3rd MEDITERRANEAN SEMINAR LACTIMED ALEXANDRIA, EGYPT, 17-18 SEPTEMBER 2014 DAIRY VALUE CHAIN AT THE INDUSTRIAL LEVEL Mr. Fethi KHAMASSI Deputy Director on Animal processing – Ministry of Energy, Industry and Mines, Tunisia

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

3rd MEDITERRANEAN SEMINAR LACTIMED ALEXANDRIA, EGYPT, 17-18 SEPTEMBER 2014

DAIRY VALUE CHAIN AT THE INDUSTRIAL LEVEL

Mr. Fethi KHAMASSI Deputy Director on Animal processing – Ministry of Energy, Industry and Mines,

Tunisia

REPUBLIC OF TUNISIA

MINISTRY OF ENERGY INDUSTRY AND MINES

DAIRY VALUE CHAIN AT INDUSTRIAL LEVEL

Fethi khamassi

Deputy Director on Animal Product Processing

Alexandria 09 / 18 /2014

2

SUMMARY 1. Economic indicators of the Agro Food

Industries 2. The importance of the dairy sector , 3. The current situation of the sector, - at the industrial level - on the commercial plan 4. Regulatory mechanisms

3

This sector represents:

3.7% of the GDP,

19% of the add value of the industry sector ,

22% of the value of the industry investments,

10% of the value of the total exportations

Economic indicators of the AFI sector

4

Entreprises en partenariat

France (35)

29%

Répartition par pays

Italy (33)

53%

31%

Activities Number of companies TE

Fruis and vegetables Packaging 82

Processing and preserving of fish 38

Other food insdustries 23

Oils and fats 22 Fruits and vegetables processing 29

Cereals and derivatives 11 Drinks 5 Suggar and derivatives 4 Other countries (60)

Totally exporting companies

Number of enterprises of the sector 6500 1047 enterprises (> 10 jobs), 201 totally exporting companies, 113 collaborating enterprises,

Number of jobs: 90.000 (70.985 for enterprises which job > 10)

5

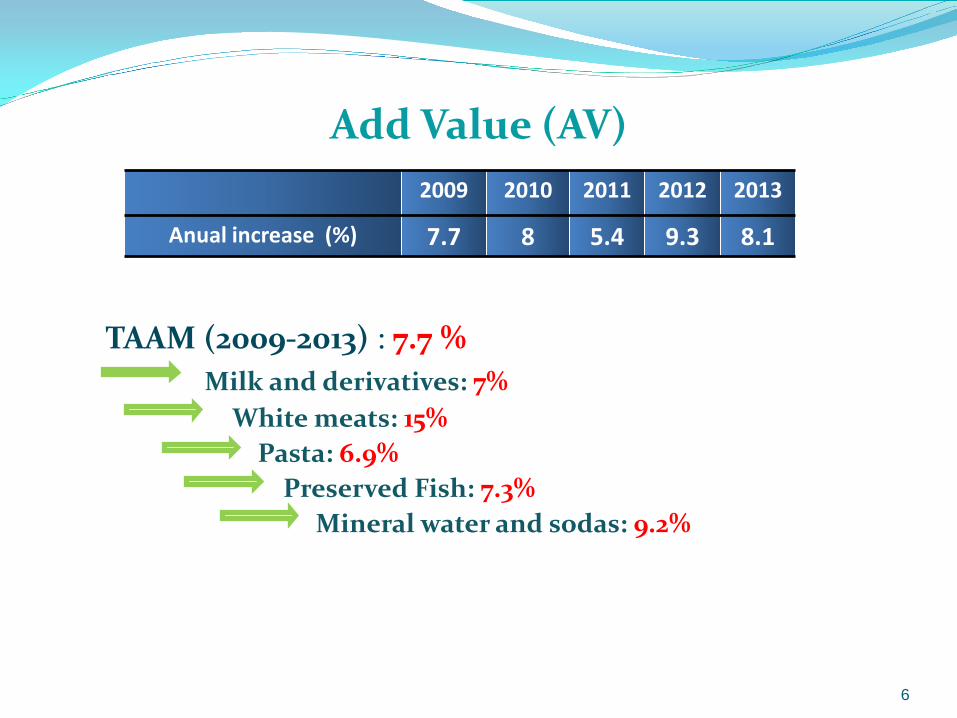

Add Value (AV)

TAAM (2009-2013) : 7.7 % Milk and derivatives: 7% White meats: 15% Pasta: 6.9% Preserved Fish: 7.3% Mineral water and sodas: 9.2%

6

2009 2010 2011 2012 2013

Anual increase (%) 7.7 8 5.4 9.3 8.1

6

Investments

7

2009 2010 2011 2012 2013

Value (MD) 300 320 357 385 425

Average investment structure of the AFI in 2013

cereals derivatives 9%

milk and derivatives 7%

oils and fats; 17%

drinks 10%Preserved food 17%

other products 41%

7

Exportations

2009 2010 2011 2012 2013

Valeur (MD) 1631 1651 2126 2065 2431

Average export structure of the AFI in 2013

Oils and fats43%

Dattes16%

Fishery products10%

Cereals derivatives

9%

Preserved food4%

Drinks3%

Milk and derivatives4%

Other products11%

8

Importations

2009 2010 2011 2012 2013

Value (MD) 1593 2209 2828 3156 3545

Average importations structure of the AFI in 2013

Cereals47%

Oils and fats14%Suggar

9%

Fishery products 3%

Coffe and tea3%

Soybean cakes3%

Milk and derivatives

2%

Other products19%

9

MAIN BRANCHES OF ACTIVITIES (type primary processing)

