NEGOTIATIONS BETWEEN DAIMLER AND CHRYSLER Yoichi Miyata

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NEGOTIATIONS BETWEEN

DAIMLER AND CHRYSLER

Yoichi Miyata

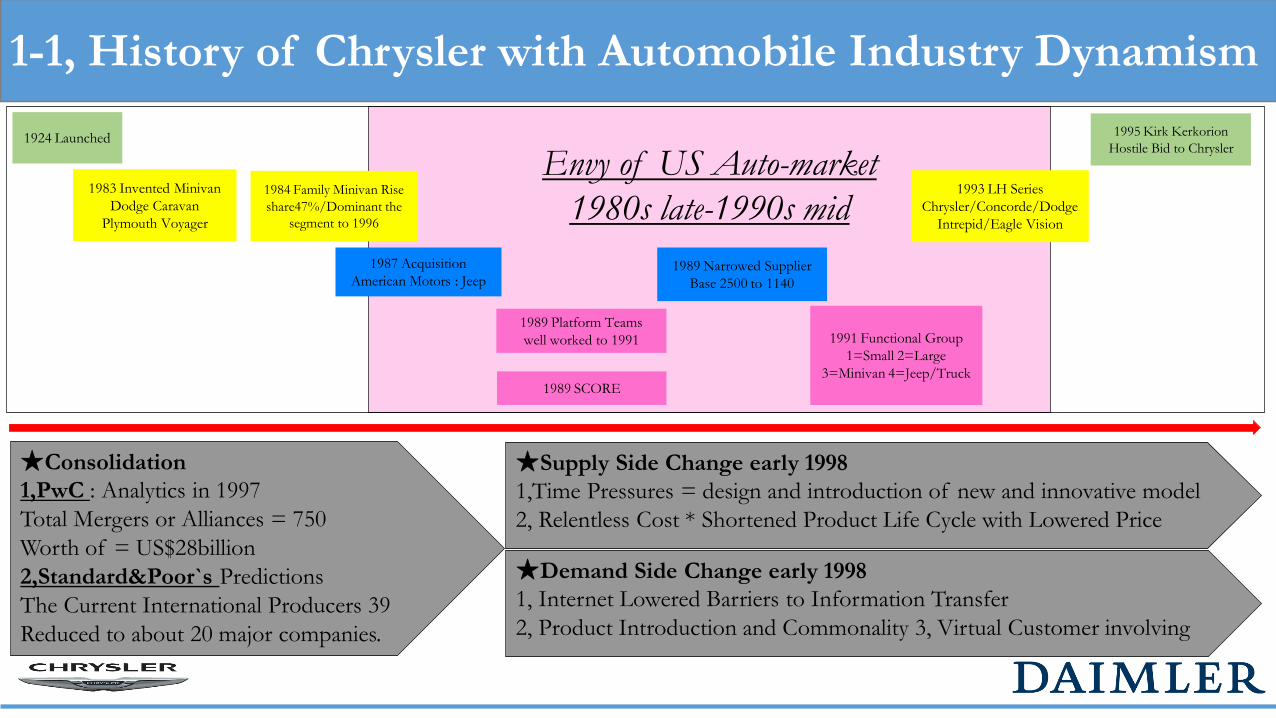

Envy of US Auto-market

1980s late-1990s mid

1-1, History of Chrysler with Automobile Industry Dynamism

1924 Launched

1984 Family Minivan Rise

share47%/Dominant the

segment to 1996

1995 Kirk Kerkorion

Hostile Bid to Chrysler

1983 Invented Minivan

Dodge Caravan

Plymouth Voyager

1989 Platform Teams

well worked to 1991 1991 Functional Group

1=Small 2=Large

3=Minivan 4=Jeep/Truck

1989 Narrowed Supplier

Base 2500 to 1140

1989 SCORE

1993 LH Series

Chrysler/Concorde/Dodge

Intrepid/Eagle Vision

1987 Acquisition

American Motors : Jeep

★Consolidation

1,PwC : Analytics in 1997

Total Mergers or Alliances = 750

Worth of = US$28billion

2,Standard&Poor`s Predictions

The Current International Producers 39

Reduced to about 20 major companies.

