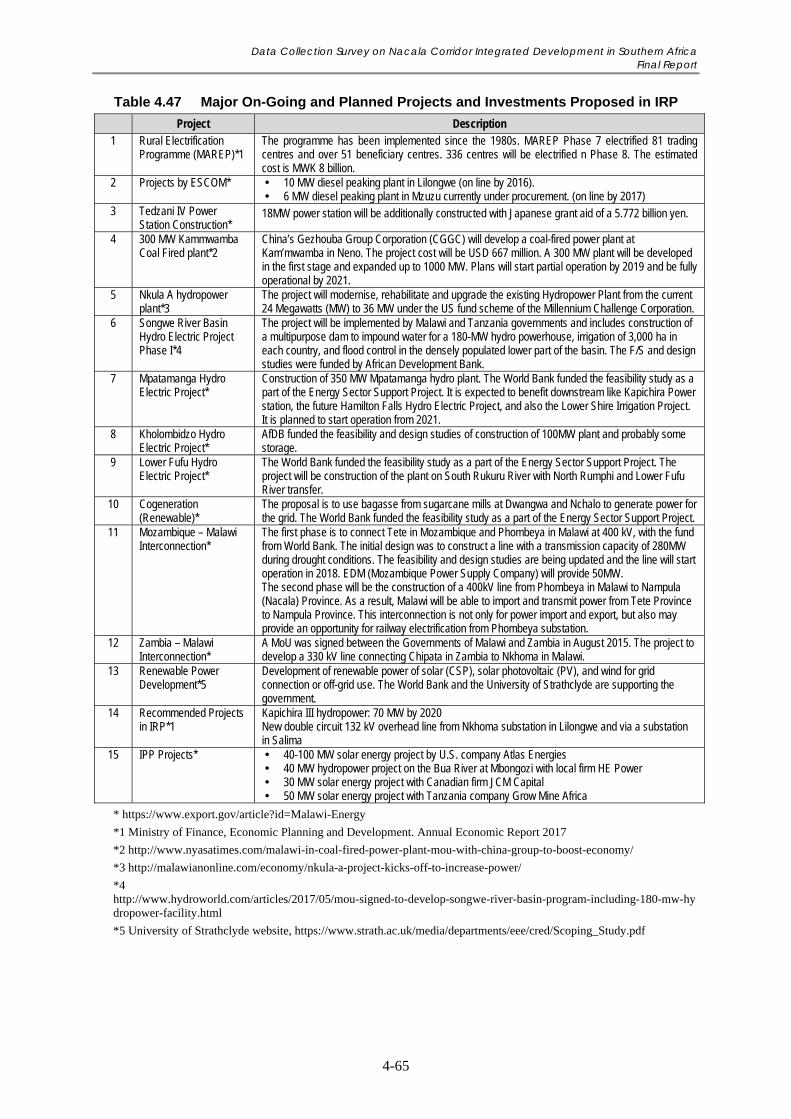

Table 4.47 Major On-Going and Planned Projects and Investments Proposed in IRP ........................... 4-65

Table 4.48 Major Large Scale Investment Projects in 2016 ................................................................... 4-67

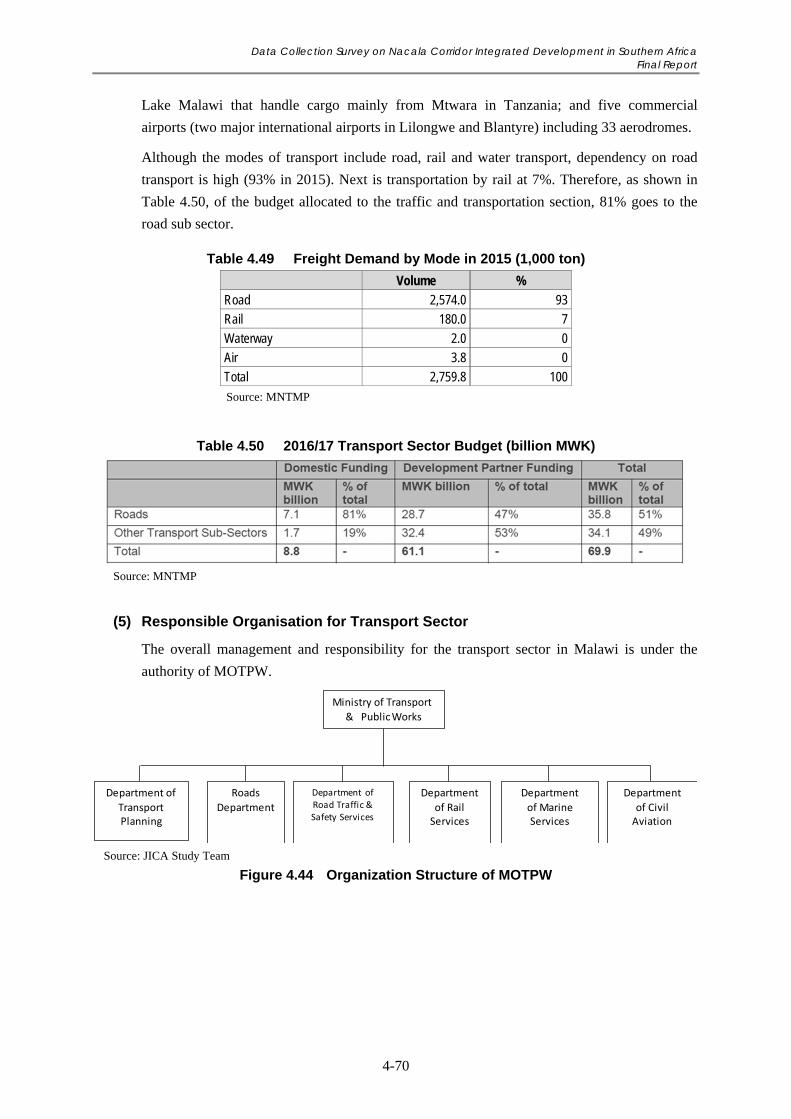

Table 4.49 Freight Demand by Mode in 2015 (1,000 ton) ..................................................................... 4-70

Table 4.50 2016/17 Transport Sector Budget (billion MWK) ................................................................ 4-70

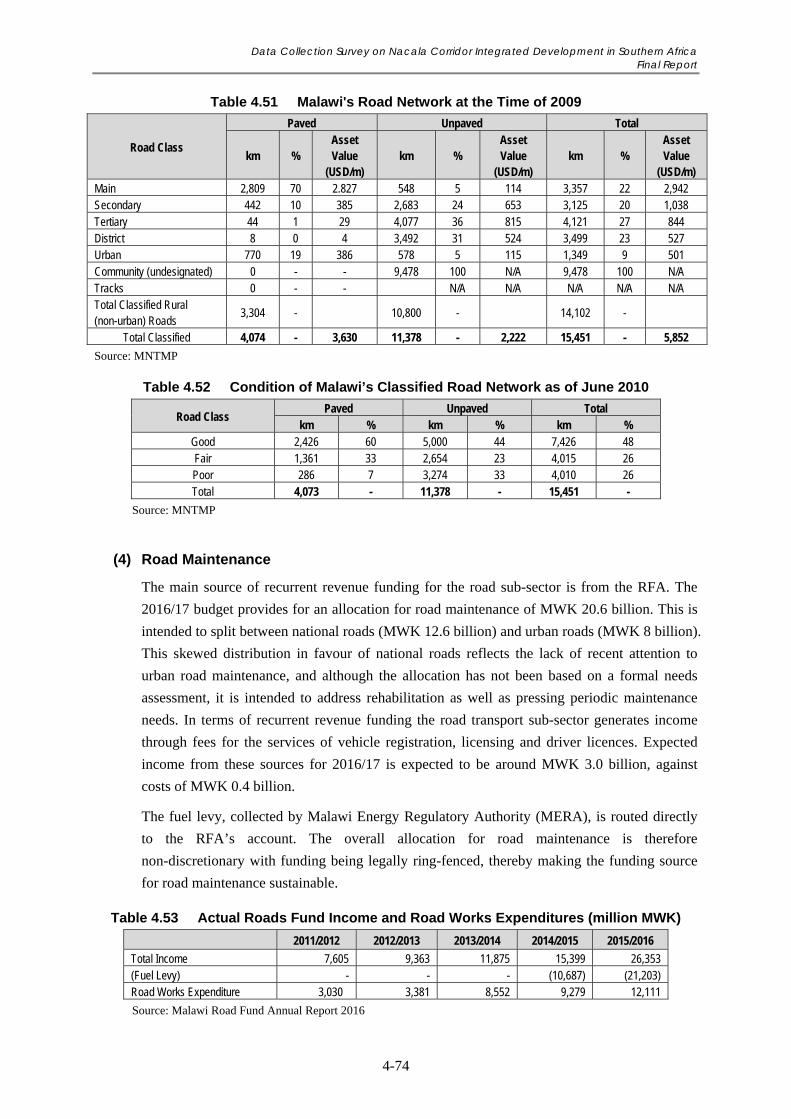

Table 4.51 Malawi's Road Network at the Time of 2009 ....................................................................... 4-74

Table 4.52 Condition of Malawi’s Classified Road Network as of June 2010 ....................................... 4-74

Table 4.53 Actual Roads Fund Income and Road Works Expenditures (million MWK) ....................... 4-74

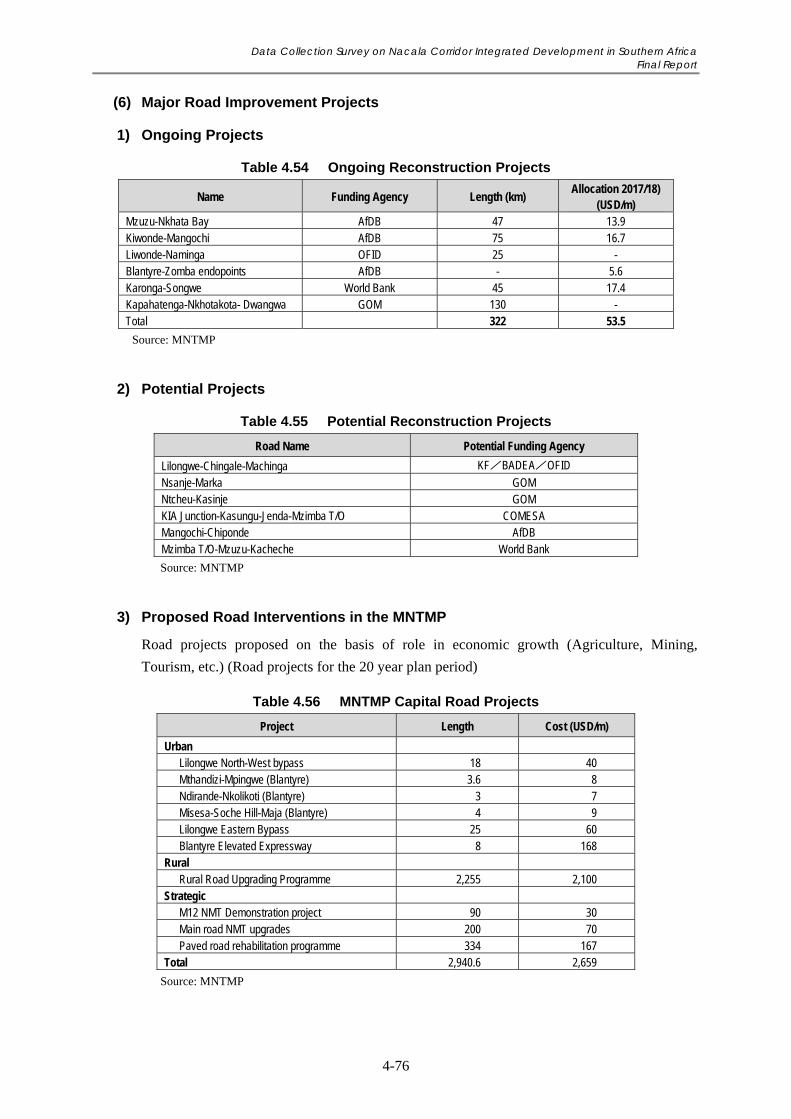

Table 4.54 Ongoing Reconstruction Projects ......................................................................................... 4-76

Table 4.55 Potential Reconstruction Projects ......................................................................................... 4-76

Table 4.56 MNTMP Capital Road Projects ............................................................................................ 4-76

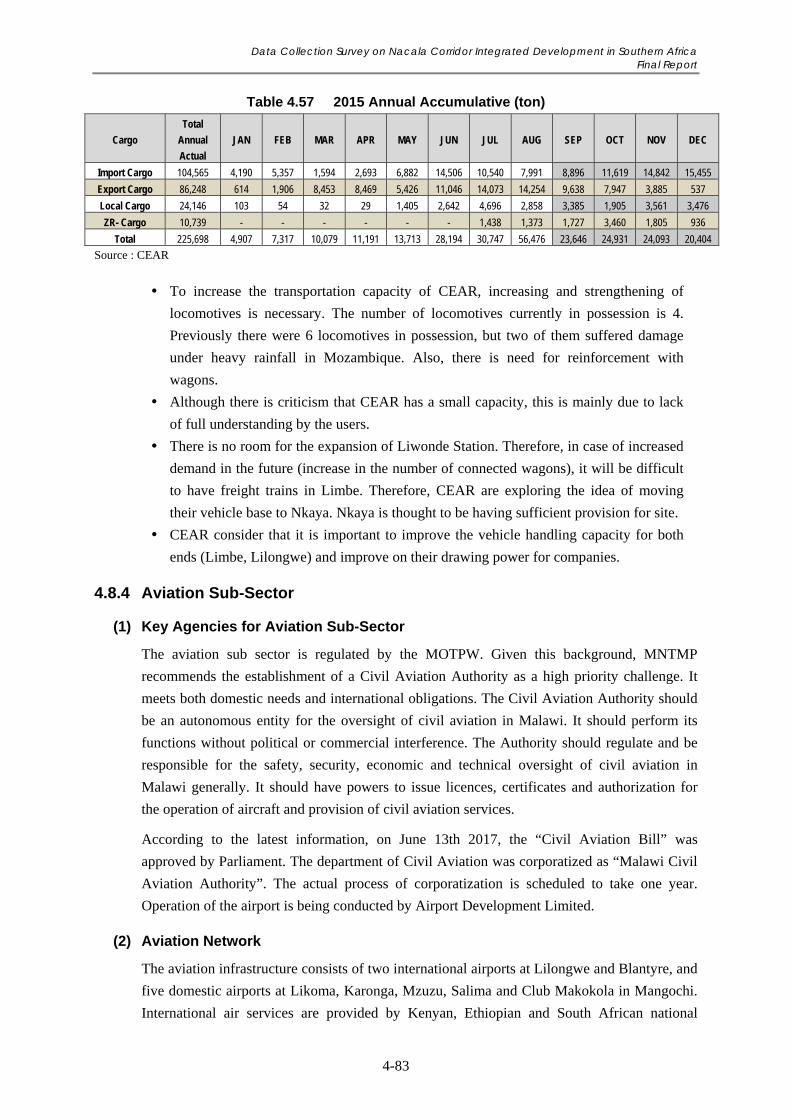

Table 4.57 2015 Annual Accumulative (ton) ......................................................................................... 4-83

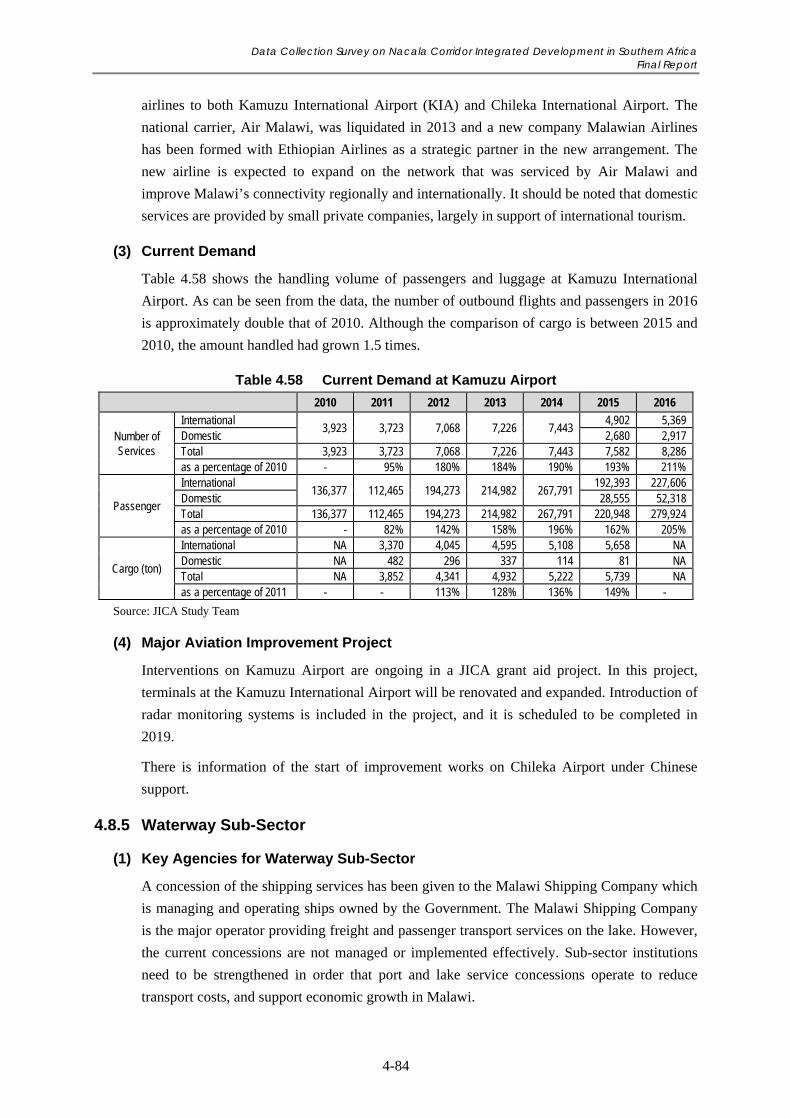

Table 4.58 Current Demand at Kamuzu Airport..................................................................................... 4-84

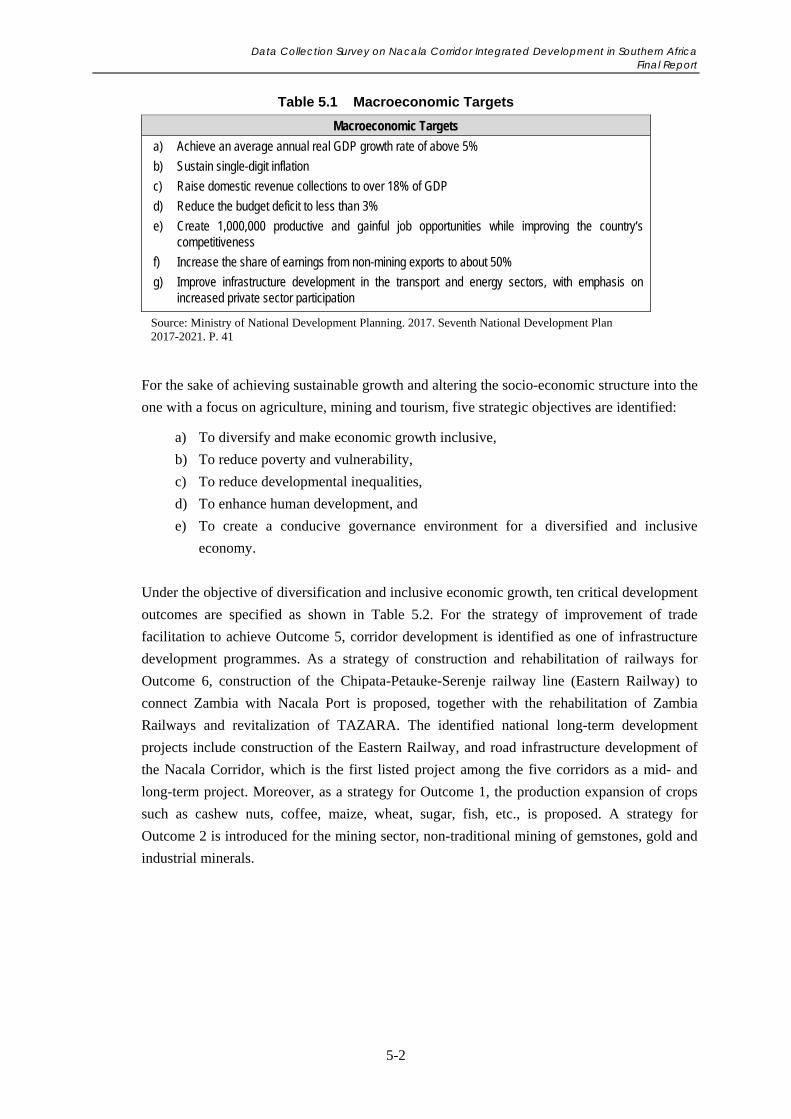

Table 5.1 Macroeconomic Targets ......................................................................................................... 5-2

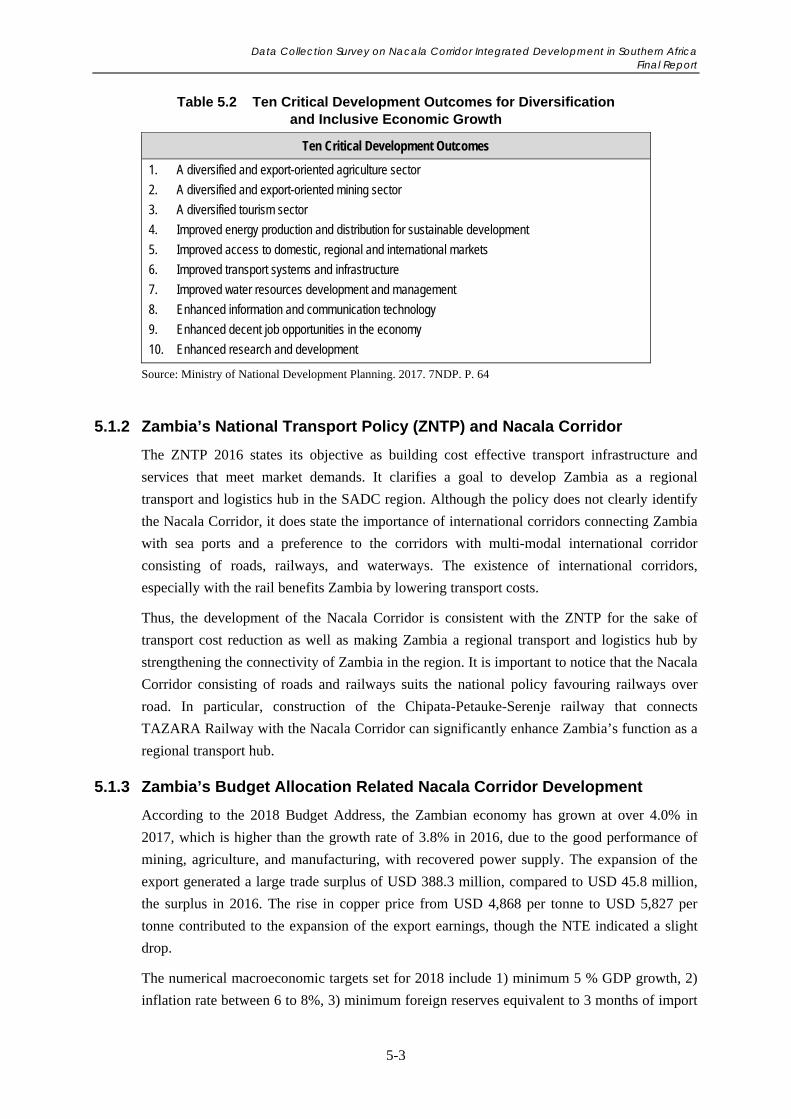

Table 5.2 Ten Critical Development Outcomes for Diversification and Inclusive Economic

Growth .................................................................................................................................... 5-3

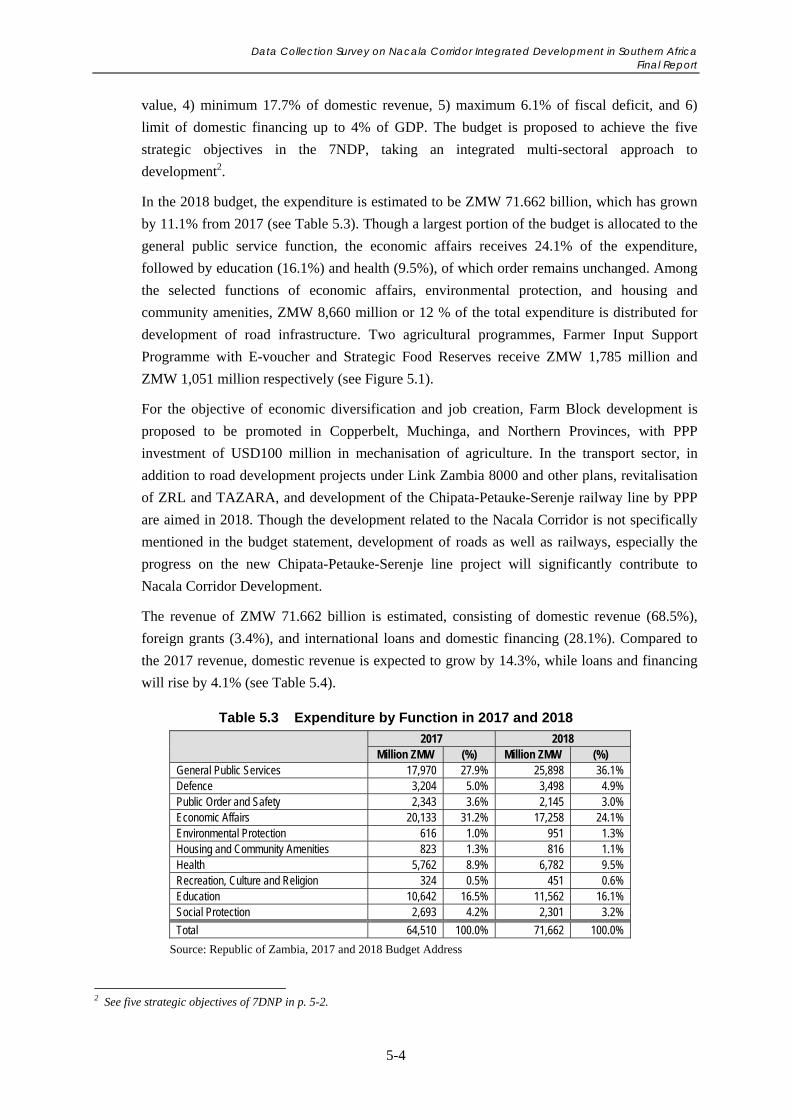

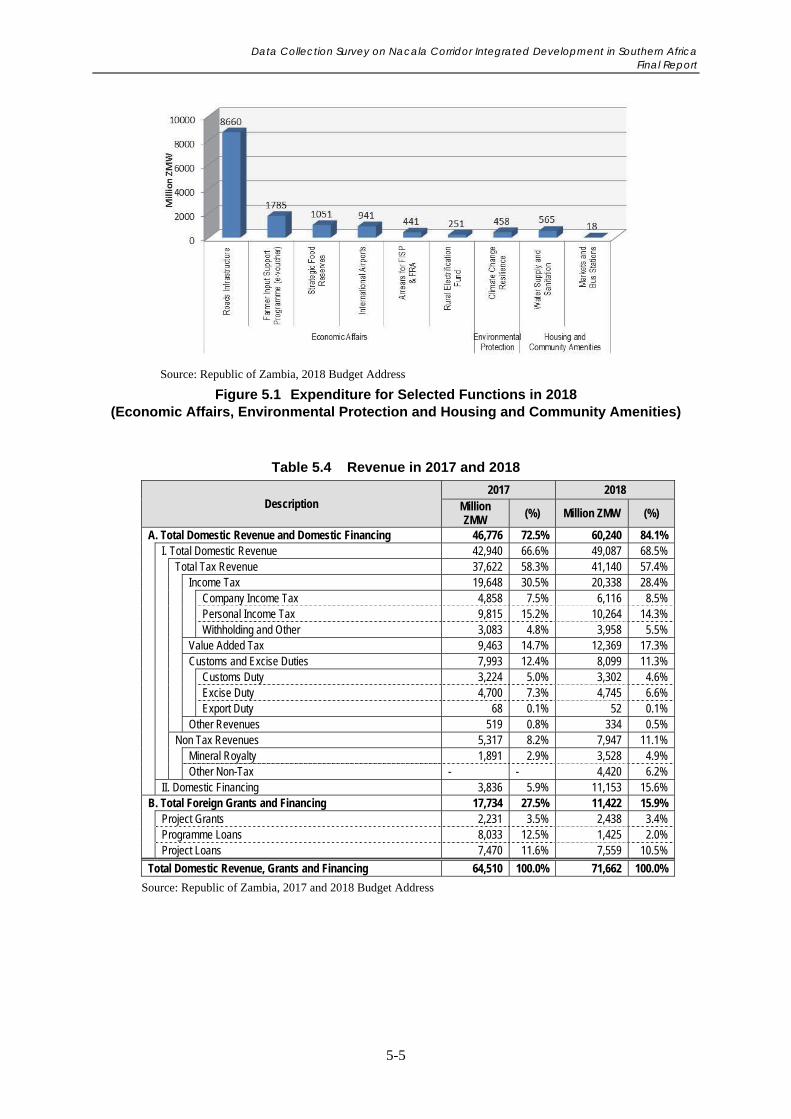

Table 5.3 Expenditure by Function in 2017 and 2018 ............................................................................ 5-4

Table 5.4 Revenue in 2017 and 2018 ...................................................................................................... 5-5

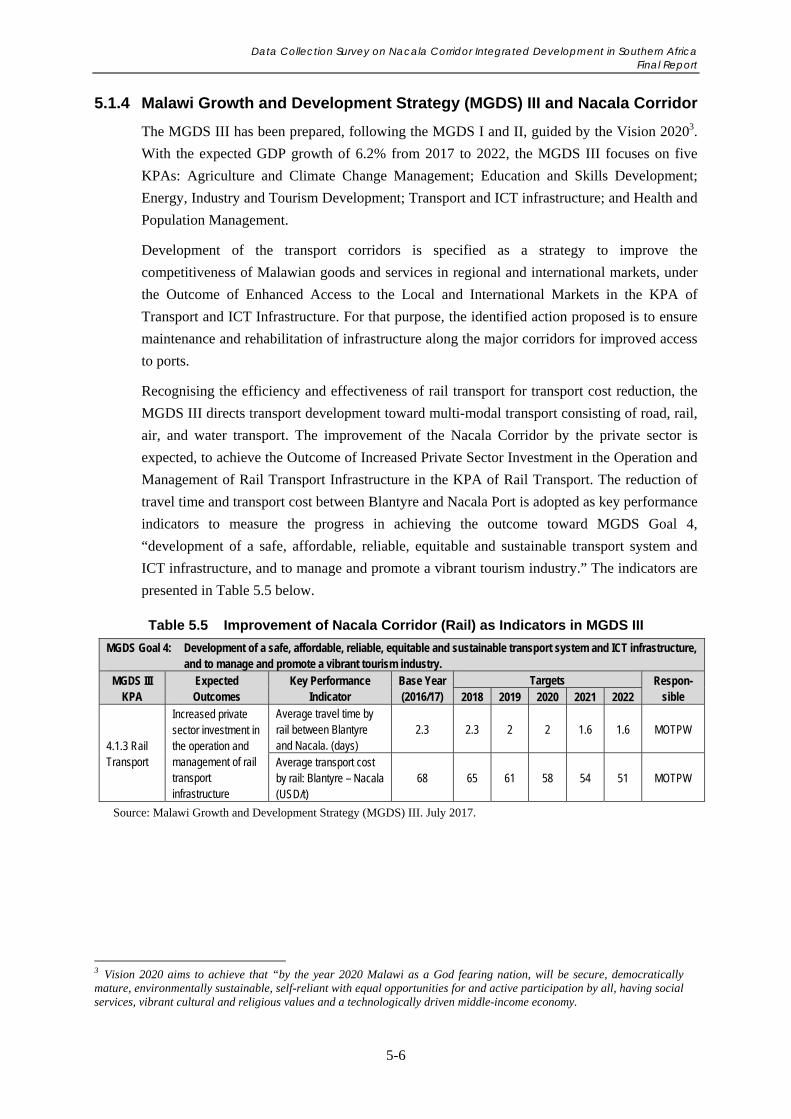

Table 5.5 Improvement of Nacala Corridor (Rail) as Indicators in MGDS III ....................................... 5-6

Table 5.6 Expenditure from 2016/17 to 2018/19 .................................................................................. 5-10

Table 5.7 Revenue, Grants and Financing from 2016/17 to 2018/19 ................................................... 5-12

Table 5.8 Food and Cash Crop Production in Eastern Province, 2005/06–2014/15 ............................. 5-15

