1 DATA BASE ACCURACY AND INTEGRITY AS A PRECONDITION FOR OVERHEAD ALLOCATIONS Harry H E Fechner Doctor of Philosophy The University of Western Sydney Sydney, Australia 2004

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

DATA BASE ACCURACY AND INTEGRITY AS A

PRECONDITION FOR OVERHEAD ALLOCATIONS

Harry H E Fechner

Doctor of Philosophy

The University of Western Sydney

Sydney, Australia

2004

2

Certification

This is to certify that to the best of my knowledge, the research presented in this

dissertation is my own and original work, except where relevant sections and

references are duly acknowledged. This dissertation has not been submitted

previously in its entirety or substantial parts of it for a higher degree qualification

at any other university or higher educational institution.

Harry H E Fechner

28 January 2004

3

Acknowledgements

There are numerous individuals that deserve special acknowledgment for their

assistance and contribution during the period of my candidature and to them I

express my sincere appreciation. Special thanks must go to my supervisor Assoc.

Prof. Rakesh Agrawal from the University of Western Sydney and co-supervisor

Prof. Graeme Harrison of Macquarie University. I am extremely grateful for the

patience and expert guidance I received from Prof. Agrawal during our many

thought-provoking discussions.

I am also grateful to a number of individuals who provided feedback and

commentary on aspects and content issues of my thesis during presentations at

international accounting conferences. While the list of these individuals is too

numerous, I would like to acknowledge the lengthy discussions I had at various

times with Prof. Malcolm Smith from the University of South Australia, Prof Clive

Emmanuel from Glasgow University, UK, Dr Michael Tayles of Bradford

University, UK, Prof Marc Massoud of Claremont College, California, USA, Prof.

Cecilie Raiborn of Layola University, Louisiana, USA, Prof. Rashid Abdel Khalik,

University of Illinois, USA, Prof Ted Davies, Aston University, UK and Prof Rob

Chenhall of Monash University, Melbourne Australia.

Additional thanks must go to the participants at the various sessions at many

international accounting conferences that provided -through questions and

4

feedback- many thought provoking additional research investigations to include

in the final dissertation.

5

Table of Contents

Certification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

List of Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

List of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Abstract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. The Study Relevance to the Discipline . . . . . . . . . . . . . . . . . . . . . . . . . . 19

1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

1.2 Contribution of Research to the Discipline . . . . . . . . . . . . . . . . . . . . 29

1.3 Research Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

1.4. Research Methodology and Methods . . . . . . . . . . . . . . . . . . . . . . . . 33

1.4.1 Mathematical Techniques employed for model development. . 35

1.5 Structure of Thesis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

1.6 Definitions, Key Assumptions and Limitations. . . . . . . . . . . . . . . . . . 40

Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Key Assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Limitations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

2. Literature Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

2.1.1. Traditional Organisational and Operational Environments . 48

2.2.2 The Full Cost (or Absorption Cost) Concept. . . . . . . . . . . . . . 51

2.2.3 The Variable Cost (or Direct Cost) Concept. . . . . . . . . . . . . . 59

2.2.4 Standard Cost Concept . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

2.2 The Changing Organisational and Operational Environments. . . . . . 63

2.2.1 Activity-Based Costing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

2.2.2 The Theory of Constraints . . . . . . . . . . . . . . . . . . . . . . . . . . 74

2.2.3 Strategic Management Accounting . . . . . . . . . . . . . . . . . . . . . 79

2.2.3.1 Critical Evaluation of Emerging

Management Accounting Systems . . . . . . . . . . 83

2.2.3.2C Case Study Based Comparison between

ABC and MAS. . . . . . . . . . . . . . . . . . . . . . . . . . 83

2.2.3.3 Error Incidence and System Accuracy . . . . . . . 92

2.2.3.4 The (IR)Relevance of Cost Management

Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

2.3 Chapter Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

6

3. Model Development. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

3.1.1. Database Integrity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

3.2 Development of a Pareto Frontier Model. . . . . . . . . . . . . . . . . . . 125

3.3 Data Base Generation and Pattern Recognition . . . . . . . . . . . . . . . 132

3.4 Chapter Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

4. Case Study Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

4.2 Case Study Analysis Stock Exchange Data. . . . . . . . . . . . . . . . . 154

4.2 Case Study Analysis University Enrolment Data . . . . . . . . . . . . . . 156

4.3 Case Study Analysis Inventory Data . . . . . . . . . . . . . . . . . . . . . . . . 166

4.4 Chapter Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173

5. Discussion of Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176

6. Summary and Future Research Suggestions . . . . . . . . . . . . . . . . . . . . 185

6.1 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 185

6.2 Major Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193

6.3 Future Research Suggestions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 194

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

List of Publications by Author relating to Thesis . . . . . . . . . . . . . . . . . . . . . . 202

7

List of Tables

TABLE 2-1 A summary of surveys: elements of cost . . . . . . . . . . . . . . . . . . . . . . . . . . 50

TABLE 2-2 [Period 1](Product unit data) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

TABLE 2-3 [Period 2](Product unit data) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

TABLE 2-4 [Period 3](Product unit data) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

TABLE 2-5 Comparison between MAS and ABC overhead allocations . . . . . . . . . . . . 89

TABLE 2-6 Regression result of Total Overhead on Direct Labour Costs . . . . . . . . . . 91

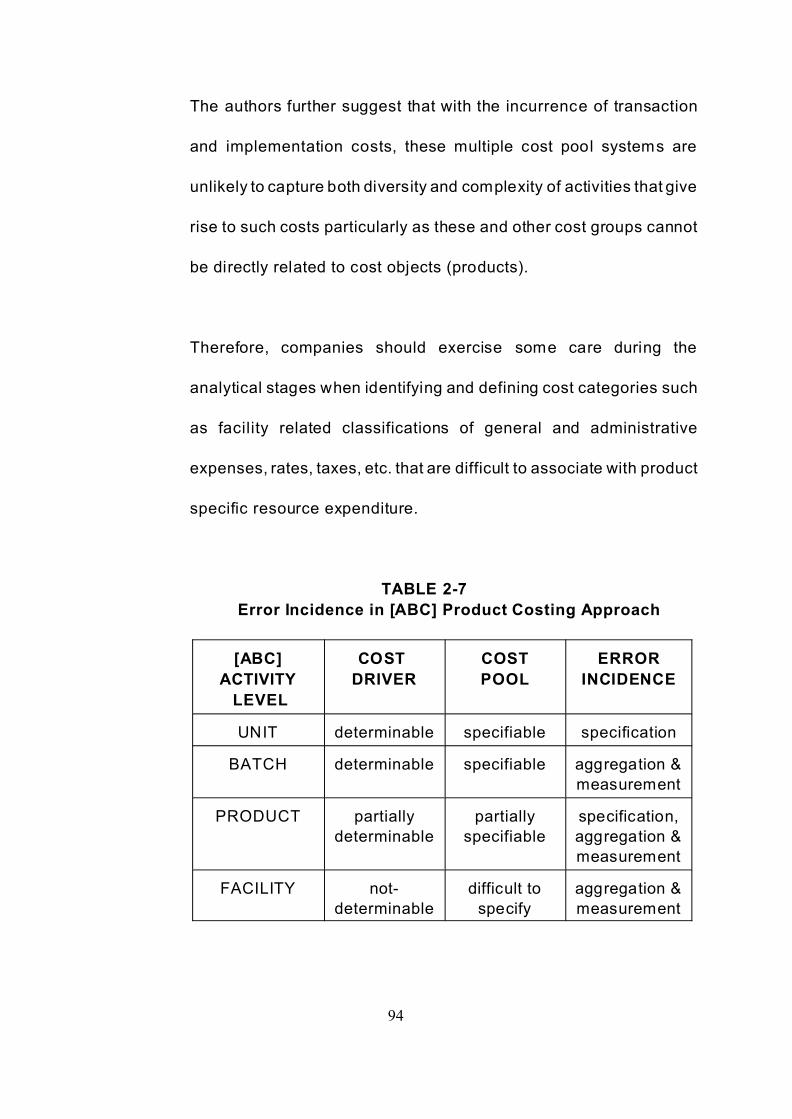

TABLE 2-7 Error incidence in [abc] product costing approach . . . . . . . . . . . . . . . . . . . 94

TABLE 2-8 (Product data taken from Pattinson and Arendt (1994:61)) . . . . . . . . . . . 100

TABLE 2-9, Product data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

TABLE 2-9a Product cost and contribution margin data . . . . . . . . . . . . . . . . . . . . . . . 106

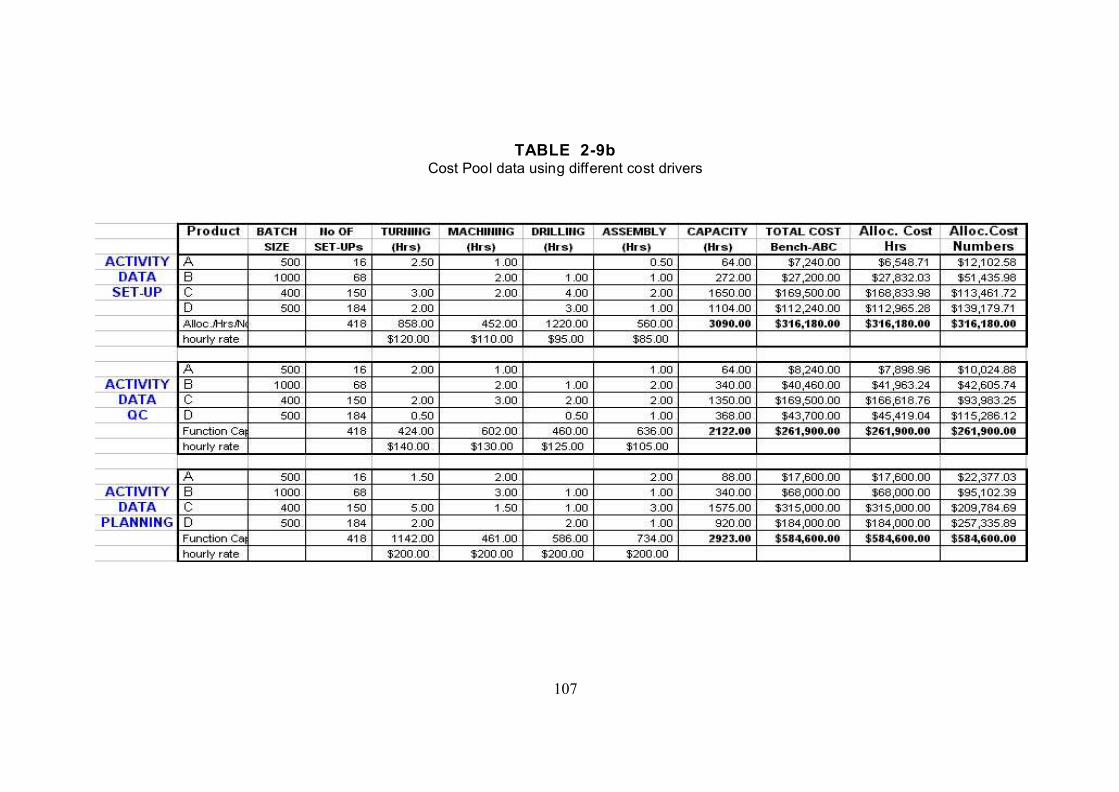

TABLE 2-9b Cost Pool data using different cost drivers . . . . . . . . . . . . . . . . . . . . . . . 107