★Supply Side Change early 1998

1,Time Pressures = design and introduction of new and innovative model

2, Relentless Cost * Shortened Product Life Cycle with Lowered Price

★Demand Side Change early 1998

1, Internet Lowered Barriers to Information Transfer

2, Product Introduction and Commonality 3, Virtual Customer involving

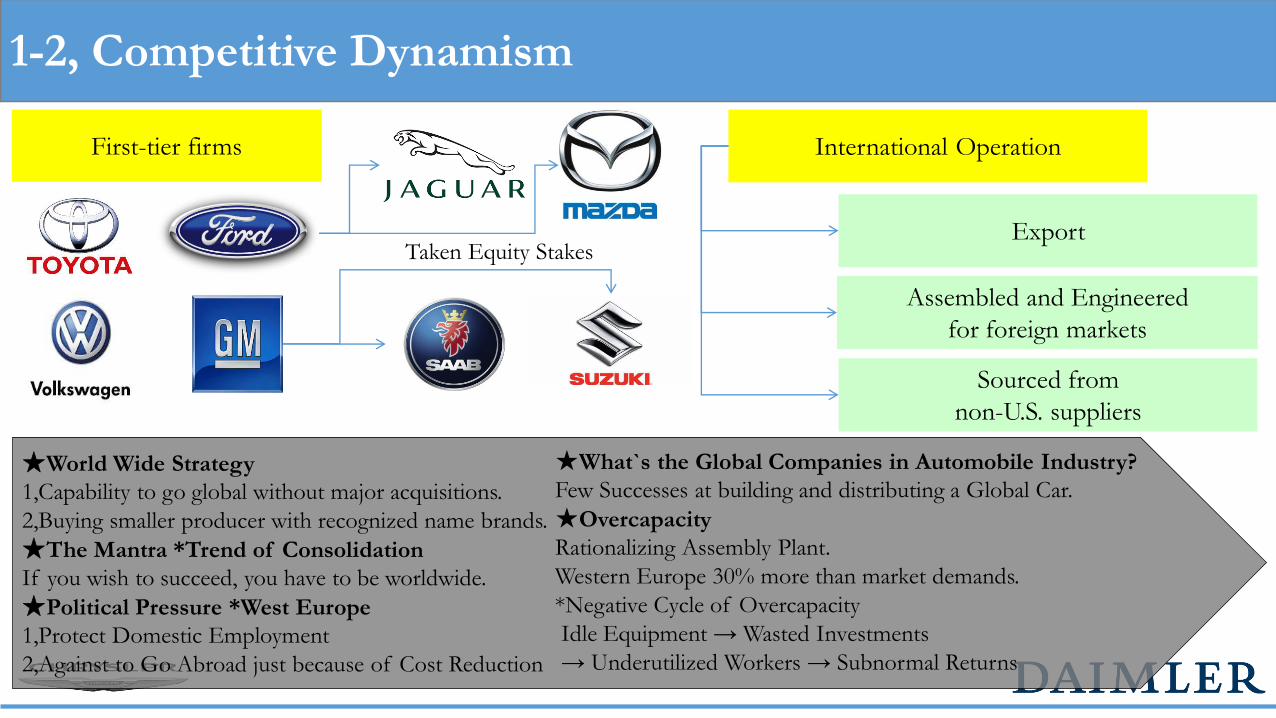

1-2, Competitive Dynamism

First-tier firms

★World Wide Strategy

1,Capability to go global without major acquisitions.

2,Buying smaller producer with recognized name brands.

★The Mantra *Trend of Consolidation

If you wish to succeed, you have to be worldwide.