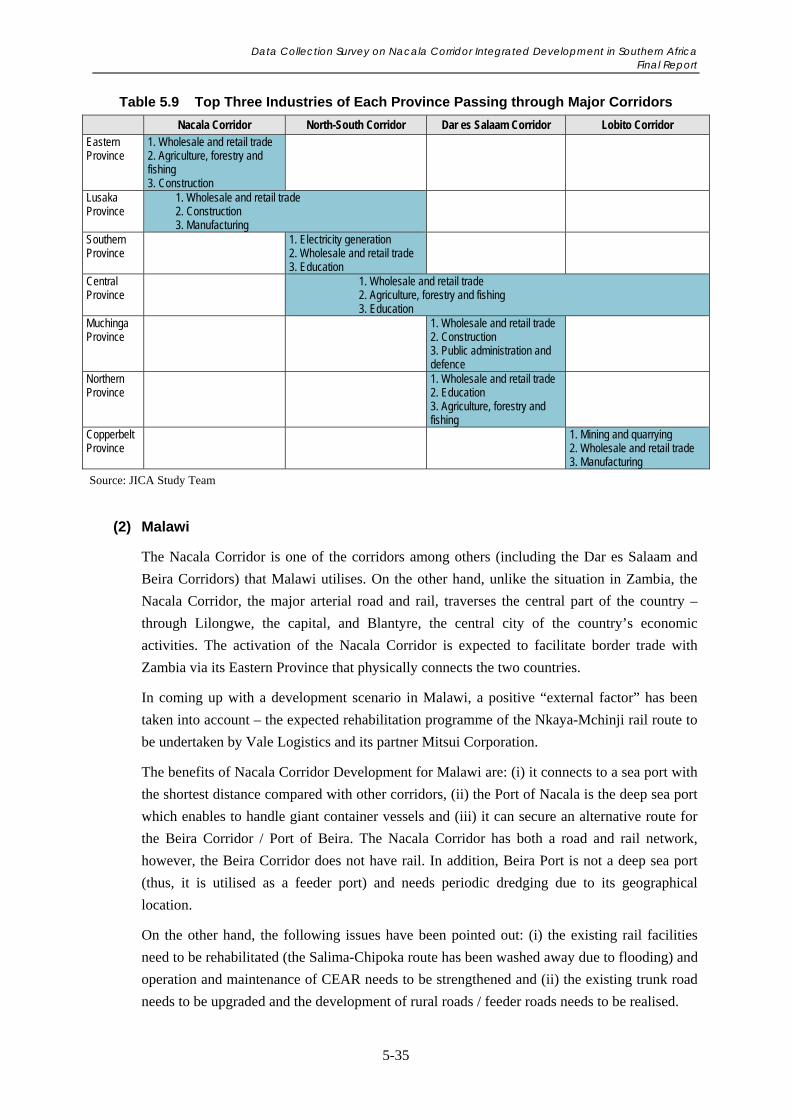

Table 5.9 Top Three Industries of Each Province Passing through Major Corridors ........................... 5-35

Table 5.10 Freight Demand by Mode in 2015 (1,000 ton) ..................................................................... 5-36

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

x

Table 5.11 Pure Transport Cost by Commodity in 2016 ........................................................................ 5-36

Table 5.12 Transit Time and Costs for the Major Towns from Various Ports ....................................... 5-37

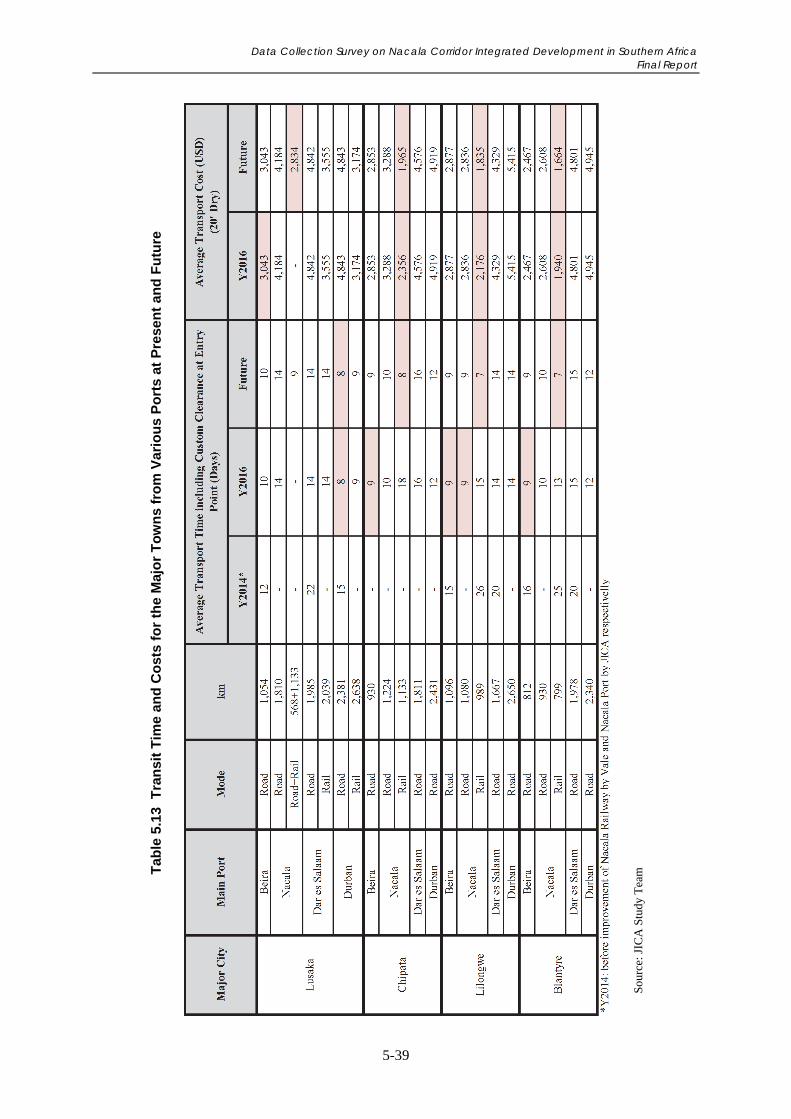

Table 5.13 Transit Time and Costs for the Major Towns from Various Ports at Present and Future ..... 5-39

Table 5.14 Impacts of Nacala Corridor Development on Transport Time and Cost .............................. 5-40

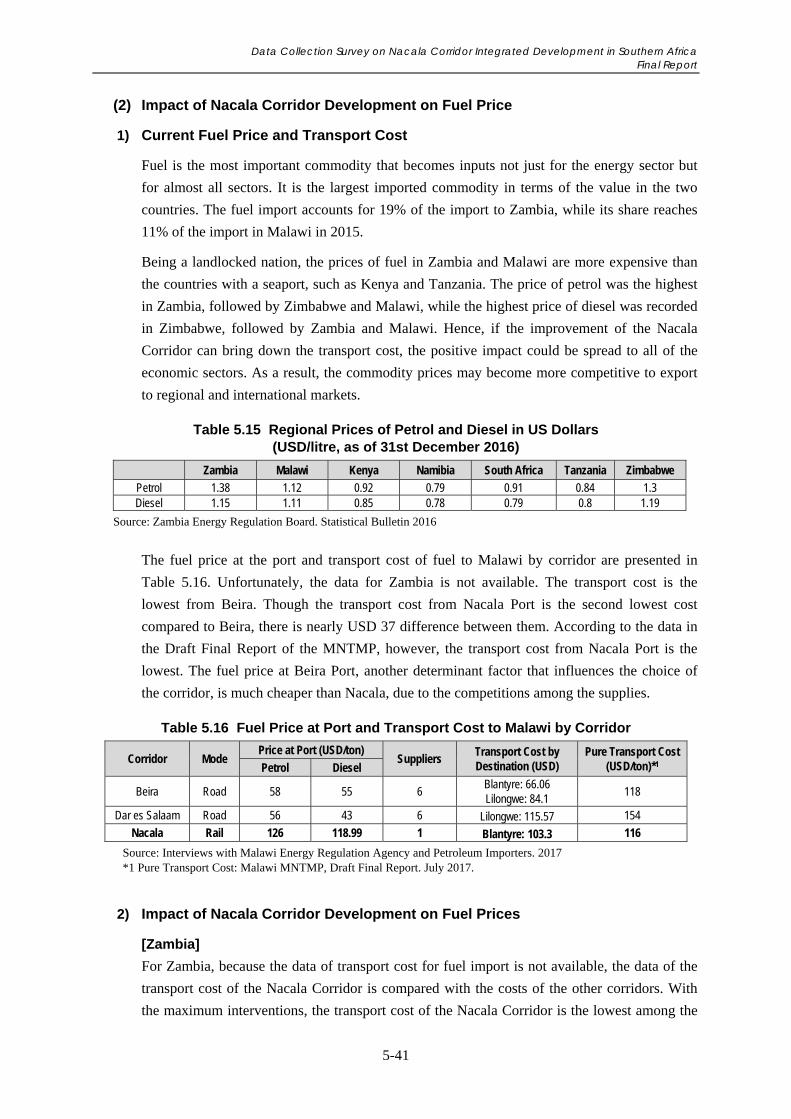

Table 5.15 Regional Prices of Petrol and Diesel in US Dollars (USD/litre, as of 31st

December 2016) .................................................................................................................... 5-41

Table 5.16 Fuel Price at Port and Transport Cost to Malawi by Corridor .............................................. 5-41

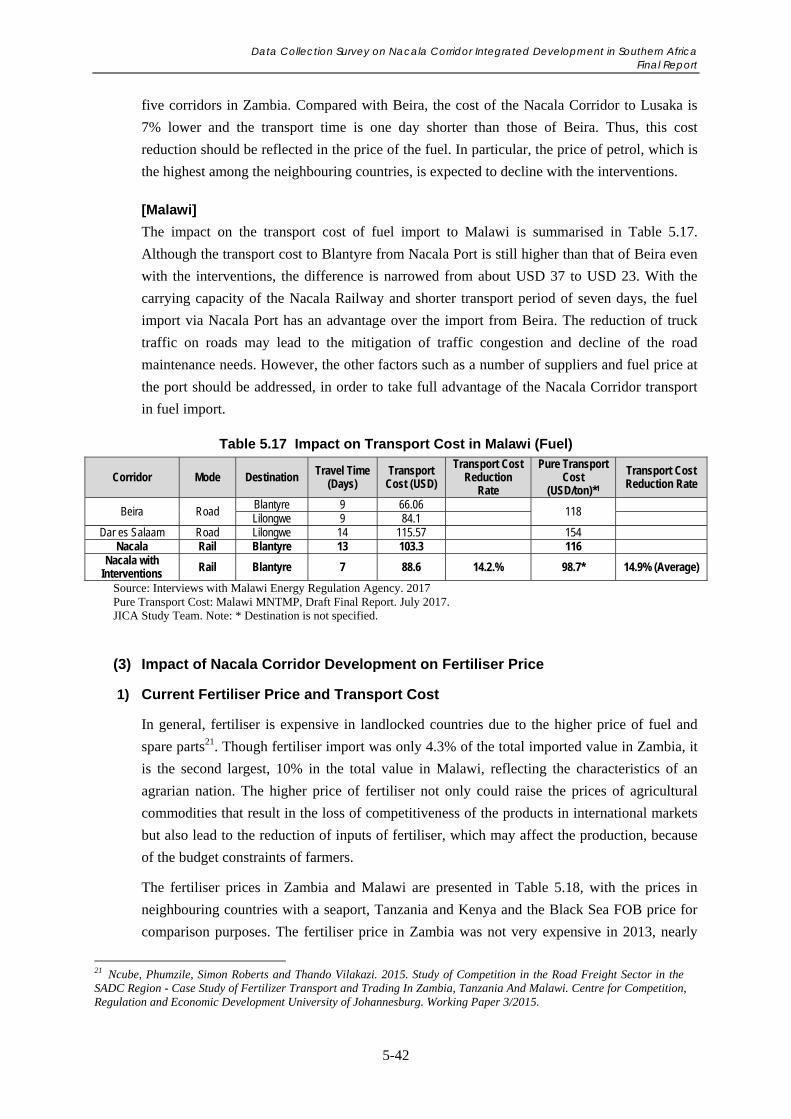

Table 5.17 Impact on Transport Cost in Malawi (Fuel) ......................................................................... 5-42

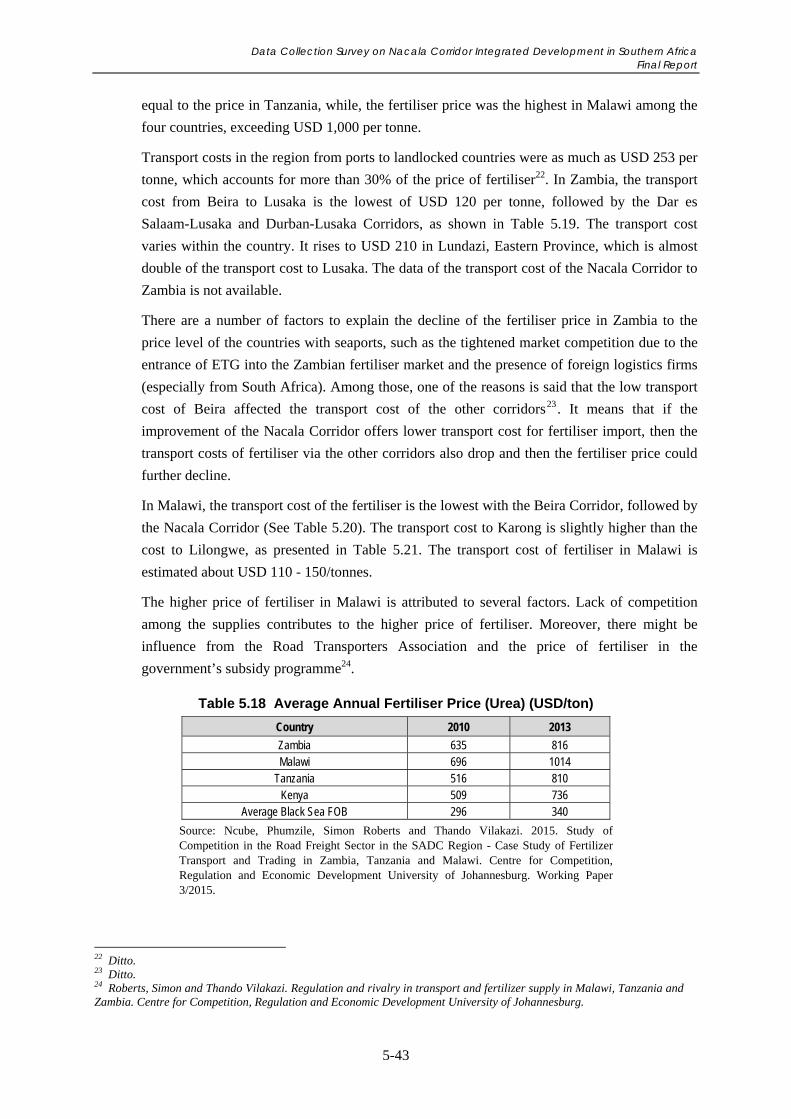

Table 5.18 Average Annual Fertiliser Price (Urea) (USD/ton) .............................................................. 5-43

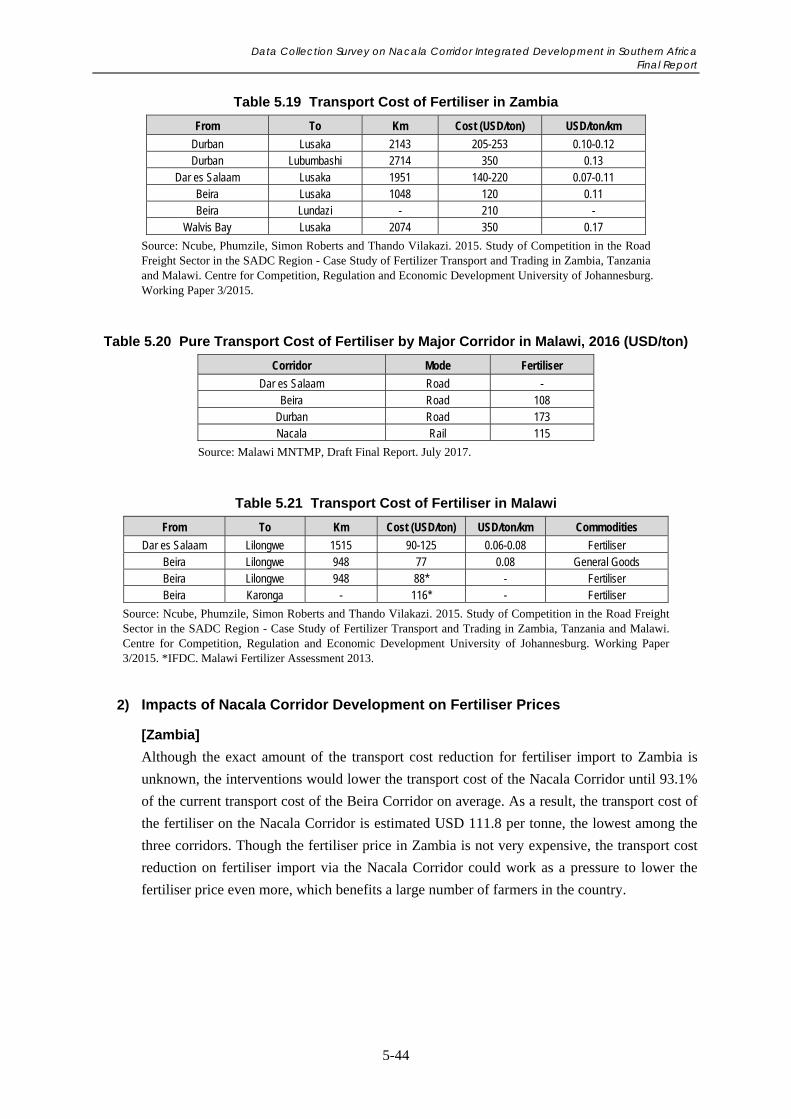

Table 5.19 Transport Cost of Fertiliser in Zambia .................................................................................. 5-44

Table 5.20 Pure Transport Cost of Fertiliser by Major Corridor in Malawi, 2016 (USD/ton) ............... 5-44

Table 5.21 Transport Cost of Fertiliser in Malawi .................................................................................. 5-44

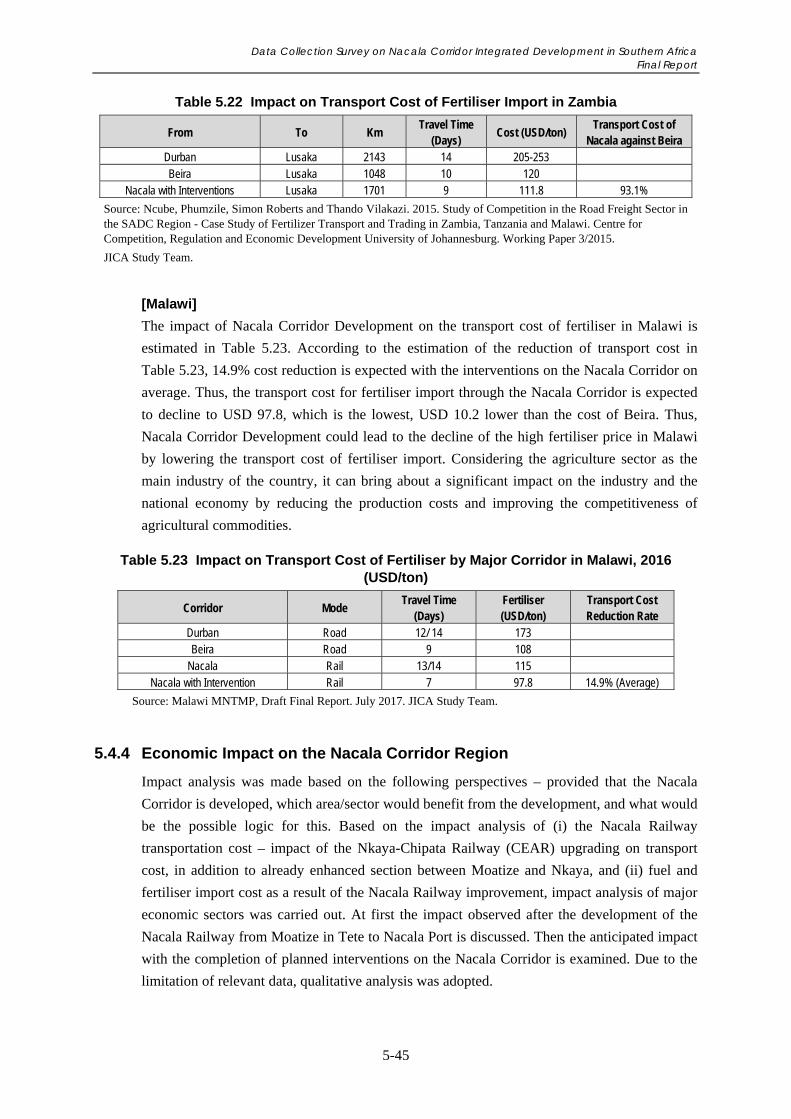

Table 5.22 Impact on Transport Cost of Fertiliser Import in Zambia ..................................................... 5-45

Table 5.23 Impact on Transport Cost of Fertiliser by Major Corridor in Malawi, 2016 (USD/ton) ...... 5-45

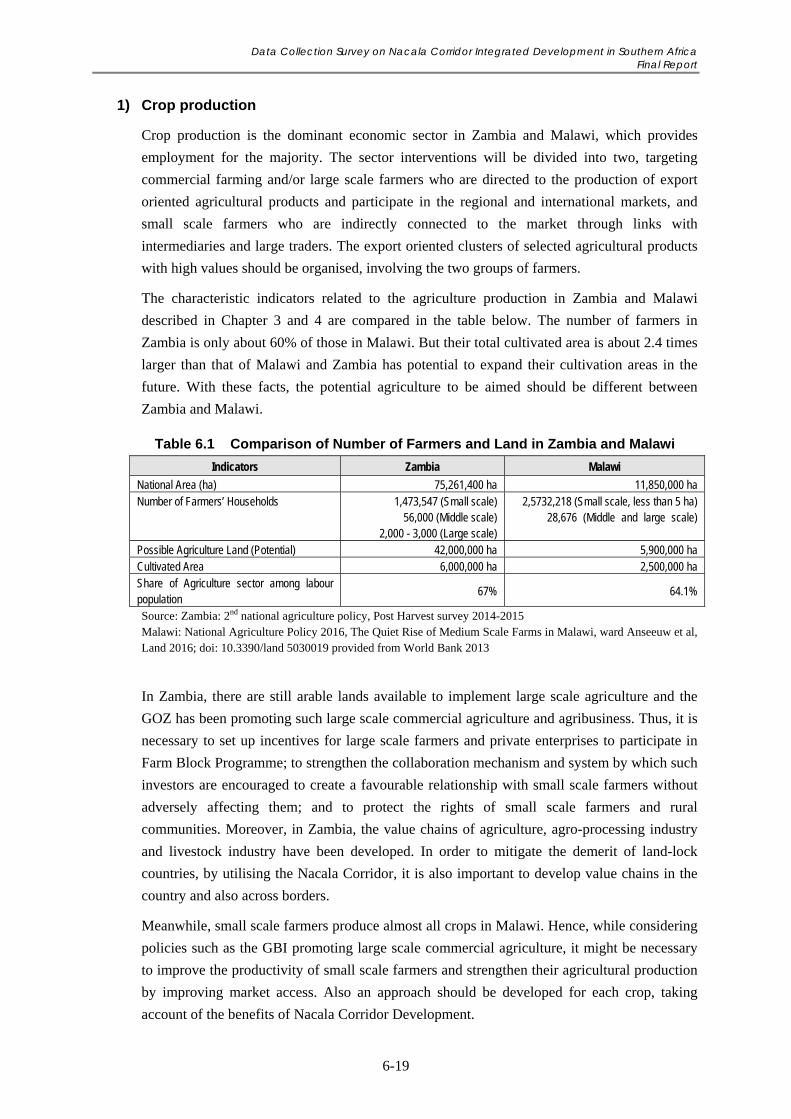

Table 6.1 Comparison of Number of Farmers and Land in Zambia and Malawi ................................. 6-19

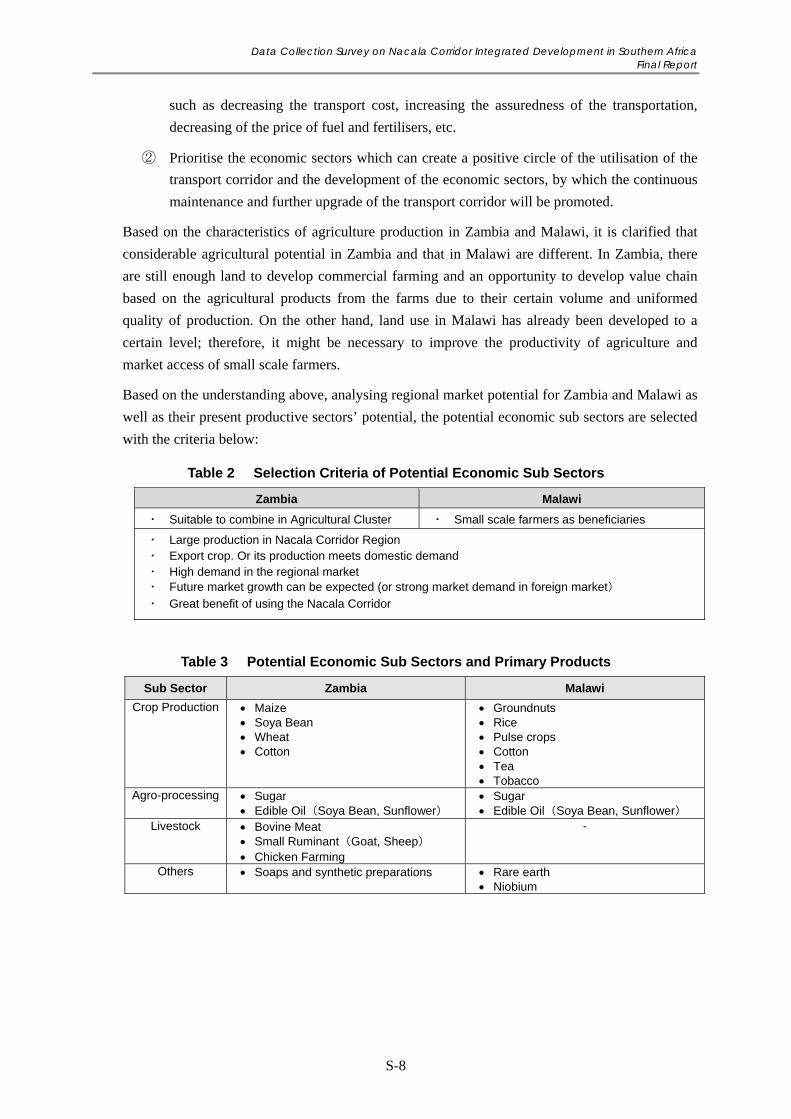

Table 6.2 Selection Criteria of Potential Economic Sub Sectors .......................................................... 6-20

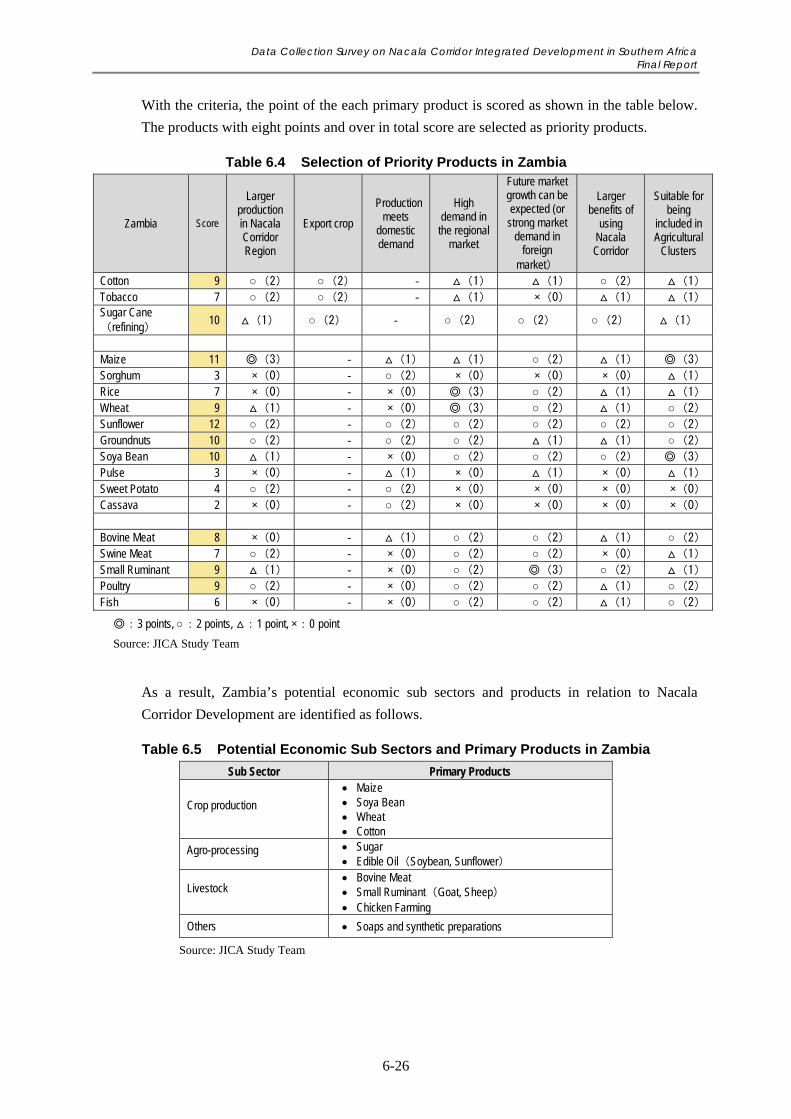

Table 6.3 Selection Criteria of Potential Economic Sub Sectors in Zambia ......................................... 6-25

Table 6.4 Selection of Priority Products in Zambia .............................................................................. 6-26

Table 6.5 Potential Economic Sub Sectors and Primary Products in Zambia ...................................... 6-26

Table 6.6 Selection Criteria of Potential Economic Sub Sectors in Malawi ......................................... 6-34

Table 6.7 Selection of Priority Products in Malawi .............................................................................. 6-34

Table 6.8 Potential Economic Sub Sectors and Primary Products for Malawi ..................................... 6-35