TABLE 2-10 Example (Set-up cost pool) of individual product activity cost calculations 108

TABLE 2- 11 Constraint Equations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109

TABLE 2- 12 Results report of LP analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

TABLE 2-13 Profitability under varying product mix selections . . . . . . . . . . . . . . . . . 113

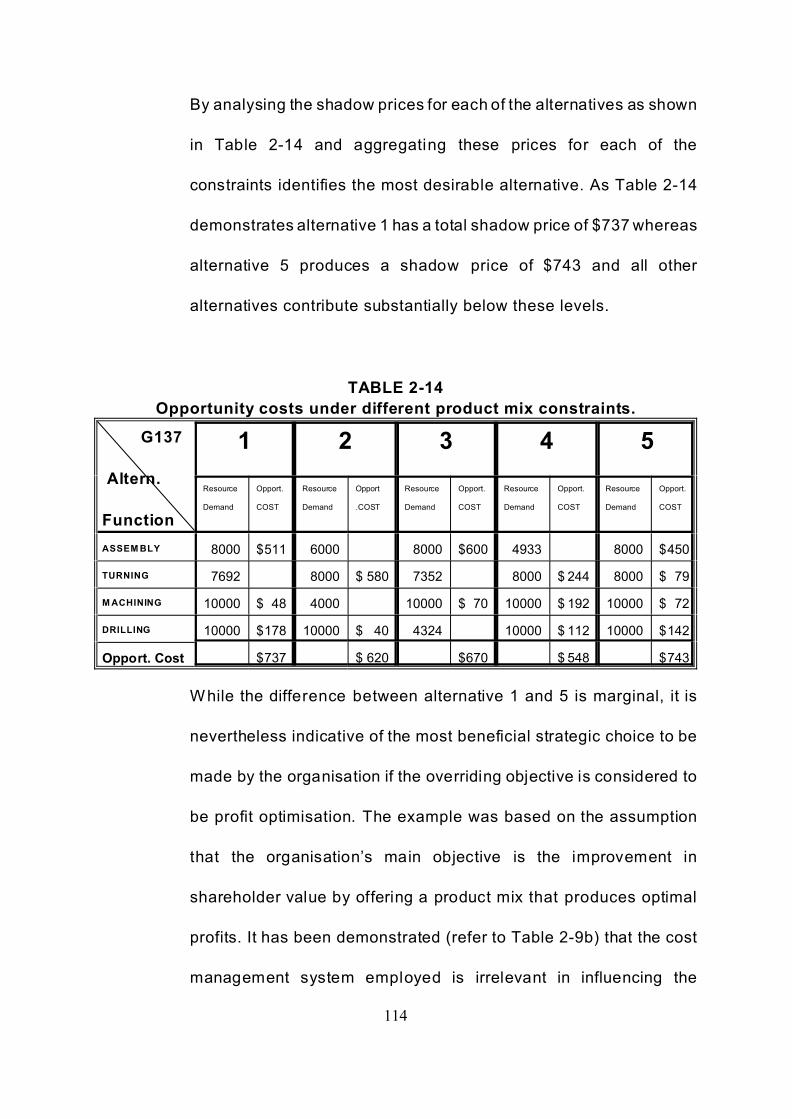

TABLE 2-14 Opportunity costs under different product mix constraints. . . . . . . . . . . . 114

TABLE 3-1 Results of ANOVA for data distribution of 8 (500 items) data bases . . . 135

TABLE 3-2 Results of ANOVA for data distribution of 8 (1000 items) data bases . . 136

TABLE 3-3 Results of ANOVA for data distribution of 8 (2500 items) data bases . . . 137

TABLE 3-4 Results of ANOVA for data distribution of 8 (4000 items) data bases . . 138

TABLE 3-5 Error data for Incremental and Point Differences . . . . . . . . . . . . . . . . . . . . . .141

TABLE 3-6 Results of ANOVA for data distribution of 5 random selected data

bases from the 500, 1000, 2500 and 4000 items data bases

with varied parameters for price, demand and shape factor. . . . . . . . . . . 149

TABLE 4-1, Results of ANOVA for Australian Share data("=.05) . . . . . . . . . . . . . . . . 155

TABLE 4-1a F-test for daily transactions/model values("=.05) . . . . . . . . . . . . . . . . . . 155

TABLE 4-3 (University 13) Results of ANOVA for 5 year DEST data ("=.05) . . . . . . 158

TABLE 4-4 (University 13) F-test for yearly enrolment records/model values (("=.05) 158

TABLE 4-5 ANOVA for each of the 12 universities’ 5 year students enrolment records160

TABLE 4-6 (University 1) F-test for yearly enrolment records/model values (("=.05) 161

TABLE 4-7 (University 2) F-test for yearly enrolment records/model values (("=.05) 161

TABLE 4-8 (University 3) F-test for yearly enrolment records/model values (("=.05) 161

8

TABLE 4-9 (University 4) F-test for yearly enrolment records/model values (("=.05) 161

TABLE 4-10 (University 5) F-test for yearly enrolment records/model values (("=.05) 162

TABLE 4-11 (University 6) F-test for yearly enrolment records/model values (("=.05) 162

TABLE 4-12 (University 7) F-test for yearly enrolment records/model values (("=.05) 162

TABLE 4-13 (University 8) F-test for yearly enrolment records/model values (("=.05) 162

TABLE 4-14 (University 9) F-test for yearly enrolment records/model values (("=.05) 163

TABLE 4-15 (University 10) F-test for yearly enrolment records/model values (("=.05) 163

TABLE 4-16 (University 11) F-test for yearly enrolment records/model values (("=.05) 163

TABLE 4-17 (University 12) F-test for yearly enrolment records/model values (("=.05) 163

TABLE 4-18 Results of ANOVA for Inventory data("=.05). . . . . . . . . .. . . . . . . . . . . . . . . . .167

TABLE 4-18a F-test for Model/Inventory("=.05) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

TABLE 4-19 Model parameters for Case study data . . . . . . . . . . . . . . . . . . . . . . . . . . 169

TABLE 4-20 Cost Allocation Variances (Actual v Confidence Limits) . . . . . . . . . . . . 171

9

List of Figures

FIGURE 1-1 Fechner’s Strategic Management Accounting Framework . . . . . . . . . . . . . 27

FIGURE 1-2 Framework for Thesis Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

FIGURE 2-1 Percentage changes of Material, Labour and Overhead costs over

3 periods for Product A, Products B, C and D show similar trends basis. 56

FIGURE 2-2, Percentage changes of Material, Labour and Overhead costs over

3 periods for Product A as proportion of the selling price; Products B, C

and D show similar trends basis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

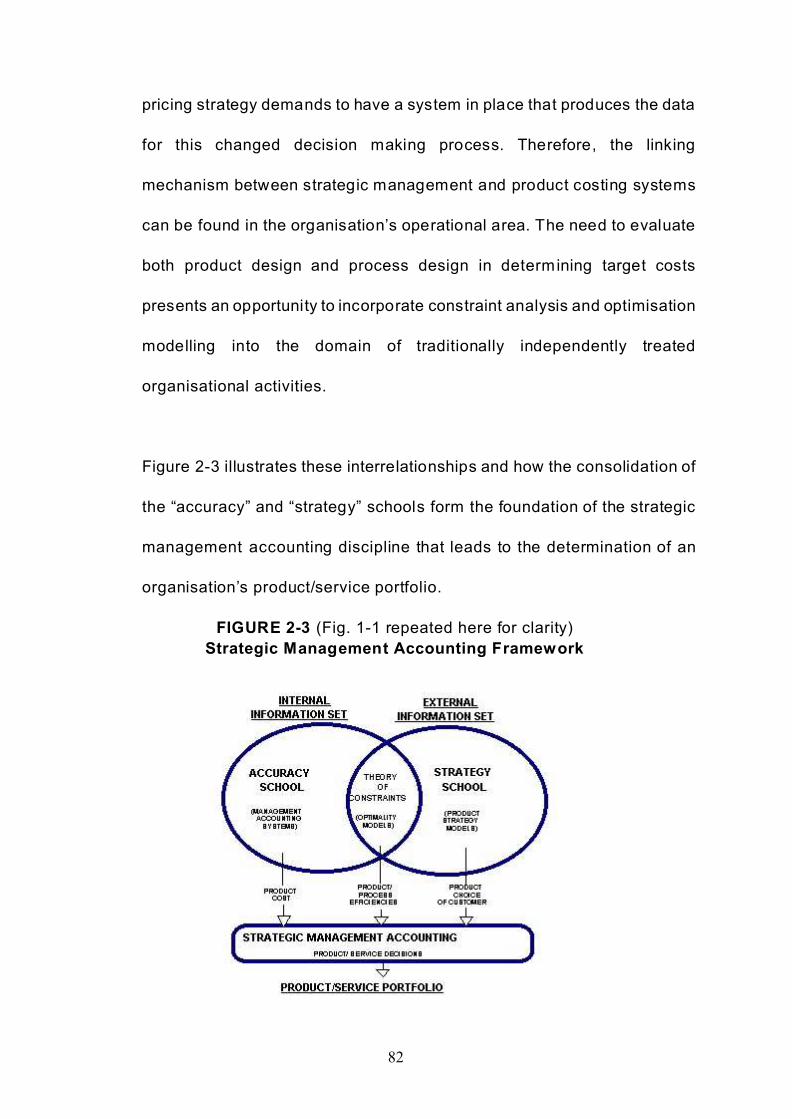

FIGURE 2-3 (Fig. 1-1 repeated here for clarity) Strategic Management Accounting

Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

FIGURE 2-4 Pareto Frontier, sorted by Direct Labour Hours . . . . . . . . . . . . . . . . . . . . . 85

FIGURE 2-5 Product over/under overhead distribution for the JDCW data . . . . . . . . . . 87

FIGURE 2-6 ABC compared to Traditional MAS Product Cost Portfolio . . . . . . . . . . . 101

FIGURE 2-7 Activity Cost Variation [Benchmark - ABC] . . . . . . . . . . . . . . . . . . . . . . . 110