★Political Pressure *West Europe

1,Protect Domestic Employment

2,Against to Go Abroad just because of Cost Reduction

Taken Equity Stakes

International Operation

Export

Assembled and Engineered

for foreign markets

Sourced from

non-U.S. suppliers

★What`s the Global Companies in Automobile Industry?

Few Successes at building and distributing a Global Car.

★Overcapacity

Rationalizing Assembly Plant.

Western Europe 30% more than market demands.

*Negative Cycle of Overcapacity

Idle Equipment → Wasted Investments

→ Underutilized Workers → Subnormal Returns

2-1, Macro Indicators

FordMotor

GeneralMotors

Chrysler NavistarHondaMotor

NissanMotor

ToyotaMotor

Daimler-Benz

Volvo BMWPeugeot-Citroen

Fiat Audi Renault

1997 Revenues $153,627 $166,445 $61,147 $6,321 $45,111 $49,358 $87,807 $68,951 $23,118 60,137 186,785 89,658 22,410 207,912

1997 Profits/Revenues 4.50% 3.77% 4.59% 2.37% 4.34% 0.77% 3.89% 2.56% 1.73% 2.07% -1.48% 2.70% 1.64% 2.61%

$153,627

$166,445

$61,147

$6,321

$45,111 $49,358

$87,807

$68,951

$23,118

60,137

186,785

89,658

22,410

207,912

4.50%

3.77%

4.59%

2.37%

4.34%

0.77%

3.89%

2.56%

1.73%

2.07%

-1.48%

2.70%

1.64%

2.61%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

$-

$50,000

$100,000

$150,000

$200,000

$250,000

Comparative Automobile Firms : Revenue and Profit Margin Ratiomillions US$

★Market Size *Based on $US Revenue

US$=661,885million Market Share : Chrysler=9.2% Daimler=10.4%

★Market Concentration Ratio

CR4 : Market Share GM + Ford + TOYOTA + Daimler-Benz=72%

★Scale and Efficiency

Revenue Chrysler=US$61,147 Daimler=US$68,951

Profit Margin Ratio Chrysler=4.59% Daimler=2.56%

⁂ Chrysler achieved most highest Profit Margin Ratio

General Motors, 25.1%

Ford Motor, 23.2%

Toyota Motor, 13.3%

Daimler-Benz, 10.4%

Chrysler, 9.2%

Nissan Motor, 7.5%

Honda Motor, 6.8%

Volvo, 3.5% Navistar, 1.0%

Market Share in 1997 excluding non-U.S.dollars audited European Firms

2-2, Micro Indicators

Cash and equivalent, 7,848 Cash and equivalent, 11,464

Accounts receivable, 1,646

Accounts receivable, 6,707

Inventory, 4,738

Inventory, 8,039 Other current assets, 15,711

Other current assets, 11,641

Net property,plant,and equipment, 17,968 Net property,plant,and equipment, 11,540

Goodwill and other intangibles, 1,573

Goodwill and other intangibles, 9,411 Other long-term assets, 10,934

Equity in income of affiliates, 1,929

Deferred taxes and other, 15,860

Accounts payble, 9,512

Accounts payble, 6,189

Other current Liabilities, 9,717 Other current Liabilities, 11,302

Total debt, 15,485 Total debt, 21,956

Other long-term liabilities, 14,342

Other long-term liabilities, 15,771

Revenues, 61,147

Revenues, 69,302

COGS, 46,743 COGS, 51,074

Selling,general,and administrative expense, 6,145

Selling,general,and administrative expense, 12,903

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Asset Liabilities Cost Revenue Asset Liabilities Cost Revenue