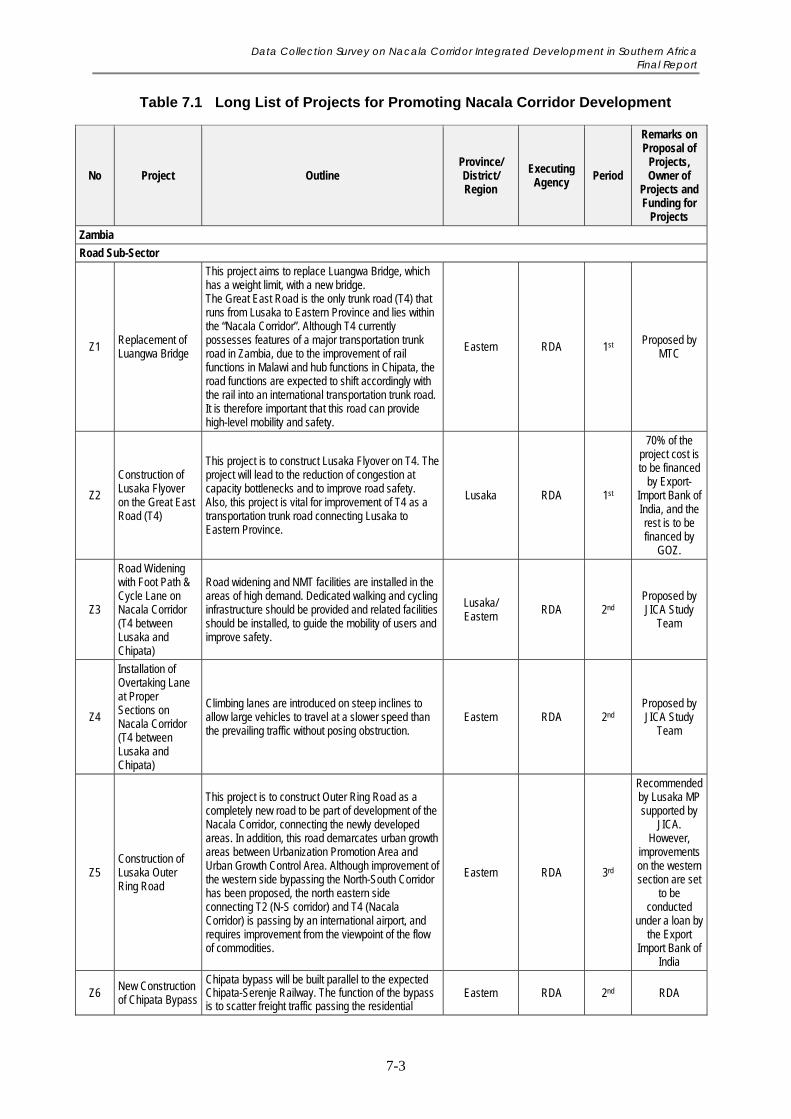

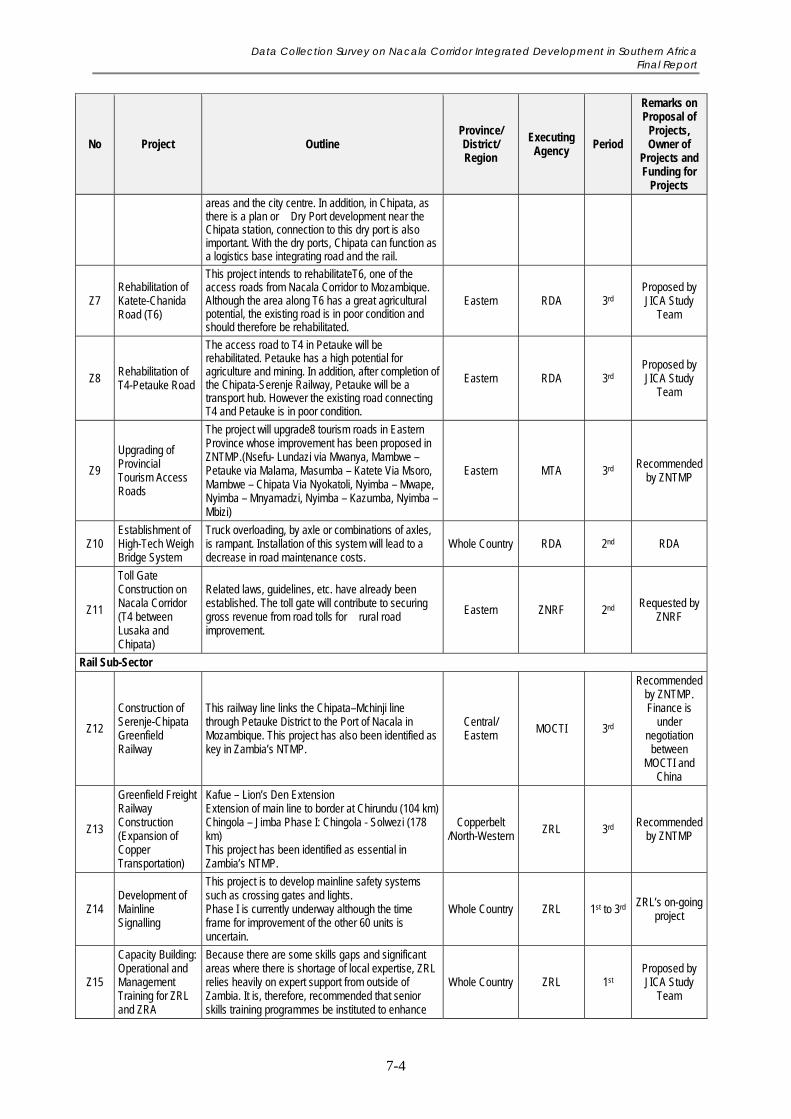

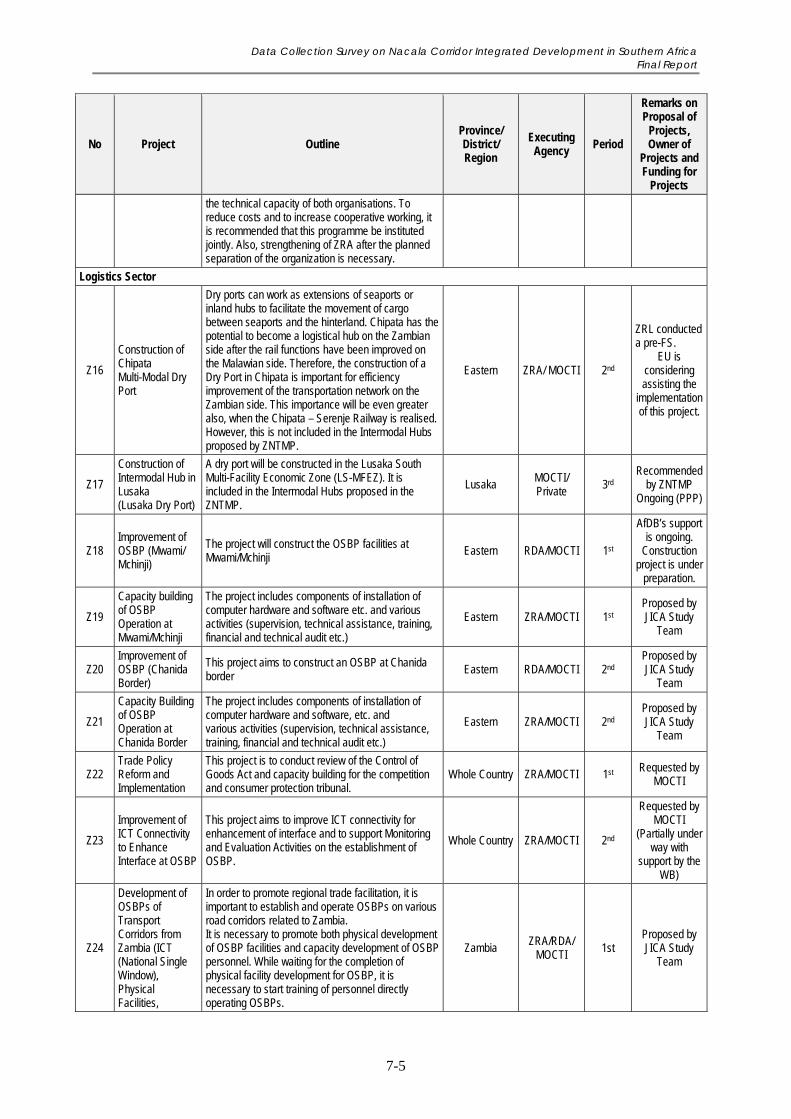

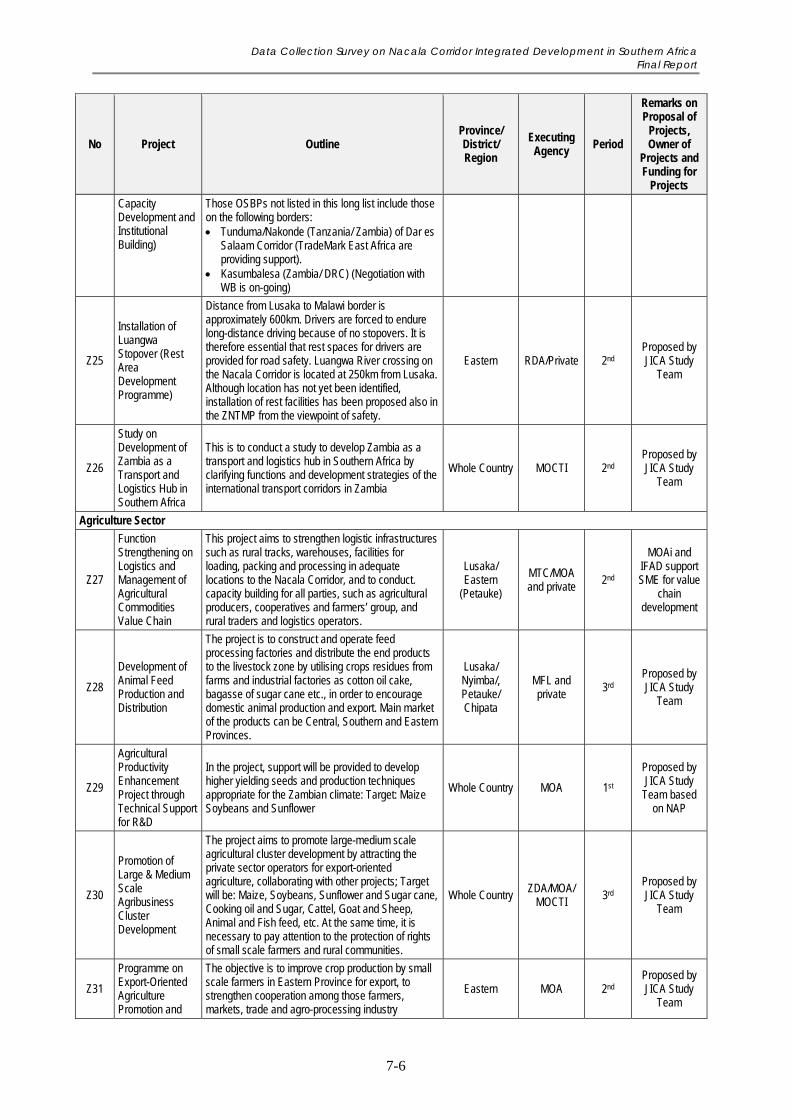

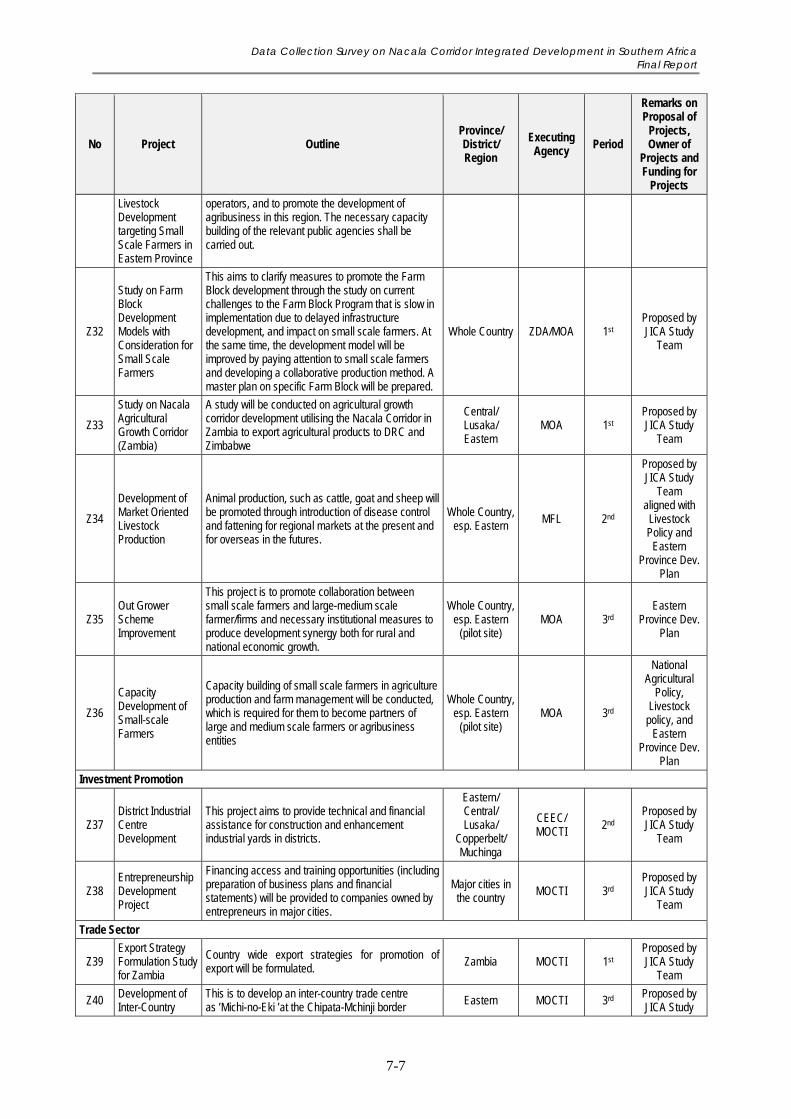

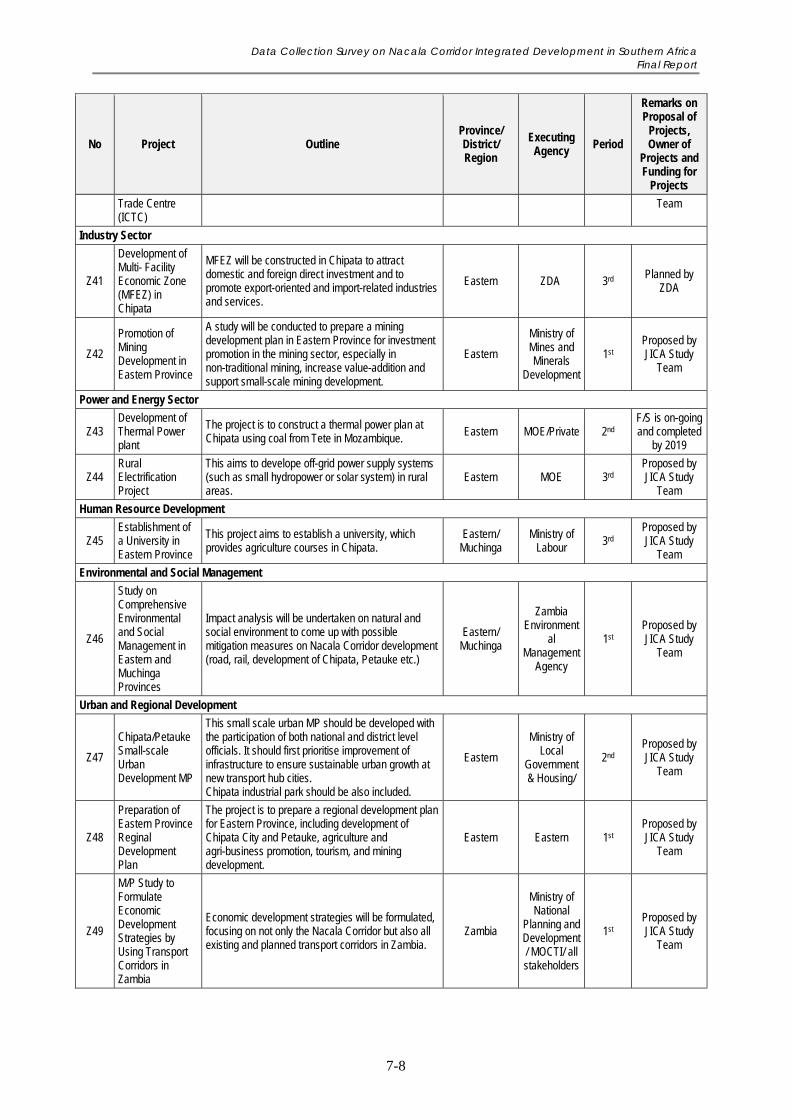

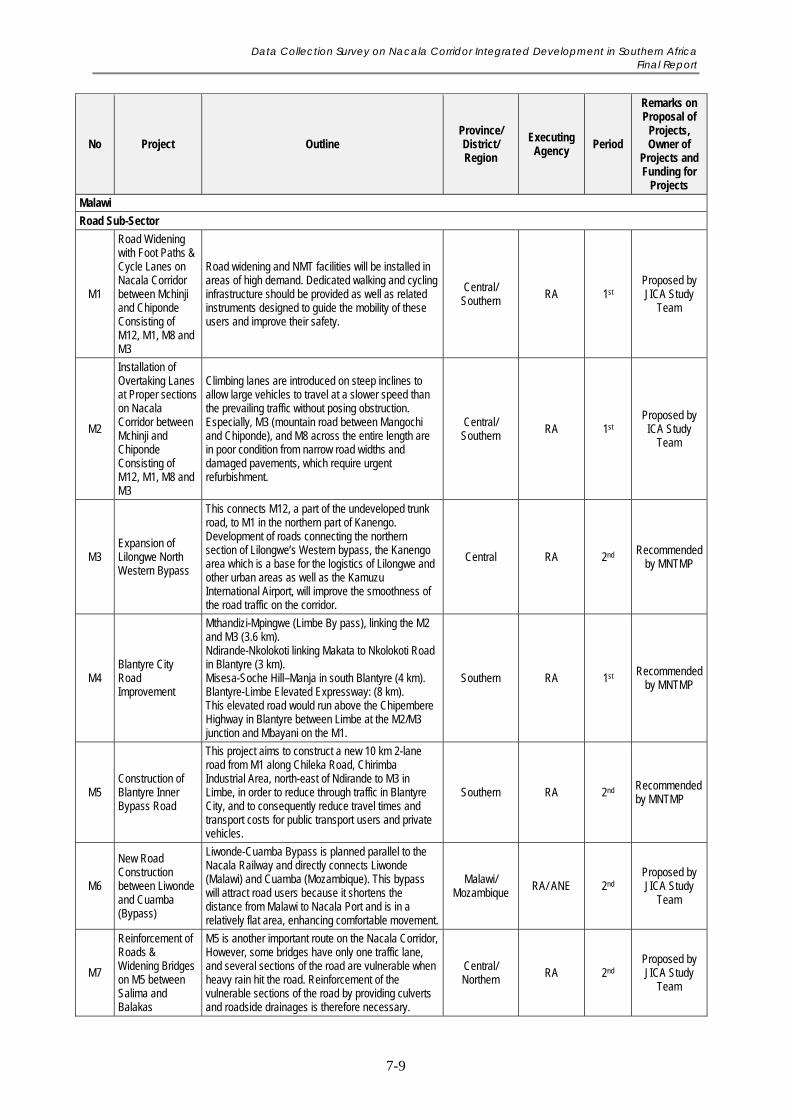

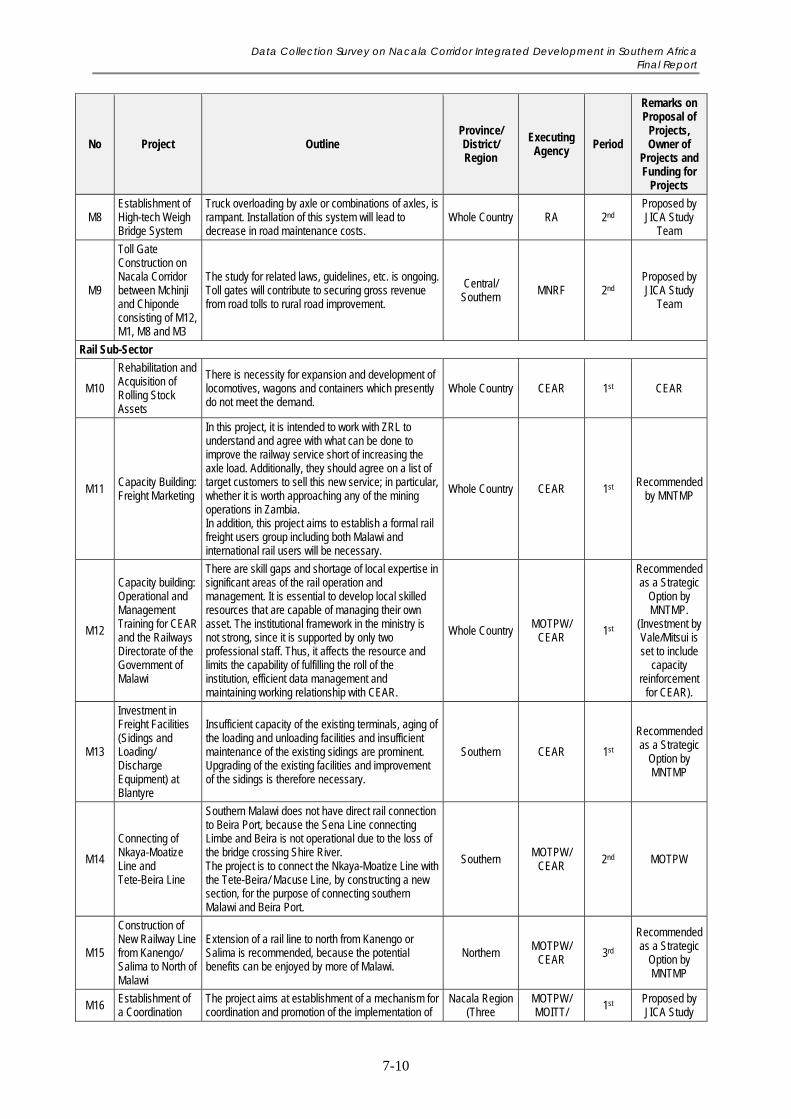

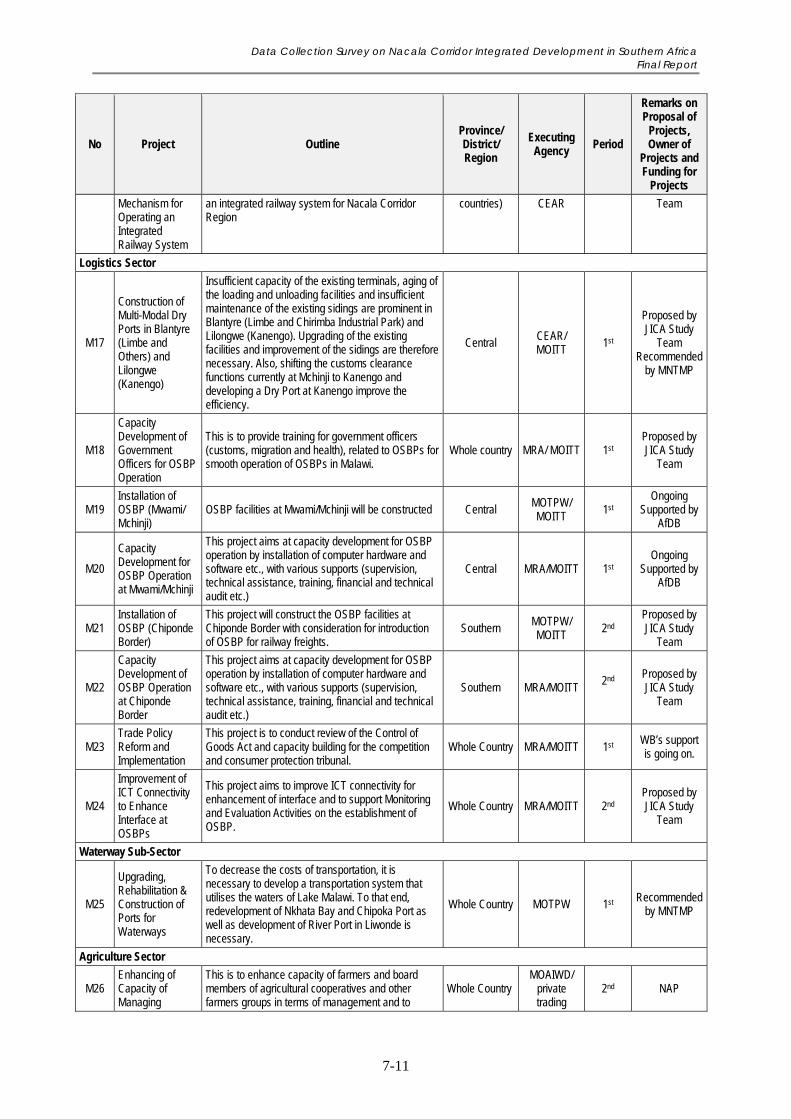

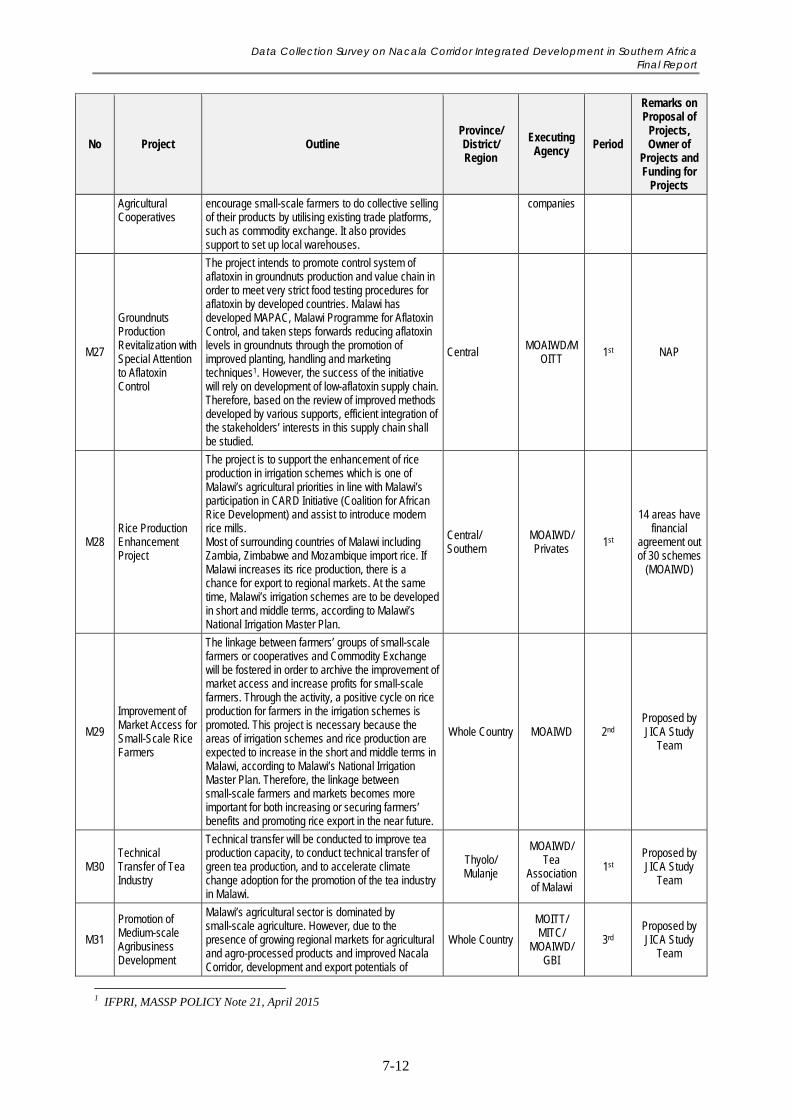

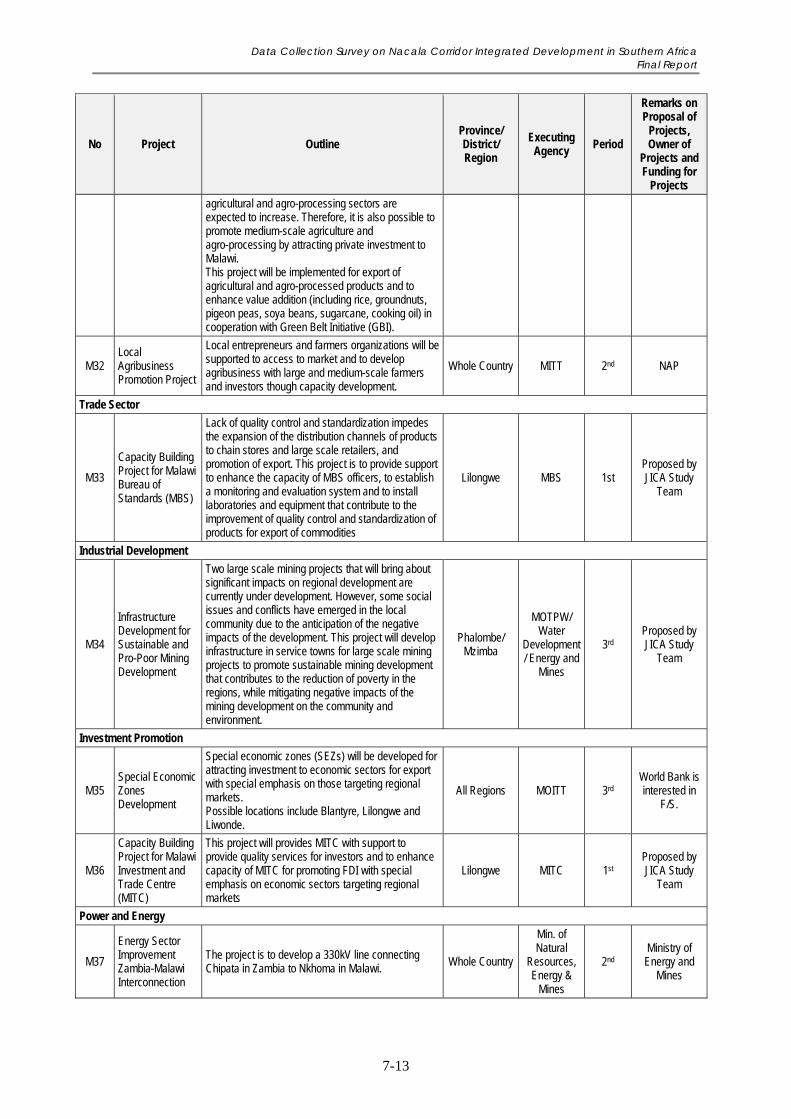

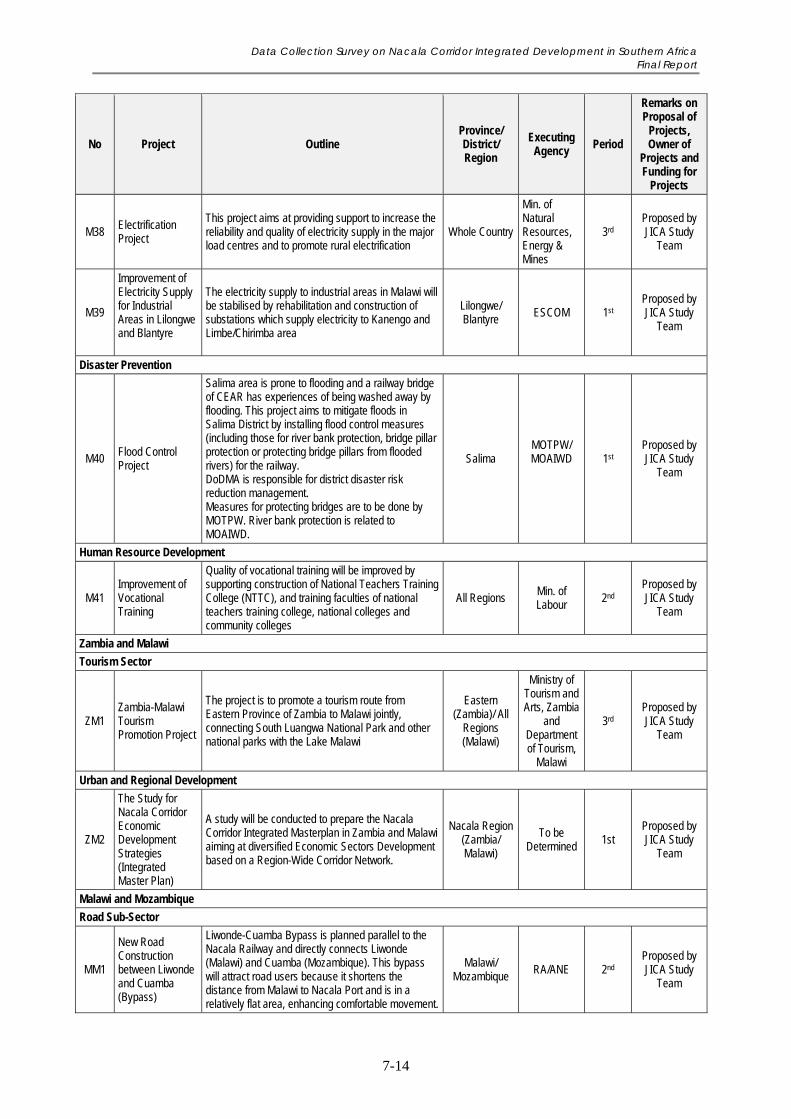

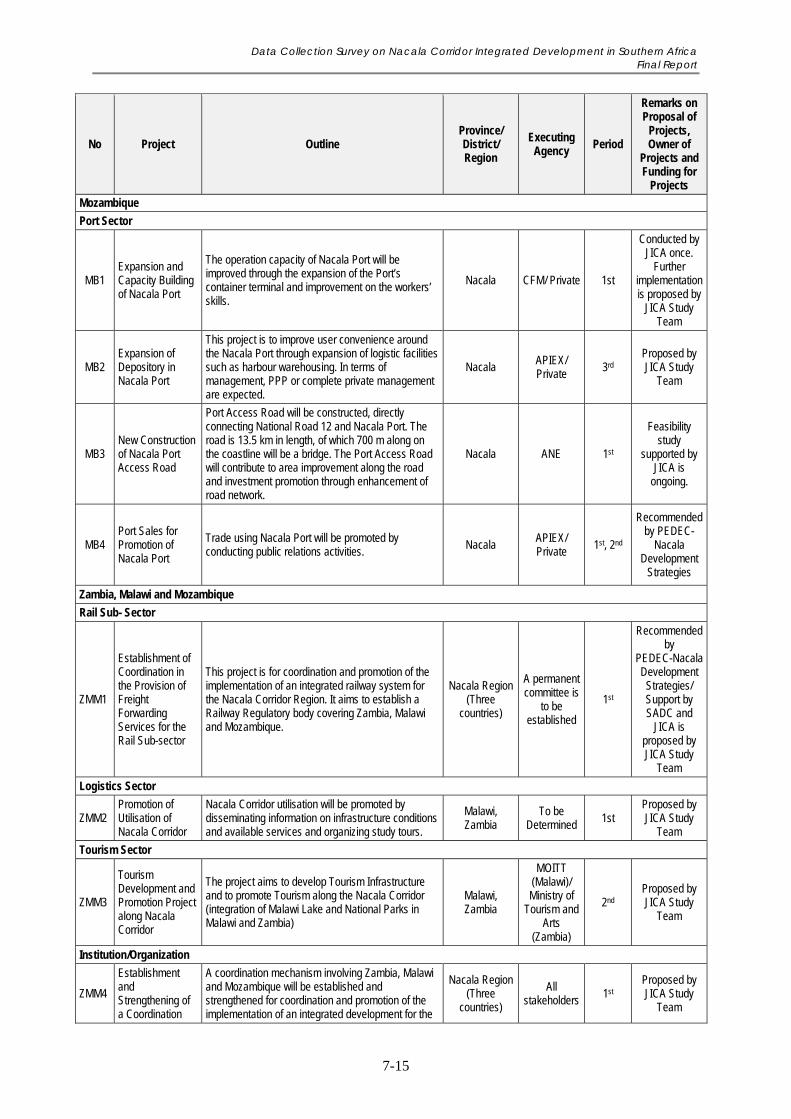

Table 7.1 Long List of Projects for Promoting Nacala Corridor Development ...................................... 7-3

Table 7.2 Basic Policy on the Selection of the Priority Projects .......................................................... 7-16