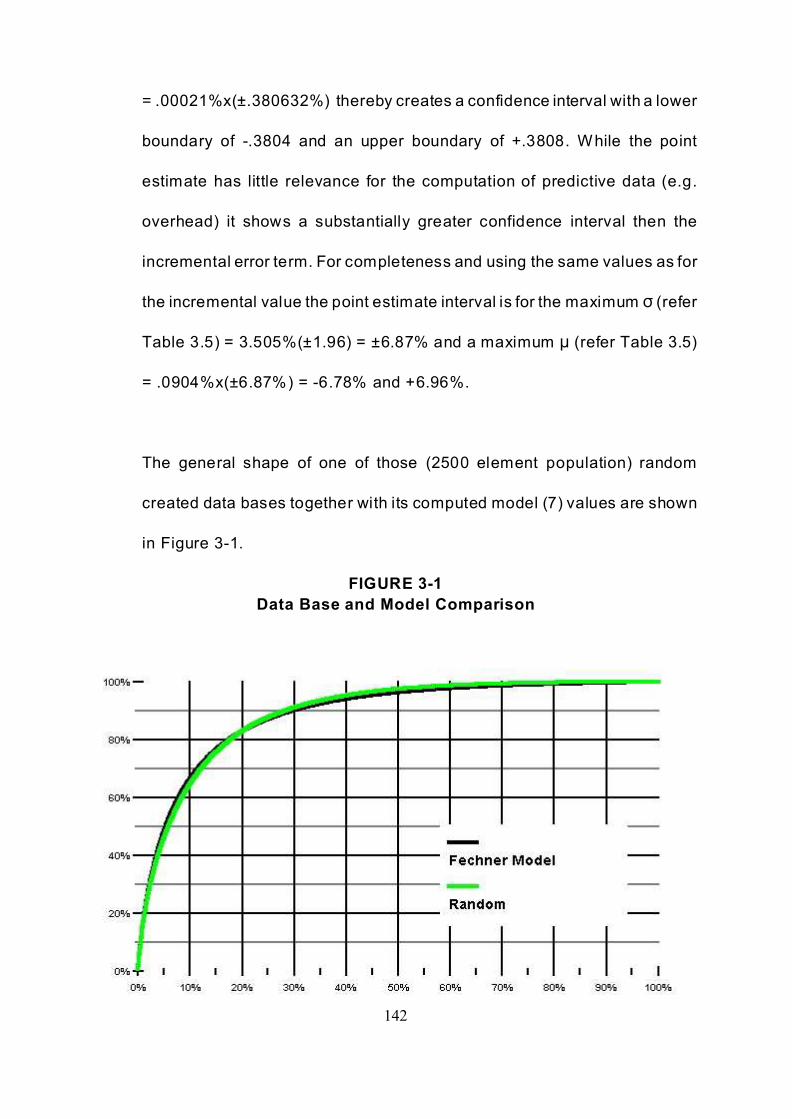

FIGURE 3-1 Data Base and Model Comparison . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

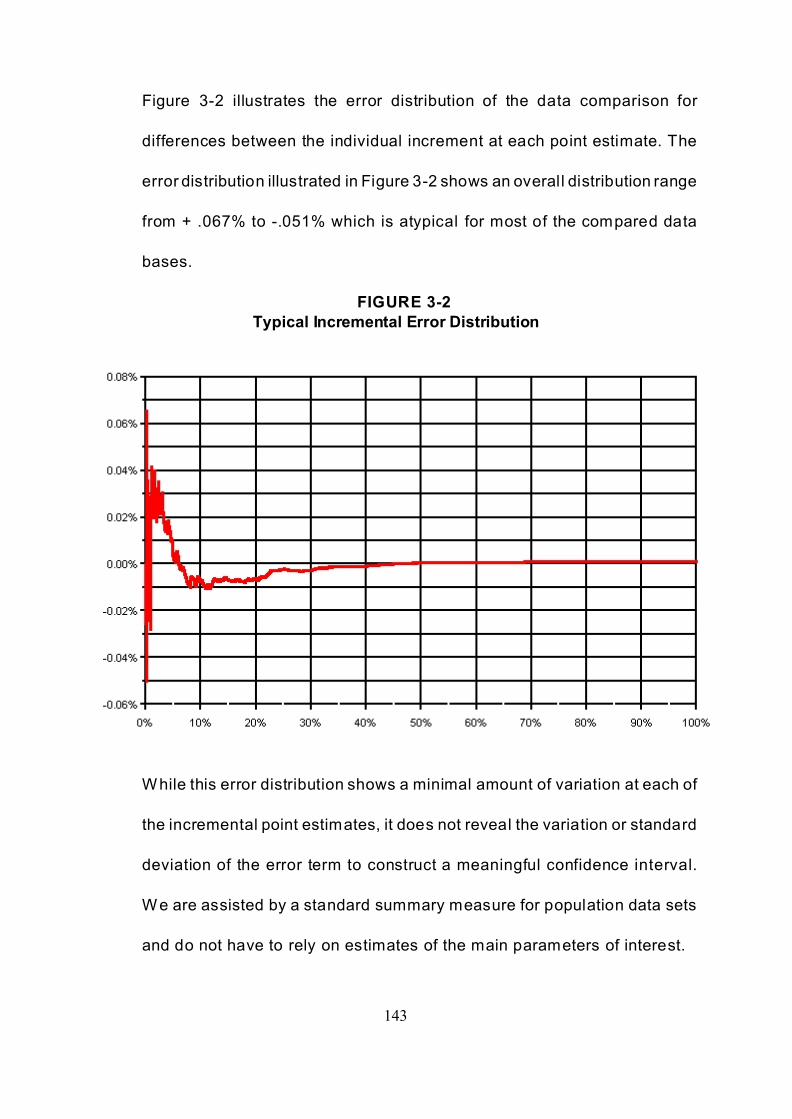

FIGURE 3-2 Typical Incremental Error Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

FIGURE 3-3 Error Distribution of Point Estimates . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

10

Abstract

Interest in more accurate assignment of overhead costs to establish credible

product/service cost profiles has assumed substantial prominence in much of the

recent debates on management accounting practices. While the promotion of

“new” cost management systems and in particular Activity Based Costing [ABC]

has promised to address many of the perceived shortcomings of more traditional

and long established techniques, the lack of its implementation success raises

some concern as to the validity and value of these “new” system designs.

Survey evidence from a number of different sources involving the evaluation of

past and current practices seem to identify the continued usage and application

of traditional cost management techniques and furthermore support a preference

by management to rely on simplistic allocation models for overhead cost

assignments. An often criticised limitation of the traditional absorption cost

system, the most popular in the survey findings, has been its reliance on a single

volume based cost driver (mostly Direct Labour Hours, DLH) for allocating

overhead costs. As organizations increasingly have employed advanced

technologies in many of their operational domains, DLH may no longer represent

a sound proxy for these allocations.

A major purpose of this thesis is the development of a mathematical model that

is capable of computing overhead allocations on the basis of organisational

11

specific dimensions other than DLH. While almost all data bases suffer from data

entry and omission errors, the information content contained in the data bases

often forms the basis for management decisions without first confirming the

accuracy of the data base content. The model has been successfully applied and

tested to detect internal consistency and data element detail accuracy. A total of

3200 random number generated data bases with varying number of elements as

well as characteristics that typify general inventory data base records were tested

and statistically evaluated to confirm the validity of the model. It was found to be

robust under all the subjected varying parameters and therefore able to detect

domain consistencies and data element inconsistencies.

Future research may test the applicability of the model with more diverse data

bases to confirm its generalisability as an investigative as well as predictive

model.

12

Executive Summary

This thesis has developed a mathematical model that mirrors the general pareto

or unbalanced distribution of data base elements given pre-specified element

parameters. To test the model’s robustness, standard statistical analysis (ANOVA

and F-test) of comparing paired elements between random number generated

data and model computed data, as well as incremental data comparisons

revealed non significant outcomes, thereby confirming the validity of the model to

detect data base inconsistencies.

Data mining of existing data bases revealed pattern consistency over a number

of periods that allowed the application of the model to detect data base integrity

or domain consistency (data belonging to the same organisation over a number

of periods) and data element accuracy (empirical evidence identified the

existence of data element errors through inaccurate entry or omissions) by

comparing the existing data base elements with the model generated data.

A further contribution of the thesis is the application of the model to identify data

base errors in an organisation’s inventory and production records and applying the

model’s generated values for the allocation of overhead costs. This concept of

overhead allocations parallels the simplicity of the traditional absorption technique

but increases the accuracy of the allocation method. This application is not limited

to manufacturing organisations but can be equally well applied to service

organisations.

13

Overhead allocations have consistently been criticised as arbitrary, incorrigible

and misleading in determining accurate product costs. Literature evidence, both

article and textbook based, often presents examples in which the overhead cost

component exceeds 45% of total product costs. Under these circumstances, any

different method (new?) of overhead allocations (assignment, distribution)

produces convincing results for consideration of such new methods, e.g ABC

costing methods. Surprisingly, a number of recent surveys of manufacturing

industries in different countries found that the average proportion of both

manufacturing and non-manufacturing overheads combined is around 30% (Drury

and Tayles, 1994; Joyce and Blaney, 1990; Dean et at., 1991). At this level, the

perceived benefit from a "more accurate" cost assignment method is substantially

reduced, which might explain that reported survey results on the subject of

overhead allocations often find no significant modifications to existing

Management Accounting System [MAS] practices.

While the debate about alternative management accounting systems remains a

contemporary issue amongst academics and practitioners alike, the most popular

of the suggested alternatives, Activity Based Costing [ABC], has had only limited

success when compared with the continued application of traditional MAS

techniques (Shim and Sudit, 1995). Survey results on the adoption and

implementation of ABC indicate that, in countries like the US, UK, Canada,

Australia, Japan and some European countries, the acceptance/implementation

14

rate varies between 6% and 12% across the industry spectrum (Cobb et al.,1993;

Cooper et al, 1988; Drury and Tayles, 1994; Dean et al., 1991; Fechner, 1995;

Armitage and Nicholson, 1993).

A persistent problem mentioned in the literature on ABC implementation is the

substantial cost involved in maintaining the system apart from the initial costs of

implementation. Other comments have questioned the benefits of more “accurate”

product costs as some of the overhead allocation problems remain and require

similar subjective judgmental allocations as experienced in traditional MAS

(Kaplan, 1994a).

Furthermore, anecdotal evidence and testimonials question the benefit of a

system replacement that is difficult to assess as to its final value. In addition the

initial operational analysis as to the totality of all value adding activities and the

determination of appropriate cost drivers presents many managements with

system complexities that are difficult to conceptualise as to the overall

improvements that can be achieved. This overwhelming complexity of the

activity/cost driver matrix and the extent of the organisation’s product range are

recurring comments throughout much of the related literature in identifying the

reluctance by management to implement an ABC system.