Chrysler Daimler-Benz

Hirei-Shukusyaku Zu based on 1997 Operation Results in million US$

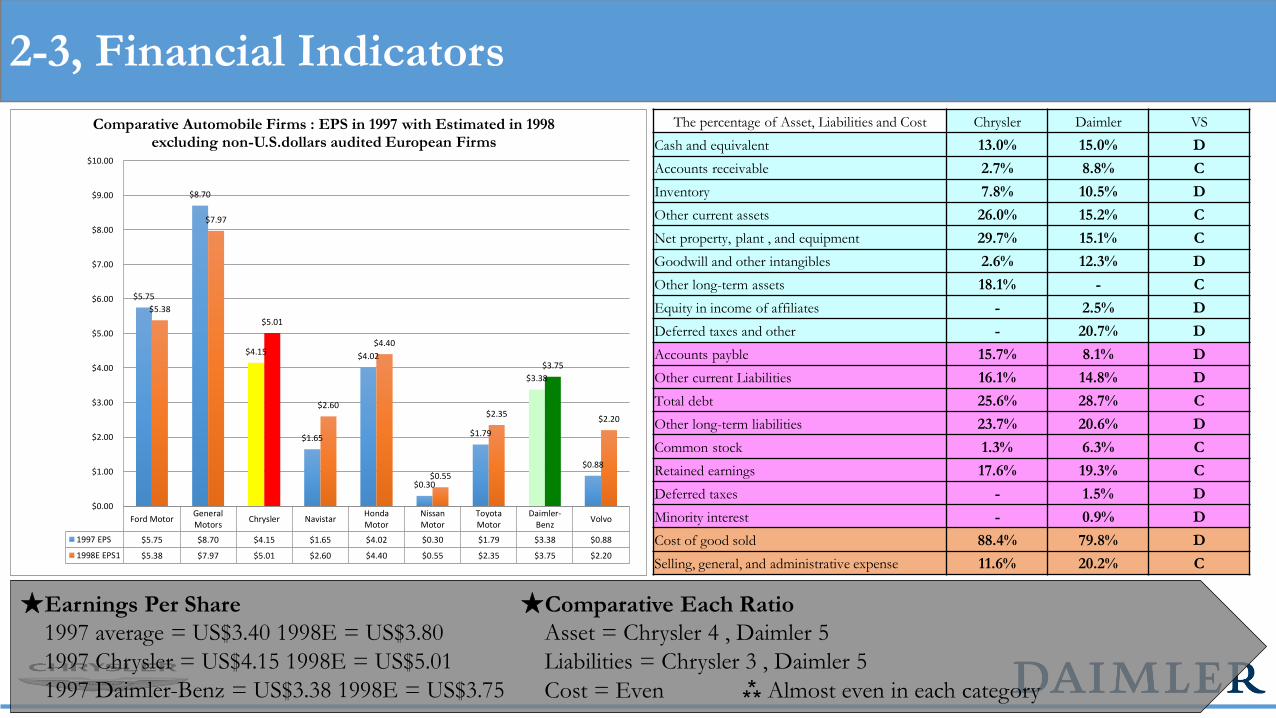

2-3, Financial Indicators

Ford MotorGeneralMotors

Chrysler NavistarHondaMotor

NissanMotor

ToyotaMotor

Daimler-Benz

Volvo

1997 EPS $5.75 $8.70 $4.15 $1.65 $4.02 $0.30 $1.79 $3.38 $0.88

1998E EPS1 $5.38 $7.97 $5.01 $2.60 $4.40 $0.55 $2.35 $3.75 $2.20

$5.75

$8.70

$4.15

$1.65

$4.02

$0.30

$1.79

$3.38

$0.88

$5.38

$7.97

$5.01

$2.60

$4.40

$0.55

$2.35

$3.75

$2.20

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

Comparative Automobile Firms : EPS in 1997 with Estimated in 1998excluding non-U.S.dollars audited European Firms

