The Rodney Dangerfield of Investment Strategies www.clothiersprings.com For Investment Professionals Only | Page 1 The Rodney Dangerfield of Investment Strategies or If Outcomes are the New Alpha, Buy-Writes are the New Core Exposure

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 1

The Rodney Dangerfield of Investment Strategies!!or!!If Outcomes are the New Alpha, Buy-Writes are the New Core Exposure!!

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 2

Executive Summary The humble buy-write is the Rodney Dangerfield of strategies—it gets no respect. !Buy-writes suffer from two kinds of misunderstanding. First, most investment professionals have a rudimentary understanding of how a buy-write performs. As such, they know in a basic way that buy-writes trade an uncertain upside potential for a known cash flow received from selling a call option. For most of them— focused on their tenuous understanding of the moving parts instead of the strategy outcome—their understanding stops there and buy-writes as an investment strategy get slotted into a dark and forgotten corner of their mental filing system under “sells the upside.”!Second, for those investment professionals steeped in the world of option trading—who understand the gamut of derivative pricing characteristics and behaviors—they tend to approach hedging generally and buy-writes specifically wearing their trading hats. They hold out the potential to actively trade an option hedge overlay and add value.!We have an observation for both groups:!To the first group: you’re missing a great opportunity to enhance portfolio outcomes. !To the second group: you’re doing it wrong.!The fundamental truth of the buy-write is simply this: it capitalizes on market uncertainty by selling a call option and collecting an historically richly-priced cash flow. It harvests the equity risk premium now, rather than waiting for it to materialize later.!If you hear buy-write and think “selling my upside” you are technically correct but missing the larger picture. The operative word is “selling.” The proceeds from that sale insulate the portfolio in the short run and enhance total return in the long run.!A fuller appreciation would have you understand that a buy-write:!• Sells an uncertain upside potential for a known and historically rich option

premium

• Introduces a new, negatively correlated portfolio exposure • Harvests the equity risk premium immediately • Adds short volatility as a portfolio exposure • Increases portfolio diversification • Sharply reduces portfolio risk in all market environments • Enhances portfolio returns in all but strong up-markets

Better Outcomes Why does any of this matter? Because all those intrinsic characteristics of the buy-write lead to better outcomes. At the end of the day, investors are looking for the best outcome for their level of risk tolerance. They simply want to meet their objectives in the most direct and efficient way. They don’t necessarily care if it takes stocks, bonds, CDs, market-neutral, merger arbitrage, or whatever. Investors looking for better outcomes would benefit from including low-cost, liquid and transparent buy-writes in their asset mix.!We have an invitation for both groups:!To the first group: we invite you to expand your appreciation of the humble buy-write and how it can improve portfolio outcomes. If your clients are looking for alternative exposures, more diversification, less risk, better outcomes and more transparency, you should look at buy-writes.!To the second group: keep it up. Keep up the counterproductive and overactive trading, rolling, lifting, adjusting and other fiddling with the option hedge overlay. Keep trying to outguess the random, short-term movements of the market. Keep spending your client’s money on commissions, market impact and opportunity costs. Keep making short-term trading decisions in real-time and hope you (your clients) end up on the right side of the ledger. Keep on charging those hefty fees to your clients who have bought into the premise that you can add value. We compete against you and you are making us look good. !When we first looked at the return data for the CBOE Options-based indexes almost ten years ago, we saw that the outcomes were optimal. In 2004, the long-term returns of the CBOE S&P 500 Buy-Write (BXM) were better than the S&P 500 with 40% less risk. We thought that was a desirable outcome. We still do. The data continue to confirm that reality. The graphs on the next few pages show the Buy-write advantage.