15

The premise of any of the proposed “new” systems is that the organisation will

benefit from better decision support systems and thereby ultimately improve

profitability. Although this premise is defensible, its validation can only be

supported if the organisation’s current operations are well within its existing

resource capacities. To demonstrate this proposition, an example of capacity

(operational) constraints for a given product mix is submitted to optimisation

analysis (Theory of Constraints). This example tests the usefulness of a number

of alternative overhead cost allocation systems to provide evidence for the

indifference that any of these systems offer in determining an organisation’s

optimal profitability.

Most of the operational analyses that precede the evaluation and subsequent

implementation relies on an organisation’s existing data bases. However, there

also seems to be a reliance on data base integrity without the necessary

verification for such assumption. One of the discernible characteristics of almost

all data bases is their unbalanced distribution of element items when ranked on

the basis of two dimensions of interest.

Alfredo Pareto was the first scholar to recognise such relationships and since his

introduction of this phenomenon subsequent writings on the subject have referred

to it as the Pareto principle or the 80/20 rule. A well known application of the

80/20 rule within the accounting domain is the A-B-C classification employed in

16

inventory control system design. Identifying products on the basis of their

individual value in relation to the total value of inventories provides a sound

approach for determining the resources to be expanded in controlling a major

asset in most organisations. An extension to this product classification as to the

individual product value within the total product portfolio would be to analyse if the

product cost profiles follow a similar distribution with particular emphasis on the

overhead proportion. While it is hypothesised that the resource consumption of

products parallels this of the inventory classification ranking, normal statistical

analysis is applied to support such conjecture.

Chapter 3 covers the major contribution of this thesis. The development of a

mathematical model to determine the exact 80/20 relationship (or any other

combination) on the basis of the total number of products. Such a computational

model provides the analyst (management accountant) with a tool to determine the

individual product contributions and thereby assists in establishing a hypothetical

benchmark for resource comparison. Although such a model is useful in

determining the hypothetical resource allocations, and therefore a benchmark, the

model does not, however, identify any existing inefficiencies in product or process

design. The model developed (as shown):

17

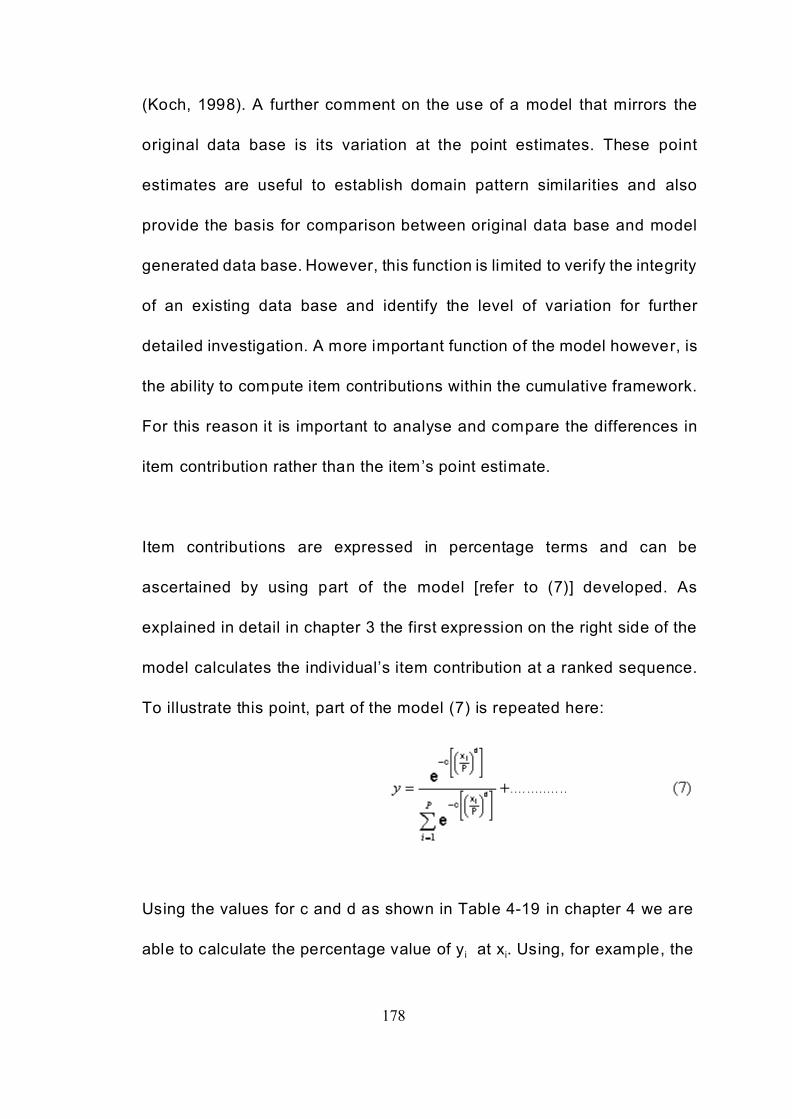

where P = total number of products in portfolioxi = ith product rank within portfolioyi cum = cumulative percentage of ith product contributionc = constant for a given data base.(xi/P)d = term that determines the shape parametere = base of natural logarithm (2.718281)

is capable of identifying existing data base inaccuracies that indicate domain

consistency and data item inconsistencies, therefore providing a sound basis for

data element attribute predictions. As the interest of the thesis is in comparing the

usefulness of existing overhead allocations methods, the model will be applied in

computing overhead allocations based on its pair wise comparison with the actual

data of an organisation’s inventory and production records. The benefit provided

by such overhead allocation method, is its application simplicity as well as the

accepted - but criticised - absorption costing method.

In chapter 4, three specific data bases (case studies) have been selected for their

perceived data integrity and to test the robustness of the model against actual,

rather than random number generated, data bases. Statistical analysis establishes

the accuracy of data element attributes as well as identifying domain

consistencies. While the outcome of the analysis was hypothesised, the results

were still somewhat surprising.

18

Stock Exchange daily transaction data should be audited prior to its release into

the public arena and therefore display a high level of data accuracy. The data

contained inaccuracies that were explained by the providers of the data records

as rounding applications of nonmarketable securities.

Australian university data of student enrolments on the other hand is often

presented unaudited to governmental funding authorities and thereby invites

suspicion as to the accuracy of the data recorded. Again data analysis revealed

both domain inconsistencies and data item inaccuracies.

The third case study is a current research study in which the organisation is

preparing to implement an ABC system that has been imposed by its European

based parent company. Many of the pre-requites of system change over were not

well understood by the operations personnel and the existing system has no

separate overhead classification but a rather inappropriate single conversion cost

distribution by cost centre. The application of the developed model identified

existing data base inaccuracies and provided operations management of the

organisation with evidence of data entry and omission errors for investigation and

correction where appropriate.

Chapter 5 discusses in detail the analysis of error terms from the 3200 random

number generated data bases its implications and application to the inventory and

19

production data base. It further provides application specific statistical error term

calculations that are necessary for the computation of data element parameters.

The final chapter provides a summary and direction for future research in the area

of model extension and resource efficiency improvements.

19

1. The Study Relevance to the Discipline

1.1 Introduction

Early research investigating the effect of technology on organisational

design suggested that organisational structure will experience modifications

with the implementation and use of technologies (Woodward, 1965;

Perrow, 1967; Thompson,1967; Duncan, 1972). However, to modify and

then maintain those structures, control systems have to be designed to

achieve these objectives. The realisation of the existence of organisational

design interdependencies lead to the development of contingency theory

(Gordon and Miller, 1975; Hayes, 1983; Waterhouse and Tiessen, 1978).

Organisational theorists embraced this new framework as it had the

promise of explaining a large number of organisational variables and their

interdependencies.

From the basis of the contingency model a number of diverse studies were

conducted to support the hypothesised relationships between selected

variables. Technology, as one of the organisational variables of interest in

explaining organisational design changes, became a credible explanation

for the operations structural changes and the need to match control system

design with the new operational environment (Daft and Mclntosh, 1978;

Merchant, 1984; Mclntosh and Daft, 1987). The latter aspect has created

a substantial body of research with divided opinions about the relevance of

20

management accounting systems in these new Advanced Manufacturing

Technologies [AMT] production environments (Kaplan, 1983, 1986b;

Johnson and Kaplan, 1987). There is, however, an equally substantial body

of research that argues in favour of retaining the traditional management

accounting techniques in modified forms to match the organisation’s

information needs (Drucker, 1990).

Traditional management accounting practices have received increasing

attention from accounting academics who question the relevance of these

traditional practices in an environment of expanding advanced technology

based production. Kaplan (1983, 1984, 1986a,1988, Johnson and Kaplan,

1987) has become the most prominent and vociferous critique of the

management accounting irrelevance movement. His contention is largely

based on anecdotal and case study testimonials, suggesting that, with the

advent of large scale adaptation of Advanced Manufacturing Technologies

by manufacturing industries, the function of traditional Management

Accounting Systems [MAS] as a tool for planning and control is no longer

defensible. He attributes this diminished functional role of MAS to the lack

of perceived independence from the financial accounting function.

This argument has some credibility, especially if the origin and

development of many of the currently practiced management accounting

21

techniques can historically be traced to the scientific management era. It

was in this environment that production engineers developed most of our

contemporary management accounting techniques (Kaplan, 1986a).

Therefore, it appears to be quite reasonable to again consult with

production engineers and planners to gain a better understanding of what

type of operational measurement requirements are needed in an AMT

environment. Management accountants thereby have some obligation to

become more familiar with production operations to develop appropriate

modifications to existing MAS.

The adoption and implementation of AMTs by organisations are driven by

the organisation's desire to gain or maintain a competi tive advantage

whereby consumer needs of constant high quality products or services at

competitive prices become the motivating objective. To meet this dual but

previously sought to be mutually exclusive criteria, firms have concentrated

on cost reductions often in the areas of direct and indirect labour costs. The

product cost profile of organisations who have implemented some form of

AMT should therefore indicate a shift in the components of the product cost

profile. Furthermore, recent surveys (Drury and Tayles, 1994; Joyce and

Blaney, 1990) have indicated that differences in product cost components

between various industry groups exist.

22

Such differences may also be indicative of the treatment of product cost

determinations within different industries and provide some information on

the overhead allocation methods applied. Overhead allocations have

consistently been criticised as arbitrary, incorrigible (Thomas, 1975) and

misleading in determining accurate product costs. Surprisingly, a number

of recent surveys of manufacturing industries in different countries found

that the average proportion of both manufacturing and non-manufacturing

overheads combined is less than 30% (W hittle, 2000; Drury and Tayles,

1994; Joyce and Blaney, 1990, Dean et al., 1991). At this level, the

perceived benefits from a "more accurate" cost allocation method are

substantially reduced, which might explain that reported survey results on

the subject of overhead allocations often find no significant modifications

to existing MAS practices.

However, if the overhead component constitutes only some 30% of the total

product costs, given the evidence of recent surveys, the question arises at

what level of overhead proportion will the traditional allocation methods

become questionable and jeopardise the value of information that is

conveyed to management for product related decision making. Literature

evidence, both article and textbook based, often presents examples in

which the overhead cost component exceeds 45% of total product costs.