The percentage of Asset, Liabilities and Cost Chrysler Daimler VS

Cash and equivalent 13.0% 15.0% D

Accounts receivable 2.7% 8.8% C

Inventory 7.8% 10.5% D

Other current assets 26.0% 15.2% C

Net property, plant , and equipment 29.7% 15.1% C

Goodwill and other intangibles 2.6% 12.3% D

Other long-term assets 18.1% - C

Equity in income of affiliates - 2.5% D

Deferred taxes and other - 20.7% D

Accounts payble 15.7% 8.1% D

Other current Liabilities 16.1% 14.8% D

Total debt 25.6% 28.7% C

Other long-term liabilities 23.7% 20.6% D

Common stock 1.3% 6.3% C

Retained earnings 17.6% 19.3% C

Deferred taxes - 1.5% D

Minority interest - 0.9% D

Cost of good sold 88.4% 79.8% D

Selling, general, and administrative expense 11.6% 20.2% C

★Earnings Per Share

1997 average = US$3.40 1998E = US$3.80

1997 Chrysler = US$4.15 1998E = US$5.01

1997 Daimler-Benz = US$3.38 1998E = US$3.75

★Comparative Each Ratio

Asset = Chrysler 4 , Daimler 5

Liabilities = Chrysler 3 , Daimler 5

Cost = Even ⁂ Almost even in each category

★Unbalanced Product Portfolio = Sales Heavily Rely on Trucks

★Increased Competition on the Chrysler`s competitive and profitable sales zone by New Products

⁂ Chrysler need to Reinforce it`s car segment competitiveness by themselves or by leverage other`s capability in Strategic Way