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 3

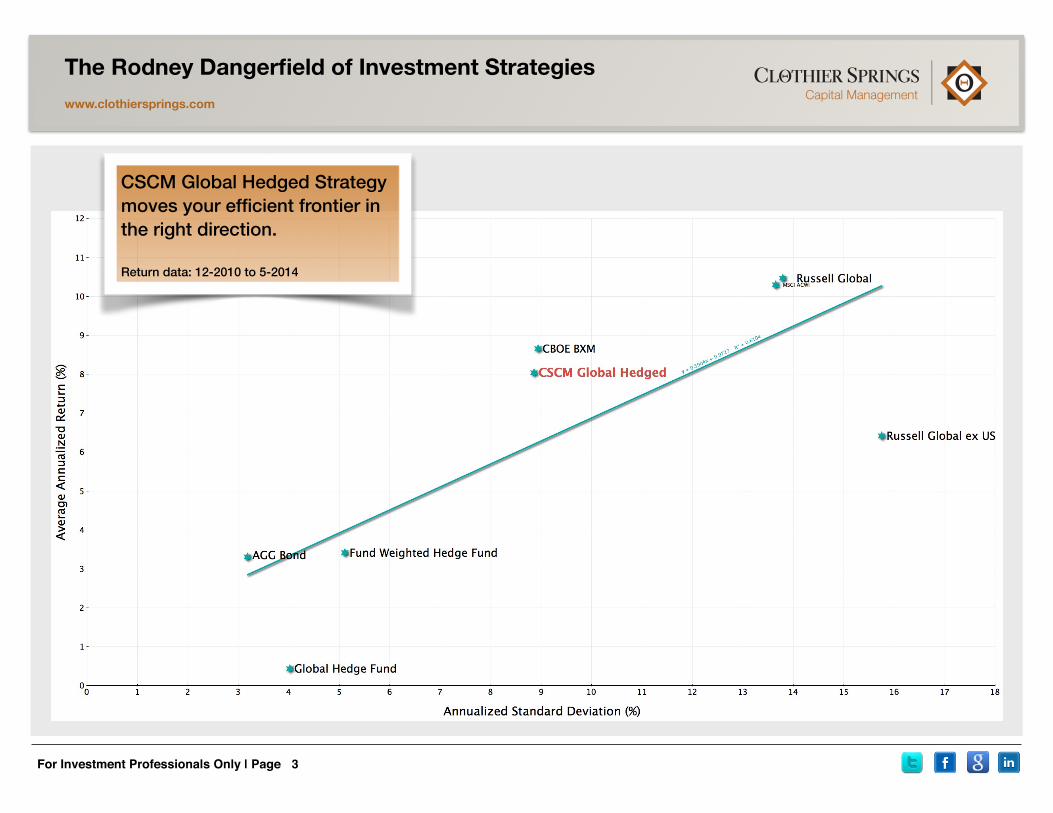

CSCM Global Hedged Strategy moves your efficient frontier in the right direction. !Return data: 12-2010 to 5-2014