Under these circumstances a different method of overhead allocations

23

produces convincing results for consideration of such new methods, e.g

ABC costing methods. Activity-based-cost [ABC] overhead allocations, a

method popularised by academics and consultants as an alternative to

traditionally based allocations methods, lacks the universality of application

as it depends largely on product diversity and product level overhead cost

pools (Cooper, 1988).

It is encouraging to note the recent change in management accounting

thought toward strategic cost management. This relatively new approach

to the traditional management accounting practices provides a desired

integrative framework for linking management accounting, operations

management and strategic management to create a cohesive group of

functional activities. W ithin this framework, technology is regarded as a

consequence of strategic choices and management accounting systems

are tools that aid in the implementation of those strategies (Govindarajan

and Shank, 1990).

Strategic management accounting [SMA], is a relatively new development

in understanding the relationships that dominate organisational design and

its maintenance mechanisms through the appropriate application of

internal control systems. It has been advanced as the natural progression

of earlier contingency theory prescriptions. While the underlying

24

assumptions of this approach are not new, the framework does however,

recognise the functional interrelationships of strategic management,

operations management and management accounting (Govindarajan and

Shank, 1990). It further identifies the relative importance of product life

cycle [PLC] analysis as a linking mechanism between strategic choice and

supporting management accounting system designs.

Much of the MAS irrelevance debate (Kaplan, 1983, 1986b, 1988; Johnson

and Kaplan, 1987) has been concentrating on the lack of modification to the

traditional management accounting practices in organisations after the

implementation of some form of an AMT. The main arguments are based

on the presumption that AMTs tend to reduce the direct labour content as

a proportion of total product costs and at the same time substantially

increase the proportion of manufacturing overheads. The allocations of the

presumed increased overheads on traditional based labour costs as well

as capacity volume related distributions are considered to provide

inaccurate cost data for product related decisions (make v buy, retain or

abandon, product mix, etc.) and it is argued that for these reasons they

have lost their relevance as a management decision support system.

As Kawada and Johnson (1993) point out the difference between the

”accuracy school” represented by ABC advocates and strategic

25

management accounting is the emphasis each of these “schools” attach to

organisational issues.

Whereas the accuracy movement stresses that the internal product cost

accuracy leads to improved profitability, the strategic movement stresses

that the analysis of the external environment mandates corrections and

adjustments to the internal control system structures and decision support

systems. Both movements, however, tend to agree that the traditional

financial based cost management system is no longer appropriate for either

task.

To provide a clearer example of the differences in the way of thinking these

schools represent can best be demonstrated by the product/services

related questions they address. The ABC school (internal focus)

emphasises improved profits through accurate product/service costing

while the strategists (external focus) are preoccupied with the question of

what products the company should produce.

The relevance of either emphasis may be revealed by the strategic stance

the company adopts with regard to cost leadership or product/service

differentiation. Therefore, accepting that both schools of thought have a

valuable contribution to make to the survival and growth of organisations

26

requires the development of techniques that combine the assessment of

product cost profile accuracy with the evaluation of product desirability and

viability. The literature in general has treated each of these emerging

issues as separate and distinct paradigms with specific contributions to the

overall functioning of organisations. However, there seems to be a

considerable commonality between these issues and represents an

opportunity to develop a linkage that offers a synergy between them.

In a contemporary survey (Shields and McEwen, 1996) it was found that the

successful implementation of ABC, amongst other factors, is dependent on

linking it to the “company’s competitive strategy regarding organizational

design, new product development, product mix and pricing and technology”

(p.18). However, while the authors offered a number of examples where

such a linkage would be beneficial, there was no suggestion as to the

concept or operational technique that would promote such

interdependence. A common thread that links all company objectives is the

realisation that available resources are limited and that these limitations

impose resource constraints that require efficient management.

To evaluate the effect resource constraints impose on the optimisation of

the organisation’s objectives, a number of operations management

techniques have been available for some time, most prominent amongst

them is the Theory of Constraints (ToC).

27

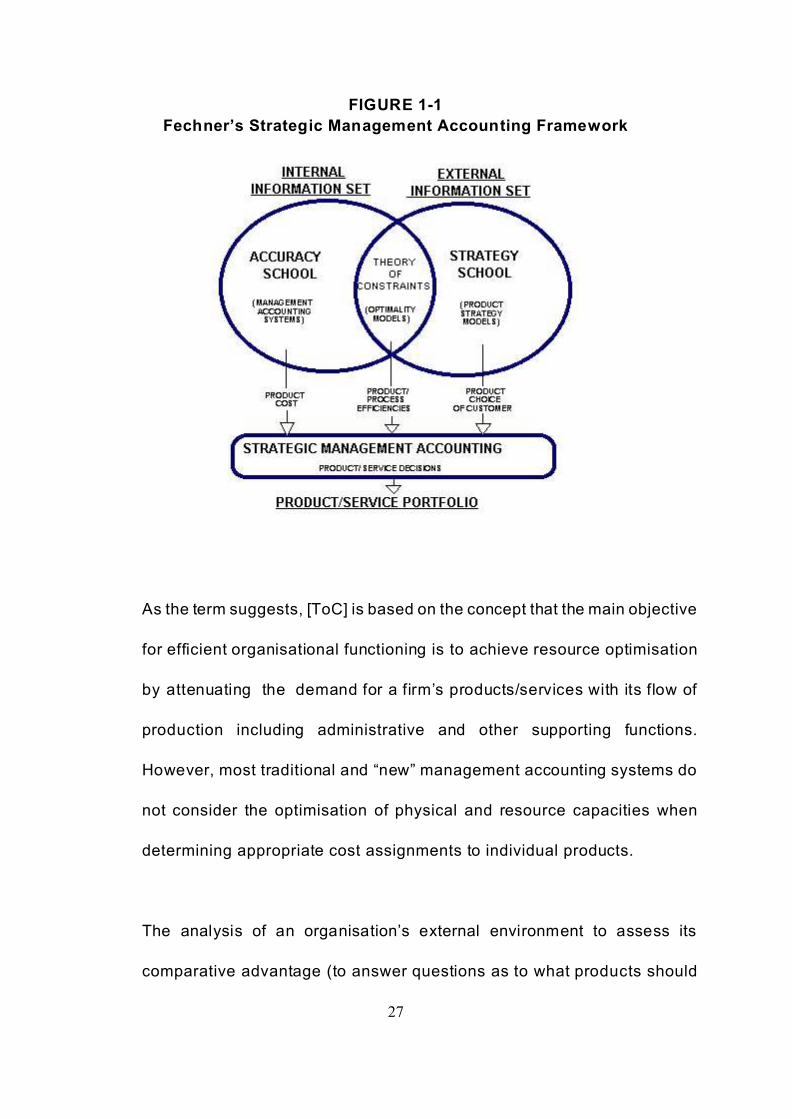

FIGURE 1-1

Fechner’s Strategic Management Accounting Framework

As the term suggests, [ToC] is based on the concept that the main objective

for efficient organisational functioning is to achieve resource optimisation

by attenuating the demand for a firm’s products/services with its flow of

production including administrative and other supporting functions.

However, most traditional and “new” management accounting systems do

not consider the optimisation of physical and resource capacities when

determining appropriate cost assignments to individual products.

The analysis of an organisation’s external environment to assess its

comparative advantage (to answer questions as to what products should

28

be produced) must be linked to the organisation’s capacity to produce these

products efficiently and within the expected cost boundaries. Figure 1-1

illustrates these interrelationships and how the consolidation of the

“accuracy” and “strategy” schools form the foundation of the strategic

management accounting discipline that leads to the determination of an

organisation’s product/service portfolio.

The determination of an organisation’s optimal product/service mix requires

the utilisation of optimality models. Most common amongst these are

Linear [LP] and Mixed Integer programming [MIP] applications. For a more

detailed discussion refer to Kee and Schmidt (2000). Although, the TOC is

sometimes criticised for relying on deterministic assumptions and thereby

reducing its value in predicting product mix compositions, stochastic

models are less appropriate as “production related activities are

deterministic in nature” (Kee and Schmidt 2000:5). The authors further

suggest that neither the ABC model nor the TOC model will be able to

compute an optimal product mix when both labour and overhead costs are

of a discretionary nature but that their general model (Mixed Integer

Programming, MIP) computes an optimal product mix.

This analysis provides an opportunity to discover that profit optimisation is

dependent on capacity utilisation and/or market demand constraints which

29

illustrate that cost accounting systems of whatever design will have no

influence on the profitability outcome of the organisation (refer to Table 2.9,

2.9a, and 2.9b). Such results may help to explain the continued popularity

of traditional cost accounting techniques and the reluctance by

managements’ to implement contemporary systems such as Activity-Based

Costing.

This generalisation, however, needs to be moderated as it is difficult to

apply optimality models organisation wide and maybe restricted to the

analysis of functional units within the corporate framework.

Rather then suggesting that cost management systems are irrelevant when

determining an organizations profitability, the difficulty in implementing

optimality analysis corporate wide, refocuses the emphasis on cost

accounting systems capable of assigning or allocating overhead costs to

individual products/services on a credible basis.

1.2 Contribution of Research to the Discipline

Survey results (Drury and Tayles, 1994; Joyce and Blaney, 1990; Dean et

al., 1991; Fechner, 1995; Whittle, 2000) as well as a historical review

(Boer, 1994) clearly indicate that overhead cost proportions within a

product’s cost profile have not substantially changed over time and

30

organisations continue to prefer simplistic overhead allocation methods.

Although some of the evidence suggests that traditional allocation models

produce some inequitable overhead allocations within the organisation’s

total product portfolio it appears to be more appropriate to develop an

overhead allocation method that incorporates the changing environmental

circumstances but maintains the simplicity of an overall overhead allocation

method.

A major problem that has not been addressed by previous research is the

accuracy and integrity of organisational data bases that form the basis for

cost accumulation and subsequent cost allocations. Incomplete or

inaccurate cost accumulation pools may contribute to the claimed cost

distortions that have been identified in comparative cost management

system examples and case studies.

To address the dual problems of data base integrity and more equitable

overhead cost allocations this thesis will adopt a data mining technique to

identify data patterns within random number generated data bases from

which a predictive model can be developed. This model will then be tested

for its robustness against publicly available stock exchange data,

Australian university student enrolment records and company data bases.

Statistical tests to evaluate the model parameters against the actual data

will be applied to confirm its predictive value in determining overhead cost

allocations.

31

1.3 Research Objectives

This thesis will:

- develop a robust model for the allocation of overheads that is

based on the historical data pattern of the company’s

inventory and production records.

- analyse and test the commonal ity of data base patterns to

confirm the empirical evidence as to the existence of the

Pareto distribution - or 80/20 rule - in a number data bases.

- develop a mathematical model that mirrors the data

distribution of Pareto ranked cumulative element

arrangements to test its robustness under varying parameters.