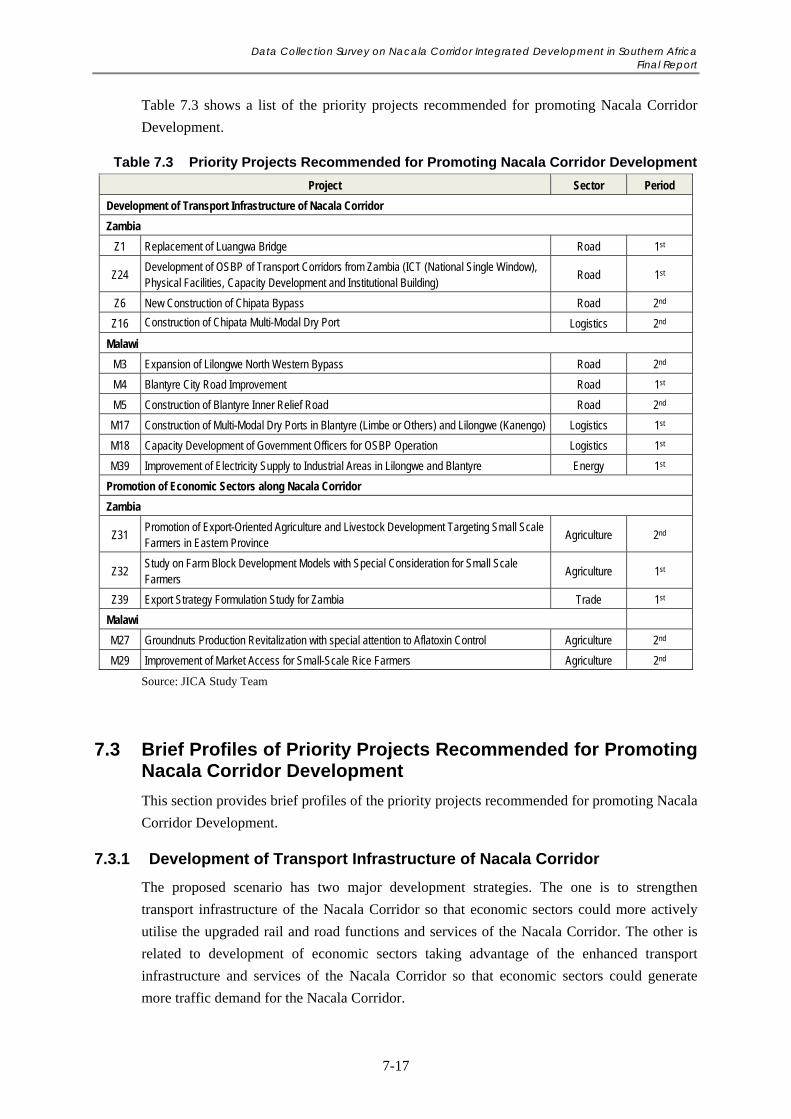

Table 7.3 Priority Projects Recommended for Promoting Nacala Corridor Development ................... 7-17

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xi

LIST OF FIGURES Page

Figure 1.1 Study Area: Nacala Corridor Region ...................................................................................... 1-2

Figure 1.2 Workflow ................................................................................................................................ 1-4

Figure 2.1 Corridors Supplying Zambia and Malawi ............................................................................... 2-4

Figure 2.2 National Transport Corridor Coordination Secretariat ........................................................... 2-8

Figure 2.3 Current Conditions of Development of Nacala Corridor ........................................................ 2-8

Figure 2.4 Traffic Volume on Main Roads in Zambia and Malawi (2015) ........................................... 2-17

Figure 2.5 Major Border Posts Related to Zambia and Malawi ............................................................. 2-17

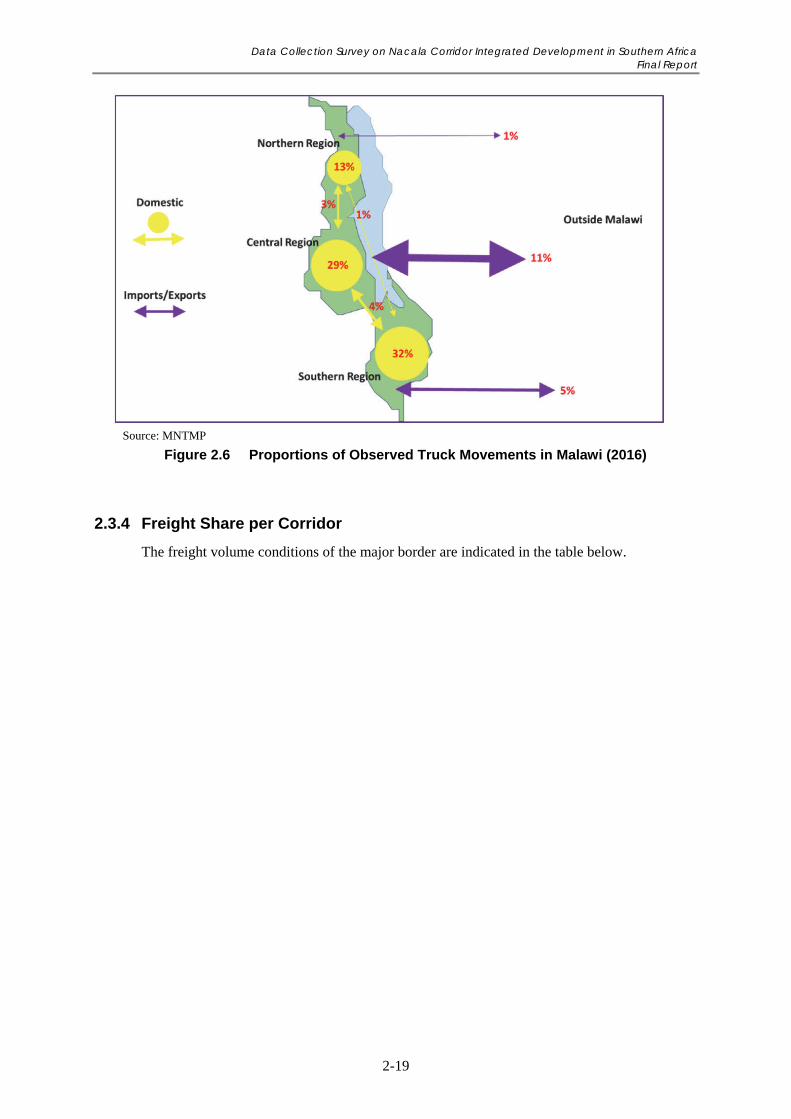

Figure 2.6 Proportions of Observed Truck Movements in Malawi (2016) ............................................ 2-19

Figure 2.7 Imports and Exports by Seaport (ton) ................................................................................... 2-21

Figure 3.1 Nacala Corridor Region in Zambia ......................................................................................... 3-1

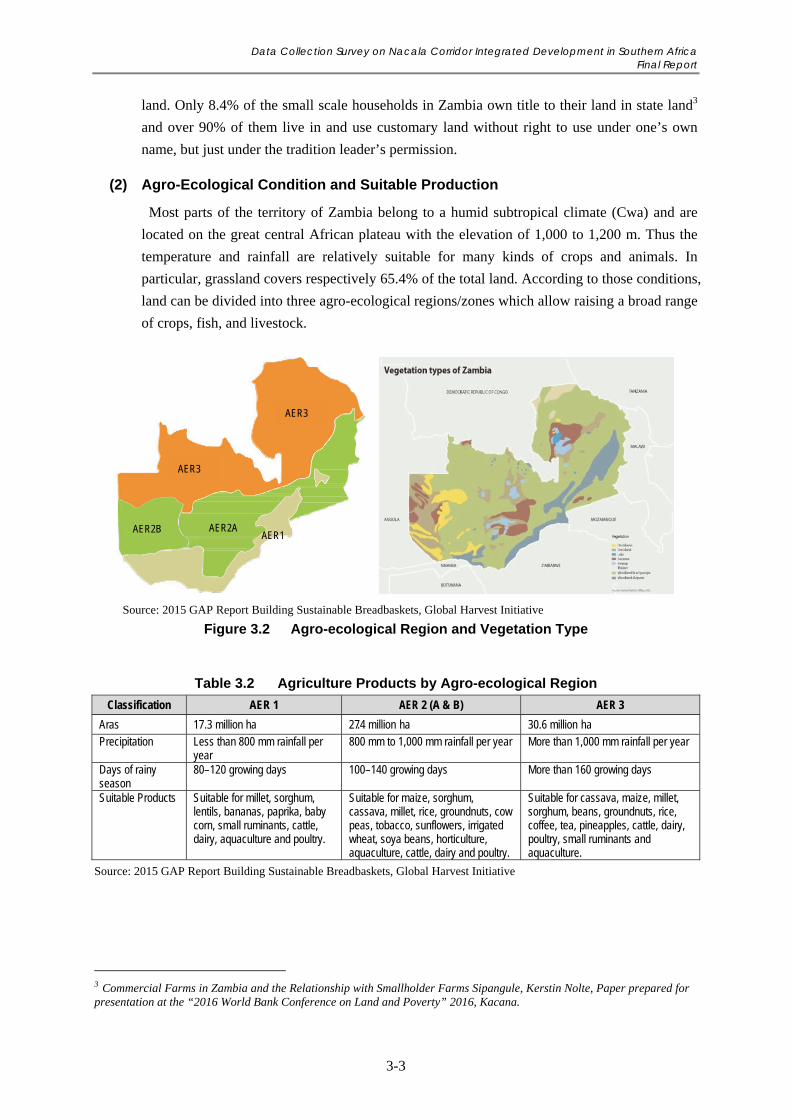

Figure 3.2 Agro-ecological Region and Vegetation Type ....................................................................... 3-3

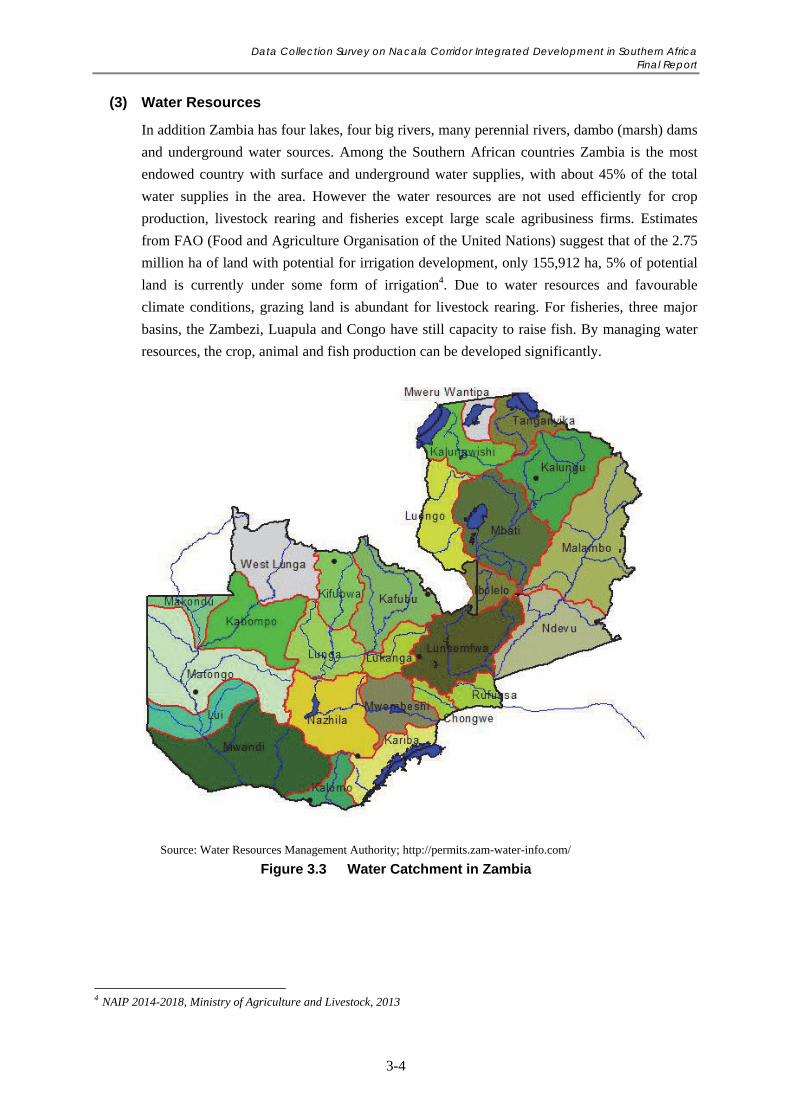

Figure 3.3 Water Catchment in Zambia ................................................................................................... 3-4

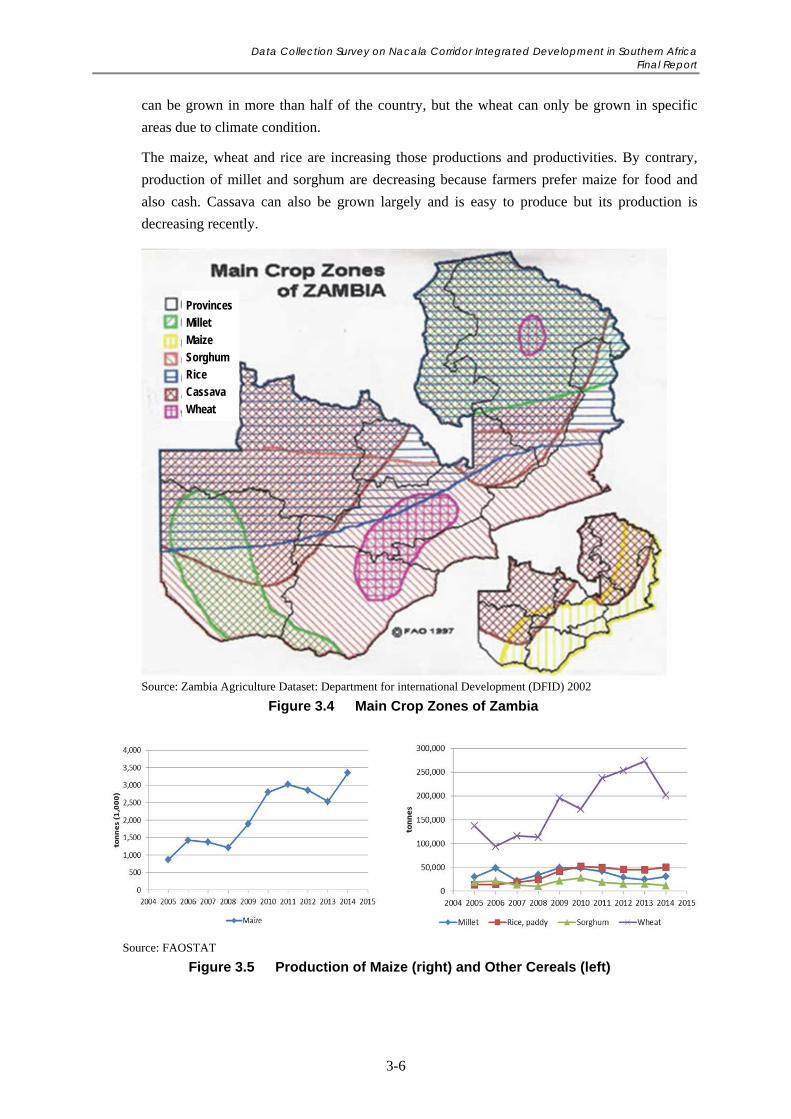

Figure 3.4 Main Crop Zones of Zambia ................................................................................................... 3-6

Figure 3.5 Production of Maize (right) and Other Cereals (left) .............................................................. 3-6

Figure 3.6 Production of Oil Crops .......................................................................................................... 3-7

Figure 3.7 Production of Tobacco, Cotton and Coffee ............................................................................ 3-7

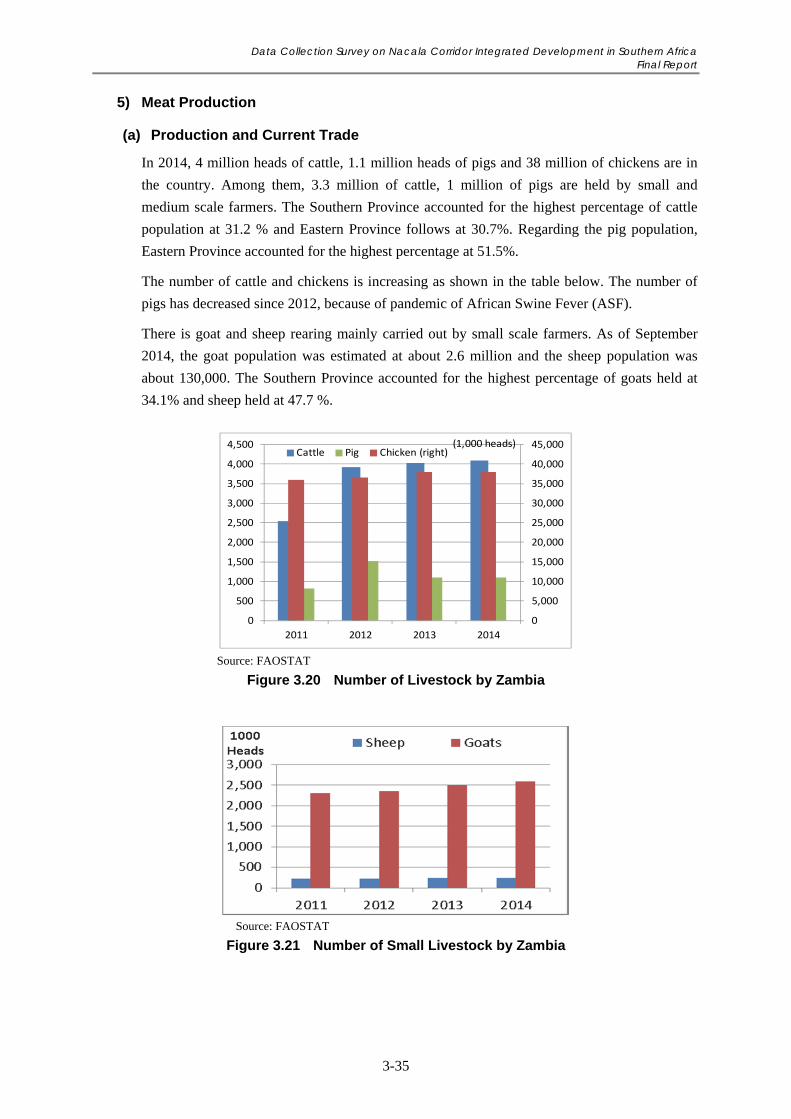

Figure 3.8 Number of Livestock – Cattle, Goats, Pigs, Sheep (right) and Chicken (left) ........................ 3-8

Figure 3.9 Concentration of Food Manufacturing Firms in Zambia, and the Spatial Analysis

of New Entrants .................................................................................................................... 3-10

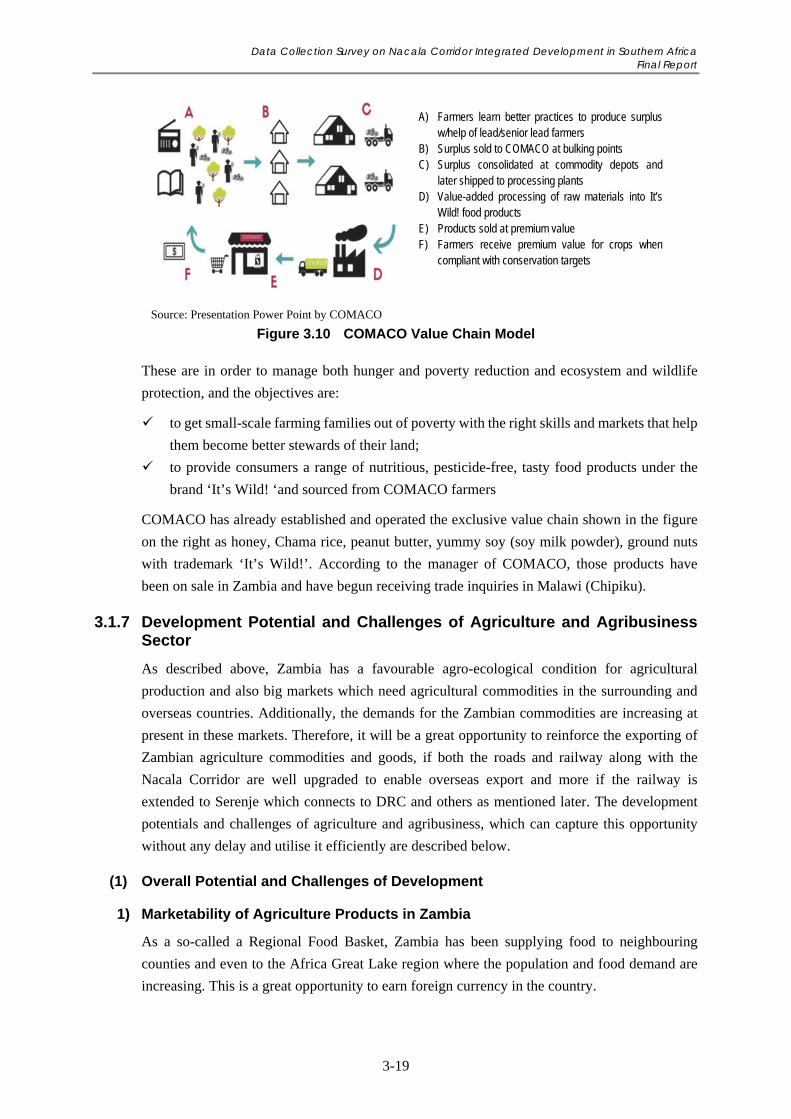

Figure 3.10 COMACO Value Chain Model ............................................................................................ 3-19

Figure 3.11 Net Agricultural Export Value in Zambia ............................................................................ 3-20

Figure 3.12 Production of Maize by Zambia and its Export by Country ................................................. 3-24

Figure 3.13 Import of Maize by Country in the Integrated Region .......................................................... 3-25

Figure 3.14 Production and Trade of Soya Bean by Zambia ................................................................... 3-27

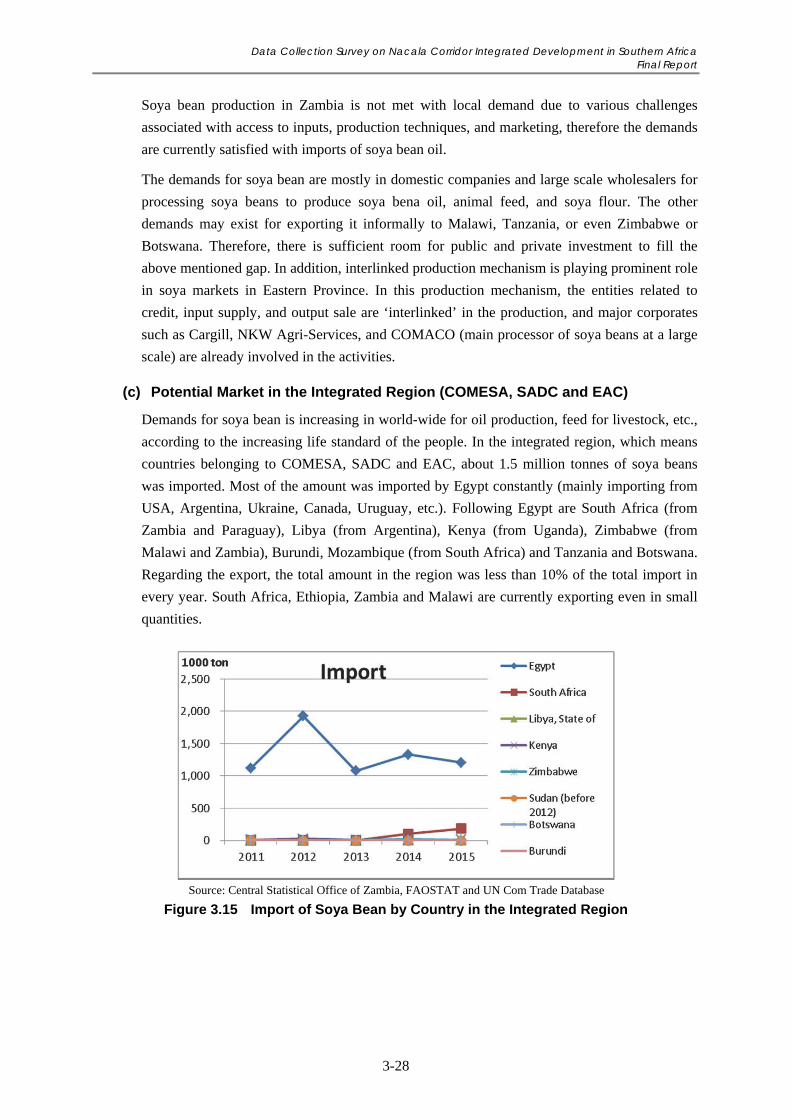

Figure 3.15 Import of Soya Bean by Country in the Integrated Region .................................................. 3-28

Figure 3.16 Production and Trade of Wheat by Zambia .......................................................................... 3-30

Figure 3.17 Import of Wheat by Country in the Integrated Region ......................................................... 3-31

Figure 3.18 Production and Trade of Cotton Lint by Zambia .................................................................. 3-32

Figure 3.19 Import of Cotton Lint by County in the Integrated Region .................................................. 3-34

Figure 3.20 Number of Livestock by Zambia .......................................................................................... 3-35

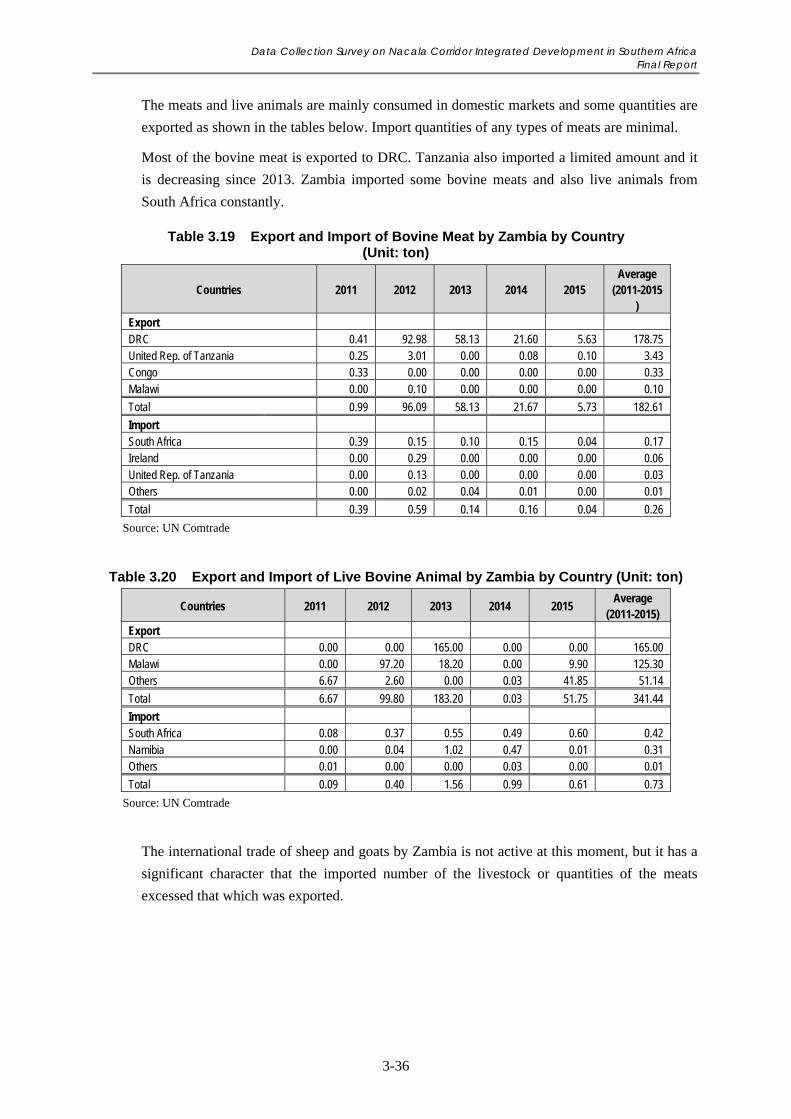

Figure 3.21 Number of Small Livestock by Zambia ................................................................................ 3-35

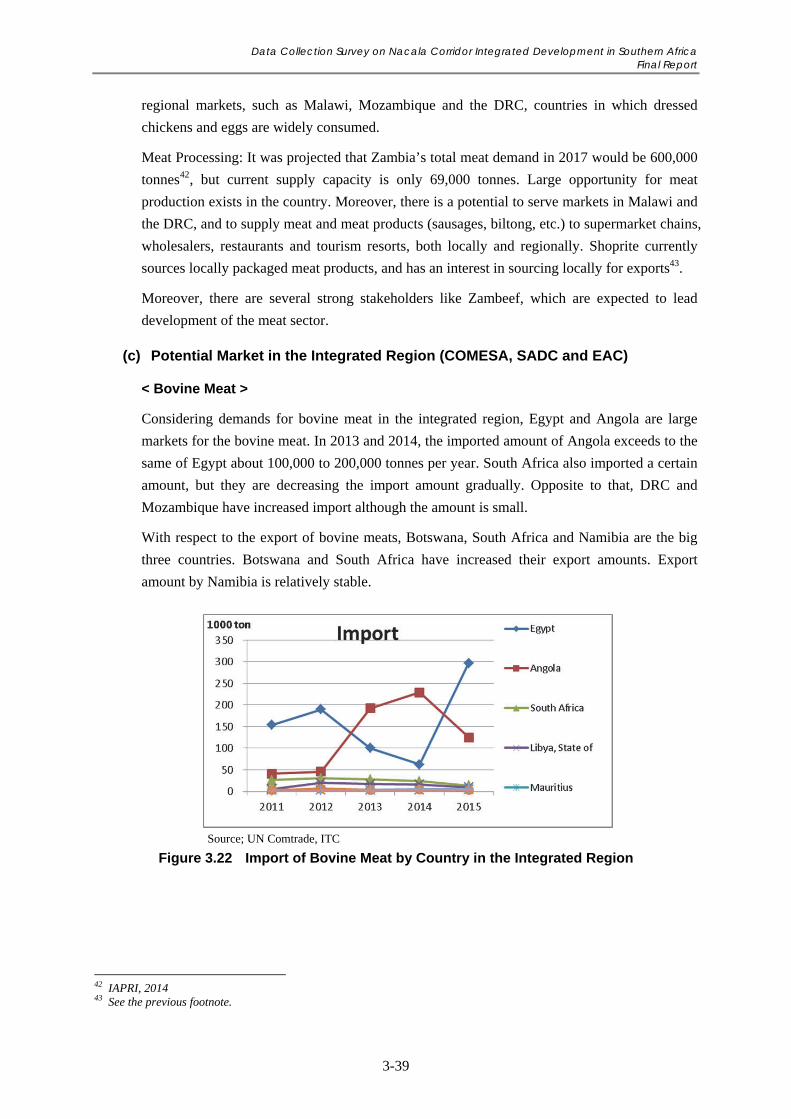

Figure 3.22 Import of Bovine Meat by Country in the Integrated Region ............................................... 3-39

Figure 3.23 Import of Meat of Sheep and Goat by Country in the Integrated Region ............................. 3-41

Figure 3.24 Fish Production 2011-2014 by Zambia ................................................................................. 3-43

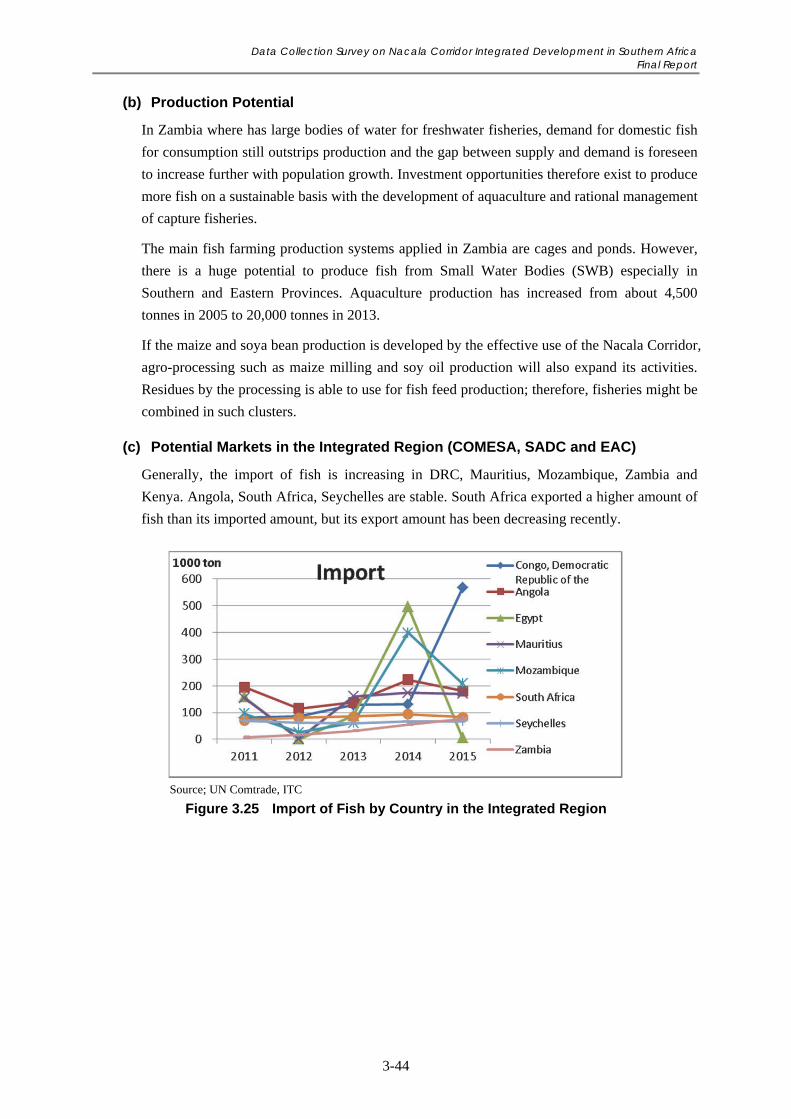

Figure 3.25 Import of Fish by Country in the Integrated Region ............................................................. 3-44