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 4

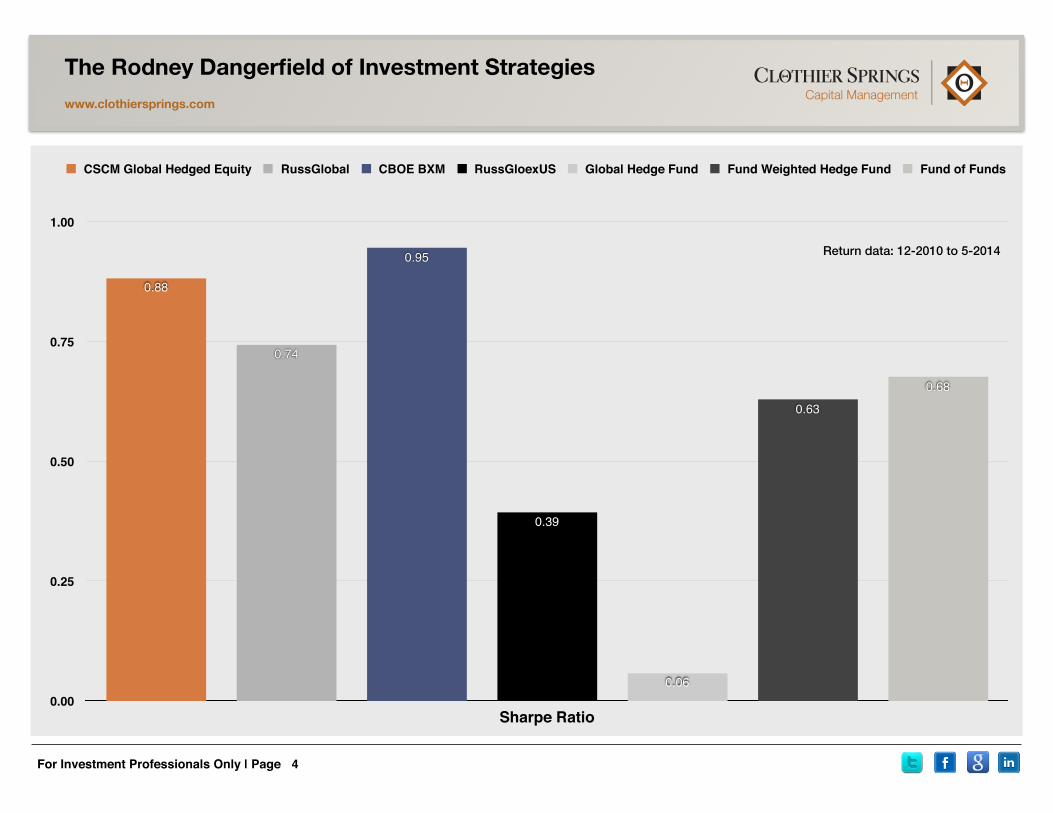

0.00

0.25

0.50

0.75

1.00

Sharpe Ratio

0.68

0.63

0.06

0.39

0.95

0.74

0.88

CSCM Global Hedged Equity RussGlobal CBOE BXM RussGloexUS Global Hedge Fund Fund Weighted Hedge Fund Fund of Funds