To test such robustness standard statistical analysis of paired

element comparisons (Anova and F-test) as well as error term

analysis for incremental values and point estimates will be

conducted.

- identify data base integrity and data accuracy (as empirical

evidence suggests that almost all data bases contain data

element errors through inaccurate entry and omissions) by

comparing the initial data base with the model generated data

base for pattern consistency.

While the model will have universal applicability its parameters need to be

determined on the data pattern history of the individual organisation. By

32

accepting that each data base will have its unique pattern, it is

hypothesised that the data pattern within a given domain (organisation) will

display pattern consistency while such consistency is not expected across

different domains even within the same industry grouping.

If such findings are revealed by the analysis then a further benefit from the

model would be its ability to detect pattern inconsistencies within a domain

as unexpected and alert appropriate management levels to the possibility

of data errors and inaccuracies.

Once the data base integrity of a domain has been established, the model

will be applied to compute individual product overhead cost allocations on

the basis of the ranked data base element distribution of pre-specified

product attributes. Such pre-specified product attributes could include

product demand, material consumption and resource consumption amongst

others.

33

1.4. Research Methodology and Methods

Most data bases display nonlinear relationships between any dual content

data items of interest. Steindl (1965:18) recognised this fact and stated that

“for a very long time, the Pareto law [ the 80/20 principle] has lumbered the

economic scene like an erratic block on the landscape; an empirical law

which nobody can explain.” While this observation in itself does not provide

any new insights into the existence of such phenomenon, it does, however,

provide an opportunity to quantify through mathematical modelling the

individual data item contribution to the distinctive shape of the cumulative

distribution curve.

The application of the Pareto principle relies on the availability of a data

base that constitutes the population of data items of interest. Ranking of

items on the basis of two dimensions of interest will produce a typical

Pareto distribution. The development of a model that can mirror the Pareto

frontier produced by the ranking of data items, will allow the application of

such a model as a prediction tool of the items of interest. The purpose of

this thesis is to use mathematical modelling techniques to develop such a

model and apply it in the prediction of overhead costs for a company’s

product portfolio.

34

The development of the model required the testing of the specified model

parameters against a substantial number of data bases to ensure that it has

the robustness required to become a credible prediction tool.

The initial database testing will use a substantial number of random number

generated data bases with different data item populations. These data

bases will contain typical product cost characteristics where each of the

cost components of material, direct labour and overhead allocations are

randomly varied. To accomplish this task, a standard spreadsheet

application (Quattro Pro in this case) will be employed which has the

desired random number generator function to establish the database

combinations. Although there is no relevant literature to provide guidance

as to the population size required for mathematical modelling, a reasonable

population size that mirrors average inventory holdings of manufacturing

organisations in the range from 500, 1000, 2500 and 4000 items would

appear to be adequate. For each of the populations 100 random number

generated data bases ( a total of 3200 populations) will be compared with

the developed model to establish a statistically adequate sample size. To

further improve on the robustness of the model, an error term (deviation

between model computed values and database values) of +/- 5% in the fat

tail region of the distribution is considered appropriate. This level is

suggested as an acceptable error term as most standard statistical tests of

significance are set at a 5% level for model prediction validity.

35

The model will be tested against each random generated data base to

calculate the error term of its parameters against the item values of the

data base. A paired comparison using single ANOVA statistics together

with a standard F test will be used to establish the validity of the model

parameters.

1.4.1 Mathematical techniques employed for the model development

For the development and application of the model a number of

mathematical techniques were used to establish data base pattern

consistency as well as the analytical evaluation of existing overhead

assignment techniques. To establish the existence of a generalised Pareto

distribution (GPD) as suggested by Koch (1998) existing data bases need

to be investigated for pattern similarities in a data mining approach.

Data mining in the context of this thesis refers to the investigation of

appropriate existing data bases (populations), given some pre-determined

parameters or element characteristics, to identify data element patterns that

confirm the general accepted but anecdotal evidence of the Pareto principal

or unbalanced distribution.

The Pareto principal or unbalanced distribution should not confused with

the theoretical Pareto optimality concept. Pareto optimality is achieved

36

when the distribution of goods/services falls on the contract curve in a

modeled Edgeworth-Box diagram and represents the condition of optimal

resource/commodity/welfare distribution. The exchange of goods/services

beyond a point on the contract curve leads one consumer to be worth of in

his (her) indifference towards a bundle of goods/services. Although the

concept can also be applied to the production possibility frontier

hypothesis, it is not the purpose of this thesis to deal with the economic

rationale of Pareto optimality but instead introduces the concept of Pareto

efficiency in which a vital few and not the trivial many affect the output

condition of the firm.

Pareto’s original discovery of the wealth distribution in a certain population

followed a 20/80 pattern (20% of the population enjoyed 80% of the

wealth). Further investigation by Pareto (Koch, 1998:6) revealed that this

unbalanced distribution was repeated consistently over different

populations and different time periods. This repetition of the same pattern

followed an almost mathematical precision. While the generalised Pareto

distribution has been mathematically formalised, it is mostly applied in the

analysis of fat or thin tail distributions.

While the unbalanced distribution clearly identifies the existence of non

linear relationships between variables of interest another form of data

37

element analysis and prediction is based on the assumption of linear

relationships between data element variables. Linear programming as well

as linear regression analysis assumes linear relationships amongst the

variables of interest. A number of overhead allocation techniques have

been based on the concept of linear behaviour of variables in predicting

future outcomes and cost assignments.

Linear programming (LP) on the other hand tends to establish a optimal

solution to a given set of constraints within a given and pre-specified

environment. Resource utilisation and capacity analysis are two of the most

popular applications of LP. A more contemporary application of LP can be

found in the Theory of Constraints (ToC). Here the presumption exists that

in any operating environment a bottleneck situation can be found and

through its initial elimination other bottleneck situations are revealed for

further analysis and elimination. This step approach will ultimately lead to

a optimal solution that ensures operational efficiency. As the ToC assumes

linearity relationships some of its analysis are open to criticism. The

assumption of labour resources, as a capacity variable, behave linear has

been shown to be inaccurate as the learning curve concept was empirically

validated. However, the concept of LP is relevant in comparing a number

of different overhead assignment techniques to determine if any of these

techniques are superior in predicting optimal profitabilty of an organisation.

38

By comparing the outcome of the LP computations of the different overhead

assignment techniques, sensitivity analysis in the form of shadow price

differences provides a useful analytical tool.

Sensitivity analysis is a concept that ensures the testing of computational

outcomes by evaluating the results of a number of input variable changes.

This concept is a pre-requisite for any model development to determine the

robustness of the model’s predictive and analytical ability. Sensitivity

analysis is mostly based on statistical evaluation of the computed value

within pre-defined error limits.

39

Use of Model

derived data

Thesis Contribution Existing Applications

Data Entry

Keyboard Entry

Barcode

Electronic Data Transfer

Develop mathematical

Model for testing Data Audit (Sample testing)

base accuracy

Evaluate existing Comparison of

allocation models Contemporary

using optimisation Allocation Models

techniques

Compare Results.

Statistically evaluate results

of available Databases and

compute model-based data

element properties.

Apply to Overhead Allocations.

FIGURE 1-2

Framework for Thesis Structure

Establish

Databases

Testing Database

Accuracy

Modeling of

Database

Prediction (Forecasting) Modeling

Transfer to other Databases

Overhead Allocation Models

Use of partially

corrected data

Application of

Data

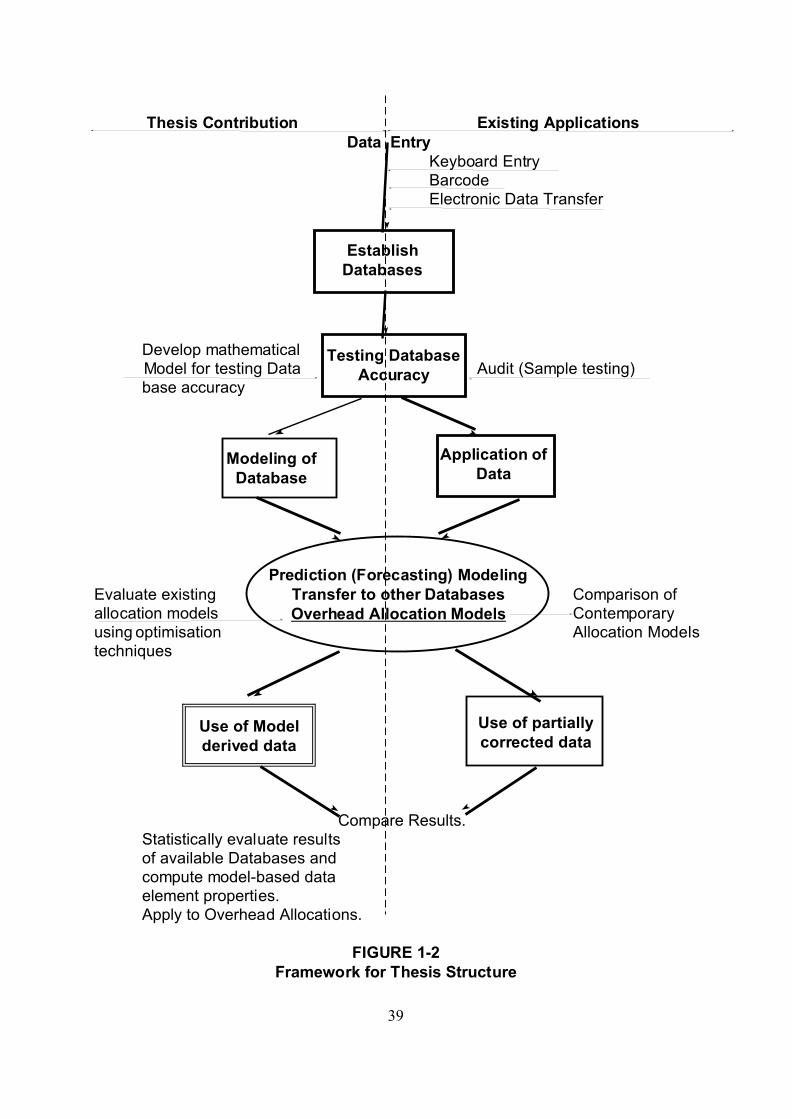

40

1.5 Structure of Thesis

The thesis comprises six chapters that follow a traditional development of

literature review, formulation of a hypothesis or in the case of this thesis the

development of a mathematical model that will be tested against existing

data bases to validate its robustness. A comparative analysis between the

computed model values and the existing data bases will be conducted and

the results are reported in a separate chapter. Finally, a summary of the

comparative analysis and recommendations for future research

applications of the model is presented. Figure 1-2 depicts a graphical

presentation of the thesis structure.