Olive Oil, Cereal derivatives, Milk and derivatives, Sea food, Canned fruits and vegetables, Packaging of dattes, Wine products,

10

• The milk sector represents: • 11% of the value of the agricultural production, • 25 % of the value of animal production, • 7 % of the value on the food industry

Importation: milk powder, cheese for melting, condensed milk and (sometimes) drinking milk

Exportation : drinking milk, melted cheese, yogurt and dairy dessert.

The importance of the milk sector

11

• 9 functional dairies ( 3,9 ML/Day),

1 unit producing only milk derivatives,

40 cheese dairies (280 mL/Day) of which 4 units of melted cheese,

1 unit for drying milk (150 mL/Day) , 4 unities for yogurt production (250 mL/Day) .

Important processing capacity 3,9 ml / Day higher

than the collecting capacity 2,5 ML/ Day

INDUSTRIAL STRUCTURE

12

13

• Manufactured quantity (2013) : 850 milions of liters meaning 65% of the national production, as follows: Drinkig milk: (60 %),

Derivatives: (Yogurt, dairy desserts, cheeses, leben, raïeb, etc.) (38.4 %),

Dried: Powder milk (1.6 %).

National Milk Production (ML)

14

2009 2010 2011 2012 2013 Production Nat. 1030 1059 1096 1124 1150 collecte 602 650 664 709 747

0

200

400

600

800

1000

1200

1400

15

2009 2010 2011 2012 2013 Prod. dérivés 84 75 89 110 84 Lait UHT 400 428 475 508 503

400 428

475 508 503 84 75

89 110

84

0

100

200

300

400

500

600

700

UHT Milk production and derivatives(ML)

Production and milk sales (ML)

2009 2010 2011 2012 2013 Prod.lait UHT 400 456 447 509 510 Vente lait 400 428 475 508 503

400

456 447

509 510

400 428

475 508 503

0

100

200

300

400

500

600

16

17

Criteria in Europe Criteria in Tunisia

38> 30> MG g/l

32> 28> Protein g/l

Less of 300 milles /ml

I Less of 1 ML/ml

Microbial burden Million germs/ml

Not considered 1028≥ Density à 20 °c

Quality criteria applied

18

Lait stérilisé ½ écrémé en

bouteille plastique 3 couches

5%

Lait stérilisé ½ écrémé en

bouteille Plastique

10 %

Lait UHT demi de 1 litre écrémé en paquet

85 %

Price of a litre ( 2013 )

1020 1010 1060 Retail price ( DT)

Retail price of a litre of milk is 1060 DT = 0,5 euro

Price of 1 litre of milk mil/l

19

Lait stérilisé ½ écrémé en

bouteille plastique 3 couches

5%

Lait stérilisé ½ écrémé en

bouteille Plastique

10 %

Lait UHT demi de 1 litre écrémé

en paquet 85 %

709 709 709 Costs of raw material

190 160 260 Costs of conditioning and packaging

69 60 72 Logistics costs at the manufactured level

184 160 154 Industrial costs

31 31 31 Distribution margin

1183 1120 1226 Total costs

1020 1010 1060 Retail price

120 120 120 Subsidies

The P.R of a litre of stirilized milk

Regulatory mechanisms

20

Regulatory mechanisms

21

Buffer stock; Exportation; Drying process

Buffer Stock

22

Since 1999, it exists a fresh milk buffer stock; The buffer stock on sterilized fresh milk is set each

year; ( 50 ML ) Government subsides: 50 mL/litre /month

market supply throughout the year

10 MD

12 MD 3,5 MD

4 MD 10 MD

Regulatory

2009 2010 2011 2012 2013 Stock lait en ML 48,6 55,7 39 37,8 46,5

0

10

20

30

40

50

60

23

Subsides

24

Year 2007 2008 2009 2010 2011 2012

Exportation 6 2 - - 7,5 -

Importation 3,3 7,5 - - - 0,8

Exportation- Importation

Unity : ML

2009 2010 2011 2012 2013

Qt. Fresh milk ( ML) 0 0 9,75 0 13,6

Qt. Dried milk (T) 0 0 750 0 1072

The drying process

The drying process is an important regulatory mechanism on dairy sector.

25

Subside policy

26

Subside policy

FODEC (competitiveness development funds), FODECAP (competitiveness development funds for agriculture and fishing sector)

- CAISSE GENERALE DE COMPENSATION

At collecting level, ( 60 ML/litre) At buffer regulatory level, ( 50 ML/litre/month ) At industry level, ( 120 ML / manufactured litre ) At drying process level ( subsides from the gouvernment at drying costs)

27

Thank you

28

Related Documents