Return data: 12-2010 to 5-2014

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 5

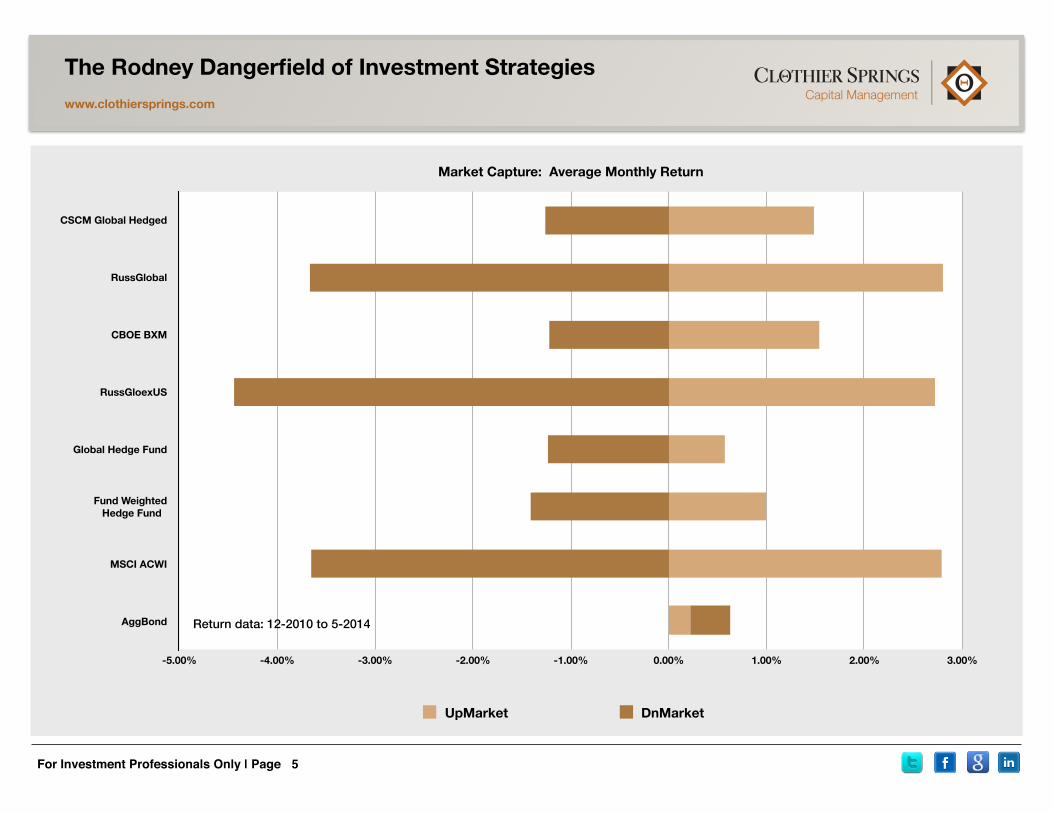

Market Capture: Average Monthly Return

CSCM Global Hedged

RussGlobal

CBOE BXM

RussGloexUS

Global Hedge Fund

Fund Weighted Hedge Fund

MSCI ACWI

AggBond

-5.00% -4.00% -3.00% -2.00% -1.00% 0.00% 1.00% 2.00% 3.00%

UpMarket DnMarket

Return data: 12-2010 to 5-2014

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 6

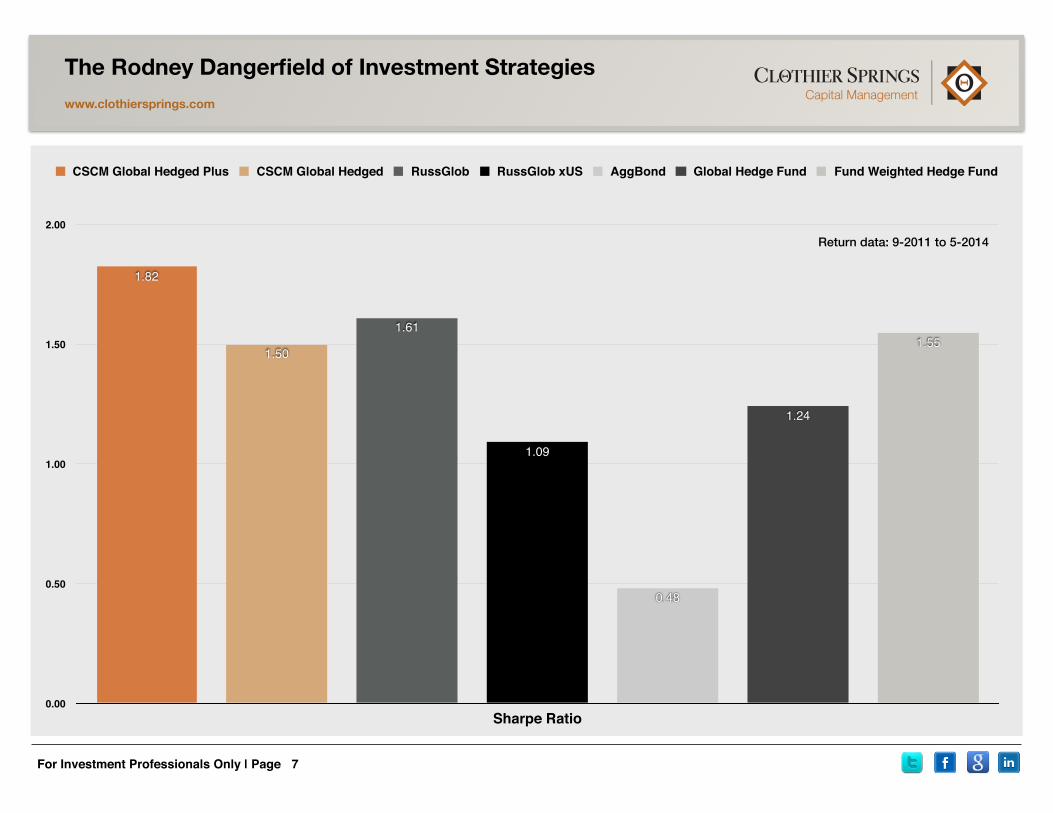

CSCM Global Hedged Plus Strategy moves your efficient frontier in the right direction. !Return data: 9-2011 to 5-2014