Figure 3.26 Production and Trade of Edible Oil by Zambia .................................................................... 3-46

Figure 3.27 Import of Soya Bean Oil by Country in the Integrated Region ............................................ 3-47

Figure 3.28 Import of Sunflower Oil by Country in the Integrated Region ............................................. 3-48

Figure 3.29 Production of Sugar Cane and Trade of Sugar by Zambia ................................................... 3-49

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xii

Figure 3.30 Production and Trade of Refined Sugar ................................................................................ 3-50

Figure 3.31 Trade of Sugar Confectionery by Zambia ............................................................................ 3-51

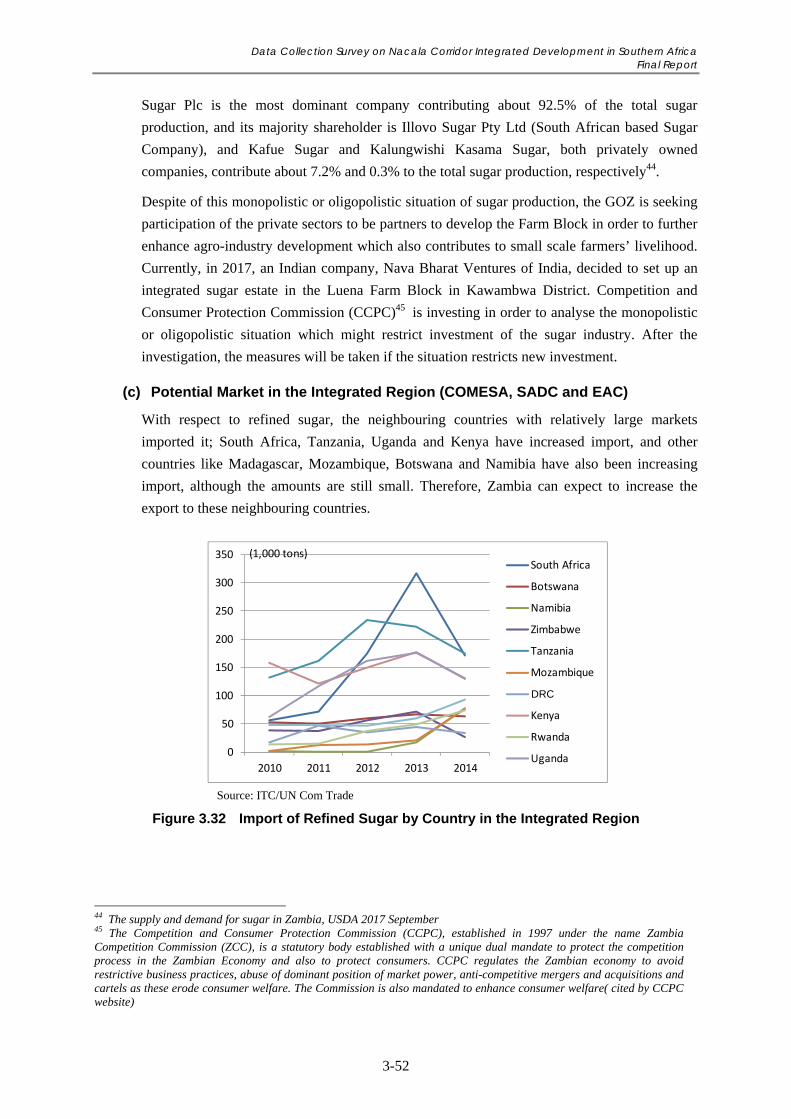

Figure 3.32 Import of Refined Sugar by Country in the Integrated Region ............................................. 3-52

Figure 3.33 Import of Sugar Confectionery by Country in the Integrated Region .................................. 3-54

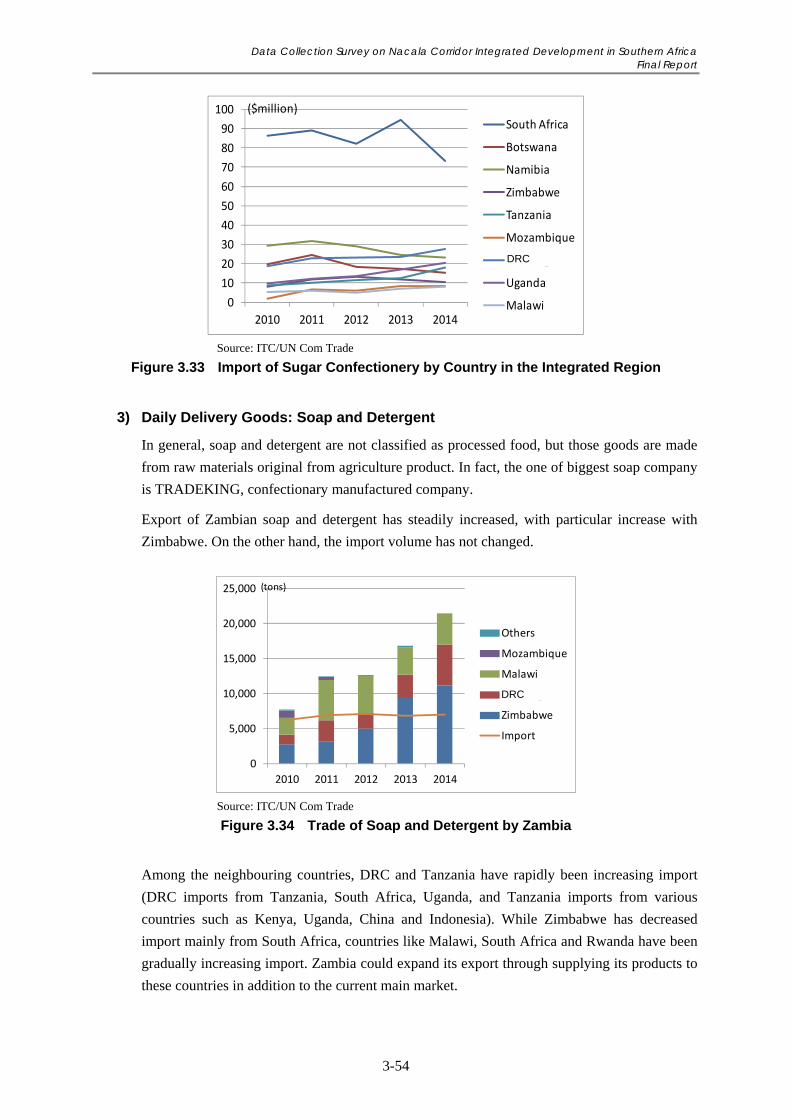

Figure 3.34 Trade of Soap and Detergent by Zambia .............................................................................. 3-54

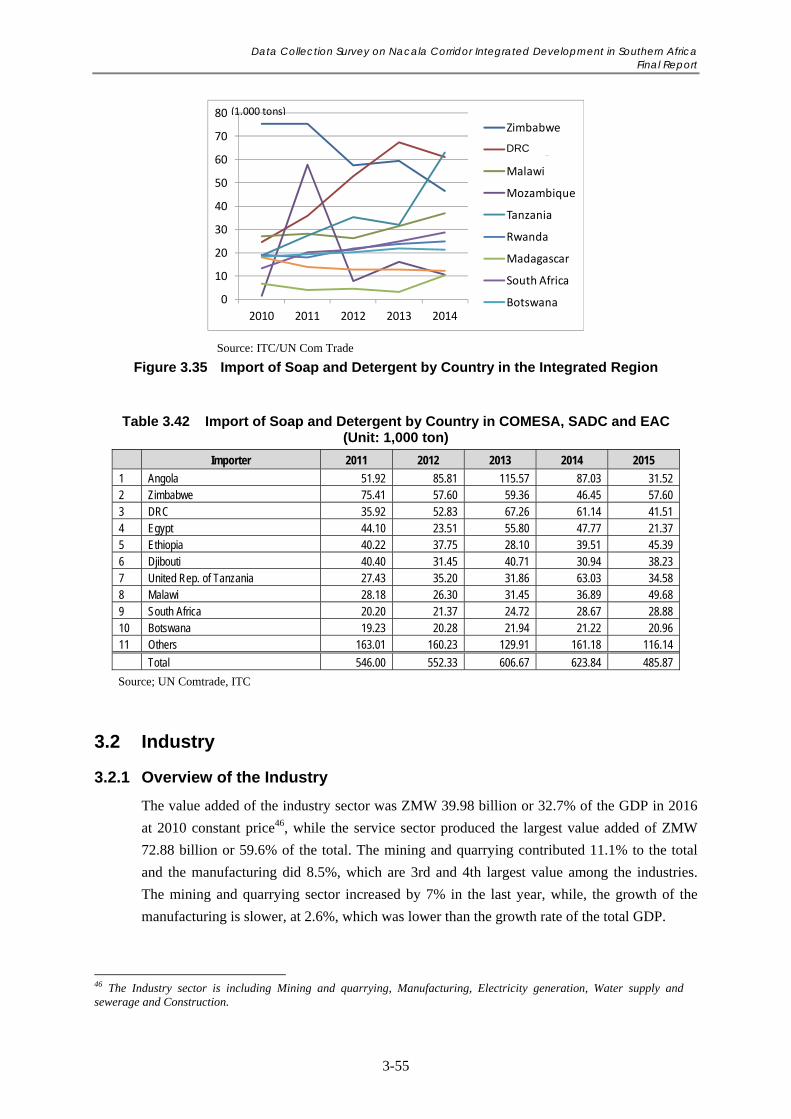

Figure 3.35 Import of Soap and Detergent by Country in the Integrated Region .................................... 3-55

Figure 3.36 Copper Production and Copper Price ................................................................................... 3-59

Figure 3.37 Export and Import Values from 2006 to 2015 ...................................................................... 3-64

Figure 3.38 Top 10 Export Partners in 2015 ............................................................................................ 3-65

Figure 3.39 Top 10 Import Partners in 2015 ............................................................................................ 3-65

Figure 3.40 Traditional and Non-Traditional Export from 2007 to 2017 ................................................ 3-66

Figure 3.41 Export by Product Category from 2006 to 2015 ................................................................... 3-67

Figure 3.42 Import by Product Category from 2006 to 2015 ................................................................... 3-67

Figure 3.43 Export and Import Values at Mwami Border Post ................................................................ 3-69

Figure 3.44 Tourist Arrivals by Continent ............................................................................................... 3-73

Figure 3.45 Tourist Arrivals by Purpose of Visit ..................................................................................... 3-74

Figure 3.46 Tourist Arrivals by Top Ten Overseas Markets in 2015 ...................................................... 3-74

Figure 3.47 Tourist Arrivals by Top Ten Africa Markets in 2015 ........................................................... 3-75

Figure 3.48 Tourists Visited Major National Parks ................................................................................. 3-75

Figure 3.49 Installed Capacity by Type of Generation ............................................................................ 3-81

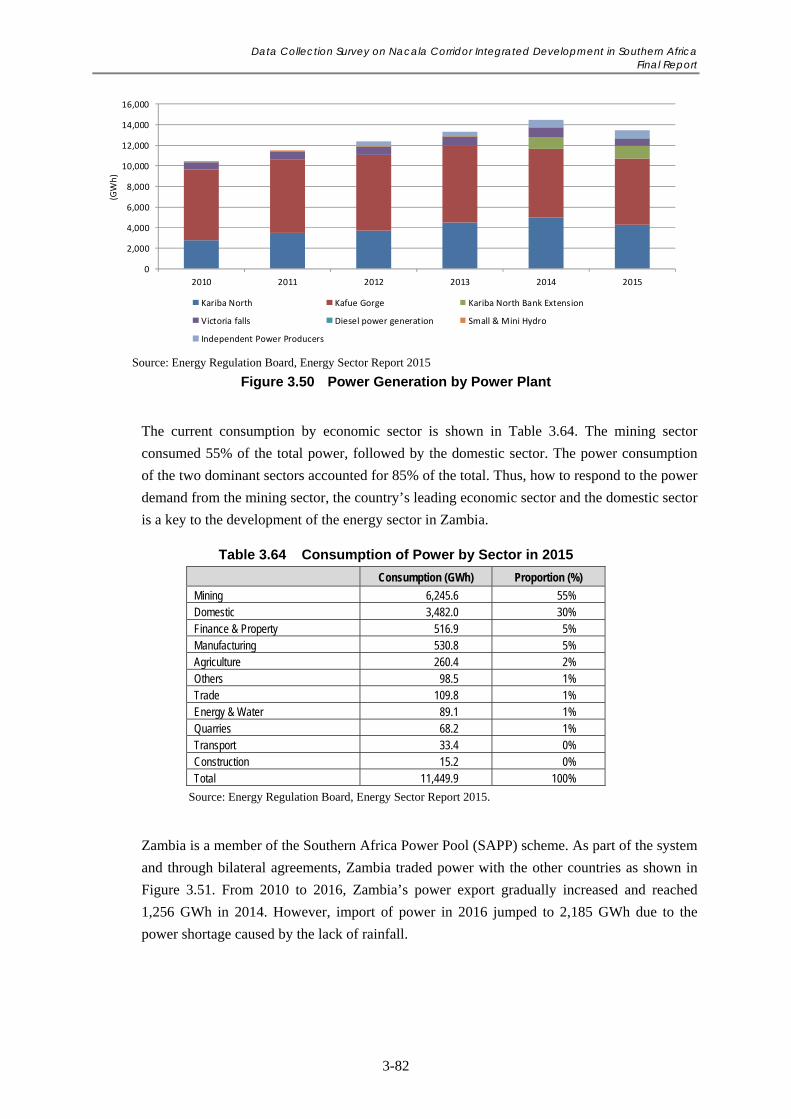

Figure 3.50 Power Generation by Power Plant ........................................................................................ 3-82

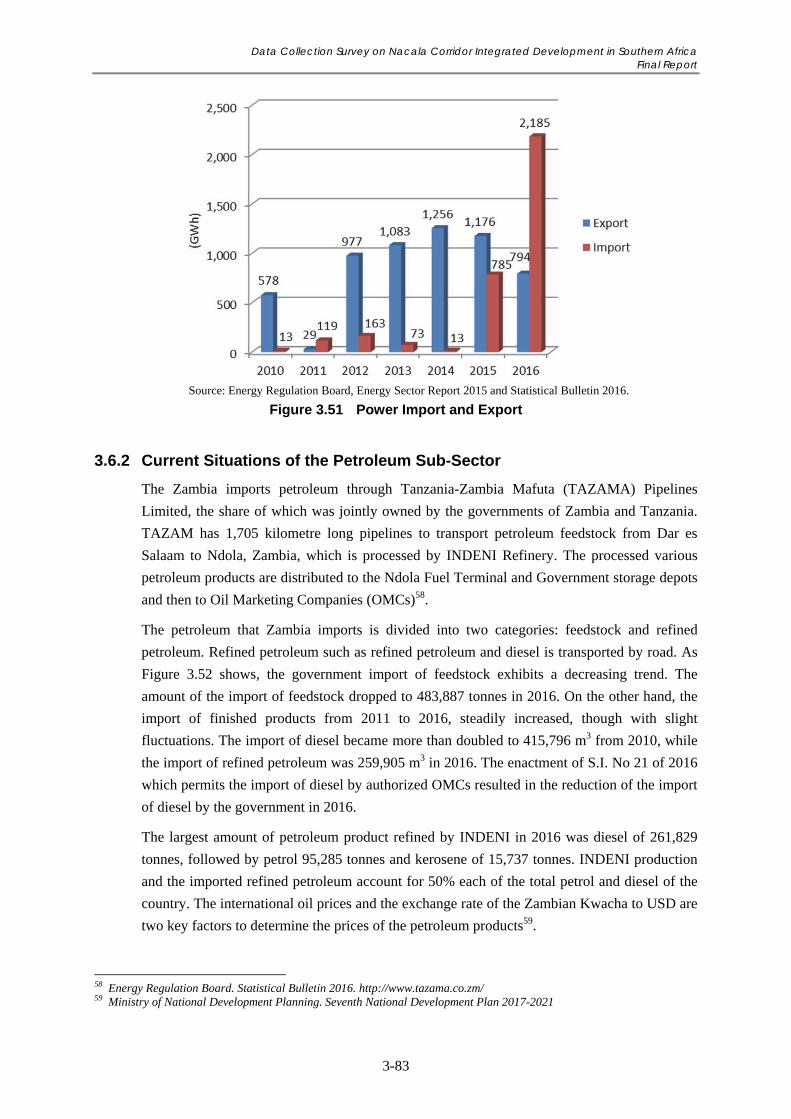

Figure 3.51 Power Import and Export ...................................................................................................... 3-83

Figure 3.52 Government Import of Petroleum Feedstock and Finished Products from 2011 to 2016 ..... 3-84

Figure 3.53 Refinery Production of Petroleum Products in 2016 ............................................................ 3-84

Figure 3.54 Investment in Zambia (Pledged base, 2010-2016) ................................................................ 3-88

Figure 3.55 Investment in Zambia (Pledged base, 2010-2016) by Sector ............................................... 3-88

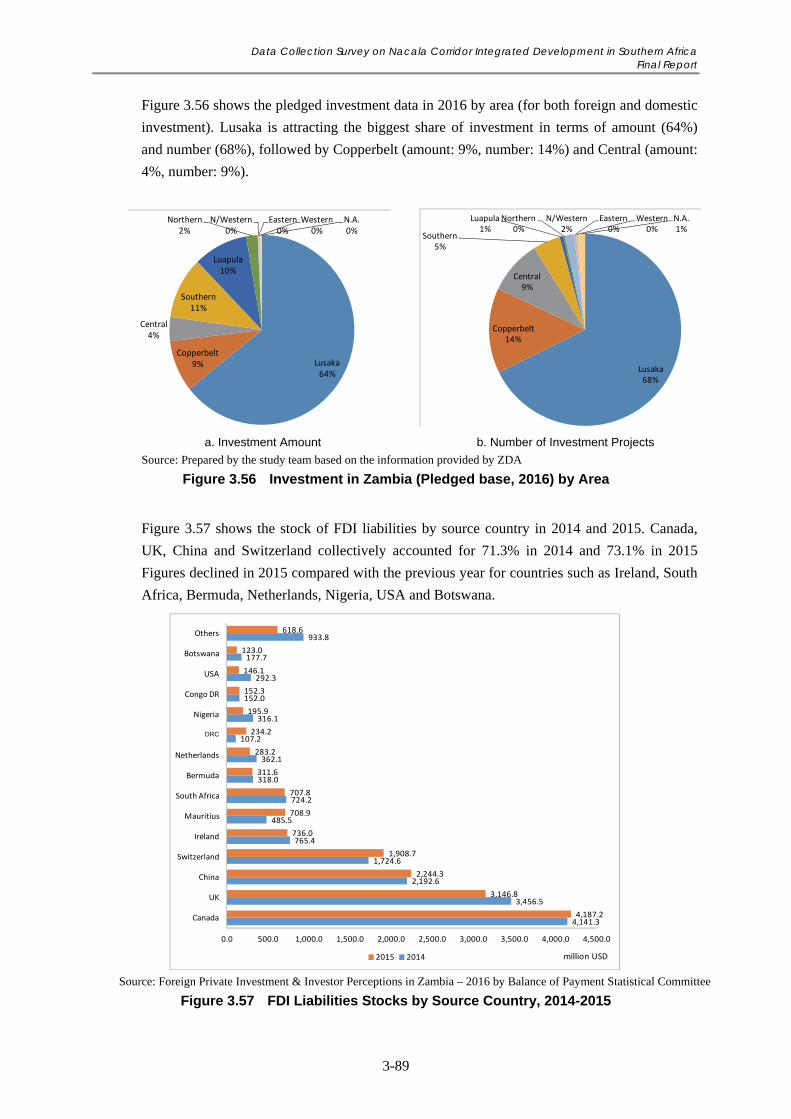

Figure 3.56 Investment in Zambia (Pledged base, 2016) by Area ........................................................... 3-89

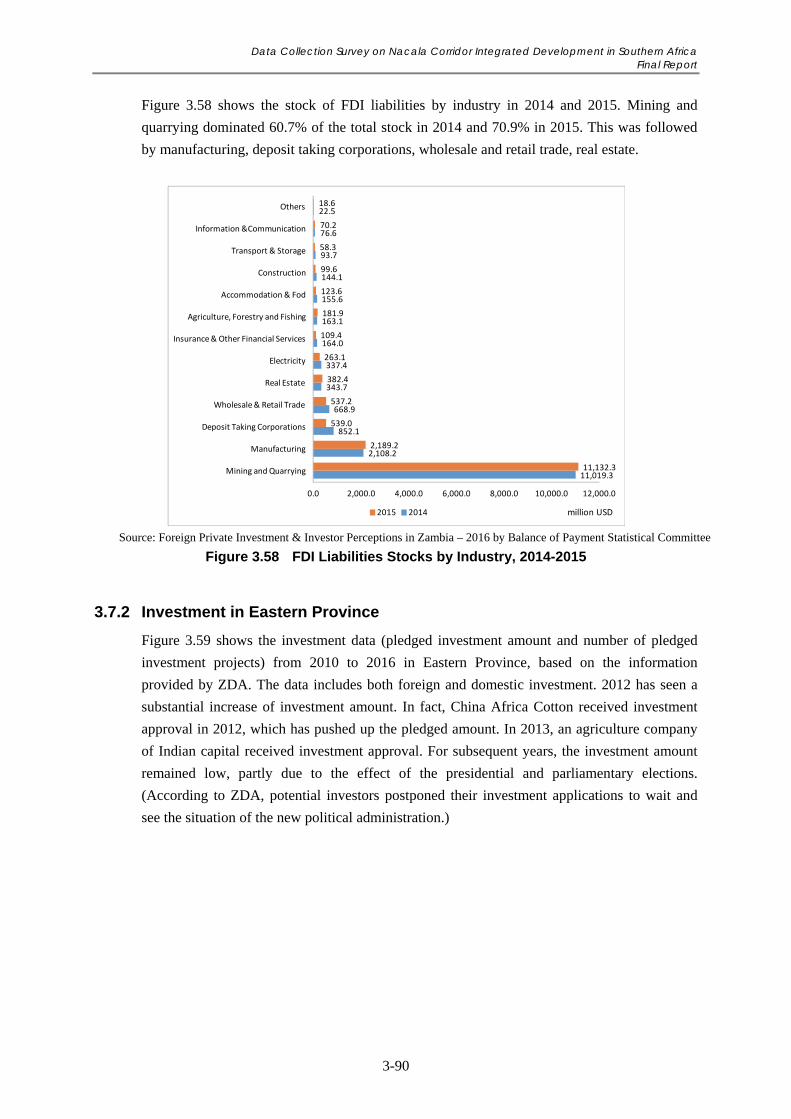

Figure 3.57 FDI Liabilities Stocks by Source Country, 2014-2015 ......................................................... 3-89

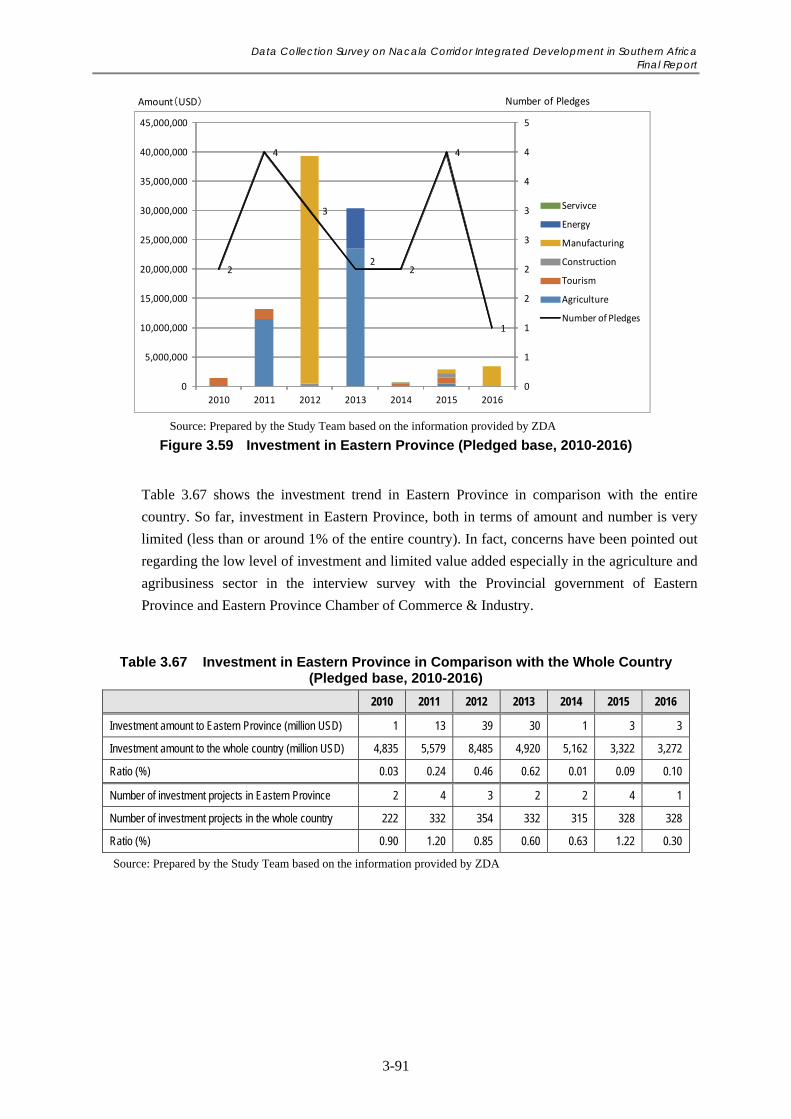

Figure 3.58 FDI Liabilities Stocks by Industry, 2014-2015 ..................................................................... 3-90

Figure 3.59 Investment in Eastern Province (Pledged base, 2010-2016) ................................................. 3-91

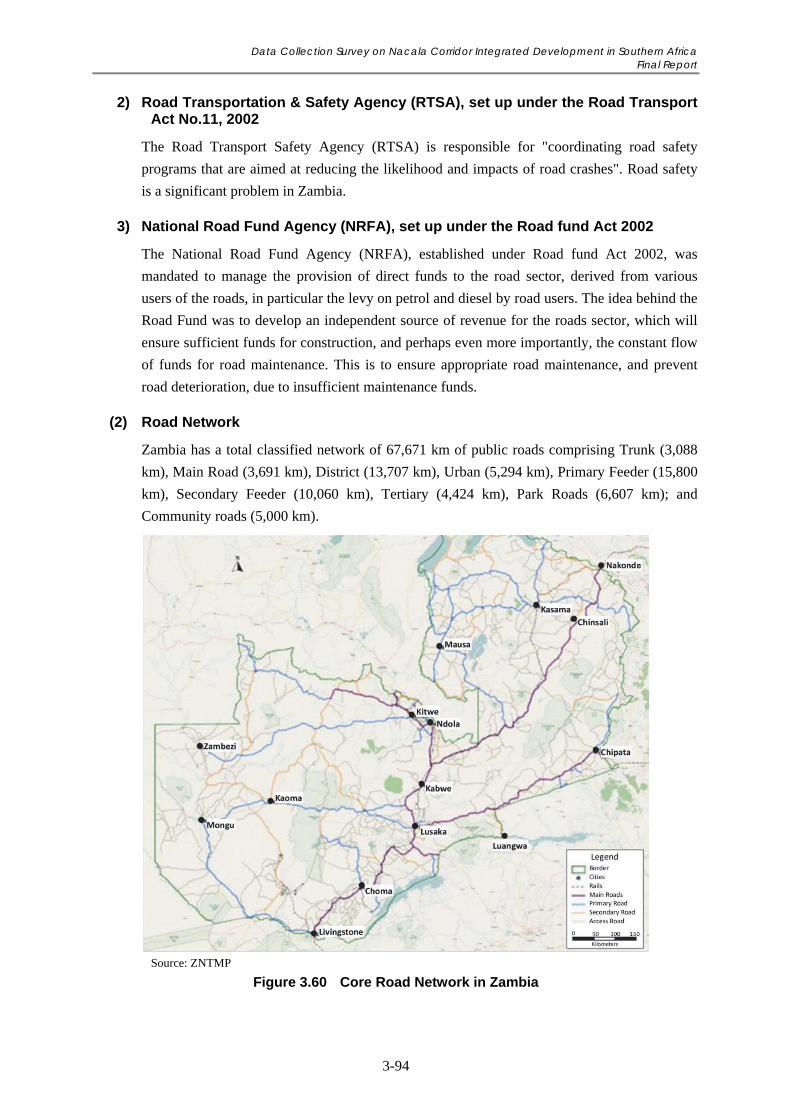

Figure 3.60 Core Road Network in Zambia ............................................................................................. 3-94

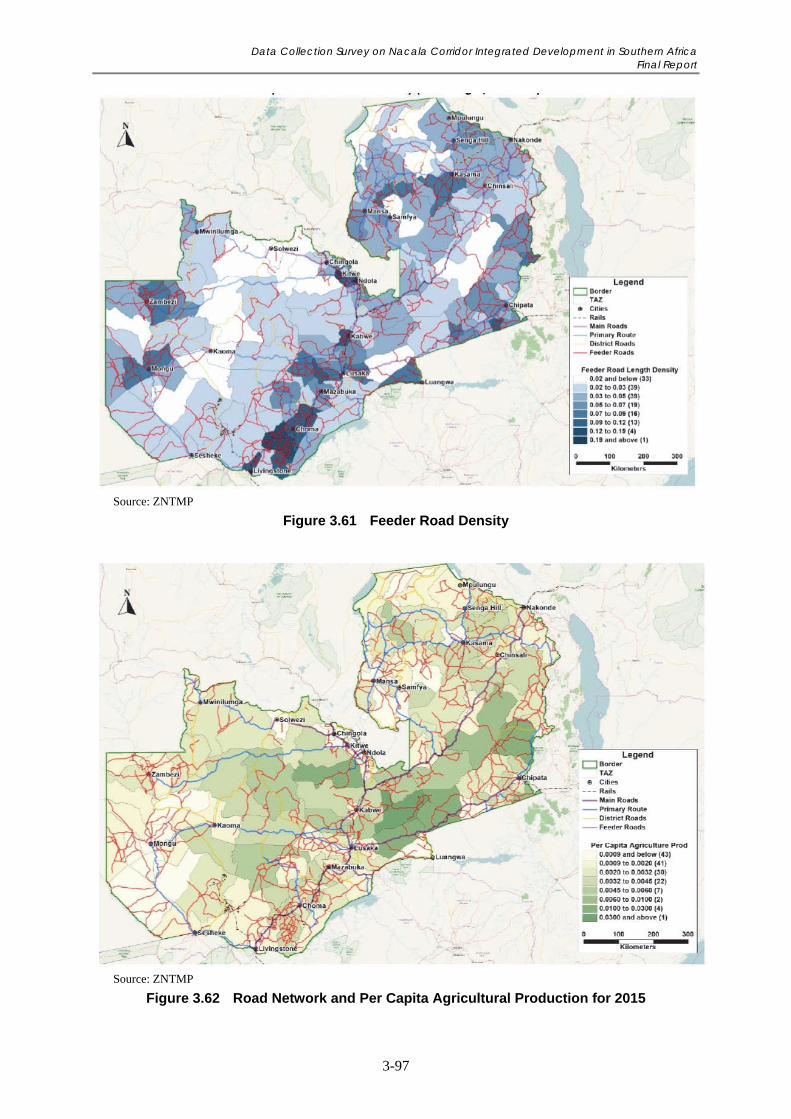

Figure 3.61 Feeder Road Density ............................................................................................................. 3-97

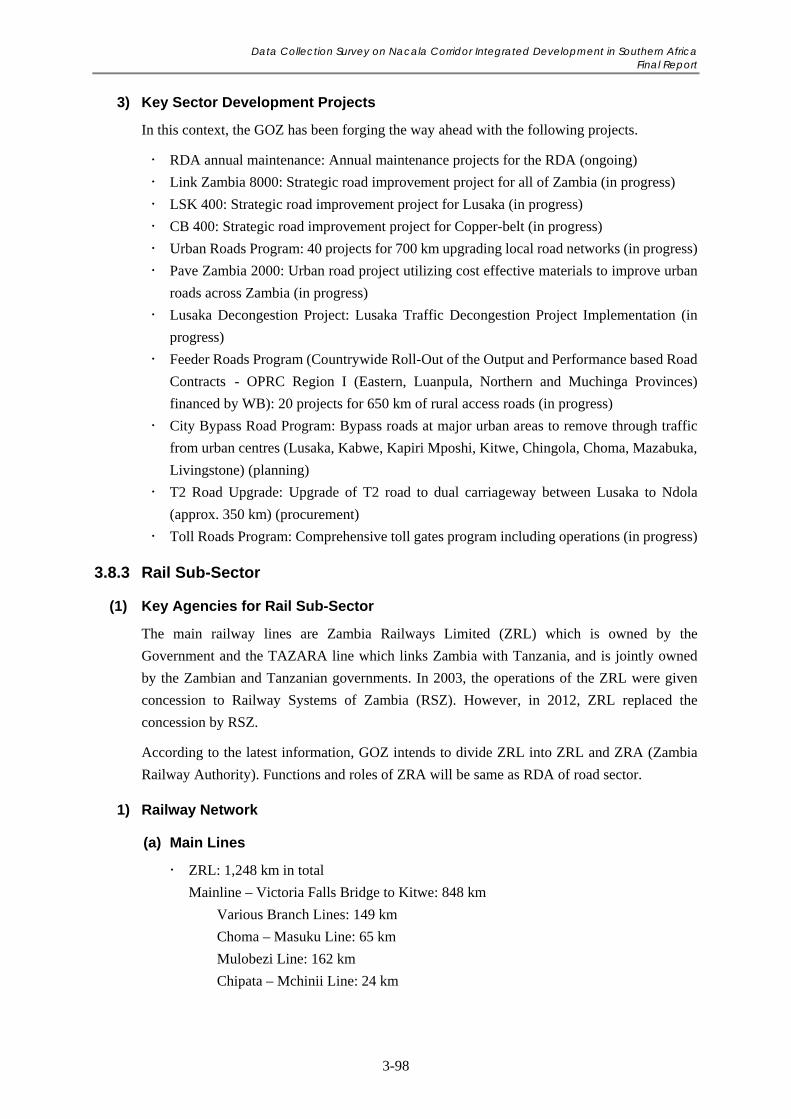

Figure 3.62 Road Network and Per Capita Agricultural Production for 2015 ......................................... 3-97