3-1, Chrysler`s Product Portfolio

Trucks

Sport-Utility

VehiclesJeep

Wrangler

Jeep Cherokee

Dodge

Durango

Pick-up Trucks Dodge Ram

Minivan

Share 47%

Plymouth

Voyager

Cars

1/3 of Total Sales in 1997

$US61,147million*0.3=18,344

2/3 of Total Sales in 1997

$US61,147million*0.67=40,968

High Profitability

Price

Range

Increased

Competition

Increased

Competition

Chrysler

Dodge

Plymouth

Chrysler`s 3 Brand

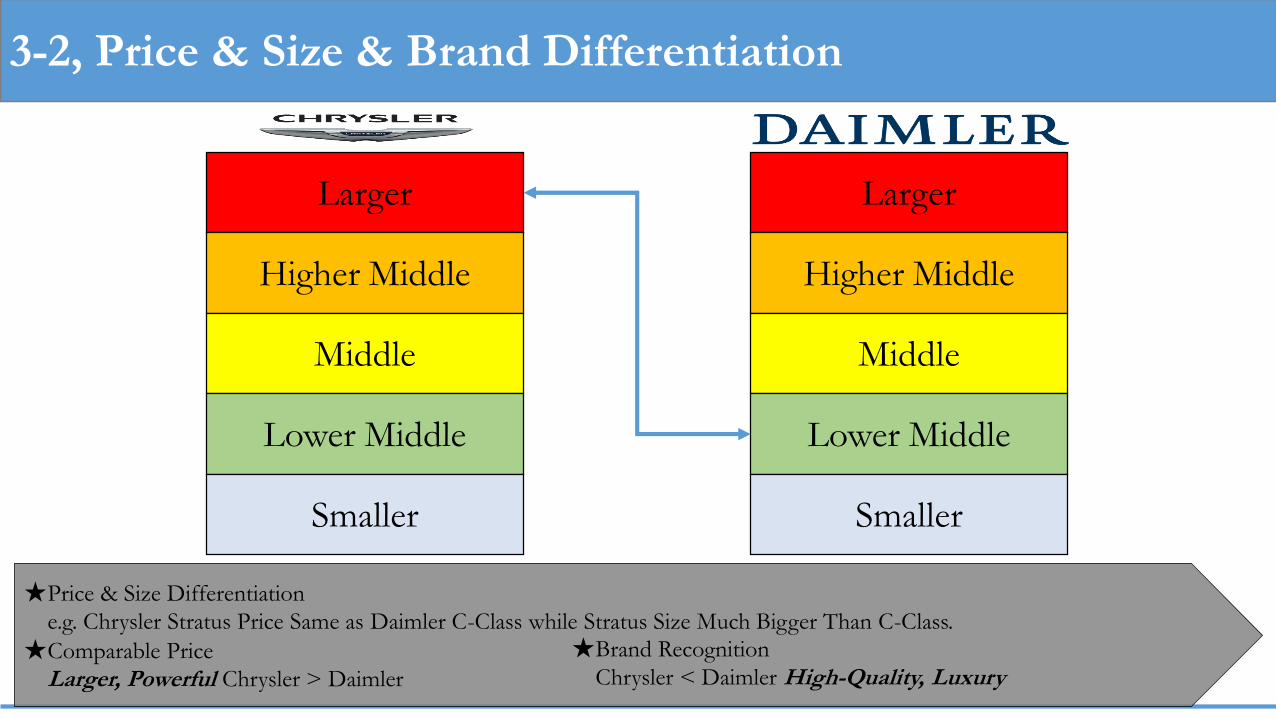

3-2, Price & Size & Brand Differentiation

Larger

Higher Middle

Middle

Lower Middle

Smaller

Larger

Higher Middle

Middle

Lower Middle

Smaller

★Price & Size Differentiation

e.g. Chrysler Stratus Price Same as Daimler C-Class while Stratus Size Much Bigger Than C-Class.

★Comparable Price

Larger, Powerful Chrysler > Daimler

★Brand Recognition

Chrysler < Daimler High-Quality, Luxury

3-3, Chrysler`s International Market Strategy

★Outside North America Vehicle Sales

1990 = 50thousand units

1997 = 237thousand units → 10% of total unit sales of Chrysler.

★Chrysler Need to Broaden or Expand it`s distribution

channel more Internationally.