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 7

0.00

0.50

1.00

1.50

2.00

Sharpe Ratio

1.55

1.24

0.48

1.09

1.61

1.50

1.82

CSCM Global Hedged Plus CSCM Global Hedged RussGlob RussGlob xUS AggBond Global Hedge Fund Fund Weighted Hedge Fund

Return data: 9-2011 to 5-2014

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 8

Market Capture: Average Monthly Return

CSCM Global Hedged Plus

CSCM Global Hedged

RussGlob

RussGlob xUS

AggBond

Global Hedge Fund

Fund Weighted Hedge Fund

-4.00% -3.00% -2.00% -1.00% 0.00% 1.00% 2.00% 3.00%

UpMarket DnMarket

Return data: 9-2011 to 5-2014

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 9

Analysis Brief!We are living in the golden age of product development in the investment industry. The ascension of Exchange Traded Funds (ETFs) to the asset gathering throne has spawned an unprecedented scramble for assets. This in turn has generated legions of new indexes and product ideas to be packaged within the ETF wrapper—some good, some less so.!Smart Beta, Fundamental Indexing, Low-Volatility and Liquid Alternatives are all new paradigms being positioned and promoted by product sponsors. A new investment management entity—the ETF Strategist—until recent years an almost unimaginable variation on the stockpicker-portfolio manager theme is now the most viable and robust competitor on the landscape. !Much of that is being driven by the growing acknowledgment by most objective observers that active management does not pull its weight. One prominent report supporting that reality is the study from McKinsey from two years ago asserting that “Outcomes are the New Alpha.” This is just the new way of saying that clients can’t eat relative returns and asset allocation is where the heavy lifting happens. The truth is, all clients have ever wanted is to meet their objectives as directly, efficiently and cost-effectively as possible. It was always the insular investment management industry that was far too obsessed with alpha and excess returns, and always in the effort to justify fatter fees. !Much, if not most, of the Managed ETF product we see coming to market is unfortunately tactical in nature. We are skeptical that the active management of asset classes will deliver any more alpha than the active management of securities. What the proliferation of ETFs has rightly supported is the delivery of fully allocated, institutional quality portfolios to almost any account, with liquidity, transparency and at low-cost.

!The Best of Both Worlds The two broadly allocated ETF strategies we manage at CSCM take a different approach. We seek to blend the superior return and risk profiles of hedged investing with the advantages of passive investing: low-cost, liquidity and transparency. !As a result, the returns generated by our strategies are a function of the portfolio and hedge structure, not the active management of asset classes and hedging. The exhibits on the previous pages demonstrate that buy-writes generally and our multi-market buy-write strategies specifically occupy a very attractive spot on the return / risk matrix. Their Sharpe Ratios reveal the highest returns earned per unit of risk among the traditional and hedged benchmarks examined, with healthy absolute returns. !The positive asymmetry of their market capture is also very robust: more of the good stuff, less of the bad stuff. And these metrics have been generated in a super-normal up-market environment—the least favorable for buy-writes. These are powerful outcomes.!Even in an equity market (U.S. equities) that over the past five years has outpaced its historic average annual returns by a factor of 2, the buy-write benchmarks and our strategies have delivered very robust returns, with sharply reduced risk and superior market capture asymmetry.!Systematically harvesting the equity risk premium across multiple markets delivers less volatility, better returns & superior structural positive asymmetry. You want outcomes, we’ve got outcomes. And they come with full liquidity, transparency and very low cost. And best of all, they are structural, not the result of the unreliable, unrepeatable and expensive activities of active management.