Figure 3.63 Railway Network in Zambia ................................................................................................. 3-99

Figure 4.1 The Nacala Corridor Region in Malawi .................................................................................. 4-1

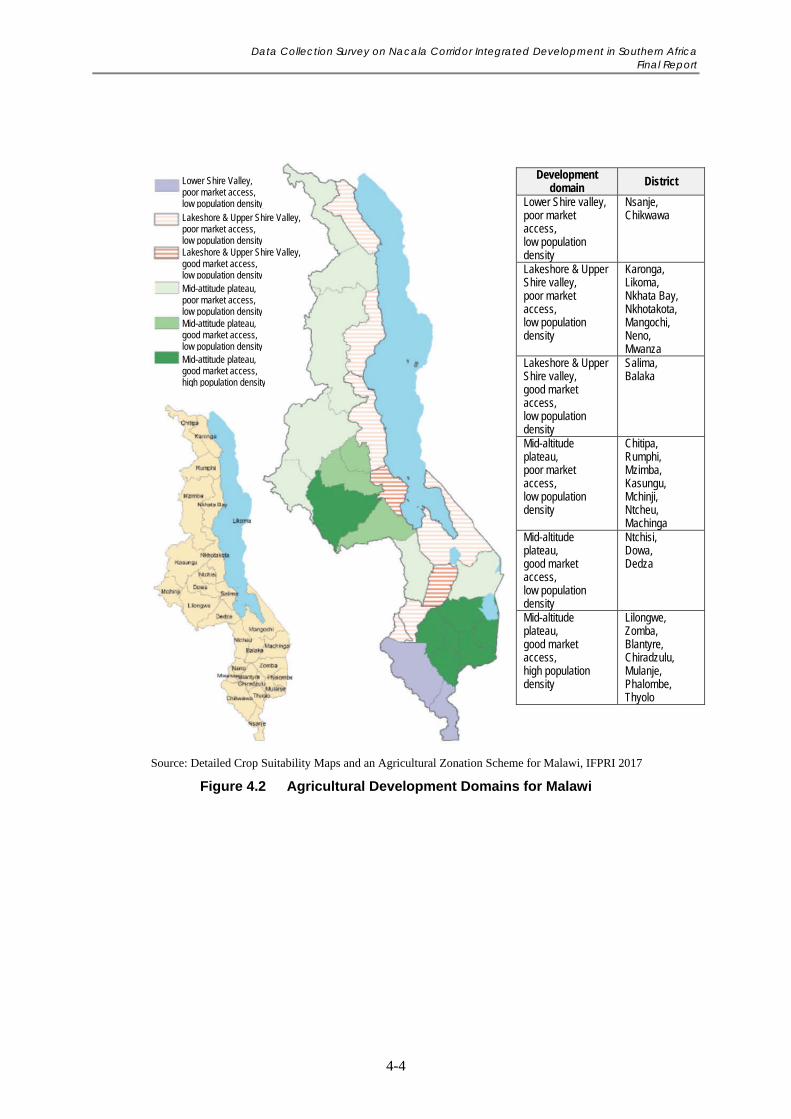

Figure 4.2 Agricultural Development Domains for Malawi .................................................................... 4-4

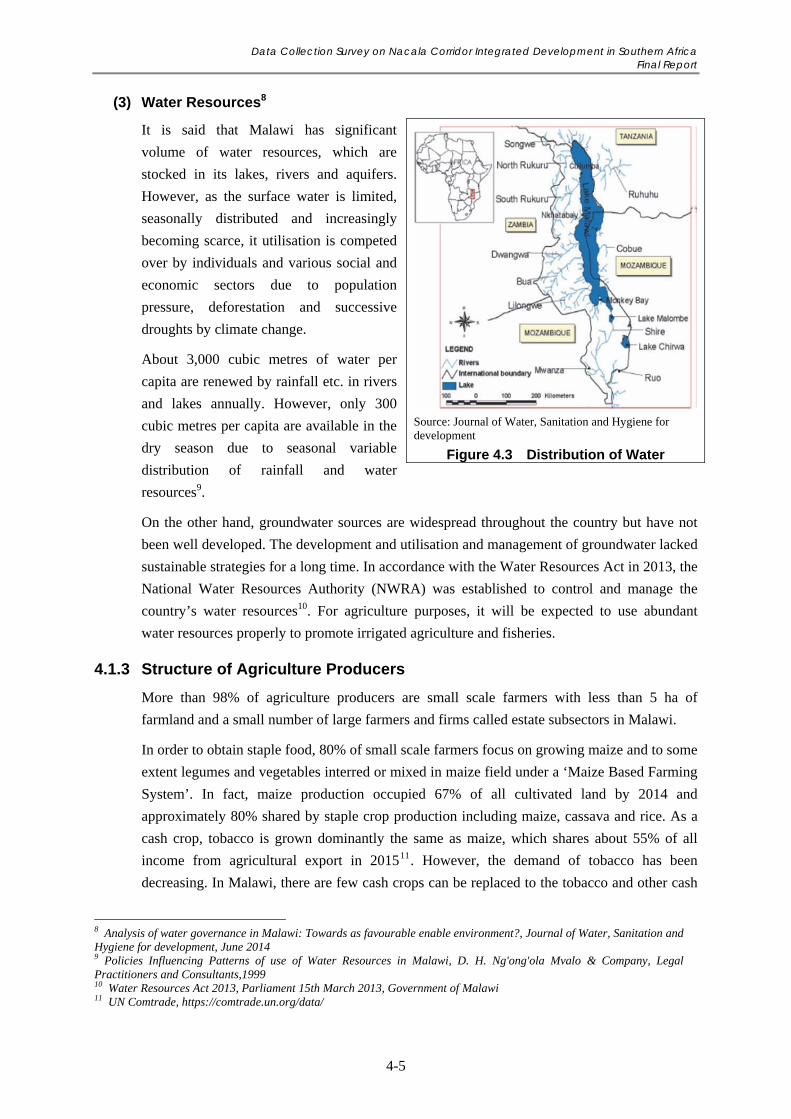

Figure 4.3 Distribution of Water .............................................................................................................. 4-5

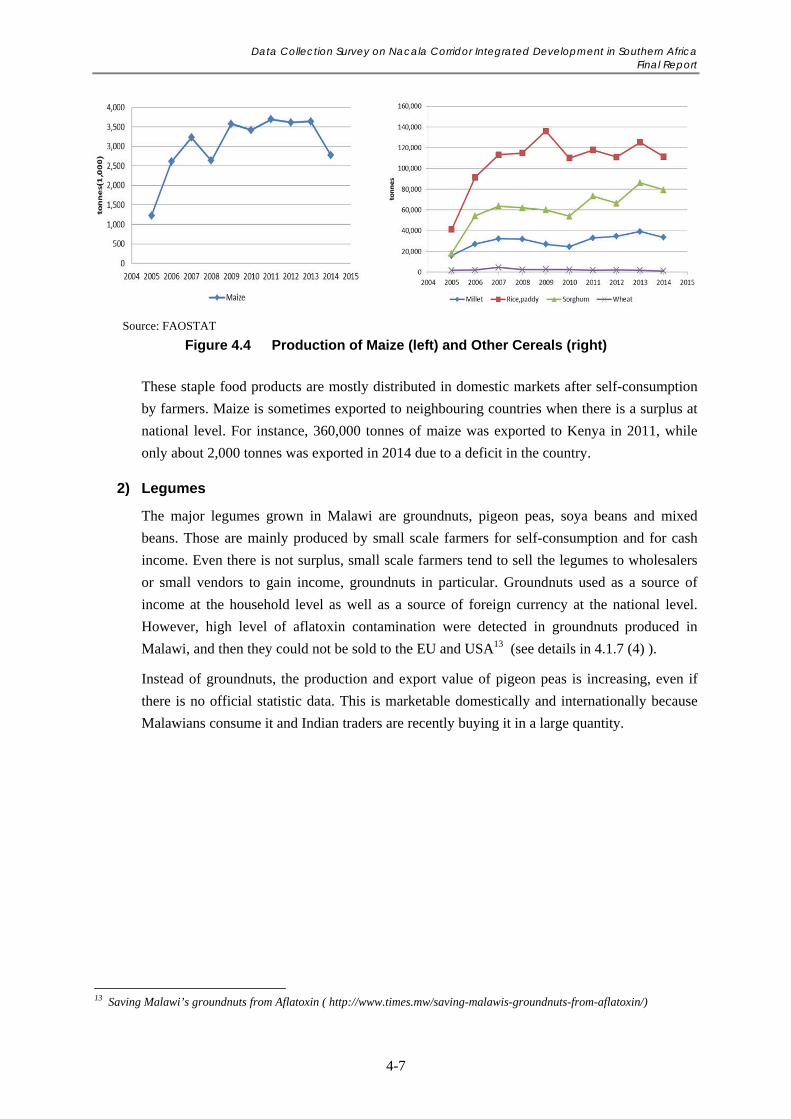

Figure 4.4 Production of Maize (left) and Other Cereals (right) .............................................................. 4-7

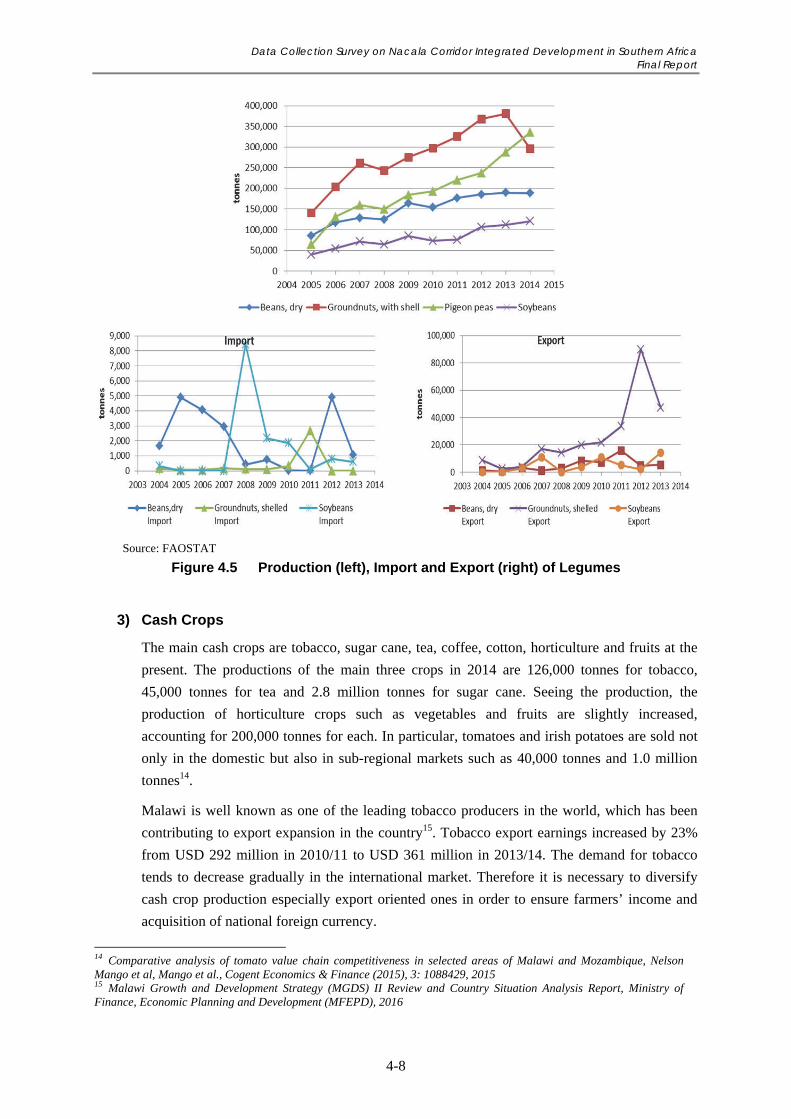

Figure 4.5 Production (left), Import and Export (right) of Legumes ....................................................... 4-8

Figure 4.6 Production of Cash Crops ....................................................................................................... 4-9

Figure 4.7 Volume of Export Crops ......................................................................................................... 4-9

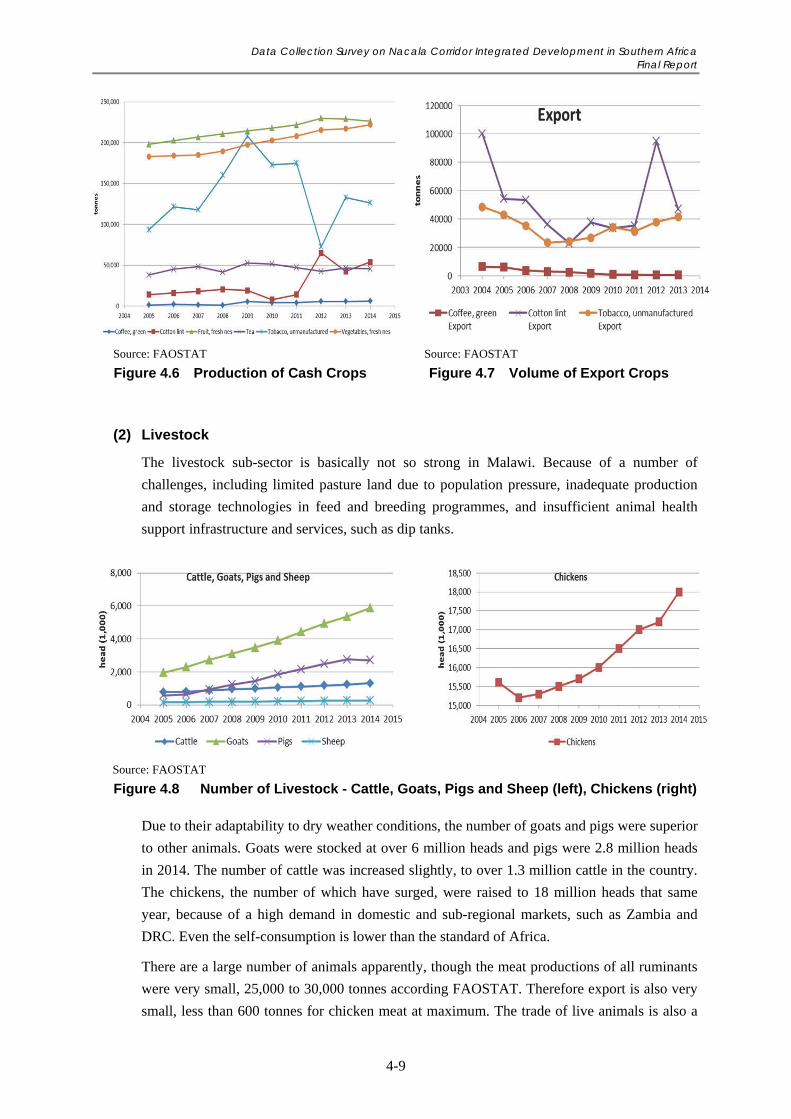

Figure 4.8 Number of Livestock - Cattle, Goats, Pigs and Sheep (left), Chickens (right) ....................... 4-9

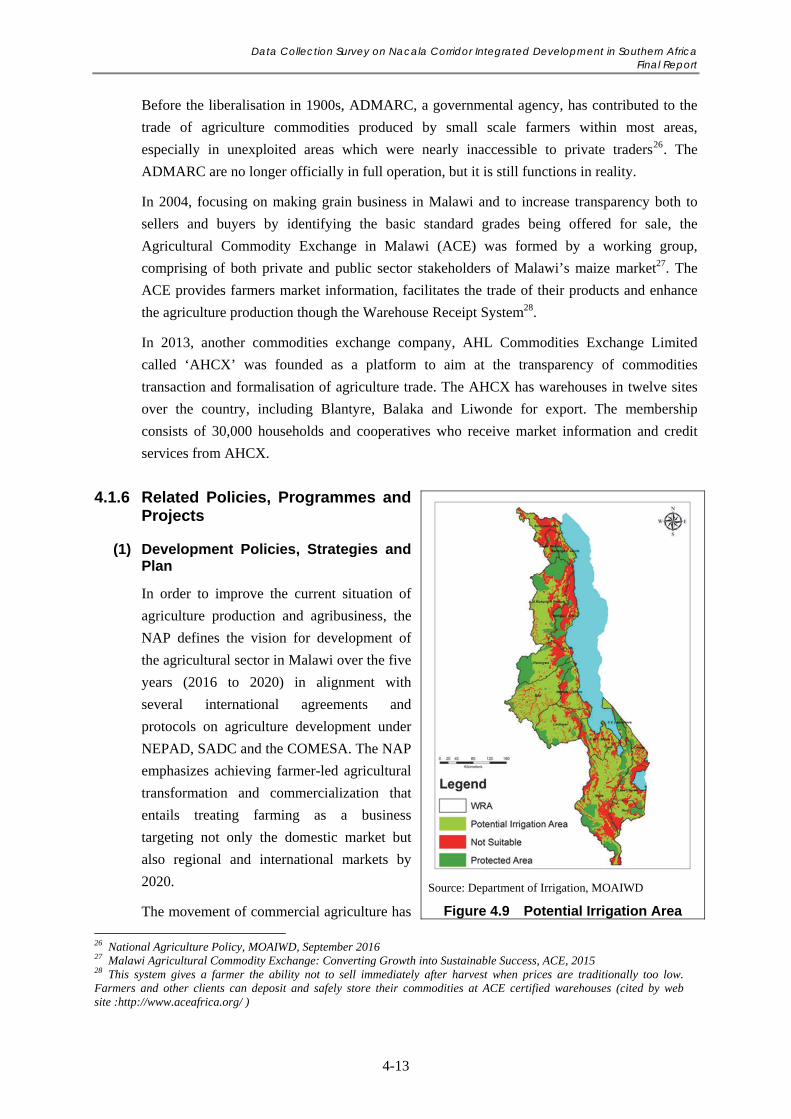

Figure 4.9 Potential Irrigation Area ....................................................................................................... 4-13

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xiii

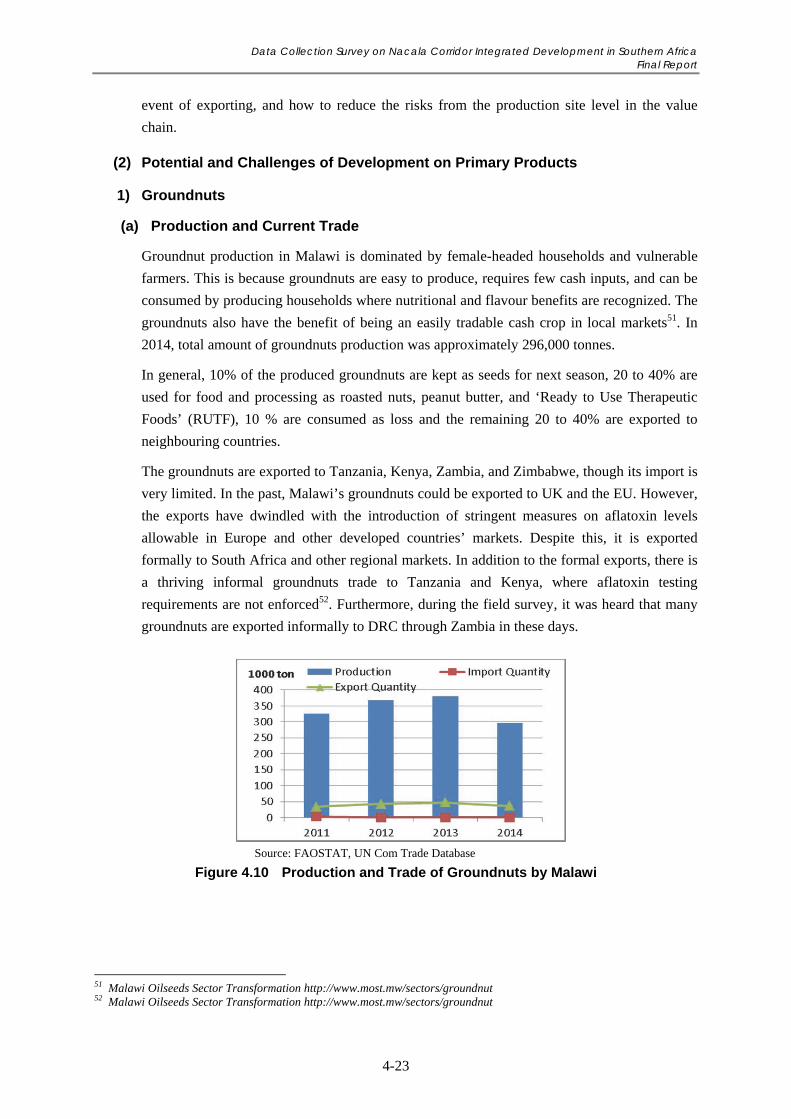

Figure 4.10 Production and Trade of Groundnuts by Malawi.................................................................. 4-23

Figure 4.11 Import of Groundnuts by Country in the Integrated Region ................................................. 4-25

Figure 4.12 Export of Groundnuts by Country in the Integrated Region ................................................. 4-26

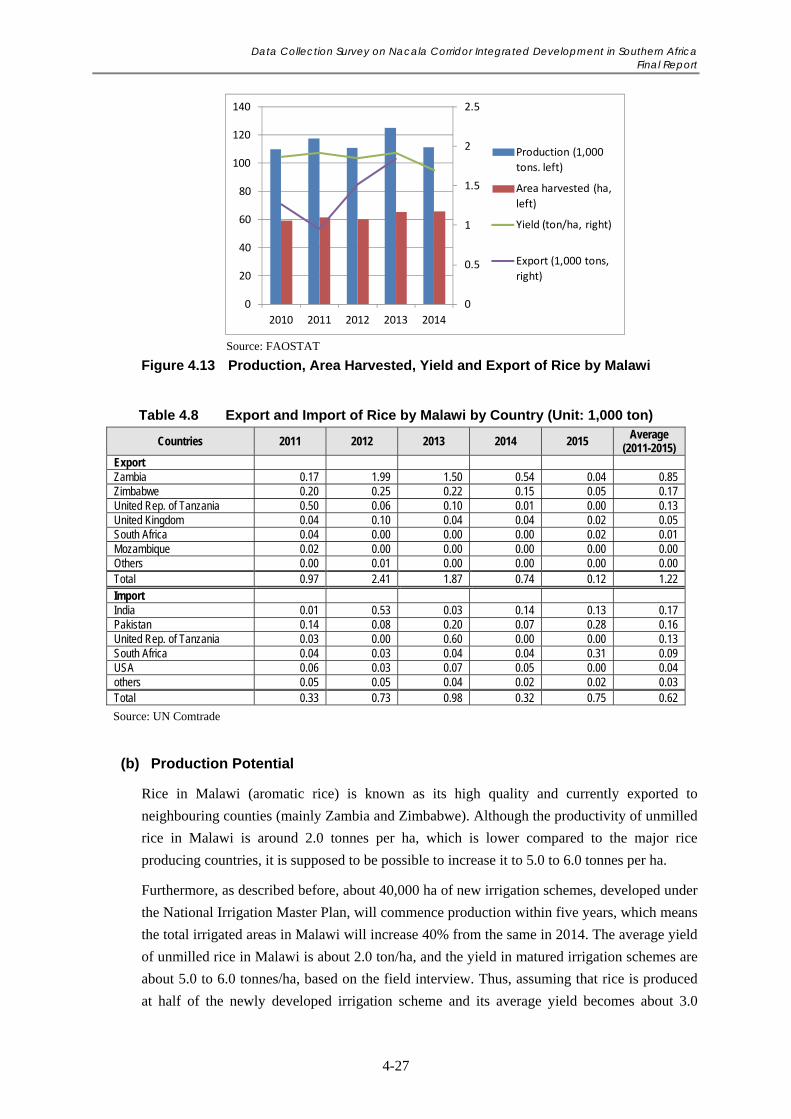

Figure 4.13 Production, Area Harvested, Yield and Export of Rice by Malawi ...................................... 4-27

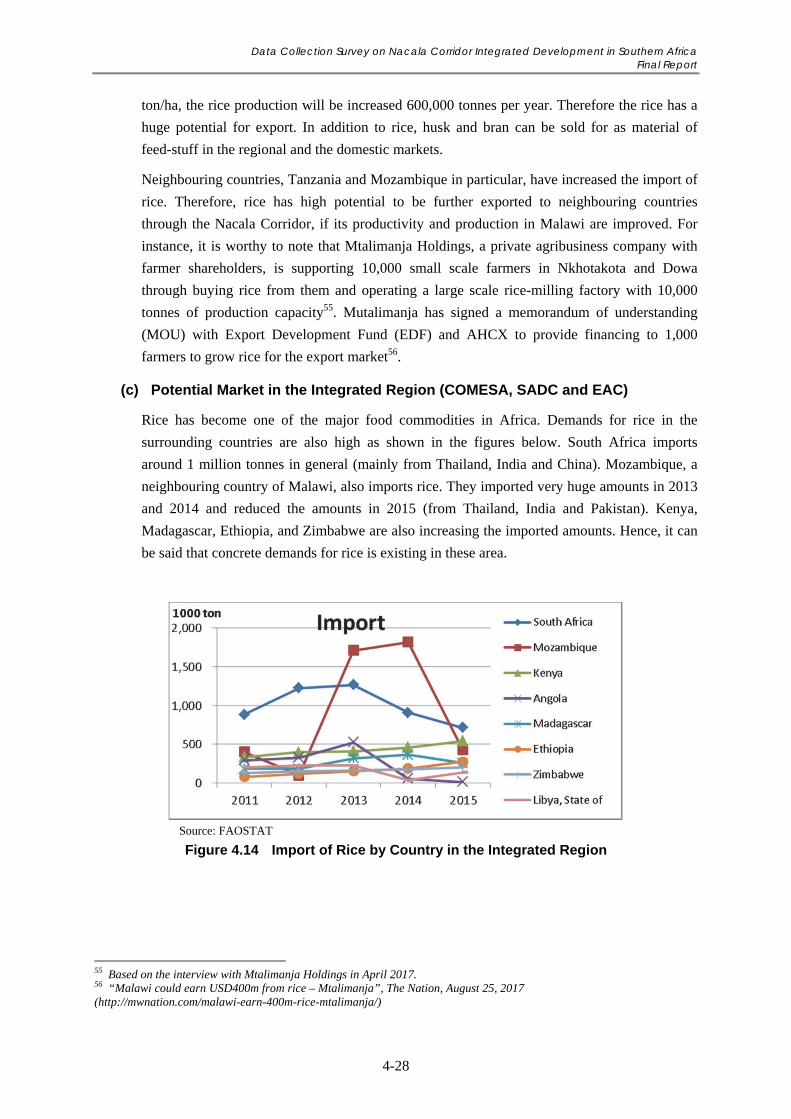

Figure 4.14 Import of Rice by Country in the Integrated Region ............................................................ 4-28

Figure 4.15 Production and Export of Legumes by Malawi .................................................................... 4-30

Figure 4.16 Import of Chickpeas by Country in the Integrated Region ................................................... 4-31

Figure 4.17 Export of Pigeon Pea by Country in the Integrated Region .................................................. 4-32

Figure 4.18 Production and Export of Cotton Lint by Malawi ................................................................ 4-33

Figure 4.19 Production and Trade of Tobacco by Malawi ....................................................................... 4-34

Figure 4.20 Import of Tobacco by Country in the Integrated Region ...................................................... 4-36

Figure 4.21 Production and Trade of Raw Sugar by Malawi ................................................................... 4-37

Figure 4.22 Production, and Trade of Refined Sugar by Malawi ............................................................ 4-38

Figure 4.23 Production and Export of Tea by Malawi ............................................................................. 4-39

Figure 4.24 Import of Tea by Country in the Integrated Region .............................................................. 4-40

Figure 4.25 Production and Export of Oil Seeds in Malawi .................................................................... 4-41

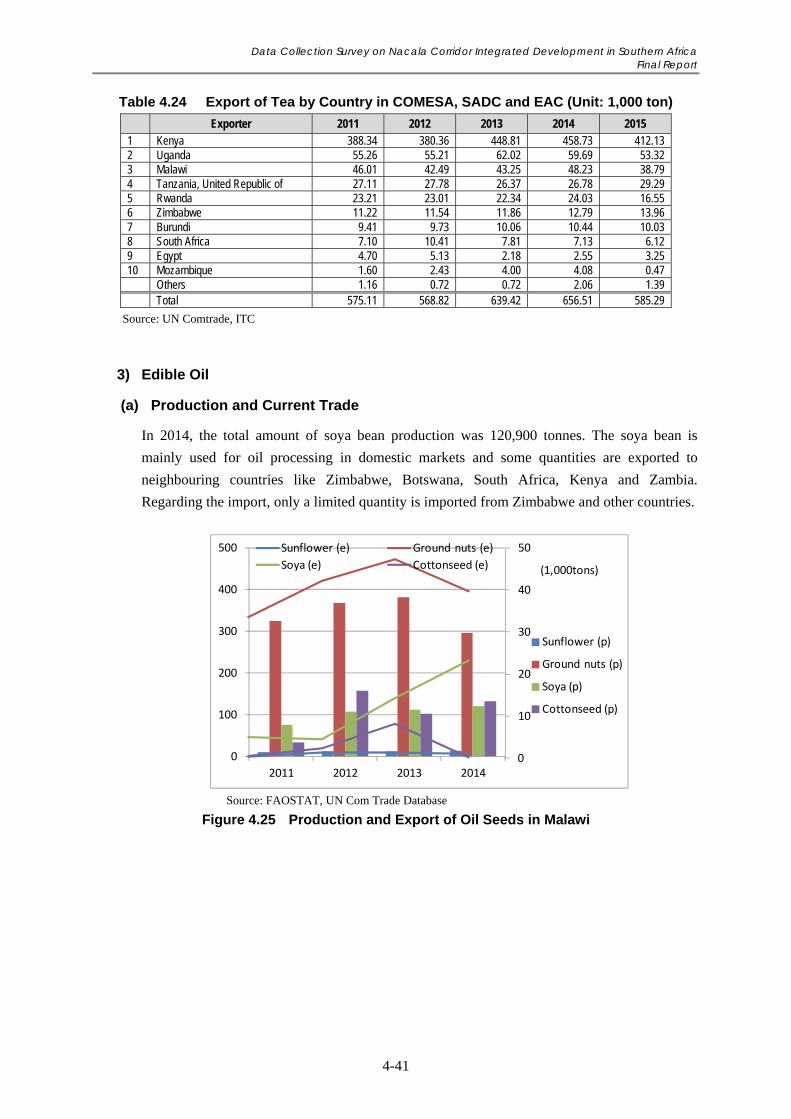

Figure 4.26 Production and Trade of Edible Oil by Malawi .................................................................... 4-42

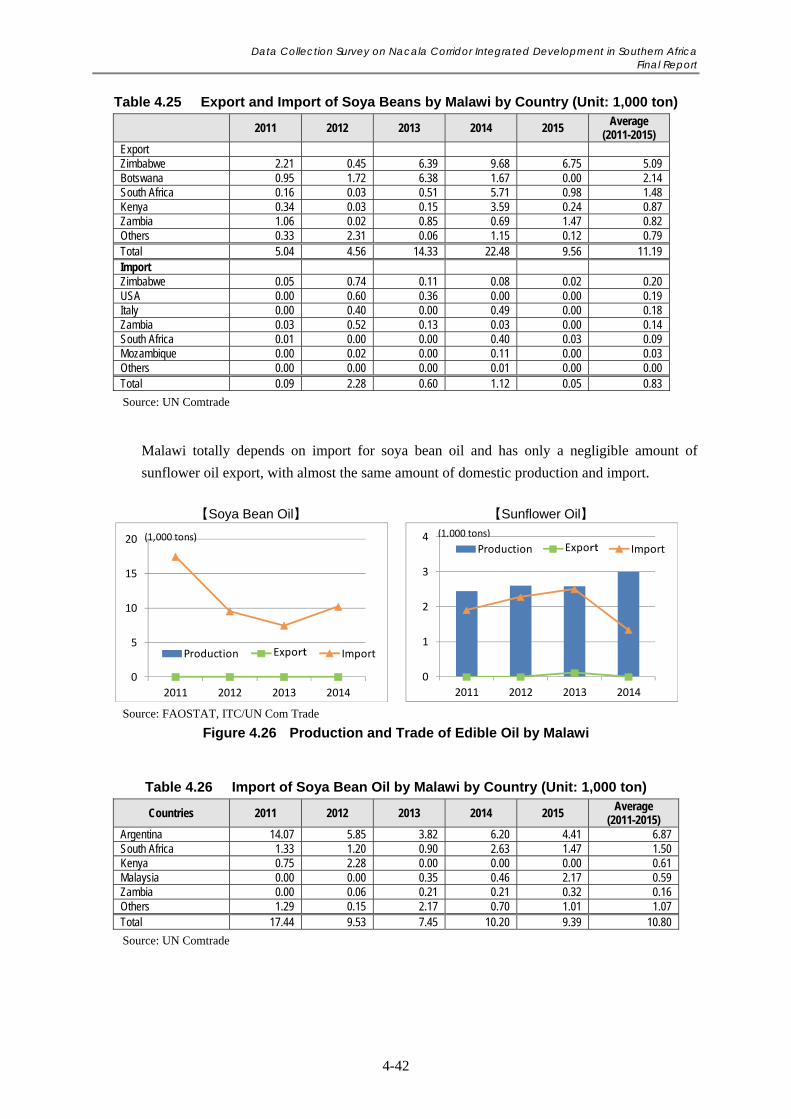

Figure 4.27 Export and Import Values from 2006 to 2015 ...................................................................... 4-49