★The Focused Latin America

1996 → 1997 region sales growth more than 100%

★Venezuela ⁂No.1 oversee Market but ranked No.4

Retail Sales 20thousand units

★Venezuela ratio to Oversee Sales

roughly 8.4%

Cherokee

sport-utility vehicles

Jeep Grand Cherokee

Neon passenger car

Local

Distribution

Export

Carababo

Assembly

PlantLuritiba

New Plant

950thousand

square meters

Jeep Grand Cherokee

Dodge Dakota

Pick up truck

JV US$500million

Engine plantWarehouse

Technical Training Center

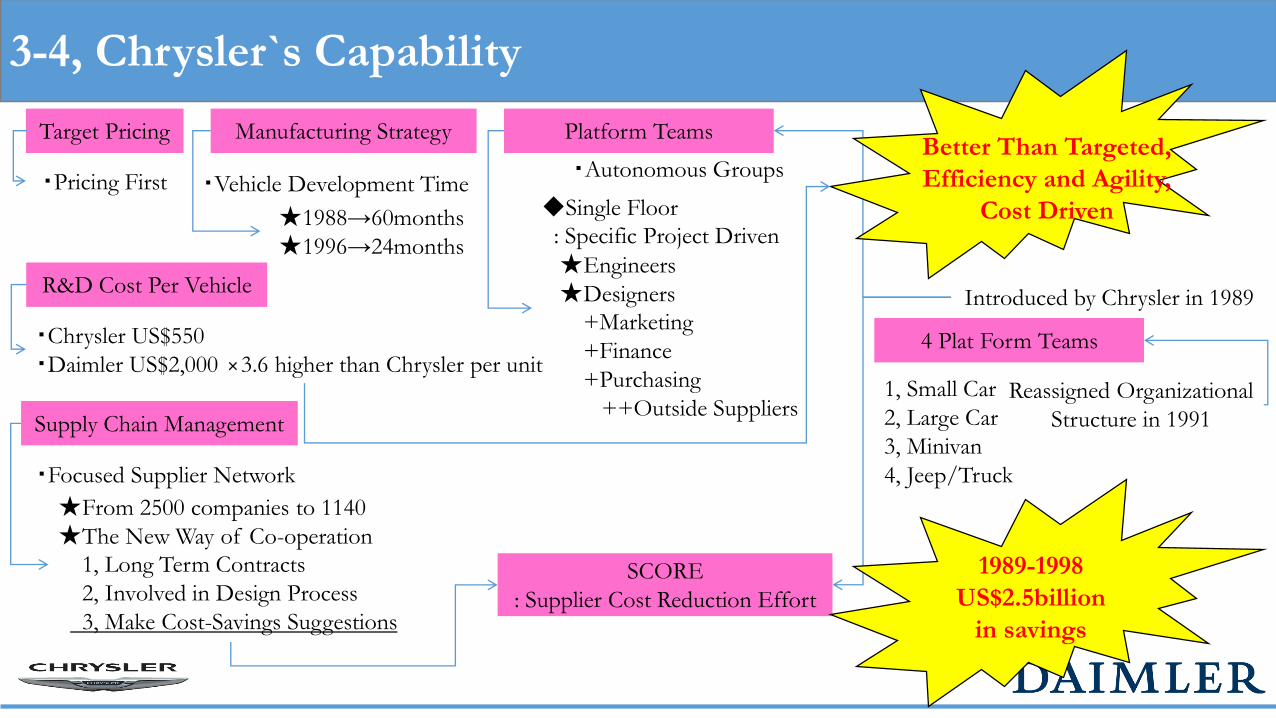

3-4, Chrysler`s Capability

Manufacturing Strategy

・Vehicle Development Time

★1988→60months

★1996→24months

Platform Teams

・Autonomous Groups

◆Single Floor

: Specific Project Driven

★Engineers

★Designers

+Marketing

+Finance

+Purchasing

++Outside Suppliers

Target Pricing

・Pricing First

Introduced by Chrysler in 1989

Supply Chain Management

・Focused Supplier Network

★From 2500 companies to 1140

★The New Way of Co-operation

1, Long Term Contracts

2, Involved in Design Process

3, Make Cost-Savings Suggestions

SCORE

: Supplier Cost Reduction Effort

1989-1998

US$2.5billion

in savings

Better Than Targeted,

Efficiency and Agility,

Cost Driven

R&D Cost Per Vehicle

・Chrysler US$550

・Daimler US$2,000 ×3.6 higher than Chrysler per unit4 Plat Form Teams

1, Small Car

2, Large Car

3, Minivan

4, Jeep/Truck

Reassigned Organizational

Structure in 1991

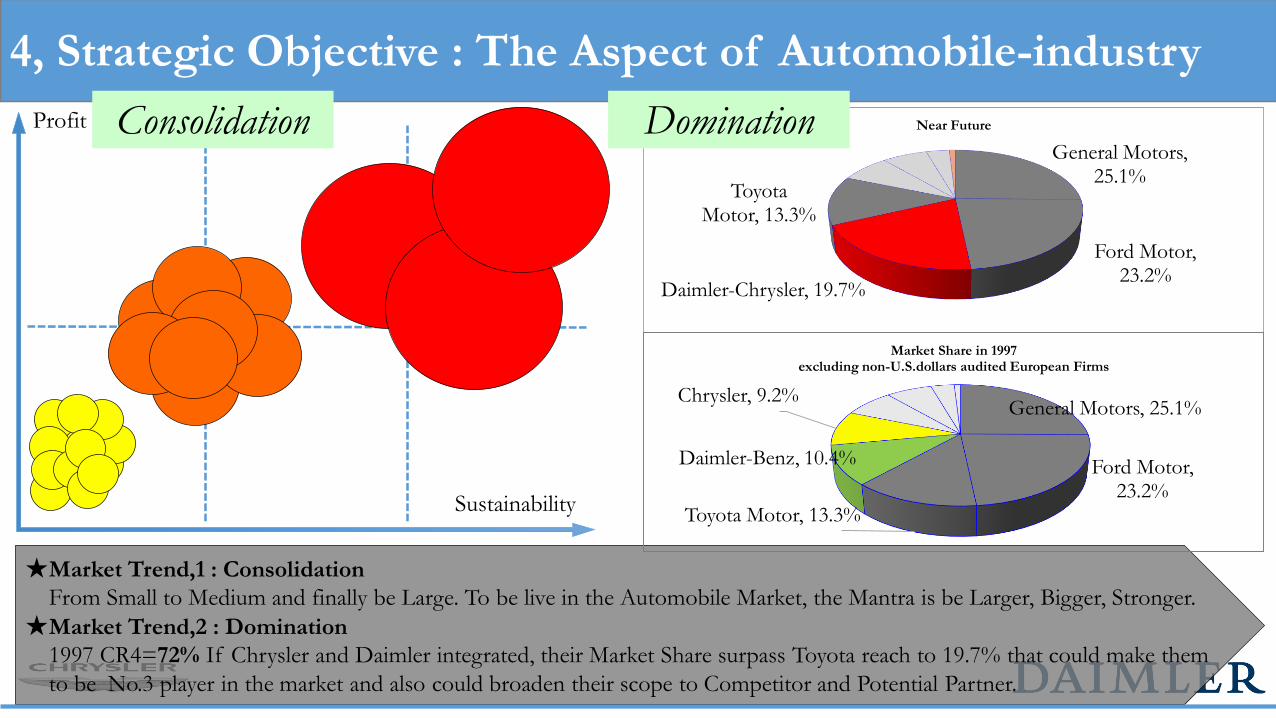

★Market Trend,1 : Consolidation

From Small to Medium and finally be Large. To be live in the Automobile Market, the Mantra is be Larger, Bigger, Stronger.

★Market Trend,2 : Domination

1997 CR4=72% If Chrysler and Daimler integrated, their Market Share surpass Toyota reach to 19.7% that could make them

to be No.3 player in the market and also could broaden their scope to Competitor and Potential Partner.