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 10

About the Strategies & Benchmarks!!CSCM Global Hedged (composite inception 12-31-2010)!A Managed ETF strategy allocated to the global equity markets and hedged with short call options on a passive, rules basis. The global allocation is strategic with weightings driven by consideration of three primary factors: global equity capitalizations, relative valuations and available annualized premium capture of the hedge(s). Entire portfolio is hedged at all times with no tactical adjustments.!!CSCM Global Hedged Plus (composite inception 9-30-2011)!A Managed ETF strategy with a risk-averse profile, strategically allocated to the global markets, including traditional long-only exposures and hedged exposures. The equity allocations are split equally between long exposures and the CSCM Hedged Equity strategies. Strategy is fully invested at all times and the hedged exposures are maintained at all times with no tactical adjustments.!!CBOE BXM!The CBOE S&P 500 BuyWrite Index (BXM) is a benchmark index designed to track the performance of a hypothetical buy-write strategy on the S&P 500 Index. The BXM is a passive total return index based on (1) buying an S&P 500 stock index portfolio, and (2) "writing" (or selling) the near-term S&P 500 Index (SPXSM) "covered" call option, generally on the third Friday of each month. The SPX call written will have about one month remaining to expiration, with an exercise price just above the prevailing index level (i.e., slightly out of the money). The SPX call is held until expiration and cash settled, at which time a new one-month, near-the-money call is written.!!Russell Global!The Russell Global index measures the performance of the global equity market based on all investable equity securities. All securities in the Russell Global index are classified according to size, region, country, and sector, as a result the index can be segmented into thousands of distinct benchmarks. The Russell Global index is constructed to provide a comprehensive and unbiased barometer for the

global segment and is completely reconstituted annually to accurately reflect the changes in the market over time.!!Russell Global ex U.S.!The Russell Global ex-US index measures the performance of the global equity market based on all investable equity securities, excluding companies assigned to the United States. The Russell Global ex-US index is constructed to provide a comprehensive and unbiased barometer for the global segment and is completely reconstituted annually to accurately reflect the changes in the market over time.!!MSCI ACWI!MSCI ACWI captures large and mid cap representation across 23 Developed Markets (DM) and 23 Emerging Markets (EM) countries. With 2,433 constituents, the index covers approximately 85% of the global investable equity opportunity set.!!Global Hedge Fund Index!The Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies; including but not limited to convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage, and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry.!!Fund Weighted Composite!The Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to the Database. Constituent funds report monthly net of all fees performance in US Dollar and have a minimum of $50 Million under management or a twelve (12) month track record of active performance. The Fund Weighted Composite Index does not include Funds of Hedge Funds.!!Barclay’s U.S. Aggregate Bond!An index composed of the total U.S. investment-grade bond market.

The Rodney Dangerfield of Investment Strategies !www.clothiersprings.com

For Investment Professionals Only | Page 11

About Clothier Springs Capital Management:!We manage portfolios that combine the advantages of passive investing with the risk-reducing characteristics of a consistently-applied, options-based hedge. The result is a portfolio with a superior return and risk profile, compared to the underlying equity index, at very low-cost and with full liquidity and complete transparency.!!Each of our strategies combines one or more traditional long-market exposures with a consistently applied option-hedging component. All are managed passively according to strict, rules-based protocols.!!By applying passive management precepts, we avoid the unreliable and!counterproductive features associated with active management and can offer our portfolios at a compellingly low cost. Our low-cost, liquid and transparent hedged equity strategies help institutional and individual investors meet their objectives with greater certainty and less risk. !!For more: www.clothiersprings.com!!!Clothier Springs Capital Management, LLC!305 Clothier Springs Rd. | Phoenixville, PA 19460!WHQ: [email protected]

Thomas F. McKeon, CFA [email protected]: 610.933.3925M: 610.937.3919

Timothy R. Ringler [email protected] O: 610.933.3925M: 484.888.1686