1.6 Definitions, Key Assumptions and Limitations.

Definitions

There are a number of terms introduced throughout the thesis that require

explanation and clarification. The major part of the thesis is devoted to the

development and testing of a mathematical model that enables users to

detect data base domain consistency and data base integrity by comparing

computed model values forming a Pareto frontier with the Pareto frontier

generated by the existing data base. Once these conditions are confirmed,

the model can be applied to allocate organisational overheads to products

or services to establish a credible cost profile and serve as a prediction

model for budget considerations and preparation.

41

A data base domain in the context of this thesis refers to the data base

composition of share trading records, university records and organisational

inventory records over a number of periods were each period’s data base

element ranking remains statistically similar. While only three different data

base groups were selected for analysis, empirical evidence (Koch, 1998)

suggests that the Pareto distribution (80/20 rule) can be applied to almost

any data base collection.

Statistically similar implies that the F and P values display insignificance,

thereby supporting the contention of domain consistency over successive

periods. However, inventory records from different organisations, share

trading records from different stock exchanges and student enrolment

records from different universities will have different Pareto frontier

characteristics and therefore can be identified as not belonging to the

domain of interest. An example, two university enrolment data base records

would show statistical significance - coming from different domains - while

the enrolment data records from the same university over a number of

periods are expected to show no statistically significant differences. While

there is no theory for such propositions the mathematical modeling process

to generate random number (characteristic) data bases employed for the

testing of this proposition will provide the basis for the lack of existing

theory.

42

Data base integrity should be understood as the correctness and

completeness of data base elements that have been compiled by recording

transactions or similar events into a common data base designed for the

capture of element characteristics with information content that infers

attribute commonalities. Empirical evidence, although sparse, suggests that

most, if not all, data bases contain data entry and data omission errors and

thereby impinge on the data base integrity.

A Pareto frontier refers to the curvature that is formed when a data base is

ranked and sorted on two predetermined dimensions and the item

frequency distribution is arranged in a cumulative ascending sequence such

that x1 > x2 >x3 >.......xn. Although the Pareto principle has been accepted,

its validation has only been confirmed through practical applications of

element ranking and ordering.

43

Key Assumptions

A number of assumptions have been made in the development of the

model. Firstly, the assumption is made that all data bases follow an

unbalanced distribution (the Pareto principle) but there are no tools or

techniques that detect data base inaccuracies as the element arrangement

can only use the available data.

Secondly, any data base which involves the recording of events or

transactions that are compiled by operators with or without technical

support systems will contain data entry and omission errors. While other

sources of errors have been discussed in various literature, for the purpose

of this thesis, entry and omission errors are the most relevant components

of interest.

Thirdly, simplified overhead allocations are preferred by practitioners which

is supported by recent survey evidence on overhead assignment methods

and further reveal a lesser reliance of these methods in decision support

system applications by corporate managements.

Fourthly, the generation of random number generated data bases is a

better proxy of “real” data bases as these are free of both data entry and

data omission errors and, furthermore, allow the varying of data base

44

element characteristics at random as well as varying the Pareto frontier or

shape factor to mirror any “real” data base Pareto frontier.

Limitations

A number of limitations must be identified. The major limitation is the model

testing against random generated data bases as validation of its robustness

using a limited number of element characteristics. Furthermore, the use of

data base analysis on the basis of only two predetermined element

characteristics may limit the model’s application in more complex and

interdependent data base element relationships. This limitation may apply

to the model’s general applicability but it must be understood the purpose

of the model development was to provide an alternative overhead

allocation method. The most popular practiced techniques also rely on a

simple two-dimensional allocation, volume and demand. Overhead

allocations in general have been criticised as incorrigible and arbitrary and

as such, the model does not resolve this allocation problem. The model

does, however, redress the allocation problem associated with product

additions and deletions by the re-ranking process rather than the continued

application of a single volume denominator.

Another limitation that could be advanced is the need to analyse an existing

data base before any model application can become effective. While such

a precondition may have been a limitation in past periods where

45

computational resources were scarce and expensive, contemporary

inexpensive availability of extensive computer resources and software

applications are no longer a defensible restriction.

46

2. Literature Review

2.1 Introduction

The allocation problem has plagued accounting theory for many decades.

Accounting allocations are found in many areas ranging from financial

accounting standards of generally accepted accounting principles (GAAP)

to the internal or management accounting practices involving the allocation

of general overheads to products for purposes of inventory valuations and

managerial decision making concerning product mix and product viability

determinations.

Athur L, Thomas could be credited with being a most prominent opponent

of the allocation debate. In a 1975 article he suggested that any form of

accounting allocations are almost always incorrigible and therefore never

preferable to a refusal to allocate. He reaches this conclusion after careful

theoretical analysis and provides a number of examples that demonstrate

the limitation of any one allocation method over any other. He further

argues that the incorrigible nature of allocations makes it highly unlikely the

accounting profession will ever achieve a consensus on what can be

regarded as the “best” allocation scheme while there are alternative

schemes that compete for dominance. Thomas (1975) concludes that the

best alternative must therefore be, not to allocate.

47

While the theoretical arguments that underpin the non allocation position

proposed by Thomas are grounded in rational economic thought, these

concepts find limited acceptance in management accounting approaches

to determine product costs and thereby direct resource allocations, yet

another area of incorrigible allocations. Much of the recent debate

concerning the relevance or otherwise of traditional management

accounting is concerned with the perceived inappropriateness of overhead

allocation techniques. One of the most prominent proponents of the

irrelevance movement Robert S. Kaplan argues convincingly that the need

to allocate overhead costs on a single volume based cost driver is

inappropriate in a changed environment that is dominated by advanced

product and process technologies. His suggested alternative of Activity

Based Costing [ABC] has found some resonance in organisations, whi le

some of his critics claim that this technique is based on historical data and

relies also on subjective allocations for some of the identified overhead

classifications.

Another contemporary approach to modify traditional management

accounting techniques has been advanced by Eli Goldratt (Goldratt and

Cox, 1992) in promoting the need for organisational constraint recognition

and the subsequent effort to reduce or eliminate such constraints. Goldratt’s

Theory of Constraints [TOC] further suggests that any current management

48

accounting technique is stifling the application of TOC and has little

relevance in improving an organisation’s profitability. He defends this

proposition by claiming that the main purpose of any organisation is the

creation of wealth and that the generation of improved cash flows becomes

a consequence of improved process efficiencies.

Each of these theories does contribute to a better understanding of the

issues that have confronted the accounting profession for decades but

provides only limited application relevant to the practising accounting

profession. In the following sections a number of techniques for each of the

stated theories are discussed and the final section provides a critical

evaluation of the issues presented.

2.1.1. Traditional Organisational and Operational Environments

The need to determine the cost of individual products in an organisation’s

product mix is a basic information requirement for managerial decision

making. The development of fundamental techniques to produce accurate

product cost data goes back in history to the establishment of organisations

involved in the production of manufactured goods. As mechanisation of the

production process was limited to the prevailing technology most of the

production processes were reliant on manual labour skills. The conversion

process of materials to sellable products required a substantial amount of

49

direct labour effort and volume production was a function of labour capacity.

What was less determinable were the indirect costs of production as these

related to the productive output. Planning, control and monitoring functions

are an integral part of organisational life and incur a substantial cost. These

indirect costs have been referred to in various terms. Most common

amongst the terminology are overhead costs, manufacturing burden or

production on-costs. ‘Overhead costs’ seem to be the most commonly

referred to cost term of these genre and will be used throughout this thesis.

Accepting the early industrial setting of production capacity being a function

of labour skills availability, it was a common sense assumption to base the

distribution of overhead costs on the consumption of direct labour involved

in the production of manufactured goods. Such reasoned approach allowed

the allocation of overhead cost to individual products on the basis of direct

labour hours consumed in the production of these goods. As competitive

environments were of lesser consideration, the product’s final price was

determined by the total manufacturing costs (material, labour and

overhead) to which a percentage was added to recover other related

organisational costs (selling, administration, etc.) to ensure that a

satisfactory profit was attained.

50

TABLE 2-1,

A summary of surveys: elements of cost

Cost

elements

Whittle

(2000)

%

ACCA

(1993)

%

Murphy &

Braund

(1990)

(1985)

%

Kerreman

(1991)

%

Schwarzbach

(1985)

%

D.Mat 57 50 50 47 55 58

D.Labour 15 12 18 18 21 13

O/H Var.

Fixed

11

14

38* 32* 35* 24* 29*

Other 3

Total Costs 100 100 100 100 100 100

*Split between fixed and variable not reported in survey results

Source: Whittle, N., (July/August 2000), “Older and Wiser”, Management Accounting, p.35

W hittle (2000) has compiled an overview of a number of surveys that

investigated the ratio of product cost components over a 13-year period.

W hile such compilation cannot be regarded as definitive, it does,

nevertheless, provide a less biased review of changing product cost

elements.

What is noticeable in Table 2-1 over the review period is the rather

constant proportion of direct labour as a proportion of total product costs.

A similar review (Boer, 1994) covering an extended period from 1850 to

1987 supports this trend by claiming that differences in labour percentages

across industries have existed for many years but trends within industries

51

have experienced little change. As most of the surveys cover a broad

sample of industries, the data refers to averages, therefore allowing for

industries to be either substantially above or below these percentages.

Another aspect of the accuracy debate is the analysis of existing processes

and activities and a subsequent regrouping of these activities into

homogeneous cost pools. Such analysis is limited as it does not investigate

the current process inefficiencies or resource constraints to recommend

optimisation strategies. A useful starting point in any operational analysis

is the identification of capacity and resource constraints. Capacity

constraints can be limited to the physical means of production whereas

resource constraints should include availability of human resources and

supply chain limitations.

2.1.2 The Full Cost (or Absorption Cost) Concept.

The full cost concept (or absorption cost concept) was therefore an

acceptable method for product pricing purposes and managerial decision

making with regard to product mix considerations and (dis)continuation of

individual product manufacture. Another often cited advantage of the full

cost concept is the risk reduction in managerial pricing decisions as the full

cost constitutes the fundamental part of the pricing equation. One of the

drawbacks, however, is related to efficiencies. Should the labour skill levels

52

differ amongst a number of operatives in producing a given unit, the total

direct labour hours vary resulting in different overhead applications for the

same unit of production. Such potential inconsistencies were overcome by

establishing production standards as benchmark for comparison and led to

the development of standard costing practices. It was not uncommon in the

earlier part of the industrial revolution to have a labour cost content in

excess of 50% with materials contributing another 30% to 40% and the

reminder of the total product cost being the allocated overhead.

An example will demonstrate the initial product cost profile and through the

development of labour reducing production processes the change in the

main cost components (material, direct labour and allocated overhead

costs). The example is based on a number of premises that establish the

parameters of the computational results.

Firstly, a product that has remained fairly consistent in appearance,

functionality and consumer demand over a longer temporal dimension has

to be identified (eg. Kellogs Corn Flakes, Coca Cola, Household Furniture

to name a few). For simplicity the products are referred to as A, B, C, D.