4, Strategic Objective : The Aspect of Automobile-industry

Profit

Sustainability

Consolidation

General Motors, 25.1%

Ford Motor, 23.2%

Toyota Motor, 13.3%

Daimler-Benz, 10.4%

Chrysler, 9.2%

Market Share in 1997 excluding non-U.S.dollars audited European Firms

General Motors, 25.1%

Ford Motor, 23.2%

Daimler-Chrysler, 19.7%

Toyota Motor, 13.3%

Near FutureDomination

5, Why M&A? Why Daimler – Benz?

3, Repositioning : What

Competing

Integrating

1, Vision : Why

・To Be No.1

Automobile/Car

Maker

・Maximize,

Shareholder,

Customer, Society

and all other

Stakeholder`s Value

2, Advantages : How

M:Cost Driven Management

H:Innovative Team Building

P:Competitive Truck Segment

M:Two Headed Bord

H:Worker`s Involvement

P:Luxuary

Full C

ar Lin

e-up, B

rand

, Distrib

utio

n,

Cap

ital, Co

st Red

uctio

n E

ffect, Barg

ainin

g

4, Goal

★Sales

★Profitability

★Innovation

★Quality

★Brand

★Benefit

★Stakeholders

★Lead Industry

★Why, How, What?

In order to meet all stakeholder`s value and maximize it, Chrysler and Daimler should be the No. 1 maker. Follow to market

shift, to catch on it or to lead it, the integration of Chrysler and Daimler with leverage each other`s advantage is much more

efficient and speedy way to achieve it. To achieve it, integrated two companies could aggressively compete with Top-tier maker

and at the same time aggressively offer integration to small producers. The cycle could make them be dominant player.

6, Interim Report

Transaction Execution

Validation ExecutionIntegration

Target

Screening

Internal

Valuation

ObjectivesCriteria

Development

Position

Assessment

Strategy

Development

Implementation

Planning

Target

Identification

Long-list

Long-list

Evaluation

Short-list

Merger Benefit

Potential

Market

Context

Desirability Achievability

Related Documents