Figure 4.28 Top 10 Export Partners in 2015 ............................................................................................ 4-50

Figure 4.29 Top 10 Import Partners in 2015 ............................................................................................ 4-50

Figure 4.30 Export by Product Category from 2006 to 2015 ................................................................... 4-51

Figure 4.31 Import by Product Category from 2006 to 2015 ................................................................... 4-51

Figure 4.32 Tourist Arrivals in 2005 by Continent .................................................................................. 4-54

Figure 4.33 Tourist Arrivals by Purpose of Visit ..................................................................................... 4-54

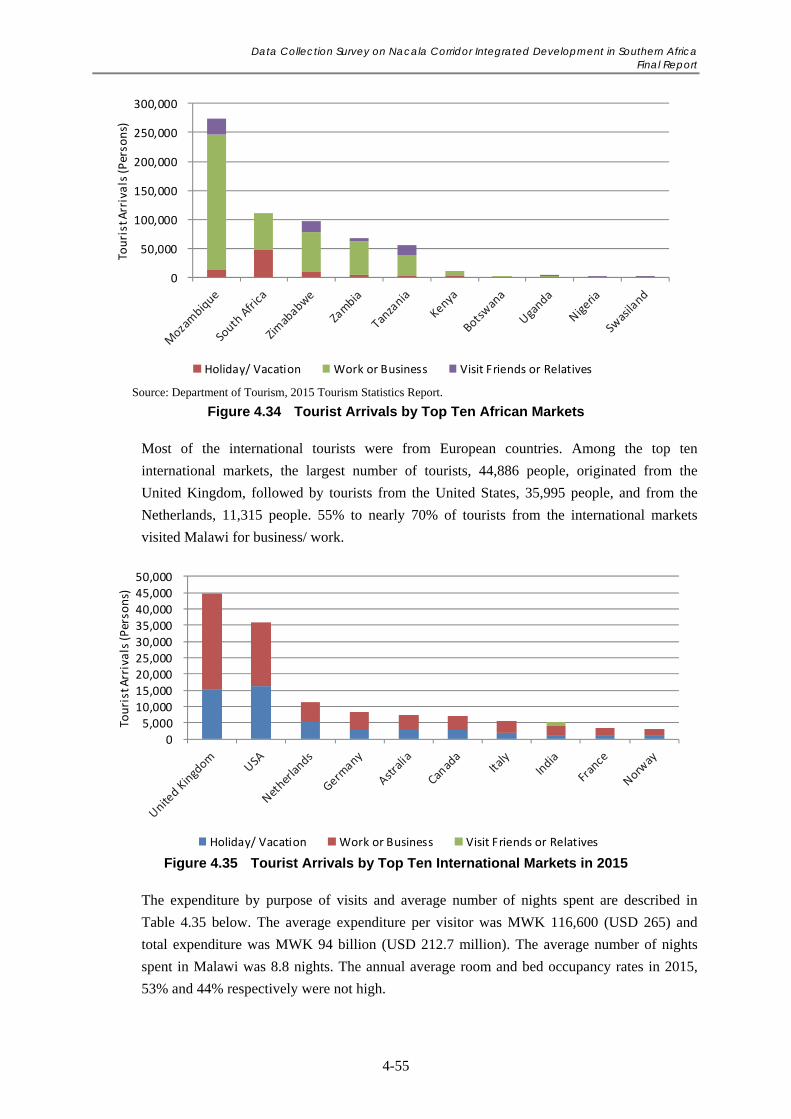

Figure 4.34 Tourist Arrivals by Top Ten African Markets ...................................................................... 4-55

Figure 4.35 Tourist Arrivals by Top Ten International Markets in 2015 ................................................. 4-55

Figure 4.36 Tourist Arrivals by Port of Entry in 2015 ............................................................................. 4-56

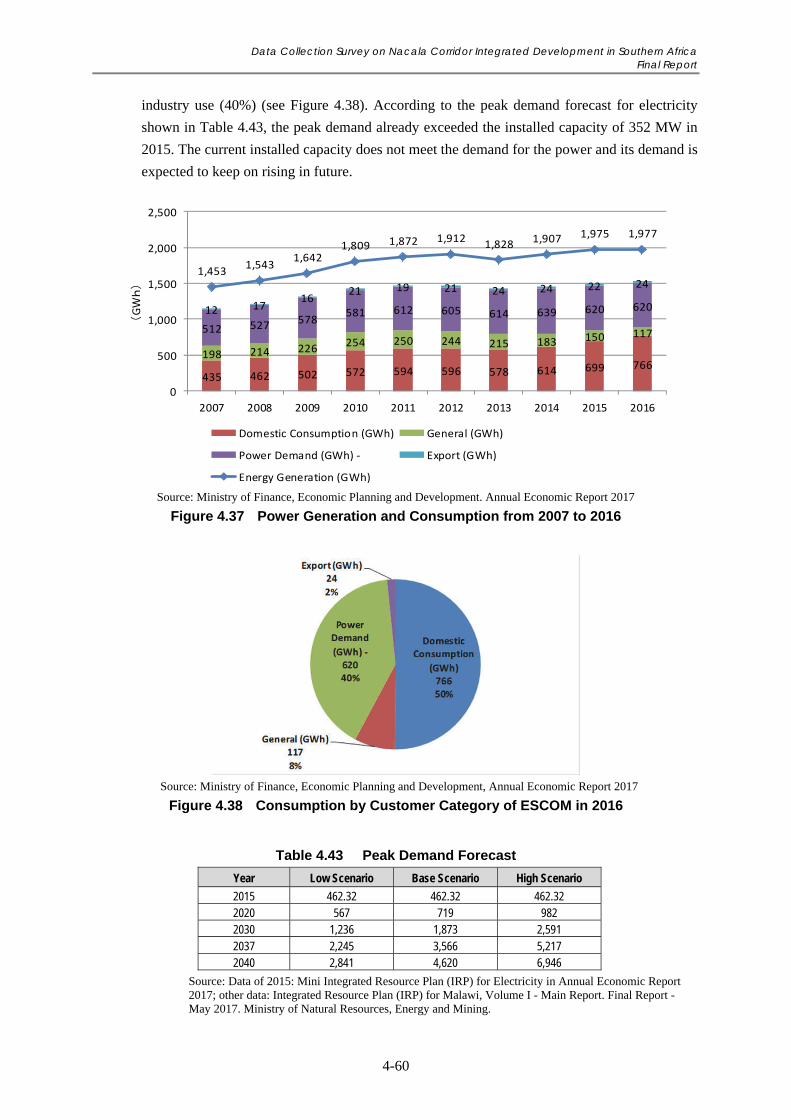

Figure 4.37 Power Generation and Consumption from 2007 to 2016 ..................................................... 4-60

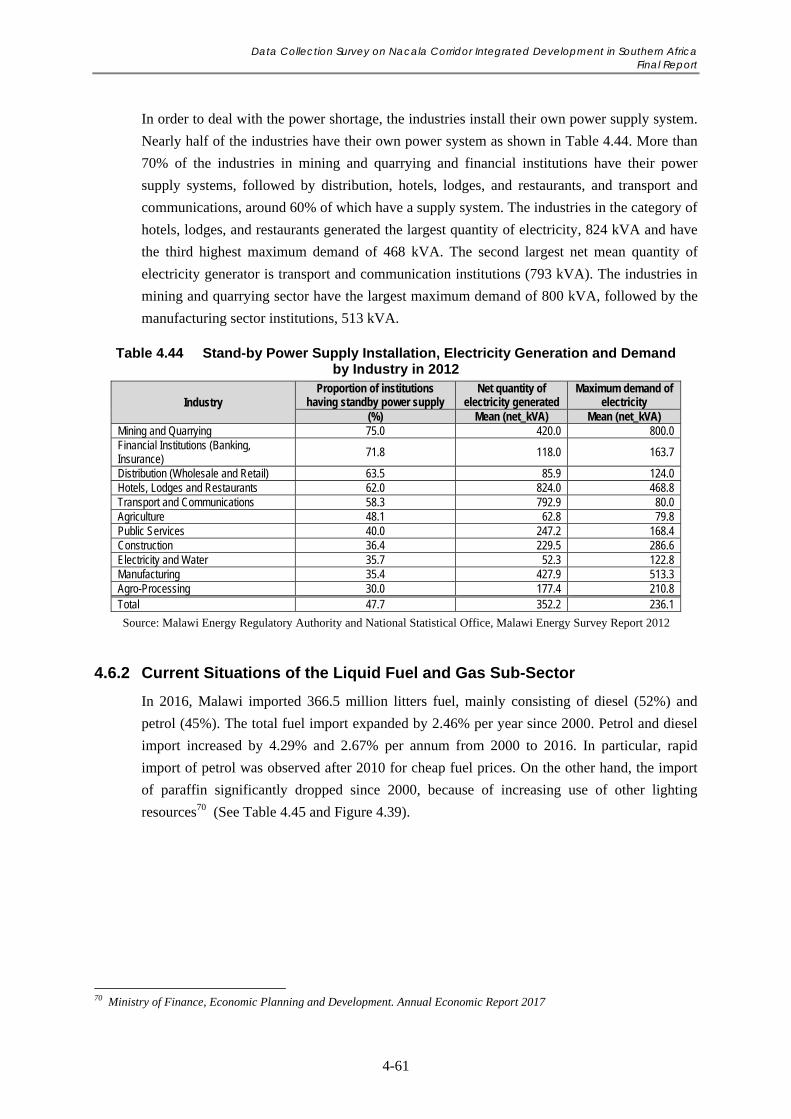

Figure 4.38 Consumption by Customer Category of ESCOM in 2016 .................................................... 4-60

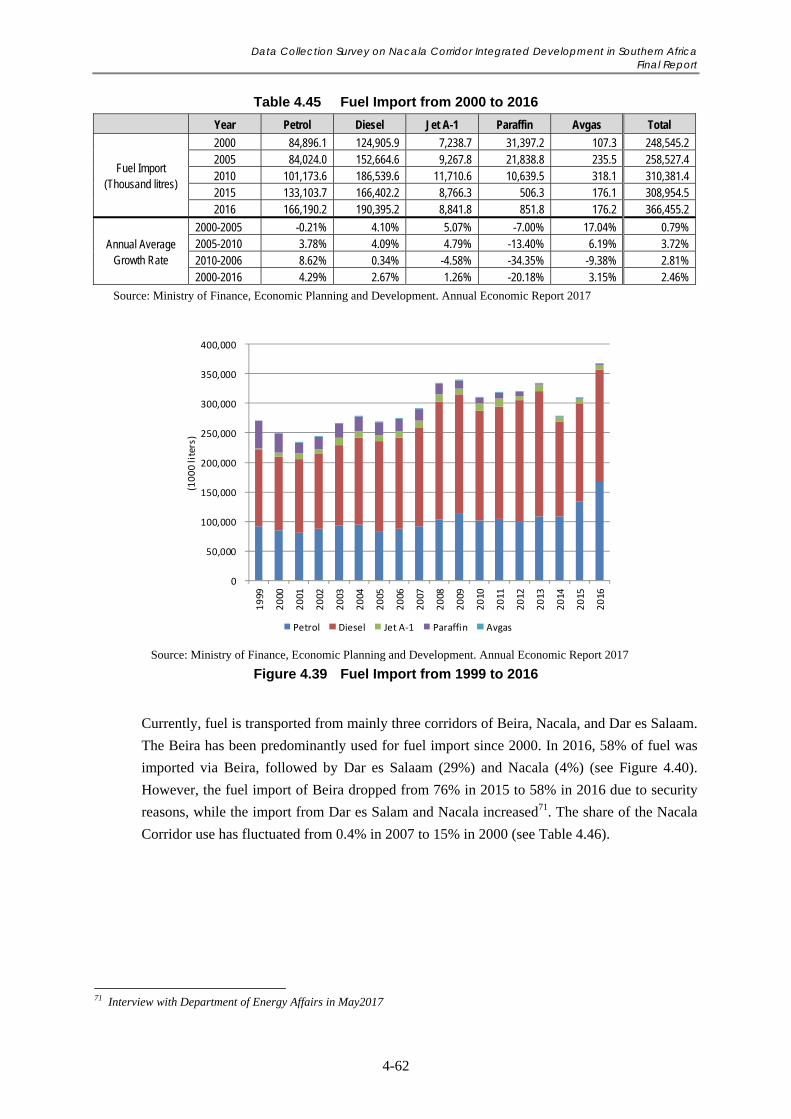

Figure 4.39 Fuel Import from 1999 to 2016 ............................................................................................. 4-62

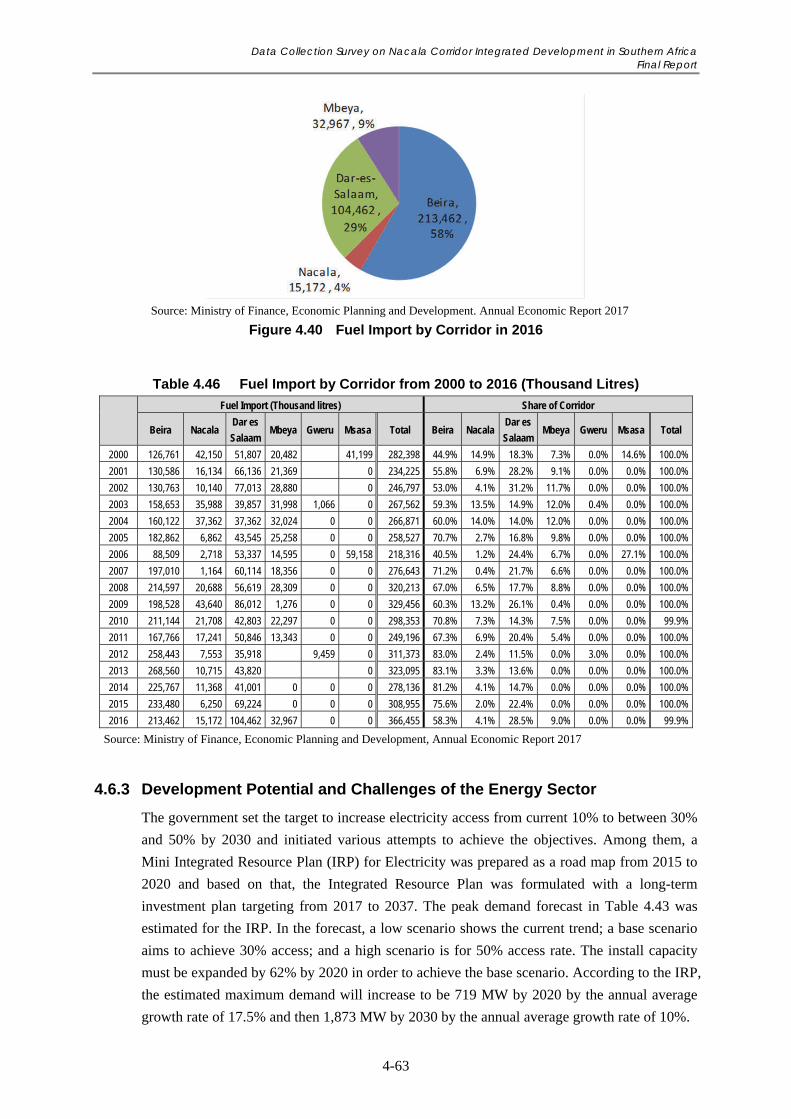

Figure 4.40 Fuel Import by Corridor in 2016 ........................................................................................... 4-63

Figure 4.41 FDI Inflow to Malawi (2011-2014) ...................................................................................... 4-66

Figure 4.42 FDI Inflow to Malawi by Sector (2014) ............................................................................... 4-66

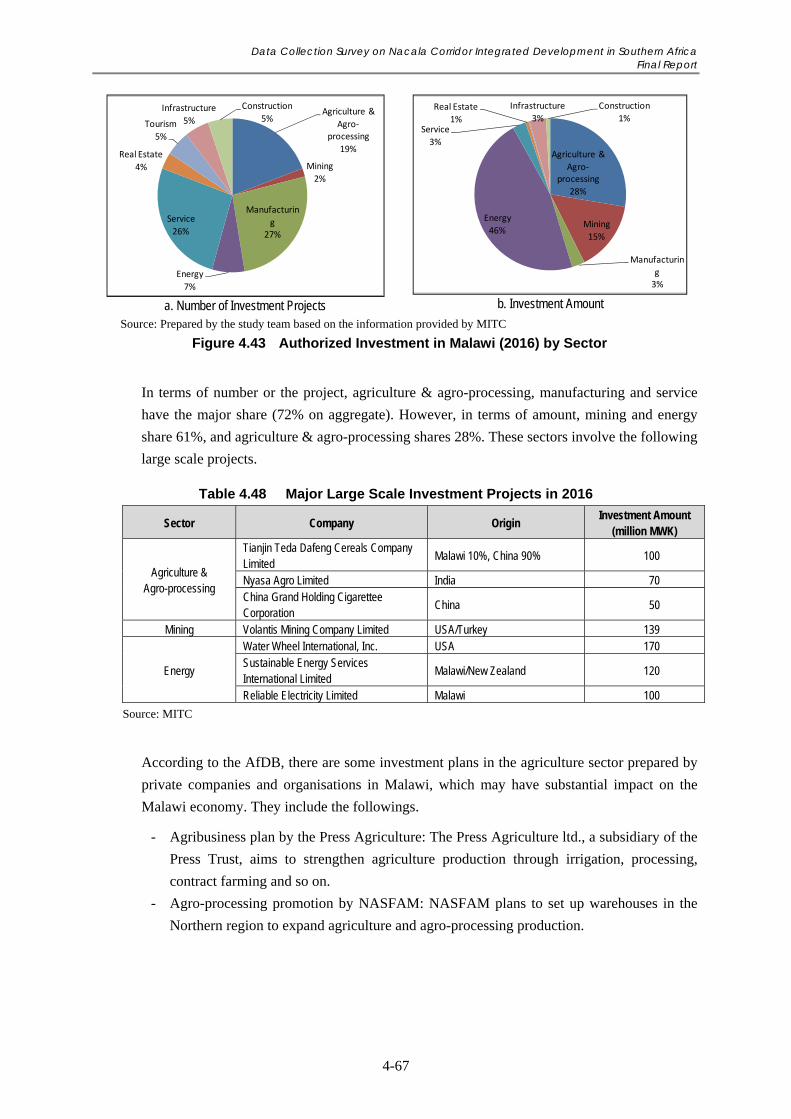

Figure 4.43 Authorized Investment in Malawi (2016) by Sector ............................................................. 4-67

Figure 4.44 Organization Structure of MOTPW ...................................................................................... 4-70

Figure 4.45 Institutions Relating to Road Traffic .................................................................................... 4-71

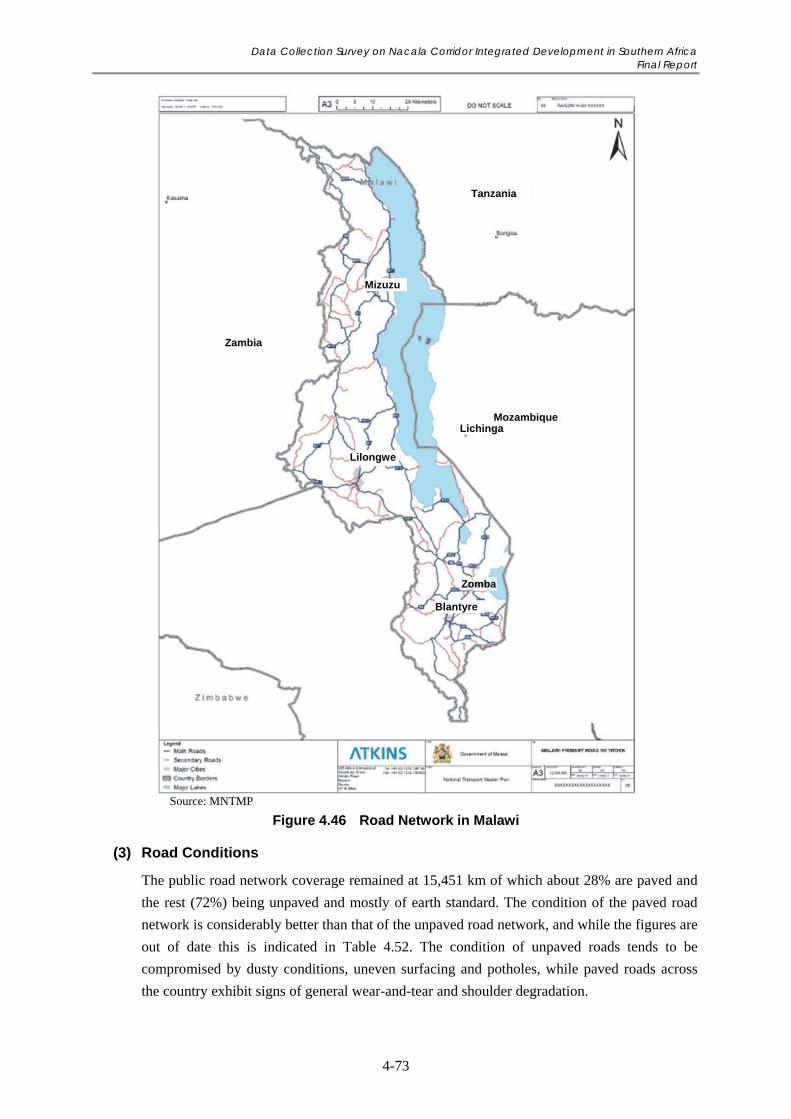

Figure 4.46 Road Network in Malawi ...................................................................................................... 4-73

Figure 4.47 Historic Development of the Railway Network in Malawi .................................................. 4-79

Figure 4.48 Freight Volume at Nayuchi from 2012 to 2016 .................................................................... 4-82

Figure 5.1 Expenditure for Selected Functions in 2018 (Economic Affairs, Environmental

Protection and Housing and Community Amenities) ............................................................. 5-5

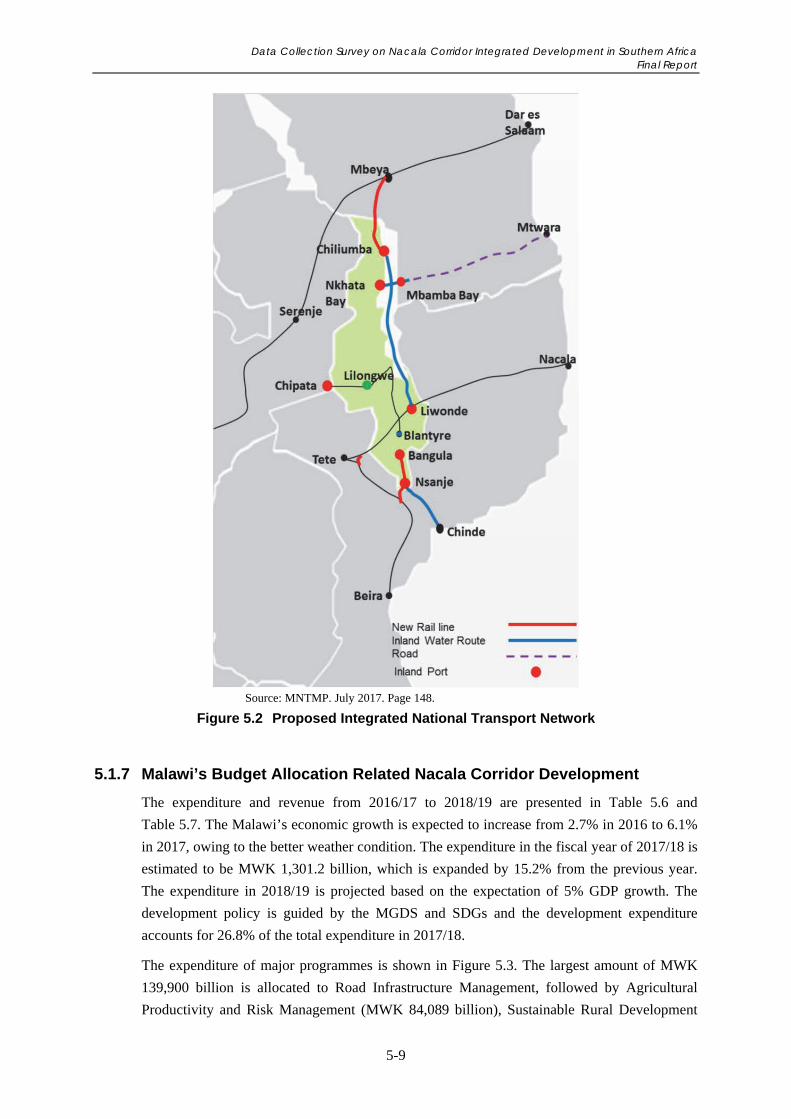

Figure 5.2 Proposed Integrated National Transport Network .................................................................. 5-9

Figure 5.3 Expenditure of Major Programmes ....................................................................................... 5-11

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xiv

Figure 5.4 Location of Chipata- Petauke-Serenje Rail Line .................................................................. 5-16

Figure 5.5 Location of Possible Driving Force Projects and Plans ........................................................ 5-23

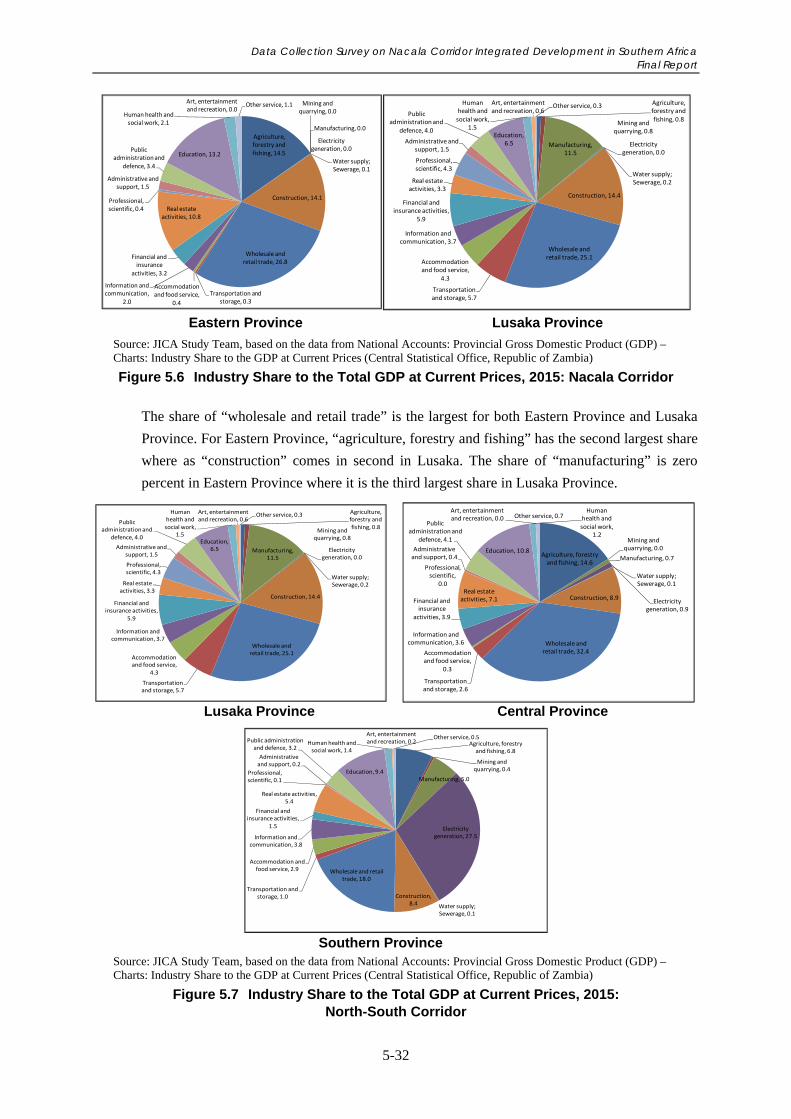

Figure 5.6 Industry Share to the Total GDP at Current Prices, 2015: Nacala Corridor ......................... 5-32

Figure 5.7 Industry Share to the Total GDP at Current Prices, 2015: North-South Corridor ................ 5-32

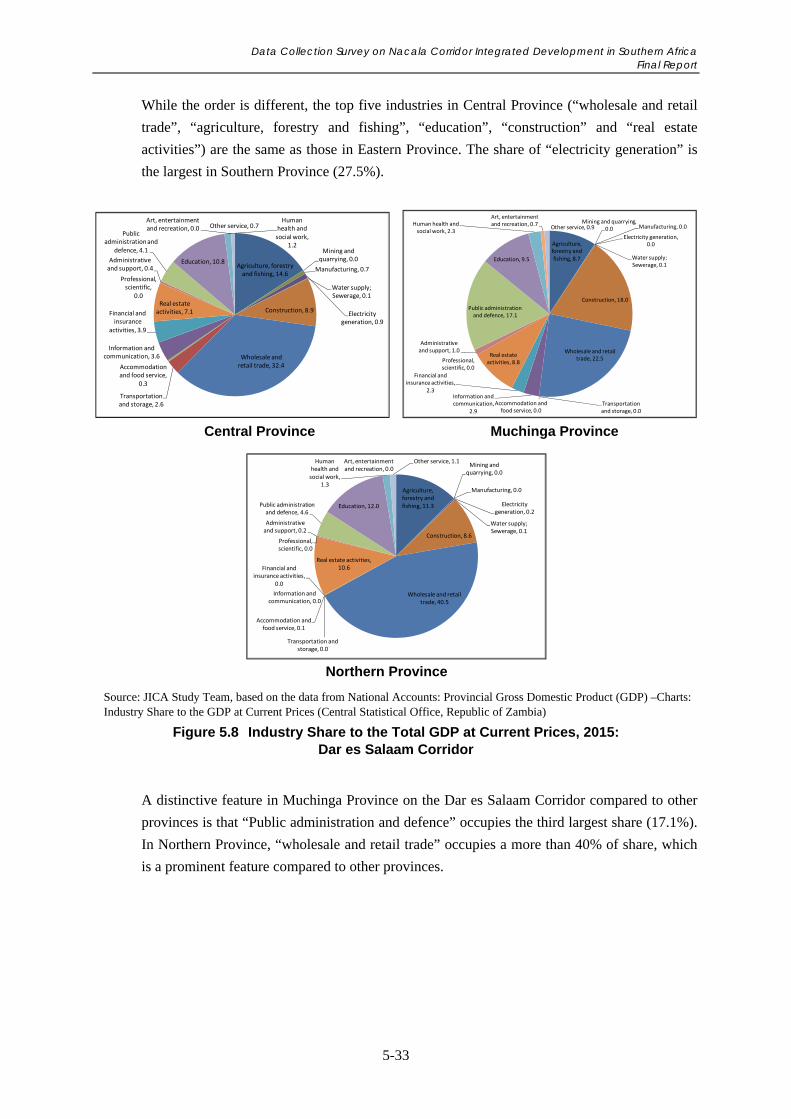

Figure 5.8 Industry Share to the Total GDP at Current Prices, 2015: Dar es Salaam Corridor ............. 5-33

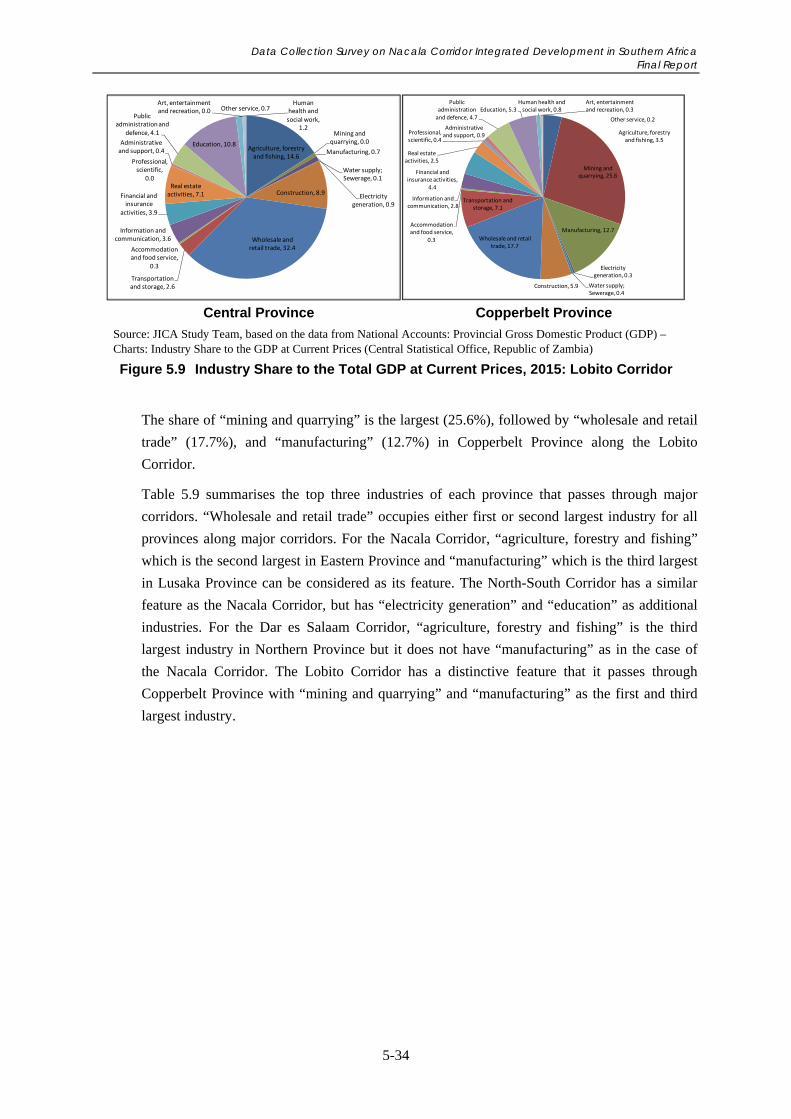

Figure 5.9 Industry Share to the Total GDP at Current Prices, 2015: Lobito Corridor.......................... 5-34