Next the operating capacities have to be established. The annual

production capacity is based on 100,000 direct labour hours [DLH] with a

53

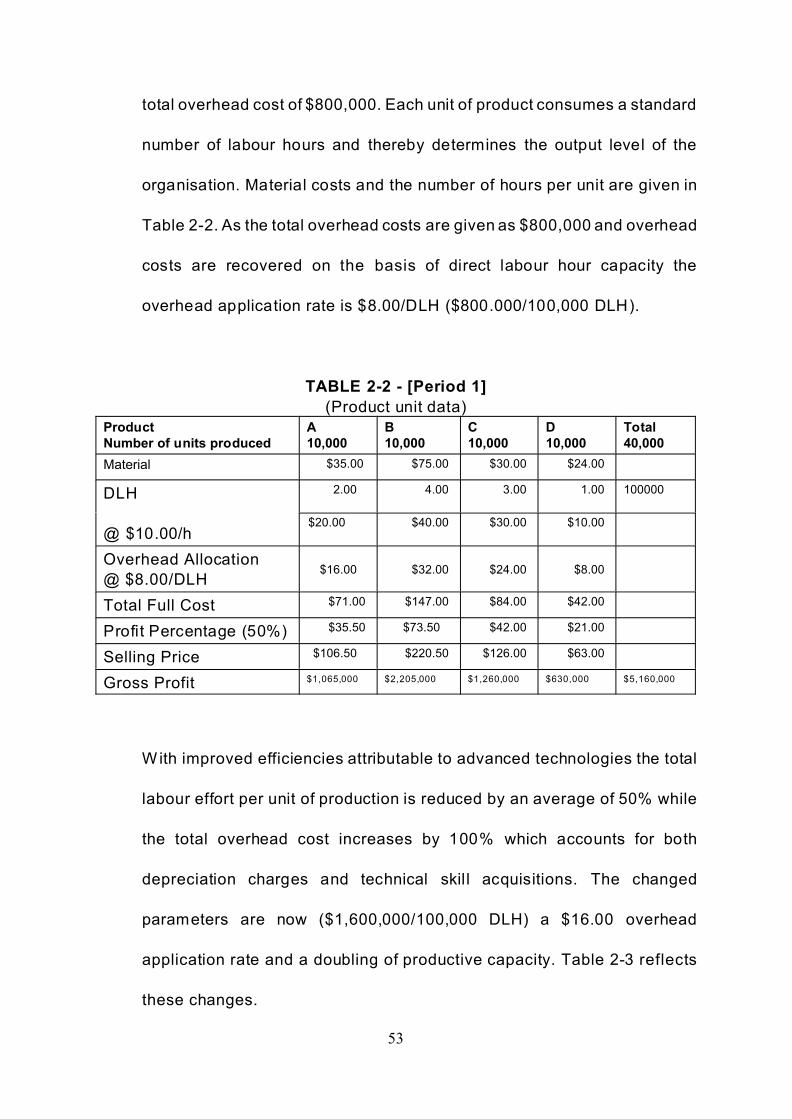

total overhead cost of $800,000. Each unit of product consumes a standard

number of labour hours and thereby determines the output level of the

organisation. Material costs and the number of hours per unit are given in

Table 2-2. As the total overhead costs are given as $800,000 and overhead

costs are recovered on the basis of direct labour hour capacity the

overhead application rate is $8.00/DLH ($800.000/100,000 DLH).

TABLE 2-2 - [Period 1]

(Product unit data)

Product

Number of units produced

A

10,000

B

10,000

C

10,000

D

10,000

Total

40,000

Material $35.00 $75.00 $30.00 $24.00

DLH

@ $10.00/h

2.00 4.00 3.00 1.00 100000

$20.00 $40.00 $30.00 $10.00

Overhead Allocation

@ $8.00/DLH$16.00 $32.00 $24.00 $8.00

Total Full Cost $71.00 $147.00 $84.00 $42.00

Profit Percentage (50%) $35.50 $73.50 $42.00 $21.00

Selling Price $106.50 $220.50 $126.00 $63.00

Gross Profit $1,065,000 $2,205,000 $1,260,000 $630,000 $5,160,000

With improved efficiencies attributable to advanced technologies the total

labour effort per unit of production is reduced by an average of 50% while

the total overhead cost increases by 100% which accounts for both

depreciation charges and technical skil l acquisitions. The changed

parameters are now ($1,600,000/100,000 DLH) a $16.00 overhead

application rate and a doubling of productive capacity. Table 2-3 reflects

these changes.

54

TABLE 2-3 - [Period 2]

(Product unit data)

Product

Number of units

produced

A

20,000

B

20,000

C

20,000

D

20,000

Total

80,000

Material $35.00 $75.00 $30.00 $24.00

DLH

@ $10.00/h

1.00 2.00 1.50 0.50 100000

$10.00 $20.00 $15.00 $5.00

Overhead Allocation

@ $16.00/DLH$16.00 $32.00 $24.00 $8.00

Total Full Cost $61.00 $127.00 $69.00 $37.00

Profit Percentage (50%) $30.50 $63.50 $34.50 $18.50

Selling Price $91.50 $190.50 $103.50 $55.50

Gross Profit $1,830,000 $3,810,000 $2,070,000 $1,110,000 $8,820,000

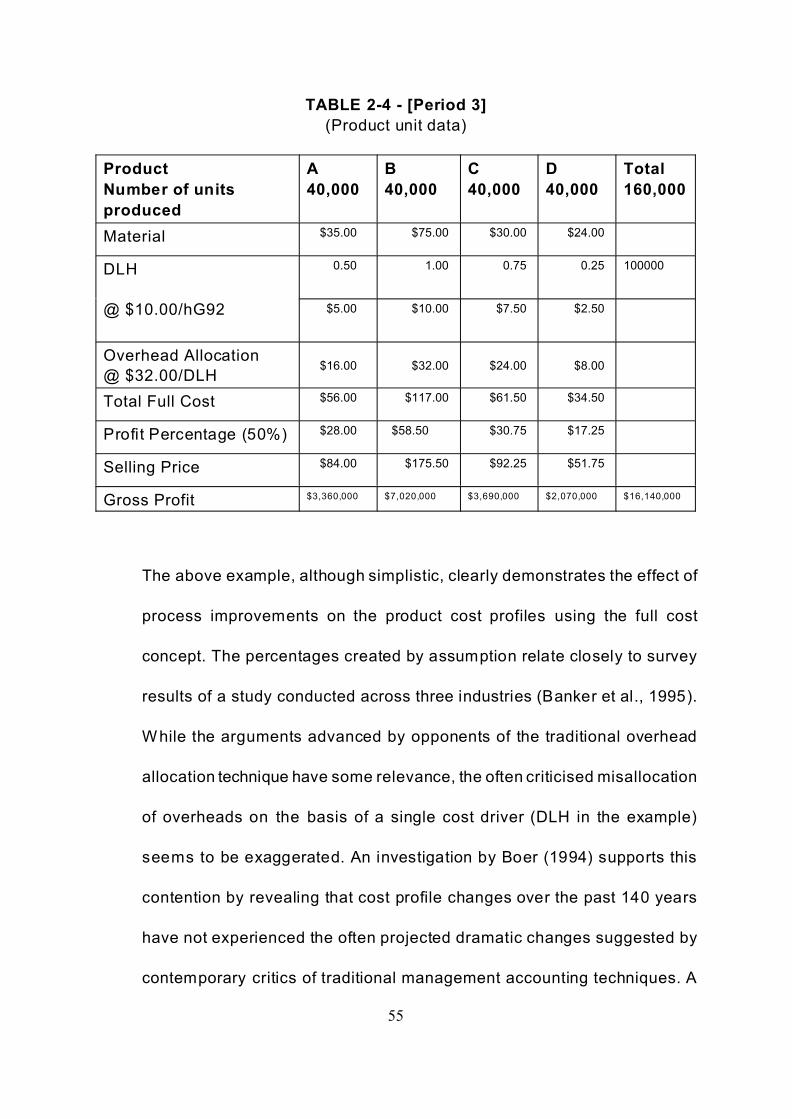

Assuming similar changes for a third period would produce an overhead

application rate of $32.00 ($3,200,000/100,000 DLH). In addition it is

assumed that the cost of materials remains unchanged due to component

reduction and less expensive alternative material supplies. Labour rates

have also been kept constant on the assumption that technology

replacement reduced the labour skills requirements and therefore would

reduce the cost of labour as well as the time required to produce a unit of

production. Table 2-4 reflects these additional changes.

55

TABLE 2-4 - [Period 3]

(Product unit data)

Product

Number of units

produced

A

40,000

B

40,000

C

40,000

D

40,000

Total

160,000

Material $35.00 $75.00 $30.00 $24.00

DLH

@ $10.00/hG92

0.50 1.00 0.75 0.25 100000

$5.00 $10.00 $7.50 $2.50

Overhead Allocation

@ $32.00/DLH$16.00 $32.00 $24.00 $8.00

Total Full Cost $56.00 $117.00 $61.50 $34.50

Profit Percentage (50%) $28.00 $58.50 $30.75 $17.25

Selling Price $84.00 $175.50 $92.25 $51.75

Gross Profit $3,360,000 $7,020,000 $3,690,000 $2,070,000 $16,140,000

The above example, although simplistic, clearly demonstrates the effect of

process improvements on the product cost profiles using the full cost

concept. The percentages created by assumption relate closely to survey

results of a study conducted across three industries (Banker et al., 1995).

While the arguments advanced by opponents of the traditional overhead

allocation technique have some relevance, the often criticised misallocation

of overheads on the basis of a single cost driver (DLH in the example)

seems to be exaggerated. An investigation by Boer (1994) supports this

contention by revealing that cost profile changes over the past 140 years

have not experienced the often projected dramatic changes suggested by

contemporary critics of traditional management accounting techniques. A

56

1990 Australian survey of manufacturing organisations across 13 different

industry groups revealed that the average product cost profile follows a

55%-20%-25% (material - labour - overhead) profile but varies substantially

across industries captured by the survey.

FIGURE 2-1, Percentage changes of Material, Labour and Overhead costs over 3 periods for

Product A, Products B, C and D show similar trends basis.

57

FIGURE 2-2, Percentage changes of Material, Labour and Overhead costs over 3 periods for

Product A as proportion of the selling price; Products B, C and D show similar trends basis

The example provided in Tables 2-2, 2-3 and 2-4 and illustrated in Figures

2-1 and 2-2 reflects the general status of these findings and confirms the

need to control and allocate overhead costs on a more computational

basis. The more dramatic cost profile change appears to be in the direct

labour and material groupings. As mentioned before both of these

categories have been held constant in relative cost terms over the three

periods but would produce a more dramatic change if these groups

experience increases over the review period. Overhead costs, however,

who had the most significant cost increases during the review period have