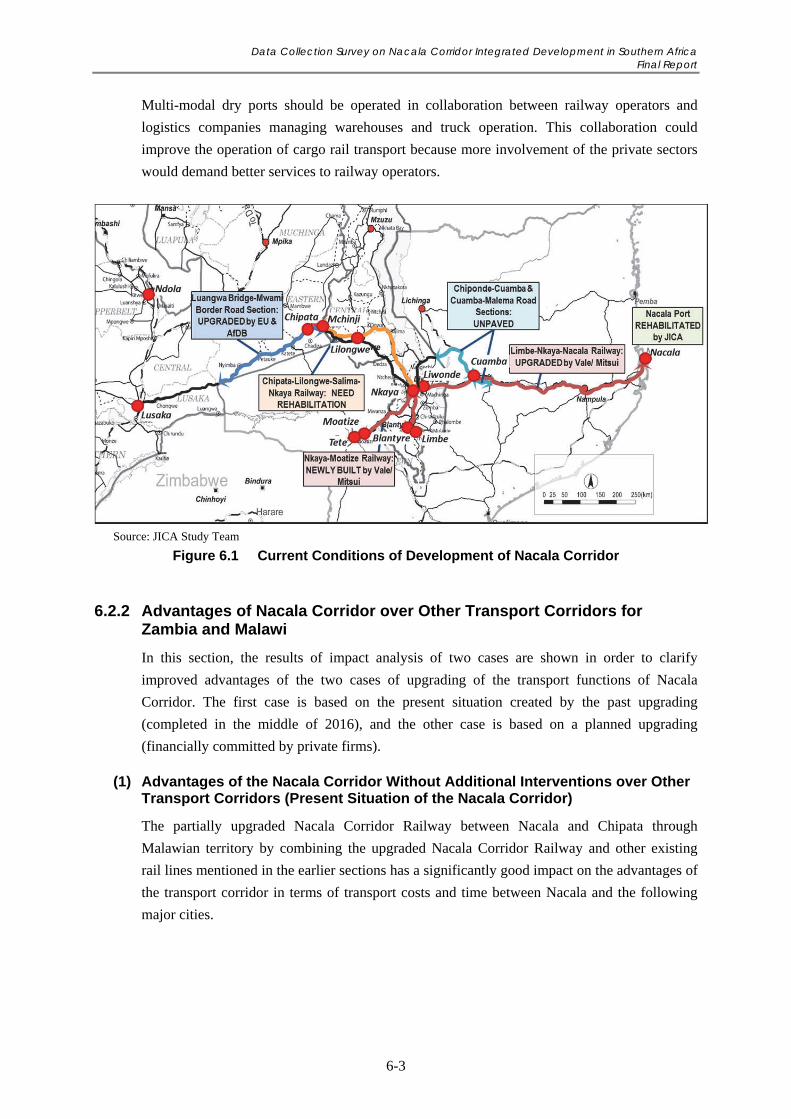

Figure 6.1 Current Conditions of Development of Nacala Corridor ........................................................ 6-3

Figure 6.2 Transport Cost: Comparison of Transport Corridors Related to Zambia and Malawi ............ 6-8

Figure 6.3 Transport Time: Comparison of Transport Corridors Related to Zambia and Malawi ........... 6-9

Figure 6.4 Concept of Corridor Development ....................................................................................... 6-11

Figure 6.5 COMESA-EAC-SADC Tripartite FTA: Expanding Regional Market

-Urban Population 2030 of Major Cities in the Region ..................................................... 6-13

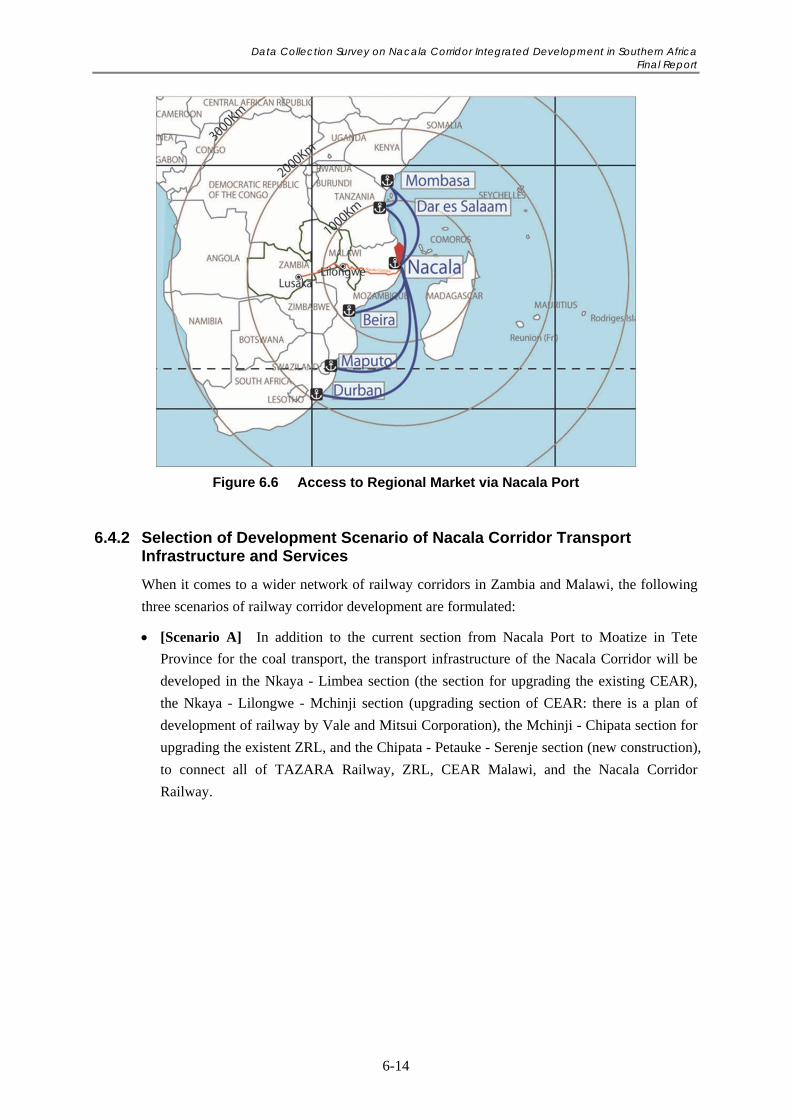

Figure 6.6 Access to Regional Market via Nacala Port ......................................................................... 6-14

Figure 6.7 Wide Railway Network in Zambia and Malawi: Scenario A ............................................... 6-15

Figure 6.8 Wide Railway Network in Zambia and Malawi: Scenario B ................................................ 6-15

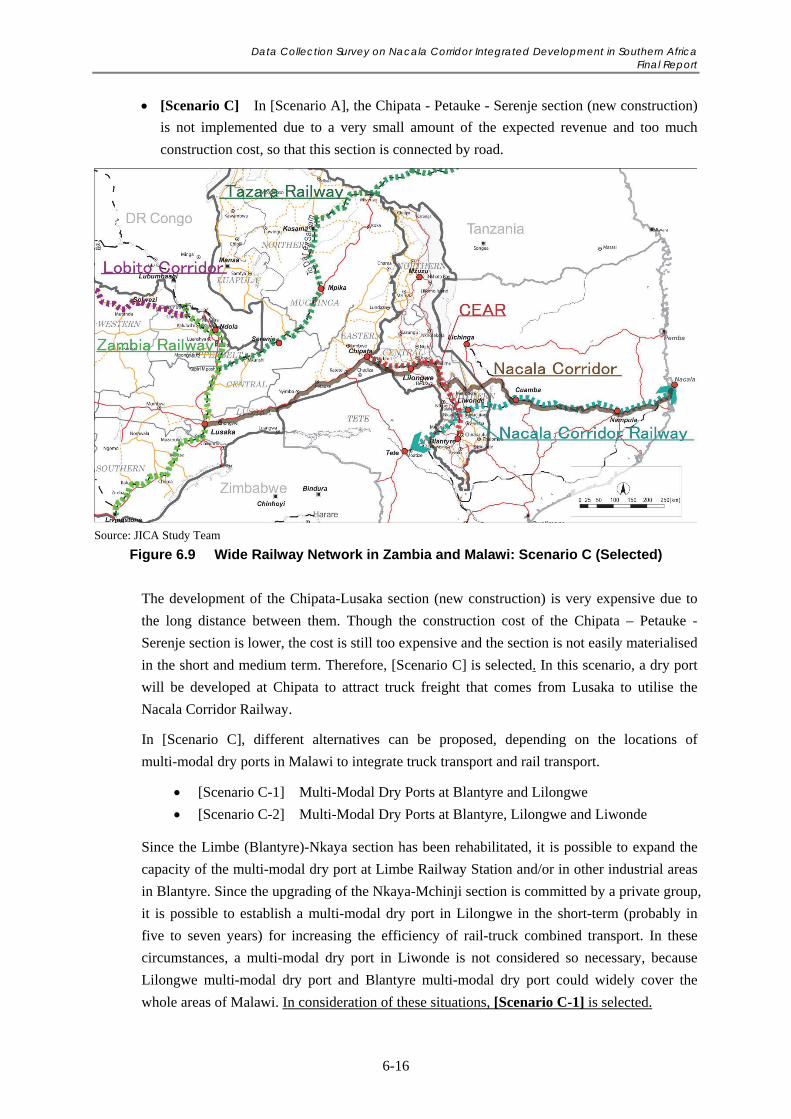

Figure 6.9 Wide Railway Network in Zambia and Malawi: Scenario C (Selected) .............................. 6-16

Figure 6.10 Railway Network (Scenario C: Selected) with Areas of Potential Economic Sectors .......... 6-39

Figure 7.1 Development Stages and Implementation Periods .................................................................. 7-2

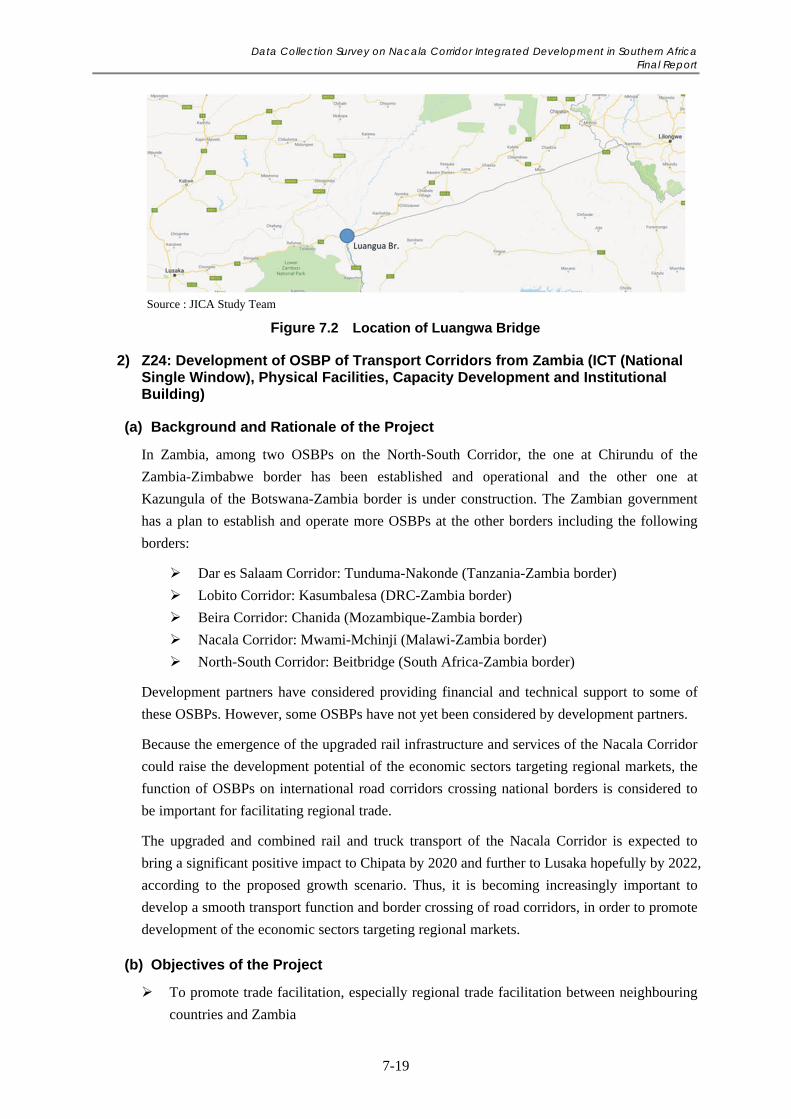

Figure 7.2 Location of Luangwa Bridge ................................................................................................ 7-19

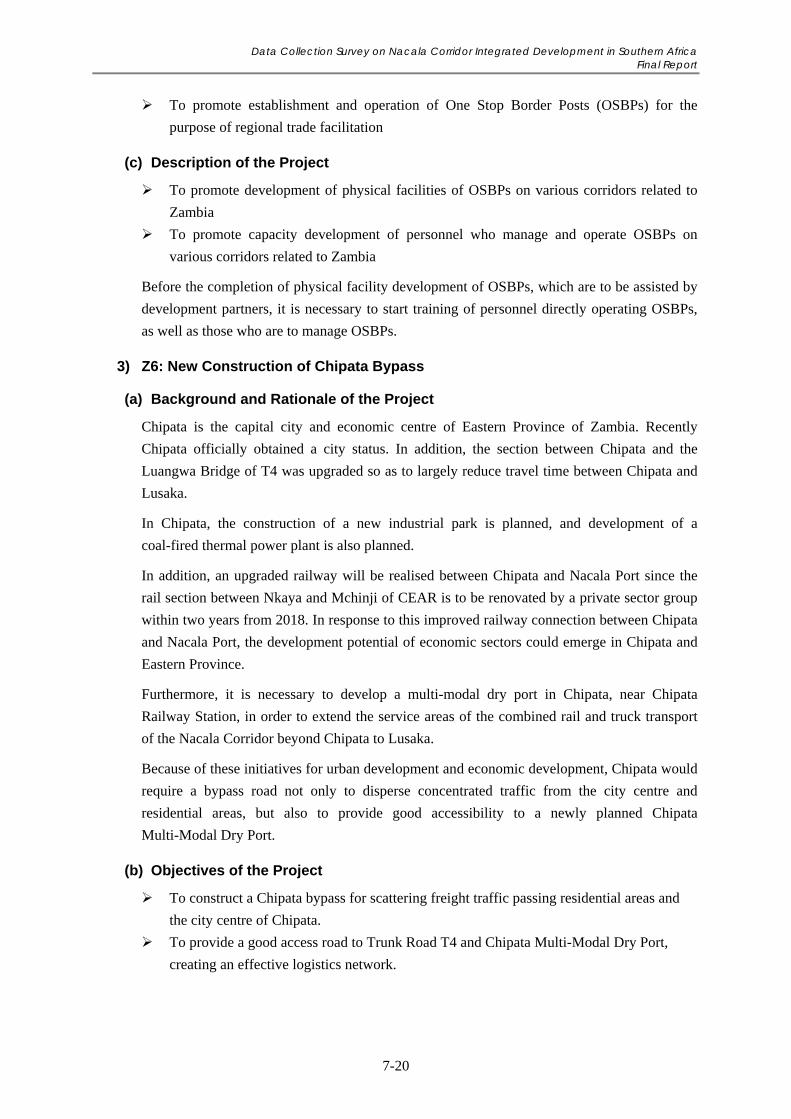

Figure 7.3 Chipata Bypass ..................................................................................................................... 7-21

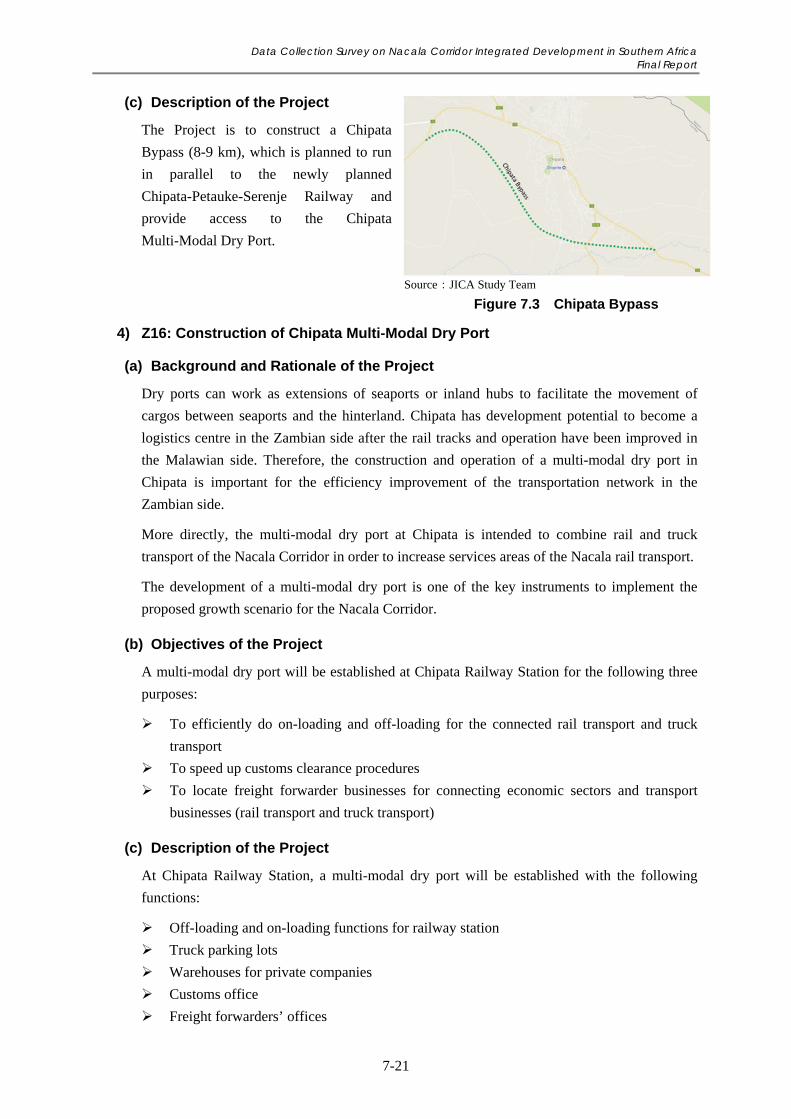

Figure 7.4 Lilongwe North-West Bypass ............................................................................................... 7-23

Figure 7.5 Location of Blantyre City Road Improvement Project ......................................................... 7-24

Figure 7.6 Blantyre Inner Relief Road ................................................................................................... 7-24

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xv

LIST OF ABBREVIATION

7NDP Seventh National Development Plan ACE Agricultural Commodity Exchange (Malawi) ADMARC Agricultural Development and Marketing Corporation AfDB African Development Bank AGCOM Agricultural Commercialization Project for Malawi AHCX Auction Holdings Limited Commodity Exchange (Malawi) ANE National Road Agency(Mozambique)

AP-SEZ Agro-Processing Special Economic Zone ASF African Swine Fever ASWAp Agriculture Sector Wide Approach CAA Civil Aviation Authority CAADP Comprehensive Africa Agriculture Development Programme CAZ Cotton Association of Zambia CBPP Contagious Bovine Pleuropneumonia CCPC Competition and Consumer Protection Commission CDN Corredor de Desenvolvimento do Norte CEAR Central East African Railways CEEC Citizens Economic Empowerment Commission CFM Caminhos de Ferro de Moçambique CCGC China’s Gezhouba Group Corporation CLN Corredor Logístico Integrado do Norte COMACO Community Markets for Conservation COMESA Common Market for Eastern and Southern Africa C-SAAP Country-led Situation Analysis and Action Planning DCA Department of Civil Aviation DCC Dar es Salaam Corridor Coordinating Committee DRC Democratic Republic of the Congo DRI Direct Reduced Iron DRTSS Directorate of Road Traffic and Safety Services (Malawi) EAC East African Community EAPP East Africa Power Pool ECF East Coast Fever ECOWAS Economic Community of West African States EDF Export Development Fund EIA Environmental Impact Assessment EIB European Investment Bank EIF Enhanced Integrated Framework ESCOM Electricity Supply Corporation of Malawi Limited E-SLIP Enhanced Smallholder Livestock Investment Project EU European Union F/S Feasibility Study FAO Food and Agriculture Organisation FAOSTAT Food and Agriculture Organisation Statistics FDI Foreign Direct Investment FISP Farmer Input Support Programme (Zambia) FISP Farm Inputs Subsidy Programme (Malawi) FMCG Fast Moving Consumer Goods

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xvi

FRA Food Reserve Agency FSP Fertilizer Support Program FTA Free Trade Area FTC Farmer Training Centre FUM Farmers Union of Malawi GBI Green Belt Initiative GDP Gross Development Product GIZ Deutsche Gesellschaft für Internationale Zusammenarbeit GMA Game Management Areas GOM Government of Malawi GOZ Government of Zambia GW Giga Watt (109 watt) HFO Heavy Fuel Oil ICD Inland Container Depot ICT Information Communications Technology ICTC Inter-Country Trade Centre IDA International Development Association IDC Industrial Development Cooperation IFAD International Fund for Agricultural Development IPPs Independent Power Producers IRP Integrated Resource Plan (Malawi) JICA Japan International Cooperation Agency KIA Kamuzu International Airport KPAs Key Priority Areas MAPAC Malawi Programme for Aflatoxin Control MBS Malawi Bureau of Standards MERA Malawi Energy Regulatory Authority MFEZ Multi Facility Economical Zone MFL Ministry of Fisheries and Livestock (Zambia) MGDS Malawi Growth and Development Strategy MHID Ministry of Housing and Infrastructure Development (Zambia) MIDP Medium Scale Irrigation Development Project MITC Malawi Investment and Trade Centre MNLP Malawi National Land Policy MNTMP Malawi National Transport Master Plan MNTP Malawi National Transport Policy MOA Ministry of Agriculture (Zambia) MOAIWD Ministry of Agriculture, Irrigation and Water Development (Malawi) MOCTI Ministry of Commerce, Trade and Industry (Zambia) MOE Ministry of Energy MOITT Ministry of Industry, Trade and Tourism (Malawi) MOTPW Ministry of Transport and Public Works (Malawi) MOU Memorandum of Understanding MRA Malawi Revenue Authority MT Metric Ton MTC Ministry of Transport & Communications (Zambia) MW Mega Watt MWK Malawian Kwacha

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xvii

MWS Ministry of Works & Supply (Zambia) NAIP National Agricultural Investment Plan NAP National Agriculture Policy NAS National Agriculture Strategy NASFAM National Smallholder Farmers’ Association of Malawi NCIC National Construction Industry Council NEPAD New Partnership for Africa's Development NEPAD-IPPF NEPAD Infrastructure Project Preparation Facility NES National Export Strategy NGO Non-Governmental Organization NMT Non-Motorised Transport NRFA National Road Fund Agency (Zambia) NTE Non Traditional Exports NWRA National Water Resources Authority O&M Operation and Maintenance OFID OPEC (Organization of the Petroleum Exporting Countries) Fund for International

Development OPRC Output and Performance Based Road Contracting System OSBP One Stop Border Post PACA Partnership for Aflatoxin Control in Africa Petromoc Petróleos de Moçambique PPP Private Public Partnership PSO Public Service Obligation PTA Preferential Trade Area RA Roads Authority (Malawi) RDA Road Development Agency (Zambia) RDC Railroad Development Corporation REO Rare Earth Oxides RFA Road Fund Administration (Malawi) RGCs Rural Growth Centres RISDP Regional Indicative Strategic Development Plan RSS Road Sector Strategy RSZ Railway Systems of Zambia RTSA Road Transportation & Safety Agency

RUTF Ready to Use Therapeutic Foods SA South Africa SADC Southern African Development Community SAPP Smallholder Agribusiness Promotion Programme SAPP Southern African Power Pool SDI Spatial Development Initiative SEZ Special Economic Zone SLIP Smallholder Livestock Investment Project SMEs Small and Medium Enterprises SNAP Second National Agriculture Policy SPS Sanitary and Phytosanitary SVIP Shire Valley Irrigation Project SWB Small Water Bodies T4 Great East Road

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

xviii

TAZAMA Tanzania-Zambia Mafuta TAZARA Tanzania-Zambia Railway Authority TEU Twenty Feet Equivalent Unit TFCAs Transfrontier Conservation Areas TIP SWAp Trade Industry and Private Sector Development Sector Wide Approach TWG Technical Working Group UAE United Arab Emirates UEMOA West African Economic and Money Union USAID United States Agency for International Development UNDP United Nations Development Programme UNSD United Nations Statistics Division WB World Bank WBCG Walvis Bay Corridor Group WITS World Integrated Trade Solution WTO World Trade Organization ZAMACE Zambian Commodity Exchange ZDA Zambia Development Agency ZMW Zambian Kwacha ZNFU Zambia National Farmers Union ZNTMP Zambia National Transport Master Plan ZNTP Zambia National Transport Policy ZRA Zambia Revenue Authority ZRA Zambia Railways Authority ZRL Zambia Railways Limited

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

S-1

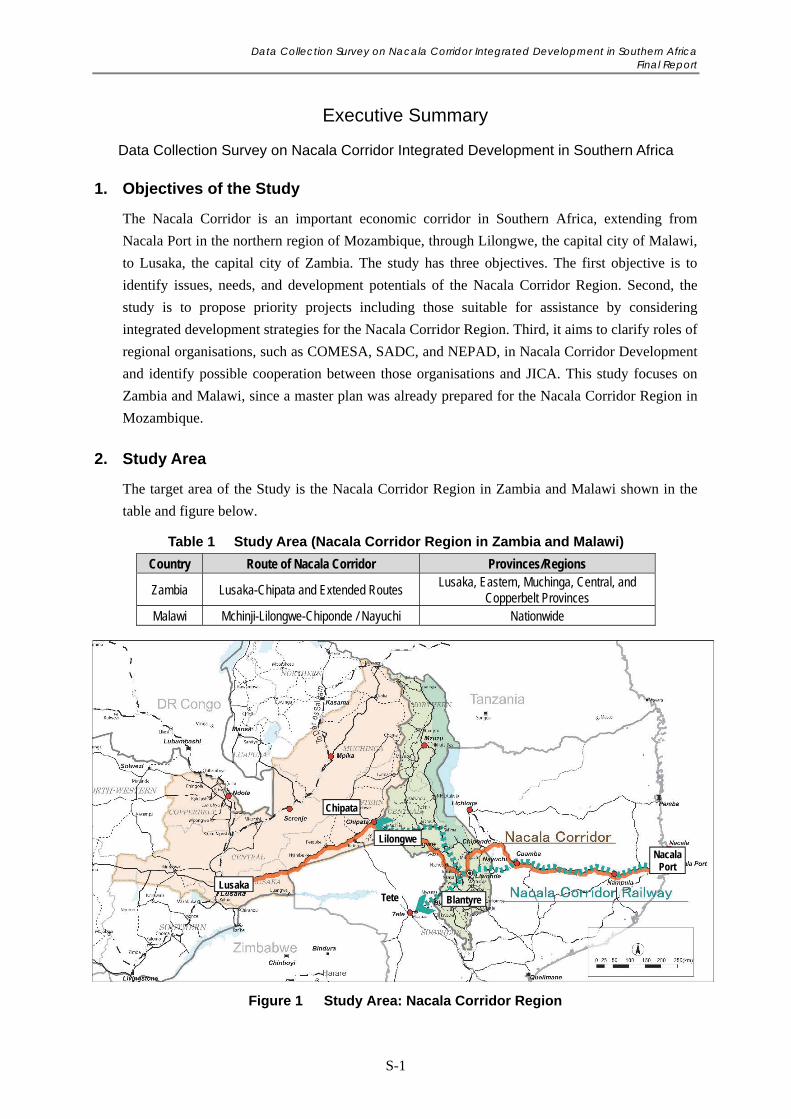

Executive Summary

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa

1. Objectives of the Study

The Nacala Corridor is an important economic corridor in Southern Africa, extending from

Nacala Port in the northern region of Mozambique, through Lilongwe, the capital city of Malawi,

to Lusaka, the capital city of Zambia. The study has three objectives. The first objective is to

identify issues, needs, and development potentials of the Nacala Corridor Region. Second, the

study is to propose priority projects including those suitable for assistance by considering

integrated development strategies for the Nacala Corridor Region. Third, it aims to clarify roles of

regional organisations, such as COMESA, SADC, and NEPAD, in Nacala Corridor Development

and identify possible cooperation between those organisations and JICA. This study focuses on

Zambia and Malawi, since a master plan was already prepared for the Nacala Corridor Region in

Mozambique.

2. Study Area

The target area of the Study is the Nacala Corridor Region in Zambia and Malawi shown in the

table and figure below.

Table 1 Study Area (Nacala Corridor Region in Zambia and Malawi)

Country Route of Nacala Corridor Provinces/Regions

Zambia Lusaka-Chipata and Extended Routes Lusaka, Eastern, Muchinga, Central, and

Copperbelt Provinces Malawi Mchinji-Lilongwe-Chiponde / Nayuchi Nationwide

Figure 1 Study Area: Nacala Corridor Region

Tete Lusaka

Chipata

Lilongwe

Blantyre

Nacala Port

Data Collection Survey on Nacala Corridor Integrated Development in Southern Africa Final Report

S-2

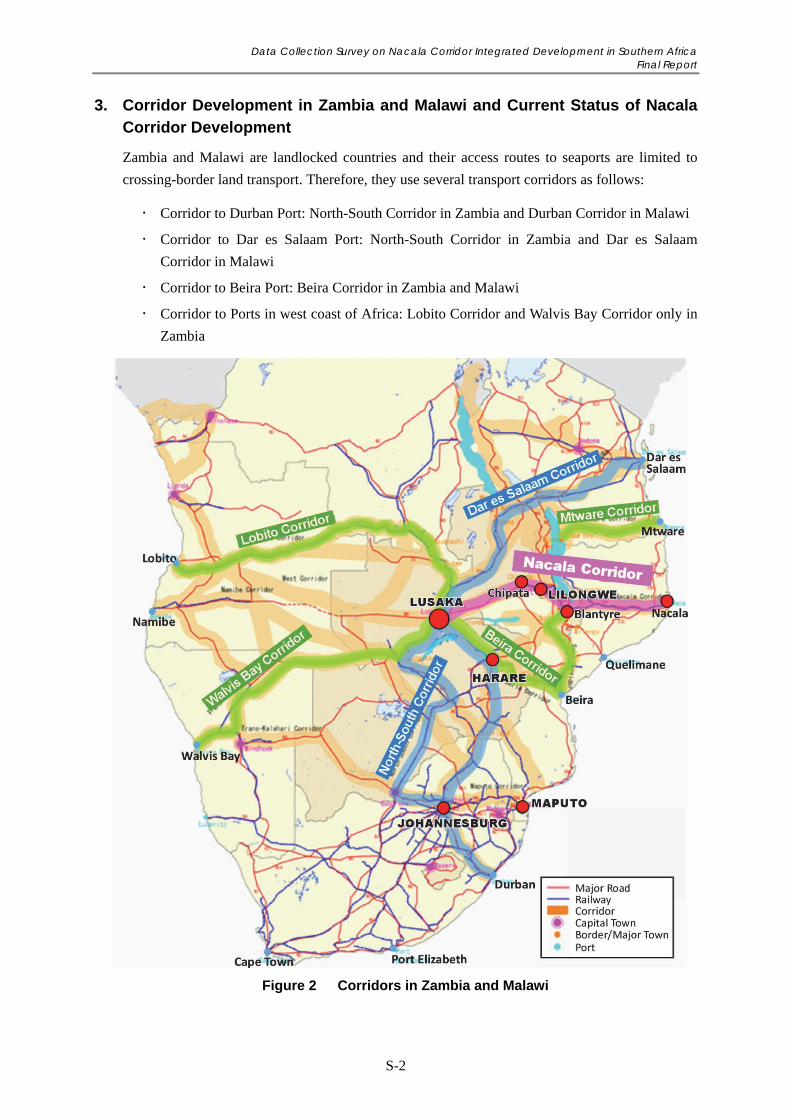

3. Corridor Development in Zambia and Malawi and Current Status of Nacala Corridor Development

Zambia and Malawi are landlocked countries and their access routes to seaports are limited to

crossing-border land transport. Therefore, they use several transport corridors as follows:

Corridor to Durban Port: North-South Corridor in Zambia and Durban Corridor in Malawi

Corridor to Dar es Salaam Port: North-South Corridor in Zambia and Dar es Salaam

Corridor in Malawi

Corridor to Beira Port: Beira Corridor in Zambia and Malawi

Corridor to Ports in west coast of Africa: Lobito Corridor and Walvis Bay Corridor only in

Zambia